Exhibit 99.(c)(2)

| January 2021 Valuation Report Heron Lake BioEnergy, LLC. |

| Privileged and Confidential Agenda 2 ➢ Ethanol Industry Overview ➢ HLBE Valuation ✓ Plant Profile and Market Overview ✓ Market Access ✓ EBITDA Benchmarking ✓ Valuation Due Diligence Summary ✓ HLBE Valuation in Context of Liquidity Challenges ✓ Valuation ▪ DCF Valuation ▪ Comparable Transaction Valuation ✓ Valuation Summary ➢ Discussions and Questions |

| Privileged and Confidential Ethanol Industry Overview 3 |

| Privileged and Confidential 4 ▪ The U.S. ethanol industry has changed more dramatically in the last 20 years then almost any other industry related to agriculture. The industry has expanded eleven-fold and provided the biggest investment opportunities for rural investors in a lifetime. The economic drivers of that 2000 to 2010 ethanol expansion: ▪ Environmental Solution to Replace MTBE (Oxygenate) ▪ 9/11/01 Terrorist Attack, Middle East Conflicts and the push for U.S. Energy Independence ▪ Growing Fuel Demand in the U.S. & Abroad ▪ Peak Oil Supply and High Prices (oil price from $30/brl in 2002 to $160/brl in 08) ▪ Ag and Rural Economic Development and Support ▪ Adoption of the Renewable Fuel Standard ▪ The economic drivers, that propelled that investment cycle, seem like they may be structurally changing at an accelerated rate. Some of these changes could provide opportunity, but there are a growing number that could create greater risk to today's ethanol business model. ▪ In a commodity business like ethanol, complacency is one of the biggest risks to business and if not addressed, it always ends up destroying shareholder value. Ethanol Industry - Introduction |

| Privileged and Confidential 5 ▪ Current ethanol economic drivers: ▪ The growth in transportation fuels will be outside the U.S. ▪ U.S. transportation fuel demand has plateaued and may start to decline because of higher fuel efficiency requirements and the growth in electric vehicle usage. ▪ Oil prices fell from $110/brl to $36/brl from 2014 to 2016. Price seemed to stabilize above $50/brl before Covid-19 this year. The Pandemic caused demand and prices to fall precipitately in March but has since recovered back above $50/brl. The U.S. shale fracking/ horizontal drilling technology has made the U.S. energy independent but will likely keep a lid on upward price pressure. ▪ The climate change issue continues to expand emphasis on carbon emissions providing opportunities and threats for ethanol. Ethanol has an opportunity to be a carbon reduction and pollution solution internationally, but risks being displaced by other renewable energies and technologies like wind, solar and electric vehicles. ▪ There is enough evidence of structural change that it should compel success minded ethanol companies to take a hard look at the potential changes to their business model. This will allow them to understand how the new business realities for competing in ethanol can be pursued proactively to get the right plan for their business and shareholders. Ethanol Industry - Introduction |

| Privileged and Confidential 6 ▪ World Economic and Energy Growth – It makes sense that the less developed countries with large populations and growing incomes will be the drivers of growth in vehicle sales and energy consumption in coming years. The biggest opportunity for ethanol growth is to be a carbon and pollution solution for growing gasoline consumption in China, India, Other Asia and Africa. China’s E10 mandate could create up to 5 billion gallons of demand if the U.S. gets market access. ▪ Carbon & Pollution Reduction - With the U.S. greenhouse gas reduction in electric generation, due to the transition from coal generation to natural gas and renewable electricity generation, transportation fuels carbon emissions are projected to be greater than all the other U.S. energy sources combined. This will keep transportation fuels emissions as a key pain point for the U.S. greenhouse gas reduction focus. Other countries where the U.S. has better relationships are also expanding carbon and pollution reduction efforts like Mexico and Japan. ▪ U.S. Fuel Efficiency - The Trump administration is attempting to slow fuel efficiency standards set by the Obama administration by freezing fuel standards and targeting more stringent state regulations like California. This issue is far from resolved, but it does point to the likelihood that fuel efficiency will not increase at the levels projected by EIA in their Jan 2019 energy outlook. Therefore, the decrease in projected gas consumption is likely overstated for the U.S. That being said, it doesn’t mean gas demand will likely grow. It is more likely that gas demand won’t decrease as drastically as projected by EIA. ▪ Electric Vehicle Adoption - The EIA EV projections all depends on the investment put to work in the next several years and the pace of consumer adoption. If they build it (invest $90B), will the consumer come? U.S. EV sales in 2018 were about 2% (200k) of new car sales and gas electric hybrids were about 8%. EIA projects that to be 10% (800k) by 2025 (5 years) and about 20% (2M) by 2050 (30 years). If there is broad adoption and the adoption curve applies here, it is likely that the 2025 % may be high, but the 2050 % might be to low. Regardless of the exact numbers, the trend for EV sales is very likely higher. Ethanol Industry – Opportunity & Threat Summary |

| Privileged and Confidential 7 ▪ Electric Vehicle Adoption - The accelerated adoption of EV at the global level is more likely to happen as developing countries, like China and India, with oil deficits and major pollution problems, look to solar and wind for more energy independence and pollution control. Of the approximately 2M EV sold in 2018, China purchased about 50%. By 2025, global EV production could be 15M to 20M, of which the U.S. would be a declining share of new car purchases from 10% to around 5% in 5 years. The global expansion of EVs and continued focus on GHG reduction, means the U.S. EV trend isn’t likely to subside regardless of political pressure that would push against EV expansion. ▪ Energy Supply and Prices - The U.S. shale fracking/horizontal drilling technology phenomenon that started in the 1980s and hit critical mass in 1990s for natural gas and 2000s for oil, has stabilized prices sub $60/brl for oil and sub $3/mmbtu for natural gas. It has also moved the U.S. from a major net importer of energy to a net exporter of energy in 20 years. EIA projects both of these energy sources to continue production growth for at least 5 years, but that isn’t where the production expansion stops. This predominantly U.S. technology is now moving global into China, Europe, Africa and others. Barring major energy shocks, these factors should hold down energy prices for many years. ▪ Ethanol Policy – As we look at the policy landscape, the reapplication of the Small Refiner Exemption has been critical to U.S. demand destruction and is a material driver to lower margins. In addition, there are numerous new changes coming from the RFS Reset Rule, with the potential for change to the RFS program after 2022 and a new administration. It is not clear if the current administration or future political changes will create opportunities or threats for ethanol going forward. The policy decisions we have seen like the Small Refiner Exemption, have destroyed ethanol demand. It is yet to be seen if the recent 10th circuit court ruling against 2017 SRE and the recently negotiated Phase I trade deal with China opens the E10 market. One of the most important drivers of the future of U.S. ethanol policy will likely be decided by the new administration. Ethanol Industry – Opportunity & Threat Summary |

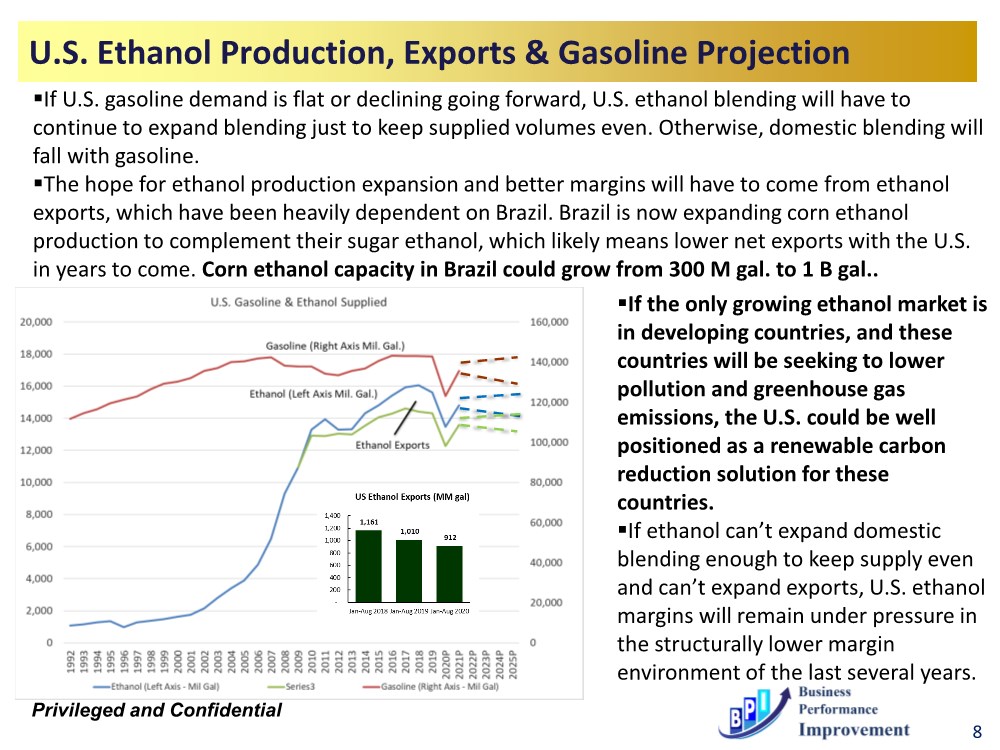

| Privileged and Confidential U.S. Ethanol Production, Exports & Gasoline Projection 8 ▪If U.S. gasoline demand is flat or declining going forward, U.S. ethanol blending will have to continue to expand blending just to keep supplied volumes even. Otherwise, domestic blending will fall with gasoline. ▪The hope for ethanol production expansion and better margins will have to come from ethanol exports, which have been heavily dependent on Brazil. Brazil is now expanding corn ethanol production to complement their sugar ethanol, which likely means lower net exports with the U.S. in years to come. Corn ethanol capacity in Brazil could grow from 300 M gal. to 1 B gal.. ▪If the only growing ethanol market is in developing countries, and these countries will be seeking to lower pollution and greenhouse gas emissions, the U.S. could be well positioned as a renewable carbon reduction solution for these countries. ▪If ethanol can’t expand domestic blending enough to keep supply even and can’t expand exports, U.S. ethanol margins will remain under pressure in the structurally lower margin environment of the last several years. |

