Table of Contents

As filed with the Securities and Exchange Commission on September 4, 2013

Registration No. 333-189821

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

PRE-EFFECTIVE AMENDMENT NO. 2

TO

FORM S-11

FOR REGISTRATION

UNDER

THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

SOTHERLY HOTELS LP

(Exact name of Registrant as specified in its governing instruments)

410 W. Francis Street

Williamsburg, Virginia 23185

(757) 229-5648

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Andrew M. Sims

Chief Executive Officer

Sotherly Hotels Inc.

410 W. Francis Street

Williamsburg, Virginia 23185

(757) 229-5648

(757) 564-8801 (Telecopy)

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| Thomas J. Egan, Jr., Esq. Pamela K. Dayanim, Esq. Baker & McKenzie LLP 815 Connecticut Avenue, NW Washington, DC 20006 (202) 452-7000 |

John A. Good, Esq. Justin R. Salon, Esq. Bass, Berry & Sims PLC 1201 Pennsylvania Avenue, Suite 300 Washington, DC 20004 (202) 827-2957 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the Securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. (See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Securities Exchange Act of 1934).

| Large Accelerated Filer | ¨ | Accelerated Filer | ¨ | |||

| Non-accelerated Filer | x | Smaller reporting company | ¨ |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed or supplemented without notice. We may not sell the securities described in this preliminary prospectus until the registration statement that we have filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and we are not soliciting offers to buy these securities, in any state where the offer or sale of these securities is not permitted.

SUBJECT TO COMPLETION, DATED SEPTEMBER 4, 2013

PROSPECTUS

$

SOTHERLY HOTELS LP

% Senior Unsecured Notes Due 2018

Sotherly Hotels LP, which we refer to in this prospectus as the Issuer or the Operating Partnership, is offering and selling % Senior Unsecured Notes due 2018, or the notes. The notes will be issued in denominations of $25 and integral multiples of $25 in excess thereof, will mature on , 2018 and will bear interest at a fixed rate of % per year. Interest on the notes will be payable quarterly in arrears, beginning , 2013.

The notes will be unsecured obligations of the Issuer and will rank equally with all of the Issuer’s existing and future unsecured indebtedness and senior in right of payment to any of the Issuer’s future obligations that are by their terms expressly subordinated or junior in right of payment to the notes.

We may, at our option, on or after , 2016 redeem some or all of the notes as described in “Description of Notes–Optional Redemption.” We have applied to list the notes on the NASDAQ® Global Market under the symbol “SOHOL.” We expect trading in the notes to begin within 30 days of 2013, the original issue date. We may from time to time purchase the notes in the open market or otherwise.

Investing in the notes involves certain risks. See “Risk Factors” beginning on page 14.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Public Offering Price(1) |

Underwriting Discounts and Commissions(2) |

Proceeds to Issuer(3) |

||||||||

| Per note |

$ | $ | ||||||||

| Total |

$ | $ | ||||||||

| (1) | Plus accrued interest, if any, from . |

| (2) | See “Underwriting” for additional disclosure regarding the underwriting discounts and expenses payable to the underwriters by us. |

| (3) | Before deducting expenses of the offering. |

The underwriters may also purchase up to an additional $ aggregate principal amount of the notes from us at the public offering price per note, less the underwriting discounts and commissions, within 30 days from the date of this prospectus, solely to cover over-allotments, if any.

It is expected that delivery of the notes in book-entry form only will be made through the facilities of The Depository Trust Company on or about against payment therefor in immediately available funds.

We expect to deliver the notes on or about , 2013.

The date of this prospectus is , 2013.

Table of Contents

Table of Contents

| Page | ||||

| 1 | ||||

| 13 | ||||

| 14 | ||||

| 33 | ||||

| MARKET PRICE OF AND DIVIDENDS ON THE REGISTRANT’S COMMON EQUITY |

34 | |||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

40 | |||

| 57 | ||||

| INVESTMENT POLICIES AND POLICIES WITH RESPECT TO CERTAIN ACTIVITIES |

76 | |||

| 80 | ||||

| 84 | ||||

| 88 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

92 | |||

| 95 | ||||

| 109 | ||||

| 113 | ||||

| 128 | ||||

| 129 | ||||

| 131 | ||||

| 131 | ||||

| 131 | ||||

| F-1 | ||||

i

Table of Contents

You should rely only on the information contained in this prospectus. Neither the underwriters nor we have authorized any other person to provide you with different or additional information. If anyone provides you with different, additional or inconsistent information, you should not rely on it. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which such an offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so, or to any person to whom it is unlawful to make such offer or solicitation. Neither the delivery of this prospectus nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in our affairs or that information contained herein is correct as of any time subsequent to the date hereof.

All brand and trade names, logos or trademarks contained or referred to in this prospectus are the property of their respective owners, and their appearance in this prospectus may not in any way be construed as participation by, or endorsement of, this offering by any of our franchisors. For more information, see “Our Principal Agreements — Franchise Agreements.”

We use market data and industry forecasts and projections throughout this prospectus, including data from publicly available information and industry publications. These sources generally state that the information they provide has been obtained from sources believed to be reliable, but that the accuracy and completeness of the information are not guaranteed. The forecasts and projections are based on industry surveys and the preparers' experience in the industry and there can be no assurance that any of the forecasts or projections will be achieved. We believe that the surveys and market research others have performed are reliable, but we have not independently investigated or verified this information.

ii

Table of Contents

This summary highlights the information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before deciding whether to invest in the notes. You should carefully read this entire prospectus, including the information under the heading “Risk Factors” and all information included in this prospectus.

Explanatory Note

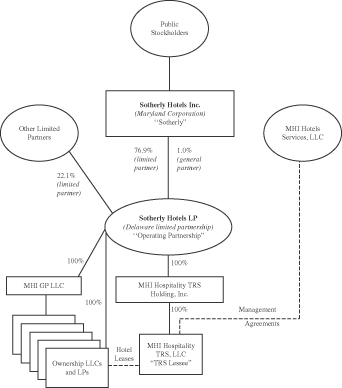

Unless the context otherwise requires or where otherwise indicated, in this prospectus, all references to “Operating Partnership” or the “Issuer” means only Sotherly Hotels LP, formerly MHI Hospitality, L.P., a Delaware limited partnership. All references in this prospectus to “Sotherly” means only Sotherly Hotels Inc., a Maryland corporation and the sole general partner of the Operating Partnership. All references in this prospectus to the “Company,” “we,” “us” and “our” refer to Sotherly Hotels Inc. and its subsidiaries and predecessors, including the Operating Partnership, unless the context otherwise requires or where otherwise indicated.

There are a few differences between Sotherly and the Operating Partnership, which are reflected in the disclosure in this prospectus. We believe it is important to understand the differences between Sotherly and the Operating Partnership in the context of how Sotherly Hotels Inc. and Sotherly Hotels LP operate as an interrelated consolidated company. Sotherly Hotels Inc. is a self-managed and self-administered real estate investment trust, or REIT, whose only material asset is its ownership of partnership interests of Sotherly Hotels LP. As a result, Sotherly Hotels Inc. does not conduct business itself, other than acting as the sole general partner of Sotherly Hotels LP, and issuing public equity from time to time. As general partner with control of Sotherly Hotels LP, Sotherly consolidates Sotherly Hotels LP for financial reporting purposes. Substantially all of the Company’s operations are conducted through Sotherly Hotels LP, and Sotherly Hotels LP holds, directly or indirectly, substantially all the assets of the Company and ownership interests in the Company’s joint venture. Sotherly Hotels LP conducts the operations of the Company’s business and is structured as a limited partnership with no publicly traded equity. Except for net proceeds from public equity issuances by Sotherly Hotels Inc., which are generally contributed by Sotherly to Sotherly Hotels LP in exchange for partnership units, Sotherly Hotels LP generates the capital required by the Company’s business through Sotherly Hotels LP’s operations or by Sotherly Hotels LP’s direct or indirect incurrence of indebtedness.

