UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

(Mark One)

|

x

|

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2010

|

¨

|

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to

Commission file number: 001-34528

ZAGG INCORPORATED

|

NEVADA

|

20-2559624

|

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

|

3855 S 500 W, Suite J, Salt Lake City, UT

|

84115

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Issuer’s telephone number: (801) 263-0699

Securities registered under 12(b) of the Exchange Act: None

Securities registered under 12 (g) of the Exchange Act:

Common Stock, par value $0.001

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes o No þ

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 2 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No þ

Indicated by check mark whether the registrant:(1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark if disclosure of delinquent filings pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o Non-accelerated filer o Smaller reporting company þ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of June 30, 2010, was $47,475,026. For purposes of the foregoing calculation only, directors and executive officers and holders of 10% or more of the issuer’s common capital stock have been deemed affiliates.

The number of shares of the Registrant’s common stock outstanding as of March 17, 2011, was 24,128,874.

ZAGG INCORPORATED

2010 FORM 10-K

TABLE OF CONTENTS

|

Page

|

||

|

PART I

|

||

|

ITEM 1.

|

BUSINESS

|

1

|

|

ITEM 1A.

|

RISK FACTORS

|

10

|

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

17

|

|

ITEM 2.

|

PROPERTIES

|

17

|

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

17

|

|

ITEM 4.

|

[REMOVED AND RESERVED]

|

17

|

|

PART II

|

||

|

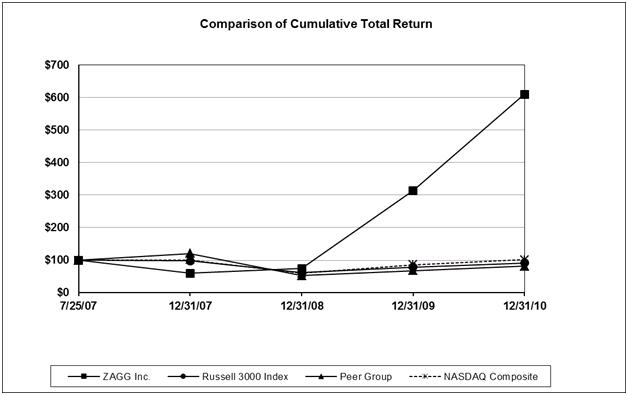

ITEM 5.

|

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

18

|

|

ITEM 6.

|

SELECTED FINANCIAL DATA

|

21

|

|

ITEM 7.

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

21

|

|

ITEM 7A.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

29

|

|

ITEM 8.

|

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

29

|

|

ITEM 9.

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

|

29

|

|

ITEM 9A.

|

CONTROLS AND PROCEDURES

|

30

|

|

ITEM 9B.

|

OTHER INFORMATION

|

33

|

|

PART III

|

||

|

ITEM 10.

|

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

33

|

|

ITEM 11.

|

EXECUTIVE COMPENSATION

|

33

|

|

ITEM 12.

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

33

|

|

ITEM 13.

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

|

33

|

|

ITEM 14.

|

PRINCIPAL ACCOUNTING FEES AND SERVICES

|

33

|

|

PART IV

|

||

|

ITEM 15.

|

EXHIBITS, FINANCIAL STATEMENT SCHEDULES

|

33

|

|

SIGNATURES

|

35 |

PART I

Special Note Regarding Forward-Looking Statements

Information included or incorporated by reference in this Annual Report on Form 10-K contains forward-looking statements. All forward-looking statements are inherently uncertain as they are based on current expectations and assumptions concerning future events or future performance of the Company. Readers are cautioned not to place undue reliance on these forward-looking statements, which are only predictions and speak only as of the date hereof. Forward-looking statements may contain the words “estimate,” “anticipate,” “believe,” “expect,” “forecast,” or similar expressions, and are subject to numerous known and unknown risks and uncertainties. Additionally, statements relating to implementation of business strategy, future financial performance, acquisition strategies, capital raising transactions, performance of contractual obligations, and similar statements may contain forward-looking statements. In evaluating such statements, prospective investors and shareholders should carefully review various risks and uncertainties identified in this Report, including the matters set forth under the captions “Risk Factors” and in the Company’s other SEC filings. These risks and uncertainties could cause the Company’s actual results to differ materially from those indicated in the forward-looking statements. The Company disclaims any obligation to update or publicly announce revisions to any forward-looking statements to reflect future events or developments.

Although forward-looking statements in this Annual Report on Form 10-K reflect the good faith judgment of our management, such statements can only be based on facts and factors currently known by us. Consequently, forward-looking statements are inherently subject to risks and uncertainties, and actual results and outcomes may differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, without limitation, those specifically addressed under the heading “Risk Factors Related to Our Business” below, as well as those discussed elsewhere in this Annual Report on Form 10-K. Readers are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this Annual Report on Form 10-K. We file reports with the Securities and Exchange Commission (“SEC”). You can read and copy any materials we file with the SEC at the SEC’s Public Reference Room, 100 F. Street, NE, Washington, D.C. 20549. You can obtain additional information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including us.

We disclaim any obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this Annual Report on Form 10-K. Readers are urged to carefully review and consider the various disclosures made throughout the entirety of this annual report, which attempt to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

| ITEM 1. | BUSINESS |

Our Business

Headquartered in Salt Lake City, Utah, ZAGG Incorporated designs, manufactures and distributes protective coverings, audio accessories and power solutions for consumer electronic and hand-held devices under the brand names invisibleSHIELD®, ZAGGskins™, ZAGGbuds™, ZAGGsparq™, and ZAGGmate™.

Our flagship product, the invisibleSHIELD, is made from a protective film covering that was developed originally to protect the leading edges of rotary blades of military helicopters. We determined that this same film product could be configured to fit onto the surface of electronic devices and marketed to consumers for use in protecting such devices from everyday wear and tear, including scratches, scrapes, debris and other surface blemishes. The film also permits touch sensitivity, meaning it can be used on devices that have a touch-screen interface. The invisibleSHIELD film material is highly reliable and durable because it was originally developed for use in a high friction, high velocity context within the aerospace industry. The film provides long lasting protection for the surface of electronic devices subject to normal wear and tear. The film is a form of polyurethane substance, akin to a very thin, pliable, flexible and durable clear plastic that adheres to the surface and shape of the object it is applied to.

1

The invisibleSHIELD is designed specifically for iPods®, iPads®, laptops, cell phones, digital cameras, watch faces, GPS systems, gaming devices, and other items. The product is “cut” to fit specific devices and packaged together with a moisture activating solution which makes the invisibleSHIELD adhere to the surface of the device, literally “like a second skin,” and virtually invisible to the eye. The patent-pending invisibleSHIELD is the first scratch protection solution of its kind on the market. The invisibleSHIELD is not ornamental, but rather provides a long lasting barrier to preserve the brand new look of the surface of an electronic device. In early 2010 we introduced the invisibleSHIELD DRY through retail partners, which is a protective film made from the same material as the original invisibleSHIELD, and engineered to be clearer, smoother to the touch, and apply without the need for fluid. In the beginning of 2011 we added the invisibleSHIELD Smudge-Proof to our line, which also incorporates the invisibleSHIELD film with added features that eliminate smudges, fingerprints, and glare from the device display.