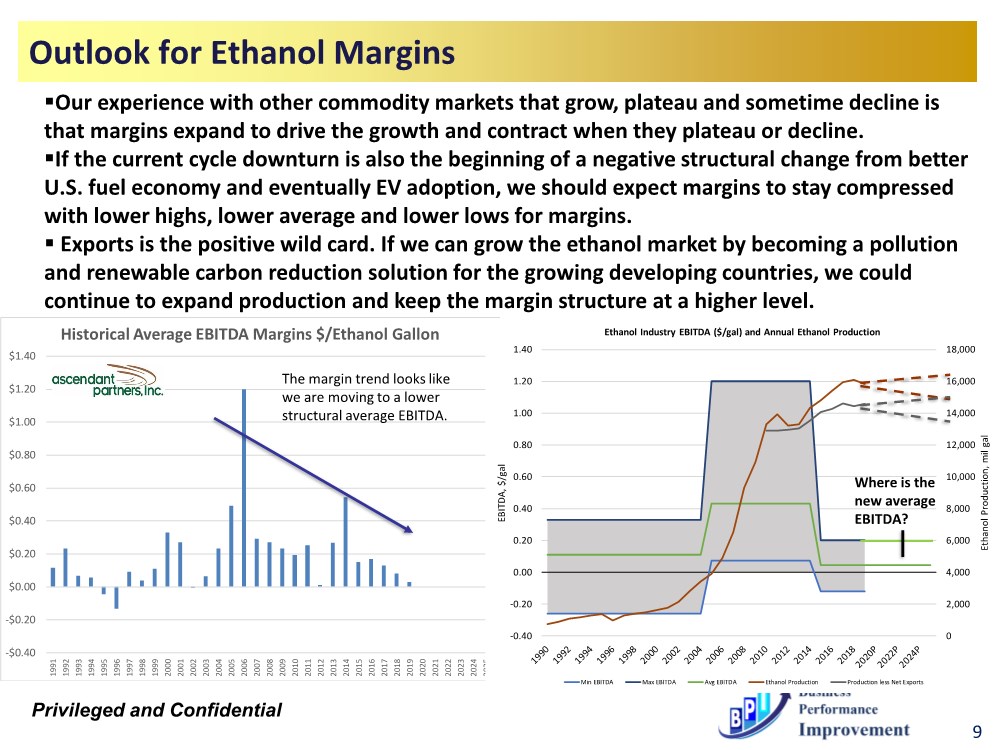

| Privileged and Confidential Outlook for Ethanol Margins 9 -$0.40 -$0.20 $0.00 $0.20 $0.40 $0.60 $0.80 $1.00 $1.20 $1.40 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 Historical Average EBITDA Margins $/Ethanol Gallon 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 -0.40 -0.20 0.00 0.20 0.40 0.60 0.80 1.00 1.20 1.40 Ethanol Production, mil gal EBITDA, $/gal Ethanol Industry EBITDA ($/gal) and Annual Ethanol Production Min EBITDA Max EBITDA Avg EBITDA Ethanol Production Production less Net Exports ▪Our experience with other commodity markets that grow, plateau and sometime decline is that margins expand to drive the growth and contract when they plateau or decline. ▪If the current cycle downturn is also the beginning of a negative structural change from better U.S. fuel economy and eventually EV adoption, we should expect margins to stay compressed with lower highs, lower average and lower lows for margins. ▪ Exports is the positive wild card. If we can grow the ethanol market by becoming a pollution and renewable carbon reduction solution for the growing developing countries, we could continue to expand production and keep the margin structure at a higher level. Where is the new average EBITDA? The margin trend looks like we are moving to a lower structural average EBITDA. |

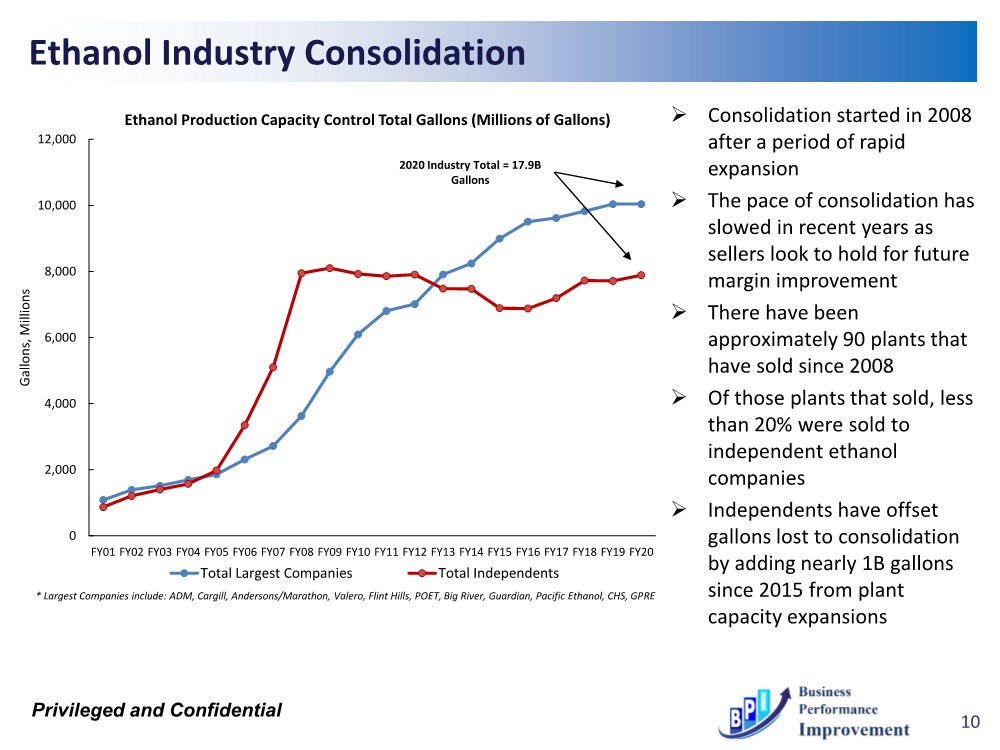

| Privileged and Confidential 0 2,000 4,000 6,000 8,000 10,000 12,000 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 Gallons, Millions Ethanol Production Capacity Control Total Gallons (Millions of Gallons) Total Largest Companies Total Independents 2020 Industry Total = 17.9B Gallons Ethanol Industry Consolidation 10 ➢ Consolidation started in 2008 after a period of rapid expansion ➢ The pace of consolidation has slowed in recent years as sellers look to hold for future margin improvement ➢ There have been approximately 90 plants that have sold since 2008 ➢ Of those plants that sold, less than 20% were sold to independent ethanol companies ➢ Independents have offset gallons lost to consolidation by adding nearly 1B gallons since 2015 from plant capacity expansions * Largest Companies include: ADM, Cargill, Andersons/Marathon, Valero, Flint Hills, POET, Big River, Guardian, Pacific Ethanol, CHS, GPRE |

| Privileged and Confidential 11 Stand-Alone ▪ There is a growing risk that this is not a long-term option that allows the company to be viable and sustain value for shareholders unless the company is a top EBITDA producer or the U.S. ethanol can be seen by other countries as a transportation fuel carbon and pollution reduction solution. Sale ▪ The sale values for this option have declined materially in the last year. Where active Midwest plants used to produce dividends and sell for $1.00/gal to $1.45/gal, the lower margin environment and difficult outlook have lowered value for the same businesses $0.30/gal to $1.25/gal (decline of 14% to 70% in value). If the outlook for lower domestic demand is wrong or policy begins to favor ethanol again or exports expand robustly, margins and valuations may move back to normalized levels. If the outlook presented comes to fruition and margins stay compressed, ethanol plant valuations will continue to decline. Diversification ▪ Ethanol plants have very robust infrastructure and strong processing capabilities. Some of these ethanol companies could invest in complementary businesses that are co-located. This would diversify the dependence on ethanol and grow the business from a strong base. Merger to Private ▪ A bigger company isn’t necessarily better. A strong company with a bigger balance sheet might be able to weather consolidation better, but it still locks owners into their concentration in the ethanol business. There isn’t a lot of overhead in independent ethanol companies that would normally be seen as a value uplift. The biggest value of private mergers of good ethanol companies is that they can invest in talent and add some regional diversification. There is still a challenge in valuation if they wanted to sell or raise more capital and a bigger company has fewer potential buyers. Mergers to Public ▪ Merging strong ethanol plants to a public company has advantages and disadvantages. The material disadvantages are that the plants would lose independence and becoming a public company can be expensive. The advantages are the same as merging to private (scale, talent and regional diversification), but the premium for stock traded in the public markets is material and can provide premium liquidity and little or no minority discounts for shareholders. It also gives the company access to growth capital to facilitate strategic investments. Ethanol Company Strategic Options for Repositioning the Business |

| Privileged and Confidential HLBE Valuation 12 |

| Privileged and Confidential Background 13 ➢ Heron Lake BioEnergy LLC (“HLBE”) owns and operates a 68MMGY denatured ethanol production facility in Heron Lake, MN. HLBE’s plant was designed by ICM Inc. as a 50MMGY plant and was built by Fagen, Inc.. The plant began operations in 2007. |

