UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2011

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______to______

Commission file number 001-52186

Kandi Technologies, Corp.

(Exact name of registrant as specified in charter)

|

Delaware

|

90-0363723

|

||

|

(State or other jurisdiction of

|

(I.R.S. Employer Identification No.)

|

||

|

incorporation or organization)

|

Jinhua City Industrial Zone

Jinhua, Zhejiang Province

People’s Republic of China

Post Code 321016

(Address of principal executive offices)

(86 - 0579) 82239856

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

Non-accelerated filer ¨

|

Smaller reporting company þ

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes No þ

As of August 8, 2011 the registrant had issued and outstanding 27,445,600 shares of common stock, par value $.001 per share.

|

Page

|

||

|

PART I— FINANCIAL INFORMATION

|

||

|

Item 1.

|

Financial Statements

|

3 |

|

Condensed Consolidated Balance Sheets as of June 30, 2011 (unaudited) and December 31, 2010

|

3 | |

|

Condensed Consolidated Statements of Income (Loss) and Comprehensive Income (Loss) (unaudited)–Ended June 30, 2011 and June 30, 2010

|

5 | |

|

Condensed Consolidated Statements of Cash Flows (unaudited)–Six months Ended June 30, 2011 and June 30, 2010

|

7 | |

|

Item 2.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

32 |

|

Item 3.

|

Quantitative and Qualitative Disclosures about Market Risk

|

41 |

|

Item 4.

|

Controls and Procedures

|

41 |

|

PART II— OTHER INFORMATION

|

||

|

Item 1

|

Legal Proceedings

|

42 |

|

Item 1A.

|

Risk Factors

|

42 |

|

Item 2.

|

Unregistered Sales of Equity Securities and Use of Proceeds

|

42 |

| Item 3. |

Defaults Upon Senior Securities

|

42 |

|

Item 4.

|

[Removed and Reserved]

|

42 |

|

Item 5.

|

Other information

|

42 |

|

Item 6.

|

Exhibits

|

43 |

2

PART I— FINANCIAL INFORMATION

Item 1. Financial Statements. (Unaudited)

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

|

June 30,

|

December 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

(Unaudited)

|

||||||||

|

ASSETS

|

||||||||

|

CURRENT ASSETS

|

||||||||

|

Cash and cash equivalents

|

$

|

9,372,223

|

$

|

7,754,166

|

||||

|

Restricted cash

|

26,768,895

|

17,398,087

|

||||||

|

Accounts receivable

|

9,292,373

|

16,999,430

|

||||||

|

Inventories

|

11,303,780

|

5,886,506

|

||||||

|

Notes receivable

|

20,848,877

|

24,865,989

|

||||||

|

Other receivables

|

1,615,858

|

814,327

|

||||||

|

Prepayments and prepaid expenses

|

57,565

|

97,298

|

||||||

|

Due from employees

|

11,288

|

36,385

|

||||||

|

Advances to suppliers

|

9,676,652

|

188,585

|

||||||

|

Marketable securities (trading)

|

-

|

300,675

|

||||||

|

Due from related party

|

-

|

-

|

||||||

|

Total Current Assets

|

|

88,947,511

|

74,341,448

|

|||||

|

LONG-TERM ASSETS

|

||||||||

|

Plant and equipment, net

|

22,443,449

|

23,911,626

|

||||||

|

Land use rights, net

|

10,952,529

|

10,833,452

|

||||||

|

Construction in progress

|

94,871

|

-

|

||||||

|

Deferred taxes

|

217,920

|

255,948

|

||||||

|

Investment in associated companies

|

261,427

|

272,241

|

||||||

|

Total Long-Term Assets

|

33,970,196

|

35,273,267

|

||||||

|

TOTAL ASSETS

|

$

|

122,917,707

|

$

|

109,614,715

|

||||

See accompanying notes to condensed consolidated financial statements

3

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

|

June 30,

|

December 31,

|

|||||||

|

2011

|

2010

|

|||||||

|

(Unaudited)

|

||||||||

|

LIABILITIES AND STOCKHOLDERS’ EQUITY

|

||||||||

|

CURRENT LIABILITIES

|

||||||||

|

Accounts payable

|

$

|

5,167,990

|

$

|

6,452,652

|

||||

|

Other payables and accrued expenses

|

670,386

|

794,625

|

||||||

|

Short-term bank loans

|

29,084,158

|

28,434,012

|

||||||

|

Customer deposits

|

73,250

|

82,127

|

||||||

|

Notes payable (net of discount of $508 and $0 as of June 30, 2011and December 31, 2010 respectively)

|

29,858,165

|

19,039,898

|

||||||

|

Income tax payable

|

188,385

|

127,339

|

||||||

|

Due to employees

|

7,887

|

12,767

|

||||||

|

Due to related party

|

841,251

|

841,251

|

||||||

|

Deferred taxes

|

43,672

|

34,083

|

||||||

|

Financial derivative

|

83

|

-

|

||||||

|

Total Current Liabilities

|

65,935,227

|

55,818,754

|

||||||

|

LONG-TERM LIABILITIES

|

||||||||

|

Note payable, (net of discount of $0 and $730 as of June 30, 2011 and December 31, 2010 respectively)

|

-

|

270

|

||||||

|

Financial derivative

|

1,568,699

|

9,321,553

|

||||||

|

Total Long-Term Liabilities

|

1,568,699

|

9,321,823

|

||||||

|

TOTAL LIABILITIES

|

67,503,926

|

65,140,577

|

||||||

|

STOCKHOLDERS’ EQUITY

|

||||||||

|

Common stock, $0.001 par value; 100,000,000 shares authorized; 27,443,100 and 27,396,101 shares issued and outstanding at June 30, 2011 and December 31, 2010, respectively

|

27,443

|

27,396

|

||||||

|

Additional paid-in capital

|

31,323,533

|

31,090,100

|

||||||

|

Retained earnings (the restricted portion is $1,319,067 at June 30, 2011 and December 31, 2010)

|

19,655,303

|

10,095,560

|

||||||

|

Accumulated other comprehensive income

|

4,407,502

|

3,261,082

|

||||||

|

TOTAL STOCKHOLDERS’ EQUITY

|

55,413,781

|

44,474,138

|

||||||

|

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY

|

$

|

122,917,707

|

$

|

109,614,715

|

||||

See accompanying notes to condensed consolidated financial statements

4

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME (LOSS) AND

COMPREHENSIVE INCOME (LOSS)

(UNAUDITED)

|

Three Months Ended

|

Six Months Ended

|

|||||||||||||||

|

June 30, 2011

|

June 30, 2010

|

June 30, 2011

|

June 30, 2010

|

|||||||||||||

|

REVENUES, NET

|

$ | 10,137,702 | $ | 9,911,884 | $ | 18,479,208 | $ | 18,166,224 | ||||||||

|

COST OF GOODS SOLD

|

(7,795,987 | ) | (7,559,235 | ) | (14,076,060 | ) | (13,963,654 | ) | ||||||||

|

GROSS PROFIT

|

2,341,715 | 2,352,649 | 4,403,148 | 4,202,570 | ||||||||||||

|

Research and development

|

574,588 | 400,370 | 1,086,540 | 743,768 | ||||||||||||

|

Selling and distribution expenses

|

92,679 | 89,685 | 149,615 | 942,013 | ||||||||||||

|

General and administrative expenses

|

827,529 | 1,147,061 | 1,501,396 | 1,797,872 | ||||||||||||

|

INCOME (LOSS) FROM OPERATIONS

|

846,919 | 715,533 | 1,665,597 | 718,917 | ||||||||||||

|

Interest income (expense), net

|

275,466 | (671,945 | ) | (21,804 | ) | (1,442,536 | ) | |||||||||

|

Change in fair value of financial instruments

|

2,367,594 | 1,213,169 | 7,752,772 | 1,775,809 | ||||||||||||

|

Government grants

|

273,139 | 45,950 | 280,727 | 75,789 | ||||||||||||

|

Investment (loss) income

|

(8,490 | ) | - | (7,276 | ) | |||||||||||

|

Other income, net

|

53,526 | 10,801 | 167,232 | 57,859 | ||||||||||||

|

INCOME (LOSS) FROM OPERATIONS BEFORE INCOME TAXES

|

3,808,154 | 1,313,508 | 9,837,248 | 1,185,838 | ||||||||||||

|

INCOME TAX (EXPENSE) BENEFIT

|

(186,811 | ) | (124,741 | ) | (277,505 | ) | (175,056 | ) | ||||||||

|

NET INCOME (LOSS)

|

3,621,343 | 1,188,767 | 9,559,743 | 1,010,782 | ||||||||||||

See accompanying notes to condensed consolidated financial statements

5

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME (LOSS) AND

COMPREHENSIVE INCOME (LOSS)

