UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended June 30, 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 001-36201

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

(332 ) 255-9818

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

| ☒ | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

On July 28, 2023, 44,595,383 shares of common stock, $0.0001 par value, were outstanding.

IMMUNIC, INC.

INDEX

| Page No. | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | |||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

2

IMMUNIC, INC.

Condensed Consolidated Balance Sheets

(In thousands, except share and per share amounts)

| June 30, 2023 | December 31, 2022 | ||||||||||

| (Unaudited) | |||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Investments - other | |||||||||||

| Other current assets and prepaid expenses | |||||||||||

| Total current assets | |||||||||||

| Property and equipment, net | |||||||||||

| Right-of-use assets, net | |||||||||||

| Other long-term assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and Stockholders’ Equity | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Long term liabilities | |||||||||||

| Operating lease liabilities | |||||||||||

| Total long-term liabilities | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies (Note 4) | |||||||||||

| Stockholders’ equity: | |||||||||||

Preferred stock, $ | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated other comprehensive income | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

3

IMMUNIC, INC.

Condensed Consolidated Statements of Operations

(In thousands, except share and per share amounts)

(Unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

| Operating expenses: | ||||||||||||||||||||||||||

| Research and development | $ | $ | $ | $ | ||||||||||||||||||||||

| General and administrative | ||||||||||||||||||||||||||

| Total operating expenses | ||||||||||||||||||||||||||

| Loss from operations | ( | ( | ( | ( | ||||||||||||||||||||||

| Other income (expense): | ||||||||||||||||||||||||||

| Interest income | ||||||||||||||||||||||||||

| Other income (expense), net | ( | ( | ||||||||||||||||||||||||

| Total other income (expense) | ( | ( | ||||||||||||||||||||||||

| Net loss | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Net loss per share, basic and diluted | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Weighted-average common shares outstanding, basic and diluted | ||||||||||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

4

IMMUNIC, INC.

Condensed Consolidated Statements of Comprehensive Loss

(In thousands)

(Unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

| Net loss | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Other comprehensive income (loss): | ||||||||||||||||||||||||||

| Foreign currency translation | ( | ( | ||||||||||||||||||||||||

| Total comprehensive loss | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

5

IMMUNIC, INC.

Condensed Consolidated Statements of Stockholders’ Equity

(In thousands, except share amounts)

(Unaudited)

| Six Months Ended June 30, 2023 | |||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Other Comprehensive Income | Accumulated Deficit | Total Stockholders’ Equity | |||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||

| Balance at January 1, 2023 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| Net loss | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Foreign exchange translation adjustment | — | — | — | — | |||||||||||||||||||||||||||||||

| Shares issued from exercise of pre-funded warrants | — | — | — | ||||||||||||||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| Net loss | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Foreign exchange translation adjustment | — | — | — | — | |||||||||||||||||||||||||||||||

| Shares issued in connection with the Company's Employee stock purchase plan | — | — | — | ||||||||||||||||||||||||||||||||

| Balance at June 30, 2023 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

6

| Six Months Ended June 30, 2022 | |||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Accumulated Other Comprehensive Loss | Accumulated Deficit | Total Stockholders’ Equity | |||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||

| Balance at January 1, 2022 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Net loss | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Foreign exchange translation adjustment | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Shares issued in connection with the Company's stock option plan | — | — | — | ||||||||||||||||||||||||||||||||

Issuance of common stock - at the market Sales Agreement net of issuance costs of $ | — | — | — | ||||||||||||||||||||||||||||||||

| Balance at March 31, 2022 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Net loss | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Foreign exchange translation adjustment | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Shares issued in connection with the Company's Employee stock purchase plan | — | — | — | ||||||||||||||||||||||||||||||||

Issuance of common stock - at the market Sales Agreement net of issuance costs of $ | — | — | — | ||||||||||||||||||||||||||||||||

| Balance at June 30, 2022 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

7

IMMUNIC, INC.

Condensed Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

| Six Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Cash flows from operating activities: | |||||||||||

| Net loss | $ | ( | $ | ( | |||||||

| Adjustments to reconcile net loss to net cash used in operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Unrealized foreign currency loss | |||||||||||

| Stock-based compensation | |||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Other current assets and prepaid expenses | |||||||||||

| Accounts payable | |||||||||||

| Accrued expenses | ( | ||||||||||

| Other liabilities | ( | ||||||||||

| Net cash used in operating activities | ( | ( | |||||||||

| Cash flows from investing activities: | |||||||||||

| Sale of investments - other | |||||||||||

| Purchases of property and equipment | ( | ( | |||||||||

| Net cash provided by (used in) investing activities | ( | ||||||||||

| Cash flows from financing activities: | |||||||||||

| Proceeds from public offering of common stock through At The Market Sales Agreement, net | |||||||||||

| Proceeds from exercise of stock options | |||||||||||

| Proceeds from shares issued in connection with the Company's employee stock purchase plan | |||||||||||

| Proceeds from the exercise of pre-funded warrants | |||||||||||

| Net cash provided by financing activities | |||||||||||

| Effect of exchange rate changes on cash and cash equivalents | ( | ||||||||||

| Net change in cash and cash equivalents | ( | ||||||||||

| Cash and cash equivalents, beginning of period | |||||||||||

| Cash and cash equivalents, end of period | $ | $ | |||||||||

| Supplemental disclosure of noncash investing and financing activities: | |||||||||||

| Operating lease right-of use asset obtained in exchange for lease obligation | $ | $ | |||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

8

IMMUNIC, INC.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

1. Description of Business and Basis of Financial Statements

Description of Business

Immunic, Inc. ("Immunic" or the "Company") is a biotechnology company developing a clinical pipeline of selective oral immunology therapies focused on treating chronic inflammatory and autoimmune diseases. The Company is headquartered in New York City with its main operations in Gräfelfing near Munich, Germany. The Company currently has approximately 75 employees.

Immunic is pursuing clinical development of orally administered, small molecule programs, each of which has unique features intended to directly address the unmet needs of patients with serious chronic inflammatory and autoimmune diseases. These include the vidofludimus calcium (IMU-838) program, which is in Phase 3 clinical development for patients with multiple sclerosis (“MS”) and which has shown therapeutic activity in Phase 2 clinical trials in patients suffering from relapsing-remitting MS and moderate-to-severe ulcerative colitis (“UC”); the IMU-856 program, which is targeted to regenerate bowel epithelium and restore intestinal barrier function, which could potentially be applicable in numerous gastrointestinal diseases, such as celiac disease, UC, Crohn’s disease or irritable bowel syndrome with diarrhea; and the IMU-381 program, which is a next generation molecule being developed to specifically address the needs of gastrointestinal diseases.

The Company’s business, operating results, financial condition and growth prospects are subject to significant risks and uncertainties, including the failure of its clinical trials to meet their endpoints, failure to obtain regulatory approval and needing additional funding to complete the development and commercialization of the Company's three development programs.

Liquidity and Financial Condition

Immunic has no products approved for commercial sale and has not generated any revenue from product sales. It has never been profitable and has incurred operating losses in each year since inception in 2016. The Company has an accumulated deficit of approximately $366.6 million as of June 30, 2023 and $317.3 million as of December 31, 2022. Substantially all of Immunic's operating losses resulted from expenses incurred in connection with its research and development programs and from general and administrative costs associated with its operations.

Immunic expects to incur significant expenses and increasing operating losses for the foreseeable future as it initiates and continues the development of its product candidates and adds personnel necessary to advance its pipeline of product candidates. Immunic expects that its operating losses will fluctuate significantly from quarter-to-quarter and year-to-year due to timing of development programs.