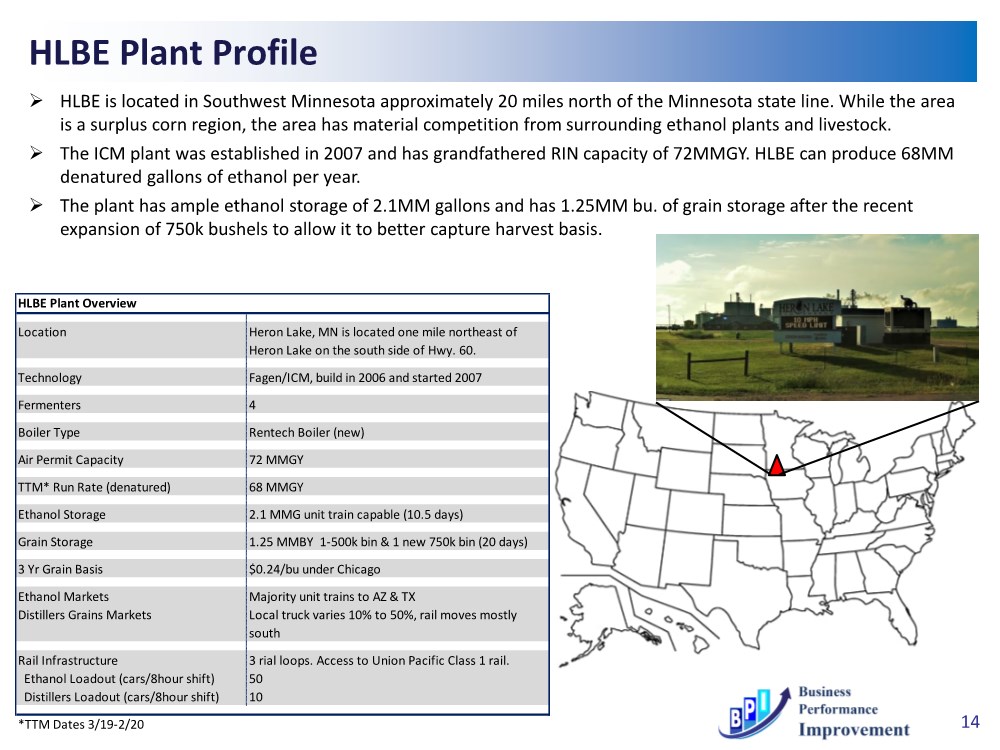

| Privileged and Confidential HLBE Plant Profile 14 ➢ HLBE is located in Southwest Minnesota approximately 20 miles north of the Minnesota state line. While the area is a surplus corn region, the area has material competition from surrounding ethanol plants and livestock. ➢ The ICM plant was established in 2007 and has grandfathered RIN capacity of 72MMGY. HLBE can produce 68MM denatured gallons of ethanol per year. ➢ The plant has ample ethanol storage of 2.1MM gallons and has 1.25MM bu. of grain storage after the recent expansion of 750k bushels to allow it to better capture harvest basis. HLBE Plant Overview Location Heron Lake, MN is located one mile northeast of Heron Lake on the south side of Hwy. 60. Technology Fagen/ICM, build in 2006 and started 2007 Fermenters 4 Boiler Type Rentech Boiler (new) Air Permit Capacity 72 MMGY TTM* Run Rate (denatured) 68 MMGY Ethanol Storage 2.1 MMG unit train capable (10.5 days) Grain Storage 1.25 MMBY 1-500k bin & 1 new 750k bin (20 days) 3 Yr Grain Basis $0.24/bu under Chicago Ethanol Markets Majority unit trains to AZ & TX Distillers Grains Markets Local truck varies 10% to 50%, rail moves mostly south Rail Infrastructure 3 rial loops. Access to Union Pacific Class 1 rail. Ethanol Loadout (cars/8hour shift) 50 Distillers Loadout (cars/8hour shift) 10 *TTM Dates 3/19-2/20 |

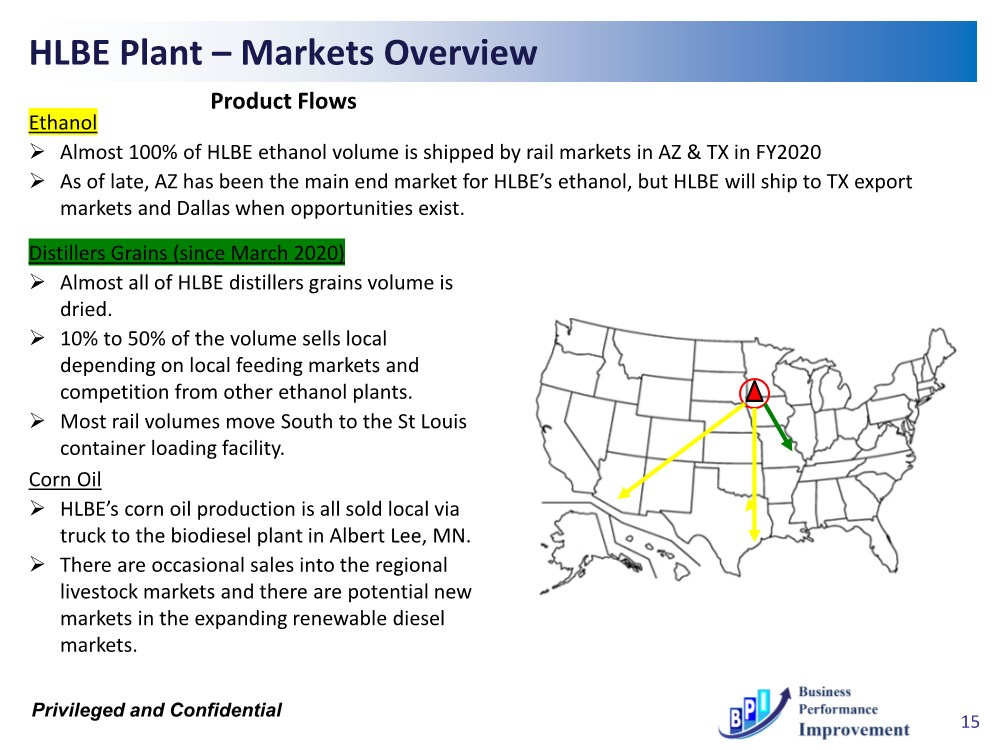

| Privileged and Confidential HLBE Plant – Markets Overview 15 Ethanol ➢ Almost 100% of HLBE ethanol volume is shipped by rail markets in AZ & TX in FY2020 ➢ As of late, AZ has been the main end market for HLBE’s ethanol, but HLBE will ship to TX export markets and Dallas when opportunities exist. Product Flows Distillers Grains (since March 2020) ➢ Almost all of HLBE distillers grains volume is dried. ➢ 10% to 50% of the volume sells local depending on local feeding markets and competition from other ethanol plants. ➢ Most rail volumes move South to the St Louis container loading facility. Corn Oil ➢ HLBE’s corn oil production is all sold local via truck to the biodiesel plant in Albert Lee, MN. ➢ There are occasional sales into the regional livestock markets and there are potential new markets in the expanding renewable diesel markets. |

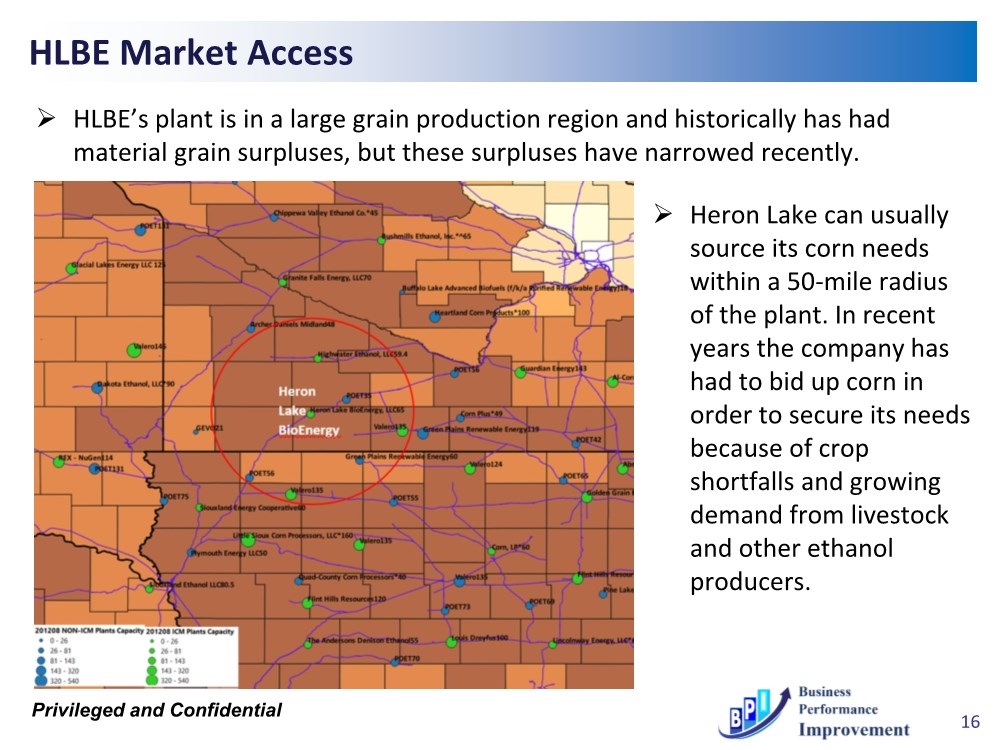

| Privileged and Confidential HLBE Market Access ➢ HLBE’s plant is in a large grain production region and historically has had material grain surpluses, but these surpluses have narrowed recently. 16 ➢ Heron Lake can usually source its corn needs within a 50-mile radius of the plant. In recent years the company has had to bid up corn in order to secure its needs because of crop shortfalls and growing demand from livestock and other ethanol producers. |

