UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark one)

For the fiscal year ended

or

For the transition period from___ to___

Commission file number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

(Address of principal executive offices)

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ | ☒ | |

Smaller reporting company | Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

The aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates as of June 30, 2021, the last business day of the registrant’s most recently completed second fiscal quarter, based on the closing sale price of the registrant’s common stock of £8.98, as reported by the AIM, a market operated by the London Stock Exchange, on that date, or approximately $12.42 per share based on the last reported exchange rate for British pounds sterling of £1.00 = $1.3829 on June 30, 2021, was approximately $

As of March 17, 2022, the registrant had

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement relating to the 2022 annual meeting of stockholders, which the registrant intends to file with the Securities and Exchange Commission not later than 120 days after the registrant’s fiscal year ended December 31, 2021, are incorporated by reference into Part III of this Annual Report on Form 10-K.

Table of Contents

2

Risk Factors Summary

Our business is subject to numerous risks that you should carefully consider. These risks are more fully described in the section titled “Risk Factors” included in this Annual Report on Form 10-K. A summary of these risks that could materially and adversely affect our business, financial condition, operating results and prospects include the following:

| ● | We are a cell engineering and life sciences company and have incurred significant losses since our inception, and we expect to incur losses for the foreseeable future. We have limited product offerings approved for commercial sale and may never achieve or maintain profitability. |

| ● | We are highly dependent on a limited number of product offerings. Our revenue has been primarily generated from the sale and licensing of our ATx, STx and GTx instruments, as well as sales of single-use disposable PAs, which require a substantial sales cycle and are prone to quarterly fluctuations in revenue. |

| ● | Our business is dependent on adoption of our products by biopharmaceutical companies and academic institutions for their research and development activities focused on cell-based therapeutics. If biopharmaceutical companies and academic institutions are unwilling to change current practices to adopt our products, it will negatively affect our business, financial condition, prospects and results of operations. |

| ● | We may be unable to compete successfully against our existing or future competitors. |

| ● | If we cannot maintain and expand current partnerships and enter into new partnerships, that generate marketed licensed products, our business could be adversely affected. |

| ● | The failure of our partners to meet their contractual obligations to us could adversely affect our business. |

| ● | Our partners may not achieve projected development and regulatory milestones and other anticipated key events in the expected timelines or at all, or may discontinue some or all of their programs, which could have an adverse impact on our business and could cause the price of our common stock to decline. |

| ● | In recent periods, we have depended on a limited number of partners for our revenue, the loss of any of which could have an adverse impact on our business. |

| ● | We may engage in future acquisitions that could disrupt our business, cause dilution to our stockholders and harm our financial condition and operating results. |

| ● | We depend on continued supply of components and raw materials for our ExPERT instruments and PAs from third-party suppliers, and if shortages of these components or raw materials arise, we may not be able to secure enough components to build new products to meet customer demand or we may be forced to pay higher prices for these components. |

| ● | We have limited experience manufacturing our PAs and if we move manufacturing of our PAs in-house in the future and are unable to manufacture our PAs in high-quality commercial quantities successfully and consistently to meet demand, our growth will be limited. |

| ● | Our results of operations will be harmed if we are unable to accurately forecast customer demand for our products and manage our inventory. |

| ● | If we are unable to successfully develop new products, adapt to rapid and significant technological change, respond to introductions of new products by competitors, make strategic and operational decisions to prioritize certain markets, technology offerings or partnerships, and develop and capitalize on markets, technologies or partnerships, our business could suffer. |

3

| ● | New product development involves a lengthy and complex process and we may be unable to develop or commercialize products on a timely basis, or at all. |

| ● | Our systems are complex in design and may contain defects that are not detected until deployed by our customers, which could harm our reputation, increase our costs and reduce our sales. If our products do not perform as expected or the reliability of the technology on which our products are based is questioned, our operating results, reputation and business will suffer. |

| ● | Our FDA Master File, and equivalent Technical Files in foreign jurisdictions, are an important part of our strategic offering which allows our partners to expedite their cellular therapies into and through the clinic. Delays in filing or obtaining, or our inability to obtain or retain, acceptance of such filings in individual countries could negatively impact the progress of our partners if they intend to run clinical trials in such countries, and as a result, could negatively affect our reputation and revenues or require disclosure of confidential information to our partners. Further, changes that we are required to make from time to time, or changes to regulations or negative data or adverse events for our partners, could impact references to our FDA Master File and Technical Files by our partners. |

| ● | We may need additional funding and may be unable to raise capital when needed, which would force us to delay, reduce, eliminate or abandon our commercialization efforts or product development programs. |

| ● | Our common stock is traded on two separate stock markets and investors seeking to take advantage of price differences between such markets may create unexpected volatility in our share price; in addition, investors may not be able to easily move shares for trading between such markets. |

4

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements about us and our industry involve substantial risks, uncertainties, and assumptions, including those described in “Risk Factors” and elsewhere in this report. All statements other than statements of historical facts contained in this report, including statements regarding our future results of operations or financial condition, business strategy and plans and objectives of management for future operations, are forward-looking statements. In some cases, you can identify forward-looking statements because they contain words such as “anticipate,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “target,” “will” or “would” or the negative of these words or other similar terms or expressions. These forward-looking statements include, but are not limited to, statements concerning the following:

| • | Our expected future growth and the success of our business model; |

| • | The potential payments we may receive pursuant to our Strategic Platform Licenses, which we refer to as SPLs; |

| • | The size and growth potential of the markets for our products, and our ability to serve those markets, increase our market share and achieve and maintain industry leadership; |

| • | The rate and degree of market acceptance of our products within the cell engineering market; |

| • | The expected future growth of our manufacturing capabilities and sales, support and marketing capabilities; |

| • | Our ability to expand our customer base and enter into additional SPLs; |

| • | Our ability to accurately forecast and manufacture appropriate quantities of our products to meet commercial demand; |

| • | Our expectations regarding development of the cell therapy market, including projected growth in adoption of non-viral delivery approaches and gene editing manipulation technologies; |

| • | Our ability to maintain our FDA Master File and Technical Files; |

| • | Our research and development for any future products, including our intention to introduce new instruments and processing assemblies and move into new applications; |

| • | The development, regulatory approval and commercialization of competing products and our ability to compete with the companies that develop and sell such products; |

| • | Our ability to retain and hire senior management and key personnel; |

| • | Regulatory developments in the United States and foreign countries; |

| • | Our expectations regarding the period during which we qualify as an emerging growth company under the JOBS Act; |

| • | Our ability to develop and maintain our corporate infrastructure, including our internal controls; |

| • | Our financial performance and capital requirements; |

| • | Our expectations regarding our ability to obtain and maintain intellectual property protection for our products, as well as our ability to operate our business without infringing the intellectual property rights of others; and |

5

| • | Our use of available capital resources. |

You should not rely on forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Annual Report primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition and operating results. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties and other factors described in the section titled “Risk Factors” and elsewhere in this Annual Report. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this report. The results, events and circumstances reflected in the forward-looking statements may not be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based on information available to us as of the date of this Annual Report on Form 10-K. And while we believe that information provides a reasonable basis for these statements, that information may be limited or incomplete. Our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely on these statements.

The forward-looking statements made in this Annual Report on Form 10-K relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Annual Report to reflect events or circumstances after the date of this Annual Report or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments.