From inception through June 30, 2023, Immunic has raised net cash of approximately $355.6 million from private and public offerings of preferred and common stock. As of June 30, 2023, the Company had cash and cash equivalents of approximately $77.3 million. With these funds, Immunic expects to be able to fund its operations beyond twelve months from the date of the issuance of the accompanying condensed consolidated financial statements.

Basis of Presentation and Consolidation

The accompanying consolidated financial statements have been prepared in conformity with United States generally accepted accounting principles, ("U.S. GAAP") and include the accounts of Immunic and its wholly-owned subsidiaries, Immunic AG and Immunic Australia Pty Ltd. All intercompany accounts and transactions have been eliminated in consolidation. Immunic manages its operations as a single reportable segment for the purposes of assessing performance and making operating decisions.

Unaudited Interim Financial Information

Immunic has prepared the accompanying interim unaudited condensed consolidated financial statements in accordance with United States generally accepted accounting principles, (“US GAAP”), for interim financial information and with the instructions to Form 10-Q and Regulation S-X of the SEC. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial statements. These interim unaudited condensed consolidated financial statements reflect all adjustments consisting of normal recurring accruals which, in the opinion of management, are necessary to

9

2. Summary of Significant Accounting Policies

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires the Company to make certain estimates and assumptions that affect the reported amounts of assets, liabilities, expenses and the disclosure of contingent assets and liabilities in the Company’s consolidated financial statements. The most significant estimates in the Company’s financial statements and accompanying notes relate to recoverability of goodwill, clinical trial expenses and share-based compensation. Management believes its estimates to be reasonable under the circumstances. Actual results could differ materially from those estimates and assumptions.

Foreign Currency Translation and Presentation

The Company’s reporting currency is United States (“U.S.”) dollars. Immunic AG is located in Germany with the euro being its functional currency. Immunic Australia Pty Ltd.’s functional currency is the Australian dollar. All amounts in the financial statements where the functional currency is not the U.S. dollar are translated into U.S. dollar equivalents at exchange rates as follows:

• assets and liabilities at reporting period-end rates;

• income statement accounts at average exchange rates for the reporting period; and

• components of equity at historical rates.

Gains and losses from translation of the financial statements into U.S. dollars are recorded in stockholders’ equity as a component of accumulated other comprehensive income (loss). Realized and unrealized gains and losses resulting from foreign currency transactions denominated in currencies other than the functional currency are reflected as general and administrative expenses in the Consolidated Statements of Operations. Foreign currency transaction gains and losses related to long-term intercompany loans that are payable in the foreseeable future are recorded in Other Income (Expense). The Consolidated Statements of Cash Flows were prepared by using the average exchange rate in effect during the reporting period which reasonably approximates the timing of the cash flows.

Cash and Cash Equivalents and Investments - other

The Company considers all highly liquid investments with an original maturity of three months or less to be cash equivalents. Time Deposits with an original maturity greater than three months are classified as Investments - other.

Cash and cash equivalents and investments - other consist of cash on hand and deposits in banks located in the U.S. of approximately $62.7 million, Germany of approximately $14.4 million and Australia of approximately $0.2 million as of June 30, 2023. The Company maintains cash and cash equivalent balances denominated in Euro and U.S. dollars with major financial institutions in the U.S. and Germany in excess of the deposit limits insured by the government. Management periodically reviews the credit standing of these financial institutions. The Company currently deposits its cash and cash equivalents with two large financial institutions. Cash and Cash equivalents in the U.S. are held at J.P. Morgan and as of June 30, 2023 are primarily held in a U.S. Government money market fund account earning interest at a rate of 5.0 %. Cash and cash equivalents in Germany are earning interest at a rate of 1.75 % to 2.75 % during the period ended June 30, 2023.

10

Investments - other consists of the following as of (in thousands):

| June 30, 2023 | December 31, 2022 | |||||||||||||

| Time Deposits | $ | $ | ||||||||||||

| $ | $ | |||||||||||||

Fair Value Measurement

Fair value is defined as the price that would be received to sell an asset or be paid to transfer a liability in an orderly transaction between market participants on the measurement date. Accounting guidance establishes a fair value hierarchy that requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. The standard describes three levels of inputs that may be used to measure fair value:

Level 1—Quoted prices in active markets for identical assets or liabilities. Level 1 assets consisted of money market funds for the periods presented. The Company had no Level 1 liabilities for the periods presented.

Level 2—Inputs other than observable quoted prices for the asset or liability, either directly or indirectly; these include quoted prices for similar assets or liabilities in active markets and quoted prices for identical or similar assets or liabilities in markets that are not active. The Company had no Level 2 assets or liabilities for the periods presented.

Level 3—Unobservable inputs to the valuation methodology that are significant to the measurement of the fair value of assets or liabilities. The Company had no Level 3 assets or liabilities for the periods presented.

The carrying value of cash and cash equivalents, other current assets and prepaid expenses, accounts payable, accrued expenses, and other current liabilities approximates fair value due to the short period of time to maturity.

Goodwill

Business combinations are accounted for under the acquisition method. The total purchase price of an acquisition is allocated to the underlying identifiable net assets, based on their respective estimated fair values as of the acquisition date. Determining the fair value of assets acquired and liabilities assumed requires management’s judgment and often involves the use of significant estimates and assumptions, including assumptions with respect to future cash inflows and outflows, probabilities of success, discount rates, and asset lives, among other items. Assets acquired and liabilities assumed are recorded at their estimated fair values. The excess of the purchase price over the estimated fair values of the net assets acquired is recorded as goodwill.

11

On October 20, 2022, the Company announced the outcome of a significant interim analysis of its Phase 1b clinical trial of izumerogant (IMU-935) in patients with moderate-to-severe psoriasis that were not deemed positive progress. On October 21, 2022, the Company experienced a significant decrease in the Company's market capitalization. The Company considered this to be a triggering event indicating that it is more likely than not that goodwill was impaired. The Company performed an analysis of the fair value compared to the Company's book value, utilizing the Company's traded stock price (a level 1 fair value input). As a result of that analysis, the Company recorded an approximately $33.0 million non-cash goodwill impairment charge in the fourth quarter of 2022, which represents a full write down of its previous goodwill balance.

Research and Development Expenses

These costs primarily include external development expenses and internal personnel expenses for its development programs, vidofludimus calcium, izumerogant and IMU-856. Immunic has spent the majority of its research and development resources on vidofludimus calcium, the Company's lead development program for clinical trials in MS, UC and COVID-19.

Research and development expenses consist of expenses incurred in research and development activities, which include clinical trials, contract research services, certain milestone payments, salaries and related employee benefits, allocated facility costs and other outsourced services. Research and development expenses are charged to operations as incurred.

The Company enters into agreements with contract research organizations (“CROs”) to provide clinical trial services for individual studies and projects by executing individual work orders governed by a Master Service Arrangement (“MSA”). The MSAs and associated work orders provide for regular recurrent payments and payments upon the completion of certain milestones. The Company regularly assesses the timing of payments against actual costs incurred to ensure a proper accrual of related expenses in the appropriate accounting period.

Collaboration Arrangements

Certain collaboration and license agreements may include payments to or from the Company of one or more of the following: non-refundable or partially refundable upfront or license fees; development, regulatory and commercial milestone payments; payment for manufacturing supply services; partial or complete reimbursement of research and development costs; and royalties on net sales of licensed products. The Company assesses whether such contracts are within the scope of Financial Accounting Standards Board (FASB) Accounting Standards Update (“ASU”) 2014-09 “Revenue from Contracts with Customers” and ASU No. 2018-18, “Collaborative Arrangements” ("ASU 2018-18"). ASU 2018-18, clarifies that certain elements of collaborative arrangements could qualify as transactions with customers in the scope of ASC 606.

