UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form

(Mark One)

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| [ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| SHELL COMPANY PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report __________________

Commission file number:

(Exact name of Registrant as specified in its charter)

not applicable

(Translation of Registrant's name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

|

Title of each class |

Name of each exchange on which registered |

|

None |

Not applicable |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

- 1 -

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

Common shares

(Title of Class)

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report.

| Title of each class | Outstanding at December 31, 2022 |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. |

||||

|

|

[ ] |

Yes |

[✓] |

|

| If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | ||||

| [ ] | Yes | [✓] | ||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ||||

| [✓] | [ ] | No | ||

| Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | ||||

| [✓] | [ ] | No | ||

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer: See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. (Check one): |

|

Large accelerated filer |

[ ] |

Accelerated filer |

[ ] |

|

[✓] |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| [✓] | International Financial Reporting as issued by the International Accounting Standards Board | [ ] | Other | [ ] |

| If "Other" has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. | ||||

| [ ] | Item 17 | [ ] | Item 18 | |

| If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | ||||

| [ ] | Yes | [ |

No | |

- 2 -

TABLE OF CONTENTS

- 3 -

- 4 -

GENERAL MATTERS

Use of Names

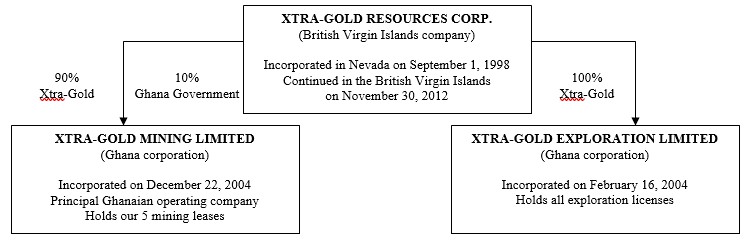

In this annual report filed on Form 20-F, the terms "Xtra-Gold", "Company", "we", and "our" refers to Xtra-Gold Resources Corp., a British Virgin Islands company, and our wholly-owned subsidiaries, Xtra-Gold Exploration Limited and Xtra Oil & Gas (Ghana) Limited and our 90% owned subsidiary, Xtra-Gold Mining Limited.

Currency

Unless otherwise specified, all dollar amounts in this annual report are expressed in United States dollars.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report, including all exhibits hereto, contains forward-looking statements and forward-looking information. Forward-looking statements are with reference to our financial condition, results of operations, business prospects, plans, objectives, goals, strategies, future events, capital expenditure, and exploration and development efforts. Words such as "anticipates", "expects", "intends", "plans", "forecasts", "projects", "budgets", "believes", "seeks", "estimates", "could", "might", "should", and similar expressions identify forward-looking statements. Although we believe that our plans, intentions and expectations reflected in these forward-looking statements are reasonable, we cannot be certain that these plans, intentions or expectations will be achieved. Actual results, performance or achievements could differ materially from those contemplated, expressed or implied by the forward-looking statements. These statements include comments regarding the establishment and estimates of mineral reserves and mineral resources, production, production commencement dates, productions costs, cash operating costs per ounce, total cash costs per ounce, grade, processing capacity, potential mine life, feasibility studies, development costs, capital and operating expenditures, exploration, the closing of certain transactions including acquisitions and offerings. All statements, other than statements of historical facts, included in this annual report, our other filings with the SEC and Canadian securities commissions and in news releases and public statements made by our officers, directors or representatives of our company, that address activities, events or developments that we expect or anticipate will or may occur in the future are forward-looking statements and forward-looking information.

The following, in addition to the factors described elsewhere in this annual report under "Risk Factors", are among the factors that could cause actual results to differ materially from the forward-looking statements:

● our ability to continue as a going concern

● the effect of COVID-19 on world economies and the company's operations;

● unexpected changes in business and economic conditions;

● significant increases or decreases in gold prices;

● changes in interest rates and currency exchange rates;

● unanticipated grade changes;

● changes in metallurgy;

● access and availability of materials, equipment, supplies, labor and supervision, power and water;

● determination of mineral resources and mineral reserves;

● availability of drill rigs; changes in project parameters;

● costs and timing of development of new mineral reserves; results of current and future exploration activities;

● results of pending and future feasibility studies; joint venture relationships;

● political or economic instability, either globally or in the countries in which we operate;

● local and community impacts and issues;

● timing of receipt of government approvals; accidents and labor disputes; environmental costs and risks; and

● competitive factors, including competition for property acquisitions; and availability of capital at reasonable rates or at all.

- 5 -

With respect to any forward-looking statement that includes a statement of its underlying assumptions or bases, we believe such assumptions or bases to be reasonable and have formed them in good faith, assumed facts or bases almost always vary from actual results, and the differences between assumed facts or bases and actual results can be material depending on the circumstances. When, in any forward-looking statement, we express an expectation or belief as to future results, that expectation or belief is expressed in good faith and is believed to have a reasonable basis, but there can be no assurance that the stated expectation or belief will result or be achieved or accomplished. All subsequent written and oral forward-looking statements attributable to us, or anyone acting on our behalf, are expressly qualified in their entirety by the cautionary statements. Except for our ongoing obligations to disclose material information under the Federal securities laws, we do not undertake any obligations to publicly release any revisions to any forward-looking statements to reflect events or circumstances after the date of this annual report or to reflect unanticipated events that may occur. These forward-looking statements speak only as of the date of this annual report and you should not rely on these statements without also considering the risks and uncertainties associated with these statements and our business.

CAUTIONARY NOTE TO INVESTORS CONCERNING RESERVE AND RESOURCE ESTIMATES AND OTHER MINING INFORMATION UNDER S-K 1300 AS COMPARED TO NI 43-101

Except where noted, the reserve and resource estimates in this Annual Report have been prepared in accordance with the requirements of SEC Regulation S-K (Subpart 1300) ("S-K 1300") which came into force on January 1, 2021 and replaces Industry Guide 7. S-K 1300 now aligns most mining disclosure for SEC registrants in accordance with the definitions provided by the Committee for Reserves International Reporting Standards ("CRIRSCO"). Investors are cautioned however, that all reserve and resource estimates previously furnished or filed by the Company with the SEC were initially prepared in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101"). NI 43-101 is a rule developed by the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. NI 43-101 was also developed in accordance with CRIRSCO guidelines.

S-K 1300 includes the adoption of terms describing mineral reserves and mineral resources that are substantially similar to the corresponding terms under CRIRSCO. As a result of the adoption of S-K 1300, the SEC will now recognize estimates of "measured mineral resources", "indicated mineral resources" and "inferred mineral resources". In addition, the SEC has amended its definitions of "proven mineral reserves" and "probable mineral reserves" to be substantially similar to CRIRSCO.

Investors are cautioned that while the above terms are substantially similar to CRIRSCO, there are differences in the definitions under S-K 1300 and CRIRSCO. Accordingly, there is no assurance any mineral reserves or mineral resources that the Company may report as "proven reserves", "probable reserves", "measured mineral resources", "indicated mineral resources" and "inferred mineral resources" under NI 43-101 would be the same had the Company prepared the reserve or resource estimates under the standards adopted under S-K 1300.

Investors are also cautioned that while the SEC will now recognize "measured mineral resources", "indicated mineral resources" and "inferred mineral resources", (i) a "measured mineral resource" has a higher level of confidence than that applying to either an "indicated mineral resource" or an "inferred mineral resource", it may be converted to a "proven mineral reserve" or to a "probable mineral reserve", (ii) an "indicated mineral resource" has a lower level of confidence than that applying to a "measured mineral resource" and may only be converted to a "probable mineral reserve", and (iii) an "inferred mineral resource" has a lower level of confidence than that applying to an "indicated mineral resource" and must not be converted to a "mineral reserve. Mineralization described using these terms has a greater amount of uncertainty as to their existence and feasibility than mineralization that has been characterized as reserves. Accordingly, investors are cautioned not to assume that any "measured mineral resources", "indicated mineral resources", or "inferred mineral resources" that the Company reports are or will be economically or legally mineable.

