UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-21726

360 Funds

(Exact name of registrant as specified in charter)

| 4300 Shawnee Mission Parkway, Suite 100, Fairway, KS | 66205 |

| (Address of principal executive offices) | (Zip code) |

The Corporation Trust Company

Corporation Trust Center

1209 Orange St.

Wilmington, DE 19801

(Name and address of agent for service)

With Copies To:

John H. Lively

Practus, LLP

11300 Tomahawk Creek Parkway, Suite 310

Leawood, KS 66211

Registrant’s telephone number, including area code: 877-244-6235

Date of fiscal year end: 09/30/2019

Date of reporting period: 09/30/2019

| ITEM 1. | REPORTS TO SHAREHOLDERS |

The Annual report to Shareholders of the RVX Emerging Markets Equity Fund, a series of the 360 Funds (the “registrant”), for the year ended September 30, 2019 pursuant to Rule 30e-1 under the Investment Company Act of 1940 (the “1940 Act”) (17 CFR 270.30e-1), as amended, is filed herewith.

RVX Emerging Market Equity Fund

Institutional Class Shares (Ticker Symbol: RVEMX)

Investor Class Shares (Ticker Symbol: RVXEX)*

A Series of the

360 Funds

ANNUAL REPORT

September 30, 2019

| Investment Adviser: | Sub-Adviser: |

| Crow Point Partners, LLC | RVX Asset Management, LLC |

| 280 Summer Street, Suite M1 | 20900 NE 30th Street, Suite 401 |

| Boston, MA 02210 | Aventura, FL 33180 |

| 1-877-327-0757 |

www.crowpointfunds.com

Distributed by Matrix 360 Distributors, LLC

Member FINRA

This report is authorized for distribution only to shareholders and to others who have received a copy of the Fund’s prospectus.

IMPORTANT NOTE: Beginning on January 1, 2021, as permitted by regulations adopted by the SEC, paper copies of the RVX Emerging Market Equity Fund’s (the “Fund”) shareholder reports will no longer be sent by mail unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive all future reports in paper free of charge. You can inform the Fund or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by calling or sending an e-mail request.

* Shares not currently offered for sale.

TABLE OF CONTENTS

We are pleased to present you with the annual report for the RVX Emerging Market Fund (the “Fund”) for the year ended September 30, 2019.

For the year ended September 30, 2019, the Fund was down 4.19%(a) and the MSCI Emerging Markets Index(b) was down 1.66%. The primary reasons for the Fund’s underperformance were the overweight positions to China from a country standpoint and Energy from a sector perspective. The value style also generally underperformed the growth style in emerging markets during the time period. We continue to maintain our overweight to both areas: our holdings in China are mostly domestic-demand oriented companies with little exposure to global trade war concerns. We also believe the market is underestimating limited spare capacity and security issues in the Energy sector and would expect a gradual rise in prices that would be beneficial for the underlying equities. The Federal Reserve’s increase in interest rates during the 4th quarter of 2018 sparked a global sell-off which especially hit emerging markets; their subsequent reversal to an easing policy stance helped to recover these losses during 2019. We remain positive on the outlook for emerging markets, where growth in many economies remains robust and valuation differentials to their developed market peers are quite compelling.

The low global interest rate environment is a headwind for profitability in the financials sector, since net interest margins generally compress in these environments. Fintech has created significant disruption in the financials sector and many of the traditional financials companies are behind in creating the online ecosystems necessary to survive this paradigm shift. Our underweight may be persistent in the near-term until we are able to see these companies enact necessary changes.

The past year has been volatile for many asset classes, but emerging market equities in particular. Because of their sensitivity to U.S. dollar moves, emerging markets react quickly to swings in U.S. interest rates. That was evident this year with a boom to bust to boom cycle evident inside of one year. We do expect trade war fears to diminish and the dollar to be less volatile going forward. An additional level of concern is the Chinese economy, which is showing signs of stress, especially in its banking sector. This is a good news/bad news scenario. If the Chinese economy is indeed under pressure (our view), China will be more inclined to cut a trade deal which would likely lift markets worldwide. If the Chinese economy tips into recession (hard to know given all the state support and muddled data), it is possible it will take the global economy with it. China, as always, warrants close attention.

But, overall, we remain positive on the outlook for emerging markets, where growth in many economies remains robust and valuation differentials to their developed market peers are quite compelling.

Thank you for being a shareholder of the Crow Point funds.

Sincerely,

Crow Point Partners.

1

(a) The performance information quoted assumes the reinvestment of all dividend and capital gain distributions, if any, and represents past performance, which is not a guarantee of future results. The returns shown do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost. Updated performance data current to the most recent month-end can be obtained by calling 1-877-244-6235. Investors should consider the investment objectives, risks, charges and expenses carefully before investing or sending money. This and other important information about the Fund can be found in the Fund’s prospectus. Please read it carefully before investing.

(b) The MSCI Emerging Markets Index is a free-float weighted equity index that captures large and mid cap representation across emerging markets countries. The MSCI Emerging Markets Index covers approximately 85% of the free-float adjusted market capitalization of each country. Please note that indices do not take into account any fees and expenses of investing in the individual securities that they track and individuals cannot invest directly in any index.

2

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

September 30, 2019 (Unaudited)

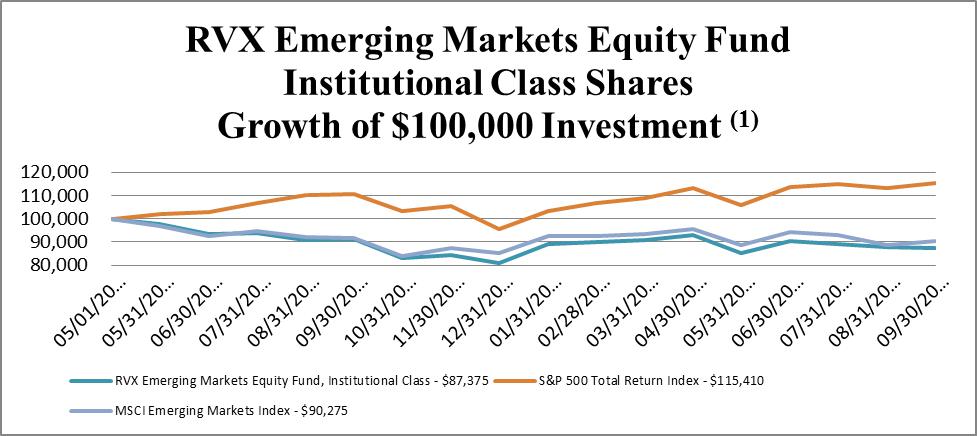

(1) The minimum initial investment for the Institutional Class is $100,000.

|

Institutional Class Returns as of September 30, 2019 |

For year ended September 30, 2019 |

Commencement of Operations through September 30, 2019* | |

| RVX Emerging Markets Equity Fund Institutional Class | (4.19)% | (9.10)% | |

| S&P 500 Total Return Index | 4.25% | 10.65% | |

| MSCI Emerging Markets Index | (1.66)% | (6.97)% |

* The RVX Emerging Markets Equity Fund Institutional Class shares commenced operations on May 1, 2018.

The performance information quoted in this annual report assumes the reinvestment of all dividend and capital gain distributions, if any, and represents past performance, which is not a guarantee of future results. The returns shown do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost. Updated performance data current to the most recent month-end can be obtained by calling 1-877-244-6235.

The above graph depicts the performance of the Fund versus the S&P 500 Total Return Index (“S&P 500”) and the MSCI Emerging Markets Index (“MSCI EM”). The S&P 500 is a broad unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general. Index returns assume reinvestment of dividends. The MSCI EM is a free-float weighted equity index that captures large and mid-cap representation across emerging markets countries. Investors may not invest in any index directly; unlike the Fund’s returns, each Index does not reflect any fees or expenses. The Fund will generally not invest in all the securities comprising each index.

3

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

INVESTMENT HIGHLIGHTS

September 30, 2019 (Unaudited)

The investment objective of the RVX Emerging Markets Equity Fund (the “Fund”) is to seek long-term capital appreciation through investments in equity securities of emerging market companies.