Company Overview

Sotherly was formed in August 2004 to own, acquire, renovate and reposition full-service, primarily upscale and upper-upscale hotel properties located in the Mid-Atlantic and Southern United States. On December 21, 2004, Sotherly successfully completed its initial public offering and elected to be treated as a self-advised REIT for federal income tax purposes. As of the date of this prospectus, Sotherly owns approximately 78.3% of the partnership units in the Operating Partnership. Limited partners (including certain of Sotherly’s officers and directors) own the remaining Operating Partnership units.

Our portfolio currently consists of ten full-service, primarily upscale and upper-upscale hotels located in seven states with an aggregate of 2,424 rooms and approximately 120,200 square feet of meeting space. Nine of these hotels are wholly-owned by subsidiaries of the Operating Partnership and operate under the Hilton, Crowne Plaza, Sheraton and Holiday Inn brands and are managed on a day-to-day basis by MHI Hotels Services, LLC, or MHI Hotels Services. We also own a 25.0% indirect noncontrolling interest in the 311-room Crowne Plaza Hollywood Beach Resort through a joint venture with The Carlyle Group, or Carlyle. Our portfolio is concentrated in markets that we believe possess multiple demand generators and have significant barriers to entry for new product delivery, which are important factors for us in identifying hotel properties that we expect will be capable of providing strong risk-adjusted returns.

1

Table of Contents

In order for Sotherly to qualify as a REIT, it cannot directly manage or operate our hotels. Therefore, our wholly-owned hotel properties are leased to MHI Hospitality TRS, LLC, or our TRS Lessee, and managed by MHI Hotels Services, an eligible independent management company owned and controlled by certain individuals, including Andrew M. Sims, Sotherly’s chairman and chief executive officer, Kim E. Sims, a current director of Sotherly, Christopher L. Sims, a former director of Sotherly, and William J. Zaiser, Sotherly’s former executive vice president and chief financial officer. Our TRS Lessee is wholly-owned by MHI Hospitality TRS Holding, Inc., or MHI Holding, a taxable REIT subsidiary that is wholly-owned by the Operating Partnership. Our TRS Lessee is disregarded as an entity separate from MHI Holding for U.S. federal income tax purposes. MHI Hotels Services and its predecessors have been in continuous operation since 1957. By using MHI Hotels Services as the management company, we intend to continue to capitalize on its extensive experience to seek above-average operating results. MHI Hotels Services and its predecessors have operated for many years in markets where we have a presence, and its operations are driven primarily by a focused sales, marketing and food and beverage strategy that is critical to the success of a full-service hotel.

The following chart generally depicts our corporate structure as of the date of this prospectus:

Market Opportunity

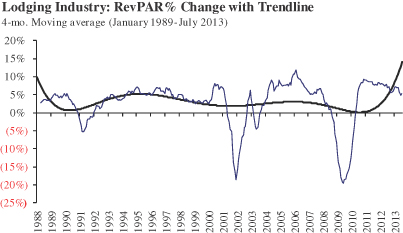

As a result of the global economic recession, commencing in 2008 through early 2010, the U.S. lodging industry experienced substantial declines in operating performance driven by declining U.S. gross domestic product, or GDP, high unemployment levels, low consumer confidence and a reduction in the availability of credit. In addition to facing declining operating results, hotel owners were adversely impacted by a significant decline in the availability of debt financing for working capital, renovations and acquisitions. For the past three years, the lodging industry has experienced a recovery in revenue per available room, or RevPAR, and in financing activity. The breadth and sustainability of the recovery will be dependent on a variety of factors,

2

Table of Contents

including asset location, individual market performance, and property condition. New supply of hotel rooms has not yet emerged as a major factor impacting the recovery, and we believe the supply of new hotels is likely to remain low for the next several years due to the limited availability of debt financing dedicated to new construction projects. As a result, we believe well-located, properly positioned, and well managed hotels will continue to benefit from the ongoing lodging recovery and demand for hotel rooms.

In addition, we believe that a continued recovery in U.S. GDP growth, coupled with limited growth in new hotel room supply, will lead to increases in lodging industry RevPAR and operating profit. In March 2013, PKF Hospitality Research, a leading industry analytic expert, reported that lodging fundamentals are currently as sound as they have been in the past 30 years, and that hotel rates and RevPAR gains should be double the historic averages through 2015.

Competitive Strengths

We believe the following factors differentiate us from other owners, acquirers and investors in hotel properties:

| • | Stable Portfolio of High Quality Properties. Our properties consist of well-located, geographically diverse, full-service hotels predominantly in the central business districts of cities in the Mid-Atlantic and Southeastern United States. Our hotels typically offer attractive amenities such as swimming pools, fitness centers, food and beverage facilities, parking and meeting space. Since Sotherly’s initial public offering, each of our hotels has undergone a substantial renovation program to enhance the quality and performance of the property. |

| • | Longtime Relationships with Leading Full-Service Hotel Brands. Our senior management team has developed strong relationships with many of the top full-service hotels brands in the upscale to upper-upscale categories, which is characterized by such brands as Hilton, Crowne Plaza, and Sheraton, and has received numerous awards from nationally recognized hotel franchisors, such as Intercontinental Hotels Group, Starwood Hotels and Hilton Hotels. |

| • | Existing Portfolio Repositioned, Relicensed and Renovated. From 2007 through 2009, we expended approximately $76.7 million in capital improvements resulting in the substantial renovation and licensing (or re-licensing) of five of our nine wholly-owned properties. For the six months ended June 30, 2013 and for the years ended December 31, 2012, 2011, and 2010, we have expended approximately $3.2 million, $2.9 million, $6.0 million and $2.9 million, respectively, for a total of approximately $14.9 million in capital improvements, which included substantial renovation of our property in Raleigh, North Carolina, which we re-branded as the DoubleTree by Hilton Raleigh Brownstone — University, and the first phase of renovation of the guest rooms at the Hilton Philadelphia Airport in Philadelphia, Pennsylvania and the Crowne Plaza Jacksonville Riverfront in Jacksonville, Florida. We believe this substantial level of capital investment and our upbranding efforts have positioned our properties to capture revenue opportunities in their respective markets and outperform our competitors as these locations mature. |

| • | Strategic Focus on Select Southern Markets. We are focusing our growth strategy on the major markets in the Southern United States, which we believe have and will continue to benefit from attractive demographic and economic growth characteristics. We believe this region also reflects an attractive business climate with respect to governmental and regulatory policies and taxation. In addition, our hotels are located predominantly in central business district markets near stable demand generators, such as large state universities, convention centers, corporate headquarters, sports venues and office parks and in markets that we believe have significant barriers to entry for new product delivery. |

| • | Prudent and Flexible Capital Structure. During the last three years, we have refinanced over 60% of the debt on our wholly-owned hotel properties, taking advantage of the current attractive interest rate |

3

Table of Contents

| environment. As of June 30, 2013, we had approximately $134.9 million of secured debt, of which approximately $85.8 million, or 63.6%, was fixed, at an average rate of 5.0% (exclusive of Sotherly’s 12.0% Series A Cumulative Redeemable Preferred Stock, or the Preferred Stock). Approximately $49.1 million, or 36.4%, of our secured debt is at a variable interest rate, which bore an average interest rate of 3.6% at June 30, 2013. |

| • | Experienced Management Team. We believe the Company’s and its predecessor’s longevity in the industry and its success through many market cycles, together with management’s experience in the lodging industry, is indicative of the Company’s conservative and disciplined approach toward hotel acquisition, ownership and operation. The members of our senior management team, led by Messrs. Sims, Folsom and Domalski, have significant experience in the lodging, capital markets, finance, and accounting industries, and have worked together at Sotherly since 2006. Mr. Sims, Sotherly’s chairman and chief executive officer, has spent his entire career with Sotherly and its predecessor, and has over 35 years of experience in the lodging industry as an operator, owner, developer, and financier. Mr. Folsom has nearly eight years of experience with Sotherly and 13 years of experience working in public real estate companies and in the real estate capital markets. Mr. Domalski has nearly 29 years of experience as an accountant and auditor and has worked at Sotherly since 2005. |

Our Strategy

Our strategy is to grow through acquisitions of full-service, upscale and upper-upscale hotel properties located in the primary markets of the Southern United States. We intend to grow our portfolio through disciplined acquisitions of hotel properties and believe that we will be able to source significant external growth opportunities through our management team’s extensive network of industry, corporate and institutional relationships.

