false2022Q1000128005812/31http://www.blackbaud.com/20220331#AccruedExpensesAndOtherCurrentLiabilitieshttp://www.blackbaud.com/20220331#AccruedExpensesAndOtherCurrentLiabilities00012800582022-01-012022-03-3100012800582022-05-02xbrli:shares00012800582022-03-31iso4217:USD00012800582021-12-31iso4217:USDxbrli:shares0001280058blkb:RecurringMember2022-01-012022-03-310001280058blkb:RecurringMember2021-01-012021-03-310001280058us-gaap:TechnologyServiceMember2022-01-012022-03-310001280058us-gaap:TechnologyServiceMember2021-01-012021-03-3100012800582021-01-012021-03-3100012800582020-12-3100012800582021-03-310001280058us-gaap:CommonStockMember2021-12-310001280058us-gaap:AdditionalPaidInCapitalMember2021-12-310001280058us-gaap:TreasuryStockMember2021-12-310001280058us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001280058us-gaap:RetainedEarningsMember2021-12-310001280058us-gaap:RetainedEarningsMember2022-01-012022-03-310001280058us-gaap:AdditionalPaidInCapitalMember2022-01-012022-03-310001280058us-gaap:CommonStockMember2022-01-012022-03-310001280058us-gaap:TreasuryStockMember2022-01-012022-03-310001280058us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-03-310001280058us-gaap:CommonStockMember2022-03-310001280058us-gaap:AdditionalPaidInCapitalMember2022-03-310001280058us-gaap:TreasuryStockMember2022-03-310001280058us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-03-310001280058us-gaap:RetainedEarningsMember2022-03-310001280058us-gaap:CommonStockMember2020-12-310001280058us-gaap:AdditionalPaidInCapitalMember2020-12-310001280058us-gaap:TreasuryStockMember2020-12-310001280058us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001280058us-gaap:RetainedEarningsMember2020-12-310001280058us-gaap:RetainedEarningsMember2021-01-012021-03-310001280058us-gaap:TreasuryStockMember2021-01-012021-03-310001280058us-gaap:CommonStockMember2021-01-012021-03-310001280058us-gaap:AdditionalPaidInCapitalMember2021-01-012021-03-310001280058us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-03-310001280058us-gaap:CommonStockMember2021-03-310001280058us-gaap:AdditionalPaidInCapitalMember2021-03-310001280058us-gaap:TreasuryStockMember2021-03-310001280058us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-03-310001280058us-gaap:RetainedEarningsMember2021-03-310001280058blkb:EVERFIMember2021-12-312021-12-310001280058blkb:EVERFIMember2021-12-310001280058blkb:EVERFIMember2022-01-012022-03-310001280058us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-03-310001280058us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-03-310001280058us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-03-310001280058us-gaap:FairValueMeasurementsRecurringMember2022-03-310001280058us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2021-12-310001280058us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2021-12-310001280058us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310001280058us-gaap:FairValueMeasurementsRecurringMember2021-12-310001280058us-gaap:RevolvingCreditFacilityMember2022-03-310001280058us-gaap:RevolvingCreditFacilityMember2021-12-31xbrli:pure0001280058us-gaap:SecuredDebtMember2022-03-310001280058us-gaap:SecuredDebtMember2021-12-310001280058us-gaap:MortgagesMember2022-03-310001280058us-gaap:MortgagesMember2021-12-310001280058us-gaap:LoansPayableMember2022-03-310001280058us-gaap:LoansPayableMember2021-12-310001280058us-gaap:ShortTermDebtMember2022-03-310001280058us-gaap:ShortTermDebtMember2021-12-310001280058us-gaap:LongTermDebtMember2022-03-310001280058us-gaap:LongTermDebtMember2021-12-3100012800582020-10-300001280058blkb:MaximumThroughDecember312023Member2022-01-310001280058blkb:MaximumAfterDecember312023Member2022-01-3100012800582022-01-310001280058blkb:GlobalHQMember2020-08-310001280058us-gaap:LoansPayableMember2020-12-310001280058blkb:November2020Swap1Member2020-11-300001280058blkb:November2020Swap2Member2020-11-300001280058blkb:November2020Swap3Member2020-11-300001280058blkb:November2020Swap4Member2020-11-300001280058blkb:July2021SwapMember2021-07-310001280058us-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestRateSwapMemberus-gaap:OtherAssetsMember2022-03-310001280058us-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestRateSwapMemberus-gaap:OtherAssetsMember2021-12-310001280058us-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestRateSwapMember2022-03-310001280058us-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestRateSwapMember2021-12-310001280058us-gaap:InterestRateSwapMemberus-gaap:CashFlowHedgingMember2022-01-012022-03-310001280058us-gaap:InterestRateSwapMemberus-gaap:CashFlowHedgingMemberus-gaap:InterestExpenseMember2022-01-012022-03-310001280058us-gaap:InterestRateSwapMemberus-gaap:CashFlowHedgingMember2021-01-012021-03-310001280058us-gaap:InterestRateSwapMemberus-gaap:CashFlowHedgingMemberus-gaap:InterestExpenseMember2021-01-012021-03-310001280058blkb:ThirdpartyTechnologyMember2022-03-3100012800582021-01-012021-12-310001280058srt:MinimumMember2022-03-310001280058srt:MaximumMember2022-03-31blkb:cases0001280058blkb:PutativeConsumerClassActionCasesMember2022-01-012022-03-310001280058blkb:PutativeConsumerClassActionCasesUSFederalCourtsMember2022-01-012022-03-310001280058blkb:PutativeConsumerClassActionCasesCanadianCourtsMember2022-01-012022-03-310001280058country:ES2021-09-012021-09-30iso4217:EUR0001280058us-gaap:CashFlowHedgingMember2021-12-310001280058us-gaap:CashFlowHedgingMember2020-12-310001280058us-gaap:CashFlowHedgingMember2022-01-012022-03-310001280058us-gaap:CashFlowHedgingMember2021-01-012021-03-310001280058us-gaap:CashFlowHedgingMember2022-03-310001280058us-gaap:CashFlowHedgingMember2021-03-310001280058us-gaap:AccumulatedTranslationAdjustmentMember2021-12-310001280058us-gaap:AccumulatedTranslationAdjustmentMember2020-12-310001280058us-gaap:AccumulatedTranslationAdjustmentMember2022-01-012022-03-310001280058us-gaap:AccumulatedTranslationAdjustmentMember2021-01-012021-03-310001280058us-gaap:AccumulatedTranslationAdjustmentMember2022-03-310001280058us-gaap:AccumulatedTranslationAdjustmentMember2021-03-3100012800582021-01-012022-03-310001280058country:US2022-01-012022-03-310001280058country:US2021-01-012021-03-310001280058country:GB2022-01-012022-03-310001280058country:GB2021-01-012021-03-310001280058us-gaap:NonUsMember2022-01-012022-03-310001280058us-gaap:NonUsMember2021-01-012021-03-310001280058blkb:USMarketsGroupMember2022-01-012022-03-310001280058blkb:USMarketsGroupMember2021-01-012021-03-310001280058blkb:InternationalMarketsGroupMember2022-01-012022-03-310001280058blkb:InternationalMarketsGroupMember2021-01-012021-03-310001280058blkb:EVERFIMember2022-01-012022-03-310001280058blkb:EVERFIMember2021-01-012021-03-310001280058us-gaap:AllOtherSegmentsMember2022-01-012022-03-310001280058us-gaap:AllOtherSegmentsMember2021-01-012021-03-310001280058blkb:ContractualRecurringMember2022-01-012022-03-310001280058blkb:ContractualRecurringMember2021-01-012021-03-310001280058blkb:TransactionalRecurringMember2022-01-012022-03-310001280058blkb:TransactionalRecurringMember2021-01-012021-03-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| | | | | |

| ☑ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the quarterly period ended March 31, 2022 |

or

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to . |

Commission file number: 000-50600

Blackbaud, Inc.

(Exact name of registrant as specified in its charter)

| | | | | |

| |

| Delaware | 11-2617163 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

65 Fairchild Street

Charleston, South Carolina 29492

(Address of principal executive offices, including zip code)

(843) 216-6200

(Registrant’s telephone number, including area code)

| | | | | | | | |

| | |

| Securities Registered Pursuant to Section 12(b) of the Act: |

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on which Registered |

| Common Stock, $0.001 Par Value | BLKB | Nasdaq Global Select Market |

| | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | ☑ | | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☑

The number of shares of the registrant’s Common Stock outstanding as of May 2, 2022 was 52,943,047.