Crow Point Partners, LLC (the “Adviser”) serves as Investment Adviser to the Fund. As the Fund’s investment adviser, the Adviser reviews, supervises and administers the Fund’s investment program and also ensures compliance with the Fund’s investment policies and guidelines. RVX Asset Management, LLC (the “Sub-Adviser”) serves as the Sub-Adviser to the Fund. The Sub-Adviser is responsible for selecting the Fund’s portfolio investments.

The Fund normally invests at least 80% of its net assets, including any borrowings for investment purposes, in a diversified portfolio of equity securities of companies that are tied economically to emerging markets (including frontier market countries) with up to 20% of the Fund’s net assets in frontier markets. The Fund will notify its shareholders at least 60 days before changing this policy. The Fund may also invest up to 20% of its net assets in developed markets. In seeking to achieve its investment objective, the Fund will allocate up to 100% of its portfolio in equity securities and other securities with equity characteristics, including but not limited to common stocks, preferred stocks, warrants (including participatory notes structured as warrants), rights (which are issued by a company to allow holders to subscribe for additional securities issued by that company), real estate investment trusts (REITs), convertible securities, depositary receipts, and derivatives (such as total return swaps, participatory notes, and currency hedges). The Fund may also invest in equity securities indirectly through the purchase of closed-end investment companies and exchange-traded funds (together, the “Underlying Funds”) that invest primarily in equity securities.

The Fund will generally invest in equity securities of those companies tied to emerging and frontier markets (i) that are listed on an exchange in an emerging market or frontier market country, (ii) that are legally domiciled in an emerging market or frontier market country; (iii) that have at least 50% of their assets in an emerging market or frontier market country; (iv) or that derive at least 50% of their revenues or profits from goods produced or sold, investments made, or services provided in an emerging market or frontier market country. The Sub-Adviser believes that emerging and frontier markets countries offer investment opportunities that arise from long-term trends in demographics, deregulation, offshore outsourcing and improving corporate governance.

Allocation of Portfolio Holdings

| Country | Percentage of Net Assets* | |||

| China | 33.21 | % | ||

| South Korea | 9.40 | % | ||

| Thailand | 6.69 | % | ||

| Brazil | 5.73 | % | ||

| Indonesia | 5.72 | % | ||

| South Africa | 5.49 | % | ||

| United States | 3.85 | % | ||

| Taiwan | 3.60 | % | ||

| Greece | 3.49 | % | ||

| Cyprus | 2.62 | % | ||

| Philippines | 1.96 | % | ||

| Malaysia | 1.93 | % | ||

| Macau | 1.84 | % | ||

| India | 1.73 | % | ||

| Singapore | 1.72 | % | ||

| UAE | 1.57 | % | ||

| Hong Kong | 1.48 | % | ||

| Egypt | 1.48 | % | ||

| Guernsey | 1.30 | % | ||

| Netherlands | 0.79 | % | ||

| Cash and Cash Equivalents | 4.40 | % | ||

| 100.00 | % | |||

* The percentages in the above table are based on the portfolio holdings of the Fund as of September 30, 2019 and are subject to change. For a detailed break-out of holdings by industry and investment type, please refer to the Schedule of Investments.

4

RVX EMERGING MARKETS EQUITY FUND

| September 30, 2019 | ANNUAL REPORT |

| COMMON STOCK - 92.13% | Shares | Value | ||||||

| Aerospace & Defense - 2.06% | ||||||||

| Embraer SA - ADR - Brazil | 7,892 | $ | 136,137 | |||||

| Auto Manufacturers - 2.11% | ||||||||

| Guangzhou Automobile Group Co. Ltd. - China | 146,000 | 139,692 | ||||||

| Banks - 7.01% | ||||||||

| Bank of China Ltd. - China | 288,000 | 113,162 | ||||||

| Bank of the Philippine Islands - Philippines | 72,190 | 129,498 | ||||||

| Bank Rakyat Indonesia Persero Tbk PT - Indonesia | 339,700 | 98,596 | ||||||

| National Bank of Greece SA - Greece (a) | 40,194 | 122,365 | ||||||

| 463,621 | ||||||||

| Beverages - 3.73% | ||||||||

| Thai Beverage PCL - Thailand | 385,400 | 246,783 | ||||||

| Commercial Services - 2.62% | ||||||||

| QIWI PLC - ADR - Cyprus | 7,889 | 173,164 | ||||||

| Diversified Financial Services - 1.81% | ||||||||

| KB Financial Group, Inc. - ADR - South Korea | 3,359 | 119,983 | ||||||

| Electric - 1.48% | ||||||||

| China Longyuan Power Group Corp. Ltd. - China | 174,000 | 97,669 | ||||||

| Electronics - 1.73% | ||||||||

| Venture Corp. Ltd. - Singapore | 10,300 | 114,097 | ||||||

| Energy - Alternate Sources - 1.48% | ||||||||

| China Everbright International Ltd. - Hong Kong | 127,000 | 97,858 | ||||||

| Food - 2.04% | ||||||||

| Indofood Sukses Makmur Tbk PT - Indonesia | 248,100 | 134,580 | ||||||

| Insurance - 3.13% | ||||||||

| Ping An Insurance Group Co. of China Ltd. - China | 18,000 | 206,782 | ||||||

| Internet - 12.81% | ||||||||

| Alibaba Group Holding Ltd. - ADR - China (a) | 1,624 | 271,582 | ||||||

| Baidu, Inc. - ADR - China (a) | 1,311 | 134,718 | ||||||

| iQIYI Inc. - ADR - China (a) | 5,731 | 92,441 | ||||||

| My EG Services Bhd - Malaysia | 381,200 | 127,440 | ||||||

| Naspers Ltd. - ADR - South Africa | 3,596 | 107,736 | ||||||

| Tencent Music Entertainment Group - ADR - China (a) | 8,881 | 113,410 | ||||||

| 847,327 | ||||||||

| Investment Companies - .79% | ||||||||

| Prosus NV - ADR - Netherlands (a) | 3,596 | 52,394 | ||||||

5

RVX EMERGING MARKETS EQUITY FUND

SCHEDULE OF INVESTMENTS

| September 30, 2019 | ANNUAL REPORT |

| COMMON STOCK - 92.13% (continued) | Shares | Value | ||||||

| Iron & Steel - 1.58% | ||||||||

| POSCO - ADR - South Korea | 2,218 | $ | 104,601 | |||||

| Lodging - 1.84% | ||||||||

| Sands China Ltd. - Macau | 26,800 | 121,372 | ||||||

| Media - 1.76% | ||||||||

| MultiChoice Group - ADR - South Africa (a) | 15,134 | 116,229 | ||||||

| Mining - 2.10% | ||||||||

| Harmony Gold Mining Co Ltd. - ADR - South Africa (a) | 48,910 | 138,904 | ||||||

| Oil & Gas - 8.18% | ||||||||

| China Petroleum & Chemical Corp. - ADR - China | 1,418 | 83,237 | ||||||

| CNOOC Ltd. - ADR - China | 840 | 127,890 | ||||||

| Kosmos Energy Ltd. - United States | 17,838 | 111,309 | ||||||

| PetroChina Co. Ltd. - ADR - China | 2,082 | 105,786 | ||||||

| Petroleo Brasileiro SA - ADR - Brazil | 7,805 | 112,938 | ||||||

| 541,160 | ||||||||

| Oil & Gas Services - 4.33% | ||||||||

| Anton Oilfield Services Group/Hong Kong - China | 896,000 | 89,158 | ||||||

| China Oilfield Services Ltd. - China | 116,000 | 138,661 | ||||||

| Hilong Holding Ltd. - China | 542,000 | 58,773 | ||||||

| 286,592 | ||||||||

| Pharmaceuticals - 5.17% | ||||||||

| Dr Reddy’s Laboratories Ltd. - ADR - India | 3,014 | 114,200 | ||||||

| Hypera SA - Brazil | 16,100 | 129,914 | ||||||

| Ibnsina Pharma SAE - Egypt | 159,664 | 97,872 | ||||||

| 341,986 | ||||||||

| Real Estate - 2.95% | ||||||||

| Amata Corp. PCL - Thailand | 239,100 | 195,343 | ||||||

| Retail - 3.84% | ||||||||

| JUMBO SA - Greece | 5,730 | 108,738 | ||||||

| Matahari Department Store Tbk PT - Indonesia | 601,600 | 145,367 | ||||||

| 254,105 | ||||||||

| Semiconductors - 7.62% | ||||||||

| Samsung Electronics Co Ltd. - ADR - South Korea | 261 | 265,698 | ||||||

| Taiwan Semiconductor Manufacturing Co. Ltd. - ADR - Taiwan | 5,121 | 238,024 | ||||||

