|

As filed with the Securities and Exchange Commission on June 25, 2012

|

OMB APPROVAL

|

|

Registration No. 333-182270

|

OMB Number: 3235-0336

Expires: October 31, 2013

Estimated average burden

hours per response. . .1312.9

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

|

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

|

/ X /

|

|

PRE-EFFECTIVE AMENDMENT NO. 1

|

/X /

|

|

POST-EFFECTIVE AMENDMENT NO. __

|

/ /

|

|

OPPENHEIMER PORTFOLIO SERIES

|

|

(Exact Name of Registrant as Specified in Charter)

|

|

6803 South Tucson Way, Centennial, Colorado 80112-3924

|

|

(Address of Principal Executive Offices)

|

|

303-768-3200

|

|

(Registrant's Area Code and Telephone Number)

|

|

Arthur S. Gabinet, Esq.

|

|

Executive Vice President & General Counsel

|

|

OppenheimerFunds, Inc.

|

|

Two World Financial Center, 225 Liberty Street

|

|

New York, New York 10281-1008

|

|

(Name and Address of Agent for Service)

|

|

As soon as practicable after the Registration Statement becomes effective.

|

|

(Approximate Date of Proposed Public Offering)

|

Title of Securities Being Registered: Class A, Class B, Class C, Class N and Class Y of Oppenheimer Portfolio Series Conservative Investor Fund

It is proposed that this filing will become effective on July 25, 2012 pursuant to Rule 488.

No filing fee is due because of reliance on Section 24(f) of the Investment Company Act of 1940, as amended.

CONTENTS OF REGISTRATION STATEMENT

This Registration Statement contains the following pages and documents:

Front Cover

Contents Page

Part A

Prospectus and Proxy Statement of Oppenheimer Portfolio Series Conservative Investor Fund

Part B

Statement of Additional Information

Part C

Other Information

Signatures

Exhibits

OPPENHEIMER TRANSITION 2010 FUND

6803 South Tucson Way, Centennial, Colorado 80112

1.800.225.5677

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON SEPTEMBER 14, 2012

To the Shareholders of Oppenheimer Transition 2010 Fund:

Notice is hereby given that a Special Meeting of the Shareholders of Oppenheimer Transition 2010 Fund (the “Target Fund”), a registered open-end management investment company, will be held at 6803 South Tucson Way, Centennial, Colorado 80112 at 1:00 p.m. Mountain time, on September 14, 2012, or any adjournments thereof (the “Meeting”). Shareholders will be asked to vote on the following proposals:

|

|

1.

|

To approve an Agreement and Plan of Reorganization (the “Reorganization Agreement”) between the Target Fund and Oppenheimer Portfolio Series: Conservative Investor Fund, a series of Oppenheimer Portfolio Series (“the Acquiring Fund”), and the transactions contemplated thereby, including: (a) the transfer of all of the assets of the Target Fund to the Acquiring Fund in exchange for Class A, Class B, Class C, Class N and Class Y shares of the Acquiring Fund, (b) the distribution of shares of the Acquiring Fund to the corresponding Class A, Class B, Class C, Class N and Class Y shareholders of the Target Fund in complete liquidation of the Target Fund, and (c) the cancellation of the outstanding shares of the Target Fund (all of the foregoing being referred to as the “Reorganization”); and

|

2. To act upon such other matters as may properly come before the Meeting.

Shareholders of record at the close of business on May 25, 2012 are entitled to notice of, and to vote at, the Meeting. The Reorganization is more fully discussed in the Combined Prospectus/Proxy Statement. Please read it carefully before telling us, through your proxy or in person, how you wish your shares to be voted. The Board of Trustees of the Target Fund believes the Reorganization is in the best interests of the Target Fund and recommends that you vote “For” the Reorganization.

YOU CAN VOTE ON THE INTERNET, BY TELEPHONE OR BY MAIL.

WE URGE YOU TO VOTE PROMPTLY.

YOUR VOTE IS IMPORTANT

PLEASE VOTE THE ENCLOSED PROXY TODAY.

YOUR VOTE IS IMPORTANT NO MATTER HOW MANY SHARES YOU OWN.

By Order of the Board of Trustees,

Arthur S. Gabinet, Secretary

July 27, 2012

OPPENHEIMER PORTFOLIO SERIES: CONSERVATIVE INVESTOR FUND

6803 South Tucson Way, Centennial, Colorado 80112

1.800.225.5677

COMBINED PROSPECTUS/PROXY STATEMENT

Dated July 27, 2012

SPECIAL MEETING OF SHAREHOLDERS OF

OPPENHEIMER TRANSITION 2010 FUND

to be held on September 14, 2012

Acquisition of the Assets of

OPPENHEIMER TRANSITION 2010 FUND

6803 South Tucson Way, Centennial, Colorado 80112

1.800.225.5677

By and in exchange for Class A, Class B, Class C, Class N and Class Y shares of

OPPENHEIMER PORTFOLIO SERIES: CONSERVATIVE INVESTOR FUND

This Combined Prospectus/Proxy Statement is furnished to you as a shareholder of Oppenheimer Transition 2010 Fund (the “Target Fund”), a Massachusetts business trust. A special meeting of shareholders of the Target Fund, or any adjournments thereof (the “Meeting”), will be held at the offices of OppenheimerFunds, Inc. (the “Manager”) at 6803 South Tucson Way, Centennial, Colorado 80112 on September 14, 2012, at 1:00 p.m., Mountain time, to consider the items that are listed below and discussed in greater detail elsewhere in this Combined Prospectus/Proxy Statement. Shareholders of record of the Target Fund as of the close of business on May 25, 2012 (the “Record Date”) are entitled to notice of, and to vote at, the Meeting. This Combined Prospectus/Proxy Statement, proxy card and accompanying Notice of Special Meeting will be sent to shareholders on July 27, 2012, or as soon as practicable thereafter.

The purposes of the Special Meeting are:

|

|

1.

|

To approve an Agreement and Plan of Reorganization (the “Reorganization Agreement”) between the Target Fund and Oppenheimer Portfolio Series: Conservative Investor Fund, a series of Oppenheimer Portfolio Series (the “Acquiring Fund), and the transactions contemplated thereby, including: (i) the transfer of all the assets of the Target Fund to the Acquiring Fund in exchange for Class A, Class B, Class C, Class N and Class Y of the Acquiring Fund, (ii) the distribution of shares of the Acquiring Fund to the corresponding Class A, Class B, Class C, Class N and Class Y shareholders of the Target Fund in complete liquidation of the Target Fund, and (iii) the cancellation of the outstanding shares of the Target Fund (all of the foregoing being referred to as the “Reorganization”); and

|

2. To act upon such other matters as may properly come before the Meeting.

At a meeting held on May 15, 2012, the Board of Trustees of the Target Fund and the Acquiring Fund (the “Boards” and each, a “Board”) unanimously approved the Reorganization by which the Target Fund, an open-end investment company, would be acquired by the Acquiring Fund, an open-end investment company. The Target Fund has an investment objective and investment policies and strategies that are similar to those of the Acquiring Fund. The investment objective of the Acquiring Fund is to seek current income with a secondary objective of long-term growth of capital. The current investment objective of the Target Fund is to seek income and secondarily capital growth. The Reorganization is part of a larger initiative to consolidate certain of the comparable Oppenheimer mutual funds to eliminate redundancies and achieve certain operating efficiencies.

Each Board requests that shareholders vote their shares by completing and returning the enclosed proxy card or by following one of the other methods for voting specified on the proxy card.