TABLE OF CONTENTS

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 1 |

| | | | | | | | |

| | CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS |

This Quarterly Report on Form 10-Q, including the documents incorporated herein by reference, contains forward-looking statements that anticipate results based on our estimates, assumptions and plans that are subject to uncertainty. These "forward-looking statements" are made subject to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements consist of, among other things, specific and overall impacts of the COVID-19 global pandemic on our financial condition and results of operations and on the markets and communities in which we and our customers and partners operate, trend analyses, statements regarding future events, future financial performance, our anticipated growth, the effect of general economic and market conditions, our business strategy and our plan to build and grow our business, our operating results, our ability to successfully integrate acquired businesses and technologies, the effect of foreign currency exchange rate and interest rate fluctuations on our financial results, the impact of expensing stock-based compensation, the sufficiency of our capital resources, our ability to meet our ongoing debt and obligations as they become due, cybersecurity and data protection risks and related liabilities, and current or potential legal proceedings involving us, all of which are based on current expectations, estimates, and forecasts, and the beliefs and assumptions of our management. Words such as “believes,” “seeks,” “expects,” “may,” “might,” “should,” “intends,” “could,” “would,” “likely,” “will,” “targets,” “plans,” “anticipates,” “aims,” “projects,” “estimates” or any variations of such words and similar expressions are also intended to identify such forward-looking statements. These forward-looking statements are subject to risks, uncertainties and assumptions that are difficult to predict. Accordingly, they should not be viewed as assurances of future performance, and actual results may differ materially and adversely from those expressed in any forward-looking statements.

Important factors that could cause actual results to differ materially from our expectations expressed in forward-looking statements include, but are not limited to, those summarized under “Part II, Item 1A. Risk factors” and elsewhere in this report, in our Annual Report on Form 10-K for the year ended December 31, 2021 and in our other filings made with the United States Securities & Exchange Commission ("SEC"). Forward-looking statements represent our management's beliefs and assumptions only as of the date of this Quarterly Report on Form 10-Q. We undertake no obligation to update or revise any forward-looking statements, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statement, whether as a result of new information, future events or otherwise.

| | | | | | | | |

2 | | First Quarter 2022 Form 10-Q |

| | | | | | | | |

| | PART I. FINANCIAL INFORMATION |

ITEM 1. FINANCIAL STATEMENTS

| | | | | | | | |

Blackbaud, Inc.

Condensed Consolidated Balance Sheets

(Unaudited) |

| (dollars in thousands) | March 31,

2022 | December 31,

2021 |

| Assets | | |

| Current assets: | | |

| Cash and cash equivalents | $ | 33,786 | | $ | 55,146 | |

| Restricted cash | 279,594 | | 596,616 | |

Accounts receivable, net of allowance of $10,772 and $11,155 at March 31, 2022 and December 31, 2021, respectively | 91,770 | | 102,726 | |

| Customer funds receivable | 2,049 | | 977 | |

| Prepaid expenses and other current assets | 99,913 | | 95,506 | |

| Total current assets | 507,112 | | 850,971 | |

| Property and equipment, net | 112,675 | | 111,428 | |

| Operating lease right-of-use assets | 51,808 | | 53,883 | |

| Software development costs, net | 126,766 | | 121,377 | |

| Goodwill | 1,056,794 | | 1,058,640 | |

| Intangible assets, net | 683,348 | | 698,052 | |

| Other assets | 90,194 | | 77,266 | |

| Total assets | $ | 2,628,697 | | $ | 2,971,617 | |

| Liabilities and stockholders’ equity | | |

| Current liabilities: | | |

| Trade accounts payable | $ | 39,490 | | $ | 22,067 | |

| Accrued expenses and other current liabilities | 72,195 | | 100,096 | |

| Due to customers | 278,179 | | 594,273 | |

| Debt, current portion | 18,116 | | 18,697 | |

| Deferred revenue, current portion | 350,952 | | 374,499 | |

| Total current liabilities | 758,932 | | 1,109,632 | |

| Debt, net of current portion | 963,109 | | 937,483 | |

| Deferred tax liability | 144,590 | | 148,465 | |

| Deferred revenue, net of current portion | 4,725 | | 4,247 | |

| Operating lease liabilities, net of current portion | 50,785 | | 53,386 | |

| Other liabilities | 1,506 | | 1,344 | |

| Total liabilities | 1,923,647 | | 2,254,557 | |

| Commitments and contingencies (see Note 10) | | |

| Stockholders’ equity: | | |

Preferred stock; 20,000,000 shares authorized, none outstanding | — | | — | |

Common stock, $0.001 par value; 180,000,000 shares authorized, 67,658,172 and 66,165,666 shares issued at March 31, 2022 and December 31, 2021, respectively | 68 | | 66 | |

| Additional paid-in capital | 993,223 | | 968,927 | |

Treasury stock, at cost; 14,715,944 and 14,182,805 shares at March 31, 2022 and December 31, 2021, respectively | (535,585) | | (500,911) | |

| Accumulated other comprehensive income | 15,295 | | 6,522 | |

| Retained earnings | 232,049 | | 242,456 | |

| Total stockholders’ equity | 705,050 | | 717,060 | |

| Total liabilities and stockholders’ equity | $ | 2,628,697 | | $ | 2,971,617 | |

| | |

| The accompanying notes are an integral part of these condensed consolidated financial statements. |

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 3 |

| | | | | | | | | | | |

Blackbaud, Inc.

