UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2021

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 001-36201

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

(332 ) 255-9818

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

| ☒ | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the common equity held by non-affiliates of the Registrant, based on the closing price of the common stock on The Nasdaq Stock Market on June 30, 2021 was $225.0 million.

On February 18, 2022, 27,906,942 shares of common stock, $0.0001 par value, were outstanding.

Documents Incorporated by Reference: Certain portions of the registrant’s definitive Proxy Statement for its 2022 Annual Meeting of Stockholders are incorporated by reference into Items 10, 11, 12, 13 and 14 of Part III of this Annual Report on Form 10-K.

Immunic, Inc.

ANNUAL REPORT ON FORM 10-K

For the Fiscal Year Ended December 31, 2021

Table of Contents

| Page | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Item 15. | ||||||||

Special Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K (“Annual Report”) contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements are based on our management’s current beliefs and assumptions and on information currently available to our management, and are contained principally in the sections entitled “Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements include all statements that are not historical facts and can be identified by terms such as “anticipates,” “believes,” “best in class,” “could,” “seeks,” “estimates,” “expects,” “first-in-class,” “focused,” “goal,” “intends,” “may,” “objective,” “opportunity,” “pipeline,” “plans,” “potential,” “predicts,” “projects,” “pursuing,” “should,” “target,” “treatment option,” “will,” “would,” “might,” “can,” “continue” or similar expressions and the negatives of those terms.

These forward-looking statements include, among other things, statements about:

•the strategies, prospects, plans, expectations and objectives of management;

•our ability to maintain compliance with Nasdaq listing standards;

•strategies with respect to our development programs, including our ability to develop and commercialize our product candidates and the timing and expected data of clinical trials and preclinical studies;

•our estimates regarding revenues, expenses, capital requirements, projected cash requirements and needs for additional financing

•possible sources of funding for future operations;

•our ability to protect intellectual property rights and our intellectual property position;

•future economic conditions or performance;

•proposed products or product candidates;

•our ability to retain key personnel;

•our ability to maintain effective internal control over financial reporting; and

•beliefs and assumptions underlying any of the foregoing.

Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements including those described in “Risk Factors” and elsewhere in this Annual Report. Given these uncertainties, you should not place undue reliance on these forward-looking statements. Also, forward-looking statements represent our management’s beliefs and assumptions only as of the date of this Annual Report, unless an earlier date is specified. You should read this Annual Report and the documents that we reference in this Annual Report and have filed with the Securities and Exchange Commission ("SEC") as exhibits hereto completely and with the understanding that our actual future results may be materially different from what we expect.

Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future.

1

PART I

Item 1. Business.

Overview

Immunic, Inc. ("Immunic," “we,” “us,” “our” or the "Company") is a clinical-stage biopharmaceutical company with a pipeline of selective oral immunology therapies focused on treating chronic inflammatory and autoimmune diseases, including relapsing multiple sclerosis (“RMS”), ulcerative colitis (“UC”), Crohn’s disease (“CD”) and psoriasis. We are headquartered in New York City with our main operations in Gräfelfing near Munich, Germany. We currently have approximately 55 employees.

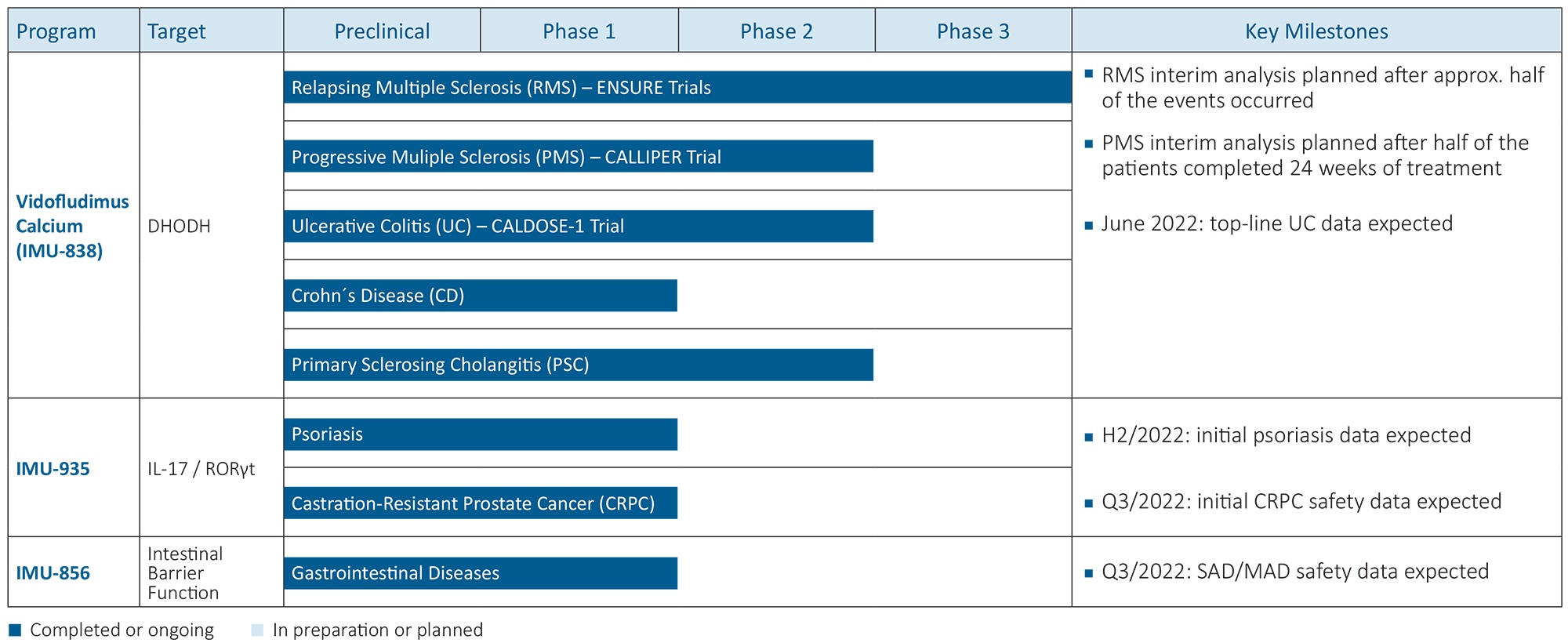

We are currently pursuing three development programs. These include the vidofludimus calcium (IMU-838) program, which is focused on the development of oral formulations of a small molecule inhibitor of the enzyme dihydroorotate dehydrogenase (“DHODH”); the IMU-935 program, which is focused on an inverse agonist of retinoic acid receptor-related orphan nuclear receptor gamma truncated (“RORγt”), an immune cell-specific isoform of RORγ; and the IMU-856 program, which involves the development of a drug targeting the restoration of intestinal barrier function and regeneration of bowel epithelium. These product candidates are being developed to address diseases such as RMS, UC, CD, and psoriasis. In addition to these large markets, these products are also being developed to address certain rare diseases with high unmet medical needs, such as primary sclerosing cholangitis (“PSC”), as well as metastatic castration-resistant prostate cancer (“mCRPC”).

The following table summarizes the potential indications, clinical targets and clinical development status of our three product candidates:

Our most advanced drug candidate, vidofludimus calcium (IMU-838), targets DHODH, a key enzyme in the intracellular metabolism of immune cells in the body. In the third quarter of 2020, we reported positive results from our Phase 2 EMPhASIS trial of vidofludimus calcium in relapsing-remitting multiple sclerosis (“RRMS”), achieving both primary and key secondary endpoints with high statistical significance. The first patient in our Phase 3 ENSURE program of vidofludimus calcium in RMS, comprising twin studies evaluating efficacy, safety, and tolerability of vidofludimus calcium versus placebo, was enrolled in November 2021. The first patient in our supportive Phase 2 CALLIPER trial of vidofludimus calcium in progressive multiple sclerosis (“PMS”) was enrolled in September 2021. In the first quarter of 2021, we announced that vidofludimus calcium showed evidence of clinical activity in our Phase 2 CALVID-1 trial in hospitalized patients with moderate coronavirus disease 2019 ("COVID-19"). Also, in the first quarter of 2021, we reported positive top-line data from an investigator-sponsored Phase 2 proof-of-concept clinical trial of vidofludimus calcium in primary sclerosing cholangitis which was conducted in collaboration with the Mayo Clinic. In addition, vidofludimus calcium is currently being tested in a Phase 2 trial in patients with ulcerative colitis (CALDOSE-1 trial), for which we expect top-line data to be available in June of 2022. Additional antiviral directed development activity remains ongoing through an investigator-sponsored Phase 2 clinical trial of vidofludimus calcium as well as preclinical development examining the potential to treat a broad set of viral indications with vidofludimus calcium and other DHODH inhibitors in combination with nucleoside analogues.