Currently, ZAGG offers over 5,000 precision pre-cut invisibleSHIELD designs with a lifetime replacement warranty through online channels, big-box retailers, electronics specialty stores, resellers, college bookstores, Mac stores, and mall kiosks. We plan to increase our product lines to offer new electronic accessories to our tech-savvy customer base, as well as an expanded array of invisibleSHIELD products for other industries. Given the amazing success of the invisibleSHIELD, ZAGG has the unique opportunity to offer additional accessories from a trusted source to gadget enthusiasts worldwide.

The ZAGGaudio brand of electronics accessories and products were first released in late 2008, and continues to focus on innovation and superior value. The flagship product within ZAGGaudio is the award winning ZAGGsmartbuds™ line, which includes ZAGGaquabuds, a water-resistant earbud introduced in late 2010. A previous winner of the coveted CES Design and Innovation award, the ZAGGsmartbuds line has been very well received by professional reviewers, experts and the consumer base. On January 12, 2010, we were awarded patent number US D 607,875 by the U.S. Patent and Trademark Office, covering design elements of ZAGGsmartbuds in-ear headphones.

ZAGGskins were introduced in November 2009, and combine customizable, high-resolution images with the scratch protection of ZAGG’s invisibleSHIELD. To create a ZAGGskin, consumers select from a library of professional designs or upload their own high-resolution personal photos or images. The printed image, custom designed for their device, is then merged with the exclusive, ultra-tough, patented invisibleSHIELD film, which allows customers to both protect and individualize their gadgets with a single product.

In early 2009 we introduced the ZAGGsparq, a small, powerful, portable battery that can recharge a power-hungry “smartphone” up to four times before the ZAGGsparq itself needs to be recharged. Featuring a 6000ma lithium polymer cell, the ZAGGsparq plugs into a wall outlet and provides two USB ports for charging mobile devices. An adapter is also included that fits many international standards. The ZAGGsparq is compatible with any USB-charged device, including the Apple® iPad and iPhone®, as well as cell phones, handheld gaming systems, and digital cameras.

We also introduced ZAGG LEATHERskins in early 2010. ZAGG LEATHERskins are thin, pliable cases that apply directly to personal electronics like a film, and are created from genuine leather. Available in typical leather shades and premium animal patterns, ZAGG LEATHERskins use an adhesive that holds the skin firmly in place on the device, but can be removed if necessary. Later in 2010, we broadened the line to include ZAGG sportLEATHER, which are also created from genuine leather and feature authentic recreations of baseball, football and basketball textures. ZAGG LEATHERskins and sportLEATHERS are available for the most popular personal electronics.

We introduced the ZAGGmate on November 26, 2010, – “Black Friday” – in select national retailers. The ZAGGmate is a protective and functional companion to the Apple iPad that accentuates both the appearance and utility of Apple's innovative device. Made from aircraft-grade aluminum with a high quality finish, the patent-pending ZAGGmate matches the design, look and feel of the iPad. The ZAGGmate line features two models, one with a simple, innovative stand and built-in wireless Bluetooth® keyboard that allows for fast, responsive typing, and interaction with the iPad's features. The second model replaces the keyboard with a more versatile stand that provides multiple angles for use. We have already seen tremendous media attention for the ZAGGmate, including an appearance on The Oprah Winfrey Show, where it was introduced to the host by rapper-turned-tech-mogul MC Hammer. The ZAGGmate has also already won several prestigious industry awards, including the Macworld Expo 2011 Best of Show and recognition as a CES Innovations Design and Engineering Honoree.

2

We maintain our corporate offices and operational facility at 3855 South 500 West, Suites B, C, J, K, L, M, O and R, Salt Lake City, Utah, 84115. The telephone number of the Company is 801-263-0699. Our website address is www.ZAGG.com. Information contained on, or accessible through, our website is not a part of, and is not incorporated by reference into, this report.

Strategy

At ZAGG, we are “Zealous About Great Gadgets.” We believe that hand-held devices and gadgets have been developed to be aesthetically pleasing as designed and that bulky silicone, plastic or leather cases impede the overall end users’ enjoyment of the form and function of their device. Consumers purchase these types of accessories to help protect their devices from getting scratched and damaged. The invisibleSHIELD provides the end consumer with an alternative to bulky cases that provides unparalleled device protection without impeding the functionality and enjoyment of the consumers’ device.

We will continue to expand our product offering and focus on innovative products and services that we can target market to our customers based on their purchase history. When a customer purchases an invisibleSHIELD from ZAGG, we know exactly what type of device they have, as the invisibleSHIELD is custom cut for each device. With that information we can develop specific marketing plans to sell additional products including power supplies, car chargers, ear buds and other accessory items. Our current lines of accessory items, including our brands ZAGGskins™, ZAGG LEATHERskins™, ZAGGbuds™, ZAGGsparq™, and ZAGGmate™, are available to our customers through our website at www.ZAGG.com and through our retail distribution channels as well.

As we continue to develop and enhance our brand name and reputation, we anticipate entering into additional complementary industries to provide support to our invisibleSHIELD product line.

Design and Packaging

We design and cut the invisibleSHIELD product for application on thousands of specific electronic devices. We acquire raw materials from third party sources that are delivered to our facilities and assembled for packaging. In addition, we out-source high volume precision-cutting of the materials, which we consider to be more cost effective. We then package the configured materials together with an installation kit consisting of a moisture adhesive-activating solution, a squeegee, and instructions for application on specific electronic devices. We also outsource some of these packaging processes to independent third parties. We have developed relationships with package assembly, shipping, and logistics companies that allow us to expand our production and shipping capacity as we continue to grow.

We have a patent pending on the process of wrapping an entire gadget body in a transparent, durable and semi-permanent film. We also custom design each cutout for the film and currently have unique designs for over 5,000 devices. The cutout designs are developed internally and owned exclusively by us. We do not own the patent for the base materials, but have an exclusive agreement with the supplier for the use of the film and believe that our relationship with the manufacturer of the raw material is on excellent terms and anticipate no interruption in our ability to acquire adequate supplies of the materials and produce products.

We have developed our retail packaging with the input of major retailers to appeal to the end consumer on a retail basis. We have designed the cardboard box packaging to be informative and attractive for point-of-sale displays.

Market for Products

The portable electronic device market, notably handheld devices, is continuing to see advancements in performance and functionality in existing models. Furthermore, the market is expanding as evidenced by new product developments in portable electronic devices. Correspondingly, the aesthetics of such devices is increasingly important to the extent that buyers are considering the look and feel of such devices, as much as performance, in making their purchasing decisions.

3

As a result, an industry and significant market has emerged in protecting portable electronic devices, notably the “high end” devices – both in terms of price, and design/functionality. Consumers are seeking ways to protect the device from wear and tear and damage, but not impede the look, feel, or functionality of the device.

We sell the invisibleSHIELD directly, and through our distributors and retail sellers, to consumers of electronic household and hand-held devices. We sell a significant amount of product for use on Apple’s iPad, iPhone, and iPod devices. According to industry reports, Apple sold over 15 million iPads in 2010 and could sell as many as 40 million iPads alone in 2011, including the release of a new model of iPad. The handheld electronics industry has continued to market and develop devices with touch screen interfaces, and several major manufacturers, including Samsung, Motorola and RIM will release competing products to the iPad in 2011. The invisibleSHIELD is the ideal device protection offering for all types of gadgets, in particular touch-screen tablets, as it does not interfere with the functionality of the device while offering complete scratchproof protection. We will continue to focus our marketing efforts around these types of gadgets as the premier protection solution while maintaining the overall form and functionality of the device.