| 503,722 | ||||||||

| Software - 4.68% | ||||||||

| Momo, Inc. - ADR - China | 3,422 | 106,014 | ||||||

| NetEase, Inc. - ADR - China | 765 | 203,628 | ||||||

| 309,642 | ||||||||

| Telecommunications - 1.99% | ||||||||

| KT Corp. - ADR - South Korea | 11,617 | 131,388 | ||||||

6

RVX EMERGING MARKETS EQUITY FUND

SCHEDULE OF INVESTMENTS

| September 30, 2019 | ANNUAL REPORT |

| COMMON STOCK - 92.13% (continued) | Shares | Value | ||||||

| Transportation - 3.28% | ||||||||

| Aramex PJSC - United Arab Emirates | 95,122 | $ | 103,852 | |||||

| ZTO Express Cayman, Inc. - ADR - China | 5,515 | 113,369 | ||||||

| 217,221 | ||||||||

| TOTAL COMMON STOCK (Cost $6,637,557) | 6,092,352 | |||||||

| EXCHANGE-TRADED FUNDS - 2.17% | ||||||||

| iShares MSCI India Small-Cap ETF - United States | 4,076 | 143,312 | ||||||

| TOTAL EXCHANGE-TRADED FUNDS (Cost $155,039) | 143,312 | |||||||

| CLOSED-END FUNDS - 1.30% | ||||||||

| VinaCapital Vietnam Opportunity Fund Ltd. - Guernsey | 20,469 | 85,937 | ||||||

| TOTAL CLOSED-END FUNDS (Cost $90,144) | 85,937 | |||||||

| SHORT-TERM INVESTMENT - 3.73% | ||||||||

| Federated Government Obligations Fund - Institutional Class, 2.29% (b) | 246,505 | 246,505 | ||||||

| TOTAL SHORT-TERM INVESTMENT (Cost $246,505) | 246,505 | |||||||

| TOTAL INVESTMENTS (Cost $7,129,245) – 99.32% | 6,568,106 | |||||||

| OTHER ASSETS IN EXCESS OF LIABILITIES, NET - 0.68% | 44,728 | |||||||

| NET ASSETS - 100% | $ | 6,612,834 | ||||||

(a) Non-income producing security.

(b) Rate shown represents the 7-day effective yield at September 30, 2019, is subject to change and resets daily.

ADR - American Depositary Receipt.

ETF - Exchange-Traded Fund

PCL - Public Company Limited

The accompanying notes are an integral part of these financial statements.

7

RVX Emerging Markets Equity Fund

Statement of Assets and Liabilities

September 30, 2019

| Assets: | ||||

| Investment securities: | ||||

| At cost | $ | 7,129,245 | ||

| Total securities at cost | $ | 7,129,245 | ||

| At value | 6,568,106 | |||

| Cash | 1,039 | |||

| Due from adviser | 38,902 | |||

| Receivables: | ||||

| Interest | 97 | |||

| Dividends | 14,035 | |||

| Prepaid expenses | 2,141 | |||

| Total assets | 6,624,320 | |||

| Liabilities: | ||||

| Due to administrator | 6,641 | |||

| Accrued expenses | 4,845 | |||

| Total liabilities | 11,486 | |||

| Net Assets | $ | 6,612,834 | ||

| Sources of Net Assets: | ||||

| Paid-in capital | $ | 7,309,749 | ||

| Total distributable earnings | (696,915 | ) | ||

| Total Net Assets | $ | 6,612,834 | ||

| Institutional Class Shares: | ||||

| Net assets | $ | 6,612,834 | ||

| Shares Outstanding (Unlimited shares of beneficial interest authorized) | 765,301 | |||

| Net Asset Value, Offering and Redemption Price Per Share | $ | 8.64 | ||

The accompanying notes are an integral part of these financial statements.

8

RVX Emerging Markets Equity Fund

September 30, 2019

| For the Year Ended September 30, 2019 | ||||

| Investment income: | ||||

| Dividends (net of foreign withholding taxes of $12,207) | $ | 137,107 | ||

| Interest | 3,742 | |||

| Total investment income | 140,849 | |||

| Expenses: | ||||

| Management fees (Note 5) | 54,923 | |||

| Accounting and transfer agent fees and expenses | 52,699 | |||

| Professional fees | 29,278 | |||

| Compliance officer fees | 15,750 | |||

| Trustee fees and expenses | 21,878 | |||

| Custodian fees | 15,217 | |||

| Pricing fees | 14,694 | |||

| Dealer network fees | 8,924 | |||

| Registration and filing fees | 5,930 | |||

| Miscellaneous | 4,023 | |||

| Insurance | 1,569 | |||

| Printing & Mailing | 838 | |||

| Total expenses | 225,723 | |||

| Less expense reimbursement: | ||||

| Fees waived/reimbursed by Adviser | (138,800 | ) | ||

| Fees waived by Administrator | (10,625 | ) | ||

| Net expenses | 76,298 | |||

| Net investment Income | 64,551 | |||

| Realized and unrealized loss: | ||||

| Net realized loss on: | ||||

| Investments | (124,825 | ) | ||

| Foreign currency transactions | (3,436 | ) | ||

| Net realized loss on investments and foreign currency transactions | (128,261 | ) | ||

| Net change in unrealized depreciation on: | ||||

| Investments | (176,886 | ) | ||

| Foreign currency translations | (81 | ) | ||

| Net change in unrealized depreciation on investments and foreign currency translations | (176,967 | ) | ||

| Net loss on investments and foreign currency | (305,228 | ) | ||

| Net decrease in net assets resulting from operations | $ | (240,677 | ) | |

The accompanying notes are an integral part of these financial statements.

9

RVX Emerging Markets Equity Fund

Statements of Changes in Net Assets

| For the Year Ended September 30, 2019 | For the Period Ended September 30, 2018 (a) | |||||||

| Increase (decrease) in net assets from: | ||||||||

| Operations: | ||||||||

| Net investment income | $ | 64,551 | $ | 59,671 | ||||

| Net realized loss on investments and foreign currency transactions | (128,261 | ) | (71,387 | ) | ||||

| Net change in unrealized depreciation on investments and foreign currency translations | (176,967 | ) | (384,238 | ) | ||||

| Net decrease in net assets resulting from operations | (240,677 | ) | (395,954 | ) | ||||

| Distributions to shareholders from: | ||||||||

| Total distributable earnings - Institutional Class | (60,284 | ) | — | |||||

| Total distributions | (60,284 | ) | — | |||||

| Transactions in shares of beneficial interest: | ||||||||

| Proceeds from shares sold: | ||||||||

| Institutional Class | 1,509,198 | 6,900,000 | ||||||

| Net asset value of shares issued in reinvestment of distributions: | ||||||||

| Institutional Class | 58,016 | — | ||||||

| Payments for shares redeemed: | ||||||||

| Institutional Class | (407,465 | ) | (750,000 | ) | ||||

| Increase in net assets from transactions in shares of beneficial interest | 1,159,749 | 6,150,000 | ||||||

| Increase in net assets | 858,788 | 5,754,046 | ||||||

| Net Assets: | ||||||||

| Beginning of year/period | 5,754,046 | — | ||||||

| End of year/period | $ | 6,612,834 | $ | 5,754,046 | ||||

| Share activity: | ||||||||

| Institutional Class: | ||||||||

| Shares sold | 173,152 | 712,106 | ||||||

| Shares reinvested | 7,298 | — | ||||||

| Shares redeemed | (45,733 | ) | (81,522 | ) | ||||

| Net increase in shares of beneficial interest | 134,717 | 630,584 | ||||||

| (a) The RVX Emerging Markets Equity Fund commenced operations on May 1, 2018. | ||||||||

| The accompanying notes are an integral part of these financial statements. | ||||||||