In October 2018, the Company entered into an option and license agreement (the "Daiichi Sankyo Agreement") with Daiichi Sankyo Co., Ltd. ("Daiichi Sankyo") which granted the Company the right to license a group of compounds, designated by the Company as IMU-856, as a potential new oral treatment option for gastrointestinal diseases such as celiac disease, inflammatory bowel disease, irritable bowel syndrome with diarrhea and other barrier function associated diseases. During the option period, the Company performed agreed upon research and development activities for which it was reimbursed by Daiichi Sankyo up to a maximum agreed-upon limit. Such reimbursement was recorded as other income. There are no additional research and development reimbursements expected under this agreement.

Government assistance

Government assistance relating to research and development performed by Immunic Australia is recorded as a component of other (income) expense. This government assistance is recognized at a rate of 43.5 % of the qualified research and development expenditures which are incurred. We also receive government assistance from the German Government for reimbursement of research and development expenses up to one million Euros per year. We recognized $0.3 million and $2.1 million of related to research activities performed during the three and six months ended June 30, 2023, respectively and $0.6 million and $1.4 million related to research activities performed during the three and six months ended June 30, 2022, respectively.

12

General and Administrative Expenses

General and administrative expenses consist primarily of salaries and related costs for personnel in executive, finance, business development and other support functions. Other general and administrative expenses include, but are not limited to, stock-based compensation, insurance costs, professional fees for legal, accounting and tax services, consulting, related facility costs and travel.

Stock-Based Compensation

The Company measures the cost of employee and non-employee services received in exchange for equity awards based on the grant-date fair value of the award recognized generally as an expense (i) on a straight-line basis over the requisite service period for those awards whose vesting is based upon a service condition, and (ii) on an accelerated method for awards whose vesting is based upon a performance condition, but only to the extent it is probable that the performance condition will be met. Stock-based compensation is (i) estimated at the date of grant based on the award’s fair value for equity classified awards and (ii) final measurement date for liability classified awards. Forfeitures are recorded in the period in which they occur.

The Company estimates the fair value of stock options using the Black-Scholes-Merton option-pricing model ("BSM"), which requires the use of estimates and subjective assumptions, including the risk-free interest rate, the fair value of the underlying common stock, the expected dividend yield of the Company’s common stock, the expected volatility of the price of the Company’s common stock, and the expected term of the option. These estimates involve inherent uncertainties and the application of management’s judgment. If factors change and different assumptions are used, the Company’s stock-based compensation expense could be materially different in the future.

Leases

The Company leases office space and office equipment. The underlying lease agreements have lease terms of less than 12 months and up to 60 months. Leases with terms of 12 months or less at inception are not included in the operating lease right of use asset and operating lease liability.

The Company has three existing leases for office space. At inception of a lease agreement, the Company determines whether an agreement represents a lease and at commencement each lease agreement is assessed as to classification as an operating or financing lease. The Company's leases have been classified as operating leases and an operating lease right-of-use asset and an operating lease liability have been recorded on the Company’s balance sheet. A right-of-use lease asset represents the Company’s right to use the underlying asset for the lease term and the lease obligation represents its commitment to make the lease payments arising from the lease. Right-of-use lease assets and obligations are recognized at the commencement date based on the present value of remaining lease payments over the lease term. As the Company’s leases do not provide an implicit rate, the Company has used an estimated incremental borrowing rate based on the information available at the commencement date in determining the present value of lease payments. The right-of-use lease asset includes any lease payments made prior to commencement and excludes any lease incentives. The lease term used in estimating future lease payments may include options to extend when it is reasonably certain that the Company will exercise that option. Operating lease expense is recognized on a straight-line basis over the lease term, subject to any changes in the lease or changes in expectations regarding the lease term. Variable lease costs such as common area costs and property taxes are expensed as incurred. Leases with an initial term of twelve months or less are not recorded on the balance sheet.

Comprehensive Income (Loss)

Comprehensive income (loss) is defined as the change in equity during a period from transactions and other events and circumstances from non-owner sources. Accumulated other comprehensive income (loss) has been reflected as a separate component of stockholders’ equity in the accompanying Consolidated Balance Sheets and consists of foreign currency translation adjustments (net of tax).

Income Taxes

The Company is subject to corporate income tax laws and regulations in the U.S., Germany and Australia. Tax regulations within each jurisdiction are subject to the interpretation of the related tax laws and regulations and require significant judgment in their application.

13

The Company utilizes the asset and liability method of accounting for income taxes which requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the audited consolidated financial statements. Deferred income tax assets and liabilities are determined based on the differences between the financial statement and tax basis of assets and liabilities using enacted tax rates in effect for the year in which the differences are expected to reverse. The effect of changes in tax rates on deferred tax assets and liabilities is recognized in operations in the period that includes the enactment date. Deferred taxes are reduced by a valuation allowance when, in the opinion of management, it is more likely than not some portion or the entire deferred tax asset will not be realized. As of June 30, 2023 and 2022, respectively, the Company maintained a full valuation allowance against the balance of deferred tax assets.

It is the Company’s policy to provide for uncertain tax positions and the related interest and penalties based upon management’s assessment of whether a tax benefit is more likely than not to be sustained upon examination by tax authorities. The Company recognizes interest and penalties accrued on any unrecognized tax benefits as a component of income tax expense. The Company is subject to U.S. federal, New York, California, Texas, German and Australian income taxes. The Company is subject to U.S. federal or state income tax examination by tax authorities for tax returns filed for the years 2003 and forward due to the carryforward of NOLs. Tax years 2016 through 2022 are subject to audit by German and Australian tax authorities. The Company is not currently under examination by any tax jurisdictions.

Warrants

The Company accounts for issued warrants either as a liability or equity in accordance with ASC 480-10, Accounting for Certain Financial Instruments with Characteristics of both Liabilities and Equity (“ASC 480-10”) or ASC 815-40, Accounting for Derivative Financial Instruments Indexed to, and Potentially Settled in, a Company’s Own Stock (“ASC 815-40”). Under ASC 480-10, warrants are considered a liability if they are mandatorily redeemable and they require settlement in cash, other assets, or a variable number of shares. If warrants do not meet liability classification under ASC 480-10, the Company considers the requirements of ASC 815-40 to determine whether the warrants should be classified as a liability or as equity. Under ASC 815-40, contracts that may require settlement for cash are liabilities, regardless of the probability of the occurrence of the triggering event. Liability-classified warrants are measured at fair value on the issuance date and at the end of each reporting period. Any change in the fair value of the warrants after the issuance date is recorded in the consolidated statements of operations as a gain or loss. If warrants do not require liability classification under ASC 815-40, in order to conclude warrants should be classified as equity, the Company assesses whether the warrants are indexed to its common stock and whether the warrants are classified as equity under ASC 815-40 or other applicable U.S. GAAP standard. Equity-classified warrants are accounted for at fair value on the issuance date with no changes in fair value recognized after the issuance date. All of the Company's 5,096,552 pre-funded warrants were exercised in January 2023.

| As of June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Options to purchase common stock | |||||||||||

Recently Issued and/or Adopted Accounting Standards

There are no recently issued accounting standards that would have a significant impact on the company's consolidated financial statements.

