Press Release

Exhibit 99.1

Manitex International, Inc. Reports Fourth Quarter and Full Year 2010 Results

Company Achieves 98% Increase in Fourth Quarter Revenue

Backlog Rises

80% to $40 million

Earnings per Share of $0.08 in the Fourth Quarter and $0.19 for the Full Year

Bridgeview, IL, March , 2011 — Manitex International, Inc. (Nasdaq: MNTX), a leading provider of engineered lifting solutions including boom truck

and rough terrain cranes, rough terrain forklifts, special mission oriented vehicles, container handling equipment and specialized engineered trailers, today announced fourth quarter and full year 2010 revenues of $29.5 million and $95.9 million

respectively, representing 98% and 72% respective year-over-year increases. Net income for the fourth quarter of 2010 was $0.9 million or $0.08 per share and $2.1 million or $0.19 per share for the full year 2010.

Fourth Quarter 2010 Financial Highlights:

| • |

|

Net revenues for the quarter ended December 31, 2010 were $29.5 million, representing a 98% increase from $14.9 million in the fourth quarter of

2009 and a sequential increase of $4.7 million or 19% from the third quarter of 2010. Excluding the impact of acquisitions and new operations, net revenues increased 38% from the prior year’s comparable period. |

| • |

|

EBITDA(1) for the fourth quarter of 2010 was $2.9 million, or 9.6% of sales, the highest yet achieved by the company, compared to $0.4 million or 2.9% for the fourth quarter of 2009. |

| • |

|

Gross profit of $7.7 million, or 25.9% of sales was an improvement of $4.2 million and 280 basis points compared to $3.4 million, or 23.1% in the

fourth quarter of 2009. On a sequential quarter basis, gross profit improved $1.8 million or 31% on a sequential sales increase of 19%. |

| • |

|

Net income for the fourth quarter of 2010 was $0.9 million or $0.08 per share (2), compared to a fourth quarter 2009 net income of $3.8 million or $0.34 per share that included the impact of a

bargain purchase gain of $2.9 million ($0.26 per share) and tax benefit of $1.7 million ($0.16 per share). |

Chairman and

Chief Executive Officer, David Langevin, commented, “We are encouraged by the significant improvement in our performance in 2010 rebounding from the severe conditions of 2009. Throughout this downturn, we have driven for expansion of our

business and financial results by embarking on a broad international diversification program combined with the addition to our portfolio of several well established and respected product lines through acquisitions and by initiating an operating

agreement with CVS which may lead to an acquisition of this business. By combining these measures with cost controls and a product emphasis on specialized lifting equipment, for the quarter and the year ended December 31, 2010, we are able to

report a significant improvement in our top line sales and record EBITDA margins. We believe that with our platform of niche products serving higher growth markets, we may well see continued expansion of the business as the overall economy continues

a slow recovery.

— more —

Net revenues of $29.5 million in the fourth quarter of 2010 increased $14.6 million or

98% over the fourth quarter of 2009. Acquisitions, the CVS Ferrari operating agreement and new operations started in

2010(3) contributed $9.0 million of this increase with the

balance of $5.6 million representing organic growth, equal to 38%. The increase in organic revenues reflects revenue increases in all major product categories, with cranes up 28%, material handling up 46% and equipment distribution up 100%. Crane

sales continue to reflect strong demand from new product introductions for the specialty energy and utility markets in both the US and internationally, while material handling products benefited from strong governmental and military demand for

specialized equipment. On a sequential quarter basis, revenues increased 19% largely due to material handling equipment, including a strong performance from the first full quarter of CVS Ferrari operations.

Gross profit of $7.7 million and gross margin of 25.9% were $4.2 million and 280 basis points, respectively, above the fourth quarter of 2009. The

improvement in gross margin percentage resulted from higher margin product mix in sales, particularly in the military material handling and higher capacity and specialized crane products, and from the restructuring and cost control actions taken

during 2009 which with increased volumes led to improved absorption. The company’s currency hedging program has also been successful in managing the volatile currency exchange rates. On a sequential quarter basis, gross profit increased 31% on

sales that increased 19% as we were able to leverage our facilities and obtain improved efficiencies as well as benefiting from improved product mix.

Operating expenses for the fourth quarter 2010 were $4.0 million excluding expenses of $1.6 million relating to acquisitions, the CVS Ferrari operating agreement and new operations started in 2010,

compared to the fourth quarter 2009 of $3.7 million, excluding the accounting treatment for the gain of $2.9 million on bargain purchase for the Loadking acquisition. SG&A expense accounted for a $0.4 million increase deriving from reinstated

compensation costs and selling costs, offset by restructuring costs reductions of $0.1 million.

Consolidated backlog at December 31,

2010 was $39.9 million, representing an increase of 80% from $22.1 million at December 31, 2009, and 21% from September 30, 2010.

Andrew Rooke, Manitex International President and Chief Operating Officer commented, “Fourth quarter 2010 results built upon the momentum from the

third quarter and were again strong on all fronts. Compared to the fourth quarter of 2009, our increase in revenues of $14.6 million generated incremental operating income of $2.3 million, a rate of 15%, after adjusting for the 2009 bargain purchase

gain. This incremental rate was also consistent for the full year of 2010 demonstrating good operating leverage in our business. EBITDA of $2.9 million or 9.6% of sales for the quarter was the highest rate achieved by the company to date. These

results were achieved despite sluggish demand in our core markets, as we were able to achieve strong performance from targeted energy, military, container handling and utility sectors as well as continued expansion into higher growth, non – US

markets that represented 38% of our revenues for 2010.

