Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT

COMPANIES

Investment Company Act file number: 811-21622

Thrivent Cash Management Trust

(Exact name of registrant as specified in charter)

625 Fourth Avenue South

Minneapolis, Minnesota 55415

(Address of principal executive offices) (Zip code)

Rebecca A. Paulzine, Assistant Secretary

625 Fourth Avenue South

Minneapolis, Minnesota 55415

(Name and address of agent for service)

Registrant’s telephone number, including area code: (612) 844-5168

Date of fiscal year end: October 31

Date of reporting period: April 30, 2013

Table of Contents

Item 1. Report to Stockholders

Table of Contents

Semiannual Report

APRIL 30, 2013

Thrivent Cash Management Trust

Table of Contents

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 14 | ||||

| 16 | ||||

Table of Contents

THRIVENT CASH MANAGEMENT TRUST

William D. Stouten, Portfolio Manager

Thrivent Cash Management Trust (the “Trust”) seeks to maximize current income to the extent consistent with the preservation of capital and liquidity and to maintain a stable $1.00 per share net asset value by (1) investing in dollar-denominated securities with a remaining maturity of 397 calendar days or less; (2) maintaining a dollar-weighted average portfolio maturity of 60 calendar days or less; or (3) maintaining a dollar-weighted average portfolio maturity of 120 calendar days or less.

Thrivent Cash Management Trust

As of April 30, 2013*

| 7-Day Yield |

0.09 | % | ||

| 7-Day Yield Gross of Waivers |

0.09 | % | ||

| 7-Day Effective Yield |

0.09 | % | ||

| 7-Day Effective Yield Gross of Waivers |

0.09 | % |

Average Annual Total Returns**

| For the Period Ended April 30, 2013 |

1-Year | 5-Year | Since

Inception, 9/16/2004 |

|||||||||

| Total Return |

0.12 | % | 0.52 | % | 2.09 | % | ||||||

| * | Seven-day yields of the Thrivent Cash Management Trust refer to the income generated by an investment in the Trust over a specified seven-day period. Effective yields reflect the reinvestment of income. A yield gross of waivers represents what the yield would have been if the investment adviser were not waiving or reimbursing certain expenses. Yields are subject to daily fluctuation and should not be considered an indication of future results. |

| ** | Average annual total returns represent past performance and reflect changes in share prices, the reinvestment of all dividends and capital gains, and the effects of compounding. The returns shown do not reflect taxes a shareholder would pay on distributions or redemptions. |

Past performance is not an indication of future results. Current performance may be lower or higher than the performance data quoted. The prospectus contains more complete information on the investment objectives, risks, charges and expenses of the Trust. Investors should read and consider carefully before investing. To obtain a prospectus, call 1-800-THRIVENT.

An investment in the Trust is not insured or guaranteed by the FDIC or any other government agency. Although the Trust seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Trust.

1

Table of Contents

(Unaudited)

As a shareholder of the Trust, you incur ongoing costs, including management fees and other Trust expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Trust and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from November 1, 2012 through April 30, 2013.

Actual Expenses

In the table below, the first line provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid during Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

In the table below, the second line provides information about hypothetical account values and hypothetical expenses based on the Trust’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Trust’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Trust and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical example that appears in the shareholder reports of the other funds.

| Beginning Account Value 11/1/2012 |

Ending Account

Value 4/30/2013 |

Expenses Paid During Period 11/1/2012 - 4/30/2013* |

Annualized

Expense Ratio |

|||||||||||||

| Thrivent Cash Management Trust |

|

|||||||||||||||

| Actual |

$ | 1,000 | $ | 1,001 | $ | 0.24 | 0.05 | % | ||||||||

| Hypothetical** |

$ | 1,000 | $ | 1,025 | $ | 0.25 | 0.05 | % | ||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 181/365 to reflect the one-half year period. |

| ** | Assuming 5% annualized total return before expenses. |

2

Table of Contents

Thrivent Cash Management Trust

Schedule of Investments as of April 30, 2013

(unaudited)

| The accompanying Notes to the Financial Statements are an integral part of this schedule. |

| 3 |

Table of Contents

Thrivent Cash Management Trust

Schedule of Investments as of April 30, 2013

(unaudited)

| The accompanying Notes to Financial Statements are an integral part of this schedule. |

| 4 |

Table of Contents

Thrivent Cash Management Trust

Schedule of Investments as of April 30, 2013

(unaudited)

| The accompanying Notes to Financial Statements are an integral part of this schedule. |

| 5 |

Table of Contents

Thrivent Cash Management Trust

Schedule of Investments as of April 30, 2013

(unaudited)

