UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________________________________________________________

Form 20-F

(Mark One)

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

or

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

or

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Commission file number: 000-51138

(Exact name of registrant as specified in its charter)

| N/A | |||||

| (Translation of registrant’s name into English) | (Jurisdiction of incorporation or organization) | ||||

_________________________________________________________________________

(Address of principal executive offices)

_________________________________________________________________________

Chief Financial Officer

Telephone: 82 ‑2‑2132‑7000

Fax: 82‑2‑2132‑7070

(Name, Telephone, E‑mail and/or Facsimile number and Address of Company Contact Person)

_________________________________________________________________________

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||||||||||||

________________________________

*Not for trading, but only in connection with the listing of American depositary shares on the NASDAQ Global Market pursuant to the requirements of the Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: Shares, par value Won 500: 6,948,900 as of December 31, 2022.

Indicate by check mark if the registrant is a well‑known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☑

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☑

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S‑T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☑ | |||||||||

| Non-accelerated filer | ☐ | Emerging growth company | |||||||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ International Financial Reporting Standards as issued by the International Accounting Standards Board ☑ Other ☐

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Exchange Act). Yes ☐ No ☑

TABLE OF CONTENTS

2

| ITEM 16.I. | ||||||||

3

CERTAIN DEFINED TERMS

Unless the context otherwise requires, references in this annual report on Form 20‑F (this “Annual Report”) to:

•“ADRs” are to the American depositary receipts that evidence our ADSs;

•“ADSs” are to our American depositary shares, each of which represents one share of our common stock;

•“China” or the “PRC” are to the People’s Republic of China (excluding, for the purposes of this Annual Report, Taiwan, Hong Kong and Macau, unless specifically indicated otherwise);

•“Chinese Yuan” are to the currency of China;

•“EUR” or “Euro” are to the currency of the Eurozone consisting of Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia and Spain;

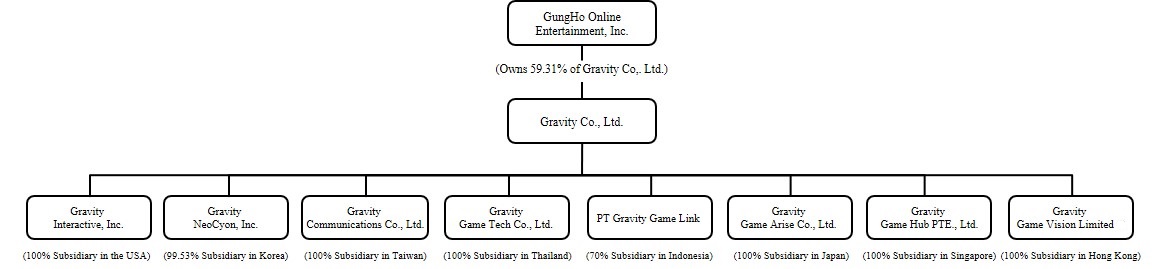

•“Gravity,” “the Company,” “we,” “us,” “our,” or “our company” are to Gravity Co., Ltd. and our subsidiaries, except as otherwise indicated or required by context;

•“Hong Kong” are to the Hong Kong Special Administrative Region of the PRC;

•“Indonesian Rupiah” are to the currency of the Republic of Indonesia;

•“Japanese Yen” or “JPY” are to the currency of Japan;

•“Korea” are to the Republic of Korea;

•“Macau” are to the Macau Special Administrative Region of the PRC;

•“NT dollar” or “NT$” are to the currency of Taiwan;

•“Philippine Peso” are to the currency of the Republic of the Philippines;

•“Taiwan” are to Taiwan, the Republic of China;

•“Thai Baht” or “THB฿” are to the currency of the Kingdom of Thailand;

•“US$,” “U.S. dollar,” or “Dollar” are to the currency of the United States of America;

•“Won,” “Korean Won,” or “W” are to the currency of Korea; and

•“SGD” or “S$” are to the currency of Singapore.

•“BRL” or “Brazil R$” are to the currency of Brazil.

For your convenience, and unless otherwise stated, this Annual Report contains translations of certain Won amounts into U.S. dollars at the noon buying rate in New York City for cable transfers in Korean Won as certified by the Federal Reserve Bank of New York for customs purposes in effect on December 30, 2022, which was Won 1,260.18 to US$ 1.00. No assurance is given that any Won or Dollar amounts could have been or may now be converted into Dollars or Won, as the case may be, at such rate, or any other rate, or at all.

Discrepancies in tables between totals and sums of the amounts listed are due to rounding.

4

FORWARD‑LOOKING STATEMENTS

This Annual Report for the year ended December 31, 2022 contains “forward‑looking statements,” as defined in Section 27A of the U.S. Securities Act of 1933, as amended, or the “Securities Act,” and Section 21E of the U.S. Securities Exchange Act of 1934, as amended, or the “Exchange Act.” The forward‑looking statements are based on our current expectations, assumptions, estimates and projections about us and our industry, and are subject to various risks and uncertainties. Generally, these forward‑looking statements can be identified by the use of forward‑looking terminology such as “anticipate,” “believe,” “considering,” “depends,” “estimate,” “expect,” “intend,” “plan,” “planning,” “planned,” “predict,” “project,” “continue” and variations of these words, similar expressions, or that certain events, actions or results “will,” “may,” “might,” “should,” “would” or “could” occur, be taken or be achieved.

Forward‑looking statements include, but are not limited to, the following:

•future prices of and demand for our products;

•future earnings and cash flow;

•estimated development and commercial launch schedule of our games in development;

•our ability to attract new customers and retain existing customers;

•the expected growth of the Korean and worldwide online and mobile gaming industries;

•the effect that economic, political or social conditions in Korea have on the revenue generated from our online or mobile game products and our results of operations;

•the effect that any global financial crisis or global economic recession will or may have on our business prospects, financial condition and results of operations; and

•our future business development and prospects, results of operations and financial condition.

We caution you not to place undue reliance on any forward‑looking statement, each of which involves risks and uncertainties. Although we believe that the assumptions on which our forward‑looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward‑looking statements based on those assumptions could be incorrect. All forward‑looking statements are based on our management’s current expectations, assumptions, estimates and projections of future events and are subject to a number of factors that could cause actual results to differ materially from those described in the forward‑looking statements. Risks and uncertainties associated with our business include, but are not limited to, risks related to changes in the regulatory environment; technology changes; potential litigation and governmental actions; changes in the competitive environment; changes in customer preference and popular culture and trends, including mobile or online gaming culture; political changes; global economic events including, but not limited to, the global social, political and economic impact of the spread of coronavirus, a significant downturn in the global economic and financial markets and a tightening of the global credit markets; changes in business and economic conditions; fluctuations in foreign exchange rates; fluctuations in the prices of our products; decreasing consumer confidence and slowing of economic growth generally; and other risks and uncertainties that are more fully described under the heading “Risk Factors” in this Annual Report, and elsewhere in this Annual Report. In light of these and other uncertainties, you should not conclude that we will necessarily achieve any plans and objectives or projected financial results referred to in any of the forward‑looking statements. Except as required by law, we undertake no obligation to update or revise any forward‑looking statements, whether as a result of new information, future events or otherwise. All subsequent forward‑looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section.