10

RVX Emerging Markets Equity Fund

The following tables set forth the per share operating performance data for a share of beneficial interest outstanding, total return ratios to average net assets and other supplemental data for the year or period indicated.

| Institutional Class | ||||||||

| For

the Year Ended September 30, 2019 | For

the Period Ended September 30, 2018 (a) | |||||||

| Net Asset Value, Beginning of Year/Period | $ | 9.12 | $ | 10.00 | ||||

| Investment Operations: | ||||||||

| Net investment income (b) | 0.09 | 0.12 | ||||||

| Net realized and unrealized loss on investments | (0.48 | ) | (1.00 | ) | ||||

| Total from investment operations | (0.39 | ) | (0.88 | ) | ||||

| Distributions: | ||||||||

| From net investment income | (0.09 | ) | — | |||||

| Total distributions | (0.09 | ) | — | |||||

| Net Asset Value, End of Year/Period | $ | 8.64 | $ | 9.12 | ||||

| Total Return (c) | (4.19 | )% | (8.80 | )%(e) | ||||

| Ratios/Supplemental Data | ||||||||

| Net assets, end of year/period (in 000’s) | $ | 6,613 | $ | 5,754 | ||||

| Ratios of expenses to average net assets: | ||||||||

| Before fees waived and expenses reimbursed (d) | 3.70 | % | 4.63 | %(f) | ||||

| After fees waived and expenses reimbursed | 1.25 | % | 1.25 | %(f) | ||||

| Ratios of net investment income to average net assets | 1.06 | % | 3.03 | %(f) | ||||

| Portfolio turnover rate | 33 | % | 31 | %(e) | ||||

| (a) | The RVX Emerging Markets Equity Fund commenced operations on May 1, 2018. |

| (b) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (c) | Total Return represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of dividends. |

| (d) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the Adviser. |

| (e) | Not annualized |

| (f) | Annualized |

The accompanying notes are an integral part of these financial statements.

11

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

NOTES

TO THE FINANCIAL STATEMENTS

September 30, 2019

| 1. | ORGANIZATION |

The RVX Emerging Markets Equity Fund (the “Fund”) was organized on March 19, 2018 as a diversified series of 360 Funds (the “Trust”). The fund commenced operations on May 1, 2018. The Trust was organized on February 24, 2005 as a Delaware statutory trust. The Trust is registered as an open-end management investment company under the Investment Company Act of 1940 (the “1940 Act”). The Fund’s investment objective is to seek long-term capital appreciation through investments in equity securities of emerging market companies. The Fund’s investment adviser is Crow Point Partners, LLC (the “Adviser”). The Fund’s sub-adviser is RVX Asset Management, LLC (the Sub-Adviser). The Fund has two classes of shares, Institutional Class and Investor Class, but currently offers only the Investor Class..

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of the significant accounting policies followed by the Fund in the preparation of its financial statements. The Fund is an investment company that follows the accounting and reporting guidance of Accounting Standards Codification Topic 946 applicable to investment companies.

a) Security Valuation – All investments in securities are recorded at their estimated fair value, as described in note 2.

b) Investment Companies – The Fund may invest in investment companies such as open-end funds (mutual funds), exchange traded funds (“ETFs”) and closed-end funds (also referred to as “Underlying Funds”) subject to limitations as defined in the Investment Company Act of 1940. Your cost of investing in the Fund will generally be higher than the cost of investing directly in the Underlying Funds. By investing in the Fund, you will indirectly bear fees and expenses charged by the Underlying Funds in which the Fund invests in addition to the Fund’s direct fees and expenses. Also, with respect to dividends paid by the Underlying Funds, it is possible for these dividends to exceed the underlying investments’ taxable earnings and profits resulting in the excess portion of such dividends being designated as a return of capital. Distributions received from investments in securities that represent a return of capital or capital gains are recorded as a reduction of the cost of investments or as a realized gain, respectively.

c) Federal Income Taxes – The Fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). It is the policy of the Fund to comply with the requirements of the Code applicable to regulated investment companies and to distribute substantially all of its net investment company taxable income and net capital gains. The Fund also intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. Therefore, no federal income tax or excise provision is required.

As of and during the year ended September 30, 2019, the Fund did not have a liability for any unrecognized tax expenses. The Fund recognizes interest and penalties, if any, related to unrecognized tax liability as income tax expense in the statement of operations. During the year ended September 30, 2019, the Fund did not incur any interest or penalties. The Fund identifies its major tax jurisdictions as U.S. Federal and Delaware state.

In addition, accounting principles generally accepted in the United States of America (“GAAP”) requires management of the Fund to analyze all open tax years, as defined by IRS statute of limitations for all major industries, including federal tax authorities and certain state tax authorities. Management has reviewed the Fund’s tax positions to be taken on federal income tax returns for the open tax periods ended September 30, 2018 and September 30, 2019 and has determined that the Fund does not have a liability for uncertain tax positions. The Fund has no examinations in progress and is not aware of any tax positions for which it is reasonably possible that the total tax amounts of unrecognized tax benefits will significantly change in the next twelve months.

d) Distributions to Shareholders – Dividends from net investment income and distributions of net realized capital gains, if any, will be declared and paid at least annually. Income and capital gain distributions, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. GAAP requires that permanent financial reporting differences relating to shareholder distributions be reclassified to paid-in capital or net realized gains.

e) Use of Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

12

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

NOTES

TO THE FINANCIAL STATEMENTS

September 30, 2019

| 2. | SIGNIFICANT ACCOUNTING POLICIES (continued) |

f) Other – Investment and shareholder transactions are recorded on trade date. The Fund determines the gain or loss realized from the investment transactions by comparing the original cost of the security lot sold with the net sales proceeds. Dividend income is recognized on the ex-dividend date or as soon as information is available to the Fund and interest income is recognized on an accrual basis. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

g) Foreign Currency Translation – Portfolio securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars based on the exchange rate of such currencies against U.S. dollars on the date of valuation. Purchases and sales of securities and income items denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date. The Fund does not separately report the effect of changes in foreign exchange rates from changes in market prices on securities held. Such changes are included in net realized and unrealized gain or loss from investments. Realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions and the difference between the recorded amounts of dividends, interest and foreign withholding taxes, and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains or losses arise from changes in foreign exchange rates on foreign currency denominated assets and liabilities other than investments in securities held at the end of the reporting period.

| 3. | SECURITIES VALUATIONS |

Processes and Structure

The Fund’s Board of Trustees has adopted guidelines for valuing securities and other derivative instruments including in circumstances in which market quotes are not readily available, and has delegated authority to the Adviser to apply those guidelines in determining fair value prices, subject to review by the Board of Trustees.

Hierarchy of Fair Value Inputs

The Fund utilizes various methods to measure the fair value of most of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation techniques used to measure fair value. The three levels of inputs are as follows:

| • | Level 1 – Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. |

| • | Level 2 – Observable inputs other than quoted prices included in level 1 that are observable for the asset or liability either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates, and similar data. |

| • | Level 3 – Unobservable inputs for the asset or liability to the extent that relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions that a market participant would use in valuing the asset or liability, and that would be based on the best information available. |

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

13

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

NOTES

TO THE FINANCIAL STATEMENTS

September 30, 2019

| 3. | SECURITIES VALUATIONS (continued) |

Fair Value Measurements

A description of the valuation techniques applied to the Trust’s major categories of assets and liabilities measured at fair value on a recurring basis follows.