2

If approved, we believe that vidofludimus calcium has the potential to be a highly selective first-in-class DHODH inhibitor in inflammatory bowel disease (“IBD”) and best-in-class DHODH inhibitor in RMS. Importantly, vidofludimus calcium has an attractive pharmacokinetic, safety and tolerability profile and has already been exposed to approximately 1,100 human subjects and patients in either of the drug’s formulations.

Our second drug candidate, IMU-935, is a highly potent and selective inverse agonist of a transcription factor called RORγt. We believe that the nuclear receptor RORγt is the main driver for the differentiation of T-helper 17 (“Th17”) cells and the release of cytokines involved in various inflammatory and autoimmune diseases. We believe this target is an attractive alternative to approved antibodies for targets, such as interleukin-23 (“IL-23”), the IL-17 receptor and IL-17 itself. We have observed strong cytokine inhibition targeting both Th1 and Th17 responses in preclinical testing, as well as indications of activity in animal models for psoriasis, graft versus host disease, MS and IBD. Preclinical experiments indicated that, while leading to a potent inhibition of Th17 differentiation and cytokine secretion, IMU-935 did not affect thymocyte maturation, one of the important physiological functions that should be maintained. Based on these preclinical data and the selectivity of the effect maintaining important physiological functions while providing the desired anti-Th17 effect, we believe that IMU-935 has potential to be a best-in-class therapy for various autoimmune diseases. A Phase 1 clinical trial exploring safety, pharmacodynamics and pharmacokinetics of IMU-935 in healthy human subjects and psoriasis patients is currently ongoing. Additionally, IMU-935 has been shown in preclinical models to target an established mechanism of treatment resistance to androgen receptor therapy, making it a potential treatment option for patients with resistant CRPC. A Phase 1 clinical trial exploring safety and tolerability of increasing doses of IMU-935 to establish the maximum tolerated dose and the recommended phase 2 dose is currently ongoing in patients with mCRPC.

Our third program, IMU-856, which we believe to be novel, is an orally available small molecule modulator that targets a protein which serves as a transcriptional regulator of intestinal barrier function and regeneration of bowel epithelium. We have not yet disclosed the molecular target for IMU-856. Based on preclinical data, we believe this compound may represent a new treatment approach, as the mechanism of action targets the restoration of the intestinal barrier function and regeneration of bowel epithelium in patients suffering from gastrointestinal diseases such as IBD, irritable bowel syndrome with diarrhea, celiac disease and other intestinal barrier function associated diseases. We believe that because IMU-856 has been shown in preclinical investigations to avoid suppression of immune cells, it may therefore have the potential to maintain immune surveillance for patients during therapy, an important advantage versus chronic treatment with potentially immunosuppressive medications. A Phase 1 clinical trial exploring safety, pharmacodynamics and pharmacokinetics of IMU-856 is currently ongoing.

We expect to continue to lead most of our research and development activities from our Gräfelfing, Germany location, where dedicated scientific, regulatory, clinical and medical teams conduct their activities. Due to these teams' key relationships with local and international service providers, we anticipate that this will result in timely, cost-effective execution of our development programs. In addition, we are using our subsidiary in Melbourne, Australia to expedite the early clinical trials for IMU-935 and IMU-856. We also conduct preclinical work in Halle/Saale, Germany through a collaboration with the Fraunhofer Institute.

Strategy

We are focused on the development of best-in-class molecules that maximize the therapeutic benefits for patients by uniquely addressing biologically relevant immunological targets. We take advantage of our established research and development infrastructure and operations in Germany and Australia to efficiently develop our product candidates in indications of high unmet need and where the product candidates have the potential to elevate the standard of care for the benefit of patients. Given the mechanisms of action and the data generated to date for our product candidates, we continue to execute on the clinical development of our programs for established indications as well as explore additional indications where patients could potentially benefit from the unique profiles of each product candidate.

We are currently focused on maximizing the potential of our development programs through the following strategic initiatives:

•Executing the ongoing ENSURE and CALLIPER clinical trial programs of vidofludimus calcium in MS.

•Delivering the results from the CALDOSE-1 trial of vidofludimus calcium in UC, with the path for future development to be assessed following analysis of the results.

•Executing the ongoing clinical studies of IMU-935 in patients with psoriasis and in patients with mCRPC, with the path for future development to be assessed following analysis of the results.

•Executing the ongoing Phase 1 clinical trials of IMU-856, with potential to expand into the treatment of patients with certain gastrointestinal diseases following sufficient safety and tolerability data.

3

•Continued preclinical research to complement the existing clinical activities, explore additional indications for future development, and where appropriate, generate additional molecules for future development.

•Facilitating readiness for potential commercial launch of our product candidates through targeted and stage-appropriate pre-commercial activities.

•Evaluating potential strategic collaborations for each product candidate in order to complement our existing research and development capabilities and to facilitate potential commercialization of these product candidates by taking advantage of the resources and capabilities of strategic collaborators in order to enhance the potential and value of each product candidate.

Liquidity and Financial Condition

Our business, operating results, financial condition and growth prospects are subject to significant risks and uncertainties, including the failure of our clinical trials to meet their endpoints, failure to obtain regulatory approval and needing additional funding to complete the development and commercialization of our three development programs.

We have no products approved for commercial sale and have not generated any revenue from product sales. We have never been profitable and has incurred operating losses in each year since inception (2016). We have an accumulated deficit of approximately $196.9 million as of December 31, 2021 and approximately $103.9 million as of December 31, 2020. Substantially all of our operating losses resulted from expenses incurred in connection with our research and development programs and from general and administrative costs associated with our operations.

We expect to continue to incur significant expenses and increasing operating losses for the foreseeable future as we continue the preclinical and clinical development of our product candidates and add personnel necessary to advance our pipeline of product candidates. We expect that our operating losses will fluctuate significantly from quarter-to-quarter and year-to-year due to timing of clinical development programs.

From inception through December 31, 2021, we have raised net cash of approximately $259.5 million from private and public offerings of preferred and common stock. As of December 31, 2021, we had cash and cash equivalents of approximately $86.9 million. We are dependent on financing activities to fund ongoing operations, and due to the inherent uncertainties in successfully completing financing transactions, and with our forecasted cash reach through the first quarter of 2023, these are indicators of an inability to continue as a going concern. However, we have the ability to manage the amount and timing of expenditures to reduce costs, have limited required fixed spend, and can manage working capital as needed and that coupled with the $16.2 million of cash raised so far in 2022 under our At The Market ("ATM") facility alleviates any uncertainty that we will have adequate liquidity to meet our obligations for at least the next 12 months from the financial statement release date.

Key Status Updates

Vidofludimus Calcium (IMU-838)

Phase 3 Program of Vidofludimus Calcium in RMS (ENSURE-1 and ENSURE-2 Trials)

On July 1, 2021, we announced U.S. Food and Drug Administration (“FDA”) clearance of our Investigational New Drug (“IND”) application for the Phase 3 ENSURE program of our lead product candidate, vidofludimus calcium in patients with RMS. The ENSURE program comprises two identical multicenter, randomized, double-blind Phase 3 trials designed to evaluate the efficacy, safety, and tolerability of vidofludimus calcium versus placebo in RMS patients. Based on vidofludimus calcium’s highly significant activity in preventing lesion formation in our Phase 2 EMPhASIS trial in RMS, the strong and consistent correlation observed between lesion formation and clinical relapse in third-party clinical trials, and the drug’s robust safety profile to date, we believe that this Phase 3 program should provide a relatively simple and straightforward path towards potential regulatory approval of vidofludimus calcium in RMS.