You should read this Annual Report and the documents that we file from time to time with the Securities and Exchange Commission, or SEC, with the understanding that our actual future results, levels of activity, performance and events and circumstances may be materially different from what we expect.

In this Annual Report on Form 10-K, unless the context requires otherwise, all references to “we,” “our,” “us,” “MaxCyte” and the “Company” refer to MaxCyte, Inc.

6

PART I

Item 1. Business

Overview

We are a leading commercial cell engineering company focused on providing enabling platform technologies to advance innovative cell-based research and development as well as next-generation cell therapeutic discovery, development and commercialization. Over the past twenty years, we have developed and commercialized our proprietary Flow Electroporation platform, which facilitates complex engineering of a wide variety of cells.

Electroporation is a method of transfection, or the process of deliberately introducing molecules into cells, that involves applying an electric field in order to temporarily increase the permeability of the cell membrane. This precisely controlled increase in permeability allows the intracellular delivery of molecules, such as genetic material and proteins, that would not normally be able to cross the cell membrane as easily.

With increased knowledge of cell complexity and systems biology in the scientific community, researchers have sought to leverage or repurpose cell functions and/or machinery for research or therapeutic purposes. The ability to engineer living cells by introducing foreign molecules, such as gene editing systems and transgenes, has led to a revolution in biological research and resulted in numerous biological discoveries. Living human cells can also be engineered ex vivo, or outside the body, where they are repaired or reprogrammed to fight disease. In this case, the engineered cell itself is the drug.

Cell therapy has emerged as one of the fastest growing and most promising treatment modalities to address a host of human diseases. Over the past few years, the success of multiple U.S. Food and Drug Administration, or FDA, approved cell therapies providing long-lasting amelioration of symptoms or presence of disease has catalyzed tremendous investment—leading to exponential growth in cell-based therapies being evaluated for therapeutic applications. The Alliance for Regenerative Medicine, or ARM, an international advocacy organization, estimated in August 2021 that the regenerative medicine sector, which consists of gene, cell, and tissue-based therapeutic developers raised an aggregate of $14.1 billion in the first half of 2021, which represents the strongest first half on record and is on pace to exceed the $19.9 billion raised in 2020. As of August 2021, ARM estimates that there were more than 2,600 ongoing clinical trials focused on regenerative and advanced medicine, which includes gene therapy, cell-based immuno-oncology, cell therapy and tissue engineering, including 1,320 industry-sponsored trials by 1,200 companies and 965 unique therapies in development, and forecasts that this number will grow to 3,100 by 2026 with 355 programs expected to be in Phase 3 development.

Our ExPERT platform, which is based on our proprietary Flow Electroporation technology, has been designed to address this rapidly expanding cell therapy market and can be utilized across the continuum of the high-growth cell therapy sector, from discovery and development through commercialization of next-generation, cell-based medicines. The ExPERT family of products includes three instruments, which we call the ATx, STx and GTx, respectively, as well as a portfolio of proprietary related disposables and consumables (as well as the VLx instrument for very large-scale cell engineering made available for sale in December 2021). These include processing assemblies, or PAs, designed for use with our instruments, as well as accessories supporting PAs such as electroporation buffer solution and software protocols. We have garnered meaningful expertise in cell engineering via our internal research and development efforts as well as our customer-focused commercial approach, which includes a growing application scientist team. The platform is also supported by a robust intellectual property portfolio with more than 130 granted U.S. and foreign patents and more than 60 pending patent applications worldwide.

From leading commercial cell therapy drug developers and top biopharmaceutical companies to top academic and government research institutions, including the U.S. National Institutes of Health, or NIH, our customers have extensively validated our technology. We believe the features and performance of our platform have led to sustained customer engagement. Our existing customer base ranges from large biopharmaceutical companies, including all of the top 10, and

7

20 of the top 25, pharmaceutical companies based on 2021 global revenue, to hundreds of biotechnology companies and academic centers focused on translational research.

Our Competitive Strengths

We believe our industry leadership position and continued growth will be driven by the following competitive strengths:

| • | Our proprietary technology platform unlocks the significant potential of advanced cell-based therapeutics. We have built our ExPERT platform to advance the growing demands for non-viral delivery and next-generation cell and gene engineering approaches. Our platform technology enables delivery of almost any molecule into almost any cell type. We believe our platform leads the industry in performance (measured by consistency, efficiency, viability, flexibility and scale). Our platform is further supported by a robust intellectual property portfolio. |

| • | Comprehensive, high-performance transfection platform. We believe our ExPERT platform offers a unique value proposition given the flexibility to scale up from research to cGMP manufacturing on a single platform— enabling the engineering of cells ranging from tens of thousands of cells to tens of billions of cells in a single transfection run in 30 minutes or less. Our long-term internal engineering expertise is supplemented by our customer focused approach—with a growing application scientist team working with our customers across increasingly diverse applications. |

| • | Positioned as a leader in the large and growing next-generation cell therapy market with the ability to capitalize on rising demand for non-viral approaches. We believe we are well positioned to capture increased market share within the large and growing next-generation cell therapy market. Since the FDA approved the first engineered CAR-T cell therapies to treat blood-based cancers in 2017, the number of cell therapy candidates being evaluated pre-clinically and clinically has grown exponentially. We expect growth to continue given the remaining high unmet medical need in cancer and other chronic conditions and predict increased investments in cell therapy product development across a variety of human diseases. We expect to grow our market share given the high performance of our platform and the ongoing adoption of non-viral delivery as the industry has trended towards developing advanced cell-based therapies with complex engineering strategies to improve efficacy, reduce time to patient treatment and expand into new indications. |

| • | Innovative partnership business model focused on value creation and shared success. Our SPLs allow us to participate in the value creation of our customers’ programs via pre-commercial milestones and in nearly all cases commercial sales-based payments. We intend to continue to build a portfolio of strategic partnerships with cell therapy developers, which provide us with a growing, diversified source of potential downstream revenue. |

In addition to the high performance and flexibility of the ExPERT platform, we believe our partnership model further reduces clinical risk and development timelines for our cell therapy partners. By entering into an SPL with us, for example, our partners gain access to our FDA Master File to support their IND-enabling studies and potentially shorten clinical development. Our FDA Master File, which is a submission to the FDA with confidential detailed information about our products, methods, processes and data, was originally established in 2002 and has been continuously updated as platform improvements are implemented to support different applications and cell types. The FDA Master File and equivalent Technical Files in other countries can be referenced by our partners to support their own regulatory submissions with the goal of accelerating regulatory submissions processes for our partners. To date, our FDA Master File and Technical Files have been referenced by our customers in over 40 clinical trials.