14

3. Balance Sheet Details

Other Current Assets and Prepaid Expenses

| June 30, 2023 | December 31, 2022 | ||||||||||

| Prepaid clinical and related costs | $ | $ | |||||||||

| VAT receivable | |||||||||||

| Australian research and development tax incentive | |||||||||||

| Other | |||||||||||

| Total | $ | $ | |||||||||

Accounts Payable

| June 30, 2023 | December 31, 2022 | ||||||||||

| Clinical costs | $ | $ | |||||||||

| Legal and audit costs | |||||||||||

| Other | |||||||||||

| Total | $ | $ | |||||||||

Accrued Expenses

| June 30, 2023 | December 31, 2022 | ||||||||||

| Accrued clinical and related costs | $ | $ | |||||||||

| Accrued legal and audit costs | |||||||||||

| Accrued compensation | |||||||||||

| Accrued other | |||||||||||

| Total | $ | $ | |||||||||

| June 30, 2023 | December 31, 2022 | |||||||||||||

| $ | $ | |||||||||||||

| Other | ||||||||||||||

| Total | $ | $ | ||||||||||||

15

4. Commitments and Contingencies

Operating Leases

The Company leases certain office space under non-cancelable operating leases. The leases terminate on July 31, 2025 for the New York City office, June 30, 2025 for the Gräfelfing, Germany office and November 30, 2028 related to the new lease of a research laboratory in Planegg, Germany. The Company formerly leased office space in Planegg-Martinsried, Germany pursuant to a modified lease that terminated on August 31, 2020. These agreements include both lease (e.g., fixed rent) and non-lease components (e.g., common-area and other maintenance costs). The non-lease components are deemed to be executory costs and are therefore excluded from the minimum lease payments used to determine the present value of the operating lease obligation and related right-of-use asset. The New York City lease was extended on December 22, 2022 for an additional 27 months resulting in the new lease termination date of July 31, 2025. The New York City lease has a renewal option, but this was not included in calculating the right of use asset and liabilities. On April 7, 2020, the Company signed a five year lease for its facility in Gräfelfing, Germany. On March 1, 2021 and August 1, 2022 the Company added additional lease space at the Gräfelfing, Germany office. Renewal options were not included in calculating the right of use asset and liabilities for this facility. In February 2023, the Company leased space in Germany for a research laboratory. The leases do not have concessions, leasehold improvement incentives or other build-out clauses. Further, the leases do not contain contingent rent provisions. The New York City lease had a six month rent holiday at the beginning of the lease as well as a three month rent holiday upon the 27 month extension starting May 2023. There were net additions of $544,000 related to the addition of new laboratory space in Planegg, Germany in February 2023.

The leases do not provide an implicit rate and, due to the lack of a commercially salable product, the Company is generally considered unable to obtain commercial credit. Therefore, the Company estimated its incremental interest rate to be 6 % for the original leases and 8 % for the New York City extension and German laboratory, considering the quoted rates for the lowest investment-grade debt and the interest rates implicit in recent financing leases. Immunic used its estimated incremental borrowing rate and other information available at the lease commencement date in determining the present value of the lease payments.

Immunic’s operating lease costs and variable lease costs were $238,000 and $136,000 for the three months ended June 30, 2023 and 2022, respectively and $433,000 and $266,000 for the six months ended June 30, 2023 and 2022, respectively. Variable lease costs consist primarily of common area maintenance costs, insurance and taxes which are paid based upon actual costs incurred by the lessor.

| 2023 | $ | |||||||

| 2024 | ||||||||

| 2025 | ||||||||

| 2026 | ||||||||

| 2027 | ||||||||

| Thereafter | ||||||||

| Total | $ | |||||||

| Interest | ||||||||

| PV of obligation | $ | |||||||

Contractual Obligations

As of June 30, 2023, the Company has non-cancelable contractual obligations under certain agreements related to its development programs for vidofludimus calcium and IMU-856 totaling approximately $3.4 million, all of which is expected to be paid in the next twelve months.

16

Other Commitments and Obligations

Daiichi Sankyo Agreement

On January 5, 2020, the Company exercised its option to obtain the exclusive worldwide right to commercialization of IMU-856. Among other things, the option exercise grants Immunic AG the rights to Daiichi Sankyo’s patent application related to IMU-856, for which the Company received a notice of allowance from the U.S. Patent & Trademark Office in August 2022. In connection with the option exercise, the Company paid a one-time upfront licensing fee to Daiichi Sankyo. Under the Daiichi Sankyo Agreement, Daiichi Sankyo is also eligible to receive future development, regulatory and sales milestone payments, as well as royalties related to IMU-856.

Legal Proceedings

The Company is not currently a party to any litigation, nor is it aware of any pending or threatened litigation, that it believes would materially affect its business, operating results, financial condition or cash flows. However, its industry is characterized by frequent claims and litigation including securities litigation, claims regarding patent and other intellectual property rights and claims for product liability. As a result, in the future, the Company may be involved in various legal proceedings from time to time.

5. Fair Value

The following fair value hierarchy tables present information about each major category of the Company’s financial assets and liabilities measured at fair value on a recurring basis (in thousands):

| Fair Value Measurement at June 30, 2023 | |||||||||||||||||||||||

| Fair Value | Level 1 | Level 2 | Level 3 | ||||||||||||||||||||

| Assets | |||||||||||||||||||||||

| Money market funds | $ | $ | $ | $ | |||||||||||||||||||

| Total assets at fair value | $ | $ | $ | $ | |||||||||||||||||||

| Fair Value Measurement at Fair Value Measurement at December 31, 2022 | |||||||||||||||||||||||

| Fair Value | Level 1 | Level 2 | Level 3 | ||||||||||||||||||||

| Assets | |||||||||||||||||||||||

| Money market funds | $ | $ | $ | $ | |||||||||||||||||||

| Total assets | $ | $ | $ | $ | |||||||||||||||||||

There were no transfers between Level 1, Level 2 or Level 3 assets during the periods presented.

For the Company’s money market funds which are included as a component of cash and cash equivalents on the consolidated balance sheet, realized gains and losses are included in interest income (expense) on the consolidated statements of operations.

Our money market fund account is held in our bank in the U.S. and was earning interest at a rate of 5.0 % in a U.S. Government money market fund.

The Company has cash balances in banks in excess of the maximum amount insured by the FDIC and other international agencies as of June 30, 2023. The Company has not historically experienced any credit losses with balances in excess of FDIC limits.

The carrying amounts of other current assets and prepaid expenses, accounts payable, accrued expenses, and other current liabilities approximate their fair values due to their short-term nature. The fair value and book value of the money market funds presented in the table above are the same.

17

6. Common Stock

Shelf Registration Statement

In November 2020, Immunic filed a shelf registration statement on Form S-3. The 2020 Shelf Registration Statement permits the offering, issuance and sale of up to $250.0 million of common stock, preferred stock, warrants, debt securities, and/or units in one or more offerings and in any combination of the foregoing. As of July 28, 2023, there is $75.0 million remaining on this shelf registration statement.

In December 2020, the Company filed a Prospectus Supplement for the offering, issuance and sale of up to a maximum aggregate offering price of $50.0 million of common stock that may be issued and sold under an at-the-market sales agreement ("December 2020 ATM") with SVB Leerink LLC (now Leerink Partners) as agent. The Company has used, and intends to continue to use the net proceeds from the offering to continue to fund the ongoing clinical development of its product candidates and for other general corporate purposes, including funding existing and potential new clinical programs and product candidates. The December 2020 ATM will terminate upon the earlier of (i) the issuance and sale of all of the shares through SVB Leerink LLC on the terms and subject to the conditions set forth in the December 2020 ATM or (ii) termination of the December 2020 ATM as otherwise permitted thereby. The December 2020 ATM may be terminated at any time by either party upon ten days’ prior notice, or by SVB Leerink LLC at any time in certain circumstances, including the occurrence of a material adverse effect on the Company. As of July 28, 2023, $8.1 million in capacity remains under the December 2020 ATM.

