UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE QUARTERLY PERIOD ENDED

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

COMMISSION FILE NUMBER

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of | (I.R.S. Employer |

(Address of registrant’s principal executive offices, including zip code)

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ⌧

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer | ☐ | |

Smaller reporting company | |||

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ◻

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

The number of outstanding shares of the registrant’s common stock, par value $0.001 per share, as of May 3, 2024, was:

MARINUS PHARMACEUTICALS, INC. AND SUBSIDIARY

INDEX TO FORM 10-Q

FOR THE QUARTER ENDED MARCH 31, 2024

Unless the context otherwise requires, all references in this Quarterly Report on Form 10-Q to the “Company,” “Marinus,” “we,” “us,” and “our” include Marinus Pharmaceuticals, Inc. and its wholly owned subsidiary, Marinus Pharmaceuticals Emerald Limited, an Ireland company.

2

PART I

FINANCIAL INFORMATION

Item 1. Consolidated Financial Statements

MARINUS PHARMACEUTICALS, INC. AND SUBSIDIARY

CONSOLIDATED BALANCE SHEETS

(in thousands, except share and per share amounts)

(unaudited)

March 31, | December 31, | ||||||

2024 | 2023 | ||||||

ASSETS |

|

|

|

| |||

Current assets: | |||||||

Cash and cash equivalents | $ | | $ | | |||

Short-term investments | | | |||||

Accounts receivable, net | | | |||||

Inventory | | | |||||

Prepaid expenses and other current assets |

| |

| | |||

Total current assets |

| |

| | |||

Property and equipment, net |

| |

| | |||

Other assets |

| |

| | |||

Total assets | $ | | $ | | |||

LIABILITIES AND STOCKHOLDERS’ (DEFICIT) EQUITY | |||||||

Current liabilities: | |||||||

Accounts payable | $ | | $ | | |||

Current portion of notes payable | | | |||||

Current portion of revenue interest financing payable | | | |||||

Accrued expenses | | | |||||

Total current liabilities |

| |

| | |||

Notes payable, net of deferred financing costs | | | |||||

Revenue interest financing payable, net of deferred financing costs | | | |||||

Contract liabilities, net | | | |||||

Other long-term liabilities | | | |||||

Total liabilities | | | |||||

Stockholders’ (deficit) equity: | |||||||

Common stock, $ |

| |

| | |||

Additional paid-in capital |

| |

| | |||

Treasury stock at cost, |

|

| |||||

Accumulated other comprehensive loss | — | ( | |||||

Accumulated deficit |

| ( |

| ( | |||

Total stockholders’ (deficit) equity |

| ( |

| | |||

Total liabilities and stockholders’ (deficit) equity | $ | | $ | | |||

See accompanying notes to consolidated financial statements.

3

MARINUS PHARMACEUTICALS, INC. AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(in thousands, except share and per share amounts)

(unaudited)

Three Months Ended March 31, | |||||||

| 2024 |

| 2023 |

| |||

Revenue: |

| ||||||

Product revenue, net |

| $ | |

| $ | | |

Federal contract revenue | | | |||||

Collaboration revenue |

| |

| — | |||

Total revenue | | | |||||

Expenses: | |||||||

Research and development | | | |||||

Selling, general and administrative |

| |

| | |||

Cost of product revenue | | | |||||

Total expenses |

| |

| | |||

Loss from operations |

| ( |

| ( | |||

Interest income |

| |

| | |||

Interest expense |

| ( |

| ( | |||

Other income, net |

| |

| | |||

Net loss applicable to common shareholders | $ | ( | $ | ( | |||

Per share information: | |||||||

Net loss per share of common stock—basic and diluted | $ | ( | $ | ( | |||

Basic and diluted weighted average shares outstanding |

| |

| | |||

Other comprehensive income: | |||||||

Unrealized gain on available-for-sale securities | | | |||||

Total comprehensive loss | $ | ( | $ | ( | |||

See accompanying notes to consolidated financial statements.

4

MARINUS PHARMACEUTICALS, INC. AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

(unaudited)

Three Months Ended March 31, |

| ||||||

2024 | 2023 |

| |||||

Cash flows from operating activities |

|

|

|

| |||

Net loss | $ | ( | $ | ( | |||

Adjustments to reconcile net loss to net cash used in operating activities: | |||||||

Depreciation and amortization |

| |

| | |||

Amortization of debt issuance costs | | | |||||

Accretion of revenue interest financing debt, net of cash paid | | | |||||

Amortization of discount on short-term investments | ( | ( | |||||

Stock-based compensation expense |

| |

| | |||

Amortization of net contract asset/liability | ( | ( | |||||

Noncash lease expense |

| |

| | |||

Noncash lease liability | | | |||||

Write off of fixed assets | — | | |||||

Changes in operating assets and liabilities: | |||||||

Net contract asset/liability |

| |

| | |||

Prepaid expenses and other current assets, non-current assets, inventory and accounts receivable |

| ( |

| ( | |||

Accounts payable and accrued expenses |

| ( |

| ( | |||

Net cash used in operating activities |

| ( |

| ( | |||

Cash flows from investing activities | |||||||

Maturities of short-term investments |

| |

| — | |||

Purchases of short-term investments | — | ( | |||||

Net cash provided by (used in) investing activities |

| |

| ( | |||

Cash flows from financing activities | |||||||

Proceeds from exercise of stock options |

| |

| — | |||

Other cash flows from financing activities | — | ( | |||||

Net cash provided by (used in) financing activities |

| |

| ( | |||

Net decrease in cash and cash equivalents |

| ( |

| ( | |||

Cash and cash equivalents—beginning of period |

| |

| | |||

Cash and cash equivalents—end of period | $ | | $ | | |||

Supplemental disclosure of cash flow information | |||||||

Unrealized gain on short-term investments | $ | | $ | | |||

Cash paid for interest during the period | $ | | $ | | |||

See accompanying notes to consolidated financial statements.

5

MARINUS PHARMACEUTICALS, INC. AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF (DEFICIT) EQUITY

(in thousands)

(unaudited)

Accumulated | ||||||||||||||||||||||||||||

Series A | Additional | Other | Total | |||||||||||||||||||||||||

Convertible Preferred Stock | Common Stock | Paid-in | Treasury Stock | Comprehensive | Accumulated | Stockholders’ | ||||||||||||||||||||||

| Shares |

| Amount |

| Shares |

| Amount |

| Capital |

| Shares |

| Amount |

| Income (Loss) |

| Deficit |

| (Deficit) Equity | |||||||||

Balance, December 31, 2022 | | $ | | | $ | | $ | | | $ | — | $ | — | $ | ( | $ | | |||||||||||

Stock-based compensation expense | — | — | — | — | | — | — | — | — | | ||||||||||||||||||

Net issuance of common stock in connection with the vesting of restricted stock | — | — | | — | — | — | — | — | — | — | ||||||||||||||||||

Unrealized gain on short-term investments | — | — | — | — | — | — | — | | — | | ||||||||||||||||||

Net Loss | — | — | — | — | — | — | — | — | ( | ( | ||||||||||||||||||

Balance, March 31, 2023 |

| | $ | | | $ | | $ | | | $ | — | | $ | ( | $ | | |||||||||||

Balance, December 31, 2023 |

| — | $ | — | | $ | | $ | | | $ | — | $ | ( | $ | ( | $ | | ||||||||||

Stock-based compensation expense | — | — | — | — | | — | — | — | — | | ||||||||||||||||||

Exercise of stock options | — | — | | — | | — | — | — | — | | ||||||||||||||||||

Net issuance of common stock in connection with the vesting of restricted stock | — | — | | — | — | — | — | — | — | — | ||||||||||||||||||

Unrealized gain on short-term investments | — | — | — | — | — | — | — | | — | | ||||||||||||||||||

Net loss | — | — | — | — | — | — | — | — | ( | ( | ||||||||||||||||||

Balance, March 31, 2024 | — | $ | — | | $ | | $ | | | $ | — | $ | — | $ | ( | $ | ( | |||||||||||

See accompanying notes to consolidated financial statements.

