________________________________________________________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2024

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO | |||||

Commission File Number: 001-32236

________________

(Exact Name of Registrant as Specified in its Charter)

________________

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | ||||

(Address of Principal Executive Offices and Zip Code)

(212 ) 832-3232

(Registrant's Telephone Number, Including Area Code)

________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | |||||||||||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of shares of the registrant's common stock, par value $0.01 per share, outstanding as of April 30, 2024 was 50,540,398 .

COHEN & STEERS, INC. AND SUBSIDIARIES

Form 10-Q

Index

| Page | ||||||||

| Part I. | Financial Information | |||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Part II. | Other Information * | |||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

* Items other than those listed above have been omitted because they are not applicable.

Forward-Looking Statements

This report and other documents filed by us contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the Exchange Act), which reflect management's current views with respect to, among other things, our operations and financial performance. You can identify these forward-looking statements by the use of words such as "outlook," "believes," "expects," "potential," "continues," "may," "will," "should," "seeks," "approximately," "predicts," "intends," "plans," "estimates," "anticipates" or the negative versions of these words or other comparable words. Such forward-looking statements are subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these forward-looking statements. We believe that these factors include, but are not limited to, the risks described in the Risk Factors section of our Annual Report on Form 10-K for the year ended December 31, 2023 (the Form 10-K), which is accessible on the Securities and Exchange Commission's website at www.sec.gov and on our website at www.cohenandsteers.com. These factors are not exhaustive and should be read in conjunction with the other cautionary statements that are included in this report, the Form 10-K and our other filings with the Securities and Exchange Commission. We undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

PART I—Financial Information

Item 1. Financial Statements

COHEN & STEERS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF FINANCIAL CONDITION (Unaudited)

(in thousands, except share data)

| March 31, 2024 | December 31, 2023 | ||||||||||

| Assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

Investments ($ | |||||||||||

| Accounts receivable | |||||||||||

Due from brokers ($ | |||||||||||

| Property and equipment—net | |||||||||||

| Operating lease right-of-use assets—net | |||||||||||

| Goodwill and intangible assets—net | |||||||||||

Other assets ($ | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities: | |||||||||||

| Accrued compensation and benefits | $ | $ | |||||||||

| Distribution and service fees payable | |||||||||||

| Operating lease liabilities | |||||||||||

| Income tax payable | |||||||||||

Due to brokers ($ | |||||||||||

Other liabilities and accrued expenses ($ | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies (See Note 11) | |||||||||||

| Redeemable noncontrolling interests | |||||||||||

| Stockholders' equity: | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

Treasury stock, at cost, | ( | ( | |||||||||

| Total stockholders’ equity attributable to Cohen & Steers, Inc. | |||||||||||

| Nonredeemable noncontrolling interests | |||||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities, redeemable noncontrolling interests and stockholders’ equity | $ | $ | |||||||||

_________________________

(1) Amounts in parentheses represent the aggregate balances at March 31, 2024 and December 31, 2023 attributable to variable interest entities consolidated by the Company. Refer to Note 4, Investments for further discussion.

See notes to condensed consolidated financial statements

1

COHEN & STEERS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

(in thousands, except per share data)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Revenue: | |||||||||||

| Investment advisory and administration fees | $ | $ | |||||||||

| Distribution and service fees | |||||||||||

| Other | |||||||||||

| Total revenue | |||||||||||

| Expenses: | |||||||||||

| Employee compensation and benefits | |||||||||||

| Distribution and service fees | |||||||||||

| General and administrative | |||||||||||

| Depreciation and amortization | |||||||||||

| Total expenses | |||||||||||

| Operating income | |||||||||||

| Non-operating income (loss): | |||||||||||

| Interest and dividend income—net | |||||||||||

| Gain (loss) from investments—net | ( | ||||||||||

| Foreign currency gain (loss)—net | ( | ||||||||||

| Total non-operating income (loss) | |||||||||||

| Income before provision for income taxes | |||||||||||

| Provision for income taxes | |||||||||||

| Net income | |||||||||||

| Net (income) loss attributable to noncontrolling interests | ( | ( | |||||||||

| Net income attributable to common stockholders | $ | $ | |||||||||

| Earnings per share attributable to common stockholders: | |||||||||||

| Basic | $ | $ | |||||||||

| Diluted | $ | $ | |||||||||

| Weighted average shares outstanding: | |||||||||||

| Basic | |||||||||||

| Diluted | |||||||||||

See notes to condensed consolidated financial statements

2

COHEN & STEERS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (Unaudited)

(in thousands)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Net income | $ | $ | |||||||||

| Net (income) loss attributable to noncontrolling interests | ( | ( | |||||||||

| Net income attributable to common stockholders | |||||||||||

| Other comprehensive income (loss): | |||||||||||

| Foreign currency translation gain (loss) | ( | ||||||||||

| Total comprehensive income attributable to common stockholders | $ | $ | |||||||||

See notes to condensed consolidated financial statements

3

COHEN & STEERS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY (Unaudited)

(in thousands, except per share data)

| Three Months Ended March 31, 2024 | ||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Income (Loss) | Treasury Stock | Nonredeemable Noncontrolling Interests | Total Stockholders' Equity | Redeemable Noncontrolling Interests | |||||||||||||||||||

| January 1, 2024 | $ | $ | $ | ( | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||

Dividends ($ | — | — | ( | — | — | — | ( | — | ||||||||||||||||||

| Issuance of common stock | — | — | — | — | — | |||||||||||||||||||||

| Repurchase of common stock | — | — | — | — | ( | — | ( | — | ||||||||||||||||||

| Issuance of restricted stock units—net | — | — | — | — | — | — | ||||||||||||||||||||

| Amortization of restricted stock units—net | — | — | — | — | — | — | ||||||||||||||||||||

| Net income (loss) | — | — | — | — | ||||||||||||||||||||||

| Other comprehensive income (loss) | — | — | — | ( | — | — | ( | — | ||||||||||||||||||

| Net contributions (distributions) attributable to noncontrolling interests | — | — | — | — | — | ( | ||||||||||||||||||||

| March 31, 2024 | $ | $ | $ | ( | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||

| Three Months Ended March 31, 2023 | ||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Deficit | Accumulated Other Comprehensive Income (Loss) | Treasury Stock | Nonredeemable Noncontrolling Interests | Total Stockholders' Equity | Redeemable Noncontrolling Interests | |||||||||||||||||||

| January 1, 2023 | $ | $ | $ | ( | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||

Dividends ($ | — | — | ( | — | — | — | ( | — | ||||||||||||||||||

| Issuance of common stock | — | — | — | — | — | |||||||||||||||||||||

| Repurchase of common stock | — | — | — | — | ( | — | ( | — | ||||||||||||||||||

| Issuance of restricted stock units—net | — | — | — | — | — | — | ||||||||||||||||||||

| Amortization of restricted stock units—net | — | — | — | — | — | — | ||||||||||||||||||||

| Net income (loss) | — | — | — | — | ( | |||||||||||||||||||||

| Other comprehensive income (loss) | — | — | — | — | — | — | ||||||||||||||||||||

| Net contributions (distributions) attributable to noncontrolling interests | — | — | — | — | — | |||||||||||||||||||||

| March 31, 2023 | $ | $ | $ | ( | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||