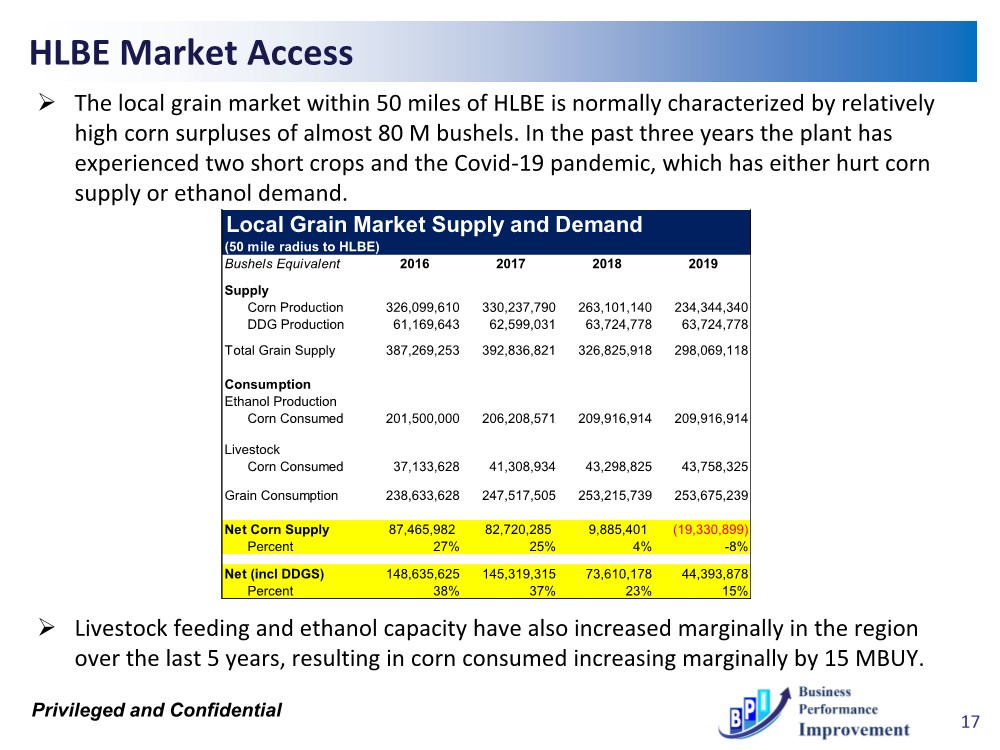

| Privileged and Confidential HLBE Market Access ➢ The local grain market within 50 miles of HLBE is normally characterized by relatively high corn surpluses of almost 80 M bushels. In the past three years the plant has experienced two short crops and the Covid-19 pandemic, which has either hurt corn supply or ethanol demand. 17 ➢ Livestock feeding and ethanol capacity have also increased marginally in the region over the last 5 years, resulting in corn consumed increasing marginally by 15 MBUY. Local Grain Market Supply and Demand (50 mile radius to HLBE) Bushels Equivalent 2016 2017 2018 2019 Supply Corn Production 326,099,610 330,237,790 263,101,140 234,344,340 DDG Production 61,169,643 62,599,031 63,724,778 63,724,778 Total Grain Supply 387,269,253 392,836,821 326,825,918 298,069,118 Consumption Ethanol Production Corn Consumed 201,500,000 206,208,571 209,916,914 209,916,914 Livestock Corn Consumed 37,133,628 41,308,934 43,298,825 43,758,325 Grain Consumption 238,633,628 247,517,505 253,215,739 253,675,239 Net Corn Supply 87,465,982 82,720,285 9,885,401 (19,330,899) Percent 27% 25% 4% -8% Net (incl DDGS) 148,635,625 145,319,315 73,610,178 44,393,878 Percent 38% 37% 23% 15% |

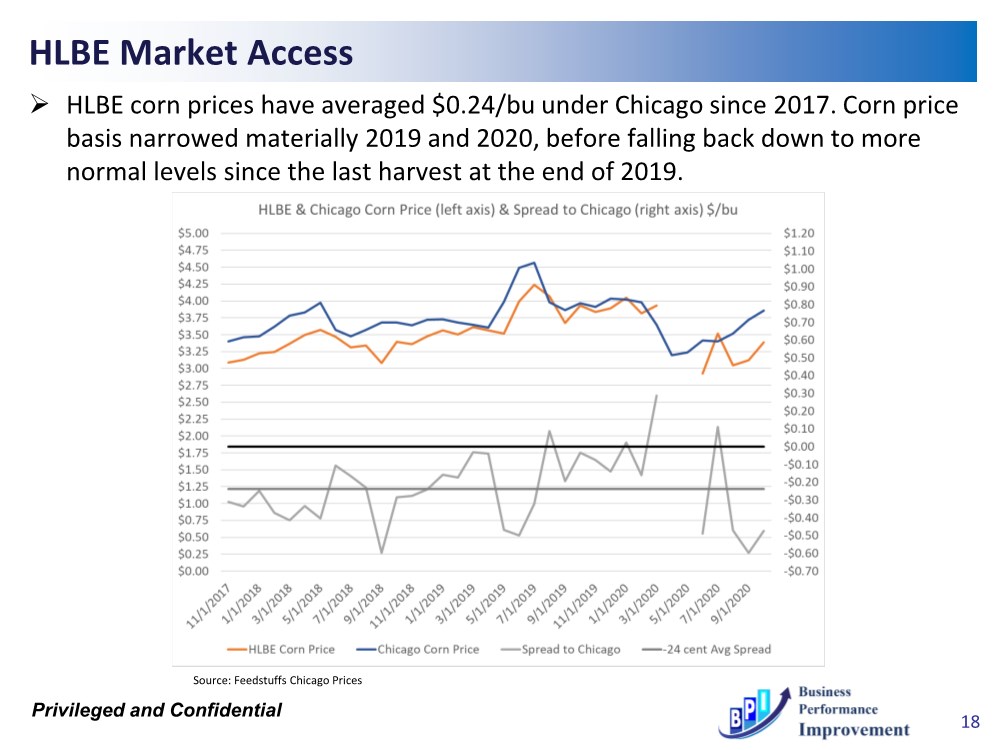

| Privileged and Confidential HLBE Market Access ➢ HLBE corn prices have averaged $0.24/bu under Chicago since 2017. Corn price basis narrowed materially 2019 and 2020, before falling back down to more normal levels since the last harvest at the end of 2019. 18 Source: Feedstuffs Chicago Prices |

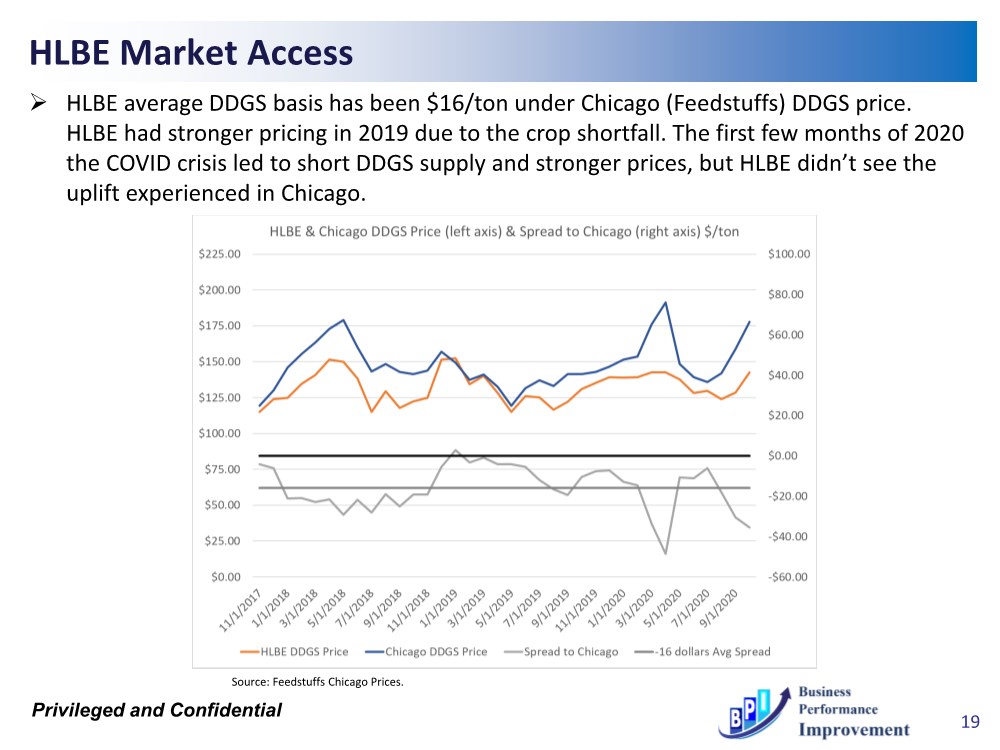

| Privileged and Confidential ➢ HLBE average DDGS basis has been $16/ton under Chicago (Feedstuffs) DDGS price. HLBE had stronger pricing in 2019 due to the crop shortfall. The first few months of 2020 the COVID crisis led to short DDGS supply and stronger prices, but HLBE didn’t see the uplift experienced in Chicago. HLBE Market Access 19 Source: Feedstuffs Chicago Prices. |