Fair Valuation Measurements

The following table is a summary of the inputs used, as of April 30, 2013, in valuing Thrivent Cash Management Trust’s assets carried at fair value or amortized cost, which approximates fair value.

| Investments in Securities |

Total | Level 1 | Level 2 | Level 3 | ||||||||||||

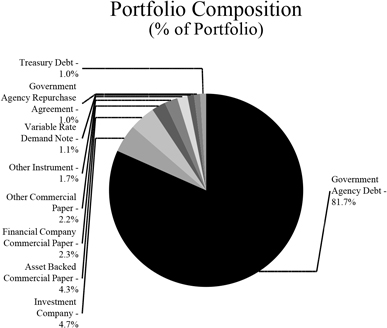

| Asset Backed Commercial Paper |

221,001,882 | – | 221,001,882 | – | ||||||||||||

| Financial Company Commercial Paper |

116,655,000 | – | 116,655,000 | – | ||||||||||||

| Government Agency Debt |

4,136,957,132 | – | 4,136,957,132 | – | ||||||||||||

| Government Agency Repurchase Agreement |

50,000,000 | 50,000,000 | – | – | ||||||||||||

| Investment Company |

239,684,000 | 239,684,000 | – | – | ||||||||||||

| Other Commercial Paper |

109,999,842 | – | 109,999,842 | – | ||||||||||||

| Other Instrument |

84,665,000 | – | 84,665,000 | – | ||||||||||||

| Treasury Debt |

50,032,203 | – | 50,032,203 | – | ||||||||||||

| Variable Rate Demand Note |

56,520,000 | – | 56,520,000 | – | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 5,065,515,059 | $ | 289,684,000 | $ | 4,775,831,059 | $ | – | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

There were no significant transfers between Levels during the period ended April 30, 2013. Transfers between Levels are identified as of the end of the period.

The accompanying Notes to Financial Statements are an integral part of this schedule.

6

Table of Contents

Thrivent Cash Management Trust

Statement of Assets and Liabilities

| As of April 30, 2013 (unaudited) |

Cash Management Trust |

|||

| Assets |

||||

| Investments at cost |

$ | 5,065,515,059 | ||

| Investments in securities at value |

5,065,515,059 | |||

| Investments at Value |

5,065,515,059 | 1 | ||

| Cash |

7,108 | |||

| Dividends and interest receivable |

2,880,027 | |||

| Prepaid expenses |

27,224 | |||

| Total Assets |

5,068,429,418 | |||

| Liabilities |

||||

| Distributions payable |

374,029 | |||

| Accrued expenses |

37,131 | |||

| Payable for investments purchased |

41,997,920 | |||

| Payable to affiliate |

196,261 | |||

| Total Liabilities |

42,605,341 | |||

| Net Assets |

||||

| Capital stock (beneficial interest) |

5,025,818,462 | |||

| Accumulated undistributed net investment income/(loss) |

2,677 | |||

| Accumulated undistributed net realized gain/(loss) |

2,938 | |||

| Total Net Assets |

$ | 5,025,824,077 | ||

| Shares of beneficial interest outstanding |

5,025,818,462 | |||

| Net asset value per share |

$ | 1.00 | ||

| 1 | Securities held by the Trust are valued on the basis of amortized cost, which approximates market value. |

The accompanying Notes to the Financial Statements are an integral part of this schedule.

7

Table of Contents

Thrivent Cash Management Trust

| For the six months ended April 30, 2013 (unaudited) |

Cash Management Trust |

|||

| Investment Income |

||||

| Dividends |

$ | 109,317 | ||

| Interest |

3,040,777 | |||

| Total Investment Income |

3,150,094 | |||

| Expenses |

||||

| Adviser fees |

928,953 | |||

| Administrative service fees |

45,000 | |||

| Audit and legal fees |

13,452 | |||

| Custody fees |

65,011 | |||

| Insurance expenses |

5,236 | |||

| Printing and postage expenses |

3,270 | |||

| Transfer agent fees |

20,814 | |||

| Trustees’ fees |

2,530 | |||

| Other expenses |

9,981 | |||

| Total Expenses Before Reimbursement |

1,094,247 | |||

| Less: |

||||

| Reimbursement from adviser |

(61,016 | ) | ||

| Custody earnings credit |

(733 | ) | ||

| Total Net Expenses |

1,032,498 | |||

| Net Investment Income/(Loss) |

2,117,596 | |||

| Realized and Unrealized Gains/(Losses) |

||||

| Net realized gains/(losses) on: |

||||

| Investments |

2,941 | |||

| Net Realized and Unrealized Gains/(Losses) |

2,941 | |||

| Net Increase/(Decrease) in Net Assets Resulting From Operations |

$ | 2,120,537 | ||

The accompanying Notes to the Financial Statements are an integral part of this schedule.