6

MARINUS PHARMACEUTICALS, INC. AND SUBSIDIARY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Description of the Business and Liquidity

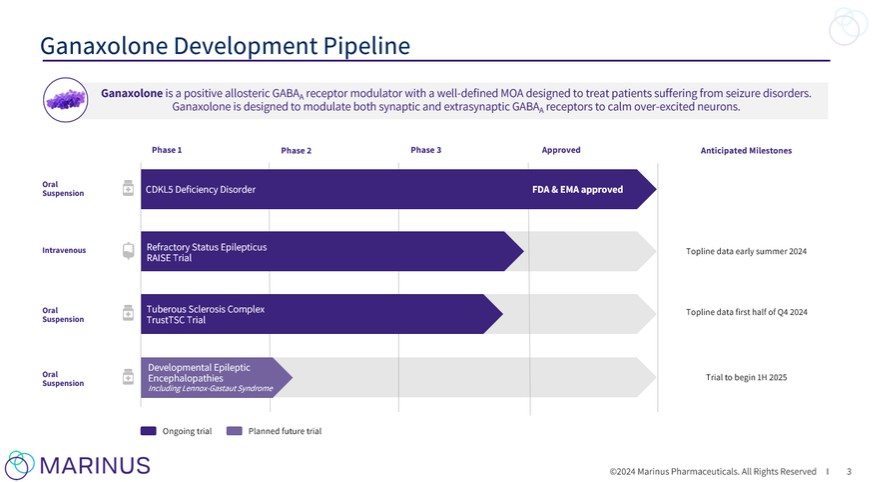

We are a commercial-stage pharmaceutical company dedicated to the development of innovative therapeutics for the treatment of seizure disorders, including rare genetic epilepsies and status epilepticus (SE). On March 18, 2022, the U.S. Food and Drug Administration (FDA) approved our new drug application (NDA) for the use of ZTALMY® (ganaxolone) oral suspension CV for the treatment of seizures associated with Cyclin-dependent Kinase-like 5 (CDKL5) Deficiency Disorder (CDD) in patients two years of age and older. ZTALMY, our first FDA approved product, became available for commercial sale and shipment in the third quarter of 2022. On July 28, 2023, the European Commission (EC) granted marketing authorization for ZTALMY for the adjunctive treatment of epileptic seizures associated with CDD in patients two to 17 years of age. ZTALMY may be continued in patients 18 years of age and older. We have an exclusive collaboration agreement with Orion Corporation (Orion) for European commercialization of ganaxolone for ZTALMY. Orion is preparing for commercial launches of ZTALMY in select European countries in 2024.

We are also developing ganaxolone for the treatment of other rare genetic epilepsies, including Tuberous Sclerosis Complex (TSC), and for the treatment of Refractory Status Epilepticus (RSE). SE is a life-threatening condition characterized by continuous, prolonged seizures or rapidly recurring seizures without intervening recovery of consciousness. If SE is not treated urgently, permanent neuronal damage may occur, which contributes to high rates of morbidity and mortality. Patients with SE who do not respond to first-line benzodiazepine treatment are classified as having Established Status Epilepticus (ESE) and those who then progress to and subsequently fail at least one second-line antiepileptic drug are classified as having RSE.

We are developing ganaxolone in formulations for two different routes of administration: intravenous (IV) and oral. The different formulations are intended to maximize potential therapeutic applications of ganaxolone for adult and pediatric patient populations, in both acute and chronic care. While the precise mechanism by which ganaxolone exerts its therapeutic effects in the treatment of seizures is unknown, its anticonvulsant effects are thought to result from positive allosteric modulation of the gamma-aminobutyric acid type A (GABAA) receptor in the central nervous system (CNS). Ganaxolone is a synthetic analog of allopregnanolone, an endogenous neurosteroid, and targets both synaptic and extrasynaptic GABAA. This unique receptor binding profile may contribute to the anticonvulsant, antidepressant and anxiolytic effects shown by neuroactive steroids in animal models, clinical trials or both.

Liquidity

Since inception, we have incurred negative cash flows from our operations, and other than for the three months ended September 30, 2022 due to a one-time net gain from the sale of our Priority Review Voucher (PRV), we have incurred net losses. We incurred a Net loss of $

We plan to finance our future operations with a combination of proceeds from the issuance of equity securities, the issuance of debt, government funding, collaborations, licensing transactions and other commercial transactions or other sources, and revenues from product sales. We have not generated positive cash flows from operations, and there are no assurances that we will be successful in obtaining an adequate level of financing for the continued development and commercialization of ganaxolone.

Management’s operating plan, which underlies the analysis of our ability to continue as a going concern, involves the estimation of the amount and timing of future cash inflows and outflows. Actual results could vary from the operating plan. We follow the provisions of Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 205-40, Presentation of Financial Statements—Going Concern, which requires management

7

to assess our ability to continue as a going concern within one year after the date the financial statements are issued. We had Cash and cash equivalents and Short-term investments of $

2. Summary of Significant Accounting Policies

Basis of Presentation

The accompanying unaudited interim consolidated financial statements include the accounts of Marinus Pharmaceuticals, Inc. (a Delaware corporation) as well as the accounts of Marinus Pharmaceuticals Emerald Limited (an Ireland company incorporated in February 2021), a wholly owned subsidiary requiring consolidation. Marinus Pharmaceuticals Emerald Limited serves as a corporate presence in the European Union for regulatory purposes. The unaudited interim consolidated financial statements included herein have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission (SEC). Accordingly, they do not include all information and disclosures necessary for a presentation of our financial position, results of operations and cash flows in conformity with generally accepted accounting principles in the U.S. (GAAP) for annual financial statements. In the opinion of management, these unaudited interim consolidated financial statements reflect all adjustments, consisting primarily of normal recurring accruals, necessary for a fair presentation of our financial position and results of operations and cash flows for the periods presented. The results of operations for interim periods are not necessarily indicative of the results for the full year. These unaudited interim consolidated financial statements should be read in conjunction with the audited financial statements for the year ended December 31, 2023 and accompanying notes thereto included in our Annual Report on Form 10-K filed with the SEC on March 5, 2024.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from such estimates.

Product Revenue, net

We recognize ZTALMY revenue in accordance with ASC 606 – Revenue from contracts with customers. Our revenue recognition analysis consists of the following steps: (i) identification of the promised goods in the contract; (ii) determination of whether the promised goods are performance obligations, including whether they are capable of being distinct; (iii) measurement of the transaction price, including the constraint on variable consideration; (iv) allocation of the transaction price to the performance obligations; and (v) recognition of revenue as we satisfy each performance obligation.

Our first FDA approved product, ZTALMY, became available for commercial sale and shipment in the third quarter of 2022. We have

8

ZTALMY revenue includes an estimate of variable consideration. Shipping and handling costs to Orsini are recorded as selling, general and administrative expenses. The components of variable consideration include:

Trade Discounts and Allowances. We provide contractual discounts, including incentive prompt payment discounts and chargebacks. Each of these potential discounts is recorded as a reduction of ZTALMY revenue and Accounts receivable in the period in which the related ZTALMY revenue is recognized. We estimate the amount of variable consideration for all discounts and allowances using the expected value method.

Product Returns and Recall. We provide for ZTALMY returns in accordance with our Return Good Policy. We estimate the amount of ZTALMY that may be returned using the expected value method, and we present this amount as a reduction of ZTALMY revenue in the period the related ZTALMY revenue is recognized. In the event of a recall, we will promptly notify Orsini and will reimburse Orsini for direct administrative expenses incurred in connection with the recall as well as the cost of replacement product.

Government Rebates. We are subject to discount obligations under state Medicaid programs, Medicare and the Tricare Retail Refund Program. We estimate reserves related to these discount programs and record these obligations in the same period the related revenue is recognized, resulting in a reduction of ZTALMY revenue.

