UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

For the quarterly period ended | ||

OR | ||

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

For the transition period from to

Commission file number:

(Exact Name of Registrant as Specified in its Charter) |

| ||

(State of other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

|

| |

| ||

(Address of Principal Executive Offices) |

| (Zip Code) |

(

(Registrant’s Telephone Number, including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

TBR | OTCQB TSX-V |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large Accelerated Filer | ☐ | Accelerated Filer | ☐ |

☒ | Small Reporting Company | ||

|

| Emerging Growth Company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

Number of shares of issuer’s common stock outstanding at May 15, 2024:

INDEX

| 2 |

| Table of Contents |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 (“Securities Act”) and Section 21E of the Securities Exchange Act of 1934 (“Exchange Act”) and the United States (“U.S.”) Private Securities Litigation Reform Act of 1995 regarding our business, financial condition, results of operations and prospects. All statements other than statements of historical fact included in and incorporated by reference into this report are “forward-looking statements”. Forward- looking statements can be identified by terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continues” or the negative of these terms or other comparable terminology. Forward-looking statements including, among other things, statements regarding our anticipated near-term capital needs, our ability to fund planned activities and potential sources of capital; information regarding the Eureka Property, including the estimates included in our mineral resource estimate and initial technical report summary; our plans regarding further advancement of the Eureka project; the potential impacts of entering into the Merger Agreement with McEwen Mining Inc.; and statements concerning our financial condition, business strategies and business and legal risks and our financial outlook for fiscal 2024, including anticipated expenditures and cash inflows during the year.

The above statements are not the exclusive means of identifying forward-looking statements herein. Although forward-looking statements contained in this report reflect our good faith judgment, such statements can only be based on facts and factors currently known to us. Forward-looking statements are always subject to risks and uncertainties, and become subject to greater levels of risk and uncertainty as they address matters further into the future.

Important factors that could cause actual results to differ materially from the forward-looking statements include, but are not limited to: inability to satisfy the closing conditions in connection with the proposed McEwen merger; unexpected changes in business and economic conditions; significant increases or decreases in gold prices; changes in interest and currency exchange rates; unanticipated grade changes; metallurgy, processing, access, availability of materials, equipment, supplies and water; results of current and future exploration and production activities; local and community impacts and issues; timing of receipt and maintenance of government approvals; accidents and labor disputes; environmental costs and risks; competitive factors, including competition for property acquisitions; and availability of external financing at reasonable rates or at all, and those set forth under Item 1A, Risk Factors of the Company’s Annual Report on Form 10-K/A for the year ended September 30, 2023 filed with the United States Securities and Exchange Commission (the “SEC”) on January 17, 2024.

Although the Company believes that the expectations reflected in the forward-looking statements are reasonable, it cannot guarantee future results, levels of activity, performance or achievements. Forward-looking statements are made based on management’s beliefs, estimates, and opinions on the date the statements are made, and the Company undertakes no obligation to update such forward-looking statements if these beliefs, estimates, and opinions should change, except as required by law.

| 3 |

| Table of Contents |

PART I — FINANCIAL INFORMATION

ITEM 1. CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

TIMBERLINE RESOURCES CORPORATION AND SUBSIDIARIES

Contents |

Page | |

|

|

FINANCIAL STATEMENTS (UNAUDITED): |

|

|

|

5 | |

|

|

6 | |

|

|

Condensed consolidated statements of changes in stockholders’ equity | 7 |

|

|

8 | |

|

|

9 - 12 |

| 4 |

| Table of Contents |

TIMBERLINE RESOURCES CORPORATION AND SUBSIDIARIES | ||||||||

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED) | ||||||||

|

|

|

|

| ||||

|

| March 31, 2024 |

|

| September 30, 2023 |

| ||

ASSETS |

|

|

|

|

|

| ||

CURRENT ASSETS: |

|

|

|

|

|

| ||

Cash |

| $ |

|

| $ |

| ||

Prepaid expenses and other current assets |

|

|

|

|

|

| ||

TOTAL CURRENT ASSETS |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

Property, mineral rights, and equipment, net |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

OTHER ASSETS: |

|

|

|

|

|

|

|

|

Reclamation bonds |

|

|

|

|

|

| ||

Deposits and other assets |

|

|

|

|

|

| ||

TOTAL OTHER ASSETS |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

TOTAL ASSETS |

| $ |

|

| $ |

| ||

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS' EQUITY |

|

|

|

|

|

|

|

|

CURRENT LIABILITIES: |

|

|

|

|

|

|

|

|

Accounts payable |

| $ |

|

| $ |

| ||

Accrued expenses |

|

|

|

|

|

| ||

Accrued payroll, benefits and taxes |

|

|

|

|

|

| ||

TOTAL CURRENT LIABILITIES |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

LONG-TERM LIABILITIES: |

|

|

|

|

|

|

|

|

Asset retirement obligation |

|

|

|

|

|

| ||

TOTAL LONG-TERM LIABILITIES |

|

|

|

|

|

| ||

TOTAL LIABILITIES |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

COMMITMENTS AND CONTINGENCIES (Note 7) |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

