ANNUAL INFORMATION FORM

For the financial year ended December 31, 2013

Dated March 29, 2014

Table of Contents

| Page | |||

| PRELIMINARY INFORMATION | 1 | ||

| Date of Information | 1 | ||

| Incorporation by Reference of Documents | 1 | ||

| Cautionary Statement Regarding Forward-Looking Statements | 1 | ||

| Cautionary Note to U.S. Investors Regarding Reserve and Resource Estimates | 3 | ||

| Currency | 3 | ||

| ITEM 1: | CORPORATE STRUCTURE | 4 | |

| 1.1 | Name, Address and Incorporation | 4 | |

| 1.2 | Intercorporate Relationships | 4 | |

| ITEM 2: | GENERAL DEVELOPMENT OF THE BUSINESS | 5 | |

| ITEM 3: | DESCRIPTION OF THE BUSINESS | 11 | |

| 3.1 | General | 11 | |

| 3.2 | Risk Factors | 15 | |

| 3.3 | Banro's Gold Properties | 28 | |

| 3.3.1 | Twangiza | 28 | |

| 3.3.2 | Namoya | 42 | |

| 3.3.3 | Lugushwa | 53 | |

| 3.3.4 | Kamituga | 57 | |

| 3.3.5 | Other Exploration Properties | 60 | |

| 3.3.6 | Qualified Persons | 61 | |

| ITEM 4: | DIVIDENDS | 61 | |

| ITEM 5: | DESCRIPTION OF CAPITAL STRUCTURE | 61 | |

| 5.1 | Authorized Share Capital | 61 | |

| 5.2 | Notes | 63 | |

| 5.3 | Warrants | 66 | |

| 5.4 | Shareholder Rights Plan | 66 | |

| 5.5 | Exchangeable Preferred Shares | 67 | |

| ITEM 6: | MARKET FOR SECURITIES | 68 | |

| 6.1 | Common Shares | 68 | |

| 6.2 | Series A Preference Shares | 68 | |

| ITEM 7: | ESCROWED SECURITIES AND SECURITIES SUBJECT TO CONTRACTUAL RESTRICTION ON TRANSFER | 69 | |

| ITEM 8: | DIRECTORS AND OFFICERS | 69 | |

| 8.1 | Name, Occupation and Security Holding | 69 | |

| 8.2 | Corporate Cease Trade Orders or Bankruptcies | 72 | |

| 8.3 | Personal Bankruptcies | 73 | |

| 8.4 | Penalties or Sanctions | 73 | |

| 8.5 | Conflicts of Interest | 73 | |

| ITEM 9: | AUDIT COMMITTEE INFORMATION | 74 | |

| ITEM 10: | PROMOTERS | 76 | |

TABLE OF CONTENTS

(continued)

| Page | ||

| ITEM 11: | LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 76 |

| ITEM 12: | INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 76 |

| ITEM 13: | TRANSFER AGENTS AND REGISTRAR | 77 |

| ITEM 14: | MATERIAL CONTRACTS | 77 |

| ITEM 15: | INTERESTS OF EXPERTS | 79 |

| 15.1 | Names of Experts | 79 |

| 15.2 | Interests of Experts | 79 |

| ITEM 16: | ADDITIONAL INFORMATION | 79 |

SCHEDULE "A" - AUDIT COMMITTEE TERMS OF REFERENCE

PRELIMINARY INFORMATION

Date of Information

All information in this annual information form ("AIF") is as at December 31, 2013, unless otherwise indicated.

Incorporation by Reference of Documents

The following documents are incorporated by reference into, and form part of, this AIF:

| (a) | the consolidated financial statements (the "Annual Financial Statements") of Banro Corporation ("Banro" or the "Company") for the year ended December 31, 2013, together with the auditors’ report thereon dated March 29, 2014; and |

| (b) | the Company’s management’s discussion and analysis (the "Annual MD&A") for the year ended December 31, 2013. |

A copy of these documents can be obtained from SEDAR at www.sedar.com and EDGAR at www.sec.gov. Certain other documents, or excerpts therefrom, as set out in item 3.3 of this AIF are also incorporated by reference into, and form part of, this AIF.

Any statement contained in a document incorporated by reference herein is not incorporated by reference to the extent that any such statement is modified or superseded by a statement contained herein. Any such modifying or superseding statement need not state that it has modified or superseded a prior statement or include any other information set forth in the document that it modifies or supersedes.

Cautionary Statement Regarding Forward-Looking Statements

This AIF and the documents (or excerpts therefrom) incorporated by reference herein contains "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995 and "forward-looking information" within the meaning of Canadian provincial securities laws (such forward-looking statements and forward-looking information are referred to herein as "forward-looking statements"). Forward-looking statements are necessarily based on a number of estimates and assumptions that are inherently subject to significant business, economic and competitive uncertainties and contingencies. All statements, other than statements which are reporting results as well as statements of historical fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future (including, without limitation, statements regarding estimates and/or assumptions in respect of gold production, revenue, cash flow and costs, estimated project economics, mineral resource and mineral reserve estimates, potential mineralization, potential mineral resources and mineral reserves, projected timing of future gold production and the Company's exploration, development and production plans and objectives with respect to its projects) are forward-looking statements. These forward-looking statements reflect the current expectations or beliefs of the Company based on information currently available to the Company. Forward-looking statements are subject to a number of risks and uncertainties that may cause the actual events or results of the Company to differ materially from those discussed in the forward-looking statements, and even if such actual events or results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: uncertainty of estimates of capital and operating costs, production and economic returns; uncertainties relating to the estimates and assumptions used in the economic studies of the Company's projects; the early stage of gold production at the Company’s Twangiza mine; delay in achieving commercial gold production at the Company’s Namoya mine by the end of the second quarter of 2014 as planned; the Company’s current level of indebtedness; failure to establish estimated mineral resources or mineral reserves; fluctuations in gold prices and currency exchange rates; inflation; gold recoveries being less than those indicated by the metallurgical testwork carried out to date (there can be no assurance that gold recoveries in small scale laboratory tests will be duplicated in large tests under on-site conditions or during production) or less than those expected following the planned expansion of the Twangiza plant; changes in equity markets; political developments in the Democratic Republic of the Congo (the "DRC"); lack of infrastructure; implementation of rules adopted by the U.S. Securities and Exchange Commission that may affect mining operations in the DRC; failure to procure or maintain, or delays in procuring or maintaining, permits and approvals; lack of availability at a reasonable cost or at all, of plants, equipment or labour; inability to attract and retain key management and personnel; changes to regulations or policies affecting the Company's activities; uncertainties relating to the availability and costs of financing in the future; the uncertainties involved in interpreting drilling results and other geological data; the Company's history of losses; the Company's ability to acquire additional commercially mineable mineral rights; risks related to the integration of any new acquisitions into the Company's existing operations; increased competition in the mining industry; and the other risks disclosed in item 3.2 ("Risk Factors") of this AIF.

| 1 |

Any forward-looking statement speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking statement, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking statements are reasonable, forward-looking statements are not guarantees of future performance and accordingly undue reliance should not be put on such statements due to the inherent uncertainty therein.

The mineral resource and mineral reserve figures referred to in this AIF are estimates and no assurances can be given that the indicated levels of gold will be produced. Such estimates are expressions of judgment based on knowledge, mining experience, analysis of drilling results and industry practices. Valid estimates made at a given time may significantly change when new information becomes available. While the Company believes that the resource and reserve estimates included in this AIF are well established, by their nature, resource and reserve estimates are imprecise and depend, to a certain extent, upon statistical inferences which may ultimately prove unreliable. If such estimates are inaccurate or are reduced in the future, this could have a material adverse impact on the Company.

Due to the uncertainty that may be attached to inferred mineral resources, it cannot be assumed that all or any part of an inferred mineral resource will be upgraded to an indicated or measured mineral resource as a result of continued exploration. Confidence in the estimate is insufficient to allow meaningful application of the technical and economic parameters to enable an evaluation of economic viability sufficient for public disclosure, except in certain limited circumstances. Inferred mineral resources are excluded from estimates forming the basis of a feasibility study.

