UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For the quarterly period ended

or

For the transition period from ______to______

Commission File Number

(Exact name of registrant as specified in charter)

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) | |

| People’s Republic of | ||

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§

232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | |

| Non-accelerated filer | ☐ | Smaller reporting company | |

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

As of May 4, 2023, the registrant had 77,678,730

shares of common stock issued and

TABLE OF CONTENTS

i

PART I — FINANCIAL INFORMATION

Item 1. Financial Statements.

KANDI TECHNOLOGIES GROUP,

INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

| March 31, 2023 | December 31, 2022 | |||||||

| (Unaudited) | ||||||||

| CURRENT ASSETS | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Restricted cash | ||||||||

| Certificate of deposit | ||||||||

| Accounts receivable (net of allowance for doubtful accounts of $ | ||||||||

| Inventories | ||||||||

| Notes receivable | ||||||||

| Other receivables | ||||||||

| Prepayments and prepaid expense | ||||||||

| Advances to suppliers | ||||||||

| TOTAL CURRENT ASSETS | ||||||||

| NON-CURRENT ASSETS | ||||||||

| Property, plant and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Land use rights, net | ||||||||

| Construction in progress | ||||||||

| Deferred tax assets | ||||||||

| Long-term investment | ||||||||

| Goodwill | ||||||||

| Other long-term assets | ||||||||

| TOTAL NON-CURRENT ASSETS | ||||||||

| TOTAL ASSETS | $ | $ | ||||||

| CURRENT LIABILITIES | ||||||||

| Accounts payable | $ | $ | ||||||

| Other payables and accrued expenses | ||||||||

| Short-term loans | ||||||||

| Notes payable | ||||||||

| Income tax payable | ||||||||

| Other current liabilities | ||||||||

| TOTAL CURRENT LIABILITIES | ||||||||

| NON-CURRENT LIABILITIES | ||||||||

| Deferred taxes liability | ||||||||

| Contingent consideration liability | ||||||||

| Other long-term liabilities | ||||||||

| TOTAL NON-CURRENT LIABILITIES | ||||||||

| TOTAL LIABILITIES | ||||||||

| STOCKHOLDER’S EQUITY | ||||||||

| Common stock, $ | ||||||||

| Less: Treasury stock ( | ( | ) | ( | ) | ||||

| Additional paid-in capital | ||||||||

| Accumulated deficit (the restricted portion is $ | ( | ) | ( | ) | ||||

| Accumulated other comprehensive loss | ( | ) | ( | ) | ||||

| TOTAL KANDI TECHNOLOGIES GROUP, INC. STOCKHOLDERS’ EQUITY | ||||||||

| Non-controlling interests | ||||||||

| TOTAL STOCKHOLDERS’ EQUITY | ||||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | $ | ||||||

See accompanying notes to condensed consolidated financial statements

1

KANDI TECHNOLOGIES GROUP, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND

COMPREHENSIVE INCOME (LOSS)

(UNAUDITED)

| Three Months Ended | ||||||||

| March 31, 2023 | March 31, 2022 | |||||||

| REVENUES FROM UNRELATED PARTIES, NET | $ | $ | ||||||

| REVENUES FROM THE FORMER AFFILIATE COMPANY AND RELATED PARTIES, NET | ||||||||

| REVENUES, NET | ||||||||

| COST OF GOODS SOLD | ( | ) | ( | ) | ||||

| GROSS PROFIT | ||||||||

| OPERATING INCOME (EXPENSE): | ||||||||

| Research and development | ( | ) | ( | ) | ||||

| Selling and marketing | ( | ) | ( | ) | ||||

| General and administrative | ( | ) | ( | ) | ||||

| TOTAL OPERATING EXPENSE | ( | ) | ( | ) | ||||

| LOSS FROM OPERATIONS | ( | ) | ( | ) | ||||

| OTHER INCOME (EXPENSE): | ||||||||

| Interest income | ||||||||

| Interest expense | ( | ) | ( | ) | ||||

| Change in fair value of contingent consideration | ( | ) | ||||||

| Government grants | ||||||||

| Other income, net | ||||||||

| TOTAL OTHER INCOME, NET | ||||||||

| INCOME (LOSS) BEFORE INCOME TAXES | ( | ) | ||||||

| INCOME TAX BENEFIT | ||||||||

| NET INCOME (LOSS) | ( | ) | ||||||

| LESS: NET INCOME (LOSS) ATTRIBUTABLE TO NON-CONTROLLING INTERESTS | ( | ) | ||||||

| NET LOSS ATTRIBUTABLE TO KANDI TECHNOLOGIES GROUP, INC. STOCKHOLDERS | ( | ) | ( | ) | ||||

| OTHER COMPREHENSIVE INCOME | ||||||||

| Foreign currency translation adjustment | ||||||||

| COMPREHENSIVE INCOME (LOSS) | $ | $ | ( | ) | ||||

| WEIGHTED AVERAGE SHARES OUTSTANDING BASIC | ||||||||

| WEIGHTED AVERAGE SHARES OUTSTANDING DILUTED | ||||||||

| NET INCOME (LOSS) PER SHARE, BASIC | $ | $ | ( | ) | ||||

| NET INCOME (LOSS) PER SHARE, DILUTED | $ | $ | ( | ) | ||||

See accompanying notes to condensed consolidated financial statements

2

KANDI TECHNOLOGIES GROUP, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(UNAUDITED)

| Number of Outstanding Shares | Common Stock | Treasury Stock | Additional Paid-in Capital | Accumulated Earning (Deficit) | Accumulated Other Comprehensive Income | Non-controlling interests | Total | |||||||||||||||||||||||||

| Balance, December 31, 2021 | $ | $ | ( | ) | $ | $ | ( | ) | $ | $ | $ | |||||||||||||||||||||

| Stock issuance and award | ||||||||||||||||||||||||||||||||

| Stock buyback | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||

| Capital contribution from shareholder | - | |||||||||||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||

| Foreign currency translation | - | |||||||||||||||||||||||||||||||

| Balance, March 31, 2022 | $ | $ | ( | ) | $ | $ | ( | ) | $ | $ | $ | |||||||||||||||||||||

| Number of Outstanding Shares | Common Stock | Treasury Stock | Additional Paid-in Capital | Accumulated Earning (Deficit) | Accumulated Other Comprehensive Income | Non-controlling interests | Total | |||||||||||||||||||||||||

| Balance, December 31, 2022 | $ | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | $ | $ | |||||||||||||||||||

| Stock issuance and award | ||||||||||||||||||||||||||||||||

| Stock based compensation | - | |||||||||||||||||||||||||||||||

| Net income (loss) | - | ( | ) | |||||||||||||||||||||||||||||

| Foreign currency translation | - | |||||||||||||||||||||||||||||||

| Balance, March 31, 2023 | $ | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | $ | $ | |||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

3

KANDI TECHNOLOGIES GROUP, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| Three Months Ended | ||||||||

| March 31, 2023 | March 31, 2022 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net income (loss) | $ | $ | ( | ) | ||||

| Adjustments to reconcile net (loss) income to net cash provided by operating activities | ||||||||

| Depreciation and amortization | ||||||||

| Provision (reversal) of allowance for doubtful accounts | ||||||||

| Change in fair value of contingent consideration | ( | ) | ||||||

| Stock award and stock based compensation expense | ||||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | ||||||||

| Notes receivable | ||||||||

| Inventories | ( | ) | ||||||

| Other receivables and other assets | ( | ) | ||||||

| Advances to supplier and prepayments and prepaid expenses | ||||||||

| Increase (Decrease) In: | ||||||||

| Accounts payable | ||||||||

| Other payables and accrued liabilities | ( | ) | ( | ) | ||||

| Notes payable | ( | ) | ( | ) | ||||

| Income tax payable | ( | ) | ( | ) | ||||

| Net cash provided by operating activities | $ | $ | ||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Purchases of property, plant and equipment, net | ( | ) | ( | ) | ||||

| Payment for construction in progress | ( | ) | ( | ) | ||||

| Certificate of deposit | ( | ) | ( | ) | ||||

| Net cash used in investing activities | $ | ( | ) | $ | ( | ) | ||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Proceeds from short-term loans | ||||||||

| Repayments of short-term loans | ( | ) | ||||||

| Contribution from non-controlling shareholder | ||||||||

| Purchase of treasury stock | ( | ) | ||||||

| Net cash used in by financing activities | $ | ( | ) | $ | ( | ) | ||

| NET DECREASE IN CASH AND CASH EQUIVALENTS AND RESTRICTED CASH | $ | ( | ) | $ | ( | ) | ||

| Effect of exchange rate changes | $ | $ | ||||||

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT BEGINNING OF YEAR | $ | $ | ||||||

