As filed with the Securities and Exchange Commission on June 29, 2020

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________

FORM 20-F

_______________

¨ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2019

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

¨ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

![]()

GOL Linhas Aéreas Inteligentes S.A.

(Exact name of registrant as specified in its charter)

GOL Intelligent Airlines Inc.

(Translation of registrant’s name into English)

_________________

The Federative Republic of Brazil

(Jurisdiction of incorporation or organization)

Richard F. Lark, Jr.

+55 11 5098-7881

Fax: +55 11 5098-2341

E-mail: ri@voegol.com.br

Praça Comandante Linneu Gomes, S/N, Portaria 3

Jardim Aeroporto

04626-020 São Paulo, São Paulo

Federative Republic of Brazil

+55 11 2128-4700

(Address of principal executive offices)

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

___________________________________________

Securities registered or to be registered pursuant to Section 12(b) of the Act.

|

Title of each class: |

Trading symbol: |

Name of each exchange on which registered: |

|

Preferred Shares, without par value |

* GOL |

New York Stock Exchange |

* Not for trading purposes, but only in connection with the trading on the New York Stock Exchange of American Depositary Shares representing those preferred shares.

40549.00011

___________________________________________

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

___________________________________________

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

___________________________________________

The number of outstanding shares of each class of stock of GOL Linhas Aéreas Inteligentes S.A. as of December 31, 2019:

2,863,682,710 Common Shares

273,868,123 Preferred Shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer x |

Accelerated filer ¨ |

Non-accelerated filer ¨ |

Emerging growth company ¨

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ¨

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP ¨ |

International Financial Reporting Standards as issued by the International Accounting Standards Board x |

Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

40549.00011

i

ii

RELIANCE ON SEC ORDER TO EXTEND FILING DEADLINE

As disclosed in our report on Form 6-K furnished to the U.S. Securities and Exchange Commission, or the SEC, on April 30, 2020, we have relied on the SEC’s order dated March 25, 2020 (Release No. 34-88465) regarding an extension to file certain reports due to circumstances relating to the COVID-19 pandemic.

The airline industry has been among the sectors of the global economy most affected by the COVID-19 pandemic and government measures to address it, which, together with the severe impact on demand for air travel, have resulted in unprecedented challenges for us. Our management has since the second half of March 2020 been focused primarily on addressing the unprecedented challenges that the COVID-19 pandemic has created for our business and employees. Consequently, this situation resulted in a delay in our completion of this annual report on Form 20-F.

Presentation of Financial and Other Data

The consolidated financial statements included in this annual report have been prepared in accordance with International Financial Reporting Standards, or IFRS, issued by the International Accounting Standards Board, or IASB, in reais.

We have translated some of the real amounts contained in this annual report into U.S. dollars. The rate used to translate such amounts in respect of the year ended December 31, 2019 was R$4.031 to US$1.00, which was the U.S. dollar selling rate as of December 31, 2019, as reported by the Brazilian Central Bank (Banco Central do Brasil), or the Central Bank. As of June 26, 2020, the U.S dollar selling rate was R$5.463 to US$1.00, as reported by the Central Bank, which represents a 35.5% depreciation of the real in 2020 to date. The U.S. dollar equivalent information presented in this annual report is provided solely for the convenience of investors and should not be construed as implying that the real amounts represent, or could have been or could be converted into, U.S. dollars at the above rate.

The consolidated financial statements included in this annual report have been prepared on a going concern basis of accounting, which contemplates continuity of operations, realization of assets and satisfaction of liabilities and commitments in the normal course of business. As such, the consolidated financial statements included in this annual report do not include any adjustments that might result from an inability to continue as a going concern. If we cannot continue as a going concern, adjustments to the carrying values and classification of our assets and liabilities and the reported amounts of income and expenses could be required and could be material. For more information, see “Item 5. Operating and Financial Review and Prospects—D. Trend Information.”

In this annual report, we use the terms “the registrant” and “GLAI” to refer to GOL Linhas Aéreas Inteligentes S.A., and “GOL,” “Company,” “we,” “us” and “our” to refer to the registrant and its consolidated subsidiaries together, except where the context requires otherwise. The term “GLA” refers to GOL Linhas Aéreas S.A., a wholly owned subsidiary of the registrant (previously named VRG Linhas Aéreas S.A., or VRG). References to “preferred shares” and “ADSs” refer to non-voting preferred shares of the registrant and American depositary shares representing those preferred shares, respectively, except where the context requires otherwise.

The phrase “Brazilian government” refers to the federal government of the Federative Republic of Brazil. The term “Brazil” refers to the Federative Republic of Brazil. The terms “U.S. dollar” and “U.S. dollars” and the symbol “US$” refer to the legal currency of the United States. The terms “real” and “reais” and the symbol “R$” refer to the legal currency of Brazil. We make statements in this annual report about our competitive position and market share in, and the market size of, the Brazilian and international airline industries. We have made these statements on the basis of statistics and other information from third party sources, governmental agencies or industry or general publications that we believe are reliable. Although we have no reason to believe any of this information or these reports are inaccurate in any material respect, we have not independently verified the competitive position, market share and market size or market growth data provided by third parties or by industry or general publications. All industry and market data contained in this annual report are from the latest publicly available information.

Certain figures included in this annual report have been rounded. Accordingly, figures shown as totals in certain tables may not be an arithmetic sum of the figures that precede them.

This annual report is incorporated by reference into our registration statement on Form F-3, filed with the SEC on July 25, 2019.

1

This annual report contains terms relating to operating performance in the airline industry that are defined as follows:

“Aircraft utilization” represents the average number of block-hours operated per day per aircraft for the total aircraft fleet.

“ATK” refers to available ton kilometers and is a measure of total capacity, considering passenger and cargo.

“Available seat kilometers” or “ASK” represents the aircraft seating capacity multiplied by the number of kilometers flown.

“Average stage length” represents the average number of kilometers flown per flight.

“Block-hours” refers to the elapsed time between an aircraft’s leaving an airport gate and arriving at an airport gate.

“Load factor” represents the percentage of aircraft seating capacity that is actually utilized (calculated by dividing revenue passenger kilometers by available seat kilometers).

“Low-cost carrier” refers to airlines with a business model focused on a single fleet type, low-cost distribution channels and a highly efficient flight network.

“MRO” refers to maintenance, repair and operations.

“Net revenue per available seat kilometer” or “RASK” represents net revenue divided by available seat kilometers.

“Operating costs and expenses per available seat kilometer” or “CASK” represents operating costs and expenses divided by available seat kilometers, which is the generally accepted industry metric to measure operational cost efficiency.

“Operating costs and expenses excluding fuel expense per available seat kilometer” or “CASK ex-fuel” represents operating costs and expenses less fuel expense, divided by available seat kilometers.

“Passenger revenue per available seat kilometer” or “PRASK” represents passenger revenue divided by available seat kilometers.

“Revenue passenger kilometers” or “RPK” represents the number of kilometers flown by revenue passengers.

“Revenue passengers” represents the total number of paying passengers flown on all flight segments.

“Yield per passenger kilometer” or “yield” represents the average amount one passenger pays to fly one kilometer.

Cautionary Statements about Forward-Looking Statements

This annual report includes forward-looking statements, principally under the captions “Risk Factors,” “Operating and Financial Review and Prospects” and “Business Overview.” We have based these forward-looking statements largely on our current beliefs, expectations and projections about future events and financial trends affecting us. Many important factors, in addition to those discussed elsewhere in this annual report, could cause our actual results to differ substantially from those anticipated in our forward-looking statements, including, among others:

· general economic, political and business conditions in Brazil, South America and the Caribbean;

· the effects of global financial markets and economic crises;

· developments relating to the spread of COVID-19, a new strain of coronavirus, and government measures to address it;

· management’s expectations and estimates concerning our financial performance and financing plans and programs;

· our level of fixed obligations;

· our capital expenditure plans;

2

· our ability to obtain financing on acceptable terms;

· our ability to service our indebtedness;

· inflation and fluctuations in the exchange rate of the real;

· changes to existing and future governmental regulations, including air traffic capacity controls;

· fluctuations in crude oil prices and its effect on fuel costs;

· increases in fuel costs, maintenance costs and insurance premiums;

· changes in market prices, customer demand and preferences, and competitive conditions;

· cyclical and seasonal fluctuations in our operating results;

· defects or mechanical problems with our aircraft;

· our ability to successfully implement our strategy;

· developments in the Brazilian civil aviation infrastructure, including air traffic control, airspace and airport infrastructure; and

· future terrorism incidents, cyber-security threats, disease outbreaks or related occurrences affecting the airline industry.