- 6 -

PART I

Item 1 Identity of Directors, Senior Management and Advisors

This Form 20-F is being filed as an annual report under the Securities Exchange Act of 1934 and, as such, there is no requirement to provide any information under this item.

Item 2 Offer Statistics and Expected Timetable

This Form 20-F is being filed as an annual report under the Securities Exchange Act of 1934 and, as such, there is no requirement to provide any information under this item.

Item 3 Key Information

A. Selected Financial Data

The following financial information has been extracted from our consolidated financial statements for the years indicated and is expressed in United States dollars. Our consolidated financial statements were prepared in accordance with U.S. generally accepted accounting principles ("U.S. GAAP"). The historical data included below and elsewhere in this annual report is not necessarily indicative of our future performance. The financial information should be read in conjunction with our consolidated financial statements and related notes included in this annual report and "Item 5. Operating and Financial Review and Prospects - A. Operating Results and B. Liquidity and Capital Resources" of this annual report.

In this annual report, all currency refers to United States Dollars (US$) unless indicated otherwise.

The following table summarizes information relating to the operations of Xtra-Gold for the last five fiscal years ended December 31.

For the Year Ended December 31

| 2022 | 2021 | 2020 | 2019 | 2018 | |

| $ | $ | $ | $ | $ | |

| Operating revenues | Nil | Nil | Nil | Nil | Nil |

| Income before tax | 1,564,849 | 2,045,713 | 2,297,023 | 2,388,347 | 1,539,294 |

| Net gain attributable to non-controlling interest | (133,082) | (121,545) | (141,782) | (140,390) | (233,111) |

| Income tax | (800,000) | (1,088,192) | (294,992) | Nil | Nil |

| Net gain (loss) attributable to Xtra-Gold Resources Corp. | 631,767 | 957,521 | 1,860,249 | 2,247,957 | 1,306,183 |

| Basic and diluted gain (loss) attributable to common shareholders per common share | 0.01 | 0.02 | 0.04 | 0.05 | 0.03 |

| Total current assets | 10,178,896 | 9,127,160 | 7,739,823 | 5,438,857 | 3,258,955 |

| Total assets | 11,881,013 | 10,758,031 | 9,340,942 | 6,875,325 | 4,790,576 |

| Total current liabilities | 1,406,679 | 1,122,483 | 426,819 | 443,540 | 624,205 |

| Total liabilities | 1,406,679 | 1,122,483 | 426,819 | 443,540 | 624,205 |

| Working capital | 8,772,217 | 8,004,677 | 7,313,004 | 4,995,317 | 2,634,750 |

| Capital stock | 46,447 | 46,688 | 46,817 | 45,844 | 46,246 |

| Total equity | 10,474,334 | 9,635,548 | 8,914,123 | 6,431,785 | 4,166,371 |

| Total Xtra-Gold Resources Corp. stockholders' equity | 10,532,448 | 9,826,744 | 9,226,864 | 6,886,308 | 4,761,284 |

| Dividends declared per share | Nil | Nil | Nil | Nil | Nil |

| Basic weighted average number of common shares outstanding | 46,542,900 | 46,779,574 | 46,645,387 | 46,095,232 | 47,089,027 |

| Diluted weighted average number of common shares outstanding | 48,822,024 | 48,925,574 | 49,033,887 | 49,589,430 | 49,405,027 |

- 7 -

B. Capitalization and Indebtedness

This Form 20-F is being filed as an annual report under the Securities Exchange Act of 1934 and, as such, there is no requirement to provide any information under this item.

C. Reasons for the Offer and Use of Proceeds

This Form 20-F is being filed as an annual report under the Securities Exchange Act of 1934 and, as such, there is no requirement to provide any information under this item.

D. Risk Factors

The securities of our company are considered speculative due to the nature of our business and the present stage of our development. Only those persons who can bear the risk of the entire loss of their investment should participate. An investor should carefully consider the risks described below and the other information that we file with the Securities and Exchange Commission and with Canadian securities regulators before investing in our common shares. The risks described below are not the only ones faced. Additional risks that we are either unaware of, or we are aware of, but we currently believe are immaterial, may become important factors that affect our business. If any of the following risks occur, or if others occur, our business, operating results and financial condition could be seriously harmed, and the investor may lose all of their investment.

Risks Associated with our Company and our Operations

Our company is currently in the exploration stage with respect to all our projects. The chance of ever reaching the production stage at our projects is uncertain. Our company cannot predict whether we will successfully effectuate our company's current business plan.

If our company does not obtain new financings, commencing from 2023, the amount of funds available to our company to pursue any further exploration activities at our projects could be reduced and our company's plan of operations may be adversely affected.

Our company has relied on private placement financings and an initial public offering completed in Canada in November 2010 to fund our exploration programs, including our drilling programs at our Kibi project. Commencing from 2023, our company will continue to require additional financing to complete our plan of operations to carry out any further exploration activities on our projects. Any impairment in our company's ability to raise additional funds through financings would reduce the available funds for such exploration activities, with the result that our company's plan of operations may be adversely affected.

Substantial additional capital may be required commencing from 2023 to continue exploration activities at all of our projects. If our company cannot raise additional capital as needed, our ability to execute our business plan and fund our ongoing operations will be in jeopardy.

Commencing from 2023, our company may need to explore various financing alternatives to meet our projected costs and expenses. Our company cannot assure our stockholders that we will be able to obtain the necessary financing for our projects on favorable terms or at all. Additionally, if the actual costs to execute our company's business plan are significantly higher than expected, our company may not have sufficient funds to cover these costs and we may not be able to obtain other sources of financing. The failure to obtain all necessary financing would prevent our company from executing our business plan and would impede our company's ability to sustain operations or become profitable, and our company could be forced to cease our operations.

To date, we have not generated revenues from operations and our company will continue to incur operating losses and there is no guarantee that we will achieve operating profits.

Our company has incurred operating losses on an annual basis for a number of years, primarily arising out of the costs related to continued exploration and development of mineral resource properties, including costs written off on properties no longer being pursued by our company. As of December 31, 2022, our company had an accumulated deficit of $21,345,398. It is anticipated that our company could experience an operating loss for fiscal 2023 until our company discovers economically mineable mineralized material and successfully develops a mine. There can be no assurance that our company will ever achieve significant revenues or profitable operations.

Our auditors have raised substantial doubts as to our ability to continue as a going concern.

Our financial statements have been prepared assuming we will continue as a going concern. Since inception we have experienced recurring losses from operations, which losses have caused an accumulated deficit of $21,345,398 as of December 31, 2022. These factors, among others, raise substantial doubt about our ability to continue as a going concern for one year from the issuance of the financial statements. Our financial statements do not include any adjustments that might result from the outcome of this uncertainty. We anticipate that we may continue to incur losses in future periods until we are successful in generating revenues which are significant enough to pay our expenses and fund our exploration efforts. There are no assurances that we will be able to raise our revenues to a level which supports profitable operations and provides sufficient funds to pay our obligations as they are incurred. If we are unable to meet those obligations, we could be forced to substantially curtail our operations and planned exploration efforts, which would have a material adverse effect on our business and operations in future periods.

- 8 -

Our company's projects are in the exploration stage and may not result in the discovery of commercial bodies of mineralization which would result in our company discontinuing that project. Substantial expenditures are required to determine if a project has economically mineable mineralized material.

Our company's projects are all in the exploration stage. Mineral exploration involves a high degree of risk and few properties which are explored are developed into producing mines. The exploration efforts of our company on our projects may not result in the discovery of commercial bodies of mineralization which would require our company to discontinue that project. Substantial expenditures are required to determine if a project has economically mineable mineralized material. It could take several years to establish proven and probable mineral resources or reserves. Due to these uncertainties, there can be no assurance that current and future exploration programs will result in the discovery of mineral resources or reserves.