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT END OF PERIOD | $ | $ | ||||||

| -CASH AND CASH EQUIVALENTS AT END OF PERIOD | ||||||||

| -RESTRICTED CASH AT END OF PERIOD | ||||||||

| SUPPLEMENTARY CASH FLOW INFORMATION | ||||||||

| Income taxes paid | $ | $ | ||||||

| Interest paid | $ | $ | ||||||

| SUPPLEMENTAL NON-CASH DISCLOSURES: | ||||||||

| Contribution from non-controlling shareholder by inventories, fixed assets and intangible assets | $ | $ | ||||||

See accompanying notes to condensed consolidated financial statements

4

NOTE 1 - ORGANIZATION AND PRINCIPAL ACTIVITIES

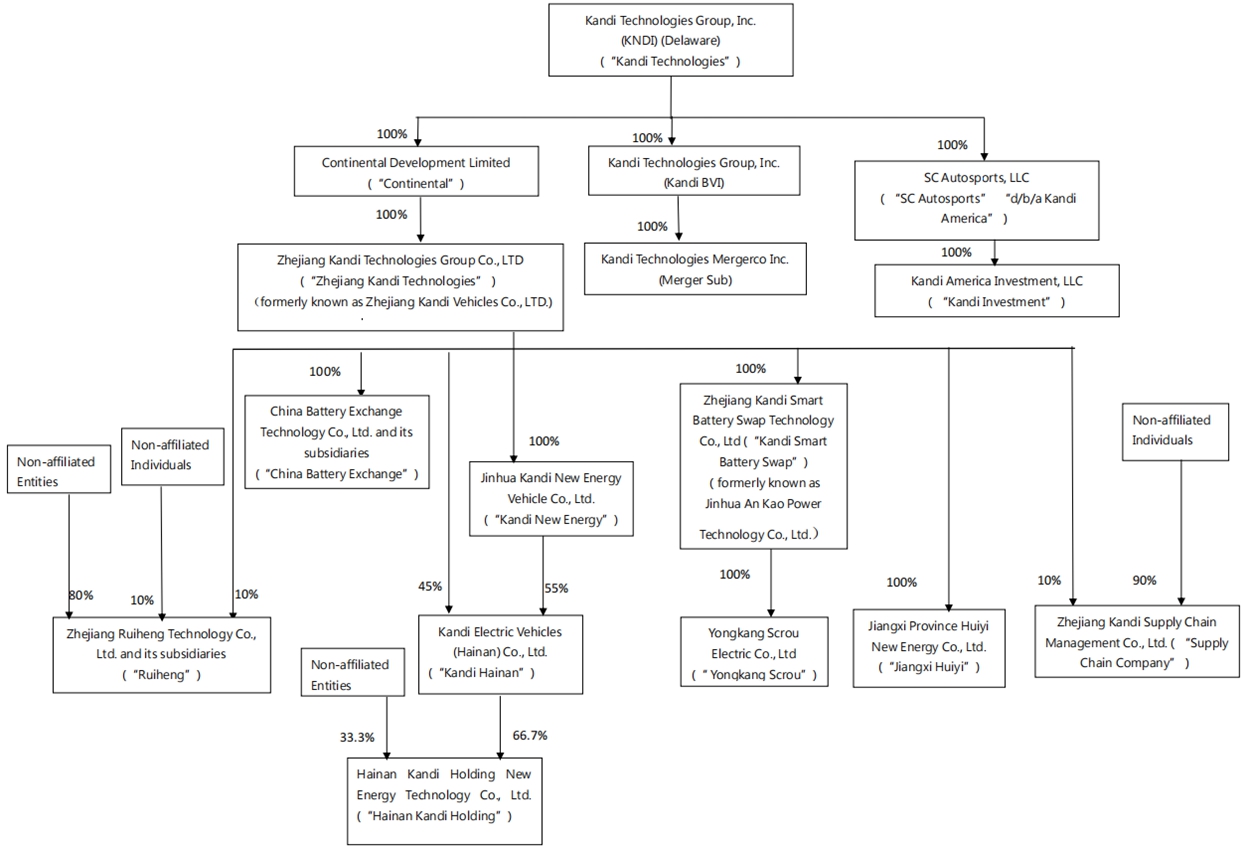

Kandi Technologies Group, Inc. (“Kandi Technologies”) was incorporated under the laws of the State of Delaware on March 31, 2004. As used herein, the terms “Company” or “Kandi” refer to Kandi Technologies and its operating subsidiaries, as described below.

Headquartered in Jinhua City, Zhejiang Province, People’s Republic of China (“China” or “PRC”), the Company is one of China’s leading producers and manufacturers of electric vehicle (“EV”) products, EV parts, and off-road vehicles for sale in the Chinese and the global markets. The Company conducts its primary business operations through its wholly-owned subsidiaries, Zhejiang Kandi Vehicles Co., Ltd. (“Kandi Vehicles”), Kandi Vehicles’ wholly and partially-owned subsidiaries, and SC Autosports, LLC (“SC Autosports”, d/b/a Kandi America) and its wholly-owned subsidiary, Kandi America Investment, LLC (“Kandi Investment”). In March 2021, Zhejiang Kandi Vehicles Co., Ltd. changed its name to Zhejiang Kandi Technologies Group Co., Ltd. (“Zhejiang Kandi Technologies”).

The Company’s organizational chart as of the date of this report is as follows:

5

NOTE 2 - LIQUIDITY

The Company had working capital of $

Although the Company expects that most of its outstanding trade receivables from customers will be collected in the next twelve months, there are uncertainties with respect to the timing in collecting these receivables.

The Company’s primary need for liquidity

stems from its need to fund working capital requirements of the Company’s businesses, its capital expenditures and its general operations,

including debt repayment. The Company has historically financed its operations through short-term commercial bank loans from Chinese banks,

as well as its ongoing operating activities by using funds from operations, external credit or financing arrangements. Currently

the Company has sufficient cash in hand to meet the existing operational needs, but the credit line is retained and can be utilized

timely when the Company has special capital needs. The PRC subsidiaries do not have any short-term bank loans and the US subsidiaries

have $

NOTE 3 - BASIS OF PRESENTATION

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim information, and with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X promulgated by the Securities and Exchange Commission (“SEC”). Accordingly, they do not include all of the information and notes required by U.S. GAAP for annual financial statements. In management’s opinion, the interim financial statements reflect all normal adjustments that are necessary to provide a fair presentation of the financial results for the interim periods presented. Operating results for interim periods are not necessarily indicative of results that may be expected for an entire fiscal year. The condensed consolidated balance sheet as of December 31, 2022 has been derived from the audited consolidated financial statements as of such date. For a more complete understanding of the Company’s business, financial position, operating results, cash flows, risk factors and other matters, please refer to its Annual Report on Form 10-K for the fiscal year ended December 31, 2022 (the “2022 Form 10-K”) filed with SEC on March 16, 2023.