Statements concerning actual mineral reserve and mineral resource estimates are also deemed to constitute forward-looking statements to the extent that they involve estimates of the mineralization that will be encountered if (or as) the relevant project or property is developed (or mined). Mineral resources that are not mineral reserves do not have demonstrated economic viability. There is no certainty that mineral resources can be upgraded to mineral reserves through continued exploration.

| 2 |

Cautionary Note to U.S. Investors Regarding Reserve and Resource Estimates

This AIF, including the documents (or excerpts therefrom) incorporated by reference herein, has been prepared in accordance with the requirements of securities laws in effect in Canada, which differ from the requirements of U.S. securities laws. Without limiting the foregoing, this AIF, including the documents (or excerpts therefrom) incorporated by reference herein, uses the terms "measured", "indicated" and "inferred" resources. U.S. investors are advised that, while such terms are recognized and required by Canadian securities laws, the U.S. Securities and Exchange Commission (the "SEC") does not recognize them. Under U.S. standards, mineralization may not be classified as a "reserve" unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. U.S. investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into reserves. Further, "inferred resources" have a great amount of uncertainty as to their existence and as to whether they can be mined legally or economically. It cannot be assumed that all or any part of the "inferred resources" will ever be upgraded to a higher category. Therefore, U.S. investors are also cautioned not to assume that all or any part of the inferred resources exist, or that they can be mined legally or economically. Disclosure of "contained ounces" is permitted disclosure under Canadian regulations, however, the SEC normally only permits issuers to report mineral deposits that do not constitute "reserves" as in place tonnage and grade without reference to unit measures. Accordingly, information concerning descriptions of mineralization and resources contained in this AIF or in the documents (or excerpts therefrom) incorporated by reference, may not be comparable to information made public by U.S. companies subject to the reporting and disclosure requirements of the SEC.

National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101") is a rule of the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Unless otherwise indicated, all reserve and resource estimates contained in or incorporated by reference in this AIF have been prepared in accordance with NI 43-101 and the Canadian Institute of Mining, Metallurgy and Petroleum Classification System. These standards differ significantly from the requirements of the SEC, and reserve and resource information contained herein and incorporated by reference herein may not be comparable to similar information disclosed by U.S. companies. One consequence of these differences is that "reserves" calculated in accordance with Canadian standards may not be "reserves" under the SEC standards.

U.S. investors are urged to consider closely the disclosure in the Company's Form 40-F Annual Report (File No. 001-32399), which may be secured from the Company, or from the SEC's website at http://www.sec.gov.

Currency

All dollar amounts in this AIF are expressed in United States dollars, except as otherwise indicated. References to "$" or "US$" are to United States dollars and references to "Cdn$" are to Canadian dollars, except as otherwise indicated. For United States dollars to Canadian dollars, based on the Bank of Canada nominal noon rate, the average exchange rate for 2013 and the exchange rate at December 31, 2013 were one United States dollar per $1.0299 and $1.0636 Canadian dollars, respectively. For reporting purposes, the Company prepares its financial statements in United States dollars and in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board.

| 3 |

ITEM 1: CORPORATE STRUCTURE

| 1.1 | Name, Address and Incorporation |

The head office and registered office of Banro is located at 1 First Canadian Place, Suite 7070, 100 King Street West, Toronto, Ontario, M5X 1E3, Canada. The Company was incorporated under the Canada Business Corporations Act (the "CBCA") on May 3, 1994 by articles of incorporation. Pursuant to articles of amendment effective May 7, 1996, the name of the Company was changed from Banro International Capital Inc. to Banro Resource Corporation and the authorized share capital of the Company was increased by creating an unlimited number of a new class of shares designated as preference shares, issuable in series. The Company was continued under the Ontario Business Corporations Act by articles of continuance effective on October 24, 1996. By articles of amendment effective on January 16, 2001, the name of the Company was changed to Banro Corporation and the Company's outstanding common shares were consolidated on a three old for one new basis. The Company was continued under the CBCA by articles of continuance dated April 2, 2004. By articles of amendment dated December 17, 2004, the Company's outstanding common shares were subdivided by changing each one of such shares into two common shares. Pursuant to articles of amendment dated April 23, 2013, (a) a series of preference shares of the Company was created consisting of an unlimited number of shares designated as Series A Preference Shares, and (b) a second series of preference shares of the Company was created consisting of an unlimited number of shares designated as Series B Preference Shares. The said articles of amendment dated April 23, 2013 (a copy of which can be obtained from SEDAR at www.sedar.com) also provided for the rights, privileges, restrictions and conditions attaching to the said Series A Preference Shares and Series B Preference Shares.

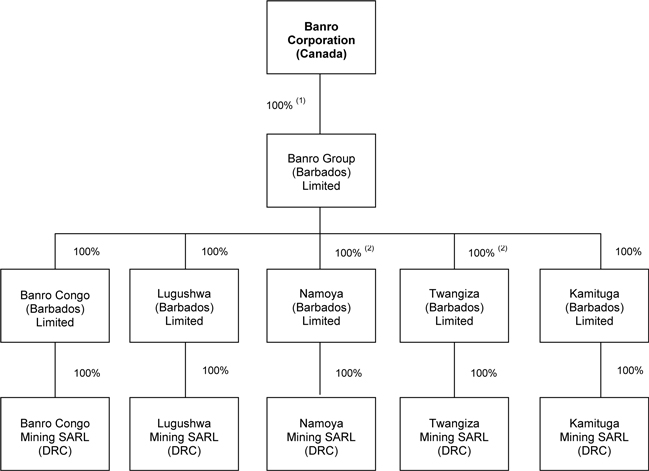

| 1.2 | Intercorporate Relationships |

The following chart illustrates the relationship between Banro and its material subsidiaries, together with the jurisdiction of incorporation of each such subsidiary and the percentage of voting securities beneficially owned, or controlled or directed, directly or indirectly, by Banro.

| 4 |

Notes to the above chart:

| (1) | Banro Group (Barbados) Limited also has outstanding preferred shares which were issued pursuant to the US$30 million private placement financing transaction completed in April 2013. See item 5.1 of this AIF ("Authorized Share Capital") for additional information in respect of this transaction and the said preferred shares. |

| (2) | Each of Namoya (Barbados) Limited and Twangiza (Barbados) Limited also has outstanding preferred shares which were issued pursuant to the US$40 million private placement financing transaction completed in February 2014 (US$20 million private placement in respect of each such subsidiary). See item 5.5 of this AIF ("Exchangeable Preferred Shares") for additional information in respect of this transaction and the said preferred shares. |

ITEM 2: GENERAL DEVELOPMENT OF THE BUSINESS

Banro is a Canadian gold mining company focused on production from the Twangiza gold mine in the DRC, which began commercial production September 1, 2012, and completion of its second gold mine at Namoya located in the DRC approximately 200 kilometres southwest of the Twangiza gold mine. Namoya commenced gold production in December 2013, with commercial production planned to be achieved at Namoya by the end of the second quarter of 2014. The Company's longer term objectives include the development of two additional major, wholly-owned gold projects, Lugushwa and Kamituga, each of which has mining licenses. The four projects are located along the 210 kilometre long Twangiza-Namoya gold belt in the South Kivu and Maniema provinces of the DRC.