Our company currently depends significantly on a limited number of projects.

Our company's activities are currently focused on our Kibi and Kwabeng projects. Our company will as a consequence be exposed to some heightened degree of risk due to the lack of property diversification. Adverse changes or developments affecting our Kibi or Kwabeng projects would have a material and adverse effect on our company's business, financial condition, results of operations and prospects.

Our company is subject to factors beyond our control which may impact our company's title in our projects.

Although our company has obtained title opinions with respect to all of our projects and has taken other reasonable measures to ensure proper title to these projects, there is no guarantee that title to any of our projects will not be challenged or impugned. Third parties may have valid claims underlying portions of our company's interests. Our projects may be subject to prior unregistered liens, agreements, transfers or claims and title may be affected by, among other things, undetected defects. In addition, our company may be unable to operate our projects as permitted or to enforce its rights with respect to our projects.

Our company's activities are and will be subject to complex laws, significant government regulations and accounting standards that may delay or prevent operations at our projects and can adversely affect our company's operating costs, the timing of our company's operations, ability to operate and financial results.

Business, exploration activities and any future development activities and mining operations are and will be subject to extensive Ghanaian, United States, Canadian, British Virgin Islands and other foreign, federal, state, territorial and local laws and regulations and also exploration, development, production, exports, taxes, labor standards, waste disposal, protection of the environment, reclamation, historic and cultural resource preservation, mine safety and occupational health, reporting and other matters, as well as accounting standards. Compliance with these laws, regulations and standards or the imposition of new such requirements could adversely affect our company's operating and future development costs, the timing of our company's operations, ability to operate and financial results. These laws and regulations governing various matters include:

● environmental protection;

● management of natural resources;

● exploration, development of mines, production and post-closure reclamation;

● export and import controls and restrictions;

● price controls;

● geopolitical risks could affect the import of consumables;

● taxation;

● labor standards and occupational health and safety, including mine safety;

● historic and cultural preservation; and

● generally accepted accounting principles.

- 9 -

The costs associated with compliance with these laws and regulations may be substantial and possible future laws and regulations, or more stringent enforcement of current laws and regulations by governmental authorities, could cause additional expense, capital expenditures, restrictions on or suspensions of our company's operations and delays in the development of our projects. These laws and regulations may allow governmental authorities and private parties to bring lawsuits based upon damages to property and injury to persons resulting from the environmental, health and safety impacts of our company's past and current operations, and could lead to the imposition of substantial fines, penalties or other civil or criminal sanctions. In addition, our company's failure to comply strictly with applicable laws, regulations and local practices relating to permitting applications or reporting requirements could result in loss, reduction or expropriation of entitlements, or the imposition of additional local or foreign parties as joint venture partners. Any such loss, reduction, expropriation or imposition of partners could have a materially adverse effect on our company's operations or business.

Our company may not be able to obtain, renew or continue to comply with all of the permits necessary to develop each of our projects which would force our company to discontinue development, if any, on that project.

Pursuant to Ghanaian law, if our company discovers economically mineable mineralized material, we must obtain various approvals, licenses or permits pertaining to environmental protection and use of water resources in connection with the development, if any, of our projects. In addition to requiring permits for the development of our mineral concessions where our projects are located, our company may need to obtain other permits and approvals during the life of our projects. Obtaining, renewing and continuing to comply with the necessary governmental permits and approvals can be a complex and time-consuming process. The failure to obtain or renew the necessary permits or licenses or continue to meet their requirements could delay future development and could increase the costs related to such activities.

The development of all of our company's projects may be delayed due to delays in receiving regulatory permits and approvals, which could impede our company's ability to develop our projects which, absent raising additional capital, could cause it to curtail or discontinue development, if any.

If our company discovers economically mineable mineralized material, our company may experience delays in developing our projects. The timing of development at our projects depends on many factors, some of which are beyond our control, including:

● taxation;

● the timely issuance of permits; and

● the acquisition of surface land and easement rights required to develop and operate our projects, (in particular, our company is required to acquire surface land through expropriation in connection with our mineral concessions).

These delays could increase development costs of our projects, affect our company's economic viability, or prevent our company from completing the development of our projects.

Our company's activities are subject to environmental laws and regulations that may increase our company's costs of doing business and may restrict our operations.

All of our company's exploration activities in Ghana are subject to regulation by governmental agencies under various environmental laws. To the extent our company conducts exploration activities or undertakes new exploration or future mining activities in other foreign countries, our company will also be subject to environmental laws and regulations in those jurisdictions. These laws address emissions into the air, discharges into water, management of waste, management of hazardous substances, protection of natural resources, antiquities and endangered species, and reclamation of lands disturbed by mining operations. Environmental legislation in many countries is evolving and the trend has been towards stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects and increasing responsibility for companies and their officers, directors and employees. Compliance with environmental laws and regulations may require significant capital outlays and may cause material changes or delays in our company's intended activities. Our company cannot assure our stockholders that future changes in environmental regulations will not adversely affect our company's business, and it is possible that future changes in these laws or regulations could have a significant adverse impact on some portion of our company's business, causing our company to re-evaluate those activities at that time.

- 10 -

In addition, our company may be exposed to potential environmental impacts during any full scale mining operation. At such time of commencement of full scale mining, if ever, our company plans to negotiate posting of a reclamation bond to quantify the reclamation costs. Our company anticipates that the dollar amount of reserves established for exposure to environmental liabilities, at December 31, 2022, will be $99,514, as to $34,714 for our Kwabeng project, $23,140 for our Banso and Muoso Projects, and $41,657 for our Pameng project, as estimated to meet the regulatory requirements of the Environmental Protection Agency of Ghana. Our company is currently unable to predict the ultimate cost of compliance or the extent of liability risks.

Our company is unable to predict the remediation costs for potential environmental liabilities.

The costs of remediation may exceed the provision that our company has made for such remediation by a material amount. Whenever a previously unrecognized remediation liability becomes known, or a previously estimated cost is increased, the amount of that liability or additional cost could adversely affect our company's exploration activities and our financial condition. At December 31, 2022, the company had accrued $99,514 for repair of environmental damage during alluvial operations. These costs are supported by the environmental bond of $296,322 posted as required by the Ghanaian government.

There may be instances where certain events occur that our company is not insured against.

Our company maintains insurance policies to protect itself against certain risks related to its operations. This insurance is maintained in amounts that our company believes to be reasonable depending upon the circumstances surrounding each identified risk. However, our company may elect not to have insurance for certain risks because of the high premiums associated with insuring those risks or for various other reasons; in other cases, insurance may not be available for certain risks. Some concern always exists with respect to investments in parts of the world where civil unrest, war, nationalist movements, political violence or economic crisis are possible. These countries may also pose heightened risks of expropriation of assets, business interruption, increased taxation and a unilateral modification of concessions and contracts. Our company does not maintain insurance policies against political risk. Occurrence of events for which our company is not insured could adversely affect our company's exploration activities and its financial condition.

Our company is subject to the potential of legal claims and the associated costs of defense and settlement.

Our company is subject to litigation risks. All industries, including the mining industry, are subject to legal claims, with and without merit. Defense and settlement costs of legal claims can be substantial, even with respect to claims that have no merit. Due to the inherent uncertainty of the litigation process, the resolution of any particular legal proceeding to which our company is or may become subject could have a material effect on its financial position, results of operations or our company's project development operations.

Our company is subject to fluctuations in currency exchange rates, which could materially adversely affect our financial position.