(UNAUDITED)

|

Three Months Ended

|

Six Months Ended

|

|||||||||||||||

|

June 30, 2011

|

June 30, 2010

|

June 30, 2011

|

June 30, 2010

|

|||||||||||||

|

OTHER COMPREHENSIVE INCOME

|

||||||||||||||||

|

Foreign currency translation

|

827,820 | 137,493 | 1,146,420 | 130,941 | ||||||||||||

|

COMPREHENSIVE INCOME (LOSS)

|

4,449,163 | 1,326,260 | 10,706,163 | 1,141,723 | ||||||||||||

|

WEIGHTED AVERAGE SHARES OUTSTANDING BASIC

|

27,440,878 | 20,866,109 | 27,431,851 | 20,424,671 | ||||||||||||

|

WEIGHTED AVERAGE SHARES OUTSTANDING DILUTED

|

28,578,592 | 24,677,264 | 28,786,145 | 22,004,992 | ||||||||||||

|

NET INCOME (LOSS) PER SHARE, BASIC

|

$ | 0.13 | $ | 0.06 | $ | 0.35 | $ | 0.05 | ||||||||

|

NET INCOME (LOSS) PER SHARE, DILUTED

|

$ | 0.13 | $ | 0.05 | $ | 0.33 | $ | 0.05 | ||||||||

See accompanying notes to condensed consolidated financial statements

6

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

|

Six Months Ended June 30

|

||||||||

|

2011

|

2010

|

|||||||

|

CASH FLOWS FROM OPERATING ACTIVITIES:

|

||||||||

|

Net income (loss)

|

$ | 9,559,743 | $ | 1,010,782 | ||||

|

Adjustments to reconcile net (loss) income to net cash (used in) provided by operating activities:

|

||||||||

|

Depreciation and amortization

|

2,317,662 | 1,935,980 | ||||||

|

Deferred taxes

|

58,459 | (10,549 | ) | |||||

|

Option and warrant expense

|

138,315 | 2,055,699 | ||||||

|

Change of derivative instrument’s fair value

|

(7,752,771 | ) | (2,205,548 | ) | ||||

|

Investment loss (income) in associated company

|

16,819 | - | ||||||

|

Changes in operating assets and liabilities:

|

||||||||

|

(Increase) Decrease In:

|

||||||||

|

Accounts receivable

|

7,991,676 | 2,757,111 | ||||||

|

Inventories

|

(5,214,768 | ) | (4,175,053 | ) | ||||

|

Other receivables

|

(773,085 | ) | (197,550 | ) | ||||

|

Due from employees

|

20,490 | (111,654 | ) | |||||

|

Prepayments and prepaid expenses

|

(9,321,749 | ) | 627,935 | |||||

|

Marketable equity securities (trading)

|

303,596 | - | ||||||

|

Increase (Decrease) In:

|

||||||||

|

Accounts payable

|

(1,413,790 | ) | 3,149,816 | |||||

|

Other payables and accrued liabilities

|

(134,299 | ) | (285,960 | ) | ||||

|

Customer deposits

|

(10,616 | ) | 110,017 | |||||

|

Income tax payable

|

57,387 | (76,918 | ) | |||||

|

Net cash (used in) provided by operating activities

|

$ | (4,156,931 | ) | $ | 4,584,108 | |||

|

CASH FLOWS FROM INVESTING ACTIVITIES:

|

||||||||

|

Purchases of plant and equipment

|

(201,490 | ) | (700,530 | ) | ||||

|

Purchase of construction in progress

|

(93,652 | ) | - | |||||

|

Issuance of notes receivable

|

(2,733,584 | ) | (17,168,835 | ) | ||||

|

Repayments of notes receivable

|

7,260,308 | 2,268,415 | ||||||

|

Net cash provided by (used in) investing activities

|

$ | 4,231,582 | $ | (15,600,950 | ) | |||

See accompanying notes to condensed consolidated financial statements

7

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

|

Six Months Ended June 30

|

||||||||

|

2011

|

2010

|

|||||||

|

CASH FLOWS FROM FINANCING ACTIVITIES:

|

||||||||

|

Restricted cash

|

$ | (8,857,647 | ) | $ | (2,342,549 | ) | ||

|

Proceeds from short-term bank loans

|

14,507,848 | 19,166,786 | ||||||

|

Repayments of short-term bank loans

|

(14,507,848 | ) | (18,142,607 | ) | ||||

|

Proceeds from notes payable

|

29,473,839 | 20,241,794 | ||||||

|

Repayments of notes payable

|

(19,224,884 | ) | (7,934,394 | ) | ||||

|

Option exercise and other financing

|

60,069 | 744,911 | ||||||

|

Repayments of advances to related parties

|

- | - | ||||||

|

Net cash provided by financing activities

|

1,451,377 | 11,733,941 | ||||||

|

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS

|

1,526,028 | 717,099 | ||||||

|

Effect of exchange rate changes on cash

|

92,029 | (55,742 | ) | |||||

|

Cash and cash equivalents at beginning of period

|

7,754,166 | 218,207 | ||||||

|

CASH AND CASH EQUIVALENTS AT END OF PERIOD

|

$ | 9,372,223 | $ | 879,564 | ||||

|

SUPPLEMENTARY CASH FLOW INFORMATION

|

||||||||

|

Income taxes paid

|

$ | 220,119 | $ | 262,591 | ||||

|

Interest paid

|

$ | 1,232,993 | $ | 891,042 | ||||

SUPPLEMENTAL NON-CASH DISCLOSURE:

During the six months ended June 30, 2011 and 2010, $0 and $0 were transferred from construction in progress to plant and equipment, respectively.

See accompanying notes to condensed consolidated financial statements

8

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 1 - ORGANIZATION AND PRINCIPAL ACTIVITIES

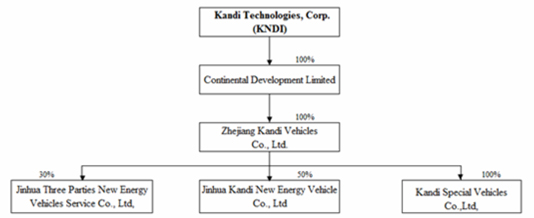

Kandi Technologies, Corp. (the “Company” or “Kandi”, formally known as Stone Mountain Resources Inc.) was incorporated under the laws of the State of Delaware on March 31, 2004. On August 13, 2007, the Company changed its name from Stone Mountain Resources, Inc. to Kandi Technologies, Corp.

The company’s organizational chart as follows:

As the organizational chart reflects, Zhejiang Kandi Vehicles Co. Ltd. has a 50% ownership (voting) interest in Jinhua Kandi New Energy Vehicle Co. Ltd.; however, per the terms and conditions of its contractual arrangement with the other equity owner, Zhejiang Kandi Vehicles Co. Ltd. is entitled to 100% of the economic rights and interests (profits and loss absorption) in Jinhua Kandi New Energy Vehicle Co. Ltd.

The primary operations of the Company are the design, development, manufacturing, and commercializing of all-terrain vehicles, go-karts, and specialized automobiles such as EVs for the PRC and global export markets. Sales are mainly made to trading companies in China, then distributed throughout the world.