5

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

ITEM 3.A. RESERVED

ITEM 3.B. CAPITALIZATION AND INDEBTEDNESS

Not applicable.

ITEM 3.C. REASONS FOR THE OFFER AND USE OF PROCEEDS

Not applicable.

ITEM 3.D. RISK FACTORS

You should carefully consider the risks described in this section, together with all of the other information included in this Form 20-F, in evaluating us and our shares. The following risk factors could adversely affect our business, financial condition, results of operations and the price of our shares.

Risk Factor Summary

The following is a summary of the principal risks discussed in greater detail in the following pages, that could materially and adversely affect our business, results of operations, cash flows, and financial condition.

Risks Relating to our Business

•We currently depend on our main game, Ragnarok Online, and games developed from Ragnarok Online, for a significant portion of our revenues.

•If we are unable to consistently and timely develop, acquire, license, launch, market or operate commercially successful online and mobile games, our business, financial condition and results of operations may be materially and adversely affected.

•We may not be successful in making our mobile games profitable, and our profit margins from mobile games may be relatively lower than the profits we have enjoyed historically for online games.

•We depend on our overseas licensees for a portion of our revenues and rely on them to distribute, market, and operate our games and comply with applicable laws and government regulations.

•We operate in a highly competitive industry and compete against many large companies.

•To continue to be successful, we must leverage the global connectivity and distribution of mobile platforms and our relationships with mobile platform providers, which in many cases have the unilateral ability to amend their policies and terms and conditions for applications and developers.

6

•We publish games developed by third parties, which exposes us to a number of potential operational, legal and reputational risks.

•Unexpected network interruptions, security breaches or computer virus attacks could harm our business and reputation.

•Unauthorized use of our intellectual property rights by third parties and the expenses incurred in protecting our intellectual property rights may adversely affect our business.

•We may be subject to claims with respect to the infringement of intellectual property rights of others, which could result in substantial costs and diversion of our financial and management resources.

•Our products and services, including those relating to P2E and NFT, may subject us to additional regulatory requirements in the future, which may be costly and difficult to comply with or adversely affect our business, and other potential risks to our business.

Risks Relating to our Company Structure

•GungHo, the licensee of our games in Japan, is our majority shareholder, which gives them control of our board of directors.

•We are a “controlled company” within the meaning of the NASDAQ Stock Market Rules and may rely on exemptions from certain corporate governance requirements.

Risks relating to our Regulatory Environment

•Our online and mobile operations and businesses are subject to laws, rules and regulations in the countries in which our games are distributed, such as Thailand, Taiwan, Korea, Japan, the United States and the Philippines, changes to which are difficult to predict, and uncertainties in interpretation and enforcement of the laws, rules, and regulations in such countries may limit the protections available to us.

•Our online and mobile games may be subject to governmental restrictions or ratings systems, which could delay or prohibit the release of new games or reduce the existing and potential scope of our user base.

•Restrictions and controls on currency exchange in Korea and in certain countries in which our games are distributed may limit our ability to effectively utilize revenues generated in Won to fund our business activities outside Korea or expenditures denominated in foreign currencies, and may limit our ability to receive and remit revenues effectively.

Risks relating to our Market Environment

•The global economy and markets where we operate may continue to be negatively impacted by the spread of coronavirus which may adversely affect our business and our financial results.

•Our businesses and partnerships may be affected by geopolitical tensions between China and the United States.

•Fluctuations in exchange rates could result in foreign currency exchange losses.

RISKS RELATING TO OUR BUSINESS

We currently depend on our main game, Ragnarok Online, and games developed from Ragnarok Online, for a significant portion of our revenues.

A significant portion of our revenues has been and is currently derived from Ragnarok Online and other games developed based on the contents of Ragnarok Online, including our mobile game, Ragnarok Origin, Ragnarok M: Eternal Love, Ragnarok X: Next Generation. In 2022 and 2021, we derived Won 86,743 million (US$ 68,834 thousand) and Won 72,177 million in revenues from Ragnarok Online, respectively, representing approximately 18.7% and 17.4% of our

7

total revenues for such periods. We derived Won 358,599 million (US$ 284,562 thousand) and Won 314,282 million in revenues from the games developed based on the contents of Ragnarok Online in 2022 and 2021, respectively, representing approximately 77.3% and 75.9% of our total revenues for such periods. In 2022 and 2021, our mobile game, Ragnarok M: Eternal Love, represented 20.1% of our total revenues, or Won 93,203 million (US$ 73,960 thousand), and 27.2% of our total revenues, or Won 112,486 million, respectively. Ragnarok X: Next Generation, our mobile game, represented 16.7% of our total revenues, or Won 77,278 million (US$ 61,323 thousand), and 30.5% of our total revenues, or Won 126,336 million respectively. Ragnarok Origin, our mobile game, represented 35.5% of our total revenues, or Won 164,787 million (US$ 130,765 thousand), and 16.0% of our total revenues, or Won 66,385 million in 2022 and 2021, respectively.

Ragnarok Online has been on the market for twenty-one years and has reached maturity in most of our principal markets. The Company has continually maintained, improved and updated Ragnarok Online and developed new games based on Ragnarok Online. If we fail to maintain, improve, update or enhance Ragnarok Online in a timely manner or fail to successfully develop new games based on Ragnarok Online, this is likely to lead to a decline in the user base of games developed from the contents of Ragnarok Online, which in turn is likely to lead to a material decline in our subscription revenues, royalties and mobile revenue. This would likely materially and adversely affect our business, financial condition and results of operations.

If we are unable to consistently and timely develop, acquire, license, launch, market or operate commercially successful online and mobile games, our business, financial condition and results of operations may be materially and adversely affected.

In order to grow our revenues and net income, we must retain our existing users and attract new users by developing, acquiring, licensing, launching, marketing, or operating other commercially successful online and mobile games. In addition to Ragnarok Online, we currently offer four other online games: Ragnarok Online II, Requiem Online, R.O.S.E. Online and Dragonica (which is also known as Dragon Saga in the United States, Canada and South America except for Brazil). None of our other online games to date has proven to be as commercially successful as Ragnarok Online.

In 2022, mobile games represented 77.4% of our total revenues, with one mobile game, Ragnarok Origin, representing 35.5% of our total revenues. Mobile games are played on mobile devices and smartphones, including Google Android compatible phones, the Apple iPhone, other feature phones and tablet computers. Following a 2015 development agreement with Shanghai The Dream Network Technology Co., Ltd. (“Dream Square”) to develop and distribute two mobile games based on the contents of Ragnarok Online, we launched six mobile games developed by Dream Square (by itself and through certain third party subcontractors), all of which are based on the contents of Ragnarok Online. For additional information, see ITEM 4.B. “BUSINESS OVERVIEW—OUR PRODUCTS—Mobile games.” Although we have achieved significant commercial success after publishing these mobile games in 2017, there is no guarantee that we will continue to be successful in the mobile game publishing business, and our revenues from mobile game publishing could decline over time.