Each of the identical twin Phase 3 trials, titled ENSURE-1 and ENSURE-2, is expected to enroll approximately 1,050 adult patients with active RMS at more than 100 sites in more than 15 countries, including the United States, India and countries in Latin America, Central and Eastern Europe. Patients will be randomized in a double-blinded fashion to either 30 mg daily doses of vidofludimus calcium or placebo and the primary endpoint for both trials is time to first relapse up to 72 weeks. Key secondary endpoints include volume of new T2-lesions, time to confirmed disability progression, time to sustained clinically relevant changes in cognition, and percentage of whole brain volume change. With regard to the disability progression endpoint, the ENSURE program will apply a pooled analysis of disability worsening across both trials.

4

The ENSURE trials will be run concurrently. The first patient in ENSURE-1 was enrolled in November 2021. The first patient in ENSURE-2 was enrolled in January 2022. An interim analysis to assess event rates is planned to occur after a certain number of relapses have occurred in the double-blind treatment periods. This analysis is intended to inform potential sample size adjustment and help ensure that final study readout is not planned to occur before sufficient events have been achieved. This interim analysis will also allow for a non-binding futility analysis.

Phase 2 Program of Vidofludimus Calcium in PMS (CALLIPER Trial)

On July 1, 2021, we announced that the FDA also cleared our separate IND application for the supportive Phase 2 CALLIPER trial of vidofludimus calcium in patients with PMS. The first patient was enrolled in September 2021.

The multicenter, randomized, double-blind, placebo-controlled Phase 2 CALLIPER trial in PMS is intended to run concurrently with and to complement the Phase 3 program in RMS. In particular, CALLIPER is focused on progressive forms of multiple sclerosis (“MS”) and is designed to corroborate vidofludimus calcium’s neuroprotective potential, as exemplified by slowing of brain atrophy and delay in disability worsening. Neurodegeneration is a key concern in both PMS and RMS, since axonal and neural damage is responsible for the increasing and often severe disability experienced by patients. We believe that, if the CALLIPER trial is successful in showing a beneficial effect of vidofludimus calcium, this data, along with the ENSURE program and vidofludimus calcium’s strong safety and tolerability profile, may allow for a meaningful clinical differentiation of vidofludimus calcium from other oral MS medications and a potentially attractive commercial positioning. Although a supportive trial, we do not believe that data from the CALLIPER trial are a pre-condition for filing a New Drug Application (“NDA”) in RMS. Additional clinical studies and the potential regulatory path forward specific to the treatment of PMS will be informed by the results of the CALLIPER trial and will be further assessed accordingly.

The Phase 2 CALLIPER trial is expected to enroll approximately 450 patients with PMS at more than 70 sites in North America, Western, Central and Eastern Europe with patients randomized to either 45 mg daily doses of vidofludimus calcium or placebo in a double-blinded fashion. The trial’s primary endpoint is the annualized rate of percent brain volume change up to 120 weeks. Key secondary endpoints include the annualized rate of change in whole brain atrophy and time to 24-week confirmed disability progression based on the expanded disability status scale which may further support disability data from the ENSURE trials.

An interim analysis comprising an unblinded analysis of serum neurofilament light chain (“NfL”) is planned to occur once approximately half of the enrolled patients have completed 24 weeks of treatment. NfL has been shown in third-party research to consistently correlate with disease activity in neurodegenerative disorders and has become one of the most important serum biomarkers for axonal damage over the past few years. As previously reported, results of the Phase 2 EMPhASIS trial of vidofludimus calcium in RRMS showed a robust decrease in serum NfL at 24 weeks (-17.0% for 30 mg and -20.5% for 45 mg), as compared to baseline values, while the patients on placebo experienced a 6.5% increase in serum NfL over the same period.

Phase 2 Trial of Vidofludimus Calcium in UC (CALDOSE-1 Trial)

On October 28, 2021, we announced completion of enrollment of our Phase 2 CALDOSE-1 trial of vidofludimus calcium in UC. At completion of patient recruitment, the trial has randomized a total of 263 patients into four arms: three active dosing arms of 10 mg, 30 mg and 45 mg, as well as placebo. Top-line data for the induction phase are expected to be available in June of 2022.

On February 18, 2022, we announced the main blinded baseline characteristics of the CALDOSE-1 trial, including:

•263 moderate-to-severe UC patients were enrolled in 78 study sites with the Ukraine and Poland representing the countries with highest number of patients and U.S. sites contributing 12.5% of the overall enrollment.

•Of the 263 patients, 148 (56.3%) were male and 115 (43.7%) were female patients. The mean age at baseline was 41.7 (18-77) years.

•All patients had to have failed at least one prior therapy option. Of the 263 patients, 83% were biologically naïve and 17% were biologically experienced (received at least 1 prior treatment with any biological agent approved in the UC indication).

•Enrolled patients had to show evidence of active moderate-to-severe UC disease. This is reflected in their baseline characteristics for patient-reported outcomes:

◦The baseline Mayo stool frequency scores were: (i) score of 3 for 59% of patients, (ii) score of 2 for 36% patients and (iii) score of 1 for 5% of patients.

5

◦The Mayo rectal bleeding scores were: (i) score of 3 in 10% of patients, (ii) score of 2 for 54% of patients and (iii) score of 1 for 31% of patients.

◦The average value for fecal calprotectin at baseline was approximately 1,320 μg/g for currently available, yet incomplete data.

•The trial employed a central independent reader to evaluate the endoscopic eligibility criteria and the following modified Mayo endoscopic scores were assessed at baseline:

◦55% of patients with a score of 3; and

◦45% of patients with a score of 2.

•At week 10 (the time point of the primary efficacy analysis), an adjudication procedure was used for endoscopy assessments. In the case of disagreement between two independent readers, a third independent reader was used for adjudication.

We believe that these blinded baseline characteristics of randomized patients and the methodology regarding endoscopic assessments contributes to ensuring an optimized study read-out.

Phase 2 Trial of Vidofludimus Calcium in PSC

On February 18, 2021, we announced positive top-line data from our investigator-sponsored proof-of-concept clinical trial of vidofludimus calcium in PSC, which was conducted at Mayo Clinic in Arizona and Minnesota, both of which are tertiary referral centers for PSC patients. As the next step in this indication, we are currently conducting a Phase 1 trial in hepatic impaired patients in order to explore dose optimization of vidofludimus calcium for potential future clinical activities in PSC. This Phase 1 trial started in September 2021 and is expected to run approximately six months.

IMU-935

Phase 1 Clinical Trial of IMU-935 in Healthy Human Subjects and Moderate to Severe Psoriasis Patients

On July 12, 2021, we provided an update on our IMU-935 program, including new preclinical and clinical data. The main result from preclinical investigations was that IMU-935 inhibits cytokine production (thought to be a pre-condition for its use in immunological and autoimmune diseases) while maintaining the known and required physiological functions of maturing T lymphocytes. In ex vivo mouse cell differentiation and maturation assays, IMU-935 was recently observed to selectively inhibit RORγt-dependent gene expression during Th17 differentiation without affecting either RORγt-dependent gene regulation relevant to thymocyte development, or the viability of these cells. In third-party research, impairment of thymocyte development has been shown to be associated with serious safety issues, including, among others, T cell malfunction and potential lymphoma formation. We believe that IMU-935's observed selectivity may enable it to inhibit both the generation of Th17 cells and the production of IL-17 cytokines that are responsible for the development of autoimmune diseases, without impairing thymocyte development, which is associated with the potential risk of lymphoma seen with other, third-party RORγt programs.

On December 14, 2021, we provided an update on the preclinical and clinical development of IMU-935, announcing that:

•Unblinded data from the single ascending dose part of the ongoing phase 1 clinical trial of a new powder-in-capsule formulation of IMU-935, in which healthy human subjects were treated with 100 mg, 200 mg, 300 mg and 400 mg of this new formulation or placebo, found these single ascending daily doses of IMU-935 to be safe and well-tolerated, and no maximum tolerated dose was reached. No serious adverse events occurred. A dose-proportional pharmacokinetic profile was observed across the investigated dose range.