Condensed Consolidated Statements of Comprehensive Income

(Unaudited) |

| | | Three months ended

March 31, |

| (dollars in thousands, except per share amounts) | | | | 2022 | 2021 |

| Revenue | | | | | |

| Recurring | | | | $ | 244,666 | | $ | 206,750 | |

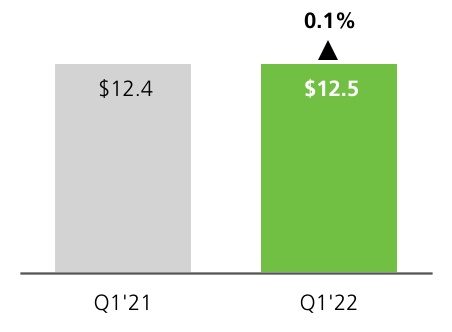

| One-time services and other | | | | 12,458 | | 12,441 | |

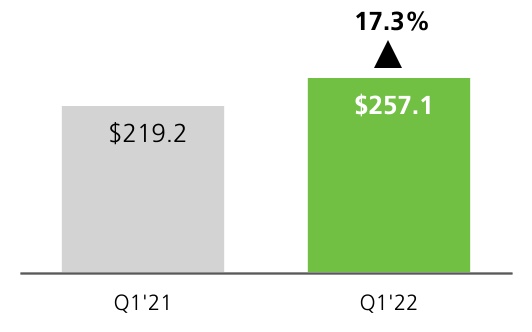

| Total revenue | | | | 257,124 | | 219,191 | |

| Cost of revenue | | | | | |

| Cost of recurring | | | | 112,174 | | 88,865 | |

| Cost of one-time services and other | | | | 11,188 | | 14,520 | |

| Total cost of revenue | | | | 123,362 | | 103,385 | |

| Gross profit | | | | 133,762 | | 115,806 | |

| Operating expenses | | | | | |

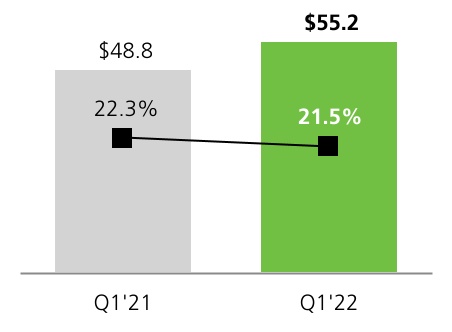

| Sales, marketing and customer success | | | | 55,216 | | 48,793 | |

| Research and development | | | | 39,952 | | 29,179 | |

| General and administrative | | | | 43,762 | | 30,587 | |

| Amortization | | | | 811 | | 549 | |

| Restructuring | | | | — | | 54 | |

| Total operating expenses | | | | 139,741 | | 109,162 | |

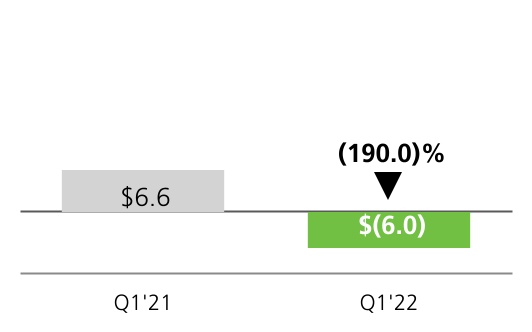

| (Loss) income from operations | | | | (5,979) | | 6,644 | |

| Interest expense | | | | (7,599) | | (5,114) | |

| Other income (expense), net | | | | 1,121 | | (1,010) | |

| (Loss) income before provision for income taxes | | | | (12,457) | | 520 | |

| Income tax (benefit) provision | | | | (2,050) | | 684 | |

| Net loss | | | | $ | (10,407) | | $ | (164) | |

| Loss per share | | | | | |

| Basic | | | | $ | (0.20) | | $ | — | |

| Diluted | | | | $ | (0.20) | | $ | — | |

| Common shares and equivalents outstanding | | | | | |

| Basic weighted average shares | | | | 51,199,717 | | 47,363,197 | |

| Diluted weighted average shares | | | | 51,199,717 | | 47,363,197 | |

| Other comprehensive income | | | | | |

| Foreign currency translation adjustment | | | | (2,132) | | 2,511 | |

| Unrealized gain on derivative instruments, net of tax | | | | 10,905 | | 4,149 | |

| Total other comprehensive income | | | | 8,773 | | 6,660 | |

| Comprehensive (loss) income | | | | $ | (1,634) | | $ | 6,496 | |

| | | | | |

| The accompanying notes are an integral part of these condensed consolidated financial statements. |

| | | | | | | | |

4 | | First Quarter 2022 Form 10-Q |

| | | | | | | | |

Blackbaud, Inc.

Condensed Consolidated Statements of Cash Flows

(Unaudited) |

| | Three months ended

March 31, |

| (dollars in thousands) | 2022 | 2021 |

| Cash flows from operating activities | | |

| Net loss | $ | (10,407) | | $ | (164) | |

| Adjustments to reconcile net loss to net cash provided by operating activities: | | |

| Depreciation and amortization | 25,545 | | 20,461 | |

| Provision for credit losses and sales returns | 1,875 | | 2,141 | |

| Stock-based compensation expense | 27,860 | | 30,005 | |

| Deferred taxes | (7,431) | | (1,142) | |

| Amortization of deferred financing costs and discount | 645 | | 506 | |

| Other non-cash adjustments | (150) | | (32) | |

| Changes in operating assets and liabilities, net of acquisition and disposal of businesses: | | |

| Accounts receivable | 9,010 | | 10,407 | |

| Prepaid expenses and other assets | (2,067) | | (17,426) | |

| Trade accounts payable | 15,919 | | 7,550 | |

| Accrued expenses and other liabilities | (13,430) | | 549 | |

| Deferred revenue | (22,865) | | (22,752) | |

| Net cash provided by operating activities | 24,504 | | 30,103 | |

| Cash flows from investing activities | | |

| Purchase of property and equipment | (4,266) | | (3,470) | |

| Capitalized software development costs | (12,683) | | (9,302) | |

| Purchase of net assets of acquired companies, net of cash and restricted cash acquired | (19,985) | | — | |

| | |

| Net cash used in investing activities | (36,934) | | (12,772) | |

| Cash flows from financing activities | | |

| Proceeds from issuance of debt | 59,400 | | 80,700 | |

| Payments on debt | (33,765) | | (59,667) | |

| | |

| | |

| Employee taxes paid for withheld shares upon equity award settlement | (34,674) | | (18,426) | |

| | |

| Change in due to customers | (315,294) | | (353,597) | |

| Change in customer funds receivable | (1,115) | | (563) | |

| Purchase of treasury stock | — | | (28,066) | |

| Net cash used in financing activities | (325,448) | | (379,619) | |

| Effect of exchange rate on cash, cash equivalents and restricted cash | (504) | | 230 | |

| Net decrease in cash, cash equivalents and restricted cash | (338,382) | | (362,058) | |

| Cash, cash equivalents and restricted cash, beginning of period | 651,762 | | 644,969 | |

| Cash, cash equivalents and restricted cash, end of period | $ | 313,380 | | $ | 282,911 | |

The following table provides a reconciliation of cash and cash equivalents and restricted cash reported within the condensed consolidated balance sheets that sum to the total of the same such amounts shown above in the condensed consolidated statements of cash flows:

| | | | | | | | |

| (dollars in thousands) | March 31,

2022 | December 31,

2021 |

| Cash and cash equivalents | $ | 33,786 | | $ | 55,146 | |

| Restricted cash | 279,594 | | 596,616 | |

| Total cash, cash equivalents and restricted cash in the statement of cash flows | $ | 313,380 | | $ | 651,762 | |

| | |

| The accompanying notes are an integral part of these condensed consolidated financial statements. |

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 5 |

Blackbaud, Inc.

Condensed Consolidated Statements of Stockholders' Equity

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | |

| (dollars in thousands) | Common stock | Additional

paid-in

capital | Treasury

stock | Accumulated

other

comprehensive

income (loss) | Retained

earnings | Total

stockholders'

equity |

| Shares | Amount |

| Balance at December 31, 2021 | 66,165,666 | | $ | 66 | | $ | 968,927 | | $ | (500,911) | | $ | 6,522 | | $ | 242,456 | | $ | 717,060 | |

| Net loss | — | | — | | — | | — | | — | | (10,407) | | (10,407) | |

Stock issuance costs related to purchase of EVERFI (see Note 3) | — | | — | | (983) | | — | | — | | — | | (983) | |

| | | | | | | |

Retirements of common stock(1) | (33,075) | | — | | (2,581) | | — | | — | | — | | (2,581) | |

| Vesting of restricted stock units | 976,312 | | — | | — | | — | | — | | — | | — | |

Employee taxes paid for 533,139 withheld shares upon equity award settlement | — | | — | | — | | (34,674) | | — | | — | | (34,674) | |

| Stock-based compensation | — | | — | | 27,860 | | — | | — | | — | | 27,860 | |

| Restricted stock grants | 580,209 | | 2 | | — | | — | | — | | — | | 2 | |

| Restricted stock cancellations | (30,940) | | — | | — | | — | | — | | — | | — | |

| Other comprehensive income | — | | — | | — | | — | | 8,773 | | — | | 8,773 | |

| Balance at March 31, 2022 | 67,658,172 | | $ | 68 | | $ | 993,223 | | $ | (535,585) | | $ | 15,295 | | $ | 232,049 | | $ | 705,050 | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

(1)Represents shares retired after determining certain EVERFI's selling shareholders would be paid in cash, rather than shares of our common stock. See Note 3 for additional information regarding our acquisition of EVERFI.

| | | | | | | | | | | | | | | | | | | | | | | |

| (dollars in thousands) | Common stock | Additional

paid-in

capital | Treasury

stock | Accumulated

other

comprehensive

income (loss) | Retained

earnings | Total

stockholders'

equity |

| Shares | Amount |

| Balance at December 31, 2020 | 60,904,638 | | $ | 61 | | $ | 544,963 | | $ | (353,091) | | $ | (2,497) | | $ | 236,714 | | $ | 426,150 | |

| Net loss | — | | — | | — | | — | | — | | (164) | | (164) | |

Purchase of 465,821 treasury shares under stock repurchase program | | | | (28,066) | | — | | — | | (28,066) | |

| Vesting of restricted stock units | 206,418 | | — | | — | | — | | — | | — | | — | |

Employee taxes paid for 240,867 withheld shares upon equity award settlement | — | | — | | — | | (18,426) | | — | | — | | (18,426) | |

| Stock-based compensation | — | | — | | 29,995 | | — | | — | | 10 | | 30,005 | |

| Restricted stock grants | 519,009 | | 1 | | — | | — | | — | | — | | 1 | |

| Restricted stock cancellations | (34,789) | | — | | — | | — | | — | | — | | — | |

| Other comprehensive income | — | | — | | — | | — | | 6,660 | | — | | 6,660 | |

| Balance at March 31, 2021 | 61,595,276 | | $ | 62 | | $ | 574,958 | | $ | (399,583) | | $ | 4,163 | | $ | 236,560 | | $ | 416,160 | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| The accompanying notes are an integral part of these condensed consolidated financial statements. |

| | | | | | | | |

6 | | First Quarter 2022 Form 10-Q |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

We are the world’s leading cloud software company powering social good. Serving the entire social good community—nonprofits, higher education institutions, K–12 schools, healthcare organizations, faith communities, arts and cultural organizations, foundations, companies and individual change agents—we connect and empower organizations to increase their impact through cloud software, services, expertise and data intelligence. Our portfolio is tailored to the unique needs of vertical markets, with solutions for fundraising and CRM, marketing, advocacy, peer-to-peer fundraising, corporate social responsibility (CSR) and environmental, social and governance (ESG), school management, ticketing, grantmaking, financial management, payment processing and analytics. Serving the industry for more than four decades, we are a remote-first company headquartered in Charleston, South Carolina, with operations in the United States, Australia, Canada, Costa Rica and the United Kingdom.

