As filed with the Securities and Exchange Commission on January 5, 2024

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21421

NEUBERGER BERMAN REAL ESTATE SECURITIES INCOME FUND INC.

(Exact Name of Registrant as specified in charter)

c/o Neuberger Berman Investment Advisers LLC

1290 Avenue of the Americas

New York, New York 10104-0002

New York, New York 10104-0002

(Address of Principal Executive Offices – Zip Code)

Joseph V. Amato

Chief Executive Officer and President

Neuberger Berman Real Estate Securities Income Fund Inc.

c/o Neuberger Berman Investment Advisers LLC

1290 Avenue of the Americas

New York, New York 10104-0002

New York, New York 10104-0002

Lori L. Schneider, Esq.

K&L Gates LLP

1601 K Street, N.W.

Washington, D.C. 20006-1600

(Names and Addresses of agents for service)

Registrant's telephone number, including area code: (212) 476-8800

Date of fiscal year end: October 31

Date of reporting period: October 31, 2023

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders

of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940, as amended (“Act”) (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory,

disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the

collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and

any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-1090. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Report to Stockholders.

(a) Following is a copy of the annual report transmitted to stockholders pursuant to Rule 30e-1 under the Act.

Contents

|

1

|

|

|

2

|

|

|

7

|

|

|

12

|

|

|

16

|

|

|

23

|

|

|

25

|

|

|

26

|

|

|

34

|

|

|

37

|

|

|

38

|

|

|

48

|

|

|

48

|

|

|

49

|

|

|

50

|

The "Neuberger Berman" name and logo and "Neuberger Berman Investment Advisers LLC" name are registered service marks of

Neuberger Berman Group LLC. The individual Fund name in this piece is either a service mark or registered service mark of Neuberger Berman Investment Advisers LLC. ©2023 Neuberger Berman Investment Advisers

LLC. All rights reserved.

President’s Letter

Dear Stockholder,

I am pleased to present this annual report for Neuberger Berman Real Estate Securities Income Fund Inc. (the Fund) for the 12 months

ended October 31, 2023 (the reporting period). The report includes a portfolio commentary, a listing of the Fund’s investments and its audited financial statements for the reporting period.

The Fund seeks to provide high current income with capital appreciation as a secondary objective. To pursue both, we have assembled a

portfolio with a broad mix of equity securities of real estate investment trusts (REITs) and other real estate companies. Our investment approach combines analysis of security fundamentals and real estate with property sector

diversification. Our disciplined valuation methodology seeks real estate company securities that we believe are attractively priced relative to both their historical growth rates and the valuation of other property sectors.

Thank you for your confidence in the Fund. We will continue to do our best to retain your trust in the years to come.

Sincerely,

Joseph V. Amato

President and CEO

Neuberger Berman Real Estate Securities Income Fund Inc.

President and CEO

Neuberger Berman Real Estate Securities Income Fund Inc.

1

Neuberger Berman Real Estate Securities Income Fund Inc.

Portfolio Commentary (Unaudited)

Neuberger Berman Real Estate Securities Income Fund Inc. (the Fund) generated a -0.92% total return on a net asset value (NAV) basis for the 12 months ended October 31, 2023 (the reporting period), outperforming its benchmark, the FTSE Nareit All Equity REITs Index (the Index), which provided a -7.89% total return for the same period. (Fund performance on a market price basis is provided in the table immediately following this commentary.) The use of leverage (typically a performance enhancer in up markets and a detractor during market retreats) detracted from the Fund’s performance during the reporting period.