6

NOTE 4 - PRINCIPLES OF CONSOLIDATION

The Company’s condensed consolidated financial statements reflect the accounts of the Company and its ownership interests in the following subsidiaries:

| (1) | Continental Development Limited (“Continental”), a wholly-owned subsidiary of the Company, incorporated under the laws of Hong Kong; |

| (2) | Zhejiang Kandi Technologies, a wholly-owned subsidiary of Continental, incorporated under the laws of the PRC; |

| (3) | Kandi New Energy Vehicle Co. Ltd. (“Kandi New Energy”), formerly, a |

| (4) | Kandi Electric Vehicles (Hainan) Co., Ltd. (“Kandi Hainan”), a subsidiary |

| (5) | Zhejiang Kandi Smart Battery Swap Technology Co., Ltd (“Kandi Smart Battery Swap”), a wholly-owned subsidiary of Zhejiang Kandi Technologies, incorporated under the laws of the PRC; |

| (6) | Yongkang Scrou Electric Co, Ltd. (“Yongkang Scrou”), a wholly-owned subsidiary of Kandi Smart Battery Swap, incorporated under the laws of the PRC; |

| (7) | SC Autosports (d/b/a Kandi America), a wholly-owned subsidiary of the Company formed under the laws of the State of Texas. |

| (8) | China Battery Exchange (Zhejiang) Technology Co., Ltd. (“China Battery Exchange”), a wholly-owned subsidiary of Zhejiang Kandi Technologies, and its subsidiaries, incorporated under the laws of the PRC; |

| (9) | Kandi America Investment, LLC (“Kandi Investment”), a wholly-owned subsidiary of SC Autosports formed under the laws of the State of Texas, USA; |

| (10) | Jiangxi Province Huiyi New Energy Co., Ltd. (“Jiangxi Huiyi”) and its subsidiaries, a wholly-owned subsidiary of Zhejiang Kandi Technologies, incorporated under the laws of the PRC; and | |

| (11) | Hainan Kandi Holding New Energy Technology Co., Ltd. (“Hainan Kandi Holding”), a subsidiary of Kandi Hainan, incorporated under the laws of the PRC; Kandi Hainan owns |

7

NOTE 5 - USE OF ESTIMATES

The preparation of the unaudited condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and related disclosures of contingent assets and liabilities at the balance sheet date, and the reported revenues and expenses during the reported period in the unaudited condensed consolidated financial statements and accompanying notes. Significant accounting estimates reflected in the Company’s unaudited condensed consolidated financial statements primarily include, but are not limited to, allowances for doubtful accounts, lower of cost and net realizable value of inventory, assessment for impairment of long-lived assets and intangible assets, valuation of deferred tax assets, change in fair value of contingent consideration, determination of share-based compensation expenses as well as fair value of stock warrants.

Management bases the estimates on historical experience and on various other assumptions that are believed to be reasonable, the results of which form the basis for making judgments about the carrying values of assets and liabilities. Actual results could differ from these estimates.

NOTE 6 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Our significant accounting policies are detailed in “Note 6 - Summary of Significant Accounting Policies” of the Company’s 2022 Form 10-K.

NOTE 7 - NEW ACCOUNTING PRONOUNCEMENTS

Accounting Pronouncements Adopted

In October 2021, the FASB issued ASU 2021-08, “Business Combinations (Topic 805) – Accounting for Contract Assets and Contract Liabilities from Contracts with Customers”, which requires that an acquirer recognize and measure contract assets and contract liabilities acquired in a business combination in accordance with Topic 606, as if it had originated the contracts. Prior to this ASU, an acquirer generally recognizes contract assets acquired and contract liabilities assumed that arose from contracts with customers at fair value on the acquisition date. The ASU is effective for fiscal years beginning after December 15, 2022, with early adoption permitted. The ASU is applied prospectively to business combinations occurring on or after the effective date of the amendment (or if adopted early as of an interim period, as of the beginning of the fiscal year that includes the interim period of early application). The Company has adopted this accounting pronouncement from January 1, 2023, and there was no material impact on its consolidated financial statements from the adoption.

8

NOTE 8 - CONCENTRATIONS

(a) Customers

For the three-month period ended March 31, 2023

and 2022, the Company’s major customers, each of whom accounted for more than

| Sales | Trade Receivable | |||||||||||

| Three Months | ||||||||||||

| Ended | ||||||||||||

| March 31, | March 31, | December 31, | ||||||||||

| Major Customers | 2023 | 2023 | 2022 | |||||||||

| Customer A | | % | | % | ||||||||

| Sales | Trade Receivable | |||||||||||

| Three Months | ||||||||||||

| Ended | ||||||||||||

| March 31, | March 31, | December 31, | ||||||||||

| Major Customers | 2022 | 2022 | 2021 | |||||||||

| Customer B | | % | | % | ||||||||

| Customer C | % | % | % | |||||||||

| Customer D | % | |||||||||||

(b) Suppliers

For the three-month period ended March 31, 2023,

there were no suppliers that accounted for more than

| Purchases | Accounts Payable | |||||||||||

| Three Months | ||||||||||||

| Ended | ||||||||||||

| March 31, | March 31, | December 31, | ||||||||||

| Major Suppliers | 2022 | 2022 | 2021 | |||||||||

| ODES USA, Inc. | % | % | |

|||||||||

| Hunan Jinfuli New Energy Co., Ltd | % | % | % | |||||||||

| Zhejiang Kandi Supply Chain Management Co., Ltd. | % | % | % | |||||||||

9

NOTE 9 - EARNINGS (LOSS) PER SHARE

The Company calculates earnings (loss) per share in accordance with ASC 260, Earnings Per Share, which requires a dual presentation of basic and diluted earnings (loss) per share. Basic earnings (loss) per share are computed using the weighted average number of shares outstanding during the reporting period. Diluted earnings (loss) per share represents basic earnings (loss) per share adjusted to include the potentially dilutive effect of outstanding stock options and warrants (using treasury stock method).

Due to the average market price of the common

stock during the period being below the exercise price of certain options and warrants, approximately

Due to the average market price of the common

stock during the period below the exercise price of the options, approximately

NOTE 10 - ACCOUNTS RECEIVABLE

Accounts receivable are summarized as follows:

| March 31, | December 31, | |||||||

| 2023 | 2022 | |||||||

| Accounts receivable | $ | $ | ||||||

| Less: allowance for doubtful accounts | ( | ) | ( | ) | ||||

| Accounts receivable, net | $ | $ | ||||||

The following table sets forth the movement of provision for doubtful accounts:

| Allowance for Doubtful Accounts | ||||

| BALANCE AT DECEMBER 31, 2021 | $ | |||

| Provision | ||||

| Recovery | ( | ) | ||

| Exchange rate difference | ( | ) | ||

| BALANCE AT DECEMBER 31, 2022 | $ | |||

| Exchange rate difference | ||||

| BALANCE AT MARCH 31, 2023 | $ | |||

10

NOTE 11 - INVENTORIES

Inventories are summarized as follows:

| March 31, | December 31, | |||||||

| 2023 | 2022 | |||||||

| Raw material | $ | $ | ||||||

| Work-in-progress | ||||||||

| Finished goods * | ||||||||

| Inventories | $ | $ | ||||||

| * |

NOTE 12 - PROPERTY, PLANT AND EQUIPMENT, NET

Property, plants and equipment as of March 31, 2023 and December 31, 2022, consisted of the following:

| March 31, | December 31, | |||||||

| 2023 | 2022 | |||||||

| At cost: | ||||||||

| Buildings | $ | $ | ||||||

| Machinery and equipment | ||||||||

| Office equipment | ||||||||

| Motor vehicles and other transport equipment | ||||||||

| Molds and others | ||||||||

| Less : Accumulated depreciation | ( | ) | ( | ) | ||||

| Property, plant and equipment, net | $ | $ | ||||||

The Company’s Jinhua factory completed the relocation to a new

industrial park in April 2021. The new location covers an area of more than

Depreciation expenses for the three months ended

March 31, 2023 and 2022 were $

11

NOTE 13 - INTANGIBLE ASSETS

Intangible assets include acquired other intangibles of trade name, customer relations, patent and technology recorded at estimated fair values in accordance with purchase accounting guidelines for acquisitions.