8

| • | Recurring revenue model provides high visibility, with drivers of potential long-term upside. Our business model enables us to generate substantial revenue from five sources: sales of instruments, disposables and consumables to new customers; additional sales of instruments, disposables and consumables to our existing installed base; annual instrument license fees from cell therapy customers; potential pre-commercial milestones under SPLs; and potential commercial sales-based payments under SPLs. We generate high recurring revenue from our ExPERT instrumentation licenses, as well as disposables and consumables (or buffer) sales, which provides visibility into future near-term revenue. Over the last three years, annual renewals of instrument licenses were greater than 80% on average—and for our SPLs were near 100%. In addition to recurring revenue, we have the potential to receive meaningful pre-commercial and commercial payments under SPLs if our customers are successful in advancing programs through the clinic and into the commercial stage. In aggregate, we have the potential to receive over $1.25 billion in pre-commercial milestone payments under our current SPLs, if all of the programs were to receive regulatory approvals. |

| • | Founder-led leadership team and workforce with deep domain knowledge. Our management team combines strong and broad subject matter expertise with a demonstrated history of commercial and operational execution. Moreover, our workforce has deep domain knowledge across a range of scientific, engineering, regulatory and business disciplines. We have supplemented our diverse technical experience by assembling a deep operational team with expertise in manufacturing, legal, sales, marketing, customer service and finance. We believe the team we have assembled with talent from multiple disciplines and a science- and customer-focused culture represents a significant competitive advantage for us. As of December 31, 2021, of our 84 full-time employees, 54 have advanced degrees including 22 with Ph.D. degrees. |

Our Technology Platform

The foundation of our technology is our proprietary and patented Flow Electroporation platform, which we have developed and optimized for more than 20 years. Electroporation, or electro-permeabilization, leverages the fundamental properties of cell membranes, the ability to create reversible permeability in the presence of an electric charge, as a universal method to introduce foreign molecules, or transfect, eukaryotic cells, which are cells with a cell membrane and neucleus. Electroporation can be applied to almost any eukaryotic cell type to deliver a broad range of molecules, including DNA, mRNA, siRNA and proteins. Our proprietary Flow Electroporation platform is fully scalable and can support small-scale research and development through large-scale cell engineering for development of commercial therapeutics.

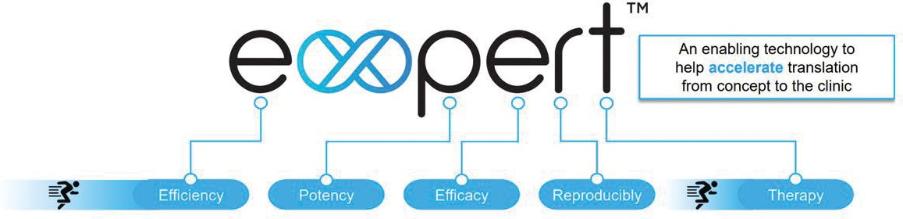

Our technology platform is marketed under the ExPERT brand. The value of our ExPERT brand starts with Efficiency—with high delivery Efficiency, users can achieve Potency, with high Potency, users improve their chances of therapeutic Efficacy, and if this can be repeated, Reproducibly from patient to patient, users have a successful Therapy. By delivering high efficiency at any scale, the ExPERT platform is designed to improve our customer’s ability to achieve the required therapeutic index, enabling accelerated, cost-efficient translation of complex cellular therapies from research to the clinic.

Our ExPERT platform consists of three instruments, the ATx, STx and GTx, which use a broad range of PAs, or disposables, of different volumes to enable scalable electroporation from tens of thousands to billions of cells to

9

facilitate the translation of complex cellular therapies from concept to the clinic, in support of the intended therapeutic commercialization.

ConceptDoEOptimizationVerification

Phase IPivotalValidation

ApprovalOn-Market

Disposables (referred to as processing assemblies) facilitate scale up on same GMP platform

Our ExPERT family of instruments and disposables support scale-up for cell therapy

Overview of our ExPERT Platform

Our Flow Electroporation Technology was designed to meet the stringent demands of clinical use—namely, the ability to safely and reproducibly modify a broad range of primary human cells with high efficiency, low cytotoxicity, and at the scale required to enable the treatment of patients across a diverse range of diseases.

We believe the current ExPERT instrument family represents the next generation of our clinically validated, electroporation technology for complex and scalable cellular engineering. By delivering high transfection efficiency with enhanced functionality and ease of use, the ExPERT platform delivers the high-end performance that we believe is essential to enabling the next wave of biological and cellular therapeutics. The combination of the ExPERT instruments, associated disposables and universal electroporation buffer provides researchers, production scientists, and cGMP facilities with a solution to transfect cells with high efficiency, viability and consistency, which are the three attributes that are consistently ranked by our customers as the top requirements when choosing a cellular or gene engineering platform for clinical use. We believe our ExPERT platform is seen as a critical enabling technology by many of the leading cell therapy companies, helping them to achieve their program goals and milestones expeditiously. Our instruments are sold or licensed for research or clinical use, while the associated disposables and electroporation buffer are sold to support pre-clinical research and development work and are compatible for integration into cGMP manufacturing environments.

We believe that the following four components of our platform have allowed us to successfully address the increasing complexity of cellular engineering approaches in the industry:

| • | Instrument design; |

| • | Electroporation and cell handling protocols; |

| • | PAs (disposables); and |

| • | Universal electroporation buffer formulation (consumables). |

In addition, we have implemented a global scientific and regulatory support strategy for our customers that is designed to accelerate clinical development and streamline the regulatory submission process, thereby potentially saving time and reducing cost and development risk.

We believe our ExPERT platform offers a compelling value proposition to our academic and biopharmaceutical customers due to: (i) the ability to use our technology to deliver almost any molecule into almost any cell type, including hard-to-transfect human primary cells, while maintaining high cell viability and function; (ii) the capacity to introduce larger and more diverse and multiple payloads compared to other intracellular delivery technologies, such as viral vectors; and (iii) the flexibility to scale up from research to current good manufacturing practices, or cGMP, manufacturing on a single platform—enabling the engineering of cells ranging from tens of thousands of cells to tens of billions of cells in a single transfection run in 30 minutes or less.

We believe our ExPERT intracellular delivery platform provides value across numerous applications in the life sciences market, including research, discovery, development, and manufacturing of next-generation, cell-based

10

therapeutics, as well as in biomanufacturing, such as transient protein production for drug discovery and manufacturing of other proteins, including biological therapeutics, viral vectors and vaccines, and small molecule drug discovery.

Our ExPERT technology platform is being used in the clinic to support the development of next-generation cell therapy approaches to treat human disease. Following the successful clinical development leading to FDA approvals of CAR-T cell therapies in blood-based cancers, developers have focused on improving efficacy, lowering the cost of manufacturing and/or expanding engineered cell therapies into new indications, such as solid tumors. To address these goals, the ex vivo cell therapy industry has trended towards developing more complex therapies that require sophisticated engineering and gene manipulation as well as the use of different starting cell types.

In addition, we are committed to continued research and development investments in technology and scientific innovation to maintain our market leadership position.