Our core strategy for our portfolio is intended to create value by acquiring performing hotel properties at significant discounts to replacement cost, as well as acquiring underperforming hotels and subsequently renovating, rehabilitating, repositioning, and up-branding these assets. Once these assets have benefited from this “turnaround” strategy, they become part of our core portfolio. We believe we can optimize performance within the portfolio by superior management practices and by timely and recurring capital expenditures to maintain and enhance the physical property.

4

Table of Contents

Our Properties

As of the date of this prospectus, our portfolio consisted of the following 10 hotel properties:

| Wholly-Owned Properties |

Number of Rooms |

Location | Date of Acquisition |

Years Built / Renovated (1) |

Chain Designation | |||||||

| Hilton Philadelphia Airport |

331 | Philadelphia, PA | December 21, 2004 | 1972/2005/2013 | Upper Upscale | |||||||

| Hilton Wilmington Riverside |

272 | Wilmington, NC | December 21, 2004 | 1970/2007 | Upper Upscale | |||||||

| Hilton Savannah DeSoto |

246 | Savannah, GA | December 21, 2004 | 1968/2008 | Upper Upscale | |||||||

| Sheraton Louisville Riverside |

180 | Jeffersonville, IN | September 20, 2006 | 1972/2008 | Upper Upscale | |||||||

| Crowne Plaza Jacksonville Riverfront |

292 | Jacksonville, FL | July 22, 2005 | 1970/2006/2013 | Upscale | |||||||

| Crowne Plaza Tampa Westshore |

222 | Tampa, FL | October 29, 2007 | 1973/2008 | Upscale | |||||||

| Crowne Plaza Hampton Marina |

173 | Hampton, VA | April 24, 2008 | 1988/2008 | Upscale | |||||||

| Holiday Inn Laurel West |

207 | Laurel, MD | December 21, 2004 | 1985/2005 | Upper MidScale | |||||||

| DoubleTree by Hilton Brownstone-University |

190 | Raleigh, NC | December 21, 2004 | 1971/2002/2011 | Upscale | |||||||

|

|

|

|||||||||||

| Total Rooms in Our Wholly-Owned Portfolio |

2,113 | |||||||||||

| Joint Venture Property |

||||||||||||

| Crowne Plaza Hollywood Beach Resort (2) |

311 | Hollywood, FL | August 9, 2007 | 1972/2006 | Upscale | |||||||

|

|

|

|||||||||||

| Total Rooms in Our Portfolio |

2,424 | |||||||||||

|

|

|

|||||||||||

| (1) | Year Renovated represents the year in which the replacement of a significant portion of the hotel’s furniture, fixtures or equipment was completed. |

| (2) | We own this hotel through a joint venture in which we have a 25% interest. |

The following table illustrates certain key operating metrics for the twelve months ended June 30, 2013 for our portfolio.

| Wholly-Owned Properties |

Average Occupancy(1) |

ADR(2) | RevPAR(3) | |||||||||

| Hilton Philadelphia Airport |

78.6 | % | $ | 135.53 | $ | 106.48 | ||||||

| Hilton Wilmington Riverside |

73.4 | % | $ | 133.25 | $ | 97.77 | ||||||

| Hilton Savannah DeSoto |

71.7 | % | $ | 136.21 | $ | 97.61 | ||||||

| Sheraton Louisville Riverside |

64.3 | % | $ | 130.06 | $ | 83.59 | ||||||

| Crowne Plaza Jacksonville Riverfront |

58.6 | % | $ | 97.54 | $ | 57.19 | ||||||

| Crowne Plaza Tampa Westshore |

67.8 | % | $ | 102.13 | $ | 69.24 | ||||||

| Crowne Plaza Hampton Marina |

53.3 | % | $ | 92.93 | $ | 49.55 | ||||||

| Holiday Inn Laurel West |

66.7 | % | $ | 88.89 | $ | 59.29 | ||||||

| DoubleTree by Hilton Brownstone-University |

71.1 | % | $ | 109.14 | $ | 77.57 | ||||||

| Totals/ Weighted Averages in Our Wholly-Owned Portfolio |

68.1 | % | $ | 117.16 | $ | 79.77 | ||||||

| Joint Venture Property |

||||||||||||

| Crowne Plaza Hollywood Beach Resort(4) |

80.7 | % | $ | 156.21 | $ | 126.10 | ||||||

| Totals/ Weighted Averages in Our Portfolio |

68.5 | % | $ | 118.79 | $ | 81.42 | ||||||

5

Table of Contents

| (1) | Average Occupancy represents the percentage of available rooms that were sold during a specified period of time and is calculated by dividing the number of rooms sold by the total number of rooms available, expressed as a percentage. |

| (2) | Average Daily Rate, or ADR, represents the average rate paid for rooms sold, calculated by dividing total daily room revenue (i.e., excluding food and beverage revenues or other hotel operations revenues such as telephone, parking and other guest services) by total daily rooms sold. |

| (3) | RevPAR is the product of ADR and average daily occupancy. RevPAR does not include food and beverage revenues or other hotel operations revenues such as telephone, parking and other guest services. |

| (4) | We own this hotel through a joint venture in which we have a 25% interest. |

The selected operating data presented above should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus.

Our Partnership Information

The Issuer is a Delaware limited partnership formed in August 2004. The Issuer changed its name from MHI Hospitality, L.P. to Sotherly Hotels LP effective August 2, 2013. Our principal executive offices are located at 410 W. Francis Street, Williamsburg, VA 23185. Our telephone number is (757) 229-5648. Our website is http://www.sotherlyhotels.com. The information contained on, or that may be accessed through, our website is not part of, and is not incorporated into, this prospectus.

Employees

We currently employ eight full-time persons. All persons employed in the day-to-day operations of the hotels are employees of MHI Hotels Services, the management company engaged by our TRS Lessee to operate such hotels.

6

Table of Contents

The Offering

The following summary contains basic information about the notes and the offering and is not intended to be complete. It does not contain all the information that is important to you. For a more complete understanding of the notes, you should read the section of this prospectus entitled “Description of Notes.”

| Issuer |

Sotherly Hotels LP |

| Securities Offered |

$ million aggregate principal amount of the notes (or $ million if the underwriters’ overallotment option is exercised in full). |

| Maturity Date |

, 2018. |

| Interest Rate |

% per annum, computed on the basis of a 360-day year of twelve 30-day months, from . |

| Interest Payment Dates |

, , , and of each year, commencing , 2013. |

| Price to Public |

% of the principal amount, plus accrued interest, if any, from . |

| Ranking |

The notes will be senior unsecured indebtedness of Sotherly Hotels LP, will rank equally with our other senior unsecured indebtedness and will be effectively subordinated to our secured indebtedness and structurally subordinated to all indebtedness of our subsidiaries. As of June 30, 2013, we had consolidated indebtedness of approximately $151.0 million, which is comprised of approximately $134.9 million of secured debt and approximately $16.1 million of unsecured debt. Of the approximately $151.0 million consolidated indebtedness outstanding at June 30, 2013, approximately $138.5 million was held by our subsidiaries and approximately $12.5 million relates to 12,458 shares of Preferred Stock, including 2,460 shares that were redeemed on August 2, 2013 for an aggregate redemption price of approximately $2.7 million and the remainder of which we intend to redeem with a portion of the net proceeds of this offering. |

| Use of Proceeds |

We estimate that the net proceeds from the offering of the notes pursuant to this prospectus, after deducting the underwriting discount and estimated offering costs and expenses payable by us, will be approximately $ (or $ if the over-allotment option is exercised in full). We intend to use a portion of the net proceeds from this offering to redeem 100% of the outstanding shares of the Preferred Stock plus any accrued but unpaid dividends and any make-whole amounts or premium then due and payable on such Preferred Stock, which we estimate to be approximately $11.0 million. We intend to use the remaining net proceeds from the offering of the notes for general corporate purposes. See “Use of Proceeds” in this prospectus. |

| Optional Redemption |

We may, at our option, redeem the notes in whole or in part at any time, or from time to time, on or after , 2016 at a |