STOCKHOLDERS' EQUITY: |

|

|

|

|

|

|

|

|

Preferred stock, $ |

|

|

|

|

|

| ||

Common stock, $ |

|

|

|

|

|

| ||

Additional paid-in capital |

|

|

|

|

|

| ||

Accumulated deficit |

|

| ( | ) |

|

| ( | ) |

TOTAL STOCKHOLDERS' EQUITY |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY |

| $ |

|

| $ |

| ||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 5 |

| Table of Contents |

TIMBERLINE RESOURCES CORPORATION AND SUBSIDIARIES CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED) |

|

|

|

|

| |||||||||||

|

|

|

|

|

|

| ||||||||||

|

| Three months ended March 31, |

|

| Six months ended March 31, |

| ||||||||||

|

| 2024 |

|

| 2023 |

|

| 2024 |

|

| 2023 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

OPERATING EXPENSES: |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Mineral exploration |

| $ |

|

| $ |

|

| $ |

|

| $ |

| ||||

Salaries and benefits |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Professional fees |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Insurance expense |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Other general and administrative |

|

|

|

|

|

|

|

|

|

|

|

| ||||

TOTAL OPERATING EXPENSES |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LOSS FROM OPERATIONS |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

OTHER INCOME (EXPENSE): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign exchange gain |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Interest expense – related party |

|

|

|

|

| ( | ) |

|

|

|

|

| ( | ) | ||

Interest expense |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

Other income |

|

|

|

|

|

|

|

|

|

|

|

| ||||

TOTAL OTHER INCOME (EXPENSE) |

|

|

|

|

| ( | ) |

|

|

|

|

| ( | ) | ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LOSS BEFORE INCOME TAXES |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INCOME TAX PROVISION (BENEFIT) |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NET LOSS |

| $ | ( | ) |

| $ | ( | ) |

| $ | ( | ) |

| $ | ( | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NET LOSS PER SHARE BASIC AND DILUTED |

| $ | (nil) |

|

| $ | (nil) |

|

| $ | (nil) |

|

| $ | (0.01 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

WEIGHTED AVERAGE NUMBER OF COMMON SHARES OUTSTANDING, BASIC AND DILUTED |

|

|

|

|

|

|

|

|

|

|

|

| ||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 6 |

| Table of Contents |

TIMBERLINE RESOURCES CORPORATION AND SUBSIDIARIES CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY (UNAUDITED) | ||||||||||||||||||||

|

|

|

|

|

| Additional |

|

|

|

|

| Total |

| |||||||

|

| Common Stock |

|

| Paid-in |

|

| Accumulated |

|

| Stockholders’ |

| ||||||||

|

| Shares |

|

| Amount |

|

| Capital |

|

| Deficit |

|

| Equity |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Balance, September 30, 2023 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

| ||||

Stock based compensation |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Common stock and warrants issued for cash |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Net loss |

|

| - |

|

|

|

|

|

|

|

|

| ( | ) |

|

| ( | ) | ||

Balance December 31, 2023 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

| ||||

Net loss |

|

| - |

|

|

|

|

|

|

|

|

| ( | ) |

|

| ( | ) | ||

Balance March 31, 2024 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

| ||||

|

|

|

|

|

| Additional |

|

|

|

| Total |

| ||||||||

|

| Common Stock |

|

| Paid-in |

|

| Accumulated |

|

| Stockholders’ |

| ||||||||

|

| Shares |

|

| Amount |

|

| Capital |

|

| Deficit |

|

| Equity |

| |||||

Balance, September 30, 2022 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

| ||||

Stock based compensation |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Net loss |

|

| - |

|

|

|

|

|

|

|

|

| ( | ) |

|

| ( | ) | ||

Balance, December 31, 2022 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

| ||||

Stock based compensation |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Net loss |

|

| - |

|

|

|

|

|

|

|

|

| ( | ) |

|

| ( | ) | ||

Balance, March 31, 2023 |

|

|

|

| $ |

|

| $ |

|

| $ | ( | ) |

| $ |

| ||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 7 |

| Table of Contents |

TIMBERLINE RESOURCES CORPORATION AND SUBSIDIARIES CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED) | ||||||||

|

| Six months Ended March 31, |

| |||||

|

| 2024 |

|

| 2023 |

| ||

CASH FLOWS FROM OPERATING ACTIVITIES: |

|

|

|

|

|

| ||

Net loss |

| $ | ( | ) |

| $ | ( | ) |

Adjustments to reconcile net loss to net cash used by operating activities: |

|

|

|

|

|

|

|

|

Stock-based compensation |

|

|

|

|

|

| ||

Accretion of asset retirement obligation |

|

|

|

|

|

| ||

Changes in assets and liabilities: |

|

|

|

|

|

|

|

|

Prepaid expenses and other current assets |

|

| ( | ) |

|

| ( | ) |

Deposits and other assets |

|

|

|

|

|

| ||

Accounts payable |

|

| ( | ) |

|

| ( | ) |

Accrued expenses |

|

|

|

|

| ( | ) | |

Accrued interest – related party |

|

|

|

|

|

| ||

Accrued payroll, benefits and taxes |

|

|

|

|

| ( | ) | |

Net cash used by operating activities |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

CASH FLOWS FROM INVESTING ACTIVITIES: |

|

|

|

|

|

|

|

|

Payments for mineral rights |

|

| ( | ) |

|

| ( | ) |

Purchase of mineral rights |

|

|

|

|

| ( | ) | |

Net cash used by investing activities |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

CASH FLOWS FROM FINANCING ACTIVITIES: |

|

|

|

|

|

|

|

|

Proceeds from sale of common stock and warrants |

|

|

|

|

|

| ||

Net cash provided by financing activities |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

Net decrease in cash and cash equivalents |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

CASH AT BEGINNING OF PERIOD |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

CASH AT END OF PERIOD |

| $ |

|

| $ |

| ||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 8 |

| Table of Contents |

TIMBERLINE RESOURCES CORPORATION AND SUBSIDIARIES NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS March 31, 2024 (Unaudited) |

NOTE 1 – ORGANIZATION AND DESCRIPTION OF BUSINESS:

Timberline Resources Corporation (“Timberline” or the “Company”) was incorporated in August of 1968 under the laws of the State of Idaho as Silver Crystal Mines, Inc., for the purpose of exploring for precious metal deposits and advancing them to production. In 2008, the Company reincorporated into the State of Delaware, pursuant to a merger agreement approved by its shareholders.