Our company's primary currency for operations is the United States dollar and, to a lesser extent, the "Cedi", the Ghanaian currency and the Canadian dollar. Our company maintains most of its working capital in Canadian dollars. Our company converts its Canadian funds to foreign currencies as certain payment obligations become due. Accordingly, our company is subject to fluctuations in the rates of currency exchange between the United States dollar and these foreign currencies and these fluctuations, which are beyond our control, could materially affect our company's financial position and results of operations. A significant portion of the operating costs of our projects are in Cedi. Our company obtains services and materials and supplies from providers in West Africa. The costs of goods and services could increase or decrease due to changes in the value of the United States dollar or the Cedi or other currencies. Consequently, exploration and development of our projects could be costlier than anticipated.

Our company's business is impacted by any instability and fluctuations in global financial systems.

Any credit crisis and related instability in the global financial system, has had, and may continue to have, an impact on our company's business and our company's financial condition. Our company may face significant challenges if conditions in the financial markets do not continue to improve. Our company's ability to access the capital markets may be severely restricted at a time when our company wishes or needs to access such markets, which could have a materially adverse impact on our company's flexibility to react to changing economic and business conditions or carry on our operations.

Our company is subject to the effects that historically high inflation rate may have on its results.

Our company's mineral properties are located in Ghana, which has historically experienced relatively high rates of inflation. High inflation rates in Ghana could cause the prices of materials obtained within Ghana to be slightly higher. As our company maintains our funds in U.S. and/or Canadian currency, the effect due to Ghanaian currency fluctuations is minimal.

The Government of Ghana has the right to increase its current ownership interest of 10% in our company's subsidiary, Xtra-Gold Mining Limited ("XG Mining"), through which our company holds, among other things, its interest in our Kibi project and our other projects, for a consideration agreed upon by the parties or by arbitration and has a right of pre-emption to purchase all minerals produced by XG Mining. If the Government of Ghana were to exercise any of its rights, our company's results of operations in future periods could be adversely impacted.

- 11 -

The Government of Ghana is granted a 10% free carried interest in all mining operations and has no obligation to contribute to development or operating expenses. The Government of Ghana currently has a 10% free carried interest in XG Mining, one of our Ghanaian subsidiaries that holds all of the mining leases securing our interest in all of the concessions where our projects are located. The Government of Ghana also has:

● the right to acquire an additional interest in XG Mining for a price to be determined by agreement or arbitration;

● the right to acquire a special share (as defined in the Minerals and Mining Act, 2006 (Act 703), as amended by the Minerals and Mining Act, 2010 (Act 794) (the "Mining Act (Ghana)") in XG Mining at any time for such consideration as the Government of Ghana and XG Mining might agree; and

● a right of pre-emption to purchase all minerals raised, won or obtained in Ghana.

While our company is not aware of the Government of Ghana having ever exercised such right of pre-emption, our company cannot assure our stockholders that the Government of Ghana would not seek to exercise one or more of these rights which, if exercised, could have an adverse affect on our company's results of operations in future periods. If the Government of Ghana should exercise its right to either acquire the additional interest in XG Mining or its right to acquire the special share, any profit that might otherwise be reported from XG Mining's operations would be proportionally reduced in the same percentage as the minority interest attributable to the Government of Ghana in that subsidiary would be increased. If the Government of Ghana should exercise its right to purchase all gold and other minerals produced by XG Mining, the price it would pay may be lower than the price our company could sell the gold or other minerals for in transactions with third parties and it could result in a reduction in any revenues our company might otherwise report from XG Mining's operations.

Our company currently relies on the continued services of key executives, including the directors of our company and a small number of highly skilled and experienced executives and personnel. The loss of their services may delay our company's exploration activities or adversely affect our business and future operations.

Due to the relatively small size of our company, the loss of these persons or our company's inability to attract and retain additional highly skilled employees may lead to our company having to delay our exploration activities or adversely affect our business and future operations.

Our company may experience difficulty in engaging the services of qualified personnel in connection with our technical operations at our projects.

If the loss of any of our company's key technical personnel occurs at any of our projects, our company may have difficulty finding qualified replacements. Our company's inability to hire and retain the services of qualified persons for these positions in a timely manner could impede our company's exploration activities at any of our projects which would have a material adverse effect on our company's ability to conduct business.

Our company is subject to changes in political stability in West Africa.

Our company conducts exploration and development activities in Ghana, West Africa. Our company's projects in Ghana may be subject to the effects of political changes, war and civil conflict, changes in government policy, lack of law enforcement and labor unrest and the creation of new laws. These changes (which may include new or modified taxes or other government levies as well as other legislation) may impact the profitability and viability of our properties. The effect of unrest and instability on political, social or economic conditions in Ghana could result in the impairment of exploration, development and mining operations. Any such changes are beyond the control of our company and may adversely affect our business.

In addition, local tribal authorities in West Africa exercise significant influence with respect to local land use, land labor and local security. From time to time, the Government of Ghana has intervened in the export of mineral concentrates in response to concerns about the validity of export rights and payment of duties. No assurances can be given that the co-operation of such authorities, if sought by our company, will be obtained, and if obtained, maintained.

The Government of Ghana also announced that it will be engaging companies to address the issue of dividend payment, exemptions and the mining sector fiscal regime, generally. As a result of these discussions, the Government of Ghana could amend the Mining Act (Ghana) or other regulations resulting in a material adverse impact on our company including increases in operating costs, capital expenditures or abandonment or delays in development of mining properties.

- 12 -

The mining industry is a competitive industry and our company may compete with larger, more established competitors for gold acquisition opportunities.

Significant and increasing competition exists for the limited number of gold acquisition opportunities available. As a result of this competition, some of which is with large established mining companies with substantial capabilities and greater financial and technical resources than our company, our company may be unable to acquire additional attractive mining properties on terms we consider acceptable.

The marketability of our company's minerals may be influenced by various industry conditions.

The marketability of minerals, if any, which may be acquired or discovered by our company, will be affected by numerous factors beyond the control of our company. These factors include market fluctuations, the proximity and capacity of mineral markets and processing equipment and government regulations, including regulations relating to prices, taxes, royalties, land tenure and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in our company not receiving an adequate return on invested capital. The probability of our company not receiving an adequate return on invested capital will be, to a significant extent, dependent upon the market price for gold. Gold prices fluctuate dramatically and are affected by numerous industry factors, such as interest rates, exchange rates, inflation or deflation, fluctuation in the value of the United States dollar and foreign currencies, global and regional supply and demand for precious metals, forward selling by producers, central bank sales and purchases of gold, production and cost levels in major gold producing regions and the political and economic conditions of major gold, copper or other mineral-producing countries throughout the world. Moreover, gold prices are also affected by macro-economic factors such as expectations for inflation, interest rates, currency exchange rates and global or regional political and economic situations. The current demand for, and supply of, gold affects gold prices, but not necessarily in the same manner as current demand and supply affect the prices of other commodities. The potential supply of gold consists of new gold mine production plus existing stocks of bullion and fabricated gold held by governments, financial institutions, industrial organizations and individuals. Since mine production in any single year constitutes a very small portion of the total potential supply of gold, normal variations in current production do not necessarily have a significant effect on the supply of gold or its price.

It may be difficult for our shareholders to enforce any judgment obtained in the United States against us or our officers or directors, which may limit the remedies otherwise available to our shareholders.

The majority of our directors and officers are residents of countries other than the United States and all or a substantial portion of such persons' assets are located outside the United States. As a result, it may be difficult or impossible for our shareholders to:

● effect service of process on our directors or officers, or

● enforce any United States judgment they receive against us or our officers or directors in a foreign court, or including judgments predicated upon the securities laws of the United States or any state thereof. In addition, there is uncertainty as to whether foreign courts would be competent to hear original actions brought in such foreign court against us or such persons predicated upon the securities laws of the United States or any state thereof. Consequently, you may be effectively prevented from pursuing remedies under U.S. federal securities laws against us or our officers and directors. The foregoing risks also apply to those experts identified in this Annual Report that are not residents of the United States.