To date, we have not partnered with any manufacturers of electronic devices to bundle our products with such devices on initial sale, or to include as part of the device, the application of our products. In the future, we may seek such an arrangement or an alternative co-marketing agreement, but we have not entered into definitive negotiations for such an arrangement as yet.

Market Segments

With over 5,000 invisibleSHIELD products/product configurations available, we have a protective covering for all major market segments of handheld electronic devices, including: iPods and other brand MP3 players, iPads and other notebook computers, cell phones, laptops, GPS devices, watch faces, and similar devices and surfaces. We intend to continue to configure the invisibleSHIELD product for use in newly developed consumer devices. Unlike manufacturers of competing device cases that need months to design and manufacture customized accessories for new devices, the invisibleSHIELD can be quickly configured and packaged for new devices as they enter the consumer marketplace, making the invisibleSHIELD available for purchase ahead of competing accessories for new electronic devices.

One of our fastest growing market segments is the smart phone consumer. Most often, smart phone buyers are drawn to the device by its elegant design, as well as its easy-to-use functionality. However, everyday use often mars the finish on most smart phone devices, screen and other areas that receive wear and tear. Traditional protective products are bulky and detract from a smart phone’s elegance by covering it up. Other common protectors either do not offer enough protection, or they are not durable enough to properly protect the device. However, an invisibleSHIELD covering is exactly that – invisible – meaning it does not cover up the design, form or functionality of the smart phone and doesn’t inhibit the touch sensitivity for smart phones with touch screen technology.

As sales of electronics continue to grow, we anticipate that sales of our complimentary products will continue to grow, as well. Four of the largest areas of our market opportunities relate to sales of iPods, cellular telephones, digital cameras and tablet computing devices. According to industry sources, over 48.7 million iPods, 47.4 million iPhones, and 14.7 million iPads were sold by Apple Corporation for the year ended December 31, 2010. Early estimates conclude that over 1.38 billion cell phones and over 109.9 million digital cameras were sold worldwide in 2010. ZAGG is positioned to serve all of these markets with its after-market invisibleSHIELD products.

Marketing and Distribution

We sell our products directly on our website, through distributors, through kiosk vendors in shopping malls and retail centers, and through electronics retailers. Our products are available for sale worldwide via our website. Currently we advertise our products on the Internet and through point of sale displays at retail locations. We also advertise our products on television and radio both locally and nationally. We intend to expand our advertising while continuing our advertising strategy over the course of 2011. We are also seeking to create strategic partnerships with makers of cellular phone devices and electronic accessories.

Indirect Channels

We sell our invisibleSHIELD products through indirect channels including big box retailers, domestic and international distributors, independent Apple retailers, university bookstores, and small independently owned consumer electronics stores. For the year ended December 31, 2010, we sold approximately $55,396,674 of product through these indirect channels, or approximately 73% of our overall net sales for 2010. We require all indirect channel partners to enter into a reseller agreement with us.

4

We continue to utilize multiple distributors to market and place our products for sale in the United States and abroad. We have entered into distribution agreements for many geographic locations including the United States, United Kingdom, Australia, Hong Kong, Saudi Arabia, South Korea, Mexico, Germany and South America for the marketing, distribution and sale of our products.

We are continuously negotiating for new distribution relationships in the United States and abroad to increase the marketing and sale of our products in retail locations.

Website Sales

We sell our products worldwide directly to consumers on our website at www.ZAGG.com. For the year ended December 31, 2010, we sold approximately $14,033,683 of product on our website, or approximately 18% of our overall net sales for 2010.

We also generated revenue from shipping charges to customers. For the year ended December 31, 2010, we generated approximately $1,883,623 from shipping charges, primarily from our internet customers, or approximately 2% of our overall net sales for 2010.

Mall Kiosk Vendors

We sell our invisibleSHIELD products to kiosk vendors in shopping malls and retail centers. We enter into agreements with such vendors who purchase the products and resell them to consumers. For the year ended December 31, 2010, we sold approximately $4,641,734 of product, or approximately 7% of our overall net sales for 2010, through our corporate owned mall carts and to licensed cart owners. The third party licensed cart owners are required to enter into a standard license and resale agreement with us wherein we charge an upfront license fee that is recognized into revenue over the life of the license. For the year ended December 31, 2010, we recognized $179,306 related to these license agreements.

Company Organization

Our operations are divided and organized as follows: marketing and sales, which includes the development and maintenance of our website, customer service, production, distribution and shipping, art and graphics, product design, and general and administration functions.

Warranties

We offer a lifetime guaranty of the durability of our invisibleSHIELD products. If the invisibleSHIELD is ever scratched or damaged (in the course of normal use), a customer simply needs to send back the old product and we will replace it for free. The products that the invisibleSHIELD is applied to, typically have relatively short lives which helps to limit our exposure for warranty claims. We also offer limited warranties on our audio and charging product lines that are fully covered by our manufacturing partners for these products.

Intellectual Property Rights:

ZAGG owns U.S. Patents that relate to its invisibleSHIELD® protective films for electronic gadgets, and continues to actively pursue additional protection for its invisibleSHIELD® protective films in both the United States and Internationally. ZAGG is currently seeking patent protection for (i) durable transparent films that cover and protect all of the outer surfaces of consumer electronic devices; (ii) both wet and dry apply processes for securing protective films to consumer electronic devices; and (iii) dry-apply protective films. ZAGG has also obtained and continues to seek patent protection for its popular ZAGGbud™ in-ear headphones. In addition, ZAGG has filed patent applications for its ZAGGmate™ protective cases (with and without a keyboard) which provide protection for tablet computers without distracting from their appearance. As of December 31, 2010, ZAGG was only selling ZAGGmate™ protective cases for the Apple iPad.

ZAGG is the owner of more than 5,000 designs for ZAGG’s invisibleSHIELD protective films which are currently available for various consumer electronic devices. New designs are routinely added to ZAGG’s IP portfolio. ZAGG is also actively developing new designs for its ZAGGmate. ZAGG has filed design applications in the United States and abroad to protect many of its most popular designs.

5

ZAGG claims common law protection for and/or has applied to register a variety of trademarks and service marks in the United States and a number foreign countries for “ZAGG” and various ZAGG logos, “invisibleSHIELD” and various invisibleSHIELD logos, “ZAGGmate,” “Military Grade,” “Made for Smartphones,” and numerous other trademarks and service marks.

In addition, ZAGG has strategically developed exclusive relationships and exclusive agreements with a number of critical third party vendors, suppliers and partners. ZAGG’s long-standing relationships with its raw materials suppliers and its manufacturers expand the scope of potential intellectual protection available to ZAGG including development of innovative solutions for protective films. These exclusive relationships also provide ZAGG with a reasonable expectation that it will be able to supply its customers with products long into the future.