8

Table of Contents

Thrivent Cash Management Trust

Statement of Changes in Net Assets

| Cash Management Trust | ||||||||

| For the periods ended |

4/30/2013 (unaudited) |

10/31/2012 | ||||||

| Operations |

||||||||

| Net investment income/(loss) |

$ | 2,117,596 | $ | 746,911 | ||||

| Net realized gains/(losses) |

2,941 | 12,127 | ||||||

| Net Change in Net Assets Resulting From Operations |

2,120,537 | 759,038 | ||||||

| Distributions to Shareholders |

||||||||

| From net investment income |

(2,114,919 | ) | (746,911 | ) | ||||

| From net realized gains |

(12,130 | ) | (10,103 | ) | ||||

| Total Distributions to Shareholders |

(2,127,049 | ) | (757,014 | ) | ||||

| Capital Stock Transactions |

||||||||

| Sold |

9,507,378,574 | 7,580,627,600 | ||||||

| Redeemed |

(7,035,376,403 | ) | (5,636,704,553 | ) | ||||

| Total Capital Stock Transactions |

2,472,002,171 | 1,943,923,047 | ||||||

| Net Increase/(Decrease) in Net Assets |

2,471,995,659 | 1,943,925,071 | ||||||

| Net Assets, Beginning of Period |

2,553,828,418 | 609,903,347 | ||||||

| Net Assets, End of Period |

$ | 5,025,824,077 | $ | 2,553,828,418 | ||||

| Accumulated Undistributed Net Investment Income/(Loss) |

$ | 2,677 | $ | – | ||||

| Capital Stock Share Transactions |

||||||||

| Sold |

9,507,378,574 | 7,580,627,600 | ||||||

| Redeemed |

(7,035,376,403 | ) | (5,636,704,553 | ) | ||||

|

|

|

|

|

|||||

| Total Capital Stock Share Transactions |

2,472,002,171 | 1,943,923,047 | ||||||

|

|

|

|

|

|||||

The accompanying Notes to the Financial Statements are an integral part of this schedule.

9

Table of Contents

Thrivent Cash Management Trust

April 30, 2013

(unaudited)

10

Table of Contents

Thrivent Cash Management Trust

Notes to Financial Statements

April 30, 2013

(unaudited)

11

Table of Contents

Thrivent Cash Management Trust

Notes to Financial Statements

April 30, 2013

(unaudited)

12

Table of Contents

[THIS PAGE INTENTIONALLY LEFT BLANK]

13

Table of Contents

Thrivent Cash Management Trust

FOR A SHARE OUTSTANDING THROUGHOUT EACH PERIOD*

| Income from Investment Operations | Less

Distributions From |

|||||||||||||||||||||||

| Net

Asset Value, Beginning of Period |

Net Investment Income /(Loss) |

Net Realized and Unrealized Gain/(Loss) on Investments(a) |

Total from Investment Operations |

Net Investment Income |

Net Realized Gain on Investments |

|||||||||||||||||||

| CASH MANAGEMENT TRUST |

||||||||||||||||||||||||

| Period Ended 4/30/2013 (unaudited) |

$ | 1.00 | $ | – | $ | – | $ | – | $ | – | $ | – | ||||||||||||

| Year Ended 10/31/2012 |

1.00 | – | – | – | – | – | ||||||||||||||||||

| Year Ended 10/31/2011 |

1.00 | – | – | – | – | – | ||||||||||||||||||

| Year Ended 10/31/2010 |

1.00 | – | – | – | – | – | ||||||||||||||||||

| Year Ended 10/31/2009 |

1.00 | 0.01 | – | 0.01 | (0.01 | ) | – | |||||||||||||||||

| Year Ended 10/31/2008 |

1.00 | 0.03 | – | 0.03 | (0.03 | ) | – | |||||||||||||||||

| (a) | The amount shown may not correlate with the change in aggregate gains and losses of portfolio securities due to the timing of sales and redemptions of fund shares. |

| * | All per share amounts have been rounded to the nearest cent. |

The accompanying Notes to the Financial Statements are an integral part of this schedule.