Risks Relating to our Common Shares

Broker-dealers may be discouraged from effecting transactions in our common shares because they are considered a penny stock and are subject to the penny stock rules.

Rules 15g-1 through 15g-9 promulgated under the Exchange Act impose sales practice and disclosure requirements on certain brokers-dealers who engage in certain transactions involving a "penny stock". Subject to certain exceptions, a penny stock generally includes any equity security not listed on a stock exchange that has a market price of less than $5.00 per share. Our common shares have traded below $5.00 per share throughout its trading history.

A broker-dealer selling penny stock to anyone other than an established customer or "accredited investor", generally, an individual with net worth in excess of $1,000,000 or an annual income exceeding $200,000, or $300,000 together with his or her spouse, must make a special suitability determination for the purchaser and must receive the purchaser's written consent to the transaction prior to sale, unless the broker-dealer or the transaction is otherwise exempt. In addition, the penny stock regulations require the broker-dealer to deliver, prior to any transaction involving a penny stock, a disclosure schedule prepared by the United States Securities and Exchange Commission relating to the penny stock market, unless the broker-dealer or the transaction is otherwise exempt. A broker-dealer is also required to disclose commissions payable to the broker-dealer and the registered representative and current quotations for the securities. Finally, a broker-dealer is required to send monthly statements disclosing recent price information with respect to the penny stock held in a customer's account and information with respect to the limited market in penny stocks. The additional sales practice and disclosure requirements imposed upon broker-dealers may discourage broker-dealers from effecting transactions in our common shares, which could severely limit the market liquidity of our common shares and impede the sale of our common shares in the secondary market.

- 13 -

The price of our common shares is likely to be highly volatile and possibly illiquid, which could cause the value of investments to decline.

The market price of our common shares may be highly volatile and possibly illiquid. Our shareholders may not be able to resell their common shares following periods of volatility because of the market's adverse reaction to volatility. Factors that could cause such volatility may include, among other things:

● actual or anticipated fluctuations in our quarterly operating results;

● large purchases or sales of our common shares;

● additions or departures of key personnel;

● investor perception of our company's business prospects;

● conditions or trends in other industry related companies;

● changes in the market valuations of publicly traded companies in general and other industry-related companies; and

● world-wide political, economic and financial conditions.

The markets for our common shares is limited.

There is currently only a limited trading market for our common shares. Our common shares trade on the OTC Bulletin Board under the symbol "XTGRF" which is a limited market in comparison to the NASDAQ Global Market, the NYSE MKT LLC and other national securities exchanges. Our securities are also listed on the Toronto Stock Exchange (the "TSX") under the trading symbol "XTG". The market for our securities on the TSX commenced in November 2010 and, to date, trading has been limited. There is no assurance that the market for our common shares on the OTC Bulletin Board or TSX will develop into active trading markets.

In connection with future stock offerings, the value of our company's common shares may become diluted as more of our common shares are issued and outstanding.

Our company may undertake in the future additional offerings of our common shares or of securities convertible into our common shares. The increase in the number of our common shares issued and outstanding and the possibility of sales of such common shares may depress the price of our common shares. In addition, as a result of such additional common shares, the voting power of our company's existing shareholders will be diluted.

We are authorized to issue up to 250,000,000 of shares without prior shareholder consent which will be dilutive to our shareholders.

Xtra-Gold is authorized to issue up to 250,000,000 of common shares with a par value of $0.001 of a single class which may be issued by our Board of Directors without further action or approval of our shareholders. While our Board of Directors is required to fulfill its fiduciary obligation in connection with the issuance of such shares, the shares may be issued in transaction with which not all shareholders agree, and the issuance of such shares will cause dilution to the ownership interest of our company's shareholders.

We have never paid cash dividends on our common shares.

We have never paid dividends on our common shares and do not presently intend to pay cash dividends on our common shares. Any future decisions as to the payment of dividends will be at the discretion of our Board of Directors, subject to applicable law.

Risks Related to our Company Post Continuation

In November 2012, as a result of the adoption by our shareholders of certain resolutions, at a special meeting of shareholders held on November 16, 2012 and a plan of conversion (the "Plan of Conversion") under Chapter 92A of the Nevada Revised Statutes filed with the Nevada Secretary of State and the subsequent filing of a memorandum of association and articles of association (the "Memorandum and Articles") with the Registrar of Corporate Affairs in the British Virgin Islands (the "BVI"), both of which were filed on November 30, 2012, we changed the jurisdiction of incorporation of our company from Nevada to the BVI (the "Continuation").

- 14 -

We will still be treated as a U.S. corporation and taxed on our worldwide income after the Continuation.

The Continuation of our company from Nevada to the BVI was for corporate purposes a migration from Nevada to the BVI. Transactions whereby a U.S. corporation migrates to a foreign jurisdiction are considered by the United States Congress to be a potential abuse of the U.S. tax rules because after the migration the foreign entity is not subject to U.S. tax on its worldwide income. As a result, Section 7874(b) of the Code was enacted in 2004 to address this potential abuse. Section 7874(b) of the Code provides generally that a corporation that migrates from the United States will still remain subject to U.S. tax on its worldwide income unless the migrating entity has substantial business activities in the foreign country in which it is migrating when compared to its total business activities.

Section 7874(b) of the Code applies to the migration of our company from Nevada to the BVI, causing our company to be subject to United States federal income taxation on our worldwide income because our company does not have substantial business activities in the BVI when compared to its total business activities. Our administrative functions and our business operations are primarily located outside of the BVI. Substantially, all of our shareholders reside outside of the BVI and historically most of our funds have been raised outside of the BVI. Accordingly, we believe that our company will continue to be treated as a U.S. domestic corporation under Section 7874 of the Code after the Continuation.

Moreover, while we believe we have addressed the material U.S. federal income tax considerations as to the exchange of the shares of common stock of our company, as a Nevada company for shares of our company, as a BVI company pursuant to the Continuation, we cannot assure Holders that we have addressed the material U.S. federal income tax consequences to persons who may be subject to special provisions of the U.S. federal income tax law based on their individual circumstances. Holders should review the discussion under "Material United Federal Tax Consequences" in its entirety, including the definitions of "U.S. Holder" and "Non-U.S. Holder" described therein.

Under the BVI Business Companies Act, 2004 (the "BVI Act"), the number of shareholder votes required to approve certain fundamental matters, including amendments to our articles and business combination transactions, may be less than under Nevada law with the result that these transactions may more easily be approved under the BVI Act than under Nevada law.

Under the BVI Act, shareholder approval by resolution, being a majority approval, is required to approve certain fundamental changes, including amendments to our articles and mergers, which are the equivalent of mergers under Nevada law. Under the BVI Act, the majority approval is determined based upon those shareholders present at the meeting and entitled to vote on the fundamental change. While majority approval is required, the number of shares required may be significantly less than 50% of the outstanding share capital, which is the requirement under Nevada law, due to the fact that the quorum requirement for shareholders meetings is only two individuals present in person, each of whom is a stockholder or a proxyholder entitled to vote at a meeting.

Pursuant to the Memorandum and Articles of our company, our shareholders will have greater rights of dissent, with the result that dissenting shareholders may impede our ability to make fundamental corporate changes or increase the cost to us of making these changes.

Pursuant to our Memorandum and Articles, our shareholders will have the right to dissent when we amend our articles to change any provisions restricting or constraining the issue, transfer or ownership of shares of that class. Our shareholders will also have dissenters' rights when we propose to amend our articles to add, change or remove any restrictions on our business or businesses that we may carry on, merge (other than a vertical short-form merger with a wholly-owned subsidiary), continue to another jurisdiction, sell, lease or exchange all or substantially all of our property, or carry out a going private or squeeze-out transaction. The exercise by shareholders of their dissent and appraisal rights when we attempt to complete any of these fundamental changes could impede our ability to make fundamental corporate changes or increase the cost to us of making these changes.