Our Industry Background

As the cell therapy market continues to evolve, more complex approaches are being deployed to improve efficacy, reduce time to patient and expand the application of cell therapy to additional indications. The use of viral vectors carries several challenges, however, especially given the increase in complexity of these “next-generation” ex vivo cell therapy approaches, such as:

| • | Viral payload limitations. Many methods of gene manipulation require insertion of relatively large molecules, including proteins such as CAS9 RNP for CRISPR or plasmids. Viral vectors, particularly AAV, have fundamental payload capacity limitations, curtailing their utility for complex engineering systems. Additionally, the industry has continued to shift to using complexed molecules including combination of proteins and mRNA which cannot be delivered by viral means. |

| • | Concerns around toxicity. Given viruses used in gene therapy by default infect human cells, there continue to be questions around the safety profile associated with viruses. In particular, there are concerns over the potential for random integration of lentivirus and the widespread presence of neutralizing antibodies against many AAV serotypes used in gene therapies. |

| • | Costs and time to market. Concerns exist regarding viral vector manufacturing capacity and the cost associated with viral development and manufacturing. Additional bottlenecks arise from demand for viral approaches, which has led to subsequent demand for cGMP plasmids. The ongoing COVID-19 pandemic has further exacerbated demand, particularly for adenovirus, and suspension cells, which are difficult to engineer at high volume. Concurrently, regulatory scrutiny and product characterization requirements are increasing as more gene and cell therapy products reach the clinic, as noted by the FDA’s revised guidelines for viral vector analytics in early 2020. |

Novel intracellular delivery approaches are needed to support the increased complexity of the burgeoning cell therapy pipeline. Characteristics include reducing immunogenicity risk of viral vectors, the need to drive high efficiency of multi-molecule delivery while maintaining high cell viability and potency, reducing the risk of potential genotoxicity of multiplex editing (potential for translocations), the need to deliver a large number of molecules at scale, the ability to deliver to a large number of cell types in a time efficient matter, and the need to manufacture in a cGMP environment—all at a manageable cost.

The challenges of viral delivery methods and increased complexity of next-generation cell therapies has driven increased adoption of non-viral delivery technologies, such as electroporation. We believe our ExPERT technology is well positioned as a non-viral delivery platform in the cell therapy market. Originally developed in 1999 for the cell therapy market, we have systematically designed and improved the platform to deliver any molecule, into any cell at any scale, with high efficiency and under cGMP conditions. Our ExPERT platform is now the delivery backbone for a number of next-generation cell therapy programs that are in the clinic.

11

Our Agreements with Customers

We have a diverse portfolio of clinical partners and licensees that mirror the overall next-generation engineered ex vivo cell therapies. While difficult to predict given uncertainty around regulatory approvals and clinical risk, according to Evaluate Pharma, a provider of commercial intelligence and predictive analytics to the pharmaceutical industry, the first next-generation ex vivo cell therapies using non-viral approaches could be approved in the United States as early as 2023.

Our platform’s ability to engineer a diversity of cell types (including CAR-T, chimeric antigen receptor Natural Killer cells, or CAR-NK/NK, T cell receptor, or TCR, and stem cells) and cell sources (autologous and allogeneic) enhances our opportunity by potentially providing for SPL revenues regardless of which approaches advance in the coming years. Additionally, our instruments and platform are well validated, having been used in over 40 clinical trials to date and having been involved in the development of drugs to treat a variety of indications spanning from hematological malignancies to solid tumors to inherited genetic disorders. We believe that the increasing number of publications highlighting the performance of our platform compared to other electroporation, transfection and transduction approaches will continue to drive acceptance of our products in the cellular engineering market segments.

In addition to sales of our instruments, as part of our business model we enter into the following types of instrument license agreements with our customers:

Research Licenses

Research licenses are agreements we have entered into with customers (which could be academic institutions or commercial entities), which provide access to the use of our instruments for pre-clinical research-only purposes, without the rights or ability to produce material for use in the clinic. Research licenses provide the customer with the ability to use the platform for research in exchange for a non-refundable, annual lease payment of typically $150,000 per instrument per year, or in certain circumstances under a sale of an instrument to a cell therapy user. We have entered into many research licenses to-date, either as (i) stand-alone research license agreements, (ii) research and clinical license agreements that do not have associated commercial rights or (iii) under an SPL, which allows a customer to use the instrument for clinical development and potential commercial sale of a therapeutic product. Research licenses under a stand-alone research license agreement (as well as instruments purchased for research use) could represent opportunities for future SPLs.

Clinical Licenses

Clinical licenses are agreements with academic institutions or commercial entities that provide access to the use of our instruments in the clinical evaluation and development of a therapeutic product intended for human use. In a clinical license, we retain title to the instrument and provide the customer with the ability to use the platform for production of clinical material for human clinical use, as well as access to our application scientist team, all in exchange for an annual lease payment that typically approximates $250,000 per instrument per year for commercial customers. Academic clinical licenses can represent opportunities for future SPLs to the extent that commercial entities seek and obtain rights to such programs from the academic institution.

Strategic Platform Licenses (SPLs)

Given our value proposition in non-viral delivery, we have established strategic relationships in the form of SPLs with a growing number of leading cell therapy developers as they work to bring next-generation cell therapies into and through the clinic and advance those candidates to potential commercialization.

12

Under these SPLs and other license agreements with our customers, we retain title to the licensed instrument and associated intellectual property, and in exchange for an annual license fee per instrument, we provide our customers with non-exclusive access, for a defined field of use to our:

| • | cGMP-compatible platform, which enables early-optimization and scale-up from pre-clinical research into clinical development using our intellectual property portfolio; |

| • | FDA Master File and Technical Files, which may accelerate and streamline development and reduce regulatory risk in the creation and development of our partners’ therapeutic drug candidates; |

| • | Experienced commercial team of sales personnel and application scientists who work directly with our customers to solve cell engineering problems; and |

| • | Continuous know-how and cell engineering process improvements. |

In return, these SPLs provide us with the ability to secure downstream program-related pre-commercial milestones and, in most cases, commercial sales-based payments. In addition, from our SPL customers, we receive both annual research and clinical license fees as well as payments from sales of our proprietary disposables as recurring revenue streams. Given growth in the cell therapy pipeline and increased investment in the space, we estimate that the number of potential SPLs for us will continue to grow significantly, based on our estimates of growth in the cell therapy pipeline, growth in the number of therapeutic delivery entrants into the market and ongoing shift to non-viral delivery.

Our customer relationships may evolve to an SPL after the customer’s drug candidate optimization and verification process nears completion and the clinical process development stage begins. Specifically, if a customer wishes to use our products in the clinical phase of process development, they will need to enter into an SPL, as a customer must obtain clinical rights to perform clinical process development, including for engineering runs. Customer discussion for an SPL can take place any time during our engagement.

Our SPL customers typically pay an annual license fee per instrument per year for a research license (for pre-clinical use) or per instrument per year for a clinical license (for clinical or commercial use) or in certain circumstances purchase an instrument for research use. Partners also purchase associated single-use disposables and consumables as needed. Our SPL partners also commit to pay pre-commercial milestone payments for each therapeutic licensed under the agreement and produced using our platform, as they achieve key pre-commercial clinical development events (including for example, IND filing, dosing of an agreed number of patients in a Phase 1 clinical trial, initiating a pivotal clinical trial, and BLA approvals in specified regions). Almost all of our SPLs also include a commitment to pay us post-approval sales-based payments for commercialized therapeutics.

We view our ability to sign SPLs as a key measure of our success in partnering with leading therapeutic developers in the clinic and supports the high performance of our platform.