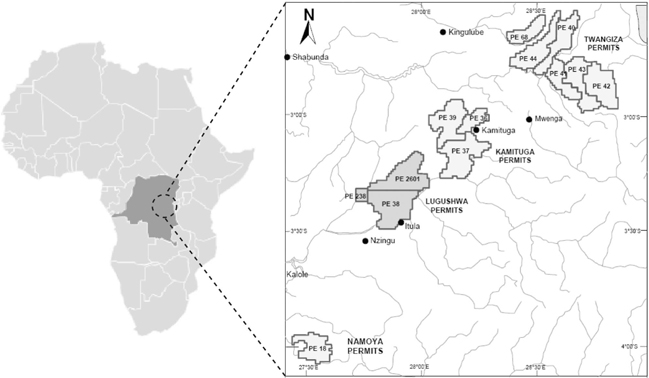

The Company holds a 100% interest in its said four gold properties (Twangiza, Namoya, Lugushwa and Kamituga) through four DRC subsidiaries (which in turn are held by Barbados subsidiaries of the Company; see the chart in item 1.2 of this AIF ("Intercorporate Relationships") above). These properties, totalling approximately 2,612 square kilometres, are covered by a total of 13 exploitation permits (or mining licenses) and cover all the major, historical producing areas of the gold belt. The Company also holds, through its fifth DRC subsidiary, 14 exploration permits covering an aggregate of 2,638 square kilometres. Ten of the exploration permits are located in the vicinity of the Company's Twangiza property and four are located in the vicinity of the Company's Namoya property.

General Development of the Business

Background

In 1996, the Company acquired, by way of several transactions, 72% of the outstanding shares of the DRC company, Société Zaïroise Minière et Industrielle du Kivu S.A.R.L. ("SOMINKI"). The DRC government held the remaining 28% of SOMINKI's shares as a participating interest. SOMINKI, which held 100% of the Twangiza, Namoya, Lugushwa and Kamituga properties, was an operating, very well-established mining company in the DRC with a long production history. With the acquisition of control of SOMINKI, the Company also acquired SOMINKI's significant library of geological and exploration data that had accumulated since the early 1920s.

In early 1997, the DRC government ratified a new 25 year (subsequently extended to 30 years) mining convention (the "Mining Convention") among itself, SOMINKI and the Company. The Mining Convention provided for the transfer of all of the mineral assets and real property of SOMINKI to a newly created DRC company, Société Aurifère du Kivu et du Maniema S.A.R.L. ("SAKIMA"), and that 93% of SAKIMA's shares were to be held by the Company, with the remaining 7% to be owned by the DRC government as a non-dilutive interest. The Mining Convention also provided for, among other things, confirmation of title in respect of all of the Twangiza, Namoya, Lugushwa and Kamituga properties.

| 5 |

Commencing in August 1997 and ending in April 1998, the Company carried out a phase I exploration program on the Twangiza property which consisted of geological mapping, surveying, data verification, airborne geophysical surveying, diamond drilling and resource modeling.

In July 1998, the DRC government, without prior warning or consultation, issued Presidential decrees which effectively resulted in the expropriation of the Company's properties.

In April 2002, the DRC government formally signed a settlement agreement (the "Settlement Agreement") with the Company. The Settlement Agreement called for, among other things, the Company to hold a 100% interest in the Twangiza, Namoya, Lugushwa and Kamituga properties under a revived Mining Convention. In accordance with the Settlement Agreement, the Company reorganized the said properties by transferring them from SAKIMA to four newly-created, wholly-owned DRC subsidiaries of the Company (which are named Twangiza Mining SARL, Namoya Mining SARL, Lugushwa Mining SARL and Kamituga Mining SARL), each of which owns 100% of its respective property.

In late 2003, the Company re-opened its exploration office in the town of Bukavu in eastern DRC.

Recruitment of Management

During 2004, the Company recruited a management team with extensive African and gold industry experience. Included in the people who joined the Company during 2004 were Peter N. Cowley as Chief Executive Officer, President and a director, Simon F.W. Village as Chairman of the Board and a director, Michael B. Skead as Exploration Manager (later promoted to Vice President, Exploration) and Dr. John A. Clarke as a director (Dr. Clarke was appointed Chief Executive Officer and President of the Company in 2013; see below).

Resumption of Exploration

In November 2004, the Company commenced exploration activities at the Namoya property and in January 2005 the Company commenced exploration activities at the Lugushwa property. The Company commenced the second phase of exploration at the Twangiza property in October 2005.

Stock Exchange Listings

On March 28, 2005, the Company's common shares began trading on the American Stock Exchange (which is now called the NYSE MKT LLC) (the "NYSE MKT"). On November 10, 2005, the Company's common shares began trading on the Toronto Stock Exchange (the "TSX") and ceased trading on the TSX Venture Exchange concurrent with the TSX listing. RBC Capital Markets acted as sponsor to Banro in its application for listing on the TSX.

Financings (2004 to 2006)

In March 2004, the Company completed a Cdn$16,000,000 private placement financing.

In July 2005, the Company completed an Cdn$18,375,000 private placement financing. This placement was made to an investment fund managed by Capital Research and Management Company and to institutional accounts managed by affiliates of Capital Group International, Inc.

| 6 |

In October 2005, the Company completed a non-brokered Cdn$13,000,000 private placement financing. The subscribers in respect of this financing were an investment fund managed by Actis Capital LLP and an investment fund co-managed by Actis Capital LLP and Cordiant Capital Inc.

In May 2006, the Company completed an equity financing for total gross proceeds of Cdn$56,012,800. The underwriters who conducted this financing were RBC Capital Markets as lead manager, Raymond James Ltd. and MGI Securities Inc.

Acquisition of Additional Properties

In March 2007, the Company announced that its wholly-owned DRC subsidiary, Banro Congo Mining SARL, had acquired 14 exploration permits covering certain ground located between and contiguous to the Company's Twangiza, Kamituga and Lugushwa properties. The applications for these permits were originally filed with the Mining Cadastral shortly after implementation of the DRC's new Mining Code in June 2003.

2007 Preliminary Assessments of Twangiza and Namoya

In July 2007, the Company announced the results of its preliminary assessments (i.e. "scoping studies") of its Namoya and Twangiza properties.

Hiring of New CEO in 2007

Michael J. Prinsloo was appointed Chief Executive Officer of the Company effective September 17, 2007. Mr. Prinsloo was hired to lead the Company's transition from gold explorer to developer. Prior to joining Banro, Mr. Prinsloo had accumulated some 35 years of experience in the gold mining industry, including acting as Head of South African Operations of Gold Fields Limited from 2002 to 2006. Mr. Prinsloo was also appointed President of the Company in March 2008 following the retirement of Peter N. Cowley as President.

Twangiza Pre-Feasibility Study

In July 2008, the Company announced results of the pre-feasibility study of the Company's Twangiza property.

2008 Financing

In September 2008, the Company completed an equity financing for total gross proceeds of US$21,000,000. This financing was completed through a syndicate of underwriters led by RBC Capital Markets and including CIBC World Markets Inc., UBS Securities Canada Inc. and Raymond James Ltd.

Twangiza Feasibility Study

In January 2009, the Company announced results of the feasibility study of the Company's Twangiza property.

Twangiza Updated Feasibility Study

In June 2009, the Company announced updated results of the feasibility study of the Company's Twangiza property.

| 7 |

2009 Financings

In February 2009, the Company completed a non-brokered equity financing for total gross proceeds of US$14,000,000.

In June 2009, the Company completed an equity financing for total gross proceeds of Cdn$100,001,700. The financing was conducted through a syndicate of underwriters co-led by GMP Securities L.P. and CIBC World Markets Inc.

Title Confirmation and Ratification of Fiscal Arrangement

In February 2009, the Company announced that following discussions it has received official confirmation from the DRC government that all aspects of the Company's Mining Convention and its mining licenses respecting the Twangiza, Namoya, Lugushwa and Kamituga properties are in accordance with Congolese law.