•Unblinded data from the multiple ascending dose part of the ongoing phase 1 clinical trial, in which healthy human subjects were dosed for 14 days with 150 mg either once or twice daily doses of IMU-935 or placebo, found these multiple ascending doses of IMU-935 to be safe and well-tolerated, and no maximum tolerated dose was reached. Treatment emergent adverse events were generally mild in severity, with moderate treatment emergent adverse events reported in one of eleven IMU-935 treated subjects, compared with one of four subjects on placebo. No serious adverse events were reported. No dose-dependent changes in laboratory values (including no effects on liver enzymes or in hematological parameters), vital signs or in electrocardiographic evaluations were found. Pharmacokinetic analysis showed that stable steady-state plasma concentrations were achieved within the first week of dosing with an accumulation factor for IMU-935 allowing predictable trough levels during daily dosing.

6

•Based on the favorable safety and tolerability data observed in healthy human subjects, our phase 1 clinical trial of IMU-935 was expanded in October 2021 to include a third portion, part C, in which moderate to severe psoriasis patients are to be randomized to 28-day treatment of IMU-935 or placebo. Planned assessments include safety, tolerability, pharmacokinetic and pharmacodynamic markers, as well as skin evaluations. Recruitment of part C depends on several external factors which are not under our direct control, including, in particular, the relatively restrictive COVID-19-related rules in effect in Australia and New Zealand. This situation has and may further influence our ability to enroll study participants and/or perform on-site monitoring at clinical sites in those locations. In light of this, we have already initiated remedial measures, including the potential addition of sites outside of Australia and New Zealand, for the ongoing part C of IMU-935 in psoriasis patients. As a result, initial results from the third portion of the Phase 1 clinical trial in patients with moderate-to-severe psoriasis are now expected to be available in the second half of 2022, instead of at the end of the second quarter of 2022, as previously announced.

•In previous preclinical in vitro data, it was shown that IMU-935 selectively inhibits Th17 differentiation and IL-17 production, whereas RORγt was unaffected by IMU-935 during thymocyte maturation and, therefore, does not harm normal thymocyte maturation. Newly obtained data from acute and chronic treatment of mice corroborated in vivo that IMU-935 is the first molecule observed to impact neither thymus size, thymocyte numbers, nor the maturation status of thymocytes, in contrast to two other known inhibitors of RORγt.

Phase 1 Clinical Trial of IMU-935 in mCRPC

On July 12, 2021, we also presented new preclinical data highlighting IMU-935's therapeutic potential in CRPC. Recently published third-party studies have shown that RORγ plays an important pro-tumor role by driving expression of the androgen receptor (“AR”), leading to tumor growth. During tumor progression, AR tends to mutate into AR-V7, leading to resistance of AR-axis-targeted therapies. In preclinical studies, IMU-935 was observed to inhibit the expression of mutated AR-V7, and the tumor growth of prostate cancer cell lines in vitro. Finally, we believe IMU-935's potency in inhibiting tumorigenesis-promoting IL-17 and Th17 cells in vitro may result in further antitumoral activity in humans.

Based on these strong preclinical results, we have initiated an open-label Phase 1 dose-escalation trial designed to evaluate the safety and tolerability of increasing doses of IMU-935 to establish the maximum tolerated dose and the recommended phase 2 dose. The trial will also evaluate the anti-tumor activity of IMU-935 by means of prostate-specific antigen levels, circulating tumor cell numbers, and radiographic response assessments of tumor progression. The trial’s Principal Investigator is Johann Sebastian de Bono, MD, PhD, Regius Professor of Cancer Research and Professor in Experimental Cancer Medicine, The Institute of Cancer Research, London, and The Royal Marsden NHS Foundation Trust, London, United Kingdom. The trial was approved by the Medicines and Healthcare products Regulatory Agency (MHRA), the Research Ethics Committee (REC) and the Health Research Authority (HRA) in the United Kingdom. The first patient was enrolled in December 2021. Initial clinical safety data are expected to be available in the third quarter of 2022.

IMU-856

Phase 1 Clinical Trial of IMU-856

A Phase 1 clinical trial of IMU-856 is ongoing and progressing in Australia. The trial includes single and multiple ascending dose parts in healthy human subjects designed to assess safety, pharmacodynamics and pharmacokinetics of IMU-856. All planned single ascending dose cohorts for the current tablet formulation of IMU-856 have been completed but have not yet been unblinded. Based on the favorable data available so far, the Ethics Committee in Australia has agreed to proceed to the multiple ascending dose part which is currently being dosed. Unblinded safety data from the single and multiple ascending dose parts in healthy human subjects are expected to be available in the third quarter of 2022.

We also plan to extend this trial to assess biomarkers, disease symptoms, safety and drug trough levels in patients with a model disease of altered intestinal barrier function to provide initial activity data. Initiation of this third portion of the Phase 1 clinical trial is expected in the first half of 2022.

Product Acquisition History

Our wholly-owned subsidiary Immunic AG acquired IMU-838 and IMU-935 in September 2016 through asset acquisitions from 4SC AG (hereinafter, “4SC”), a publicly traded company based in Planegg-Martinsried, Germany. On March

7

31, 2021, Immunic AG and 4SC entered into a Settlement Agreement, pursuant to which Immunic AG settled its remaining obligation of a 4.4% royalty on net sales for $17.25 million. The payment was made 50% in cash and 50% in shares of Immunic’s common stock.

Our rights to IMU-856 are secured pursuant to an option and license agreement (the “Daiichi Sankyo Option”) with Daiichi Sankyo Co., Ltd. (hereinafter, "Daiichi Sankyo") in Tokyo, Japan. On January 5, 2020, Immunic AG exercised its option under the Daiichi Sankyo Option to acquire the exclusive global rights to commercialize IMU-856. The license also grants Immunic AG the rights to Daiichi Sankyo’s patent application related to IMU-856. Concurrent with the option exercise, Immunic AG paid to Daiichi Sankyo a one-time upfront licensing fee. Going forward, Daiichi Sankyo is eligible to receive future development, regulatory and sales milestone payments, as well as royalties related to IMU-856.

Leadership

We are led by a team of dedicated and committed experienced professionals with an entrepreneurial spirit and track record of successful licensing transactions in the healthcare industry worldwide (EU, the United States and Asia). The team brings together several decades of leadership experience in the pharmaceutical industry with a strong scientific background and sound knowledge in drug discovery, product development, chemistry, manufacturing and controls processes, intellectual property, clinical trial design, health economics and market access, merger and acquisitions, capital markets, corporate finance, business development, regulatory affairs and project valuation. Our team members are inventors on project-related patents and have successfully published project-related scientific publications.

Product Candidates

Vidofludimus Calcium (IMU-838)

Vidofludimus calcium is a small molecule investigational drug in development as an oral tablet formulation for the treatment of RMS, IBD and other chronic inflammatory and autoimmune diseases. By inhibiting DHODH, a key enzyme of pyrimidine de novo biosynthesis, highly metabolically activated T and B immune cells experience metabolic stress, which leads to a modulation of their activity and function. Thereby, pro-inflammatory cytokines, such as interferon gamma (“IFNγ”), tumor necrosis factor alpha (“TNFα”), IL-17A and IL-17F, produced by activated Th1 and Th17 cells, which represent subtypes of so-called T helper cells, are repressed and thereby reduce the inflammation associated with IBD, MS and other chronic inflammatory diseases.

In preclinical studies of vidofludimus, the active moiety and free acid form of vidofludimus calcium, apoptosis (or programmed cell death) was induced in activated T cells, which we believee may also play a crucial role in the activity of the drug in IBD by further dampening the inflammatory response. We believe that a key advantage of DHODH inhibition, in general, is that the sensitivity of specific immune cells to DHODH inhibition correlates with their intracellular metabolic activation state, and therefore may not negatively impact “normal” immune and bone marrow cells. In animal studies of vidofludimus calcium, animals treated with large doses of the active moiety of vidofludimus calcium were shown to lack detrimental effects on bone marrow, supporting the lack of an unspecific anti-proliferative effect regularly seen with many traditional immunomodulators.