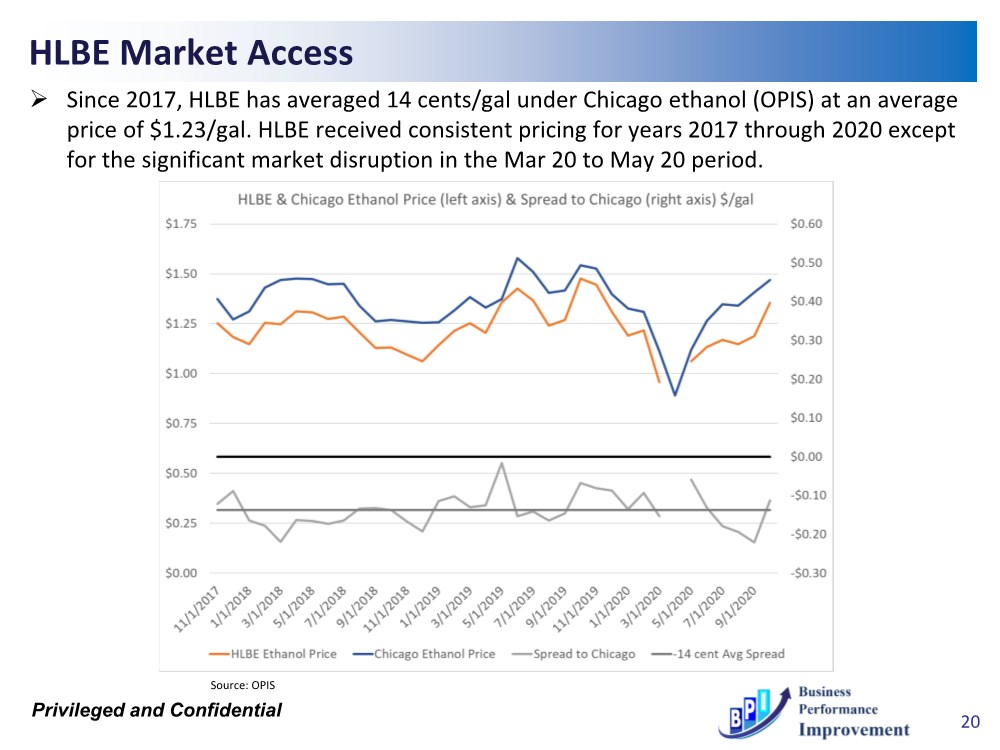

| Privileged and Confidential HLBE Market Access ➢ Since 2017, HLBE has averaged 14 cents/gal under Chicago ethanol (OPIS) at an average price of $1.23/gal. HLBE received consistent pricing for years 2017 through 2020 except for the significant market disruption in the Mar 20 to May 20 period. 20 Source: OPIS |

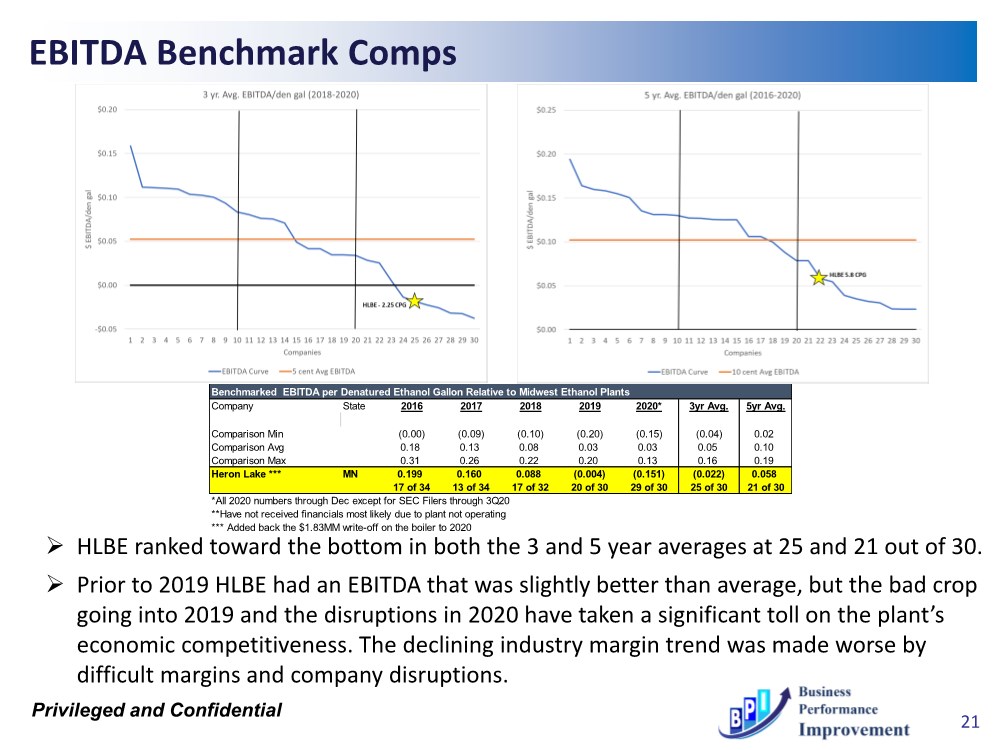

| Privileged and Confidential EBITDA Benchmark Comps 21 ➢ HLBE ranked toward the bottom in both the 3 and 5 year averages at 25 and 21 out of 30. ➢ Prior to 2019 HLBE had an EBITDA that was slightly better than average, but the bad crop going into 2019 and the disruptions in 2020 have taken a significant toll on the plant’s economic competitiveness. The declining industry margin trend was made worse by difficult margins and company disruptions. Benchmarked EBITDA per Denatured Ethanol Gallon Relative to Midwest Ethanol Plants Company State 2016 2017 2018 2019 2020* 3yr Avg. 5yr Avg. Comparison Min (0.00) (0.09) (0.10) (0.20) (0.15) (0.04) 0.02 Comparison Avg 0.18 0.13 0.08 0.03 0.03 0.05 0.10 Comparison Max 0.31 0.26 0.22 0.20 0.13 0.16 0.19 Heron Lake *** MN 0.199 0.160 0.088 (0.004) (0.151) (0.022) 0.058 17 of 34 13 of 34 17 of 32 20 of 30 29 of 30 25 of 30 21 of 30 *All 2020 numbers through Dec except for SEC Filers through 3Q20 **Have not received financials most likely due to plant not operating *** Added back the $1.83MM write-off on the boiler to 2020 |

| Privileged and Confidential Summary Market and Performance Implications ➢ A plant’s position on the EBITDA curve and the sustainability of that position should provide insight into market competitiveness, which is paramount for evaluating the best strategic options for the business. ➢ Why does your EBITDA curve position matter? ✓ Defines competitiveness ✓ Provides insight into long-term sustainability, which allows companies to assess strategic options ✓ Cash flow generation going forward ✓ Asset marketability ➢ Ultimately, marginal plants positioned near the bottom of the cost curve have to be more informed (as compared to top performing assets) of market conditions and how their competitiveness is changing in a consolidating and maturing industry. ➢ Large companies like GPRE and Valero can more easily idle marginal assets to bring supply down—this is much harder for small operators. 22 |

| Privileged and Confidential Valuation Due Diligence Summary ➢ The role of Due Diligence in Valuation ✓ The importance of due diligence reviews in valuation is to evaluate key business documentation to assess possible factors that might detract or enhance the valuation of the business for the seller and/or an outside buyer. ➢ BPI was able to review material due diligence items and didn’t find items that would either enhance or detract from the valuation of the company. ✓ In July 2020, the Company experienced major issues with its boiler, which negatively impacted production. The Company operated with temporary boilers from August 2020 through part of January 2021. The Company determined that the purchase and installation of a new boiler would be more economical and efficient than attempted repairs to the failing boiler. On September 2, 2020, the Company received notice of approval of the new boiler from the Minnesota Pollution Control Agency. As a result, the Company abandoned the failing boiler at that time. The Company recorded the loss on disposal as a component of operating expenses during the fourth fiscal quarter of the fiscal year ended October 31, 2020 of approximately $1.9 million. The new boiler was placed in service in January 2021 at an estimated cost of approximately $5.2 million. ✓ HLBE has received temporary approval for the new boiler from the MN Pollution Control Agency. It is expected to take up to two years for full approval of the new permit. 23 |

| Privileged and Confidential HLBE Valuation in Context of Liquidity Challenges ➢ The DCF valuation model is not intendant to assess a businesses cash flow from a liquidity standpoint. The DCF valuation method is used to estimate the value of an investment based on its expected future cash flows. DCF analysis attempts to figure out the value of an investment today, based on projections of how much money it will generate in the future. ➢ HLBE needs to move swiftly to keep their current liquidity crisis from becoming a solvency crisis, which permanently destroys equity in the business. The debt load generated over the last 18 months from investments, losses and structural changes to working capital, in conjunction with projected losses, are unsustainable for the business without a material capital injection. ➢ BPI recommends the company implement a 13-week cash flow tool to get a better handle on liquidity. The tool is a direct method to forecast weekly cash receipts less cash disbursements. The forecast is frequently used in turnaround situations when a company enters financial distress in order to provide visibility into the company's short-term options. ➢ The next step is to put together a recapitalization plan for the bank to give the company time to recapitalize the business. Recapitalization is the process of restructuring a company's debt and equity mixture, by raising money to stabilize a company's capital structure. The process mainly involves the exchange of one form of financing for another, such as removing debt from the company's capital structure and replacing it with new equity. 24 |

| Privileged and Confidential Valuation Approach Overview ➢ Two methods, discounted cash flow (DCF) and comparable transactions, were used to value HLBE operations: 25 ➢ DCF Method: ✓ Use historical performance to create a financial model with which to base future cash flow stream projections ✓ Project future company cash flows and discount back to present value using the cost of capital as the discount rate ➢Advantages ✓ Cash flow focus ✓ Grounded in actual historical performance ✓ Provides insight into key drivers of shareholder value ➢Challenges ✓ The challenge of reliably projecting future cash flows ✓ The importance of determining the appropriate discount rates ✓ The difficulty associated with estimating terminal value ✓ Doesn’t incorporate target specific, strategic value or discounts (e.g. grain assets) ➢ Comparable Transactions Method: ✓ ID comparable sales transactions and data ✓ Select subset of most comparable sales transactions ✓ Define key value drivers ✓ Assess premium/discounts based on plant attributes and timing ✓ Estimate range of expected sales values ➢ Advantages ✓ Based on actual sales values ✓ Provides insight into how buyers value ethanol operations ➢ Challenges ✓ Limited recent transaction set ✓ Selecting comparable transactions ✓ Subject to market conditions at the time of transaction |

| Privileged and Confidential DCF Model Approach and Assumptions ➢ The Company’s current fiscal year budget is used for the first year of projections, thereafter the five-year average EBITDA is used. ✓ Note, BPI used the highest EBITDA value, which is the 5 yr. avg EBITDA (5.8 cpg) with the FY2021 budget (-6.9 cpg) for the valuation. ➢ Total annual denatured ethanol production of 68MM gal. is used for the current and future fiscal years. ➢ Maintenance Capex of $0.55MM per year was assumed going forward to maintain the current plant operations. ➢ Total Debt of $25.7MM was projected using an expected principal payments ($3MM to $4MM annually) ✓ CoBank - Term Revolver $13MM, Term Note $2.7MM, Bridge Note (Due Jun 2021) $5MM & Granite Falls (boiler) $5MM ✓ The use of debt has been $5MM for the boiler, $3MM for new grain storage and the rest has been used to fund losses and meet the increased working capital requirements. CoBank wants a recapitalization plan by Apr 1, 2021. ➢ Discount rate calculated as the Weighted Average Cost of Capital (“WACC”) based on the Company’s borrowing rate, a 15% cost of equity, and the current actual capital structure. ➢ Tax Rate of 30%, and Working Capital based on historical Days Inventory, Payable, and Receivable. ➢ Depreciation is based on stepped up basis assuming a new buyer purchases the assets and gains the tax benefits of greater depreciation. ➢ The DCF calculates an Enterprise Value which we adjust to a Property, Plant, and Equipment (PPE) value by backing out normalized working capital of $.10/gal. ➢ Terminal Value Multiple of 5X EBITDA. 26 |

