As filed with the Securities and Exchange Commission on

Securities Act Registration No. 333-123290

Investment Company Act Reg. No. 811-21726

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

|

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

☒ |

|

|

|

Pre-Effective Amendment No. |

☐ |

|

|

Post-Effective Amendment No. 161 |

☒ |

|

and/or |

|

|

|

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 |

☒ |

|

|

|

Amendment No. 162 |

☒ |

(Check appropriate box or boxes.)

(Exact Name of Registrant as Specified in Charter)

4300 Shawnee Mission Parkway, Suite 100, Fairway, Kansas 66205

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (877) 244-6235

The Corporation Trust Company

Corporation Trust Center

1209 Orange Street

Wilmington, Delaware 19801

(Name and Address of Agent for Service)

With Copies To:

Bo J. Howell

Strauss Troy Co., LPA

150 E. 4th Street, 4th Floor

Cincinnati, Ohio 45202

Approximate Date of Proposed Public Offering: Immediately following effectiveness of this post-effective amendment.

It is proposed that this filing will become effective (check appropriate box)

|

☒ |

immediately upon filing pursuant to paragraph (b) |

|

☐ |

On pursuant to paragraph (b) |

|

☐ |

60 days after filing pursuant to paragraph (a)(1) |

|

☐ |

on (date) pursuant to paragraph (a)(1) |

|

☐ |

75 days after filing pursuant to paragraph (a)(2) |

|

☐ |

on (date) pursuant to paragraph (a)(2) of rule 485. |

If appropriate, check the following box:

|

☐ |

This post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

IMS Capital Management, Inc.

IMS Capital Value Fund

Institutional Class Shares (Ticker Symbol: )

IMS Strategic Income Fund

Institutional Class Shares (Ticker Symbol: )

each a series of the

360 Funds

PROSPECTUS

This Prospectus relates to one class of shares (Institutional Class shares), currently offered by IMS Capital Management, Inc., for each of the IMS Capital Value Fund and IMS Strategic Income Fund, for questions or for Shareholder Services, please call (877) 244-6235.

These securities have not been approved or disapproved by the Securities and Exchange Commission or any state securities commission nor has the Securities and Exchange Commission or any state securities commission passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

IMPORTANT NOTE: As permitted by regulations adopted by the SEC, paper copies of the Fund’s shareholder reports will no longer be sent by mail unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. You may elect to receive all future reports in paper free of charge. You can inform the Fund or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by calling or sending an e-mail request. Your election to receive reports in paper will apply to all funds held with the Fund complex/your financial intermediary.

Table of Contents

|

1 |

|

|

1 |

|

|

1 |

|

|

1 |

|

|

1 |

|

|

1 |

|

|

3 |

|

|

4 |

|

|

5 |

|

|

5 |

|

|

5 |

|

|

Payments to Broker-Dealers and Other Financial Intermediaries |

5 |

|

6 |

|

|

6 |

|

|

6 |

|

|

6 |

|

|

7 |

|

|

7 |

|

|

7 |

|

|

10 |

|

|

11 |

|

|

11 |

|

|

11 |

|

|

Payments to Broker-Dealers and Other Financial Intermediaries |

11 |

|

INVESTMENT OBJECTIVES, STRATEGIES, RISKS AND PORTFOLIO HOLDINGS |

12 |

|

The Funds’ Investment Objectives and Principal Investment Strategies |

12 |

|

12 |

|

|

13 |

|

|

14 |

|

|

14 |

|

|

14 |

|

|

15 |

|

|

16 |

|

|

20 |

|

|

20 |

|

|

21 |

|

|

21 |

|

|

22 |

|

|

22 |

|

|

22 |

|

|

22 |

|

|

22 |

|

|

22 |

|

|

22 |

|

|

22 |

|

23 |

|

|

23 |

|

|

23 |

|

|

24 |

|

|

24 |

|

|

24 |

|

|

Important Information about Procedures for Opening a New Account |

24 |

|

25 |

|

|

25 |

|

|

25 |

|

|

25 |

|

|

25 |

|

|

25 |

|

|

26 |

|

|

27 |

|

|

27 |

|

|

27 |

|

|

27 |

|

|

27 |

|

|

28 |

|

|

28 |

|

|

29 |

|

|

29 |

|

|

29 |

|

|

30 |

|

|

33 |

|

|

35 |

The investment objective of the IMS Capital Value Fund (the “Value Fund”) is long-term growth from capital appreciation,

and secondarily, income from dividends.

This table describes the fees and expenses that you may pay if you buy and hold shares of the Value Fund.

|

|

Institutional |

|

Redemption Fees (as a % of amount redeemed, a redemption fee will be assessed on shares of the Fund that are held for 90 days or less) |

|

|

|

Institutional |

|

Management Fees |

|

|

Other Expenses |

|

|

Interest Expense |

|

|

Total Annual Fund Operating Expenses |

|

This Example is intended to help you compare the cost of investing in the Value Fund with the cost of investing in other mutual funds.

This expense example assumes that you invest $10,000 in the Value Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The expense example also assumes that your investment has a 5% return each year and the Value Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your cost would be:

|

Period Invested |

1 Year |

3 Years |

5 Years |

10 Years |

|

Institutional Class |

$ |

$ |

$ |

$ |

The Value Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Value Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Expense Example above, affect the Value Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was

The investment objective of the Value Fund is long-term growth from capital appreciation, and secondarily, income from dividends. The Value Fund invests primarily in common stocks of mid-cap and large-cap U.S. companies. With respect to both mid-cap and large-cap stocks, the Adviser employs a selection process designed to produce a diversified portfolio of companies exhibiting both value and positive momentum characteristics. Value characteristics include a historically low stock price, as well as historically low fundamental ratios such as price to earnings, price to sales, price to book value and price to cash flow. Positive momentum characteristics include positive earnings revisions, positive earnings surprises, relative price strength and other developments that may favorably affect a company’s stock price, such as a new product or change in management.

1

The Adviser seeks to reduce risk through diversification and through the ownership of undervalued companies, which may be less volatile than overpriced companies whose fundamentals do not support their valuations. The Value Fund typically invests in mid-cap securities, which the Adviser defines as those with a market capitalization of approximately $2 billion to $11 billion, and in large-cap securities, which the Adviser defines as those with a market capitalization of greater than $11 billion. The Adviser generally seeks companies that it believes are well-capitalized, globally diversified, and that have the resources to weather negative business conditions successfully.

Most stocks in the Value Fund’s portfolio fall into one of the Adviser’s seven strategic focus areas: healthcare, technology, financial services, communications/entertainment, consumer, consolidating industries (i.e., companies buying other companies in an industry) and industries that, in the past, have declined less than others during general market declines (i.e., defensive industries). The Adviser believes that stocks in these focus areas have the potential to produce superior long-term returns. In addition, the Adviser carefully diversifies the Value Fund’s holdings to ensure representation in all ten major broad-based industry sectors as defined by Standard & Poor’s, Inc.

Although the Value Fund intends to be invested primarily in mid-cap and large-cap stocks as described above, the Value Fund may also invest in common stocks of any capitalization. The Value Fund may pursue its investment objective directly or indirectly through investments in other investment companies (including exchange-traded funds (“ETFs”) and open-end and closed-end mutual funds) that invest in the securities described above.