See notes to condensed consolidated financial statements

4

COHEN & STEERS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

(in thousands)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Cash flows from operating activities: | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by (used in) operating activities: | |||||||||||

| Stock-based compensation expense—net | |||||||||||

| Depreciation and amortization | |||||||||||

| Amortization of right-of-use assets | |||||||||||

| Amortization (accretion) of premium (discount) on U.S. Treasury securities | ( | ( | |||||||||

| (Gain) loss from investments—net | ( | ||||||||||

| Deferred income taxes | |||||||||||

| Foreign currency (gain) loss | ( | ||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Accounts receivable | ( | ( | |||||||||

| Due from brokers | ( | ( | |||||||||

| Investments within consolidated investment vehicles | ( | ||||||||||

| Other assets | ( | ( | |||||||||

| Accrued compensation and benefits | ( | ( | |||||||||

| Distribution and service fees payable | ( | ||||||||||

| Operating lease liabilities | ( | ||||||||||

| Due to brokers | |||||||||||

| Income tax payable | |||||||||||

| Other liabilities and accrued expenses | ( | ||||||||||

| Net cash provided by (used in) operating activities | ( | ||||||||||

| Cash flows from investing activities: | |||||||||||

| Purchases of investments | ( | ( | |||||||||

| Proceeds from sales and maturities of investments | |||||||||||

| Purchases of property and equipment | ( | ( | |||||||||

| Net cash provided by (used in) investing activities | ( | ( | |||||||||

| Cash flows from financing activities: | |||||||||||

| Issuance of common stock—net | |||||||||||

| Repurchase of common stock for employee tax withholding | ( | ( | |||||||||

| Dividends to stockholders | ( | ( | |||||||||

| Net contributions (distributions) from noncontrolling interests | ( | ||||||||||

| Other | ( | ( | |||||||||

| Net cash provided by (used in) financing activities | ( | ( | |||||||||

| Net increase (decrease) in cash and cash equivalents | ( | ( | |||||||||

| Effect of foreign exchange rate changes on cash and cash equivalents | ( | ||||||||||

| Cash and cash equivalents, beginning of the period | |||||||||||

| Cash and cash equivalents, end of the period | $ | $ | |||||||||

See notes to condensed consolidated financial statements

5

COHEN & STEERS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS—(Continued)

(UNAUDITED)

Supplemental disclosures of cash flow information:

The following table provides a reconciliation of cash and cash equivalents reported within the condensed consolidated statements of financial condition to the cash and cash equivalents reported within the condensed consolidated statements of cash flows above:

| As of March 31, | |||||||||||

| (in thousands) | 2024 | 2023 | |||||||||

Cash and cash equivalents | $ | $ | |||||||||

Cash included in investments (1) | |||||||||||

Total cash and cash equivalents within condensed consolidated statements of cash flows | $ | $ | |||||||||

________________________

(1) Cash included in investments represents operating cash held in consolidated investment vehicles.

During the three months ended March 31, 2024 and 2023, the Company paid taxes, net of tax refunds, of $1.2 million and $3.3 million, respectively.

Supplemental disclosures of non-cash investing and financing activities:

In connection with its stock incentive plan, the Company issued dividend equivalents in the form of restricted stock units, net of forfeitures, in the amount of $0.9 million and $0.8 million for the three months ended March 31, 2024 and 2023, respectively. These amounts are included in the issuance of restricted stock units—net and in dividends in the condensed consolidated statements of changes in stockholders' equity.

6

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

1. Organization and Description of Business

Cohen & Steers, Inc. (CNS) was organized as a Delaware corporation on March 17, 2004. CNS is the holding company for its direct and indirect subsidiaries, including Cohen & Steers Capital Management, Inc. (CSCM), Cohen & Steers Securities, LLC (CSS), Cohen & Steers UK Limited (CSUK), Cohen & Steers Ireland Limited (CSIL), Cohen & Steers Asia Limited (CSAL), Cohen & Steers Japan Limited (CSJL) and Cohen & Steers Singapore Private Limited (CSSG) (collectively, the Company).

The Company is a global investment manager specializing in real assets and alternative income, including listed and private real estate, preferred securities, infrastructure, resource equities, commodities, as well as multi-strategy solutions. Founded in 1986, the Company is headquartered in New York City, with offices in London, Dublin, Hong Kong, Tokyo and Singapore.

2. Basis of Presentation and Significant Accounting Policies

The condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (GAAP). The condensed consolidated financial statements set forth herein include the accounts of CNS and its direct and indirect subsidiaries. Intercompany balances and transactions have been eliminated in consolidation.

The condensed consolidated financial statements of the Company included herein are unaudited and have been prepared in accordance with the instructions to Form 10-Q pursuant to the rules and regulations of the Securities and Exchange Commission (SEC). In the opinion of management, all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of the interim results have been made. The Company's condensed consolidated financial statements and the related notes should be read together with the consolidated financial statements and the related notes included in the Company's Annual Report on Form 10-K for the year ended December 31, 2023.

Recently Adopted Accounting Pronouncements—In June 2022, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update 2022-03 (ASU), Fair Value Measurement (Topic 820): Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions. The standard clarifies that contractual sale restrictions are not considered in measuring the fair value of equity securities, which would be a change in practice for certain entities. The ASU also indicates that a contractual sale restriction is not a separate unit of account, and requires new disclosures for all entities with equity securities subject to a contractual sale restriction. This new guidance became effective on January 1, 2024. The Company's adoption of this new standard did not have an impact on the Company's condensed consolidated financial statements.

In November 2023, the FASB issued ASU 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures. The standard requires enhanced disclosure of the reportable segments and additional information about a segment’s expenses. This new guidance became effective on January 1, 2024. The Company's adoption of this new standard did not have an impact on the Company's condensed consolidated financial statements.

Accounting Estimates—The preparation of the condensed consolidated financial statements in conformity with GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosures of contingent assets and liabilities at the dates of the condensed consolidated financial statements and the reported amounts of revenue and expenses during the reporting periods. Management believes the estimates used in preparing the condensed consolidated financial statements are reasonable and prudent. Actual results could differ from those estimates.

Consolidation of Investment Vehicles—The Company's financial interests in investment vehicles, including the management fees that are received, are evaluated at inception and thereafter, if there is a reconsideration event, in order to determine whether to apply the Variable Interest Entity (VIE) model or the Voting Interest Entity (VOE) model.

A VIE is an entity in which either the equity investment at risk is not sufficient to permit the entity to finance its own activities without additional financial support or the group of holders of the equity investment at risk lack certain characteristics of a controlling financial interest. The primary beneficiary is the entity that has the power to direct the

7

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

activities of the VIE that most significantly affect its performance, and the obligation to absorb losses of the entity or the right to receive benefits from the entity that could potentially be significant to the VIE. Subscriptions and redemptions or amendments to the governing documents of the respective entities could affect an entity's status as a VIE or the determination of the primary beneficiary. Limited partnerships and similar entities are determined to be a VIE generally when the Company is the general partner and the limited partners do not hold substantive kick-out or participation rights. The Company assesses whether it is the primary beneficiary of any VIEs identified by evaluating its economic interests in the entity held either directly by the Company and its affiliates or indirectly through employees. VIEs for which the Company is deemed to be the primary beneficiary are consolidated.

Investments that are determined to be VOEs are consolidated when the Company’s ownership interest is greater than 50% of the outstanding voting interests of the vehicle.

Cash and Cash Equivalents—Cash and cash equivalents include short-term, highly liquid investments, which are readily convertible into cash.

Due from/to Brokers—The Company, including the consolidated investment vehicles, may transact with brokers for certain investment activities. The clearing and custody operations for these investment activities are performed pursuant to contractual agreements. The due from/to brokers balances represent cash and/or cash collateral balances at brokers/custodians and/or receivables and payables for unsettled securities transactions with brokers/custodians.

Investments—Management of the Company determines the appropriate classification of its investments at the time of purchase and re-evaluates such determination no less than on a quarterly basis. The Company's investments are categorized as follows:

•Equity investments at fair value generally represent common stocks, limited partnership interests, master limited partnership interests, preferred securities, non-traded REIT and other seed investments in Company-sponsored vehicles.

•Trading investments generally represent U.S. Treasury securities and investment-grade corporate debt securities.