Based on the selectivity toward metabolically activated cells (with a high need for ribonucleic acid and deoxyribonucleic acid production), DHODH inhibition also leads to a direct antiviral effect, which has been observed in various virus infected cells, such as Epstein-Barr virus (“EBV”) infections, hepatitis C virus infections, severe acute respiratory syndrome coronavirus 2 (“SARS-CoV-2”) infections, cytomegalovirus infections and even hemorrhagic fever-causing viruses, such as Arena virus infections. Treatment with vidofludimus calcium may avoid virus infections and reactivations, one of the major drawbacks of the long-term use of traditional immunomodulators in IBD and MS patients. Recently, we presented preclinical data demonstrating the activity of vidofludimus calcium to prevent the reactivation of latent EBV infection into lytic infection

(Marschall et al. 2021). This mechanism may lead to reduce the regular cycle of reactivations and reinfections in the medium term, and thus the latent persistent EBV infection in patients in the long term.

Efficacy of vidofludimus has been observed in several animal disease models for IBD, MS, as well as systemic lupus erythematosus and transplant rejection. Previous filings by us with the SEC have summarized the development history of vidofludimus and the previous amorphous formulation of the free acid form of vidofludimus. After the consummation of the asset acquisition from 4SC, Immunic developed and filed a patent application for a new specific polymorph of the calcium salt formulation of vidofludimus, vidofludimus calcium, which we believe exhibits improved physicochemical and pharmacokinetic properties. In 2017, we completed two Phase 1 studies of single or repeated once-daily doses of vidofludimus calcium in

8

healthy volunteers, where we observed results supporting tolerability of repeated daily dosing of up to 50 mg of vidofludimus calcium.

Indication: Multiple Sclerosis

Diagnosis and Prevalence

MS is an autoimmune disease that affects the brain, spinal cord and optic nerve. In MS, myelin, the coating that protects the nerves, is attacked and damaged by the immune system. Thus, MS is considered an immune-mediated demyelinating disease of the central nervous system ("CNS"). MS is a progressive disease which, without effective treatment, leads to severe disability. We are developing vidofludimus calcium for the treatment of RRMS, the most common form of MS. Approximately 85% of patients with MS are expected to develop RRMS, with some of these patients later developing more progressive forms of the disease. RRMS is characterized by clearly defined attacks of new or increasing neurologic symptoms. These relapses are followed by periods of remissions, or partial or complete recovery. During remissions, all symptoms may disappear, or some symptoms may continue and become permanent.

MS is a disease with unpredictable symptoms that can vary widely. Common early signs of MS include vision problems, tingling and numbness or other unspecific neurological symptoms. Diagnosis of MS is confirmed via blood tests and a spinal tap, in which a small sample of fluid is removed from the spinal cord. However, most important for diagnosis are characteristic CNS lesions found using magnetic resonance imaging ("MRI").

According to DRG (Market Forecast Dashboard, Multiple Sclerosis (2020-2030), December 2021), MS affects more than 500,000 people in the United States, and more than 1.1 million people in the G7 countries (US, UK, Canada, Japan, Germany, France, Italy). The disease has a large economic impact as it affects mainly young adults in the prime working age, peaking around 30 years old, although MS can occur in children and in adults. MS is up to three times more common in women than in men. MS affects twice as many women and men in certain age cohorts and is more common in areas inhabited by people of northern European ancestry, such as Europe, the United States, Canada, New Zealand and parts of Australia.

A recent publication shed new light on the role of infection with the EBV previously postulated to trigger MS. Bjornevik et al. (2022) analyzed EBV antibodies in serum from 801 individuals who developed MS among a cohort of more than 10 million people active in the US military over a 20-year period (1993 to 2013). Risk of MS increased 32-fold after infection with EBV but was not increased after infection with other viruses, including the similarly transmitted cytomegalovirus. Serum levels of neurofilament light chain, a biomarker of axonal damage, increased only after EBV seroconversion. These findings cannot be explained by any known risk factor for MS and suggest EBV as the leading cause of MS. In addition, antibody producing cells directed against the latent EBV protein EBNA1 were found in the CSF of MS patients. Cross reactivity of anti-EBNA1 antibodies against GlialCAM, a protein that is predominantly expressed in glial cells in the CNS and potentially important in the myelination process of axons, further corroborates the connection between EBV infections and pathologic processes in MS (Lanz et al. 2022).

Current Treatment Options

There are currently two main treatment types available for RRMS. Some therapies, such as short-term corticosteroid medications, are used for treating relapses of MS symptoms. Other approaches are used as long-term treatments to reduce the number of relapses and prevent disability progression. The latter are referred to as disease-modifying therapies. We intend to develop vidofludimus calcium as a disease-modifying therapy for RRMS.

The initial treatment options for RRMS patients are often beta interferons (either as interferon beta-1a or interferon beta-1b) or glatiramer acetate, all of which are given by injection. For patients requiring more advanced treatment options, there are several oral medications, such as dimethyl fumarate, fingolimod, siponimod, teriflunomide, ozanimod or cladribine, and biologics, such as natalizumab, ocrelizumab, ofatumumab or alemtuzumab, approved for commercial use in MS in various countries. In addition, some of these drugs already have generic versions available in some countries and other drugs will become generic in the next years.

There is no specific guidance on which therapies or medications are used in which sequence of the MS disease course. Typically, treatments are escalated over time, considering:

9

•Persistent high MS disease activity under treatment with base medications (relapse(s), disability worsening, MRI lesions),

•Risks of long-term immunosuppression,

•Patient preferences or risks perceptions, and

•Safety/tolerability aspects.

Many drugs approved for patients with RRMS suppress the immune system, either broadly or by targeting classes of immune cells, altering how the immune system functions and fights certain infections. As a result, people who take these therapies are at higher risk for John Cunningham virus infection or re-activation, which is believed to be the cause of a rare and often lethal viral disease of the brain called progressive multifocal leukoencephalopathy ("PML"). To date, occurrences of PML have been reported in individuals with RRMS treated with natalizumab, dimethyl fumarate and fingolimod. No case of PML has yet been reported for the DHODH inhibitor teriflunomide, which has been one of the key differentiators of teriflunomide from other disease-modifying therapies in RRMS. The active moiety of vidofludimus calcium has also shown direct antiviral effects in several models of virus-infected cells, which we believe is caused by DHODH inhibition. Subject to further clinical trials, we believe that this could be a “class effect” of the DHODH inhibitors and if shown, could be an important potential differentiator against other drug classes in RRMS.

Depending on the results of future clinical trials, we believe that vidofludimus calcium has the potential to demonstrate medically important advantages compared with other treatments, particularly for the early treatment of RRMS patients, due to its anti-inflammatory and neuroprotective properties and safety and tolerability profile. Vidofludimus calcium could provide RRMS patients with a distinctive combination of the following properties:

•Targeted effect on hyperactive immune cells without suppression of normal immune function.

•Pronounced MRI lesion suppression of vidofludimus calcium compares favorably to other oral medications commercially available in RRMS.

•Improved rates of disability worsening, particularly in light of the apparent class effect of DHODH inhibition to disproportionally improve disability progression over the long-term.

•Robust decrease in serum neurofilament light chain, a biomarker for axonal damage, was observed for vidofludimus calcium and provides evidence of vidofludimus calcium’s potential neuroprotective activity.

•A very low discontinuation rate for vidofludimus calcium-treated RRMS patients, substantially below placebo, indicates an encouraging combination of tolerability and efficacy as well as maintenance of normal quality-of-life

•Absence of hepatotoxicity signals and other relevant adverse events leading to discontinuations distinguishes vidofludimus calcium well from other oral RRMS treatments.

•Broad spectrum antiviral effect of vidofludimus calcium may support in lowering the rate of viral infections and reactivations, including EBV reactivation, potentially resulting in slowing potential EBV-related neurodegenerative processes.