The Value Fund typically will sell a portfolio company if both of the following occur: (1) a company’s stock price exceeds the Adviser’s target sell price; and (2) the company demonstrates that it may be losing positive momentum as described above. The Value Fund also could sell a portfolio company earlier if the Adviser believes that the company’s stock price may not reach the Adviser’s target sell price due to a material event, such as major industry-wide change, a significant change in the company’s management or direction, the emergence of a better opportunity within the same industry, or if the company becomes involved in a merger or acquisition.

The Value Fund’s primary objective is capital appreciation. The Value Fund seeks to achieve its secondary objective of income by investing in dividend-paying stocks.

As a result of the Adviser’s overall strategy, the Value Fund engages in active trading of portfolio securities which causes the Value Fund to experience a high portfolio turnover rate.

2

|

● |

Market risk – Market risk refers to the risk that the value of securities in the Value Fund’s portfolio may decline due to daily fluctuations in the securities markets, including fluctuation in interest rates, national and international economic conditions and general equity market conditions. |

|

● |

Turnover risk – Through active trading, the Value Fund may have a high portfolio turnover rate, which can mean greater distributions taxable to shareholders as ordinary income for federal income tax purposes and lower performance due to increased brokerage costs. |

|

● |

Mid-cap risk – The Value Fund invests in mid-cap companies, which may be more vulnerable to adverse business or economic events than larger, more established companies. In particular, mid-sized companies may pose additional risks, including liquidity risk, because such companies tend to have limited product lines, markets and financial resources, and depend upon a relatively small management group. |

|

● |

Large-cap risk – Larger, more established companies may be unable to attain the high growth rates of successful, smaller companies during periods of economic expansion. |

|

● |

Management style risk – The Value Fund intends to invest in value-oriented stocks (stocks that the Adviser believes are undervalued), and the Value Fund’s performance may at times be better or worse than that of similar funds with other focuses or that have a broader investment style. |

|

● |

Value securities risk – Value stocks are those that appear to be underpriced based upon valuation measures, such as lower price-to-earnings ratios and price-to-book ratios. Investments in value-oriented securities may expose the Value Fund to the risk of underperformance during periods when value stocks do not perform as well as other kinds of investments or market averages. |

|

● |

Investment company securities risk – When the Value Fund invests in other investment companies, including ETFs, it will indirectly bear its proportionate share of any fees and expenses payable directly by the other investment company. Therefore, the Value Fund will incur higher expenses, many of which may be duplicative. In addition, the Value Fund may be affected by losses of the underlying funds and the level of risk arising from the investment practices of the underlying funds (such as the use of leverage by the underlying funds). ETFs are subject to additional risks such as the fact that the ETF’s shares may trade at a market price that is above or below its net asset value or an active market may not develop. To the extent that the Value Fund invests in ETFs that invest in commodities, the Value Fund will be subject to the risk that the demand and supply of these commodities may fluctuate widely. Commodity ETFs may use derivatives, which exposes them to further risks, including counterparty risk (i.e., the risk that the institution on the other side of their trade will default). |

|

● |

Industry risk – The value of securities in a particular industry (such as financial services, technology or healthcare) may decline because of changing expectations for the performance of a particular industry. The Fund intends to hold a number of different individual securities, seeking to manage risks in a particular industry. However, the Fund does concentrate on the healthcare, technology, financial services, communications/entertainment, consumer, consolidating and defensive industries. As a consequence, the share price of the Fund may fluctuate in response to factors affecting a particular industry, and may fluctuate more widely than a fund that invests in a broader range of industries. The Fund may be more susceptible to any single economic, political, or regulatory occurrence affecting the aforementioned industries. |

3

|

● |

Large shareholder risk – Certain shareholders, including other funds advised by the Adviser or an affiliate of the Adviser, may from time to time own a substantial amount of shares of the Fund. In addition, a third party investor, the Adviser or an affiliate of the Adviser, or another entity may invest in the Fund and hold its investment for a limited period of time solely to facilitate commencement of the Fund or to facilitate the Fund’s achieving a specified size or scale. There can be no assurance that any large shareholder would not redeem its investment of that the size of the Fund would be maintained at such levels. Redemptions by large shareholders could have a significant negative impact on the Fund. Similarly, large purchases of shares of the Fund may adversely affect the Fund’s performance to the extent that the Fund is delayed in investing new cash and is required to maintain a larger cash position than it ordinarily would. The Fund may hold a relatively large proportion of its assets in cash in anticipation of large redemptions, diluting its investment returns. |

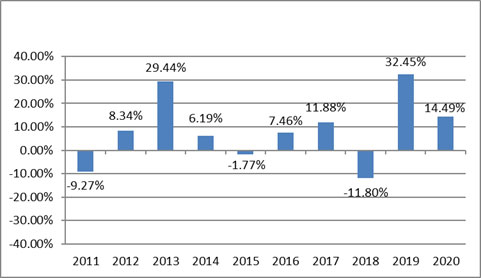

The Value Fund’s as of was %. During the periods shown in the bar chart, the was % during the quarter ended and the was % during the quarter ended .

Average Annual Total Returns

(for the periods ended December 31, 2020)

|

IMS Capital Value Fund |

One Year |

Five Years |

Ten Years |

|

Return Before Taxes |

|

|

|

|

Return After Taxes on Distributions |

|

|

|

|

Return After Taxes on Distributions and Sale of Fund Shares |

|

|

|

|

S&P 500 Index (reflects no deduction for fees, expenses, or taxes) |

|

|

|

4

Current performance

of the Value Fund may be lower or higher than the performance quoted above. Updated performance information may be obtained by

calling (877) 244-6235 or accessed on the Adviser’s website at

Management. IMS Capital Management, Inc. serves as the Value Fund’s investment adviser. Mr. Carl W. Marker is the Value Fund’s portfolio manager and is primarily responsible for the day-to-day management of the Value Fund’s portfolio.

Purchase and Sale of Fund Shares. The minimum initial investment in Institutional Class shares of the Value Fund is $5,000 for regular accounts and $2,000 for Coverdell Savings Accounts and UGMAs. Subsequent investments must be amounts of at least $100. You may sell your shares on days when the Value Fund is open for business. The Adviser may waive such fee for certain qualified retirement plan and advisory fee-based platforms.

You can purchase or redeem shares directly from the Value Fund on any business day the New York Stock Exchange is open directly by calling the Value Fund at (877) 244-6235, where you may also obtain more information about purchasing or redeeming shares by mail, facsimile or bank wire. The Value Fund has also authorized certain broker-dealers to accept purchase and redemption orders on its behalf. Investors who wish to purchase or redeem Value Fund shares through a broker-dealer should contact their broker-dealer directly.

Tax Information. The Value Fund’s distributions will generally be taxed to you as ordinary income or capital gains, unless you are investing through a tax deferred arrangement, such as a 401(k) plan or an IRA. Distributions on investments made through tax deferred arrangements such as 401(k) plans or IRAs may be taxed later upon a withdrawal of assets from those accounts.

Payments to Broker-Dealers and Other Financial Intermediaries. If you purchase shares of the Value Fund through a broker-dealer or other financial intermediary (such as a bank), the Value Fund and its related companies may pay the intermediary for the sale of Value Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Value Fund over another investment. Ask your salesperson or visit your financial intermediary’s Web site for more information.

5

The investment objective of the IMS Strategic Income Fund (the “Income Fund”) is current income,

and a secondary objective is capital appreciation.