The Company has elected the fair value option for a seed investment that otherwise would have been accounted for using the equity method of accounting. The fair value of this seed investment is based on the monthly published net asset value (NAV), which is an observable transaction price, however, shares are not actively traded as subscription and redemption activity happens monthly. Realized and unrealized gains and losses are recorded in gain (loss) from investments—net in the Company's condensed consolidated statements of operations. Distributions, if any, from this seed investment are recorded in interest and dividend income—net in the Company's condensed consolidated statements of operations when earned.

Realized and unrealized gains and losses on the Company's investments are recorded in gain (loss) from investments—net in the Company's condensed consolidated statements of operations.

From time to time, the Company, including the consolidated investment vehicles, may enter into derivative contracts, including options, futures and swaps contracts, to gain exposure to the underlying commodities markets or to economically hedge market risk of the underlying portfolios. Gains and losses on derivative contracts are recorded in gain (loss) from investments—net in the Company's condensed consolidated statements of operations. The fair values of these instruments are recorded in other assets or other liabilities and accrued expenses on the Company's condensed consolidated statements of financial condition.

Additionally, from time to time, the Company, including the consolidated investment vehicles, may enter into forward foreign exchange contracts to economically hedge currency exposure. These instruments are measured at fair value based on the prevailing forward exchange rate with gains and losses recorded in foreign currency gain (loss)—net in the Company’s condensed consolidated statements of operations. The fair values of these contracts are recorded in other assets or other liabilities and accrued expenses on the Company’s condensed consolidated statements of financial condition.

8

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

Leases—The Company determines if an arrangement is a lease at inception. The Company has operating leases for corporate offices and certain information technology equipment which are included in operating lease right-of-use (ROU) assets and operating lease liabilities on the Company’s condensed consolidated statements of financial condition.

ROU assets represent the right to use an underlying asset for the lease term and lease liabilities represent obligations to make lease payments arising from the lease. Operating lease ROU assets and lease liabilities are recognized at commencement date based on the net present value of lease payments over the life of the lease and thereafter, are remeasured if there is a change in lease terms. The majority of the Company’s lease agreements do not provide an implicit rate. As a result, the Company used its estimated incremental borrowing rate based on the information available as of the applicable lease commencement date in determining the present value of lease payments. The operating lease ROU assets reflect any upfront lease payments made as well as lease incentives received.

The lease terms may include options to extend or terminate the lease and these are factored into the determination of the ROU asset and lease liability at lease inception when and if it is reasonably certain that the Company will exercise that option. Lease expense for fixed lease payments is recognized on a straight-line basis over the lease term.

The Company has certain lease agreements with non-lease components such as maintenance and executory costs, which are accounted for separately and not included in ROU assets.

ROU assets are tested for impairment whenever changes in facts or circumstances indicate that the carrying amount of an asset may not be recoverable. Modification of a lease term would result in remeasurement of the lease liability and a corresponding adjustment to the ROU asset.

Noncontrolling Interests—Noncontrolling interests consist of nonredeemable and redeemable third-party interests in the Company's consolidated investment vehicles. Noncontrolling interests that are not redeemable at the option of the investors are classified as nonredeemable noncontrolling interests and are included in stockholders’ equity. Noncontrolling interests that are redeemable at the option of the investors are classified as redeemable noncontrolling interests and are not treated as permanent equity. Noncontrolling interests are recorded at fair value which approximates the net asset value at each reporting period.

Investment Advisory and Administration Fees—The Company earns revenue by providing asset management services to institutional accounts, open-end and closed-end funds as well as model-based portfolios. Investment advisory fees are earned pursuant to the terms of investment management agreements and are generally based on a contractual fee rate applied to the average assets under management. The Company also earns administration fees from certain open-end and closed-end funds pursuant to the terms of underlying administration contracts. Administration fees are based on the average daily assets under management of such funds. Investment advisory and administration fee revenue is recognized when earned and is recorded net of any fund reimbursements. The investment advisory and administration contracts each include a single performance obligation as the services provided are not separately identifiable and are accounted for as a series satisfied over time using a time-based method (days elapsed). Additionally, investment advisory and administration fees represent variable consideration, as fees are based on average assets under management which fluctuate daily.

In certain instances, the Company may earn performance fees when specified performance hurdles are met during the performance period. Performance fees are forms of variable consideration and are not recognized until it becomes probable that there will not be a significant reversal of the cumulative revenue recognized.

Distribution and Service Fee Revenue—Distribution and service fee revenue is based on the average daily net assets of certain share classes of U.S. open-end funds. Distribution and service fee revenue is earned daily and is recorded gross of any third-party distribution and service fee expense for applicable share classes.

Distribution fee agreements include a single performance obligation that is satisfied at a point in time when an investor purchases shares in an open-end fund. For all periods presented, a portion of the distribution fee revenue recognized in the period may relate to performance obligations satisfied (or partially satisfied) in prior periods. Service fee agreements include a single performance obligation as the services provided are not separately identifiable and are accounted for as a series satisfied over time using a time-based method (days elapsed). Additionally, distribution and service fees represent variable consideration, as fees are based on average assets under management which fluctuate daily.

9

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

Distribution and Service Fee Expense—Distribution and service fee expense includes distribution fees, shareholder servicing fees and intermediary assistance payments.

Distribution fees represent payments made to qualified intermediaries for assistance in connection with the distribution of certain open-end funds' shares and for other expenses such as advertising, printing and distribution of prospectuses to investors. Such amounts may also be used to pay financial intermediaries for services as specified in the terms of written agreements complying with Rule 12b-1 of the Investment Company Act of 1940. Distribution fees are based on average daily net assets under management of certain share classes of certain of the funds.

Shareholder servicing fees represent payments made to qualified intermediaries for shareholder account service and maintenance. These services are provided pursuant to written agreements with such qualified institutions. Shareholder servicing fees are generally based on average daily net assets under management.

Intermediary assistance payments represent payments to qualified intermediaries for activities related to distribution, shareholder servicing as well as marketing and support of certain open-end funds and are incremental to those described above. Intermediary assistance payments are generally based on average daily net assets under management.

Stock-based Compensation—The Company recognizes compensation expense for the grant-date fair value of restricted stock unit awards to certain employees. This expense is recognized over the period during which employees are required to provide service. Forfeitures are recorded as incurred. Any change to the key terms of an employee’s award subsequent to the grant date is evaluated and, if necessary, accounted for as a modification. If the modification results in the remeasurement of the fair value of the award, the remeasured compensation cost is recognized over the remaining service period.

Income Taxes—The Company records the current and deferred tax consequences of all transactions that have been recognized in the condensed consolidated financial statements in accordance with the provisions of the enacted tax laws. Deferred tax assets are recognized for temporary differences that will result in deductible amounts in future years at tax rates that are expected to apply in those years. Deferred tax liabilities are recognized for temporary differences that will result in taxable income in future years at tax rates that are expected to apply in those years. The Company records a valuation allowance, when necessary, to reduce deferred tax assets to an amount that more likely than not will be realized. The effective tax rate for interim periods is based on the Company's best estimate of the effective tax rate expected to be applied to the full fiscal year adjusted for discrete tax items during the period.

The calculation of tax liabilities involves uncertainties in the application of complex tax laws and regulations across the Company's global operations. A tax benefit from an uncertain tax position is recognized when it is more likely than not that the position will be sustained upon examination, including resolution of any related appeals or litigation processes, on the basis of the technical merits. The Company records potential interest and penalties related to uncertain tax positions in the provision for income taxes in the condensed consolidated statements of operations.

Comprehensive Income—The Company reports all changes in comprehensive income in the condensed consolidated statements of comprehensive income. Comprehensive income generally includes net income or loss attributable to common stockholders and amounts attributable to foreign currency translation gain (loss).