Current Development Plan and Ongoing Studies

Phase 2 Trial of Vidofludimus Calcium in RRMS (EMPhASIS Trial)

Our Phase 2 EMPhASIS trial of vidofludimus calcium in RRMS consisted of two cohorts: The full data set of Cohort 1, which evaluated efficacy and safety of 30 mg or 45 mg once daily vidofludimus calcium compared to placebo, was published by us in August and September 2020, respectively. Cohort 2, which evaluates efficacy and safety of 10 mg once daily vidofludimus calcium compared to placebo, was meanwhile also completed.

On August 2, 2020, we announced positive top-line data from our Phase 2 EMPhASIS trial of vidofludimus calcium in patients with RRMS. The study achieved statistical significance on all primary and key secondary endpoints, indicating activity in RRMS patients. In particular, the study met its primary endpoint, demonstrating a statistically significant reduction in the cumulative number of combined unique active (“CUA”) magnetic resonance imaging (“MRI”) lesions up to week 24 in patients receiving 45 mg of vidofludimus calcium once daily, by 62% (p=0.0002), as compared to placebo. The study also met its key secondary endpoint, showing a statistically significant reduction in the cumulative number of CUA MRI lesions for the 30 mg once daily dose by 70% (p<0.0001), as compared to placebo. On September 11, 2020, we published the full unblinded clinical data set from our Phase 2 EMPhASIS trial of vidofludimus calcium in patients with RRMS. The data confirmed and expanded on the previously announced top-line results.

10

On April 15, 2021, we announced interim data from Cohort 2 after 59 randomized patients completed week 12 MRI assessments. We concluded from this data, along with previously published data from Cohort 1, that 30 mg once daily vidofludimus calcium is the most appropriate anti-inflammatory dose for Phase 3 trials in patients with RMS.

Meanwhile, final data from Cohort 2 are also available showing that the anti-inflammatory effects of vidofludimus calcium at the 10 mg dose were observed to be lower (13% reduction of gadolinium-enhancing magnetic resonance imaging lesions up to 24 weeks, as compared to placebo) than those found with the 30 mg vidofludimus calcium dose in the pooled Cohort 1 and 2 data (78% reduction), providing further support for the selection of 30 mg dosing in the ongoing ENSURE trials in RMS. Final Cohort 2 data also provide evidence of dose-proportional neuroprotective activity. For instance, the highest decrease of the biomarker serum neurofilament light chain was observed with the 45 mg dose of vidofludimus calcium versus placebo (-26.0% median of differences between percentage change of serum neurofilament, Hodges-Lehmann estimation), a substantial decrease was seen with the 30 mg dose (-18.0%), while the smallest decrease was observed with the 10 mg dose of Cohort 2 (-9.0%). The 10 mg group in Cohort 2 also showed a signal with respect to improvement in Expanded Disability Status Scale (“EDSS”), consistent with those signals seen with the higher doses in Cohort 1, although all of these early signals need to be confirmed in a larger patient population with longer follow-up periods. Taken together, these last two observations suggest that higher doses, such as 45 mg vidofludimus calcium, may be preferred doses for clinical trials in which neuroprotective effects are the main mechanism for improvement, such as in PMS.

While Cohort 1 blinded treatment was completed right before the COVID-19 pandemic started, final Cohort 2 data provide additional evidence that ongoing vidofludimus calcium treatment may reduce the risk of COVID-19 infections, presumably related to its known antiviral activity. In the entire Cohort 2 population of 59 patients, who were enrolled during pandemic conditions, incidental COVID-19 infections in the active treatment group were less frequent (8.5%, n=4/47) than in the placebo group (25.0%, n=3/12). Additionally, we recently obtained new preclinical data underlining that vidofludimus calcium shows potent anti-EBV activity. We also confirmed that vidofludimus calcium can be detected to a noteworthy degree in the cerebrospinal fluid of animals, after oral dosing. We believe that this finding suggests that vidofludimus calcium may be able to act directly within the central nervous system.

We have designed the Phase 3 trials in RMS and the Phase 2 trial in PMS to provide additional insights how vidofludimus calcium may address all aspects of the MS disease, in particular, monitoring of potential neuroprotective effects. The EMPhASIS trial continues as an open-label extension (“OLE”) treatment to obtain long-term safety data in RRMS patients. Currently, more than 200 patients are still on OLE treatment.

Further information regarding our EMPhASIS trial in RRMS can be found on ClinicalTrials.gov under the identifier NCT03846219.

Phase 3 Program of Vidofludimus Calcium in RMS (ENSURE-1 and ENSURE-2 Trials)

On July 1, 2021, we announced FDA clearance of our IND application for the Phase 3 ENSURE program of vidofludimus calcium in patients with RMS. The ENSURE program comprises two identical multicenter, randomized, double-blind Phase 3 trials designed to evaluate the efficacy, safety, and tolerability of vidofludimus calcium versus placebo in RMS patients. Based on vidofludimus calcium’s highly significant activity in preventing lesion formation in our Phase 2 EMPhASIS trial in RMS, the strong and consistent correlation observed between lesion formation and clinical relapse in third-party clinical trials, and the drug’s robust safety profile to date, we believe that this Phase 3 program should provide a relatively simple and straightforward path towards potential regulatory approval of vidofludimus calcium in RMS.

Each of the identical twin Phase 3 trials, titled ENSURE-1 and ENSURE-2, is expected to enroll approximately 1,050 adult patients with active RMS at more than 100 sites in more than 15 countries, including the United States, India and countries in Latin America, Central and Eastern Europe. Patients will be randomized in a double-blinded fashion to either 30 mg daily doses of vidofludimus calcium or placebo and the primary endpoint for both trials is time to first relapse up to 72 weeks. Key secondary endpoints include volume of new T2-lesions, time to confirmed disability progression, time to sustained clinically relevant changes in cognition, and percentage of whole brain volume change. With regard to the disability progression endpoint, the ENSURE program will apply a pooled analysis of disability worsening across both trials.

The ENSURE trials will be run concurrently. The first patient in ENSURE-1 was enrolled in November 2021. The first patient in ENSURE-2 was enrolled in January 2022. An interim analysis to assess event rates is planned to occur after a certain number of relapses have occurred in the double-blind treatment periods. This analysis is intended to inform potential sample

11

size adjustment and help ensure that final study readout is not planned to occur before sufficient events have been achieved. This interim analysis will also allow for a non-binding futility analysis.

Further information regarding our ENSURE program in RMS can be found on ClinicalTrials.gov under the identifiers NCT05134441 (ENSURE-1) and NCT05201638 (ENSURE-2), respectively.

The execution of clinical Phase 3 trials usually requires the use of a commercial formulation of the investigational drug manufactured at commercially usable quantities. Manufactures under contract with us have developed and produced a roller compactor formulation of vidofludimus calcium (IMU-838-RC) which would allow commercially usable production batches. An Phase 1 bioequivalence study between the previous wet granulation and the new IMU-838-RC formulation of vidofludimus calcium has completed the experimental phase and showed bioequivalence regarding drug exposure curve in blood plasma (area under the curve). A confirmatory relative bioavailability and food effect study demonstrated a high bioavailability of IMU-838-RC tablets as compared to a drinking solution and confirmed the in vitro finding of a complete and fast dissolution profile in human subjects. No food effect on the uptake or elimination of vidofludimus after administration of the IMU-838-RC tablet was observed.

Additional investigations regarding metabolite characterization, metabolic modeling and potential drug-drug interactions, as well as other activities relating to clinical pharmacology are also being finalized at this time in anticipation for presentation to regulatory authorities.

We are currently working with clinical and regulatory advisors to propose a pediatric development plan for vidofludimus calcium in RRMS in the near future.

Phase 2 Program of Vidofludimus Calcium in PMS (CALLIPER Trial)

On July 1, 2021, we announced that the FDA also cleared our separate IND application for the supportive Phase 2 CALLIPER trial of vidofludimus calcium in patients with PMS. The first patient was enrolled in September 2021.