In August 2009, the DRC government ratified the fiscal arrangement between the DRC government and the Company. The Company has agreed to enhance its existing commitment to the DRC and the local communities of South Kivu and the Maniema provinces through:

| · | An advance payment of US$2 million to the DRC government when the Company completes the equity and debt financing process for construction of the mine at Twangiza, with the funds to be used to support social infrastructure development in the Twangiza and Luhwindja communities and to be credited against future taxes; |

| · | A pledge of US$200,000 to settle legacy issues with SOMINKI and the transfer to the central government of certain real estate assets redundant to the Company's operations; |

| · | 4% of net profits, after return of capital, allocated through the central government to the communities of South Kivu and Maniema provinces for the building of infrastructure projects, including roads and bridges, schools and health care facilities; and |

| · | A royalty of 1% on gold revenues. |

Purchase of Gold Plant and Commencement of Construction of Gold Mine at Twangiza

The Company completed in September 2009 the purchase of a refurbished gold processing plant capable of achieving an upgraded throughput capacity of 1.3 million tonnes per annum. SENET Engineering was selected as the overall project manager and also to manage the erection and commissioning of the plant. The Company began mobilizing equipment at Twangiza in January 2010 in order to facilitate the commencement of construction activities in February 2010. The resettlement process involving all consultative activities with local community members and the construction of resettlement houses commenced during the fourth quarter of 2009. Work on bridge upgrades and roads to the Twangiza site commenced in February 2010.

2010 Financing

In May 2010, the Company completed an equity financing for total gross proceeds of Cdn$137,555,000. The financing was conducted through a syndicate of underwriters co-led by GMP Securities L.P. and CIBC World Markets Inc.

| 8 |

Management Changes in 2010

In August 2010, the Company announced the restructuring of its executive management group and that it had fully staffed the mine development team responsible for constructing the Twangiza gold mine. The restructuring included the departure of Michael J. Prinsloo as President and Chief Executive Officer of the Company in September 2010. Simon F.W. Village, who was Banro’s Chairman of the Board at the time of Mr. Prinsloo’s departure, succeeded Mr. Prinsloo as President and Chief Executive Officer of the Company. Gary Chapman, who joined Banro in July 2010, took over responsibility for mine development from Mr. Prinsloo.

2011 Preliminary Assessment of Namoya Heap Leach Project

In January 2011, the Company announced the results of a preliminary assessment of a heap leach project at Namoya (the "2011 Namoya Study"). The 2011 Namoya Study, which was prepared with input from a number of independent consultants, followed on from the 2007 preliminary assessment of Namoya (see "Preliminary Assessments of Twangiza and Namoya" above) which assumed a CIL (carbon-in-leach) only processing route for the mineral resources. The 2011 Namoya Study assumed a heap leach only processing route and was undertaken to assess a lower capital cost alternative to the previous CIL option.

2011 Financing

In February 2011, the Company completed an equity financing for total gross proceeds of Cdn$56,875,000. The financing was conducted through a syndicate of investment dealers led by GMP Securities L.P. and included CIBC World Markets Inc., Cormark Securities Inc. and Raymond James Canada Inc.

Twangiza Oxide Project Economic Assessment

In March 2011, the Company announced the results of an economic assessment in respect of the Twangiza oxide project. This economic assessment was prepared with input from a number of independent consultants.

Commencement of Gold Production at Twangiza

In October 2011, the Company announced first gold production at its Twangiza property.

Updated Economic Assessment of Namoya Project

In January 2012, the Company announced the results of an updated economic assessment for the Namoya project (the "2012 Namoya Study"). The Namoya project was planned to have two phases, with Phase 1 involving a CIL/gravity and heap leach process ("gravity heap leach") for the recovery of easily leachable oxide and transitional ores and Phase II involving a milling/carbon-in-leach (CIL) plant to treat the fresh rock and optimize recoveries. The 2012 Namoya Study relates only to the Namoya project Phase 1 production potential.

The 2011 Namoya Study, which utilized the delineated measured, indicated and inferred mineral resources at that time, was based on an agglomerated heap leach model for ore processing. The 2012 Namoya Study was based on a gravity heap leach operation without the need to agglomerate, and uses the updated measured and indicated mineral resources for Namoya announced by the Company in December 2011.

| 9 |

2012 Debt Financing

In March 2012, the Company closed a brokered private placement debt financing for total gross proceeds of US$175 million. The financing was conducted by a syndicate of investment dealers comprising GMP Securities and BMO Capital Markets (as co-lead managers and co-book-runners) and CIBC World Markets Inc., Cormark Securities Inc. and Dundee Securities Ltd. as co-managers.

This debt financing involved an offering by the Company of 175,000 units consisting of US$175,000,000 aggregate principal amount of senior secured notes with an interest rate of 10% and a maturity date of March 1, 2017 (the "Notes") and 8,400,000 warrants (the "Warrants") to purchase an aggregate of 8,400,000 common shares of the Company. Each such unit consisted of US$1,000 principal amount of Notes and 48 Warrants, with each Warrant entitling the holder to purchase one common share of the Company at a price of US$6.65 for a period of five years from the date of issuance of the Warrant.

Commencement of Construction of Banro’s Second Gold Mine

The Company commenced construction of its second gold mine, at Namoya, in 2012.

Commencement of Commercial Production at Twangiza

Effective September 1, 2012, commercial production was declared by the Company at its Twangiza gold mine.

New CEO in 2013

In March 2013, the Company announced that Simon F.W. Village had stepped down from his roles as President and Chief Executive Officer of the Company, and that the board of directors of the Company had appointed Dr. John A. Clarke (who has served on Banro's board of directors since 2004) to the role of interim President and Chief Executive Officer of the Company. In December 2013, the Company announced that Dr. Clarke has been appointed to the permanent role of President and Chief Executive Officer from the interim President and Chief Executive Officer role he had been filling since March 2013.

2013 Financings

In April 2013, the Company closed a short form prospectus offering (the "Offering") of common shares of the Company and series A preference shares of the Company, together with a concurrent private placement (the "Concurrent Offering") of preferred shares of a subsidiary of the Company ("Subco Shares") and associated series B preference shares of the Company ("Series B Shares"). The Offering consisted of 50,218,634 common shares of the Company priced at Cdn$1.35 per share for gross aggregate proceeds of Cdn$67,795,156 and 116,000 series A preference shares of the Company priced at US$25.00 per share for gross aggregate proceeds of US$2,900,000. The Concurrent Offering consisted of 1,200,000 Subco Shares and 1,200,000 associated Series B Shares priced at US$25.00 per Subco Share and Series B Share for gross aggregate proceeds of US$30,000,000. The Offering was conducted by a syndicate of agents. Reference is made to item 5.1 of this AIF ("Authorized Share Capital") for additional information with respect to the said series A preference shares, Subco Shares and Series B Shares.

The Company also secured during 2013 US$53 million in short term loans from several lenders. Reference is made to the Annual Financial Statements (which are incorporated by reference into, and form part of, this AIF) for the details in respect of these loans.

| 10 |

Commencement of Gold Production at Banro’s Second Mine

In December 2013, the Company announced first gold production at its Namoya project. Commercial production at Namoya is planned to be achieved by the end of the second quarter of 2014.

2014 Financing

In February 2014 the Company closed a US$40 million financing involving the issue of exchangeable preferred shares to investment funds managed by Gramercy Funds Management LLC by way of a non-brokered private placement. Reference is made to item 5.5 of this AIF ("Exchangeable Preferred Shares") for additional information with respect to the said preferred shares.

ITEM 3: DESCRIPTION OF THE BUSINESS

| 3.1 | General |

Banro is a Canadian gold mining company focused on production from the Twangiza gold mine in the DRC, which began commercial production September 1, 2012, and completion of its second gold mine at Namoya located in the DRC approximately 200 kilometres southwest of the Twangiza gold mine. Namoya commenced gold production in December 2013, with commercial production planned to be achieved at Namoya by the end of the second quarter of 2014. The Company's longer term objectives include the development of two additional major, wholly-owned gold projects, Lugushwa and Kamituga, each of which has mining licenses. The four projects are located along the 210 kilometre long Twangiza-Namoya gold belt in the South Kivu and Maniema provinces of the DRC.