Our revenues from mobile games increased by 12.1% to Won 358,772 million (US$ 284,699 thousand) in 2022 from Won 320,164 million in 2021. This was mainly due to a 148.2% increase in revenues from Ragnarok Origin to Won 164,787 million (US$ 130,765 thousand) in 2022 from Won 66,385 million in 2021, driven by new launching in Taiwan, Hong Kong and Macau in September 2022. However, mobile revenue from customers in Korea decreased from Won 50,966 million in 2021 to Won 25,282 million in 2022. Mobile revenue from customers in Thailand decreased from Won 67,592 million in 2021 to Won 45,800 million in 2022. Although the decreases in mobile revenue in Korea and Thailand were more than offset by mobile revenue increases in other markets, such as Taiwan and the United States, we may also experience declines in mobile game revenue from these or other markets in the future. A game’s commercial success largely depends on appealing to the tastes and preferences of a critical mass of users as well as the willingness of such users to purchase the game and/or in‑game items, and to continue as paying subscribers, all of which are difficult to predict prior to a game’s development and introduction. Developing games requires substantial development costs, including the costs of employing skilled developers and acquiring or developing game engines which enable the creation of games with the latest technological features. For us to continue to succeed, we must acquire, license or develop promising games at acceptable costs and ensure technical support for the successful operation of such games. The online and mobile gaming industries are highly competitive, and we may not be able to acquire, license or develop promising games at acceptable costs. In order to successfully distribute and operate a game, we also need a sizable game management and support staff, continued investment in technology and a substantial marketing budget.

8

In 2022 and 2023, we launched numerous mobile games in new markets including: Milkmaid Of The Milky Way in Korea, Japan, Taiwan, Hong Kong and Macau; Paladog Tactics in Korea; Raganarok: The Lost Memories in North America, Brazil, Korea, South America, Australia, and New Zealand; Ragnarok Tactics II in Thailand; Ragnarok Monster's Arena in Taiwan, Hong Kong and Macau; Ragnarok Arena in Korea, Southeast Asia, the Middle East, and Oceania; Ragnarok Begins in North America; Ragnarok Origin in Taiwan, Hong kong, Macau and Southeast Asia; Ragnarok V: Returns in Oceania; Ragnarok Labyrinth NFT globally and Ragnarok X: Next Generation in Korea. We cannot assure you that the games we develop or publish will be attractive to users or otherwise be commercially successful, launched as scheduled or able to successfully compete with games operated by our competitors. If we are not able to consistently develop, acquire, license, launch, market or operate commercially successful games, we may not be able to generate enough revenues to offset our initial development, acquisition, licensing and/or marketing costs and our business, financial condition, and results of operations may be materially and adversely affected.

We may not be successful in making our mobile games profitable, and our profit margins from mobile games may be relatively lower than the profits we have enjoyed historically for online games.

Our profit margins from our mobile games, even if the games are successful, are generally lower than our profits generated from online games. This is because, in order to gain access to our games on mobile app stores, the primary distribution channel for our mobile games, we must enter into revenue-sharing arrangements that result in lower profit margins compared with those of our online games.

We have devoted and expect to continue to devote a significant amount of resources to the development of our mobile games, but the relatively lower profit margins and other uncertainties make it difficult to know whether we will succeed in making our mobile game operations more profitable. If we do not succeed in doing so, our business and results of operations will be adversely affected.

If we fail to achieve and maintain an effective system of internal controls over financial reporting, we may be unable to accurately report our financial results or do so on a timely basis and our ability to prevent or detect fraud may be reduced and investor confidence and the market price of our ADSs may be adversely affected.

We are subject to Section 404 of the Sarbanes‑Oxley Act of 2002, which requires us to, among other things, maintain an effective system of internal controls over financial reporting, and requires our management to provide a certification on the effectiveness of our internal controls on an annual basis.

Although we have determined that our internal control over financial reporting was effective as of December 31, 2022, we may in the future determine that we have a material weakness in our internal controls over financial reporting. If we fail to maintain an effective system of internal controls over financial reporting, we may be unable to accurately report our financial results in a timely manner or prevent errors or fraud. Any of these possible outcomes could result in an adverse reaction in the financial marketplace due to loss of investor confidence in the reliability of our consolidated financial statements and could result in investigations or sanctions by the SEC, NASDAQ, or other regulatory authorities or in stockholder litigation. Any of these factors could ultimately harm our business and could adversely impact the market price of our ADSs. See ITEM 15. “CONTROLS AND PROCEDURES.”

We depend on our overseas licensees for a portion of our revenues and rely on them to distribute, market, and operate our games and comply with applicable laws and government regulations.

In certain markets, we license our games to overseas operators or distributors for license fees and royalty payments based on a percentage of revenues generated from our games in such markets. Overseas license fees and royalty payments generated from our mobile games represented 20.8% of our total revenues in 2022 and 37.6% of our total revenues in 2021, with 79.6% of our 2022 revenues from mobile game license fees and royalty payments attributable to license arrangements with Nuverse (Hong Kong) Limited (“Nuverse”). Under the applicable licensing contract, Nuverse is to provide the service for a term of two years commencing on the date of Ragnarok X: Next Generation's commercialization in Taiwan, Hong Kong, Macau and Southeast Asia, with an automatic one-year extension thereafter. Overseas license fees and royalty payments generated from our online games represented 1.9% of our total revenues in 2022 and 2.6% of our total revenues in 2021, with 86.6% of our 2022 revenues from online game license fees and royalty payments attributable to license arrangements with GungHo Online Entertainment Inc. (“GungHo”), which has been our largest shareholder and beneficially owns, as of the date hereof, 59.3% of our common shares.

9

Deterioration of our relationships with material licensees or material adverse changes in the terms of our licenses with such licensees could have a material adverse effect on our business, prospects, financial condition and results of operations. In addition, deterioration or any adverse developments in the operations, including changes in senior management, of our overseas licensees may materially and adversely affect our business, financial condition and results of operations.

Our overseas licensees generally have the exclusive right to distribute our games in their respective markets for a term of two or three years and may also operate or publish other online and mobile games developed or offered by our competitors, and we may not be able to easily terminate the license agreements as the agreements do not specify particular financial or performance criteria that need to be met by our licensees. For example, GungHo, which is our 59.3% shareholder, also has its own mobile games business. If our overseas licensees devote greater time and resources to marketing their proprietary games or those of our competitors, we may not be able to terminate our license agreements or enter into new license agreements with different licensees, and our revenues and net profit may be adversely impacted. Also, a failure to satisfy our obligation to provide technical and other consulting services to the licensees under the license agreements may negatively affect user satisfaction and loyalty and hinder our licensees’ efforts to increase market share, which may lead the licensees to focus their attention on our competitors’ games or request modifications to or terminate our licensing agreements and/or not renew expired license agreements.