The multicenter, randomized, double-blind, placebo-controlled Phase 2 CALLIPER trial is intended to run concurrently with and to complement the Phase 3 program in RMS. In particular, CALLIPER is focused on progressive forms of MS and designed to corroborate vidofludimus calcium’s neuroprotective potential, as exemplified by slowing of brain atrophy and delay in disability worsening. Neurodegeneration is a key concern in both PMS and RMS, since axonal and neural damage is responsible for the increasing and often severe disability experienced by patients. We believe that, if the CALLIPER trial is successful in showing a beneficial effect of vidofludimus calcium, this data, along with the ENSURE program and vidofludimus calcium’s strong safety and tolerability profile, may allow for a meaningful clinical differentiation of vidofludimus calcium from other MS medications and potentially attractive commercial positioning. Although a supportive trial, we do not believe that data from the CALLIPER trial are a pre-condition for filing an NDA in RMS. Additional clinical studies and the potential regulatory path forward specific to the treatment of PMS will be informed by the results of the CALLIPER trial and will be further assessed accordingly.

The Phase 2 CALLIPER trial is expected to enroll approximately 450 patients at more than 70 sites in North America, Western, Central and Eastern Europe with patients randomized to either 45 mg daily doses of vidofludimus calcium or placebo in a double-blinded fashion. The trial’s primary endpoint is the annualized rate of percent brain volume change up to 120 weeks. Key secondary endpoints include the annualized rate of change in whole brain atrophy and time to 24-week confirmed disability progression based on the expanded disability status scale which may further support disability data from the ENSURE trials.

An interim analysis comprising an unblinded analysis of serum NfL is planned to occur once approximately half of the enrolled patients have completed 24 weeks of treatment. NfL has been shown in third-party research to consistently correlate with disease activity in neurodegenerative disorders and has become one of the most important serum biomarkers for axonal damage over the past few years. As previously reported, results of the Phase 2 EMPhASIS trial of vidofludimus calcium in RRMS showed a robust decrease in serum NfL at 24 weeks (-17.0% for 30 mg and -20.5% for 45 mg), as compared to baseline values, while the patients on placebo experienced a 6.5% increase in serum NfL over the same period.

Further information regarding our CALLIPER trial in PMS can be found on ClinicalTrials.gov under the identifier NCT05054140.

12

Indication: Ulcerative Colitis

Diagnosis and Prevalence

UC is a chronic inflammatory disease characterized by diffuse inflammation of the mucosa of the colon and rectum. The hallmark clinical symptoms of UC are diarrhea and bloody stool, and its clinical course is marked by exacerbations and remissions, which may occur spontaneously or in response to treatment changes or intercurrent illnesses.

UC is most commonly diagnosed in late adolescence or early adulthood, but it can occur at any age. The occurrence of UC worldwide has increased over the past few years, particularly in Latin America, Asia and Eastern Europe (Burisch et al. 2015). According to DRG (Market Forecast Dashboard, UC (2020-2030), November 2021), approximately one million patients are affected by UC in the United States, and more than 2.2 million in the G7 countries (US, UK, Canada, Japan, Germany, France, Italy). UC is almost equally distributed between genders (Kappelman et al. 2007).

Current Treatment Options

The severity and extent of UC are characterized based on clinical and endoscopic findings. The treatment approach often depends on disease severity and typically follows a stepwise treatment regimen. Patients with mild disease may initially receive aminosalicylates or non-systemic steroids, such as budesonide. Patients with moderate to severe disease activity may receive traditional immunomodulators (such as azathioprine or 6-mercaptopurine) or steroids (such as prednisone). If patients fail to respond to these therapies, treatment may be escalated to the use of biologics or selective immunomodulators (such as tofacitinib). The most common category of biologics used to treat UC includes TNFα antibody drugs, such as infliximab or adalimumab. New biologic options are alpha-4-beta-7 (α4ß7) integrin-specific antibodies, such as vedolizumab and anti-IL-12/IL-23 antibodies, such as ustekinumab. All biologics currently used to treat UC are injectables. Biologics are usually the most expensive treatment option and reserved for patients who have failed other therapies.

Currently, there are several new oral treatment options for UC patients in advanced clinical development or in regulatory review. Most of them fall into one of the following two categories: sphingosine-1-phosphate (“S1P”) agonists, or Janus kinase (“JAK”) inhibitors. Some of these drug candidates have been or may be approved by regulatory authorities for commercial use before vidofludimus calcium may receive approval. However, depending on the results of future clinical trials, we believes that vidofludimus calcium has the potential to demonstrate medically important advantages compared with other treatments, particularly for long-term therapy in UC patients, due to the selectivity of DHODH targeting of metabolically activated lymphocytes, the absence of general detrimental effects on bone marrow and the immune system, its safety and tolerability profile and the direct antiviral activity.

Treatment of UC is differentiated between induction treatment (during periods of disease symptoms or following relapse) and maintenance treatment (often a long-term treatment to keep a patient relapse-free). Since UC patients ultimately fail to respond to treatments, cease to respond to their treatments or develop unacceptable side effects, there is a need for safe and effective treatments for UC with novel mechanisms. Additionally, patients often prefer the convenience of oral treatments over injections. For some of the currently available oral immunomodulators or those in clinical testing, a higher rate of infections (particularly virus re-activations) have been reported versus placebo control, which can be a medically significant event for patients.

Vidofludimus calcium is being developed to be a new treatment option for patients with moderate to severe UC who are candidates for therapy escalation. As a potentially highly selective, first-in-class oral therapy, vidofludimus calcium has the potential to become a new standard of care in the treatment armamentarium for patients with moderate to severe UC. This potential is supported by the following properties of vidofludimus calcium:

•Targeted effect on hyperactive immune cells without suppression of normal immune function.

•First-in-class mode of action targeting relevant immune cell populations not currently addressed by existing therapeutic options, particularly in patients who are not sufficiently responsive to available therapies.

•Potential best-in-class safety and tolerability profile, as has been observed to date across the full scope of clinical trials for vidofludimus calcium.

•Potential for combination treatment with established biologics through synergistic effects.

•Increased flexibility for dosing and administration outside of infusion centers.

•Long-term treatment potential with small molecule approach, avoiding the decreasing responsiveness shown with existing antibody treatments as a result of anti-drug antibody development.

13

•Antiviral effects that potentially avoid virus reactivations which is known to be connected to several currently approved medications in UC.

Clinical Development Plan and Ongoing/Planned Clinical Studies

Before commencing clinical development in IBD, including UC, we had developed a clinical development plan in collaboration with a group of well-known and experienced physicians from North America and Europe, and had received formal regulatory advice for our Phase 2 development program from the FDA.

Phase 2 Trial of Vidofludimus Calcium in UC (CALDOSE-1 Trial)

The CALDOSE-1 trial of vidofludimus calcium in moderate to severe UC is a Phase 2b, dose-finding, multicenter, double-blind, placebo-controlled study including a blinded induction and maintenance phase, with double randomization (initial randomization for induction and second randomization for maintenance). The trial also includes an option for an open-label treatment extension for patients discontinuing from or completing blinded treatment. The primary endpoint comprises a composite of patient-reported outcome and endoscopy-assessed outcome, both evaluated following ten weeks of induction treatment with vidofludimus calcium or placebo. We have an active IND application for vidofludimus calcium in UC with the FDA.

CALDOSE-1 is being conducted at more than 100 sites in 19 countries, including the United States and Western, Central and Eastern Europe. Enrollment in the study includes a central, blinded and independent assessment of endoscopy at screening to confirm patient eligibility. We believe that it has taken prudent steps to ensure that the study is conducted in a manner that is consistent with the study protocol in all countries in which the study is being conducted, even though such countries have varying healthcare systems and practices. This includes an endoscopy-based patient eligibility assessment by a central independent reader and a multiple read and potential adjudication process for week 10 endoscopy when the primary study endpoint is assessed.

On October 28, 2021, we announced that the final patient has been enrolled and randomized in the CALDOSE-1 trial. At the completion of patient recruitment, the trial has randomized a total of 263 patients into four arms: three active dosing arms of 10 mg, 30 mg and 45 mg, as well as placebo. Top-line data for the induction phase are expected to be available in June of 2022.