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES:

a. Basis of Presentation and Going Concern – The unaudited condensed consolidated financial statements have been prepared by the Company in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information, as well as the instructions to Form 10-Q. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of the Company’s management, all adjustments (consisting of only normal recurring accruals) considered necessary for a fair statement of the interim condensed consolidated financial statements have been included. Operating results for the six-month period ended March 31, 2024 are not necessarily indicative of the results that may be expected for the fiscal year ending September 30, 2024.

For further information refer to the consolidated financial statements and footnotes thereto in the Company’s Annual Report on Form 10-K for the year ended September 30, 2023.

The accompanying condensed consolidated financial statements have been prepared under the assumption that the Company will continue as a going concern. The Company has incurred losses since its inception. The Company does not have sufficient cash to fund normal operations and meet all of its obligations for the next 12 months without raising additional funds. In connection with the Merger described in Note 8 - Subsequent Events, the Company entered into a bridge financing with McEwen Mining Inc. pursuant to which McEwen has agreed to provide Loans totaling approximately $

b. New Accounting Pronouncements –In August 2023, the Financial Accounting Standards Board issued Accounting Standards Update (“ASU”) 2023-05, Business Combinations - Joint Venture Formations (Subtopic 805-60): Recognition and Initial Measurement, which clarifies the business combination accounting for joint venture formations. The amendments in the ASU seek to reduce diversity in practice that has resulted from a lack of authoritative guidance regarding the accounting for the formation of joint ventures in separate financial statements. The amendments also seek to clarify the initial measurement of joint venture net assets, including businesses contributed to a joint venture. The guidance is applicable to all entities involved in the formation of a joint venture. The amendments are effective for all joint venture formations with a formation date on or after January 1, 2025. Early adoption and retrospective application of the amendments are permitted. We do not expect adoption of the new guidance to have a material impact on our consolidated financial statements and disclosures.

In November 2023, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update 2023-07 (“ASU 2023-07”), Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures, amending reportable segment disclosure requirements to include disclosure of incremental segment information on an annual and interim basis. Among the disclosure enhancements are new disclosures regarding significant segment expenses that are regularly provided to the chief operating decision-maker and included within each reported measure of segment profit or loss, as well as other segment items bridging segment revenue to each reported measure of segment profit or loss. The amendments in ASU 2023-07 are effective for fiscal years beginning after December 15, 2023, and for interim periods within fiscal years beginning after December 15, 2024, and are applied retrospectively. Early adoption is permitted. We are currently evaluating the impact of this update on our consolidated financial statements and disclosures.

In December 2023, the FASB issued Accounting Standards Update 2023-09 (“ASU 2023-09”), Income Taxes (Topic 740): Improvement to Income Tax Disclosures, amending income tax disclosure requirements for the effective tax rate reconciliation and income taxes paid. The amendments in ASU 2023-09 are effective for fiscal years beginning after December 15, 2024, and are applied prospectively. Early adoption and retrospective application of the amendments are permitted. We are currently evaluating the impact of this update on our consolidated financial statements and disclosures.

Other accounting standards that have been issued or proposed by FASB that do not require adoption until a future date are not expected to have a material impact on the consolidated financial statements upon adoption.

| 9 |

| Table of Contents |

TIMBERLINE RESOURCES CORPORATION AND SUBSIDIARIES NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS March 31, 2024 (Unaudited) |

c. Principles of Consolidation – The condensed consolidated financial statements include the accounts of the Company and its wholly owned subsidiaries, BH Minerals USA, Inc.; Wolfpack Gold (Nevada) Corp.; Staccato Gold Resources, Ltd.; Lookout Mountain LLC, and Talapoosa Development Corp., after elimination of intercompany accounts and transactions.

d. Net Income (Loss) per Share – Basic earnings per share (“EPS”) is computed as net income (loss) available to common shareholders divided by the weighted-average number of common shares outstanding for the period. Diluted EPS reflects the potential dilution that could occur from common shares issuable through stock options, warrants, and other convertible securities.

The dilutive effect of outstanding securities as of March 31, 2024 and 2023 is as follows:

|

| March 31, 2024 |

|

| March 31, 2023 |

| ||

Stock options |

|

|

|

|

|

| ||

Warrants |

|

|

|

|

|

| ||

Total potential dilution |

|

|

|

|

|

| ||

At March 31, 2024 and 2023, the effect of the Company’s common stock equivalents would have been anti-dilutive.