Patient Assistance. We offer a voluntary co-pay patient assistance program intended to provide financial assistance to eligible patients with a prescription drug co-payment required by payors and coupon programs for cash payors. The calculation of the Current liability for this assistance is based on an estimate of claims and the cost per claim that we expect to receive associated with ZTALMY that has been recognized as Product revenue but remains in the distribution channel inventories at the end of each reporting period.

Federal Contract Revenue

We recognize Federal contract revenue from the BARDA Contract in the period in which the allowable research and development expenses are incurred, and receivables associated with this revenue are included within Accounts receivable, net on our interim consolidated balance sheets. This revenue is not within the scope of ASC 606 – Revenue from contracts with customers.

Short-term Investments

We classify our Short-term investments as available-for-sale securities, which include U.S. government agency debt securities and U.S. treasury debt securities with original maturities of greater than three months. These securities are carried at fair market value, with unrealized gains and losses reported in Other comprehensive loss and Accumulated other comprehensive income (loss) within stockholders’ equity. All of our investments were short-term in nature as of March 31, 2024.

Accounts Receivable, net

Net trade receivables related to ZTALMY sales, which are recorded in Accounts receivable, net on the consolidated balance sheets, were approximately $

Excluding net trade receivables, Accounts receivable, net represents amounts due to us under the BARDA contract for valid expenditures expected to be reimbursed to us under the terms of the BARDA contract and current amounts due to us from Orion Corporation (Orion) under the collaboration agreement (Note 12).

9

Inventory

Inventories are recorded using actual costs and may consist of raw materials (ganaxolone API), work in process and finished goods. We began capitalizing Inventory related to ZTALMY subsequent to the March 2022 FDA approval of ZTALMY, as the related costs were expected to be recoverable through the commercialization and subsequent sale of ZTALMY. Prior to FDA approval of ZTALMY, costs estimated at approximately $

Debt Issuance Costs

Debt issuance costs incurred in connection with Note payable (Note 10) and Revenue interest financing payable (Note 11) are amortized to Interest expense over the term of the respective financing arrangement using the effective-interest method. Debt issuance costs, net of related amortization, are deducted from the carrying value of the related debt.

Contract Liabilities, net

When consideration is received, or such consideration is unconditionally due, from a customer prior to completing our performance obligation to the customer under the terms of a contract, a Contract liability is recorded. Contract liabilities expected to be recognized as revenue or a reduction of expense within the 12 months following the balance sheet date are classified as Current liabilities. Contract liabilities not expected to be recognized as revenue within the 12 months following the balance sheet date are classified as Long-term liabilities. In accordance with ASC 210-20, our Contract liabilities were partially offset by our Contract assets at March 31, 2024, as further discussed in Note 12.

Liability Related to Revenue Interest Financing and Non-Cash Interest Expense

In October 2022, we recognized a liability related to the Revenue Interest Financing Agreement with Sagard Healthcare Royalty Partners, LP (Sagard) under ASC 470-10 Debt and ASC 835-30 Interest - Imputation of Interest. The initial funds received by us from Sagard pursuant to the terms of the Revenue Interest Financing Agreement were recorded as a liability and will be accreted under the effective interest method upon the estimated amount of future royalty payments to be made pursuant to the Revenue Interest Financing Agreement. The issuance costs were recorded as a direct deduction to the carrying amount of the liability and will be amortized under the effective interest method over the estimated period the liability will be repaid. We estimated the total amount of future product revenue to be generated over the life of the Revenue Interest Financing Agreement, and a significant increase or decrease in these estimates could materially impact the liability balance and the related Interest expense. If the timing or amounts of any estimated future revenue and related payments change, we will prospectively adjust the effective interest and the related amortization of the liability and related issuance costs. The liability related to the Revenue Interest Financing Agreement with Sagard is further discussed in Note 11.

Collaboration and Licensing Revenue

We may enter into collaboration and licensing arrangements for research and development, manufacturing, and commercialization activities with counterparties for the development and commercialization of our product candidates. These arrangements may contain multiple components, such as (i) licenses, (ii) research and development activities, and (iii) the manufacturing of certain material. Payments pursuant to these arrangements may include non-refundable and refundable payments, payments upon the achievement of significant regulatory, development and commercial milestones, sales of product at certain agreed-upon amounts, and royalties on product sales. The amount of variable consideration is constrained until it is probable that the revenue is not at a significant risk of reversal in a future period.

10

In determining the appropriate amount of revenue to be recognized as we fulfill our obligations under a collaboration agreement, we perform the following steps: (i) identification of the promised goods or services in the contract; (ii) determination of whether the promised goods or services are performance obligations, including whether they are capable of being distinct; (iii) measurement of the transaction price, including the constraint on variable consideration; (iv) allocation of the transaction price to the performance obligations; and (v) recognition of revenue as we satisfy each performance obligation.

We must develop estimates and assumptions that require judgment to determine the underlying stand-alone selling price for each performance obligation, which determines how the transaction price is allocated among the performance obligations. The estimation of the stand-alone selling price may include such estimates as forecasted revenues and costs, development timelines, discount rates and probabilities of regulatory and commercial success. We also apply significant judgment when evaluating whether contractual obligations represent distinct performance obligations, allocating transaction price to performance obligations within a contract, determining when performance obligations have been met, assessing the recognition and future reversal of variable consideration and determining and applying appropriate methods of measuring progress for performance obligations satisfied over time.

3. Cash, Cash Equivalents and Short-Term Investments

As of March 31, 2024, our Cash and cash equivalents included $

The following table provides details regarding our portfolio of Short-term investments (in thousands) as of March 31, 2024 and December 31, 2023:

| Amortized Cost |

| Unrealized Gains |

| Unrealized Losses |

| Fair Value | |||||

March 31, 2024 | ||||||||||||

U.S. Treasury securities | $ | | $ | | $ | ( | $ | | ||||

Total | $ | | $ | | $ | ( | $ | | ||||

December 31, 2023 | ||||||||||||

U.S. Treasury securities | $ | | $ | | $ | ( | $ | | ||||

U.S. Government Agency securities | | | ( | | ||||||||

Total | $ | | $ | | $ | ( | $ | | ||||

4. Fair Value Measurements

FASB accounting guidance defines fair value as the price that would be received to sell an asset or paid to transfer a liability (the exit price) in an orderly transaction between market participants at the measurement date. The accounting guidance outlines a valuation framework and creates a fair value hierarchy in order to increase the consistency and comparability of fair value measurements and the related disclosures. In determining fair value, we use quoted prices and observable inputs. Observable inputs are inputs that market participants would use in pricing the asset or liability based on market data obtained from independent sources.

The fair value hierarchy is broken down into three levels based on the source of inputs as follows:

| ● | Level 1 — Valuations based on unadjusted quoted prices in active markets for identical assets or liabilities. |

11

| ● | Level 2 — Valuations based on observable inputs and quoted prices in active markets for similar assets and liabilities. |

| ● | Level 3 — Valuations based on inputs that are unobservable and models that are significant to the overall fair value measurement. |

If the inputs used to measure fair value fall within different levels of the hierarchy, the category level is based on the lowest priority level input that is significant to the fair value measurement of the instrument. As of March 31, 2024 and December 31, 2023, all of our financial assets and liabilities were classified as Level 1 or Level 2 valuations.

We estimate the fair values of our financial instruments categorized as Level 2 in the fair value hierarchy, including U.S. Treasury securities and U.S. Government Agency securities, by taking into consideration valuations obtained from third-party pricing services. The pricing services use industry standard valuation models, including both income- and market-based approaches, for which all significant inputs are observable, either directly or indirectly, to estimate fair value. These inputs include reported trades of and broker/dealer quotes on the same or similar securities, benchmark yields, issuer credit spreads, benchmark securities, and other observable inputs. We obtain a single price for each financial instrument and do not adjust the prices obtained from the pricing service.