Equity securities (common stock and ETFs) – Securities traded on a national securities exchange (or reported on the NASDAQ national market) are stated at the last reported sales price on the day of valuation. To the extent these securities are actively traded, and valuation adjustments are not applied, they are categorized in level 1 of the fair value hierarchy. Certain foreign securities may be fair valued using a pricing service that considers the correlation of the trading patterns of the foreign security to the intraday trading in the U.S. markets for investments such as American Depositary Receipts, financial futures, Exchange Traded Funds, and the movement of the certain indexes of securities based on a statistical analysis of the historical relationship and that are categorized in level 2. Preferred stock and other equities traded on inactive markets or valued by reference to similar instruments are also categorized in level 2.

Money market funds – Money market funds are valued at their net asset value of $1.00 per share and are categorized as level 1.

Derivative instruments – Listed derivatives, including options, that are actively traded, are valued based on quoted prices from the exchange and categorized in level 1 of the fair value hierarchy. Options held by the Fund for which no current quotations are readily available and which are not traded on the valuation date are valued at the mean price and are categorized within level 2 of the fair value hierarchy. Over-the-counter (OTC) derivative contracts include forward, swap, and option contracts related to interest rates; foreign currencies; credit standing of reference entities; equity prices; or commodity prices, and warrants on exchange-traded securities. Depending on the product and terms of the transaction, the fair value of the OTC derivative products can be modeled taking into account the counterparties’ creditworthiness and using a series of techniques, including simulation models. Many pricing models do not entail material subjectivity because the methodologies employed do not necessitate significant judgments, and the pricing inputs are observed from actively quoted markets, as is the case of interest rate swap and option contracts. OTC derivative products valued using pricing models are categorized within level 2 of the fair value hierarchy.

In accordance with the Trust’s good faith pricing guidelines, the Adviser is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. No single standard exists for determining fair value, because fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of an issue of securities being valued by the Adviser would appear to be the amount which the owner might reasonably expect to receive for them upon their current sale. Methods which are in accordance with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt issues, or a combination of these and other methods. Good faith pricing is permitted if, in the Adviser’s opinion, the validity of market quotations appears to be questionable based on factors such as evidence of a thin market in the security based on a small number of quotations, a significant event occurs after the close of a market but before the Fund’s NAV calculation that may affect a security’s value, or the Adviser is aware of any other data that calls into question the reliability of market quotations. Good faith pricing may also be used in instances when the bonds in which the Fund invests may default or otherwise cease to have market quotations readily available.

The Trustees of the Trust adopted the M3Sixty Consolidated Valuation Procedures, which established a Valuation Committee to work with the Adviser and report to the Board of Trustees (the “Board”) on securities being fair valued or manually priced. The Independent Chairman and Trustee of the Trust, along with the Trust’s Principal Financial Officer and Chief Compliance Officer and other officers of the Trust are members of the Valuation Committee which meets at least monthly or, as required, to review the interim actions and coordination with the Adviser in pricing fair valued securities, and consideration of any unresolved valuation issue or a request to change the methodology for manually pricing a security. In turn, the Independent Chairman provides updates to the Board at the regularly scheduled board meetings as well as interim updates to the board members on substantive changes in a daily valuation or methodology issue.

If

the Adviser decides that a price provided by the pricing service does not accurately reflect the fair value of the securities,

when prices are not readily available from a pricing service, or when certain restricted or illiquid securities are being valued,

securities are valued at fair value as determined in good faith by the Adviser, in conformity with guidelines adopted by and subject

to review of the Board and the Fair Valuation Committee. These securities will be categorized as level 3 securities.

14

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

NOTES

TO THE FINANCIAL STATEMENTS

September 30, 2019

| 3. | SECURITIES VALUATIONS (continued) |

The following tables summarize the inputs used to value the Fund’s assets and liabilities measured at fair value as of September 30, 2019.

| Financial Instruments – Assets | ||||||||||||||||

| Security Classification | Level 1 | Level 2 | Level 3 | Totals | ||||||||||||

| Common Stock (1) | $ | 6,092,352 | $ | — | $ | — | $ | 6,092,352 | ||||||||

| Exchange-Traded Funds (1) | 143,312 | — | — | 143,312 | ||||||||||||

| Closed-End Funds (1) | 85,937 | — | — | 85,937 | ||||||||||||

| Short-Term Investments | 246,505 | — | — | 246,505 | ||||||||||||

| Total Assets | $ | 6,568,106 | $ | — | $ | — | $ | 6,568,106 | ||||||||

(1) For a detailed break-out of common stock, closed-end funds by industry or asset class, please refer to the Schedule of Investments.

There were no transfers into and out of any level during the year ended September 30, 2019. It is the Fund’s policy to recognize transfers between levels at the end of the reporting period.

| 4. | INVESTMENT TRANSACTIONS |

For the year ended September 30, 2019, aggregate purchases and sales of investment securities (excluding short-term investments) for the Fund were as follows:

| Purchases | Sales | |||||

| $ | 3,084,258 | $ | 1,965,004 | |||

There were no Government securities purchased or sold during the period.

| 5. | ADVISORY FEES AND OTHER RELATED PARTY TRANSACTIONS |

The Fund has entered into an Investment Advisory Agreement (the “Advisory Agreement”) with the Adviser. As the Fund’s investment adviser, the Adviser reviews, supervises and administers the Fund’s investment program and also ensures compliance with the Fund’s investment policies and guidelines.

The Adviser is responsible for selecting the Fund’s sub-advisor(s), subject to approval by the Board. The Adviser selects a sub-advisor that has shown good investment performance in its areas of expertise. Crow Point considers various factors in evaluating a sub-advisor, including: (i) level of knowledge and skill; (ii) performance as compared to its peers or benchmark; (iii) level of compliance with investment rules and strategies; (iv) employees’ facilities and financial strength; and (v) quality of service.

The Adviser has entered into an Investment Sub-Advisory Agreement with the Sub-Adviser. The Adviser will also continually monitor the Sub-Adviser’s performance through various analyses and through in person, telephone, and written consultations with the Sub-Adviser. The Adviser discusses its expectations for performance with the Sub-Adviser and provides evaluations and recommendations to the Board, including whether or not the Sub-Adviser’s contract should be renewed, modified, or terminated.

The Adviser is also responsible for running all of the operations of the Fund, except those that are subcontracted to the Sub-Adviser, custodian, transfer agent, administrative agent, or other parties. For its services, the Adviser is entitled to receive an investment advisory fee from the Fund at an annualized rate of 0.90%, based on the average daily net assets of the Fund. Crow Point pays a sub-advisory fee to the Sub-Adviser from its advisory fee. For the annual period ended September 30, 2019, the Adviser earned $54,923 of advisory fees.

15

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

NOTES

TO THE FINANCIAL STATEMENTS

September 30, 2019

| 5. | ADVISORY FEES AND OTHER RELATED PARTY TRANSACTIONS (continued) |

The Adviser has entered into a written expense limitation agreement, through at least March 31, 2021, under which it has agreed to limit the total expenses of the Fund (excluding interest, taxes, brokerage fees and commissions, other expenditures that are capitalized in accordance with generally accepted accounting principles, acquired fund fees and expenses, other extraordinary expenses not incurred in the ordinary course of the Fund’s business, interest and dividend expense on securities sold short, and amounts, if any payable pursuant to a plan adopted in accordance with Rule 12b-1 under the Investment Company Act of 1940, as amended (the “1940 Act”) to an annual rate of 1.25% of the average daily net assets of the Fund. Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Fund within three fiscal years following the fiscal year in which the expense was incurred, provided that the Fund is able to make the repayment without exceeding the expense limitation in place at the time of the waiver or reimbursement and at the time the waiver or reimbursement is recouped. This expense cap agreement may be terminated by either party upon 90 days’ written notice provided that, in the case of termination by the Adviser, such action shall be authorized by resolution of a majority of the Independent Trustees of the Trust or by a vote of a majority of the outstanding voting securities of the Fund.

For the year ended September 30, 2019, the Adviser waived advisory fees of $54,923 and reimbursed expenses of $83,877.