The following table provides the gross carrying value and accumulated amortization for each major class of our intangible assets, other than goodwill:

| Remaining | March 31, | December 31, | ||||||||

| useful life | 2023 | 2022 | ||||||||

| Gross carrying amount: | ||||||||||

| Patent | $ | |||||||||

| Technology | ||||||||||

| Less : Accumulated amortization | ||||||||||

| Patent | $ | ( | ) | ( | ) | |||||

| Technology | ( | ) | ( | ) | ||||||

| ( | ) | ( | ) | |||||||

| Less : impairment for intangible assets | ( | ) | ||||||||

| Intangible assets, net | $ | $ | ||||||||

The aggregate amortization expenses for those

intangible assets that continue to be amortized is reflected in amortization of intangible assets in the Unaudited Condensed Consolidated

Statements of Income and Comprehensive Income and were $

Amortization expenses for the next five years and thereafter are as follows:

| Nine months ended December 31, 2023 | $ | |||

| Years ended December 31, | ||||

| 2024 | ||||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| Thereafter | ||||

| Total | $ |

12

NOTE 14 - LAND USE RIGHTS, NET

The Company’s land use rights consist of the following:

| March 31, | December 31, | |||||||

| 2023 | 2022 | |||||||

| Cost of land use rights | $ | $ | ||||||

| Less: Accumulated amortization | ( | ) | ( | ) | ||||

| Land use rights, net | $ | $ | ||||||

The amortization expenses for the three months

ended March 31, 2023 and 2022, were $

Amortization expenses for the next five years and thereafter are as follows:

| Nine months ended December 31, 2023 | $ | |||

| Years ended December 31, | ||||

| 2024 | ||||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| Thereafter | ||||

| Total | $ |

NOTE 15 - OTHER LONG TERM ASSETS

Other long term assets as of March 31, 2023 and December 31, 2022, consisted of the following:

| March 31, | December 31, | |||||||

| 2023 | 2022 | |||||||

| Prepayments for land use right (i) | $ | |||||||

| Right - of - use asset (ii) | ||||||||

| Others | ||||||||

| Total other long-term asset | $ | $ | ||||||

| (i) |

| (ii) |

13

NOTE 16 - TAXES

(a) Corporation Income Tax

Pursuant to the tax laws and regulations of the

PRC, the Company’s applicable corporate income tax (“CIT”) rate is

The Company’s provision or benefit from

income taxes for interim periods is determined using an estimate of the Company’s annual effective tax rate, adjusted for discrete

items, if any, that are taken into account in the relevant period. Each quarter the Company updates its estimate of the annual effective

tax rate, and if its estimated tax rate changes, management makes a cumulative adjustment. For 2023, the Company’s effective tax

rate is favorably affected by a super-deduction for qualified research and development costs and adversely affected by non-deductible

expenses such as stock rewards for non-US employees, and part of entertainment expenses. The Company records valuation allowances against

the deferred tax assets associated with losses and other timing differences for which we may not realize a related tax benefit.

The quarterly tax provision, and the quarterly

estimate of the Company’s annual effective tax rate, is subject to significant variation due to several factors, including variability

in accurately predicting the Company’s pre-tax and taxable income and loss, acquisitions (including integrations) and investments,

changes in its stock price, changes in its deferred tax assets and liabilities and their valuation, return to provision true-up, foreign

currency gains (losses), changes in regulations and interpretations related to tax, accounting, and other areas. Additionally, the Company’s

effective tax rate can be volatile based on the amount of pre-tax income or loss. The income tax provision for the three months ended

March 31, 2023 and 2022 was tax benefit of $

Under ASC 740 guidance relating to uncertain tax positions, which addresses the determination of whether tax benefits claimed or expected to be claimed on a tax return should be recorded in the financial statements, the Company may recognize the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the financial statements from such a position should be measured based on the largest benefit that has a greater than fifty percent likelihood of being realized upon ultimate settlement. ASC 740 also provides guidance on de-recognition, classification, interest and penalties on income taxes, accounting in interim periods and requires increased disclosures. As of March 31, 2023, the Company did not have any liability for unrecognized tax benefits. The Company files income tax returns with the U.S. Internal Revenue Services (“IRS”) and those states where the Company has operations. The Company is subject to U.S. federal or state income tax examinations by the IRS and relevant state tax authorities. During the periods open to examination, the Company has net operating loss carry forwards (“NOLs”) for U.S. federal and state tax purposes that have attributes from closed periods. Since these NOLs may be utilized in future periods, they remain subject to examination. The Company also files certain tax returns in the PRC. As of March 31, 2023, the Company was not aware of any pending income tax examinations by U.S. or PRC tax authorities. The Company records interest and penalties on uncertain tax provisions as income tax expense. As of March 31, 2023, the Company has no accrued interest or penalties related to uncertain tax positions.

The tax effected aggregate Net Operating Loss

(“NOL”) was $

14

(b) Tax Holiday Effect

For the three months ended March 31, 2023 and

2022, the PRC CIT rate was

The combined effects of income tax expense exemptions and reductions available to the Company for the three months ended March 31, 2023 and 2022 are as follows:

| Three Months Ended | ||||||||

| March 31, | ||||||||

| 2023 | 2022 | |||||||

| Tax benefit (holiday) credit | $ | $ | ||||||

| Basic net income per share effect | $ | $ | ||||||

NOTE 17 - LEASES AND RIGHT-OF-USE-ASSETS

During October 2020, land use right of gross value

of $

The Company has entered into a lease for Hangzhou

office, with a term of 48 months from January 1, 2022 to December 31, 2025. The Company recorded operating lease assets and operating

lease liabilities on January 1, 2022, with a remaining lease term of

The Company also elected to apply the short-term lease exception for lease arrangements with a lease term of 12 months or less at commencement. Lease terms used to compute the present value of lease payments do not include any option to extend, renew or terminate the lease that the Company is not able to reasonably certain to exercise upon the lease inception. Accordingly, operating lease right-of-use assets and liabilities do not include leases with a lease term of 12 months or less.

As of March 31, 2023, the Company’s operating

lease right-of-use assets (grouped in other long-term assets on the balance sheet) was $

Supplemental information related to operating leases was as follows:

| Three Months Ended | ||||||||

| March 31, | ||||||||

| 2023 | 2022 | |||||||

| Cash payments for operating leases | $ | $ | ||||||

Maturities of lease liabilities as of March 31, 2023 were as follow:

| Maturity of Lease Liabilities: | Lease payable | |||

| Years ended December 31, 2023 | $ | |||

| 2024 | ||||

| 2025 | ||||

15

NOTE 18 - CONTINGENT CONSIDERATION LIABILITY

On October 31, 2021, the Company completed the

acquisition of

The Company recorded contingent consideration liability of the estimated fair value of the contingent consideration the Company currently expects to pay to the KSBS Shareholders and Jiangxi Huiyi’s former members upon the achievement of certain milestones. The fair value of the contingent consideration liability associated with remaining shares of restrictive common stock was estimated by using the Monte Carlo simulation method, which took into account all possible scenarios. This fair value measurement is classified as Level 3 within the fair value hierarchy prescribed by ASC Topic 820, Fair Value Measurement and Disclosures. In accordance with ASC Topic 805, Business Combinations, the Company will re-measure this liability each reporting period and record changes in the fair value through a separate line item within the Company’s consolidated statements of income.

As of March 31, 2023 and December 31, 2022,

the Company’s contingent consideration liability to former members of Jiangxi Huiyi was $

NOTE 19 - STOCK OPTIONS

On September 7, 2022, the Compensation Committee

of the Board of Directors of the Company approved the grant of stock options to purchase

16

NOTE 20 - STOCK AWARD

In connection with the appointment of Mr. Henry

Yu as a member of the Board of Directors (the “Board”), the Board authorized the Company to compensate Mr. Henry Yu with

As compensation for Mr. Jerry Lewin’s services

as a member of the Board, the Board authorized the Company to compensate Mr. Jerry Lewin with

As compensation for Ms. Kewa Luo’s services

as the Company’s investor relation officer, the Board authorized the Company to compensate Ms. Kewa Luo with

On May 15, 2020, the Board appointed Mr. Jehn

Ming Lim as the Chief Financial Officer. Mr. Lim was entitled to receive

On January 10, 2023, the Board appointed Dr. Xueqin

Dong as the Chief Executive Officer, Dr. Dong was entitled to receive

The fair value of stock awards with service condition is determined based on the closing price of the common stock on the date the shares are granted. The compensation costs for awards of common stock are recognized over the requisite service period.