This table describes the fees and expenses that you may pay if you buy and hold shares of the Income Fund.

|

|

Institutional |

|

Redemption Fees (as a % of amount redeemed, a redemption fee will be assessed on shares of the Fund that are held for 90 days or less) |

|

|

|

Institutional |

|

Management Fees |

|

|

Other Expenses |

|

|

Acquired Fund Fees and Expenses |

|

|

Total Annual Fund Operating Expenses |

|

|

Fee Waivers and/or Expense Reimbursement1 |

( |

|

Total Annual Fund Operating Expenses after Fee Waivers and/or Expense Reimbursement |

|

| 1 |

|

This Example is intended to help you compare the cost of investing in the Income Fund with the cost of investing in other mutual funds.

This expense example assumes that you invest $10,000 in the Income Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The expense example also assumes that your investment has a 5% return each year, the Income Fund’s operating expenses remain the same, and the contractual agreement to limit expenses remains in effect only through October 31, 2022. Although your actual costs may be higher or lower, based on these assumptions your cost would be:

|

Period Invested |

1 Year |

3 Years |

5 Years |

10 Years |

|

Institutional Class |

$ |

$ |

$ |

$ |

6

The Income Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Income Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Income Fund’s performance. During the most recent fiscal year, the Income Fund’s portfolio turnover rate was

The investment objective of the Income Fund is current income, and a secondary objective is capital appreciation. The Adviser has the flexibility to invest in a broad range of fixed income and equity securities that produce current income. The Adviser allocates the Income Fund’s assets among different types of securities based on its assessment of potential risks and returns, and the Adviser may change the weighting among securities as market conditions change, in an effort to obtain the most attractive combination of current income and, secondarily, capital appreciation.

In pursuing its investment objectives, the Income Fund generally invests in corporate bonds, government bonds, dividend-paying common stocks, preferred and convertible preferred stocks, income trusts (including business trusts, oil royalty trusts and real estate investment trusts), money market instruments and cash equivalents. The Income Fund may also invest in structured products, such as reverse convertible notes, a type of structured note, and in 144A securities that are purchased in private placements and thus are subject to restrictions on resale (either as a matter of contract or under federal securities laws), but only where the Adviser has determined that a liquid trading market exists. Under normal circumstances, the Income Fund will invest at least 80% of its assets in dividend paying or other income producing securities.

The Income Fund can invest in debt securities of any duration and maturity. The Income Fund considers investment-grade securities to be those rated BBB- or higher by Standard & Poor’s Corporation (“S&P”) or Fitch Investors Service, Inc. (“Fitch”), or Baa3 or higher by Moody’s Investor Services, Inc. (“Moody’s”), or if unrated, determined by the Adviser to be of comparable quality, each at the time of purchase. The Income Fund may invest up to 100% (measured at the time of purchase) of its assets in domestic investment grade fixed income securities of any duration and maturity. The Income Fund may also invest up to 45% (measured at the time of purchase) of its assets in domestic high yield fixed income securities (“junk bonds”) of any duration and maturity. The Income Fund may invest in distressed securities, including securities that are in default or the issuers of which are in bankruptcy, so long as the Adviser has determined that the securities are liquid. At times, the Income Fund’s position in illiquid securities may comprise a significant portion of the portfolio. Illiquid securities are subject to a number of risks which are discussed below. If market quotations for illiquid securities are not readily available, or are deemed unreliable by the Adviser, the security will be valued at a fair value determined in good faith by the Adviser. There is no assurance that the Income Fund will receive fair valuation upon the sale of a security. The Income Fund may invest up to 35% (measured at the time of purchase) of its assets in foreign equity and debt securities that pay dividends or interest, including foreign debt securities and foreign sovereign debt of any duration, quality and maturity, as well as securities of issuers located in emerging markets.

Subject to the limitations described above, the Income Fund may pursue its investment objective directly or indirectly through investments in other investment companies (including ETFs, and open-end and closed-end mutual funds) that invest in the securities described above.

As a result of the Adviser’s overall strategy, the Income Fund engages in active trading of portfolio securities which causes the Income Fund to experience a high portfolio turnover rate.

|

● |

Fixed income securities risk – The value of the Income Fund may fluctuate based upon changes in interest rates and market conditions. As interest rates rise, the value of most income producing instruments decreases to adjust the price to market yields. Interest rate risk is greater for long-term debt securities than for short-term and floating rate securities. It is possible that an issuer of a security will become unable to meet its obligations. This risk is greater for securities that are rated below investment grade or that are unrated. |

7

|

● |

High yield securities risk – The Income Fund may be subject to greater levels of price volatility as a result of investing in high yield fixed-income securities and unrated securities of similar credit quality (commonly known as junk bonds). The issuers of such bonds have a lower ability to make principal and interest payments, and are thus more likely to default. If this occurs, or is perceived as likely to occur, the values of these securities will generally be more volatile and are likely to fall. A default or expected default could also make it difficult for the Income Fund to sell the securities at the value the Income Fund previously placed on them. An economic downturn, a period of rising interest rates or increased price volatility could adversely affect the market for these securities, and reduce the number of buyers should the Income Fund need to sell these securities (liquidity risk). Should an issuer declare bankruptcy, the Income Fund could also lose its entire investment. When the Income Fund invests in foreign high yield bonds (including sovereign debt), it will be subject to additional risks not typically associated with investing in U.S. securities. These risks are described below under “Foreign securities risk.” |

|

● |

Distressed securities risk – Investments in distressed securities are speculative and involve substantial risks in addition to the risks of investing in high yield securities. Issuers of distressed securities may be engaged in restructuring or bankruptcy proceedings, or may be in default on the payment of principal or interest. The Income Fund may incur costs participating in legal proceedings involving the issuer or otherwise protecting its investment. The Income Fund generally will not receive interest payments on distressed securities, and there is a substantial risk that principal will not be repaid. If the issuer of a distressed security is engaged in restructuring or bankruptcy proceedings, the Income Fund may lose the entire value of its investment in the distressed security or be required to accept payment of cash or securities with a value far less than the Income Fund’s original investment. Distressed securities also may have restrictions on resale. |

|

● |

Liquidity risk – Illiquid and/or restricted securities in the Income Fund’s portfolio may reduce the Income Fund’s returns because the Income Fund may be unable to sell such illiquid securities at an advantageous time or when required to do so (such as in response to redemption requests), or may be able to sell them only at less than their market value. Securities particularly sensitive to illiquidity include U.S. and foreign high yield debt obligations and private placement securities. |

|

● |

Dividend strategy risk – There can be no assurances that the Adviser will be able to correctly anticipate the level of dividends that companies will pay in any given timeframe. If the Adviser’s expectations as to potential dividends are wrong, the Income Fund’s performance may be adversely affected. The strategy also will expose the Income Fund to increased trading costs and potential for short-term capital losses or gains. |

|

● |

Dividend tax risk – There can be no assurances that the dividends received by the Income Fund from its investments will consist of tax-advantaged qualifying dividends eligible for either the dividends-received deduction for corporate Income Fund shareholders that are otherwise eligible for such deduction or for treatment as qualified dividends eligible for long-term capital gain rates in respect of non-corporate Income Fund shareholders. Furthermore, there is no guarantee that dividends received by the Income Fund will continue to receive favorable tax treatment in future years. |