The following fair value hierarchy table presents information about each major category of our financial assets and liabilities measured at fair value on a recurring basis (in thousands):

| Level 1 |

| Level 2 |

| Level 3 |

| Total |

| |||||

March 31, 2024 | |||||||||||||

Assets | |||||||||||||

Cash | $ | | $ | — | $ | — | $ | | |||||

Money market funds (cash equivalents) | | — | — | | |||||||||

U.S. Treasury securities | — | | — | | |||||||||

Total assets | $ | | $ | | $ | — | $ | | |||||

December 31, 2023 | |||||||||||||

Assets | |||||||||||||

Cash | $ | | $ | — | $ | — | $ | | |||||

Money market funds (cash equivalents) | | — | — | | |||||||||

U.S. Treasury securities | — | | — | | |||||||||

Agency securities | — | | — | | |||||||||

Total assets | $ | | $ | | $ | — | $ | | |||||

5. Inventory

Inventories are stated at actual costs and consisted of the following (in thousands):

March 31, | December 31, | ||||||

2024 | 2023 | ||||||

Raw materials | $ | | $ | |

| ||

Work in process | | | |||||

Finished goods | | | |||||

Total Inventories | $ | | $ | | |||

12

6. Accrued Expenses

Accrued expenses consisted of the following (in thousands):

March 31, | December 31, | ||||||

2024 | 2023 | ||||||

Payroll and related costs | $ | | $ | |

| ||

Clinical trials and drug development | | | |||||

Accrued license agreement payment | | | |||||

Professional fees | | | |||||

Selling and commercial liabilities | | | |||||

Short-term lease liabilities | | | |||||

Other | | | |||||

Total accrued expenses | $ | | $ | | |||

7. Loss Per Share of Common Stock

Basic loss per share of common stock is computed by dividing Net loss attributable to common stockholders by the Weighted average number of shares of common stock outstanding during each period. Diluted loss per share of common stock includes the effect, if any, from the potential exercise or conversion of securities, such as convertible preferred stock, stock options and unvested restricted stock, which would result in the issuance of incremental shares of common stock. In computing the Basic and diluted net loss per share applicable to common stockholders, the Weighted average number of shares remains the same for both calculations due to the fact that when a Net loss exists, dilutive shares are not included in the calculation. These potentially dilutive securities are more fully described in Note 8.

The pre-funded warrants to purchase common stock issued in connection with the November 2022 offering are included in the calculation of Basic and diluted net loss per share as the exercise price of $

The following potentially dilutive securities have been excluded from the computation of diluted weighted-average shares of common stock outstanding, as they would be anti-dilutive:

Three Months Ended | ||||||

March 31, | ||||||

2024 | 2023 | |||||

Convertible preferred stock | — | |

| |||

Restricted stock awards and restricted stock units | | |

| |||

Stock options | | |

| |||

| |

| ||||

8. Stockholders’ Equity

In 2005, we adopted the 2005 Stock Option and Incentive Plan (2005 Plan) that authorizes us to grant stock options, restricted stock and other equity-based awards. As of March 31, 2024,

Effective August 2014, we adopted our 2014 Equity Incentive Plan, as amended (2014 Plan), that authorizes us to grant stock options, restricted stock, and other equity-based awards, subject to adjustment in accordance with the 2014 Plan. As of March 31, 2024,

13

in connection with the 2014 Plan, and

Stock Options

There were

Restricted Stock and Restricted Stock Units

All issued and outstanding restricted shares of common stock are time-based, and become vested within

During the three months ended March 31, 2024, we granted

Total compensation cost recognized for all stock options, restricted stock awards and restricted stock units in the statements of operations is as follows (in thousands):

Three Months Ended | |||||||

March 31, | |||||||

2024 | 2023 | ||||||

Research and development |

| $ | |

| $ | |

|

Selling, general and administrative |

| |

| | |||

Total | $ | | $ | | |||

Preferred Stock

As of March 31, 2024 all shares of our Series A Convertible Preferred Stock (Preferred Stock) had been converted and

Underwritten Public Offering

In connection with an underwritten public offering in November 2022 and the closing of the related exercise of the underwriters’ option in December 2022, we issued a total of

14

with its affiliates, would beneficially own more than

Sales Pursuant to Equity Distribution Agreement

On July 9, 2020, we entered into an Equity Distribution Agreement (EDA) with JMP Securities LLC (JMP), as amended by the March 31, 2023 Amendment No. 1 to the EDA (Amended EDA), to create an at the market equity program under which we from time to time may offer and sell shares of our common stock without a maximum aggregate offering price. The Amended EDA was entered into in connection with our filing of a Registration Statement on Form S-3 (File No. 333-271041) with the SEC (the 2023 Registration Statement), which includes a prospectus supplement covering the offering, issuance and sale by us of up to $

9. Leases

We have entered into one operating lease for real estate and several operating leases for clinical site equipment. Our real estate operating lease has a term of

As of March 31, 2024 and December 31, 2023, ROU assets were $

Because the rate implicit in each lease is not readily determinable, we use our incremental borrowing rate to determine the present value of the lease payments. The weighted average incremental borrowing rate used to determine the initial value of ROU assets and lease liabilities was

ROU assets for operating leases are periodically reduced by impairment losses. We use the long-lived assets impairment guidance in ASC Subtopic 360-10, Property, Plant, and Equipment – Overall, to determine whether an ROU asset is impaired, and if so, the amount of the impairment loss to recognize. As of March 31, 2024 and December 31, 2023, we have

15

Maturities of operating lease liabilities as of March 31, 2024 were as follows (in thousands):

|

| |||

Remainder of 2024 | $ | | ||

2025 |

| | ||

| ||||

Less: imputed interest | ( | |||

Total lease liabilities | $ | | ||

$ | | |||

| ||||

Total lease liabilities | $ | | ||

10. Notes Payable

On May 11, 2021 (Closing Date) and as amended on May 17, 2021, May 23, 2022 and October 28, 2022 (Credit Agreement), we entered into the Credit Agreement with Oaktree Fund Administration, LLC as administrative agent (Oaktree) and the lenders party thereto (collectively, the Lenders) that provided for a

Upon entering into the Credit Agreement in May 2021, we borrowed $

The Credit Agreement contains a minimum liquidity covenant that requires us to maintain cash and cash equivalents of at least $

The Term Loans will be guaranteed by certain of our future subsidiaries (Guarantors). Our obligations under the Credit Agreement are secured by a pledge of substantially all of our assets and will be secured by a pledge of substantially all of the assets of the Guarantors.

The Term Loans mature on May 11, 2026 (Maturity Date). The Term Loans bear interest at a fixed per annum rate (subject to increase during an event of default) of

16

At the time of borrowing any tranche of the Term Loans, we were required to pay an upfront fee of

We may prepay all or any portion of the Term Loans, and are required to make mandatory prepayments of the Term Loans from the proceeds of asset sales, casualty and condemnation events, and prohibited debt issuances, subject to certain exceptions. All mandatory and voluntary prepayments of the Term Loans are subject to prepayment premiums equal to (i)

In addition, we are required to pay an exit fee in an amount equal to

In addition to the minimum liquidity covenant, we are subject to a number of affirmative and restrictive covenants under the Credit Agreement, including limitations on our ability and our subsidiaries’ abilities, among other things, to incur additional debt, grant or permit additional liens, make investments and acquisitions, merge or consolidate with others, dispose of assets, pay dividends and distributions, and enter into affiliate transactions, subject to certain exceptions. As of March 31, 2024, we were in compliance with all covenants.

Upon the occurrence of certain events, including but not limited to our failure to satisfy our payment obligations under the Credit Agreement, the breach of certain of our other covenants under the Credit Agreement, the occurrence of cross defaults to other indebtedness, or defaults related to enforcement action by the FDA or other Regulatory Authority or recall of ganaxolone, Oaktree and the Lenders will have the right, among other remedies, to accelerate all amounts outstanding under the Term Loans and declare all principal, interest, and outstanding fees immediately due and payable.