On December 30, 2013, the Board approved a proposal

(as submitted by the Compensation Committee) of an award (the “Board’s Pre-Approved Award Grant Sub-Plan under the 2008 Plan”)

for certain executives and other key employees. The fair value of each award granted under the 2008 Plan is determined based on the closing

price of the Company’s stock on the date of grant of such award. On September 26, 2016, the Board approved to terminate the previous

Board’s Pre-Approved Award Grant Sub-Plan under the 2008 Plan and adopted a new plan to grant the total number of shares of common

stock of the stock award for selected executives and key employees

On March 13, 2023 (the “Signing Date”), Kandi Technologies Group, Inc., a Delaware corporation (the “Company”), entered into an Equity Incentive Agreement (the “Equity Incentive Agreement”) with Pan Guoqing (the “Receiving Party”), who is the presentative of the project management team of the project of crossover golf carts of Kandi Electric Vehicles (Hainan) Co., Ltd. (“Kandi EV Hainan”), a wholly owned subsidiary of the Company organized under the laws of the People’s Republic of China. The Receiving Party was originally the management team of golf crossover project of Hainan Kandi Holding New Energy Technology Co., Ltd. (“Hainan Kandi Holding”), a company organized under the laws of the People’s Republic of China. The Receiving Party has agreed to be employed as management team of Kandi EV Hainan, responsible for the operation of the golf crossover project of Kandi EV Hainan, and stop production and operation of Hainan Kandi Holding’s business. An English translated copy of the Equity Incentive Agreement is filed as an exhibit and incorporated by reference in its entirety to this report.

17

Pursuant

to the Equity Incentive Agreement, for the next three calendar years ending in December 31, 2025 (the “Incentive Period”),

the Company will provide equity incentives to the Receiving Party, subject to the Receiving Party meeting certain performance milestones

in its role as the management team of the golf crossover project (the “Crossover Project”) of Kandi EV Hainan. The performance

milestones are measured in terms of the net profit of the Crossover Project after deducting relevant operating costs and income taxes,

excluding various incentives, allowances and rebates, among others, and shall be audited and confirmed by the third party auditor designated

by the granting party, or the Company. The net profit target (the “Net Profit Target”) for the Incentive Period is RMB

The Receiving Party has no relationship to the Company other than as described above. The Equity Incentive Agreement is subject to the Company’s approval.

For the three months ended March 31, 2023 and

2022, the Company recognized $

NOTE 21 - COMMITMENTS AND CONTINGENCIES

Guarantees and pledged collateral for bank loans to other parties

| (1) | Guarantees for bank loans |

On March 15, 2013,

| (2) | Pledged collateral for bank loans for which the parties other than the Company are the borrowers. |

As of March 31, 2023 and December 31, 2022, none of the Company’s land use rights or plants and equipment was pledged as collateral securing bank loans for which the parties other than the Company are the borrowers.

Litigation

Beginning in March 2017, putative shareholder class actions were filed against Kandi Technologies Group, Inc. (“Kandi”) and certain of its current and former directors and officers in the United States District Court for the Central District of California and the United States District Court for the Southern District of New York. The complaints generally alleged violations of the federal securities laws based on Kandi’s disclosure in March 2017 that its financial statements for the years 2014, 2015 and the first three quarters of 2016 would need to be restated, and sought damages on behalf of putative classes of shareholders who purchased or acquired Kandi’s securities prior to March 13, 2017. Kandi moved to dismiss the remaining cases, all of which were pending in the New York federal court, that motion was granted in September 2019, and the time to appeal has run. In June 2020, a similar but separate putative securities class action was filed against Kandi and certain of its current and former directors and officers in California federal court. This action was transferred to the New York federal court in September 2020, Kandi moved to dismiss in March 2021, and that motion was granted in October 2021. The plaintiff in this case subsequently filed an amended complaint, Kandi moved to dismiss that complaint in January 2022, and the motion was granted in part and denied in part in September 2022. Discovery is ongoing as to the remaining claims and defendants.

18

Beginning in May 2017, purported shareholder derivative actions based on the same underlying events described above were filed against certain current and former directors of Kandi in the United States District Court for the Southern District of New York. The New York federal court confirmed the voluntary dismissal of these actions in April 2019.

In October 2017, a shareholder filed a books and records action against the Company in the Delaware Court of Chancery pursuant to 8 Del. C. Section 220 seeking the production of certain documents generally relating to the same underlying items described above as well as attorney’s fees (the “Section 220 Litigation”). On September 28, 2018, the parties, through their respective counsel, agreed to dismiss the Section 220 Litigation with prejudice and with each party bearing its own attorney’s fees, costs, and expenses, thereby concluding the action. In February 2019, this same shareholder commenced a derivative action against certain current and former directors of Kandi in the Delaware Court of Chancery. A motion to dismiss this derivative action was filed in May 2019 and that motion was denied on April 27, 2020. Discovery is ongoing.

Separately, in connection with allegations of misconduct identified in pre-suit demands made by putative shareholders of Kandi, Kandi formed a Special Litigation Committee (“SLC”) and retained a Delaware law firm as independent counsel to the SLC to aid in the SLC’s investigation of, and to ultimately report on, the allegations of misconduct set forth in the pre-suit demands. The SLC recommended to Kandi’s board of directors in June 2020 that the SLC be dissolved in light of the ongoing derivative action pending in the Delaware Court of Chancery, and this recommendation was adopted by the board in August 2020.

In December 2020, a putative securities class action was filed against Kandi and certain of its current officers in the United States District Court for the Eastern District of New York. The complaint generally alleges violations of the federal securities laws based on claims made in a report issued by Hindenburg Research in November 2020, and seeks damages on behalf of a putative class of shareholders who purchased or acquired Kandi’s securities prior to March 15, 2019. Kandi moved to dismiss in February 2022, and that motion remains pending.

While the Company believes that the claims in these litigations are without merit and will defend itself vigorously, the Company is unable to estimate the possible loss, if any, associated with these litigations. The ultimate outcome of any litigation is uncertain and the outcome of these matters, whether favorable or unfavorable, could have a negative impact on the Company’s financial condition or results of operations due to defense costs, diversion of management resources and other factors. Defending litigation can be costly, and adverse results in the litigations could result in substantial monetary judgments. No assurance can be made that litigation will not have a material adverse effect on the Company’s future financial position.

NOTE 22 - SEGMENT REPORTING

The Company has

The following table sets forth disaggregation of revenue:

| Three Months Ended March 31 | ||||||||

| 2023 | 2022 | |||||||

| Sales Revenue | Sales Revenue | |||||||

| Primary geographical markets | ||||||||

| U.S. and other countries/areas | $ | $ | ||||||

| China | ||||||||

| Total | $ | $ | ||||||

| Major products | ||||||||

| EV parts | $ | $ | ||||||

| EV products | ||||||||

| Off-road vehicles and associated parts | ||||||||

| Electric Scooters, Electric Self-Balancing Scooters and associated parts | ||||||||

| Battery exchange equipment and Battery exchange service | ||||||||

| Lithium-ion cells | ||||||||

| Total | $ | $ | ||||||

| Timing of revenue recognition | ||||||||

| Products transferred at a point in time | $ | $ | ||||||

| Total | $ | $ | ||||||

19

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

This report contains forward-looking statements within the meaning of the federal securities laws that relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminologies, such as “may,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “predict,” “intend,” “potential” or “continue” or the negative of such terms or other comparable terminologies, although not all forward-looking statements contain such terms.

In addition, these forward-looking statements include, but are not limited to, statements regarding implementing our business strategy; development and marketing of our products; our estimates of future revenue and profitability; our expectations regarding future expenses, including research and development, sales and marketing, manufacturing and general and administrative expenses; difficulty or inability to raise additional financing, if needed, on terms acceptable to us; our estimates regarding our capital requirements and our needs for additional financing; attracting and retaining customers and employees; sources of revenue and anticipated revenue; and competition in our market.