NOTE 2 – LIQUIDITY

As of June 30, 2011, the Company’s working capital surplus was $23,012,284; in addition, the Company the Company has credit lines from Chinese commercial banks for $48,267,327, of which $29,084,158 was used as of June 30, 2011.

The Company believes that its cash flows generated internally may not be sufficient, if needed, to support growth of future operations and repay short term bank loans for the next twelve months. However, if necessary, management will pursue financing arrangements including the issuance of debt or equity securities or will reduce expenditures, in order to meet the Company’s cash requirements. Further, the Company believes its access to existing financing sources and established relationships with PRC banks that will enable it to meet its obligations and fund its ongoing operations. That said, there is no assurance that, if required, the Company will be able to raise additional capital or reduce discretionary spending to provide the required liquidity which, in turn, may have an adverse effect on our results of operations and financial position

The Company has historically financed itself through short-term commercial bank loans from PRC banks. The term of these loans are typically for one year, and upon the payment of all outstanding principal and interest in a respective loan, the banks have typically rolled over the loans for additional one-year terms, with adjustments made to the interest rate to reflect prevailing market rates. The Company believes this situation has not changed and the short-term bank loan will be available on normal trade terms if needed.

9

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 3 - BASIS OF PRESENTATION

The Company maintains its general ledger and journals with the accrual method accounting for financial reporting purposes. The financial statements and notes are representations of management. These condensed consolidated financial statements have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”). Accounting policies adopted by the Company conform to U.S. generally accepted accounting principles (“GAAP”) and have been consistently applied in the presentation of financial statements. The results of operations for the three and six month periods ended June 30, 2011 are not necessarily indicative of the results expected for the entire fiscal year ending December 31, 2011.

NOTE 4 – PRINCIPLES OF CONSOLIDATION

The consolidated financial statements reflect the accounts of Kandi and its ownership in following subsidiaries:

|

(i)

|

Continental Development, Ltd. (“Continental”) (a wholly-owned subsidiary of the Company)

|

|

(ii)

|

Zhejiang Kandi Vehicles Co., Ltd. (“Kandi Vehicles”) (a wholly-owned subsidiary of Continental)

|

|

(iii)

|

Kandi Special Vehicles Co., Ltd. (“KSV”, formerly known as Kandi New Energy Vehicles Co., Ltd. “KNE”) (a wholly-owned subsidiary of Kandi Vehicles)

|

|

(iv)

|

Jinhua Three Parties New Energy Vehicles Service Co., Ltd. (“Jinhua Service”) (a 30% owned subsidiary of Kandi Vehicles)

|

|

(v)

|

Jinhua Kandi New Energy Vehicles Co., Ltd. (“Kandi New Energy”) (a 50% owned subsidiary of Kandi Vehicles with 100% profits and loss absorption due to contractual agreement.)

|

Inter-company accounts and transactions have been eliminated in consolidation.

NOTE 5 – USE OF ESTIMATES

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements, and the reported amounts of revenue and expenses during the reporting period. Management makes these estimates using the best information available at the time the estimates are made; however actual results when ultimately realized could differ from those estimates.

NOTE 6 – RISKS AND UNCERTAINTIES AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(a) Economic; Exchange Rate; Political Risks

The Company’s operations are conducted in the PRC. Accordingly, the Company’s business, financial condition and results of operations may be influenced by the political, economic and legal environments in the PRC, and by the general state of the PRC economy.

Our operations are conducted mainly in the PRC. As such, our earnings are subject to movements in foreign currency exchange rates when transactions are denominated in RMB, which is our functional currency. Accordingly, our operating results are affected by changes in the exchange rate between the U.S. dollar and those currencies.

The Company’s operations in the PRC are subject to special considerations and significant risks not typically associated with companies in North America and Western Europe. These include risks associated with, among others, the political, economic and legal environment and foreign currency exchange. The Company’s results may be adversely affected by changes in the political and social conditions in the PRC, and by changes in governmental policies with respect to laws and regulations, anti-inflationary measures, currency conversion, remittances abroad, and rates and methods of taxation, among other things.

10

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 6 – RISKS AND UNCERTAINTIES AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(b) Fair Value of Financial Instruments

ASC 820 establishes a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value. The hierarchy prioritizes the inputs into three levels based on the extent to which inputs used in measuring fair value are observable in the market.

These tiers include:

|

·

|

Level 1—defined as observable inputs such as quoted prices in active markets;

|

|

·

|

Level 2—defined as inputs other than quoted prices in active markets that are either directly or indirectly observable; and

|

|

·

|

Level 3—defined as unobservable inputs in which little or no market data exists, therefore requiring an entity to develop its own assumptions.

|

The assets measured at fair value on a recurring basis subject to the disclosure requirements of ASC 820 as of June 30, 2011 are as follows:

|

Fair Value Measurements at Reporting Date Using Quoted Prices in

|

||||||||||||||||

|

Carrying value as

|

Active Markets for

Identical Assets

|

Significant Other

Observable Inputs

|

Significant

Unobservable

Inputs

|

|||||||||||||

|

of June 30, 2011

|

(Level 1)

|

(Level 2)

|

(Level 3)

|

|||||||||||||

|

Cash and cash equivalents

|

$ | 9,372,223 | $ | 9,372,223 | - | - | ||||||||||

|

Restricted cash

|

26,768,895 | 26,768,895 | - | - | ||||||||||||

|

Conversion features

|

83 | - | 83 | - | ||||||||||||

|

Warrants

|

1,568,699 | - | 1,568,699 | - | ||||||||||||

Cash and cash equivalents consist primarily of highly rated money market funds at a variety of well-known institutions with original maturities of three months or less. Restricted cash represents time deposits on account to secure short-term bank loans and notes payable. The original cost of these assets approximates fair value due to their short term maturity.

Warrants and conversion features embedded in the convertible notes, which are accounted as liabilities, are treated as derivative instruments, which will be measured at each reporting date for their fair value using Level 2 inputs. Also see Note 6 section (s) and (t).

The Company’s non-financial assets are measured on a recurring basis. These non-financial assets are measured for impairment annually on the Company’s measurement date at the reporting unit level using Level 3 inputs. For most assets, ASC 820 requires that the impact of changes resulting from its application be applied prospectively in the year in which the statement is initially applied.

The Company’s non-financial assets measured on a non-recurring basis include the Company’s property, plant and equipment and finite-use intangible assets which are measured for recoverability when indicators for impairment are present. ASC 820 requires companies to disclose assets and liabilities measured on a non-recurring basis in the period in which the remeasurement at fair value is performed. The Company has reviewed its long-lived assets as of June 30, 2011 and determined that there are no significant assets to be tested for recoverability under ASC 360 and as such, no fair value measurements related to non-financial assets have been made during the six months ended June 30, 2011.

11

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 6 – RISKS AND UNCERTAINTIES AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(c) Cash and Cash Equivalents

The Company considers highly liquid investments purchased with original maturities of three months or less to be cash equivalents.

Restricted cash on June 30, 2011 and December 31, 2010 represent time deposits on account to secure short-term bank loans and notes payable. Also see Notes 14 and 15.

(d) Inventories

Inventories are stated at the lower of cost or net realizable value (market value). The cost of raw materials is determined on the basis of weighted average. The cost of finished goods is determined on the weighted average basis and comprises direct materials, direct labor and an appropriate proportion of overhead.

Net realizable value is based on estimated selling prices less any further costs expected to be incurred for completion and selling expense.

(e) Accounts Receivable

Accounts receivable are recognized and carried at net realizable value. An allowance for doubtful accounts will be recorded in the period when a loss is probable based on an assessment of specific evidence indicating troubled collection, historical experience, accounts aging, ongoing business relation and other factors. Accounts are written off after exhaustive efforts at collection. If accounts receivable are to be provided for, or written off, they would be recognized in the consolidated statement of operations within operating expenses. At June 30, 2011 and December 31, 2010, the Company has an allowance for doubtful accounts of $0, as per the management's judgment based on their best knowledge.