Mr. Rooke continued, “In addition to driving financial results, we continue

to focus on maintaining a healthy balance sheet as we move into more of a growth phase. In the third quarter 2010 our operating working capital as a percentage of annualized last quarter’s sales improved to 35%, from 49% at December 31,

2009, and we continued this improvement in the fourth quarter, moving to 31%. Our initial target in this regard is to return to the quarter four 2008 levels of 25% as the supply chain firms up its delivery capabilities.”

Full Year 2010 Highlights

| • |

|

Net sales for the year ended December 31, 2010 were $95.9 million, representing a 72% increase from the full year 2009.

|

| • |

|

Gross profit of $23.3 million was a $12.2 million increase on full year 2009, and at 24.3% gross margin was an improvement of 430 basis points from the

full year of 2009. |

| • |

|

Net income of $2.1 million for the year ended December 31, 2010 compared to a net loss of ($0.2) million, after adjusting for bargain purchase

gains on the acquisitions of Badger and Loadking, for the year ended December 31, 2009. |

| • |

|

Working capital at December 31, 2010 was $31.7 million, compared to $25.6 million at December 31, 2009. Operating working capital improved to

31% of annualized last quarter’s sales compared to 49% at December 31, 2009. |

| • |

|

EBITDA (1) for the year ended December 31, 2010 was $8.7 million, or 9.0% of sales, compared to $2.0 million or 3.5% for the full year 2009. This is the highest rate yet achieved by the company.

|

(1) EBITDA is a non-GAAP (generally accepted accounting principles in the United States of America) financial measure.

This measure may be different from non-GAAP financial measures used by other companies. We encourage investors to review the section below entitled “Non-GAAP Financial Measures.”

(2) Weighted average diluted shares outstanding for the fourth quarter and full year of 2010 were 11,395,814 and

11,380,966 respectively. Weighted average diluted shares outstanding for the fourth quarter and full year of 2009 were 11,173,332 and 10,965,444 respectively.

(3) Acquisitions, the CVS Ferrari operating agreement and new operations started in 2010 refer to the Loadking

acquisition completed on December 31, 2009, the agreement signed June 30th 2010 to rent CVS assets, and the establishment of the new division of Equipment Distribution, North American Equipment Exchange (NAEE) started in June 2010.

Outlook

With the visibility from our

year end backlog of $40 million, current production schedules and projected sales of CVS Ferrari which is performing profitably in line with our expectations, we expect a solid improvement in our sales for the first quarter of 2011 when compared

with the first quarter of 2010, which was approximately $22 million. First quarter profits will be impacted by the higher than normal quarterly accounting and legal costs because of our year end SEC filings which we estimate will be approximately

$250,000, as well as expenses associated with our participation in a large equipment show, ConExpo, that is held once every three years. We estimate the expenses associated with this very important show to be approximately $450,000. As a result the

first quarter will be adversely impacted by these unusually high costs of $700,000. In spite of these expenses and assuming we produce everything in our first quarter schedule, we expect our first quarter EPS to exceed the comparable period of 2010

which was $0.03 cents per share.

For the remainder of the year, we expect our strategy of serving specialty markets, such as, energy,

railroads, and utilities to continue to serve us well and lead to double digit growth in sales on a year over year comparison in our existing businesses. Additionally we expect incremental sales from our CVS operating agreement. Our expectations are

for a slow recovery in the overall economy. However, with the improving economy we are experiencing increases in pricing for components and raw materials and we will continue to be diligent in working with our suppliers to control these costs. We

should also be able to see improvements in cost absorption that comes with increases in our volume. In conclusion, our overall message is that our business model puts us on firm footing as we enter 2011 and that we expect to continue to implement

this strategy and build upon it as the economy improves.

Conference Call:

Management will today host a conference call at 4:30 p.m. Eastern Time to discuss the results with the investment community.

Those interested in participating should call 1-877-941-8601 if calling within the United States or

1-480-629-9810 if calling internationally. A re-play will be available until March 24, 2011, which can be accessed by dialing 1-877-870-5176 if calling within the United States or 1-858-384-5517 if calling internationally. Please use pass code

4415833 to access the replay.

The call will also be accompanied by a webcast over the Internet with slides, which are also accessible at the

Investor Relations section of the Company’s corporate website at www.manitexinternational.com.

About Manitex International, Inc.

Manitex International, Inc. is a leading provider of engineered lifting solutions including cranes, rough terrain forklifts, indoor electric

forklifts and special mission oriented vehicles, including parts support. Our Manitex subsidiary manufactures and markets a comprehensive line of boom trucks and sign cranes through a national and international dealership network. Our boom trucks

and crane products are primarily used in industrial projects, energy exploration and infrastructure development, including roads, bridges, and commercial construction. Our Crane and Machinery division is a Chicago-based distributor of cranes

including Terex truck and rough terrain cranes, Fuchs material handlers and our own Manitex product line. Crane and Machinery provides after market service in its local market as well as being a leading distributor of OEM crane parts, supplying

parts to customers throughout the United States and internationally. Our Manitex Liftking subsidiary is a provider of material handling equipment including the Noble straight-mast rough terrain forklift product line, Lowry high capacity cushion

tired forklift and Schaeff electric indoor forklifts as well as specialized carriers, heavy material handling transporters and steel mill equipment. Manitex Liftking’s rough terrain forklifts are used in both commercial and military

applications. In July 2009, we acquired through a stock purchase, Badger Equipment Company, a Winona, Minnesota-based manufacturer of specialized rough terrain cranes and material handling products. In December 2009, we acquired Load King Trailers,

a manufacturer of specialized custom trailers and hauling systems typically used for transporting heavy equipment. In June 2010, we signed an agreement to operate on an exclusive rental basis, CVS Ferrari, located near Milan, Italy, which designs

and manufacturers a range of reach stackers and associated lifting equipment for the global container handling market, sold through a broad dealer network.