Currency Translation and Transactions—Assets and liabilities of subsidiaries having non-U.S. dollar functional currencies are translated at exchange rates at the applicable condensed consolidated statement of financial condition date. Revenue and expenses of such subsidiaries are translated at average exchange rates during the period. The gains or losses resulting from translating non-U.S. dollar functional currency into U.S. dollars are included in the Company's condensed consolidated statements of comprehensive income. The cumulative translation adjustment was $(8.7 ) million and $(7.7 ) million at March 31, 2024 and December 31, 2023, respectively, and was reported within accumulated other comprehensive income (loss) on the condensed consolidated statements of financial condition. Gains or losses resulting from transactions denominated in currencies other than the U.S. dollar within certain foreign subsidiaries and gains and losses arising on revaluation of U.S. dollar-denominated assets and liabilities held by certain foreign subsidiaries are included in foreign currency gain (loss)—net in the Company’s condensed consolidated statements of operations.

10

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

Recently Issued Accounting Pronouncements—In December 2023, the FASB issued ASU 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures. The standard requires disaggregated information about a reporting entity’s effective tax rate reconciliation as well as additional information on income taxes paid. The standard is intended to benefit investors by providing more detailed income tax disclosures that would be useful in making capital allocation decisions. This new guidance will be effective on January 1, 2025. The Company is currently evaluating the impact that the adoption of this new standard will have on the Company's condensed consolidated financial statements.

In March 2024, the FASB issued ASU 2024-01, Compensation-Stock Compensation (Topic 718): Scope Application of Profits Interest and Similar Awards. The standard clarifies how an entity determines whether a profits interest or similar award is (1) within the scope of ASC 718 or (2) not a share-based payment arrangement and therefore within the scope of other guidance. The guidance in ASU 2024-01 applies to all entities that issue profits interest awards as compensation to employees or nonemployees in exchange for goods or services. This new guidance will be effective on January 1, 2025. The Company is currently evaluating the impact that the adoption of this new standard will have on the Company's condensed consolidated financial statements.

3. Revenue

The following tables summarize revenue recognized from contracts with customers by client domicile and by investment vehicle:

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2024 | 2023 | |||||||||

| Client domicile: | |||||||||||

| North America | $ | $ | |||||||||

| Japan | |||||||||||

| Europe, Middle East and Africa | |||||||||||

| Asia Pacific excluding Japan | |||||||||||

| Total | $ | $ | |||||||||

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2024 | 2023 | |||||||||

| Investment vehicle: | |||||||||||

| Open-end funds | $ | $ | |||||||||

| Institutional accounts | |||||||||||

| Closed-end funds | |||||||||||

| Total | $ | $ | |||||||||

11

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

4. Investments

The following table summarizes the Company's investments:

| (in thousands) | March 31, 2024 | December 31, 2023 | |||||||||

| Equity investments at fair value | $ | $ | |||||||||

| Trading | |||||||||||

| Equity method | |||||||||||

| Total investments | $ | $ | |||||||||

The following table summarizes gain (loss) from investments—net, including derivative financial instruments, the majority of which are used to economically hedge certain exposures (see Note 6, Derivatives):

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2024 | 2023 | |||||||||

| Net realized gains (losses) during the period | $ | ( | $ | ( | |||||||

Net unrealized gains (losses) during the period on investments still held at the end of the period | |||||||||||

Gain (loss) from investments—net (1) | $ | $ | ( | ||||||||

________________________

(1) Included gain (loss) attributable to noncontrolling interests.

The following tables summarize the statements of financial condition attributable to the Company's consolidated VIEs:

| (in thousands) | March 31, 2024 | December 31, 2023 | |||||||||

Assets (1) | |||||||||||

| Investments | $ | $ | |||||||||

| Due from brokers | |||||||||||

| Other assets | |||||||||||

| Total assets | |||||||||||

Liabilities (1) | |||||||||||

| Due to brokers | $ | $ | |||||||||

| Other liabilities and accrued expenses | |||||||||||

| Total liabilities | |||||||||||

| Net assets | $ | $ | |||||||||

| Attributable to the Company | $ | $ | |||||||||

| Attributable to noncontrolling interests | |||||||||||

| Net assets | $ | $ | |||||||||

_________________________

(1) The assets may only be used to settle obligations of each VIE and the liabilities are the sole obligation of each VIE, for which creditors do not have recourse to the general credit of the Company.

12

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

5. Fair Value

ASC Topic 820, Fair Value Measurement specifies a hierarchy of valuation classifications based on whether the inputs to the valuation techniques used in each valuation classification are observable or unobservable. These classifications are summarized in the three broad levels listed below:

•Level 1—Unadjusted quoted prices for identical instruments in active markets.

•Level 2—Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations in which all significant inputs and significant value drivers are observable.

•Level 3—Valuations derived from valuation techniques in which significant inputs or significant value drivers are unobservable.

These levels are not necessarily an indication of the risk or liquidity associated with the investments.

The following tables present fair value measurements:

| March 31, 2024 | |||||||||||||||||||||||||||||

| (in thousands) | Level 1 | Level 2 | Level 3 | Investments Measured at NAV (1) | Total | ||||||||||||||||||||||||

| Cash equivalents | $ | $ | — | $ | — | $ | — | $ | |||||||||||||||||||||

| Equity investments at fair value: | |||||||||||||||||||||||||||||

| Common stocks | $ | $ | $ | — | $ | $ | |||||||||||||||||||||||

| Limited partnership interests | — | ||||||||||||||||||||||||||||

| Master limited partnership interests | — | — | — | ||||||||||||||||||||||||||

| Preferred securities | — | — | |||||||||||||||||||||||||||

| Non-Traded REIT | — | — | — | ||||||||||||||||||||||||||

| Other | — | — | |||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Trading investments: | |||||||||||||||||||||||||||||

| Fixed income | $ | $ | $ | — | $ | $ | |||||||||||||||||||||||

| Equity method investments | $ | $ | $ | — | $ | $ | |||||||||||||||||||||||

| Total investments | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Derivatives - assets: | |||||||||||||||||||||||||||||

| Total return swaps | $ | $ | $ | — | $ | — | $ | ||||||||||||||||||||||

| Forward contracts - foreign exchange | — | — | — | ||||||||||||||||||||||||||

| Total | $ | $ | $ | — | $ | — | $ | ||||||||||||||||||||||

| Derivatives - liabilities: | |||||||||||||||||||||||||||||

| Total return swaps | $ | — | $ | $ | — | $ | — | $ | |||||||||||||||||||||

| Total | $ | $ | $ | — | $ | — | $ | ||||||||||||||||||||||

________________________

(1) Comprised of certain investments measured at fair value using net asset value (NAV) as a practical expedient.

13

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

| December 31, 2023 | |||||||||||||||||||||||||||||

| (in thousands) | Level 1 | Level 2 | Level 3 | Investments Measured at NAV (1) | Total | ||||||||||||||||||||||||

| Cash equivalents | $ | $ | — | $ | — | $ | — | $ | |||||||||||||||||||||

| Equity investments at fair value: | |||||||||||||||||||||||||||||

| Common stocks | $ | $ | $ | — | $ | — | $ | ||||||||||||||||||||||

| Limited partnership interests | — | ||||||||||||||||||||||||||||

| Master limited partnership interests | — | — | — | ||||||||||||||||||||||||||

| Preferred securities | — | — | |||||||||||||||||||||||||||

| Other | — | — | |||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Trading investments: | |||||||||||||||||||||||||||||

| Fixed income | $ | — | $ | $ | — | $ | $ | ||||||||||||||||||||||

| Equity method investments | $ | — | $ | $ | — | $ | $ | ||||||||||||||||||||||

| Total investments | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Derivatives - assets: | |||||||||||||||||||||||||||||

| Total return swaps | $ | — | $ | $ | — | $ | — | $ | |||||||||||||||||||||

| Total | $ | $ | $ | — | $ | — | $ | ||||||||||||||||||||||

| Derivatives - liabilities: | |||||||||||||||||||||||||||||

| Total return swaps | $ | — | $ | $ | — | $ | — | $ | |||||||||||||||||||||

| Forward contracts - foreign exchange | — | — | — | ||||||||||||||||||||||||||

| Total | $ | $ | $ | — | $ | — | $ | ||||||||||||||||||||||

________________________

(1) Comprised of certain investments measured at fair value using NAV as a practical expedient.