Our overseas licensees remit royalty payments to us based on a percentage of sales from our games after deducting certain expenses. Some licensees may be allowed to deduct certain expenses before calculating royalty payments depending on the terms of the applicable contracts. Failure by our licensees to maintain a stable and efficient billing, recording, distribution and payment collection network in their respective markets may result in inaccurate recording of sales or insufficient collection of payments (or an illicit diversion of payments) from such markets and may materially and adversely affect our financial condition and results of operations. Although we have audit rights pursuant to our license agreements to ensure that proper payment amounts are being recorded and remitted, such activities can be disruptive and time consuming and as a result, we do not exercise such rights on a regular basis.

Furthermore, our overseas licensees are responsible for complying with local laws, including obtaining and maintaining the requisite government licenses and permits. Failure by our overseas licensees to do so may result in, among others, a suspension of service of our games in such market which may result in user complaints and a decrease in the use of our games which would likely have a material adverse effect on our business, financial condition and results of operations.

Disruptions in the political environments in which our licensees operate may also have a negative impact on their business and in turn materially and adversely affect our business, financial condition and results of operations.

We operate in a highly competitive industry and compete against many large companies.

Increased competition in the online and mobile gaming industry from existing and potential competitors could make it difficult for us to retain existing users and attract new users, and could reduce the number of hours users spend playing our current or future games or cause us and our licensees to reduce the fees charged to play our current or future games. In some of our principal markets, such as Korea, Japan, Taiwan and Thailand. growth of the market for online games has continued to slow while competition remains strong. We expect more companies to enter the online and mobile game industries and a wider range of online and mobile games to be introduced in our current and future markets. If we are unable to compete effectively in our principal markets, our business, financial condition and results of operations could be materially and adversely affected.

Our competitors in the online and mobile game industries vary in size from small companies to very large companies with dominant market shares. Many of our competitors have significantly greater financial, marketing and game development resources than we have. As a result, we may not be able to devote adequate resources to develop, acquire or license new games, undertake extensive marketing campaigns, adopt aggressive pricing policies or adequately compensate our game developers or third‑party game developers to the same degree as many of our competitors do.

As the online and mobile game industries are characterized by rapid technological changes, especially in the technical capabilities of devices for mobile games, and changing interests and preferences of users, continuous investment is required to develop and publish new games. Also, as the online and mobile game industries in many of our markets are rapidly evolving, our current or future competitors may adapt to the changing competitive landscape and market conditions and compete more successfully than us. In particular, online and mobile game products are becoming increasingly similar

10

to each other, thus becoming more commoditized and less differentiated. In such an environment, larger companies with relative economies of scale have a clear advantage over smaller companies like us, as they are able to develop games in a more cost efficient manner, diversify their risks with broader categories of games and genres and increase their chances of offering widely popular games. In addition, any of our competitors may offer products and services that have significant performance, price, creativity or other advantages over those offered by us. These products and services may weaken the market strength of our brand name and achieve greater market acceptance than ours. In addition, any of our current or future competitors may be acquired by, receive investments from or enter into strategic relationships with larger and more well established financed companies and therefore may be able to obtain significantly greater financial marketing, game licensing and development resources than we can.

Furthermore, compared with the online or console game genres, the mobile game market has relatively low barriers to entry because development of a mobile game requires relatively less time and personnel, due to the limitations of the devices on which mobile games are played such as screen size and processing power. Moreover, development tools for mobile games are easier to obtain and use, and open marketplaces, such as the Google Play Store and Apple’s App Store, enable developers to easily distribute mobile games to a large global audience. Global game engine companies are also offering game developers support programs to lower the barrier to entry. Therefore, we expect the number of mobile game developers to continually increase in the future and competition to become more intense. See ITEM 4.B. “BUSINESS OVERVIEW—COMPETITION.”

To continue to be successful, we must leverage the global connectivity and distribution of mobile platforms and our relationships with mobile platform providers, which in many cases have the unilateral ability to amend their policies and terms and conditions for applications and developers.

Our mobile games increasingly leverage the global connectivity and distribution of mobile platforms including Apple’s App Store for iOS devices and the Google Play Store for Android devices. Our games are distributed on these platforms and the virtual items we sell in our games are purchased using the payment processing systems of these platform providers. In 2022, 56.4% of our revenues were generated through third-party mobile platforms. We are subject to the standard policies and terms of service of these third party platforms, which govern the promotion, distribution and operation of games on the platform, and can be changed by the platform providers, in their sole discretion, at any time. Such changes may decrease the visibility or availability of our games, limit our distribution capabilities, prevent access to our existing games and reduce revenue we may recognize from in-game purchases, increase our costs to operate on these platforms or result in the exclusion or limitation of our games on such third party platforms. Any such changes could significantly harm our business in both the short-term and long-term. If we violate, or a platform provider believes we have violated, the terms of service for a platform, our access to the platform could be limited or discontinued, which may materially and adversely affect our business.

We also rely on the continued functionality of the Apple App Store and the Google Play Store. If our players or potential players are not able to access our games through these platforms or encounter difficulties in doing so, we may lose players, resulting in decreased revenue. The level of service provided by these storefronts may also impact users’ purchase and usage of and satisfaction with virtual goods or game money, and adversely affect our business and profitability. Further, in the past these digital storefronts have experienced interruptions in service or issues with their in-app purchasing functionality. If these types of interruptions were to occur regularly or on a prolonged basis, or other similar issues arise that impact our ability to generate revenues from these storefronts, our business, financial condition and results of operations may be materially and adversely affected.

Our investments in joint ventures or partnerships, or acquisitions of other companies, related to the development or service of online and mobile games may not be successful.

Since 2004, we have made investments in joint ventures and entered into partnership arrangements with third parties to invest in developing and/or servicing online and mobile games. In many cases, the success of such joint ventures and partnership arrangements is heavily dependent on third parties and their investment decisions because we do not have significant voting or other control over such entities.

Joint venture and partnership arrangements may involve risks not otherwise present in investments made solely by us, including:

•we may not control the joint ventures or our partners;

11

•where we do not have substantial decision-making authority, we may experience impasses or disputes with our joint venture partners on certain decisions, which could require us to expend additional resources to resolve such impasses or disputes, including litigation or arbitration;

•our joint venture partners may become insolvent or bankrupt, fail to fund their share of required capital contributions or fail to fulfil their obligations as a joint venture partner;

•the arrangements governing our joint ventures may contain certain conditions or milestone events that may never be satisfied or achieved;

•our joint venture partners may have business or economic interests that are inconsistent with ours and may take actions contrary to our interests;

•we may suffer losses as a result of actions taken by our joint venture partners with respect to our joint venture investments;

•it may be difficult for us to exit a joint venture if an impasse arises or if we desire to sell our interest for any reason; and

•we may make capital investments in our joint ventures or partnership arrangements, which may limit our ability to apply our resources to other endeavors that we find attractive, or decide not to participate in capital investments with our joint venture partners which may result in the dilution of our ownership and corresponding impact to our decision-making authority and share of future profits or losses.