8

|

● |

Market risk – Market risk refers to the risk that the value of securities in the Income Fund’s portfolio may decline due to daily fluctuations in the securities markets, including fluctuation in interest rates, national and international economic conditions and general equity market conditions. |

|

● |

Management style risk – Different styles of management tend to shift into and out of favor with stock market investors depending on market and economic conditions. The strategy used by the Adviser may fail to produce the intended results and you could lose money. |

|

● |

Turnover risk – Through active trading, the Income Fund may have a high portfolio turnover rate, which can mean greater distributions taxable to shareholders as ordinary income for federal income tax purposes and lower performance due to increased brokerage costs. |

|

● |

Preferred stock risk – Preferred stocks rated in the lowest categories of investment grade have speculative characteristics. Preferred stock generally is subject to risks associated with fixed income securities, including credit risk and sensitivity to interest rates. Changes in economic conditions or other circumstances that have a negative impact on the issuer may lead to a weakened capacity to pay the preferred stock obligations. Preferred stock issuers, under certain conditions, may skip or defer dividend payments for long periods of time. As with common stock, preferred stock is subordinated to bonds and other debt instruments in any issuer’s capital structure in terms of priority to corporate income and liquidation payments, and therefore is subject to greater credit risk than those debt instruments. |

|

● |

REIT risk – To the extent that the Income Fund invests in companies that invest in real estate, such as REITs, the Income Fund may be subject to risk associated with the real estate market as a whole, such as taxation, regulations, and economic and political factors that negatively impact the real estate market, and with direct ownership of real estate, such as a decrease in real estate values, overbuilding, environmental liabilities and increases in operating costs, interest rates and/or property taxes. |

|

● |

Investment company securities risk – When the Income Fund invests in other investment companies, including ETFs, it will indirectly bear its proportionate share of any fees and expenses payable directly by the other investment company. Therefore, the Income Fund will incur higher expenses, many of which may be duplicative. In addition, the Income Fund may be affected by losses of the underlying funds and the level of risk arising from the investment practices of the underlying funds (such as the use of leverage by the underlying funds). ETFs are subject to additional risks such as the fact that the ETF’s shares may trade at a market price that is above or below its net asset value or an active market may not develop. Inverse and leveraged ETFs use investment techniques and financial instruments that may be considered aggressive, including the use of derivative transactions and short selling techniques. To the extent that the Income Fund invests in ETFs that invest in commodities, the Income Fund will be subject to the risk that the demand and supply of these commodities may fluctuate widely. Commodity ETFs may use derivatives, which exposes them to further risks, including counterparty risk (i.e., the risk that the institution on the other side of their trade will default). |

|

● |

Structured notes risk – Structured notes, such as reverse convertible notes, are subject to a number of fixed income risks including general market risk, interest rate risk, as well as the risk that the issuer on the note may fail to make interest and/or principal payments when due, or may default on its obligations entirely. In addition, as a result of imbedded derivative features in these securities, structured notes generally are subject to more risk than investing in a simple note or bond issued by the same issuer. |

|

● |

Income trust risk – Investments in income trusts are subject to various risks related to the underlying operating companies controlled by such trusts, including dependence upon specialized management skills and the risk that such management may lack or have limited operating histories. When the Income Fund invests in oil royalty trusts, its return on the investment will be highly dependent on oil and gas prices, which can be highly volatile. Moreover, oil royalty trusts are subject to the risk that the underlying oil and gas reserves attributable to the royalty trust may be depleted. As a group, business trusts typically invest in a broad range of industries and therefore the related risks will vary depending on the underlying industry represented in the business trust’s portfolio. |

9

|

● |

Credit risk – An issuer of debt securities may not make timely payments of principal and interest. |

|

● |

Large shareholder risk – Certain shareholders, including other funds advised by the Adviser or an affiliate of the Adviser, may from time to time own a substantial amount of shares of the Fund. In addition, a third party investor, the Adviser or an affiliate of the Adviser, or another entity may invest in the Fund and hold its investment for a limited period of time solely to facilitate commencement of the Fund or to facilitate the Fund’s achieving a specified size or scale. There can be no assurance that any large shareholder would not redeem its investment of that the size of the Fund would be maintained at such levels. Redemptions by large shareholders could have a significant negative impact on the Fund. Similarly, large purchases of shares of the Fund may adversely affect the Fund’s performance to the extent that the Fund is delayed in investing new cash and is required to maintain a larger cash position than it ordinarily would. The Fund may hold a relatively large proportion of its assets in cash in anticipation of large redemptions, diluting its investment returns. |

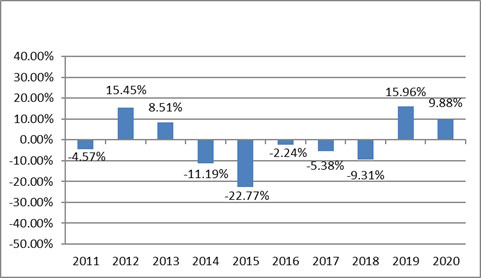

The Income Fund’s as of was %. During the period shown in the bar chart, the was % during the quarter ended and the was % during the quarter ended .

10

Average Annual Total Returns

(for the periods ended December 31, 2020)

|

IMS Strategic Income Fund |

One Year |

Five Years |

Ten Years |

|

Return Before Taxes |

|

|

( |

|

Return After Taxes on Distributions |

|

( |

( |

|

Return After Taxes on Distributions and Sale of Fund Shares |

|

( |

( |

|

Barclay’s U.S. Aggregate Bond Index (reflects no deduction for fees, expenses, or taxes) |

|

|

|

Current performance of the Income Fund may be lower or higher than the performance quoted above. Updated performance information may be obtained by calling (877) 244-6235 or accessed on the Adviser’s website at

Management. IMS Capital Management, Inc. serves as the Income Fund’s investment adviser. Carl W. Marker is the Income Fund’s portfolio manager and is primarily responsible for the day-to-day management of the Income Fund’s portfolio.

Purchase and Sale of Fund Shares. The minimum initial investment in Institutional Class shares of the Income Fund is $5,000 for regular accounts and $2,000 for Coverdell Savings Accounts and UGMAs. Subsequent investments must be amounts of at least $100. You may sell your shares on days when the Income Fund is open for business. The Adviser may waive such fee for certain qualified retirement plan and advisory fee-based platforms.

You can purchase or redeem shares directly from the Income Fund on any business day the New York Stock Exchange is open directly by calling the Income Fund at (877) 244-6235, where you may also obtain more information about purchasing or redeeming shares by mail, facsimile or bank wire. The Income Fund has also authorized certain broker-dealers to accept purchase and redemption orders on its behalf. Investors who wish to purchase or redeem Income Fund shares through a broker-dealer should contact their broker-dealer directly.

Tax Information. The Income Fund’s distributions will generally be taxed to you as ordinary income or capital gains, unless you are investing through a tax deferred arrangement, such as a 401(k) plan or an IRA. Distributions on investments made through tax deferred arrangements such as 401(k) plans or IRAs may be taxed later upon a withdrawal of assets from those accounts.

Payments to Broker-Dealers and Other Financial Intermediaries. If you purchase shares of the Income Fund through a broker-dealer or other financial intermediary (such as a bank), the Income Fund and its related companies may pay the intermediary for the sale of Income Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Income Fund over another investment. Ask your salesperson or visit your financial intermediary’s Web site for more information.

11

INVESTMENT OBJECTIVES, STRATEGIES, RISKS AND PORTFOLIO HOLDINGS

The Funds’ Investment Objectives and Principal Investment Strategies. This section of the Prospectus provides additional information about the investment practices and related risks of the IMS Capital Value Fund (the “Value Fund”) and IMS Strategic Income Fund (the “Income Fund,” and together, a “Fund” or the “Funds”). Each Fund’s investment objective may be changed without shareholder approval; however, a Fund will provide 60 days’ advance notice to shareholders before implementing a change in its investment objective.