The words “believe,” “may,” “will,” “aim,” “estimate,” “continue,” “anticipate,” “intend,” “expect” and similar words are intended to identify forward-looking statements. Forward-looking statements include information concerning our possible or assumed results of operations, business strategies, financing plans, competitive position, industry environment, potential growth opportunities and the effects of regulation and of competition. Forward‑looking statements are valid only as of the date they were made, and we undertake no obligation to update publicly or to revise any forward-looking statements after we distribute this annual report because of new information, events or other factors. In light of the risks and uncertainties described above, the forward-looking events and circumstances discussed in this annual report might not occur and are not guarantees of future performance.

PART I

ITEM 1. Identity of Directors, Senior Management and Advisers

Not applicable.

ITEM 2. Offer Statistics and Expected Timetable

Not applicable.

We present in this section the following summary consolidated financial data:

· Summary financial information derived from our audited consolidated financial statements as of December 31, 2019 and 2018 and for the years ended December 31, 2019, 2018 and 2017, included elsewhere in this annual report; and

· Summary financial information derived from our audited consolidated financial statements as of and for the year ended December 31, 2017, not included in this annual report.

We adopted IFRS 16 – Leases, or IFRS 16, on January 1, 2019 using the modified retrospective method and we did not restate our financial information for the years ended December 31, 2017 and 2018 for comparative purposes. Consequently, information regarding our indebtedness as of December 31, 2019 is not comparable to information regarding our indebtedness as of December 31, 2017 and 2018. Since our adoption of IFRS 16, our indebtedness includes our total short and long-term loans and financings and leases. For more information, see “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Recent Accounting Pronouncements” and note 19 to our audited consolidated financial statements included elsewhere in this annual report.

3

The following tables set forth summary consolidated financial and operating data as of and for each of the periods indicated:

Summary Financial Data

|

|

Year ended December 31, | |||

|

|

2017 |

2018 |

2019 |

2019(1) |

|

Statements of Operations Data: |

(in thousands of R$, except per share/ADS information) |

(in thousands of US$) | ||

|

Net revenue: |

|

|

|

|

|

Passenger |

9,564,041 |

10,633,488 |

13,077,743 |

3,244,292 |

|

Mileage program, cargo and other |

764,993 |

777,866 |

786,961 |

195,227 |

|

Total net revenue |

10,329,034 |

11,411,354 |

13,864,704 |

3,439,519 |

|

Operating costs and expenses: |

|

|

|

|

|

Salaries, wages and benefits |

(1,708,111) |

(1,903,852) |

(2,361,268) |

(585,777) |

|

Aircraft fuel |

(2,887,737) |

(3,867,673) |

(4,047,344) |

(1,004,055) |

|

Aircraft rent(2) |

(939,744) |

(1,112,837) |

- |

- |

|

Landing fees |

(664,170) |

(743,362) |

(759,774) |

(188,483) |

|

Aircraft, traffic and mileage servicing |

(628,140) |

(613,768) |

(707,392) |

(175,488) |

|

Passenger service expenses |

(437,045) |

(474,117) |

(578,744) |

(143,573) |

|

Sales and marketing |

(590,814) |

(581,977) |

(670,392) |

(166,309) |

|

Maintenance, materials and repairs |

(368,719) |

(570,333) |

(569,229) |

(141,213) |

|

Depreciation and amortization(2) |

(505,425) |

(668,516) |

(1,727,982) |

(428,673) |

|

Other income (expenses), net |

(610,310) |

524,656 |

(309,917) |

(76,883) |

|

Total operating costs and expenses |

(9,340,215) |

(10,011,779) |

(11,732,042) |

(2,910,454) |

|

Equity pick up method |

544 |

387 |

77 |

19 |

|

Income before financial results, exchange rate variation, net and income taxes |

989,363 |

1,399,962 |

2,132,739 |

529,084 |

|

Financial income |

213,446 |

259,728 |

389,563 |

96,642 |

|

Financial expense |

(1,050,461) |

(1,061,089) |

(1,748,265) |

(433,705) |

|

Income before exchange rate variation, net and income taxes |

152,348 |

598,601 |

774,037 |

192,021 |

|

Exchange rate variation, net |

(81,744) |

(1,081,197) |

(385,092) |

(95,533) |

|

Income (loss) before income taxes |

70,604 |

(482,596) |

388,945 |

96,488 |

|

Income taxes |

307,213 |

(297,128) |

(209,607) |

(51,999) |

|

Net income (loss) for the year |

377,817 |

(779,724) |

179,338 |

44,489 |

|

Attributable to non-controlling interests |

359,025 |

305,669 |

296,611 |

73,582 |

|

Attributable to equity holders of GLAI. |

18,792 |

(1,085,393) |

(117,273) |

(29,093) |

|

|

Year ended December 31, | |||

|

|

2017 |

2018 |

2019 |

2019(1) |

|

Earnings per Share and Other Information: |

(in R$ except number of shares) |

(in US$ except number of shares) | ||

|

Basic income (loss) per preferred share |

0.05 |

(3.12) |

(0.33) |

(0.08) |

|

Basic income (loss) per common share |

0.00 |

(0.09) |

(0.01) |

(0.00) |

|

Basic income (loss) per share(3) |

0.06 |

(3.11) |

(0.33) |

(0.08) |

|

Basic income (loss) per ADS |

0.11 |

(1.56) |

(0.66) |

(0.17) |

|

Diluted income (loss) per preferred share |

0.05 |

(3.12) |

(0.33) |

(0.08) |

|

Diluted income (loss) per common share |

0.00 |

(0.09) |

(0.01) |

(0.00) |

|

Diluted income (loss) per share(3) |

0.05 |

(3.12) |

(0.33) |

(0.08) |

|

Diluted income (loss) per ADS |

0.11 |

(1.56) |

(0.66) |

(0.17) |

|

Weighted average number of outstanding shares in relation to basic income (loss) per preferred share (in thousands) |

204,664 |

266,676 |

270,053 |

270,053 |

|

Weighted average number of outstanding shares in relation to basic income (loss) per common share (in thousands) |

4,981,350 |

2,863,683 |

2,863,683 |

2,863,683 |

|

Weighted average number of outstanding shares in relation to basic income (loss) per share (in thousands)(3) |

346,988 |

348,496 |

351,873 |

351,873 |

|

Weighted average number of outstanding ADSs in relation to basic income (loss) per share (in thousands)(3) |

173,494 |

174,248 |

175,936 |

175,936 |

|

Weighted average number of outstanding shares in relation to diluted income (loss) per preferred share (in thousands) |

207,278 |

266,676 |

270,053 |

270,053 |

|

Weighted average number of outstanding shares in relation to diluted income (loss) per common share (in thousands) |

4,981,350 |

2,863,683 |

2,863,683 |

2,863,683 |

|

Weighted average number of outstanding shares in relation to diluted income (loss) per share (in thousands)(3) |

349,602 |

348,496 |

351,873 |

351,873 |

|

Weighted average number of outstanding ADSs in relation to diluted income (loss) per share (in thousands)(2) |

