UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21681

Guggenheim Enhanced Equity Income Fund

(Exact name of registrant as specified in charter)

2455 Corporate West Drive, Lisle, IL 60532

(Address of principal executive offices) (Zip code)

Amy J. Lee

2455 Corporate West Drive, Lisle, IL 60532

(Name and address of agent for service)

Registrant's telephone number, including area code: (630) 505-3700

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

Item 1. Reports to Stockholders.

The registrant's annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”) is as follows:

WWW.GUGGENHEIMINVESTMENTS.COM/GPM

... YOUR LINK TO THE LATEST, MOST UP-TO-DATE INFORMATION ABOUT THE GUGGENHEIM ENHANCED EQUITY INCOME FUND

The shareholder report you are reading right now is just the beginning of the story. Online at www.guggenheiminvestments.com/gpm, you will find:

|

●

|

Daily, weekly and monthly data on share prices, distributions and more

|

|

●

|

Portfolio overviews and performance analyses

|

|

●

|

Announcements, press releases and special notices

|

|

●

|

Fund and adviser contact information

|

Guggenheim Partners Investment Management, LLC and Guggenheim Funds Investment Advisors, LLC are constantly updating and expanding shareholder information services on the Fund’s website, in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed, and the results of our efforts. It is just one more small way we are working to keep you better informed about your investment in the Fund.

| December 31, 2012 |

DEAR SHAREHOLDER

We thank you for your investment in the Guggenheim Enhanced Equity Income Fund (the “Fund”). This report covers the Fund’s performance for the fiscal year ended December 31, 2012.

The Fund’s primary investment objective is to seek a high level of current income and gains with a secondary objective of long-term capital appreciation.

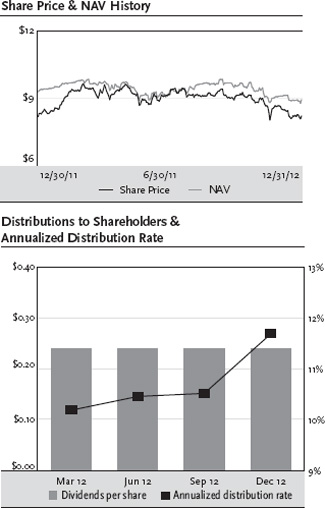

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the 12 months ended December 31, 2012, the Fund provided a total return based on market price of 11.52% and a total return based on NAV of 6.60%. On December 31, 2012, the Fund’s last closing market price of $8.20 per share represented a discount of 8.17% to its NAV of $8.93 per share. As of June 30, 2012, the Fund’s market price of $9.16 per share represented a discount of 1.93% to its NAV of $9.34 per share. Past performance does not guarantee future results. The market price of the Fund’s shares fluctuates from time to time, and it may be higher or lower than the Fund’s NAV.

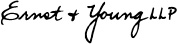

The Fund has paid a distribution of $0.24 each quarter since June 2009. The most recent dividend represents an annualized distribution rate of 11.71% based on the Fund’s closing market price of $8.20 as of December 31, 2012.

Guggenheim Funds Investment Advisors, LLC (“GFIA” or the “Adviser”) serves as the investment adviser to the Fund. Guggenheim Partners Investment Management, LLC (“GPIM” or the “Sub-Adviser”) serves as the Fund’s investment sub-adviser and is responsible for the management of the Fund’s portfolio of investments. Each of the Adviser and the Sub-Adviser is an affiliate of Guggenheim Partners, LLC (“Guggenheim”), a global diversified financial services firm.

GPIM seeks to achieve the Fund’s investment objective by obtaining broadly diversified exposure to the equity markets, currently through a portfolio of exchange-traded funds (“ETFs”), and utilizing a covered call strategy which follows GPIM’s proprietary dynamic rules-based methodology. The Fund seeks to earn income and gains through underlying equity security performance, dividends paid on securities owned by the Fund, and cash premiums received from selling (writing) covered call options.

In connection with the implementation of GPIM’s strategy, the Fund utilizes financial leverage. The goal of the use of financial leverage is to enhance shareholder value, consistent with the Fund’s investment objective, and provide superior risk-adjusted returns. The Fund’s use of financial leverage is intended to be flexible in nature and is monitored and adjusted, as appropriate, on an ongoing basis by GFIA and GPIM. The Fund may utilize financial leverage up to the limits imposed by the Investment Company Act of 1940 (the “1940 Act”), as amended. Under current market conditions, the Fund intends to utilize financial leverage in an amount not to exceed 30% of the Fund’s total assets (including the proceeds of such financial leverage) at the time utilized. The Fund employs financial leverage through a line of credit with a major European bank. As of December 31, 2012, the amount of leverage was approximately 27% of the Fund’s total assets.

We encourage shareholders to consider the opportunity to reinvest their distributions from the Fund through the Dividend Reinvestment Plan (“DRIP”), which is described in detail on page 24 of this report. When shares trade at a discount to NAV, the DRIP takes advantage of the discount by reinvesting the quarterly dividend distribution in common shares of the Fund purchased in the market at a price less than NAV. Conversely, when the market price of the Fund’s common shares is at a premium above NAV, the DRIP reinvests participants’ dividends in newly-issued common shares at NAV, subject to an Internal Revenue Service (“IRS”) limitation that the purchase price cannot be more than 5% below the market price per share. The DRIP provides a cost-effective means to accumulate additional shares and enjoy the potential benefits of compounding returns over time.

|

GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT | 3

|

|

DEAR SHAREHOLDER continued

|

December 31, 2012

|

To learn more about the Fund’s performance and investment strategy for the 12 months ended December 31, 2012, we encourage you to read the Questions & Answers section of the report, which begins on page 5.

We appreciate your investment and look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Fund’s website at www.guggenheiminvestments.com/gpm.

Sincerely,

Donald C. Cacciapaglia

Chief Executive Officer

Guggenheim Enhanced Equity Income Fund

January 31, 2013

|

4 | GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

|

|

QUESTIONS & ANSWERS

|

December 31, 2012

|

The Guggenheim Enhanced Equity Income Fund (the “Fund”) is managed by a team of seasoned professionals at Guggenheim Partners Investment Management, LLC (“GPIM” or the “Sub-Adviser”). This team includes B. Scott Minerd, Chief Investment Officer; Anne Bookwalter Walsh, CFA, JD, Assistant Chief Investment Officer; Farhan Sharaff, Assistant Chief Investment Officer, Equities; Jayson Flowers, Senior Managing Director; and Jamal Pesaran, Portfolio Manager. In the following interview, the investment team discusses the market environment and the Fund’s performance for the annual period ended December 31, 2012.

Please describe the Fund’s investment objective and explain how GPIM’s investment strategy seeks to achieve it.

The Fund’s investment objective is to seek a high level of current income and gains with a secondary objective of long-term capital appreciation. Under normal market conditions, the Fund invests at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in equity securities.

GPIM seeks to achieve the Fund’s investment objective by obtaining broadly diversified exposure to the equity markets and utilizing a covered call strategy developed by GPIM. The Fund may seek to obtain exposure to equity markets through investments in exchange-traded funds or other investment funds that track equity market indices, through investments in individual equity securities and/or through derivative instruments that replicate the economic characteristics of exposure to equity securities or markets. The Fund has the ability to write call options on indices and/or securities, which will typically be at or out of the money. GPIM’s strategy typically targets one-month options, although options of any strike price or maturity may be utilized.