NOTE 3 – PROPERTY, MINERAL RIGHTS, AND EQUIPMENT:

The following is a summary of property, mineral rights, and equipment and accumulated depreciation at March 31, 2024 and September 30, 2023, respectively:

|

| Expected Useful Lives (years) |

|

| March 31, 2024 |

|

| September 30, 2023 |

| |||

|

|

|

|

|

|

|

|

|

| |||

Mineral rights – Eureka |

|

| - |

|

| $ |

|

| $ |

| ||

Mineral rights – Seven Troughs, New York Canyon and other |

|

| - |

|

|

|

|

|

|

| ||

ARO Asset |

|

|

|

|

|

|

|

|

|

| ||

Total mineral rights |

|

|

|

|

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

|

|

|

|

Equipment and vehicles |

|

|

|

|

|

|

|

| ||||

Office equipment and furniture |

|

|

|

|

|

|

|

| ||||

Land |

|

| - |

|

|

|

|

|

|

| ||

Total property and equipment |

|

|

|

|

|

|

|

|

|

| ||

Less accumulated depreciation |

|

|

|

|

|

| ( | ) |

|

| ( | ) |

Property, mineral rights, and equipment, net |

|

|

|

|

| $ |

|

| $ |

| ||

Mineral rights at Eureka increased by $

NOTE 4 – RELATED PARTY PAYABLE:

The Company has accrued amounts to the Company’s Chief Executive Officer and Vice President of Exploration for amounts earned but not yet paid. Beginning in July 2023 and through March 31, 2024, the salaries have not been paid in full and at March 31, 2024, $

| 10 |

| Table of Contents |

TIMBERLINE RESOURCES CORPORATION AND SUBSIDIARIES NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS March 31, 2024 (Unaudited) |

NOTE 5 – COMMON STOCK, WARRANTS AND PREFERRED STOCK:

On December 28, 2023, the Company closed a non-brokered private placement to accredited investors at a price of $

During the six months ended March 31, 2024,

At March 31, 2024, the Company has a total of

NOTE 6 – STOCK-BASED AWARDS:

On

The following is a summary of options issued and outstanding:

|

| Options |

|

| Weighted Average Exercise Price |

| ||

Outstanding at September 30, 2022 |

|

|

|

|

|

| ||

Granted |

|

| - |

|

|

|

| |

Expired |

|

| ( | ) |

|

| (0.18 | ) |

Outstanding at September 30, 2023 |

|

|

|

| $ |

| ||

Granted |

|

| - |

|

|

|

| |

Expired |

|

| ( | ) |

|

| ( | ) |

Outstanding at March 31, 2024 |

|

|

|

|

|

| ||

Outstanding and exercisable at March 31, 2024 |

|

|

|

| $ |

| ||

Weighted average remaining contractual term (years) |

|

|

|

|

|

|

| |

The aggregate of options exercisable as of March 31, 2024 had no intrinsic value, based on the closing price of $

NOTE 7 – COMMITMENTS AND CONTINGENCIES:

The Company has the following commitments and contingencies:

Mineral Exploration

A portion of the Company’s mining claims on the Company’s properties are subject to lease and option agreements including advance minimum royalty payments, with various terms, obligations, and royalties payable in certain circumstances.

The Company pays federal and county claim maintenance fees on unpatented claims that are included in the Company’s mineral exploration properties. Should the Company continue to explore all of the Company’s mineral properties, it estimates annual fees to total $

| 11 |

| Table of Contents |

TIMBERLINE RESOURCES CORPORATION AND SUBSIDIARIES NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS March 31, 2024 (Unaudited) |

NOTE 8 – SUBSEQUENT EVENTS:

On April 16, 2024, the Company entered into an Agreement and Plan of Merger (the “Merger Agreement”) with McEwen Mining Inc., a Colorado corporation (“McEwen”), and Lookout Merger Sub, Inc., a Delaware corporation and direct subsidiary of McEwen (“Merger Sub”). The Merger Agreement provides that, among other things and subject to the terms and conditions of the Merger Agreement, Merger Sub will merge with and into the Company, with the Company surviving and continuing as the surviving corporation as a direct, wholly owned subsidiary of McEwen (such transaction, the “Merger”).

At the effective date of the Merger, each outstanding share of common stock of the Company will be converted into the right to receive 0.01 of a share of common stock of McEwen. The Company will call a special meeting of its stockholders to consider and approve the Merger. If approved by the Company’s stockholders, the Merger is expected to be consummated in the third calendar quarter of 2024.

Bridge Financing

In connection with the Merger Agreement, on April 16, 2024, the Company and McEwen entered into a Note whereby McEwen will provide the Company with loans totaling approximately $

| 12 |

| Table of Contents |

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

As used in herein, the terms “Timberline,” the “Company,” “we,” “us,” and “our” refer to Timberline Resources Corporation.

This discussion and analysis should be read in conjunction with the accompanying unaudited consolidated financial statements and related notes. The discussion and analysis of the financial condition and results of operations are based upon the unaudited condensed consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires the Company to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of any contingent liabilities at the financial statement date and reported amounts of revenue and expenses during the reporting period. On an on-going basis the Company reviews its estimates and assumptions. The estimates were based on historical experience and other assumptions that the Company believes to be reasonable under the circumstances. Actual results are likely to differ from those estimates under different assumptions or conditions, but the Company does not believe such differences will materially affect our condensed consolidated financial position or results of operations. Critical accounting policies, the policies the Company believes are most important to the presentation of its consolidated financial statements and require the most difficult, subjective and complex judgments are outlined below in “Critical Accounting Policies” and have not changed significantly.

Merger Agreement

On April 16, 2024, the Company entered into an Agreement and Plan of Merger (the “Merger Agreement”) with McEwen Mining Inc., a Colorado corporation (“McEwen”), and Lookout Merger Sub, Inc., a Delaware corporation and direct subsidiary of McEwen (“Merger Sub”). The Merger Agreement provides that, among other things and subject to the terms and conditions of the Merger Agreement, Merger Sub will merge with and into the Company, with the Company surviving and continuing as the surviving corporation as a direct, wholly owned subsidiary of McEwen (such transaction, the “Merger”).