ZAGG regularly files applications to protect its inventions, designs and trademarks. While ZAGG believes that the ownership of intellectual property protection is important to its business, and that its success is based in part upon the ownership of intellectual property rights, ZAGG’s success is also based upon the innovation competencies of its qualified and creative team.

Patents

ZAGG has been awarded US Patent D607,875 by the United States Patent and Trademark Office. The patent covers, among other things, design elements of ZAGG’s popular ZAGGbuds™ in-ear headphones. ZAGG is seeking further patent protection for its ZAGGbuds™ in-ear headphones through the patent application that has been published as U.S. Patent Application Publication 2010/0272305.

ZAGG has acquired the U.S. Patents 7,389,869 and 7,784,610. These patents provide ZAGG with exclusive rights to certain kits and methods for applying protective films to mobile electronic devices.

ZAGG’s U.S. Patent Application Publication 2009/0086415, titled Protective Covering for An Electronic Device, has been filed to provide ZAGG with exclusive patent rights to protective coverings and systems and methods for covering mobile electronic devices with thin protective films. This includes both partial coverings and full coverings.

U.S. Patent Application Publication 2010/0270189, titled Protective Covering with Customizable Image for An Electronic Device is intended to protect our ZAGGskin™ products.

A significant number of additional yet-to-be published patent applications have been filed by ZAGG to protect its innovations.

Trademarks

We have received the following Trademark Registrations from the United States Patent and Trademark Office:

|

·

|

SHIELD DESIGN TRADEMARK, Registration 3,923,393

|

|

·

|

INVISIBLE SHIELD, Registration 3,825,458

|

|

·

|

ZAGG, Registration 3,838,237

|

6

We have the following Trademark Applications pending with the United States Patent and Trademark Office:

|

·

|

INVISIBLE SHIELD

|

|

·

|

ZAGG

|

|

·

|

APPSPACE

|

|

·

|

ZAGGBOX

|

|

·

|

ZAGG with design

|

|

·

|

SHIELD ZONE

|

|

·

|

MADE FOR SMARTPHONES

|

|

·

|

MADE FOR SMARTPHONES logo

|

|

·

|

Z with design

|

|

·

|

SPARQ

|

We also claim common law trademark rights in the U.S. to each of the trademarks listed above as well as to the following marks: the ZAGG shield logo, “ShieldSpray,” “Invisible Invincible,” “Protect Your Digital Life,” “Ultimate Scratch Protection,” “Military Grade”, Military Grade logo, “Rise Above,” “ZAGGbuds,” “ZAGGfoam,” “ZAGGmate,” “ZAGGwipes,” “Zealous About Great Gadgets,” “ZAGGskins,” “ZAGGaudio,” “ZAGGsparq,” “Z with design,” “Z.buds,” “ZAGGsmartbuds,” “Z.buds Edge,” “ZAGGbox,” “Nano-Memory,”and “Enhancing and Protecting the Mobile Experience.”

We have also received the following trademark registrations outside of the U.S.:

|

·

|

ZAGG, CTM No. 006328215 – EUROPEAN UNION

|

|

·

|

ZAGG, Reg. No. 5234734 – JAPAN

|

|

·

|

ZAGG, Reg. No. 1266121 – AUSTRALIA

|

|

·

|

ZAGG, Reg. No. 301217754 – HONG KONG

|

|

·

|

ZAGG, No. 40-2008-0048050 – SOUTH KOREA

|

|

·

|

ZAGG, Reg. No. 1098228 – MEXICO

|

|

·

|

ZAGG, Reg. No. 744833 - CHINA

|

|

·

|

INVISIBLE SHIELD, Resolution No. 63779 - COLUMBIA

|

|

·

|

INVISIBLE SHIELD with design, CTM. No. 8492051 – EUROPEAN UNION

|

We have filed the following trademark applications with the trademark office in India:

|

·

|

INVISIBLE SHIELD with Design

|

We have filed trademark applications for the mark APPSPACE in the following jurisdictions:

|

·

|

United States

|

|

·

|

Canada

|

|

·

|

European Union

|

|

·

|

Australia

|

|

·

|

China

|

|

·

|

Japan

|

7

We have filed trademark applications for the mark ZAGG pending in the following jurisdictions:

|

·

|

United States

|

|

·

|

Canada

|

|

·

|

India

|

|

·

|

Columbia

|

We have filed trademark applications for mark INVISIBLE SHIELD in the following jurisdictions:

|

·

|

United States

|

|

·

|

Canada

|

|

·

|

Columbia

|

Government Regulations

Our operations are subject to various federal, state and local employee workplace protection regulations including those of the Occupational Safety and Health Administration (“OSHA”). We believe that compliance with federal, state and local environmental protection regulations will not have a material adverse effect on our capital expenditures, earnings and competitive and financial position. Although we believe that our worker and employee safety procedures are adequate and in compliance with law, we cannot completely eliminate the risk of injury to our employees, or that we may occasionally, unintentionally, be out of compliance with application law. In such event, we could be liable for damages or fines or both.

Employees

We have 156 full-time employees and 27 part time employees including our management team. We have 61 employees in sales and marketing including our website and design, 10 in general and administration, 10 in operations, 13 in technology support, and 64 customer service agents. We have 25 employees employed on an hourly or part-time basis at our retail cart/kiosk locations. No employee is represented by a labor union, and we have never suffered an interruption of business caused by labor disputes. We believe our relationship with our employees is good.

Our Corporate History

We were formed as a Nevada corporation on April 2, 2004, under the name Amerasia Khan Enterprises Ltd (“AKE”). On February 8, 2007, AKE executed an Agreement and Plan of Merger (the “Merger Agreement”) by and between AKE and its wholly owned subsidiary, SZC Acquisition, Inc., a Nevada corporation (“Subsidiary”) on the one hand, and ShieldZone Corporation, a Utah corporation (“ShieldZone”) on the other hand. Pursuant to the Merger Agreement, ShieldZone merged with Subsidiary, with ShieldZone surviving the merger and Subsidiary ceasing to exist (the “Merger”).

Following the Merger, ShieldZone was reincorporated in Nevada as a subsidiary of AKE. On March 7, 2007, ShieldZone was merged up and into AKE. At that time, AKE changed its name to ZAGG Incorporated, and the operations of the surviving entity (ZAGG Incorporated) are solely that of ShieldZone. As a result of these transactions, the historical financial statements of ZAGG Incorporated are the historical financial statements of ShieldZone. The fiscal year end of the Company is December 31.

We changed our name from ShieldZone Corporation to ZAGG Incorporated to better position the company to become a large and encompassing enterprise in the electronics’ accessories industry through organic growth and through making targeted acquisitions. The ShieldZone name was very specific to the invisibleSHIELD product line, and although the invisibleSHIELD is and will continue to be our core product, the name change has brought us the opportunity to easily add new products to our product offering. ZAGG will continue to search out other complimentary proven products and companies that fit the ZAGG lifestyle and strategy for fast growth.