The Fund seeks to earn income and gains through underlying equity security performance, dividends paid on securities owned by the Fund, and cash premiums received from selling (writing) covered call options. Although the Fund will receive premiums from the options written, by writing a covered call option, the Fund forgoes any potential increase in value of the underlying securities above the strike price specified in an option contract through the expiration date of the option. To the extent GPIM’s strategy seeks to achieve broad equity exposure through a portfolio of common stocks, the Fund would hold a diversified portfolio of stocks. To the extent GPIM’s equity exposure strategy is implemented through investment in broad-based equity exchange-traded funds or other investment funds or instruments, the Fund’s portfolio may comprise fewer holdings. At present, the Fund obtains exposure to equity markets by investing primarily in a portfolio of exchange-traded funds.

As part of GPIM’s strategy, the Fund is currently using financial leverage. The goal of financial leverage is to enhance shareholder value, consistent with the Fund’s investment objective, and provide superior risk-adjusted returns. The Fund may utilize financial leverage up to the limits imposed by the 1940 Act. The Fund’s use of financial leverage is intended to be flexible in nature and is monitored and adjusted, as appropriate, on an ongoing basis by Guggenheim Funds Investment Advisers, LLC (“GFIA”) and GPIM. Under current market conditions, the Fund intends to utilize financial leverage in an amount not to exceed 30% of the Fund’s total assets (including the proceeds of such financial leverage) at the time utilized. The Fund employs financial leverage through a line of credit with a major European bank. Use of financial leverage creates an opportunity for increased income and capital appreciation but, at the same time, creates special risks. There can be no assurance that a leveraging strategy will be successful. Financial leverage may cause greater changes in the Fund’s net asset value and returns than if leverage had not been used.

Please provide an overview of the economic and market environment during 2012.

The U.S. economy continues its positive expansion, although the risks of delinquencies, diminished consumer demand, and the knock-on effect of Europe continue to weigh on the market. Unprecedented policy actions by the Federal Reserve (“the Fed”) continue to provide ample liquidity and accommodation to stimulate growth of the U.S. economy. Recent Fed action, such as the third round of quantitative easing announced in September 2012, shows an increased tolerance for potentially higher levels of inflation. The Fed was aggressive in its policy action by announcing an open-ended bond purchasing program that focused on agency mortgages. Operation Twist, the Fed’s program of buying longer duration Treasury securities while simultaneously selling shorter duration securities, was also extended.

The underlying thesis over the past few months still holds true—that the U.S. economy has shown resiliency through the many headwinds which it has faced, and that better-than-expected growth is anticipated in 2013. State and local governments are starting to be net contributors to employment. The economy is also experiencing the start of the recovery in the housing market, which is supportive of economic growth. While economic conditions in the U.S. are expected to improve throughout 2013, it will be some time before the unemployment rate falls below an acceptable level for policymakers. Furthermore, inflationary pressures will likely stay muted, as history has shown, there will not be a secular rise in inflation until capacity utilization rises to a level far higher than where it is currently.

Central banks around the world have tagged along with U.S. policymakers and are engaging in their own forms of accommodative policy actions, which should continue to benefit risk assets and assets linked to inflation. While the European Central Bank has made considerable strides to reduce stress emanating from troubled eurozone nations, it is evident that restructuring of toxic debt will take considerable time and effort. The

|

GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT | 5

|

|

QUESTIONS & ANSWERS continued

|

December 31, 2012

|

eurozone currency still remains at a relatively high value compared to the U.S. dollar, which makes European countries less competitive with respect to exports. Despite all of these headwinds, the U.S. economy appears to have the momentum, albeit at a slow pace, to withstand an imminent European recession. In China, it appears that we are past the bottom in economic growth, and there are signs that things are turning positive. Industrial production, stock prices, even real estate prices are beginning to rise. The positive news for China could also be good news for the emerging markets.

The over-all environment for the period was one of falling volatility and a market that trended significantly higher. For the 12-month period ended December 31, 2012, return of the Standard & Poor’s 500 Index (the “S&P 500”), which is generally regarded as an indicator of the broad U.S. stock market, was 16.00%. The “VIX,” which is the ticker symbol for the Chicago Board Options Exchange Market Volatility Index, a measure of the implied volatility of S&P 500 options, fell about 25%. It represents a measure of the market’s expectation of stock market volatility over the next 30-day period. Quoted in percentage points, the VIX represents the expected daily movement in the S&P 500 over the next 30-day period, which is then annualized.

How did the Fund perform for the full year of 2012?

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the 12 months ended December 31, 2012, the Fund provided a total return based on market price of 11.52% and a total return net of fees based on NAV of 6.60%. Past performance does not guarantee future results.

In comparison, the return of the S&P 500 was 16.00% for the 12 months ended December 31, 2012, and the return of CBOE S&P 500 BuyWrite Index (“BXM”), the covered call benchmark, was 5.20%. The BXM is a benchmark index designed to show the hypothetical performance of a portfolio that purchases all the constituents of the S&P 500 and then sells at-the-money (meaning same as purchase price) calls of one-month duration against those positions.

The discount of the Fund narrowed over the entire year, but has widened since June 30, 2012. On December 31, 2011, the Fund’s market price of $8.16 per share represented a discount of 11.97% to its NAV of $9.27 per share. One year later, on December 31, 2012, the Fund’s last closing market price of $8.20 per share represented a discount of 8.17% to its NAV of $8.93 per share. The Fund traded at a premium to NAV on several days in June and early July, and on June 30, 2012, the Fund’s market price of $9.16 per share represented a discount of 1.93% to its NAV of $9.34 per share. The market price of the Fund’s shares fluctuates from time to time, and it may be higher or lower than the Fund’s NAV.

GPIM believes the narrowing of the discount over the course of 2012 may reflect investors’ improving understanding of the Fund’s investment strategy, which seeks to provide long-term returns similar to the S&P 500, while seeking higher income and risk similar to the S&P 500. Risk is generally measured by the standard deviation of returns, which was 11.4% for the Fund during 2012, compared with 12.8% for the S&P 500.

The widening of the discount of shares to NAV toward year-end may have been due to the general wariness of dividend-paying investments at a time when increased taxes on dividends was being considered as part of the U.S. fiscal cliff negotiations.

The Fund has paid a distribution of $0.24 each quarter since June 2009. The most recent dividend represents an annualized distribution rate of 11.71% based on the Fund’s closing market price of $8.20 as of December 31, 2012.

What investment decisions had the greatest effect on the Fund’s performance?

The year was highlighted by a number of extreme market moves and low realized volatility, which presented a difficult combination for a strategy like GPM, which collects premiums from selling covered calls in anticipation of a near-term market move. Volatility, as measured by the VIX, generally fell over the course of the year, starting around 24% and remaining in the range of 13%-15% for most of the year before ending around 18%. The Fund’s underperformance stemmed from the inherent nature of the strategy, which through selling covered calls caps its upside, and not being compensated for the risk the Fund took in selling the calls.

To give an example of the whipsaw nature of the market, the S&P 500 rose about 8% over January options expiry, extending the move in February, higher by 3.5%, and then 3.2% in March. After a quiet April, the market fell 6% in May expiry, before continuing with a 3.7% rise in June and 4.1% rise in August. At year end the whipsaw continued with a 5.1% drop during November expiry followed by a rise of 5.2% in December. Implied volatility did not materialize after these moves higher or other moves lower, such as in May and November. We attribute this disconnect between market moves and volatility to the massive liquidity injections by the U.S. Federal Reserve as well as other major central banks.