Our failure to address these risks or resolve any deadlock situations arising out of disagreements with our partners or other problems encountered in connection with our existing or future joint ventures or partnerships could cause us to fail to realize the anticipated benefits of such joint ventures or partnerships and could adversely affect our business, financial condition, results of operations and prospects. In addition, we may, in certain circumstances, be liable for the actions of our joint venture partners or other partners.

If our partners or the joint ventures and partnerships in which we and our partners have invested or companies acquired by us are unable to manage their investments, develop promising online and/or mobile games or market or operate commercially successful online and/or mobile games, such joint ventures and partnerships or companies will be unable to attain their investment, development or other business objectives, which may materially and adversely affect the value of our investments and commitments and which may have a material adverse effect on our business, financial condition and results of operations.

We publish games developed by third parties, which exposes us to a number of potential operational, legal and reputational risks.

In 2022, we derived 77.2% of our revenues from online games and mobile games that were developed by third-party developers, 72.3% of which comprises revenues from mobile games developed by our former key third-party developer Dream Square (by itself and through subcontracting to certain third-parties, including X.D. Network Inc. ("Xindong") and Shanghai Rexue Network Technology Co., Ltd., with each of whom we now have a direct contractual relationship). Under our license agreements for these games, we rely on such third-party developers to provide game updates, enhancements and new versions; provide materials and other assistance in promoting the games; and resolve game programming errors and issues with intrusions. In particular, our key mobile game, Ragnarok M: Eternal Love, which represented 20.1% of our total revenues in 2022, was developed by Dream Square (by itself and through subcontracting to certain third-parties), as is the case of Ragnarok Origin and Ragnarok X: Next Generation, which represented 35.5% and 16.7%, respectively, of our total revenues in 2022.

Any failure of third-party developers to provide game updates, enhancements and new versions that are appealing to game players in a timely manner, and provide assistance that enables us to effectively promote the games, could adversely affect the game-playing experience of our game players, damage our reputation, or shorten the life-spans of those games, any of which could result in the loss of game players, acceleration of our amortization of the license fees we have paid for those games, or a decrease in our revenues from those games. Since July 2017, technical assistance with respect to certain of our games has been provided by Dream Square (by itself and through subcontracting to certain third-parties) pursuant to a publishing and technical support agreement (the “PTSA”), which expired in March 2021. See ITEM

12

4.A. “INFORMATION ON THE COMPANY – HISTORY AND DEVELOPMENT OF THE COMPANY.” We have no plans to renew or further extend the PTSA. Dream Square will continue to provide the service to any games developed by it which were launched prior to the expiration of the PTSA for an additional period of two years commencing on the date of such game’s commercialization, with an automatic one-year extension thereafter. We are in discussions with other prospective service partners regarding arrangements for these games following their current service terms. Any agreement with new publishing or technical service partners for our games could be at terms that are less favorable than those under the PTSA, and we cannot provide any assurance that any change in publishing or technical service partners will not impact our ability to effectively promote the games or the game-playing experience of our game players.

Publishing games developed by third parties also exposes us to a number of potential operational, legal and reputational risks. For example, we may be required to provide third party developers with upfront license fees or non-recoupable minimum guaranteed royalties in order to obtain the rights to publish their games, and we may incur significant marketing costs for these games before or after they have been commercially launched. We must often make such commitments and investments without knowing whether the games we are licensing or jointly developing will be successful and generate sufficient revenues to enable us to recoup our costs or for the games to be profitable. In addition, if any of the games created by third party developers with which we work infringe intellectual property owned by others, or otherwise violate any third party’s rights or any applicable laws and regulations, such as laws with respect to data collection and privacy, we would be exposed to potential legal risks by publishing these games, which could adversely affect our reputation and business. Further, should one of the companies with whom we do business become the subject of any negative attention, reports, publicity or media, our business and reputation may be harmed.

Our revenues fluctuate significantly and may adversely impact the trading price of our ADSs, or any other securities which become publicly traded. We also may not be able to sustain our recent rapid growth in revenue.

Our revenues and results of operations have varied significantly in the past and may continue to fluctuate in the future. Many of the factors that cause such fluctuation, such as competition, regulatory changes, and general economic conditions, are outside our control. In addition, usage of our online and mobile games typically increase slightly around holidays, including the Lunar New Year holidays and during winter and summer holidays for schools. Further, our recent significant growth in revenue may not be sustainable, as our mobile games business may not continue to grow at its current pace. Accordingly, you should not rely on year-to-year, or quarter-to-quarter, comparisons of our results of operations as an indication of our future performance. It is possible that future fluctuations may cause our results of operations to be below the expectations of market analysts and investors, and cause the trading price of our ADSs to decline.

If we fail to hire and retain skilled and experienced game developers or other key personnel to design and develop new online and mobile games and additional game features, we may be unable to achieve our business objectives.

In order to meet our business objectives and maintain our competitiveness, we need to attract and retain qualified employees, including skilled and experienced online and mobile game developers. We compete to attract and retain skilled and experienced personnel with other companies in the online and mobile game industries as well as in the broader entertainment, media and Internet industries, many of which offer superior compensation arrangements and career opportunities. In addition, our ability to train and integrate new employees into our operations may not meet the changing demands of our business. We cannot assure you that we will be able to attract and retain qualified game developers or other key personnel and successfully train and integrate them to achieve our business objectives, which could materially harm our business prospects.

Undetected programming errors or flaws in our games could harm our reputation or decrease market acceptance of our games, which would materially and adversely affect our business prospects, reputation, financial condition and results of operations.

Our current and future games may contain programming errors or flaws which may become apparent only after their release. In addition, our online and mobile games are developed using programs and engines developed by and licensed from third party vendors, which may include programming errors or flaws over which we have little or no control. If our users have negative experiences with our games related to or caused by undetected programming errors or flaws, they may be less inclined to use our games or recommend our games to other potential users.

While we have not experienced any material disruptions to our business from such errors or flaws in our games or in the programs and engines that we use to develop our games, these risks are inherent to our industry and, if realized, could severely harm our reputation, cause our users to cease playing our games, divert our resources, or delay market

13

acceptance of our games, any of which could materially and adversely affect our business, financial condition and results of operations.

Unexpected network interruptions, security breaches or computer virus attacks could harm our business and reputation.