The overall U.S. equity market has performed well, led by mega-cap growth stocks buoyed by excess liquidity, flows and optimism around

artificial intelligence. Inflation, though sticky, has moderated some. During the September Federal Open Market Committee meeting, the U.S. Federal Reserve Board kept the fed funds rate unchanged at a 22-year high and reiterated a

hawkish economic outlook. The global macro-economic environment has remained resilient as we approach what appears to be the end of major central bank hiking cycles. We believe sticky core inflation will keep interest rates higher for

longer, which could affect economic growth in the coming quarters. All told, the S&P 500® Index returned 10.14% during the reporting period. Comparatively, Real Estate Investment Trusts (REITs), as measured by the Index, declined by -7.89% over the reporting period and underperformed the broad U.S.

equity market.

On average, the Fund had roughly a 34% allocation to REIT preferred shares during the reporting period. We invested in REIT preferred

shares to pursue the Fund’s dual objectives of income generation and capital appreciation. This was additive to both absolute and relative performance as preferred shares, as measured by the FTSE Nareit Preferred Stock Index, returned

4.27% during the reporting period.

Stock selection was additive for performance whereas sector allocation detracted from relative results. From a stock selection

perspective, holdings in the Diversified, Lodging/Resorts, and Self Storage sectors were the most additive to relative performance. On the downside, holdings in the Data Centers, Infrastructure REITs and Gaming REITs sectors detracted

the most from relative returns. In terms of sector positioning, an underweight to Infrastructure REITs and an overweight to Shopping Centers versus the Index were the most beneficial for performance. Conversely, an underweight to Data

Centers and an overweight to Diversified were the largest headwinds for results.

Recently, we have seen a handful of real estate financing deals and a few sizable acquisitions that may signal that real estate market

participants are adjusting to the higher rate environment. Significant discount to NAVs coupled with increasing capital costs have negatively impacted earnings, the transaction market and by extension, values. This has resulted in

M&A activity picking up in the public-to-public space. If real estate transaction markets continue to thaw this could serve as a catalyst to improve investor sentiment.

We believe we are close to the inflection point of the rate hikes. REITs have historically performed well in periods following the

conclusion of rate tightening cycles. Demand for high quality real estate, low leverage, attractive valuations, and demand drivers that lean more defensive should be positive for REITs moving forward, in our view. We continue to focus

on select companies with visible earnings growth opportunities and strong balance sheets that we believe can better withstand increased market volatility.

Sincerely,

Steve Shigekawa and Brian Jones

Portfolio Co-Managers

Portfolio Co-Managers

The portfolio composition, industries and holdings of the Fund are subject to change without notice.

The opinions expressed are those of the Fund's portfolio managers. The opinions are as of the date of this report and are

subject to change without notice.

The value of securities owned by the Fund, as well as the market value of shares of the Fund’s common stock, may decline in

response to certain events, including those directly involving the issuers whose securities are owned by the Fund; conditions affecting the general economy; overall market changes; local, regional, national or global political, social

or economic instability; regulatory or legislative developments; price, currency and interest rate fluctuations, including those resulting from changes in central bank policies; and changes in investor sentiment.

2

Real Estate Securities Income Fund Inc. (Unaudited)

|

TICKER SYMBOL

|

|

|

Real Estate Securities Income

Fund Inc.

|

NRO

|

|

SECTOR ALLOCATION

|

|

|

(as a % of Total Investments*)

|

|

|

Apartments

|

6.4

%

|

|

Data Centers

|

4.4

|

|

Diversified

|

11.3

|

|

Free Standing

|

4.1

|

|

Health Care

|

8.4

|

|

Industrial

|

6.1

|

|

Infrastructure REITs

|

8.9

|

|

Lodging/Resorts

|

4.8

|

|

Manufactured Homes

|

3.3

|

|

Mortgage Commercial Financing

|

4.5

|

|

Mortgage Home Financing

|

2.7

|

|

Office

|

6.3

|

|

Regional Malls

|

4.6

|

|

Self Storage

|

8.2

|

|

Shopping Centers

|

7.9

|

|

Single Family Homes

|

3.1

|

|

Specialty

|

4.5

|

|

Short-Term Investments

|

0.5

|

|

Total

|

100.0

%

|

|

*

|

Does not include the impact of the Fund’s

open positions in derivatives, if any.