The Company holds a 100% interest in its said four gold properties (Twangiza, Namoya, Lugushwa and Kamituga) through four DRC subsidiaries (which in turn are held by Barbados subsidiaries of the Company; see the chart in item 1.2 of this AIF ("Intercorporate Relationships") above). These properties, totalling approximately 2,612 square kilometres, are covered by a total of 13 exploitation permits (or mining licenses) and cover all the major, historical producing areas of the gold belt. See items 3.3.1, 3.3.2, 3.3.3 and 3.3.4 of this AIF for additional information relating to the said four properties. The Company also holds, through its fifth DRC subsidiary (Banro Congo Mining SARL), 14 exploration permits covering an aggregate of 2,638 square kilometres. Ten of the exploration permits are located in the vicinity of the Company's Twangiza property and four are located in the vicinity of the Company's Namoya property.

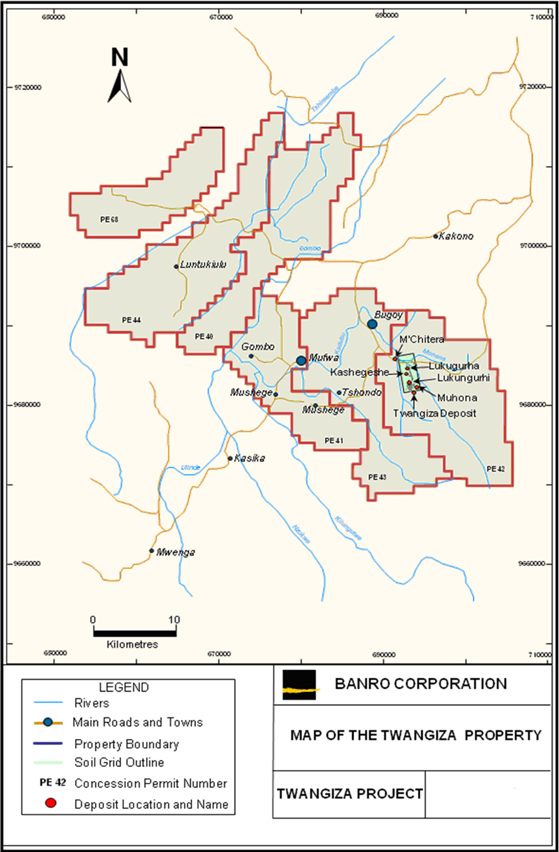

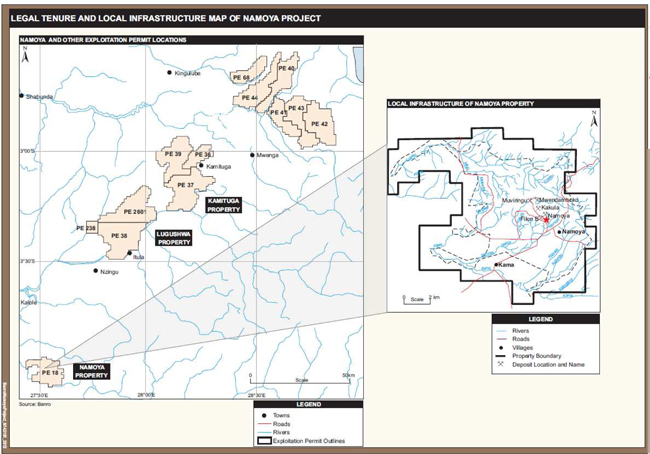

The diagram on the next page illustrates the location of the Company's four principal properties and the related exploitation permits.

Under DRC mining law, an exploitation permit entitles the holder thereof to the exclusive right to carry out, within the perimeter over which it is granted and during its term of validity, exploration, development, construction and exploitation works in connection with the mineral substances for which the permit has been granted and associated substances if the holder has obtained an extension of the permit. In addition, an exploitation permit entitles the holder to: (a) enter the exploitation perimeter to conduct mining operations; (b) build the installations and infrastructures required for mining exploitation; (c) use the water and wood within the mining perimeter for the requirements of the mining exploitation, provided that the requirements set forth in the environmental impact study and the environmental management plan of the project are complied with; (d) use, transport and freely sell the holder's products originating from within the exploitation perimeter; (e) proceed with concentration, metallurgical or technical treatment operations, as well as the transformation of the mineral substances extracted from the exploitation perimeter; and (f) proceed to carry out works to extend the mine.

| 11 |

Without an exploitation permit, the holder of an exploration permit may not conduct exploitation work on the perimeter covered by the exploration permit. So long as a perimeter is covered by an exploitation permit, no other application for a mining or quarry right for all or part of the same perimeter can be processed.

An exploration permit entitles the holder thereof to the exclusive right, within the perimeter over which it is granted and for the term of its validity, to carry out mineral exploration work for mineral substances, substances for which the licence is granted and associated substances if an extension of the permit is obtained. However, the holder of an exploration permit cannot commence work on the property without obtaining approval in advance of its mitigation and rehabilitation plan. An exploration permit also entitles its holder to the right to obtain an exploitation permit for all or part of the mineral substances and associated substances, if applicable, to which the exploration permit or any extension thereto applies if the holder discovers a deposit which can be economically exploited.

On February 13, 1997, the Company entered into a mining convention with the Republic of Zaire (now called the Democratic Republic of the Congo) and SOMINKI (the "Mining Convention"). In July 1998, the Company was expropriated of all its properties, rights and titles by Presidential decree. The Company initiated arbitration procedures against the DRC State seeking compensation for this expropriation. A settlement agreement between the DRC State and the Company was signed in April 2002 (the "Settlement Agreement"). The Settlement Agreement effectively revived the expropriated Mining Convention. Under the revived Mining Convention, the Company held a 100% equity interest in its Twangiza, Namoya, Lugushwa and Kamituga properties and was entitled to a ten-year tax holiday from the start of production.

| 12 |

On July 11, 2002, the DRC State enacted a Mining Code (the "Mining Code") to govern all the exploration and exploitation of mineral resources in the DRC. Holders of mining rights who derived their rights from previously existing mining conventions had the option to choose between being governed, either exclusively by the terms and conditions of their own mining convention with the DRC State or by the provisions of the Mining Code. Pursuant to this right of option which is prescribed in Section 340 paragraph 1 of the Mining Code, the Company elected to remain subject to the terms and conditions of its Mining Convention with respect to its 13 exploitation permits it acquired before the enactment of the Mining Code. Nevertheless, the 14 exploration permits (which were acquired by the Company after the implementation of the Mining Code) are exclusively governed by the provisions of the Mining Code and related mining regulations.

Sales of Gold

The Company commenced commercial production at its Twangiza gold mine on September 1, 2012. The Company recorded revenues from the Twangiza mine of US$42.631 million on sales of 24,963 ounces of gold during the four month period of September 1, 2012 to December 31, 2012. The Company recorded revenues from the Twangiza mine of US$111.808 million on sales of 80,497 ounces of gold during the twelve months ended December 31, 2013. The Company’s second gold mine, Namoya, is planned to commence commercial production by the end of the second quarter of 2014. There are numerous purchasers of gold, therefore the Company is not dependent upon any one purchaser. Current production from Twangiza is in the form of doré bars which are flown from the Twangiza site to the capital city of Kinshasa, DRC, and then shipped by air to a refinery in South Africa. The Company carries out owner-operated mining at Twangiza.

Skill and Knowledge

The Company has built a management team of skilled mining, environmental, financial and administrative personnel. The specialized knowledge and skills required in all areas of mining include engineering, geology, metallurgy, environmental permitting, drilling and exploration program planning. The Twangiza mine was the first new commercial gold mining operation in the DRC in over 50 years. Training and re-training of local staff in all aspects of mining operations is and has been a priority of the Company.

Employees

As at December 31, 2013, the Company and its subsidiaries had a total of 1,358 employees. The following provides a breakdown of these employees by location/project:

| Location/Project | Number of Employees | |||

| Office in Toronto, Canada | 10 | |||

| Office in Kinshasa, DRC | 17 | |||

| Twangiza mine | 682 | |||

| Namoya project (development) | 463 | |||

| Exploration and office in Bukavu, DRC | 175 | |||

| Banro Foundation | 11 | |||

| Total: | 1,358 | |||

| 13 |

Neither the Company nor any of its subsidiaries has any unionized employees.