174,801 |

174,248 |

175,936 |

175,936 |

|

Dividends declared per preferred share (net of withheld income taxes) |

- |

- |

- |

- |

4

|

|

Year ended December 31, | |||

|

|

2017 |

2018 |

2019 |

2019(1) |

|

Other Financial Data: |

(in thousands of R$ except percentages) |

(in thousands of US$) | ||

|

EBITDA(4) |

1,494,788 |

2,068,478 |

3,860,721 |

957,758 |

|

EBITDA margin(5) |

14.5% |

18.1% |

27.8% |

27.8% |

|

Operating margin(6) |

9.6% |

12.3% |

15.4% |

15.4% |

|

Total liquidity(7) |

3,186,976 |

2,980,011 |

4,273,023 |

1,060,040 |

|

Net cash flows from (used in) operating activities |

672,753 |

2,081,869 |

2,461,076 |

610,537 |

|

Net cash flows from (used in) investing activities |

(559,805) |

(1,587,256) |

(754,611) |

(187,202) |

|

Net cash flows from (used in) financing activities |

359,673 |

(753,189) |

(892,173) |

(221,328) |

Summary Operating Data

|

|

Year ended December 31 | ||

|

|

2017 |

2018 |

2019 |

|

|

|

|

|

|

Operating aircraft at year end |

119 |

121 |

130 |

|

Total aircraft at year end |

119 |

121 |

137 |

|

Revenue passengers carried (in thousands)(8) |

32,507 |

33,446 |

36,445 |

|

Revenue passenger kilometers (RPK) (in millions)(8) |

37,408 |

38,423 |

41,863 |

|

Available seat kilometers (ASKs) (in millions)(8) |

46,695 |

48,058 |

51,065 |

|

Load-factor |

80.1% |

80.0% |

82.0% |

|

Break-even load factor |

72.4% |

70.1% |

66.3% |

|

Aircraft utilization (block hours per day) |

12.1 |

11.8 |

12.3 |

|

Average fare (R$) |

294 |

318 |

359 |

|

Passenger revenue yield per RPK (R$ cents) |

25.6 |

27.6 |

31.2 |

|

PRASK (R$ cents) |

20.5 |

22.1 |

25.6 |

|

RASK (R$ cents) |

22.1 |

23.7 |

27.2 |

|

CASK (R$ cents) |

20.0 |

20.8 |

22.0 |

|

CASK ex-fuel (R$ cents) |

13.8 |

12.8 |

14.1 |

|

Departures |

250,654 |

250,040 |

259,377 |

|

Departures per day |

687 |

685 |

711 |

|

Destinations served |

64 |

69 |

77 |

|

Average stage length (kilometers) |

1,094 |

1,098 |

1,114 |

|

Active full-time equivalent employees at year end |

14,532 |

15,259 |

16,113 |

|

Fuel liters consumed (in millions) |

1,379 |

1,403 |

1,475 |

|

Average fuel expense per liter (R$) |

2.15 |

2.91 |

2.79 |

_____________

(1) Translated for convenience using the U.S. dollar selling rate as reported by the Central Bank of R$4.031 to US$1.00 as of December 31, 2019. As of June 26, 2020, the U.S. dollar selling rate as reported by the Central Bank was R$5.463 to US$1.00.

(2) We adopted IFRS 16 on January 1, 2019 using the modified retrospective method and we did not restate our financial information for the years ended December 31, 2017 and 2018 for comparative purposes. For more information, see “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Recent Accounting Pronouncements” and note 19 to our audited consolidated financial statements included elsewhere in this annual report.

(3) Common shares divided by 35 to calculate weighted average number of shares, to reflect the ratio of 35 common shares for each preferred share. This is not a measure of financial performance recognized under IFRS, nor should it be considered an alternative to numbers calculated per preferred share and per common share. We believe that calculations per share provide useful information as they equalize the common share economic rights and number of shares to those of our preferred shares.

(4) We calculate EBITDA as net income (loss) plus financial results, net, exchange rate variation, net, income taxes and depreciation and amortization. EBITDA is not a measure of financial performance recognized under IFRS, nor should it be considered an alternative to net income (loss) as a measure of operating performance, or as an alternative to operating cash flows, or as a measure of liquidity. EBITDA is not calculated using a standard methodology and may not be comparable to the definition of EBITDA or similarly titled measures used by other companies. Because our calculation of EBITDA eliminates financial results, net, exchange rate variation, net, income taxes and depreciation and amortization, we believe that our EBITDA provides an indication of our general economic performance, without giving effect to interest rate or exchange rate fluctuations, changes in income and social contribution tax rates or depreciation and amortization.

5

(5) We calculate EBITDA margin as EBITDA divided by total net revenue for the relevant period.

(6) We calculate operating margin as income before financial results, exchange rate variation, net and income taxes divided by total net revenue.

(7) We calculate total liquidity as the sum of cash and cash equivalents, restricted cash, short-term investments and trade receivables.

(8) Source: National Civil Aviation Agency (Agência Nacional de Aviação Civil), or ANAC.

Reconciliation and Calculation of Certain Non-GAAP Measures

Reconciliation of Net Income (Loss) for the Year to EBITDA

|

|

Year ended December 31, | |||

|

|

2017 |

2018 |

2019 |

2019(1) |

|

|

(in thousands of R$ except as otherwise indicated) |

(in thousands of US$) | ||

|

Net income (loss) |

377,817 |

(779,724) |

179,338 |

44,501 |

|

(+) Income taxes |

(307,213) |

297,128 |

209,607 |

52,012 |

|

(+) Financial results, net |

837,015 |

801,361 |

1,358,702 |

337,147 |

|

(+) Exchange rate variation, net |

81,744 |

1,081,197 |

385,092 |

95,555 |

|

(+) Depreciation and amortization |

505,425 |

668,516 |

1,727,982 |

428,780 |

|

EBITDA(2) |

1,494,788 |

2,068,478 |

3,860,721 |

957,995 |

_____________

(1) Translated for convenience using the U.S. dollar selling rate as reported by the Central Bank of R$4.031 to US$1.00 as of December 31, 2019. As of June 26, 2020, the U.S. dollar selling rate as reported by the Central Bank was R$5.463 to US$1.00.

(2) We calculate EBITDA as net income (loss) plus financial results, net, exchange rate variation, net, income taxes and depreciation and amortization. EBITDA is not a measure of financial performance recognized under IFRS, nor should it be considered an alternative to net income (loss) as a measure of operating performance, or as an alternative to operating cash flows, or as a measure of liquidity. EBITDA is not calculated using a standard methodology and may not be comparable to the definition of EBITDA or similarly titled measures used by other companies. Because our calculation of EBITDA eliminates financial results, net, exchange rate variation, net, income taxes and depreciation and amortization, we believe that our EBITDA provides an indication of our general economic performance, without giving effect to interest rate or exchange rate fluctuations, changes in income and social contribution tax rates or depreciation and amortization.

Reconciliation of Operating Cash Flow to EBITDA

|

|

Year ended December 31, | |||

|

|

2017 |

2018 |

2019 |

2019(1) |

|

|

(in thousands of R$, except as otherwise indicated) |

(in thousands of US$, except as otherwise indicated) | ||

|

|

|

|

|

|

|

Net cash provided by operating activities |

672,753 |

2,081,869 |

2,461,076 |

610,537 |

|

Income taxes |

239,846 |

52,139 |

178,621 |

44,312 |

|

Trade receivables, net |

198,370 |

(95,844) |

384,147 |

95,298 |

|

Inventories |

(1,038) |

6,673 |

21,240 |

5,269 |

|

Suppliers |

202,462 |

(16,382) |

232,021 |

57,559 |

|

Suppliers - forfaiting |

(76,157) |

(267,502) |

(188,771) |

(46,830) |

|

Deposits |

(46,388) |

402,495 |

399,345 |

99,068 |

|

Payments for lawsuits and aircraft return |

270,970 |

236,882 |

317,591 |

78,787 |

|

Advances from customers |

(4,895) |

(148,249) |

153,543 |

38,091 |

|

Derivatives |

44,753 |

20,998 |

124,548 |

30,898 |

|

Others |

(5,888) |

(204,601) |

(222,640) |

(55,232) |

|

EBITDA |

1,494,788 |

2,068,478 |

3,860,721 |

957,757 |

_____________

(1) Translated for convenience using the U.S. dollar selling rate as reported by the Central Bank of R$4.031 to US$1.00 as of December 31, 2019. As of June 26, 2020, the U.S. dollar selling rate as reported by the Central Bank was R$5.463 to US$1.00.