At the effective date of the Merger, each outstanding share of common stock of the Company will be converted into the right to receive 0.01 of a share of common stock of McEwen. The Company will call a special meeting of its stockholders to consider and approve the Merger. If approved by the Company’s stockholders, the Merger is expected to be consummated in the third calendar quarter of 2024.

Corporate Overview

We are a mineral exploration business and, if and when we establish mineral reserves, a development company. Mineral exploration is essentially a research activity that does not produce a product. Successful exploration often results in increased project value that can be realized through the optioning or selling of the claimed site to larger companies. We acquire properties which we believe have potential to host economic concentrations of minerals, particularly gold and silver. These acquisitions have and may take the form of unpatented mining claims on federal land, or leasing claims on private property owned by others. An unpatented mining claim is an interest that can be acquired in the mineral rights on open lands of the federally owned public domain. Claims are staked in accordance with the Mining Law of 1872, recorded with the federal government pursuant to laws and regulations established by the Bureau of Land Management (the Federal agency that administers America’s public lands), that grant the holder of the claim a possessory interest in the mineral rights, subject to the paramount title of the United States.

We perform geological work to identify specific drill targets on the properties, and then collect subsurface samples by drilling to confirm the presence of mineralization (the presence of economic minerals in a specific area or geological formation). We may enter into option and joint venture agreements with other companies to fund further exploration and/or development work. It is our plan to focus on assembling a high-quality group of gold and silver exploration prospects using the experience and contacts of the management group. By such prospects, we mean properties that may have been previously identified by third parties, including prior owners such as exploration companies, as mineral prospects with potential for economic mineralization. Often these properties have been sampled, mapped and sometimes drilled, usually with indefinite results. Accordingly, such acquired projects will either have some prior exploration history or will have strong similarity to a recognized geologic ore deposit model. We place geographic emphasis on the western United States, and Nevada in particular.

| 13 |

| Table of Contents |

SPECIAL NOTE TO READERS: Lookout Mountain is a material property as defined by Regulation S-K Subpart 1300 (S-K 1300) issued by the Security and Exchange Commission (SEC). All other properties described in this Annual Report are not individually material under S-K 1300.

The Eureka Project includes the Lookout Mountain Property and the historical Lookout Mountain and Windfall Mines in a total property position of approximately 28 square miles (72 square kilometers). The maiden Lookout Mountain mineral resource estimate was reported in compliance with Canadian NI 43-101 in an Updated Technical Report on the Lookout Mountain Project by Mine Development Associates, effective March 1, 2013, filed on SEDAR April 12, 2013.

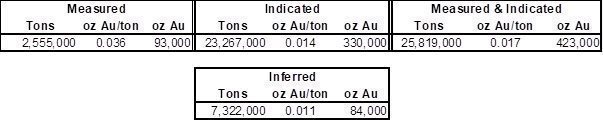

During the 2023 fiscal year, RESPEC Company LLC completed a mineral resource estimate and an initial Technical Report Summary (TRS) for the Lookout Mountain gold deposit. The TRS and mineral resource disclosure is a requirement of S-K 1300, which governs US mining projects. The updated mineral resource estimate is summarized in Table 1. The resource estimate has been constrained by optimized open pits utilizing revenue and cost inputs as summarized in the Notes to Table 1 below:

Table 1. Updated Lookout Mountain Project Gold Resources

Notes:

| · | The Mineral Resources are comprised of oxidized model blocks that lie within optimized pits at a cutoff grade of 0.005 oz Au/ton plus unoxidized blocks within the optimized pits at a 0.055 oz Au/ton cutoff. |

| · | Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. |

| · | The Mineral Resources are potentially amenable to open pit mining methods and are therefore constrained by optimized pits created using a gold price of US$1,800/oz, a throughput rate of 10,000 tons/day, assumed metallurgical recoveries of 80% for heap-leaching of oxidized materials and 86% for toll milling of unoxidized materials, a mining cost of US$2.50/ton, heap-leaching processing cost of $3.60/ton, toll milling cost of $80.00/ton, general and administrative costs of $0.83/ton processed, a reclamation cost of $0.25/ton processed, refining cost of $3.00/oz Au produced, and an NSR royalty of 3.5%. This study does not constitute an Initial Assessment under S-K 1300. |

| · | The effective date of the resource estimate is December 31, 2022. |

| · | Rounding may result in apparent discrepancies between tons, grade, and contained metal content. |

| · | The Technical Report Summary is authored by Steven Osterberg, PhD, PG (Timberline’s qualified person) and RESPEC Company LLC of Reno, Nevada |

Complete descriptions, data and analysis of the Company’s mineral interests, together with graphs, tables and diagrams, can be viewed in our fiscal 2023 annual report dated December 31, 2023, as amended, originally filed with the Securities and Exchange Commission on January 2, 2024.

In November 2023, the Timberline also announced an updated mineral resource estimate reported under Canadian National Instrument 43-101, Companion Policy 43-101CP, and Form 43-101F1, which is a Canadian Securities Administrators’ requirement for mining projects governing the disclosure of mineral reserves and resources. RESPEC Company LLC of Reno, Nevada prepared the mineral resource estimate and authored a technical report, which was subsequently filed on SEDAR+. The mineral resource estimates reported under SEC Regulation S-K 1300 and Canadian NI 43-101 are not materially different.

Detailed maps and mineral resources estimates for the Eureka Project, the 2023 Technical Report Summary and other technical reports and information on the Company’s projects may be viewed at http://timberlineresources.co.