13

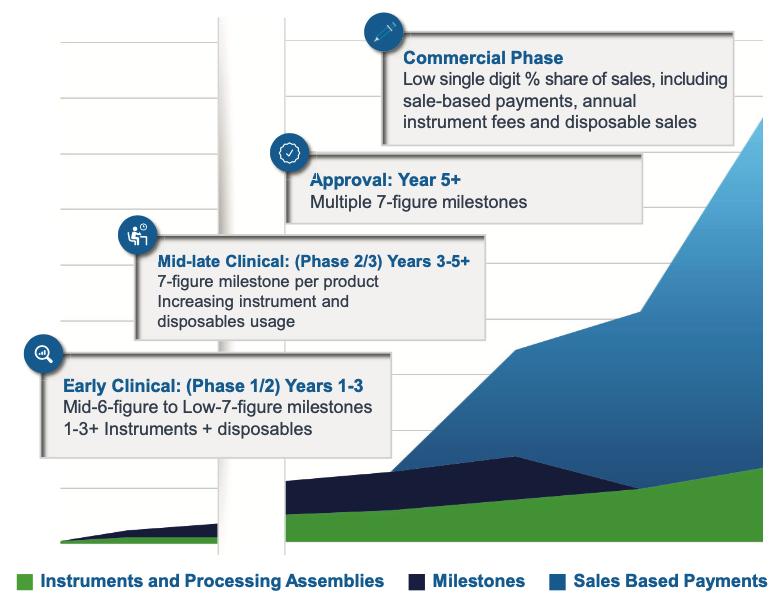

The following graphic is an example of typical single-product revenues from a representative SPL:

Our SPLs and research and clinical licenses may be terminated at the option of our customers at any time. Annual instrument lease fees are non-refundable and customers may not use our instruments or process assemblies after terminating their agreement with us. We retain title to the leased instrument in each of our licenses. Upon contract termination, our customers would be responsible for any further clinical studies or data development that regulators may require to allow a change in their cell engineering methodology. To date, none of our SPL licensees has ever terminated their contract with us.

We have entered into 16 SPLs with commercial cell therapy developers since January 1, 2017, all of which remain active as of the date of this report.

Of the over 95 potential program allowed under our current SPLs, more than 15% are in the clinic, meaning they have at least an FDA-cleared investigational new drug application, or IND. An IND is a request for authorization from the FDA to administer an investigational new drug to humans. An IND must become effective before human clinical trials may begin. The IND automatically becomes effective 30 days after receipt by the FDA, unless the FDA, within the 30-day time period, raises safety concerns or questions about the proposed clinical trial. Clinical trials then involve the administration of the investigational product to human subjects under the supervision of qualified investigators and are conducted under protocols detailing, among other things, the objectives of the study, the parameters to be used in monitoring safety and the effectiveness criteria to be evaluated.

5

Our 16 SPLs have the potential to generate over $1.25 billion in pre-commercial milestone payments if all of the licensed programs were to achieve regulatory approvals. In addition, under the SPLs, we typically have the potential to receive significant, sales-based commercial payments for approved products. However, clinical development involves a lengthy and expensive process with uncertain outcomes, including the results of pre-clinical research, as well as product

14

safety and efficacy, and therefore our customers may not begin or complete clinical development, or may never receive FDA or other regulatory approval for, all product candidates covered by their SPL agreements with us, in which case we will not receive the full potential pre-commercial milestone payments or the sales-based commercial payments or royalties contemplated by our agreements.

Our Products

The ExPERT instrument family was designed to provide a single unifying technology that can be used from concept to clinic, with both the research and clinical versions of the instrument incorporating the same underlying technology and protocols. Our customers have a choice of three different instrument versions that are standardized on the same technology to deliver the same high performance—the ATx, STx and GTx (as well as the VLx instrument for very large-scale cell engineering which became available for sale in December 2021). Customers can start with the lower to medium scale research instrument (ATx) and then scale to the clinical version (GTx), without the need for re-optimization and re-validation. The STx provides the same scale as the GTx, but is used for drug discovery applications, not for human therapeutic use, and is not covered by our FDA Master File or our Technical Files.

We believe these systems will also be supportive of the commercial marketing of our partners’ therapeutic products which we enable. By allowing our customers to perform their research and process optimization on a research platform and seamlessly scale to a clinically validated, cGMP environment and 21 CFR Part 11 compatible clinical platforms, significant time and cost savings can be realized.

All of our instruments have been designed to provide customers with the key features required for a scalable high-performance transfection solution. Each of our ExPERT instruments are benchtop with the same small footprint and have integrated touch screens with an intuitive Graphical User Interface, or GUI, designed for simple training and operation. To support use in the cGMP suite for clinical manufacturing, our GTx ExPERT software is network capable to enable upload of electronic batch records to a local shared drive and has a software intermediary to facilitate integration and automated data transfer to cloud-based data management solutions. We have integrated hardware and software design solutions, manufactured under cGMP, that are tailored for use in cGMP manufacturing of clinical products for advanced cellular therapies.

15

ExPERT ATx: Research focused, static electroporation for small to medium scale transfection

| Our ExPERT ATx static electroporation instrument is a research focused, high performance electroporation platform for small to medium scale transfection. The ATx instrument delivers high efficiency and viability at research scale and can utilize our range of PAs capable of transfecting from 75,000 up to 700 million cells. Additionally, our ATx instrument is compatible with all of our static PAs, which can also be used on our GTx instrument, allowing for a seamless transition to our clinical cGMP-compatible platform. The ATx is designed and used by our customers for early design of experiment and process optimization at small scale to minimize cell acquisition and reagent costs. Once optimized for the biological function with smaller numbers of cells, the process can be replicated and scaled before being transferred to the clinical platform (GTx) for eventual manufacturing in the cGMP suite or to the STx platform for drug discovery. |

ExPERT STx: Flow Electroporation for protein production and drug development

| Our ExPERT STx, which is used in the field of protein production as well as other drug discovery applications, also incorporates our proprietary Flow Electroporation Technology for high yield transient expression of complex proteins, viral vectors, vaccines and biologics. Our STx instrument has high efficiency and can rapidly transfect from 75,000 up to 20 billion cells. When combined with flexible media strategies, the STx allows for substantial improvement in yields of high-quality, transiently expressed proteins while enabling reduced media costs. Another key application area for the STx is expression of therapeutic targets for cell-based assays. Traditionally, drug screening has been performed using stable cell lines because conventional transfection technologies, such as lipofection, may induce changes to membrane composition, which does not offer the consistency and scalability that are critical for sensitive, high throughput screens. By enabling high efficiency transfection of multiple plasmids simultaneously into billions of cells, the STx provides drug developers with the ability to express complex, multi-subunit proteins, such as ion channels, in physiologically relevant cells. The high viability of our transfected cells leads to robust assay responses on multiple platforms, including automated electrophysiology and high content screening technologies. Moreover, precise control over loading efficiency gives assay developers the ability to “dial in” optimal assay windows. |

17

ExPERT GTx: Flow Electroporation for large scale transfection in therapeutic applications

| The ExPERT GTx incorporates our proprietary Flow Electroporation Technology for use in the cGMP manufacturing of cellular therapies for use in the clinic. By incorporating the Flow Electroporation Technology, larger volumes of up to 20 billion cells can be electroporated within 15 to 20 minutes. With a processing potential that ranges from 75,000 to 20 billion cells on a cGMP, 21 CFR Part 11 compatible system, the GTx represents a platform for clinical electroporation at large scale. The GTx integrates several design features that are critical for use in a cGMP setting, such as barcode reading capability to maintain positive identification of patient samples, 21 CFR Part 11 compatible software and networking capability for automated uploading of electronic batch records to either a central server or to a cloud-based data management platform. The GTx enables closed sample processing, on a system compatible with integration into cGMP manufacturing environments, and that has an established regulatory path supported by our FDA Master File and Technical Files. |