6

Calculation of Adjusted Net Indebtedness to EBITDA

|

|

|

|

|

As of and for the year ended December 31, 2019 |

|

|

(in thousands of R$) |

|

Loans and financing current |

(2,543,039) |

|

Loans and financing non-current |

(5,866,802) |

|

Lease liabilities current |

(1,404,712) |

|

Lease liabilities current non-current |

(4,648,068) |

|

Total indebtedness |

(14,462,621) |

|

(-) Perpetual notes |

546,750 |

|

Adjusted net indebtedness |

(13,915,871) |

|

Cash and equivalents |

1,645,425 |

|

Short-term investments |

953,762 |

|

Restricted cash current |

304,920 |

|

Restricted cash non-current |

139,386 |

|

Adjusted net indebtedness |

(10,872,378) |

|

EBITDA |

3,860,721 |

|

Adjusted net indebtedness to EBITDA ratio |

2.8x |

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

Investment in the ADSs involves a high degree of risk. You should carefully consider the risks described below, as well as the other information in this annual report, before making an investment decision regarding the ADSs. Our business, financial condition and results of operations could be materially and adversely affected by any of these risks. The trading price of the ADSs could decline due to any of these risks or other factors, and you may lose all or part of your investment. For purposes of this section, when we state that a risk, uncertainty or event may, could, would or will have an “adverse effect” on us or “adversely affect” us, we mean that the risk, uncertainty or event could have an adverse effect on our business, financial condition, results of operations, cash flow, prospects, reputation and/or the trading price of the ADSs, except as otherwise indicated.

Risks Relating to Brazil

The Brazilian government has exercised, and continues to exercise, significant influence over the Brazilian economy, and such involvement, along with general political and economic conditions, could adversely affect us.

The Brazilian government has frequently intervened in the Brazilian economy and has occasionally made drastic changes in policy and regulations. The Brazilian government’s actions to control inflation and in respect of other policies and regulations have involved, among other measures, increases in interest rates, changes in tax and social security policies, price controls, currency exchange and remittance controls, devaluations, capital controls and limits on imports. We may be adversely affected by changes in policy or regulations at the federal, state or municipal level involving factors such as:

· interest rates;

· currency fluctuations;

· monetary policies;

· inflation;

· liquidity of capital and lending markets;

7

· tax and social security policies;

· labor regulations;

· energy and water shortages and rationing; and

· other political, social and economic developments in or affecting Brazil.

Uncertainty over whether the Brazilian government will implement changes in policy or regulation affecting these or other factors may contribute to economic uncertainty in Brazil and to heightened volatility in the Brazilian securities markets and securities issued abroad by Brazilian companies.

According to the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística), or the IBGE, Brazil’s gross domestic product, or GDP, grew by 1.0% in 2017, 1.1% in 2018 and 1.1% in 2019, following an economic recession in 2015 and 2016.

Developments in the Brazilian economy may affect Brazil’s growth rates and, consequently, the use of our products and services and we have been, and will continue to be, affected by changes in the Brazilian GDP.

Political instability may adversely affect us.

Brazilian markets experienced heightened volatility in the last half decade due to uncertainties deriving from the ongoing Lava Jato investigation, which is being conducted by the Federal Prosecutor’s Office, and its impact on the Brazilian economy and political environment. Numerous members of the Brazilian government and of the legislative branch, as well as senior officers of large state-owned and private companies have been convicted of political corruption of officials accepting bribes by means of kickbacks on contracts granted by the government to several infrastructure, oil and gas and construction companies.

The ultimate outcome of these investigations is uncertain, but they had an adverse impact on the image and reputation of the implicated companies, and on the general market perception of the Brazilian economy. The development of those unethical conduct cases has and may continue to adversely affect us.

In addition, the Brazilian economy is subject to the effects of uncertainty over the performance of the Brazilian federal government under President Jair Bolsonaro, who was sworn-in in January 2019. We cannot predict the effects of further political developments on the Brazilian economy, including the policies that the President may adopt or alter during his mandate or the effect that any such policies might have on our business and on the Brazilian economy.

Risks relating to the global economy may affect the perception of risk in emerging markets, which may adversely affect the Brazilian economy, including by means of oscillations in the capital markets and, consequently, us.

The market value of securities issued by Brazilian companies is influenced, to varying degrees, by the economic and market conditions of other countries, including the United States, European Union member countries and emerging economies. The reaction of investors to events in these countries may adversely affect the market value of the securities of Brazilian companies. Crises in the United States, the European Union or emerging markets may reduce investor interest in the securities of Brazilian companies, including securities issued by us.

In addition, the Brazilian economy is affected by international economic and market conditions, especially in the United States. Stock prices on the B3 S.A. – Brasil, Bolsa, Balcão, or the B3, for example, are highly affected by fluctuations in U.S. interest rates and by the behavior of the major U.S. stock exchanges. Any increase in interest rates in other countries, especially the United States, could reduce overall liquidity and investor interest in Brazilian capital markets.

We cannot assure that Brazilian capital markets will be open to Brazilian companies and that financing costs will be favorable to Brazilian companies. Economic crises in Brazil or other emerging markets may reduce investor interest in securities of Brazilian companies, including securities issued by us. This may affect the liquidity and market price of the ADSs and our access to the Brazilian capital markets and financing on acceptable terms, which may adversely affect us.

8

Government efforts to combat inflation may hinder the growth of the Brazilian economy and materially and adversely affect us.

Historically, Brazil has experienced high inflation rates, which, together with actions taken by the Central Bank to curb inflation, have had significant adverse effects on the Brazilian economy. After the implementation of the Plano Real in 1994, the annual rate of inflation in Brazil decreased significantly, as measured by the National Broad Consumer Price Index (Índice Nacional de Preços ao Consumidor Amplo), or IPCA. According to the IBGE, inflation measured by the IPCA was 3.0%, 3.8% and 4.3% in 2017, 2018 and 2019, respectively.

The base interest rate for the Brazilian banking system is the Central Bank’s Special System for Settlement and Custody (Sistema Especial de Liquidação e Custódia) rate, or SELIC rate. The SELIC rate has been repeatedly lowered from the October 2016 rate of 14.25%. As of December 31, 2017, 2018 and 2019, the SELIC rate was 7.00%, 6.50% and 4.40%, respectively.

Inflation and the Brazilian government’s measures to curb it, principally the Central Bank’s monetary policy, have had and may again have significant effects on the Brazilian economy and us, while tight monetary policies with high interest rates may restrict Brazil’s growth and the availability of credit, more lenient government and Central Bank policies and interest rate decreases may trigger increases in inflation, and, consequently, growth volatility and the need for sudden and significant interest rate increases, which could adversely affect us. In addition, we may not be able to adjust the fares we charge our customers to offset the effects of inflation on our cost structure.

Downgrades in Brazil’s credit rating could adversely affect our credit rating, the cost of our indebtedness and the trading price of securities issued by us.