|

|

PERFORMANCE HIGHLIGHTS

|

|||||

|

|

Inception

Date

|

Average Annual Total Return

Ended 10/31/2023

|

|||

|

|

1 Year

|

5 Years

|

10 Years

|

Life of Fund

|

|

|

At NAV1

|

|||||

|

Real Estate

Securities

Income

Fund Inc.

|

10/28/2003

|

-0.92%

|

-0.53%

|

2.98%

|

2.90%

|

|

At Market Price2

|

|||||

|

Real Estate

Securities

Income

Fund Inc.

|

10/28/2003

|

-13.15%

|

-1.86%

|

3.01%

|

1.93%

|

|

Index

|

|

|

|

|

|

|

FTSE Nareit All

Equity REITs

Index3

|

|

-7.89%

|

2.69%

|

5.38%

|

7.68%

|

Listed closed-end funds, unlike open-end funds, are not continually offered. Generally, there is an initial public offering and,

once issued, shares of common stock of closed-end funds are sold in the secondary market on a stock exchange.

The performance data quoted represent past performance and do not indicate future results. Current

performance may be lower or higher than the performance data quoted. For current performance data, please visit www.nb.com/cef-performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if

any. The results do not reflect the effect of taxes a stockholder would pay on Fund distributions or on the sale of shares of the Fund’s common stock.

The investment return and market price will fluctuate and shares of the Fund’s common stock may trade at

prices above or below NAV. Shares of the Fund’s common stock, when sold, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not waived a portion of its

investment management fees during certain of the periods shown. The waived fees are from prior years that are no longer disclosed in the Financial Highlights.

3

Real Estate Securities Income Fund Inc. (Unaudited)