7

Table of Contents

| redemption price equal to % of the principal amount of the notes to be redeemed plus accrued and unpaid interest thereon to the date of redemption as described in “Description of Notes — Optional Redemption” in this prospectus. The notes will not be entitled to the benefit of any sinking fund. The notes will not be subject to repayment at the option of the holder at any time prior to maturity, except in connection with a Change of Control Repurchase Event as defined under “Description of Notes — Certain Covenants — Offer to Repurchase Upon a Change of Control Repurchase Event” in this prospectus. |

| Change of Control Offer to Purchase |

If a Change of Control Repurchase Event as defined under “Description of Notes — Certain Covenants — Offer to Repurchase Upon a Change of Control Repurchase Event” occurs, we must offer to repurchase the notes at a repurchase price equal to % of the aggregate principal amount plus any accrued and unpaid interest to, but not including, the repurchase date. |

| Default |

The notes will contain events of default, the occurrence of which may result in the acceleration of our obligations under the notes in certain circumstances. See “Description of Notes — Events of Default; Modification and Waiver” in this prospectus. |

| Certain Covenants |

We will issue the notes under an indenture, which is referred to as the Indenture, to be dated as of the issuance date between us and Wilmington Trust, National Association, as the trustee. The Indenture contains covenants that limit our ability to incur, or permit our subsidiaries to incur, third-party indebtedness if certain debt to asset value and/or interest coverage ratios would be exceeded. These covenants are subject to a number of important exceptions, qualifications, limitations and specialized definitions. See “Description of Notes — Certain Covenants” in this prospectus. |

| Form |

The notes will be evidenced by global notes deposited with the trustee for the notes, as custodian for The Depository Trust Company, or DTC. Beneficial interests in the global notes will be shown on, and transfers of those beneficial interests can only be made through, records maintained by DTC and its participants. See “Description of Notes — Book-entry, Delivery and Form” in this prospectus. |

| Denominations |

We will issue the notes only in denominations of $25 and integral multiples of $25 in excess thereof. |

| Payment of Principal and Interest |

Principal and interest on the notes will be payable in U.S. dollars or other legal tender, coin or currency of the United States of America. |

| Future Issuances |

We may, from time to time, without notice to or consent of the holders, increase the aggregate principal amount of the notes outstanding by issuing additional notes in the future with the same terms as the notes, except for the issue date and offering price, and such additional notes shall be consolidated with the notes issued in this offering and form a single series. |

8

Table of Contents

| Listing |

We have applied to list the notes on the NASDAQ® Global Market under the symbol “SOHOL.” If the listing is approved, trading of the notes on the NASDAQ® Global Market is expected to commence within a 30-day period after the initial delivery of the notes. Currently, there is no public market for the notes. |

| Trustee, Registrar and Paying Agent |

Wilmington Trust, National Association. |

| Governing Law |

The Indenture and the notes will be governed by the laws of the State of New York. The Indenture will be subject to the provisions of the Trust Indenture Act of 1939, as amended. |

| Material Tax Considerations |

You should consult your tax advisors concerning the U.S. federal income tax consequences of owning the notes in light of your own specific situation, as well as consequences arising under the laws of any other taxing jurisdiction. See “Material U.S. Federal Income Tax Considerations.” |

| Risk Factors |

An investment in the notes involves certain risks. You should carefully consider the risks described under “Risk Factors” beginning on page 14 of this prospectus before making an investment decision. |

9

Table of Contents

Summary Financial Information

The following table sets forth, on an historical basis, certain summary consolidated financial and operating data for Sotherly Hotels LP and its subsidiaries. The financial results for the Crowne Plaza Hollywood Beach Resort, in which we have a 25.0% indirect interest, are not consolidated as we account for our investment under the equity method of accounting. You should read the following summary historical financial and operating data in conjunction with the consolidated historical financial statements and notes thereto of Sotherly Hotels LP and its subsidiaries and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” included in this prospectus.

| Year Ended December 31, 2012 |

Year Ended December 31, 2011 |

Year Ended December 31, 2010 |

Year Ended December 31, 2009 |

Year Ended December 31, 2008 |

||||||||||||||||

| Statement of Operations |

||||||||||||||||||||

| Total Revenues |

$ | 87,343,220 | $ | 81,172,504 | $ | 77,382,344 | $ | 71,518,726 | $ | 70,762,732 | ||||||||||

| Total Operating Expenses excluding Depreciation and Amortization |

(68,376,569 | ) | (65,807,786 | ) | (62,451,362 | ) | (59,224,407 | ) | (58,810,002 | ) | ||||||||||

| Depreciation and Amortization |

(8,661,769 | ) | (8,702,880 | ) | (8,506,802 | ) | (8,420,085 | ) | (6,346,222 | ) | ||||||||||

| Net Operating Income |

10,304,882 | 6,661,838 | 6,424,180 | 3,874,234 | 5,606,509 | |||||||||||||||

| Interest Income |

16,158 | 14,808 | 22,305 | 41,999 | 72,547 | |||||||||||||||

| Interest Expense |

(12,382,146 | ) | (10,821,815 | ) | (10,030,517 | ) | (9,661,871 | ) | (6,811,460 | ) | ||||||||||

| Other Income (Expense) — Net |

(1,965,376 | ) | (1,424,620 | ) | 546,115 | 927,924 | (1,263,304 | ) | ||||||||||||

| Income Tax Benefit (Provision) |

(1,301,229 | ) | (905,455 | ) | (214,344 | ) | 1,807,126 | 1,475,695 | ||||||||||||

| Net Loss |

(5,327,711 | ) | (6,475,243 | ) | (3,252,261 | ) | (3,010,587 | ) | (920,014 | ) | ||||||||||

| Statement of Cash Flows |

||||||||||||||||||||

| Cash from Operations — net |

$ | 9,011,957 | $ | 7,550,142 | $ | 4,728,270 | $ | 3,182,605 | $ | 7,214,566 | ||||||||||

| Cash used in Investing — net |

(3,156,121 | ) | (6,130,273 | ) | (3,469,608 | ) | (11,007,214 | ) | (51,931,701 | ) | ||||||||||

| Cash from (used in) Financing — net |

(3,090,079 | ) | (2,798 | ) | (1,756,261 | ) | 9,595,949 | 42,447,582 | ||||||||||||

| Net Increase (Decrease) in Cash and Cash Equivalents |

$ | 2,765,757 | $ | 1,417,071 | $ | (497,599 | ) | $ | 1,771,340 | $ | (2,269,553 | ) | ||||||||

| Balance Sheet (1) |

||||||||||||||||||||

| Investments in Hotel Properties — net |

$ | 176,427,904 | $ | 181,469,432 | $ | 183,898,660 | $ | 188,587,507 | $ | 154,295,611 | ||||||||||

| Properties Under Development |

— | — | — | — | 33,101,773 | |||||||||||||||

| Total Assets |

204,030,869 | 209,299,446 | 209,583,431 | 213,959,755 | 211,218,434 | |||||||||||||||

| Line of Credit |

— | 25,537,290 | 75,197,858 | 75,522,858 | 73,187,858 | |||||||||||||||

| Mortgage Loans |

135,674,432 | 94,157,825 | 72,192,253 | 72,738,250 | 72,256,168 | |||||||||||||||

| Series A Preferred Interest |

14,227,650 | 25,353,698 | — | — | — | |||||||||||||||

| Total Liabilities |

166,698,739 | 165,416,203 | 158,775,128 | 160,118,529 | 157,442,238 | |||||||||||||||