Expense waivers and reimbursements are subject to possible recoupment from the Funds in future years on a rolling three year basis (within the three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits. As of September 30, 2019, the total amount of expenses waived/reimbursed subject to recapture and their expiration dates, pursuant to the waiver agreements, was as follows:

| Amount Subject to Recoupment | Expiration Dates | |||

| $ | 61,352 | September 30, 2021 | ||

| 138,800 | September 30, 2022 | |||

The Fund has entered into an Investment Company Services Agreement (“ICSA”) with M3Sixty Administration, LLC (“M3Sixty”). Pursuant to the ICSA, M3Sixty is responsible for a wide variety of functions, including but not limited to: (a) Fund accounting services; (b) financial statement preparation; (c) valuation of the Fund’s portfolio securities; (d) pricing the Fund’s shares; (e) assistance in preparing tax returns; (f) preparation and filing of required regulatory reports; (g) communications with shareholders; (h) coordination of Board and shareholder meetings; (i) monitoring the Fund’s legal compliance; and (j) maintaining shareholder account records.

For the year ended September 30, 2019, M3Sixty earned $52,699, including out of pocket expenses.

The Fund has also entered into a Chief Compliance Officer Service Agreement (“CCO Agreement”) with M3Sixty. Pursuant to the CCO Agreement, M3Sixty agrees to provide a Chief Compliance Officer (“CCO”), as described in Rule 38a-l of the 1940 Act, to the Fund for the period and on the terms and conditions set forth in the CCO Agreement. Pursuant to the CCO Agreement, M3Sixty earned $15,750 during the year ended September 30, 2019.

M3Sixty has also agreed to voluntarily waive certain fees until certain thresholds are met by the Fund. During the annual period ended September 30, 2019, M3Sixty waived $10,625 of fees.

Certain officers and an interested Trustee of the Trust are also employees or officers of M3Sixty.

Matrix 360 Distributors, LLC (the “Distributor”) acts as the principal underwriter and distributor of the Fund’s shares for the purpose of facilitating the registration of shares of the Fund under state securities laws and to assist in sales of the Fund’s shares pursuant to a Distribution Agreement (the “Distribution Agreement”) approved by the Trustees. The Distribution Agreement between the Fund and the Distributor requires the Distributor to use all reasonable efforts in connection with the distribution of the Fund’s shares. However, the Distributor has no obligation to sell any specific number of shares and will only sell shares for orders it receives.

The Distributor is an affiliate of M3Sixty.

16

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

NOTES

TO THE FINANCIAL STATEMENTS

September 30, 2019

| 5. | ADVISORY FEES AND OTHER RELATED PARTY TRANSACTIONS (continued) |

The Fund with respect to its Investor Class shares has adopted a Distribution Plan in accordance with Rule 12b-1 (“Distribution Plan”) under the 1940 Act. The Distribution Plan provides that the Fund may compensate or reimburse the Distributor for services rendered and expenses borne in connection with activities primarily intended to result in the sale of the Fund’s shares (this compensation is commonly referred to as “12b-1 fees”).

| 6. | EMERGING AND FRONTIER MARKETS RISK |

Additional risks are involved when investing in countries with emerging economies or securities markets. The Fund invests primarily in emerging and frontier market issuers. Emerging and frontier market countries generally are located in the Asia and Pacific regions, the Middle East, Eastern Europe, Central and South America and Africa. Such countries may include, but are not limited to, Angola, Argentina, Azerbaijan, Bahrain, Bangladesh, Belarus, Belize, Bolivia, Brazil, Bulgaria, Chile, China, Colombia, Costa Rica, Cote D’Ivoire, Croatia, Dominican Republic, Ecuador, Egypt, El Salvador, Gabon, Georgia, Ghana, Guatemala, Honduras, Hungary, India, Indonesia, Iraq, Jamaica, Jordan, Kazakhstan, Latvia, Lebanon, Lithuania, Malaysia, Mexico, Mongolia, Morocco, Namibia, Nigeria, Pakistan, Panama, Paraguay, Peru, Philippines, Poland, Romania, Russia, Senegal, Serbia, South Africa, Sri Lanka, Tanzania, Turkey, Ukraine, Uruguay, Venezuela, Vietnam, Zambia and Zimbabwe. Political and economic structures in many of these countries may be undergoing significant evolution and rapid development, and these countries may lack the social, political and economic stability characteristics of developed countries. In general, the securities markets of these countries are less liquid, are especially subject to greater price volatility, have smaller market capitalizations, have less government regulation and are not subject to as frequent accounting, financial and other reporting requirements as the securities markets of more developed countries as has historically been the case. As a result, the risks presented by investments in these countries are heightened. These countries also have problems with securities registration and custody.

Additionally, settlement procedures in emerging and frontier market countries are frequently less developed and reliable than those in the United States, and may involve the Fund’s delivery of securities before receipt of payment for their sale. Settlement or registration problems may make it more difficult for the Fund to value its portfolio securities and could cause the Fund to miss attractive investment opportunities, to have a portion of its assets un-invested or to incur losses due to the failure of a counterparty to pay for securities the Fund has delivered or the Fund’s inability to complete its contractual obligations. The Fund’s purchase and sale of portfolio securities in certain emerging and frontier market countries may be constrained by limitations relating to daily changes in the prices of listed securities, periodic trading or settlement volume and/or limitations on aggregate holdings of foreign investors. Such limitations may be computed based on the aggregate trading volume or holdings of the Fund, the Sub-Adviser, their affiliates and their respective clients and other service providers. The Fund may not be able to sell securities in circumstances where price, trading or settlement volume limitations have been reached. As a result of these and other risks, investments in these countries generally present a greater risk of loss to the Fund. Investments in some emerging and frontier market countries, such as those located in Asia, may be restricted or controlled. In some countries, direct investments in securities may be prohibited and required to be made through investment funds controlled by such countries. These limitations may increase transaction costs and adversely affect a security’s liquidity, price, and the rights of the Fund in connection with the security. Unanticipated political, economic or social developments may affect the value of the Fund’s investments in emerging and frontier market countries and the availability to the Fund of additional investments in these countries. Some of these countries may in the past have failed to recognize private property rights and have at times nationalized or expropriated the assets of private companies. There have been occasional limitations on the movements of funds and other assets between different countries. The small size and inexperience of the securities markets in certain of such countries and the limited volume of trading in securities in those countries may make the Fund’s investments in such countries illiquid and more volatile than investments in Japan or most Western European countries, and the Fund may be required to establish special custodial or other arrangements before making certain investments in those countries. There may be little financial or accounting information available with respect to issuers located in certain of such countries, and it may be difficult as a result to assess the value or prospects of an investment in such issuers. Many emerging market countries are subject to rapid currency devaluations and high inflation and/or economic recession and significant debt levels. These economic factors can have a material adverse effect on these countries’ economies and their securities markets. Moreover, many emerging market countries’ economies are based on only a few industries and/or are heavily dependent on global trade. Therefore, they may be negatively affected by declining commodity prices, factors affecting their trading markets and partners, exchange controls and other trade barriers, currency valuations and other protectionist measures. From time to time, certain of the companies in which the Fund may invest may operate in, or have dealings with, countries subject to sanctions or embargoes imposed by the U.S. government and the United Nations and/or countries identified by the U.S. government as state sponsors of terrorism. A company may suffer damage to its reputation if it is identified as a company which operates in, or has dealings with, countries subject to sanctions or embargoes imposed by the U.S. government and the United Nations and/or countries identified by the U.S. government as state sponsors of terrorism. As an investor in such companies, the Fund will be indirectly subject to those risks.