Forward-Looking Statement

Safe Harbor Statement under the U.S. Private Securities

Litigation Reform Act of 1995: This release contains statements that are forward-looking in nature which express the beliefs and expectations of management including statements regarding the Company’s expected results of operations or

liquidity; statements concerning projections, predictions, expectations, estimates or forecasts as to our business, financial and operational results and future economic performance; and statements of management’s goals and objectives and other

similar expressions concerning matters that are not historical facts. In some cases, you can identify forward-looking statements by terminology such as “anticipate,” “estimate,” “plan,” “project,”

“continuing,” “ongoing,” “expect,” “we believe,” “we intend,” “may,” “will,” “should,” “could,” and similar expressions. Such statements are based on current

plans, estimates and expectations and involve a number of known and unknown risks, uncertainties and other factors that could cause the Company’s future results, performance or achievements to differ significantly from the results, performance

or achievements expressed or implied by such forward-looking statements. These factors and additional information are discussed in the Company’s filings with the Securities and Exchange Commission and statements in this release should be

evaluated in light of these important factors. Although we believe that these statements are based upon reasonable assumptions, we cannot guarantee future results. Forward-looking statements speak only as of the date on which they are made, and the

Company undertakes no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future developments or otherwise.

|

|

|

|

|

| Company Contact |

|

|

|

|

| Manitex International, Inc. |

|

Hayden IR |

|

|

| David Langevin |

|

Peter Seltzberg |

|

|

| Chairman and Chief Executive Officer |

|

Investor Relations |

|

|

| (708) 237-2060 |

|

646-415-8972 |

|

|

| djlangevin@manitexinternational.com |

|

peter@haydenir.com |

|

|

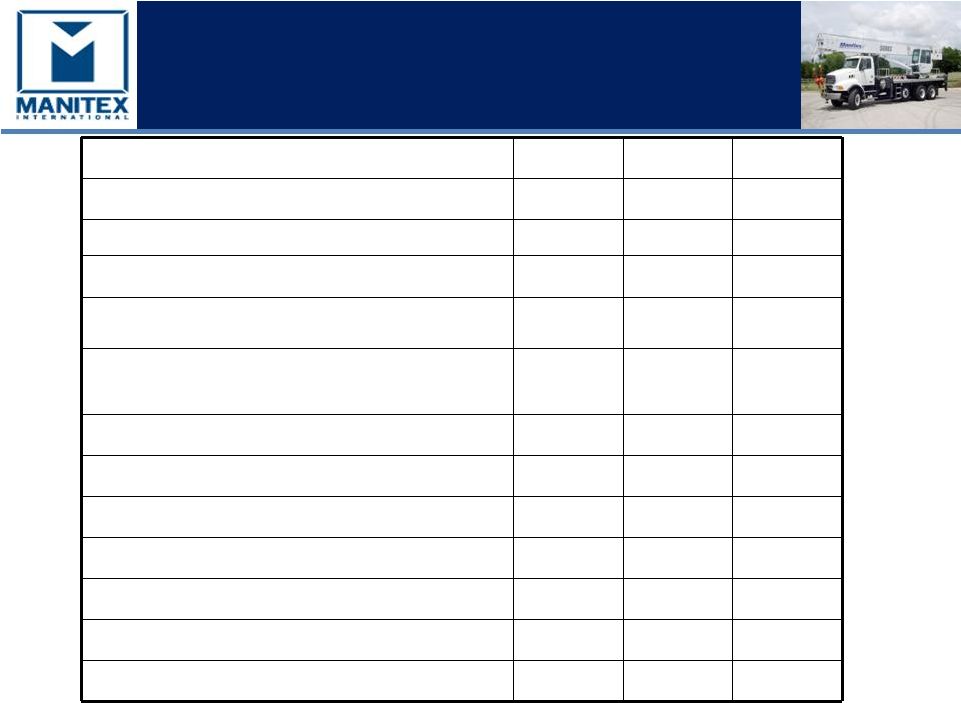

MANITEX INTERNATIONAL, INC.