| Partners’ Capital |

37,332,130 | 43,883,243 | 50,808,303 | 53,841,226 | 53,776,196 | |||||||||||||||

| Operating Data |

||||||||||||||||||||

| Average Number of Available Rooms |

2,113 | 2,111 | 2,110 | 2,071 | 1,775 | |||||||||||||||

| Total Number of Available Room Nights |

773,358 | 770,334 | 770,150 | 755,942 | 649,499 | |||||||||||||||

| Occupancy Percentage(2) |

68.9 | % | 66.2 | % | 66.0 | % | 60.4 | % | 62.0 | % | ||||||||||

| Average Daily Rate (ADR)(3) |

$ | 114.22 | $ | 110.24 | $ | 104.42 | $ | 107.21 | $ | 119.50 | ||||||||||

| RevPAR |

$ | 78.65 | $ | 72.94 | $ | 68.93 | $ | 64.74 | $ | 74.04 | ||||||||||

| Additional Financial Data |

||||||||||||||||||||

|

FFO(5) |

$ | 3,924,733 | $ | 2,923,539 | $ | 5,971,900 | $ | 5,997,948 | $ | 6,292,400 | ||||||||||

| Adjusted FFO(5) |

9,470,684 | 5,577,805 | 5,315,321 | 2,848,314 | 4,881,390 | |||||||||||||||

| Hotel EBITDA(6) |

22,439,770 | 18,708,019 | 17,639,548 | 14,771,907 | 14,224,058 | |||||||||||||||

| (1) | As of the period end. |

| (2) | Occupancy Percentage is calculated by dividing the total daily number of rooms sold by the total daily number of rooms available, expressed as a percentage. |

| (3) | ADR is calculated by dividing the total daily room revenue (i.e., excluding food and beverage revenues or other hotel operations revenues such as telephone, parking and other guest services) by the total daily number of rooms sold. |

10

Table of Contents

| (4) | RevPAR is the product of ADR and occupancy, and does not include food and beverage revenues or other hotel operations revenues such as telephone, parking and other guest services. |

| (5) | Industry analysts and investors use Funds from Operations, or FFO, as a supplemental operating performance measure of an equity REIT. FFO is calculated in accordance with the definition adopted by the Board of Governors of the National Association of Real Estate Investment Trusts, or NAREIT. FFO, as defined by NAREIT, represents net income or loss determined in accordance with U.S. generally accepted accounting principles, or GAAP, excluding extraordinary items as defined under GAAP and gains or losses from sales of previously depreciated operating real estate assets, plus certain non-cash items such as real estate asset depreciation and amortization, and after adjustment for any noncontrolling interest from unconsolidated partnerships and joint ventures. |

Adjusted FFO accounts for certain additional items that are not in NAREIT’s definition of FFO, including any unrealized gain (loss) on hedging instruments or warrant derivative, loan impairment losses, losses on early extinguishment of debt, aborted offering costs, costs associated with the departure of executive officers and acquisition transaction costs.

The following is a reconciliation of net loss to FFO and Adjusted FFO for the years ended December 31, 2012, 2011, 2010, 2009 and 2008:

| Year Ended December 31, 2012 |

Year Ended December 31, 2011 |

Year Ended December 31, 2010 |

Year Ended December 31, 2009 |

Year Ended December 31, 2008 |

||||||||||||||||

| Net Loss |

$ | (5,327,711 | ) | $ | (6,475,243 | ) | $ | (3,252,261 | ) | $ | (3,010,587 | ) | $ | (920,014 | ) | |||||

| Depreciation and amortization |

8,661,769 | 8,702,880 | 8,506,802 | 8,420,085 | 6,346,222 | |||||||||||||||

| Equity in depreciation and amortization of joint venture |

590,675 | 567,803 | 546,055 | 545,580 | 545,659 | |||||||||||||||

| (Gain)/loss on disposal of assets |

— | 128,099 | 171,304 | 42,870 | 320,533 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| FFO |

$ | 3,924,733 | $ | 2,923,539 | $ | 5,971,900 | $ | 5,997,948 | $ | 6,292,400 | ||||||||||

| Unrealized (gain)/loss on hedging activities(A) |

13,752 | 77,152 | (830,614 | ) | (1,220,161 | ) | 691,268 | |||||||||||||

| Unrealized (gain)/loss on warrant derivative |

2,026,677 | 1,309,075 | — | — | — | |||||||||||||||

| (Increase)/decrease in deferred income taxes |

1,412,467 | 685,189 | 174,035 | (1,929,473 | ) | (1,652,278 | ) | |||||||||||||

| Impairment of note receivable |

110,871 | — | — | — | 300,000 | |||||||||||||||

| Aborted offering costs |

— | 582,850 | — | — | — | |||||||||||||||

| Equity in gain on extinguishment of debt of joint venture |

— | — | — | — | (750,000 | ) | ||||||||||||||

| Loss on early extinguishment of debt(B) |

1,982,184 | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted FFO |

$ | 9,470,684 | $ | 5,577,805 | $ | 5,315,321 | $ | 2,848,314 | $ | 4,881,390 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (A) | Includes equity in unrealized loss on hedging activities of joint venture. |

| (B) | Reflected in interest expense for the periods presented above. |

11

Table of Contents

| (6) | Hotel EBITDA represents the portion of net operating income before depreciation and amortization and corporate general and administrative expenses that relate to our nine wholly-owned properties. |

The following is a reconciliation of net loss to hotel EBITDA for the years ended December 31, 2012, 2011, 2010, 2009 and 2008:

| Year Ended December 31, 2012 |

Year Ended December 31, 2011 |

Year Ended December 31, 2010 |

Year Ended December 31, 2009 |

Year Ended December 31, 2008 |

||||||||||||||||

| Net Loss |

$ | (5,327,711 | ) | $ | (6,475,243 | ) | $ | (3,252,261 | ) | $ | (3,010,587 | ) | $ | (920,014 | ) | |||||

| Interest expense |

12,382,146 | 10,821,815 | 10,030,517 | 9,661,871 | 6,811,460 | |||||||||||||||

| Interest income |

(16,158 | ) | (14,808 | ) | (22,305 | ) | (41,999 | ) | (72,547 | ) | ||||||||||

| Income tax provision (benefit) |

1,301,229 | 905,455 | 214,344 | (1,807,126 | ) | (1,475,695 | ) | |||||||||||||

| Depreciation and amortization |

8,661,769 | 8,702,880 | 8,506,802 | 8,420,085 | 6,346,222 | |||||||||||||||

| Equity in (earnings)/loss of joint venture |

(172,172 | ) | 60,094 | (16,931 | ) | 249,367 | (48,496 | ) | ||||||||||||

| (Gain)/loss on disposal of assets |

— | 128,099 | 171,304 | 42,870 | 320,533 | |||||||||||||||

| Unrealized (gain)/loss on hedging activities |

— | (72,649 | ) | (700,488 | ) | (1,220,161 | ) | 691,268 | ||||||||||||

| Unrealized (gain)/loss on warrant derivative |

2,026,677 | 1,309,075 | — | — | — | |||||||||||||||

| Impairment of note receivable |

110,871 | — | — | — | 300,000 | |||||||||||||||

| Corporate general and administrative |

4,078,826 | 4,025,794 | 3,389,764 | 3,170,627 | 2,940,979 | |||||||||||||||

| Net lease rental income |

(350,000 | ) | (447,000 | ) | (443,000 | ) | (445,000 | ) | (471,862 | ) | ||||||||||

| Other fee income |

(255,707 | ) | (235,493 | ) | (238,198 | ) | (248,040 | ) | (197,790 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Hotel EBITDA |

$ | 22,439,770 | $ | 18,708,019 | $ | 17,639,548 | $ | 14,771,907 | $ | 14,224,058 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