Summary of the exploration activities for the six months ended March 31, 2024:

During the six months ended March 31, 2024, management’s efforts were directed toward securing additional financing to advance the mineral rights owned by the Company, in which it was successful in the short term, as well as in the long term, with the expected closing of the Merger with McEwen announced on April 16, 2024. The funds required to support the operating activities and administration of the Company through the first trimester of the year were secured with a cash infusion of $630,000 to the Company from the sale of common shares and warrants in a private placement transaction. Timberline subsequently arranged a $500,000 interim financing as part of the Merger Agreement.

| 14 |

| Table of Contents |

Exploration Plans and Budgets

Timberline’s focus during fiscal 2024 will continue to be on the Eureka Project. The results of our drilling, mapping, geochemical and geophysical work completed during fiscal years 2020 through 2022 exploration seasons significantly advanced our understanding of the overall geologic setting of the Eureka Project, highlighting several areas with potential for significant gold mineralization. Our most significant advances during this period were the strong drill results announced in FY 2022, the acquisition of patented claims in New York Canyon, surface sampling results for silver and gold in New York Canyon, and the growing potential of carbonate replacement silver-lead-zinc deposits (CRD) on the Eureka Project and more broadly in the district. During fiscal year 2023, management conducted extensive analysis of historical data, newer geophysical and geological data, and district geology to advance integrated targets for CRD silver-lead-zinc and Carlin-type gold exploration. Subject to the availability of sufficient funds, this work will serve as a guide for the fiscal 2024 work program.

Execution of any 2024 exploration activities will be contingent upon the closing of the Merger with McEwen. If the Merger is consummated, there is no certainty that McEwen will continue to pursue the Company’s current exploration plan.

Results of Operations for the three and six months ended March 31, 2024 and 2023

Consolidated Results

(US$) |

| Three Months Ended March 31, |

|

| Six Months Ended March 31, |

| ||||||||||

|

| 2024 |

|

| 2023 |

|

| 2024 |

|

| 2023 |

| ||||

Exploration expenses: |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Eureka |

| $ | 14,767 |

|

| $ | 44,934 |

|

| $ | 34,686 |

|

| $ | 486,971 |

|

Other exploration properties |

|

| 42,445 |

|

|

| 51,488 |

|

|

| 81,773 |

|

|

| 132,094 |

|

Total exploration expenditures |

|

| 57,212 |

|

|

| 96,422 |

|

|

| 116,459 |

|

|

| 619,065 |

|

Non-cash expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stock option expenses |

|

| - |

|

|

| 11,087 |

|

|

| 3,669 |

|

|

| 62,795 |

|

Depreciation, amortization and accretion |

|

| 1,800 |

|

|

| 1,715 |

|

|

| 3,600 |

|

|

| 3,430 |

|

Total non-cash expenses |

|

| 1,800 |

|

|

| 12,802 |

|

|

| 7,269 |

|

|

| 66,225 |

|

Professional fees expenses |

|

| 37,572 |

|

|

| 50,651 |

|

|

| 97,033 |

|

|

| 113,511 |

|

Insurance expenses |

|

| 41,252 |

|

|

| 40,389 |

|

|

| 55,219 |

|

|

| 84,918 |

|

Salaries and benefits expenses |

|

| 75,928 |

|

|

| 67,225 |

|

|

| 149,949 |

|

|

| 127,681 |

|

Interest and other (income) expense |

|

| (2,202 | ) |

|

| 13,946 |

|

|

| (1,793 | ) |

|

| 25,393 |

|

Other general and administrative expenses |

|

| 113,217 |

|

|

| 103,064 |

|

|

| 132,930 |

|

|

| 229,249 |

|

Net loss |

| $ | 324,779 |

|

| $ | 384,499 |

|

| $ | 557,066 |

|

| $ | 1,266,042 |

|

Our consolidated net loss for the three months ended March 31, 2024 was $324,779, compared to a consolidated net loss of $384,499 for the three months ended March 31, 2023. The decrease in net loss is largely due to the significant decrease in exploration expenses, stock option expenses, professional fees, and interest expense as a result of our intentional scale-back of operating activities during management’s efforts to raise funds for operations.

Our consolidated net loss for the six months ended March 31, 2024 was $557,066, compared to a consolidated net loss of $1,266,042 for the six months ended March 31, 2023. The decrease in net loss is largely due to the significant decrease in exploration expenses, stock option expenses and other general and administrative expenses as a result of our intentional scale-back of operating activities during management’s efforts to raise funds for operations.

Financial Condition and Liquidity

At March 31, 2024, we had assets of $14,949,927, consisting of cash in the amount of $91,612; property, mineral rights and equipment of $14,191,178, net of depreciation, reclamation bonds of $528,643, and prepaid expenses, deposits and other assets in the amount of $138,494.

On March 31, 2024, we had total liabilities of $435,544 and total assets of $14,949,927. This compares to total liabilities of $358,095 and total assets of $14,795,875 on September 30, 2023. As of March 31, 2024, our liabilities consist of $147,640 for asset retirement obligations, and $287,904 of trade payables and accrued liabilities. Of these liabilities, $287,904 are due within twelve months. The liabilities compared to September 30, 2023 have increased, due to increased accrued payroll, benefits and taxes, and accrued liabilities during the six months ended March 31, 2024.

| 15 |

| Table of Contents |

On March 31, 2024, we had negative working capital of $58,998 and stockholders’ equity of $14,514,383 compared to negative working capital of $107,701 and stockholders’ equity of $14,437,780 for the year ended September 30, 2023. Working capital experienced a favorable change due to the increase in available cash from a completed private placement financing during the six months ended March 31, 2024.