This Combined Prospectus/Proxy Statement constitutes the Prospectus of the Acquiring Fund and the Proxy Statement of the Target Fund filed on Form N-14 with the Securities and Exchange Commission (“SEC”). This Combined Prospectus/Proxy Statement sets forth concisely the information shareholders of the Target Fund should know before voting on the Reorganization and constitutes an offering of the shares of the Acquiring Fund being issued in the Reorganization. Please read it carefully and retain it for future reference. The following documents each have been filed with the SEC, and are incorporated herein by reference into (each legally forms a part of) this Combined Prospectus/Proxy Statement:

|

·

|

The Statement of Additional Information, dated July 27, 2012 (the “Reorganization SAI”), relating to this Combined Prospectus/Proxy Statement;

|

|

·

|

The Prospectus of the Acquiring Fund, dated May 30, 2012, as supplemented (the “Acquiring Fund Prospectus”). The Acquiring Fund Prospectus includes additional information about the Acquiring Fund and is enclosed herewith and accompanies this Combined Prospectus/Proxy Statement.

|

|

·

|

The Statement of Additional Information relating to the Acquiring Fund dated May 30, 2012, as supplemented (the “Acquiring Fund SAI”);

|

|

·

|

The Annual Report to shareholders of the Acquiring Fund for the fiscal year ended January 31, 2012 (the “Acquiring Fund Annual Report”);

|

|

·

|

The Prospectus of the Target Fund, dated June 27, 2012, as supplemented (the “Target Fund Prospectus”);

|

|

·

|

The Statement of Additional Information of the Target Fund dated June 27, 2012, as supplemented (the “Target Fund SAI”)

|

|

·

|

The Annual Report to shareholders of the Target Fund for the fiscal year ended February 29, 2012 (the “Target Fund Annual Report”);

|

The Funds are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and the Investment Company Act of 1940, as amended (the “Investment Company Act”), and in accordance therewith, file reports and other information, including proxy materials and charter documents, with the SEC.

You may request a free copy of the foregoing documents and any more recent reports filed after the date hereof by writing to OppenheimerFunds Services (the “Transfer Agent”) at P.O. Box 5270, Denver, Colorado 80217, visiting the OppenheimerFunds Internet website at www.oppenheimerfunds.com or calling toll-free 1.800.225.5677.

You also may view or obtain these documents from the SEC:

|

In Person:

|

At the SEC’s Public Reference Room at 100 F Street, N.E.,

Washington, DC 20549

|

|

By Phone:

|

(202) 551-8090

|

|

By Mail:

|

Public Reference Section

Office of Consumer Affairs and Information Services

Securities and Exchange Commission

100 F Street, N.E.

Washington, DC 20549

(duplicating fee required)

|

|

By E-mail:

|

publicinfo@sec.gov

(duplicating fee required)

|

|

By Internet:

|

www.sec.gov

|

Mutual fund shares are not deposits or obligations of any bank, and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other U.S. government agency. Mutual fund shares involve investment risks, including the possible loss of principal.

As with all mutual funds, the Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this Combined Prospectus/Proxy Statement. Any representation to the contrary is a criminal offense.

This Combined Prospectus/Proxy Statement is dated July 27, 2012.

TABLE OF CONTENTS

COMBINED PROSPECTUS/PROXY STATEMENT

|

Page

|

|||

|

Synopsis

|

|||

|

The Proposed Reorganization

|

|||

|

Investment Objectives and Principal Investment Strategies

|

|||

|

Fees and Expenses

|

|||

|

Portfolio Turnover

|

|||

|

U.S. Federal Income Tax Consequences of the Reorganization

|

|||

|

Purchase, Exchange, Redemption and Valuation of Shares

|

|||

|

Comparison of the Funds

|

|||

|

Principal Investment Risks

|

|||

|

Fundamental Investment Restrictions

|

|||

|

Performance Information

|

|||

|

Management of the Funds

|

|||

|

Investment Advisory Agreements

|

|||

|

Pending Litigation

|

|||

|

Distribution Services

|

|||

|

Payments to Financial Intermediaries and Service Providers

|

|||

|

Dividends and Distributions

|

|||

|

Purchase, Exchange, Redemption and Valuation of Shares

|

|||

|

Fund Service Providers

|

|||

|

Shareholder Rights

|

|||

|

Information About the Reorganization

|

|||

|

Terms of the Reorganization Agreement

|

|||

|

Board Consideration of the Reorganization

|

|||

|

Expenses of the Reorganization

|

|||

|

Material U.S. Federal Income Tax Consequences of the Reorganization

|

|||

|

Voting Information

|

|||

|

How to Vote

|

|||

|

Quorum and Required Vote

|

|||

|

Solicitation of Proxies

|

|||

|

Revoking a Proxy

|

|||

|

Other Matters to be Voted upon at the Meeting

|

|||

|

Shareholder Proposals and Communications

|

|||

|

Additional Information About the Funds

|

|||

|

Capitalization of the Funds

|

|||

|

Householding of Reports to Shareholders and Other Fund Documents

|

|||

|

Shareholder Information

|

|||

|

Exhibit A: Form of Agreement and Plan of Reorganization

|

A-

|

||

|

Exhibit B: Principal Shareholders

|

B-

|

||

|

Exhibit C: More Information about the Underlying Funds

|

C-

|

||

|

Exhibit D: Pro Forma Proxy Financial Statements

|

D-

|

||

|

Exhibit E: Proxy Card

|

E-

|

||

Enclosures:

Prospectus of Oppenheimer Portfolio Series: Conservative Investor Fund dated May 30, 2012

SYNOPSIS

This is only a summary and is qualified in its entirety by the more detailed information contained in or incorporated by reference in this Combined Prospectus/Proxy Statement and by the Reorganization Agreement, which is attached as Exhibit A. Shareholders should carefully review this Combined Prospectus/Proxy Statement and the Reorganization Agreement in their entirety and the Acquiring Fund Prospectus which accompanies this Combined Prospectus/Proxy Statement and is incorporated herein by reference.

The Proposed Reorganization

If shareholders of the Target Fund vote to approve the Reorganization Agreement and the Reorganization on the Closing Date (as such term is defined in the Reorganization Agreement attached hereto as Exhibit A), all of the assets of the Target Fund will be transferred to the Acquiring Fund in exchange for the assumption of all liabilities and for full and fractional shares of the Acquiring Fund having an aggregate net asset value equal to the aggregate net asset value of the shareholder’s Target Fund shares as of the Valuation Date (as such term is defined in the Reorganization Agreement) according to the following chart:

|

Target Fund – Share Class Exchanged

|

Acquiring Fund – Share Class Received

|

|

Class A

|

Class A

|

|

Class B

|

Class B

|

|

Class C

|

Class C

|

|

Class N

|

Class N

|

|

Class Y

|

Class Y

|

Immediately thereafter, the Target Fund will distribute these shares of the Acquiring Fund to its shareholders. After distributing these shares, the Target Fund will be terminated. No sales charge will be imposed on the shares of the Acquiring Fund received by Target Fund shareholders in connection with the Reorganization. However, any other purchase or redemption would be subject to any applicable sales charges. After the Reorganization is completed, any contingent deferred sales charge (“CDSC”) on the redemption of shares of the Acquiring Fund received in the Reorganization would be calculated from the date of original purchase of the Target Fund’s shares.

The Reorganization Agreement is subject to approval by the shareholders of the Target Fund. The Reorganization, if approved by shareholders of the Target Fund, is scheduled to be effective as of the close of business on October 19, 2012, or on such later date as the parties may agree (“Closing Date”). As a result of the Reorganization, each shareholder of the Target Fund will become the owner of the number of full and fractional shares of the Acquiring Fund having an aggregate net asset value equal to the aggregate net asset value of the shareholder’s Target Fund shares as of the close of business on the Valuation Date (hereinafter defined). Class A, Class B, Class C, Class N and Class Y shareholders of the Target Fund will receive the same class of shares of the Acquiring Fund. See “Information About the Reorganization” below.