The following table sets forth the operating data on a weighted average basis for the Operating Partnership, inclusive of its 25.0% indirect interest in the Crowne Plaza Hollywood Beach Resort:

| Year Ended December 31, 2012 |

Year Ended December 31, 2011 |

Year Ended December 31, 2010 |

Year Ended December 31, 2009 |

Year Ended December 31, 2008 |

||||||||||||||||

| Operating Data |

||||||||||||||||||||

| Weighted Average Number of Available Rooms |

2,197 | 2,188 | 2,188 | 2,149 | 1,857 | |||||||||||||||

| Pro-rata Total of Available Room Nights |

801,815 | 798,713 | 798,529 | 784,321 | 677,956 | |||||||||||||||

| Occupancy Percentage(1) |

69.2 | % | 66.6 | % | 66.5 | % | 60.8 | % | 61.8 | % | ||||||||||

| Average Daily Rate (ADR)(2) |

$ | 115.56 | $ | 111.22 | $ | 105.12 | $ | 107.79 | $ | 120.78 | ||||||||||

| RevPAR(3) |

$ | 80.00 | $ | 74.11 | $ | 69.92 | $ | 65.49 | $ | 74.69 | ||||||||||

| (1) | Occupancy Percentage is calculated by dividing the total daily number of rooms sold by the total daily number of rooms available, expressed as a percentage. |

| (2) | ADR is calculated by dividing the total daily room revenue (i.e., excluding food and beverage revenues or other hotel operations revenues such as telephone, parking and other guest services) by the total daily number of rooms sold. |

| (3) | RevPAR is the product of ADR and occupancy, and does not include food and beverage revenues or other hotel operations revenues such as telephone, parking and other guest services. |

12

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

We make forward-looking statements in this prospectus. The forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements.

Forward-looking statements, which are based on certain assumptions and describe our current strategies, expectations and future plans, are generally identified by our use of words, such as “intend,” “plan,” “may,” “should,” “will,” “project,” “estimate,” “anticipate,” “believe,” “expect,” “continue,” “potential,” “opportunity,” and similar expressions, whether in the negative or affirmative, but the absence of these words does not necessarily mean that a statement is not forward-looking. The factors listed under “Risk Factors” in this prospectus, as well as any cautionary language in this prospectus, provide examples of risks, uncertainties and events that may cause our actual results to differ materially from the expectations we describe in our forward-looking statements. Such risks and uncertainties include, among other things, risks and uncertainties related to:

| • | national and local economic and business conditions that affect occupancy rates and revenues at our hotels and the demand for hotel products and services; |

| • | risks associated with the hotel industry, including competition, increases in wages and other labor costs, energy costs and other operating costs; |

| • | the magnitude and sustainability of the economic recovery in the hospitality industry and in the markets in which we operate; |

| • | the availability and terms of financing and capital and the general volatility of the securities markets; |

| • | risks associated with the level of our indebtedness and our ability to meet covenants in our debt agreements and, if necessary, to refinance or seek an extension of the maturity of such indebtedness or modify such debt agreements; |

| • | management and performance of our hotels; |

| • | risks associated with redevelopment and repositioning projects, including delays and cost overruns; |

| • | supply and demand for hotel rooms in our current and proposed market areas; |

| • | our ability to maintain adequate insurance coverage; and |

| • | other factors, including those discussed in “Risk Factors” in this prospectus. |

These risks and uncertainties should be considered in evaluating any forward-looking statement contained in this prospectus. All forward-looking statements speak only as of the date of this prospectus. All subsequent written and oral forward-looking statements attributable to us or any person acting on our behalf are qualified by the cautionary statements in this section. We undertake no obligation to update or publicly release any revisions to forward-looking statements to reflect events, circumstances or changes in expectations after the date of this prospectus, except as required by law. In addition, our past results are not necessarily indicative of our future results.

13

Table of Contents

An investment in the notes involves various risks. The following are the material risks that apply to an investment in the notes. You should carefully consider the risks described below, together with the other information included in this prospectus before making a decision to invest in the notes. Any of the following risks could materially adversely affect our business, operations, industry or financial position or our future financial performance.

Risks Related to the Offering

The notes are unsecured obligations of the Operating Partnership and not obligations of Sotherly or our subsidiaries and will be subordinated to any of the Operating Partnership’s future secured indebtedness to the extent of the value of the assets securing such indebtedness and effectively subordinated to any future obligations of the Operating Partnership’s subsidiaries. Structural subordination increases the risk that we will be unable to meet our obligations on the notes when they mature.

The notes will be unsecured unsubordinated obligations of the Operating Partnership and will rank equally in right of payment with all of the Operating Partnership’s other unsecured indebtedness and senior in right of payment to any of the Operating Partnership’s future obligations that are by their terms expressly subordinated or junior in right of payment to the notes. The notes will be effectively subordinated to any of the Operating Partnership’s existing or future secured indebtedness to the extent of the value of the assets securing such indebtedness. At June 30, 2013, we had consolidated debt of approximately $151.0 million, which is comprised of approximately $134.9 million of secured debt and approximately $16.1 million of unsecured debt.

The notes are obligations exclusively of the Operating Partnership and not of any of its subsidiaries. None of the Operating Partnership’s subsidiaries is a guarantor of the notes and the notes are not required to be guaranteed by any subsidiaries we, the Operating Partnership, may acquire or create in the future. The notes are also effectively subordinated to all of the liabilities of the Operating Partnership’s subsidiaries, to the extent of their assets, since they are separate and distinct legal entities with no obligation to pay any amounts due under the Issuer’s indebtedness, including the notes, or to make any funds available to make payments on the notes, whether by paying dividends or otherwise. The Operating Partnership’s right to receive any assets of any subsidiary in the event of a bankruptcy or liquidation of the subsidiary, and therefore the right of the Operating Partnership’s creditors to participate in those assets, will be effectively subordinated to the claims of that subsidiary’s creditors, including trade creditors, in each case to the extent that the Operating Partnership is not recognized as a creditor of such subsidiary. In addition, even where the Operating Partnership is recognized as a creditor of a subsidiary, the Operating Partnership’s rights as a creditor with respect to certain amounts are subordinated to other indebtedness of that subsidiary, including secured indebtedness to the extent of the assets securing such indebtedness. As of June 30, 2013, 100% of our consolidated secured indebtedness, or $134.9 million, was in the form of mortgages secured by properties owned by subsidiaries of the Operating Partnership, and none of our properties were unencumbered as of June 30, 2013.

The notes restrict, but do not eliminate, the Operating Partnership’s ability to incur additional debt or take other action that could negatively impact holders of the notes.

Subject to specified limitations in the Indenture and as described under “Description of Notes—Certain Covenants,” the Indenture does not contain any provisions that would limit the Operating Partnership’s ability or the ability of its subsidiaries to incur indebtedness, including indebtedness that would be senior to the notes.

There are limited covenants in the Indenture.

The Indenture does not:

| • | prevent our subsidiaries from incurring indebtedness which would effectively rank senior to the notes; |

14

Table of Contents

| • | prevent us from incurring secured indebtedness that would rank senior to the notes to the extent of the value of the assets securing the indebtedness; or |

| • | prevent us from incurring unsecured indebtedness that is equal or subordinate in right of payment to the notes. |

For these reasons, you should not consider the covenants in the Indenture as a significant factor in evaluating whether to invest in the notes.

An increase in the level of our outstanding indebtedness, or other events, could have an adverse impact on our business, properties, capital structure, financial condition, results of operations or prospects, which could adversely impact the trading prices for, or the liquidity of, the notes. Any such event could also adversely affect our cost of borrowing, limit our access to the capital markets or result in more restrictive covenants in future debt agreements.

Certain financial covenants in the Indenture rely on definitions that use non-GAAP measures and/or are subject to management’s good faith discretion, which could make it difficult for holders of our notes to determine independently whether we are in compliance with certain financial covenants relating to the notes.