Credit ratings affect investors’ perceptions of risk and, as a result, the yields required on indebtedness issuances in the financial markets. Rating agencies regularly evaluate Brazil and its sovereign ratings, taking into account a number of factors, including macroeconomic trends, fiscal and budgetary conditions, indebtedness and the prospect of change in these factors. Downgrades in Brazil’s credit rating can lead to downgrades in our credit rating and increase the cost of our indebtedness as investors may require a higher rate of return to compensate a perception of increased risk. In January 2018, Standard & Poor’s lowered Brazil’s credit rating to BB- with a stable outlook, which it changed to positive in December 2019 and back to stable in April 2020. In February 2018, Fitch downgraded Brazil’s credit rating to BB-, which it affirmed in May 2019 with a stable outlook and in May 2020 with a negative outlook. Moody’s rating is Ba2 with a stable outlook. Each of Standard & Poor’s, Fitch and Moody’s upgraded our credit rating in 2019.

Exchange rate instability may materially and adversely affect us.

The Brazilian currency has, during the last decades, experienced frequent and substantial variations in relation to the U.S. dollar and other foreign currencies. As of December 31, 2017, the U.S. dollar selling rate was R$3.308 per US$1.00. In 2018, the real depreciated against the U.S. dollar and, as of December 31, 2018, the U.S. dollar selling rate was R$3.875 per US$1.00. In 2019, the real depreciated further against the U.S. dollar and the U.S. dollar selling rate was R$4.031 per US$1.00 as of December 31, 2019. As of March 31, 2020 and June 26, 2020, the U.S dollar selling rate was R$5.199 to US$1.00 and R$5.463 to US$1.00, respectively, as reported by the Central Bank, representing a 35.5% depreciation of the real from December 31, 2019 through June 26, 2020. There can be no assurance that the real will not depreciate further against the U.S. dollar.

In 2019, 86.3% of our passenger revenue and other revenue were denominated in reais and a significant part of our operating costs and expenses, such as fuel, aircraft and engine maintenance services and aircraft insurance, are denominated in, or linked to, U.S. dollars. In 2019, 40.9% of our total operating costs and expenses were either denominated in or linked to U.S. dollars. The market and resale value of the majority of our operating assets, our aircraft, is denominated in U.S. dollars. As of December 31, 2019, R$13,839.1 million, or 95.7%, of our indebtedness was denominated in U.S. dollars and we had a total of R$9,245.1 million in non-cancelable U.S. dollar denominated future lease payments.

We are also required to maintain U.S. dollar denominated deposits and maintenance reserve deposits under the terms of some of our aircraft operating leases. We may incur substantial additional amounts of U.S. dollar‑denominated leases or financial obligations and U.S. dollar denominated indebtedness and be subject to fuel cost increases linked to the U.S. dollar. While in the past we have generally adjusted our fares in response to, and to alleviate the effect of, depreciation of the real against the U.S. dollar and increases in the price of jet fuel (which is priced in U.S. dollars) and have entered into hedging arrangements to protect us against the short‑term effects of such developments, there can be no assurance that we will be able to continue to do so.

9

Depreciation of the real against the U.S. dollar creates inflationary pressures in Brazil and causes increases in interest rates, which adversely affects the growth of the Brazilian economy as a whole, curtails access to foreign financial markets and may prompt government intervention, including recessionary governmental policies. Depreciation of the real against the U.S. dollar has also, as in the context of an economic slowdown, led to decreased consumer spending, deflationary pressures and reduced growth of the economy as a whole. Depreciation of the real also reduces the U.S. dollar value of distributions and dividends on the ADSs and the U.S. dollar equivalent of the market price of our preferred shares and, as a result, the ADSs. On the other hand, appreciation of the real against the U.S. dollar and other foreign currencies could lead to a deterioration of the Brazilian foreign exchange current accounts, as well as dampen export-driven growth. Depending on the circumstances, either depreciation or appreciation of the real could materially and adversely affect us.

Risks Relating to Us and the Brazilian Airline Industry

The outbreak and spread of COVID-19 have materially and adversely affected, and may further materially and adversely affect, the airline industry and us.

In December 2019, cases of COVID-19 were first reported in Wuhan, China, and the virus has now spread globally. The World Health Organization declared COVID-19 a pandemic and, in March 2020, governments around the world, including those of the United States, Brazil and most Latin American countries, declared states of emergency and implemented measures to halt the spread of the virus, including enhanced screenings, quarantine requirements and severe travel restrictions.

We have, beginning in the second half of March 2020, been redesigning our flight network and reduced our total flight capacity by approximately 92% in domestic markets and 100% in international markets. We suspended all regular regional and international operations and have maintained an essential network of 50 daily flights in April 2020 (representing 8% of the daily flights we operated in April 2019), 70 daily flights in May 2020 (representing 12% of the daily flights we operated in May 2019) and 120 daily flights in June 2020 (representing 16% of the daily flights we operated in June 2019), and we forecast approximately 240 daily flights in July 2020 (representing 32% of the daily flights we operated in July 2019). We continue to work with the Brazilian government to maintain minimum flight links for emergency reasons and to operate rescue and medical flights when requested to do so.

We have implemented a number of initiatives to reduce expenses and protect our liquidity, including deferral of non-essential capital expenditures and agreements with our employees. In addition, we are negotiating with lessors and creditors to adjust and defer certain of our payment obligations. We cannot assure you that travel restrictions or decreased demand for air travel will not persist or deteriorate for an extended period of time, in which case we may need to take additional measures to preserve our liquidity.

We may not be able to maintain adequate liquidity and our cash flows from operations and financings may not be sufficient to meet our current obligations.

Our liquidity, cash flows from operations and financings have been and may be adversely affected by exchange rates, fuel prices and the impact of adverse economic conditions in Brazil on the demand for air travel. As of December 31, 2019, our indebtedness was R$14,462.6 million, as compared to R$7,084.5 million as of December 31, 2018, mainly due to our adoption of IFRS 16 as of January 1, 2019. Despite the reduced air passenger demand caused by the COVID-19 pandemic and government measures to address it, we are operating at cash break-even and believe we have, as of the date of this annual report, liquidity for over 12 months, but we cannot assure you that this scenario will remain in case the economic downturn worsens or lasts longer than expected.

Certain of our indebtedness agreements contain covenants that require the maintenance of specified financial ratios. Our ability to meet these financial ratios and other restrictive covenants may be affected by events beyond our control and we cannot assure that we will meet those ratios. Failure to comply with any of these covenants or payment obligations under our finance and lease obligations could result in an event of default under these agreements and others, as a result of cross default provisions. If we were unable to comply with our indebtedness covenants, we need to seek waivers from our creditors. We cannot guarantee that we will be successful in complying with our covenants or in obtaining or renewing any waivers.

10

Our independent auditors have included a going concern emphasis paragraph in their opinion due to the significant drop in demand for air travel as a result of the effects of developments relating to the COVID-19 pandemic, and specifically the actions taken by the Brazilian government to address it, which are largely out of our control.

The consolidated financial statements included in this annual report have been prepared on a going concern basis of accounting, which contemplates continuity of operations, realization of assets and satisfaction of liabilities and commitments in the normal course of business. However, because of the significant drop in worldwide demand for air travel caused by the COVID-19 pandemic that has affected the entire airline industry, and the significant travel restrictions that have been placed by numerous countries, including Brazil, our independent registered public accounting firm, in its report on our consolidated financial statements as of and for the year ended December 31, 2019, has expressed substantial doubt regarding our ability to continue as a going concern.

Although we have, in response to the significantly reduced demand for air travel caused by the COVID-19 pandemic, taken a number of measures to protect our liquidity and cash provision, including adjusting our flight network, rolling over and extending certain debt, deferring certain lease obligations and significantly reducing fixed and variable costs, we cannot guarantee that we will be successful in implementing these initiatives.

We rely on one manufacturer for our aircraft and engines and further prolonged grounding of the Boeing 737 MAX aircraft would materially and adversely affect us.

One of the key elements of our business strategy and a key element of the low-cost carrier business model is to reduce costs by operating a standardized aircraft fleet. After extensive research and analysis, we chose the 737-700/800 Next Generation aircraft manufactured by The Boeing Company, or Boeing, and 56-7B engines manufactured by CFM International, or CFM. We expect to continue to rely on Boeing and CFM for the foreseeable future.