As of June 30, 2011 and December 31, 2010, the longest credit term for certain customers are both 120 days.

(f) Note receivable

Notes receivable represents short-term loans to third parties with the maximum term of one year. Interest income is recognized according to each agreement between a borrower and the Company on an accrual basis. If notes receivable are to be provided for, or written off, they are recognized in the relevant year if the loan default is probable, reasonably sure and the loss can be reasonably estimated. The Company recognizes income if the written-off loan is recovered at a future date. In case of foreclosure procedures or legal actions being taken, the Company provides accrual for the related foreclosure expense and related litigation expenses.

(g) Prepayments

Prepayments represent cash paid in advance to suppliers for raw materials used in the manufacturing process. For fiscal quarter ended June 30, 2011, prepayments was primarily comprised of advancements to mold manufactures. However, prepaid expenses, such as water and electricity fees, also contributed to the total number.

(h) Plant and Equipment

Plant and equipment are carried at cost less accumulated depreciation. Depreciation is provided over their estimated useful lives, using the straight-line method. Leasehold improvements are amortized over the life of the asset or the term of the lease, whichever is shorter. Estimated useful lives are as follows:

|

Buildings

|

30 years

|

|

Machinery and equipment

|

10 years

|

|

Office equipment

|

5 years

|

|

Motor vehicles

|

5 years

|

|

Molds

|

5 years

|

12

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 6 – RISKS AND UNCERTAINTIES AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

The cost and related accumulated depreciation of assets sold or otherwise retired are eliminated from the accounts and any gain or loss is included in the statement of income. The cost of maintenance and repairs is charged to expense as incurred, whereas significant renewals and betterments are capitalized.

(i) Construction in Progress

Construction in progress represents direct costs of construction or the acquisition cost of buildings or machinery and design fees. Capitalization of these costs ceases and the construction in progress is transferred to plant and equipment when substantially all the activities necessary to prepare the assets for their intended use are completed. No depreciation is provided until the assets are completed and ready for their intended use.

(j) Land Use Rights

According to the laws of China, land in the PRC is owned by the government and cannot be sold to an individual or a company. However, the government grants the user a “land use right” to use the land. The land use rights granted to the Company are being amortized using the straight-line method over the lease term of fifty years.

(k) Accounting for the Impairment of Long-Lived Assets

The Company periodically evaluates the carrying value of long-lived assets to be held and used, including intangible assets subject to amortization, when events and circumstances warrant such a review, pursuant to the guidelines established in ASC No. 350. The carrying value of a long-lived asset is considered impaired when the anticipated undiscounted cash flow from such asset is separately identifiable and is less than its carrying value. In that event, a loss is recognized based on the amount by which the carrying value exceeds the fair market value of the long-lived asset. Fair market value is determined primarily using the anticipated cash flows discounted at a rate commensurate with the risk involved. Losses on long-lived assets to be disposed of are determined in a similar manner, except that fair market values are reduced for the cost to dispose.

During the reporting period, there was no impairment loss.

(l) Revenue Recognition

Revenues represent the invoiced value of goods sold, recognized upon the shipment of goods to customers. Revenues are recognized when all of the following criteria are met:

· Persuasive evidence of an arrangement exists;

· Delivery has occurred or services have been rendered;

· The seller’s price to the buyer is fixed or determinable; and

· Collectability is reasonably assured.

(m) Research and Development

Expenditures relating to the development of new products and processes, including significant improvement to existing products are expensed as incurred. Research and development expenses were $1,086,540 and $743,768 for the six months ended June 30, 2011 and 2010, respectively.

(n) Government Grant

Grants received from the PRC Government for assisting in the Company’s technical research and development efforts are netted against the relevant research and development costs incurred when the proceeds are received or collectible.

For the six months ended June 30, 2011 and 2010, $280,727 and $75,789, respectively, was received from the PRC government for the Company’s contribution to the local economy.

13

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 6 – RISKS AND UNCERTAINTIES AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(o) Income Taxes

The Company accounts for income tax using an asset and liability approach and allows for recognition of deferred tax benefits in future years. Under the asset and liability approach, deferred taxes are provided for the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. A valuation allowance is provided for deferred tax assets if it is more likely than not these items will either expire before the Company is able to realize their benefits, or that future realization is uncertain.

(p) Foreign Currency Translation

The accompanying consolidated financial statements are presented in United States dollars. The functional currency of the Company is the Renminbi (RMB). Capital accounts of the consolidated financial statements are translated into United States dollars from RMB at their historical exchange rates when the capital transactions occurred.

Assets and liabilities are translated at the exchange rates as of balance sheet date. Income and expenditures are translated at the average exchange rate of the reporting period, which was obtained from website: http://www.oanda.com

|

June 30,

2011

|

December 31,

2010

|

June 30,

2010

|

||||||||||

|

Period end RMB : USD exchange rate

|

6.4640 | 6.6118 | 6.8086 | |||||||||

|

Average period RMB : USD exchange rate

|

6.5482 | 6.7788 | 6.8347 | |||||||||

(q) Comprehensive Income

Comprehensive income is defined to include all changes in equity except those resulting from investments by owners and distributions to owners. Among other disclosures, all items that are required to be recognized under current accounting standards as components of comprehensive income are required to be reported in a financial statement that is presented with the same prominence as other financial statements. Comprehensive income includes net income and the foreign currency translation changes.

(r) Stock Option Cost

The Company’s stock option cost is recorded in accordance with ASC 718 and ASC 505.

The fair value of stock options is estimated using the Black-Scholes-Merton model. The Company’s expected volatility assumption is based on the historical volatility of the Company’s stock. The expected life assumption is primarily based on the expiration date of the option. The risk-free interest rate for the expected term of the option is based on the U.S. Treasury yield curve in effect at the time of grant.

Stock option expense recognized is based on awards expected to vest, and there were no estimated forfeitures. ASC standards requires forfeitures to be estimated at the time of grant and revised in subsequent periods, if necessary, if actual forfeitures differ from those estimates.

The stock based compensation expense for the period ended June 30, 2011 is $138,315. Also see Note 17.

14

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 6 – RISKS AND UNCERTAINTIES AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(s) Warrant Cost

The Company’s warrant costs are recorded in liabilities and equities respectively in accordance with ASC 480, ASC 505 and ASC 815.

The fair value of warrant is estimated using the Black-Scholes-Merton model. The Company’s expected volatility assumption is based on the historical volatility of the Company’s stock. The expected life assumption is primarily based on the expiration date of the warrant. The risk-free interest rate for the expected term of the option is based on the U.S. Treasury yield curve in effect at the time of measurement.

The Company determined that the equity based warrants are not considered derivatives under ASC 815, while the warrants, which are freestanding derivatives and are classified as liabilities on the balance sheet, will be measured at fair value on each reporting date, with changes in fair value recognized in earnings as interest expense.

(t) Fair Value of Conversion features

In accordance with ASC 815, the conversion feature of the Convertible Notes is separated from the debt instrument and accounted for separately as a derivative instrument. On the date the Convertible Notes are issued, the conversion feature was recorded as a liability at its fair value, and future decreases in fair value recognized in earnings while increases in fair values recognized in expenses as interest expense.

The Company used the Black-Scholes-Merton option-pricing model to obtain the fair value of the conversion feature. The Company’s expected volatility assumption is based on the historical volatility of the Company’s stock. The expected life assumption is primarily based on the expiration date of the conversion features. The risk-free interest rate for the expected term of the conversion features is based on the U.S. Treasury yield curve in effect at the time of measurement.