Forward-looking statements are only predictions. Although we believe that the expectations reflected in these forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. All of our forward-looking information is subject to risks and uncertainties that could cause actual results to differ materially from the results expected. Although it is not possible to identify all factors, these risks and uncertainties include the risk factors and the timing of any of those risk factors described in the 2022 Form 10-K and those set forth from time to time in our other filings with the SEC. These documents are available on the SEC’s Electronic Data Gathering and Analysis Retrieval System at http://www.sec.gov.

Critical Accounting Policies and Estimates

The preparation of the condensed consolidated financial statements in conformity with U.S. GAAP requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities, as of the date of the financial statements, and the reported amounts of revenue and expenses during the reported period. If these estimates differ significantly from actual results, the impact to the condensed consolidated financial statements may be material. There have been no material changes in our critical accounting policies and estimates from those disclosed in on the 2022 Form 10-K. Please refer to Part II, Item 7 of such a report for a discussion of our critical accounting policies and estimates.

Overview

For the three months ended March 31, 2023, the Company recognized total revenue of $22,862,108 as compared to $24,891,404 for the same period of 2022, a decrease of $2,029,296 or 8.2%. For the three months ended March 31, 2023, we recorded $8,029,230 of gross profit, an increase of $5,642,067 or 236.4% from $2,387,163 for the same period of 2022. Gross margin for the three months ended March 31, 2023, was 35.1%, compared to 9.6% for the same period of 2022. We recorded a net income of $595,457 for the three months ended March 31, 2023, compared to a net loss of $1,619,013 in the same period of 2022, an increase of $2,214,470.

Thanks to our business strategy adjustment, we made considerable progress in electric off-road vehicles, despite the resurgences of COVID-19 in 2022, which has been causing frequent lockdowns in many cities and severe disruption of supply chain. Now with the global trend of “fuel to electrification” of off-road vehicles becoming more and more obvious, we have successfully developed electric crossover golf carts and put them on the market in batches, which have been favored by users. Next, we will successively launch various electric off-road vehicles, including electric crossover golf carts and electric UTVs. With the successively introduction of new products, we are confident to achieve sustained growth in the field of the pure electric off-road vehicles. As for our EV business, due to the fact that the Chinese EV market has not entered a healthy and orderly development stage, currently the Company will continue to operate in small-scale, and join back as appropriate when the EV market of China entered a healthy and orderly development stage.

20

Results of Operations

Comparison of the Three Months Ended March 31, 2023 and 2022

The following table sets forth the amounts and percentage to revenue of certain items in our condensed consolidated statements of operations and comprehensive income (loss) for the three months ended March 31, 2023 and 2022.

| Three Months Ended | ||||||||||||||||||||||||

| March 31, 2023 | % of Revenue | March 31, 2022 | % of Revenue | Change in Amount | Change in % | |||||||||||||||||||

| REVENUES FROM UNRELATED PARTIES, NET | $ | 22,862,108 | 100.0 | % | $ | 24,891,404 | 100.0 | % | (2,029,296 | ) | (8.2 | )% | ||||||||||||

| REVENUES FROM THE FORMER AFFILIATE COMPANY AND RELATED PARTIES, NET | - | 0.0 | % | - | 0.0 | % | - | - | ||||||||||||||||

| REVENUES, NET | 22,862,108 | 100.0 | % | 24,891,404 | 100.0 | % | (2,029,296 | ) | (8.2 | )% | ||||||||||||||

| COST OF GOODS SOLD | (14,832,878 | ) | (64.9 | %) | (22,504,241 | ) | (90.4 | %) | 7,671,363 | (34.1 | )% | |||||||||||||

| GROSS PROFIT | 8,029,230 | 35.1 | % | 2,387,163 | 9.6 | % | 5,642,067 | 236.4 | % | |||||||||||||||

| OPERATING INCOME (EXPENSE): | ||||||||||||||||||||||||

| Research and development | (878,980 | ) | (3.8 | %) | (1,140,586 | ) | (4.6 | %) | 261,606 | (22.9 | )% | |||||||||||||

| Selling and marketing | (1,827,729 | ) | (8.0 | %) | (1,193,699 | ) | (4.8 | %) | (634,030 | ) | 53.1 | % | ||||||||||||

| General and administrative | (7,559,452 | ) | (33.1 | %) | (5,756,531 | ) | (23.1 | %) | (1,802,921 | ) | 31.3 | % | ||||||||||||

| TOTAL OPERATING EXPENSE | (10,266,161 | ) | (44.9 | %) | (8,090,816 | ) | (32.5 | %) | (2,175,345 | ) | 26.9 | % | ||||||||||||

| LOSS FROM OPERATIONS | (2,236,931 | ) | (9.8 | %) | (5,703,653 | ) | (22.9 | %) | 3,466,722 | (60.8 | )% | |||||||||||||

| OTHER INCOME (EXPENSE): | ||||||||||||||||||||||||

| Interest income | 2,100,343 | 9.2 | % | 1,222,304 | 4.9 | % | 878,039 | 71.8 | % | |||||||||||||||

| Interest expense | (173,370 | ) | (0.8 | %) | (148,144 | ) | (0.6 | %) | (25,226 | ) | 17.0 | % | ||||||||||||

| Change in fair value of contingent consideration | (361,000 | ) | (1.6 | %) | 2,690,000 | 10.8 | % | (3,051,000 | ) | (113.4 | )% | |||||||||||||

| Government grants | 620,404 | 2.7 | % | 244,098 | 1.0 | % | 376,306 | 154.2 | % | |||||||||||||||

| Other income, net | 266,465 | 1.2 | % | 43,782 | 0.2 | % | 222,683 | 508.6 | % | |||||||||||||||

| TOTAL OTHER INCOME, NET | 2,452,842 | 10.7 | % | 4,052,040 | 16.3 | % | (1,599,198 | ) | (39.5 | )% | ||||||||||||||

| INCOME (LOSS) BEFORE INCOME TAXES | 215,911 | 0.9 | % | (1,651,613 | ) | (6.6 | %) | 1,867,524 | (113.1 | )% | ||||||||||||||

| INCOME TAX BENEFIT | 379,546 | 1.7 | % | 32,600 | 0.1 | % | 346,946 | 1064.3 | % | |||||||||||||||

| NET INCOME (LOSS) | 595,457 | 2.6 | % | (1,619,013 | ) | (6.5 | %) | 2,214,470 | (136.8 | )% | ||||||||||||||

(a) Revenue

For the three months ended March 31, 2023, Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ revenue was $22,862,108 compared to $24,891,404 for the same period of 2022, representing a decrease of $2,029,296 or 8.2%.

21

The following table summarizes Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ revenues by product types for the three months ended March 31, 2023 and 2022:

| Three Months Ended March 31, | ||||||||

| 2023 | 2022 | |||||||

| Sales | Sales | |||||||

| EV parts | $ | 27,365 | $ | 3,667,778 | ||||

| EV products | - | 339,955 | ||||||

| Off-road vehicles and associated parts | 20,786,134 | 10,713,741 | ||||||

| Electric Scooters, Electric Self-Balancing Scooters and associated parts | 145,991 | 2,127,365 | ||||||

| Battery exchange equipment and Battery exchange service | 97,683 | 25,511 | ||||||

| Lithium-ion cells | 1,804,935 | 8,017,054 | ||||||

| Total | $ | 22,862,108 | $ | 24,891,404 | ||||

EV Parts

During the three months ended March 31, 2023, Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ revenues from the sales of EV parts were $27,365, representing a decrease of $3,640,413 or 99.3% from $3,667,778 for the same quarter of 2022. The decrease was primarily due to the reduced demand from the market during the three months ended March 31, 2023. In addition, due to the large demand from the US market, the Company has been focusing on the production of off-road vehicles, especially crossover golf carts, which could bring in better profit margin.

Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ revenue for the three months ended March 31, 2023 primarily consisted of revenue from the sales of battery packs, body parts, EV controllers, air conditioning units and other auto parts for use in the manufacturing of EV products. These sales accounted for 0.1% of total sales.