Contractors and local labour hire companies engaged by the Company’s DRC subsidiaries employed a total of 2,483 employees as at December 31, 2013 in respect of the Company’s DRC projects.

Social and Environmental Policies

(a) The Banro Foundation

Since launching its current exploration programs in late 2004, Banro has been working with local communities to promote development. In late 2005, the Company formalized this commitment to community development with the creation of the Banro Foundation. The Banro Foundation is a registered charity in the DRC with a mandate to support education, health and infrastructure improvements, principally in the local communities where Banro operates. The Banro Foundation also provides humanitarian assistance as required and helps to sponsor major community events. Beginning in 2014, it will also focus on fostering sustainable agricultural projects in communities near Banro’s operations. The Company funds the Banro Foundation and has created a management structure that ensures local participation in decision-making. The Foundation focuses on needs that have been identified by local committees of community leaders and invests in improvements that will benefit communities as a whole. Promotion of opportunities for women is an important guiding principle of the Foundation. To the extent possible, the Foundation employs local labour in all initiatives. Since 2009, the projects completed by the Banro Foundation include the construction of 10 new schools and the rehabilitation of two schools (the 12 schools are educating a current total of over 7,000 students), the building of potable water delivery systems serving over 30,000 people, the construction or re-construction of over 100 kilometres of roads and bridges, four health care facilities, a women’s resource centre and three separate distributions of medical equipment from Canada to regional hospitals and clinics in South Kivu province. Additional information with respect to the Banro Foundation, including a list of projects undertaken by the Banro Foundation to date, can be found on the Company's web site at www.banro.com.

(b) Job Creation

Banro is committed to the creation of jobs and economic opportunities for local Congolese. In a short period of time, Banro has gone from having no presence in the eastern DRC to being one of the largest private employers in the region. As it has grown, the Company has deliberately created opportunities for many local Congolese. As of December 31, 2013, the Company employed 1,218 Congolese directly and an additional 2,361 Congolese indirectly through contractors and local labour hire companies.

(c) Environmental Protection and Workplace Safety

As set out in the Business Conduct Policy adopted by the Company (a copy of this policy can be obtained from the System for Electronic Document Analysis and Retrieval ("SEDAR") at www.sedar.com), the Company believes that effectiveness in environmental standards, along with occupational health and safety, is an essential part of achieving success in the mineral exploration, development and mining business. The Business Conduct Policy states that Banro will therefore work at continuous improvement in these areas and will be guided by the following principles: (a) creating a safe work environment; (b) minimizing the environmental impacts of its activities; (c) building cooperative working relationships with local communities and governments in the Company's areas of operations; (d) reviewing and monitoring environmental and safety performance; and (e) prompt and effective response to any environmental and safety concerns.

| 14 |

Banro adheres to the E3 Environmental Excellence in Exploration guidelines, which were developed by the Prospectors and Developers Association of Canada.

Banro's management has also taken steps to ensure that all employees and suppliers respect and adhere to the laws of the DRC with respect to the protection of threatened and endangered species.

The Company is working to international best practice standards in environmental and social appraisal. SRK Consulting (South Africa) (Pty) Ltd. was contracted to develop an Equator Principles 2-compliant environmental and social impact assessment report and associated environmental and social impact mitigation and management plan in respect of the development of the Twangiza and Namoya mines. This work was completed by SLR Consulting (Africa) (Pty) Ltd.

| 3.2 | Risk Factors |

There are a number of risks that may have a material and adverse impact on the future operating and financial performance of Banro and could cause the Company's operating and financial performance to differ materially from the estimates described in forward-looking statements relating to the Company. These include widespread risks associated with any form of business and specific risks associated with Banro's business and its involvement in the gold exploration, development and mining industry.

An investment in the Company's common shares is considered speculative and involves a high degree of risk due to, among other things, the nature of Banro's business (which is the exploration, development and mining of gold properties), the present stage of its development and the location of Banro's projects in the DRC. In addition to the other information presented in this AIF, a prospective investor should carefully consider the risk factors set out below and the other information that Banro files with Canadian securities regulators and with the SEC in the U.S. before investing in the Company's common shares. The Company has identified the following non-exhaustive list of inherent risks and uncertainties that it considers to be relevant to its operations and business plans. Such risk factors could materially affect the Company's future operating results and could cause actual events to differ materially from those described in forward-looking statements relating to the Company. As well, while the following sets out the material risk factors which the Company is aware of, there may be additional risks that the Company is unaware of or that are currently believed to be immaterial that may become important factors that affect the Company's business.

| 15 |

Risks of Operating in the DRC

Banro's projects are located in the DRC. The assets and operations of the Company are therefore subject to various political, economic and other uncertainties, including, among other things, the risks of war and civil unrest, expropriation, nationalization, renegotiation or nullification of existing licenses, permits, approvals and contracts, taxation policies, foreign exchange and repatriation restrictions, changing political conditions, international monetary fluctuations, currency controls and foreign governmental regulations that favour or require the awarding of contracts to local contractors or require foreign contractors to employ citizens of, or purchase supplies from, a particular jurisdiction. Changes, if any, in mining or investment policies or shifts in political climate in the DRC may adversely affect Banro's operations. Operations may be affected in varying degrees by government regulations with respect to, but not limited to, restrictions on production, price controls, export controls, currency remittance, income taxes, foreign investment, maintenance of claims, environmental legislation, land use, land claims of local people, water use and mine safety. Failure to comply strictly with applicable laws, regulations and local practices relating to mineral rights, could result in loss, reduction or expropriation of entitlements. In addition, in the event of a dispute arising from operations in the DRC, the Company may be subject to the exclusive jurisdiction of foreign courts or may not be successful in subjecting foreign persons to the jurisdiction of courts in Canada. The Company also may be hindered or prevented from enforcing its rights with respect to a governmental instrumentality because of the doctrine of sovereign immunity. It is not possible for the Company to accurately predict such developments or changes in laws or policy or to what extent any such developments or changes may have a material adverse effect on the Company's operations. There are also risks associated with the enforceability of the Company's mining convention with the DRC and the government of the DRC could choose to review the Company's titles at any time. Should the Company's rights, its mining convention or its titles not be honoured or become unenforceable for any reason, or if any material term of these agreements is arbitrarily changed by the government of the DRC, the Company's business, financial condition and prospects will be materially adversely affected.

Some or all of the Company's properties are located in regions where political instability and violence is ongoing (for example, in November 2012, the M23 rebel group took over the city of Goma (Banro's operations are located about 200 kilometres southwest of Goma), but subsequently withdrew from Goma under international pressure). Some or all of the Company's properties are inhabited by artisanal miners. These conditions may interfere with work on the Company's properties and present a potential security threat to the Company's employees. There is a risk that operations of the Company may be delayed or interfered with, due to the conditions of political instability, violence and the inhabitation of the properties by artisanal miners. The Company uses its best efforts to maintain good relations with the local communities in order to minimize such risks.

The DRC is a developing nation which recently emerged from a period of civil war and conflict. Physical and institutional infrastructure throughout the DRC is in a debilitated condition. The DRC is in transition from a largely state controlled economy to one based on free market principles, and from a non-democratic political system with a centralized ethnic power base, to one based on more democratic principles. There can be no assurance that these changes will be effected or that the achievement of these objectives will not have material adverse consequences for Banro and its operations. The DRC continues to experience instability in parts of the country due to certain militia and criminal elements. While the government and United Nations forces are working to support the extension of central government authority throughout the country, there can be no assurance that such efforts will be successful.

No assurance can be given that the Company will be able to maintain effective security in connection with its assets or personnel in the DRC where civil war and conflict have disrupted exploration and mining activities in the past and may affect the Company's operations or plans in the future.

HIV/AIDS, malaria and other diseases represent a serious threat to maintaining a skilled workforce in the mining industry in the DRC. HIV/AIDS is a major healthcare challenge faced by the Company's operations in the country. There can be no assurance that the Company will not lose members of its workforce or workforce man-hours or incur increased medical costs, which may have a material adverse effect on the Company's operations.