IMS Capital Value Fund. The investment objective of the Value Fund is long-term growth from capital appreciation, and secondarily, income from dividends. The Value Fund invests primarily in common stocks of mid-cap and large-cap U.S. companies. With respect to both mid-cap and large-cap stocks, IMS Capital Management, Inc. (the “Adviser”) employs a selection process designed to produce a diversified portfolio of companies exhibiting both value and positive momentum characteristics. Value characteristics include a historically low stock price, as well as historically low fundamental ratios such as price to earnings, price to sales, price to book value and price to cash flow. Positive momentum characteristics include positive earnings revisions, positive earnings surprises, relative price strength and other developments that may favorably affect a company’s stock price, such as a new product or change in management. The Adviser selects stocks based on value characteristics; however, the Value Fund will not invest in an undervalued stock until it also exhibits positive momentum characteristics.

The Adviser seeks to reduce risk through diversification and through the ownership of undervalued companies, which may be less volatile than overpriced companies whose fundamentals do not support their valuations. Companies selected generally will have a total market capitalization at the time of purchase from $2 billion up to $11 billion, which the Adviser considers to be “mid-cap” companies, or greater than $11 billion, which the Adviser considers to be “large-cap” companies. The Value Fund may continue to hold a security even after it falls below these capitalization levels. The Adviser generally seeks companies that the Adviser believes are well-capitalized, globally diversified, and that have the resources to weather negative business conditions successfully. The Adviser believes mid-cap companies have the potential to deliver the best characteristics of both small and large companies – the flexible, innovative, high-growth aspects of small companies and the proven management, products, liquidity and global diversification of large companies.

Most stocks in the Value Fund’s portfolio fall into one of the Adviser’s seven strategic focus areas: healthcare, technology, financial services, communications/entertainment, consumer, consolidating industries (i.e., companies buying other companies in an industry) and industries that, in the past, have declined less than others during general market declines (i.e., defensive industries). The Adviser believes that stocks in these focus areas have the potential to produce superior long-term returns. In addition, the Adviser carefully diversifies the Value Fund’s holdings to ensure representation in all ten major broad-based industry sectors as defined by Standard & Poor’s, Inc.

The Adviser employs a patient approach to the stock selection process, believing that most traditional value managers tend to purchase companies too early. The Adviser believes that after a stock experiences a significant decline, it will tend to underperform the market during what the Adviser terms its “seasoning” period, usually at least 18 months. Once an undervalued company has been researched, deemed attractive, and has seasoned, the Adviser further delays the purchase until the company develops several positive momentum characteristics as described above.

The Value Fund may borrow money from a bank, provided that immediately after such borrowing there is asset coverage of 300% for all borrowings of the Value Fund. The Value Fund does not intend to borrow in excess of 5% of its total assets at the time of borrowing. The Value Fund may borrow to purchase securities, and it may borrow to prevent the Value Fund from selling a portfolio security at a disadvantageous time in order to meet shareholder redemptions.

12

Although the Value Fund intends to be invested primarily in mid-cap and large-cap stocks as described above, the Fund may also invest in common stock of any capitalization. The Value Fund may pursue its investment objective directly or indirectly through investments in other investment companies (including ETFs and open-end and closed-end mutual funds) that invest in the securities described above. The Value Fund typically will sell a security if both of the following occur: (1) the company’s stock price exceeds the Adviser’s target sell price and (2) the company demonstrates that it may be losing positive momentum. A variety of conditions could result in the sale of a company before it has reached the Adviser’s target sell price. Some examples include a major industry-wide change, a significant change in the company’s management or direction, the emergence of a better opportunity within the same industry, or if the company becomes involved in a merger or acquisition.

As a result of the Adviser’s overall strategy, the Value Fund engages in active trading of portfolio securities which causes the Value Fund to experience a high portfolio turnover rate.

IMS Strategic Income Fund. The investment objective of the Income Fund is current income and a secondary objective is capital appreciation. The Adviser has the flexibility to invest in a broad range of fixed income and equity securities that produce current income. The Adviser allocates the Income Fund’s assets among different types of securities based on its assessment of potential risks and returns, and the Adviser may change the weighting among securities as market conditions change, in an effort to obtain the most attractive combination of current income and, secondarily, capital appreciation.

In pursuing its investment objectives, the Income Fund generally invests in corporate bonds, government bonds, dividend-paying common stocks, preferred and convertible preferred stocks, income trusts (including business trusts, oil royalty trusts and real estate investment trusts), money market instruments and cash equivalents. The Income Fund may invest up to 100% (measured at the time of purchase) of its assets in domestic investment grade fixed income securities of any duration and maturity. The Income Fund may also invest in structured products, such as reverse convertible notes. Reverse convertible notes are short-term notes that are linked to individual equity securities or indexes, and typically make a single coupon payment at maturity. The holder of the reverse convertible notes generally has the right to receive at maturity either a fixed cash payment or a fixed number of shares of common stock, depending on the price history of the underlying common stock. The Income Fund may invest in securities that are purchased in private placements, and are thus subject to restrictions on resale (either as a matter of contract or under federal securities laws). Under normal circumstances, the Income Fund will invest at least 80% of its assets in dividend paying or other income producing securities.

In order to maximize the level of dividend income that the Income Fund receives from common stocks, the Adviser may buy stocks based on their scheduled dividend payment date, often purchasing a common stock close to the expected dividend announcement. Following payment of a dividend, the period of time after which the stock is sold will vary depending upon the Adviser’s perception of the stock’s capital appreciation potential. The Adviser believes that receiving dividends from several issuers during a short time period could augment the Income Fund’s total dividend income.

The Income Fund can invest in debt securities of any duration and maturity. The Income Fund considers investment-grade securities to be those rated BBB- or higher by Standard & Poor’s Corporation (“S&P”) or Fitch Investors Service, Inc. (“Fitch”), or Baa3 or higher by Moody’s Investor Services, Inc. (“Moody’s”), or if unrated, determined by the Adviser to be of comparable quality, each at the time of purchase. The Income Fund may also invest up to 45% (measured at the time of purchase) of its assets in domestic high yield fixed income securities (“junk bonds”) of any duration and maturity. The Income Fund may invest in distressed securities, including securities that are in default or the issuers of which are in bankruptcy, so long as the Adviser has determined that the securities are liquid. At times, the Income Fund’s position in illiquid securities may comprise a significant portion of the portfolio. Illiquid securities are subject to a number of risks which are discussed below. If market quotations for illiquid securities are not readily available, or are deemed unreliable by the Adviser, the security will be valued at a fair value determined in good faith by the Adviser. The Income Fund may invest up to 35% (measured at the time of purchase) of its assets in foreign fixed income and equity securities, including foreign debt securities and foreign sovereign debt of any duration, quality and maturity, as well as securities of issuers located in emerging markets.

13

The Adviser seeks to invest in debt securities it expects will have a high yield to maturity or dividend yield relative to potential price volatility, such as securities of an issuer which the Adviser believes have a stable or improving financial condition with a higher than average yield for its asset class, or securities that the Adviser expects will continue to pay dividends and increase in price.

The Income Fund typically will sell a portfolio security if any of the following occur: (1) the security price exceeds the Adviser’s target sell price; (2) market conditions or the issuer’s financial condition threaten the security’s price or coupon/dividend payment; or (3) the Adviser identifies a security it deems more attractive or better suited to achieving the Fund’s investment objective.