In May 2022, the Company filed a Prospectus Supplement for the offering, issuance and sale of up to a maximum aggregate offering price of $80.0 million of common stock that may be issued and sold under another at-the-market sales agreement ("May 2022 ATM") with SVB Leerink LLC as agent. The Company intends to use the net proceeds from the offering to continue to fund the ongoing clinical development of its product candidates and for other general corporate purposes, including funding existing and potential new clinical programs and product candidates. The May 2022 ATM will terminate upon the earlier of (i) the issuance and sale of all of the shares through SVB Securities LLC on the terms and subject to the conditions set forth in the May 2022 ATM or (ii) termination of the May 2022 ATM as otherwise permitted thereby. The May 2022 ATM may be terminated at any time by either party upon ten days’ prior notice, or by SVB Securities LLC at any time in certain circumstances, including the occurrence of a material adverse effect on the Company. As of July 28, 2023, $80.0 million in capacity remains under the May 2022 ATM.

The Company has agreed to pay SVB Securities LLC a commission equal to 3.0 % of the gross proceeds from the sales of common shares pursuant to both ATM's and has agreed to provide SVB Securities LLC with customary indemnification and contribution rights.

The Company did not have any ATM activity during the three or six months ended June 30, 2023.

In the three months ended June 30, 2022, the Company raised gross proceeds of $10.3 million pursuant to the December 2020 ATM through the sale of 1,300,000 shares of common stock at a weighted average price of $7.90 per share. The net proceeds from the December 2020 ATM were $10.0 million after deducting underwriter commissions of $0.3 million. In the six months ended June 30, 2022, the Company raised gross proceeds of $40.9 million pursuant to the December 2020 ATM through the sale of 4,204,113 shares of common stock at a weighted average price of $9.72 per share. The net proceeds from the December 2020 ATM were $39.6 million after deducting underwriter commissions of $1.2 million.

Equity Offerings

$60 Million Private Placement Equity Financing

On October 10, 2022, Immunic entered into a Securities Purchase Agreement (the “Purchase Agreement”) for a private placement (the “Private Placement”) with select accredited investors and certain existing investors (each, a “Purchaser” and collectively, the “Purchasers”). Pursuant to the Purchase Agreement, the Company agreed to sell to the Purchasers (i) 8,696,552 shares of the Company’s common stock, par value $0.0001 per share (the “Shares”), at a purchase price of $4.35 per Share, and (ii) 5,096,552 pre-funded warrants (the “Pre-Funded Warrants”) to purchase Common Stock (the “Warrant Shares” and together with the Shares and the Pre-Funded Warrants, the “Securities”), at a purchase price of $4.34 per Pre-Funded Warrant. The Pre-Funded Warrants are classified as a component of permanent equity because they are freestanding financial instruments that are legally detachable and separately exercisable from the shares of common stock with which they were issued, are immediately exercisable, do not embody an obligation for the Company to repurchase its shares, and permit the

18

holders to receive a fixed number of shares of common stock upon exercise. In addition, the Pre-Funded Warrants do not provide any guarantee of value or return. All of the pre-funded warrants were exercised in January of 2023.

Common Stock

As of June 30, 2023, the Company’s certificate of incorporation, as amended and restated, authorized the Company to issue 130,000,000 shares of common stock, par value of $0.0001 per share. The voting, dividend and liquidation rights of the holders of the Company’s common stock are subject to and qualified by the rights, powers and preferences of any holders of preferred stock.

Each share of common stock entitles the holder to one vote on all matters submitted to a vote of the Company’s stockholders. Common stockholders are entitled to receive dividends, as may be declared by the board of directors, if any. Through June 30, 2023, no

Preferred Stock

The Company’s certificate of incorporation, as amended and restated, authorizes the Company to issue 20 million shares of $0.0001 par value preferred stock, having rights and preferences to be set by the Board of Directors. No preferred shares were outstanding as of June 30, 2023.

Stock Reserved for Future Issuance

| Number of Shares | |||||

| Common stock reserved for issuance for: | |||||

| 2021 Employee Stock Purchase Plan | |||||

| Outstanding stock options | |||||

| Common stock options available for future grant: | |||||

| 2014 Equity Incentive Plan | |||||

| 2017 Inducement Equity Incentive Plan | |||||

| 2019 Omnibus Equity Incentive Plan | |||||

| Total common shares reserved for future issuance | |||||

7. Stock-Based Compensation Plans

2021 Employee Stock Purchase Plan

On April 25, 2021, the Company adopted the 2021 Employee Stock Purchase Plan ("ESPP"), which was approved by stockholder vote at the 2021 Annual Meeting of Stockholders held on June 10, 2021. The ESPP provides eligible employees of the Company with an opportunity to purchase common stock of the Company through accumulated payroll deductions, which are included in other current liabilities until they are used to purchase Company shares. Eligible employees participating in the bi-annual offering period can choose to have up to the lesser of 15 % of their annual base earnings or the IRS annual share purchase limit of $25,000 in aggregate market value to purchase shares of the Company’s common stock. The purchase price of the stock is the lesser of (i) 85 % of the closing market price on the date of purchase and (ii) the closing market price at the beginning of the bi-annual offering period. The maximum number of shares reserved for delivery under the plan is 200,000 shares.

The first enrollment period under the plan commenced on August 1, 2021 and the Company has issued 167,642 shares life-to-date under the ESPP. The Company recognized $37,000 and $83,000 of expense related to the plan during the three and six months ended June 30, 2023, respectively. The Company recognized $25,000 and $53,000 of expense related to the plan during the three and six months ended June 30, 2022, respectively.

19

Stock Option Programs

In July 2019, the Company’s stockholders approved the 2019 Omnibus Equity Incentive Plan (the “2019 Plan”) which was adopted by the Board of Directors (the "Board") with an effective date of June 14, 2019. The 2019 Plan allows for the grant of equity awards to employees, consultants and non-employee directors. An initial maximum of 1,500,000 shares of the Company’s common stock were available for grant under the 2019 Plan. The 2019 Plan included an evergreen provision that allowed for the annual addition of up to 4 % of the Company’s fully-diluted outstanding stock, with a maximum allowable increase of 4,900,000 shares over the term of the 2019 Plan. In accordance with this provision, the shares available for grant were increased in 2020 through 2023 by a total of 4,408,871 shares. At the Company's Annual Shareholders meeting on June 28, 2023, shareholders voted to increase the allowable shares under the 2019 plan by 4,440,000 shares as well as to eliminate the evergreen provision. The 2019 Plan is currently administered by the Board, or, at the discretion of the Board, by a committee of the Board, which determines the exercise prices, vesting schedules and other restrictions of awards under the 2019 Plan at its discretion. Options to purchase stock may not have an exercise price that is less than the fair market value of underlying shares on the date of grant, and may not have a term greater than ten years . Incentive stock options granted to employees typically vest over four years . Non-statutory options granted to employees, officers, members of the Board, advisors, and consultants of the Company typically vest over or four years .

Shares that are expired, terminated, surrendered or canceled under the 2019 Plan without having been fully exercised will be available for future awards.