Of the three factors affecting Fund performance—security selection, strike price of options written and leverage—security selection was a detractor to return. In security selection, a strategy using anything other than the S&P 500 in pursuing its strategy in 2012 fell short, since the S&P 500 was the

|

6 | GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

|

|

QUESTIONS & ANSWERS continued

|

December 31, 2012

|

best-performing broad measure of the equity market. Our portfolio tends to be composed of a more broad set of U.S. equity index exposures.

Much of the performance of the S&P 500 was largely a result of the impact of the mega-cap rally in 2012 and the return of one of the largest stocks, Apple, Inc. It was up about 40% for the first half of the year, before it began a reversal in the third quarter that brought its gain to about 33% for the year.

Underlying call exposures were also detractors from performance, given the drop-off in implied volatility and slow realized moves. Leverage contributed to performance for the period, which is generally the case during rising markets.

The degree of leverage employed is determined based on analysis of the securities in the portfolio and the strike price selected. In general, leverage is lower when the strike price is higher, and higher when the strike price is close to the price of the underlying security. The impact of this strategy is that the Fund has more leverage when GPIM believes volatility is most attractive. Leverage is generally maintained between 20% and 30% of the Fund’s total assets.

The quantitative easing from the world’s central banks did not cause us to dramatically change how we manage the strategy, but from time to time we did seek to improve performance by selling covered calls at a higher strike price and reducing leverage, which we typically do in a period of low implied volatility. Leverage was slightly lower at the end of 2012 compared with earlier in the year (27% of the Fund’s total assets on December 31, 2012, compared with 28% on June 30, 2012).

Index Definitions

Indices are unmanaged, reflect no expenses and it is not possible to invest directly in an index.

The S&P 500 is an unmanaged, capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Chicago Board Options Exchange Market Volatility Index, often referred to as the VIX (its ticker symbol), the fear index or the fear gauge, is a measure of the implied volatility of S&P 500 options. It represents a measure of the market’s expectation of stock market volatility over the next 30 day period. Quoted in percentage points, the VIX represents the expected daily movement in the S&P 500 over the next 30-day period, which is then annualized.

The CBOE S&P 500 BuyWrite Index (BXM) is a benchmark index designed to show the hypothetical performance of a portfolio that purchases all the constituents of the S&P 500 and then sells at-the-money (meaning same as purchase price) calls of one-month duration against those positions.

Risks and Other Considerations

The views expressed in this report reflect those of the portfolio managers only through the report period as stated on the cover. These views are subject to change at any time, based on market and other conditions and should not be construed as a recommendation of any kind. The material may also include forward looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass. There can be no assurance that the Fund will achieve its investment objectives. The value of the Fund will fluctuate with the value of the underlying securities. Historically, closed-end funds often trade at a discount to their net asset value. Risk is inherent in all investing, including the loss of your entire principal. Therefore, before investing you should consider the following risks carefully.

Equity Securities and Related Market Risk. The market price of common stocks and other equity securities (including ETFs) may go up or down, sometimes rapidly or unpredictably. Equity securities may decline in value due to factors affecting equity securities markets generally, particular industries represented in those markets or the issuer itself. The values of equity securities may decline due to general market conditions which are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment generally. They may also decline due to factors which affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. The value of equity securities may also decline for a number of other reasons which directly relate to the issuer, such as management performance, financial leverage, the issuer’s historical

|

GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT | 7

|

|

QUESTIONS & ANSWERS continued

|

December 31, 2012

|

and prospective earnings, the value of its assets and reduced demand for its goods and services. Equity securities generally have greater price volatility than bonds and other debt securities.

Other Investment Companies Risk. The Fund may invest in securities of other open- or closed-end investment companies, including ETFs. As a stockholder in an investment company, the Fund will bear its ratable share of that investment company’s expenses, and would remain subject to payment of the Fund’s investment management fees with respect to the assets so invested. Shareholders would therefore be subject to duplicative expenses to the extent the Fund invests in other investment companies. In addition, these other investment companies may utilize financial leverage, in which case an investment would subject the Fund to additional risks associated with leverage.

The Fund may invest in “leveraged” and/or “inverse” ETFs which seek returns equal to a specified multiple of the underlying index returns for a given day. These ETFs may be more volatile and subject to greater risk than traditional ETFs. However, the longer-term returns of “leveraged” or “inverse” ETFs may have little correlation to the returns of the underlying index.

Options Risk. There are various risks associated with the Fund’s covered call option strategy. The purchaser of an index option written by the Fund has the right to any appreciation in the cash value of the index over the strike price on the expiration date. Therefore, as the writer of an index call option, the Fund forgoes the opportunity to profit from increases in the index over the strike price of the option. However, the Fund has retained the risk of loss (net of premiums received) should the price of the Fund’s portfolio securities decline. Similarly, as the writer of a call option on an individual security held in the Fund’s portfolio, the Fund forgoes, during the option’s life, the opportunity to profit from increases in the market value of the security covering the call option above the sum of the premium and the strike price of the call but has retained the risk of loss (net of premiums received) should the price of the underlying security decline.

The value of options written by the Fund, which will be priced daily, will be affected by, among other factors, changes in the value of underlying securities (including those comprising an index), changes in the dividend rates of underlying securities, changes in interest rates, changes in the actual or perceived volatility of the stock market and underlying securities and the remaining time to an option’s expiration. The value of an option also may be adversely affected if the market for the option is reduced or becomes less liquid.

There are significant differences between the securities and options markets that could result in an imperfect correlation between these markets, causing a given transaction not to achieve its objectives. A decision as to whether, when and how to use options involves the exercise of skill and judgment, and even a well conceived transaction may be unsuccessful to some degree because of market behavior or unexpected events. In the case of index options, GPIM will attempt to maintain for the Fund written call options positions on equity indexes whose price movements, taken in the aggregate, are closely correlated with the price movements of common stocks and other securities held in the Fund’s equity portfolio. However, this strategy involves significant risk that the changes in value of the indexes underlying the Fund’s written call options positions will not correlate closely with changes in the market value of securities held by the Fund. To the extent that there is a lack of correlation, movements in the indexes underlying the options positions may result in losses to the Fund, which may more than offset any gains received by the Fund from options premiums. In these and other circumstances, the Fund may be required to sell portfolio securities to satisfy its obligations as the writer of an index call option, when it would not otherwise choose to do so, or may choose to sell portfolio securities to realize gains to supplement Fund distributions. Such sales would involve transaction costs borne by the Fund and may also result in realization of taxable capital gains, including short-term capital gains taxed at ordinary income tax rates, and may adversely impact the Fund’s after-tax returns.