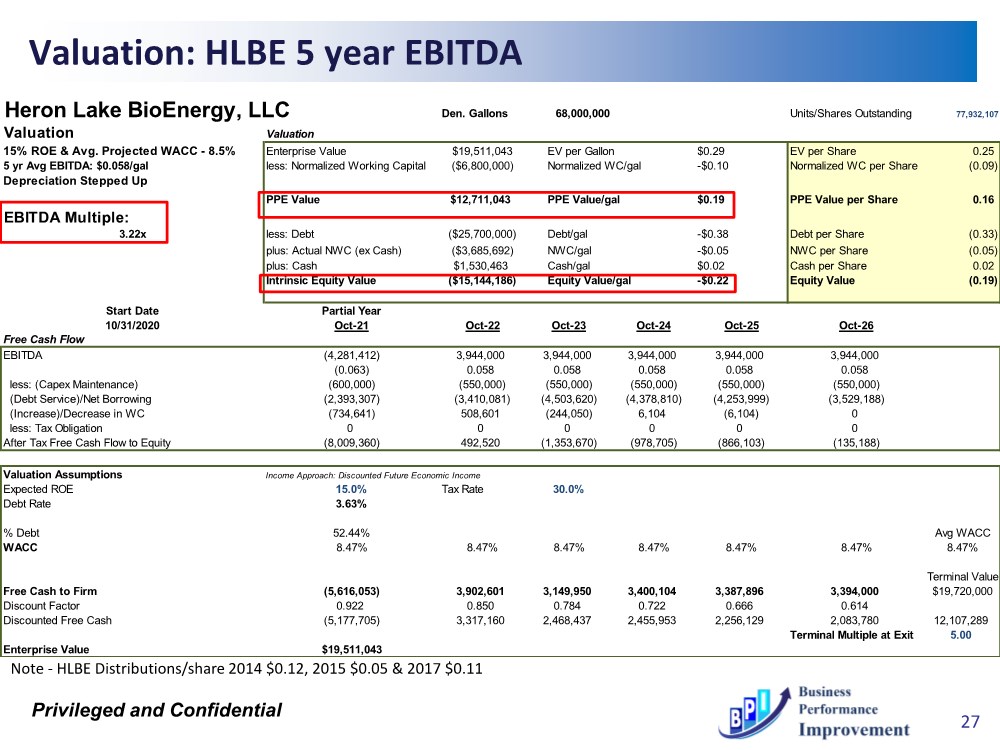

| Privileged and Confidential Heron Lake BioEnergy, LLC Den. Gallons 68,000,000 Units/Shares Outstanding 77,932,107 Valuation Valuation 15% ROE & Avg. Projected WACC - 8.5% Enterprise Value $19,511,043 EV per Gallon $0.29 EV per Share 0.25 5 yr Avg EBITDA: $0.058/gal less: Normalized Working Capital ($6,800,000) Normalized WC/gal -$0.10 Normalized WC per Share (0.09) Depreciation Stepped Up PPE Value $12,711,043 PPE Value/gal $0.19 PPE Value per Share 0.16 EBITDA Multiple: 3.22x less: Debt ($25,700,000) Debt/gal -$0.38 Debt per Share (0.33) plus: Actual NWC (ex Cash) ($3,685,692) NWC/gal -$0.05 NWC per Share (0.05) plus: Cash $1,530,463 Cash/gal $0.02 Cash per Share 0.02 Intrinsic Equity Value ($15,144,186) Equity Value/gal -$0.22 Equity Value (0.19) Start Date Partial Year 10/31/2020 Oct-21 Oct-22 Oct-23 Oct-24 Oct-25 Oct-26 Free Cash Flow EBITDA (4,281,412) 3,944,000 3,944,000 3,944,000 3,944,000 3,944,000 (0.063) 0.058 0.058 0.058 0.058 0.058 less: (Capex Maintenance) (600,000) (550,000) (550,000) (550,000) (550,000) (550,000) (Debt Service)/Net Borrowing (2,393,307) (3,410,081) (4,503,620) (4,378,810) (4,253,999) (3,529,188) (Increase)/Decrease in WC (734,641) 508,601 (244,050) 6,104 (6,104) 0 less: Tax Obligation 0 0 0 0 0 0 After Tax Free Cash Flow to Equity (8,009,360) 492,520 (1,353,670) (978,705) (866,103) (135,188) Valuation Assumptions Income Approach: Discounted Future Economic Income Expected ROE 15.0% Tax Rate 30.0% Debt Rate 3.63% % Debt 52.44% Avg WACC WACC 8.47% 8.47% 8.47% 8.47% 8.47% 8.47% 8.47% Terminal Value Free Cash to Firm (5,616,053) 3,902,601 3,149,950 3,400,104 3,387,896 3,394,000 $19,720,000 Discount Factor 0.922 0.850 0.784 0.722 0.666 0.614 Discounted Free Cash (5,177,705) 3,317,160 2,468,437 2,455,953 2,256,129 2,083,780 12,107,289 Terminal Multiple at Exit 5.00 Enterprise Value $19,511,043 Valuation: HLBE 5 year EBITDA 27 Note - HLBE Distributions/share 2014 $0.12, 2015 $0.05 & 2017 $0.11 |

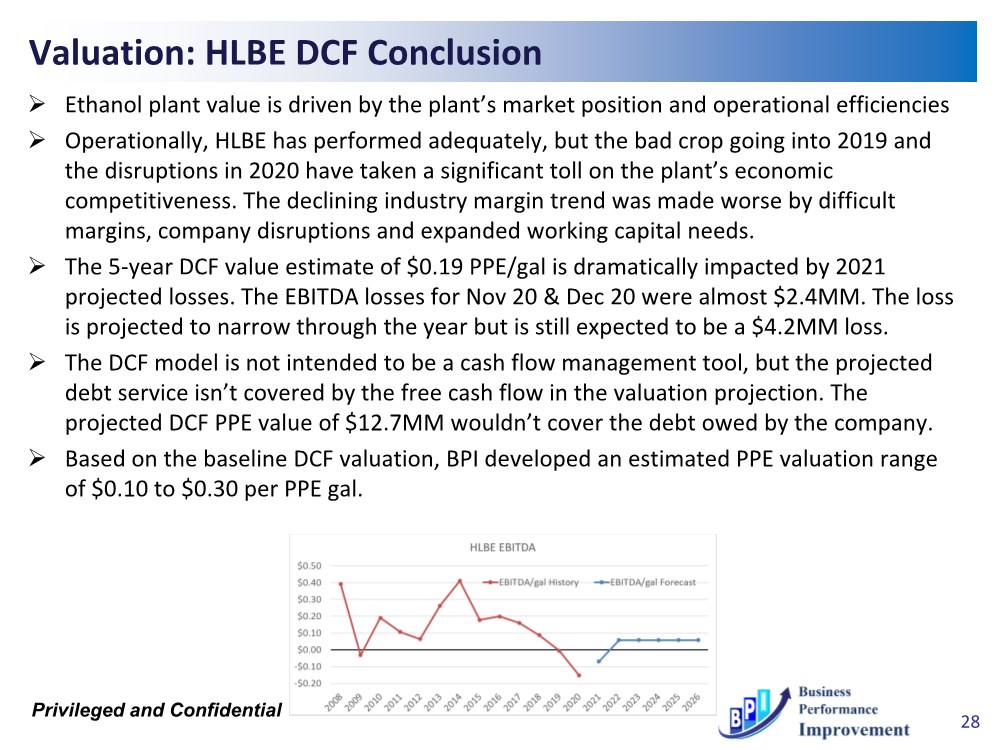

| Privileged and Confidential Valuation: HLBE DCF Conclusion ➢ Ethanol plant value is driven by the plant’s market position and operational efficiencies ➢ Operationally, HLBE has performed adequately, but the bad crop going into 2019 and the disruptions in 2020 have taken a significant toll on the plant’s economic competitiveness. The declining industry margin trend was made worse by difficult margins, company disruptions and expanded working capital needs. ➢ The 5-year DCF value estimate of $0.19 PPE/gal is dramatically impacted by 2021 projected losses. The EBITDA losses for Nov 20 & Dec 20 were almost $2.4MM. The loss is projected to narrow through the year but is still expected to be a $4.2MM loss. ➢ The DCF model is not intended to be a cash flow management tool, but the projected debt service isn’t covered by the free cash flow in the valuation projection. The projected DCF PPE value of $12.7MM wouldn’t cover the debt owed by the company. ➢ Based on the baseline DCF valuation, BPI developed an estimated PPE valuation range of $0.10 to $0.30 per PPE gal. 28 |