Unaudited condensed consolidated interim financial statements

The accompanying condensed consolidated interim financial statements have been prepared pursuant to the rules and regulations of the United States Securities and Exchange Commission ("SEC") for interim financial reporting. These consolidated statements are unaudited and, in the opinion of management, include all adjustments (consisting of normal recurring adjustments and accruals) necessary to state fairly the consolidated balance sheets, consolidated statements of comprehensive income, consolidated statements of cash flows and consolidated statements of stockholders’ equity, for the periods presented in accordance with accounting principles generally accepted in the United States ("U.S.") ("GAAP"). The consolidated balance sheet at December 31, 2021 has been derived from the audited consolidated financial statements at that date. Operating results and cash flows for the three months ended March 31, 2022 are not necessarily indicative of the results that may be expected for the fiscal year ending December 31, 2022, or any other future period. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with GAAP have been omitted in accordance with the rules and regulations for interim reporting of the SEC. These condensed consolidated interim financial statements should be read in conjunction with the consolidated financial statements and notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2021, and other forms filed with the SEC from time to time.

Basis of consolidation

The condensed consolidated financial statements include the accounts of Blackbaud, Inc. and its wholly owned subsidiaries. All intercompany balances and transactions have been eliminated in consolidation.

Reportable segment

We report our operating results and financial information in one operating and reportable segment. Our chief operating decision maker uses consolidated financial information to make operating decisions, assess financial performance and allocate resources. Our chief operating decision maker is our chief executive officer.

As discussed in Note 13 to these condensed consolidated financial statements, beginning in the second quarter of 2021, we combined our General Markets Group ("GMG") and Enterprise Markets Group ("EMG") into a single U.S. Markets Group ("UMG") and moved our Corporations vertical under our International Markets Group ("IMG"). This change was made to better align our resources toward customer retention and growth which, are key objectives as we progress toward our long-term aspirational goals. We also acquired EVERFI (as defined below) as of December 31, 2021. As we are working to integrate EVERFI into our business, it has not yet been included in one of our market groups. These changes did not impact our conclusions that we have one operating and reportable segment and one goodwill reporting unit.

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 7 |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Risks and uncertainties related to COVID-19

We are subject to risks and uncertainties as a result of the global COVID-19 pandemic. We believe that COVID-19 may continue to significantly impact our vertical markets and geographies, but the magnitude of the impact on our business cannot be determined at this time due to numerous uncertainties, including the duration of the outbreak, the severity of variants which may develop, travel restrictions and business closures, the effectiveness of vaccination programs and other actions taken to contain the disease and other unforeseeable consequences.

Use of estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, as well as the reported amounts of revenues and expenses during the reporting periods. On an ongoing basis, we reconsider and evaluate our estimates and assumptions, including those that impact revenue recognition, long-lived and intangible assets, income taxes, business combinations, stock-based compensation, capitalization of software development costs, our allowances for credit losses and sales returns, costs of obtaining contracts, valuation of derivative instruments, loss contingencies and insurance recoveries, among others. Changes in the facts or circumstances underlying these estimates, including due to COVID-19, could result in material changes and actual results could materially differ from these estimates.

Recently issued accounting pronouncements

There are no recently issued accounting pronouncements that we expect to have a material impact on our consolidated financial statements when adopted in the future.

Summary of significant accounting policies

There have been no material changes to our significant accounting policies described in our Annual Report on Form 10-K for the year ended December 31, 2021, filed with the SEC on March 1, 2022.

2021 Acquisition

EVERFI

On December 31, 2021, we acquired all of the outstanding equity securities, including all voting equity interests, of EVERFI, Inc., a Delaware corporation ("EVERFI"), pursuant to an agreement and plan of merger. The acquisition advanced our position as a leader in the rapidly evolving ESG and CSR spaces. We acquired the equity securities for approximately $442.7 million in cash consideration and 3,811,348 shares of the company's common stock, valued at approximately $301.1 million, for an aggregate purchase price of approximately $743.8 million, subject to closing adjustments. The cash consideration and related expenses were funded primarily through cash on hand and new borrowings under the 2020 Credit Facility (as defined below). As a result of the acquisition, EVERFI has become a wholly owned subsidiary of ours. The operating results of EVERFI have been included in our consolidated financial statements from the date of acquisition. In accordance with applicable accounting rules, we determined that the impact of this acquisition was not material to our consolidated financial statements; therefore, revenue and earnings since the acquisition date and pro forma information are not required to be presented.

The fair values assigned to the assets acquired and liabilities assumed in our acquisition of EVERFI are based on our best estimates and assumptions as of the reporting date and are considered preliminary pending finalization. The estimates and assumptions are subject to change as we obtain additional information during the measurement period, which may be up to one year from the acquisition date. The assets and liabilities, pending finalization, include the valuation of intangible assets as well as the assumed deferred income tax balances. During the three months ended March 31, 2022, we recorded an insignificant measurement period adjustment to the estimated fair value of the EVERFI assets acquired and liabilities assumed following the receipt of new information. The adjustment resulted in an increase to net working capital, excluding deferred revenue, with the corresponding offset to goodwill.

| | | | | | | | |

8 | | First Quarter 2022 Form 10-Q |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

| | |

| 4. Goodwill and Other Intangible Assets |

The change in goodwill during the three months ended March 31, 2022, consisted of the following:

| | | | | |

| (dollars in thousands) | Total |

| Balance at December 31, 2021 | $ | 1,058,640 | |

| |

Adjustments related to prior year business combinations(1) | (203) | |

| Effect of foreign currency translation | (1,643) | |

| Balance at March 31, 2022 | $ | 1,056,794 | |

(1)See Note 3 to these condensed consolidated financial statements for a discussion of the measurement period adjustment during the three months ended March 31, 2022 to the estimated fair value of the EVERFI assets acquired and liabilities assumed.

We compute basic earnings (loss) per share by dividing net income available to common stockholders by the weighted average number of common shares outstanding during the period. Diluted earnings (loss) per share is computed by dividing net income available to common stockholders by the weighted average number of common shares and dilutive potential common shares outstanding during the period. Diluted earnings (loss) per share reflect the assumed exercise, settlement and vesting of all dilutive securities using the “treasury stock method” except when the effect is anti-dilutive. Potentially dilutive securities consist of shares issuable upon the exercise of stock options, settlement of stock appreciation rights and vesting of restricted stock awards and units. Diluted loss per share for the three months ended March 31, 2022 was the same as basic loss per share as there was a net loss in the period and inclusion of potentially dilutive securities was anti-dilutive.

The following table sets forth the computation of basic and diluted earnings (loss) per share:

| | | | | | | | | | | |

| | | | Three months ended March 31, |

| (dollars in thousands, except per share amounts) | | | | 2022 | 2021 |

| Numerator: | | | | | |

| Net loss | | | | $ | (10,407) | | $ | (164) | |

| Denominator: | | | | | |

| Weighted average common shares | | | | 51,199,717 | | 47,363,197 | |

| Add effect of dilutive securities: | | | | | |

| Stock-based awards | | | | — | | — | |

| Weighted average common shares assuming dilution | | | | 51,199,717 | | 47,363,197 | |

| Earnings per share: | | | | | |

| Basic | | | | $ | (0.20) | | $ | — | |

| Diluted | | | | $ | (0.20) | | $ | — | |

| | | | | |

| Anti-dilutive shares excluded from calculations of diluted earnings per share | | | | 1,558,751 | | 1,360,378 | |

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 9 |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

| | |

| 6. Fair Value Measurements |

We use a three-tier fair value hierarchy to measure fair value. This hierarchy prioritizes the inputs into three broad levels as follows:

•Level 1 - Quoted prices for identical assets or liabilities in active markets;

•Level 2 - Quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets in markets that are not active, and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets; and

•Level 3 - Valuations derived from valuation techniques in which one or more significant inputs are unobservable.