The stock price of our common shares may be volatile. In addition, demand in the United States for our common shares may be decreased by the change in domicile.

The market price of our common shares may be subject to significant fluctuations in response to variations in results of operations and other factors. Developments affecting the mining industry generally, including general economic conditions and government regulation, could also have a significant impact on the market price for our common shares. In addition, the stock market has experienced a high level of price and volume volatility. Market prices for the stock of many similar companies have experienced wide fluctuations which have not necessarily been related to the operating performance of such companies. These broad market fluctuations, which are beyond our control, could have a material adverse effect on the market price of our common shares. We cannot predict what effect, if any, the Continuation will have on the market price prevailing from time to time or the liquidity of our common shares. The change in domicile may decrease the demand for our common shares in the United States. The decrease may not be offset by increased demand for our common shares in the BVI.

- 15 -

As a reporting issuer under Section 15(d) of the Exchange Act, we file more limited reports with the SEC than do companies who are registered under Section 12(g) of the Exchange Act. As we have elected "foreign private issuer" status following our Continuation into the BVI, our reporting obligations under U.S. securities laws is more limited than if we had remained a domestic issuer. This lack of transparency may make it more difficult for investors in our securities to make informed investment decisions.

While we are subject to Section 15(d) of the Exchange Act, we do not have a class of securities registered under Section 12(g) of the Exchange Act. Consequently, we file more limited reports with the SEC than do companies whose shares are registered under Section 12(g). For example, as a company reporting under Section 15(d) of the Exchange Act, we are not subject to the SEC's proxy rules and our officers, directors and principal shareholders are not required to file reports under Section 16(a) of the Exchange Act, and such persons are not subject to the short-swing profit rules of Section 16(b) of the Exchange Act.

Following our Continuation into the BVI, we have qualified as a foreign private issuer under U.S. securities laws and we have elected foreign private issuer status. While we will remain subject to limited reporting obligations under U.S. federal securities law, as a foreign private issuer:

we are not required to file quarterly reports on Form 10-Q with the SEC; although since our securities are listed on the TSX we are a reporting issuer in Canada and subject to the rules of the Canadian securities administrators (the "CSA") which includes the applicable provincial securities commissions in the provinces of British Columbia, Alberta and Ontario, we will file quarterly reports containing unaudited interim financial statements and MD&A with the CSA via SEDAR (System for Electronic Delivery of Analysis and Retrieval) and, in accordance with SEC rules, post copies of such reports on our website;

we are not required to file current reports on Form 8-K; although we are required to file current reports on Form 6-K but for less mandatory items than are required under Form 8-K, and since our securities are listed on the TSX and subject to the rules of the CSA, we will file material change reports with the CSA via SEDAR and, under SEC rules, post copies of such reports on our website;

our officers, directors and principal shareholders are not subject to Section 16 of the Exchange Act, which otherwise requires them to file ownership reports with the SEC and subjects them to "short-swing" profit liability;

we are not subject to the SEC's proxy rules; and

we are not subject to the provisions of Regulation FD which is designed to prevent selective disclosure of material information.

While we believe that the disclosure requirements of the TSX and the CSA, and SEC regulations applicable to foreign private issuers, will collectively provide transparency to the investment community and allow informed investment decisions to be made by investors in our securities, there is no assurance that the reduced transparency afforded to foreign private issuers will not also reduce the information available to investors and make investment decisions in our securities more difficult.

Item 4 Information on Xtra-Gold

A. History and Development of Xtra-Gold

On November 30, 2012, we completed the Continuation to the BVI which resulted in the change of the jurisdiction of incorporation of our company from Nevada to the BVI.

B. Business Overview

We are engaged in the exploration of gold properties exclusively in Ghana, West Africa in the search for mineral deposits, mineral resources and/or mineral reserves which could be economically and legally extracted or produced. Our exploration activities include the review of existing data, grid establishment, geological mapping, geophysical surveying, trenching and pitting to test the areas of anomalous soil samples and reverse circulation (RC) and/or diamond drilling to test targets followed by infill drilling, if successful, to define a mineral resource and, perhaps ultimately, a mineral reserve.

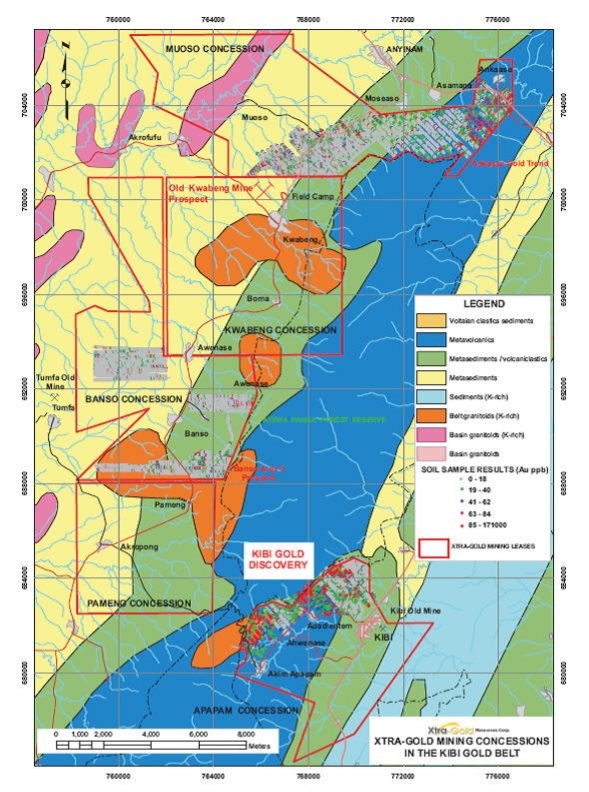

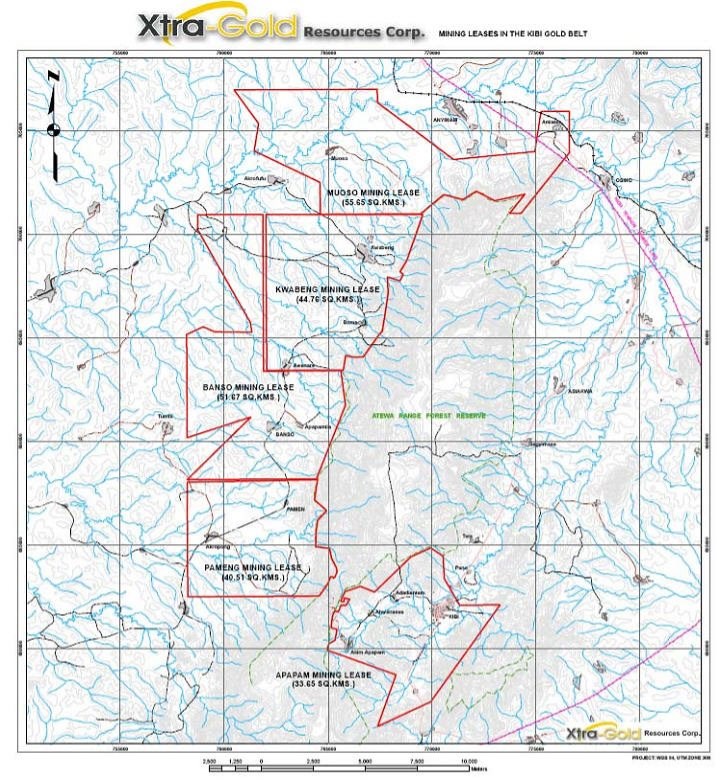

Our mining portfolio currently consists of 225.87 square kilometers comprised of 33.65 square kilometers for our Kibi project, 51.67 square kilometers for our Banso project, 55.28 square kilometers for our Muoso project, 44.76 square kilometers for our Kwabeng project, and 40.51 square kilometers for our Pameng project, or 55,873 acres, pursuant to the leased areas set forth in our mining leases.