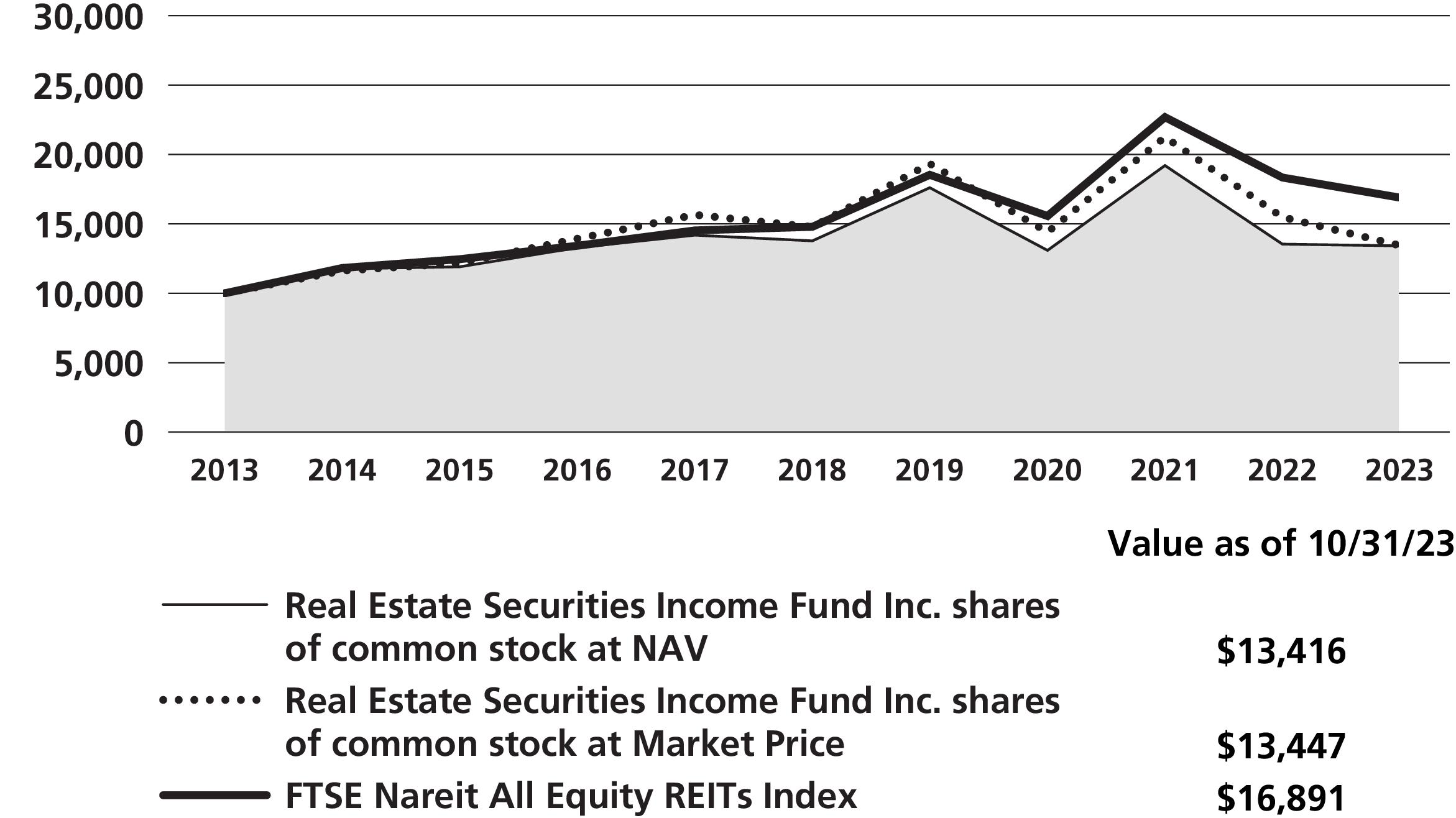

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The graph is based on the

Fund’s shares of common stock both at net asset value (NAV) and at market price. The Fund’s common stock may trade at market prices above or below NAV per share (see Performance Highlights chart). The result is compared with a

broad-based market index. The market index has not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any, at prices

obtained under the Fund’s Distribution Reinvestment Plan. The results do not reflect the effect of taxes a stockholder would pay on Fund distributions or on the sale of Fund shares. Results represent past performance and do not indicate

future results.

Impact of the Fund’s Distribution Policy

The Fund has a practice of seeking to maintain a relatively stable level of distributions to common stockholders. In general,

this practice does not affect the Fund’s investment strategy and may reduce the Fund’s NAV. Management believes the practice helps maintain the Fund’s competitiveness and may benefit the Fund’s market price and its premium/discount to

the Fund’s NAV per share. During the 12-month period ended October 31, 2023, the Fund made distributions to common stockholders totaling $0.37 per share, of which $0.27 will be treated as a return of capital for tax purposes.

4

Endnotes (Unaudited)

|

1

|

Returns based on the NAV of the Fund.

|

|

2

|

Returns based on the market price of shares of the Fund’s common stock on the NYSE American.

|

|

3

|

The FTSE Nareit All Equity REITs Index is a free float-adjusted, market capitalization-weighted

index that

tracks the performance of U.S. equity real estate investment trusts (REITs) that are listed on

the New York

Stock Exchange or NASDAQ. Equity REITs include all tax qualified REITs with more than 50% of

total assets

in qualifying real estate assets other than mortgages secured by real property that also meet

minimum size

and liquidity criteria. Please note that the index does not take into account any fees and

expenses or any

tax consequences of investing in the individual securities that it tracks and that individuals

cannot invest

directly in any index. Data about the performance of this index are prepared or obtained by NBIA

and

include reinvestment of all income dividends and other distributions, if any. The Fund may

invest in

securities not included in the index and generally does not invest in all securities included in

the index.

|

For more complete information on Neuberger Berman Real Estate Securities Income Fund Inc., call Neuberger Berman Investment Advisers LLC at

(877) 461-1899, or visit our website at www.nb.com.