NOTE 7 – NEW ACCOUNTING PRONOUNCEMENTS

Recent Accounting Pronouncements

In May 2011, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update No. 2011-04, Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and International Financial Reporting Standards (Topic 820)-Fair Value Measurement ("ASU 2011-04"), to provide a consistent definition of fair value and ensure that the fair value measurement and disclosure requirements are similar between GAAP and International Financial Reporting Standards. ASU 2011-04 changes certain fair value measurement principles and enhances the disclosure requirements. The provisions of this new guidance are effective for fiscal years, and interim periods within those years, beginning after December 15, 2011. The guidance is not expected to have a material impact on our consolidated financial statements.

In June 2011, the FASB issued Accounting Standards Update No. 2011-05, Comprehensive Income (Topic 220)-Presentation of Comprehensive Income ("ASU 2011-05"), to require an entity to present the total of comprehensive income, the components of net income, and the components of other comprehensive income either in a single continuous statement of comprehensive income or in two separate but consecutive statements. ASU 2011-05 eliminates the option to present the components of other comprehensive income as part of the statement of equity. The provisions of this new guidance are effective for fiscal years, and interim periods within those years, beginning after December 15, 2011. The guidance is not expected to have a material impact on our financial position or results of operations.

15

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 8 – CONCENTRATIONS

(a) Customers

The Company’s major customers for the period ended June 30, 2011 accounted for the following percentages of total sales and accounts receivable as follows:

|

Sales

|

Accounts Receivable

|

|||||||||||||||

|

Major

Customers

|

Six Months

Ended June 30,

2011

|

Six Months Ended

June 30, 2010

|

June 30, 2011

|

December 31,

2010

|

||||||||||||

|

Company A

|

63 | % | 27 | % | 32 | % | 61 | % | ||||||||

|

Company B

|

15 | % | 63 | % | 23 | % | 20 | % | ||||||||

|

Company C

|

11 | % | 6 | % | 21 | % | 14 | % | ||||||||

|

Company D

|

2 | % | - | 2 | % | - | ||||||||||

|

Company E

|

1 | % | - | - | - | |||||||||||

(b) Suppliers

The Company’s major suppliers for the six months ended June 30, 2011 accounted for the following percentage of total purchases and accounts payable as follows:

|

Purchases

|

Accounts Payable

|

|||||||||||||||

|

Major Suppliers

|

Six Months

Ended June 30,

2011

|

Six Months Ended

June 30, 2010

|

June 30, 2011

|

December 31,

2010

|

||||||||||||

|

Company F

|

77 | % | 87 | % | - | 26 | % | |||||||||

|

Company G

|

2 | % | 2 | % | 2 | % | 4 | % | ||||||||

|

Company H

|

1 | % | 1 | % | 5 | % | 1 | % | ||||||||

|

Company I

|

1 | % | 1 | % | 5 | % | 1 | % | ||||||||

|

Company J

|

1 | % | 1 | % | 6 | % | 1 | % | ||||||||

Because the Company is dependent on a small number of suppliers and customers, it is reasonably possible that a permanent or temporary disruption in these relationships could result in a severe impact on our results of operations.

NOTE 9 –INCOME (LOSS) PER SHARE

The Company calculates earnings per share in accordance with ASC 260, Earnings Per Share, which requires a dual presentation of basic and diluted earnings per share. Basic earnings per share are computed using the weighted average number of shares outstanding during the fiscal year. Diluted earnings per share represents basic earnings per share adjusted to include the potentially dilutive effect of outstanding stock options, warrants and convertible note (using the if-converted method). For the six months ended June 30, 2011, there are 1,359,290 potentially dilutive common shares.

16

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

The following table sets forth the computation of basic and diluted net income per common share:

|

Six months Ended June 30,

|

2011

|

2010

|

||||||

|

Net income (loss)

|

$ | 9,559,743 | $ | 1,010,782 | ||||

|

Weighted – average shares of common stock outstanding

|

||||||||

|

Basic

|

27,431,851 | 20,424,671 | ||||||

|

Dilutive shares

|

1,354,294 | 1,580,321 | ||||||

|

Diluted

|

28,786,145 | 22,004,992 | ||||||

|

Basic income (loss) per share

|

$ | 0.35 | $ | 0.05 | ||||

|

Diluted income (loss) per share

|

$ | 0.33 | $ | 0.05 | ||||

Also see Note 17.

NOTE 10 - INVENTORIES

Inventories are summarized as follows:

|

June 30, 2011

(Unaudited)

|

December 31, 2010

|

|||||||

|

Raw material

|

$ | 1,510,763 | $ | 1,754,216 | ||||

|

Work-in-progress

|

9,006,694 | 3,668,104 | ||||||

|

Finished goods

|

786,323 | 464,186 | ||||||

| 11,303,780 | 5,886,506 | |||||||

|

Less: reserve for slow moving inventories

|

- | - | ||||||

|

Inventories, net

|

$ | 11,303,780 | $ | 5,886,506 | ||||

Net inventories increased $5,417,274 from December 31, 2010 to June 30, 2011. This increase resulted primarily from the mass production of EV for the Chinese market.

NOTE 11 - NOTES RECEIVABLE

Notes receivable are summarized as follows:

|

June 30, 2011

(Unaudited)

|

December 31,

2010

|

|||||||

|

Notes receivable from unrelated companies:

|

||||||||

|

Due March 3, 2011, interest at 6.0% per annum 1

|

$ | - | $ | 1,205,026 | ||||

|

Due March 5, 2011, interest at 6.0% per annum 2

|

- | 423,168 | ||||||

|

Due April 13, 2011, interest at 9.6% per annum 3

|

- | 1,512,448 | ||||||

|

Due April 29, 2011, interest at 5.31% per annum 4

|

- | 756,224 | ||||||

|

Due September 30, 2011, interest at 9.6% per annum (collected part of principal during this reporting period) 5

|

20,848,877 | 20,969,123 | ||||||

| 20,848,877 | 24,865,989 | |||||||

|

Bank acceptance notes:

|

||||||||

|

Bank acceptance notes

|

- | - | ||||||

|

Notes receivable

|

$ | 20,848,877 | $ | 24,865,989 | ||||

17

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

Details of Notes receivable from unrelated parties as of December 31, 2010

|

Index

|

Amount ($)

|

Counter party

|

Relationship

|

Purpose of Loan

|

Manner of

settlement

|

|||||

|

1

|

1,205,026

|

Hangzhou YuanHai Property Co., Ltd.

|

No relationship beyond loan

|

Receive interest income

|

Repaid in cash

|

|||||

|

2

|

423,168

|

Hangzhou YuanHai Property Co., Ltd.

|

No relationship beyond loan

|

Receive interest income

|

Repaid in cash

|

|||||

|

3

|

1,512,448

|

Yongkang BoTao Trading Co., Ltd.

|

No relationship beyond loan

|

Receive interest income

|

Repaid in cash

|

|||||

|

4

|

756,224

|

JiangXi De’er Chemical Co., Ltd. (*)

|

No relationship beyond loan

|

Receive interest income

|

Repaid in cash

|

|||||

|

5

|

|

20,969,123

|

|

Yongkang HuiFeng Guarantee Co., Ltd.

|

|

No relationship beyond loan

|

|

Receive interest income

|

|

Not due

|

(*) JiangXi De’er Chemical Co., Ltd. is 85% owned by Kandi Investment Group Co. (“KIGC”). KIGC is the guarantor of the Company’s bank loan of $4,234,853 and was also a lender of the note payable of $134,305 as of December 31, 2010. Also see note 15 and note 16 of Form 10-K, as amended, for fiscal year ended 2010. KIGC was a major shareholder of Kandi Vehicles but it transferred all its equity in Kandi Vehicles to Continental Development Limited in November 2006. Since then, Kandi Investment Group has been unrelated to the Company or its affiliates.

Details of Notes receivable from unrelated parties as of June 30, 2011

|

Index

|

Amount ($)

|

Counter party

|

Relationship

|

Purpose of Loan

|

Manner of

settlement

|

|||||

|

5

|

|

20,848,877

|

|

Yongkang HuiFeng

Guarantee Co., Ltd.

|

|

No relationship

beyond loan

|

|

Receive interest

income

|

|

Not due

|

For the six months ended June 30, 2011, the interest income generated from the notes receivable issued to third parties was $902,153.