Approval of the Reorganization of the Target Fund will require the affirmative vote of a majority of the outstanding voting securities of the Target Fund, as defined in the Investment Company Act. A “majority of the outstanding voting securities” is defined in the Investment Company Act as the lesser of (a) 67% or more of the voting power of the voting securities present at the Meeting, if the holders of more than 50% of the outstanding voting securities of the Target Fund are present at the Meeting or represented by proxy, or (b) more than 50% of the voting power of the outstanding voting securities of the Target Fund. See “Voting Information – Quorum and Required Vote” below.

In the absence of sufficient votes to approve the Reorganization, the Meeting shall be adjourned until a quorum shall attend. Additional information on voting and quorum requirements is provided in the section “Voting Information - Quorum and Required Vote.”

The Acquiring Fund, following the completion of the Reorganization, may be referred to as the “Combined Fund” in this Combined Prospectus/Proxy Statement. The Target Fund, the Acquiring Fund, and the Combined Fund may also be generally referred to as a “Fund” or the “Funds.”

OppenheimerFunds, Inc. (the “Manager”) serves as the investment adviser of each of the Funds. The Manager believes that the Acquiring Fund has greater prospects for attracting new assets than the Target Fund. The Funds seek to provide certain combinations of long-term growth of capital and current income by investing in both equity and fixed income funds. The Funds are all “fund of funds” because they primarily invest in other OppenheimerFunds mutual funds (“Underlying Funds”). The Funds have been managed in a substantially similar manner and the performance of the Funds is similar. The Target Fund was launched in 2006 among other similar Lifecycle Transition funds to support the Manager’s proprietary retirement plan business by serving as a Fund to accommodate a range of investor preferences and retirement time horizons. Each of those Transition funds is managed based on an approximate retirement year (the “transition” date in each fund's name) and their investments in the Underlying Funds change over time in a manner designed to help the fund become more conservative both as the transition date gets closer and for 10 years after that date. Recently, the Manager exited its retirement plan business. As the Manager has exited this business, the Target Fund would be unlikely to gain market share in the target date fund marketplace. As a result, the Target Fund may not continue to grow its assets, and may experience reverse economies of scale. A declining asset base could result in an increase in “other expenses” for Target Fund shareholders in the future.

The Manager believes that shareholders of each Fund will have the benefit of additional assets as a result of the Reorganization and the corresponding potential for lower total expenses as a percentage of net assets in the future. In addition, Target Fund shareholders will be in an actively sold product, which has the opportunity to continue to garner assets and gain economies of scale. As a result, the Manager believes that the shareholders of each Fund generally will benefit more from the potential operating efficiencies and economies of scale that may be achieved by combining the Fund’s assets in the Reorganization, than by continuing to operate the Funds separately. The Manager believes that the Acquiring Fund’s investment objective and strategies make it a compatible fund within the OppenheimerFunds complex for a reorganization with the Target Fund. As a result of the similar investment objectives and strategies of the Funds, there is substantial overlap in the portfolio securities currently owned by the Funds.

Since the Funds are “fund of funds” and primarily invest in other mutual funds, they do not charge a direct management fee, but rather indirectly collect management fees through their investments in Underlying Funds. As shown in the fee tables below, based on assets as of January 31, 2012, the Acquired Fund Fees and Expenses for the Combined Fund are lower than the Target Fund. Additionally, the Total Expenses for the Target Fund’s shareholders will generally decrease following the Reorganization.

Consistent with the flexibility permitted by each Fund’s investment strategies, the portfolio management team is generally managing the Funds in a substantially similar manner. In particular, as of March 31, 2012, 99.98% of the Target Fund’s assets were invested in securities that were also held by the Acquiring Fund and 99.76% of the Acquiring Fund's assets were invested in securities that were also held by the Target Fund.

The Board of the Target Fund reviewed and discussed with the Manager and the Board’s independent legal counsel the proposed Reorganization. Information with respect to, but not limited to, each Fund’s respective investment objectives and policies, advisory fees, distribution fees and other operating expenses, historical performance and asset size, was also considered by the Board of the Target Fund.

Based on the considerations discussed above and the reasons more fully described under “Information About the Proposed Reorganization—Board Consideration of the Reorganization,” the Board of the Target Fund, including all of the Board members (each, a “Board Member”) who are not “interested persons” of the Funds under the Investment Company Act (the “Independent Board Members”), has unanimously concluded that participation in the Reorganization of the Target Fund is in the best interests of the Target Fund and its shareholders and that the interests of the Target Fund’s existing shareholders would not be diluted as a result of the Reorganization. The Board, therefore, is hereby submitting the Reorganization Agreement to the shareholders of the Target Fund and recommending that shareholders of the Target Fund vote “FOR” the Reorganization Agreement effecting the Reorganization. The Board of the Acquiring Fund has also approved the Reorganization on behalf of the Acquiring Fund. Shareholders of the Acquiring Fund do not vote on the Reorganization.

THE BOARD, INCLUDING ALL OF THE INDEPENDENT BOARD MEMBERS, RECOMMENDS THAT YOU VOTE “FOR” APPROVAL OF THE REORGANIZATION AGREEMENT.

Investment Objectives and Principal Investment Strategies

Investment Objectives. The investment objectives of the Funds are similar. The current investment objective of the Target Fund is to seek income and secondarily capital growth. The investment objective of the Acquiring Fund is to seek current income with a secondary objective of long-term growth of capital. The investment objective of each Fund is non-fundamental, which means it may be changed without the approval of the Fund’s shareholders. Should each Fund’s Board determine that the investment objective of the Fund should be changed, shareholders must be given advance notice before any such change is implemented. Certain investment objectives and strategies of the Underlying Funds are fundamental policies and others are non-fundamental policies, as indicated in each Underlying Fund's prospectus or Statement of Additional Information. Each Underlying Fund's Board can change non-fundamental policies without shareholder approval, including without the approval of the Fund.

Principal Investment Strategies. The Target Fund and the Acquiring Fund employ substantially similar principal investment strategies in achieving their respective objectives. The similarities and differences of the principal investment strategies of the Funds are described in the chart below.

|

Target Fund

|

Acquiring Fund

|

|

Principal Investment Strategies

|

|

|

The Fund is a special type of mutual fund known as a “fund of funds” because it primarily invests in other mutual funds. Those funds are referred to as the “Underlying Funds.” To accommodate a range of investor preferences and retirement time horizons, the Oppenheimer LifeCycle Funds offer seven funds with different asset allocations. Each of those funds is

managed based on an approximate retirement year (the “transition” date in each fund’s name) and their investments in the Underlying Funds change over time in a manner designed to help the Fund become more conservative both as the transition date gets closer and for 10 years after that date. This approach is designed to help investors accumulate the assets needed to generate income during their retirement years.

Choosing a fund with an earlier transition date generally represents a more conservative choice; choosing a Fund with a later transition date generally represents a more aggressive choice. The Transition 2010 Fund had the earliest transition date of the seven LifeCycle funds. Although it has passed its transition date, the Fund’s asset allocations will continue to change over the next 10 years, as illustrated in its “glide path” shown below, and then remain at its final allocation targets. The Fund has, and is expected to continue to maintain, some equity exposure. Equity securities generally have higher risks, however they have historically offered higher rates of return than fixed-income securities over the long term, and may play a role both in preparing for and during retirement.

The Fund currently allocates its assets among the Underlying Funds based on asset allocation targets of approximately 30% in U.S. equities, 8% in foreign equities, 43% in U.S. fixed-income, 9% in foreign fixed-income and 10% in alternatives funds that are designed to help provide asset diversification.

The portfolio managers may use some or all of the Underlying Funds in different combinations to implement the Fund’s target allocations and the relative mix of those Underlying Funds will vary over time. The current target allocations for individual Underlying Funds are provided below in the Comparison.

Equity securities include common stock, preferred stock, rights and warrants, and securities convertible into common stock. Fixed income securities (also referred to as “debt securities”) represent money borrowed by the issuer that must be repaid. Some Underlying Funds invest in debt securities that are rated below investment grade (commonly referred to as “junk bonds”) and certain of them may invest most or a significant percentage of their assets in those securities. Some of the Underlying Funds invest partially or primarily in securities of issuers outside of the United States, including issuers in emerging or developing markets countries. The alternatives Underlying Funds that are used for asset diversification may invest in commodities, gold and other special metals, real estate (including through equity

or other securities) or in inflation protected securities. For temporary periods, the Fund may hold a greater portion of its assets in money market funds, money market securities, cash or other similar, liquid investments. This may occur at times when the Manager is unable to immediately invest cash received from purchases of Fund shares or from redemptions of its investments.

|

The Fund is a special type of mutual fund known as a "fund of funds" because it invests in other mutual funds. Those funds are referred to as the "Underlying Funds." Under normal market conditions, the Fund will invest in shares of some or all of the following Underlying Funds that were chosen based on the Manager's determination that they could provide income and, secondarily, long-term growth of capital: Oppenheimer Capital Appreciation Fund, Oppenheimer Champion Income Fund, Oppenheimer Commodity Strategy Total Return Fund, Oppenheimer Core Bond Fund, Oppenheimer Developing Markets Fund, Oppenheimer Discovery Fund, Oppenheimer Global Fund, Oppenheimer Global Opportunities Fund, Oppenheimer Gold & Special Minerals Fund, Oppenheimer Institutional Money Market Fund, Oppenheimer International Bond Fund, Oppenheimer International Growth Fund, Oppenheimer International Small Company Fund, Oppenheimer International Value Fund, Oppenheimer Limited-Term Government Fund, Oppenheimer Main Street Fund,® Oppenheimer Main Street Select Fund,® Oppenheimer Main Street Small- & Mid-Cap Fund,® Oppenheimer Master Inflation Protected Securities Fund, LLC, Oppenheimer Master International Value Fund, LLC, Oppenheimer Master Loan Fund, LLC, Oppenheimer Real Estate Fund, Oppenheimer Rising Dividends Fund, Oppenheimer Small- & Mid-Cap Value Fund, Oppenheimer U.S. Government Trust and Oppenheimer Value Fund.

Equity securities include common stock, preferred stock, rights and warrants, and securities convertible into common stock. Fixed-income securities (also referred to as "debt securities") represent money borrowed by the issuer that must be repaid. Some Underlying Funds invest in debt securities that are rated below investment grade (commonly referred to as "junk bonds") and certain of them may invest most or a significant percentage of their assets in those securities. Some of the Underlying Funds invest partially or primarily in securities of issuers outside of the United States, including issuers in emerging or developing markets. The Underlying Funds that are used for asset diversification may include investments related to commodities, gold and other special metals, real estate or that are inflation protected.

For temporary periods, the Fund may hold a portion of its assets in cash, money market securities or other similar, liquid investments. This will generally occur at times when the Manager is unable to immediately invest cash received from purchases of Fund shares or from redemptions of other investments.

|

|

How Securities are Selected

|

|

|

Investments in individual Underlying Funds are determined by the Manager in seeking to meet the Fund’s asset allocation targets and achieve its investment objective. The Fund’s actual asset allocations will usually change daily, based on changes in the market values of the securities held by the Underlying Funds, and they will generally vary from the Fund’s target allocations. The Manager monitors the Underlying Fund selections and periodically rebalances the Fund’s investments to bring them closer to their target asset allocations.

The Fund’s most recent month-end investments in the individual Underlying Funds are available on its website. Its quarter-end asset allocations to the individual Underlying Funds are also available in its Annual and Semi-Annual Reports and in its Forms N-Q. In response to changing market or economic conditions, the Manager may change the Underlying Funds or the Fund’s target asset allocations at any time, without prior approval from or notice to shareholders.

Under normal market conditions, the Fund will invest in shares of some or all of the following Underlying Funds that were chosen based on the Manager’s determination that they may provide income and secondarily capital growth: Oppenheimer Capital Appreciation Fund, Oppenheimer Champion Income Fund, Oppenheimer Commodity Strategy Total Return Fund, Oppenheimer Core Bond Fund, Oppenheimer Developing Markets Fund, Oppenheimer Discovery Fund, Oppenheimer Global Fund, Oppenheimer Global Opportunities Fund, Oppenheimer Gold & Special Minerals Fund, Oppenheimer Institutional Money Market Fund, Oppenheimer International Bond Fund, Oppenheimer International Growth Fund, Oppenheimer International Small Company Fund, Oppenheimer International Value Fund, Oppenheimer Limited-Term Government Fund, Oppenheimer Main Street Fund®, Oppenheimer Main Street Select Fund®, Oppenheimer Main Street Small- & Mid-Cap Fund®, Oppenheimer Real Estate Fund, Oppenheimer Rising Dividends Fund, Oppenheimer Small- & Mid- Cap Value Fund, Oppenheimer Master Inflation Protected Securities Fund, LLC, Oppenheimer Master Loan Fund, LLC, Oppenheimer Master International Value, LLC, Oppenheimer U.S. Government Trust and Oppenheimer Value Fund. At times, the Fund may invest in other Oppenheimer funds, including Oppenheimer money market funds.

The transition date represents an approximate retirement date and investors may plan to retire either before or after that date. Some investors may choose to stop making additional contributions to the Fund or to withdraw some or all of their investment at the transition date, however, the Fund’s glide path is intended to continue after the transition date to an allocation designed to place greater emphasis on income and to seek to reduce investors’ overall risks through their retirement years.

Approximately 10 years after the Fund’s stated “transition” year, the Fund’s asset allocation will reach and remain at approximately 15% in U.S. equities, 3% in foreign equities, 61% in U.S. fixed-income, 11% in foreign fixed-income and 10% in alternatives funds (which may result in up to 10% additional equity exposure).

|

The Manager seeks to diversify the Fund's assets by selecting Underlying Funds with different investment guidelines and styles. Under normal market conditions, the Fund allocates its assets among the Underlying Funds based on asset allocation target ranges of 60-70% in fixed-income funds, 20-25% in U.S. equity funds, up to 5% in foreign equity funds and up to 15% in alternatives funds that provide asset diversification. The Fund's asset allocation targets may vary in particular cases and may change over time.

The Manager monitors the Underlying Fund selections and periodically rebalances the Fund's investments to bring them back within their target asset allocation ranges. In response to changing market or economic conditions, the Manager may change the Underlying Funds or the Fund's target asset allocation ranges at any time, without prior approval from or notice to shareholders.

|

|

Who is the Fund Designed For?

|

|

|

The Fund is designed primarily for investors seeking to simplify the accumulation of assets prior to and during retirement. Investors must weigh many factors when considering retirement, including when to retire, what their retirement needs will be, and what other sources of income they may have. In general, the Fund's investment program assumes a retirement age of 65 but the transition date does not necessarily represent the specific year you intend to retire or start drawing retirement assets. It should be used as an approximate guide, depending on your investment goals and risk tolerance. Investors should realize that the Fund is not a complete solution to their retirement needs.

|

The Fund is designed primarily for investors seeking current income and, secondarily, long-term growth of capital. Because some of the Underlying Funds invest primarily in stocks, those investors should be willing to assume the risks of share price fluctuations of stock investments. The Fund is not a complete investment program. You should carefully consider your own investment goals and risk tolerance before investing in the Fund.

|

Comparison. As shown in the chart above, the Target Fund’s current investment objective focuses on seeking income and secondarily capital growth. Similarly, the Acquiring Fund seeks current income with a secondary objective of long-term growth of capital. These investment objectives are similar in that each Fund is designed to provide total return (or a combination of growth of capital and current income). Each Fund employs substantially similar investment strategies in order to achieve their respective investment objectives, by investing in both equity and fixed income funds. The Funds are both “fund of funds” because they primarily invest in other Underlying Funds. The one primary difference in management style is that the Target Fund’s portfolio holdings in Underlying Funds are periodically rebalanced based on established “glidepaths” based on an approximate retirement year (the “transition” date in the Fund's name) in a manner designed to help the Fund become more conservative both as the transition date gets closer and for 10 years after that date. The Target Fund's allocations to various asset classes is illustrated in the following chart, which reflects an investor's need to pursue a reduction in investment risks both before and after his or her approximate retirement year.

The Target Fund currently allocates its assets among the Underlying Funds based on the following approximate asset allocation targets (rounded to the nearest percentage):

|

Underlying Funds Target Percentage

|

|

|

U.S. Equities

|

30%

|

|

Oppenheimer Value Fund

|

15%

|

|

Oppenheimer Capital Appreciation Fund

|

11%

|

|

Oppenheimer Main Street Small- & Mid-Cap Fund®

|

4%

|

|

Foreign Equities

|

8%

|

|

Oppenheimer International Growth Fund

|

4%

|

|

Oppenheimer International Value Fund

|

2%

|

|

Oppenheimer Developing Markets Fund

|

1%

|

|

U.S. Fixed-Income

|

43%

|

|

Oppenheimer Core Bond Fund

|

21%

|

|

Oppenheimer Limited-Term Government Fund

|

15%

|

|

Oppenheimer Champion Income Fund

|

3%

|

|

Oppenheimer Institutional Money Market Fund

|

3%

|

|

Foreign Fixed-Income

|

9%

|

|

Oppenheimer International Bond Fund

|

9%

|

|

Alternatives

|

10%

|

|

Oppenheimer Master Inflation Protected Securities Fund, LLC

|

4%

|

|

Oppenheimer Commodity Strategy Total Return Fund

|

4%

|

|

Oppenheimer Real Estate Fund

|

1%

|

|

Oppenheimer Gold & Special Minerals Fund

|

1%

|

In contrast, the Acquiring Fund contains generally static Underlying Fund allocations designed to fit an appropriate risk portfolio. Instead of a “glidepath,” under normal market conditions the Acquiring Fund will allocate its assets among the Underlying Funds based on asset allocation target ranges of 20-25% in U.S. equity funds, up to 5% in foreign equity funds, 60-70% in fixed-income funds and up to 15% in alternatives funds that provide asset diversification. The Acquiring Fund's asset allocation targets may vary in particular cases and may change over time.

The Target Fund and the Acquiring Fund may invest in generally the same Underlying Funds. In addition, at times, the Funds may invest in other Oppenheimer mutual funds, including Oppenheimer money market funds. With respect to each Fund, the mix of the Underlying Funds was chosen to seek diversification and to implement the Fund's allocation strategies. The choice of the Underlying Funds, the objectives and policies of the Underlying Funds and the Fund's allocations to the Underlying Funds may change from time to time without approval by the Fund's shareholders.

Notwithstanding the differences in the investment strategies of the Funds, as noted above, because of the similar investment objectives and substantially similar investment strategies there is substantial overlap in the portfolio securities currently owned by the Funds. Consistent with the flexibility permitted by each Fund’s investment strategies, the portfolio management teams are generally managing the Funds in a substantially similar manner. The portfolio managers are also identical for the Funds. Alan Gilston and Krishna Memani are the portfolio managers of the Target Fund and the Acquiring Fund. The portfolio management team of the Acquiring Fund is expected to manage the Combined Fund after the Reorganization. In particular, as noted above, as of March 31, 2012, 99.98% of the Target Fund’s assets were invested in securities that were also held by the Acquiring Fund and 99.76% of the Acquiring Fund’s assets were invested in securities that were also held by the Target Fund. The portfolio managers of the Acquiring Fund have reviewed the portfolio holdings of the Target Fund and do not anticipate disposing of, or requesting the disposition of, any material portion of the assets of the Target Fund in preparation for, or as a result of, the Reorganization. Thus, the proposed Reorganization is not expected to cause significant portfolio turnover or transaction expenses associated with the sale of securities held by the Target Funds

Fees and Expenses

The tables below compare the fees and expenses of each class of shares of the Funds, assuming the Reorganization had taken place on January 31, 2012 and the estimated pro forma fees and expenses attributable to each class of shares of the Combined Fund’s Pro Forma combined portfolio. Future fees and expenses may be greater or less than those indicated below. For information concerning the net assets of each Fund as of January 31, 2012, see “Additional Information About the Funds - Capitalization of the Funds.” You may qualify for sales charge discounts if you (or you and your spouse) invest, or agree to invest in the future, at least $25,000 in certain funds in the Oppenheimer family of funds. More information about these and other discounts is available from your financial professional and in the section “About Your Account” in the Acquiring Fund Prospectus, and is incorporated herein by reference and in the sections “How to Buy Shares” and “Appendix A” of the Acquiring Fund SAI, which is incorporated herein by reference.

Fee Tables of the Target Fund, the Acquiring Fund, and the Combined Fund (as of January 31, 2012 (unaudited)

|

Target Fund

Class A

|

Acquiring Fund

Class A

|

Acquiring Fund Pro Forma Combined Fund

Class A

|

|

|

Shareholder Fees (fees paid directly from your investment)

|

|||

|

Maximum Sales Charge (Load) imposed on purchases (as a % of offering price)

|

5.75%

|

5.75%

|

5.75%

|

|

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds)

|

None1

|

None1

|

None1

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|||

|

Management Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Distribution and/or Service (12b-1) Fees

|

0.25%

|

0.25%

|

0.25%

|

|

Other Expenses

|

0.26%

|

0.22%

|

0.21%

|

|

Acquired Fund Fees and Expenses

|

0.66%

|

0.63%

|

0.63%

|

|

Total Annual Fund Operating Expenses

|

1.17%

|

1.10%

|

1.09%

|

|

Fee Waiver and/or Expense Reimbursement

|

0.00%

|

(0.10)%5

|

(0.10)%5

|

|

Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement

|

1.17%

|

1.00%

|

0.99%

|

|

Target Fund

Class B

|

Acquiring Fund

Class B

|

Acquiring Fund Pro Forma Combined Fund

Class B

|

|

|

Shareholder Fees (fees paid directly from your investment)

|

|||

|

Maximum Sales Charge (Load) imposed on purchases (as a % of offering price)

|

None

|

None

|

None

|

|

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds)

|

5.00%2

|

5.00%2

|

5.00%2

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|||

|

Management Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Distribution and/or Service (12b-1) Fees

|

1.00%

|

1.00%

|

1.00%

|

|

Other Expenses

|

0.45%

|

0.33%

|

0.33%

|

|

Acquired Fund Fees and Expenses

|

0.66%

|

0.63%

|

0.63%

|

|

Total Annual Fund Operating Expenses

|

2.11%

|

1.96%

|

1.96%

|

|

Fee Waiver and/or Expense Reimbursement

|

0.00%

|

(0.10)%5

|

(0.10)%5

|

|

Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement

|

2.11%

|

1.86%

|

1.86%

|

|

Target Fund

Class C

|

Acquiring Fund

Class C

|

Acquiring Fund Pro Forma Combined Fund

Class C

|

|

|

Shareholder Fees (fees paid directly from your investment)