ExPERT VLx: Designed for very large volume cell-engineering

| The VLx Large-Scale Transfection System is a cGMP compliant instrument specifically designed for very large volume cell-engineering. Using proprietary Flow Electroporation Technology, the VLx supports the ability to transfect up to 200 billion cells in less than 30 minutes—10 times the capacity of the STx and GTx. This system is designed for the rapid and large-scale production of recombinant proteins, monoclonal antibodies, viral vectors, vaccines, virus-like particles, or VLPs, and allogeneic cell therapies. We introduced the VLx under the ExPERT umbrella in December 2021 to provide our customers with an easier to use system that incorporates the benefits of the ExPERT platform. We plan to expand the functionality of the VLx into new applications, such as large-scale bioprocessing. We expect that additional investment will be needed to build out process development capabilities, manufacturing capacity, for new processing assembly design and the addition of large-scale bioprocessing-specific field resources. |

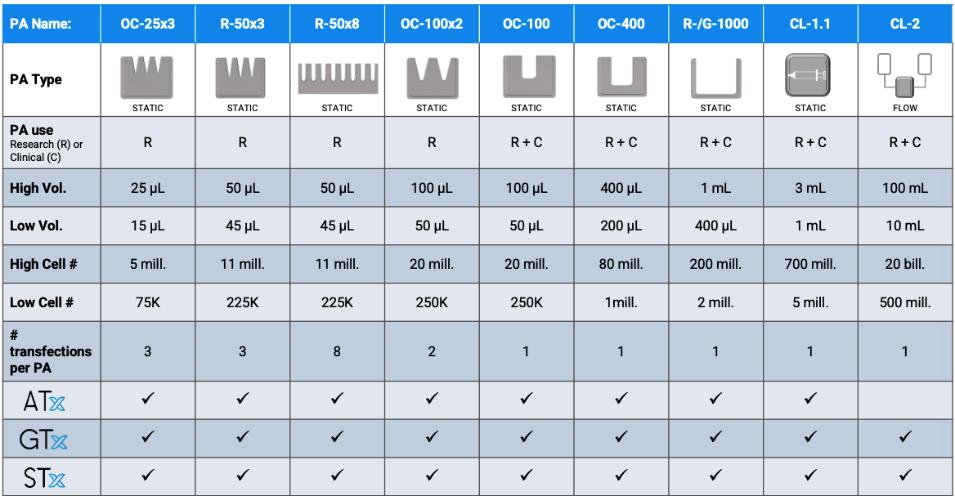

Disposables—Processing Assemblies (PAs)

Our range of disposable PAs is an important differentiator for us. We are not aware of any other company with the breadth and diversity of volume ranges and designs to enable high efficiency electroporation in flow, single-well and multi-well formats, for use in both the research and clinical settings. We view the PA design as one of the key contributors to the high efficiency and viability of the ExPERT platform.

We have designed a range of PAs that are specially designed to process and electroporate the user’s chosen quantity of cells. Each PA contains two electrodes, between which a medical-grade gasket is sandwiched that has a unique well design consistent with the processing volume required and to allow maximum retrieval of cells. We have designed a unique range of PAs capable of electroporating cell volumes from small to large scale, in single and multi-well formats, for both research and clinical use. Cells are placed into the sample bag in large scale PAs or into the well or wells in

18

small scale PAs and the PA is then connected to the instrument for processing. The instrument touch screen allows the operator to select the desired cell protocol that encodes the electroporation parameters, select the type of PA to be used and enter any sample specific information. Once the sample information has been entered, the operator will touch the “Start Processing” icon on the user interface and the sample will be rapidly processed. Larger volumes of cells are accommodated by larger capacity PAs and a set of simple software commands through the intuitive GUI.

Our ExPERT system uses two PA designs — a static cuvette used for smaller cell volume requirements (from 75,000 cells up to 200 million cells) and a cartridge that is used for both static and Flow Electroporation for larger cell volumes (700 million up to tens of billions of cells). The Flow Electroporation PA (CL-2) allows for processing of cellular volumes ranging from 10 mL to 100 mL and up to tens of billions of cells. The CL-2 consists of bags and associated tubing, made from medical grade materials, that are connected to the electroporation cartridge. Users will transfer their cells and loading molecules to the sample bag, and the pump on either the GTx or STx instrument pumps a fixed volume of cells into the cartridge chamber where they are electroporated. Once the electroporation is complete, the cells are pumped to the collection bag and the chamber is filled with the next volume of cells for electroporation. This process is repeated until the entire sample volume is processed. The maximum volume of 100 mL of cells can be processed in approximately 15–20 minutes.

Our two ExPERT PA designs are shown in the pictures below:

We have conducted extensive end-user research over the last several years to continue to improve the design of the PAs and the range of products available. As a result, we launched the ExPERT cuvette in 2020 based on customer feedback, which incorporated a new design to improve handling and ease of use. In 2021, we expanded the availability of the ExPERT PA design, continuing to roll it out across the entire range of cuvettes. Conversion of the portfolio will be completed in 2022. We also expanded our portfolio of multi-well cuvettes, which reduce manual handling and improve productivity in the lab, with the launch of our R-50x8. The R-50x8 is an 8-well cuvette capable of processing up to 225,000 cells in each well. By enabling eight samples to be processed in the same cuvette, a more efficient process can be achieved by users.

19

The following matrix shows our full line of currently available PAs and their respective specifications and features, including the ExPERT instruments with which they can be used:

We are committed to continuing to strategically invest in improvements in the PA design and range of products to ensure that customers have solutions that address all of their volume and use requirements, in both research and clinical settings, including current development of advancements for PA(s) that support the VLx.

Supporting Products

Our proprietary electroporation buffer, a balanced salt solution that protects cells during transfection, is formulated for use with all our instrument platforms and PAs. This consumable is used for all cell types, eliminating the need to change buffers as users switch protocols, cell types or scale up. The buffer is made in a cGMP facility, is fully chemically defined and is free of human or animal components, and is tested to meet technical, sterility and endotoxin specifications. This buffer formulation is a key contributing factor, in combination with instrument and PA design features, to the flexibility, high efficiency and viability that can be achieved by customers across the broad range of cell types processed using our platform.

Sales and Marketing

We follow a direct sales model in North America, the United Kingdom, and Europe, while also selling through third-party distributors in Asia and some regions of Europe. As of December 31, 2021, we have over 20 field sales and application scientists located in the United States, the United Kingdom, and several regions in Europe and Asia. Since the commercial launch of our first Flow Electroporation instrument, the installed base of our instruments has grown to more than 500 instruments globally.

Our sales force and field application scientists and international partners inform our current and potential customers of current product offerings, new target applications and advances in our technologies and products. As our primary point of contact in the marketplace, our field teams focus on delivering a consistent marketing message and high level of customer support, while also working to help us better understand the evolving market and customer needs. We intend to expand our sales, support, and marketing efforts in regions such as the Asia-Pacific region. We currently use distributors

20

in countries in these regions, such as in China and Japan, and continuously assess the need for direct sales and local support personnel to supplement our distributors’ resources. As we expand into a new geography, we generally rely initially on third-party distributors until we are able to recruit a direct sales force, field application scientists and business development resources in the country or region.