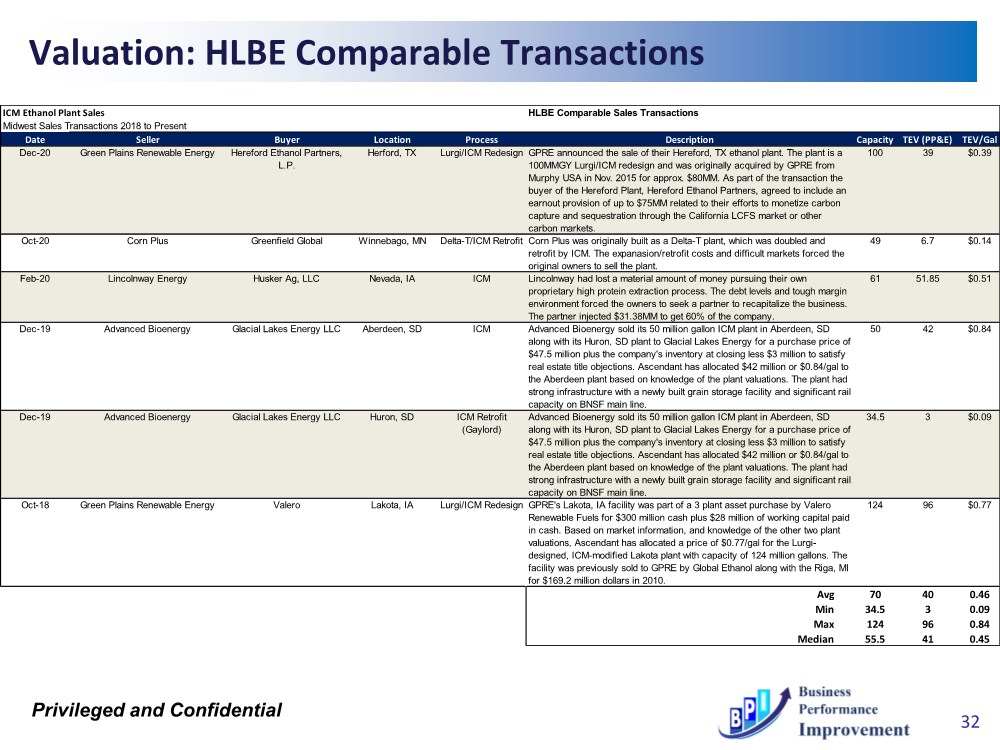

| Privileged and Confidential Valuation: Comparable Transaction Approach ➢ HLBE has several factors that influence the comparable transaction approach including: ✓ HLBE’s 68MMGY facility is an average size and doesn’t carry any premium or discount. ✓ Prospective buyers would like the robust infrastructure. ✓ ICM Designed facility is superior to a Delta-T plant because of lower maintenance cost and better energy efficiency ✓ Average historical yields and conversions are neutral ✓ EBITDA struggles would be the most important factor to prospective buyers in a tough market environment ➢ BPI selected comparable transactions on the basis of similar markets and plants positioned similarly on the EBITDA curve. ➢ While each transaction is unique and influenced by specific situations, comparable transactions serve to ground the valuation in a market-based approach. 29 |

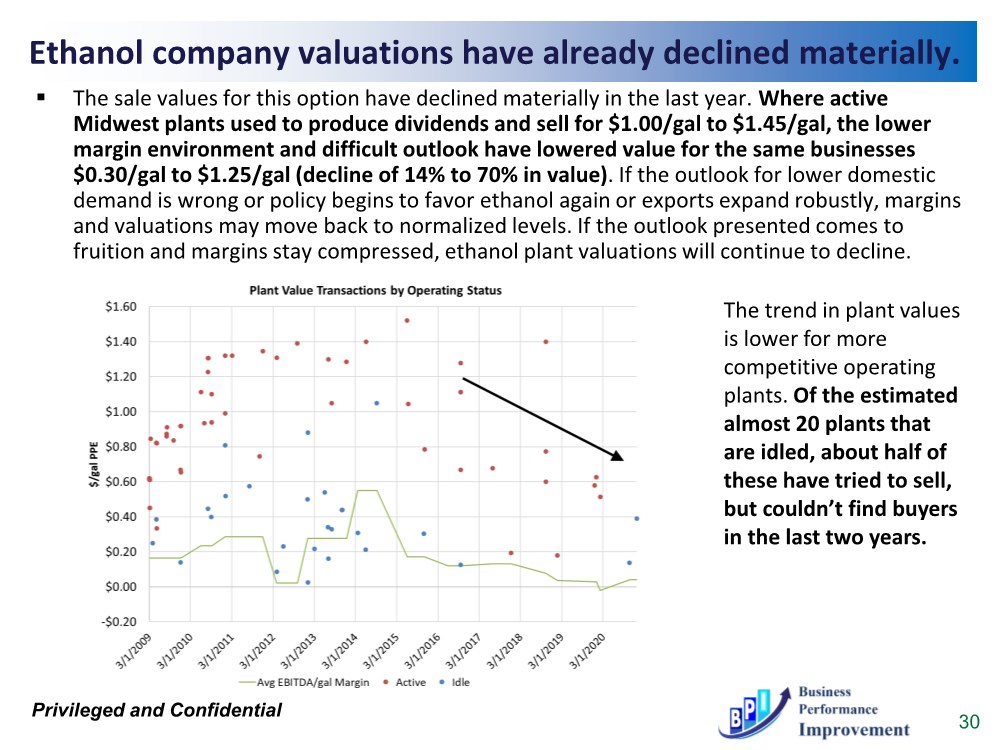

| Privileged and Confidential 30 ▪ The sale values for this option have declined materially in the last year. Where active Midwest plants used to produce dividends and sell for $1.00/gal to $1.45/gal, the lower margin environment and difficult outlook have lowered value for the same businesses $0.30/gal to $1.25/gal (decline of 14% to 70% in value). If the outlook for lower domestic demand is wrong or policy begins to favor ethanol again or exports expand robustly, margins and valuations may move back to normalized levels. If the outlook presented comes to fruition and margins stay compressed, ethanol plant valuations will continue to decline. Ethanol company valuations have already declined materially. The trend in plant values is lower for more competitive operating plants. Of the estimated almost 20 plants that are idled, about half of these have tried to sell, but couldn’t find buyers in the last two years. |

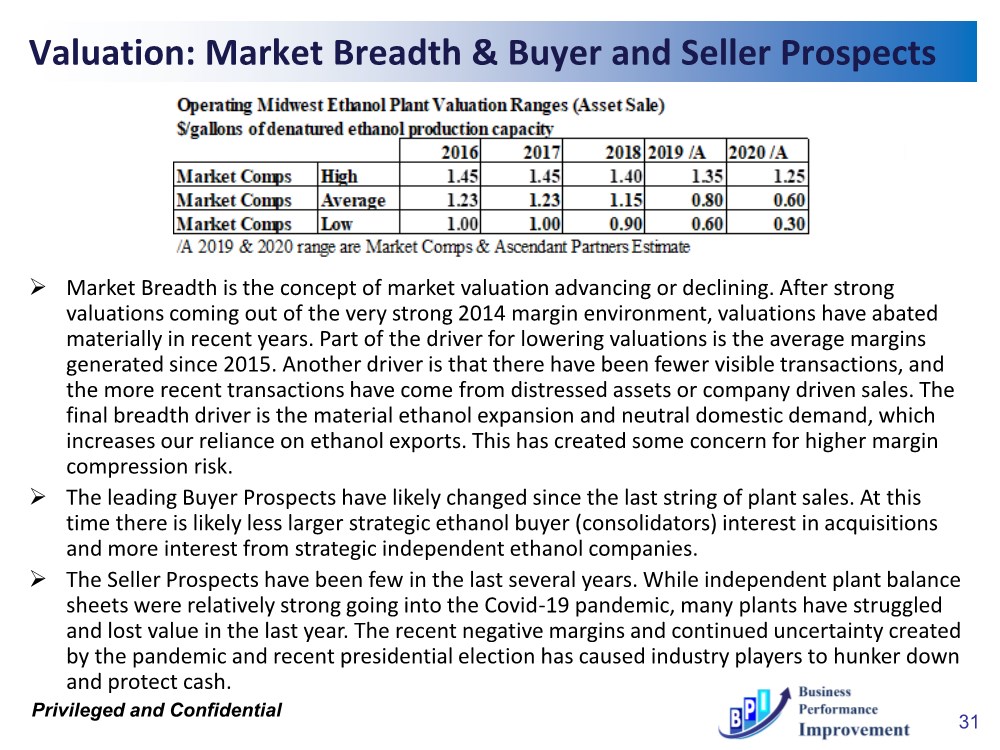

| Privileged and Confidential Valuation: Market Breadth & Buyer and Seller Prospects ➢ Market Breadth is the concept of market valuation advancing or declining. After strong valuations coming out of the very strong 2014 margin environment, valuations have abated materially in recent years. Part of the driver for lowering valuations is the average margins generated since 2015. Another driver is that there have been fewer visible transactions, and the more recent transactions have come from distressed assets or company driven sales. The final breadth driver is the material ethanol expansion and neutral domestic demand, which increases our reliance on ethanol exports. This has created some concern for higher margin compression risk. ➢ The leading Buyer Prospects have likely changed since the last string of plant sales. At this time there is likely less larger strategic ethanol buyer (consolidators) interest in acquisitions and more interest from strategic independent ethanol companies. ➢ The Seller Prospects have been few in the last several years. While independent plant balance sheets were relatively strong going into the Covid-19 pandemic, many plants have struggled and lost value in the last year. The recent negative margins and continued uncertainty created by the pandemic and recent presidential election has caused industry players to hunker down and protect cash. 31 |