Equity investments at fair value classified as Level 2 included common stocks, the Company's non-traded REIT Cohen & Steers Income Opportunities REIT, Inc. (CNSREIT) and preferred securities, for which quoted prices in active markets are not available. Fair values were generally based on quoted prices for similar instruments in active markets. Effective January 1, 2024, the Company deconsolidated its investment in CNSREIT and elected the fair value option to align the measurement of the seed investment and the related gains and losses with other seed investments. The fair value of the seed investment in CNSREIT was $23.9 million and the Company's ownership interest was 49.8 % at March 31, 2024. For the three months ended March 31, 2024, the unrealized gain on the seed investment in CNSREIT, which is included in gain (loss) from investments—net in the Company's condensed consolidated statements of operations, was $71,366 .

Equity investments at fair value classified as Level 3 were comprised of limited partnership interests in joint ventures that hold investments in private real estate.

Trading investments classified as Level 2 were comprised of U.S. Treasury securities and corporate debt securities. Fair values were generally determined using third-party pricing services. The pricing services may utilize evaluated pricing models that vary by asset class and incorporate available trade, bid and other market information.

Investments measured at NAV were comprised of certain investments measured at fair value using NAV (or its equivalent) as a practical expedient as follows:

•Equity investments at fair value included:

◦limited partnership interests in private real estate funds; and

◦the Company's co-investment in a Cayman trust invested in global listed infrastructure securities (which is included in "Other" in the leveling table).

14

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

•Equity method investments included the Company's partnership interests in Cohen & Steers Global Realty Partners III-TE, L.P. (GRP-TE) and Cohen & Steers Global Listed Infrastructure Fund L.P. (LPGI). GRP-TE invests in non-registered real estate funds and LPGI invests in global infrastructure securities. The Company's ownership interest in GRP-TE was approximately 0.2 % at each of March 31, 2024 and December 31, 2023. The Company's ownership interest in LPGI was approximately 0.01 % at each of March 31, 2024 and December 31, 2023.

At March 31, 2024 and December 31, 2023, the Company did not have the ability to redeem its limited partnership interests in private real estate funds or its interest in GRP-TE. There were no contractual restrictions on the Company's ability to redeem its interest in the Cayman trust or LPGI.

Investments measured at NAV as a practical expedient have not been classified in the fair value hierarchy. The amounts presented in the above tables are intended to permit reconciliation of the fair value hierarchy to the amounts presented on the condensed consolidated statements of financial condition.

Total return swap contracts classified as Level 2 were valued based on the underlying futures contracts or equity indices.

Foreign currency exchange contracts classified as Level 2 were valued based on the prevailing forward exchange rate, which is an input that is observable in active markets.

The following table summarizes the changes in Level 3 investments measured at fair value on a recurring basis:

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2024 | 2023 | |||||||||

| Balance at beginning of period | $ | ||||||||||

| Purchases/contributions | |||||||||||

| Unrealized gains (losses) | ( | ( | |||||||||

| Balance at end of period | $ | $ | |||||||||

Unrealized gains (losses) and realized gains (losses), if any, in the above table were recorded in gain (loss) from investments—net in the Company's condensed consolidated statements of operations.

Valuation Techniques

In certain instances, debt and equity securities are valued on the basis of prices from an orderly transaction between market participants provided by reputable broker-dealers or independent pricing services. In determining the value of a particular investment, independent pricing services may use information with respect to transactions in such investments, broker quotes, pricing matrices, market transactions in comparable investments and various relationships between investments. As part of its independent price verification process, the Company generally performs reviews of valuations provided by broker-dealers or independent pricing services. Investments in funds are valued at their closing price or NAV (or its equivalent) as a practical expedient.

In the absence of observable market prices, the Company values its investments using valuation methodologies applied on a consistent basis. For some investments, little market activity may exist; management's determination of fair value is then based on the best information available in the circumstances, and may incorporate management's own assumptions and involve a significant degree of judgment, taking into consideration a combination of internal and external factors. Such investments are valued no less than on a quarterly basis, taking into consideration any changes in key inputs and changes in economic and other relevant conditions, and valuation models are updated accordingly. The Company has established a valuation committee, comprised of senior members from various departments within the Company, to administer, implement and oversee the valuation policies and procedures (the Valuation Committee). Additionally, the Company has retained an independent valuation services firm to assist in the determination of the fair value of certain private real estate investments.

15

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

The following table summarizes the valuation techniques and significant unobservable inputs approved by the Valuation Committee for Level 3 investments measured at fair value on a recurring basis:

Fair Value as of March 31, 2024 (in thousands) | Valuation Technique | Unobservable Inputs | Value | |||||||||||||||||||||||

Limited partnership interests | $ | Discounted cash flow | Discount rate Terminal capitalization rate | |||||||||||||||||||||||

| Transaction price | n/a | |||||||||||||||||||||||||

Fair Value as of December 31, 2023 (in thousands) | Valuation Technique | Unobservable Inputs | Value | |||||||||||||||||||||||

Limited partnership interests | $ | Discounted cash flow | Discount rate Terminal capitalization rate | |||||||||||||||||||||||

| Transaction price | n/a | |||||||||||||||||||||||||

Changes in the significant unobservable inputs in the above tables may result in a materially higher or lower fair value measurement.

6. Derivatives

The following tables summarize the notional amount and fair value of the outstanding derivative financial instruments, none of which were designated in a formal hedging relationship:

| As of March 31, 2024 | |||||||||||||||||||||||

| Notional Amount | Fair Value (1) | ||||||||||||||||||||||

| (in thousands) | Long | Short | Assets | Liabilities | |||||||||||||||||||

| Corporate derivatives: | |||||||||||||||||||||||

| Total return swaps | $ | $ | $ | $ | |||||||||||||||||||

| Forward contracts - foreign exchange | |||||||||||||||||||||||

| Total corporate derivatives | $ | $ | $ | $ | |||||||||||||||||||

| As of December 31, 2023 | |||||||||||||||||||||||

| Notional Amount | Fair Value (1) | ||||||||||||||||||||||

| (in thousands) | Long | Short | Assets | Liabilities | |||||||||||||||||||

| Corporate derivatives: | |||||||||||||||||||||||

| Total return swaps | $ | $ | $ | $ | |||||||||||||||||||

| Forward contracts - foreign exchange | |||||||||||||||||||||||

| Total corporate derivatives | $ | $ | $ | $ | |||||||||||||||||||

________________________

(1)The fair value of derivative financial instruments is recorded in other assets and other liabilities and accrued expenses on the Company's condensed consolidated statements of financial condition.

The Company's corporate derivatives included:

•Total return swaps which are utilized to economically hedge a portion of the market risk of certain seed investments and to gain exposure for the purpose of establishing a performance track record; and

•Forward foreign exchange contracts which are utilized to economically hedge currency exposure arising from certain non-U.S. dollar investment advisory fees.

Collateral pledged for forward and swap contracts totaled $2.5 million and $4.5 million at March 31, 2024 and December 31, 2023, respectively.