There can be no assurance that a liquid market will exist when the Fund seeks to close out an option position. Reasons for the absence of a liquid secondary market on an exchange include the following: (i) there may be insufficient trading interest in certain options; (ii) restrictions may be imposed by an exchange on opening transactions or closing transactions or both; (iii) trading halts, suspensions or other restrictions may be imposed with respect to particular classes or series of options; (iv) unusual or unforeseen circumstances may interrupt normal operations on an exchange; (v) the facilities of an exchange or The Options Clearing Corporation (the “OCC”) may not at all times be adequate to handle current trading volume; or (vi) one or more exchanges could, for economic or other reasons, decide or be compelled at some future date to discontinue the trading of options (or a particular class or series of options). If trading were discontinued, the secondary market on that exchange (or in that class or series of options) would cease to exist. However, outstanding options on that exchange that had been issued by the OCC as a result of trades on that exchange would continue to be exercisable in accordance with their terms. In the event that the Fund were unable to close out a call option that it had written on a portfolio security, it would not be able to sell the underlying security unless the option expired without exercise. To the extent that the Fund owns unlisted (or “over-the-counter”) options, the Fund’s ability to terminate these options may be more limited than with exchange-traded options and may involve enhanced risk that counterparties participating in such transactions will not fulfill their obligations.

The hours of trading for options may not conform to the hours during which the securities held by the Fund are traded. To the extent that the options markets close before the markets for the underlying securities, significant price and rate movements can take place in the underlying markets that cannot be reflected in the options markets. Additionally, the exercise price of an option may be adjusted downward before the option’s expiration as a result of the occurrence of certain corporate events affecting underlying securities, such as extraordinary dividends, stock splits, mergers or other extraordinary distributions or events. A reduction in the exercise price of an option might reduce the Fund’s capital appreciation potential on underlying securities held by the Fund.

The Fund’s use of purchased put options on equity indexes as a hedging strategy would involve certain risks similar to those of written call options, including that the strategy may not work as intended due to a lack of correlation between changes in value of the index underlying the put option and changes in the market value of the Fund’s portfolio securities. Further, a put option acquired by the Fund and not sold prior to expiration will expire worthless if the cash value of the index or market value of the underlying security at expiration exceeds the exercise price of the option, thereby causing the Fund to lose its entire investment in the option.

|

8 | GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

|

|

QUESTIONS & ANSWERS continued

|

December 31, 2012

|

The Fund’s options transactions will be subject to limitations established by each of the exchanges, boards of trade or other trading facilities on which the options are traded. These limitations govern the maximum number of options in each class which may be written or purchased by a single investor or group of investors acting in concert, regardless of whether the options are written or purchased on the same or different exchanges, boards of trade or other trading facilities or are held or written in one or more accounts or through one or more brokers. Thus, the number of options which the Fund may write or purchase may be affected by options written or purchased by other investment advisory clients of GPIM. An exchange, board of trade or other trading facility may order the liquidation of positions found to be in excess of these limits, and it may impose other sanctions.

Other Derivatives Risk. Derivatives are subject to a number of risks such as liquidity risk, equity securities risk, issuer risk, interest rate risk, credit risk, leveraging risk, counterparty risk, management risk and, if applicable, medium and smaller company risk. They also involve the risk of mispricing or improper valuation, the risk of ambiguous documentation and the risk that changes in the value of a derivative may not correlate perfectly with an underlying asset, interest rate or index. Suitable derivative transactions may not be available in all circumstances and there can be no assurance that the Fund will engage in these transactions to reduce exposure to other risks when that would be beneficial. The use of derivatives transactions may result in losses greater than if they had not been used, may require the Fund to sell or purchase portfolio securities at inopportune times or for prices other than current market values, may limit the amount of appreciation the Fund can realize on an investment or may cause the Fund to hold a security that it might otherwise sell. Additionally, amounts paid by the Fund as premiums and cash or other assets held in margin accounts with respect to derivatives transactions are not otherwise available to the Fund for investment purposes.

Proposed legislation regarding regulation of the financial sector could change the way in which derivative instruments are regulated and/or traded. Among the legislative proposals are requirements that derivative instruments be traded on regulated exchanges and cleared through central clearinghouses, limitations on derivative trading by certain financial institutions, reporting of derivatives transactions, regulation of derivatives dealers and imposition of additional collateral requirements. There can be no assurance such regulation, if enacted, may impact the availability, liquidity and cost of derivative instruments. There can be no assurance that such legislation or regulation will not have a material adverse effect on the Fund or will not impair the ability of the Fund to achieve its investment objective.

The Fund may enter into derivatives transactions that may in certain circumstances produce effects similar to leverage and expose the Fund to related risks. See “Financial Leverage Risk” below.

Counterparty Risk. The Fund will be subject to risk with respect to the counterparties to the derivative contracts purchased or sold by the Fund. If a counterparty becomes bankrupt or otherwise fails to perform its obligations under a derivative contract due to financial difficulties, the Fund may experience significant delays in obtaining any recovery under the derivative contract in a bankruptcy or other reorganization proceeding. The Fund may obtain only a limited recovery or may obtain no recovery in these circumstances.

Financial Leverage Risk. Use of financial leverage creates an opportunity for increased income and capital appreciation but, at the same time, creates special risks. There can be no assurance that a leveraging strategy will be utilized or will be successful. Financial leverage is a speculative technique that exposes the Fund to greater risk and increased costs than if it were not implemented. Increases and decreases in the value of the Fund’s portfolio will be magnified when the Fund uses financial leverage. As a result, financial leverage may cause greater changes in the Fund’s net asset value and returns than if financial leverage had not been used. The Fund will also have to pay interest on its indebtedness, if any, which may reduce the Fund’s return. This interest expense may be greater than the Fund’s return on the underlying investment, which would negatively affect the performance of the Fund.

During the time in which the Fund is utilizing financial leverage, the amount of the fees paid to the Adviser and the Sub-Adviser for investment advisory services will be higher than if the Fund did not utilize financial leverage because the fees paid will be calculated based on the Fund’s Managed Assets, including proceeds of financial leverage. This may create a conflict of interest between the Adviser and the Sub-Adviser and common shareholders. Common shareholders bear the portion of the investment advisory fee attributable to the assets purchased with the proceeds of financial leverage, which means that common shareholders effectively bear the entire advisory fee. In order to manage this conflict of interest, any use of financial leverage must be approved by the Board of Trustees and the Board of Trustees will receive regular reports from the Adviser and the Sub-Adviser regarding the Fund’s use of financial leverage and the effect of financial leverage on the management of the Fund’s portfolio and the performance of the Fund.

Reverse repurchase agreements involve the risks that the interest income earned on the investment of the proceeds will be less than the interest expense and Fund expenses, that the market value of the securities sold by the Fund may decline below the price at which the Fund is obligated to repurchase such securities and that the securities may not be returned to the Fund.

Recent Market Developments Risk. Global and domestic financial markets have experienced periods of unprecedented turmoil. Recently, markets have witnessed more stabilized economic activity as expectations for an economic recovery increased. However, risks to a robust resumption of growth persist. Continuing uncertainty as to the status of the euro and the European Monetary Union has created significant volatility in currency and financial markets generally. A return to unfavorable economic conditions or sustained economic slowdown could adversely impact the Fund’s portfolio. Financial market conditions, as well as various social and political tensions in the United States and around the world, have contributed to increased market volatility and may have long-term effects on the United States and worldwide financial markets and cause further economic uncertainties or deterioration in the United States and worldwide. The Adviser and Sub-Adviser do not know how long the financial markets will continue to be affected by these events and cannot predict the effects of these or similar events in the future on the United States and global economies and securities markets.