- 16 -

Our interests in our projects are held by our Ghanaian subsidiary, XG Mining, through mining leases granted by the Government of Ghana and registered to XG Mining for leased areas located within and upon concessions in Ghana. A concession is a grant of a tract of land made by a government or other controlling authority in exchange for an agreement that the land will be used for a specific purpose. The mining lease areas for our projects total approximately 226 square kilometers and are located at the northern extremity of the Kibi Gold Belt which is a greenstone belt, as defined in all the geological publications in Ghana, and is one of the four main greenstone belts located in Ghana.

Development of our Business During 2022

Exploration activities for the 2022 year continued to focus on the Company's flagship Kibi Gold Project (Apapam Mining Lease) with the continuation of the Zone 3 resource expansion target generation drill program initiated in 2021. Eighty-one (81) diamond core boreholes totalling 15,012 metres ("m") were completed by the Company's in-house drilling crews in 2022, including 62 holes (12,396 m) dedicated to the further delineation of the Boomerang East gold system identified in late 2021. Drilling efforts for the current year also included 16 holes (2,240 m) designed to test structural geology and geophysical targets on the grassroots Cobra Creek (Zone 5) auriferous shear corridor prospect.

We did not conduct any field exploration activities on our Kwabeng, Pameng, Banso and Muoso projects during the 2022 year.

As at the date of this annual report, we have the following five projects all of which are in the exploration stage.

Kibi Project. Our flagship Kibi Gold Project is located on the Apapam concession and is our only material project.

The present Boomerang East drilling work forms part of an exploration initiative targeting resource expansion opportunities along the southwestern (Zone 3) segment of the over three-kilometre-long Zone 2 - Zone 3 anticlinal fold structure; stretching over one kilometre beyond the limits of the current Mineral Resource footprint area. Drill results for a total of 90 holes (15,551.5 m) have been reported to date for the ongoing Zone 3 resource expansion drill program initiated following the database close-out date for the current resource estimate.

The current Mineral Resource Estimate for the Kibi Gold Project, with an effective date of September 30, 2021, encompasses eight (8) gold deposits lying within approximately 1.6 kilometres of each other, estimated to contain an Indicated Mineral Resource of 623,700 ounces of gold based on 13,893,000 tonnes at an average grade of 1.40 grams per tonne ("g/t") gold and an additional Inferred Mineral Resource of 180,700 ounces of gold based on 5,694,000 tonnes at an average grade of 0.96 g/t gold (at a base case 0.5 g/t cut-off). The Mineral Resource Estimate was filed in accordance with National Instrument 43-101 (NI 43-101) requirements with the Technical Report entitled "Xtra-Gold Resources Corporation Kibi Gold Project", jointly prepared by Pivot Mining Consultants (Pty) Ltd and Tect Geological Consulting of Johannesburg and Somerset West, South Africa, respectively, and dated November 16, 2021, filed under the Company's profile on SEDAR at www.sedar.com.

Gold mineralization within the resource footprint area consists predominantly of tensional arrays of auriferous quartz-carbonate veins hosted by folded diorite bodies with an interpreted Belt-type granitoid affinity. The gold-bearing zones occupy the hinges and limbs of predominantly anticlinal fold structures. Over 20 significant gold occurrences hosted by Belt (Dixcove)- and Basin (Cape Coast)-type granitoids are known in Ghana, with a number constituting significant deposits. These deposits represent a relatively new style of gold mineralization for orogenic gold deposits within the West African Birimian terrain. Belt-type intrusion-hosted gold deposits include Newmont Mining's Subika deposit at their Ahafo mine and Asante Gold's Chirano deposit (formerly Kinross Mining) within the Sefwi gold belt, as well as the former Golden Star Resources' Hwini-Butre deposit at the southern extremity of the Ashanti gold belt.

Cautionary Note on Mineral Resources: Mineral Resources are not Mineral Reserves and by definition do not demonstrate economic viability. The Mineral Resource Estimate disclosed herein includes Inferred Mineral Resources that are normally considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as Mineral Reserves. There is also no certainty that these Inferred Mineral Resources will be converted to the Measured and Indicated resource categories through further drilling, or into Mineral Reserves, once economic considerations are applied. The stated figures for contained gold are in-situ Mineral Resources.

Drilling activities on the Kibi Gold Project for the 2022 year primarily targeted resource expansion opportunities along the southwestern (Zone 3) segment of the over three-kilometre-long Zone 2 - Zone 3 anticlinal fold structure, including: 62 holes (12,396 m) dedicated to the further delineation of the Boomerang East gold system identified in late 2021; and three scout holes (376 m) to test prospective litho-structural gold settings. The assay results for 50 boreholes (10,135 m) completed from January to mid-November 2022 on the Boomerang East gold system were reported by the Company on February 18, June 23, September 27 and December 21, 2022, including the following highlights:

- 17 -

Boomerang East: Upper Shoot (s)

- 16.5 metres ("m") at 6.23 grams per tonne gold ("g/t Au"), including 6.5 m at 13.74 g/t Au, from 1.5 m in hole KBDD22455

- 11.3 m at 2.41 g/t Au, including 6.0 m at 3.40 g/t Au, from 11.0 m in hole KBDD22464

- 9.1 m at 1.21 g/t Au from 93.9 m in hole KBDD22469; followed by second interval of 16.3 m at 2.06 g/t Au from 141.7 m, including 5.7 m at 3.10 g/t Au

- 13.5 m at 3.20 g/t Au from 37.0 m in hole KBDD22478

Boomerang East: Lower Shoot (main gold zone)

- 77.0 m at 1.59 g/t Au, including 31.0 m at 3.23 g/t Au, from 122.0 m in hole KBDD22481

- 46.0 m at 1.39 g/t Au, including 20.0 m at 2.01 g/t Au, from 127.0 m in hole KBDD22475

- 43.0 m at 1.57 g/t Au, including 13.0 m at 3.21 g/t Au, from 52.0 m in hole KBDD22480

- 50.0 m at 1.35 g/t Au from 180.2 m in hole KBDD22484

- 45.0 m at 1.32 g/t Au, including 21.0 m at 2.03 g/t Au, from 12.0 m in hole KBDD22485

- 33.0 m at 1.76 g/t Au, including 15.0 m at 2.48 g/t Au, from 233.0 m in hole KBDD22463

Footwall Shoot (in footwall of main Lower Shoot gold zone)

- 22.0 m at 2.40 g/t Au, including 7.0 m at 5.35 g/t Au, from 226.0 m in KBDD22497

- 19.0 m at 0.76 g/t Au, including 7.0 m at 1.70 g/t Au, from 313.0 m in KBDD22495

Current 3D litho-structural modelling indicates that the Boomerang East gold system is emplaced within the inner arc of a tight, moderate NE-plunging, isoclinally folded diorite body. The mineralization appears to occur as a system of stacked, flat-lying to concave-shaped, NE-plunging gold shoots occupying the apparent fold hinge of the NE-trending Zone 2 - Zone 3 anticlinal fold structure.

Drilling to date has outlined three (3) principal gold shoots, including the Upper Shoot (s), the Lower Shoot, and the Footwall Shoot, across an approximately 250 m cross-plunge distance. The Lower Shoot, presently the most prominent mineralization shoot of the Boomerang East gold system, has so far been delineated from practically surface to a down-plunge depth of approximately 400 m along the fold hinge structure (approximately 275 m vertical depth from surface), and across an approximately 175 m NW-SE lateral distance. With the recently identified Footwall Shoot, a parallel mineralization zone lying approximately 25 m - 45 m below the main Lower Shoot gold zone (i.e., in the footwall), traced to date along the entire, approximately 400 m plunge-length of the Lower Shoot, and across an approximately 50 m - 150 m lateral distance.