Recurring fair value measurements

Assets and liabilities that are measured at fair value on a recurring basis consisted of the following, as of the dates indicated below:

| | | | | | | | | | | | | | | | | | | | | | | |

| Fair value measurement using | | |

| (dollars in thousands) | Level 1 | | Level 2 | | Level 3 | | Total |

| Fair value as of March 31, 2022 | | | | | | | |

| Financial assets: | | | | | | | |

| Derivative instruments | $ | — | | | $ | 21,947 | | | $ | — | | | $ | 21,947 | |

| Total financial assets | $ | — | | | $ | 21,947 | | | $ | — | | | $ | 21,947 | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| Fair value as of December 31, 2021 | | | | | | | |

| Financial assets: | | | | | | | |

| Derivative instruments | $ | — | | | $ | 7,160 | | | $ | — | | | $ | 7,160 | |

| Total financial assets | $ | — | | | $ | 7,160 | | | $ | — | | | $ | 7,160 | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

Our derivative instruments within the scope of Accounting Standards Codification ("ASC") 815, Derivatives and Hedging, are required to be recorded at fair value. Our derivative instruments that are recorded at fair value include interest rate swaps. See Note 9 to these condensed consolidated financial statements for additional information about our derivative instruments.

The fair value of our interest rate swaps was based on model-driven valuations using LIBOR rates, which are observable at commonly quoted intervals. Accordingly, our interest rate swaps are classified within Level 2 of the fair value hierarchy. The Financial Conduct Authority in the U.K. has stated that it plans to phase out all tenors of LIBOR by June 2023. We do not currently anticipate a significant impact to our financial position or results of operations as a result of this action as we expect that our financial contracts currently indexed to LIBOR will either expire or be modified without significant financial impact before the phase out occurs.

We believe the carrying amounts of our cash and cash equivalents, restricted cash, accounts receivable, trade accounts payable, accrued expenses and other current liabilities and due to customers approximate their fair values at March 31, 2022 and December 31, 2021, due to the immediate or short-term maturity of these instruments.

We believe the carrying amount of our debt approximates its fair value at March 31, 2022 and December 31, 2021, as the debt bears interest rates that approximate market value. As LIBOR and SOFR rates are observable at commonly quoted intervals, our debt under the 2020 Credit Facility (as defined below) is classified within Level 2 of the fair value hierarchy. Our fixed rate debt is also classified within Level 2 of the fair value hierarchy.

| | | | | | | | |

10 | | First Quarter 2022 Form 10-Q |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

We did not transfer any assets or liabilities among the levels within the fair value hierarchy during the three months ended March 31, 2022. Additionally, we did not hold any Level 3 assets or liabilities during the three months ended March 31, 2022.

Non-recurring fair value measurements

Assets and liabilities that are measured at fair value on a non-recurring basis include long-lived assets, intangible assets, goodwill and operating lease right-of-use ("ROU") assets. These assets are recognized at fair value during the period in which an acquisition is completed or at lease commencement, from updated estimates and assumptions during the measurement period, or when they are considered to be impaired. These non-recurring fair value measurements, primarily for long-lived assets, intangible assets acquired and operating lease ROU assets, are based on Level 3 unobservable inputs. In the event of an impairment, we determine the fair value of these assets other than goodwill using a discounted cash flow approach, which contains significant unobservable inputs and, therefore, is considered a Level 3 fair value measurement. The unobservable inputs in the analysis generally include future cash flow projections and a discount rate. For goodwill impairment testing, we estimate fair value using market-based methods including the use of market capitalization and consideration of a control premium.

There were no material non-recurring fair value adjustments to our long-lived assets, intangible assets, goodwill and operating lease ROU assets during the three months ended March 31, 2022.

| | |

| 7. Consolidated Financial Statement Details |

Restricted cash

| | | | | | | | |

| (dollars in thousands) | March 31,

2022 | December 31,

2021 |

| Restricted cash due to customers | $ | 276,130 | | $ | 593,296 | |

| Letters of credit for operating leases | 2,193 | | 2,256 | |

| Real estate escrow balances | 1,271 | | 1,064 | |

| Total restricted cash | $ | 279,594 | | $ | 596,616 | |

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 11 |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Prepaid expenses and other assets

| | | | | | | | |

| (dollars in thousands) | March 31,

2022 | December 31,

2021 |

Costs of obtaining contracts(1)(2) | $ | 76,482 | | $ | 78,465 | |

Prepaid software maintenance and subscriptions(3) | 33,950 | | 28,880 | |

| Derivative instruments | 21,947 | | 7,160 | |

Receivables for probable insurance recoveries(4)(5) | 12,715 | | 18,202 | |

Implementation costs for cloud computing arrangements, net(6)(7) | 11,354 | | 11,892 | |

| Prepaid insurance | 11,237 | | 5,363 | |

| Unbilled accounts receivable | 5,545 | | 5,443 | |

| Taxes, prepaid and receivable | 4,006 | | 3,986 | |

| Deferred tax assets | 1,569 | | 1,546 | |

| Other assets | 11,302 | | 11,835 | |

| Total prepaid expenses and other assets | 190,107 | | 172,772 | |

| Less: Long-term portion | 90,194 | | 77,266 | |

| Prepaid expenses and other current assets | $ | 99,913 | | $ | 95,506 | |

(1)Amortization expense from costs of obtaining contracts was $8.5 million and $9.2 million for the three months ended March 31, 2022 and 2021, respectively.

(2)The current portion of costs of obtaining contracts as of March 31, 2022 and December 31, 2021 was $29.7 million and $30.2 million, respectively.

(3)The current portion of prepaid software maintenance and subscriptions as of March 31, 2022 and December 31, 2021 was $29.8 million and $24.7 million, respectively.

(4)All receivables for probable insurance recoveries are classified as current.

(5)See discussion of the Security Incident at Note 10 to these condensed consolidated financial statements.

(6)These costs primarily relate to the multi-year implementations of our new global enterprise resource planning and customer relationship management systems.

(7)Amortization expense from capitalized cloud computing implementation costs was insignificant for the three months ended March 31, 2022 and 2021. Accumulated amortization for these costs was $3.5 million and $3.0 million as of March 31, 2022 and December 31, 2021, respectively.

Accrued expenses and other liabilities

| | | | | | | | |

| (dollars in thousands) | March 31,

2022 | December 31,

2021 |

Taxes payable(1) | $ | 23,305 | | $ | 19,777 | |

Accrued legal costs(2) | 12,208 | | 11,724 | |

| Operating lease liabilities, current portion | 8,930 | | 9,170 | |

| Customer credit balances | 7,403 | | 8,403 | |

| Accrued commissions and salaries | 4,656 | | 7,872 | |

| Accrued health care costs | 2,601 | | 3,042 | |

| Accrued vacation costs | 2,210 | | 2,234 | |

| Accrued bonuses | 1,460 | | 5,829 | |

| Accrued transaction-based costs related to payments services | 1,418 | | 5,427 | |

| Unrecognized tax benefit | 1,409 | | 1,248 | |

Amounts payable to former EVERFI option holders(3) | — | | 17,404 | |

| Other liabilities | 8,101 | | 9,310 | |

| Total accrued expenses and other liabilities | 73,701 | | 101,440 | |

| Less: Long-term portion | 1,506 | | 1,344 | |

| Accrued expenses and other current liabilities | $ | 72,195 | | $ | 100,096 | |

(1)We deferred payments of the employer's portion of Social Security taxes during 2020 under the Coronavirus, Aid, Relief and Economic Security Act, half of which was due by the end of calendar year 2021 with the remainder due by the end of calendar year 2022.

(2)All accrued legal costs are classified as current.

| | | | | | | | |

12 | | First Quarter 2022 Form 10-Q |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

(3)Represents amounts that had not been paid by EVERFI to its former option holders as of December 31, 2021, solely due to the timing of the acquisition on the last day of 2021. See Note 3 to these condensed consolidated financial statements for additional information regarding our acquisition of EVERFI.