We derive benefits from a fleet comprised of a standardized type of aircraft while still having the flexibility to match the capacity and range of the aircraft to the demands of each route. If we had to lease or purchase aircraft of another manufacturer, we could lose these benefits. We cannot assure you that any such replacement aircraft would have the same operating advantages as the Boeing aircraft or that we could lease or purchase engines that would be as reliable and efficient as the CFM engines. Our operations could also be disrupted by the failure or inability of Boeing or CFM to provide sufficient parts or related support services on a timely basis.

In 2012, Boeing and CFM released new aircraft and engines, the Boeing 737-8 MAX and LEAP-1B, to replace the Boeing 737-700/800 Next Generation. Delivery and operation of the Boeing 737 MAX aircraft are crucial to our strategy and fleet modernization initiatives.

Following two accidents involving Boeing 737 MAX, regulators grounded the aircraft in March 2019, which Boeing now expects will return to operations in the second half of 2020. Further, Boeing has suspended MAX deliveries following the groundings and is not currently manufacturing new MAX aircraft. Because Boeing no longer manufactures versions of the 737 other than the 737 MAX family of aircraft and our operations have been designed around the single fleet model, if there is continued prolonged grounding of the MAX aircraft that we have already received and additional delays in delivery of our ordered aircraft, we may face increased maintenance costs on our aircraft, experience operational disruptions and decreases in customer ratings, be unable to realize our expected fuel cost efficiencies, incur increased aircraft lease costs and risk facing a shortage of available aircraft, which may limit our growth plans and the execution of our long-term strategy.

Further prolonged grounding would likely increase the adverse effects upon us, and we cannot assure you that we will receive adequate compensation from Boeing for the negative impacts we have suffered or may suffer from the grounding of the MAX. In addition, any accidents or incidents involving our or any other Boeing 737 Next Generation or Boeing 737-8 MAX aircraft or the aircraft of any major airline have and may again cause negative public perceptions about us, and, consequently, adversely affect us.

The airline industry is particularly sensitive to changes in macroeconomic conditions and adverse macroeconomic conditions would likely adversely affect us.

Our operations and the airline industry in general are particularly sensitive to changes in macroeconomic conditions. Unfavorable macroeconomic conditions in Brazil, a constrained credit market and increased business operating costs reduce spending on both leisure and business travel, as well as cargo transportation. Any slowdown in the Brazilian economy may adversely affect industries with significant spending in travel, including government, oil and gas, mining and construction, which would affect the quality of demand, reducing the number of higher yield tickets we can sell. Unfavorable macroeconomic conditions can also affect our ability to raise fares to counteract increased fuel, labor and other costs. Any of these factors may negatively affect us.

11

Unfavorable economic conditions, a significant decline in demand for air travel or continued instability of the credit and capital markets could also result in pressure on our indebtedness costs, operating results and financial condition and would affect our growth and investment plans. These factors could also negatively affect our ability to obtain financing on acceptable terms and liquidity generally.

Substantial fluctuations in fuel costs would harm us.

International and local fuel prices are subject to high volatility depending on multiple factors, including geopolitical issues and supply and demand. The price of West Texas Intermediate crude oil, a benchmark widely used for crude oil prices that is measured in barrels and quoted in U.S. dollars, affects our fuel costs and constitutes a significant portion of our total operating costs and expenses. The average price per barrel of West Texas Intermediate crude oil was US$50.85, US$64.90 and US$57.04 in 2017, 2018 and 2019, respectively. Fuel costs represented 31%, 39% and 34% of our total operating costs and expenses in 2017, 2018 and 2019, respectively.

Although we enter into hedging arrangements to reduce our exposure to fuel price fluctuations and have historically passed on the majority of fuel price increases by adjusting our fare structure, the price and availability of fuel cannot be predicted with any degree of certainty. As of the date of this annual report, we have approximately US$100.0 million invested in a portfolio of 17 million barrels of oil for the monthly periods through December 2022. This amount is based on our 2019 fuel costs of approximately R$4.0 billion, and recent historical fuel price volatility of around 15-20%. Approximately 65% of this portfolio is in out-of-the-money call options (US$55 average exercise price) with premiums paid for in prior periods. The remaining 35% of this portfolio is in zero cost collars with Brent puts that are immunized at US$20 and that are fully marked-to-market and fully invested in deposits with top-tier counterparties. We have a hedge ratio of 60% for 2020 consumption in the low $60 per barrel price range, and hedge ratios of 30% for 2021 and 2022 at oil prices in the mid-$40 range. Our hedging activities and fare adjustments may not be sufficient to protect us fully from fuel price increases.

Substantially all of our fuel is supplied by one source, Petrobras Distribuidora S.A., or Petrobras Distribuidora. If Petrobras Distribuidora is unable or unwilling to continue to supply fuel at the times and in the quantities that we require, we may not be able to find a suitable replacement or to purchase fuel at the same cost, which would likely adversely affect us. See “Item 4. Information on the Company—B. Business Overview—Airline Business—Fuel.”

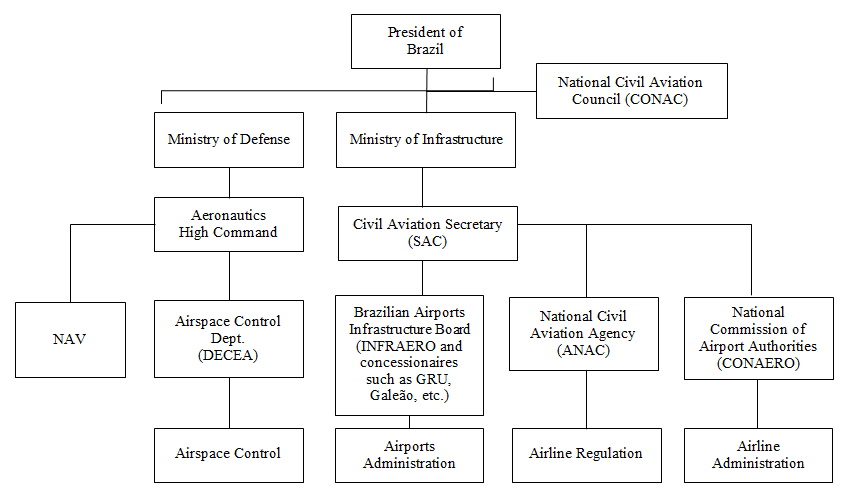

Changes to the Brazilian civil aviation regulatory framework, including rules regarding slot distribution, fare restrictions and fees associated with civil aviation, may adversely affect us.

Brazilian aviation authorities monitor and influence the developments in Brazil’s airline market. For example, airport services are regulated by ANAC and, in many cases, still managed by the Brazilian Airport Infrastructure Company (Empresa Brasileira de Infraestrutura Aeroportuária), or INFRAERO, a government-owned corporation. ANAC addressed overcapacity in the system in 2014 by establishing strict criteria that must be met before new routes or additional flight frequencies are awarded. ANAC policies as well as those of other aviation supervisory authorities have and may again adversely affect us. In July 2014, ANAC published new rules governing the allocation of slots in coordinated/slotted airports, including Congonhas and Guarulhos, which are the two main airports for the city of São Paulo. In 2016, additional airports, but non-coordinated nowadays, became subject to these rules, such as Brasília (Distrito Federal), Galeão (Rio de Janeiro), Florianópolis (Santa Catarina) and others. ANAC considers operating history and efficiency (on-time performance and regularity) as the main criteria for the allocation of slots. Under these rules, on-time performance and regularity are assessed twice per year, following the International Air Transport Association, or IATA, summer and winter calendars, between April and September and between October and March. The minimum regularity performance target for each series of slots in a season is 90% at Congonhas airport (São Paulo) and 80% for Guarulhos (São Paulo), Santos Dumont (Rio de Janeiro) and Recife. The on-time performance, since 2018, is measured through the method of statistical tendency that compares the performance of all airlines for each airport. Airlines forfeit slots used below the minimum criteria in a season. Forfeited slots are redistributed first to new entrants, which includes airlines that operate fewer than five slots in the affected airport in the given weekday, and are subsequently returned to the slots database and redistribuided according to regulations. We cannot foresee these and other changes to the Brazilian civil aviation regulatory framework, which could increase our costs, change the competitive dynamics of our industry and adversely affect us including as discussed in “—We operate in a highly competitive industry.”