8

Recent Developments

In June 2008, a former member of our board of directors, Lorance Harmer, introduced us to a potential consumer electronics product, which became known as the ZAGGbox. The ZAGGbox aggregates digital content such as music, pictures, videos and movies in a single location and allows the user to share the content with most other networked media players, including mobile devices. After investigating the market opportunity for the ZAGGbox, we determined in June 2009 to license certain rights for the development and sale of the ZAGGbox in North America. Thereafter, we entered into a Distribution and License Agreement with Teleportall, LLC, the owner of the technology used in the ZAGGbox, under which Teleportall agreed to manufacture and deliver ZAGGboxes to us and we were appointed the exclusive distributor for the ZAGGbox in North American. On June 17, 2009, we issued our initial purchase order for 15,000 ZAGGbox units and advanced to Teleportall a total of $1,152,500 representing a $200,000 NRE fee and $952,500 in payment of 30% of the total purchase price for the 15,000 units ordered by us.

Teleportall proceeded to develop and test prototypes of the ZAGGbox and provided periodic progress reports to us. We continued to conduct market analysis for the product and requested several changes to the functions and features of the ZAGGbox. Teleportall did not deliver the product in time for the 2009 Christmas selling season.

Development of the product continued in 2010 with the expectation that the product would be delivered in time for the 2010 Christmas selling season. We made additional payments for long lead-time parts to Teleportall in the aggregate amount of $2,747,410. When it became obvious to us that the product would not be ready to market and sell during the 2010 Christmas season, we commenced discussions to restructure the Distribution and License Agreement with Teleportall. During the course of those discussions, we learned in January 2011 that Mr. Harmer had an indirect interest of 25% in Teleportall. As a result, on March 23, 2011, we entered into a settlement agreement with Mr. Harmer and several entities owned or controlled by Mr. Harmer, pursuant to which the parties agreed to terminate the Distribution and License Agreement on the following terms:

|

·

|

Mr. Harmer, Teleportall, and certain of their affiliates delivered a promissory note (the “Note”) dated March 23, 2011 to us in the original principal amount of $4,125,902 which accrues interest at the rate of LIBOR plus 4% per annum (adjusted quarterly) payable as follows: (i) interest only payments (a) on September 23, 2011, and thereafter (b) on or before the last day of each calendar quarter, (ii) 50% of the net profits of each ZAGGbox sale by Teleportall and its affiliates to be applied, first, to accrued interest and, second, to the principal balance of the Note, and (iii) the unpaid balance due in full on March 23, 2013. The principal amount of the Note is the aggregate amount of the payments made by us to Teleportall and the internal cost of the ZAGGbox project incurred by us. The Note is secured by certain real property, interests in entities that own real property and restricted securities.

|

|

·

|

Teleportall and the Company entered into a License Agreement on March 23, 2011 under which we licensed to Teleportall the use certain ZAGG names and marks to sell and distribute the ZAGGbox product. Teleportall shall pay ZAGG a 10% royalty on net sales of ZAGGboxes per calendar quarter.

|

|

·

|

Teleportall and ZAGG entered into a non-exclusive Commission Agreement on March 23, 2011, under which Teleportall may make introductions of many ZAGG products in all countries where ZAGG does not currently have exclusive dealing agreements in respect of the marketing, distribution or sale of its products. The Commission Agreement is for a term of two (2) years; provided that (a) the Commission Agreement shall automatically terminate concurrent with any uncured default under the Note, and (b) the term may be extended for an additional term on reasonable terms if Teleportall’s introductions during the initial term result in the purchase of no less than $25,000,000 of ZAGG products during the initial term. Payment terms of the Commission Agreement are as follows:

|

|

·

|

10.0% commission payments on orders received by us from retailers and distributors first introduced to the company by Teleportall during the first 60 days after the introduction is made (the “Load-in Period”) to be split 50/50 between cash to Teleportall and principal payments on the Note. However, all commission payments will be paid to ZAGG if Teleportall is in breach of the terms of the Note or any other agreements between the parties; and

|

|

·

|

3.0% commission on all orders within the first 24 months after the Load-in Period, and 2.0% thereafter, from any orders generated in the countries where Teleportall is paid a commission under the terms set forth in the preceding bullet point (excluding the United States) regardless of Teleportall’s involvement in ZAGG’s receipt of the order for 5 years. The 3.0% and 2.0% commissions will be split 50/50 between cash to Teleportall and principal payments on the Note.

|

9

HzO Transaction

On November 18, 2010, we filed a Current Report on Form 8-K to disclose the conversion of a bridge loan into shares of HzO Series A Preferred Stock, and the resulting acquisition of 55% of HzO by us. The assets acquired consisted of approximately $150,000 in equipment and certain intangible assets. As such, we determined that we were not required to file an amendment to the Current Report to provide separate financial information relating to HzO. All required financial information relating to HzO is included in the financial statements and related footnotes of this Report.

Changes to Board of Directors

On March 14, 2011, Lorence A. Harmer resigned as a director of the Company. Mr. Harmer had served on several of our Committees through November 5, 2010 including serving as the Chairman of the Company’s Audit Committee; as a member of our Compensation and Stock Option Committee; and as a member of our Nominating and Corporate Governance Committee. Effective November 5, 2010, Randall Hales was appointed as the chairman of our Audit Committee.

On March 9, 2011, the Company appointed Cheryl Larabee as a member of the Company’s Board of Directors. Ms. Larabee will serve on the Audit Committee of the Company’s Board of Directors.

Ms. Larabee is the Associate Vice President for University Advancement at Boise State University. She has campus-wide responsibility for development activities with a focus on the College of Business & Economics where she also serves as an adjunct faculty member.

Ms. Larabee had a 25-year corporate banking career focused on financial problem-solving with clients ranging from start-ups to the Fortune 500. She is the former Senior Vice President and Western U.S. Regional Manager of the Corporate Banking Division at KeyBank. Previously she managed middle market teams at U.S. Bank in Portland, Oregon, and served a national client base at Crocker Bank in San Francisco, California.

Ms. Larabee currently serves on the boards of Norco Inc., Jacksons Food Stores, Healthwise Inc., Syringa Bancorp, Bogus Basin Recreation Association and the Capital City Development Corporation.

Amended and Restated Loan Agreement

On March 8, 2011, we entered into an Amended and Restated Loan Agreement dated March 7, 2011 (the “A&R Loan Agreement”), with U.S. Bank National Association (“U.S. Bank”), and a Security Agreement dated March 7, 2011, with U.S. Bank (the “Security Agreement”) and related agreements described in the Loan Agreement and Security Agreement. The A&R Loan Agreement amends certain terms from a prior Loan Agreement between the Registrant and U.S. Bank dated May 13, 2010, and is discussed more fully below in the Section “Liquidity and Capital Resources.”

| ITEM 1A. | RISK FACTORS |

Risks Related to our Financial Condition

If we are unable to maintain our line of credit facility with US Bank, we could face a deficiency in our short term cash needs that would negatively impact our business.

We have secured a line of credit from US Bank that allows us to borrow up to $20 million. This provides us with the ability to access cash needed to finance certain costs and expenses. At December 31, 2010, we had financing availability of $5.0 million under this line which was increased to $20 million by amendment dated March 7, 2011. We pay fees based on LIBOR plus 1.75% for any monies borrowed under the line and an unused line fee that ranges from 0% to 0.2% per annum depending on the unused amount. We are also required to maintain a fixed charge coverage ratio of no less than 1.25 to 1.00 measured quarterly on a trailing twelve month basis and a leverage ratio of no greater than 2.5 to 1.0 measured quarterly on a trailing twelve month basis. If we are not compliant with the covenants, US Bank may decide to limit our ability to access the line of credit at any time in its discretion. In such event, our short-term cash requirements may exceed available cash on hand resulting in material adverse consequences to our business.