5

Legend October 31, 2023 (Unaudited)

Neuberger Berman Real Estate Securities Income Fund Inc.

|

Benchmarks:

|

|

|

LIBOR

|

= London Interbank Offered Rate

|

|

SOFR

|

= Secured Overnight Financing Rate

|

|

Other Abbreviations:

|

|

|

Management or NBIA

|

= Neuberger Berman Investment Advisers LLC

|

6

Schedule of Investments Real Estate Securities Income Fund Inc.^

October 31, 2023

|

Number of Shares

|

Value

|

|

|

Common Stocks 84.9%

|

||

|

Apartments 8.7%

|

||

|

128,015

|

Apartment Income REIT Corp.

|

$3,739,318

(a)

|

|

83,290

|

Equity Residential

|

4,608,436

(a)

|

|

18,572

|

Essex Property Trust, Inc.

|

3,972,922

(a)

|

|

|

|

12,320,676

|

|

Data Centers 4.3%

|

||

|

30,507

|

Digital Realty Trust, Inc.

|

3,793,851

(a)

|

|

3,288

|

Equinix, Inc.

|

2,399,056

(a)

|

|

|

|

6,192,907

|

|

Diversified 1.3%

|

||

|

35,600

|

WP Carey, Inc.

|

1,909,940

|

|

Free Standing 2.3%

|

||

|

68,724

|

Realty Income Corp.

|

3,256,143

(a)

|

|

Health Care 11.3%

|

||

|

163,023

|

Omega Healthcare Investors, Inc.

|

5,396,061

(a)

|

|

79,984

|

Ventas, Inc.

|

3,396,121

(a)

|

|

86,564

|

Welltower, Inc.

|

7,237,616

(a)

|

|

|

|

16,029,798

|

|

Industrial 8.2%

|

||

|

91,719

|

Prologis, Inc.

|

9,240,689

(a)

|

|

74,533

|

STAG Industrial, Inc.

|

2,475,986

(a)

|

|

|

|

11,716,675

|

|

Infrastructure REITs 12.0%

|

||

|

56,976

|

American Tower Corp.

|

10,152,553

(a)

|

|

74,315

|

Crown Castle, Inc.

|

6,909,809

(a)

|

|

|

|

17,062,362

|

|

Manufactured Homes 4.0%

|

||

|

50,316

|

Equity LifeStyle Properties, Inc.

|

3,310,793

|

|

21,118

|

Sun Communities, Inc.

|

2,349,166

(a)

|

|

|

|

5,659,959

|

|

Mortgage Commercial Financing 5.7%

|

||

|

182,043

|

Blackstone Mortgage Trust, Inc. Class A

|

3,631,758

(a)

|

|

252,347

|

Starwood Property Trust, Inc.

|

4,479,159

(a)

|

|

|

|

8,110,917

|

|

Mortgage Home Financing 3.6%

|

||

|

308,541

|

AGNC Investment Corp.

|

2,277,033

|

|

182,510

|

Annaly Capital Management, Inc.

|

2,848,981

(a)

|

|

|

|

5,126,014

|

|

Office 1.6%

|

||

|

123,776

|

Highwoods Properties, Inc.

|

2,214,353

(a)

|

|

Regional Malls 6.2%

|

||

|

80,260

|

Simon Property Group, Inc.

|

8,819,771

(a)

|

See Notes to Financial Statements

7

Schedule of Investments Real Estate Securities Income Fund Inc.^ (cont’d)

|

Number of Shares

|

Value

|

|

|

Self Storage 3.3%

|

||

|

19,493

|

Public Storage

|

$4,653,174

(a)

|

|

Shopping Centers 4.9%

|

||

|

161,017

|

Kimco Realty Corp.

|

2,888,645

(a)

|

|

180,020

|

Tanger Factory Outlet Centers, Inc.