Movements during the year

The following table summarizes stock option activity for the six months ended June 30, 2023 and 2022, respectively, for the 2019 Plan:

| Options | Weighted- Average Exercise Price | Weighted- Average Remaining Contractual Term (Years) | Aggregate Intrinsic Value | ||||||||||||||||||||

| Outstanding as of January 1, 2023 | $ | ||||||||||||||||||||||

| Granted | $ | ||||||||||||||||||||||

| Exercised | $ | — | |||||||||||||||||||||

| Forfeited or expired | ( | $ | |||||||||||||||||||||

| Outstanding as of June 30, 2023 | $ | $ | |||||||||||||||||||||

| Options vested and expected to vest as of June 30, 2023 | $ | $ | |||||||||||||||||||||

| Options exercisable as of June 30, 2023 | $ | $ | |||||||||||||||||||||

| Options | Weighted- Average Exercise Price | Weighted- Average Remaining Contractual Term (Years) | Aggregate Intrinsic Value | ||||||||||||||||||||

| Outstanding as of January 1, 2022 | $ | ||||||||||||||||||||||

| Granted | $ | ||||||||||||||||||||||

| Exercised | ( | $ | |||||||||||||||||||||

| Forfeited or expired | ( | $ | |||||||||||||||||||||

| Outstanding as of June 30, 2022 | $ | $ | |||||||||||||||||||||

| Options vested and expected to vest as of June 30, 2022 | $ | $ | |||||||||||||||||||||

| Options exercisable as of June 30, 2022 | $ | $ | |||||||||||||||||||||

20

Measurement

The weighted-average assumptions used in the BSM option pricing model to determine the fair value of the employee and non-employee stock option grants relating to the 2019 Plan were as follows:

Risk-Free Interest Rate

The risk-free rate assumption is based on U.S. Treasury instruments with maturities similar to the expected term of the stock options.

Expected Dividend Yield

The Company has not issued any dividends and does not expect to issue dividends over the life of the options. As a result, the Company has estimated the dividend yield to be zero .

Expected Volatility

Due to the Company’s limited operating history and a lack of company specific historical and implied volatility data, the Company estimates expected volatility based on the historical volatility of its own stock combined with a group of comparable companies that are publicly traded. The historical volatility data was computed using the daily closing prices for the selected companies’ shares during the equivalent period of the calculated expected term of the stock-based awards.

Expected Term

The expected term of options is estimated considering the vesting period at the grant date, the life of the option and the average length of time similar grants have remained outstanding in the past.

The weighted-average grant date fair value of stock options granted under the 2019 Plan during the six months ended June 30, 2023 and 2022 was $1.17 and $7.25 , respectively. The following are the underlying assumptions used in the Black-Scholes option pricing model to determine the fair value of stock options granted to employees and to non-employees under this stock plan:

| Six Months Ended June 30, | ||||||||

| 2023 | 2022 | |||||||

| Risk-free interest rate | ||||||||

| Expected dividend yield | ||||||||

| Expected volatility | ||||||||

| Expected term of options (years) | ||||||||

Stock-Based Compensation Expense

Total stock-based compensation expense for all stock awards recognized in the accompanying unaudited condensed consolidated statements of operations is as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

| Research and development | $ | $ | $ | $ | ||||||||||||||||||||||

| General and administrative | ||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

As of June 30, 2023, there was $13.9 million in total unrecognized compensation expense relating to the 2019 Plan to be recognized over a weighted average period of 2.88 years.

Summary of Equity Incentive Plans Assumed from Vital Therapies

Upon completion of the Transaction with Vital Therapies, Inc. ("Vital") on April 12, 2019, Vital’s 2012 Stock Option

21

Plan (the “2012 Plan”), Vital’s 2014 Equity Incentive Plan (the “2014 Plan”) and Vital’s 2017 Inducement Equity Incentive Plan (the “Inducement Plan”), were assumed by the Company. All awards granted under these plans have either been forfeited or expired.

There remain 43,311 shares available for grant under the 2014 Plan as of June 30, 2023.

In September 2017, Vital’s board of directors approved the Inducement Plan, which was amended and restated in November 2017. Under the Inducement Plan 46,250 shares of Vital’s common stock were reserved to be used exclusively for non-qualified grants to individuals who were not previously employees or directors as an inducement material to a grantee's entry into employment within the meaning of Rule 5635(c)(4) of the Nasdaq Listing Rules.

8. Related Party Transactions

Executive Chairman Agreement with Duane Nash

On April 15, 2020, the compensation committee of the Board of Directors of the Company independently reviewed and approved entering into an employment agreement with the Executive Chairman of the Board, Duane Nash, MD, JD, MBA (the “Executive Chairman Agreement”) and pursuant to such approval, on April 17, 2020, the Company and Dr. Nash entered into the Executive Chairman Agreement. The Executive Chairman Agreement establishes an “at will” employment relationship. On December 28, 2022, the Company and Dr. Nash entered into Addendum No. Four, which extended the term of employment from December 31, 2022 to December 31, 2023 with a base salary of $30,250 per month (which includes the cash retainer payable for serving on the Company’s Board or for acting as the Chairman of the Board). All other terms of the Executive Chairman Agreement remain the same.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of financial condition and results of operations should be read in conjunction with our unaudited interim condensed consolidated financial statements and notes thereto included in Item 1 “Financial Statements” in this Quarterly Report and audited Consolidated Financial Statements for the years ended December 31, 2022 and 2021 of Immunic, Inc. filed with the Securities and Exchange Commission ("SEC"), in our Annual Report on Form 10-K on February 23, 2023. As used in this report, unless the context suggests otherwise, “we,” “us,” “our,” “the Company” or “Immunic” refer to Immunic, Inc. and its subsidiaries.

Forward-Looking Statements

In addition to historical information, this Quarterly Report includes forward-looking statements within the meaning of federal securities laws. Forward-looking statements are subject to certain risks and uncertainties, many of which are beyond our control. Such statements include, but are not limited to, statements preceded by, followed by or that otherwise include the words, “believe,” “may,” “might,” “can,” “could,” “will,” “would,” “should,” “estimate,” “continue,” “anticipate,” “intend,” “seek,” “plan,” “project,” “expect,” “potential,” “predicts,” or similar expressions and the negatives of those terms.

Forward-looking statements discuss matters that are not historical facts. Our forward-looking statements involve assumptions that, if they ever materialize or prove correct, could cause our results to differ materially from those expressed or implied by such forward-looking statements. In this Quarterly Report, for example, we make forward-looking statements, among others, regarding potential strategic options; financial estimates and projections; and the sufficiency of our capital resources to fund our operations.

The inclusion of any forward-looking statements in this Quarterly Report should not be regarded as a representation that any of our plans will be achieved. Our actual results may differ from those anticipated in our forward-looking statements as a result of various factors, including those noted below under the caption “Part II, Item 1A-Risk Factors” and in the section headed “Risk Factors” in our Annual Report on Form 10-K filed with the SEC on February 23, 2023, and the differences may be material. These risk factors include, but are not limited to statements relating to our three development programs and the targeted diseases; the potential for vidofludimus calcium, IMU-856 and IMU-381 to safely and effectively target diseases;

22

preclinical and clinical data for the Company’s development programs; the timing of current and future clinical trials and anticipated clinical milestones; the nature, strategy and focus of the Company; expectations regarding our capitalization and financial resources; the development and commercial potential of any product candidates of the Company; the Company’s expected cash runway; and our ability to retain certain personnel important to our ongoing operations and to maintain effective internal control over financial reporting.

Although our forward-looking statements reflect the good faith judgment of our management, these statements are based only on facts and factors currently known by us. As a result, investors are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. All forward-looking statements are qualified in their entirety by this cautionary statement, and we undertake no obligation to revise or update such statements to reflect events or circumstances after the date hereof, except as required by law.

Overview

Immunic, Inc. ("Immunic," “we,” “us,” “our” or the "Company") is a biotechnology company developing a clinical pipeline of selective oral immunology therapies focused on treating chronic inflammatory and autoimmune diseases. We are headquartered in New York City with our main operations in Gräfelfing near Munich, Germany. We currently have approximately 75 employees.

We are pursuing clinical development of orally administered, small molecule programs, each of which has unique features intended to directly address the unmet needs of patients with serious chronic inflammatory and autoimmune diseases. These include the vidofludimus calcium (IMU-838) program, which is in Phase 3 clinical development for patients with multiple sclerosis (“MS”) and which has shown therapeutic activity in Phase 2 clinical trials in patients suffering from relapsing-remitting MS and moderate-to-severe ulcerative colitis (“UC”); the IMU-856 program, which is targeted to regenerate bowel epithelium and restore intestinal barrier function, which could potentially be applicable in numerous gastrointestinal diseases, such as celiac disease, UC, Crohn’s disease or irritable bowel syndrome with diarrhea; and the IMU-381 program, which is a next generation molecule being developed to specifically address the needs of gastrointestinal diseases.