Risks Related to our Company and Business

Because sales in consumer electronic accessories are dependent on new products, product development and consumer acceptance, we could experience sharp decreases in our sales and profit margin if we are unable to continually introduce new products and achieve consumer acceptance.

The consumer and mobile electronics accessory industries are subject to constantly and rapidly changing consumer preferences based on performance features and industry trends. As of the date of this Report, we generated substantially all of our sales from our consumer and mobile electronics accessories business. We cannot assure you that we will be able to continue to grow the revenues of our business or maintain profitability. Our consumer accessories business depends, to a large extent, on the introduction and availability of innovative products and technologies. Significant sales of our products in the niche consumer electronic accessories market have fueled the recent growth of our business. We believe that our future success will depend in large partly upon our ability to enhance our existing products and to develop, introduce and market new products and improvements to our existing products.

10

However, if we are not able to continually introduce new products that achieve consumer acceptance, our sales and profit margins may decline. Our revenues and profitability will depend on our ability to maintain and generate additional customers and develop new products. A reduction in demand for our existing products would have a material adverse effect on our business. The sustainability of current levels of our business and the future growth of such revenues, if any, will depend on, among other factors:

|

§

|

the overall performance of the economy and discretionary consumer spending,

|

|

§

|

competition within key markets,

|

|

§

|

customer acceptance of newly developed products and services, and

|

|

§

|

the demand for other products and services.

|

We cannot assure you that we will maintain or increase our current level of revenues or profits from sales from the consumer and mobile electronics accessories business in future periods.

While we are pursuing and will continue to pursue product development opportunities, there can be no assurance that such products will come to fruition or become successful. Furthermore, while a number of those products are being tested, we cannot provide any definite date by which they will be commercially available. We cannot provide assurance that these products will prove to be commercially viable. We may experience operational problems with such products after commercial introduction that could delay or defeat the ability of such products to generate revenue or operating profits. Future operational problems could increase our costs, delay our plans or adversely affect our reputation or our sales of other products which, in turn, could have a material adverse effect on our success and our ability to satisfy our obligations. We cannot predict which of the many possible future products will meet evolving industry standards and consumer demands. We cannot provide assurance that we will be able to adapt to such technological changes, offer such products on a timely basis or establish or maintain a competitive position.

Because we face intense competition, including competition from companies with significantly greater resources than ours, if we are unable to compete effectively with these companies, our market share may decline and our business could be harmed.

Our market is highly competitive with numerous competitors. Some of our competitors may have substantially greater financial, technical, marketing, and other resources than we possess, which may afford them competitive advantages over us. As a result, our competitors may introduce products that have advantages over our products in terms of features, functionality, ease of use, and revenue producing potential. They may also have more fully developed sales channels for consumer sales including large retail seller arrangements and international distribution capabilities. In addition, new companies may enter the markets in which we compete, further increasing competition in the consumer electronics accessories industry. We may not be able to compete successfully in the future, and increased competition may result in price reductions, reduced profit margins, loss of market share and an inability to generate cash flows that are sufficient to maintain or expand our development and marketing of new products, which would adversely impact the trading price of our common shares.

Because we are dependent on third party sources to acquire sufficient quantities of raw materials to produce our products, any interruption in those relationships could harm our results of operations and our revenues.

We acquire substantially all of our raw materials that we use in our products from five suppliers. Accordingly, we can give no assurance that:

|

§

|

our supplier relationships will continue as presently in effect,

|

|

§

|

our suppliers will not become competitors,

|

|

§

|

our suppliers will be able to obtain the components necessary to produce high-quality, technologically-advanced products for us,

|

|

§

|

we will be able to obtain adequate alternatives to our supply sources should they be interrupted,

|

|

§

|

if obtained, alternatively sourced products of satisfactory quality would be delivered on a timely basis, competitively priced, comparably featured or acceptable to our customers, and

|

|

§

|

our suppliers have sufficient financial resources to fulfill its obligations.

|

Our inability to supply sufficient quality and quantities of products that are in demand could reduce our profitability and have a material adverse effect on our relationships with our customers. If our supplier relationship was terminated or interrupted, we could experience an immediate or long-term supply shortage, which could have a material adverse effect on our business.

11

Because we do not develop the technology for our products, the impact of technological advancements may cause price erosion and adversely impact our profitability and inventory value

Because we do not make any of our own products and do not conduct our own research, we cannot assure you that we will be able to source technologically advanced products in order to remain competitive. Furthermore, the introduction or expected introduction of new products or technologies may depress sales of existing products and technologies. This may result in declining prices and inventory obsolescence. Since we maintain a substantial investment in product inventory, declining prices and inventory obsolescence could have a material adverse effect on our business and financial results.

Our estimates of excess and obsolete inventory may prove to be inaccurate; in which case the provision required for excess and obsolete inventory may be understated or overstated. Although we make every effort to ensure the accuracy of our forecasts of future product demand, any significant unanticipated changes in demand or technological developments could have a significant impact on the value of our inventory and operating results.

There can be no guarantee that we will be able to enter into additional complementary industries or to continue configure our products to match new products or devices.

Although we anticipate entering into additional complementary industries to provide support to our invisibleSHIELD line of products, there can be no guarantee that we will be successful in connecting with such industries. Numerous factors, including market acceptance, contract partners that are acceptable to ZAGG, and general market and economic conditions, could prevent us from participating in these complementary industries or markets, which could limit our ability to implement our business strategy.

Similarly, although we intend to continue to configure the invisibleSHIELD for new products and devices, there can be no guarantee that we will be able to either match the demand for our products as new devices and products are introduced, or that purchasers of such devices and products will want to purchase our products for use in connection with them. Any limitation in our ability to match demand or gain market acceptance of our products in connection with new devices and products could have a material adverse effect on our business.

If we fail to maintain proper inventory levels, our business could be harmed.

We produce our products prior to the time we receive customers’ orders. We do this to minimize purchasing costs, the time necessary to fill customer orders and the risk of non-delivery. However, we may be unable to sell the products we have produced in advance. Inventory levels in excess of customer demand may result in inventory write-downs, and the sale of excess inventory at discounted prices could significantly impair our brand image and have a material adverse effect on our operating results and financial condition. Conversely, if we underestimate demand for our products or if we fail to produce the quality products that we require at the time we need them, we may experience inventory shortages. Inventory shortages might delay shipments to customers, negatively impact distributor relationships, and diminish brand loyalty.

The products that we protect with the invisibleSHIELD typically have short life cycles. We may be left with obsolete inventory if we do not accurately project the life cycle of different hand held electronic devices. The charges associated with reserving for slow-moving or obsolete inventory as a result of not accurately estimating the useful life of hand held electronics could negatively impact the value of our inventory and operating results.

Because we are dependent for our success on key executive officers, our inability to retain these officers would impede our business plan and growth strategies, which would have a negative impact on our business and the value of your investment.