Our business model is focused on identifying new applications in cell engineering to enable our customers to develop better medicines and maximize use across our customers’ value chains. This is enabled through customer partnerships that allows us to further understand the critical applications for our technology and inform our future developments and market expansion.

Research and Development

Investment in research and development is at the core of our business strategy. Members of our research and development team specialize in many functional areas including molecular biology, cellular biology, physics, gene editing, cell culture, protein manufacturing, mechanical engineering, cell handling processes, electroporation algorithm development and customer technical support.

Our research and development teams are aligned into two teams, applications and instrumentation. The application team is responsible for developing data on key applications, including improving approaches to cell handling and cell culture; designing, developing and enhancing electroporation protocols; developing and enhancing cell engineering applications, and performing product testing and quality assurance activities. The instrumentation engineering team focuses on developing and improving electroporation instruments and PA disposables to meet our partners’ wide range of needs from research to commercialization in a GMP environment. The research and development functional teams work together as a core team, following a stage-gate process to develop, qualify and launch new products to market.

Other research and development activities include customer technical support such as lab cell processing techniques, instrumentation training and application support. Most of our research and development operations are conducted in our Maryland facility.

We have made substantial investments in product and technology development since our inception. Research and development expenses totaled $15.4 million, $17.7 million and $17.6 million in the years ended December 31, 2021, 2020 and 2019, respectively.

Although our CARMA pre-clinical and clinical development was concluded in the first half of 2021, we expect our research and development expenses outside of CARMA to increase significantly for the foreseeable future as we develop data supporting the use of our products in various applications and continue to enhance our existing products as well as develop new products for our current and new markets.

Manufacturing and Supply

We design our single use PA disposables and conduct final functional testing in our Maryland facility. In addition, we design, develop and manufacture the ExPERT instruments in-house. Our in-house manufacturing and design function is certified as ISO 9001 compliant and our manufacturing facility and controlled-access shipping, receiving and storage spaces are located at our current headquarters in Maryland. We intend to relocate our manufacturing to a significantly larger space in a new facility during 2022.

Instruments

Our range of ExPERT instruments are manufactured, tested and shipped from our Maryland facility under cGMP. Several custom components of our ExPERT instruments are fabricated by third-party suppliers. The assembly of technology-sensitive components and the final assembly is completed in-house. Presently, our Maryland manufacturing

21

facility can support the production of ExPERT instruments in excess of current demand, and we will continue to obtain the space and staffing necessary to meet customer demand for the foreseeable future.

Processing Assemblies

Our family of ExPERT instruments incorporate a broad range of proprietary single use PAs that are specially designed to meet the needs of our customers for cell volume, single- or multi-well configuration, and static or flow processing. These PAs are only available from us and are designed for use only with our instruments and, our range of PAs are designed, developed, tested and shipped from our Maryland facility. We currently outsource manufacturing of components and final clean-room disposables assembly to third parties. We plan to move the cleanroom assembly activities in-house in order to enhance operational control over quality, expand capacity, enable automation implementation and improve other areas of operations. In addition, in-house manufacturing is expected to allow research and development to more rapidly develop new products and enhancements when manufacturing and research and development are in the same facility. We are currently constructing a new facility for occupancy in mid-2022 that will include new cleanroom space for assembly of processing assemblies. Staffing and manufacturing process development for in-house PA manufacturing began in early 2022. We will seek to establish commercial scale PA production capacity by the end of 2022 and full initial capacity during 2023.

Supply

For both instrument and PA manufacturing, we regularly assess our supply chain to ensure availability of components, our ability to respond to customer demand for our products and to qualify multiple suppliers. We have relationships with several custom parts manufacturers and electronics suppliers that can provide components for our instruments, including components currently provided by a single source. Approximately 33% of our inventory held at December 31, 2021, was purchased from one supplier. Single source suppliers are chosen for their business stability and scalability to minimize risk. If a single source supplier has a part or process that is time-consuming to transfer to another supplier, our approach is to hold enough inventory of that part to allow adequate time for technical transfer and qualification wherever possible. Our ongoing strategy is to maintain adequate levels of inventories at all times and to qualify at least two suppliers for critical quality components, and we plan to continue the diversification of our supply chain as we scale. This inventory strategy was designed to minimize supply chain risk and as a result we are currently able to ship on demand and to date have never had a backorder for a product.

Competition

The life sciences market is highly competitive and dynamic, reflecting rapid technological evolution and continually evolving customer requirements. There are other companies, both established and early-stage, that have or are developing electroporation and other non-viral delivery technologies that could be applicable to both bioprocessing and cell engineering. These companies include Lonza Group AG, Thermo Fisher Scientific Inc., Miltenyi Biotec, Bio-Rad Laboratories, Inc. and Harvard Biosciences Inc. (BTX), as well as several other smaller companies, including spinouts from academic labs.

Some of these companies may have substantially greater financial and other resources than us, including larger research and development staff or more established sales forces. Other competitors are in the process of developing novel technologies for the life sciences market which may lead to products that rival or replace our products.

For further discussion of the risks we face as a result of competition, see “Risk Factors—Risks Related to Our Business and Growth Strategy—We may be unable to compete successfully against our existing or future competitors.”

Intellectual Property

Our intellectual property strategy has been, and still is, to obtain patent protection in relevant jurisdictions over our instruments, methods utilizing our instruments, as well as design patents over the ExPERT system. As part of this

22

strategy, we have focused on obtaining protection for our non-viral delivery platform to the extent possible, particularly in the United States and other key jurisdictions of commercial value. As of February 11, 2022, we have more than 130 granted U.S. and foreign patents, including in foreign jurisdictions such as Australia, Canada, Japan, China, South Korea and certain countries in Europe, as well as over 60 pending patent applications worldwide. The main focus of our patent coverage is to protect our Flow Electroporation, processing chambers/disposables, control and process elements, and methods/applications of using our non-viral delivery platform. Our patent portfolio provides protection over our instruments and related methods through at least 2028 and over our electroporation applications and methods through 2034. We are also working to secure design protection of the ExPERT system, which has the potential to provide protection through at least 2036.

In addition to our granted patents and filed applications, we maintain and protect a number of different trade secrets related to our cell processing technology and other core technology areas, such as improvements made to protocols, pulsing patterns, proprietary buffer and formulations developed by us. Our years of accumulated know-how and the technical expertise of our employees provide us with a competitive advantage. We use our know-how and technical expertise to optimize and update our proprietary methods and protocols, such as cell handling and preparation techniques unique to different cells and target molecules, which we confidentially share with our customers.

We maintain the confidentiality of our trade secrets, know-how and proprietary methods and protocols to protect our intellectual property from competitors. One key element of this protection is our FDA Master File and Technical Files described in more detail below, which allow us to submit to the regulatory authorities confidential detailed information about our ExPERT system and disposables. The relevant submission can be referenced by our customers or licensees to support their own regulatory filings without the need for us to disclose the confidential information contained in the FDA Master File and Technical Files.

We also seek to protect our brand through procurement of trademark rights. As of March 14, 2022, we owned 15 registered trademarks in the United States, 146 registered foreign trademarks, 15 pending U.S. trademark applications, and more than 58 pending foreign trademark applications. Our registered trademarks and pending trademark applications include trademarks for MaxCyte, CARMA, a stylized version of ExPERT and our logo. In order to supplement protection of our brand, we have also registered several internet domain names.