The following table summarizes our debt balances and the related weighted average effective interest rates, which includes the effect of interest rate swap agreements.

| | | | | | | | | | | | | | | | | |

| Debt balance at | | Weighted average

effective interest rate at |

| (dollars in thousands) | March 31,

2022 | December 31,

2021 | | March 31,

2022 | December 31,

2021 |

| Credit facility: | | | | | |

| Revolving credit loans | $ | 290,000 | | $ | 260,000 | | | 3.06 | % | 3.27 | % |

| Term loans | 635,938 | | 640,000 | | | 2.93 | % | 3.02 | % |

| Real estate loans | 59,177 | | 59,480 | | | 5.22 | % | 5.22 | % |

| Other debt | 537 | | 1,694 | | | 5.00 | % | 5.00 | % |

| Total debt | 985,652 | | 961,174 | | | 3.11 | % | 3.23 | % |

| Less: Unamortized discount and debt issuance costs | 4,427 | | 4,994 | | | | |

| Less: Debt, current portion | 18,116 | | 18,697 | | | 3.16 | % | 3.11 | % |

| Debt, net of current portion | $ | 963,109 | | $ | 937,483 | | | 3.11 | % | 3.23 | % |

2020 credit facility

In October 2020, we entered into a five-year $900.0 million senior credit facility (the "2020 Credit Facility"). At March 31, 2022, we were in compliance with our debt covenants under the 2020 Credit Facility.

First incremental term loan

In December 2021, we entered into the First Incremental Term Loan Agreement (the "Incremental Amendment"). The Incremental Amendment amended the 2020 Credit Facility and, among other things, provided for a $250.0 million incremental term loan (the “2021 Incremental Term Loan”).

Financing for EVERFI acquisition

On December 31, 2021, we acquired EVERFI for approximately $442.7 million in cash consideration and 3,811,348 shares of the company's common stock, valued at approximately $301.1 million, for an aggregate purchase price of approximately $743.8 million, subject to closing adjustments. We financed the cash consideration and related expenses through cash on hand and new borrowings under the 2020 Credit Facility, including $250.0 million under the 2021 Incremental Term Loan (as defined above).

First amendment to 2020 Credit Facility

On January 31, 2022, we entered into the First Amendment to Credit Agreement (the “Amendment”). The Amendment amended the 2020 Credit Facility to, among other things, (i) modify the definition of “Applicable Margin”, (ii) modify the net leverage ratio financial covenant to require a net leverage ratio of (A) 4.00:1.00 or less for the fiscal quarter ended December 31, 2021 and for fiscal quarters ending thereafter through December 31, 2023 and (B) 3.75:1.00 or less for the fiscal quarters ending March 31, 2024 and thereafter, (iii) reset the $250.0 million fixed dollar basket with respect to the accordion feature and (iv) modify certain negative covenants to provide additional operational flexibility.

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 13 |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Real estate loans

In August 2020, we completed the purchase of our global headquarters facility. As part of the purchase price, we assumed the seller’s obligations under two senior secured notes with a then-aggregate outstanding principal amount of $61.1 million (collectively, the “Real Estate Loans”). At March 31, 2022, we were in compliance with our debt covenants under the Real Estate Loans.

Other debt

From time to time, we enter into third-party financing agreements for purchases of software and related services for our internal use. Generally, the agreements are non-interest-bearing notes requiring annual payments. Interest associated with the notes is imputed at the rate we would incur for amounts borrowed under our then-existing credit facility at the inception of the notes.

The following table summarizes our currently effective financing agreements as of March 31, 2022:

| | | | | | | | | | | | | | |

| (dollars in thousands) | Term

in Months | Number of

Annual Payments | First Annual

Payment Due | Original Loan

Value |

| Effective dates of agreements: | | | | |

| December 2019 | 51 | 4 | | January 2020 | $ | 2,150 | |

| | | | |

| | | | |

| | |

| 9. Derivative Instruments |

Cash flow hedges

We generally use derivative instruments to manage our variable interest rate risk. We have entered into interest rate swap agreements, which effectively convert portions of our variable rate debt under the 2020 Credit Facility to a fixed rate for the term of the swap agreements. We designated each of the interest rate swap agreements as a cash flow hedge at the inception of the contracts.

The terms and notional values of our derivative instruments were as follows as of March 31, 2022:

| | | | | | | | |

| (dollars in thousands) | Term of derivative instrument | Notional

value |

| Derivative instruments designated as hedging instruments: | | |

| Interest rate swap | November 2020 - October 2024 | $ | 60,000 | |

| Interest rate swap | November 2020 - October 2024 | 60,000 | |

| Interest rate swap | June 2021 - October 2024 | 120,000 | |

| Interest rate swap | July 2021 - October 2024 | 120,000 | |

| Interest rate swap | July 2021 - October 2024 | 75,000 | |

| | $ | 435,000 | |

The fair values of our derivative instruments were as follows as of:

| | | | | | | | | | | | | | | |

| | Asset derivatives | | | |

| (dollars in thousands) | Balance sheet location | March 31,

2022 | December 31,

2021 | | | | |

| Derivative instruments designated as hedging instruments: | | | | | | | |

| | | | | | | |

Interest rate swaps, long-term | Other assets | 21,947 | | 7,160 | | | | | |

| Total derivative instruments designated as hedging instruments | | $ | 21,947 | | $ | 7,160 | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | | |

14 | | First Quarter 2022 Form 10-Q |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

The effects of derivative instruments in cash flow hedging relationships were as follows:

| | | | | | | | | | | | | |

| Gain (loss) recognized

in accumulated other

comprehensive

loss as of | Location

of gain (loss)

reclassified from

accumulated other

comprehensive

loss into income | | | Gain (loss) reclassified from accumulated

other comprehensive loss into income |

| (dollars in thousands) | March 31,

2022 | | | Three months ended March 31, 2022 |

| Interest rate swaps | $ | 21,947 | | Interest expense | | | $ | (358) | |

| | | | | |

| March 31,

2021 | | | | Three months ended March 31, 2021 |

| Interest rate swaps | $ | 1,420 | | Interest expense | | | $ | (1,376) | |

Our policy requires that derivatives used for hedging purposes be designated and effective as a hedge of the identified risk exposure at the inception of the contract. Accumulated other comprehensive income (loss) includes unrealized gains or losses from the change in fair value measurement of our derivative instruments each reporting period and the related income tax expense or benefit. Changes in the fair value measurements of the derivative instruments and the related income tax expense or benefit are reflected as adjustments to accumulated other comprehensive income (loss) until the actual hedged expense is incurred or until the hedge is terminated at which point the unrealized gain (loss) is reclassified from accumulated other comprehensive income (loss) to current earnings. The estimated accumulated other comprehensive income as of March 31, 2022 that is expected to be reclassified into earnings within the next twelve months is $5.7 million. There were no ineffective portions of our interest rate swap derivatives during the three months ended March 31, 2022 and 2021. See Note 12 for a summary of the changes in accumulated other comprehensive income (loss) by component.

| | |

| 10. Commitments and Contingencies |

Leases

We have operating leases for corporate offices, subleased offices and certain equipment and furniture. As of March 31, 2022, we did not have any operating leases that had not yet commenced.

The following table summarizes the components of our lease expense:

| | | | | | | | | | | |

| | | Three months ended March 31, |

| (dollars in thousands) | | | | 2022 | 2021 |

Operating lease cost(1) | | | | $ | 2,532 | | $ | 2,841 | |

| Variable lease cost | | | | 437 | | 699 | |

| Sublease income | | | | (431) | | (460) | |

| Net lease cost | | | | $ | 2,538 | | $ | 3,080 | |

(1)Includes short-term lease costs, which were immaterial.

Other commitments

The term loans under the 2020 Credit Facility require periodic principal payments. The balance of the term loans and any amounts drawn on the revolving credit loans are due upon maturity of the 2020 Credit Facility in October 2025. The Real Estate Loans also require periodic principal payments and the balance of the Real Estate Loans are due upon maturity in April 2038.

We have contractual obligations for third-party technology used in our solutions and for other services we purchase as part of our normal operations. In certain cases, these arrangements require a minimum annual purchase commitment by us. As of March 31, 2022, the remaining aggregate minimum purchase commitment under these arrangements was approximately $31.7 million through 2025.