Our success depends on the skills, experience and performance of key members of our management team including Robert G. Pedersen II, our CEO, and Brandon T. O’Brien, our CFO. We do not have an employment agreement with Mr. Pedersen or Mr. O’Brien. We do not have employment agreements with any other members of our senior management team. Each of those individuals without long-term employment agreements may voluntarily terminate his employment with the Company at any time upon short notice. Were we to lose one or more of these key executive officers, we would be forced to expend significant time and money in the pursuit of a replacement, which would result in both a delay in the implementation of our business plan and the diversion of working capital. We can give you no assurance that we can find satisfactory replacements for these key executive officers at all, or on terms that are not unduly expensive or burdensome to our company. Although we intend to issue stock options or other equity-based compensation to attract and retain employees, such incentives may not be sufficient to attract and retain key personnel.

12

One of our retailers accounts for a significant amount of our net sales, and the loss of, or reduced purchases from, this or other retailers could have a material adverse effect on our operating results.

Best Buy accounted for 41% of our net sales in 2010. We do not have long-term contracts with any of our retailers, including Best Buy, and all of our retailers generally purchase from us on a purchase order basis. As a result, these retailers generally may, with little or no notice or penalty, cease ordering and selling our products, or materially reduce their orders. If certain retailers, including Best Buy, choose to no longer sell our products, to slow their rate of purchase of our products or to decrease the number of products they purchase, our results of operations would be adversely affected.

We may be adversely affected by the financial condition of our retailers and distributors.

Some of our retailers and distributors have experienced financial difficulties in the past. A retailer or distributor experiencing such difficulties will generally not purchase and sell as many of our products as it would under normal circumstances and may cancel orders. In addition, a retailer or distributor experiencing financial difficulties generally increases our exposure to uncollectible receivables. We extend credit to our retailers and distributors based on our assessment of their financial condition, generally without requiring collateral. While such credit losses have historically been within our estimated reserves for allowances for bad debts, we cannot assure you that this will continue to be the case. Financial difficulties on the part of our retailers or distributors could have a material adverse effect on our results of operations and financial condition. As of December 31, 2010, Best Buy accounted for 64% of accounts receivable and Target represented 17% of our outstanding accounts receivable.

If we fail to attract, train and retain sufficient numbers of our qualified personnel, our prospects, business, financial condition and results of operations will be materially and adversely affected.

Our success depends to a significant degree upon our ability to attract, retain and motivate skilled and qualified personnel. Failure to attract and retain necessary technical personnel, sales and marketing personnel and skilled management could adversely affect our business. If we fail to attract, train and retain sufficient numbers of these highly qualified people, our prospects, business, financial condition and results of operations will be materially and adversely affected.

If our products contain defects, our reputation could be harmed and our results of operations adversely affected.

Some of our products may contain undetected defects due to imperfections in the underlying base materials used for our invisibleSHIELD product line, or manufacturing defects related to our audio, charging and other products. The occurrence of defects or malfunctions could result in financial losses for our customers and in turn increased warranty claims from our customers and diversion of our resources. Any of these occurrences could also result in the loss of or delay in market acceptance of our products and loss of sales.

Because we experience seasonal and quarterly fluctuations in demand for our products, no one quarter is indicative of our results of operations for the entire fiscal year.

Our quarterly results may fluctuate quarter to quarter as a result of market acceptance of our products, the mix, pricing and presentation of the products offered and sold, the hiring and training of additional personnel, the timing of inventory write downs, the cost of materials, the incurrence of other operating costs and factors beyond our control, such as general economic conditions and actions of competitors. We are also affected by seasonal buying cycles of consumers, such as the holiday season, and the introduction of popular consumer electronics, such as a new introduction of products from Apple Corporation. Accordingly, the results of operations in any quarter will not necessarily be indicative of the results that may be achieved for a full fiscal year or any future quarter.

Because we have limited protection on the intellectual property underlying our products, we may not be able to protect our products from the infringement of others and may be prevented from marketing our products.

We do not own proprietary rights with respect to the film we use in our products. We have a patent pending with respect to the covering of electronic devices with clear protective films. In addition, we own and keep confidential the design configurations of the film and the product cut designs which are our copyrights. We seek to protect our intellectual property rights through confidentiality agreements with our employees, consultants and partners. However, no assurance can be given that such measures will be sufficient to protect our intellectual property rights or that the intellectual property rights that we have are sufficient to protect other persons from creating and marketing substantially similar products. If we cannot protect our rights, we may lose our competitive advantage. Moreover, if it is determined that our products infringe on the intellectual property rights of third parties, we may be prevented from marketing our products.

Any claims relating to the infringement of third-party proprietary rights, even if not meritorious, could result in costly litigation, divert management’s attention and resources, or require us to either enter into royalty or license agreements which are not advantageous to us or pay material amounts of damages. In addition, parties making these claims may be able to obtain an injunction, which could prevent us from selling our products.

13

The current economy is affecting consumer spending patterns, which could adversely affect our business.

Consumer spending patterns, especially discretionary spending for products such as mobile, consumer and accessory electronics, are affected by, among other things, prevailing economic conditions, energy costs, raw material costs, wage rates, inflation, interest rates, consumer debt consumer confidence and consumer perception of economic conditions. A general slowdown in the U.S. and certain international economies or an uncertain economic outlook could have a material adverse effect on our sales and operating results.

The recent disruptions in the national and international economies and financial markets and the related increases in unemployment are depressing consumer confidence and spending. If such conditions persist, consumer spending will likely decline further and this would have an adverse effect on our business and our results of operations.

If we are unable to effectively manage our growth, our operating results and financial condition will be adversely affected.

We intend to grow our business by expanding our sales, administrative and marketing organizations. Any growth in or expansion of our business is likely to continue to place a strain on our management and administrative resources, infrastructure and systems. As with other growing businesses, we expect that we will need to refine and expand our business development capabilities, our systems and processes and our access to financing sources. We also will need to hire, train, supervise and manage new employees. These processes are time consuming and expensive, will increase management responsibilities and will divert management attention. We cannot assure you that we will be able to:

|

§

|

expand our systems effectively or efficiently or in a timely manner;

|

|

§

|

allocate our human resources optimally;

|

|

§

|

meet our capital needs;

|

|

§

|

identify and hire qualified employees or retain valued employees; or

|

|

§

|

incorporate effectively the components of any business or product line that we may acquire in our effort to achieve growth.

|

Our inability or failure to manage our growth and expansion effectively could harm our business and materially and adversely affect our operating results and financial condition.

For example, we have a variable interest in HzO, Inc. (“HzO”) for which we are the primary beneficiary and therefore consolidate the operations of HzO. We anticipate having sales associated with the HzO technology beginning in 2011, but there can be no guarantee that such sales will occur in 2011 or ever. Factors such as delays in development of the technology, increased research and development costs, and market acceptance of the technology could cause a delay in sales associated with the HzO technology, which could have a material adverse effect on our business and implementation of our business plan.

If our competitors misappropriate our proprietary know-how and trade secrets, it could have a material adverse affect on our business.