During the six months ended March 31, 2024, we used cash from operating activities of $600,612, compared to cash used of $1,853,183 for the six months ended March 31, 2023. As a result of our intentional scale-back of operating activities and reduced cash position, we experienced a significant change in our operating assets and liabilities. The change at March 31, 2024 was $(50,814) compared to $(653,366) for the six-month period ended March 31, 2023. The use of cash from operating activities results primarily from the net loss of $557,066 for the six-month period ended March 31, 2024, compared to net loss of $1,266,042 for the six-month period ended March 31, 2023. Changes to the net loss for the comparative periods are described above.

During the six-month period ended March 31, 2024, cash of $36,000 was used by investment activities, compared with cash of $114,170 used for the six-month period ended March 31, 2023. During the six months ended March 31, 2024, we paid $36,000 for mineral rights, compared to $36,000 paid for mineral rights and $78,170 paid for the purchase of mineral locations for the six months ended March 31, 2023.

During the six-month period ended March 31, 2024, we completed a private placement financing resulting in cash of $630,000 provided by financing activities compared to $nil for the six months ended March 31, 2023.

Going Concern

The audit opinion and notes that accompany our consolidated financial statements for the year ended September 30, 2023 disclose a ‘going concern’ qualification to our ability to continue in business. These consolidated financial statements have been prepared on the basis that the Company is a going concern, which contemplates the realization of our assets and the settlement of our liabilities in the normal course of our operations. Disruptions in the credit and financial markets over the past several years have had a material adverse impact on a number of financial institutions and investors and have limited access to capital and credit for many companies. In addition, commodity prices and mining equities have seen significant volatility which increases the risk to precious metal investors. Market disruptions and alternative investment options, among other things, make it more difficult for us to obtain, or increase our cost of obtaining, capital and financing for our operations. Our access to additional capital may not be available on terms acceptable to us or at all. If we are unable to obtain financing through equity investments, we will seek multiple solutions including, but not limited to, asset sales, corporate transactions, credit facilities or debenture issuances in order to continue as a going concern.

At March 31, 2024, we had negative working capital of $58,998. We had $287,904 outstanding in current liabilities and a cash balance of $91,612. As of the date of this report on Form 10-Q, we do not have sufficient cash to meet our normal operating commitments for the next 12 months without additional financing. In connection with the Merger, we entered into a bridge financing with McEwen pursuant to which McEwen has agreed to provide Loans totaling approximately $500,000 to fund the Company’s ongoing expenses through the closing. The closing of the Merger will allow the Company to exit the going concern condition as it becomes a subsidiary of McEwen Mining. If the Merger is not completed, all borrowed amounts will become due on October 15, 2024, or sooner in some circumstances. In that event, the Company will require additional financing in order to repay the borrowed amounts and obtain sufficient funds in order to continue as a going concern.

Financing Activities

On December 28, 2023, we closed a non-brokered private placement to accredited investors at a price of $0.04 per unit. Units consist of one share of common stock and one series P warrant share. We issued 15,750,000 common shares and a like number of warrants for cash proceeds of $630,000. The warrants have a term of four years and are exercisable at $0.06 per common share.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements that are reasonably likely to have a current or future effect on our financial condition, revenues, results of operations, liquidity or capital expenditures.

| 16 |

| Table of Contents |

Critical Accounting Policies and Estimates

There have been no significant changes to the critical accounting policies and estimates disclosed in Management’s Discussion and Analysis of Financial Condition and Results of Operation in our 2023 Form 10-K/A.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not applicable.

ITEM 4. CONTROLS AND PROCEDURES

Conclusions of Management Regarding Effectiveness of Disclosure Controls and Procedures

At the end of the period covered by this Quarterly Report on Form 10-Q, an evaluation was carried out under the supervision of and with the participation of our management, including the Principal Executive Officer and the Principal Financial Officer of the effectiveness of the design and operations of our disclosure controls and procedures (as defined in Rule 13a – 15(e) and Rule 15d – 15(e) under the Exchange Act) as of the end of the period covered by this report.Based upon that evaluation, it was concluded that our disclosure controls were effective as of the end of the period covered by this report, to ensure that: (i) information required to be disclosed by the Company in the reports that it files under the Exchange Act is recorded, processed, summarized, and reported within required time periods specified by the Securities & Exchange Commission rules and forms, and (ii) material information required to be disclosed in reports filed under the Exchange Act is accumulated and communicated to our management, including our Chief Executive Officer and Chief Accounting Officer, as appropriate, to allow for accurate and timely decision regarding required disclosure.

Internal Control over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting. This internal control system has been designed to provide reasonable assurance to the Company’s management and Board of Directors regarding the preparation and fair statement of the Company’s published financial statements.

All internal control systems, no matter how well designed, have inherent limitations. Therefore, even those systems determined to be effective can provide only reasonable assurance with respect to financial statement preparation and presentation.

Our management has assessed the effectiveness of the Company’s internal control over financial reporting as of March 31, 2024. To make this assessment, we used the criteria for effective internal control over financial reporting described in Internal Control-Integrated Framework (2013), issued by the Committee of Sponsoring Organizations of the Treadway Commission. Based on our assessment, we believe that, as of March 31, 2024, the Company’s internal control over financial reporting is effective.

Changes in Internal Control over Financial Reporting

There was no material change in internal control over financial reporting in the quarter ended March 31, 2024 that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

| 17 |

| Table of Contents |

PART II — OTHER INFORMATION

ITEM 1. LEGAL PROCEEDINGS.