The DRC has historically experienced relatively high rates of inflation.

| 16 |

Production Risk

As is typically the case with the mining industry, no assurances can be given that future gold production estimates will be achieved. Estimates of future production for the Company’s mining operations are derived from the Company’s mining plans. These estimates and plans are subject to change. The Company cannot give any assurance that it will achieve its production estimates. The Company’s failure to achieve its production estimates could have a material and adverse effect on the Company’s future cash flows, results of operations, production cost, financial condition and prospects. The plans are developed based on, among other things, mining experience, reserve estimates, assumptions regarding ground conditions, hydrologic conditions and physical characteristics of ores (such as hardness and presence or absence of certain metallurgical characteristics) and estimated rates and costs of production. Actual production may vary from estimates for a variety of reasons, including risks and hazards of the types discussed above, and as set out below, including:

| • | equipment failures; |

| • | shortages of principal supplies needed for operations; |

| • | natural phenomena such as inclement weather conditions, floods, droughts, rock slides and earthquakes; |

| • | accidents; |

| • | mining dilution; |

| • | encountering unusual or unexpected geological conditions; |

| • | changes in power costs and potential power shortages; |

| • | strikes and other actions by labour; and |

| • | regulatory restrictions imposed by government agencies. |

Such occurrences could, in addition to stopping or delaying gold production, result in damage to mineral properties, injury or death to persons, damage to the Company’s property or the property of others, monetary losses and legal liabilities. These factors may also cause a mineral deposit that has been mined profitably in the past to become unprofitable. Estimates of production from properties not yet in production or from operations that are to be expanded are based on similar factors (including, in some instances, feasibility studies prepared by the Company’s personnel and outside consultants) but it is possible that actual operating costs and economic returns will differ significantly from those currently estimated. It is not unusual in new mining operations or mine expansion to experience unexpected problems during the start-up phase. Delays often can occur in the commencement of production.

Commodity Prices

The future price of gold will significantly affect the development of Banro's projects and results of its mining operations. Gold prices are subject to significant fluctuation and are affected by a number of factors which are beyond Banro's control. Such factors include, but are not limited to, interest rates, inflation or deflation, fluctuation in the value of the United States dollar and foreign currencies, global and regional supply and demand, and the political and economic conditions of major gold-producing countries throughout the world. The price of gold has fluctuated widely in recent years, and future price declines could cause development of and commercial production from Banro's mineral interests to be impracticable. If the price of gold decreases, projected cash flow from planned mining operations may not be sufficient to justify ongoing operations and Banro could be forced to discontinue development and sell its projects. Future production from Banro's projects is dependent on gold prices that are adequate to make these projects economic.

Mineral reserve calculations and life-of-mine plans using lower gold prices could result in material write-downs of the Company’s investment in mining properties and increased amortization, reclamation and closure charges.

As fuel costs are a significant component of the Company’s operating costs, changes in the price of diesel could have a significant effect on the Company’s operating costs.

| 17 |

Risks Related to the Notes Issued under the Debt Financing and Other Financial Obligations

The Company’s substantial indebtedness could adversely affect the Company’s financial condition.

In March 2012 the Company closed a US$175 million debt financing (see item 2 of this AIF ("General Development of the Business")). As well, during 2013 the Company secured an additional US$53 million in short term loans (the "Short Term Loans") from several lenders. The Company therefore has a significant amount of indebtedness. The Company’s high level of indebtedness could have important adverse consequences, including:

| · | limiting the Company’s ability to obtain additional financing to fund future working capital, capital expenditures, acquisitions or other general corporate requirements; |

| · | requiring a substantial portion of the Company’s cash flows to be dedicated to debt service payments instead of other purposes, thereby reducing the amount of cash flows available for working capital, capital expenditures, acquisitions and other general corporate purposes; |

| · | increasing the Company’s vulnerability to general adverse economic and industry conditions; |

| · | limiting the Company’s flexibility in planning for and reacting to changes in the industry in which it competes; |

| · | placing the Company at a disadvantage compared to other, less leveraged competitors; and |

| · | increasing the cost of borrowing. |

The Company may not be able to generate sufficient cash to service all of its indebtedness (including the Notes and the Short Term Loans) and obligations with respect to outstanding preferred shares, and may be forced to take other actions to satisfy its obligations under such indebtedness or with respect to such preferred shares, which may not be successful.

The Company’s ability to make scheduled payments on or refinance the Company’s debt obligations (including the Notes and the Short Term Loans) and to make payments with respect to outstanding preferred shares (see item 5 of this AIF (“Description of Capital Structure”) regarding the outstanding preferred shares of the Company and certain of its subsidiaries) depends on its financial condition and operating performance, which are subject to prevailing economic and competitive conditions and to certain financial, business, legislative, regulatory and other factors beyond its control. The Company may be unable to maintain a level of cash flows from operating activities sufficient to permit it to pay the principal, premium, if any, and interest on its indebtedness or to make required payments with respect to outstanding preferred shares.

If the Company’s cash flows and capital resources are insufficient to fund its debt service obligations or required preferred share payments, the Company could face substantial liquidity problems and could be forced to reduce or delay investments and capital expenditures or to dispose of material assets or operations, seek additional debt or equity capital or restructure or refinance the Company’s indebtedness. Banro may not be able to effect any such alternative measures on commercially reasonable terms or at all and, even if successful, those alternatives may not allow the Company to meet its scheduled financial obligations. The indenture under which the Notes were issued (the "Note Indenture") restricts the Company’s ability to dispose of assets and use the proceeds from those dispositions and may also restrict the Company’s ability to raise debt or equity capital to be used to repay other indebtedness when it becomes due. The Company may not be able to consummate those dispositions or to obtain proceeds in an amount sufficient to meet any financial obligations then due.

| 18 |

In addition, Banro is a holding company, and as such it conducts all operations through subsidiaries. Accordingly, repayment of indebtedness (including the Notes and the Short Term Loans) and payments in relation to preferred shares are dependent on the generation of cash flow by subsidiaries and their ability to make cash available to make such payments. Banro’s subsidiaries may not be able to, or may not be permitted to, make distributions to enable such payments to be made. Each subsidiary is a distinct legal entity, and, under certain circumstances, legal and contractual restrictions may limit the ability to obtain cash from subsidiaries. In the event that distributions are not received from subsidiaries, it may not be possible to make required principal and interest payments on indebtedness or payments with respect to preferred shares.

Banro’s inability to generate sufficient cash flows to satisfy its debt or preferred share obligations, or to refinance the Company’s indebtedness on commercially reasonable terms or at all, would materially and adversely affect the Company’s financial position and results of operations and its ability to satisfy its financial obligations.

If the Company cannot make scheduled payments on its debt, the Company will be in default and holders of the Notes could declare all outstanding principal and interest to be due and payable, causing a cross-acceleration or cross-default under certain of the Company’s other debt agreements, and the Company could be forced into bankruptcy or liquidation. The Company could also be forced into bankruptcy or liquidation if required payments with respect to preferred shares are not made.

The terms of the Note Indenture restrict the Company’s current and future operations, particularly the Company’s ability to respond to changes or to take certain actions.

The Note Indenture contains a number of restrictive covenants that impose significant operating and financial restrictions on the Company and may limit the Company’s ability to engage in acts that may be in its long-term best interest, including restrictions on the Company’s ability to:

| · | incur additional indebtedness; |

| · | pay dividends or make other distributions or repurchase or redeem capital stock; |

| · | prepay, redeem or repurchase certain debt; |

| · | make loans and investments; |

| · | sell assets; |

| · | incur liens; |

| · | enter into transactions with affiliates; |

| · | alter the businesses it conducts; |

| · | enter into agreements restricting its subsidiaries’ ability to pay dividends; and |

| · | consolidate, amalgamate, merge or sell all or substantially all of its assets. |

A breach of the covenants under the Note Indenture or the Company’s other debt instruments from time to time could result in an event of default under the applicable indebtedness. Such a default may allow the creditors to accelerate the related debt and may result in the acceleration of any other debt to which a cross-acceleration or cross-default provision applies. In the event the Noteholders or lenders accelerate the repayment of the Company’s borrowings, Banro may not have sufficient assets to repay that indebtedness.

| 19 |

As a result of these restrictions, Banro may be:

| · | limited in how it conducts its business; |

| · | unable to raise additional debt or equity financing to operate during general economic or business downturns; or |

| · | unable to compete effectively or to take advantage of new business opportunities. |

These restrictions may affect the Company’s ability to grow in accordance with its strategy.