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 15 |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Solution and service indemnifications

In the ordinary course of business, we provide certain indemnifications of varying scope to customers against claims of intellectual property infringement made by third parties arising from the use of our solutions or services. If we determine that it is probable that a loss has been incurred related to solution or service indemnifications, any such loss that could be reasonably estimated would be recognized. We have not identified any losses and, accordingly, we have not recorded a liability related to these indemnifications.

Legal proceedings

We are subject to legal proceedings and claims that arise in the ordinary course of business, as well as certain other non-ordinary course proceedings, claims and inquiries, as described below. We make a provision for a loss contingency when it is both probable that a material liability has been incurred and the amount of the loss can be reasonably estimated. If only a range of estimated losses can be determined, we accrue an amount within the range that, in our judgment, reflects the most likely outcome; if none of the estimates within that range is a better estimate than any other amount, we accrue the low end of the range. For proceedings in which an unfavorable outcome is reasonably possible but not probable and an estimate of the loss or range of losses arising from the proceeding can be made, we disclose such an estimate, if material. If such a loss or range of losses is not reasonably estimable, we disclose that fact. We review any such loss contingency provisions at least quarterly and adjust them to reflect the impacts of negotiations, settlements, rulings, advice of legal counsel and other information and events pertaining to a particular case. We recognize insurance recoveries, if any, when they are probable of receipt. All associated costs due to third-party service providers and consultants, including legal fees, are expensed as incurred.

Legal proceedings are inherently unpredictable. However, we believe that we have valid defenses with respect to the legal matters pending or threatened against us and intend to defend ourselves vigorously against all claims asserted. It is possible that our consolidated financial position, results of operations or cash flows could be materially negatively affected in any particular period by an unfavorable resolution of one or more of such legal proceedings.

Security incident

As previously disclosed, we are subject to risks and uncertainties as a result of a ransomware attack against us in May 2020 in which a cybercriminal removed a copy of a subset of data from our self-hosted environment (the "Security Incident"). Based on the nature of the Security Incident, our research and third party (including law enforcement) investigation, we have no reason to believe that any data went beyond the cybercriminal, was or will be misused, or will be disseminated or otherwise made available publicly. Our investigation into the Security Incident by our cybersecurity team and third-party forensic advisors remains ongoing.

As a result of the Security Incident, we are currently subject to certain legal proceedings, claims, inquiries and investigations, as discussed below, and could be the subject of additional legal proceedings, claims, inquires and investigations in the future that might result in adverse judgments, settlements, fines, penalties, or other resolution. To limit our exposure to losses related to claims against us, including data breaches such as the Security Incident, we maintain $50 million of insurance above a $250 thousand deductible payable by us. As noted below, this coverage has reduced our financial exposure related to the Security Incident, and we will continue to seek recoveries under these insurance policies.

We recorded expenses and offsetting probable insurance recoveries related to the Security Incident as follows:

| | | | | | | | | | | |

| | | Three months ended March 31, |

| (dollars in thousands) | | | | 2022 | 2021 |

| Gross expense | | | | $ | 9,005 | | $ | 12,814 | |

| Offsetting probable insurance recoveries | | | | (1,804) | | (12,813) | |

| Net expense | | | | $ | 7,201 | | $ | 1 | |

| | | | | | | | |

16 | | First Quarter 2022 Form 10-Q |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

The following summarizes our cumulative expenses, probable insurance recoveries and insurance recoveries paid as of:

| | | | | | | | |

| (dollars in thousands) | March 31,

2022 | December 31,

2021 |

| Cumulative gross expense | $ | 59,396 | | $ | 50,391 | |

| Cumulative offsetting insurance recoveries | (49,913) | | (48,109) | |

| Cumulative net expense | $ | 9,483 | | $ | 2,282 | |

| | |

| Cumulative offsetting insurance recoveries paid | $ | (37,277) | | $ | (29,968) | |

Due to the time required to submit and process such insurance claims, we have not yet received all of the accrued insurance recoveries. Recorded expenses consisted primarily of payments for legal fees related to governmental inquiries and investigations and customer constituent class actions. We present expenses and insurance recoveries related to the Security Incident in general and administrative expense on our consolidated statements of comprehensive income and as operating activities on our consolidated statements of cash flows. Total costs related to the Security Incident that we expect will be recoverable exceeded the limit of our insurance coverage during the first quarter of 2022. We expect to continue to experience significant expenses related to our response to the Security Incident, resolution of legal proceedings, claims, inquiries and investigations discussed below, and our efforts to further enhance our security measures. For full year 2022, we currently expect net cash outlays of approximately $25.0 million to $35.0 million for ongoing legal fees related to the Security Incident. In line with our policy as discussed above, legal fees are expensed as incurred.

Based on our analysis of the factors described above, we have not recorded a liability for a loss contingency related to the Security Incident as of March 31, 2022 because we are unable at this time to reasonably estimate the possible loss or range of loss.

Customer claims. To date, we have received approximately 260 specific requests for reimbursement of expenses ("Customer Reimbursement Requests") and approximately 400 reservations of the right to seek expense recovery in the future from customers or their attorneys in the U.S., U.K. and Canada related to the Security Incident (none of which have as yet been filed in court). Of the Customer Reimbursement Requests received to date, approximately 190 have been fully resolved and closed. In addition, insurance companies representing various customers’ interests through subrogation claims have contacted us. One insurance company has filed a subrogation claim in court. Customer and insurer subrogation claims generally seek reimbursement of their costs and expenses associated with notifying their own customers of the Security Incident and taking steps to assure that personal information has not been compromised as a result of the Security Incident. Our review of customer and subrogation claims includes analyzing individual customer contracts into which we have entered, the specific claims made and applicable law.

Customer constituent class actions. Presently, we are a defendant in 19 putative consumer class action cases [17 in U.S. federal courts (which have been consolidated under multi district litigation to a single federal court) and 2 in Canadian courts] alleging harm from the Security Incident. The plaintiffs in these cases, who purport to represent various classes of individual constituents of our customers, generally claim to have been harmed by alleged actions and/or omissions by us in connection with the Security Incident and assert a variety of common law and statutory claims seeking monetary damages, injunctive relief, costs and attorneys’ fees, and other related relief.

Lawsuits that are putative class actions require a plaintiff to satisfy a number of procedural requirements before proceeding to trial. These requirements include, among others, demonstration to a court that the law proscribes in some manner our activities, the making of factual allegations sufficient to suggest that our activities exceeded the limits of the law and a determination by the court—known as class certification—that the law permits a group of individuals to pursue the case together as a class. If these procedural requirements are not met, the lawsuit cannot proceed as a class action and the plaintiff may lose the financial incentive to proceed with the case. Frequently, a court’s determination as to these procedural requirements is subject to appeal to a higher court. As a result of these uncertainties, we may be unable to determine the probability of loss until, or after, a court has finally determined that a plaintiff has satisfied the applicable class action procedural requirements.

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 17 |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Furthermore, for putative class actions, it is often not possible to estimate the possible loss or a range of loss amounts, even where we have determined that a loss is reasonably possible. Generally, class actions involve a large number of people and raise complex legal and factual issues that result in uncertainty as to their outcome and, ultimately, making it difficult for us to estimate the amount of damages that a plaintiff might successfully prove. This analysis is further complicated by the fact that the plaintiffs lack contractual privity with us.

Governmental inquiries and investigations. To date, we have received a consolidated, multi-state Civil Investigative Demand issued on behalf of 49 state Attorneys General and the District of Columbia and a separate Civil Investigative Demand from the office of the California Attorney General relating to the Security Incident. We also are subject to the following pending governmental actions:

•an investigation by the U.S. Federal Trade Commission;

•a formal investigation by the SEC;

•an investigation by the U.S. Department of Health and Human Services;

•an investigation by the Office of the Australian Information Commissioner; and

•an investigation by the Office of the Privacy Commissioner of Canada.

On September 28, 2021, the Information Commissioner's Office in the United Kingdom under the U.K Data Protection Act 2018 (the "ICO") notified us that it has closed its investigation of the Security Incident. Based on its investigation and having considered our actions before, during and after the Security Incident, the ICO issued our European subsidiary a reprimand in accordance with Article 58(2)(b) of the U.K. General Data Protection Regulation ("U.K. GDPR") due to our non-compliance, in the ICO's view, with the requirements set out in Article 32 of the U.K. GDPR regarding the processing of personal data. The ICO did not impose a penalty related to the Security Incident, nor did it impose any requirements for further action by us.