The Indenture governing the notes contains financial covenants that restrict us or any of our subsidiaries from incurring indebtedness in amounts that would cause certain ratios specified in the Indenture, or Covenant Ratios, not to exceed certain fixed values (see “Description of Notes—Certain Covenants—Limitations on Incurrence of Debt”). The Covenant Ratios are calculated by reference to various specialized definitions specific to the Indenture, some of which utilize non-GAAP financial measures. If we had been subject to the covenants in the Indenture as of June 30, 2013, our Ratio of Debt to Adjusted Total Asset Value would have been 0.42 and our Ratio of Stabilized Consolidated Income Available for Debt Service to Stabilized Consolidated Interest Expense would have been 3.32. For instance, certain definitions on which the Covenant Ratios rely reflect various adjustments to add or subtract certain items from GAAP consolidated net income and interest expense. In addition, management of Sotherly, our general partner, has discretion in calculating certain elements of the Covenant Ratios. For example, the definition of Consolidated Income Available for Debt Service allows management of Sotherly to determine in good faith whether, and the extent to which, certain non-recurring or other unusual items will be added back to our consolidated net income (calculated in accordance with GAAP) for purposes of calculating the Covenant Ratios. As a result of the foregoing, the financial statements that we include in future filings with the SEC, which are required to be prepared in accordance with GAAP, may employ different financial measures from those used in the Covenant Ratios, which may make it difficult for holders of our notes to determine independently whether we are in compliance with certain financial covenants.

Under certain circumstances, we may redeem the notes before maturity, and you may be unable to reinvest the proceeds at the same or a higher rate of return.

We may redeem all or a portion of the notes at any time after 2016, as described under “Description of Notes–Optional Redemption.” If a redemption does occur, you may be unable to reinvest the money you receive in the redemption at a rate that is equal to or higher than the rate of return on the notes.

General market conditions and other unpredictable factors could materially and adversely affect market prices for the notes.

There can be no assurance about the market prices for the notes. Several factors, many of which are beyond our control, will influence the market value of the notes. Factors that might influence the market value of the notes include, but are not limited to:

| • | our creditworthiness, financial condition, performance and prospects; |

| • | the market for similar securities; and |

| • | economic, financial, geopolitical, regulatory or judicial events that affect us or the financial markets generally (including the occurrence of market disruption events). |

15

Table of Contents

If you purchase notes, whether in this offering or in the secondary market, the notes may subsequently trade at a discount to the price that you paid for them.

There is no established trading market for the notes, which could make it more difficult for you to sell your notes and could adversely affect their price.

The notes constitute a new issue of securities for which no established trading market exists. Consequently, it may be difficult for you to sell your notes. If the notes are traded after their initial issuance, they may trade at a discount, depending upon:

| • | our financial condition; |

| • | prevailing interest rates; |

| • | the time remaining on the maturity of the notes; |

| • | their subordination to our existing and future liabilities; |

| • | the outstanding principal amount of the notes; |

| • | the market for similar securities; and |

| • | other factors beyond our control, including general economic conditions and conditions affecting lodging companies. |

We have applied to list the notes on the NASDAQ® Global Market; however, we cannot assure you of the development or liquidity of any trading market for the notes following this offering.

Risks Related to Our Debt and Financing

We may not be able to generate sufficient cash to service our debt obligations, including our obligations under the notes. Increased leverage as a result of this offering may harm our financial condition and results of operations.

Our ability to make payments on and to refinance our indebtedness, including the notes, will depend on our financial and operating performance, which is subject to prevailing economic and competitive conditions and to certain financial, business and other factors beyond our control. As of June 30, 2013, we had consolidated debt of approximately $151.0 million, which is comprised of approximately $134.9 million secured and approximately $16.1 million unsecured debt. Of the approximately $16.1 million of unsecured debt as of June 30, 2013, approximately $12.5 million is related to the 12,458 shares of Preferred Stock issued and outstanding as of June 30, 2013 (of which 2,460 shares were redeemed on August 2, 2013 for an aggregate redemption price of approximately $2.7 million). We intend to redeem the remaining 9,998 shares of Preferred Stock with a portion of the net proceeds of this offering. The Preferred Stock is treated as debt under GAAP. See “Use of Proceeds.”

Our level of indebtedness could have important consequences to you, because:

| • | it could affect adversely the Operating Partnership’s ability to satisfy its financial obligations, including those relating to the notes; |

| • | a portion of our cash flows from operations will have to be dedicated to interest and principal payments and may not be available for operations, working capital, capital expenditures, expansion, acquisitions or general corporate or other purposes; |

| • | it may impair our ability to obtain additional financing in the future and/or to refinance existing debt; |

| • | it could require us to agree to additional restrictions and limitations on our business operations and capital structure to obtain financing; |

| • | it may force us to dispose of one or more of our properties, possibly on unfavorable terms; |

| • | it may limit our flexibility in planning for, or reacting to, changes in our business and industry; and |

| • | it may make us more vulnerable to downturns in our business, our industry or the economy in general. |

16

Table of Contents

We have debt obligations maturing in 2014, and if we are not successful in extending the term of this indebtedness or in refinancing this debt on acceptable economic terms or at all, our overall financial condition could be materially and adversely affected.

We will be required to seek additional capital in the near future to refinance or replace existing long-term mortgage debt that is maturing. Based on current market conditions, the availability of financing is, and may continue to be, limited. There can be no assurance that we will be able to obtain future financings on acceptable terms, if at all. On June 28, 2013, we entered into an agreement with TowneBank to extend the maturity of the mortgage on the Crowne Plaza Hampton Marina in Hampton, Virginia, until June 30, 2014. Under the terms of the extension, we made a principal payment of approximately $1.1 million to reduce the principal balance on the loan to $6.0 million. Subject to certain terms and conditions, we may extend the maturity date of the loan to June 30, 2015. In August 2014, our indebtedness to an affiliate of Carlyle related to our joint venture investment in the Crowne Plaza Hollywood Beach Resort matures. In August 2014, the mortgage on our Hilton Philadelphia Airport matures, but we may extend such mortgage until March 2017 pursuant to certain terms and conditions. The total aggregate amount of our debt obligations maturing in 2014 is approximately $38.3 million, which represents approximately 25.7% of our total debt obligations.

We will need to, and plan to, renew, replace or extend our long-term indebtedness prior to their respective maturity dates. If we are unable to extend these loans, we may be required to repay the outstanding principal amount at maturity or a portion of such indebtedness upon refinance. If we do not have sufficient funds to repay any portion of the indebtedness, it may be necessary to raise capital through additional debt financing, private or public offerings of debt securities or equity financings. We are uncertain whether we will be able to refinance these obligations or if refinancing terms will be favorable. If, at the time of any refinancing, prevailing interest rates or other factors result in higher interest rates on refinancing, increases in interest expense would lower our cash flow, and, consequently, cash available to meet our financial obligations. If we are unable to obtain alternative or additional financing arrangements in the future, or if we cannot obtain financing on acceptable terms, we may not be able to execute our business strategies or we may be forced to dispose of hotel properties on disadvantageous terms, potentially resulting in losses and potentially reducing cash flow from operating activities if the sale proceeds in excess of the amount required to satisfy the indebtedness could not be reinvested in equally profitable real property investments. Moreover, the terms of any additional financing may restrict our financial flexibility, including the debt we may incur in the future, or may restrict our ability to manage our business as we had intended. To the extent we cannot repay our outstanding debt, we risk losing some or all of our hotel properties to foreclosure and we could be required to invoke insolvency proceedings including, but not limited to, commencing a voluntary case under the U.S. Bankruptcy Code.

For tax purposes, a foreclosure of any of our hotels would be treated as a sale of the hotel for a purchase price equal to the outstanding balance of the debt secured by the mortgage. If the outstanding balance of the debt secured by the mortgage exceeds our tax basis in the hotel, we would recognize taxable income on foreclosure, but we would not receive any cash proceeds, which could hinder Sotherly’s ability to meet the REIT distribution requirements imposed by the Internal Revenue Code of 1986, as amended, or the Code. In addition, we may give full or partial guarantees to lenders of mortgage debt on behalf of the entities that own our hotels. When we give a guarantee on behalf of an entity that owns one of our hotels, we will be responsible to the lender for satisfaction of the debt if it is not paid by such entity. See “Description of Notes – Events of Default” for a discussion of potential implications should any of our hotels be foreclosed on due to a default.

We must comply with financial covenants in our mortgage loan agreements.

Our mortgage loan agreements contain various financial covenants. Failure to comply with these financial covenants could result from, among other things, changes in the local competitive environment, general economic conditions and disruption caused by renovation activity or major weather disturbances.