Failure to maintain satisfactory performance, reliability, security and availability of our network infrastructure, whether maintained by us or by our licensees, may cause significant harm to our reputation and negatively impact our ability to attract and maintain users. Major risks relating to our network infrastructure include:

•any breakdowns or system failures, including from fire, flood, earthquake, hurricane or other natural disasters, power loss or telecommunications failure, resulting in a sustained shutdown of all or a material portion of our servers;

•any disruptions, failures or unscheduled service interruptions with data center hosting facilities managed by third party service providers, which may be due to unforeseen events that are beyond our control or the control of our third-party service providers;

•any disruption or failure in the national or international backbone telecommunications network, which would prevent users in certain countries in which our games are distributed from logging onto or playing our games for which the game servers are located in such countries; and

•any security breach caused by hacking, loss or corruption of data or malfunctions of software, hardware or other computer equipment and the inadvertent transmission of computer viruses.

“Hacking” involves efforts to gain unauthorized access to information or systems or to cause intentional malfunctions or loss or corruption of data, software, hardware or other computer equipment. Hackers, if successful, could misappropriate proprietary information or cause disruptions in our service. For example, in March and July 2021 and May and August 2022, we experienced a series of incidents where unauthorized users accessed or attempted to access our database or server, by exploiting remote code security vulnerabilities in order to, among others, cause illicit updates to be made to such users' player data on our database. In response, we took immediate remedial actions such as changing the password for the database, removing the malicious codes identified, and adopting a tool that enables the detection of abnormal queries. No personal information was compromised as a result of these incidents. We have taken steps to ensure these security vulnerabilities have been patched in our systems, but we cannot guarantee that all vulnerabilities have been patched in every system upon which we are dependent or that additional critical vulnerabilities will not be discovered by hackers in the future. While these past incidents have not materially disrupted or damaged our systems or platforms or the performance of our business, there is no assurance that we can anticipate all evolving future attacks, viruses or intrusions, implement adequate preventative measures, or remediate any security vulnerabilities. Any mitigation or remediation efforts we may have to undertake in the future in response to any such attacks may also require the attention of management and expenditures of significant capital and human resources, which can result in a significant financial impact on our operations and financial results. In addition, we cannot ensure that any measures we take against hacking will be effective. A well‑publicized computer security breach could significantly damage our reputation and materially and adversely affect our business.

We host our servers at third-party data centers located in the U.S., Indonesia, Korea, Taiwan and Thailand. Given that we lease these data center spaces from third-party data center providers, we do not control the operations of these third-party facilities. Consequently, we have been, and may continue to be, subject to service disruptions, failures, unscheduled service interruptions or failures to provide adequate support for reasons which are beyond our control or the control of our third party service providers. All of our data center facilities and network infrastructure are vulnerable to damage or interruption from a variety of sources including earthquakes, floods, fires, power loss, system failure, computer vulnerabilities, physical or electronic break-ins, human errors, malfeasance or interference, including by employees, former employees, or contractors, terrorism and other catastrophic events. For example, on December 2, 2021, a fire broke out at our third-party data center hosting facility in Indonesia, IDC Indonesia, which services PT Gravity Game Link (“Gravity Game Link”), our 70%‑owned subsidiary in Indonesia. Although basic network infrastructure such as web servers, mails and virtual private networks (VPN) was restored within 48 hours, and all other services including download servers were restored on the third day after the fire, we experienced a temporary disruption in our services during this period due to continued outages. While all our data and servers were fully restored after the incident, and this incident did not result in a material adverse impact on our operating results, there can be no assurance that any such incidents which could cause an interruption in our services will not occur again. The disaster recovery arrangements and data redundancy plans of our

14

Company and our third party service providers may not be adequate to account for disasters or similar events that may occur in the future and may not effectively permit us to continue operating in the event of any problems with respect to our systems or those of our third-party data centers or any other third-party facilities. If any such event were to occur to our business, our operations could be impaired and our business, financial condition, and results of operations may be materially and adversely affected.

We have been, may continue to be, subject to denial of service attacks that have caused, and could cause, portions of our network to be inaccessible for limited periods of time. For example, in March 2022, we experienced a distributed denial of service (“DDOS”) attack on the Amazon Web Services cloud platform, which we use for the Ragnarok Online service in Malaysia, Singapore and the Philippines. While this attack caused our service to be unstable intermittently for a period of two weeks, we were able to mitigate the attack by subscribing to AWS Shield, a DDOS protection service, and taking preventive measures. In September 2022, another DDOS attack occurred on the network of IDC Korea, our third party data center hosting facility in Korea, resulting in the server becoming inaccessible. We restored access to the server within 24 hours and took remedial actions including changing the Canonical NAME (CNAME) record in the Domain Name System (DNS) and adopting Cloudflare's solution. Although the attacks we have experienced did not cause material losses or damages, we cannot ensure that any protective measures we have implemented, including those by our third party service providers, will be adequate or effective against future hacking efforts and that any such attacks in the future will not have a material adverse effect on our business, results of operations, financial condition, or prospects.

In addition, computer viruses may cause delays or other service interruptions on our systems and expose us to a material risk of loss or litigation and possible liability. We may be required to expend significant capital and other resources to protect our Web sites against the threat of such computer viruses and to address and resolve any problems resulting from such viruses. Moreover, if a computer virus affecting our system is highly publicized, our reputation could be materially damaged and our visitor traffic may decrease.

Any of the foregoing factors could reduce our users’ satisfaction, harm our business and reputation and have a material adverse effect on our business, financial condition and, results of operations.

Failure to protect personal information could adversely affect our business, reputation and results of operations.

We collect, process, store and transmit personal information of game users worldwide for our global game service. Our business may be subject to a number of federal, state, local and foreign laws and regulations governing data privacy and security, including with respect to the collection, processing, storage, use, transmission and protection of personal information and other consumer data on the Internet and mobile platforms, the scope of which are continually changing and subject to differing interpretations, and which may be inconsistent among countries or otherwise in conflict with other laws or regulations. These obligations may be interpreted and applied in a manner that is inconsistent from one jurisdiction to another and may conflict with other laws or regulations or our practices. Also, the failure to prevent or mitigate the loss of personal information data or other game user data, including as a result of breaches of our vendors’ technologies and systems, could expose us or our game users to a risk of loss or misuse of such information. Any such failure or perceived failure by us to comply with our privacy policies, our privacy-related obligations to players or other third parties, or our privacy-related legal obligations, including without limitation any compromise of security that results in the unauthorized release or transfer of personally identifiable information or other player data, may result in governmental enforcement actions, litigation or public statements against us by consumer advocacy groups or others and could cause our players to lose trust in us, which may have an adverse effect on our business, reputation and results of operations. See ITEM 4.B. “BUSINESS OVERVIEW—LAWS AND REGULATIONS” for a detailed discussion regarding laws of Thailand, Taiwan, Korea, Japan, the United States and the Philippines that may materially impact our operations.