On September 24, 2021, we received notice from the Spanish Data Protection Authority that it has concluded its investigation of the Security Incident, pursuant to which our European subsidiary paid a penalty of €60,000 in relation to the alleged late notification of two Spanish data controllers regarding the Security Incident.

On January 15, 2021, we were notified by the Data Protection Commission of Ireland that it has concluded its investigation of the Security Incident without taking any action against us.

We continue to cooperate with all ongoing inquiries and investigations, which include various requests for documents, policies, narratives and communications, as well as requests to interview or depose various Company-related personnel. As noted above, each of these separate governmental inquiries and investigations could result in adverse judgements, settlements, fines, penalties, or other resolution, the amount, scope and timing of which we are currently unable to predict, but could have a material adverse impact on our results of operations, cash flows, or financial condition.

| | | | | | | | |

18 | | First Quarter 2022 Form 10-Q |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

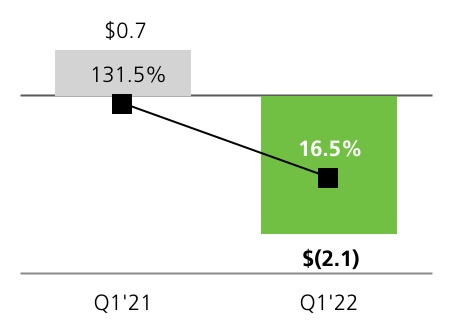

Our income tax (benefit) provision and effective income tax rates, including the effects of period-specific events, were:

| | | | | | | | | | | |

| | | | Three months ended March 31, |

| (dollars in thousands) | | | | 2022 | 2021 |

| Income tax (benefit) provision | | | | $ | (2,050) | | $ | 684 | |

| Effective income tax rate | | | | 16.5 | % | 131.5 | % |

For the three months ended March 31, 2022, we have utilized the discrete effective tax rate method, as allowed by ASC 740-270-30-18, Income Taxes—Interim Reporting, to calculate our interim income tax provision. The discrete method is applied when the application of the estimated annual effective tax rate is impractical because it is not possible to reliably estimate the annual effective tax rate. The discrete method treats the year-to-date period as if it was the annual period and determines the income tax expense or benefit on that basis. We believe that, at this time, the use of this discrete method is more appropriate than the annual effective tax rate method as our full-year forecasted pre-tax income, relative to our forecasted permanent differences, has the potential to distort our estimated annual effective tax rate.

The decrease in our effective income tax rate for the three months ended March 31, 2022 when compared to the same period in 2021 was primarily attributable to the impact of stock based compensation. The 2022 effective tax rate was negatively impacted by increased tax expense attributable to stock based compensation against pre-tax loss for the period.

Changes in accumulated other comprehensive income (loss) by component

The changes in accumulated other comprehensive income (loss) by component, consisted of the following:

| | | | | | | | | | | |

| | | Three months ended March 31, |

| (dollars in thousands) | | | | 2022 | 2021 |

| Accumulated other comprehensive income (loss), beginning of period | | | | $ | 6,522 | | $ | (2,497) | |

| By component: | | | | | |

| Gains and losses on cash flow hedges: | | | | | |

| Accumulated other comprehensive income (loss) balance, beginning of period | | | | $ | 5,257 | | $ | (3,101) | |

| | | | | |

Other comprehensive income (loss) before reclassifications, net of tax effects of $(3,789) and $(1,100) | | | | 10,641 | | 3,130 | |

| Amounts reclassified from accumulated other comprehensive income to interest expense | | | | 358 | | 1,376 | |

| Tax benefit included in provision for income taxes | | | | (94) | | (357) | |

| Total amounts reclassified from accumulated other comprehensive income | | | | 264 | | 1,019 | |

| Net current-period other comprehensive income | | | | 10,905 | | 4,149 | |

| Accumulated other comprehensive income balance, end of period | | | | $ | 16,162 | | $ | 1,048 | |

| Foreign currency translation adjustment: | | | | | |

| Accumulated other comprehensive income balance, beginning of period | | | | $ | 1,265 | | $ | 604 | |

| Translation adjustments | | | | (2,132) | | 2,511 | |

| Accumulated other comprehensive (loss) income balance, end of period | | | | (867) | | 3,115 | |

| Accumulated other comprehensive income, end of period | | | | $ | 15,295 | | $ | 4,163 | |

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 19 |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Transaction price allocated to the remaining performance obligations

As of March 31, 2022, approximately $984 million of revenue is expected to be recognized from remaining performance obligations. We expect to recognize revenue on approximately 60% of these remaining performance obligations over the next 12 months, with the remainder recognized thereafter.

We applied the practical expedient in ASC 606-10-50-14 and have excluded the value of unsatisfied performance obligations for (i) contracts with an original expected length of one year or less (one-time services); and (ii) contracts for which we recognize revenue at the amount to which we have the right to invoice for services performed (transactional revenue).

Contract balances

Our contract assets as of March 31, 2022 and December 31, 2021 were insignificant. Our opening and closing balances of deferred revenue were as follows:

| | | | | | | | |

| (in thousands) | March 31,

2022 | December 31,

2021 |

| Total deferred revenue | $ | 355,677 | | $ | 378,746 | |

The decrease in deferred revenue during the three months ended March 31, 2022 was primarily due to a seasonal decrease in customer contract renewals. Historically, due to the timing of customer budget cycles, we have an increase in customer contract renewals at or near the beginning of our third quarter. Generally, our lowest balance of deferred revenue during the year is at the end of our first quarter. The amount of revenue recognized during the three months ended March 31, 2022 that was included in the deferred revenue balance at the beginning of the period was approximately $152 million. The amount of revenue recognized during the three months ended March 31, 2022 from performance obligations satisfied in prior periods was insignificant.

Disaggregation of revenue

We sell our cloud solutions and related services in three primary geographical markets: to customers in the United States, to customers in the United Kingdom and to customers located in other countries. The following table presents our revenue by geographic area based on the address of our customers:

| | | | | | | | | | | |

| | | Three months ended March 31, |

| (dollars in thousands) | | | | 2022 | 2021 |

| United States | | | | $ | 214,394 | | $ | 185,327 | |

| United Kingdom | | | | 27,660 | | 22,305 | |

| Other countries | | | | 15,070 | | 11,559 | |

| Total revenue | | | | $ | 257,124 | | $ | 219,191 | |

Beginning in the second quarter of 2021, we combined our General Markets Group ("GMG") and Enterprise Markets Group ("EMG") into a single U.S. Markets Group ("UMG") and moved our Corporations vertical under our International Markets Group ("IMG"). This change was made to better align our resources toward customer retention and growth, which are key objectives as we progress toward our long-term aspirational goals.

| | | | | | | | |

20 | | First Quarter 2022 Form 10-Q |

Blackbaud, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

The UMG, IMG and EVERFI comprised our go-to-market organizations as of March 31, 2022. The following is a description of each market group as of that date:

•The UMG focuses on sales primarily to all prospects and customers inside of the U.S.; and

•The IMG focuses on sales primarily to all prospects and customers outside of the U.S, as well as corporations.

•We acquired EVERFI as of December 31, 2021 as discussed in Note 3 to these condensed consolidated financial statements. As we are working to integrate EVERFI into our business, it has not yet been included in one of our market groups.

The following table presents our revenue by market group:

| | | | | | | | | | | |

| | | Three months ended March 31, |

| (dollars in thousands) | | | | 2022 | 2021(1) |

| UMG | | | | $ | 182,489 | | $ | 173,467 | |

IMG | | | | 48,054 | | 45,769 | |

EVERFI | | | | 26,975 | | — | |

| Other | | | | (394) | | (45) | |

| Total revenue | | | | $ | 257,124 | | $ | 219,191 | |

(1)Due to the market group change discussed above, we have recast our revenue by market group for the three months ended March 31, 2021 to present them on a consistent basis with the current year.

The following table presents our recurring revenue by type:

| | | | | | | | | | | |

| | | Three months ended March 31, |

| (dollars in thousands) | | | | 2022 | 2021 |

| Contractual recurring | | | | $ | 174,531 | | $ | 146,821 | |

| Transactional recurring | | | | 70,135 | | 59,929 | |

| Total recurring revenue | | | | $ | 244,666 | | $ | 206,750 | |

| | | | | | | | |

First Quarter 2022 Form 10-Q | | 21 |

Blackbaud, Inc.

(Unaudited)

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS