VirtualScopics, Inc.

Annual Stockholders’ Meeting

June 12, 2012

Business

Portion of Annual Meeting Script

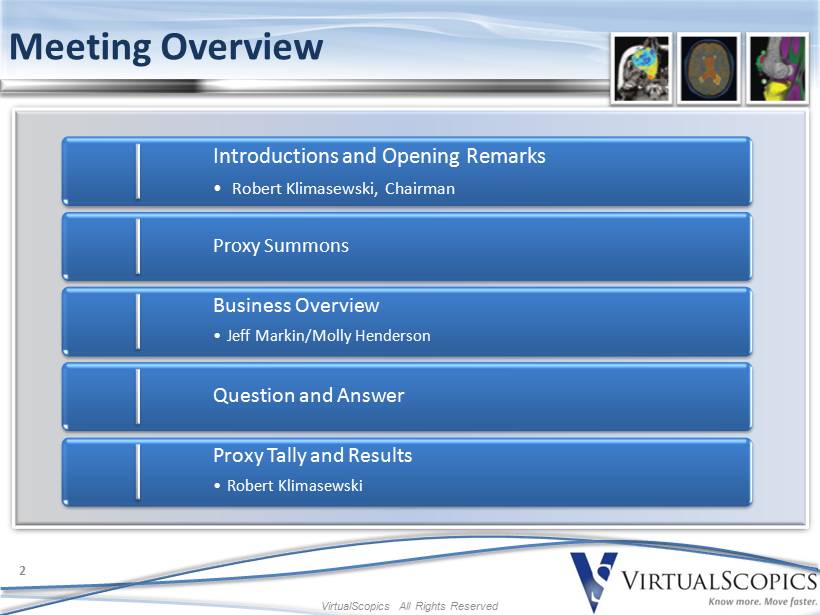

Advance to Slide 6

MARKIN:

Before I begin my prepared remarks I would like to recognize

members of the Executive Management team who are at the meeting today. They are:

Erik Jensen - Vice President of Global Marketing and Business

Development, Ron Way- Director of Operations, Nicole Vespone – Director of Quality and Regulatory Affairs, Dr. Edward Ashton

– Chief Scientific Officer, Dr. Jon Riek – Chief Technology Officer, Dr. Mark Tengowski – Vice President Regulatory

Affairs, and Colin Rhodes – Vice President Software Development. Molly and I get the opportunity to talk directly with you

about the company, working with us are a very talented and dedicated team of people who work every day to meet the needs of our

customers while building long term value in the company.

Advance to Slide 7

Molly and I will be splitting today’s

discussion. First I will provide some background as to who we are as a company, especially for people in the audience who may be

new to the company.

Then I will talk about the two businesses we are focused on;

the clinical trials business which delivers all of our sales today and then I will review the status of our entry into personalized

medicine. Molly will further the discussion on personalized medicine with a focus on commercialization and then she will take us

through a financial review including a historical summary of our performance, a look at industry comparisons and multiples along

with an update on our 2012 outlook. We will then conduct a short Q&A session.

We will be reading our prepared remarks which will be released

subsequent to the meeting.

I would ask that you hold any questions you have until the end

of our prepared remarks.

Advance to Slide 8

Fundamentally our Mission, and that of our clients, is to improve

the lives of those impacted by disease and disability. Some of these diseases impact lifestyle and quality of life like Arthritis,

while some are life threatening or life altering like cancer or Alzheimer’s. I think we can all relate to these impacts on

a very personal level. I know that our employees do on a daily basis. And it drives us to do the very best we can on each study.

Advance to Slide 9

As I said earlier our business focus is centered on two distinct

segments. First I will review our participation in the Drug development industry and during the 2nd half of my prepared

remarks I will review with Molly our participation in our emerging business in personalized medicine.

Advance to Slide 10

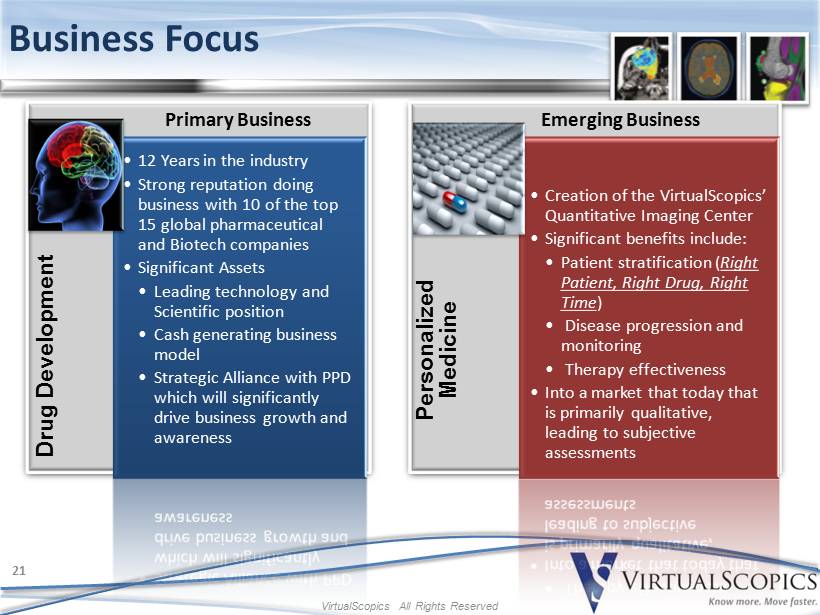

In the greater than 12 years we have been addressing the clinical

trial market we have supplied many of the world’s leading pharmaceutical, biotech, and device companies with a full suite

of medical imaging analysis services generating:

| • | A strong reputation doing business with 10 of the top 15 global pharmaceutical and Biotech companies |

| • | We have accrued some very significant assets including: |

| • | A leading technology and Scientific position in quantitative imaging |

| • | Cash generating business model |

| • | Strategic Alliance with PPD which we believe will significantly drive business growth and awareness |

While we are proud of our accomplishments and confident in our

plans within each of these markets we can also point to prominent external confirmation that supports and validates our focus in

these areas and the capabilities we bring to the table. At the end of each business segment I will review these external perspectives.

Advance to Slide 11

The ultimate goal of our customers in the clinical trials business

is to discover and commercialize new therapies to impact these life threatening or life altering diseases. These large Pharmaceutical

companies come to organizations like ours to use medical imaging technologies to tell them if patients that are participating in

their clinical trials are responding to these new drugs and if the drugs are working as intended.

We are the premier provider of quantitative image-based solutions

to these companies offering:

| · | An integrated solution delivered as a series of services that manage the imaging portion of these trials from inception to

data submission |

| · | Highly automated quantitative analysis vs. conventional qualitative radiologist driven analysis utilized by others in the industry.

Using software algorithms to measure very precisely biological structures and processes in a repeatable fashion with much lower

variability than what can be accomplished by radiologists alone. We have a world class customer base, doing business with 10 of

the 15 leading pharmaceutical, biotechnology and medical device companies |

Advance to Slide 12

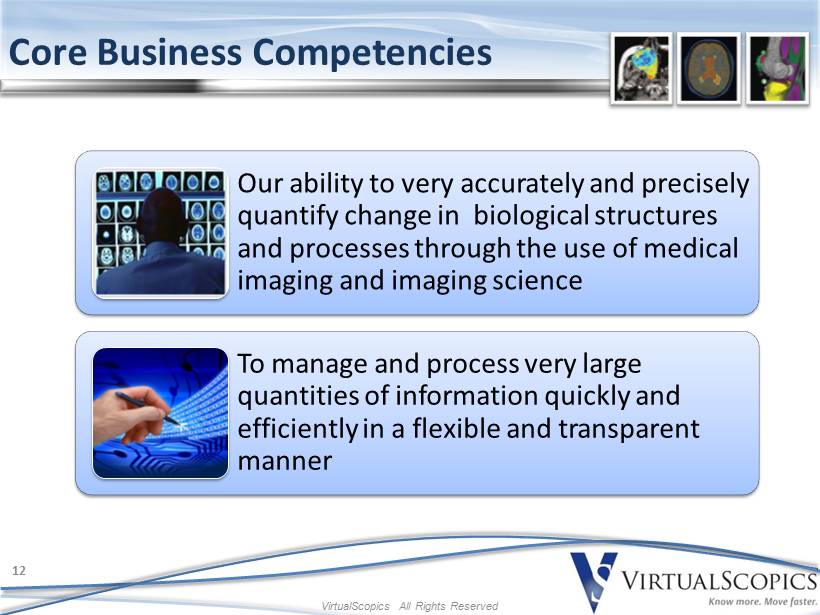

At the heart of the company our core competencies are:

| • | our ability to very accurately and precisely quantify change in biological structures |

| • | To manage and process very large quantities of information quickly and efficiently |

Each of these competencies is fundamental to our ability to

meet the needs of our clients today in the clinical trial market and is also a critical component of the company’s ability

to meet the needs of our future clients in personalized medicine.

Advance to Slide 13

For us to provide our solution to clients we need to bring together

a key set of disciplines within the company in a very coordinated fashion with full time staff. This includes imaging scientists,

MD’s, and software professionals working as an integrated team. We believe this is a key difference between ourselves and

our competitors who tend to primarily utilize consultants or purchase imaging technology externally. While this is very important

in the clinical trials business it also becomes even more important as we move into personalized medicine.

Advance to slide 14

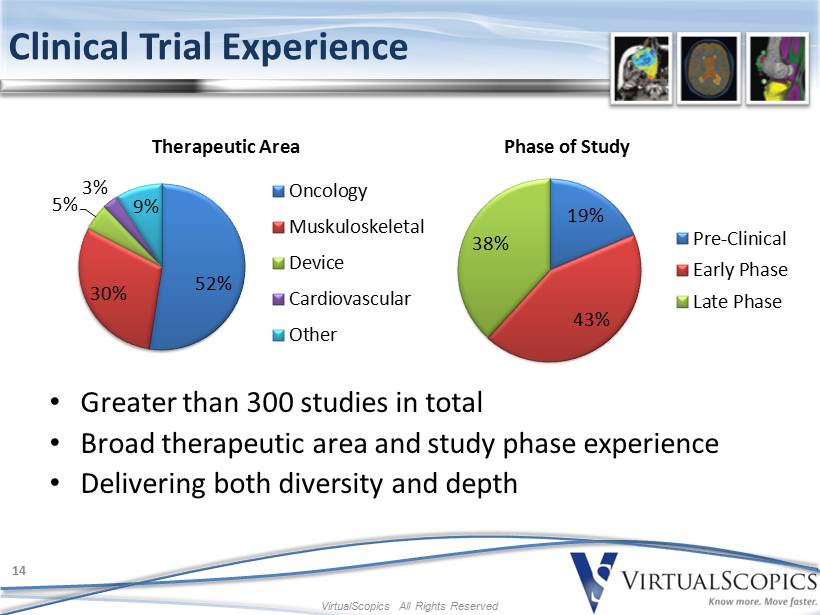

Our reputation in the industry and the maturing of our quantitative

imaging technology is a direct result of our experience in drug development. As these charts show we have worked on over 300 studies

with close to 40% of these being late phase studies. While early development is still very important to us, in fact it’s

where we have our most prominent reputation; it’s those later phase studies that will drive the most significant growth for

the company.

Having a solid reputation as both an early and late phase company

is a strong asset to leverage going forward.

Advance to slide 15

As I discussed during our February Investor Call we have 5 key

initiatives for the clinical trials business. They are:

| · | Employee Satisfaction which is important in any business but is even more critical in a services based business. |

| · | Customer Loyalty which goes beyond just satisfying our clients but working to delight them such that we become their partner

of choice |

| · | Productivity and Efficiency such that we are able to scale our processes with an increasing level of efficiency |

And the last two initiatives which go together being

| · | Bookings growth which represents signed contracts with our clients for future studies |

| · | And Expansion of the PPD partnership which is a key driver to our growth in bookings |

While the time we have today does not allow me to go into detail

on our plans in each of these areas I want to touch on Bookings Growth and the Expansion of the PPD alliance in more detail.

Advance to Slide 16

With respect to bookings growth and more generally the topic

of sales we have discussed in our last two investor calls that we experienced a slowdown in new study contracts which began to

impact our revenues towards the end of last year and has continued to impact us this year. The executive management team and the

board have spent considerable time on this situation. While I can’t go into detail on the full extent of those plans I have

listed here the general process used and some of the actions that we implemented.

To assess the problem we undertook a:

| – | Critical assessment of our strengths and weaknesses along with client interviews and an assessment of the morale and satisfaction

of our employees |

| – | We also initiated a broad set of discussions with PPD Management to identify what has worked good and what needs to change

to accelerate our collective performance |

Coming out of those discussions we initiated:

| – | Series of internal changes we implemented last year |

| – | Earlier this year we made some changes to our Business Development team to enhance focus |

| • | New Vice President of Business Development in April |

| • | Two new regionally based Directors of Business Development starting in June |

| – | Along with seven separate initiatives underway with PPD to increase the number of opportunities and our chances of winning

those opportunities |

Advance to Slide 17

Based on those assessments and the series of initiatives

completed and underway we set an objective in 2012 to double the amount of Requests for Proposals (RFPs) that we responded to through

PPD and a 50% increase in the quantity of RFPs that we drove on a direct basis through our sales team.

This slide represents the quantity of RFPs that we

responded to in the first quarter of 2012 vs. our goal in the first quarter. As you can see we are on track to deliver this increase

in RFPs which is a critical precursor to ultimately winning a growing number of projects. Let me be clear on one point though…We

understand that the goal is not just to quote on more projects we have to win them!

Advance to Slide 18

The 5th company initiative is the growth of the PPD

Alliance. As I just reviewed within the context of bookings this alliance is a very important component of our future growth. Given

that, I thought it would be worthwhile to provide a little background on them as well as a few comments on the criteria they used

to determine that we were the company they wanted to partner with as they pursued an imaging partner.

| · | PPD is a company of greater than 11,000 employees |

| · | 84 offices in 42 countries |

| · | Been in business providing development services since 1985 |

| · | They are the number 3 player in the broader CRO market |

| · | Revenue in excess of $1.4B and project backlog $3.4B |

| · | Recognized by Forbes as one of America’s best big companies |

Advance to Slide 19

From an external perspective PPD was recognized last

year with 2 important industry awards. They were the:

| • | Scrip Awards 2011 – PPD named Best Contract Research Organization and honored for Best Technological Development in Clinical

Trials |

| – | Recognized for expertise and innovation in helping clients develop life-changing medical treatments. PPD noted as “a

great organization – open for new approaches, even more for driving new technologies.” |

| • | 2011 Center Watch Global Site Survey – Rated No. 1 CRO |

| – | 84.3 percent of participants rated PPD's overall relationship quality as "excellent" or "good.” |

| – | Scored among the top three CROs in 25 of 29 survey attributes |

As you can see PPD is a very well regarded company

and one that we are very pleased to be working with in this important strategic alliance.

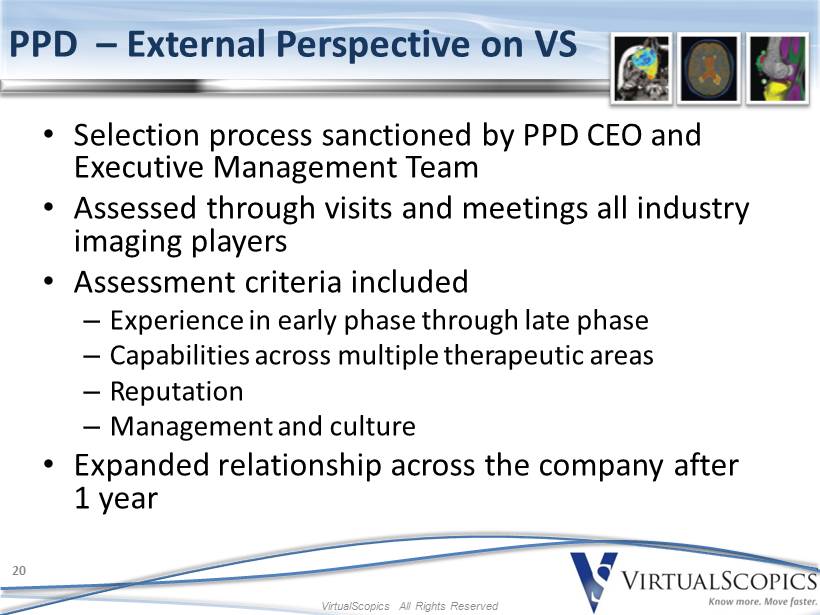

Advance to Slide 20

As I mentioned in the opening of our company update that while

we believe we have a great company with great employees, clients, and technology it is always good to have external validation

of this. To that end the process that PPD used to decide that VS was the company they wanted to partner with for imaging is a good

example of this external validation.

| • | The overall selection process sanctioned by the PPD CEO and Executive Management Team |

| • | Assessed through visits and meetings all industry imaging players |

| • | Assessment criteria included |

| – | Experience in early phase through late phase studies |

| – | Capabilities across multiple therapeutic areas |

| – | Quality of company management and a customer oriented culture |

| • | These represent many of the same attributes or assets we have discussed this morning. After their assessment of all the players

in the market they selected us as their partner. Furthermore they agreed to contractually expand the relationship from Oncology

to the other therapeutic areas they participate in. A very significant external confirmation of the company and our position in

the industry. |

Advance to Slide 21

Now I would like to move the discussion from a focus on the

clinical trials business to a review of our developing business in personalized medicine.

Advance to Slide 22

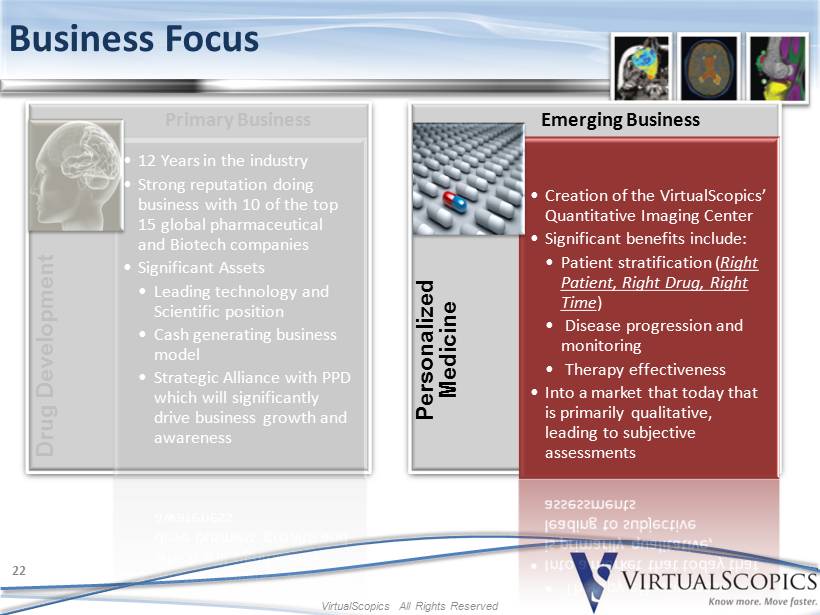

The entry to this business begins with the:

| • | Creation of the VirtualScopics’ Quantitative Imaging Center |

| • | Significant benefits include: |

| • | Patient stratification (Right Patient, Right Drug, Right Time) |

| • | Disease progression and monitoring |

| • | Into a market that today that is primarily qualitative, leading to assessments that can be subjective in nature |

Advance to Slide 23

The market opportunity we are pursuing is one that can be characterized

by providing:

| • | An emphasis on controlling the increasing cost of healthcare |

| • | Utilizing products and services that assist in patient stratification and rapid determination of efficacy or futility for expensive

therapies are critical |

| • | Securing what we believe to be significant financial returns for organizations like ours that deliver differentiated value. |

We believe Quantitative medical imaging offers significant advancements

towards these imperatives

Delivering The right treatment, for the right patient, at

the right time.

Advance to Slide 24

The benefits of quantitative imaging are

very compelling:

| · | Enable early diagnosis and drug mechanism of action confirmation |

The same three benefits we provide every day to the clinical

trial marketplace!

Yet, the majority of assessments done today

are still qualitative

Providing what we believe to be a significant opportunity to

expand the imaging market by demonstrating the benefits of quantitative imaging and showing stronger patient outcome correlation

and better economics than alternate approaches

Advance to Slide 25

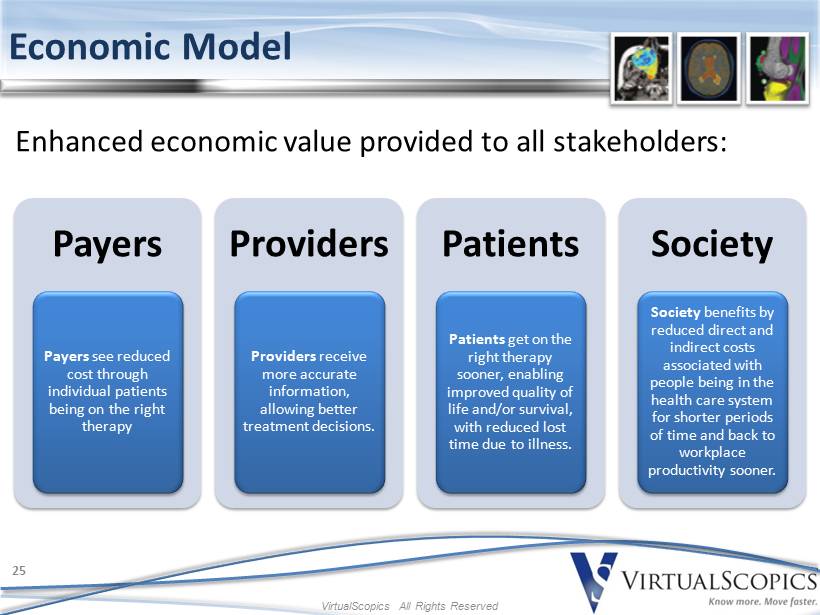

The economic model we feel is very compelling to all of the

stake holders with:

| • | Payers see reduced cost through individual patients being on the right therapy |

| • | Providers receive more accurate information, allowing better treatment decisions for their patients |

| • | Patients get on the right therapy sooner, enabling improved quality of life and/or survival, with reduced lost time due to

illness. |

| • | Society benefits by reduced direct and indirect costs associated with people being in the health care system for shorter periods

of time and back to workplace productivity sooner. |

Advance to Slide 26

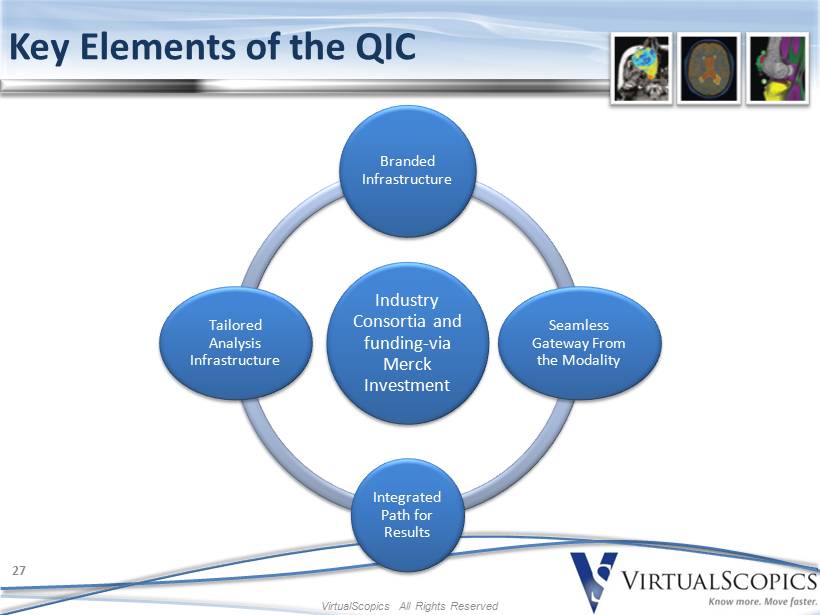

At the heart of our offering is what we are calling the Quantitative

Imaging Center (QIC).

| · | A centralized lab that receives medical images from global healthcare facilities and processes and delivers back quantitative

assessments enabling improved patient outcomes at reduced cost. We believe this center to be the first of its kind in the market. |

Advance to Slide 27

Key elements of the QIC include:

| · | Branded Infrastructure that will provide name recognition to the initiative and VirtualScopics |

| · | Seamless gateway from the imaging modality at the healthcare facility to the QIC |

| · | Integrated Path for the results of the exam to be sent back to the health care facility and the referring physician |

| · | Tailored analysis infrastructure within the QIC that can perform multiple analysis endpoints like those tailored to Oncology,

Cardiovascular Disease, and others as they become commercialized |

| · | And lastly industry consortia and funding-facilitated by our collaboration with Merck via their Investment in the company |

Advance to Slide 28

As in the example I referenced earlier with PPD, external validation

of our initiatives provides needed assistance to advance these initiatives along with a degree of confidence that we are on the

right path with a compelling opportunity. Merck Global Health Innovations provides that validation for our personalized medicine

initiative with the QIC.

These next two slides are taken from the Merck GHI website.

In this first slide they talk of developing a portfolio of opportunities

in a number of key spaces, each of which has the potential to reshape health care in the years ahead

Advance to Slide 29

In this second slide they talk of their global experience, health

care expertise and worldwide connections that significantly enhance the value of an investment from GHI.

Both of these slides underscore the importance of the Merck

as investors in the company but also the external validation of where we are heading as a company.

Advance to Slide 30

This slide outlines our key initiatives for 2012 within the

personalized medicine business

| · | Reimbursement Strategy For our DCE-MRI bloodflow measurement application which is our first product |

| · | Standalone platform infrastructure which forms the backbone of the QIC |

| · | Design and site selection for prospective trial for DCE MRI which will provide the needed scientific data for the reimbursement

authorities |

| · | Acceptance of our 510K application for blood flow measurement device which provides the regulatory pathway for us to begin

providing services |

| · | Initiation of a Scientific Advisory Board that can advise us on our commercialization product priorities as well as providing

external validation of our approach and initiatives in the clinical marketplace |

Advance to Slide 31

I would now like to turn the podium over to Molly who will Molly

will further the discussion on personalized medicine with a focus on commercialization and then she will take us through a financial

review including a historical summary of our performance, a look at industry comparisons and multiples along with an update on

our 2012 outlook.

HENDERSON:

Thanks Jeff.

Jeff discussed the concept of the quantitative imaging center,

or QIC, in support of our personalized medicine initiative. I will now provide a summary of our plan to execute our strategy to

improve patient care across the globe.

As with all products there are stages of development that the

product, in our case, a software application or application as I’ll refer to it, goes through in order to ensure it is successfully

developed, marketed and ultimately launched. By adhering to a process-driven and well planned and developed approach, the likelihood

of success significantly increases as well as the ability to detect problems and foresee issues early in the process. Early detection

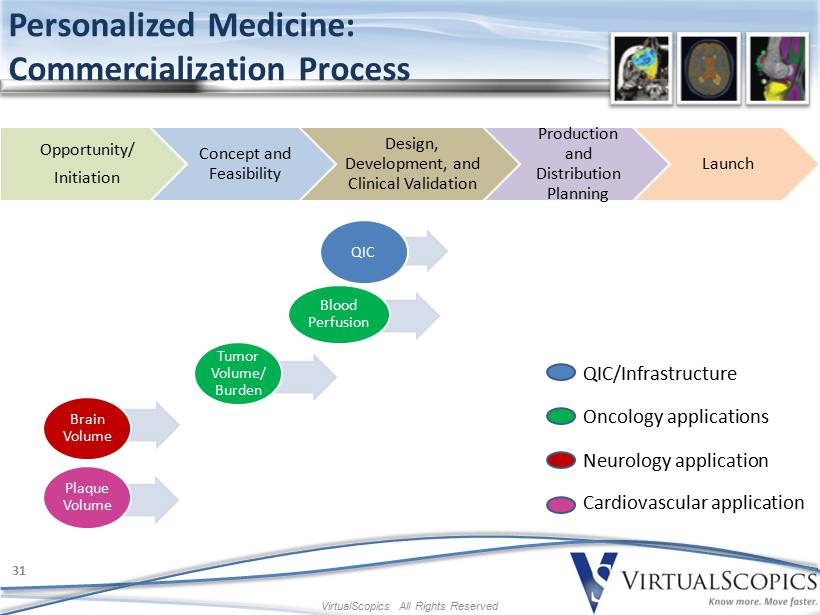

ensures critical resources aren’t wasted or key products or applications delayed. Across the top of this chart you see our

5 key elements for commercialization of our personalized medicine applications. I will touch upon each of the areas to provide

you an overview. I will follow this with an update on where we are with each of our products and the development of the infrastructure,

or QIC.

Our first stage of development begins with the opportunity and

initiation. This is where concepts are made, ideas are hashed out and brainstorming begins. For us this began over 2 years ago

as we began to assess the broader opportunities for our software technology. After many sessions on our opportunities, selected

areas for our software tools were identified as potential areas of market need. These selected areas were further researched within

the next stage of concept and feasibility. This is where we define our business objective, obtain market data, conduct market research,

review our IP positioning, develop product specifications, create a system architecture plan, explore the regulatory strategy and

requirements, perform early financial modeling and began creating a quality system framework, all in support of creating a product

that addresses a strong market need with supporting pharmacoeconomic benefits. After the feasibility and concept stage our next

steps are to begin the actual development of our applications within the regulatory and quality system framework that was determined

within the second stage. It’s stage 3 where a significant amount of the heavy lifting is done, so to speak. The application

is actually created and developed during this stage. Depending on the application, our average development lifecycle runs approximately

12-18 months. Other key activities within this stage are obtaining the clinical validation in support of demonstrating the pharmacoeconomic

benefits, developing a reimbursement strategy for obtaining a reimbursement code if one doesn’t exist, submitting the required

filings with the FDA and finalizing budgets. It’s in this stage we will also begin to develop our strategy for marketing

and distribution of the application. From a time duration standpoint, this stage is the most lengthy within our planned development

lifecycle and we estimate it can range anywhere from 2-3 years. Near the conclusion of stage 3 and as the clinical data is generated

and the results are gathered and conclusions reached, we begin our production, distribution and marketing planning.

Stage 4, which can be referred to as the milestone stage, is

where a significant amount of the external milestones are reached, specifically, FDA clearance, finalizing and publishing clinical

validation study results, completion of a quality assessment which is paramount prior to inspection from the FDA and registering

our site with the FDA. These may occur at various times but all are required for us to move to the final stage which is product

launch.

A key element of success for any medical application is obtaining

a reimbursement, or CPT code from insurance companies, which are the payers. This is a lengthy process so it’s important

to begin this as early as stage 3 but also heavily reliant upon the results from the clinical validation performed in stage 3 as

its those results which will demonstrate the pharmacoeconomics needed. The last stage is product launch, this is when marketing

plans go live, field support and the production environment is fully deployed and reimbursement contracts are negotiated and ideally

finalized. All operational, financial, IT, customer service and supporting activities are in place and functional. Although we

may pause for a brief moment to celebrate the launch, the real meaningful work is just beginning as we actually start performing

the assessments that we’ve believed will begin to help patients and physicians get an early look at the effectiveness of

the patient’s therapy.

Now that you have a sense of our commercialization process,

I’ll provide a quick summary of where we are with the overarching infrastructure, the QIC and the related products to hit

the market. Relative to the QIC we are in stage 3, we have completed the software architecture and are in the building phase. As

this is the foundation of our personalized medicine initiative it is important that we ensure that we meet the quality system requirements

and effectively plan how the system can support a scalable operation.

The first application to fall within the QIC is our blood perfusion

product which measures blood flow and vascular permeability to aid in the assessment of anti-angiogenic cancer therapies. We are

in the 3rd stage of development with this application and have begun the design phase of the clinical validation study,

filed the 510k application with the FDA and have had multiple rounds of review with the FDA. We are diligently working towards

addressing their comments and barring any additional issues raised we believe we are narrowing in on a final application. We have

also begun developing our reimbursement strategy and are working with consultants to refine the strategy in addition to forming

a payer panel whereby we will get the feedback from leading decision makers from the insurance industry on our trial design in

order to make sure the trial is designed in a way that supports the clinical utility, and the resulting pharmacoeconomic benefit

that will ultimately support a decision to provide a reimbursement code. We are also actively hiring software developers in support

of creating our standalone software application for this product which will later be installed in the QIC.

The second application we are pursuing is our tumor volume tool.

We believe the industry is poised to benefit from a more reliable and accurate assessment for cancer patients of their tumor size,

its growth, or shrinkage, and changes in response to therapy. We are into the concept and feasibility phase of this application.

We have done market assessments, research and sizing and continue to believe there is a strong need in the market for a more precise

and reliable tool to assess overall tumor burden rates and changes. The next product area we believe will have strong market need

is within the neurology, specifically Alzheimers Disease, and cardiovascular fields. The market is still maturing as it relates

to these disease areas but we believe over the next 2-5 years, imaging will play a critical role in the early diagnosis, treatment

and prevention markets for these two critical areas.

We truly believe through hard work, dedication and creativity

we will make this concept a reality and be the first global provider of quantitative image analysis in support of personalizing

medicine.

Advance to Slide 32

The next area I will discuss is our historical financial performance.

The chart on the left shows our annual revenues over the past

6 years. We have experienced steady increases in our revenues over this period driven by the heightened demand of our services.

We have found that customers most value our imaging expertise and knowledge as well as our flexible approach and accommodating

staff. The chart of the right highlights our gross profit over the past 6 years. In 2010, we began experiencing heightened pricing

pressure as a result of the consolidating pharmaceutical industry which increased the pricing leverage of these large companies

and thereby, increased the amount of discounts required in order to achieve, or maintain, select preferred provider status. Currently,

we are on the preferred provider list of 7 of the top 15 pharma and medical device companies.

Advance to Slide 33

The chart on the left shows the revenue concentration by phase

of study. Over the past six years we have significantly changed the landscape of our business. Since our inception, we have performed

work for over 300 projects accumulating to over $92 million in total project value. Through 2007, we predominately served the early

phase clinical trial market, meaning research, proof of concept studies and Phase I studies as we needed to demonstrate our capabilities

to our customers and the market. In 2008, we began gaining the confidence of our customers who then rewarded us with larger, longer

term Phase II studies. And in 2009, we received our first award of a Phase III study. That trend has continued through 2011 as

the largest component of our revenues are now from Phase III studies which have significantly higher dollar values, are longer

term and higher profile. Our strategy is to continue to develop our capabilities to support large Phase III studies as the Phase

III market represents the largest portion of the total market within imaging for clinical trials. The PPD relationship that Jeff

discussed is an important driver to successfully penetrating the Phase III market and a relationship that we continue to invest

in and cultivate.

Advance to Slide 34

The graph on the right breaks down revenues by therapeutic area.

In 2007, the majority of our revenues were generated from musculoskeletal projects. At that time, we recognized that the landscape

would change and we began seeing a reduction in pharmaceutical companies’ investment in musculoskeletal diseases, specifically

osteoarthritis. That unfolded in 2007 as many major players within the pharmaceutical industry began exiting the OA market largely

because of the adverse side effects of OA compounds. Prior to this occurring, we enhanced our investment in our Oncology products

as Oncology represented, and still does represent, the largest segment of the clinical trial market.

Today our revenue composition more closely resembles the market

from a phase and therapeutic area perspective. Our capabilities have grown significantly over the years and we will continue to

enhance our offerings so we can more broadly diversify and support the changing demands of the industry. An important focus of

ours is to continue to diversify our product mix and customer base to protect against downward forces in any one area or customer.

Advance to Slide 35

Equally important, if not more, than revenue and margin, is

cash. This slide shows the amount of cash used and generated, as in the case in 2009 through 2011, from operations (which we define

as Adjusted EBITDA) over the past six years. The several years of cash burn prior to 2009 were largely a result of the necessary

investments needed to develop our capabilities, including the required regulatory environment, to capitalize on the broader imaging

clinical trial market. Therefore, although these look like years of loss, they were essential in building the framework of the

company we are today.

As we look ahead to the remainder of 2012, we will continue

to closely monitor the rate and level of new business we are awarded and the status of our backlog to assess how we are performing

against our financial goals. As we’ve mentioned on previous earnings calls and further to Jeff’s comments today, we

experienced a slowdown in our bookings over the past 18 months which will begin to impact our quarterly results. We frequently

review these leading indicators, as well as several others, to plan our investments and expenditures and we will continue to provide

updates to the financial markets on our progress towards our financial goals.

Advance to Slide 36

In turning briefly to the financial markets. Those within these

markets often use industry multiples as a way to compare companies of different sizes within an industry. Traditional multiples

are revenues and EBITDA, meaning how many times revenue or EBITDA does it take to achieve the companies’ marketcap, or valuation.

The average revenue multiple of CRO’s, or contract research organizations, which is the industry we are in today, is 1.6x

with a range of revenue multiples of 1x – 2.3x. Meaning, 1.6 times revenues equals the marketcap. The average EBITDA multiple

is 18x with a range of 17 – 22x. We are currently trading at a 2x revenue multiple and a 21x EBITDA multiple. As we continue

to develop our personalized medicine applications and demonstrate some early successes through the achievement of some of the milestones

we have mentioned, we believe we will start trending towards the multiples closer associated with the Healthcare IT and personalized

medicine/diagnostic market. Companies within these spaces are generally afforded higher industry multiples. The average revenue

and EBITDA multiples for Healthcare IT companies are 2.5 and 6.2, respectively, and the average revenue multiple for personalized

medicine/diagnostic companies is 16, many of these companies are earlier in the revenue lifecycle and therefore are operating at

losses and therefore, do not have a meaningful EBITDA multiple. The higher multiples are afforded to these companies due to the

market opportunity, stage of development and growth projections. As we achieve milestone successes in our pursuit of this market

we would anticipate being rewarded with an industry multiples that are more consistent within these other, high growth sectors.

Advance to Slide 37

Lastly, here is a summary of our capitalization and a list of

a few of our material stockholders as of April 5, 2012, our record date. We currently have approximately 29 million shares of common

stock outstanding with another 6 million in preferred representing series A, B and C. We have several institutional funds that

own approximately 800,000 to 1M shares and therefore, fall below the threshold for filing with the SEC and therefore, not specifically

identified here. Our goal is to continue to attract institutional investors into the stock in order to promote the daily trading

volume as well as ensure reputable and knowledgeable investors, both retail and institutional, are a part of our company.

Before we open the meeting for questions, I wanted to spend

a few minutes reflecting on our mission statement and why we’re here.

Although financial and shareholder return is why we’re

here today, our mission stands alone.

Advance to Slide 38

In the fall of 2009, a colleague asked if I wanted to go visit

one of our colleagues who was in hospice after a 1½ year battle with esophageal cancer. The treatments proved to be ineffective

for Joerg and the focus was on making sure he was comfortable and not in pain during his remaining months, weeks and days. There

were quite a few pressing items that needed to get done that day but it was difficult to put any of them in front of visiting someone

nearing the end of his life. Needless to say, we took a drive to see him. The cancer had taken away his ability to sit up or speak

but it was apparent that he recognized our presence and we hope that he found some comfort in our stay. After about a 40 minute

visit we returned to the office. Not more than an hour later we received the call that he had just passed.

Two weeks ago another colleague underwent a very extensive surgery

to remove a significant amount of tumors that had spread throughout her abdominal area. She continues to show strength in her recovery

but her recovery will undoubtedly be a lengthy process. Whether it is esophageal, appendix, breast, prostate or kidney cancer,

VirtualScopics employees have battled the disease. It’s too easy to get engrossed in the day to day activities of a job,

but it’s these examples and times that make the employees of VirtualScopics want to do our best. Either through an early

diagnosis or a determination whether a particular drug is indeed working for a friend or family member, is where our passion comes

from and further drives our initiatives on a daily basis. It’s not about any one of us, it’s not about the job, it’s

about having a positive impact to society. That’s why we’re here.

MARKIN

Thanks Molly. Before we open the meeting up for questions I

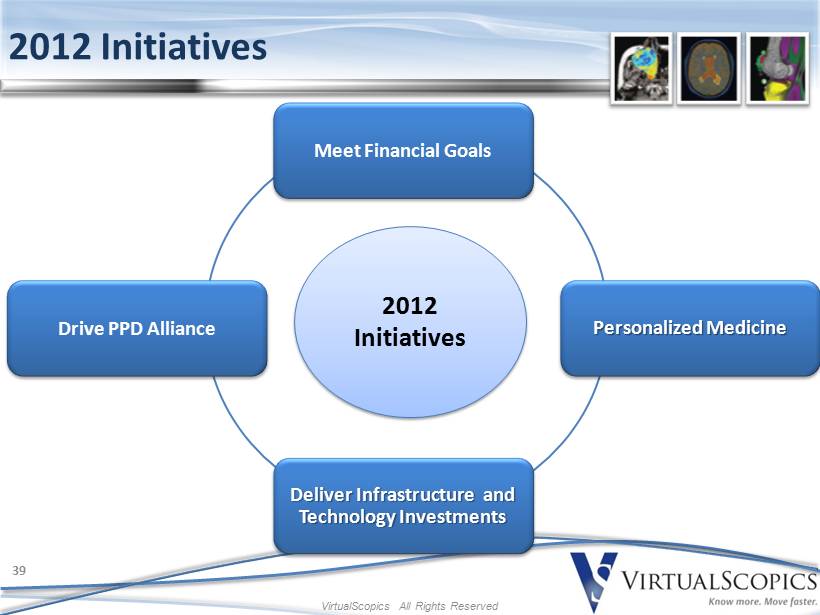

wanted to close out our prepared remarks with a summary of our 2012 initiatives which are:

| • | To meet our financial goals |

| • | To deliver on our planned infrastructure and technology

enhancements |

| • | To deliver on our plans for personalized medicine |

We would now like to open up the floor to a short Q&A.