Further, we may not be able to adequately adapt our internal policies and/or procedures to evolving regulations, which may require us to change our practices in a manner adverse to our business or limit access to our products and services in certain countries. As a result, our reputation and brand may be harmed, we could incur substantial costs, and we could lose both customers and revenues. For example, the European General Data Protection Regulation (“GDPR”), which became effective as of May 2018, contains significant penalties for non-compliance and apply to us as we receive or process the personal data of residents of the European Union. If we fail to comply with such GDPR regulations, or other data protection laws and regulations globally, we may be subject to significant penalties and sanctions which may have a material adverse effect on our business, financial condition and results of operations.

15

Electronic embezzlement could negatively impact the popularity of our online and mobile games and adversely affect our reputation and results of operations.

Some of our employees or licensees’ employees with high‑level security access to our network, or other employees or persons who hack into or otherwise gain unauthorized access to certain sectors of our network, may succeed in breaching internal security systems and engage in electronic embezzlement by creating or diverting game money used in our online and mobile games and publicly or privately selling the game money for their financial benefit. We and our overseas licensees may not be successful in preventing electronic embezzlement. Incidents of electronic embezzlement may negatively impact the reputation of our games, which may materially and adversely affect our business, financial condition and results of operations.

Cheating by users of online and mobile games could negatively impact the popularity of our online and mobile games and adversely affect our reputation and results of operations.

We have experienced numerous incidents where users were able to modify the published rules of our online and mobile games. Users were able to modify the rules of our online and mobile games during game play in a manner that allowed them to cheat and disadvantage other online game users. For example, users have utilized auto‑run programs that enabled games to be continuously and automatically played without user participation to quickly accumulate in‑game points, causing many other players to stop using the game and shortening the game’s life cycle. For mobile games, some users have purchased game money or in‑game items through cloned mobile phones and sold such illegally obtained property to other users, which resulted in a shortfall between total sales and our actual revenues. Such unauthorized manipulation of our games may negatively impact users’ perception of our games and damage our reputation as well as our results of operations. We or our licensees may not be successful in taking the corrective measures necessary to prevent users from modifying the terms of our games in a timely manner.

Unauthorized use of our intellectual property rights by third parties and the expenses incurred in protecting our intellectual property rights may adversely affect our business.

Our intellectual property rights such as copyrights, service marks, trademarks and trade secrets are critical to our business. Unauthorized use of the intellectual property rights used in our business, whether owned by us or licensed to us, may materially and adversely affect our business and reputation. We rely on trademark and copyright law, trade secret protection and confidentiality agreements with our employees, customers, business partners, and others to protect our intellectual property rights. It may be possible for third parties to obtain and use our intellectual property without authorization.

Since the commercialization of Ragnarok Online in August 2002, we have discovered that the server‑end software of Ragnarok Online has been unlawfully released on a consistent basis in most of the countries and markets in which Ragnarok Online has been offered. This enables unauthorized parties to set up local server networks to operate Ragnarok Online, which may result in the diversion of a significant number of paying users. We designate certain employees to be responsible for detecting such illegal servers. In Korea, we report offenders to the relevant enforcement authority for possible prosecution relating to crimes on the Internet. In markets outside of Korea, we cooperate with and rely on our licensees to seek enforcement actions against operators of illegal servers. For example, in December 2007 and June 2008, Gravity Interactive, Inc. (“Gravity Interactive”), our wholly owned subsidiary in the United States which manages Ragnarok Online game operations in the United States, petitioned the Federal Bureau of Investigation for remission or mitigation of forfeiture of the property of two illegal server operators of Ragnarok Online, which property was deemed proceeds of copyright infringement violations by the illegal server operators, and US$ 154,674.73 was returned to Gravity Interactive, Inc. in April 2011. We may incur considerable costs in the future in order to remedy software piracy of our server software and enforce our rights against the operators of unauthorized server networks.

The validity, enforceability, enforcement mechanisms and scope of protection of intellectual property in Internet‑related industries are uncertain and evolving. In particular, the laws and enforcement regimes of Korea, Japan, Taiwan, the Philippines, China, Thailand and certain other countries in which our games are distributed are uncertain or may not protect intellectual property rights to the same extent as do the laws and enforcement procedures of the United States. Moreover, litigation may be necessary in the future to enforce our intellectual property rights. Such litigation could result in substantial costs and diversion of our resources, disruption of our business, and have a material adverse effect on our business, prospects, financial condition and results of operations.

16

We may be subject to claims with respect to the infringement of intellectual property rights of others, which could result in substantial costs and diversion of our financial and management resources.

We cannot be certain that our online and mobile games do not or will not infringe upon patents, copyrights or other intellectual property rights held by third parties. We have in the past been and may in the future become subject to legal proceedings and claims from time to time relating to the intellectual property of other parties. For Example, in November 2010, Gravity Interactive, which manages Dragonica game operations under the name Dragon Saga in the United States and Canada, THQ*ICE LLC, the former game distributor of Dragonica in the United States and Canada, and THQ Inc., the former joint venture partner of THQ*ICE LLC, were accused of trademark infringement. The owner of the registered trademark of Dragonica in the United States filed a lawsuit with the United States District Court for the Southern District of Florida seeking damages and any profits and gains to the defendants through the alleged trademark infringement. The lawsuit was settled in March 2012. If we are found to have violated the intellectual property rights of other parties, we may be enjoined from using such intellectual property rights, be required to pay penalties and fines and pay for the unauthorized use of such intellectual property, and may need to incur additional license fees or be forced to develop alternative technology or obtain other licenses. We may incur substantial expenses in defending against these third party infringement claims, regardless of their merit. In addition, certain of our employees were recruited from other online and mobile game developers, including current and potential competitors. To the extent these employees have been and are involved in the development of our games that are similar to the games they helped develop at their former employers, we may become subject to claims that we or such employees have improperly used or disclosed trade secrets or other proprietary information. Although we are not aware of any pending or threatened claims of this type, if any such claims were to arise in the future, litigation or other dispute resolution procedures might be necessary to retain our ability to offer our current and future games, which could result in substantial costs and diversion of our financial and management resources.

Successful infringement or licensing claims against us may result in substantial monetary damages, which may materially disrupt our business operations and have a material adverse effect on our reputation, business, financial condition and results of operations.

Our products and services, including those involving play-to-earn ("P2E") features and non-fungible tokens ("NFT"), may subject us to additional regulatory requirements in the future, which may be costly and difficult to comply with or adversely affect our business, and other potential risks to our business.

We currently offer the market NFT Item created using our game contents, and will continue to develop and launch games integrated with P2E and NFT elements. For example, users of the Sand Box can purchase certain virtual items as NFTs, using Ragnarok Online IP, on the Sandbox Platform, which they can in turn use in their virtual land. And the P2E game we are developing allows users to earn rewards through game play which can be exchanged for certain types of cryptocurrency trading on cryptocurrency exchanges. We may become subject to regulatory requirements in the future in Korea and other countries for providing such products and services.