16

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

The following table summarizes net gains (losses) from derivative financial instruments:

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2024 | 2023 | |||||||||

| Corporate derivatives: | |||||||||||

| Total return swaps | $ | ( | $ | ( | |||||||

| Forward contracts - foreign exchange | |||||||||||

Total (1) | $ | $ | ( | ||||||||

________________________

(1)Gains and losses on total return swaps are included in gain (loss) from investments—net in the Company's condensed consolidated statements of operations. Gains and losses on forward foreign exchange contracts are included in foreign currency gain (loss)—net in the Company's condensed consolidated statements of operations.

7. Earnings Per Share

Basic earnings per share is calculated by dividing net income attributable to common stockholders by the weighted average shares outstanding. Diluted earnings per share is calculated by dividing net income attributable to common stockholders by the total weighted average shares of common stock outstanding and common stock equivalents determined using the treasury stock method. Common stock equivalents are comprised of dilutive potential shares from restricted stock unit awards and are excluded from the computation if their effect is anti-dilutive.

The following table reconciles income and share data used in the basic and diluted earnings per share computations:

| Three Months Ended March 31, | |||||||||||

| (in thousands, except per share data) | 2024 | 2023 | |||||||||

| Net income | $ | $ | |||||||||

| Net (income) loss attributable to noncontrolling interests | ( | ( | |||||||||

| Net income attributable to common stockholders | $ | $ | |||||||||

| Basic weighted average shares outstanding | |||||||||||

| Dilutive potential shares from restricted stock units | |||||||||||

| Diluted weighted average shares outstanding | |||||||||||

| Basic earnings per share attributable to common stockholders | $ | $ | |||||||||

| Diluted earnings per share attributable to common stockholders | $ | $ | |||||||||

| Anti-dilutive common stock equivalents excluded from the calculation | |||||||||||

17

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

8. Income Taxes

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| U.S. statutory tax rate | % | % | |||||||||

| State and local income taxes, net of federal benefit | |||||||||||

| Non-deductible executive compensation | |||||||||||

| Excess tax benefits related to the vesting and delivery of restricted stock units | ( | ( | |||||||||

| Valuation allowance on corporate seed investments | ( | ||||||||||

| Unrecognized tax benefit adjustments | |||||||||||

| Other | ( | ||||||||||

| Effective income tax rate | % | % | |||||||||

9. Related Party Transactions

The Company is an investment adviser to, and has administration agreements with, Company-sponsored funds and investment products for which certain employees are officers and/or directors.

The following table summarizes revenue the Company earned from these affiliated funds:

| Three Months Ended March 31, | |||||||||||

| (in thousands) | 2024 | 2023 | |||||||||

Investment advisory and administration fees (1) | $ | $ | |||||||||

| Distribution and service fees | |||||||||||

| Total | $ | $ | |||||||||

_________________________

(1) Investment advisory and administration fees are reflected net of fund reimbursements of $3.9 million and $4.6 million for the three months ended March 31, 2024 and 2023, respectively.

Included in accounts receivable at March 31, 2024 and December 31, 2023 are receivables due from Company-sponsored funds, which are generally collectible the next business day, of $34.6 million and $32.5 million, respectively. Included in accounts payable at March 31, 2024 and December 31, 2023 are payables due to Company-sponsored funds of $0.2 million and $1.9 million, respectively.

Included in other assets at March 31, 2024 and December 31, 2023 is an advance to CNSREIT of $7.5 million and $7.3 million, respectively. CNSREIT will reimburse the Company ratably over a 60-month period commencing at the earlier of December 31, 2025, or the month that CNSREIT's NAV is at least $1.0 billion. At March 31, 2024 and December 31, 2023, the Company determined the advance to be collectible.

See discussion of commitments to Company-sponsored vehicles in Note 11.

10. Credit Agreement

On January 20, 2023, the Company entered into a Credit Agreement with Bank of America, N.A. (the Credit Agreement) providing for a $100.0 million senior unsecured revolving credit facility maturing on January 20, 2026. Borrowings under the Credit Agreement bear interest at a variable annual rate equal to, at the Company’s option, either, (i) in respect of Term Secured Overnight Financing Rate (SOFR) Loans (as defined in the Credit Agreement), a rate equal to Term SOFR (as defined in the Credit Agreement) in effect for such period plus an applicable rate as determined according to a performance pricing grid and, (ii) in respect of Base Rate Loans (as defined in the Credit Agreement), a rate equal to a Base

18

COHEN & STEERS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(UNAUDITED)

Rate (as defined in the Credit Agreement) plus an applicable rate as determined according to a performance pricing grid. The Company is also required to pay a quarterly commitment fee determined according to a performance pricing grid and based on the actual daily unused amount of the Credit Agreement.

Borrowings under the Credit Agreement may be used for working capital and other general corporate purposes. The Credit Agreement contains affirmative, negative and financial covenants, which are customary for facilities of this type, including with respect to leverage and interest coverage, limitations on priority indebtedness, asset dispositions and fundamental corporate changes. As of March 31, 2024, the Company was in compliance with these covenants.

To date, the Company has not drawn upon the credit agreement.

11. Commitments and Contingencies

From time to time, the Company is involved in legal matters relating to claims arising in the ordinary course of business. There are currently no such matters pending that the Company believes could have a material adverse effect on its consolidated results of operations, cash flows or financial position.

The Company has committed to invest up to $50.0 million in Cohen & Steers Real Estate Opportunities Fund, L.P. As of March 31, 2024, the Company had funded $21.7 million of this commitment. On May 1, 2024, the Company funded an additional $6.6 million of this commitment.

In addition, the Company has committed to invest up to $125.0 million in CNSREIT. As of March 31, 2024, the Company had funded $23.8 million of this commitment.

The timing for funding the remaining portion of the Company's commitments is uncertain.

12. Concentration of Credit Risk

The Company's cash and cash equivalents are principally on deposit with major national financial institutions and are subject to credit risk should these financial institutions be unable to fulfill their obligations. The Company limits its exposure to such credit risks by diversifying its cash and cash equivalents among several highly rated national financial institutions.

13. Subsequent Events

The Company has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date the condensed consolidated financial statements were issued. Other than the items described below, the Company determined that there were no additional subsequent events that require disclosure and/or adjustment.

On April 22, 2024, the Company issued 1,007,057 shares of its common stock through an “at-the-market” equity offering program (the ATM Program). The net proceeds to the Company, after deducting commissions and estimated offering expenses, were approximately $68.4 million. The Company will not offer or sell any additional shares of its common stock under the ATM Program and has terminated the program effective April 22, 2024.

On May 2, 2024, the Company declared a quarterly dividend on its common stock in the amount of $0.59 per share. This dividend will be payable on May 23, 2024 to stockholders of record at the close of business on May 13, 2024.

19

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations

Set forth on the following pages is management's discussion and analysis of our financial condition and results of operations for the three months ended March 31, 2024 and 2023. Such information should be read in conjunction with our condensed consolidated financial statements and the related notes included herein. The condensed consolidated financial statements of the Company are unaudited. When we use the terms "Cohen & Steers," the "Company," "we," "us," and "our," we mean Cohen & Steers, Inc., a Delaware corporation, and its consolidated subsidiaries.

Executive Overview

General

We are a global investment manager specializing in real assets and alternative income, including listed and private real estate, preferred securities, infrastructure, resource equities, commodities, as well as multi-strategy solutions. Founded in 1986, we are headquartered in New York City, with offices in London, Dublin, Hong Kong, Tokyo and Singapore.

Our primary investment strategies include U.S. real estate, preferred securities, including low duration preferred securities, private real estate solutions, global/international real estate, global listed infrastructure, real assets multi-strategy, as well as global natural resource equities. Our strategies seek to achieve a variety of investment objectives for different risk profiles and are actively managed by specialist teams of investment professionals who employ fundamental-driven research and portfolio management processes. We offer our strategies through a variety of investment vehicles, including U.S. and non-U.S. registered funds and other commingled vehicles, separate accounts and subadvised portfolios.