In March 2022, we borrowed $

In September 2021, we borrowed $

In May 2021, we borrowed $

For the three months ended March 31, 2024, we recognized interest expense of $

17

The following table summarizes the composition of Notes payable as reflected on the consolidated balance sheet as of March 31, 2024 (in thousands):

Gross proceeds | $ | | |

Contractual exit fee |

| | |

Unamortized debt discount and issuance costs |

| ( | |

Total note payable | $ | | |

Current portion of note payable | | ||

Non-current portion of note payable | | ||

Total note payable | $ | |

The aggregate maturities of Notes payable as of March 31, 2024 are as follows (in thousands):

Remainder of 2024 | $ | | |

2025 | | ||

2026 | | ||

Total | $ | |

11. Revenue Interest Financing Agreement

On October 28, 2022 (Closing Date), we entered into a revenue interest financing agreement (Revenue Interest Financing Agreement) with Sagard Healthcare Royalty Partners, LP (Sagard) pursuant to which we received $

In exchange for the Investment Amount, we have agreed to make quarterly payments to Sagard (Payments) as follows: (i) for each calendar quarter from and after the Closing Date through and including the quarter ended June 30, 2026, an amount equal to

The Payments are subject to a hard cap equal to

If Sagard has not received aggregate payments equaling at least

The obligations under the Revenue Interest Financing Agreement, including the Payments, will be guaranteed by certain of our future subsidiaries that are required to become a party thereto as guarantors (Guarantors). Our obligations under the Revenue Interest Financing Agreement and the guarantee of such obligations are secured, subject to customary permitted liens and other agreed upon exceptions and subject to an intercreditor agreement with Oaktree as administrative agent for the lenders under our credit agreement (as described below, the Credit Agreement), by a pledge of substantially all of our and the Guarantors’ assets that relate to, or are used or held for use for, the development, manufacture, use and/or

18

commercialization of ZTALMY and all other pharmaceutical products that contain ganaxolone in the U.S., including the Product Revenue, pursuant to the terms of the Security Agreement dated as of the Closing Date by and among us, the Guarantors from time to time party thereto, and Sagard (Security Agreement).

At any time, we have the right, but not the obligation (Call Option), to repurchase all, but not less than all, of Sagard’s interest in the Payments at a repurchase price (Put/Call Price) equal to: (a) on or before the third anniversary of the Closing Date,

The Revenue Interest Financing Agreement contains certain restrictions on our and our subsidiaries’ abilities, among other things, to incur additional debt, grant or permit additional liens, make investments and acquisitions, dispose of assets, pay dividends and distributions and enter into affiliate transactions, in each case, subject to certain exceptions. In addition, the Revenue Interest Financing Agreement contains a financial covenant that requires us to maintain at all times cash and cash equivalents in certain deposit accounts in an amount at least equal to (i) from the Closing Date until the repayment of the loans under the Credit Agreement, $

In connection with the Revenue Interest Financing Agreement, on the Closing Date, we entered into the Credit Agreement Amendment with Oaktree which is fully described in Note 10.

Issuance costs pursuant to the Revenue Interest Financing Agreement consisted primarily of advisory and and totaled $

19

The following table summarizes the activity of the Revenue Interest Financing Agreement for the three months ended March 31, 2023 and March 31, 2024 (in thousands):

For the three months ended March 31, 2023 | ||||

Revenue Interest Financing Balance at December 31, 2022 | $ | | ||

Non-cash interest expense in the three months ended March 31, 2023 | | |||

Amortization of debt discount in the three months ended March 31, 2023 | | |||

Payments made in the three months ended March 31, 2023 | ( | |||

Revenue Interest Financing Balance at March 31, 2023 | $ | | ||

Current portion of revenue interest financing liability | | |||

Long-term portion of revenue interest financing liability | | |||

Revenue Interest Financing Balance at March 31, 2023 | $ | | ||

For the three months ended March 31, 2024 | ||||

Revenue Interest Financing Balance at December 31, 2023 | $ | | ||

Non-cash interest expense in the three months ended March 31, 2024 | | |||

Amortization of debt discount in the three months ended March 31, 2024 | | |||

Payments made in the three months ended March 31, 2024 | ( | |||

Revenue Interest Financing Balance at March 31, 2024 | $ | | ||

Current portion of revenue interest financing liability | $ | | ||

Long-term portion of revenue interest financing liability | | |||

Revenue Interest Financing Balance at March 31, 2024 | $ | |

12. Collaboration Revenue

Orion Collaboration Agreement

In July 2021, we entered into a collaboration agreement (Orion Collaboration Agreement) with Orion. The Orion Collaboration Agreement falls under the scope of ASC Topic 808, Collaborative Arrangements (ASC 808) as both parties are active participants in the arrangement that are exposed to significant risks and rewards. While this arrangement is in the scope of ASC 808, we analogize to ASC 606 for some aspects of this arrangement, including for the delivery of a good or service (i.e., a unit of account). Revenue recognized by analogizing to ASC 606 is recorded as collaboration revenue on the consolidated statements of operations.

Under the terms of the Orion Collaboration Agreement, we granted Orion an exclusive, royalty-bearing, sublicensable license to certain of our intellectual property rights with respect to commercializing biopharmaceutical products incorporating our product candidate ganaxolone (Licensed Products) in the European Economic Area, the United Kingdom and Switzerland (collectively, the Territory) for the diagnosis, prevention and treatment of certain human diseases, disorders or conditions (Field), initially in the indications of CDD, TSC and RSE. We will be responsible for the continued development of Licensed Products and regulatory interactions related thereto, including conducting and sponsoring all clinical trials, provided that Orion may conduct certain post-approval studies in the Territory. Orion will be responsible, at Orion’s sole cost and expense, for the commercialization of any Licensed Product in the Field in the Territory.

Under the terms of the Orion Collaboration Agreement, we received a €

20

we would have been required to refund Orion

The Orion Collaboration Agreement shall remain effective until the date of expiration of the last to expire Royalty Term, which is defined as the period beginning on the date of the first commercial sale Licensed Product in such country and ending on the latest to occur of (a) the tenth (10th) anniversary of the first commercial sale of Licensed Product in such country, (b) the expiration of the last-to-expire licensed patent covering the manufacture, use or sale of such Licensed Product in such country, and (c) the expiration of regulatory exclusivity period, if any, for such Licensed Product in such country. The Orion Collaboration Agreement has a term of at least ten () years since a commercial sale has yet to occur. The Orion Collaboration Agreement allows for termination in certain specific events, such as material breach, in the event Orion challenges the validity, enforceability or scope of the licensed patent rights, termination for forecast failure, insolvency and force majeure, none of which are probable at contract inception.

In accordance with the guidance, we identified the following commitments under the arrangement: (i) exclusive rights to develop, use, sell, have sold, offer for sale and import any product comprised of Licensed Product (License) (ii) development and regulatory activities (Development and Regulatory Activities), and (iii) requirement to supply Orion with the Licensed Product at an agreed upon price (Supply of Licensed Product). We determined that these three commitments represent distinct performance obligations for purposes of recognizing revenue or reducing expense, which we will recognize such revenue or expense, as applicable, as we fulfill these performance obligations.