14

Table of Contents

Thrivent Cash Management Trust

Financial Highlights—continued

RATIOS / SUPPLEMENTAL DATA

| Ratio to Average Net Assets** | Ratios to Average Net Assets Before Expenses Waived, Credited or Paid Indirectly** |

|||||||||||||||||||||||||||||||

| Total Distributions |

Net Asset Value, End of Period |

Total Return(b) |

Net Assets, End of Period (in millions) |

Expenses | Net Investment Income/(Loss) |

Expenses | Net Investment Income/(Loss) |

Portfolio Turnover Rate |

||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||

|

$ – |

$ | 1.00 | 0.05 | % | $ | 5,025.8 | 0.05 | % | 0.10 | % | 0.05 | % | 0.10 | % | N/A | |||||||||||||||||

| – |

1.00 | 0.13 | % | 2,553.8 | 0.05 | % | 0.12 | % | 0.08 | % | 0.09 | % | N/A | |||||||||||||||||||

| – |

1.00 | 0.15 | % | 609.9 | 0.05 | % | 0.15 | % | 0.08 | % | 0.12 | % | N/A | |||||||||||||||||||

| – |

1.00 | 0.22 | % | 779.4 | 0.05 | % | 0.21 | % | 0.08 | % | 0.19 | % | N/A | |||||||||||||||||||

| (0.01) |

1.00 | 0.76 | % | 746.7 | 0.05 | % | 0.92 | % | 0.06 | % | 0.91 | % | N/A | |||||||||||||||||||

| (0.03) |

1.00 | 3.38 | % | 2,461.9 | 0.05 | % | 3.36 | % | 0.05 | % | 3.36 | % | N/A | |||||||||||||||||||

| (b) | Total investment return assumes dividend reinvestment and does not reflect any deduction for applicable sales charges. Not annualized for periods less than one year. |

| ** | Computed on an annualized basis for periods less than one year. |

The accompanying Notes to the Financial Statements are an integral part of this schedule.

15

Table of Contents

(unaudited)

PROXY VOTING

The policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities are attached to the Trust’s Statement of Additional Information. You may request a free copy of the Statement of Additional Information or the report of how the Trust voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 by calling 1-800-847-4836. You also may review the Statement of Additional Information or the report of how the Trust voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 at www.sec.gov.

QUARTERLY SCHEDULE OF PORTFOLIO HOLDINGS

The Trust files its Schedule of Portfolio Holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. You may request a free copy of the Trust’s Forms N-Q by calling 1-800-847-4836. The Trust’s Forms N-Q also are available at www.sec.gov. You also may review and copy the Forms N-Q for the Trust at the SEC’s Public Reference Room in Washington, DC. You may get information about the operation of the Public Reference Room by calling 1-800-SEC-0330.

BOARD APPROVAL OF INVESTMENT ADVISORY AGREEMENT

Both the Investment Company Act of 1940 (the “Investment Company Act”) and the terms of the investment advisory agreement of the Thrivent Cash Management Trust (the “Trust”) require that the agreement be approved annually by the Board of Trustees (the “Board”), including a majority of the Trustees who are not “interested persons” of the Trust, as defined in the Investment Company Act (the “Independent Trustees”). The nine-member Board consists of eight Independent Trustees, including the Chairman.

At its meeting on November 28, 2012, the Board voted unanimously to renew the existing investment advisory agreement, as amended, to reflect the name change from Thrivent Financial Securities Lending Trust to Thrivent Cash Management Trust, between the Trust and Thrivent Asset Management (the “Adviser”). In connection with its evaluation of the agreement with the Adviser, the Board reviewed a broad range of information requested for this purpose and considered a variety of factors, including the following:

| 1. | The nature, extent, and quality of the services provided by the Adviser; |

| 2. | The performance of the Trust; |

| 3. | The advisory fee and net operating expense ratio of the Trust compared to a peer group; |

| 4. | The cost of services provided and profit realized by the Adviser; |

| 5. | The extent to which economies of scale may be realized as the Trust grows; |

| 6. | Whether the fee levels reflect these economies of scale for the benefit of the Trust shareholders; |

| 7. | Other benefits realized by the Adviser or its affiliates from their relationship with the Trust; and |