| Privileged and Confidential Valuation: HLBE Comparable Transactions 32 ICM Ethanol Plant Sales HLBE Comparable Sales Transactions Midwest Sales Transactions 2018 to Present Date Seller Buyer Location Process Description Capacity TEV (PP&E) TEV/Gal Dec-20 Green Plains Renewable Energy Hereford Ethanol Partners, L.P. Herford, TX Lurgi/ICM Redesign GPRE announced the sale of their Hereford, TX ethanol plant. The plant is a 100MMGY Lurgi/ICM redesign and was originally acquired by GPRE from Murphy USA in Nov. 2015 for approx. $80MM. As part of the transaction the buyer of the Hereford Plant, Hereford Ethanol Partners, agreed to include an earnout provision of up to $75MM related to their efforts to monetize carbon capture and sequestration through the California LCFS market or other carbon markets. 100 39 $0.39 Oct-20 Corn Plus Greenfield Global Winnebago, MN Delta-T/ICM Retrofit Corn Plus was originally built as a Delta-T plant, which was doubled and retrofit by ICM. The expanasion/retrofit costs and difficult markets forced the original owners to sell the plant. 49 6.7 $0.14 Feb-20 Lincolnway Energy Husker Ag, LLC Nevada, IA ICM Lincolnway had lost a material amount of money pursuing their own proprietary high protein extraction process. The debt levels and tough margin environment forced the owners to seek a partner to recapitalize the business. The partner injected $31.38MM to get 60% of the company. 61 51.85 $0.51 Dec-19 Advanced Bioenergy Glacial Lakes Energy LLC Aberdeen, SD ICM Advanced Bioenergy sold its 50 million gallon ICM plant in Aberdeen, SD along with its Huron, SD plant to Glacial Lakes Energy for a purchase price of $47.5 million plus the company's inventory at closing less $3 million to satisfy real estate title objections. Ascendant has allocated $42 million or $0.84/gal to the Aberdeen plant based on knowledge of the plant valuations. The plant had strong infrastructure with a newly built grain storage facility and significant rail capacity on BNSF main line. 50 42 $0.84 Dec-19 Advanced Bioenergy Glacial Lakes Energy LLC Huron, SD ICM Retrofit (Gaylord) Advanced Bioenergy sold its 50 million gallon ICM plant in Aberdeen, SD along with its Huron, SD plant to Glacial Lakes Energy for a purchase price of $47.5 million plus the company's inventory at closing less $3 million to satisfy real estate title objections. Ascendant has allocated $42 million or $0.84/gal to the Aberdeen plant based on knowledge of the plant valuations. The plant had strong infrastructure with a newly built grain storage facility and significant rail capacity on BNSF main line. 34.5 3 $0.09 Oct-18 Green Plains Renewable Energy Valero Lakota, IA Lurgi/ICM Redesign GPRE's Lakota, IA facility was part of a 3 plant asset purchase by Valero Renewable Fuels for $300 million cash plus $28 million of working capital paid in cash. Based on market information, and knowledge of the other two plant valuations, Ascendant has allocated a price of $0.77/gal for the Lurgi- designed, ICM-modified Lakota plant with capacity of 124 million gallons. The facility was previously sold to GPRE by Global Ethanol along with the Riga, MI for $169.2 million dollars in 2010. 124 96 $0.77 Avg 70 40 0.46 Min 34.5 3 0.09 Max 124 96 0.84 Median 55.5 41 0.45 |

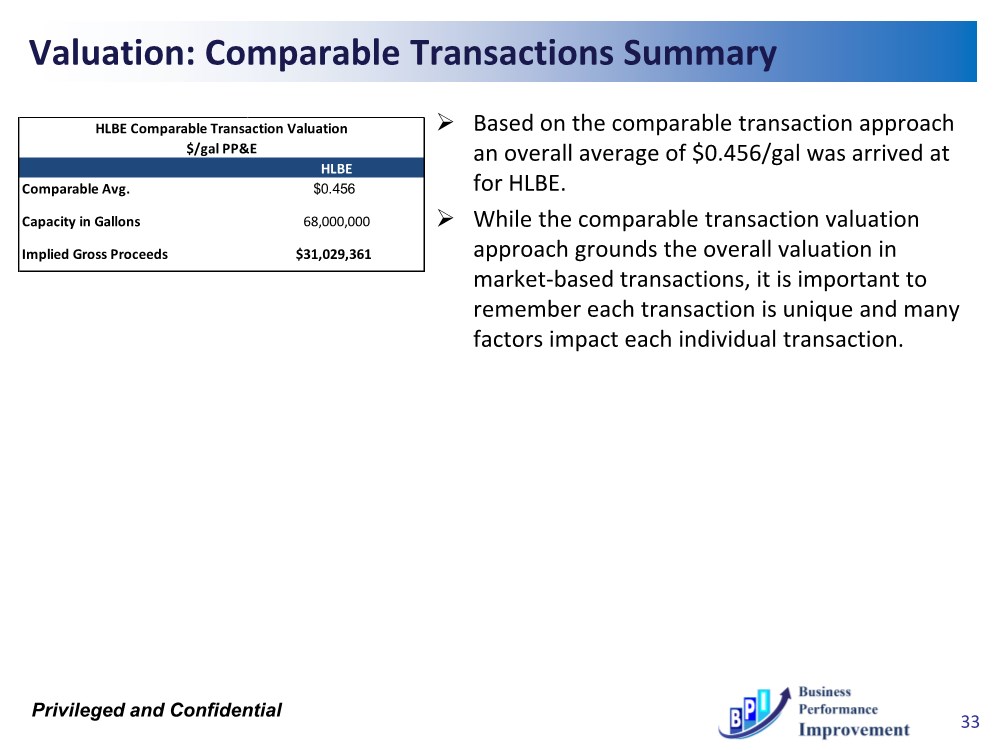

| Privileged and Confidential Valuation: Comparable Transactions Summary ➢ Based on the comparable transaction approach an overall average of $0.456/gal was arrived at for HLBE. ➢ While the comparable transaction valuation approach grounds the overall valuation in market-based transactions, it is important to remember each transaction is unique and many factors impact each individual transaction. 33 HLBE Comparable Avg. $0.456 Capacity in Gallons 68,000,000 Implied Gross Proceeds $31,029,361 HLBE Comparable Transaction Valuation $/gal PP&E |

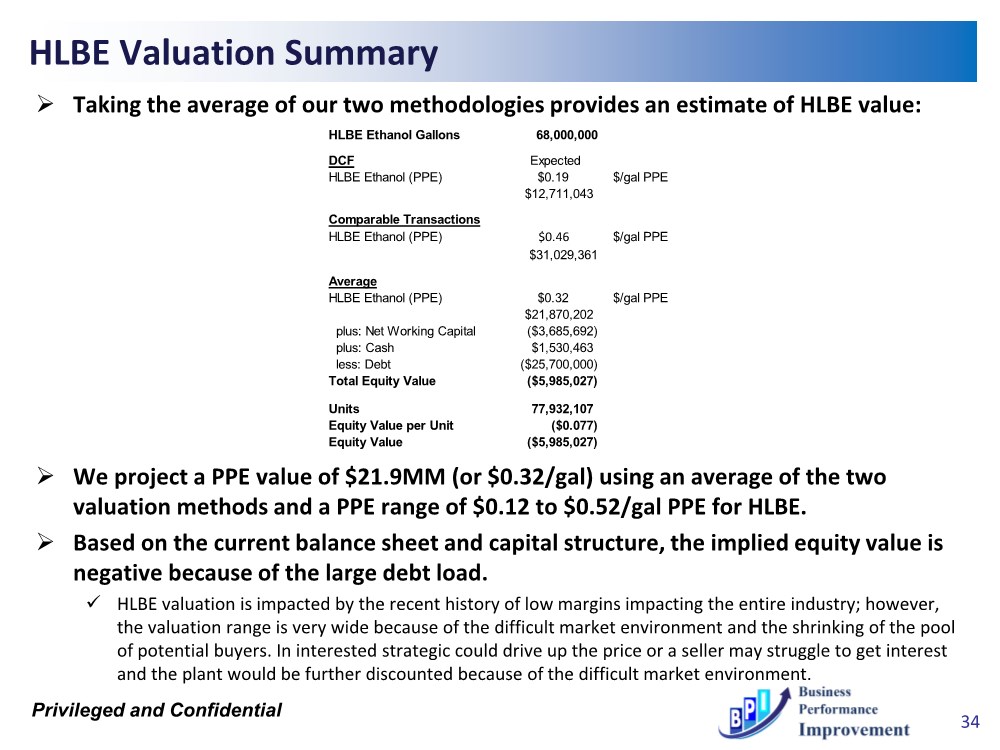

| Privileged and Confidential HLBE Valuation Summary ➢ Taking the average of our two methodologies provides an estimate of HLBE value: ➢ We project a PPE value of $21.9MM (or $0.32/gal) using an average of the two valuation methods and a PPE range of $0.12 to $0.52/gal PPE for HLBE. ➢ Based on the current balance sheet and capital structure, the implied equity value is negative because of the large debt load. ✓ HLBE valuation is impacted by the recent history of low margins impacting the entire industry; however, the valuation range is very wide because of the difficult market environment and the shrinking of the pool of potential buyers. In interested strategic could drive up the price or a seller may struggle to get interest and the plant would be further discounted because of the difficult market environment. 34 HLBE Ethanol Gallons 68,000,000 DCF Expected HLBE Ethanol (PPE) $0.19 $/gal PPE $12,711,043 Comparable Transactions HLBE Ethanol (PPE) $0.46 $/gal PPE $31,029,361 Average HLBE Ethanol (PPE) $0.32 $/gal PPE $21,870,202 plus: Net Working Capital ($3,685,692) plus: Cash $1,530,463 less: Debt ($25,700,000) Total Equity Value ($5,985,027) Units 77,932,107 Equity Value per Unit ($0.077) Equity Value ($5,985,027) |

| Privileged and Confidential Discussions and Questions 35 |