We are not aware of any material pending litigation or of any proceedings known to be contemplated by governmental authorities which are, or would be, likely to have a material adverse effect upon us or our operations, taken as a whole. No director, officer or affiliate of Timberline and no owner of record or beneficial owner of more than 5% of our securities or any associate of any such director, officer or security holder is a party adverse to Timberline or has a material interest adverse to Timberline in reference to any currently pending litigation.

ITEM 1A. RISK FACTORS

Due to the proposed Merger with McEwen, there have been material changes to the risk factors included under Part I, Item 1A of the Company’s Annual Report on Form 10-K/A for the year ended September 30, 2023. For a complete discussion of the Company’s risk factors, refer to the risk factors included under Item 1A, Risk Factors of the Company’s Annual Report on Form 10-K/A for the year ended September 30, 2023, and the following risk factors:

We will be subject to business uncertainties while the Merger is pending, which could adversely affect our businesses.

Uncertainty about the effect of the Merger on employees and those that do business with us may have an adverse effect to Timberline. These uncertainties may impair our ability to attract, retain and motivate key personnel until the Merger is completed and for a period of time thereafter, and could cause those that transact with us to seek to change their existing business relationships with us. Employee retention at Timberline may be challenging during the pendency of the Merger, as employees may experience uncertainty about their roles. In addition, the Merger Agreement restricts us from entering into certain corporate transactions, entering into certain material contracts, making certain changes to our capital budget, incurring certain indebtedness and taking other specified actions without the consent of McEwen, and generally requires us to continue our operations in the ordinary course of business during the pendency of the Merger. These restrictions may prevent us from pursuing attractive business opportunities or adjusting our capital plan prior to the completion of the Merger.

Completion of the Merger is subject to a number of conditions, and if these conditions are not satisfied or waived, the Merger will not be completed. Failure to complete, or significant delays in completing, the Merger could negatively affect the trading prices of our common stock and our future business and financial results.

Completion of the Merger is subject to satisfaction or waiver of certain closing conditions, including (i) the receipt of the required approval from Timberline stockholders, (ii) the absence of any order or law prohibiting consummation of the Merger, and (iii) the authorization for listing on the New York Stock Exchange and the Toronto Stock Exchange of the shares of McEwen common stock to be issued in connection with the Merger. There can be no assurance that the conditions to the completion of the Merger will be satisfied or waived or that the Merger will be completed.

If the Merger is not completed, or if there are significant delays in completing the Merger, the trading prices of our common stock and our future business and financial results could be negatively affected, and we may be subject to several risks, including the following:

| · | the requirement that we pay McEwen a termination fee of approximately $400,000 under certain circumstances provided in the Merger Agreement; |

|

|

|

| · | negative reactions from the financial markets, including declines in the prices of our common stock due to the fact that current prices may reflect a market assumption that the Merger will be completed; |

|

|

|

| · | having to pay certain significant costs relating to the Merger; and |

|

|

|

| · | the attention of our management will have been diverted to the Merger rather than our own operations and pursuit of other opportunities that could have been beneficial to us. |

The Merger Agreement limits our ability to pursue alternatives to the Merger.

The Merger Agreement contains provisions that may discourage a third party from submitting a competing proposal that might result in greater value to our stockholders than the Merger or may result in a potential competing acquirer of the Company proposing to pay a lower per share price to acquire us than it might otherwise have proposed to pay. These provisions include a general prohibition on us from soliciting or, subject to certain exceptions relating to the exercise of fiduciary duties by our Board of Directors, entering into discussions with any third party regarding any competing proposal or offer for a competing transaction.

| 18 |

| Table of Contents |

ITEM 2. UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS.

None

ITEM 3. DEFAULTS UPON SENIOR SECURITIES.

None.

ITEM 4. MINE SAFETY DISCLOSURES

We consider health, safety and environmental stewardship to be a core value for the Company.

Pursuant to Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, issuers that are operators, or that have a subsidiary that is an operator, of a coal or other mine in the United States are required to disclose in their periodic reports filed with the SEC information regarding specified health and safety violations, orders and citations, related assessments and legal actions, and mining-related fatalities with respect to mining operations and properties in the United States that are subject to regulation by the Federal Mine Safety and Health Administration (“MSHA”) under the Federal Mine Safety and Health Act of 1977 (the “Mine Act”). During the six months ended March 31, 2024, our U.S. exploration properties were not subject to regulation by the MSHA under the Mine Act.

ITEM 5. OTHER INFORMATION

None.

| 19 |

| Table of Contents |

ITEM 6. EXHIBITS.

101.INS* | XBRL Instance Document |

101.SCH* | XBRL Taxonomy Extension Schema Document |

101.CAL* | XBRL Taxonomy Extension Calculation Linkbase Document |

101.DEF* | XBRL Taxonomy Extension Definition Linkbase Document |

101.LAB* | XBRL Taxonomy Extension Label Linkbase Document |

101.PRE* | XBRL Taxonomy Extension Presentation Linkbase Document |

* - Filed herewith

| 20 |

| Table of Contents |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the Company has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| TIMBERLINE RESOURCES CORPORATION |

| |

|

|

|

|

| By: | /s/ Patrick Highsmith |

|

|

| Patrick Highsmith |

|

|

| President and Chief Executive Officer |

|

|

| (Principal Executive Officer) |

|

|

|

| |

| Date: May 15, 2024 |

| |

|

|

|

|

| By: | /s/ Ted R. Sharp |

|

|

| Ted R. Sharp |

|

|

| Chief Financial Officer |

|

|

| (Principal Financial and Accounting Officer) |

|

|

|

| |

| Date: May 15, 2024 |

| |

| 21 |