The Fund is subject to additional risks, including management risk, medium and smaller company risk, foreign investment risk, inflation/deflation, portfolio turnover, as well as risks from market developments, market disruption, legislation and geopolitical risk. Please see www.guggenheiminvestments.com/gpm for a more detailed discussion about Fund risks and considerations.

|

GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT | 9

|

|

FUND SUMMARY (Unaudited)

|

December 31, 2012

|

|

Fund Statistics

|

|||

|

Share Price

|

$

|

8.20

|

|

|

Common Share Net Asset Value

|

$

|

8.93

|

|

|

Premium/(Discount) to NAV

|

-8.17%

|

||

|

Net Assets ($000)

|

$

|

170,253

|

|

Total Returns(1)

|

|||||

|

(Inception 8/25/05)

|

Market

|

NAV

|

|||

|

One Year

|

11.52 % | 6.60 % | |||

|

Three Year - average annual

|

9.96 % | 9.05 % | |||

|

Five Year - average annual

|

-0.37 % | -2.71 % | |||

|

Since Inception - average annual

|

-1.11 % | -0.24 % |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. For the most recent month-end performance figures, please visit www.guggenheiminvestments.com/gpm. The investment return and principal value of an investment will fluctuate with changes in the market conditions and other factors so that an investor’s shares, when sold, may be worth more or less than their original cost.

|

Long-Term Holdings

|

% of Long-Term

Investments

|

|||

|

SPDR S&P 500 ETF Trust

|

42.4

|

%

|

||

|

SPDR Dow Jones Industrial Average ETF Trust

|

28.6

|

%

|

||

|

iShares Russell 2000 Index

|

12.0

|

%

|

||

|

SPDR S&P MidCap 400 ETF Trust

|

4.8

|

%

|

||

|

Industrial Select Sector SPDR

|

4.8

|

%

|

||

|

PowerShares QQQ Trust, Series 1

|

4.5

|

%

|

||

|

SPDR S&P Retail ETF

|

2.4

|

%

|

||

|

Health Care Select Sector SPDR

|

0.5

|

%

|

||

Portfolio composition and holdings are subject to change daily. For more information, please visit www.guggenheiminvestments.com/gpm. The above summaries are provided for informational purposes only and should not be viewed as recommendations. Past performance does not guarantee future results.

(1) Performance prior to June 22, 2010, under the name Old Mutual/Claymore Long-Short Fund was achieved through an investment strategy of a long-short strategy and an opportunistic covered call writing strategy by the previous investment sub-adviser, Analytic Investors, LLC, and factors in the Fund’s fees and expenses.

|

Fund Breakdown

|

% of Net

Assets

|

|||

|

Long-Term Investments

|

137.3

|

%

|

||

|

Short-Term Investment

|

0.4

|

%

|

||

|

Total Investments

|

137.7

|

%

|

||

|

Total Value of Options Written

|

-1.2

|

%

|

||

|

Liabilities in excess of Other Assets

|

-0.1

|

%

|

||

|

Borrowings

|

-36.4

|

%

|

||

|

Total Net Assets

|

100.0

|

%

|

||

|

10 | GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

|

|

PORTFOLIO OF INVESTMENTS

|

December 31, 2012

|

|

Number

of Shares

|

Description

|

Value

|

||||

|

Long-Term Investments – 137.3%

|

||||||

|

Exchange Traded Funds (a) – 137.3%

|

||||||

|

27,800

|

Health Care Select Sector SPDR(b)

|

$

|

1,110,610

|

|||

|

294,900

|

Industrial Select Sector SPDR(b)

|

11,176,710

|

||||

|

332,900

|

iShares Russell 2000 Index

|

28,060,141

|

||||

|

162,000

|

PowerShares QQQ Trust, Series 1(b)

|

10,547,820

|

||||

|

510,700

|

SPDR Dow Jones Industrial Average ETF Trust(b)

|

66,850,630

|

||||

|

696,200

|

SPDR S&P 500 ETF Trust(b)

|

99,222,424

|

||||

|

60,200

|

SPDR S&P MidCap 400 ETF Trust(b)

|

11,179,742

|

||||

|

89,100

|

SPDR S&P Retail ETF

|

5,560,731

|

||||

|

(Cost $233,709,978)

|

233,708,808

|

|||||

|

Short-Term Investment – 0.4%

|

||||||

|

Money Market Fund – 0.4%

|

||||||

|

796,565

|

Dreyfus Treasury Prime Cash Management Institutional Shares

|

796,565

|

||||

|

(Cost $796,565)

|

||||||

|

Total Investments – 137.7%

|

||||||

|

(Cost $234,506,543)

|

234,505,373

|

|||||

|

Liabilities in excess of Other Assets – (0.1%)

|

(167,818

|

)

|

||||

|

Total Value of Options Written – (1.2%)

|

||||||

|

(Premiums received $2,788,818)

|

(2,084,449

|

)

|

||||

|

Borrowings – (36.4% of Net Assets or 26.4% of Total Investments)

|

(62,000,000

|

)

|

||||

|

Net Assets – 100.0%

|

$

|

170,253,106

|

|

Contracts

(100 shares

per contract)

|

Options Written

|

Expiration

Month

|

Exercise

Price

|

Value

|

|||||||

|

Call Options Written (c) – (1.2%)

|

|||||||||||

|

278

|

Health Care Select Sector SPDR

|

January 2013

|

$

|

41.00

|

$

|

(3,336

|

)

|

||||

|

2,949

|

Industrial Select Sector SPDR

|

January 2013

|

39.00

|

(53,082

|

)

|

||||||

|

3,329

|

iShares Russell 2000 Index

|

January 2013

|

84.00

|

(584,239

|

)

|

||||||

|

1,620

|

PowerShares QQQ Trust, Series 1

|

January 2013

|

66.00

|

(119,880

|

)

|

||||||

|

5,107

|

SPDR Dow Jones Industrial Average ETF Trust

|

January 2013

|

133.00

|

(416,221

|

)

|

||||||

|

6,962

|

SPDR S&P 500 ETF Trust

|

January 2013

|

145.00

|

(675,314

|

)

|

||||||

|

602

|

SPDR S&P MidCap 400 ETF Trust

|

January 2013

|

188.00

|

(109,865

|

)

|

||||||

|

891

|

SPDR S&P Retail ETF

|

January 2013

|

62.00

|

(122,512

|

)

|

||||||

|

Total Value of Options Written – (1.2%)

|

|||||||||||

|

(Premiums received $2,788,818)

|

$

|

(2,084,449

|

)

|

S&P – Standard & Poor’s

|

(a)

|

Securities represent cover for outstanding options written.

|

|

(b)

|

These securities have been physically segregated as collateral for borrowings outstanding.

|

|

(c)

|

Non-income producing security.

|

|

See notes to financial statements.

|

|

GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT | 11

|

|

STATEMENT OF ASSETS AND LIABILITIES

|

December 31, 2012

|

|

Assets

|

||||

|

Investments, at value (cost $234,506,543)

|

$

|

234,505,373

|

||

|

Dividends receivable

|

141,666

|

|||

|

Other assets

|

31,566

|

|||

|

Total assets

|

234,678,605

|

|||

|

Liabilities

|

||||

|

Borrowings

|

62,000,000

|

|||

|

Options written, at value (premiums received of $2,788,818)

|

2,084,449

|

|||

|

Advisory fee payable

|

161,409

|

|||

|

Interest due on borrowings

|

58,965

|

|||

|

Administration fee payable

|

5,306

|

|||

|

Accrued expenses

|

115,370

|

|||

|

Total liabilities

|

64,425,499

|

|||

|

Net Assets

|

$

|

170,253,106

|

||

|

Composition of Net Assets

|

||||

|

Common stock, $.01 par value per share; unlimited number of shares authorized, 19,054,684 shares issued and outstanding

|

$

|

190,547

|

||

|

Additional paid-in capital

|

241,111,219

|

|||

|

Net unrealized appreciation on investments and options

|

703,199

|

|||

|

Accumulated net realized loss on investments and options

|

(71,751,859

|

)

|

||

|

Net Assets

|

$

|

170,253,106

|

||

|

Net Asset Value (based on 19,054,684 common shares outstanding)

|

$

|

8.93

|

|

See notes to financial statements.

|

|

12 | GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

|

|

STATEMENT OF OPERATIONS For the year ended December 31, 2012

|

December 31, 2012

|

|

Investment Income

|

|||||||

|

Dividends

|

$

|

1,087,057

|

|||||

|

Total income

|

|

$

|

1,087,057

|

||||

|

Expenses

|

|||||||

|

Advisory fee

|

2,179,916

|

||||||

|

Interest expense

|

628,387

|

||||||

|

Professional fees

|

167,764

|

||||||

|

Trustees’ fees and expenses

|

75,711

|

||||||

|

Fund accounting

|

66,407

|

||||||

|

Administration fee

|

63,443

|

||||||

|

Printing expense

|

50,864

|

||||||

|

Custodian fee

|

47,848

|

||||||

|

Insurance

|

25,264

|

||||||

|

NYSE listing fee

|

21,409

|

||||||

|

Transfer agent fee

|

18,204

|

||||||

|

Miscellaneous

|

8,420

|

||||||

|

Total expenses

|

|

3,353,637

|

|||||

|

Advisory fees waived

|

|

(242,213

|

)

|

||||

|

Net expenses

|

|

3,111,424

|

|||||

|

Net investment loss

|

|

(2,024,367

|

)

|

||||

|

Realized and Unrealized Gain (Loss) on Investments and Options:

|

|

||||||

|

Net realized gain (loss) on:

|

|

||||||

|

Investments

|

|

$

|

21,934,927

|

||||

|

Options

|

|

(6,403,948

|

)

|

||||

|

Net change in unrealized appreciation (depreciation) on:

|

|

||||||

|

Investments

|

|

(4,456,356

|

)

|

||||

|

Options

|

|

2,759,989

|

|||||

|

Net realized and unrealized gain on investments and options

|

|

13,834,612

|

|||||

|

Net Increase in Net Assets Resulting from Operations

|

|

$

|

11,810,245

|

|

See notes to financial statements.

|

|

GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT | 13

|

|

STATEMENT OF CHANGES IN NET ASSETS

|

December 31, 2012

|

|

For the

Year Ended

December 31, 2012

|

For the

Year Ended

December 31, 2011

|

||||||

|

Increase (Decrease) in Net Assets from Operations

|

|||||||

|

Net investment income (loss)

|

$

|

(2,024,367

|

)

|

$

|

219,222

|

||

|

Net realized gain (loss) on investments and options

|

15,530,979

|

13,818,723

|

|||||

|

Net change in unrealized appreciation (depreciation) on investments and options

|

(1,696,367

|

)

|

(2,767,879

|

)

|

|||

|

Net increase (decrease) in net assets resulting from operations

|

11,810,245

|

11,270,066

|

|||||

|

Distributions to Shareholders

|

|||||||

|

From and in excess of net investment income

|

(18,289,205

|

)

|

(18,265,472

|

)

|

|||

|

Capital Share Transactions

|

|||||||

|

Net proceeds from common shares issued through dividend reinvestment

|

64,197

|

405,853

|

|||||

|

Net increase from capital share transactions

|

64,197

|

405,853

|

|||||

|

Total decrease in net assets

|

(6,414,763

|

)

|

(6,589,553

|

)

|

|||

|

Net Assets

|

|||||||

|

Beginning of period

|

176,667,869

|

183,257,422

|

|||||

|

End of period (including accumulated net investment

|

|||||||

|

income of $0 and $0, respectively)

|

$

|

170,253,106

|

$

|

176,667,869

|

|

See notes to financial statements.

|

|

14 | GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

|

|

STATEMENT OF CASH FLOWS For the year ended December 31, 2012

|

December 31, 2012

|

|

Cash Flows from Operating Activities:

|

||||

|

Net increase in net assets resulting from operations

|

$

|

11,810,245

|

||

|

Adjustments to Reconcile Net Increase in Net Assets Resulting from Operations to Net Cash Used

|

||||

|

by Operating and Investing Activities:

|

||||

|

Net change in unrealized depreciation on investments

|

4,456,356

|

|||

|

Net change in unrealized appreciation on options

|

(2,759,989

|

)

|

||

|

Net realized gain on investments

|

(21,934,927

|

)

|

||

|

Net realized loss on options

|

6,403,948

|

|||

|

Purchase of long-term investments

|

(1,725,280,624

|

)

|

||

|

Proceeds from sale of long-term investments

|

1,720,941,422

|

|||

|

Net purchase of short-term investments

|

(673,798

|

)

|

||

|

Cost of written options closed

|

(36,996,075

|

)

|

||

|

Premiums received on options written

|

41,597,559

|

|||

|

Decrease in dividends receivable

|

474,977

|

|||

|

Decrease in other assets

|

5,328

|

|||

|

Increase in interest due on borrowings

|

55,321

|

|||

|

Increase in advisory fee payable

|

14,431

|

|||

|

Increase in administration fee payable

|

358

|

|||

|

Decrease in accrued expenses

|

(20,878

|

)

|

||

|

Net Cash Used by Operating and Investing Activities

|

$

|

(1,906,346

|

)

|

|

|

Cash Flows From Financing Activities:

|

||||

|

Proceeds from borrowings

|

69,500,000

|

|||

|

Payments on borrowings

|

(49,500,000

|

)

|

||

|

Distributions to common shareholders

|

(18,225,008

|

)

|

||

|

Net Cash Provided by Financing Activities

|

1,774,992

|

|||

|

Net decrease in cash

|

(131,354

|

)

|

||

|

Cash at Beginning of Period

|

131,354

|

|||

|

Cash at End of Period

|

$

|

—

|

||

|

Supplemental Disclosure of Cash Flow Information: Cash paid during the year for interest

|

$

|

573,066

|

||

|

Supplemental Disclosure of Non Cash Operating Activity: Options exercised during the year

|

$

|

13,787,056

|

||

|

Supplemental Disclosure of Non Cash Financing Activity: Dividend reinvestment

|

$

|

64,197

|

|

See notes to financial statements.

|

|

GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT | 15

|

|

FINANCIAL HIGHLIGHTS

|

December 31, 2012

|

|

Per share operating performance for a common share outstanding throughout the period

|

For the

Year Ended

|

For the

Year Ended |

For the

Year Ended |

For the

Year Ended |

For the

Year Ended |

|||||||||||

|

Net asset value, beginning of period

|

$

|

9.27

|

$

|

9.64

|

$

|

9.40

|

$

|

10.24

|

$

|

17.79

|

||||||

|

Income from investment operations

|

||||||||||||||||

|

Net investment income (loss) (a)

|

(0.11

|

)

|

0.01

|

(0.01

|

)

|

0.04

|

0.05

|

|||||||||

|

Net realized and unrealized gain (loss) on investments, futures, options, securities sold short, forwards and foreign currency

|

0.73

|

0.58

|

1.21

|

0.24

|

(6.00

|

)

|

||||||||||

|

Total from investment operations

|

0.62

|

0.59

|

1.20

|

0.28

|

(5.95

|

)

|

||||||||||

|

Distributions to Common Shareholders

|

||||||||||||||||

|

From and in excess of net investment income

|

(0.96

|

)

|

(0.96

|

)

|

(0.50

|

)

|

—

|

(0.14

|

)

|

|||||||

|

Return of capital

|

—

|

—

|

(0.46

|

)

|

(1.12

|

)

|

(1.46

|

)

|

||||||||

|

Total distributions to common shareholders

|

(0.96

|

)

|

(0.96

|

)

|

(0.96

|

)

|

(1.12

|

)

|

(1.60

|

)

|

||||||

|

Net asset value, end of period

|

$

|

8.93

|

$

|

9.27

|

$

|

9.64

|

$

|

9.40

|

$

|

10.24

|

||||||

|

Market value, end of period

|

$

|

8.20

|

$

|

8.16

|

$

|

9.33

|

$

|

8.52

|

$

|

7.98

|

||||||

|

Total investment return (b)

|

||||||||||||||||

|

Net asset value

|

6.60

|

%

|

6.78

|

%

|

13.95

|

%

|

3.51

|

%

|

-35.09

|

%

|

||||||

|

Market value

|

11.52

|

%

|

-2.42

|

%

|

22.18

|

%

|

22.85

|

%

|

-39.88

|

%

|

||||||

|

Ratios and supplemental data

|

||||||||||||||||

|

Net assets, end of period (thousands)

|

$

|

170,253

|

$

|

176,668

|

$

|

183,257

|

$

|

178,680

|

$

|

194,666

|

||||||

|

Ratios to average net assets:

|

||||||||||||||||

|

Net operating expense ratio, including fee waivers

|

1.38

|

%

|

1.38

|

%

|

1.57

|

%

|

1.77

|

%

|

1.41

|

%

|

||||||

|

Interest expense

|

0.35

|

%

|

0.28

|

%

|

0.16

|

%

|

N/A

|

N/A

|

||||||||

|

Dividends paid on securities sold short

|

N/A

|

N/A

|

0.07

|

%

|

0.65

|

%

|

0.85

|

%

|

||||||||

|

Total net expense ratio

|

1.73

|

%(c)

|

1.66

|

%(c)

|

1.80

|

%(c)

|

2.42

|

%

|

2.26

|

%

|

||||||

|

Gross operating expense ratio, excluding fee waivers

|

1.52

|

%

|

1.51

|

%

|

1.64

|

%

|

1.77

|

%

|

1.41

|

%

|

||||||

|

Interest expense

|

0.35

|

%

|

0.28

|

%

|

0.16

|

%

|

N/A

|

N/A

|

||||||||

|

Dividends paid on securities sold short

|

N/A

|

N/A

|

0.07

|

%

|

0.65

|

%

|

0.85

|

%

|

||||||||

|

Total gross expense ratio

|

1.87

|

% (c)

|

1.79

|

%(c)

|

1.87

|

%(c)

|

2.42

|

%

|

2.26

|

%

|

||||||

|

Net investment income (loss) ratio

|

(1.13

|

) %

|

0.12

|

%

|

(0.15

|

) %

|

0.38

|

%

|

0.36

|

%

|

||||||

|

Net investment income (loss) ratio, excluding fee waivers

|

(1.27

|

) %

|

(0.01

|

)%

|

(0.22

|

) %

|

0.38

|

%

|

0.36

|

%

|

||||||

|

Portfolio turnover(d)

|

705

|

%

|

405

|

%

|

497

|

%(e)

|

256

|

%

|

223

|

%

|

||||||

|

Senior Indebtedness

|

||||||||||||||||

|

Total borrowings outstanding (in thousands)

|

$

|

62,000

|

$

|

42,000

|

$

|

50,500

|

N/A

|

N/A

|

||||||||

|

Asset Coverage per $1,000 of indebtedness(f)

|

$

|

3,746

|

$

|

5,206

|

$

|

4,629

|

N/A

|

N/A

|

|

N/A

|

Not applicable

|

|

(a)

|

Based on average shares outstanding during the period.

|

|

(b)

|

Total investment return is calculated assuming a purchase of a common share at the beginning of the period and a sale on the last day of the period reported either at net asset value (“NAV”) or market price per share. Dividends and distributions are assumed to be reinvested at NAV for NAV returns or the prices obtained under the Fund’s Dividend Reinvestment Plan for market value returns. Total investment return does not reflect brokerage commissions. A return calculated for a period of less than one year is not annualized.

|

|

(c)

|

The ratios of total expenses to average net assets do not reflect fees and expenses incurred indirectly by the Fund as a result of its investment in shares of other investment companies. If these fees were included in the expense ratios, the expense ratios would increase by 0.25%, 0.21%, and 0.28% for the years ended December 31, 2012, 2011 and 2010, respectively.

|

|

(d)

|

Portfolio turnover is not annualized for periods of less than one year.

|

|

(e)

|

The increase in the portfolio turnover compared to prior years is the result of the change in the Fund’s Sub-Adviser and the resulting reallocation of the portfolio holdings.

|

|

(f)

|

Calculated by subtracting the Fund’s total liabilities (not including the borrowings) from the Fund’s total assets and dividing by the total borrowings.

|

|

See notes to financial statements.

|

|

16 | GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

|

|

NOTES TO FINANCIAL STATEMENTS

|

December 31, 2012

|

Note 1 – Organization:

Guggenheim Enhanced Equity Income Fund (the “Fund”) was organized as a Massachusetts business trust on December 3, 2004. The Fund is registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”).

The Fund’s primary investment objective is to seek to provide a high level of current income and current gains, with a secondary objective of long-term capital appreciation. The Fund seeks to achieve its investment objective by obtaining broadly diversified exposure to the equity markets and utilizing a covered call strategy which will follow a proprietary dynamic rules-based methodology. The Fund seeks to earn income and gains both from dividends paid by the securities owned by the Fund and cash premiums received from selling options.

Note 2 – Accounting Policies:

The preparation of the financial statements in accordance with U.S. generally accepted accounting principles (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from these estimates.

The following is a summary of significant accounting policies followed by the Fund.

(a) Valuation of Investments and Derivatives

The Fund values equity securities at the last reported sale price on the principal exchange or in the principal over-the-counter (“OTC”) market in which such securities are traded, as of the close of regular trading on the New York Stock Exchange (“NYSE”) on the day the securities are being valued, or if there are no sales, at the mean between the last available bid and ask prices on that day. Securities traded on NASDAQ are valued at the NASDAQ Official Closing Price. Debt securities are valued by independent pricing services or dealers using the bid price for such securities or, if such prices are not available, at prices for securities of comparable maturity, quality and type. Exchange traded options are valued at the mean between the last available bid and asked prices on the principal exchange on which they are traded. The Fund values money market funds at net asset value. Short-term securities with maturities of 60 days or less at time of purchase are valued at amortized cost, which approximates market value.