CONSOLIDATED STATEMENT OF OPERATIONS

(In thousands, except per share data)

|

|

|

|

|

|

|

|

|

| |

|

For the three months ended

December 31, |

|

| |

|

2010 |

|

|

2009 |

|

| |

|

Unaudited |

|

|

Unaudited |

|

| Net revenues |

|

$ |

29,544 |

|

|

$ |

14,934 |

|

| Cost of sales |

|

|

21,884 |

|

|

|

11,490 |

|

|

|

|

|

|

|

|

|

|

| Gross profit |

|

|

7,660 |

|

|

|

3,444 |

|

| Operating expenses |

|

|

|

|

|

|

|

|

| Research and development costs |

|

|

294 |

|

|

|

341 |

|

| Restructuring expenses |

|

|

18 |

|

|

|

75 |

|

| Selling, general and administrative expense |

|

|

5,293 |

|

|

|

3,275 |

|

| Gain on bargain purchase |

|

|

— |

|

|

|

(2,915 |

) |

|

|

|

|

|

|

|

|

|

| Total operating expenses |

|

|

5,605 |

|

|

|

776 |

|

|

|

|

|

|

|

|

|

|

| Operating income |

|

|

2,055 |

|

|

|

2,668 |

|

| Other income expense |

|

|

|

|

|

|

|

|

| Interest income |

|

|

— |

|

|

|

— |

|

| Interest (expense) |

|

|

(620 |

) |

|

|

(556 |

) |

| Foreign currency transaction gain (loss) |

|

|

6 |

|

|

|

(13 |

) |

| Other income |

|

|

(64 |

) |

|

|

(1 |

) |

|

|

|

|

|

|

|

|

|

| Total other expense |

|

|

(678 |

) |

|

|

(570 |

) |

|

|

|

|

|

|

|

|

|

| Income from continuing operations before income taxes |

|

|

1,377 |

|

|

|

2,098 |

|

|

|

|

|

|

|

|

|

|

| Provision (benefit) for taxes on income |

|

|

445 |

|

|

|

(1,744 |

) |

|

|

|

|

|

|

|

|

|

| Net income |

|

$ |

932 |

|

|

$ |

3,842 |

|

|

|

|

|

|

|

|

|

|

| Basic earning per share: |

|

|

|

|

|

|

|

|

| Income from continuing operations |

|

$ |

0.08 |

|

|

$ |

0.34 |

|

|

|

|

|

|

|

|

|

|

| Net earnings |

|

$ |

0.08 |

|

|

$ |

0.34 |

|

|

|

|

|

|

|

|

|

|

| Diluted earnings per share: |

|

|

|

|

|

|

|

|

| Income from continuing operations |

|

$ |

0.08 |

|

|

$ |

0.34 |

|

|

|

|

|

|

|

|

|

|

| Net earnings |

|

$ |

0.08 |

|

|

$ |

0.34 |

|

|

|

|

|

|

|

|

|

|

| Shares used to calculate earnings per share: |

|

|

|

|

|

|

|

|

| Basic |

|

|

11,387,895 |

|

|

|

11,150,396 |

|

| Diluted |

|

|

11,395,814 |

|

|

|

11,173,332 |

|

— more —

MANITEX INTERNATIONAL, INC.

CONSOLIDATED BALANCE SHEET

(In thousands, except per share data)

|

|

|

|

|

|

|

|

|

| |

|

As of December 31, |

|

| |

|

2010 |

|

|

2009 |

|

| |

|

Unaudited |

|

|

|

|

| ASSETS |

|

|

|

|

|

|

|

|

| Current assets |

|

|

|

|

|

|

|

|

| Cash |

|

$ |

662 |

|

|

$ |

287 |

|

| Trade receivables (net) |

|

|

19,557 |

|

|

|

10,969 |

|

| Other receivables |

|

|

1,440 |

|

|

|

49 |

|

| Inventory (net) |

|

|

30,694 |

|

|

|

27,277 |

|

| Deferred tax asset |

|

|

650 |

|

|

|

673 |

|

| Prepaid expense and other |

|

|

1,700 |

|

|

|

892 |

|

|

|

|

|

|

|

|

|

|

| Total current assets |

|

|

54,703 |

|

|

|

40,147 |

|

|

|

|

|

|

|

|

|

|

| Total fixed assets (net) |

|

|

10,659 |

|

|

|

11,804 |

|

|

|

|

|

|

|

|

|

|

| Intangible assets (net) |

|

|

20,403 |

|

|

|

22,401 |

|

| Deferred tax asset |

|

|

5,249 |

|

|

|

5,796 |

|

| Goodwill |

|

|

14,452 |

|

|

|

14,452 |

|

| Other long-term assets |

|

|

51 |

|

|

|

85 |

|

|

|

|

|

|

|

|

|

|

| Total assets |

|

$ |

105,517 |

|

|

$ |

94,685 |

|

|

|

|

|

|

|

|

|

|

| LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

| Current liabilities |

|

|

|

|

|

|

|

|

| Notes payable—short term |

|

$ |

2,646 |

|

|

$ |

2,624 |

|

| Current portion of capital lease obligations |

|

|

564 |

|

|

|

520 |

|

| Accounts payable |

|

|

14,447 |

|

|

|

8,565 |

|

| Accounts payable related parties |

|

|

481 |

|

|

|

618 |

|

| Accrued expenses |

|

|

4,335 |

|

|

|

2,145 |

|

| Other current liabilities |

|

|

538 |

|

|

|

97 |

|

|

|

|

|

|

|

|

|

|

| Total current liabilities |

|

|

23,011 |

|

|

|

14,569 |

|

|

|

|

|

|

|

|

|

|

| Long-term liabilities |

|

|

|

|

|

|

|

|

| Revolving term credit facilities |

|

|

20,007 |

|

|

|

16,788 |

|

| Deferred tax liability |

|

|

5,473 |

|

|

|

5,952 |

|

| Notes payable |

|

|

6,119 |

|

|

|

8,323 |

|

| Capital lease obligations |

|

|

4,683 |

|

|

|

5,256 |

|

| Deferred gain on sale of building |

|

|

2,789 |

|

|

|

3,169 |

|

| Other long-term liabilities |

|

|

161 |

|

|

|

200 |

|

|

|

|

|

|

|

|

|

|

| Total long-term liabilities |

|

|

39,232 |

|

|

|

39,688 |

|

|

|

|

|

|

|

|

|

|

| Total liabilities |

|

|

62,243 |

|

|

|

54,257 |

|

|

|

|

|

|

|

|

|

|

| Commitments and contingencies |

|

|

|

|

|

|

|

|

| Shareholders’ equity |

|

|

|

|

|

|

|

|

| Preferred Stock—Authorized 150,000 shares, no shares issued or outstanding at December 31, 2009 and December 31,

2008 |

|

|

— |

|

|

|

— |

|

| Common Stock—no par value, Authorized, 20,000,000 shares authorized Issued and outstanding, 11,394,621 and 11,160,455 at

December 31, 2010 and December 31, 2009, respectively |

|

|

46,920 |

|

|

|

46,375 |

|

| Warrants |

|

|

1,788 |

|

|

|

1,788 |

|

| Paid in capital |

|

|

6 |

|

|

|

93 |

|

| Accumulated deficit |

|

|

(6,148 |

) |

|

|

(8,257 |

) |

| Accumulated other comprehensive income |

|

|

708 |

|

|

|

429 |

|

|

|

|

|

|

|

|

|

|

| Total shareholders’ equity |

|

|

43,274 |

|

|

|

40,428 |

|

|

|

|

|

|

|

|

|

|

| Total liabilities and shareholders’ equity |

|

$ |

105,517 |

|

|

$ |

94,685 |

|

|

|

|

|

|

|

|

|

|

MANITEX INTERNATIONAL, INC.

CONSOLIDATED STATEMENT OF OPERATIONS

(In thousands, except per share data)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the years ended December 31, |

|

| |

|

2010 |

|

|

2009 |

|

|

2008 |

|

| |

|

Unaudited |

|

|

|

|

|

|

|

| Net revenues |

|

$ |

95,875 |

|

|

$ |

55,887 |

|

|

$ |

106,341 |

|

| Cost of sales |

|

|

72,541 |

|

|

|

44,730 |

|

|

|

88,876 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gross profit |

|

|

23,334 |

|

|

|

11,157 |

|

|

|

17,465 |

|

| Operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

| Research and development costs |

|

|

1,173 |

|

|

|

836 |

|

|

|

819 |

|

| Restructuring expenses |

|

|

176 |

|

|

|

255 |

|

|

|

329 |

|

| Selling, general and administrative expense |

|

|

16,448 |

|

|

|

10,537 |

|

|

|

12,909 |

|

| Gain on bargain purchase |

|

|

— |

|

|

|

(3,815 |

) |

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total operating expenses |

|

|

17,797 |

|

|

|

7,813 |

|

|

|

14,057 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Operating income |

|

|

5,537 |

|

|

|

3,344 |

|

|

|

3,408 |

|

| Other income expense |

|

|

|

|

|

|

|

|

|

|

|

|

| Interest income |

|

|

— |

|

|

|

— |

|

|

|

— |

|

| Interest (expense) |

|

|

(2,450 |

) |

|

|

(1,864 |

) |

|

|

(1,961 |

) |

| Foreign currency transaction gain (loss) |

|

|

(65 |

) |

|

|

59 |

|

|

|

(99 |

) |

| Other income |

|

|

113 |

|

|

|

3 |

|

|

|

44 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total other expense |

|

|

(2,402 |

) |

|

|

(1,802 |

) |

|

|

(2,016 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income from continuing operations before income taxes |

|

|

3,135 |

|

|

|

1,542 |

|

|

|

1,392 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Provision (benefit) for taxes on income |

|

|

1,026 |

|

|

|

(2,097 |

) |

|

|

(407 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income from continuing operations |

|

|

2,109 |

|

|

|

3,639 |

|

|

|

1,799 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Discontinued operations: |

|

|

|

|

|

|

|

|

|

|

|

|

| Income from discontinued operations, net of income taxes (benefit) of $0 in 2008 |

|

|

— |

|

|

|

— |

|

|

|

199 |

|

| Gain on sale or closure of discontinued operations, net of $0 income tax in 2008 |

|

|

— |

|

|

|

— |

|

|

|

200 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income |

|

$ |

2,109 |

|

|

$ |

3,639 |

|

|

$ |

2,198 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basic earning per share: |

|

|

|

|

|

|

|

|

|

|

|

|

| Income from continuing operations |

|

$ |

0.19 |

|

|

$ |

0.33 |

|

|

$ |

0.18 |

|

| Income from discontinued operations, net of income taxes |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

0.02 |

|

| Gain on sales or closure of discontinued operations, net of income taxes |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

0.02 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net earnings |

|

$ |

0.19 |

|

|

$ |

0.33 |

|

|

$ |

0.22 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Diluted earnings per share: |

|

|

|

|

|

|

|

|

|

|

|

|

| Income from continuing operations |

|

$ |

0.19 |

|

|

$ |

0.33 |

|

|

$ |

0.17 |

|

| Income from discontinued operations, net of income taxes |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

0.02 |

|

| Gain on sales or closure of discontinued operations, net of income taxes |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

0.02 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net earnings |

|

$ |

0.19 |

|

|

$ |

0.33 |

|

|

$ |

0.21 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Shares used to calculate earnings per share: |

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

|

11,362,361 |

|

|

|

10,957,646 |

|

|

|

10,071,585 |

|

| Diluted |

|

|

11,380,966 |

|

|

|

10,965,444 |

|

|

|

10,375,062 |

|

MANITEX INTERNATIONAL, INC.

CONSOLIDATED STATEMENT OF CASH FLOWS

(Thousands of Dollars)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the years ended December 31, |

|

| |

|

2010 |

|

|

2009 |

|

|

2008 |

|

| |

|

Unaudited |

|

|

|

|

|

|

|

| Cash flows from operating activities: |

|

|

|

|

|

|

|

|

|

|

|

|

| Net income |

|

$ |

2,109 |

|

|

$ |

3,639 |

|

|

$ |

2,198 |

|

| Adjustments to reconcile net income to cash provided by operating activities: |

|

|

|

|

|

|

|

|

|

|

|

|

| Depreciation and amortization |

|

|

3,139 |

|

|

|

2,453 |

|

|

|

2,008 |

|

| Gain on bargain purchases |

|

|

— |

|

|

|

(3,815 |

) |

|

|

— |

|

| Provisions for customer allowances |

|

|

67 |

|

|

|

(46 |

) |

|

|

(47 |

) |

| Gain on disposal of assets |

|

|

(39 |

) |

|

|

— |

|

|

|

(36 |

) |

| Deferred income taxes |

|

|

93 |

|

|

|

(1,949 |

) |

|

|

(461 |

) |

| Inventory reserves |

|

|

123 |

|

|

|

54 |

|

|

|

47 |

|

| Reserves for uncertain tax positions |

|

|

(39 |

) |

|

|

(27 |

) |

|

|

13 |

|

| Stock based deferred compensation |

|

|

78 |

|

|

|

86 |

|

|

|

339 |

|

| Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

| (Increase) decrease in accounts receivable |

|

|

(9,785 |

) |

|

|

7,856 |

|

|

|

(650 |

) |

| (Increase) decrease in accounts receivable – related party |

|

|

— |

|

|

|

— |

|

|

|

(277 |

) |

| (Increase) decrease in inventory |

|

|

(3,002 |

) |

|

|

(54 |

) |

|

|

(5,328 |

) |

| (Increase) decrease in prepaid expenses |

|

|

(793 |

) |

|

|

(533 |

) |

|

|

491 |

|

| (Increase) decrease in other assets |

|

|

34 |

|

|

|

(85 |

) |

|

|

— |

|

| Increase (decrease) in accounts payable |

|

|

5,676 |

|

|

|

(4,307 |

) |

|

|

2,080 |

|

| Increase (decrease) in accounts payable related parties |

|

|

(137 |

) |

|

|

430 |

|

|

|

— |

|

| Increase (decrease) in accrued expense |

|

|

2,135 |

|

|

|

(1,234 |

) |

|

|

(1,719 |

) |

| Increase (decrease) in other current liabilities |

|

|

438 |

|

|

|

(225 |

) |

|

|

(126 |

) |

| Discontinued operations – cash provided by (used) for operating activities |

|

|

— |

|

|

|

— |

|

|

|

(93 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net cash provided by (used) by operating activities |

|

|

97 |

|

|

|

2,243 |

|

|

|

(1,561 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash flows from investing activities: |

|

|

|

|

|

|

|

|

|

|

|

|

| Proceeds from sale of fixed assets |

|

|

216 |

|

|

|

10 |

|

|

|

58 |

|

| Purchase of property and equipment |

|

|

(511 |

) |

|

|

(139 |

) |

|

|

(630 |

) |

| Acquisition of business, net of cash acquired |

|

|

— |

|

|

|

(139 |

) |

|

|

(817 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net cash (used) for provided by investing activities |

|

|

(295 |

) |

|

|

(268 |

) |

|

|

(1,389 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash flows from financing activities: |

|

|

|

|

|

|

|

|

|

|

|

|

| Borrowing on revolving credit facility |

|

|

4,077 |

|

|

|

2,419 |

|

|

|

3,219 |

|

| Repayment on revolving credit facility |

|

|

(1,107 |

) |

|

|

(3,163 |

) |

|

|

— |

|

| New borrowings – notes payable |

|

|

1,209 |

|

|

|

997 |

|

|

|

1,809 |

|

| Note payments |

|

|

(3,016 |

) |

|

|

(1,943 |

) |

|

|

(1,879 |

) |

| Shares repurchased for income tax withholding on share-based compensation |

|

|

(20 |

) |

|

|

(6 |

) |

|

|

(7 |

) |

| New capital leases |

|

|

— |

|

|

|

51 |

|

|

|

— |

|

| Repayment on capital lease obligations |

|

|

(529 |

) |

|

|

(376 |

) |

|

|

(284 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net cash provided by (used) for financing activities |

|

|

614 |

|

|

|

(2,021 |

) |

|

|

2,858 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Effect of exchange rate change on cash |

|

|

(41 |

) |

|

|

(92 |

) |

|

|

(52 |

) |

| Net decrease in cash and cash equivalents |

|

|

416 |

|

|

|

(46 |

) |

|

|

(92 |

) |

| Cash and cash equivalents at the beginning of the year |

|

|

287 |

|

|

|

425 |

|

|

|

569 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents at end of year |

|

$ |

662 |

|

|

$ |

287 |

|

|

$ |

425 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Supplemental disclosure of cash flow information: |

|

|

|

|

|

|

|

|

|

|

|

|

| Cash paid during the year for |

|

|

|

|

|

|

|

|

|

|

|

|

| Interest |

|

$ |

2,443 |

|

|

$ |

1,828 |

|

|

$ |

2,024 |

|

| Income taxes |

|

$ |

65 |

|

|

$ |

16 |

|

|

$ |

161 |

|

Supplemental Information

Non-GAAP Financial Measures

This

press release includes the following non-GAAP financial measure: “EBITDA” (earnings before interest, tax, depreciation and amortization). This non-GAAP term, as defined by the Company, may not be comparable to similarly titled measures

used by other companies. EBITDA is not a measure of financial performance under generally accepted accounting principles. Items excluded from EBITDA are significant components in understanding and assessing financial performance. EBITDA should not

be considered in isolation or as a substitute for net earnings, operating income and other consolidated earnings data prepared in accordance with GAAP or as a measure of our profitability. A reconciliation of net income to EBITDA is provided below.

The Company’s management believes that EBITDA and EBITDA as a percentage of sales represent key operating metrics for its business.

Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) is a key indicator used by management to evaluate operating performance. While EBITDA is not intended to replace any presentation included in our consolidated financial

statements under generally accepted accounting principles (GAAP) and should not be considered an alternative to operating performance or an alternative to cash flow as a measure of liquidity, we believe this measure is useful to investors in

assessing our capital expenditure and working capital requirements. This calculation may differ in method of calculation from similarly titled measures used by other companies. A reconciliation of EBITDA to GAAP financial measures for the three and

twelve month periods ended December 31st, 2010 and December 31st 2009 is included with this press release below and with the Company’s related Form 8-K.

Reconciliation of GAAP Net Income from Continuing Operations to Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) from Continuing Operations (in thousands)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Three Months Ended |

|

|

Twelve Months Ended |

|

| |

|

December 31,

2010 |

|

|

December 31,

2009 |

|

|

December 31,

2010 |

|

|

December 31,

2009 |

|

| Net income from continuing operations |

|

|

932 |

|

|

|

3,842 |

|

|

|

2,109 |

|

|

|

3,639 |

|

| Income tax (benefit) |

|

|

445 |

|

|

|

(1,744 |

) |

|

|

1,026 |

|

|

|

(2,097 |

) |

| Interest expense |

|

|

620 |

|

|

|

556 |

|

|

|

2,450 |

|

|

|

1,864 |

|

| Foreign currency transaction losses (gain) |

|

|

(6 |

) |

|

|

13 |

|

|

|

65 |

|

|

|

(59 |

) |

| Other (income) expense |

|

|

64 |

|

|

|

1 |

|

|

|

(113 |

) |

|

|

(3 |

) |

| Gain on Bargain Purchase |

|

|

— |

|

|

|

(2,915 |

) |

|

|

— |

|

|

|

(3,815 |

) |

| Depreciation & Amortization |

|

|

795 |

|

|

|

673 |

|

|

|

3,139 |

|

|

|

2,453 |

|

| Earnings before interest, taxes, depreciation and amortization (EBITDA) |

|

|

2,850 |

|

|

|

426 |

|

|

|

8,676 |

|

|

|

1,982 |

|

| EBITDA % to sales |

|

|

9.6 |

% |

|

|

2.9 |

% |

|

|

9.0 |

% |

|

|

3.5 |

% |

In an effort to provide investors with additional information regarding the Company’s results, Manitex

International refers to various non-GAAP (U.S. generally accepted accounting principles) financial measures which management believes provides useful information to investors. These measures may not be comparable to similarly titled measures being

disclosed by other companies. In addition, the Company believes that non-GAAP financial measures should be considered in addition to, and not in lieu of, GAAP financial measures.

Manitex International believes that this information is useful to understanding its operating results and the ongoing performance of its underlying businesses. Management of Manitex International uses

these non–GAAP financial measures to establish internal budgets and targets and to evaluate the Company’s financial performance against such budgets and targets.

The amounts described below are unaudited, are reported in thousands of U.S. dollars, and are as of or for the period ended December 31, 2010, unless otherwise indicated.

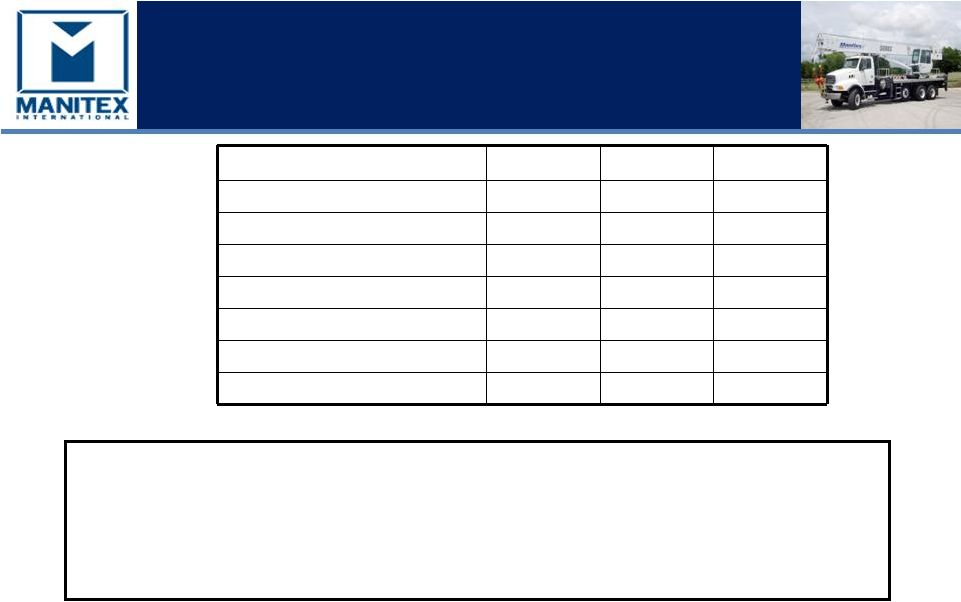

Backlog

Backlog is defined as firm

orders that have been received by the Company. The disclosure of backlog aids in the analysis the Company’s customers’ demand for product, as well as the ability of the Company to meet that demand. Backlog is not necessarily indicative of

sales to be recognized in a specified future period.

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

December 31,

2010 |

|

|

September 30,

2010 |

|

|

December 31,

2009 |

|

| Backlog |

|

$ |

39,905 |

|

|

$ |

32,847 |

|

|

$ |

22,122 |

|

| 12/31/2010 increase v prior period |

|

|

— |

|

|

|

21.5 |

% |

|

|

80.4 |

% |

Current Ratio is calculated

by dividing current assets by current liabilities.

|

|

|

|

|

|

|

|

|

| |

|

December 31,

2010 |

|

|

December 31,

2009 |

|

| Current Assets |

|

$ |

54,703 |

|

|

$ |

40,147 |

|

| Current Liabilities |

|

$ |

23,011 |

|

|

$ |

14,569 |

|

| Current Ratio |

|

|

2.4 |

|

|

|

2.8 |

|

Days Sales Outstanding,

(DSO), is calculated by taking the sum of net trade and related party receivables divided by annualized sales per day (sales for the quarter, multiplied by 4, and the sum divided by 365).

Days Payables Outstanding, (DPO), is calculated by taking the sum of net trade and related party

payables divided by annualized cost of sales per day (cost of goods sold for the quarter, multiplied by 4, and the sum divided by 365).

Debt is calculated using the Condensed Consolidated Balance Sheet amounts for current and long term portion of long term debt, capital lease

obligations, notes payable and lines of credit.

|

|

|

|

|

|

|

|

|

| |

|

December 31,

2010 |

|

|

December 31,

2009 |

|

| Current portion of long term debt |

|

$ |

2,646 |

|

|

$ |

2,624 |

|

| Current portion of capital lease obligations |

|

|

564 |

|

|

|

520 |

|

| Lines of credit |

|

|

20,007 |

|

|

|

16,788 |

|

| Notes payable – long term |

|

|

6,119 |

|

|

|

8,323 |

|

| Capital lease obligations |

|

|

4,683 |

|

|

|

5,256 |

|

| Debt |

|

$ |

34,019 |

|

|

$ |

33,511 |

|

Inventory turns are

calculated by multiplying cost of goods sold for the referenced three month period by 4 and dividing that figure by inventory as at the referenced period.

Manufacturing Expenses include manufacturing wages, salaries, fixed and variable overhead costs.

Operating Working Capital is calculated using the Consolidated Balance Sheet amounts for Trade receivables (net of allowance) plus other receivables, plus inventories, less Accounts payable. The

Company considers excessive working capital as an inefficient use of resources, and seeks to minimize the level of investment without adversely impacting the ongoing operations of the business.

|

|

|

|

|

|

|

|

|

| |

|

December 31,

2010 |

|

|

December 31,

2009 |

|

| Trade receivables (net) |

|

$ |

19,557 |

|

|

$ |

10,969 |

|

| Other receivables |

|

|

1,440 |

|

|

|

49 |

|

| Inventory (net) |

|

|

30,694 |

|

|

|

27,277 |

|

| Less: Accounts payable |

|

|

14,928 |

|

|

|

9,183 |

|

| Total Operating Working Capital |

|

$ |

36,763 |

|

|

$ |

29,112 |

|

| % of Trailing Three Month Annualized Net Sales |

|

|

31.1 |

% |

|

|

48.7 |

% |

Trailing Three Month Annualized Net Sales is calculated using the net sales for quarter, multiplied

by four.

|

|

|

|

|

|

|

|

|

| |

|

Three Months Ended |

|

| |

|

December 31,

2010 |

|

|

December 31,

2009 |

|

| Net sales |

|

$ |

29,544 |

|

|

$ |

14,934 |

|

| Multiplied by 4 |

|

|

4 |

|

|

|

4 |

|

| Trailing Three Month Annualized Net Sales |

|

$ |

118,176 |

|

|

$ |

59,736 |

|

Working capital is

calculated as total current assets less total current liabilities

|

|

|

|

|

|

|

|

|

| |

|

December 31,

2010 |

|

|

December 31,

2009 |

|

| Total Current Assets |

|

$ |

54,703 |

|

|

$ |

40,147 |

|

| Less: Total Current Liabilities |

|

|

23,011 |

|

|

|

14,569 |

|

| Working Capital |

|

$ |

31,692 |

|

|

$ |

25,578 |

|