NOTE 12 – LAND USE RIGHTS

Land use rights consist of the following:

|

June 30, 2011

(Unaudited)

|

December 31, 2010

|

|||||||

|

Cost of land use rights

|

$ | 11,813,206 | $ | 11,549,134 | ||||

|

Less: Accumulated amortization

|

(860,677 | ) | (715,682 | ) | ||||

|

Land use rights, net

|

$ | 10,952,529 | $ | 10,833,452 | ||||

As of June 30, 2011 and December 31, 2010, the net book value of land use rights pledged as collateral for the Company’s bank loans was $4,042,644 and $3,998,555 respectively. Also see Note 15.

As of June 30, 2011 and December 31, 2010, the net book value of land use rights pledged as collateral for bank loans borrowed by Zhejiang Mengdeli Electronic Co., Ltd. (“ZMEC”), an unrelated party of the Company was $6,909,885 and $6,834,897. Also see Notes 19.

It is a common business practice among companies in the region of China where Kandi is located to exchange guarantees for bank debt with no consideration given. It is considered a “favor for favor” business practice and is commonly required by the lending banks as in these cases. ZMEC has provided a guarantee for certain of the Company’s bank loans. As of June 30, 2011, ZMEC had guaranteed bank loan of the Company for a total of $15,470,296. In exchange, the Company provided guarantee for bank loans being borrowed by ZMEC and allowing ZMEC to pledge the Company’s assets. The banks involved in these guarantee transactions typically allow a maximum loan amount based on a 30% to 70% discount on the net book value of the pledged collateral. ZMEC is also a supplier of the Company. Also see Note 14.

18

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

The amortization expense for the six months ended June 30, 2011 and 2010 was $126,977 and $122,121 respectively.

Amortization expense for the next five years and thereafter is as follows:

|

2011 (six months)

|

$ | 126,977 | ||

|

2012

|

253,954 | |||

|

2013

|

253,954 | |||

|

2014

|

253,954 | |||

|

2015

|

253,954 | |||

|

Thereafter

|

9,809,736 | |||

|

Total

|

$ | 10,952,529 |

NOTE 13 – PLANT AND EQUIPMENT

Plant and equipment consist of the following:

|

June 30, 2011

(Unaudited)

|

December 31, 2010

|

|||||||

|

At cost:

|

||||||||

|

Buildings

|

$ | 13,487,784 | $ | 13,073,777 | ||||

|

Machinery and equipment

|

9,921,983 | 9,733,241 | ||||||

|

Office equipment

|

178,253 | 153,441 | ||||||

|

Motor vehicles

|

241,610 | 188,277 | ||||||

|

Moulds

|

14,687,344 | 14,307,730 | ||||||

| 38,516,974 | 37,456,466 | |||||||

|

Less : Accumulated depreciation

|

||||||||

|

Buildings

|

$ | (1,694,510 | ) | $ | (1,437,172 | ) | ||

|

Machinery and equipment

|

(7,406,970 | ) | (6,755,599 | ) | ||||

|

Office equipment

|

(119,117 | ) | (108,034 | ) | ||||

|

Motor vehicles

|

(151,198 | ) | (129,113 | ) | ||||

|

Molds

|

(6,701,730 | ) | (5,114,921 | ) | ||||

| (16,073,525 | ) | (13,544,840 | ) | |||||

|

Plant and equipment, net

|

$ | 22,443,449 | $ | 23,911,626 | ||||

As of June 30, 2011 and December 31, 2010, the net book value of plant and equipment pledged as collateral for the bank loans was $7,155,744 and $7,002,375, respectively. Also see Note 14.

As of June 30, 2011 and December 31, 2010, the net book value of plant and equipment pledged as collateral for bank loans borrowed by Zhejiang Mengdeli Electronic Co., Ltd. (“ZMEC”), a supplier but unrelated party of the Company was $4,637,530 and $4,634,487. Also see Note 19.

Depreciation expense for six months ended June 30, 2011 and 2010 was $2,190,463 and $1,813,859 respectively.

19

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 14 – SHORT TERM BANK LOANS

Short-term loans are summarized as follows:

|

June 30,

2011

(Unaudited)

|

December 31,

2010

|

|||||||

|

Loans from China Communication Bank-Jinhua Branch

|

||||||||

|

Monthly interest only payments at 5.84% per annum, due February 4, 2011, guaranteed by Zhejiang Shuguang industrial Co., Ltd. Mr. Hu Xiaoming, and Mr. Yan Guanwei.

|

$ | - | $ | 756,224 | ||||

|

Monthly interest only payments at 6.66% per annum, due August 18, 2011, guaranteed by Zhejiang Shuguang industrial Co., Ltd. Mr. Hu Xiaoming, and Mr. Yan Guanwei.

|

773,515 | - | ||||||

|

Loans from Commercial Bank-Jiangnan Branch

|

||||||||

|

Monthly interest only payments at 5.84% per annum, due January 5, 2011, guaranteed by Zhejiang Kangli Metal Manufacturing Company, Mr. Hu Xiaoming, Lv Qingjiang, Lv Qingbo, and Ms. Ling Yueping. and pledged by the assets of Jingdezheng Changzhou Export & Import Company

|

- | 3,024,895 | ||||||

|

Monthly interest only payments at 5.84% per annum, due October 15, 2011, guaranteed by Mr. Hu Xiaoming, and Ms. Ling Yueping. and pledged by Company’s assets. Also see Note 12 and Note 13.

|

1,547,030 | 1,512,447 | ||||||

|

Monthly interest only payments at 5.84% per annum, due December 5, 2011, guaranteed by Mr. Hu Xiaoming, and Ms. Ling Yueping. and pledged by Company’s asset. Also see Note 12 and Note 13.

|

773,515 | 756,224 | ||||||

|

Monthly interest only payments at 5.81% per annum, due January 3, 2012, guaranteed by Zhejiang Kangli Metal Manufacturing Company, Mr. Hu Xiaoming, Lv Qingjiang, and Ms. Ling Yueping. and pledged by the assets of Jingdezheng Changzhou Export & Import Company

|

3,094,059 | - | ||||||

|

Loans from Huaxia Bank

|

||||||||

|

Monthly interest only payments at 5.73% per annum, due September 20, 2011, secured by the assets of the Company, guaranteed by Mr.Hu Xiaoming, Ms.Ling Yueping, Zhejiang Kangli Metal Manufacturing Company and Kandi Investment Group Co.

|

4,331,684 | 4,234,853 | ||||||

|

Loans from China Ever-bright Bank

|

||||||||

|

Monthly interest only payments at 5.84% per annum, due April 7, 2011, secured by the assets of the Company, guaranteed by Mr. Hu Xiaoming, Ms. Ling Yueping, Nanlong Group Co., Ltd. and Zhejiang Mengdeli Electric Co., Ltd.

|

- | 4,537,342 | ||||||

|

Monthly interest only payments at 5.84% per annum, due October 11, 2011, secured by the assets of the Company, guaranteed byMr. Hu Xiaoming, Ms. Ling Yueping, Nanlong Group Co., Ltd. and Zhejiang Mengdeli Electric Co., Ltd.

|

4,641,089 | 4,537,342 | ||||||

|

Monthly interest only payments at 5.10% per annum, due November 1, 2011, secured by the assets of the Company, guaranteed byMr. Hu Xiaoming, Ms. Ling Yueping, Nanlong Group Co., Ltd. and Zhejiang Mengdeli Electric Co., Ltd.

|

- | 3,024,895 | ||||||

|

Monthly interest only payments at 5.10% per annum, due September 30, 2011, secured by the assets of the Company, guaranteed byMr. Hu Xiaoming, Ms. Ling Yueping, Nanlong Group Co., Ltd. and Zhejiang Mengdeli Electric Co., Ltd.