The Income Fund may borrow money from a bank, provided that immediately after such borrowing there is asset coverage of 300% for all borrowings of the Income Fund. The Income Fund does not intend to borrow in excess of 5% of its total assets at the time of borrowing. The Income Fund may borrow to purchase securities, and it may borrow to prevent the Income Fund from selling a portfolio security at a disadvantageous time in order to meet shareholder redemptions.

Due to the nature of some of its investments, the Income Fund may be more volatile than other income funds, the effects of which are described below under “Market Risk” and “Liquidity Risk”. Subject to the limitations described above, the Income Fund may pursue its investment objective directly or indirectly through investments in other investment companies (including ETFs, and open-end and closed-end mutual funds) that invest in the securities described above. The Income Fund may also use exchange-traded put and call options on individual securities or market indices to hedge interest rate risk. For example, if the Adviser expects interest rates to rise, the Income Fund may seek to hedge interest rate risk by purchasing an exchange-traded put option on a 10-year U.S. Treasury futures contract. Income Fund assets invested in options (including premiums paid and any assets that are required to be segregated to cover the Income Fund’s potential obligations under the options contracts) are not expected to exceed 5% of the Income Fund’s net assets (measured at the time of entering into the option contract).

As a result of the Adviser’s overall strategy, the Income Fund engages in active trading of portfolio securities which causes the Income Fund to experience a high portfolio turnover rate.

Temporary Defensive Positions. The Funds may, from time to time, take temporary defensive positions that are inconsistent with such Fund’s principal investment strategies in an attempt to respond to adverse market, economic, political or other conditions. During such an unusual set of circumstances, the Fund may hold up to 100% of its portfolio in cash or cash equivalent positions. When a Fund takes a temporary defensive position, such Fund may not be able to achieve its investment objective.

Portfolio Turnover. Although each Fund’s strategy emphasizes longer-term investments that typically result in portfolio turnover less than 100%, the Funds may, from time to time, have a higher portfolio turnover when the Adviser’s implementation of a Fund’s investment strategy or a temporary defensive position results in frequent trading. Since each Fund’s trades cost such Fund a brokerage commission, high portfolio turnover may have a significant adverse impact on the Fund’s performance. In addition, because sales of securities in the Fund’s portfolio may result in taxable gain or loss, high portfolio turnover may result in significant tax consequences for shareholders.

|

“Portfolio Turnover” is a ratio that indicates how often the securities in a mutual fund’s portfolio change during a year’s time. In general, higher numbers indicate a greater number of changes, and lower numbers indicate a smaller number of changes. |

General Information Regarding Investing in a Fund. An investment in a Fund should not be considered a complete investment program. Your investment needs will depend largely on your financial resources and individual investment goals and objectives, and you should consult with your financial professional before making an investment in a Fund.

14

Additional Information. To the extent a Fund makes investments regulated by the Commodities Futures Trading Commission, it intends to do so in accordance with Rule 4.5 under the Commodity Exchange Act (“CEA”). The Adviser, on behalf of the Funds, has filed a notice of eligibility for exclusion from the definition of the term “commodity pool operator” in accordance with Rule 4.5 and therefore, the Funds are not subject to registration or regulation as a commodity pool operator under the CEA.

15

PRINCIPAL RISKS OF INVESTING IN A FUND

All investments carry risks, and investment in a Fund is no exception. No investment strategy works all the time, and past performance is not necessarily indicative of future performance. You may lose money on your investment in a Fund. To help you understand the risks of investing in a Fund, the principal risks of an investment in a Fund are generally set forth below:

|

● |

Market risk – Stock prices are volatile. Market risk refers to the risk that the value of securities in the Funds’ portfolio may decline due to daily fluctuations in the securities markets generally. The Funds’ performance per share will change daily based on many factors that may generally affect the stock market, including fluctuation in interest rates, national and international economic conditions and general equity market conditions. In a declining stock market, stock prices for all companies (including those in the Funds’ portfolio) may decline, regardless of their long-term prospects. |

|

● |

Management style risk – Different styles of management tend to shift into and out of favor with stock market investors depending on market and economic conditions. The strategies used by the Adviser may fail to produce the intended results and you could lose money. |

|

● |

Turnover risk – Through active trading, the Funds may have a high portfolio turnover rate, which can mean greater distributions taxable to shareholders as ordinary income for federal income tax purposes and lower performance due to increased brokerage costs. |

|

● |

Investment company securities risk – If the Funds invest in an underlying mutual fund or ETF, the Funds indirectly will bear its proportionate share of any fees and expenses payable directly by the underlying fund. Therefore, the Funds will incur higher expenses, many of which may be duplicative. In addition, the Funds may be affected by losses of the underlying funds and the level of risk arising from the investment practices of the underlying funds (such as the use of leverage by the underlying funds). The Funds have no control over the investments and related risks taken by the underlying funds in which it invests. ETFs are subject to additional risks such as the fact that the ETF’s shares may trade at a market price that is above or below its net asset value, an active market may not develop, it may employ a strategy that utilizes high leverage ratios, and trading of its shares may be halted under certain circumstances. To the extent that a Fund invests in inverse or leveraged ETFs, the value of the Fund’s investment will decrease when the index underlying the ETF’s benchmark rises, a result that is the opposite from traditional equity or bond funds. The net asset value and market price of leveraged or inverse ETFs are usually more volatile than the value of the tracked index or of other ETFs that do not use leverage. Inverse and leveraged ETFs use investment techniques and financial instruments that may be considered aggressive, including the use of derivative transactions and short selling techniques. To the extent that a Fund invests in ETFs that invest in commodities, which are real assets such as oil, agriculture, livestock, industrial metals, and precious metals such as gold or silver, the Fund will be subject to additional risks. The values of commodity-based ETFs are highly dependent on the prices of the related commodity and the demand and supply of these commodities may fluctuate widely. Commodity ETFs may use derivatives, which exposes them to further risks, including counterparty risk (i.e., the risk that the institution on the other side of their trade will default). |

|

● |

Borrowing and leverage risk – Borrowing magnifies the potential for gain or loss by the Funds and, therefore, increases the possibility of fluctuation in the Funds’ net asset values. This is the speculative factor known as leverage. Because the Funds’ investments will fluctuate in value, while the interest on borrowed amounts may be fixed, the Funds’ net asset values may tend to increase more as the value of its investments increases, or to decrease more as the value of its investments decreases, during times of borrowing. Unless profits on investments acquired with borrowed funds exceed the costs of borrowing, the use of borrowing will cause a Fund’s investment performance to decrease. |

16

|

● |

Large shareholder risk – Certain shareholders, including other funds advised by the Adviser or an affiliate of the Adviser, may from time to time own a substantial amount of shares of the Fund. In addition, a third party investor, the Adviser or an affiliate of the Adviser, or another entity may invest in the Fund and hold its investment for a limited period of time solely to facilitate commencement of the Fund or to facilitate the Fund’s achieving a specified size or scale. There can be no assurance that any large shareholder would not redeem its investment of that the size of the Fund would be maintained at such levels. Redemptions by large shareholders could have a significant negative impact on the Fund. Similarly, large purchases of shares of the Fund may adversely affect the Fund’s performance to the extent that the Fund is delayed in investing new cash and is required to maintain a larger cash position than it ordinarily would. The Fund may hold a relatively large proportion of its assets in cash in anticipation of large redemptions, diluting its investment returns. |

In addition to the risks set forth under “Principal Risks of Investing in the Fund” and the Principal Risks of Investing in a Fund, the IMS Capital Value Fund is subject to the following risks:

|

● |

Mid-cap risk – Stocks of mid-cap companies are generally considered more risky than stocks of larger capitalization companies. Mid-cap companies typically have greater earnings fluctuations and greater reliance on a few key customers than larger companies. Many of these companies may be young with a limited track record. Their securities may trade less frequently and in more limited volume than those of larger companies. This may disproportionately affect their market price, tending to make them fall more in response to selling pressure than is the case with larger companies. Mid-cap companies may also have limited markets, product lines or financial resources and may lack management experience. The prospects for a company or its industry may deteriorate because of a variety of factors, including disappointing operating results or changes in the competitive environment. |

|

● |

Large-cap risk – Larger, more established companies may be unable to attain the high growth rates of successful, smaller companies during periods of economic expansion. |

|

● |

Value securities risk – Value stocks are those that appear to be underpriced based upon valuation measures, such as lower price-to-earnings ratios and price-to-book ratios. Investments in value-oriented securities may expose these Funds to the risk of underperformance during periods when value stocks do not perform as well as other kinds of investments or market averages. |

|

● |

Industry risk – the value of securities in a particular industry (such as financial services, technology or healthcare) may decline because of changing expectations for the performance of a particular industry. The Fund intends to hold a number of different individual securities, seeking to manage risks in a particular industry. However, the Fund does concentrate on the healthcare, technology, financial services, communications/entertainment, consumer, consolidating and defensive industries. As a consequence, the share price of the Fund may fluctuate in response to factors affecting a particular industry, and may fluctuate more widely than a fund that invests in a broader range of industries. The Fund may be more susceptible to any single economic, political, or regulatory occurrence affecting the aforementioned industries. |

In addition to the risks set forth under “Principal Risks of Investing in the Fund” and the Principal Risks of Investing in a Fund, the IMS Strategic Income Fund is subject to the following risks:

|

● |

Foreign securities risk – When the Fund invests in foreign securities (including sovereign debt), it will be subject to additional risks not typically associated with investing in U.S. government securities and securities of domestic companies. There may be less publicly available information about a foreign issuer than a domestic one, and foreign companies are not generally subject to uniform accounting, auditing and financial standards and requirements comparable to those applicable to U.S. companies. In addition, the value of securities denominated in foreign currency can change when foreign currencies strengthen or weaken relative to the U.S. dollar. These currency movements may negatively impact the value of the Funds’ portfolio even when there is no change in the value of the related security in the issuer’s home country. Sovereign debt differs from debt obligations issued by private entities in that, generally, remedies for defaults must be pursued in the courts of the defaulting party. Legal recourse is therefore limited. Political conditions, especially a sovereign entity’s willingness to meet the terms of its debt obligations are of considerable significance. When the Fund invests in securities of issuers located in foreign emerging markets, it will be subject to additional risks that may be different from, or greater than, risks of investing in securities of issuers based in foreign, developed countries. These risks include illiquidity, significant price volatility, restrictions on foreign investment or repatriation, possible nationalization of investment income and capital, currency declines, and inflation (including rapid fluctuations in inflation rates). |

17

|

● |

REIT risk – To the extent that the Fund invests in companies that invest in real estate, such as REITs, the Fund may be subject to risk associated with the real estate market as a whole, such as taxation, regulations, and economic and political factors that negatively impact the real estate market, and with direct ownership of real estate, such as a decrease in real estate values, overbuilding, environmental liabilities and increases in operating costs, interest rates and/or property taxes. |

|

● |

High yield securities risk – The Fund may be subject to greater levels of price volatility as a result of investing in high yield fixed income securities and unrated securities of similar credit quality (commonly known as junk bonds) than funds that do not invest in such securities. Such bonds are rated below BBB-/Baa3 because of the greater possibility that the issuer will fail to make principal and interest payments, and thus default. If this occurs, or is perceived as likely to occur, the values of these securities will generally be more volatile and are likely to fall. A default or expected default could also make it difficult for the Fund to sell the securities at the value the Fund previously placed on them. As a result, high yield securities are considered predominately speculative. An economic downturn, a period of rising interest rates or increased price volatility could adversely affect the market for these securities, and reduce the number of buyers should the Fund need to sell these securities (liquidity risk). Should an issuer declare bankruptcy, there may be potential for partial recovery of the value of the bonds, but the Fund could also lose its entire investment. When the Fund invests in foreign high yield bonds (including sovereign debt), it will be subject to additional risks not typically associated with investing in U.S. securities. These risks are described below under “Foreign securities risk.” |

|

● |

Distressed securities risk – Investments in distressed securities are speculative and involve substantial risks in addition to the risks of investing in high yield securities. Issuers of distressed securities may be engaged in restructuring or bankruptcy proceedings, or may be in default on the payment of principal or interest. The Fund may incur costs participating in legal proceedings involving the issuer or otherwise protecting its investment. The Fund generally will not receive interest payments on distressed securities, and there is a substantial risk that principal will not be repaid. If the issuer of a distressed security is engaged in restructuring or bankruptcy proceedings, the Fund may lose the entire value of its investment in the distressed security or be required to accept payment of cash or securities with a value far less than the Fund’s original investment. Distressed securities also may have restrictions on resale. |

18

|

● |

Dividend tax risk – There can be no assurances that the dividends received by the Fund from its investments will consist of tax-advantaged qualifying dividends eligible either for the dividends-received deduction for corporate Fund shareholders that are otherwise eligible for such deduction or for treatment as qualified dividends eligible for long-term capital gain rates in respect of non-corporate Fund shareholders. To receive dividends-received or qualifying dividend income tax treatment, the Fund must meet holding period and other requirements with respect to the security, and Fund shareholders must meet holding period and other requirements with respect to their Fund’s shares. Furthermore, there is no guarantee that dividends received by the Fund will continue to receive favorable tax treatment in future years. |

|

● |

Income trust risk – Investments in income trusts are subject to various risks related to the underlying operating companies controlled by such trusts, including dependence upon specialized management skills and the risk that such management may lack or have limited operating histories. To the extent the Fund invests in income trusts that invest in real estate, it may be subject to risk associated with the real estate market as a whole, such as taxation, regulations and economic and political factors that negatively impact the real estate market and with direct ownership of real estate, such as a decrease in real estate values, overbuilding, environmental liabilities and increases in operating costs, interest rates and or property taxes. When the Fund invests in oil royalty trusts, its return on the investment will be highly dependent on oil and gas prices, which can be highly volatile. Moreover, oil royalty trusts are subject to the risk that the underlying oil and gas reserves attributable to the royalty trust may be depleted. As a group, business trusts typically invest in a broad range of industries and therefore the related risks will vary depending on the underlying industry represented in the business trust’s portfolio. |

|

● |

Dividend strategy risk – The Fund’s dividend capture strategy enables the Adviser to identify and exploit opportunities that the Adviser believes may lead to high current dividend income for the Fund. There can be no assurances that the Adviser will be able to correctly anticipate the level of dividends that companies will pay in any given timeframe. If the Adviser’s expectations as to potential dividends are wrong, the Fund’s performance may be adversely affected. In addition, the dividend policies of the Fund’s target companies are heavily influenced by the current economic climate and the favorable federal tax treatment afforded to dividends. Any change in the favorable provisions of the federal tax laws may limit the ability of the Fund to take advantage of further income enhancing strategies utilizing dividend paying securities. The use of dividend capture strategies also will expose the Fund to increased trading costs and potential for short-term capital losses or gains, particularly in the event of significant short-term price movements of stocks subject to dividend capture trading. |