Our distribution network encompasses two major channels, wealth and institutional. Our wealth channel includes registered investment advisers, wirehouses, independent and regional broker dealers and bank trusts. Our institutional channel includes sovereign wealth funds, corporate plans, insurance companies and public funds, including defined benefit and defined contribution plans, as well as other financial institutions that access our investment management services directly or through consultants and other intermediaries.

Our revenue from the wealth channel is primarily derived from investment advisory, administration, distribution and service fees from open-end and closed-end funds as well as other commingled vehicles. Our revenue from the institutional channel is derived from fees received from our clients for managing advised and subadvised accounts. Our fees are based on contractually specified rates applied to the value of the assets we manage and, in certain cases, may include a performance-based fee. Our revenue fluctuates with changes in the total value of our assets under management, which may occur as a result of market appreciation and depreciation, contributions or withdrawals from investor accounts and distributions. This revenue is recognized over the period that the assets are managed.

20

Assets Under Management

By Investment Vehicle

(in millions)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Open-end Funds | |||||||||||

| Assets under management, beginning of period | $ | 37,032 | $ | 36,903 | |||||||

| Inflows | 3,302 | 3,474 | |||||||||

| Outflows | (2,733) | (3,779) | |||||||||

| Net inflows (outflows) | 569 | (305) | |||||||||

| Market appreciation (depreciation) | 356 | 110 | |||||||||

| Distributions | (272) | (281) | |||||||||

| Total increase (decrease) | 653 | (476) | |||||||||

| Assets under management, end of period | $ | 37,685 | $ | 36,427 | |||||||

| Percentage of total assets under management | 46.4 | % | 45.6 | % | |||||||

| Average assets under management | $ | 36,923 | $ | 38,440 | |||||||

| Institutional Accounts | |||||||||||

| Assets under management, beginning of period | $ | 35,028 | $ | 32,373 | |||||||

| Inflows | 902 | 715 | |||||||||

| Outflows | (3,445) | (833) | |||||||||

| Net inflows (outflows) | (2,543) | (118) | |||||||||

| Market appreciation (depreciation) | 123 | 608 | |||||||||

| Distributions | (184) | (259) | |||||||||

| Total increase (decrease) | (2,604) | 231 | |||||||||

| Assets under management, end of period | $ | 32,424 | $ | 32,604 | |||||||

| Percentage of total assets under management | 39.9 | % | 40.8 | % | |||||||

| Average assets under management | $ | 32,284 | $ | 33,409 | |||||||

| Closed-end Funds | |||||||||||

| Assets under management, beginning of period | $ | 11,076 | $ | 11,149 | |||||||

| Inflows | 4 | 11 | |||||||||

| Outflows | — | (85) | |||||||||

| Net inflows (outflows) | 4 | (74) | |||||||||

| Market appreciation (depreciation) | 200 | (47) | |||||||||

| Distributions | (154) | (154) | |||||||||

| Total increase (decrease) | 50 | (275) | |||||||||

Assets under management, end of period | $ | 11,126 | $ | 10,874 | |||||||

| Percentage of total assets under management | 13.7 | % | 13.6 | % | |||||||

| Average assets under management | $ | 10,968 | $ | 11,353 | |||||||

| Total | |||||||||||

| Assets under management, beginning of period | $ | 83,136 | $ | 80,425 | |||||||

| Inflows | 4,208 | 4,200 | |||||||||

| Outflows | (6,178) | (4,697) | |||||||||

| Net inflows (outflows) | (1,970) | (497) | |||||||||

| Market appreciation (depreciation) | 679 | 671 | |||||||||

| Distributions | (610) | (694) | |||||||||

| Total increase (decrease) | (1,901) | (520) | |||||||||

| Assets under management, end of period | $ | 81,235 | $ | 79,905 | |||||||

| Average assets under management | $ | 80,175 | $ | 83,202 | |||||||

21

Assets Under Management - Institutional Accounts

By Account Type

(in millions)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Advisory | |||||||||||

| Assets under management, beginning of period | $ | 20,264 | $ | 18,631 | |||||||

| Inflows | 687 | 222 | |||||||||

| Outflows | (2,883) | (621) | |||||||||

| Net inflows (outflows) | (2,196) | (399) | |||||||||

| Market appreciation (depreciation) | 128 | 258 | |||||||||

| Total increase (decrease) | (2,068) | (141) | |||||||||

| Assets under management, end of period | $ | 18,196 | $ | 18,490 | |||||||

| Percentage of institutional assets under management | 56.1 | % | 56.7 | % | |||||||

| Average assets under management | $ | 18,066 | $ | 19,123 | |||||||

| Japan Subadvisory | |||||||||||

| Assets under management, beginning of period | $ | 9,026 | $ | 8,376 | |||||||

| Inflows | 43 | 385 | |||||||||

| Outflows | (355) | (59) | |||||||||

| Net inflows (outflows) | (312) | 326 | |||||||||

| Market appreciation (depreciation) | 5 | 270 | |||||||||

| Distributions | (184) | (259) | |||||||||

| Total increase (decrease) | (491) | 337 | |||||||||

| Assets under management, end of period | $ | 8,535 | $ | 8,713 | |||||||

| Percentage of institutional assets under management | 26.3 | % | 26.7 | % | |||||||

| Average assets under management | $ | 8,640 | $ | 8,739 | |||||||

| Subadvisory Excluding Japan | |||||||||||

| Assets under management, beginning of period | $ | 5,738 | $ | 5,366 | |||||||

| Inflows | 172 | 108 | |||||||||

| Outflows | (207) | (153) | |||||||||

| Net inflows (outflows) | (35) | (45) | |||||||||

| Market appreciation (depreciation) | (10) | 80 | |||||||||

| Total increase (decrease) | (45) | 35 | |||||||||

| Assets under management, end of period | $ | 5,693 | $ | 5,401 | |||||||

| Percentage of institutional assets under management | 17.6 | % | 16.6 | % | |||||||

| Average assets under management | $ | 5,578 | $ | 5,547 | |||||||

| Total Institutional Accounts | |||||||||||

| Assets under management, beginning of period | $ | 35,028 | $ | 32,373 | |||||||

| Inflows | 902 | 715 | |||||||||

| Outflows | (3,445) | (833) | |||||||||

| Net inflows (outflows) | (2,543) | (118) | |||||||||

| Market appreciation (depreciation) | 123 | 608 | |||||||||

| Distributions | (184) | (259) | |||||||||

| Total increase (decrease) | (2,604) | 231 | |||||||||

| Assets under management, end of period | $ | 32,424 | $ | 32,604 | |||||||

| Average assets under management | $ | 32,284 | $ | 33,409 | |||||||

22

Assets Under Management

By Investment Strategy

(in millions)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| U.S. Real Estate | |||||||||||

| Assets under management, beginning of period | $ | 38,550 | $ | 35,108 | |||||||

| Inflows | 2,089 | 2,033 | |||||||||

| Outflows | (1,728) | (1,599) | |||||||||

| Net inflows (outflows) | 361 | 434 | |||||||||

| Market appreciation (depreciation) | (79) | 907 | |||||||||

| Distributions | (356) | (437) | |||||||||

| Transfers | — | 68 | |||||||||

| Total increase (decrease) | (74) | 972 | |||||||||

| Assets under management, end of period | $ | 38,476 | $ | 36,080 | |||||||

| Percentage of total assets under management | 47.4 | % | 45.2 | % | |||||||

| Average assets under management | $ | 37,737 | $ | 36,772 | |||||||

| Preferred Securities | |||||||||||

| Assets under management, beginning of period | $ | 18,164 | $ | 19,767 | |||||||