Governments of different countries have responded differently to cryptoassets (including cryptocurrency and NFTs). Governments of various countries may adopt laws, regulations, or policies that could adversely affect P2E or NFT by restricting rights to acquire, own, hold, sell, use or trade cryptoassets or to exchange them for fiat currency. In addition, there is significant uncertainty regarding the tax treatment of cryptoassets. We cannot rule out the possibility that such restrictions and uncertainties could have a material adverse effect on our ability to pursue P2E, NFT and/or adjacent business, financial condition, and the results of operations.

Furthermore, our P2E and NFT related businesses may be subject to cybersecurity risks. We cannot rule out the possibility that such risks become materialized affecting our business, financial condition, and the results of operations.

We may not be able to successfully implement our growth and profit improvement strategies.

We are pursuing a number of growth and profit improvement strategies, including the following:

•distributing games developed in‑house;

•publishing games acquired from or developed by third parties through licensing arrangements;

•intellectual property licensing to or from third parties for game development;

•offering our games in countries where such games have not yet been launched;

17

•optimizing our marketing and research and development expenditures;

•cross‑selling our popular online games through other lines of businesses, such as mobile games, console games, animation and character merchandising;

•pursuing strategic relationships with game development and service companies; and

•strengthening localized services through the establishment of local subsidiaries in our major markets.

We cannot assure you that we will be successful in implementing any of these strategies. Certain of our strategies relate to new services or products for which there are no established markets, or in which we lack experience and expertise. If we are unable to successfully implement our growth and profit improvement strategies, our revenues, profitability, and competitiveness may be materially and adversely affected.

We have limited business insurance coverage, and business interruption could have a material adverse effect on our business.

While we carry insurance coverage against certain risks to our property and assets, such as fire, flood and earthquake, as well as directors’ and officers’ liability insurance, we do not separately maintain casualty and liability insurance against litigation, risks or disruptions related to our business. The occurrence of any natural disaster, fire, power loss, telecommunications failure, break‑ins, sabotage, computer viruses, intentional acts of Internet vandalism, human error or other similar events may damage our facilities or network servers and disrupt the operation of our business. As we do not carry sufficient natural disaster or business interruption insurance to compensate us for all types or amounts of loss that could arise, any damage or disruption from such events might result in our incurring substantial costs and the diversion of our resources, and have a material adverse effect on our business, financial condition and results of operations. See ITEM 4.B. “BUSINESS OVERVIEW—INSURANCE.”

As we introduce new games, we face the risk that a significant number of users of our existing games may migrate to our new games.

We expect that as we introduce new games, a certain number of our existing users may migrate from our existing games to the new games, which may lead to a decrease in the player base of our existing games and in turn make those existing games less playable to other game players, resulting in decreased revenues from our existing games. Players of our existing games may also spend less money to purchase in‑game items in our new games than they would have spent if they had continued playing our existing games. In addition, our game players may migrate from our existing games with a higher profit margin to new games with a lower profit margin. If any of the forgoing occurs, our revenues and profitability are likely to be materially and adversely affected.

New or changed game features in our online games may not be well received by our game players.

In the course of launching and operating online games, including the release of updates and expansion packs to existing games, certain game features may periodically be introduced, changed or removed. We cannot assure you that the introduction, change or removal of any game feature will be well received by our game players, who may decide to reduce or eliminate their playing time in response to any such introduction, change or removal. As a result, any introduction, change or removal of game features may adversely impact our business, financial condition and results of operations.

We believe that we were a PFIC for taxable years 2008 through 2016 and 2022, and we may be a PFIC in future years. As a result of being a PFIC in 2022 and prior years, and because of the possibility that we may have been a PFIC for taxable years 2017 through 2021, and may be a PFIC in future taxable years, U.S. investors could be subject to adverse U.S. federal income tax consequences.

The rules governing PFICs can have adverse consequences for U.S. investors for U.S. federal income tax purposes. The tests for determining PFIC status for a taxable year depend upon the relative values of certain categories of assets and the relative amounts of certain kinds of income. As discussed in ITEM 10.E. “TAXATION—MATERIAL U.S. FEDERAL INCOME TAX CONSIDERATIONS,” we believe that we were a PFIC for the taxable year 2022 and for taxable years 2008 through 2016 (though we believe we may not have been a PFIC for taxable years 2017 through 2021), and we may be a PFIC in future years. The determination of whether we are a PFIC must be made annually after the end of each taxable year, and our PFIC status for each taxable year will depend on particular facts and circumstances (such as the

18

composition of our income and assets, and the valuation of our assets, including goodwill and other intangible assets, which may be determined by reference to the market price of our ADSs, which has fluctuated and may continue to fluctuate significantly over time) and may be affected by differing interpretations of the PFIC rules. In light of the foregoing, no assurance can be provided that we were not a PFIC for the taxable years 2017 through 2021 or that we will not become a PFIC in the current year or any future taxable year. In addition, our U.S. counsel expresses no opinion with respect to our PFIC status for our past, current or future taxable years. Furthermore, if we are treated as a PFIC, and one or more of our subsidiaries are also treated as PFICs, U.S. Holders will be subject to the PFIC rules with respect to their indirect interests in those subsidiaries. Accordingly, U.S. Holders should invest in our ADSs only if they are willing to bear the U.S. federal income tax consequences associated with investments in PFICs.

If we were characterized as a PFIC for any taxable year, and a U.S. Holder (as defined in ITEM 10.E. “TAXATION—MATERIAL U.S. FEDERAL INCOME TAX CONSIDERATIONS.”) held our ADSs or common shares during such taxable year, we generally will continue to be treated as a PFIC with respect to that U.S. Holder for all succeeding taxable years during which the U.S. Holder holds ADSs or common shares, even if we cease to meet the requirements for PFIC status. In such case, U.S. Holders of our common shares and ADSs would be subject to adverse U.S. federal income tax consequences, such as ineligibility for any preferential tax rates on capital gains or on actual or deemed dividends, interest charges on certain taxes treated as deferred, and additional reporting requirements under U.S. federal income tax laws and regulations. Whether U.S. Holders of our common shares or ADSs make (or are eligible to make) a timely qualified electing fund, or QEF, election or a mark-to-market election may affect the U.S. federal income tax consequences to U.S. Holders with respect to the acquisition, ownership, and disposition of our common shares and ADSs and any distributions such U.S. Holders may receive. We do not, however, expect to provide the information regarding our income that would be necessary in order for a U.S. Holder to make a QEF election if we are classified as a PFIC. Investors should consult their own tax advisors regarding all aspects of the application of the PFIC rules to our common shares and ADSs.

Rapid technological developments and changes in market environment may limit our ability to recover game development costs and adversely affect our financial condition and results of operations due to impairment loss.

The online and mobile game industries are subject to rapid technological developments and changes in market environment, which could render our online and mobile games under development and commercialized games obsolete or unattractive to users. Any resulting failure to recover capitalized development costs and the recognition of impairment loss for such costs may materially and adversely affect our financial condition and results of operations.

We could suffer losses due to asset impairment charges.