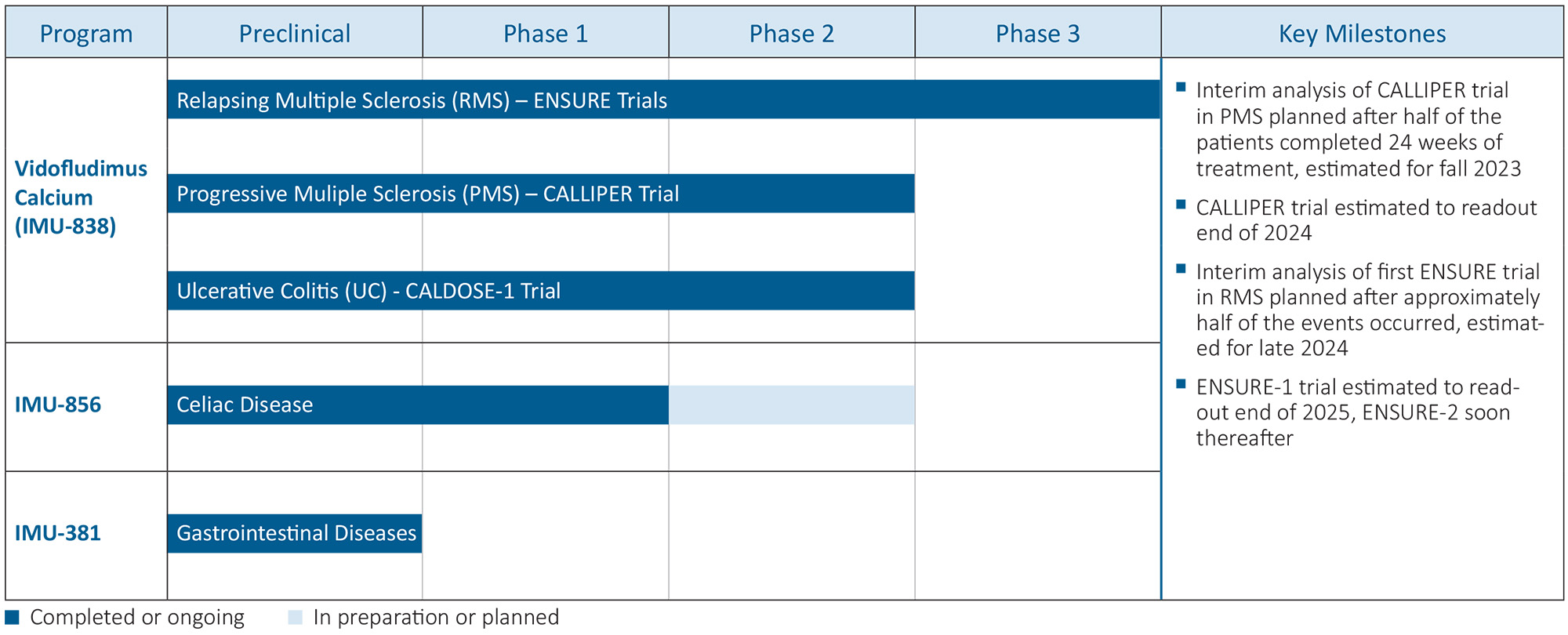

The following table summarizes the potential indications, clinical targets and clinical development status of our three product candidates:

Our most advanced drug candidate, vidofludimus calcium (IMU-838), is being tested in several ongoing MS trials as part of its overall clinical program in order to support a potential approval for patients with MS in major markets. The Phase 3 ENSURE program of vidofludimus calcium in relapsing multiple sclerosis (“RMS”), comprising twin studies evaluating efficacy, safety, and tolerability of vidofludimus calcium versus placebo, and the supportive Phase 2 CALLIPER trial of vidofludimus calcium in progressive multiple sclerosis (“PMS”) are ongoing and actively enrolling patients. Our current expectation is to report data from the interim analysis of the CALLIPER trial in fall of 2023 and to read-out top-line data at the end of 2024. Moreover, we currently expect to report data from the interim analysis of the ENSURE program in late 2024 and to read-out the first of the ENSURE trials at the end of 2025. Although we currently believe that each of these goals is achievable, they are each dependent on numerous factors, most of which are not under our direct control and can be difficult to predict. We plan to periodically review this assessment and provide updates of material changes as appropriate.

23

If approved, we believe that vidofludimus calcium, with combined anti-inflammatory, anti-viral, and neuroprotective effects, has the potential to be a unique treatment option targeted to the complex pathophysiology of MS. Recently published preclinical data showed that vidofludimus calcium activates the neuroprotective transcription factor nuclear receptor related 1 (“Nurr1”), which is associated with direct neuroprotective properties and may enhance the potential benefit for patients. Additionally, vidofludimus calcium is a known inhibitor of the enzyme dihydroorotate dehydrogenase (“DHODH”), which is a key enzyme in the metabolism of overactive immune cells and virus-infected cells. This mechanism is associated with the anti-inflammatory and anti-viral effects of vidofludimus calcium. We believe that the combined mechanisms of vidofludimus calcium are unique in the MS space and support the therapeutic performance shown in our Phase 2 EMPhASIS trial in relapsing-remitting MS patients, in particular, via data illustrating the potential to reduce magnetic resonance imaging lesions, prevent relapses, reduce the rate of disability progression, and reduce levels of serum neurofilament light chain (“NfL”), an important biomarker of neuronal death. Vidofludimus calcium has shown a consistent pharmacokinetic, safety and tolerability profile and has already been exposed to more than 1,400 human subjects and patients in either of the drug’s formulations.

IMU-856 is an orally available and systemically acting small molecule modulator that targets Sirtuin 6 (“SIRT6”), a protein which serves as a transcriptional regulator of intestinal barrier function and regeneration of bowel epithelium. Based on preclinical data, we believe this compound may represent a unique treatment approach, as the mechanism of action targets the restoration of the intestinal barrier function and bowel wall architecture in patients suffering from gastrointestinal diseases such as celiac disease, inflammatory bowel disease, irritable bowel syndrome with diarrhea and other intestinal barrier function associated diseases. We believe that, because IMU-856 has been shown in preclinical investigations to avoid suppression of immune cells, it may therefore have the potential to maintain immune surveillance for patients during therapy, which would be an important advantage versus immunosuppressive medications and may allow the potential for combination treatments with available treatments in gastroenterological diseases..

Data from the final portion of a Phase 1 clinical trial in celiac disease patients during periods of gluten-free diet and gluten challenge demonstrated positive effects for IMU-856 over placebo in four key dimensions of celiac disease pathophysiology: protection of the gut architecture, improvement of patients’ symptoms, biomarker response, and enhancement of nutrient absorption. IMU-856 was also observed to be safe and well-tolerated in this trial. We are currently preparing clinical Phase 2 testing of IMU-856 in ongoing active celiac disease, while also considering further potential clinical applications in other gastrointestinal disorders.

Immunic has selected IMU-381 as a development candidate to specifically address the needs of gastrointestinal diseases. IMU-381 is a next generation molecule with improved overall properties, supported by a series of chemical derivatives. IMU-381 is currently in preclinical testing.

Additional antiviral-directed development activities remain ongoing through preclinical research examining the potential to treat a broad set of viral indications with new antiviral molecules. We are exploring several options to possibly support further development of our antiviral portfolio, including a potential spin-off into a new or existing company and potential licensing transactions.