12

Technical and operational problems in the Brazilian civil aviation infrastructure, including air traffic control systems, airspace and airport infrastructure, may adversely affect us.

We depend on improvements in the coordination and development of Brazilian airspace control and airport infrastructure, which continue to require substantial improvements and government investments.

If the measures taken and investments made by the Brazilian government and regulatory authorities do not prove sufficient or effective, air traffic control, airspace management and sector coordination difficulties might reoccur or worsen, which may adversely affect us.

Slots at Congonhas airport in São Paulo, the most important airport for our operations and the busiest one in Brazil, are fully utilized on weekdays. The Santos Dumont airport in Rio de Janeiro, a highly utilized airport with half‑hourly shuttle flights between São Paulo and Rio de Janeiro, also has certain slot restrictions. Several other Brazilian airports, including the Brasília, Campinas, Salvador, Confins and São Paulo (Guarulhos) international airports, have limited the number of slots per day due to infrastructural limitations at these airports. Any condition that would prevent or delay our access to airports or routes that are vital to our strategy or our inability to maintain our existing slots, and obtain additional slots, may adversely affect us. In addition, we cannot assure that any investments will be made by the Brazilian government in the Brazilian aviation infrastructure (by expanding additional or developing new airports) to permit our growth.

We have significant recurring aircraft expenses, and we will incur significantly more fixed costs that could hinder our ability to meet our strategic goals.

We have significant costs, relating primarily to leases for our aircraft and engines. Following negotiations with Boeing in March 2020, as of the date of this annual report, we have commitments of R$26,739.5 million (US$6,633.5 million) for deliveries through 2028. We expect that we will incur additional fixed obligations and indebtedness as we take delivery of the new aircraft and other equipment to implement our strategy.

These significant fixed payment obligations:

· could limit our ability to obtain additional financing to support expansion plans and for working capital and other purposes;

· divert substantial cash flows from our operations to service our fixed obligations under aircraft operating leases and aircraft purchase commitments;

· if interest rates increase, require us to incur significantly more lease or interest expense than we currently do; and

· could limit our ability to react to changes in our business, the airline industry and general economic conditions.

Our ability to make scheduled payments on our fixed obligations will depend on our operating performance and cash flow, which will in turn depend on prevailing macroeconomic and political conditions and financial, competitive, regulatory, business and other factors, many of which are beyond our control. In addition, our ability to raise our fares to compensate for an increase in our fixed costs may be limited by competition and regulatory factors.

We operate in a highly competitive industry.

We face intense competition on all routes we operate from existing scheduled airlines, charter airlines and potential new entrants in our market. Competition from other airlines has a relatively greater impact on us when compared to our competitors because we have a greater proportion of flights connecting Brazil’s busiest airports, where competition is more intense. In contrast, some of our competitors have a greater proportion of flights connecting less busy airports, where there is little or no competition. In addition, we cannot foresee how the recent financial distress of our main competitors will affect the competitive landscape.

The Brazilian airline industry also faces competition from ground transportation alternatives, such as interstate buses. In addition, the Brazilian government and regulators could give preference to new entrants and existing competitors when granting new and current slots in Brazilian airports in order to promote competition.

13

Existing and potential competitors have in the past and may again undercut our fares or increase capacity on their routes in an effort to increase their market share of business traffic (high value-added customers). In any such event, we cannot assure you that our level of fares or passenger traffic would not be adversely affected.

Changes in the Brazilian and global airline industry framework may adversely affect us.

As a result of the competitive environment, there may be further changes in the Brazilian and global airline industry, whether by means of acquisitions, joint ventures, partnerships or strategic alliances. We cannot predict the effects of further consolidation on the industry. For example, most recently, Oceanair Linhas Aéreas S.A., which operated under the name Avianca Brasil, filed for judicial restructuring in December 2018 and terminated operations in 2019, which resulted in further industry consolidation. Consolidation in the airline industry and changes in international alliances will continue to affect the competitive landscape in the industry and may result in the formation of airlines and alliances with greater financial resources, more extensive global networks and lower cost structures than we can obtain.

In December 2018, the former Brazilian president approved Provisional Measure No. 863 (Medida Provisória No. 863), which revoked restrictions on foreign ownership of Brazilian airlines’ voting stock. The measure was endorsed by the Brazilian government that took office in January 2019 and, in June 2019, was partially converted into Law No. 13,842, which allows companies with 100% foreign capital to invest in airlines operating in Brazil, revoking the prior limitation of 20% of foreign capital, provided that foreign companies are constituted in accordance with Brazilian law and provided that they have their headquarters and management in Brazil. We cannot foresee how this law will affect us and the competitive environment in Brazil.

We rely on complex systems and technology and any operational or security inadequacy or interruption could materially and adversely affect us.

In the ordinary course of our business, our systems and technology require ongoing modification and refinements, which can to be expensive to implement and may divert management’s attention from other matters. In addition, our operations could be adversely affected, or we could face regulatory penalties, if we were unable to timely or effectively modify our systems as necessary.

We have occasionally experienced system interruptions and delays that make our websites and services unavailable or slow to respond, which could prevent us from efficiently processing customer transactions or providing services. This could reduce our net revenue and the attractiveness of our services. Our computer and communications systems and operations could be damaged or interrupted by catastrophic events such as fires, floods, earthquakes, power loss, computer and telecommunications failures, acts of war or terrorism, computer viruses, cybersecurity breaches and similar events or disruptions. Any of these events could cause system interruptions, delays and loss of critical data, and could prevent us from processing customer transactions or providing services, which could make our business and services less attractive and subject us to liability. Any of these events could damage our reputation and be expensive to remedy.

We rely on maintaining a high daily aircraft utilization rate to increase our revenues and reduce our costs.

One of the key elements of our business strategy and an important element of the low-cost carrier business model is to maintain a high daily aircraft utilization rate, which we measured as 12.3 block hours per day in 2019. High daily aircraft utilization allows us to generate more revenue from our aircraft and dilute our fixed costs, and is achieved in part by operating with quick turnaround times at airports so we can fly more hours on average in a day. Our rate of aircraft utilization could be adversely affected by a number of different factors that are beyond our control, including, among others, air traffic and airport congestion, adverse weather conditions and delays by third-party service providers relating to matters such as fueling and ground handling.

We may be adversely affected by events out of our control, including accidents and pandemics.

Accidents or incidents involving our aircraft could result in significant claims by injured passengers and others, as well as significant costs related to the repair or replacement of damaged aircraft and temporary or permanent loss from service. We are required by ANAC and lessors of our aircraft under our operating lease agreements to carry liability insurance. Although we believe we maintain liability insurance in amounts and of the type generally consistent with industry practice, the amount of such coverage may not be adequate and we may be forced to bear substantial losses in the event of an accident. Substantial claims resulting from an accident in excess of our related insurance coverage would harm us. Accidents or incidents involving our or any other Boeing 737 Next Generation or Boeing 737-8 MAX aircraft or the aircraft of any major airline have and may again cause negative public perceptions about us, and, consequently, adversely affect us.

14

In 2020, the outbreak of the COVID-19 pandemic, combined with government measures to address it and related media responses, has led to severe travel restrictions and significantly reduced demand for air travel around the world, significantly reducing our revenue in the period since April 2020. We cannot predict how this global pandemic will evolve and further affect us, but we expect demand at significantly reduced levels at least through year-end 2020, which will adversely affect our results of operations and financial position.