Expatriate and Third-Party Nationals Skills Risk

The Company’s Twangiza mine was the first new commercial gold mining operation in the DRC in over 50 years. As a result, the Company is reliant on attracting and retaining expatriate and third-party nationals with mining experience to staff key operations and administration management positions. The Company’s inability to attract and retain personnel with the skills and experience to manage the operation and train and develop staff, due to the intense international competition for such individuals, may adversely affect its business and future operations.

Need for Additional Reserves

Given that mines have limited lives based on proven and probable mineral reserves, the Company must continually replace and expand its reserves at its mines. The life-of-mine estimates included in the Company’s continuous disclosure documents filed on SEDAR and EDGAR are subject to adjustment. The Company’s ability to maintain or increase its annual production of gold will be dependent in significant part on its ability to bring new mines into production and to expand reserves at existing mines.

Labour Risk

The Company is dependent on its workforce to extract and process minerals, and is therefore sensitive to a labour disruption of the Company's mining activities. The Company endeavours to maintain good relations with its workforce in order to minimize the possibility of strikes, lock-outs and other stoppages at its work sites. Relations between the Company and its employees may be impacted by changes in labour relations which may be introduced by, among other things, employee groups, unions, and the relevant governmental authorities.

Construction and Start-Up of New Mines and Mine Expansion

The Company is currently completing the construction of its second mine at Namoya, and its first mine, at Twangiza, is undergoing a plant upgrade. The success of construction projects, plant expansions and the start-up of new mines by the Company is subject to a number of factors including the availability and performance of engineering and construction contractors, suppliers and consultants, the receipt of required governmental approvals and permits in connection with the construction of mining facilities and the conduct of mining operations, including environmental permits, price escalation on all components of construction and start-up, the underlying characteristics, quality and unpredictability of the exact nature of mineralogy of a deposit and the consequent accurate understanding of dore or concentrate production, the successful completion and operation of ore passes and conveyors to move ore and other operational elements. Any delay in the performance of any one or more of the contractors, suppliers, consultants or other persons on which the Company is dependent in connection with its construction activities, a delay in or failure to receive the required governmental approvals and permits in a timely manner or on reasonable terms, or a delay in or failure in connection with the completion and successful operation of the operational elements in connection with new mines could delay or prevent the construction and start-up of new mines as planned. There can be no assurance that current or future construction and start-up plans implemented by the Company will be successful.

| 20 |

The SEC has Adopted Rules That May Affect Mining Operations in the DRC

The Company’s business is subject to evolving corporate governance and public disclosure regulations that have increased both the Company’s compliance costs and the risk of noncompliance, which could have an adverse effect on the Company’s stock price.

The Company is subject to changing rules and regulations promulgated by a number of United States and Canadian governmental and self-regulated organizations, including the SEC, the Canadian Securities Administrators, the New York Stock Exchange, the Toronto Stock Exchange, and the International Accounting Standards Board. These rules and regulations continue to evolve in scope and complexity and many new requirements have been created in response to laws enacted by the United States Congress, making compliance more difficult and uncertain. For example, on July 21, 2010, the United States Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act, which is expected to result in the SEC adopting rules that will require the Company to disclose on an annual basis certain payments made by the Company, its subsidiaries or entities controlled by it, to the U.S. government and foreign governments, including sub-national governments. The SEC has also adopted rules under the Dodd Frank Act that will require a company filing reports with the SEC to disclose on an annual basis, beginning in 2014, whether certain “conflict minerals” necessary to the functionality or production of a product manufactured by such company originated in the DRC or any adjoining country. The Company currently holds properties located in the DRC. It is possible that the new SEC rules regarding conflict minerals could adversely affect the value of the minerals mined in the DRC, which may impact the value of the Company’s interests in those properties. The Company’s efforts to comply with the Dodd-Frank Act, the rules and regulations promulgated thereunder, and other new rules and regulations have resulted in, and are likely to continue to result in, increased general and administration expenses and a diversion of management time and attention from revenue-generating activities to compliance activities.

No History of Profitability with respect to Development Properties

The Company's properties are in the exploration or development stage, other than the Company’s first producing mine at Twangiza. The development of properties found to be economically feasible requires the construction and operation of mines, processing plants and related infrastructure. As a result, Banro is subject to all of the risks associated with establishing new mining operations and business enterprises including: the timing and cost, which can be considerable, of the construction of mining and processing facilities; the availability and costs of skilled labour and mining equipment; the availability and costs of appropriate smelting and/or refining arrangements; the need to obtain necessary environmental and other governmental approvals and permits, and the timing of those approvals and permits; and, the availability of funds to finance construction and development activities. The costs, timing and complexities of mine construction and development are increased by the remote location of the Company's properties. It is common in new mining operations to experience unexpected problems and delays during construction, development, and mine start-up. In addition, delays in the commencement of mineral production often occur. Accordingly, there are no assurances that the Company's activities at one of its development projects will result in profitable mining operations or that the Company will successfully establish mining operations or profitably produce gold at one of its development projects.

| 21 |

Government Regulation

Banro's mineral exploration, development and mining activities are subject to various laws governing prospecting, mining, development, production, taxes, labour standards and occupational health, mine safety, toxic substances, land use, water use, land claims of local people and other matters. Although Banro's exploration, development and mining activities are currently carried out in accordance with applicable rules and regulations, no assurance can be given that new rules and regulations will not be enacted or that existing rules and regulations will not be applied in a manner which could limit or curtail development.

Many of Banro's mineral rights and interests are subject to government approvals, licenses and permits. Such approvals, licenses and permits are, as a practical matter, subject to the discretion of the DRC government. No assurance can be given that Banro will be successful in maintaining any or all of the various approvals, licenses and permits in full force and effect without modification or revocation. To the extent such approvals are not maintained, Banro may be delayed, curtailed or prohibited from continuing or proceeding with planned exploration, development or mining of mineral properties.

Failure to comply with applicable laws, regulations and permitting requirements may result in enforcement actions thereunder, including orders issued by regulatory or judicial authorities causing operations to cease or be delayed or curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment, or remedial actions. Parties engaged in the exploration, development or mining of mineral properties may be required to compensate those suffering loss or damage by reason of the activities and may have civil or criminal fines or penalties imposed for violations of applicable laws or regulations.

Amendments to current laws and regulations governing operations or more stringent implementation thereof could have a substantial adverse impact on Banro and cause increases in expenses, capital expenditures or require abandonment or delays in development of mineral interests.

Exploration and Mining Risks

The Company's properties are in the exploration or development stage, other than the Company’s first producing mine at Twangiza. The exploration for and development of mineral deposits involves significant risks that even a combination of careful evaluation, experience and knowledge may not eliminate. While the discovery of an ore body may result in substantial rewards, few properties that are explored are ultimately developed into producing mines. Major expenditures are required to locate and establish mineral reserves, to develop metallurgical processes and to construct mining and processing facilities at a particular site. Whether a mineral deposit, once discovered, will be commercially viable depends on a number of factors, some of which are: the particular attributes of the deposit, such as size, grade and proximity to infrastructure; metal prices which are highly cyclical; and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in Banro not receiving an adequate return on invested capital.

There is no certainty that the expenditures made by Banro towards the search for and evaluation of mineral deposits will result in discoveries that are commercially viable. In addition, in the case of a commercial ore-body, depending on the type of mining operation involved, several years can elapse from the initial phase of drilling until commercial operations are commenced.

| 22 |