| Inflows | 1,233 | 1,454 | |||||||||

| Outflows | (1,251) | (2,326) | |||||||||

| Net inflows (outflows) | (18) | (872) | |||||||||

| Market appreciation (depreciation) | 625 | (492) | |||||||||

| Distributions | (181) | (195) | |||||||||

| Transfers | (1) | 2 | |||||||||

| Total increase (decrease) | 425 | (1,557) | |||||||||

| Assets under management, end of period | $ | 18,589 | $ | 18,210 | |||||||

| Percentage of total assets under management | 22.9 | % | 22.8 | % | |||||||

| Average assets under management | $ | 18,420 | $ | 20,227 | |||||||

| Global/International Real Estate | |||||||||||

| Assets under management, beginning of period | $ | 15,789 | $ | 14,782 | |||||||

| Inflows | 620 | 273 | |||||||||

| Outflows | (2,828) | (417) | |||||||||

| Net inflows (outflows) | (2,208) | (144) | |||||||||

| Market appreciation (depreciation) | (124) | 202 | |||||||||

| Distributions | (16) | (8) | |||||||||

| Transfers | 1 | (70) | |||||||||

| Total increase (decrease) | (2,347) | (20) | |||||||||

| Assets under management, end of period | $ | 13,442 | $ | 14,762 | |||||||

| Percentage of total assets under management | 16.5 | % | 18.5 | % | |||||||

| Average assets under management | $ | 13,547 | $ | 15,321 | |||||||

23

Assets Under Management

By Investment Strategy - continued

(in millions)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Global Listed Infrastructure | |||||||||||

| Assets under management, beginning of period | $ | 8,356 | $ | 8,596 | |||||||

| Inflows | 80 | 135 | |||||||||

| Outflows | (184) | (124) | |||||||||

| Net inflows (outflows) | (104) | 11 | |||||||||

| Market appreciation (depreciation) | 193 | 35 | |||||||||

| Distributions | (50) | (46) | |||||||||

| Total increase (decrease) | 39 | — | |||||||||

| Assets under management, end of period | $ | 8,395 | $ | 8,596 | |||||||

| Percentage of total assets under management | 10.3 | % | 10.8 | % | |||||||

| Average assets under management | $ | 8,191 | $ | 8,682 | |||||||

| Other | |||||||||||

| Assets under management, beginning of period | $ | 2,277 | $ | 2,172 | |||||||

| Inflows | 186 | 305 | |||||||||

| Outflows | (187) | (231) | |||||||||

| Net inflows (outflows) | (1) | 74 | |||||||||

| Market appreciation (depreciation) | 64 | 19 | |||||||||

| Distributions | (7) | (8) | |||||||||

| Total increase (decrease) | 56 | 85 | |||||||||

| Assets under management, end of period | $ | 2,333 | $ | 2,257 | |||||||

| Percentage of total assets under management | 2.9 | % | 2.8 | % | |||||||

| Average assets under management | $ | 2,280 | $ | 2,200 | |||||||

| Total | |||||||||||

| Assets under management, beginning of period | $ | 83,136 | $ | 80,425 | |||||||

| Inflows | 4,208 | 4,200 | |||||||||

| Outflows | (6,178) | (4,697) | |||||||||

| Net inflows (outflows) | (1,970) | (497) | |||||||||

| Market appreciation (depreciation) | 679 | 671 | |||||||||

| Distributions | (610) | (694) | |||||||||

| Total increase (decrease) | (1,901) | (520) | |||||||||

| Assets under management, end of period | $ | 81,235 | $ | 79,905 | |||||||

| Average assets under management | $ | 80,175 | $ | 83,202 | |||||||

24

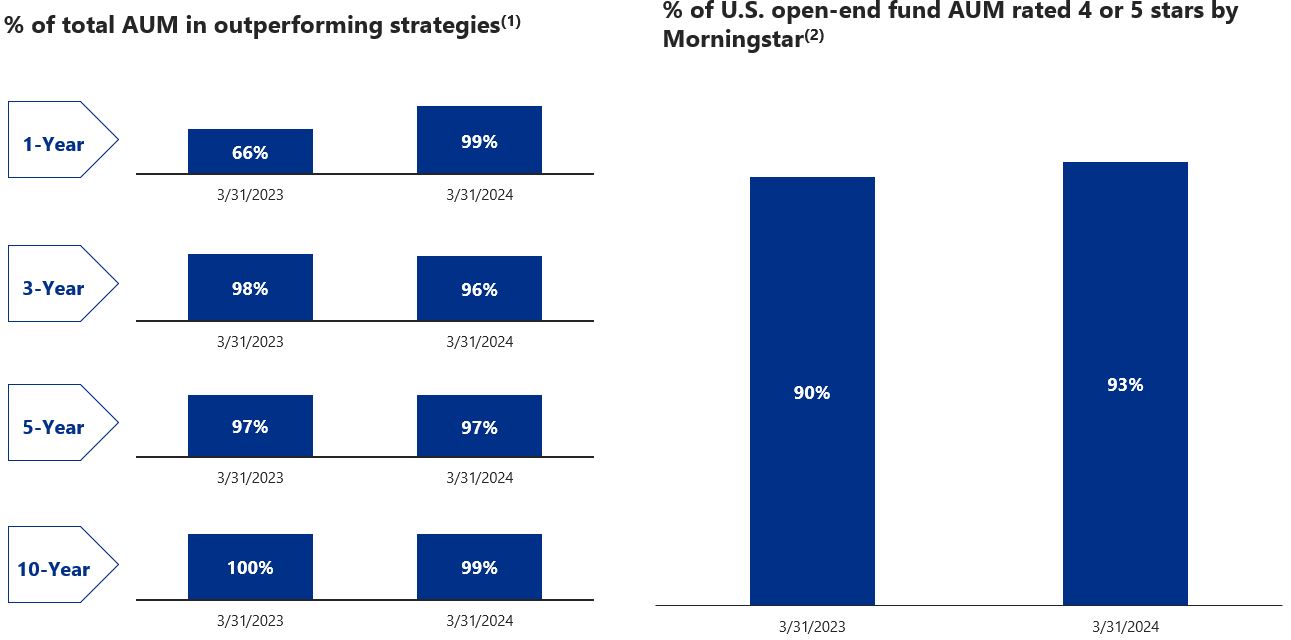

Investment Performance at March 31, 2024

_________________________

_________________________(1) Past performance is no guarantee of future results. Outperformance is determined by comparing the annualized investment performance of each investment strategy to the performance of specified reference benchmarks. Investment performance in excess of the performance of the benchmark is considered outperformance. The investment performance calculation of each investment strategy is based on all active accounts and investment models pursuing similar investment objectives. For accounts, actual investment performance is measured gross of fees and net of withholding taxes. For investment models, for which actual investment performance does not exist, the investment performance of a composite of accounts pursuing comparable investment objectives is used as a proxy for actual investment performance. The performance of the specified reference benchmark for each account and investment model is measured net of withholding taxes, where applicable. This is not investment advice and may not be construed as sales or marketing material for any financial product or service sponsored or provided by Cohen & Steers.

(2) © 2024 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Morningstar calculates its ratings based on a risk-adjusted return measure that accounts for variation in a fund's monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive five stars, the next 22.5% receive four stars, the next 35% receive three stars, the next 22.5% receive two stars and the bottom 10% receive one star. Past performance is no guarantee of future results. Based on independent rating by Morningstar, Inc. of investment performance of each Cohen & Steers-sponsored open-end U.S.-registered mutual fund for all share classes for the overall period at March 31, 2024. Overall Morningstar rating is a weighted average based on the 3-year, 5-year and 10-year Morningstar rating. Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in the distribution percentages. This is not investment advice and may not be construed as sales or marketing material for any financial product or service sponsored or provided by Cohen & Steers.

Overview