We expect to continue to lead most of our research and development activities from our Gräfelfing, Germany location, where dedicated scientific, regulatory, clinical and medical teams conduct their activities. Due to these teams' key relationships with local and international service providers, we anticipate that this will result in more timely and cost-effective execution of our development programs. In addition, we are using our subsidiary in Melbourne, Australia to expedite the early clinical trials for IMU-856. We also conduct preclinical work in Halle/Saale, Germany through a collaboration with the Fraunhofer Institute.

Our business, operating results, financial condition and growth prospects are subject to significant risks and uncertainties, including the failure of our clinical trials to meet their endpoints, failure to obtain regulatory approval and failure to obtain needed additional funding on acceptable terms, if at all, to complete the development and commercialization of our three development programs.

Strategy

We are focused on the development of new molecules that maximize the therapeutic benefits for patients by uniquely addressing biologically relevant immunological targets. We take advantage of our established research and development infrastructure and operations in Germany and Australia to more efficiently develop our product candidates in indications of high unmet need and where the product candidates have the potential to elevate the standard of care for the benefit of patients. Given the mechanisms of action and the data generated for our product candidates, to date, we continue to execute on the clinical development of our programs for established indications as well as explore additional indications where patients could potentially benefit from the unique profiles of each product candidate.

24

We are currently focused on maximizing the potential of our development programs through the following strategic initiatives:

•Executing the ongoing Phase 3 ENSURE and Phase 2 CALLIPER clinical trial programs of vidofludimus calcium in MS.

•Exploring potential next steps for vidofludimus calcium in UC and other inflammatory bowel disease indications.

•Executing the IMU-856 development program, including preparation of a Phase 2 clinical trial in patients with ongoing active celiac disease.

•Continued preclinical research to complement the existing clinical activities, explore additional indications for future development, and where appropriate, generate additional molecules for future development.

•Facilitating readiness for potential commercial launch of our product candidates through targeted and stage-appropriate pre-commercial activities.

•Evaluating potential strategic collaborations for each product candidate in order to complement our existing research and development capabilities and to facilitate potential commercialization of these product candidates by taking advantage of the resources and capabilities of strategic collaborators in order to enhance the potential and value of each product candidate.

Recent Events

Vidofludimus Calcium Acts as Potent Nurr1 Activator, Reinforcing Neuroprotective Potential in MS

On May 17, 2023, we announced the publication of preclinical data showing that vidofludimus calcium acts as a potent Nurr1 activator, in addition to its known mode of action as a DHODH inhibitor. Activation of Nurr1 could be responsible for the drug’s postulated neuroprotective effects and may contribute to the previously reported reduction of confirmed disability worsening events in MS patients. Specifically, preclinical data shows potent Nurr1 activation by vidofludimus calcium at low concentrations in several test systems. The data was published in the peer-reviewed, high impact Journal of Medicinal Chemistry, in a paper entitled, “Development of a potent Nurr1 agonist tool for in vivo applications.”

Presentation of Clinical and Preclinical Data for IMU-856 at Digestive Disease Week 2023, Including Its Molecular Mode of Action

On May 6, 2023, we announced the presentation of clinical and preclinical data for IMU-856 as a virtual e-poster at Digestive Disease Week 2023. Included in this presentation were new data on IMU-856’s mode of action as a potent modulator of SIRT6, a protein which serves as a transcriptional regulator of intestinal barrier function and regeneration of bowel epithelium.

Positive Results From Phase 1b Clinical Trial of IMU-856 in Celiac Disease

On May 4, 2023, we announced positive results from the part C portion of our Phase 1 clinical trial of IMU-856 in patients with celiac disease. The data demonstrated positive effects for IMU-856 over placebo in four key dimensions of celiac disease pathophysiology: protection of the gut architecture, improvement of patients’ symptoms, biomarker response, and enhancement of nutrient absorption. IMU-856 was also observed to be safe and well-tolerated in this trial.

We believe that this data set provides initial clinical proof-of-concept for an entirely new therapeutic approach to gastrointestinal disorders by promoting regeneration of bowel architecture. The data provides first clinical evidence that IMU-856’s ability, observed in preclinical studies, to re-establish proper gut cell renewal translates into clinical benefits for patients with celiac disease. Most importantly, the observed protection of intestinal villi from gluten-induced destruction, independent of targeting immune mechanisms involved specifically in celiac disease, appears to be unique among proposed therapeutic approaches and may be applicable to other gastrointestinal diseases such as UC, Crohn’s disease or irritable bowel syndrome with diarrhea.

25

Appointment of Richard Rudick, M.D. to Board of Directors

On April 27, 2023, we announced the appointment of Dr. Richard Rudick as a member of our Board of Directors, effective as of April 26, 2023. As a Class III director, Dr. Rudick’s initial term lasted until our 2023 Annual Meeting of Stockholders held on June 28, 2023, at which meeting he was elected to a three year term expiring at the 2026 Annual Meeting of Stockholders.

Dr. Richard Rudick, age 72, has over 35 years of experience in the biopharmaceutical industry and academic medicine. Since January 2023, Dr. Rudick has been the President and CEO of Astoria Biologic, a private biotechnology company developing novel therapies for MS. Previously, Dr. Rudick served as the Vice President of Development Science at Biogen, Inc., a biotechnology company which engages in discovering, developing, and delivering therapies for neurological and neurodegenerative diseases, from May 2014 until September 2020. Dr. Rudick also served as a staff neurologist and director of the Mellen Center for the Cleveland Clinic from January 1987 until May 2014. Dr. Rudick holds an M.D. from Case Western Reserve University School of Medicine. The Nominating and Corporate Governance Committee and the Board believe that Dr. Rudick‘s extensive leadership in clinical research and development of MS treatments provides valuable clinical, strategy and management skills to the Board.

Director Not Standing for Re-Election at the 2023 Annual Meeting

Additionally, on April 26, 2023, Dr. Vincent Ossipow notified our Board that he plans to retire from the Board at the end of his current term and will not stand for re-election at the 2023 Annual Meeting. Dr. Ossipow continued to serve as a member of the Board until the date of the Annual Meeting, and as a member of the Nominating and Corporate Governance Committee until the date of the Annual Meeting, June 28, 2023. Dr. Ossipow’s decision not to stand for re-election was not the result of any disagreement with the Company or its management on any matter relating to the Company’s operations, policies or practices.

Positive Data from Maintenance Phase of Phase 2 CALDOSE-1 Trial of Vidofludimus Calcium in Moderate-to-Severe UC

On April 5, 2023, we reported positive data from the maintenance phase of our Phase 2b CALDOSE-1 trial of vidofludimus calcium in patients with moderate-to-severe UC. The data showed a dose-linear increase in clinical remission as compared to placebo at week 50. Moreover, an exploratory statistical analysis confirmed the 30 mg dose of vidofludimus calcium to be statistically superior (p=0.0358) in achieving clinical remission at week 50, with a 33.7% absolute improvement over placebo. A similar effect on clinical remission rates at week 50 was also found among those patients who received corticosteroids during the induction phase. Finally, a dose-linear increase in endoscopic healing was observed, with the 30 mg dose of vidofludimus calcium being associated with a 37.8% absolute improvement over placebo and also achieving statistical significance in an exploratory statistical analysis (p=0.0259).

We believe that the maintenance phase data of CALDOSE-1 confirms vidofludimus calcium's activity in the absence of chronic corticosteroid co-administration. Consistent with prior data sets in other patient populations, administration of vidofludimus calcium in the maintenance phase of this trial was observed to be safe and well-tolerated.

Deprioritization of Izumerogant (IMU-935) Development Program