EV Products

During the three months ended March 31, 2023, Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ revenue from the sale of EV Products was $0, representing a decrease of 100% from $339,955 for the same quarter of 2022. The decrease was primarily due to less demand from the market for our EV products. In addition, due to the large demand from the US market, the Company has been focusing on the production of off-road vehicles, especially crossover golf carts, which could bring in better profit margin.

Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ EV Products business line accounted for 0% of the total net revenue for the three months ended March 31, 2023.

Off-Road Vehicles and Associated Parts

During the three months ended March 31, 2023, Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ revenue from the sales of off-road vehicles and associated parts, including go karts, all-terrain vehicles (“ATVs”) and others, were $20,786,134, representing an increase of $10,072,393 or 94.0% from $10,713,741, for the same quarter of 2022. The increase was primarily because of the increasing sales of our crossover golf carts in US market during the three months ended March 31, 2023.

Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ off-road vehicles business line accounted for approximately 90.9% of the total net revenue for the three months ended March 31, 2023.

22

Electric Scooters, Electric Self-Balancing Scooters and associated parts

During the three months ended March 31, 2023, Zhejiang Kandi Technologies and its subsidiaries’ revenue from the sales of electric scooters, electric self-balancing scooters and associated parts, were $145,991, representing a decrease of $1,981,374 or 93.1% from $2,127,365, for the same quarter of 2022. The decrease was primarily due to the fact that the Company has been focusing on the production of off-road vehicles, especially crossover golf carts, which could bring in better profit margin due to the demand from the US market.

Zhejiang Kandi Technologies and its subsidiaries’ electric scooters, electric self-balancing scooters and associated parts business line accounted for approximately 0.6% of the total net revenue for the three months ended March 31, 2023.

Battery Exchange Equipment and Battery Exchange Service

During the three months ended March 31, 2023, Zhejiang Kandi Technologies and its subsidiaries’ revenue from the sale of battery exchange equipment and battery exchange service was $97,683, representing an increase of $72,172 or 282.9% from $25,511 for the same period of 2022, due to increase of demands from the car-hailing platforms.

Zhejiang Kandi Technologies and its subsidiaries’ sale of battery exchange equipment and battery exchange service business line accounted for approximately 0.4% of the total net revenue for the three months ended March 31, 2023.

Lithium-ion cells

During the three months ended March 31, 2023, Zhejiang Kandi Technologies and its subsidiaries’ revenue from the sale of Lithium-ion cells was $1,804,935, representing a decrease of $6,212,119 or 77.5% from $8,017,054, for the same quarter of 2022. The decrease was primarily due to less demand from the market.

Zhejiang Kandi Technologies and its subsidiaries’ sale of lithium-ion cells business line accounted for approximately 7.9% of the total net revenue for the three months ended March 31, 2023.

The following table shows the breakdown of Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ net revenues:

| Three Months Ended March 31, | ||||||||

| 2023 | 2022 | |||||||

| Sales Revenue | Sales Revenue | |||||||

| Primary geographical markets | ||||||||

| U.S. and other countries/areas | $ | 20,717,818 | $ | 10,736,375 | ||||

| China | 2,144,290 | 14,155,029 | ||||||

| Total | $ | 22,862,108 | $ | 24,891,404 | ||||

| Major products | ||||||||

| EV parts | $ | 27,365 | $ | 3,667,778 | ||||

| EV products | - | 339,955 | ||||||

| Off-road vehicles and associated parts | 20,786,134 | 10,713,741 | ||||||

| Electric Scooters, Electric Self-Balancing Scooters and associated parts | 145,991 | 2,127,365 | ||||||

| Battery exchange equipment and Battery exchange service | 97,683 | 25,511 | ||||||

| Lithium-ion cells | 1,804,935 | 8,017,054 | ||||||

| Total | $ | 22,862,108 | $ | 24,891,404 | ||||

| Timing of revenue recognition | ||||||||

| Products transferred at a point in time | $ | 22,862,108 | $ | 24,891,404 | ||||

| Total | $ | 22,862,108 | $ | 24,891,404 | ||||

23

(b) Cost of goods sold

Cost of goods sold was $14,832,878 during the three months ended March 31, 2023, representing a decrease of $7,671,363, or 34.1%, compared to $22,504,241 for the same period of 2022. The decrease was primarily due to the corresponding decrease in sales. Please refer to the Gross Profit section below for product margin analysis.

(c) Gross profit

Zhejiang Kandi Technologies, its subsidiaries and SC Autosports’ margins by product for the three months ended March 31, 2023 and 2022 are as set forth below:

| Three Months Ended March 31, | ||||||||||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||||||||||

| Sales | Cost | Gross Profit | Margin % | Sales | Cost | Gross Profit | Margin % | |||||||||||||||||||||||||

| EV parts | $ | 27,365 | 35,366 | (8,001 | ) | -29.2 | % | $ | 3,667,778 | 3,328,203 | 339,575 | 9.3 | % | |||||||||||||||||||

| EV products | - | - | - | - | 339,955 | 319,715 | 20,240 | 6.0 | % | |||||||||||||||||||||||

| Off-road vehicles and associated parts | 20,786,134 | 12,657,151 | 8,128,983 | 39.1 | % | 10,713,741 | 9,288,200 | 1,425,541 | 13.3 | % | ||||||||||||||||||||||

| Electric Scooters, Electric Self-Balancing Scooters and associated parts | 145,991 | 144,230 | 1,761 | 1.2 | % | 2,127,365 | 1,855,115 | 272,250 | 12.8 | % | ||||||||||||||||||||||

| Battery exchange equipment and Battery exchange service | 97,683 | 67,053 | 30,630 | 31.4 | % | 25,511 | 31,720 | (6,209 | ) | -24.3 | % | |||||||||||||||||||||

| Lithium-ion cells | 1,804,935 | 1,929,078 | (124,143 | ) | -6.9 | % | 8,017,054 | 7,681,288 | 335,766 | 4.2 | % | |||||||||||||||||||||

| Total | $ | 22,862,108 | 14,832,878 | 8,029,230 | 35.1 | % | $ | 24,891,404 | 22,504,241 | 2,387,163 | 9.6 | % | ||||||||||||||||||||

Gross profit for the first quarter of 2023 increased 236.4% to $8,029,230, compared to $2,387,163 for the same period last year. This was primarily attributable to product mix with higher concentration to our off-road vehicles, especially crossover golf carts, that brought us with significantly higher gross margin. Higher gross profit was resulted despite less sales was generated in this period. Consequently, our gross margin increased to 35.1% compared to 9.6% for the same period of 2022.

24

(d) Research and development

Research and development expenses, including materials, labor, equipment depreciation, design, testing, inspection, and other related expenses, totaled $878,980 for the first quarter of 2023, a decrease of $261,606 or 22.9% compared to $1,140,586 for the same period in 2022. The decrease was mainly due to less research and development projects were being carried out in the current period.

(e) Sales and marketing

Selling and distribution expenses were $1,827,729 for the first quarter of 2023, compared to $1,193,699 for the same period in 2022, representing an increase of $634,030 or 53.1%. The increase was mainly due to higher commission offered for the sales of off-road vehicles, as well as higher shipping and related expenses incurred due to larger volume of exports to the US market.

(f) General and administrative expenses

General and administrative expenses were $7,559,452 for the first quarter of 2023, compared to $5,756,531 for the same period in 2022, representing an increase of $1,802,921 or 31.3%. For the three months ended March 31, 2023, general and administrative expenses included $1,003,818 as expenses for common stock awards and stock options to employees and Board members, compared to $22,925 of common stock awards and stock options expenses for the same period in 2022. Besides stock compensation expense, our net general and administrative expenses for the three months ended March 31, 2023 were $6,555,634, representing an increase of $822,028, from $5,733,606 for the same period in 2022, which was largely due to expansion of the employees headcount as well as increase in storage fee resulted from the increase of inventories kept in US.