If we violate the financial covenants contained in these agreements, we may attempt to negotiate waivers of the violations or amend the terms of the applicable mortgage loan agreement with the lender; however, we can

17

Table of Contents

make no assurance that we would be successful in any such negotiation or that, if successful in obtaining waivers or amendments, such waivers or amendments would be on attractive terms. Some mortgage loan agreements provide alternate cure provisions which may allow us to otherwise comply with the financial covenants by obtaining an appraisal of the hotel, prepaying a portion of the outstanding indebtedness or by providing cash collateral until such time as the financial covenants are met by the collateralized property without consideration of the cash collateral. Alternate cure provisions which include prepaying a portion of the outstanding indebtedness or providing cash collateral may have a material impact on our liquidity.

If we are unable to negotiate a waiver or amendment or satisfy alternate cure provisions, if any, or unable to meet any alternate cure requirements and a default were to occur, we would possibly have to refinance the debt through additional debt financing, private or public offerings of debt securities, or additional equity financing. We are uncertain whether we will be able to refinance these obligations or if refinancing terms will be favorable.

Our organizational documents have no limitation on the amount of indebtedness we may incur. As a result, we may become highly leveraged in the future, which could materially and adversely affect us.

Our business strategy contemplates the use of both secured and unsecured debt to finance long-term growth. In addition, our organizational documents contain no limitations on the amount of debt that we may incur, and Sotherly’s board of directors may change our financing policy at any time. As a result, we may be able to incur substantial additional debt, including secured debt, in the future. Incurring debt could subject us to many risks, including the risks that:

| • | our cash flows from operations may be insufficient to make required payments of principal and interest; |

| • | our debt may increase our vulnerability to adverse economic and industry conditions; |

| • | we may be required to dedicate a substantial portion of our cash flows from operations to payments on our debt, thereby reducing cash available for funds available for operations and capital expenditures, future business opportunities or other purposes; and |

| • | the terms of any refinancing may not be in the same amount or on terms as favorable as the terms of the existing debt being refinanced. |

Risks Related to Our Business and Properties

If the economy falls back into a recessionary period or fails to maintain positive growth, our operating performance, financial results and ability to meet our financial obligations may be harmed by declines in occupancy, average daily room rates and/or other operating revenues.

The performance of the lodging industry and the general economy historically have been closely linked. In an economic downturn, business and leisure travelers may seek to reduce costs by limiting travel and/or reducing costs on their trips. Our hotels, which are all full-service hotels, may be more susceptible to a decrease in revenue, as compared to hotels in other categories that have lower room rates. A decrease in demand for hotel stays and hotel services will negatively affect our operating revenues, which will lower our cash flow and may affect our ability to maintain compliance with our debt obligations, including the Operating Partnership’s obligations under the notes. We incurred a net loss of approximately $5.3 million for our 2012 fiscal year. A renewed economic downturn may produce continued losses. A weakening of the economy may adversely and materially affect our industry, business, results of operations and ability to meet our financial obligations and we cannot predict the likelihood, severity or duration of any such downturn. Moreover, reduced revenues as a result of a weakening economy may also reduce our working capital and impact our long-term business strategy.

Geographic concentration of our hotels makes our business vulnerable to economic downturns in the Mid-Atlantic and Southern United States.

Our hotels are located in the Mid-Atlantic and Southern United States. As a result, economic conditions in the Mid-Atlantic and Southern United States significantly affect our revenues and the value of our hotels to a greater

18

Table of Contents

extent than if we had a more geographically diversified portfolio. Business layoffs or downsizing, industry slowdowns, changing demographics and other similar factors that may adversely affect the economic climate in these areas could have a significant adverse impact on our business. Any resulting oversupply or reduced demand for hotels in the Mid-Atlantic and Southern United States and in our markets in particular would therefore have a disproportionate negative impact on our revenues and limit our ability to meet our financial obligations.

We own a limited number of hotels and significant adverse changes at one hotel may impact our ability to meet our financial obligations.

As of June 30, 2013, our portfolio consisted of nine wholly-owned properties and one joint venture property with a total of 2,424 rooms. Significant adverse changes in the operations of any one hotel could have a material adverse effect on our financial performance and, accordingly, on our ability to meet our financial obligations.

We are subject to risks of increased hotel operating expenses and decreased hotel revenues.

Our leases with our TRS Lessee provide for the payment of rent based in part on gross revenues from our hotels. Our TRS Lessee is subject to hotel operating risks including decreased hotel revenues and increased hotel operating expenses, including but not limited to the following:

| • | wage and benefit costs; |

| • | repair and maintenance expenses; |

| • | energy costs; |

| • | property taxes; |

| • | insurance costs; and |

| • | other operating expenses. |

Any increases in these operating expenses can have a significant adverse impact on our TRS Lessee’s ability to pay rent and other operating expenses and, consequently, our earnings, cash flow and ability to meet our financial obligations.

In keeping with our investment strategy, we may acquire, renovate and/or re-brand hotels in new or existing geographic markets as part of our repositioning strategy. Unanticipated expenses and insufficient demand for newly repositioned hotels could adversely affect our financial performance and our ability to meet our financial obligations.

We have in the past and may continue to develop or acquire hotels in geographic areas in which our management may have little or no operating experience. Additionally, those properties may also be renovated and re-branded as part of a repositioning strategy. Potential customers may not be familiar with our newly renovated hotel or be aware of the brand change. As a result, we may have to incur costs relating to the opening, operation and promotion of those new hotel properties that are substantially greater than those incurred in other geographic areas. These hotels may attract fewer customers than expected and we may choose to increase spending on advertising and marketing to promote the hotel and increase customer demand. Unanticipated expenses and insufficient demand at new hotel properties, therefore, could adversely affect our financial performance and our ability to meet our financial obligations.

We do not have the authority to require any hotel to be operated in a particular manner or to govern any particular aspect of the daily operations of any hotel and as a result, our financial performance and ability to meet our financial obligations are dependent on the management of our hotels by MHI Hotels Services.

Since federal income tax laws restrict REITs and their subsidiaries from operating or managing hotels, we do not operate or manage our hotels. Instead, we lease all of our hotels to subsidiaries of our TRS Lessee, and our TRS Lessee retains third-party managers to operate our hotels pursuant to management agreements.

19

Table of Contents

Under the terms of our management agreements with MHI Hotels Services and the REIT qualification rules, our ability to participate in operating decisions regarding the hotels is limited. We will depend on MHI Hotels Services to operate our hotels as provided in the management agreements. We do not have the authority to require any hotel to be operated in a particular manner or to govern any particular aspect of the daily operations of any hotel. Thus, even if we believe our hotels are being operated inefficiently or in a manner that does not result in satisfactory occupancy rates, RevPAR and ADR, we may not be able to force MHI Hotels Services to change its method of operation of our hotels. Additionally, in the event that we need to replace MHI Hotels Services or any other management companies in the future, we may be required by the terms of the applicable management agreement to pay substantial termination fees and may experience significant disruptions at the affected hotels.

Our ability to meet our financial obligations is subject to fluctuations in our financial performance, operating results and capital improvements requirements.

We lease all of our hotels to our TRS Lessee. Our TRS Lessee is subject to hotel operating risks, including risks of sustaining operating losses after payment of hotel operating expenses, including management fees. Among the factors which could cause our TRS Lessee to fail to make required rent payments are reduced net operating profits or operating losses, increased debt service requirements and capital expenditures at our hotels, including capital expenditures required by the franchisors of our hotels. Among the factors that could reduce the net operating profits of our TRS Lessee are decreases in hotel revenues and increases in hotel operating expenses. Hotel revenue can decrease for a number of reasons, including increased competition from a new supply of hotel rooms and decreased demand for hotel rooms. These factors can reduce both occupancy and room rates at our hotels. We cannot assure you that we will continue to generate sufficient cash to meet our financial obligations.

Hedging against interest rate exposure may adversely affect us and our hedges may fail to protect us from the losses that the hedges were designed to offset.