Government Regulation

The FDA and similar governmental authorities regulate, among other things, the research, development, testing, manufacturing, clearance, approval, labeling, storage, recordkeeping, advertising, promotion, marketing, distribution, post-market monitoring and reporting, as well as import and export of technologies including biological drug products.

Our biopharmaceutical and life sciences customers are subject to extensive regulations by the FDA and equivalent regulatory authorities in other countries, regarding the conduct of pre-clinical studies and clinical trials, in the manufacture of product candidates and products for use in humans (i.e., “Good Manufacturing Practice” laws and regulations) and the marketing authorization and commercialization of biological drug products.

The activities of sponsors, applicants and manufacturers are subject to regulation of those jurisdictions where the research or manufacturing occur, and also jurisdictions for which applications are planned or have been made and the product is intended to be marketed.

Although we are not engaged in directly regulated activities, our customers will generally assess our products for sufficiency in meeting their regulatory needs, and may impose rigorous quality or other regulatory compliance requirements on us as their supplier through supplier qualification processes and customer contracts.

We have established a quality management system (under ISO 9001:2015 standards) which is designed to respond to customer expectations and needs and support customer adherence to applicable regulatory requirements. The

23

technologies we offer for potential use by customers in a cGMP environment are produced under this ISO 9001:2015 quality management system.

Master Files and Technical Files to Support Customer Regulatory Submissions

Our core business is focused on developing our proprietary and patented electroporation technology platform, which is used by our customers in research and development applications as well as for manufacture of commercial cell therapies. In order to support our customers’ use of our platform, we have voluntarily submitted a Master File to the FDA, Center for Biologics Evaluation and Research and Master Files or Technical Files to comparable regulatory authorities in other jurisdictions, including Canada, Japan, the United Kingdom and Austria, and provide nonexclusive Letters of Authorization to the Master or Technical Files under contractual agreements with our customers. We have also discussed the potential to submit a Master File with the Therapeutic Goods Administration in Australia. In this way, the regulatory body may review information on our platform in the context of its utilization by our partners in regulated products, for example, as described in our customers’ Investigational New Drug (IND) applications. We continuously update the Master and Technical Files in order to support the regulatory activities of our customers. The FDA and regulators in other countries allow Master and Technical Files, but they do not approve them. Rather, they review them in the context of evaluating the submissions by our customers wherein our files are referenced.

U.S. Healthcare Laws and Reform

In the United States, there are federal and state healthcare laws that constrain the business or financial arrangements and relationships through which our customers who use our platform and we, if we develop a product, research, sell, market and distribute products. Such laws include federal and state anti-kickback laws, false claims laws, transparency laws and health information privacy and security laws. Violations of these laws can lead to significant administrative, civil and criminal penalties, including sanctions, damages, disgorgement, monetary fines, possible exclusion from participation in government healthcare programs such as Medicare and Medicaid, imprisonment, additional reporting requirements and/or oversight obligations, contractual damages, reputational harm, diminished profits and future earnings and curtailment or restructuring of operations.

Additionally, in the United States and some foreign jurisdictions there have been, and continue to be, several legislative and regulatory changes and proposed reforms of the healthcare system in an effort to contain costs, improve quality, and expand access to care, including the proposed modification to some of the aforementioned laws. In the United States, there have been and continue to be a number of healthcare-related legislative initiatives that have significantly affected the healthcare industry. These reform initiatives may, among other things, result in modifications to the aforementioned laws and/or the implementation of new laws affecting the healthcare industry. Similarly, a significant trend in the healthcare industry is cost containment. Third-party payors have attempted to control costs by limiting coverage and the amount of reimbursement for particular medications. Our ability to commercialize any of our products successfully, and our customers and collaborators’ ability to commercialize their products successfully, will depend in part on the extent to which coverage and adequate reimbursement for these products and will be available from third-party payors. As such, cost containment reform efforts may result in an adverse effect on our operations.

The Foreign Corrupt Practices Act

The Foreign Corrupt Practices Act, or FCPA, prohibits any U.S. individual or business from paying, offering, or authorizing payment or offering of anything of value, directly or indirectly, to any foreign official, political party or candidate for the purpose of influencing any act or decision of the foreign entity in order to assist the individual or business in obtaining or retaining business. The FCPA also obligates companies whose securities are listed in the United States to comply with accounting provisions requiring the company to maintain books and records that accurately and fairly reflect all transactions of the corporation, including international subsidiaries, and to devise and maintain an adequate system of internal accounting controls for international operations.

24

Data Privacy and Security Laws and Regulations

In the ordinary course of business, we may process personal data (including, without limitation, clinical trial data and other data concerning health). Accordingly, we may be subject to numerous data privacy and security obligations, including federal, state, local and foreign laws, regulations, guidance, and industry standards related to data privacy, security, and protection. These frameworks are evolving and may impose potentially conflicting obligations. Such obligations may include, without limitation, the Federal Trade Commission Act, the Telephone Consumer Protection Act of 1991, the Controlling the Assault of Non-Solicited Pornography And Marketing Act of 2003, the California Consumer Privacy Act of 2018 (“CCPA”), the European Union’s General Data Protection Regulation 2016/679 (“EU GDPR”), the EU GDPR as it forms part of United Kingdom (“UK”) law by virtue of section 3 of the European Union (Withdrawal) Act 2018 (“UK GDPR”), the ePrivacy Directive, and the Payment Card Industry Data Security Standard (“PCI DSS”). In addition, several states within the United States have enacted or proposed data privacy laws. For example, Virginia passed the Consumer Data Protection Act, and Colorado passed the Colorado Privacy Act.

The EU GDPR and CCPA are examples of the increasingly stringent and evolving regulatory frameworks related to personal data processing may increase our compliance obligations and exposure for any noncompliance. European data privacy and security laws (including the EU GDPR and UK GDPR) impose significant and complex compliance obligations on entities that are subject to those laws. For example, in the European Economic Area, or EEA, the processing of personal data is principally governed by the provisions of the EU GDPR. The EU GDPR applies to any processing operations carried out in the context of an establishment in the EEA as well as any processing operations relating to the offering of goods or services to individuals in the EEA and/or the monitoring of their behavior in the EEA and to companies established outside the EEA that process personal data in connection with the offering of goods or services to data subjects in the EEA or the monitoring of the behavior of data subjects in the EEA.

The GDPR enhances data protection obligations for controllers of personal data (such as clinical trial sponsors). These obligations may include limiting personal data processing to only what is necessary for specified, explicit, and legitimate purposes; requiring a legal basis for personal data processing; limiting the collection and retention of personal data; increasing rights for data subjects; formalizing a heightened and codified standard of data subject consents; requiring the implementation and maintenance of technical and organizational safeguards for personal data; mandating notice of certain personal data breaches to the relevant supervisory authority(ies) and affected individuals; and mandating the appointment of representatives in the UK and/or the EU in certain circumstances. In the United Kingdom, the UK Data Protection Act 2018 complements the UK GDPR in this regard. This fact may lead to greater divergence on the law that applies to the processing of such categories of personal data across the EEA and/or United Kingdom.