|

|||

|

Maximum Sales Charge (Load) imposed on purchases (as a % of offering price)

|

None

|

None

|

None

|

|

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds)

|

1.00%3

|

1.00%3

|

1.00%3

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|||

|

Management Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Distribution and/or Service (12b-1) Fees

|

1.00%

|

1.00%

|

1.00%

|

|

Other Expenses

|

0.42%

|

0.23%

|

0.24%

|

|

Acquired Fund Fees and Expenses

|

0.66%

|

0.63%

|

0.63%

|

|

Total Annual Fund Operating Expenses

|

2.08%

|

1.86%

|

1.87%

|

|

Fee Waiver and/or Expense Reimbursement

|

0.00%

|

(0.10)%5

|

(0.11)%5,6

|

|

Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement

|

2.08%

|

1.76%

|

1.76%

|

|

Target Fund

Class N

|

Acquiring Fund

Class N

|

Acquiring Fund Pro Forma Combined Fund

Class N

|

|

|

Shareholder Fees (fees paid directly from your investment)

|

|||

|

Maximum Sales Charge (Load) imposed on purchases (as a % of offering price)

|

None

|

None

|

None

|

|

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds)

|

1.00%4

|

1.00%4

|

1.00%4

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|||

|

Management Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Distribution and/or Service (12b-1) Fees

|

0.50%

|

0.50%

|

0.50%

|

|

Other Expenses

|

0.32%

|

0.26%

|

0.25%

|

|

Acquired Fund Fees and Expenses

|

0.66%

|

0.63%

|

0.63%

|

|

Total Annual Fund Operating Expenses

|

1.48%

|

1.39%

|

1.38%

|

|

Fee Waiver and/or Expense Reimbursement5

|

0.00%

|

(0.10)%5

|

(0.10)%5

|

|

Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement

|

1.48%

|

1.29%

|

1.28%

|

|

Target Fund

Class Y

|

Acquiring Fund

Class Y

|

Acquiring Fund Pro Forma Combined Fund

Class Y

|

|

|

Shareholder Fees (fees paid directly from your investment)

|

|||

|

Maximum Sales Charge (Load) imposed on purchases (as a % of offering price)

|

None

|

None

|

None

|

|

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds)

|

None

|

None

|

None

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|||

|

Management Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Distribution and/or Service (12b-1) Fees

|

None

|

None

|

None

|

|

Other Expenses

|

0.36%

|

0.16%

|

0.16%

|

|

Acquired Fund Fees and Expenses

|

0.66%

|

0.63%

|

0.63%

|

|

Total Annual Fund Operating Expenses

|

1.02%

|

0.79%

|

0.79%

|

|

Fee Waiver and/or Expense Reimbursement5

|

0.00%

|

(0.10)%

|

(0.10)%

|

|

Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement

|

1.02%

|

0.69%

|

0.69%

|

|

1.

|

A Class A contingent deferred sales charge may apply to redemptions of investments of $1 million or more or to certain retirement plan redemptions.

|

|

2.

|

Applies to redemptions in the first year after purchase. The contingent deferred sales charge gradually declines from 5.00% to 1.00% during years one through six and is eliminated after that.

|

|

3.

|

Applies to shares redeemed within 12 months of purchase.

|

|

4.

|

May apply to shares redeemed within 18 months of a retirement plan's first purchase of Class N shares.

|

|

5.

|

The Manager of the Acquiring Fund has voluntarily agreed to waive fees and/or reimburse certain Fund expenses at an annual rate of 0.10% as calculated on the daily net assets of the Acquiring Fund. This fee waiver and/or expense limitation may not be amended or withdrawn until one year from the date of the Acquiring Fund’s current Prospectus.

|

|

6.

|

The Manager has voluntarily agreed to waive fees and/or reimburse the Combined Fund for certain expenses in order to limit "Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement" (excluding any applicable dividend expense, taxes, interest and fees from borrowing, any subsidiary expenses, Acquired Fund Fees and Expenses, brokerage commissions, extraordinary expenses and certain other Fund expenses) so that such expenses of the Combined Fund do not exceed those of the Acquiring Fund to the extent any difference is attributed to the Reorganization. This fee waiver and/or expense limitation may not be amended or withdrawn until one year from the Closing Date of the Reorganization.

|

Example

This Example is intended to help you compare the cost of investing in the relevant Fund with the cost of investing in other mutual funds. This Example assumes that you invest $10,000 in the Funds for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

|

If shares are redeemed1:

|

1 Year

|

3 Years

|

5 Years

|

10 Years

|

|

Target Fund Class A

|

$688

|

$927

|

$1,185

|

$1,921

|

|

Acquiring Fund Class A

|

$672

|

$897

|

$1,140

|

$1,836

|

|

Acquiring Fund Pro Forma Combined Fund Class A

|

$671

|

$894

|

$1,135

|

$1,825

|

|

If shares are not redeemed2:

|

||||

|

Target Fund Class A

|

$688

|

$927

|

$1,185

|

$1,921

|

|

Acquiring Fund Class A

|

$672

|

$897

|

$1,140

|

$1,836

|

|

Acquiring Fund Pro Forma Combined Fund Class A

|

$671

|

$894

|

$1,135

|

$1,825

|

|

If shares are redeemed1:

|

1 Year

|

3 Years

|

5 Years

|

10 Years3

|

|

Target Fund Class B

|

$716

|

$968

|

$1,346

|

$1,998

|

|

Acquiring Fund Class B

|

$691

|

$911

|

$1,258

|

$1,864

|

|

Acquiring Fund Pro Forma Combined Fund Class B

|

$691

|

$911

|

$1,258

|

$1,859

|

|

If shares are not redeemed2:

|

||||

|

Target Fund Class B

|

$216

|

$668

|

$1,146

|

$1,998

|

|

Acquiring Fund Class B

|

$191

|

$611

|

$1,058

|

$1,864

|

|

Acquiring Fund Pro Forma Combined Fund Class B

|

$191

|

$611

|

$1,058

|

$1,859

|

|

If shares are redeemed1:

|

1 Year

|

3 Years

|

5 Years

|

10 Years

|

|

Target Fund Class C

|

$313

|

$658

|

$1,130

|

$2,435

|

|

Acquiring Fund Class C

|

$280

|

$580

|

$1,006

|

$2,191

|

|

Acquiring Fund Pro Forma Combined Fund Class C

|

$280

|

$582

|

$1,010

|

$2,201

|

|

If shares are not redeemed2:

|

||||

|

Target Fund Class C

|

$213

|

$658

|

$1,130

|

$2,435

|

|

Acquiring Fund Class C

|

$180

|

$580

|

$1,006

|

$2,191

|

|

Acquiring Fund Pro Forma Combined Fund Class C

|

$180

|

$582

|

$1,010

|

$2,201

|

|

If shares are redeemed:

|

1 Year

|

3 Years

|

5 Years

|

10 Years

|

|

Target Fund Class N

|

$252

|

$471

|

$814

|

$1,781

|

|

Acquiring Fund Class N

|

$232

|

$433

|

$756

|

$1,671

|

|

Acquiring Fund Pro Forma Combined Fund Class N

|

$231

|

$430

|

$751

|

$1,660

|

|

If shares are not redeemed:

|

||||

|

Target Fund Class N

|

$152

|

$471

|

$814

|

$1,781

|

|

Acquiring Fund Class N

|

$132

|

$433

|

$756

|

$1,671

|

|

Acquiring Fund Pro Forma Combined Fund Class N

|

$131

|

$430

|

$751

|

$1,660

|

|

If shares are redeemed:

|

1 Year

|

3 Years

|

5 Years

|

10 Years

|

|

Target Fund Class Y

|

$105

|

$326

|

$566

|

$1,254

|

|

Acquiring Fund Class Y

|

$71

|

$243

|

$431

|

$972

|

|

Acquiring Fund Pro Forma Combined Fund Class Y

|

$71

|

$243

|

$431

|

$972

|

|

If shares are not redeemed:

|

||||

|

Target Fund Class Y

|

$105

|

$326

|

$566

|

$1,254

|

|

Acquiring Fund Class Y

|

$71

|

$243

|

$431

|

$972

|

|

Acquiring Fund Pro Forma Combined Fund Class Y

|

$71

|

$243

|

$431

|

$972

|

|

1.