|

3,094,059 | - | ||||||

20

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 14 - SHORT TERM BANK LOANS (CONTINUED)

|

June 30,

2011

(Unaudited)

|

December 31,

2010

|

|||||||

|

Monthly interest only payments at 6.16% per annum, due October 2, 2011, secured by the assets of the Company, guaranteed by Mr. Hu Xiaoming, Ms. Ling Yueping, Nanlong Group Co., Ltd. and Zhejiang Mengdeli Electric Co., Ltd.

|

4,641,089 | - | ||||||

|

Loans from Shanghai Pudong Development Bank

|

||||||||

|

Monthly interest only payments at 6.10% per annum, due December 28, 2011, secured by the property of Mr. Hu Xiaoming and Ms. Ling Yueping, guaranteed by Nanlong Group Co., Ltd. and Mr. Hu Xiaoming

|

3,094,059 | 3,024,895 | ||||||

|

Loans from China Ever-growing Bank

|

||||||||

|

Monthly interest only payments at 5.61% per annum, due April 27, 2011, guaranteed by Zhejiang Shuguang industrial Co., Ltd. and Zhejiang Mengdeli Electric Company.

|

- | 3,024,895 | ||||||

|

Monthly interest only payments at 7.57% per annum, due April 27, 2012, guaranteed by Mr. Hu Xiaoming, Ms. Ling Yueping, Zhejiang Shuguang industrial Co., Ltd. and Zhejiang Mengdeli Electric Company.

|

3,094,059 | - | ||||||

|

Total

|

$ | 29,084,158 | $ | 28,434,012 | ||||

Short term bank loans interest expense for the six month ended June 30, 2011 and 2010 was $870,597, and $749,407, respectively.

As of June 30, 2011, the aggregate amount of short-term loans that are guaranteed by various third parties is $29,084,158,

Of this amount, $15,470,296 is guaranteed by Zhejiang Mengdeli Electric Co., Ltd. whose bank loans of $6,899,752 and bank note of $1,237,624 are guaranteed by the Company, or secured by the Company’s assets; the net book value of plant and equipment pledged as collateral is $4,637,530, and the net book value of land use right pledged as collateral is $6,909,885. Also see Note 19.

Of this amount, $7,425,743 is guaranteed by Zhejiang Kangli Metal Manufacturing Company, whose bank loans of $4,641,089 are guaranteed by the Company. Also see Note 19. $3,094,059 is guaranteed by Lv Qingjiang, the major shareholder of Zhejiang Kangli Metal Manufacturing Company.

Of this amount, $3,867,574 is guaranteed by Zhejiang Shuguang industrial Co., Ltd. whose bank loans of $3,094,059 are also guaranteed by the Company. Also see Note 19. $773,515 is guaranteed by Mr. Yan Guanwei, who is also the major shareholder of Zhejiang Shuguang industrial Co., Ltd.

Of this amount, $15,470,296 is guaranteed by Nanlong Group Co., Ltd. whose bank loans of $3,094,059 are also guaranteed by the Company. Also see Note 19.

This is a common business practice among companies in the region of China where Kandi is located to exchange guarantees for bank debt with no consideration given. It is considered a “favor for favor” business practice and is commonly required by the lending banks as in these cases.

21

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 15 – NOTES PAYABLE

Notes payable are summarized as follows:

|

June 30,

2011

(Unaudited)

|

December 31,

2010

|

|||||||

|

Bank acceptance notes:

|

||||||||

|

Due January 13, 2011

|

$ | - | $ | 1,512,447 | ||||

|

Due March 2, 2011

|

- | 1,209,958 | ||||||

|

Due March 13, 2011

|

- | 1,512,447 | ||||||

|

Due March 16, 2011

|

- | 1,209,958 | ||||||

|

Due April 18, 2011

|

- | 1,134,336 | ||||||

|

Due April 18, 2011

|

- | 930,155 | ||||||

|

Due April 18, 2011

|

- | 960,404 | ||||||

|

Due April 20, 2011

|

- | 1,361,203 | ||||||

|

Due April 26, 2011

|

- | 2,268,671 | ||||||

|

Due May 5, 2011

|

- | 756,224 | ||||||

|

Due May 10, 2011

|

- | 3,024,895 | ||||||

|

Due May 16, 2011

|

- | 3,024,895 | ||||||

|

Due July 17, 2011 (subsequently repaid on its due date)

|

9,282,178 | - | ||||||

|

Due August 23, 2011

|

1,547,030 | - | ||||||

|

Due September 9, 2011

|

3,094,059 | - | ||||||

|

Due September 15, 2011

|

1,547,030 | - | ||||||

|

Due September 21, 2011

|

1,547,030 | - | ||||||

|

Due September 22, 2011

|

1,547,030 | - | ||||||

|

Due September 23, 2011

|

1,237,624 | |||||||

|

Due October 18, 2011

|

3,094,059 | |||||||

|

Due October 20, 2011

|

1,547,030 | |||||||

|

Due October 21, 2011

|

2,320,544 | |||||||

|

Due November 20, 2011

|

3,094,059 | - | ||||||

|

Subtotal

|

$ | 29,857,673 | $ | 18,905,593 | ||||

|

Notes payable to unrelated companies:

|

||||||||

|

Due April 24, 2011 (Interest rate 6.0% per annum)

|

$ | - | $ | 134,305 | ||||

|

Due January 20, 2012 (Interest rate 6.0% per annum)

|

1,000 | 1,000 | ||||||

|

Subtotal

|

1,000 | 135,305 | ||||||

|

Total

|

$ | 29,858,673 | $ | 19,040,898 | ||||

All the bank acceptance notes do not bear interest, but are subject to bank charges of 0.005% of the principal as commission on each transaction.

22

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 15 – NOTES PAYABLE (CONTINUED)

Restricted cash of $23,669,554 is held as collateral for the following notes payable at June 30, 2011:

|

Due July 17, 2011 (subsequently repaid on its due date)

|

9,282,178 | |||

|

Due August 23, 2011

|

1,547,030 | |||

|

Due September 9, 2011

|

3,094,059 | |||

|

Due September 15, 2011

|

1,547,030 | |||

|

Due September 21, 2011

|

1,547,030 | |||

|

Due September 22, 2011

|

1,547,030 | |||

|

Due September 23, 2011

|

1,237,624 | |||

|

Due October 18, 2011

|

3,094,059 | |||

|

Due October 20, 2011

|

1,547,030 | |||

|

Due October 21, 2011

|

2,320,544 | |||

|

Due November 20, 2011

|

3,094,059 | |||

|

Total

|

$ | 29,857,673 |

Through issuing Bank note payable rather than paying cash to suppliers, the Company can defer the payments to the date bank note payable is due. Simultaneously, the Company needs to deposit restricted cash in banks to back up the bank note payable, while the restricted cash deposited in banks at the rate of 3.05% annually for this reporting period will generate interest income.

NOTE 16 – TAX

(a) Corporation Income Tax (“CIT”)

On March 16, 2007, the National People’s Congress of China approved the Corporate Income Tax Law of the People’s Republic of China (the “new CIT law”), which went into effect on January 1, 2008. In accordance with the relevant tax laws and regulations of the PRC, the applicable corporate income tax rate is 25%.

Prior to January 1, 2008, the CIT rate applicable to the Company was 33%. Kandi’s first profitable tax year for income tax purposes as a foreign-invested company was 2007. As a foreign-invested company, the income tax rate of Kandi is entitled to a 50% tax holiday based on 25% for the years from 2009 through 2011. During the transition period, the above tax concession granted to the Company prior to the new CIT law will be grandfathered according to the interpretations of the new CIT law.

KSV and Kandi New Energy are subsidiaries of the Company and their applicable corporate income tax rates are both 25%.