At contract inception, we determined that the non-refundable portion of the upfront payment plus the research and development reimbursement constitutes the transaction price as of the outset of the Orion Collaboration Agreement. The refundable portion of the upfront payment and the future potential regulatory and development milestone payments were fully constrained at contract inception as the risk of significant revenue reversal related to these amounts had not yet been resolved. During 2022, the refundable portion of the upfront payment was determined to be included in the transaction price as the final genotoxicity study on the M2 metabolite of ganaxolone was received as described above and the remaining $

The transaction price was allocated to the

As of December 31, 2023, there was a total contract liability of $

21

Transaction Price and Net Contract Liability as of December 31, 2023:

Cumulative Collaboration | ||||||||

Transaction | Revenue Recognized | Contract | ||||||

Price |

| as of December 31, 2023 |

| Liability | ||||

License | $ | | $ | | $ | - | ||

Development and Regulatory Services | | | | |||||

Supply of Licensed Product | | - | | |||||

$ | | $ | | $ | | |||

Less Total Contract Asset | | |||||||

Net Contract Liability | $ | | ||||||

During the three months ended March 31, 2024, we amortized $

Transaction Price and Net Contract Liability as of March 31, 2024:

Cumulative Collaboration | ||||||||

Transaction | Revenue Recognized | Contract | ||||||

Price |

| as of March, 2024 |

| Liability | ||||

License | $ | | $ | | $ | - | ||

Development and Regulatory Services | | | | |||||

Supply of Licensed Product | | - | | |||||

$ | | $ | | $ | | |||

Less Total Contract Asset | | |||||||

Net Contract Liability | $ | | ||||||

We incurred $

Tenacia Collaboration Agreement

On November 16, 2022 (Effective Date), we entered into a Collaboration and Supply Agreement (Tenacia Collaboration Agreement) with Tenacia Biotechnology (Shanghai) Co., Ltd. (Tenacia). The Tenacia Collaboration Agreement falls under the scope of ASC Topic 808, Collaborative Arrangements (ASC 808) as both parties are active participants in the arrangement that are exposed to significant risks and rewards. While this arrangement is in the scope of ASC 808, we analogize to ASC 606 for some aspects of this arrangement, including for the delivery of a good or service (i.e., a unit of account). Revenue recognized by analogizing to ASC 606 is recorded as collaboration revenue on the consolidated statements of operations.

Under the terms of the Tenacia Collaboration Agreement, we granted Tenacia an exclusive, royalty-bearing, sublicensable license to certain of our intellectual property rights to develop, commercialize and otherwise exploit certain products incorporating certain oral and intravenous formulations of our product candidate ganaxolone (Licensed Products) in Mainland China, Hong Kong, Macau and Taiwan (collectively, Territory) for the diagnosis, prevention and treatment of certain human diseases, disorders or conditions (Field), initially for the treatment of cyclin-dependent

22

kinase-like 5 deficiency disorder, tuberous sclerosis complex and SE (including refractory and established SE) (collectively, the Initial Indications). The collaboration can be expanded to include additional indications and formulations of ganaxolone pursuant to a right of first negotiation.

Under the terms of the Tenacia Collaboration Agreement, Tenacia agreed to pay us an upfront cash payment of $

Tenacia will be primarily responsible for the development of Licensed Products in the Territory and regulatory interactions related thereto, including conducting and sponsoring clinical studies in the Field in the Territory to support regulatory filings in the Territory. All regulatory approvals filed by Tenacia in the Territory will be in the name of and owned by us unless otherwise required by applicable law, in which case such regulatory approvals would be in the name of and owned by Tenacia for the benefit of us. We and Tenacia have agreed to enter into clinical and commercial supply agreements pursuant to which we will supply Tenacia with its requirements of Licensed Products necessary for Tenacia to develop and commercialize Licensed Products in the Field in the Territory. The parties entered into the clinical and commercial supply agreement in May 2023. The agreement contains pricing, delivery, acceptance, payment, termination, forecasting, and other terms consistent with the Tenacia Collaboration Agreement, as well as certain quality assurance, indemnification, liability and other standard industry terms. Tenacia will be responsible for, at Tenacia’s sole cost and expense, obtaining regulatory approval and commercializing the Licensed Product in the Field in Mainland China. Tenacia is enrolling patients in our Phase 3 randomized, double blind, placebo-controlled trial (TrustTSC trial) of adjunctive ganaxolone.

The term of the Tenacia Collaboration Agreement extends for so long as royalties are payable anywhere in the Territory. Subject to the terms of the Tenacia Collaboration Agreement, (i) for a specified period of time after the Effective Date, Tenacia may terminate the Tenacia Collaboration Agreement in its entirety for any or no reason upon written notice to us, and (ii) either party may terminate the Tenacia Collaboration Agreement for the other party’s material breach following a cure period or insolvency.

In accordance with the guidance, we identified the following commitments under the arrangement: (i) grant to Tenacia the exclusive rights to develop, commercialize and otherwise exploit Licensed Product in the Field in the Territory (License) and (ii) requirement to supply Tenacia with the Licensed Product at an agreed upon price (Supply of Licensed Product). We determined that these

The transaction price was allocated to the

23

approach and considered several factors including, but not limited to, discount rate, development timeline, regulatory risks, estimated market demand and future revenue potential using an adjusted market approach. The stand-alone selling price of the Supply of Licensed Product was estimated using the expected cost-plus margin approach.

There was no activity during each of the three months ended March 31, 2024 and 2023. The cumulative collaboration revenue recognized as of March 31, 2024 and December 31, 2023 is $

Transaction Price and Net Contract Liability as of March 31, 2024 and December 31, 2023:

Cumulative Collaboration | ||||||||

Transaction | Revenue Recognized | Contract | ||||||

Price |

| as of March 31, 2024 and December 31, 2023 |

| Liability | ||||

License | $ | | $ | | $ | - | ||

Supply of Licensed Product | | - | | |||||

$ | | $ | | $ | | |||

Less Total Contract Asset | | |||||||

Net Contract Liability | $ | | ||||||

We incurred $

Biologix Distribution and Supply Agreement

In May 2023, we entered into an exclusive distribution and supply agreement (Biologix Agreement) with Biologix FZCo (Biologix), whereby Biologix has the right to distribute and sell ganaxolone in Algeria, Bahrain, Egypt, Iraq, Jordan, Kingdom of Saudi Arabia, Kuwait, Lebanon, Libya, Morocco, Oman, Qatar, Tunisia and United Arab Emirates. In exchange for distribution rights, we will be the exclusive supplier of our products to Biologix on terms set forth in the respective agreements in exchange for a negotiated purchase price for the products. Upon execution of the Biologix Agreement, we received an upfront payment of $

13. Subsequent Events

On April 15, 2024, we announced that the independent Data Monitoring Committee (DMC) completed its review of the interim analysis of the RAISE trial. The trial did not meet the pre-defined interim analysis stopping criteria on the co-primary endpoints, and the DMC recommendation was that the RAISE trial may continue without

24

modification. We have decided to complete enrollment in the RAISE trial at

Cost reduction activities are being implemented with expected impact beginning in the second quarter of 2024. On April 30, 2024, we implemented a reduction-in-force (RIF) which impacted approximately

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Cautionary Note Regarding Forward-Looking Statements

This Quarterly Report on Form 10-Q contains forward-looking statements, within the meaning of the U.S. Private Securities Litigation Reform Act of 1995, that involve substantial risks and uncertainties. In some cases, you can identify forward-looking statements by the words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “objective,” “ongoing,” “plan,” “predict,” “project,” “potential,” “should,” “will,” or “would,” and or the negative of these terms, or other comparable terminology intended to identify statements about the future. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from the information expressed or implied by these forward-looking statements. Although we believe that we have a reasonable basis for each forward-looking statement contained in this Quarterly Report on Form 10-Q, we caution you that these statements are based on a combination of facts and factors currently known by us and our expectations of the future, about which we cannot be certain.