For those securities where quotations or prices are not available, the valuations are determined in accordance with procedures established in good faith by management and approved by the Board of Trustees. Valuations in accordance with these procedures are intended to reflect each security’s (or asset’s) “fair value”. Fair value is the amount that the Fund might reasonably expect to receive for the security (or asset) upon its current sale. Each such determination should be based on a consideration of all relevant factors, which are likely to vary from one pricing context to another. Examples of such factors may include, but are not limited to: (i) the type of security, (ii) the initial cost of the security, (iii) the existence of any contractual restrictions on the security’s disposition, (iv) the price and extent of public trading in similar securities of the issuer or of comparable companies, (v) quotations or evaluated prices from broker-dealers and/or pricing services, (vi) information obtained from the issuer, analysts, and/or the appropriate stock exchange (for exchange traded securities), (vii) an analysis of the company’s financial statements, and (viii) an evaluation of the forces that influence the issuer and the market(s) in which the security is purchased and sold (e.g. the existence of pending merger activity, public offerings or tender offers that might affect the value of the security).

There are three different categories for valuations. Level 1 valuations are those based upon quoted prices in active markets. Level 2 valuations are those based upon quoted prices in inactive markets or based upon significant observable inputs (e.g. yield curves; benchmark interest rates; indices). Level 3 valuations are those based upon unobservable inputs (e.g. discounted cash flow analysis; non-market based methods used to determine fair valuation).

The Fund values Level 1 securities using readily available market quotations in active markets. Money market funds are valued at net asset value. The Fund values Level 2 fixed income securities using independent pricing providers who employ matrix pricing models utilizing market prices, broker quotes and prices of securities with comparable maturities and qualities. The Fund values Level 2 equity securities using independent pricing providers who employ various observable market inputs. The Fund did not have any Level 2 or Level 3 securities during the year ended December 31, 2012.

The following table represents the Fund’s investments carried on the Statement of Assets and Liabilities by caption and by level within the fair value hierarchy as of December 31, 2012:

|

Description

|

Level 1

|

Level 2

|

Level 3

|

Total

|

|||||||||

|

Valuations (in $000s)

|

|||||||||||||

|

Assets:

|

|||||||||||||

|

Exchange-Traded Funds

|

$

|

233,709

|

$

|

—

|

$

|

—

|

$

|

233,709

|

|||||

|

Money Market Fund

|

796

|

—

|

—

|

796

|

|||||||||

|

Total

|

$

|

234,505

|

$

|

—

|

$

|

—

|

$

|

234,505

|

|||||

|

Liabilities:

|

|||||||||||||

|

Call Options Written

|

$

|

2,084

|

$

|

—

|

$

|

—

|

$

|

2,084

|

|||||

|

Total

|

$

|

2,084

|

$

|

—

|

$

|

—

|

$

|

2,084

|

There were no transfers between levels during the year ended December 31, 2012.

(b) Investment Transactions and Investment Income

Investment transactions are accounted for on the trade date. Realized gains and losses on investments are determined on the identified cost basis. Dividend income is recorded net of applicable withholding taxes on the ex-dividend date and interest income is recorded on an accrual basis. Discounts or premiums on debt securities purchased are accreted or amortized to interest income over the lives of the respective securities using the effective interest method.

|

GPM | GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT | 17

|

|

NOTES TO FINANCIAL STATEMENTS continued

|

December 31, 2012

|

(c) Options

The Fund may purchase or sell (write) options on securities and securities indices which are listed on a national securities exchange or in the OTC market as a means of achieving additional return or of hedging the value of the Fund’s portfolio. An option on a security is a contract that gives the holder of the option, in return for a premium, the right to buy from (in the case of a call) or sell to (in the case of a put) the writer of the option the security underlying the option at a specified exercise or “strike” price. The writer of an option on a security has an obligation upon exercise of the option to deliver the underlying security upon payment of the exercise price (in the case of a call) or to pay the exercise price upon delivery of the underlying security (in the case of a put). When an option is written, the premium received is recorded as an asset with an equal liability and is subsequently marked to market to reflect the current market value of the option written. These liabilities are reflected as options written in the Statement of Assets and Liabilities. Premiums received from writing options which expire unexercised are recorded on the expiration date as a realized gain. The difference between the premium received and the amount paid on effecting a closing purchase transaction, including brokerage commissions, is also treated as a realized gain, or if the premium is less than the amount paid for the closing purchase transactions, as a realized loss. If a call option is exercised, the premium is added to the proceeds from the sale of the underlying security in determining whether there has been a realized gain or loss.

(d) Distributions

The Fund declares and pays quarterly distributions to shareholders. Any net realized long-term gains are distributed annually. Distributions to shareholders are recorded on the ex-dividend date. The amount and timing of distributions are determined in accordance with federal income tax regulations, which may differ from GAAP.

Note 3 – Investment Advisory Agreement, Sub-Advisory Agreement and Other Agreements:

Pursuant to an Investment Advisory Agreement (the “Advisory Agreement”) between the Fund and Guggenheim Funds Investment Advisors, LLC (“GFIA” or the “Adviser”), the Adviser furnishes offices, necessary facilities and equipment, oversees the activities of Guggenheim Partners Investment Management, LLC (“GPIM” or the “Sub-Adviser”), provides personnel including certain officers required for its administrative management and compensates the officers and trustees, if any, of the Fund who are its affiliates. Both GFIA and GPIM are indirect subsidiaries of Guggenheim Partners, LLC (“Guggenheim”), a diversified financial services firm.

Pursuant to a Sub-Advisory Agreement (the “Sub-Advisory Agreement”) among the Fund, the Adviser and the Sub-Adviser, the Sub-Adviser under supervision of the Fund’s Board of Trustees and the Adviser, provides a continuous investment program for the Fund’s portfolio; provides investment research, makes and executes recommendations for the purchase and sale of securities; and provides certain facilities and personnel.

Under the Advisory Agreement, GFIA is entitled to receive an investment advisory fee at an annual rate equal to 1.00% of the average daily value of the Fund’s total managed assets. Under the terms of a fee waiver agreement, GFIA and the Fund have contractually agreed to a permanent ten (10) basis point reduction in the advisory fee, such that the Fund pays to the Adviser an investment advisory fee at an annual rate equal to 0.90% of the average daily value of the Fund’s total managed assets. Also under the terms of a fee waiver agreement, and for so long as the investment sub-adviser of the Fund is an affiliate of GFIA, GFIA has agreed to waive an additional ten (10) basis points of its advisory fee such that the Fund pays to GFIA an investment advisory fee at an annual rate equal to 0.80% of the average daily value of the Fund’s total managed assets. Pursuant to the Sub-Advisory Agreement, the Adviser pays to GPIM a sub-advisory fee equal to 0.40% of the average daily value of the Fund’s total managed assets.

As compensation for services under the Sub-Advisory Agreement, the Adviser pays the Sub-Adviser a fee, payable monthly, in an amount equal to 0.40% of the average daily value of the Fund’s total managed assets.

The Adviser receives a fund administration fee payable monthly at the annual rate set forth below as a percentage of the average daily managed assets of the Fund:

|

Managed Assets

|

Rate

|

|

First $200,000,000

|

0.0275%

|

|

Next $300,000,000

|

0.0200%

|

|

Next $500,000,000

|

0.0150%

|

|

Over $1,000,000,000

|

0.0100%

|