(g) Interest income

Interest income was $2,100,343 for the first quarter of 2023, representing an increase of $878,039 or 71.8% compared to $1,222,304 for the same period of last year. The increase was primarily attributable to the increased interest earned on increased certificate of deposit compared to the same period in 2022.

(h) Interest expenses

Interest expenses were $173,370 in the first quarter of 2023, representing an increase of $25,226 or 17.0% compared to $148,144 for the same period of last year. The increase was primarily due to interest expenses related to increased short-term loans of the Company compared to the same period in 2022.

(i) Change in fair value of contingent consideration

For the first quarter of 2023, the loss related to changes in the fair value of contingent consideration was $361,000, a decrease of $3,051,000 or 113.4% compared to gain related to changes in the fair value of contingent consideration of $2,690,000 for the same period in 2022, which was mainly due to the adjustment of the fair value of the contingent consideration liability associated with the remaining shares of restrictive common stock (Please refer to NOTE 18 – CONTINGENT CONSIDERATION LIABILITY). The fair value of the contingent consideration liability was estimated at each reporting date by using the Monte Carlo simulation method, which took into account all possible scenarios.

25

(j) Government grants

Government grants were $620,404 for the first quarter of 2023, compared to $244,098 for the same quarter last year, representing an increase of $376,306, or 154.2%, which was primarily due to grants from Jinhua and Hainan local government in the first quarter of 2023.

(k) Other income, net

Net other income was $266,465 for the first quarter of 2023, representing an increase of $222,683 or 508.6% compared to net other income of $43,782 for the same period of last year, which was largely due to disposal of obsolete materials during the current period.

(l) Income Taxes

In accordance with the relevant Chinese tax laws and regulations, the applicable corporate income tax rate of our Chinese subsidiaries is 25%. However, four of our subsidiaries, including Zhejiang Kandi Technologies, Kandi Smart Battery Swap, Kandi Hainan and Jiangxi Huiyi are qualified as high technology companies in China and are therefore entitled to a reduced corporate income tax rate of 15%. Additionally, Hainan Kandi Holding also has an income tax rate of 15% due to its local preferred tax rate in Hainan Free Trade Port.

Each of our other subsidiaries, Kandi New Energy, Yongkang Scrou, China Battery Exchange and its subsidiaries has an applicable corporate income tax rate of 25%.

Our actual effective income tax rate for the first quarter of 2023 was a tax benefit of 175.79% on a reported income before taxes of approximately $0.2 million, compared to a tax benefit of 1.97% on a reported loss before taxes of approximately $1.7 million for the same period of last year.

(m) Net income (loss)

Net income was $595,457 for the first quarter of 2023, representing an increase of $2,214,470 compared to net loss of $1,619,013 for the same period in 2022. The increase of net income was primarily attributable to the increase in gross profit resulted from a higher concentration of sales from off-road vehicles with larger gross margin.

LIQUIDITY AND CAPITAL RESOURCES

Cash Flow

| Three Months Ended | ||||||||

| March 31, 2023 | March 31, 2022 | |||||||

| Net cash provided by operating activities | $ | 7,362,198 | $ | 6,188,441 | ||||

| Net cash used in investing activities | $ | (19,636,864 | ) | $ | (16,716,300 | ) | ||

| Net cash used in by financing activities | $ | (1,358,565 | ) | $ | (279,829 | ) | ||

| NET DECREASE IN CASH AND CASH EQUIVALENTS AND RESTRICTED CASH | $ | (13,633,231 | ) | $ | (10,807,688 | ) | ||

| Effect of exchange rate changes | $ | 676,206 | $ | 352,415 | ||||

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT BEGINNING OF YEAR | $ | 151,040,271 | $ | 168,676,007 | ||||

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT END OF PERIOD | $ | 138,083,246 | $ | 158,220,734 | ||||

26

For the first quarter of 2023, cash derived from operating activities was $7,362,198, as compared to cash derived from operating activities of $6,188,441 for the same period last year. Our operating cash inflows include cash received primarily from sales of our EV parts, off-road vehicles, electric Scooters, electric self-balancing scooters and associated parts and lithium-ion cells. These cash inflows are offset largely by cash paid primarily to our suppliers for production materials and parts used in our manufacturing process, operation expenses, employee compensation, and interest expenses of our financings. The major operating activities that provided cash for the first quarter of 2023 were a decrease of accounts receivable of $6,275,418 and an increase of accounts payable of $6,097,620. The major operating activity that used cash for first quarter of 2023 was an increase of inventories of $6,750,531 and a decrease of notes payable of $5,413,459.

For the first quarter of 2023, cash used in investing activities was $19,636,864, as compared to cash used in investing activities of $16,716,300 for the same period in 2022. The major investing activity that used cash for first quarter of 2023 was an increase of certificate of deposit of $19,001,959.

For the first quarter of 2023, cash used in financing activities was $1,358,565, as compared to cash used in financing activities of $279,829 for the same period in 2022. The major financing activities that provided cash for first quarter of 2023 were proceeds from short-term bank loans of $5,040,000. The major financing activities that used cash for first quarter of 2023 were repayments of short-term loans of $6,398,565.

Working Capital

We had a working capital of $253,144,741 as of March 31, 2023, which reflects an increase of $5,327,616 from a working capital of $247,817,125 as of December 31, 2022.

Contractual Obligations and Off-balance Sheet Arrangements

Guarantees and pledged collateral for third party bank loans

For the discussion of guarantees and pledged collateral for third party bank loans, please refer to Note 21 – COMMITMENTS AND CONTINGENCIES under Notes to Condensed Consolidated Financial Statements.

Item 3. Quantitative and Qualitative Disclosures about Market Risk

This item is not applicable to us.

Item 4. Controls and Procedures.

Evaluation of Disclosure Controls and Procedures

We have evaluated, under the supervision of our Chief Executive Officer (“CEO”) and our Chief Financial Officer (“CFO”), the effectiveness of disclosure controls and procedures (as such term is defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934 (the “Exchange Act”) as of March 31, 2023. Based on this evaluation, our CEO and CFO concluded that as of the end of the period covered by this report, our disclosure controls and procedures were effective.

Disclosure controls and procedures are controls and procedures that are designed to ensure that information required to be disclosed in our reports filed or submitted under the Exchange Act (a) is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms and (b) is accumulated and communicated to management, including our CEO and CFO, as appropriate, to allow timely decisions regarding required disclosure. Our management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving their objectives and management necessarily applies its judgment in evaluating the cost-benefit relationship of possible controls and procedures. Our disclosure controls and procedures are designed to provide reasonable assurance of achieving their objectives as described above.

Changes in Internal Control over Financial Reporting

There was no change to our internal control over financial reporting (as defined in Rules 13a-15(f) and 15d-15(f) under the Exchange Act) that occurred during the period covered by this report that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

27

PART II – OTHER INFORMATION

Item 1. Legal Proceedings.

From time to time, the Company is involved in legal matters arising in the ordinary course of business. Except as set forth in Note 21 - COMMITMENTS AND CONTINGENCIES under Notes to Condensed Consolidated Financial Statements, our management is currently not aware of any legal matters or pending litigation that would have a significant effect on the Company’s results of operation of financial statements. Furthermore, the Company is not aware of any other legal matters in which any director, officer, or any owner of record or beneficial owner of more than five percent of any class of voting securities of the Company, or any affiliate of any such director, officer, affiliate of the Company, or security holder, is a party adverse to the Company or has a material adverse interest to the Company. For the detailed discussion of our legal proceedings, please refer to Note 21 - COMMITMENTS AND CONTINGENCIES under Notes to Condensed Consolidated Financial Statements, which is incorporated by reference herein.

28

Item 6. Exhibits

| † | Exhibits filed herewith. |

29

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Date: May 10, 2023 | By: | /s/ Dong Xueqin |

| Dong Xueqin | ||

| President and Chief Executive Officer | ||

| (Principal Executive Officer) | ||

| Date: May 10, 2023 | By: | /s/ Jehn Ming Lim |

| Jehn Ming Lim | ||

| Chief Financial Officer | ||

| (Principal Financial Officer and Principal | ||

| Accounting Officer) |

30