| 8. | Any other factors that the Board deemed relevant to its consideration. |

In connection with the renewal process, the Contracts Committee of the Board (consisting of each of the Independent Trustees) met on six occasions from February 21 to November 28, 2012 to consider information relevant to the renewal process. The Independent Trustees also retained the services of Management Practice, Inc. (“MPI”) as an independent consultant to assist in the compilation, organization, and evaluation of relevant information. This information included statistical comparisons of the advisory fees and total operating expenses of the Trust in comparison to a peer group of comparable funds; information prepared by management with respect to the cost of services provided to the Trust and fees charged, including effective advisory; profit realized by the Adviser and its affiliates that provide services to the Trust; and information regarding the types of services furnished to the Trust, the personnel providing the services, changes in staff, and systems improvements. The Board also received reports from the investment management staff of the Adviser with respect to the securities lending balances of the Trust and the revenue of the securities lending program, which in part is based on the performance of the Trust. In addition to its review of the information presented to the Board during the contract renewal process and throughout the year, the Board also considered knowledge gained from discussions with management.

The Independent Trustees were represented by independent counsel throughout the review process and during executive sessions without management present to consider reapproval of the agreement. The Independent Trustees relied on their own business judgment in determining the weight to be given to each factor considered in evaluating the materials that were presented to them. The Contracts Committee’s and Board’s review and conclusions were based on a comprehensive consideration of all information presented to them and were not the result of any single controlling factor. The key factors considered and the conclusions reached are described below.

16

Table of Contents

Additional Information

(unaudited)

Nature, Extent and Quality of Services

At the Board’s regular quarterly meetings, management presented information describing the services furnished to the Trust by the Adviser. During these meetings, management reported on the investment management, securities lending activity, and compliance services provided to the Trust. During the renewal process, the Board considered the specific services provided by the Adviser. The Board also considered information relating to the investment experience and qualifications of the Adviser’s portfolio manager overseeing the Trust.

The Board received reports at its quarterly meetings from the Adviser’s Director of Fixed Income Investments and Chief Investment Officer, both of whom were present at all of the meetings. At quarterly meetings, the Director of Fixed Income Investments presented information about the Trust. At one of its quarterly meetings, a senior portfolio manager presented information about securities lending generally and the Trust’s securities lending activity in particular. These reports and presentations gave the Board the opportunity to evaluate the portfolio manager’s abilities and the quality of services he provides to the Trust. Additional information was presented to the Board describing the portfolio compliance functions performed by the Adviser. The Independent Trustees also received quarterly reports from the Trust’s Chief Compliance Officer.

The Board considered the adequacy of the Adviser’s resources used to provide services to the Trust. The Adviser reviewed with the Board the Adviser’s ongoing program to enhance portfolio management capabilities, including recruitment and retention of portfolio managers, research analysts, and other personnel, and investment in additional and updated technology systems and applications to improve investment research, trading and portfolio compliance, and investment reporting functions. The Adviser also discussed further refinements to certain compliance procedures and improved risk controls. The Board viewed these actions as a positive factor in reapproving the existing advisory agreement, as they demonstrated the Adviser’s commitment to provide the Trust with quality service. The Board concluded that, within the context of its full deliberations, the nature, extent and quality of the investment advisory services provided to the Trust by the Adviser supported renewal of the advisory agreement.

Performance of the Trust

The Board considered whether the Trust has operated in accordance with its investment objectives, which include maximizing current income consistent with preservation of capital and liquidity. In this regard, the Board reviewed stress test reports and considered the Adviser’s opinion that, in its view, the Trust could withstand events that were reasonably likely to occur within the next twelve-month period. At quarterly meetings, the Director of Fixed Income Investments reviewed with the Board the economic and market environment and risk management in connection with management of the Trust and other Thrivent fixed income funds. The Board noted that, as a money market fund, the Trust’s performance was impacted by various factors, including the low interest rate environment and increased regulatory requirements generally experienced by all money market funds.

The Board reviewed quarterly net revenues generated by securities lending activities for the benefit of other Thrivent funds, a portion of which is attributed to the performance of the Trust. The Board noted that the Trust is designed primarily for the investment and reinvestment of cash collateral on behalf of lenders participating in the Trust’s securities lending program, and to offer a sweep option for other investment companies and accounts managed by the Adviser or its affiliates and ultimately enhance the performance of those investment companies and accounts. With respect to performance, the Board considered safety of principal to be the primary goal, and it did not consider specific yield information separate from the securities lending revenue.

Advisory Fees and Fund Expenses

The Board reviewed information prepared by the Adviser comparing the Trust’s advisory fee with the advisory fees of its peer group of funds. The Board noted that the Trust’s advisory fee as compared to the Trust’s peer group was below the median. On the basis of its review, the Board concluded that the advisory fee rate charged to the Trust for investment management services was not excessive.