|

In the “If shares are redeemed” examples, expenses include the initial sales charge for Class A and the applicable Class B and Class C contingent deferred sales charges.

|

|

2.

|

In the “If shares are not redeemed” examples, the Class A expenses include the initial sales charge, but Class B and Class C expenses do not include the contingent deferred sales charges.

|

|

3.

|

Class B expenses for years 7 through 10 are based on Class A expenses, since Class B shares automatically convert to Class A shares 72 months after purchase.

|

Portfolio Turnover. Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect each Fund’s performance. During its most recent fiscal year, each Fund had the following portfolio turnover rate:

|

Fund

|

Fiscal Year End

|

Rate

|

|

Target Fund

|

February 29, 2012

|

22%

|

|

Acquiring Fund

|

January 31, 2012

|

12%

|

U.S. Federal Income Tax Consequences of the Reorganization

The Reorganization is intended to qualify as a tax-free reorganization for U.S. federal income tax purposes. As a result, it is expected that shareholders of the Target Fund will not recognize any gain or loss for U.S. federal income tax purposes as a result of the exchange of their Target Fund shares for shares of the Acquiring Fund in the Reorganization, that the aggregate tax basis of the Acquiring Fund shares received by each Target Fund shareholder in the Reorganization will be the same as the aggregate tax basis of the shareholder’s Target Fund shares exchanged therefor, and that the holding period of each Target Fund shareholder in the shares of the Acquiring Fund received in the Reorganization will include the period during which such shareholder held the Target Fund shares exchanged therefor, if such Target Fund shares were held as a capital asset at the time of the Reorganization. In addition, it is expected that the Target Fund will not recognize any gain or loss by reason of the transfer of all of its assets in exchange for shares of the Acquiring Fund and the assumption of all of its liabilities by the Acquiring Fund in the Reorganization, or upon distribution to its shareholders of shares of the Acquiring Fund in the Reorganization. You should, however, consult your tax advisor regarding the effect, if any, of the Reorganization to you in light of your individual circumstances. You should also consult your tax advisor about state and local tax consequences of the Reorganization.

For further information about the tax consequences of the Reorganization, please see the section titled “Information About the Reorganization – Material U.S. Federal Income Tax Consequences of the Reorganization.”

Purchase, Exchange, Redemption and Valuation of Shares

Procedures for the purchase, exchange, redemption and valuation of shares of the Target Fund and the Acquiring Fund are identical. For more information about these procedures, see below under “Comparison of the Funds – Purchase, Exchange, Redemption and Valuation of Shares.”

COMPARISON OF THE FUNDS

Principal Investment Risks

As a result of their similar investment objectives and substantially similar investment strategies, the Target Fund and the Acquiring Fund are subject to substantially similar principal investment risks associated with an investment in the relevant Fund. The following comparison shows the principal risks that apply to both of the Funds and the principal risks that are unique to each Fund.

The principal risks that apply to each Fund are set out below:

Principal Risks. The price of the Fund's shares can go up and down substantially. The value of the Fund's investments may change because of broad changes in the markets in which the Underlying Funds invest, because of Underlying Fund investment selection or the Fund's asset allocation, which could cause the Fund to underperform other funds with similar objectives. There is no assurance that the Fund will achieve its investment objective. When you redeem your shares, they may be worth more or less than what you paid for them. These risks mean that you can lose money by investing in the Fund.

The following summarizes the main risks that the Fund is subject to based on its investments in the Underlying Funds. The risks described below are risks to the Fund's overall portfolio. These are generally different from the main risks of any one Underlying Fund. While each Underlying Fund has its own particular risk characteristics, the strategy of allocating the Fund's assets to different Underlying Funds may allow those risks to be offset to some extent.

Main Risks of Investing in the Underlying Funds. Each of the Underlying Funds has its own investment risks, and those risks can affect the value of the Fund's investments and therefore the value of the Fund's shares. To the extent that the Fund invests more of its assets in one Underlying Fund than in another, it will have greater exposure to the risks of that Underlying Fund. The investment objective and principal investment strategies of each of the Underlying Funds are described in the section “More Information About the Underlying Funds” which is attached as Exhibit C. There is no guarantee that the Fund or any Underlying Fund will achieve its investment objective. The Underlying Funds will each pursue their investment objectives and policies without the approval of the Fund. If an Underlying Fund were to change its investment objective or policies, the Fund may be forced to sell its shares of that Underlying Fund at a disadvantageous time. The prospectuses and Statements of Additional Information of the Underlying Funds are available without charge by calling toll free at 1.800.225.5677 and can also be viewed and downloaded on the OppenheimerFunds website at www.oppenheimerfunds.com.

Allocation Risk. The Fund's ability to achieve its investment objective depends largely upon selecting the best mix of Underlying Funds. There is the risk that the Manager's evaluations and assumptions regarding the Underlying Funds' prospects may be incorrect in view of actual market conditions.

Market Risk. The value of the securities in which the Underlying Funds invest may be affected by changes in the securities markets. Securities markets may experience significant short-term volatility and may fall sharply at times. Different markets may behave differently from each other and U.S. markets may move in the opposite direction from one or more foreign markets.

Main Risks of Investing in Equity Securities. Stocks and other equity securities held by the Underlying Funds fluctuate in price in response to changes in equity markets in general, and at times equity securities may be very volatile. The prices of individual equity securities may not all move in the same direction or at the same time. For example, “growth” stocks may perform well under circumstances in which “value” stocks in general have fallen. Other factors may affect the price of a particular company's securities. Those factors include poor earnings reports, loss of customers, litigation, or changes in regulations affecting the company or its industry. To the extent that an Underlying Fund emphasizes investments in securities of a particular type, for example foreign stocks, stocks of small- or mid-sized companies, growth or value stocks, or stocks of companies in a particular industry, its share value may fluctuate more in response to events affecting the market for those types of securities.

Main Risks of Investing in Fixed-Income Securities. Fixed-income securities held by the Underlying Funds may be subject to credit risk, interest rate risk, prepayment risk and extension risk. Credit risk is the risk that the issuer of a security might not make interest and principal payments on the security as they become due. If an issuer fails to pay interest or to repay principal, the Underlying Fund's income or share value might be reduced. A downgrade in an issuer's credit rating or other adverse news about an issuer can reduce the market value of that issuer's securities. The value of debt securities are also subject to change when prevailing interest rates change. When prevailing interest rates fall, the values of already-issued debt securities generally rise. When prevailing interest rates rise, the values of already-issued debt securities generally fall, and they may sell at a discount from their face amount or from the amount the Underlying Fund paid for them. These fluctuations will usually be greater for longer-term debt securities than for shorter-term debt securities. When interest rates fall, debt securities may be repaid more quickly than expected and the Underlying Fund may be required to reinvest the proceeds at a lower interest rate. This is referred to as “prepayment risk.” When interest rates rise, the issuers may repay principal more slowly than expected. This is referred to as “extension risk.” Interest rate changes normally have different effects on variable or floating rate securities than they do on securities with fixed interest rates.