We depend heavily on the expertise of our production team. If any of our competitors copies or otherwise gains access to similar products independently, we might not be able to compete as effectively. The measures we take to protect our designs may not be adequate to prevent their unauthorized use. Further, the laws of foreign countries may provide inadequate protection of such intellectual property rights. We may need to bring legal claims to enforce or protect such intellectual property rights. Any litigation, whether successful or unsuccessful, could result in substantial costs and diversions of resources. In addition, notwithstanding the rights we have secured in our intellectual property, other persons may bring claims against us that we have infringed on their intellectual property rights or claims that our intellectual property right interests are not valid. Any claims against us, with or without merit, could be time consuming and costly to defend or litigate and therefore could have an adverse affect on our business.

If any of our facilities were to experience catastrophic loss, our operations would be seriously harmed.

Our facilities could be subject to a catastrophic loss from fire, flood, earthquake or terrorist activity. All of our activities, including sales and marketing, customer service, finance and other critical business operations are in one location. Our manufacturing activities are conducted at other facilities separate from our corporate headquarters. Any catastrophic loss at these facilities could disrupt our operations, delay production, and revenue and result in large expenses to repair or replace the facility. While we have obtained insurance to cover most potential losses, we cannot assure you that our existing insurance coverage will be adequate against all other possible losses.

If our internal control over financial reporting is not considered effective, our business and stock price could be adversely affected.

Section 404 of the Sarbanes-Oxley Act of 2002 requires us to evaluate the effectiveness of our internal controls over financial reporting as of the end of each fiscal year, and to include a management report assessing the effectiveness of internal control over financial reporting in our annual report on Form 10-K for that fiscal year. A material weakness in our internal controls over financial reporting would require management to assess our internal control over financial reporting as ineffective. If our internal controls over financial reporting are not considered effective, we may experience a loss of public confidence, which could have an adverse effect on our business and on the market price of our common stock.

14

Because we distribute products internationally, economic, political and other risks associated with our international sales and operations could adversely affect our operating results.

Since we sell our products worldwide, our business is subject to risks associated with doing business internationally. Our sales to customers outside the United States accounted for approximately 17% of our revenue from continuing operations in fiscal 2010. Accordingly, our future results could be harmed by a variety of factors, including:

|

§

|

changes in foreign currency exchange rates;

|

|

§

|

exchange controls;

|

|

§

|

changes in regulatory requirements;

|

|

§

|

changes in a specific country's or region's political or economic conditions;

|

|

§

|

tariffs, other trade protection measures and import or export licensing requirements;

|

|

§

|

potentially negative consequences from changes in tax laws or application of such tax laws;

|

|

§

|

difficulty in staffing and managing widespread operations;

|

|

§

|

changing labor regulations;

|

|

§

|

requirements relating to withholding taxes on remittances and other payments by subsidiaries;

|

|

§

|

different regimes controlling the protection of our intellectual property;

|

|

§

|

restrictions on our ability to own or operate subsidiaries, make investments or acquire new businesses in these jurisdictions; and

|

|

§

|

restrictions on our ability to repatriate dividends from our subsidiaries.

|

Our international operations are affected by global economic and political conditions. Changes in economic or political conditions in any of the countries in which we operate could result in exchange rate movement, new currency or exchange controls or other restrictions being imposed on our operations.

There can be no guarantee that additional amounts spent on marketing or advertising will result in additional sales or revenue to the Company.

In 2011, management intends to expand our advertising and to continue its marketing efforts relating to existing products and potential new product introductions. However, there can be no guarantee that such increased advertising or marketing efforts and strategies will result in increased sales to us.

Risks Related to the Company’s Securities

Because the price of our common stock has been, and may continue to be, volatile, our shareholders may not be able to resell shares of our common stock at or above the price paid for such shares.

The price for shares of our common stock has exhibited high levels of volatility with significant volume and price fluctuations, which makes our common stock unsuitable for many investors. For example, for the two years ended December 31, 2010, the closing price of our common stock ranged from a high of $8.72 to a low of $0.90 per share. At times, the fluctuations in the price of our common stock may have been unrelated to our operating performance. These broad fluctuations may negatively impact the market price of shares of our common stock. The price of our common stock may also have been influenced by:

|

§

|

fluctuations in our results of operations or the operations of our competitors or customers;

|

|

§

|

the aggregate amount of our outstanding debt and perceptions about our ability to make debt service payments;

|

|

§

|

failure of our results of operations and sales revenues to meet the expectations of stock market analysts and investors;

|

|

§

|

reductions in demand or expectations regarding future demand by our customers;

|

|

§

|

changes in stock market analyst recommendations regarding us, our competitors or our customers;

|

|

§

|

the timing and announcements of technological innovations, new products or financial results by us or our competitors;

|

|

§

|

increases in the number of shares of our common stock outstanding; and

|

|

§

|

changes in our industry.

|

Based on the above, we expect that our stock price will continue to be extremely volatile. Therefore, we cannot guarantee that our investors will be able to resell our common stock at or above the price at which they purchased it.

15

Because we may, at some time in the future, issue additional securities, shareholders are subject to dilution of their ownership.

Although we have no immediate plans to raise additional capital, we may at some time in the future do so. Any such issuance would likely dilute shareholders’ ownership interest in our company and may have an adverse impact on the price of our common stock. In addition, from time to time we may issue shares of common stock in connection with equity financing activities or as incentives to our officers and business partners. We may expand the number of shares available under stock incentive and option plans, or create new plans. All issuances of common stock would be dilutive to your holdings in our company. If your holdings are diluted, the overall value of your shares may be diminished and your ability to influence shareholder voting will also be harmed.

If our common stock fails to meet the listing requirements of NASDAQ and is delisted from trading on the NASDAQ, the market price of our common stock could be adversely affected.

Our common stock is currently listed on the NASDAQ Global Select Market under the symbol “ZAGG.” The NASDAQ’s listing requirements include a requirement that, for continued listing, an issuer’s common shares trade at a minimum bid price of $1.00 per share. This requirement is deemed breached when the bid price of an issuer’s common shares closes below $1.00 per share for 30 consecutive trading days. Our stock is not currently trading at below $1.00, and closed at $7.62 at December 31, 2010. If we were to trade below $1.00 for 30 consecutive days, we could transfer our stock listing to the NASDAQ Capital Market following receipt of a notice of delisting and receive an additional six month grace period to regain compliance, take certain other actions to increase our stock price prior to being delisted from NASDAQ, or otherwise challenge any action by NASDAQ to delist our common stock. There can be no assurance that any of these actions would be successful in maintaining our listing on NASDAQ or the trading market for our stock. A delisting of our common stock from the NASDAQ or a transfer to the Capital Market tier of NASDAQ could adversely affect the liquidity of the trading market for our stock and therefore the market price of our common stock.

Limitations on director and officer liability and indemnification of our officers and directors by us may discourage stockholders from bringing suit against a director.

Our articles of incorporation and bylaws provide, with certain exceptions as permitted by governing state law, that a director or officer shall not be personally liable to us or our stockholders for breach of fiduciary duty as a director, except for acts or omissions which involve intentional misconduct, fraud or knowing violation of law, or unlawful payments of dividends. These provisions may discourage stockholders from bringing suit against a director for breach of fiduciary duty and may reduce the likelihood of derivative litigation brought by stockholders on our behalf against a director. In addition, our articles of incorporation and bylaws may provide for mandatory indemnification of directors and officers to the fullest extent permitted by governing state law.

Because we do not expect to pay dividends for the foreseeable future, investors seeking cash dividends should not purchase our common stock.