The forward-looking statements in this Quarterly Report on Form 10-Q include, among other things, statements about:

| ● | our plans to continue to successfully commercialize ganaxolone in Cyclin-dependent Kinase-like 5 Deficiency Disorder (CDD) in the U.S.; |

| ● | our expectations about the results from the RAISE trial and the top-line data from such trial; |

| ● | our expectations that our cost reduction activities being implemented, with expected impact beginning in the second quarter of 2024, will be sufficient to fund our operating expenses and capital expenditure requirements, as well as maintain the minimum cash balance required under our debt facility, into the first quarter of 2025; |

| ● | our plans to meet our post-approval commitments to the U.S. Food and Drug Administration (FDA) and the European Commission (EC) for ganaxolone; |

| ● | our expectations regarding the commercialization of ganaxolone in the European Union (EU), including the timing thereof; |

| ● | the potential benefits of ganaxolone in indications other than CDD, and our ability to develop ganaxolone for additional indications, including Refractory Status Epilepticus (RSE), Tuberous Sclerosis Complex (TSC) and Lennox Gastaut Syndrome (LGS); |

| ● | the status, timing and results of preclinical studies and clinical trials; |

| ● | the design of and enrollment in clinical trials, availability of data from ongoing clinical trials, expectations for regulatory approvals and the attainment of clinical trial results that will be supportive of regulatory approvals; |

| ● | the timing of seeking marketing approval of ganaxolone in specific additional indications; |

25

| ● | our ability to maintain marketing approval for ganaxolone for CDD and obtain regulatory approval for ganaxolone in other indications; |

| ● | the possibility that we expand the targeted indication footprint and explore new potential formulations of ganaxolone; |

| ● | our estimates of expenses and future revenue and profitability; |

| ● | our estimates regarding our capital requirements and our needs for additional financing; |

| ● | our estimates of the size of the potential markets for ganaxolone; |

| ● | our expectations regarding our collaborations with Orion Corporation (Orion), Tenacia Biotechnology (Shanghai) Co., Ltd. (Tenacia) and Biologix FZCo (Biologix), including the expected amounts and timings of milestone, royalty and other payments, including research and development reimbursement, if applicable, pursuant thereto; |

| ● | our ability to attract collaborators with acceptable development, regulatory and commercial expertise; |

| ● | the benefits and contractual requirements derived from corporate collaborations, license agreements, and other collaborative or acquisition efforts, including those relating to the development and commercialization of ganaxolone; |

| ● | sources of revenue, including expected future sales of ganaxolone for CDD, revenue contributions from our contract (BARDA Contract) with the Biomedical Advanced Research and Development Authority (BARDA), corporate collaborations, license agreements, and other collaborative efforts for the development and commercialization of ganaxolone for CDD and in other indications being developed for ganaxolone; |

| ● | our ability to create and maintain an effective sales and marketing infrastructure where we elect to market and sell ganaxolone directly; |

| ● | the pricing and the timing and amount of reimbursement for ganaxolone; |

| ● | the success of other competing therapies that may become available; |

| ● | the manufacturing capacity and supply for ganaxolone; |

| ● | the possibility that third parties, such as Ovid Therapeutics, Inc. (Ovid), may initiate legal proceedings alleging that we are infringing their intellectual property rights, the outcome of which would be uncertain and could harm our business; |

| ● | the possibility that we expand and diversify our product pipeline through acquisitions of additional drug candidates that fit our business strategy; |

| ● | our ability to maintain and protect our intellectual property rights; |

| ● | our results of operations, financial condition, liquidity, prospects, and growth strategies; |

| ● | our ability to, among other actions, secure additional financing or strategic transactions and continue as a going concern; |

26

| ● | the enforceability of the exclusive forum provisions in our fourth amended and restated certificate of incorporation; and |

| ● | the industry in which we operate and trends which may affect the industry or us. |

You should refer to Part II Item 1A. Risk Factors of this Quarterly Report on Form 10-Q and Part I Item 1A. Risk Factors of our Annual Report on Form 10-K filed with the Securities and Exchange Commission (SEC) on March 5, 2024 for a discussion of important factors that may cause our actual results to differ materially from those expressed or implied by our forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this Quarterly Report on Form 10-Q will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame or at all. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

You should read this Quarterly Report on Form 10-Q and the documents that we reference in this Quarterly Report on Form 10-Q and have filed as exhibits to this Quarterly Report on Form 10-Q completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations should be read in conjunction with: (i) the interim consolidated financial statements and related notes thereto, which are included in this Quarterly Report on Form 10-Q; and (ii) our annual consolidated financial statements for the year ended December 31, 2023, which are included in our Annual Report on Form 10-K filed with the SEC on March 5, 2024.

Overview

We are a commercial-stage pharmaceutical company dedicated to the development of innovative therapeutics for the treatment of seizure disorders, including rare genetic epilepsies and status epilepticus (SE). On March 18, 2022, the U.S. Food and Drug Administration (FDA) approved our new drug application (NDA) for the use of ZTALMY® (ganaxolone) oral suspension CV for the treatment of seizures associated with Cyclin-dependent Kinase-like 5 (CDKL5) Deficiency Disorder (CDD) in patients two years of age and older. ZTALMY, our first FDA approved product, became available for commercial sale and shipment in the third quarter of 2022. On July 28, 2023, the European Commission (EC) granted marketing authorization for ZTALMY for the adjunctive treatment of epileptic seizures associated with CDD in patients two to 17 years of age. ZTALMY may be continued in patients 18 years of age and older. We have an exclusive collaboration agreement with Orion Corporation (Orion) for European commercialization of ganaxolone for ZTALMY. Orion is preparing for commercial launches of ZTALMY in select European countries in 2024.

We are also developing ganaxolone for the treatment of other rare genetic epilepsies, including Tuberous Sclerosis Complex (TSC), and for the treatment of Refractory Status Epilepticus (RSE). SE is a life-threatening condition characterized by continuous, prolonged seizures or rapidly recurring seizures without intervening recovery of consciousness. If SE is not treated urgently, permanent neuronal damage may occur, which contributes to high rates of morbidity and mortality. Patients with SE who do not respond to first-line benzodiazepine treatment are classified as having Established Status Epilepticus (ESE) and those who then progress to and subsequently fail at least one second-line antiepileptic drug are classified as having RSE.

We are developing ganaxolone in formulations for two different routes of administration: intravenous (IV) and oral. The different formulations are intended to maximize potential therapeutic applications of ganaxolone for adult and pediatric patient populations, in both acute and chronic care. While the precise mechanism by which ganaxolone exerts its therapeutic effects in the treatment of seizures is unknown, its anticonvulsant effects are thought to result from positive allosteric modulation of the gamma-aminobutyric acid type A (GABAA) receptor in the central nervous system (CNS). Ganaxolone is a synthetic analog of allopregnanolone, an endogenous neurosteroid, and targets both synaptic and

27

extrasynaptic GABAA. This unique receptor binding profile may contribute to the anticonvulsant, antidepressant and anxiolytic effects shown by neuroactive steroids in animal models, clinical trials or both.

Our Products and Product Candidates

ZTALMY® (ganaxolone) oral suspension CV

ZTALMY is an oral suspension given three times per day that we have developed for the treatment of CDD-associated seizures. ZTALMY was approved by the FDA in March 2022 for the treatment of seizures associated with CDD in patients two years of age and older. ZTALMY, our first FDA approved product, became available for commercial sale and shipment in the third quarter of 2022. We recorded ZTALMY net product revenue of $7.5 million and $3.3 million for the three months ended March 31, 2024 and 2023, respectively. On July 28, 2023, the EC granted marketing authorization for ZTALMY for the adjunctive treatment of epileptic seizures associated with CDD in patients two to 17 years of age. ZTALMY may be continued in patients 18 years of age and older. With the EC marketing authorization granted for ZTALMY, Orion, our commercialization partner for ZTALMY in Europe, announced it has begun preparations for the launch of ZTALMY, including engaging in the required processes for obtaining pricing and reimbursement approval in the various European countries. The pricing and reimbursement process can be time-consuming and may delay Orion’s commercial launch of ZTALMY in one or more European countries.

CDD is a serious and rare genetic disorder that is caused by a mutation of the CDKL5 gene, located on the X chromosome. CDD is a severely debilitating and potentially fatal genetic condition, which occurs with an estimated frequency of 1:40,000 live births in the U.S. It predominantly affects females and is characterized by early onset, difficult to control seizures and severe neurodevelopmental impairment. The CDKL5 gene encodes proteins essential for normal brain structure and function. Most children affected by CDD have neurodevelopmental deficits such as difficulty walking, talking and taking care of themselves. Many also suffer from scoliosis, gastrointestinal dysfunction or sleep disorders. Genetic testing is available to determine if a patient has a mutation in the CDKL5 gene.