|

● |

Structured notes risk – Structured notes, such as reverse convertible notes, are subject to a number of fixed income risks including general market risk, interest rate risk, as well as the risk that the issuer on the note may fail to make interest and/or principal payments when due, or may default on its obligations entirely. In addition, as a result of imbedded derivative features in these securities, structured notes generally are subject to more risk than investing in a simple note or bond issued by the same issuer. It is impossible to predict whether the referenced factor (such as an index or interest rate) or prices of the underlying securities will rise or fall. The actual trading prices of structured notes may be significantly different from the principal amount of the notes. If the Fund sells the structured notes prior to maturity, it may lose some of its principal. At final maturity, structured notes may be redeemed in cash or in kind, which is at the discretion of the issuer. If the notes are redeemed in kind, the Fund would receive shares of stock at a depressed price. In the case of a decrease in the value of the underlying asset, the Fund would receive shares at a value less than the original amount invested; while an increase in the value of an underlying asset will not increase the return on the note. |

19

|

● |

Preferred stock risks – Preferred stocks rated in the lowest categories of investment grade have speculative characteristics. Preferred stock generally is subject to risks associated with fixed income securities, including credit risk and sensitivity to interest rates. Changes in economic conditions or other circumstances that have a negative impact on the issuer may lead to a weakened capacity to pay the preferred stock obligations. Preferred stock may be subject to a number of other risks, including that the issuer, under certain conditions, may skip or defer dividend payments for long periods of time. If the Fund owns a preferred security that is deferring its distributions, the Fund may be required to report income for tax purposes while it is not receiving any income. In addition, holders of preferred stock typically do not have any voting rights, except in cases when dividends are in arrears beyond stated time periods. As with common stock, preferred stock is subordinated to bonds and other debt instruments in any issuer’s capital structure in terms of priority to corporate income and liquidation payments, and therefore is subject to greater credit risk than those debt instruments. |

|

● |

Fixed income risk – The value of these Funds may fluctuate based upon changes in interest rates and market conditions. As interest rates rise, the value of most income producing instruments decreases to adjust to price the market yields. Interest rate risk is greater for long-term debt securities than for short-term and floating rate securities. These Funds are subject to credit risk, which is the possibility that an issuer of a security will become unable to meet its obligations. This risk is greater for securities that are rated below investment grade or that are unrated. |

|

● |

Liquidity risk – Illiquid and/or restricted securities in these Funds’ portfolio may reduce the Funds’ returns because the Funds may be unable to sell such illiquid securities at an advantageous time or price. If the Funds are unable to sell their illiquid securities when deemed desirable, it may incur losses and may be restricted in their ability to take advantage of other market opportunities. In addition, illiquid securities may be more difficult to value, and usually require the Adviser’s judgment in the valuation process. The Adviser’s judgment as to the fair value of a security may be wrong, and there is no guarantee that the Funds will realize the entire fair value assigned to the security upon a sale. Securities particularly sensitive to illiquidity include U.S. and foreign high yield debt obligations and private placement securities. |

|

● |

Credit risk – An issuer of debt securities may not make timely payments of principal and interest. |

MANAGEMENT

Investment Adviser. IMS Capital Management, Inc. (the “Adviser”), 8995 S.E. Otty Road, Portland, Oregon 97086, serves as investment adviser to the Funds. The Adviser is an independent investment advisory firm that has been managing equity and fixed income portfolios for a select group of clients since 1988. The Adviser currently manages accounts for institutions, retirement plans, individuals, trusts and small businesses, both taxable and non-taxable. As of June 30, 2021, the Adviser managed over $280 million on a discretionary basis.

During the fiscal year ended June 30, 2021, the Adviser received compensation of 1.21% of the Value Fund’s average daily net assets, after fee waiver and/or expense reimbursement. During the fiscal year ended June 30, 2021, the Adviser received compensation of 0.58% of the Income Fund’s average daily net assets, after fee waiver and/or expense reimbursement.

With respect to each of the Funds, the Adviser contractually agreed to waive its management fee and/or reimburse expenses so that total annual fund operating expenses (excluding interest, taxes, brokerage fees and commissions, other expenditures that are capitalized in accordance with generally accepted accounting principles, acquired fund fees and expenses, other extraordinary expenses not incurred in the ordinary course of the Fund’s business, interest and dividend expense on securities sold short, and amounts, if any payable pursuant to a plan adopted in accordance with Rule 12b-1 under the 1940 Act) do not exceed 1.95% of a Fund’s average daily net assets through October 31, 2022, subject to the Adviser’s right to recoup payments on a rolling three-year basis so long as the payment would not exceed the 1.95% expense cap. This expense cap agreement may be terminated by either party upon 60 days’ written notice prior to the end of the then-current term of the agreement.

20

If you invest in a Fund through an investment adviser, bank, broker-dealer, 401(k) plan trust company or other financial intermediary, the policies and fees for transacting business may be different than those described in this Prospectus. Some financial intermediaries may charge transaction fees and may set different minimum investments or limitations on buying or selling shares. Some financial intermediaries do not charge a direct transaction fee, but instead charge a fee for services such as sub-transfer agency, accounting and/or shareholder services that the financial intermediary provides on the Funds’ behalf. This fee may be based on the number of accounts or may be a percentage, currently up to 0.50% annually, of the average value of the Funds’ shareholder accounts for which the financial intermediary provides services. The Funds may pay a portion of this fee, which is intended to compensate the financial intermediary for providing the same services that would otherwise be provided by the Funds’ transfer agent or other service providers if the shares were purchased directly from the IMS Funds. To the extent that these fees are not paid entirely by the Funds, the Adviser may pay a fee to financial intermediaries for such services.

To the extent that the Adviser, not the Funds, pays a fee to a financial intermediary for distribution or shareholder services, the Adviser may consider a number of factors in determining the amount of payment associated with such services, including the amount of sales, assets invested in the Funds and the nature of the services provided by the financial intermediary. Although neither the Funds nor the Adviser pays for the Funds to be included in a financial intermediary’s “preferred list” or other promotional program, some financial intermediaries that receive compensation as described above may have such programs in which the Funds may be included. Financial intermediaries that receive these types of payments may have a conflict of interest in recommending or selling Funds’ shares rather than other mutual funds, particularly where such payments exceed those associated with other funds.

A discussion regarding the basis for the Board’s approval of the investment advisory agreement of the Funds is available in the Funds’ annual report to shareholders for each twelve-month period ended June 30.

In addition to the advisory fees described above, the Adviser may also receive certain benefits from its management of the Fund in the form of brokerage or research services received from brokers under arrangements under Section 28(e) of the Securities Act of 1934, as amended, and the terms of the Advisory Agreement. For a description of these potential benefits, see the description under “Portfolio Transactions and Brokerage Allocation -- Brokerage Selection” in the Statement of Additional Information (“SAI”).

Portfolio Manager of the Funds. Carl W. Marker has been primarily responsible for management of each of the Value Fund and the Income Fund (including each of their predecessors) since inception.

Mr. Marker currently serves as Chairman and Chief Investment Officer and has served as primary portfolio manager of the Adviser since 1988.