Our controlling shareholders have the ability to direct our business and affairs and their interests could conflict with yours.

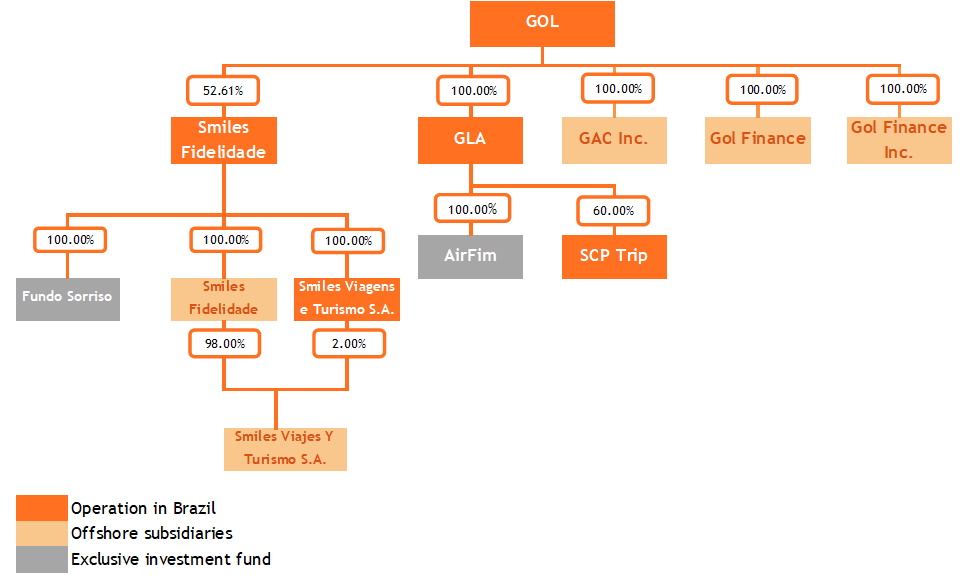

Our controlling shareholders have the power to, among other things, elect a majority of our directors and determine the outcome of any action requiring shareholder approval, including transactions with related parties, corporate reorganizations and dispositions and the timing and payment of any dividends. The chairman of our board of directors, Constantino de Oliveira Junior, has since our inception been the fundamental figure of our company, and has directed our company initially as its chief executive officer, and, since 2012, as the chairman of our board of directors. As of December 31, 2019, the Constantino family, which indirectly controls us, had 51.9% of the economic interests in us. A difference in economic exposure may intensify conflicts of interests between our controlling shareholders and you. See “Item 9. The Offer and Listing—C. Markets—Corporate Governance Practices.”

The effect of any discontinuation or replacement of the LIBOR may adversely affect us.

The U.K. Financial Conduct Authority announced in July 2017 that it intends to no longer compel banks to submit rates for the calculation of the London interbank offered rate, or LIBOR, after 2021. To mitigate any possible impact, various regulators have proposed alternative reference rates. As of December 31, 2019, we had R$446.0 million of LIBOR-indexed variable rate leases terminating after 2021. We cannot predict the effect of any discontinuation or replacement of the LIBOR at this time and, consequently, we cannot assure you that these changes will not have an adverse effect on us.

Risks Relating to the ADSs and Our Preferred Shares

The relative volatility and illiquidity of the Brazilian securities markets, and securities issued by airlines in particular, may substantially limit your ability to sell the preferred shares underlying the ADSs at the price and time you desire.

Investing in securities that trade in emerging markets, such as Brazil, often involves greater risk than investing in securities of issuers in the United States, and such investments are generally considered to be more speculative in nature. The Brazilian securities market is substantially smaller, less liquid, more concentrated and can be more volatile than major securities markets in the United States. Accordingly, although you are entitled to withdraw the preferred shares underlying the ADSs from the depositary at any time, your ability to sell the preferred shares underlying the ADSs at a price and time at which you wish to do so may be substantially limited. There is also significantly greater concentration in the Brazilian securities market than in major securities markets in the United States. The ten largest companies in terms of market capitalization represented 47.0% of the aggregate market capitalization of the B3, as of December 31, 2019.

The trading prices of shares of companies in the worldwide airline industry are relatively volatile and investors’ perception of the market value of the ADSs and preferred shares may be adversely affected by volatility and decreases in their trading prices.

Holders of the ADSs and our preferred shares may not receive any dividends.

According to our bylaws, we must pay our shareholders at least 25.0% of our annual net income as dividends, as determined and adjusted under Brazilian corporate law. Our adjusted net income may be capitalized, used to absorb losses or otherwise appropriated as allowed under Brazilian corporate law and may not be available to be paid as dividends. We may not pay dividends to our shareholders in any particular fiscal year if our board of directors determines that such distributions would be inadvisable in view of our financial condition. In the past five fiscal years, we did not distribute dividends.

15

If you surrender your ADSs and withdraw preferred shares, you risk losing the ability to remit foreign currency abroad and certain Brazilian tax advantages.

As an ADS holder, you benefit from the electronic foreign capital registration obtained by the custodian for our preferred shares underlying the ADSs in Brazil, which permits the custodian to convert dividends and other distributions with respect to the preferred shares into non-Brazilian currency and remit the proceeds abroad. If you surrender your ADSs and withdraw preferred shares, you will be entitled to continue to rely on the custodian’s electronic foreign capital registration for only five business days from the date of withdrawal. Thereafter, upon the disposition of or distributions relating to the preferred shares, you will not be able to remit non-Brazilian currency abroad unless you obtain your own electronic foreign capital registration.

If you attempt to obtain your own electronic foreign capital registration, you will incur expenses and may suffer delays in the application process, which could delay your ability to receive dividends or distributions relating to our preferred shares or the return of your capital in a timely manner.

Holders of the ADSs may be unable to exercise preemptive rights with respect to our preferred shares.

We may not be able to offer our preferred shares to U.S. holders of the ADSs pursuant to preemptive rights granted to holders of our preferred shares in connection with any future issuance of our preferred shares, unless a registration statement under the U.S. Securities Act of 1933, or the Securities Act, is effective with respect to such preferred shares and preemptive rights, or an exemption from the registration requirements of the Securities Act is available. We are not obligated to file a registration statement relating to preemptive rights with respect to our preferred shares, and we cannot assure you that we will file any such registration statement. If such a registration statement is not filed and an exemption from registration does not exist, the depositary bank will attempt to sell the preemptive rights, and you will be entitled to receive the proceeds of such sale. However, these preemptive rights will expire if the depositary does not sell them, and U.S. holders of the ADSs will not realize any value from grants of such preemptive rights.

ITEM 4. Information on the Company

A. History and Development of the Company

Overview

GOL is Brazil’s premier domestic airline and one of the largest low-cost carriers globally. We pioneered the low-cost carrier model in South America and offer the best product and customer experience to business and leisure passengers.

In 2019, we:

· were the largest Brazilian airline with over 36 million annual passengers transported and a domestic market share of 38%, as measured by RPK;

· had the lowest operating costs of any Brazilian airline, with a CASK ex-fuel of R$14.1 cents (US$3.5 cents), and one of the lowest among airlines globally;

· were among the five largest low-cost carriers globally based on annual revenue;

· achieved an aircraft utilization of 12.3 block hours per day, one of the highest in the world;

· operated the most flights at Brazil’s busiest airports;

· were a leader in technology development and digital solutions that enable us to offer the best passenger experience, with a net promoter score (NPS) of 38;

· operated the leading Brazilian airline loyalty program, with 16.9 million members as of December 31, 2019;

· were Brazil’s second largest cargo airline with a 25% market share as measured by ATKs; and

16

· operated the largest MRO facility in Brazil, with over 1.0 million square feet of hangar and ramp areas, six shops, more than 60,000 square feet of parts storage area and over 700 employees.