Drilling efforts for the 2022 year also included 16 holes (2,240 m) on the grassroots Cobra Creek (Zone 5) target; an approximately 550 m wide, NE-trending, quartz-feldspar porphyry ("QFP") hosted, multi-structure braided shear zone system traced by trenching / outcrop stripping over an approximately 850 m strike length. Xtra-Gold undertook a 43 borehole (2,639 m) Phase I diamond core drill program on the Cobra Creek gold zone in 2016. Initial drilling efforts yielded some very exploration significant high-grade mineralized intercepts, including highlights of 4.5 m grading 10.9 g/t Au and 5.2 m grading 9.51 g/t Au (see the Company's news release of October 19, 2016).

The 2022 Cobra Creek exploration drilling program included: 8 holes (774 m) designed to better target / dissect flat-lying to shallow dipping gold-bearing extensional veining arrays and/or shallow plunging auriferous shoots; and 8 scout holes (1,466 m) targeting high-priority induced polarization (IP) / resistivity anomalies along the southeastern margin and projected southwestern extension of the QFP body.

Mineralized intercept highlights for the 8 holes targeting the down-plunge extensions of veining arrays and/or shallow plunging shoots, include: 10.4 m grading 2.0 g/t Au, including 10.05 g/t Au over 1.0 m, from 18.0 m in hole #CCDD22044; 16.9 m grading 1.61 g/t Au and 2.0 m grading 4.63 g/t Au from 25.1 m and 57.0 m respectively in #CCDD22047; 8.0 m grading 2.05 g/t Au, including 6.5 g/t Au over 1.0 m, from 10.0 m in #CCDD22048; and 4.0 m grading 4.44 g/t Au from 24.0 m in #CCDD22054. None of the 8 scout holes targeting geophysical targets returned any significant auriferous intercepts.

- 18 -

In late March, also in relation to our Kibi Gold Project, Xtra-Gold engaged TechnoImaging LLC ("TechnoImaging") of Salt Lake City, Utah, USA to undertake 3D geophysical modelling of an approximately 70 km2 subset area (585 line-km) of the Company's regional helicopter-borne VTEM - Mag survey, completed by Geotech Airborne Limited in 2011, to help identify prospective litho-structural gold setting targets. The geophysical modelling work included 3D joint inversion for conductivity and chargeability of the VTEM survey data, as well as 3D inversion of the Total Magnetic Intensity (TMI) to magnetic susceptibility and magnetization vector models. The Company received the final product of the TechnoImaging geophysical modelling work in mid-July and study result compilation is currently ongoing.

In mid-November, Xtra-Gold commissioned Tect Geological Consulting of West Somerset, South Africa ("Tect") to conduct an updated structural analysis of the Zone 2 - Zone 3 resource footprint area of the Kibi Gold Project. The detailed 3D litho-structural modelling work, encompassing an additional 90 drill holes (15,551.5 m) completed since the database close-out date for the current resource estimate, in combination with the 3D VTEM / TMI inversion models produced by TechnoImaging, was undertaken to further define the structural controls of the gold mineralization and to generate high-priority exploration targets to help guide ongoing resource expansion drilling efforts. The Company received the final product of the updated structural study from Tect in mid-February 2023, and study result compilation is currently ongoing.

As at the date of this annual report, during 2023, we plan to conduct:

● follow-up trenching of Zone 1 - Zone 2 - Zone 3 early stage gold shoots / showings to guide future mineral resource expansion drilling efforts;

● prospecting, reconnaissance geology, hand augering and/or scout pitting, and trenching of high priority gold-in-soil anomalies and grassroots gold targets across the extent of the Apapam concession; and

● a diamond core drill program of approximately 15,000 metres, at an estimated cost of $850,000, to be implemented utilizing the Company's in-house operated drill rigs; consisting of a combination of expansion drilling of newly emerging gold shoots and scout drilling of prospective litho-structural gold settings within the mineral resource footprint area; and scout drilling of new grassroots gold targets across the Apapam concession.

Kwabeng Project. Our Kwabeng project is located on the Kwabeng concession.

During the fiscal year for which this annual report is being filed, lode gold exploration activity on the Kwabeng project was limited to geological / geophysical compilation to identify and/or further define grassroots targets.

See "Kwabeng Project - Prior Exploration by Xtra-Gold" for exploration activities conducted by our company during the two years preceding the fiscal year.

As at the date of this annual report, during 2023, we plan to conduct:

● ongoing geological compilation, prospecting, soil geochemical sampling, hand augering and/or scout pitting, and trenching to identify and/or further advance grassroots targets; and

● the continuation of placer gold recovery operations at this project (commenced in March 2013).

Pameng Project. Our Pameng project is located on the Pameng concession.

During the fiscal year for which this annual report is being filed, lode gold exploration activity on the Pameng project was limited to geological / geophysical compilation to identify and/or further define grassroots targets.

As of the date of this annual report, during 2023, we plan to conduct an exploration program consisting of:

● ongoing geological compilation, prospecting, soil geochemical sampling, hand augering and/or scout pitting, and trenching to identify and/or further advance grassroots targets.

Banso Project. Our Banso project is located on the Banso concession.

During the fiscal year for which this annual report is being filed, lode gold exploration activity on the Banso project was limited to geological / geophysical compilation to identify and/or further define grassroots targets.

We did not conduct any exploration work on the Banso project during the two years preceding the fiscal year.

- 19 -

As of the date of this annual report, during 2023, we plan to conduct an exploration program consisting of:

● ongoing geological compilation, prospecting, soil geochemical sampling, hand augering and/or scout pitting, and trenching to identify and/or further advance grassroots targets; and

● the continuation of placer gold recovery operations at these projects (commenced in 2015).

Muoso Project. Our Muoso project is located on the Muoso concession.

During the fiscal year for which this annual report is being filed, lode gold exploration activity on the Muoso project was limited to geological / geophysical compilation to identify and/or further define grassroots targets.

We did not conduct any exploration work on the Muoso project during the two years preceding the fiscal year.

As of the date of this annual report, during 2023, we plan to conduct an exploration program consisting of:

● ongoing geological compilation, prospecting, soil geochemical sampling, hand augering and/or scout pitting, and trenching to identify and/or further advance grassroots targets; and

● the continuation of placer gold recovery operations at these projects (commenced in 2015).

As at the date of this annual report, we have estimated $500,000 for the cost for soil sampling, hand augering and/or scout pitting, and trenching at our Kibi, Kwabeng, Pameng, Banso and Muoso projects in 2023. We estimate a cost of $850,000 to complete a 15,000-metre drill program at Kibi in 2023.

Gold Recovery Operations. We continued with placer gold recovery operations at our Kwabeng, Pameng Banso and Muoso projects during the fiscal year. We recovered 4,037 ounces of raw placer gold (Kwabeng - 688 ounces, Pameng - 1,970 ounces, Banso - 829 ounces, and Muoso - 550 ounces) and sold 3,778 ounces of fine gold for net proceeds of $3,704,167. As at the date of this annual report, during 2022, we plan to continue placer gold recovery operations at these projects.

Net proceeds from gold recoveries to the end of 2022, from all properties, amounted to $28,566,568.

As of the date of this annual report, we have:

● have achieved a series of losses since inception, although we reported a profit in 2022, 2021, and 2020;

● have minimal operations, and

● relied upon the sale of our securities and the proceeds derived from our recovery of placer gold operations to fund our operations.

Principal Capital Expenditures/Divestitures over the last Three Fiscal Years

Our company has not had any principal capital expenditures or divestitures over the last three fiscal years. We purchased a new pickup truck and a third drill in 2022. We purchased three new pickup trucks in 2021. We purchased a second exploration drill, a bulldozer, a genset, and three new pickup trucks in 2020.

C. Organizational Structure

The following organization chart sets forth our significant subsidiaries.

- 20 -