Fixed-Income Market Risks. Economic and other market developments can adversely affect fixed-income securities markets in the United States, Europe and elsewhere. At times, participants in debt securities markets may develop concerns about the ability of certain issuers of debt securities to make timely principal and interest payments, or they may develop concerns about the ability of financial institutions that make markets in certain debt securities to facilitate an orderly market. Those concerns can cause increased volatility in those debt securities or debt securities markets. Under some circumstances, as was the case during the latter half of 2008 and early 2009, those concerns could cause reduced liquidity in certain debt securities markets. A lack of liquidity or other adverse credit market conditions may hamper an Underlying Fund's ability to sell the debt securities in which it invests or to find and purchase suitable debt instruments.

Special Risks of Lower-Grade Securities. Lower-grade debt securities, whether rated or unrated, have greater risks than investment-grade securities. They may be subject to greater price fluctuations and have a greater risk that the issuer might not be able to pay interest and principal when due. The market for lower-grade securities may be less liquid and therefore they may be harder to value or to sell at an acceptable price, especially during times of market volatility or decline.

Main Risks of Foreign Investing. Foreign securities are subject to special risks. Foreign issuers are usually not subject to the same accounting and disclosure requirements that U.S. companies are subject to, which may make it difficult to evaluate a foreign company's operations or financial condition. A change in the value of a foreign currency against the U.S. dollar will result in a change in the U.S. dollar value of securities denominated in that foreign currency. The value of foreign investments may be affected by exchange control regulations, foreign taxes, higher transaction and other costs, delays in the settlement of transactions, changes in economic or monetary policy in the U.S. or abroad, expropriation or nationalization of a company's assets, or other political and economic factors. These risks may be greater for investments in emerging or developing market countries. Foreign securities owned by an Underlying Fund may trade on weekends or other days when the Fund and the Underlying Funds do not price their shares. As a result, the Fund's net asset value may change on days when you will not be able to purchase or redeem the Fund's shares. Fund shareholders may be unable to deduct or take a credit for foreign taxes paid by the Underlying Funds on their foreign investments.

Special Risks of Developing and Emerging Markets. The economies of developing or emerging market countries may be more dependent on relatively few industries that may be highly vulnerable to local and global changes. The governments of developing and emerging market countries may also be more unstable than the governments of more developed countries. These countries generally have less developed securities markets or exchanges, and less developed legal and accounting systems. Securities may be more difficult to sell at an acceptable price and may be more volatile than securities in countries with more mature markets. The value of developing or emerging market currencies may fluctuate more than the currencies of countries with more mature markets. Investments in developing or emerging market countries may be subject to greater risks of government restrictions, including confiscatory taxation, expropriation or nationalization of a company's assets, restrictions on foreign ownership of local companies and restrictions on withdrawing assets from the country. Investments in securities of issuers in developing or emerging market countries may be considered speculative.

Main Risks of Alternative Asset Classes. Some of the Underlying Funds seek investments in asset classes that are expected to perform differently from primary equity and fixed-income investments. Those asset classes may be volatile or illiquid however, particularly during periods of market instability, and they may not provide the expected uncorrelated returns.

Affiliated Portfolio Risk. In managing the Fund, the Manager will have authority to select and substitute Underlying Funds. The Manager may be subject to potential conflicts of interest in selecting Underlying Funds because the fees paid to it by some Underlying Funds are higher than the fees paid by other Underlying Funds. However the Manager monitors the investment process to seek to identify, address and resolve any potential issues.

The Target Fund also has the following additional principal risk:

Main Risks of Derivative Investments. Derivatives may involve significant risks. Some derivatives have the potential for unlimited loss, regardless of the size of the Fund's initial investment. Derivatives may be illiquid and may be more volatile than other types of investments. Derivative investments can increase portfolio turnover and transaction costs. Derivatives are subject to counter-party credit risk and may lose money if the issuer fails to pay the amounts due.

The risks described above form the expected overall risk profile of each Fund, respectively, and can affect the value of a Fund's investments, its investment performance and the price of its shares. The price of a Fund’s shares can go up and down substantially. The value of a Fund's investments may change because of broad changes in the markets in which the Fund invests or because of poor investment selection, which could cause the Fund to underperform other funds with similar investment objectives. There is no assurance that a Fund will achieve its investment objective. When you redeem your shares, they may be worth more or less than what you paid for them. These risks mean that you can lose money by investing in a Fund.

Fundamental Investment Restrictions

Both the Target Fund and the Acquiring Fund have certain additional fundamental investment restrictions that can only be changed with shareholder approval. Generally, these investment restrictions are similar between the Funds. However, the Target Fund is permitted to invest in real estate, physical commodities or commodity contracts to the extent permitted by the Investment Company Act (which does not prohibit such investments), whereas the Acquiring Fund has a fundamental restriction stating that it cannot purchase real estate or commodities, but may use commodity contracts approved by its Board. Please see the Statements of Additional Information for each Fund for descriptions of the current fundamental investment restrictions, which are incorporated by reference into this Combined Prospectus/Proxy Statements and the Reorganization SAI.

Performance Information

The bar charts and tables below provide some indication of the risks of investing in each Fund by showing changes in the Fund's performance from year to year and by showing how each Fund's average annual returns for 1 year, 5 years and the life of Class compare with those of two broad measures of market performance. The Fund's past investment performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. More recent performance information is available by calling the toll-free number on the back of a Fund’s prospectus and on the Funds’ website: https://www.oppenheimerfunds.com/fund/

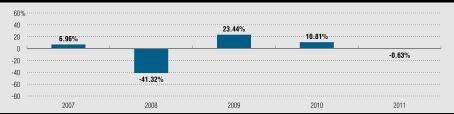

Annual Total Returns for the Target Fund (Class A) as of 12/31 each year

Sales charges and taxes are not included and the returns would be lower if they were. During the period shown, the highest return for a calendar quarter was 15.77% (2nd Qtr 09) and the lowest return was -27.00% (4th Qtr 08).

The following table shows the average annual total returns for each class of the Fund's shares. After-tax returns are calculated using the highest individual federal marginal income tax rates and do not reflect the impact of state or local taxes. Your actual after-tax returns, depending on your individual tax situation, may differ from those shown and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After-tax returns are shown for only one class and after-tax returns for other classes will vary.

|

Target Fund

|

|||

|

Average Annual Total Returns

for the periods ended December 31, 2011

|

1 Year

|

5 Years

|

Life of Class

|

|

Class A (inception 12/15/06)

Return Before Taxes

Return After Taxes on Distributions

Return After Taxes on Distributions and Sale of Fund Shares

|

(6.34)%

(6.99)%

(4.00)%

|

(4.27)%

(4.69)%

(3.75)%

|

(4.27)%

(4.69)%

(3.75)%

|

|

Class B (inception 12/15/06)

|

(6.50)%

|

(4.33)%

|

(4.17)%

|

|

Class C (inception 12/15/06)

|

(2.48)%

|

(3.93)%

|

(3.95)%

|

|

Class N (inception 12/15/06)

|

(2.03)%

|

(3.38)%

|

(3.38)%

|

|

Class Y (inception 12/15/06)

|

(0.48)%

|

(2.89)%

|

(2.90)%

|

|

S&P 500 Index

(reflects no deduction or fees, expenses or taxes)

|

2.11%

|

(0.25)%

|

0.03%*

|

|

Barclays Capital U.S. Aggregate Bond Index

(reflects no deduction for fees, expenses or taxes)

|

7.84%

|

6.50%

|

6.27%*

|

* From 11/30/06

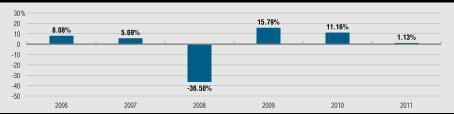

Annual Total Returns for the Acquiring Fund (Class A) as of 12/31 each year