17

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

NOTES

TO THE FINANCIAL STATEMENTS

September 30, 2019

| 6. | EMERGING AND FRONTIER MARKETS RISK (continued) |

Many emerging and frontier market countries also impose withholding or other taxes on foreign investments, which may be substantial and result in lower Fund returns. The creditworthiness of firms used by the Fund to effect securities transactions in emerging and frontier market countries may not be as strong as in some developed countries. As a result, the Fund could be subject to a greater risk of loss on its securities transactions if a firm defaults on its responsibilities. The Fund’s ability to manage its foreign currency may be restricted in emerging and frontier market countries. As a result, a significant portion of the Fund’s currency exposure in these countries may not be covered. Frontier market countries generally have smaller economies or less developed capital markets than traditional emerging markets and, as a result, the risks of investing in emerging market countries are magnified in frontier market countries. The economies of frontier market countries are less correlated to global economic cycles than those of their more developed counterparts and their markets have low trading volumes and the potential for extreme price volatility and illiquidity. This volatility may be further heightened by the actions of a few major investors. For example, a substantial increase or decrease in cash flows of mutual funds investing in these markets could significantly affect local stock prices and, therefore, the price of Fund shares. These factors make investing in frontier market countries significantly riskier than in other countries and any one of them could cause the price of the Fund’s shares to decline. The recent decline in the U.S. economy as a result of the subprime crisis may have a disproportionately more adverse effect on economies of emerging and frontier market countries.

| 7. | DISTRIBUTIONS TO SHAREHOLDERS AND TAX MATTERS |

During the year ended September 30, 2019 the Fund distributed $60,284 of ordinary income.

The tax character of distributable earnings (deficit) at September 30, 2019 was as follows:

| Undistributed Ordinary Income | Post-October Loss and Late Year Loss | Capital Loss Carry Forwards | Other Book/Tax Differences | Unrealized Appreciation/ (Depreciation) | Total Distributable Earnings/(Deficit) | |||||||||||||||||

| $ | 60,716 | $ | (110,294 | ) | $ | (85,623 | ) | $ | — | $ | (561,174 | ) | $ | (696,915 | ) | |||||||

The difference between book basis and tax basis distributable earnings/(deficit) is primarily attributable to the tax deferral of losses on wash sales and differing book/tax treatments of foreign currency gains/(losses) and unrealized appreciation from passive foreign investment companies (“PFICs”).

At September 30, 2019, the Fund had $85,623 of non-expiring short-term capital loss carry forwards for federal income tax purposes available to offset future capital gains.

Under current tax law, net capital losses realized after October 31st and net ordinary losses incurred after December 31st may be deferred and treated as occurring on the first day of the following fiscal year. As of September 30, 2019, the Fund elected to defer net post-October capital losses of $110,294 and did not defer any post-December ordinary losses.

Permanent book and tax differences, primarily attributable to the book/tax basis treatment of foreign currency gains/(losses), resulted in reclassifications for the year ended September 30, 2019 as follows:

| Paid-in Capital | Distributable Earnings | ||||||

| $ | — | $ | — | ||||

For U.S. Federal income tax purposes, the cost of securities owned, gross appreciation, gross depreciation, and net unrealized appreciation/(depreciation) of investments at September 30, 2019 were as follows:

| Cost | Gross Appreciation | Gross Depreciation | Net Depreciation | ||||||||||||

| $ | 7,129,755 | $ | 390,049 | $ | (951,763 | ) | $ | (561,714 | ) | ||||||

The difference between book basis and tax basis unrealized appreciation (depreciation) from investments is primarily attributable to the tax deferral of losses on wash sales and differing book/tax treatments of foreign currency gains/(losses) and unrealized appreciation from passive foreign investment companies (“PFICs”). The unrealized depreciation in the table above includes unrealized foreign currency depreciation of $65.

18

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

NOTES

TO THE FINANCIAL STATEMENTS

September 30, 2019

| 8. | BENEFICIAL OWNERSHIP |

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a fund creates a presumption of control of the fund, under Section 2(a)(9) of the Investment Company Act of 1940. As of September 30, 2019, the EAS Crow Point Alternatives Fund (the “EAS Fund”) held 43.33% of the Fund’s shares as an underlying investment in its portfolio. Additional information for the EAS Fund, including its financial statements, is available from the Securities and Exchange Commission’s website at www.sec.gov. and may also be requested by mail to: 360 Funds, c/o M3Sixty Administration, LLC, 4300 Shawnee Mission Parkway, Suite 100, Fairway, KS 66205.

| 9. | COMMITMENTS AND CONTINGENCIES |

In the normal course of business, the Trust may enter into contracts that may contain a variety of representations and warranties and provide general indemnifications. The Trust’s maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated; however, management considers the risk of loss from such claims to be remote.

| 10. | SUBSEQUENT EVENTS |

In accordance with GAAP, Management has evaluated the impact of all subsequent events on the Fund through the date the financial statements were issued, and has determined that there were no other subsequent events requiring recognition or disclosure in the financial statements.

| 11. | RECENT ACCOUNTING PRONOUNCEMENTS |

In August 2018, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (ASU) No. 2018-13 “Fair Value Measurement (Topic 820): Disclosure Framework – Changes to the Disclosure Requirements for Fair Value Measurement” (“ASU 2018-13”) which includes amendments intended to improve the effectiveness of disclosures in the notes to financial statements. For example, ASU 2018-13 includes additional disclosures regarding the range and weighted average of significant unobservable inputs used to develop Level 3 fair value measurements, and clarifications to the narrative description of measurement uncertainty disclosures. ASU 2018-13 is effective for interim and annual periods beginning after December 15, 2019. Management has evaluated the implications of certain provisions of ASU 2018-13 and has elected to early adopt all aspects of the amendments effective with the Fund’s financial statements within this Annual Report.

19

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders of

RVX Emerging Market Equity Fund and the

Board of Trustees of 360 Funds

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of the RVX Emerging Market Equity Fund (the “Fund”), a series of 360 Funds, including the schedule of investments, as of September 30, 2019, the related statement of operations for the year then ended, the statements of changes in net assets, and financial highlights for the year then ended and for the period May 1, 2018 (commencement of operations) through September 30, 2018, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of September 30, 2019, the results of its operations for the year then ended, the changes in its net assets, and the financial highlights for the year then ended and for the period May 1, 2018 (commencement of operations) through September 30, 2018, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB. We have served as the Fund’s auditor since 2018.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audit we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of September 30, 2019 by correspondence with the custodian. We believe that our audit provides a reasonable basis for our opinion.

| TAIT, WELLER & BAKER LLP | ||

Philadelphia, Pennsylvania

November 29, 2019

20

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

ADDITIONAL

INFORMATION

September 30, 2019

The Fund files its complete schedules of portfolio holdings with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s website at http://www.sec.gov. The Fund’s Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Commission’s Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-877-244-6235; and on the Commission’s website at http://www.sec.gov.

Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30th is available without charge, upon request, by calling 1-877-244-6235; and on the Commission’s website at http://www.sec.gov.

Shareholder Tax Information - The Fund is required to advise you within 60 days of the Fund’s fiscal year end regarding the federal tax status of distributions received by shareholders during the fiscal year. The Fund paid $60,284 of ordinary income during the year ended September 30, 2019.

Tax information is reported from the Fund’s fiscal year and not calendar year, therefore, shareholders should refer to their Form 1099-DIV or other tax information which will be mailed in 2020 to determine the calendar year amounts to be included on their 2019 tax returns. Shareholders should consult their own tax advisors.

21

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

ADDITIONAL INFORMATION

September 30, 2019

BOARD OF TRUSTEES, OFFICERS AND PRINCIPAL SHAREHOLDERS - (Unaudited)

The Trustees are responsible for the management and supervision of the Fund. The Trustees approve all significant agreements between the Trust, on behalf of the Fund, and those companies that furnish services to the Fund; review performance of the Fund; and oversee activities of the Fund. The Statement of Additional Information of the Trust includes additional information about the Fund’s Trustees and is available upon request, without charge, by calling (877) 244-6235.