Under an agreement between us and the FDA, reached during our pre-IND meeting in 2017, the UC Phase 2b trial was designed to begin enrollment with three active dosing arms of 10 mg, 30 mg and 45 mg, respectively, in addition to a placebo arm. At the end of August 2019, an interim dosing analysis was performed by an unblinded and independent data review committee, which has concluded that the lowest dose of 10 mg appeared not to be likely ineffective, the highest dose of 45 mg was not intolerable, and no safety signal was identified for any of the trial’s three doses of vidofludimus calcium. The data review committee has not shared with us any of the unblinded data underlying these conclusions, and the study remains blinded to us, the investigators and the enrolled patients. The interim dosing analysis was not designed to be a futility analysis nor was the primary endpoint or any other endpoint of the study tested statistically. As a result of these findings, the trial’s steering committee has recommended continuation of all three dosing arms, which recommendation was implemented by us. Expansion of vidofludimus calcium’s potentially effective dose range required continuation of all three dose groups and increased the overall number of patients expected to be included in the ongoing trial from a previously anticipated 195 patients, to a total of 240 patients.

Further information regarding our CALDOSE-1 trial in UC can be found on ClinicalTrials.gov under the identifier NCT03341962.

Indication: Crohn’s Disease

Diagnosis and Prevalence

CD is an idiopathic chronic inflammatory disease of unknown etiology with genetic, immunologic and environmental influences. Like UC, it is one of the major diseases that are generally characterized as IBD. Both UC and CD are caused by chronic inflammation in the gastrointestinal ("GI") tract, but CD can involve the entire GI tract, from the mouth to the anus (but it most commonly involves both the large and small intestines), whereas UC is restricted to the colon and rectum. Distinguishing CD from UC can be challenging when inflammation is confined to the colon. CD typically involves all layers of

14

the bowel wall, thereby causing complications, such as abscesses, strictures and fistulas, that regularly require surgical intervention.

Hallmark clinical symptoms of CD are chronic diarrhea and abdominal pain. However, the diagnosing physician needs to evaluate laboratory tests, endoscopy results, pathology findings and radiographic tests to arrive at a clinical diagnosis of CD. In general, it is the presence of chronic intestinal inflammation that leads to a diagnosis of CD.

CD is most commonly diagnosed in late adolescence or early adulthood, but it can manifest at any age. According to DRG (Market Forecast Dashboard, Crohn’s Disease (2020-2030), December 2021), more than 900,000 patients are affected by CD in the United States, and more than 1.7 million in the G7 countries (US, UK, Canada, Japan, Germany, France, Italy). CD is slightly more prevalent in women than in men.

Current Treatment Options

Treatment of CD is similar to treatment of UC. However, some of the therapies available for UC (such as tofacitinib) have shown varying levels of activity in CD. Conversely, and based on the treatment needs of patients with CD, some drugs have been primarily developed for CD. One such example is the biologic ustekinumab, an antibody directed against IL-12 and IL-23. There are now some approved treatments, such as alofisel, that target the specific structural complications of CD, including fistulas.

Leflunomide is used off-label in patients with CD and has shown an initial suggestion of the possible value of DHODH inhibition in this patient population (Holtmann et al. 2008, Prajapati et al. 2003). In two small investigator trials of leflunomide in CD patients, investigators observed DHODH inhibitor activity in the treatment of moderate to severe CD in patients who have failed or are intolerant to traditional immunomodulator therapy. However, the side effect profile of leflunomide included diarrhea. The prescribing information for teriflunomide, leflunomide’s active metabolite, lists a 15-18% rate of diarrhea, which makes it one of the most prevalent side effects of this DHODH inhibitor. We believe that despite the findings of efficacy for leflunomide in the investigator trials in CD patients, the side effect profile makes it unlikely that this type of DHODH inhibitor can be developed in the indication of IBD, and particularly in CD.

Current Development Plan and Ongoing Studies

We are considering our development strategy for vidofludimus calcium for the treatment of CD. During the previously noted discussions with the FDA regarding our UC trial, we and the FDA reached agreement that a clinical trial of vidofludimus calcium in CD could commence when the interim dosing analysis for the Phase 2b CALDOSE-1 trial in UC has been completed. This would allow us to execute its development of vidofludimus calcium in CD with the remaining active dose groups from CALDOSE-1 and placebo, thereby potentially allowing more efficient recruitment into this trial. We had also received additional written advice from the FDA regarding patient-reported outcomes to be used in this trial, called CALDOSE-2. Given the outcome of the interim dosing analysis of the CALDOSE-1 trial, we are currently re-evaluating the trial design in CD and also prefers to evaluate the upcoming CALDOSE-1 results prior to the start of a potential CALDOSE-2 clinical trial. In addition, we are evaluating the optimal time for efficiently executing such study following the COVID-19 pandemic.

Indication: Primary Sclerosing Cholangitis

We are also exploring the use of vidofludimus calcium in orphan diseases that may allow for an accelerated path to commercialization. We are exploring such orphan diseases in conjunction with interested investigators.

Diagnosis and Prevalence

PSC is a rare liver disease in which the bile ducts in the liver become inflamed, narrow and prevent bile from flowing properly. According to Toy et al. (2011), PSC has a prevalence of approximately 4.15 per 100,000 in the United States. The exact cause and disease mechanism of PSC are still unknown, but an autoimmune mechanism may play a role. According to Singh et al. (2013), there is an association with IBD, most often with UC and less commonly with CD. Progressive biliary and hepatic damage results in portal hypertension and hepatic failure in a significant majority of patients over a 10-15 year period from initial diagnosis.

15

Current Treatment Options

Treatment of PSC is supportive, with a focus on monitoring the disease progression and treating symptoms and complications as they arise. The only substantial treatment is liver transplantation, which may be an option when the disease progresses to cirrhosis and liver function is significantly affected. When some of the larger bile ducts become blocked in patients with PSC, one potential is to open them with endoscopy-based methods, balloon dilatation or stent placement. No medication is currently approved to treat PSC, but medications may be used to control symptoms. Although many trials have failed to meet their endpoints in PSC, there are now a few studies for medications (such as obeticholic acid) that have shown limited activity in PSC.

Current Development Plan and Ongoing Studies

We have entered into a collaboration with investigators at the Mayo Clinic to explore the use of vidofludimus calcium in PSC. An investigator-sponsored proof-of-concept clinical trial of vidofludimus calcium in PSC, for which we provided the study medication, was conducted at the Mayo Clinic in Arizona and Minnesota, both of which are tertiary referral centers for PSC patients. The study was led by Elizabeth Carey, M.D., Professor of Medicine, Division of Gastroenterology and Hepatology, Department of Internal Medicine, Mayo Clinic, who had received Investigator IND approval from the FDA and had been granted Institutional Review Board ("IRB") approval to conduct the study. The study was supported by a grant from the National Institutes of Health (“NIH”).

The study planned to enroll 30 patients with PSC, aged 18 to 75 years, who received 30 mg of vidofludimus calcium once daily for a period of 24 weeks. Enrollment for the study took place between July 2019 and September 2020, but almost all enrollment occurred in 2019 and early 2020. During the COVID-19 pandemic, recruitment for this study was hampered, as patients with PSC are at a high risk of COVID-19 infections and were advised to avoid travel and unnecessary social contacts such as those required to participate in a clinical trial. Together with the investigators, we determined to readout data of the 18 patients who were enrolled prior to the COVID-19 pandemic. The ongoing pandemic situation also triggered the principal investigator’s decision to terminate the study in late 2020, before the intended recruitment goal of 30 patients was reached.

On February 18, 2021, we announced positive top-line data from the study which was designed to investigate vidofludimus calcium's potential to improve various biochemical parameters in PSC patients and help determine whether any such activity warrants further investigation randomized PSC trials. 18 of the targeted 30 patients were enrolled in the study (intent-to-treat population, “ITT”), of whom only 11 patients completed the full vidofludimus calcium treatment course and were evaluable over the 24-week treatment period (per-protocol population, “PP”).