According to the PRC corporation income tax (“CIT”) reporting system, the CIT sales cut-off base is concurrent with the value added tax (“VAT”) which will be reported to the State Administration of Taxation (“SAT”) on a quarterly basis. Since the VAT and CIT are accounted for on a VAT tax basis that recorded all sales on a “State provided official invoices” reporting system, the Company is reporting the CIT according to the SAT prescribed tax reporting rules. Under the VAT tax reporting system, sales cut-off did not take the accrual base but rather on a VAT taxable reporting basis. Therefore, when the company adopted US GAAP on accrual basis, the sales cut-off CIT timing difference which derived from the VAT reporting system will create a temporary sales cut-off timing difference and this difference is reflected in the deferred tax assets or liabilities calculations on the income tax estimation reported in the Form 10-K.

23

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 16 – TAX (CONTINUED)

Effective January 1, 2007, the Company adopted ASC 740, Income Taxes. The interpretation addresses the determination of whether tax benefits claimed or expected to be claimed on a tax return should be recorded in the financial statements.

Under ASC 740, the Company may recognize the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the financial statements from such a position should be measured based on the largest benefit that has a greater than fifty percent likelihood of being realized upon ultimate settlement. ASC 740 also provides guidance on de-recognition, classification, interest and penalties on income taxes, accounting in interim periods and requires increased disclosures. As of June 30, 2011, the Company does not have a liability for unrecognized tax benefits. The Company files income tax returns to the Internal Revenue Services (“IRS”) and states where the Company has operation. The Company is subject to U.S. federal or state income tax examinations by IRS and relevant state tax authorities for years after 2006. During the periods open to examination, the Company has net operating loss carry forwards (“NOLs”) for U.S. federal and state tax purposes that have attributes from closed periods. Since these NOLs may be utilized in future periods, they remain subject to examination. The Company also files certain tax returns in China. As of June 30, 2011 the Company was not aware of any pending income tax examinations by China tax authorities. The Company's policy is to record interest and penalties on uncertain tax provisions as income tax expense. As of June 30, 2011, the Company has no accrued interest or penalties related to uncertain tax positions. The Company has not recorded a provision for U.S federal income tax for the six months ended June 30, 2011 due to the net operating loss carry forward in the United States.

Income tax expense (benefit) for the six months ended June 30, 2011 and 2010 is summarized as follows:

|

For the Six Months Ended

June 30,

|

||||||||

|

(Unaudited)

|

||||||||

|

2011

|

2010

|

|||||||

|

Current:

|

||||||||

|

Provision for CIT

|

$ | 277,505 | $ | 185,673 | ||||

|

Provision for Federal Income Tax

|

- | - | ||||||

|

Deferred:

|

||||||||

|

Provision for CIT

|

0 | (10,617 | ) | |||||

|

Income tax expense (benefit)

|

$ | 277,505 | $ | 175,056 | ||||

24

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 16 – TAX (CONTINUED)

The Company’s income tax expense (benefit) differs from the “expected” tax expense for the six months ended June 30, 2011 and 2010 (computed by applying the CIT rate of 25%, respectively to income before income taxes) as follows:

|

For the Six Months Ended

June 30,

|

||||||||

|

(Unaudited)

|

||||||||

|

2011

|

2010

|

|||||||

|

Computed "expected" (benefit) expense

|

$ | 302,675 | $ | 221,568 | ||||

|

Favorable tax rate

|

(277,505 | ) | (185,673 | ) | ||||

|

Permanent differences

|

165,754 | 58,159 | ||||||

|

Valuation allowance

|

86,581 | 81,002 | ||||||

|

Income tax expense (benefit)

|

$ | 277,505 | $ | 175,056 | ||||

The tax effects of temporary differences that give rise to the Company’s net deferred tax assets and liabilities as of June 30, 2011 and December 31, 2010 are summarized as follows:

|

June 30, 2011

(Unaudited)

|

December 31,

2010

|

|||||||

|

Current portion:

|

||||||||

|

Deferred tax assets:

|

||||||||

|

Expense

|

$ | (19,191 | ) | $ | (10,042 | ) | ||

|

Subtotal

|

(19,191 | ) | (10,042 | ) | ||||

|

Deferred tax liabilities:

|

||||||||

|

Sales cut-off (CIT tax reporting on VAT tax system)

|

(24,481 | ) | (24,041 | ) | ||||

|

Other

|

- | - | ||||||

|

Subtotal

|

(24,481 | ) | (24,041 | ) | ||||

|

Total deferred tax liabilities – current portion

|

(43,672 | ) | (34,083 | ) | ||||

|

Non-current portion:

|

||||||||

|

Deferred tax assets:

|

||||||||

|

Depreciation

|

438,819 | 476,847 | ||||||

|

Loss carried forward

|

86,581 | 3,524,145 | ||||||

|

Valuation allowance

|

(86,581 | ) | (3,524,145 | ) | ||||

|

Subtotal

|

438,819 | 476,847 | ||||||

|

Deferred tax liabilities:

|

||||||||

|

Accumulated other comprehensive gain

|

(220,899 | ) | (220,899 | ) | ||||

|

Subtotal

|

(220,899 | ) | (220,899 | ) | ||||

|

Total deferred tax assets – non-current portion

|

217,920 | 255,948 | ||||||

|

Net deferred tax assets

|

$ | 174,248 | $ | 221,865 | ||||

25

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

(b) Tax Holiday Effect

For the six months ended June 30, 2011 and 2010 the PRC corporate income tax rate was 25%. Certain subsidiaries of the Company are entitled to tax holidays for the six months ended June 30, 2011 and 2010.

The combined effects of the income tax expense exemptions and reductions available to the Company for the six months ended June 30, 2011 and 2010 are as follows:

|

For the Six Months Ended

June 30

(Unaudited)

|

||||||||

|

2011

|

2010

|

|||||||

|

Tax holiday credit

|

$ | 277,505 | $ | 185,673 | ||||

|

Basic net income per share effect

|

$ | 0.01 | $ | 0.01 | ||||

NOTE 17 - STOCK OPTIONS, WARRANTS AND CONVERTIBLE NOTES

(a) Stock Options

On February 11, 2009, the Compensation Committee of the Board of Directors of the Company approved the grant of stock options for 2,600,000 shares of common stock to ten of the Company's employees and directors. The stock options vest ratably over three years and expire in ten years from the grant date. The Company valued the stock options at $2,062,964 and amortizes the stock compensation expense using the straight-line method over the service period from February 11, 2009 through February 11, 2012. The value of the options was estimated using the Black Scholes Model with an expected volatility of 164%, expected life of 10 years, risk-free interest rate of 2.76% and expected dividend yield of 0.00%. On June 30, 2011, one of the Company’s director resigned, and whose 6,668 unexercised options were forfeited.

The following is a summary of the stock option activities of the Company:

|

Activity

|

Weighted Average

Exercise Price

|

|||||||

|

Outstanding as of January 1, 2011

|

1,833,304 | $ | 0.84 | |||||

|

Granted

|

- | - | ||||||

|

Exercised

|

39,999 | 0.80 | ||||||

|

Cancelled

|

6,668 | 0.80 | ||||||

|

Outstanding as of June 30, 2011

|

1,786,637 | 0.84 | ||||||

The following table summarizes information about stock options outstanding as of June 30, 2011:

|

Options Outstanding

|

Options Exercisable

|

|||||||||||||||||

|

Number of

shares

|

Exercise

Price

|

Remaining

Contractual life

(in years)

|

Number of

shares

|

Exercise

Price

|

||||||||||||||

| 1,686,637 | $ | 0.80 | 7.75 | 1,686,637 | $ | 0.80 | ||||||||||||

| 100,000 | 1.50 | 8.25 | 100,000 | 1.50 | ||||||||||||||

26

KANDI TECHNOLOGIES, CORP.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2011 (UNAUDITED)

NOTE 17 - STOCK OPTIONS, WARRANTS AND CONVERTIBLE NOTES (CONTINUED)

The fair value per share of the 2,600,000 options issued to the employees and directors is $0.7934 per share. The fair value per share of the unexercised 100,000 options issued to Wang Rui and Li Qiwen, which became exercisable on June 6, 2010, is $3.44.

(b) Warrants and Convertible Notes