Trustees and Officers. Following are the Trustees and Officers of the Trust, their age and address, their present position with the Trust or the Fund, and their principal occupation during the past five years. Each of the Trustees of the Trust will generally hold office indefinitely. The Officers of the Trust will hold office indefinitely, except that: (1) any Officer may resign or retire and (2) any Officer may be removed any time by written instrument signed by at least two-thirds of the number of Trustees prior to such removal. In case a vacancy or an anticipated vacancy on the Board of Trustees shall for any reason exist, the vacancy shall be filled by the affirmative vote of a majority of the remaining Trustees, subject to certain restrictions under the 1940 Act. Those Trustees who are “interested persons” (as defined in the 1940 Act) by virtue of their affiliation with either the Trust or the Adviser, are indicated in the table. The address of each trustee and officer is 4300 Shawnee Mission Parkway, Suite 100, Fairway, KS 66205.

| Name, Address and Year of Birth (“YOB”) | Position(s) Held with Trust | Length of Service | Principal Occupation(s) During Past 5 Years |

Number of Series Overseen | Other Directorships During Past 5 Years |

| Independent Trustees | |||||

Arthur Q. Falk YOB : 1937 |

Trustee | Since 2011 | Retired. President, Murray Hill Financial Marketing, (financial marketing consultant) (1990–2012). | Ten | None |

Tom M. Wirtshafter YOB : 1954 |

Trustee | Since 2011 | Senior Vice President, American Portfolios Financial Services, (broker-dealer), American Portfolios Advisors (investment adviser) (2009-Present). | Ten | None |

Gary W. DiCenzo YOB: 1962

|

Trustee and Independent Chairman |

Since 2014

Since 2019

|

Chief Executive Officer, Cognios Capital (investment management firm) (2015-present); President and CEO, IMC Group, LLC (asset management firm consultant) (2010-2015). | Ten | FNEX Ventures (2018-present) |

Steven D. Poppen YOB : 1968 |

Trustee | Since 2018 | Executive Vice President and Chief Financial Officer, Minnesota Vikings (professional sports organization) (1999-present). | Ten | M3Sixty Funds Trust (3 portfolios) (2015 – present); FNEX Ventures (2018- present) |

Thomas J. Schmidt YOB: 1963 |

Trustee | Since 2018 | Principal, Tom Schmidt & Associates Consulting, LLC (2015-Present); Vice President of the Mutual Fund and Alternative Investment Full Service Transfer Agent (1986-2014). | Ten | FNEX Ventures (2018-present) |

| Interested Trustee* | |||||

Randall K. Linscott YOB: 1971 |

President | Since 2013 | Chief Executive Officer, M3Sixty Administration, LLC (2013 – present); Chief Operating Officer, M3Sixty Administration LLC (2011-2013); Division Vice President, Boston Financial Data Services, (2005-2011). | Ten | M3Sixty Funds Trust (3 portfolios) (2015 – present) |

* The Interested Trustee is an Interested Trustee

22

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

ADDITIONAL INFORMATION

September 30, 2019

BOARD OF TRUSTEES, OFFICERS AND PRINCIPAL SHAREHOLDERS - (Unaudited) (continued)

| Name, Address and Year of Birth (“YOB”) | Position(s) Held with Trust | Length of Service | Principal Occupation(s) During Past 5 Years |

Number of Series Overseen | Other Directorships During Past 5 Years |

Officers

|

|||||

Andras P. Teleki YOB: 1971

|

Chief Compliance Officer and Secretary

|

Since 2015 | Chief Legal Officer, M3Sixty Administration, LLC, M3Sixty Holdings, LLC, Matrix 360 Distributors, LLC and M3Sixty Advisors, LLC (2015-present); Chief Compliance Officer and Secretary, M3Sixty Funds Trust (2016-present); Chief Compliance Officer and Secretary, WP Trust (2016-present); Secretary and Assistant Treasurer, Capital Management Investment Trust (2015); Partner, K&L Gates (2009-2015). | N/A | N/A |

Brandon J. Byrd YOB: 1981 |

Assistant Secretary and Anti-Money Laundering Officer

Vice

|

Since 2013

Since 2018 |

Chief Operating Officer, M3Sixty Administration, LLC (2013-present); Anti-Money Laundering Compliance Officer, Monteagle Funds (2015-2016); Division Manager - Client Service Officer, Boston Financial Data Services (mutual find service provider) (2010-2012). | N/A | N/A |

Larry E. Beaver, Jr.** YOB: 1969 |

Assistant Treasurer | Since 2017 | Fund Accounting, Administration and Tax Officer, M3Sixty Administration, LLC (2017-Present); Director of Fund Accounting & Administration, M3Sixty Administration, LLC (2005-2017); Chief Accounting Officer, Amidex Funds, Inc. (2003-Present); Assistant Treasurer, Capital Management Investment Trust (July 2017-Present); Assistant Treasurer, M3Sixty Funds Trust (July 2017-Present; Assistant Treasurer, WP Funds Trust (July 2017-Present); Treasurer and Assistant Secretary, Capital Management Investment Trust (2008-July 2017); Treasurer, 360 Funds Trust (2007-2017); Treasurer, M3Sixty Funds Trust (2015-July 2017); Treasurer, WP Trust (2015-July 2017); Treasurer and Chief Financial Officer, Monteagle Funds (2008-2016). | N/A | N/A |

John H. Lively YOB: 1969 |

Assistant Secretary | Since 2017 | Attorney, Practus, LLP (law firm) (2010-present). | N/A | N/A |

Ted L. Akins YOB: 1974 |

Assistant Secretary | Since 2018 | Vice President of Operations, M3Sixty Administration, LLC (2012-present). | N/A | N/A |

** Effective December 28, 2018, Larry E. Beaver, Jr. was assigned as Interim Treasurer until a new Treasurer is appointed by the Board.

23

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

ADDITIONAL INFORMATION

September 30, 2019

BOARD OF TRUSTEES, OFFICERS AND PRINCIPAL SHAREHOLDERS - (Unaudited) (continued)

Remuneration Paid to Trustees and Officers - Officers of the Trust and Trustees who are "interested persons" of the Trust or the Adviser will receive no salary or fees from the Trust. Officers of the Trust and interested Trustees do receive compensation directly from certain service providers to the Trust, including Matrix 360 Distributors, LLC and M3Sixty Administration, LLC. Each Trustee who is not an “interested person” received a fee of $1,500 each year plus $200 per Board or committee meeting attended. Effective April 25, 2019, each Trustee who is not an “interested person” (an “Independent Trustee”) will receive a $5,000 annual retainer (paid quarterly). In addition, each Independent Trustee will receive, on a per fund basis: (i) a fee of $1,500 per fund each year (paid quarterly); (ii) a fee of $200 per Board meeting attended; and (iii) a fee of $200 per committee meeting attended. The Trust will also reimburse each Trustee for travel and other expenses incurred in connection with, and/or related to, the performance of their obligations as a Trustee. Officers of the Trust will also be reimbursed for travel and other expenses relating to their attendance at Board meetings.

| Name of Trustee1 | Aggregate Compensation From each Fund2 | Pension or Retirement Benefits Accrued As Part of Portfolio Expenses | Estimated Annual Benefits Upon Retirement | Total Compensation From the Fund Paid to Trustees2 | ||||||||

| Independent Trustees | ||||||||||||

| Arthur Q. Falk | $ | 2,529 | None | None | $ | 2,529 | ||||||

| Tom M. Wirtshafter | $ | 2,529 | None | None | $ | 2,529 | ||||||

| Gary W. DiCenzo | $ | 2,529 | None | None | $ | 2,529 | ||||||

| Steven D. Poppen | $ | 2,529 | None | None | $ | 2,529 | ||||||

| Thomas J. Schmidt | $ | 2,529 | None | None | $ | 2,529 | ||||||

| Interested Trustees and Officers | ||||||||||||

| Randall K. Linscott | None | Not Applicable | Not Applicable | None | ||||||||

| 1 | Each of the Trustees serves as a Trustee to each Series of the Trust. The Trust currently offers ten (10) series of shares. |

| 2 | Figures are for the year ended September 30, 2019. |

24

| RVX Emerging Markets Equity Fund | ANNUAL REPORT |

Information About Your Fund’s Expenses (Unaudited)

As a shareholder of the Fund, you incur ongoing costs, including management fees, distribution and/or service (12b-1) fees; and other Fund expenses. The example below is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.