In June 2017, we were granted FDA orphan drug designation for ganaxolone for the treatment of CDD. The designation provides the drug developer with a seven-year period of U.S. marketing exclusivity, tax credits for clinical research costs, the ability to apply for annual grant funding, clinical research trial design assistance and waiver of Prescription Drug User Fee Act filing fees. In July 2020, the FDA granted Rare Pediatric Disease Designation (RPD Designation) for ganaxolone for the treatment of CDD. The FDA grants RPD Designation for diseases that affect fewer than 200,000 people in the U.S. and in which the serious or life-threatening manifestations occur primarily in individuals 18 years of age and younger. Upon FDA approval of ZTALMY for CDD in March 2022, the FDA awarded us a Rare Pediatric Disease Priority Review Voucher (PRV), which we monetized in August 2022 for $110.0 million in cash. In August 2022, we received a letter from Purdue in which Purdue claimed that it was owed $5.5 million by us from the sale of the PRV pursuant to the Purdue License Agreement. We responded to Purdue that we did not agree with their claim. In February 2024, following discussions with Purdue, we agreed to pay Purdue $4 million in respect of its claim. The first $2 million installment was paid to Purdue in March 2024, and the second $2 million installment will be paid on or before June 15, 2024.

In November 2019, the European Medicines Agency’s (EMA) Committee for Orphan Medicinal Products (COMP) granted orphan drug designation for ganaxolone for the treatment of CDD. Prior to the grant of the marketing authorization, the COMP was required to determine whether the orphan drug designation criteria were still met. On May 26, 2023, the COMP provided a positive opinion to maintain the orphan drug designation for ganaxolone for CDD in the EU.

The U.S. and EC approvals of ZTALMY for CDD are based on data from a Phase 3 double-blind placebo-controlled trial (Marigold Trial), in which 101 patients were randomized and treated with ZTALMY. Clinical trial patients receiving ZTALMY showed a median 30.7% reduction in 28-day major motor seizure frequency, compared to a median 6.9% reduction for those receiving placebo, achieving the trial’s primary endpoint (p=0.0036). At two years in the open label extension phase of the Marigold Trial, patients (n=50) treated with ZTALMY experienced a median 48.2% reduction in major motor seizure frequency. These data suggest that patients who remain on treatment long-term may demonstrate continued reductions in seizure frequency. The most common adverse events (AEs) in the double-blind

28

portion of the Marigold Trial were somnolence (36.0% in the ganaxolone group compared to 15.7% in the placebo group), pyrexia (18.0% and 7.8%, respectively) and salivary hypersecretion (6.0% and 2.0%, respectively).

We own families of patents and pending patent applications that claim certain formulations of ganaxolone and cover certain therapeutic uses of ganaxolone, including for treating CDD. The 20-year terms for patents, and applications that issue as patents, in these families run from 2026 through 2042, absent any available patent term adjustments or extensions. We have also licensed from Ovid certain patents that claim certain therapeutic uses of ganaxolone for the treatment of CDD. The licensed patents include a granted U.S. patent, and pending applications in the U.S. and Europe. The 20-year term for these licensed patents and applications that issue as patents will run through 2037, absent any available patent term adjustments.

U.S. Commercial Strategy. Since ZTALMY was approved by the FDA, we have been focused on the implementation and execution of an integrated launch plan to make ZTALMY available to CDD patients in the U.S. through a specialty pharmacy. Key commercial strategies have included and continue to include: (1) executing our supply chain network and quality management system to assure product is available to patients; (2) driving clinical awareness of ZTALMY as the first and only FDA approved product indicated specifically for seizures associated with CDD; (3) deploying our field sales force to target physicians who treat this rare pediatric patient population; (4) engaging commercial and government payers with the objective of obtaining insurance coverage; and (5) enhancing our internal capabilities (such as Finance, Human Resources, Information Technology, Data Analytics and Compliance) to support our first launch as a commercial company.

U.S. Marketing Strategy. Our marketing strategy in the U.S. is to reinforce that seizures are central to the constellation of CDD symptoms, establish ZTALMY as central to the comprehensive management of seizures associated with CDD, and ensure that patients have seamless access to ZTALMY from prescription through fulfillment. Our marketing campaign for ZTALMY is active, and our integrated commercial launch activities initiated in the third quarter of 2022.

U.S. Sales Strategy. Our U.S. commercial sales force includes 16 regional account managers experienced in rare disease. Our field force is targeting identified key accounts and centers of excellence for CDD. Based on our market research, we estimate the addressable patient population for ZTALMY for CDD in the U.S. is approximately 2,000 patients. As this is the first product approved by the FDA specifically for seizures associated with CDD and the International Classification of Diseases, Tenth Revision (ICD10) code for CDD was established in 2021, there is limited data available for this specific market. We have strengthened both our market access and field force teams, and both payer and customer engagement are ongoing.

U.S. Market Access. We have established a payer and reimbursement account team with the objective of obtaining and maintaining reimbursement (coverage) of ZTALMY in the U.S. We are focusing our efforts on reimbursement from commercial payers where pharmacy benefit managers (PBMs) control the majority of commercial pharmacy-benefit lives and government payers, primarily Medicaid for the target population for CDD. We expect approximately 50% of the CDD patient population will access primary coverage through Fee-for-Service or Managed Medicaid, with the remaining approximately 50% accessing primary coverage through commercial payers, with the top PBMs having significant influence. The prescribing and fulfillment process for ZTALMY in the U.S. is managed through ZTALMY One™, a comprehensive patient support program. Enrollment in the program offers various support and information to help caregivers and patients prescribed ZTALMY access their ZTALMY prescription and assist in determining eligibility for and access to co-pay support or free drug programs.

U.S. Specialty Pharmacy. We are utilizing Orsini Pharmaceutical Services, LLC (Orsini), a specialty pharmacy, to provide services for patients in the U.S., including patient enrollment, benefit verification and investigation, prior authorization support, patient education and drug counseling, dispensing of product and shipment coordination.

U.S. Specialty Distributor. We are utilizing ASD Specialty Healthcare, LLC (ASD), a specialty distributor, to provide distribution services in the U.S. in connection with ZTALMY to institutional inpatient pharmacies, U.S. governmental customers, including any Department of Veterans Affairs or Department of Defense sites, and Kaiser Permanente facilities.

29

Infrastructure. We continue to enhance our internal capabilities and processes to support a commercial stage company. We have implemented a healthcare compliance program to guide our compliance with rules and regulations regarding pharmaceutical sales.

Manufacture of Commercial Supply. We have executed commercial supply agreements for ganaxolone active pharmaceutical ingredient (API) with our current manufacturer and also with our current supplier for finished bulk drug product. Additionally, we have executed a master supply agreement with a second API supplier to undertake certain process development activities and, if successful, provide commercial supplies of API and/or API intermediates.

Regulated as a Controlled Substance in the U.S. On June 1, 2022, the Drug Enforcement Agency (DEA) published an interim final rule in the Federal Register placing ganaxolone and its salts in schedule V of the Controlled Substances Act (CSA), which rule became final December 9, 2022. Under the CSA, drugs are classified into five (5) distinct categories or schedules depending upon the drug’s acceptable medical use and the drug’s abuse or dependency potential. Schedule V is defined by the DEA as drugs with lower potential for abuse than schedule IV and consist of preparations containing limited quantities of certain narcotics. ZTALMY became available for commercial sale and shipment in the third quarter of 2022. As a controlled substance, ganaxolone is subject to the applicable CSA requirements such as registration, security, recordkeeping and reporting, storage manufacturing, distribution, importation and other requirements.