The Board also reviewed information prepared by the Adviser comparing the Trust’s overall expense ratio with the expense ratio of its peer group of funds. The Board noted that the Trust’s net operating expenses were below the median of its peer group.

Cost of Services and Profitability

The Board considered the profitability of the Adviser both overall and on a fund-by-fund basis. The Board also considered that the Adviser agreed to voluntarily reimburse the Trust for all expense in excess of 0.05% of average daily net assets. The Board considered the level of the Adviser’s profits with respect to all the Thrivent funds, including the Trust. The Board concluded that the Adviser’s profitability was reasonable.

17

Table of Contents

Additional Information

(unaudited)

Economies of Scale

The Board considered information regarding the extent to which economies of scale may be realized as the Trust’s assets increase and whether the fee levels reflect these economies of scale for the benefit of shareholders. The Adviser explained its general goal with respect to the employment of fee waivers, expense reimbursements, and breakpoints. The Board also considered management’s view that it can be difficult to generalize as to whether, or to what extent, economies in the advisory function may be realized as the Trust’s assets increase. The Board noted that expected economies of scale, where they may exist, may be shared through the use of fee waivers or reimbursements by the Adviser and/or a lower overall fee rate. The Board considered the advisory fee rate charged to the Trust and determined that the fee rate was acceptable even though the Adviser did not offer breakpoints or contractual waivers.

Other Benefits to the Adviser and its Affiliates

The Board considered information regarding potential “fall-out” or ancillary benefits that the Adviser and its affiliates may receive as a result of their relationship with the Trust, both tangible and intangible, such as their ability to leverage investment professionals who manage other portfolios, reputational benefits in the investment advisory community and the engagement of affiliates as service providers to the Trust. The Board noted that such benefits were difficult to quantify but were consistent with benefits received by other mutual fund advisers.

Based on the factors discussed above, the Contracts Committee unanimously recommended approval of the Advisory Agreement, and the Board, including all of the Independent Trustees voting separately, approved the agreement.

18

Table of Contents

This report is submitted for the information of shareholders of

Thrivent Cash Management Trust. It is not authorized

for distribution to prospective investors unless preceded or

accompanied by the current prospectus for Thrivent Cash

Management Trust, which contains more complete

information about the Trust, including investment objectives,

risks, charges and expenses.

Table of Contents

Item 2. Code of Ethics

Not applicable to semiannual report

Item 3. Audit Committee Financial Expert

Not applicable to semiannual report

Item 4. Principal Accountant Fees and Services

Not applicable to semiannual report

Item 5. Audit Committee of Listed Registrants

Not applicable

Item 6. Schedule of Investments

(a) Registrant’s Schedule of Investments is included in the report to shareholders filed under Item 1.

(b) Not applicable to this filing.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies

Not applicable

Table of Contents

Item 8. Portfolio Managers of Closed-End Management Investment Companies

Not applicable

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable

Item 10. Submission of Matters to a Vote of Security Holders

There have been no material changes to the procedures by which shareholders may recommend nominees to registrant’s board of trustees.

Item 11. Controls and Procedures

(a)(i) Registrant’s President and Treasurer have concluded that registrant’s disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940) are effective, based on their evaluation of these controls and procedures as of a date within 90 days of the filing date of this report.

(a)(ii) Registrant’s President and Treasurer are aware of no change in registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the Investment Company Act of 1940) that occurred during registrant’s most recent fiscal quarter that has materially affected, or is reasonably likely to materially affect, registrant’s internal control over financial reporting.

Item 12. Exhibits

Certifications pursuant to Rules 30a-2(a) and 30a-2(b) under the Investment Company Act of 1940 are attached hereto.

Table of Contents

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Date: June 27, 2013 | THRIVENT CASH MANAGEMENT TRUST | |||||||||

| By: | ||||||||||

| /s/ Russell W. Swansen | ||||||||||

| Russell W. Swansen | ||||||||||

| President | ||||||||||

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| Date: June 27, 2013 | By: | |||||||||

| /s/ Russell W. Swansen | ||||||||||

| Russell W. Swansen | ||||||||||

| President | ||||||||||

| Date: June 27, 2013 | By: | |||||||||

| /s/ Gerard V. Vaillancourt | ||||||||||

| Gerard V. Vaillancourt | ||||||||||

| President | ||||||||||