|

4,059,451

(a)

|

|

|

|

6,948,096

|

|

Single Family Homes 1.8%

|

||

|

47,463

|

American Homes 4 Rent Class A

|

1,553,939

(a)

|

|

31,858

|

Invitation Homes, Inc.

|

945,864

|

|

|

|

2,499,803

|

|

Specialty 5.7%

|

||

|

76,757

|

Iron Mountain, Inc.

|

4,534,036

(a)

|

|

127,673

|

VICI Properties, Inc. Class A

|

3,562,077

|

|

|

|

8,096,113

|

|

|

||

|

Total Common Stocks (Cost $131,428,150)

|

120,616,701

|

|

|

Preferred Stocks 48.4%

|

||

|

Data Centers 1.7%

|

||

|

38,326

|

Digital Realty Trust, Inc., Series K, 5.85%

|

834,740

(b)

|

|

78,449

|

Digital Realty Trust, Inc., Series L, 5.20%

|

1,528,187

(a)(b)

|

|

|

|

2,362,927

|

|

Diversified 2.4%

|

||

|

75,000

|

Armada Hoffler Properties, Inc., Series A, 6.75%

|

1,514,250

(a)(b)

|

|

80,155

|

Gladstone Commercial Corp., Series G, 6.00%

|

1,349,009

(b)

|

|

29,000

|

Global Net Lease, Inc., Series A, 7.25%

|

497,640

(b)

|

|

|

|

3,360,899

|

|

Free Standing 3.2%

|

||

|

177,350

|

Agree Realty Corp., Series A, 4.25%

|

2,851,788

(a)(b)

|

|

79,444

|

Spirit Realty Capital, Inc., Series A, 6.00%

|

1,762,862

(a)(b)

|

|

|

|

4,614,650

|

|

Lodging/Resorts 6.5%

|

||

|

125,000

|

Ashford Hospitality Trust, Inc., Series G, 7.38%

|

1,538,750

(a)(b)

|

|

181,500

|

Chatham Lodging Trust, Series A, 6.63%

|

3,613,665

(b)

|

|

9,500

|

DiamondRock Hospitality Co., Series A, 8.25%

|

242,060

(a)(b)

|

|

6,000

|

Pebblebrook Hotel Trust, Series E, 6.38%

|

109,800

(b)

|

|

40,100

|

Pebblebrook Hotel Trust, Series G, 6.38%

|

708,166

(b)

|

|

24,000

|

Pebblebrook Hotel Trust, Series H, 5.70%

|

386,160

(a)(b)

|

|

50,620

|

Summit Hotel Properties, Inc., Series E, 6.25%

|

911,160

(a)(b)

|

|

36,990

|

Summit Hotel Properties, Inc., Series F, 5.88%

|

677,287

(b)

|

|

33,000

|

Sunstone Hotel Investors, Inc., Series H, 6.13%

|

682,110

(b)

|

|

20,000

|

Sunstone Hotel Investors, Inc., Series I, 5.70%

|

391,200

(b)

|

|

|

|

9,260,358

|

|

Manufactured Homes 0.5%

|

||

|

34,673

|

UMH Properties, Inc., Series D, 6.38%

|

705,595

(b)

|

|

Mortgage Commercial Financing 0.3%

|

||

|

30,000

|

KKR Real Estate Finance Trust, Inc., Series A, 6.50%

|

489,000

(a)(b)

|

See Notes to Financial Statements

8

Schedule of Investments Real Estate Securities Income Fund Inc.^ (cont’d)

|

Number of Shares

|

Value

|

|

|

Office 6.8%

|

||

|

6,000

|

Highwoods Properties, Inc., Series A, 8.63%

|

$6,201,950

(b)

|

|

8,283

|

SL Green Realty Corp., Series I, 6.50%

|

139,734

(b)

|

|

30,000

|

Vornado Realty Trust, Series L, 5.40%

|

426,300

(b)

|

|

107,100

|

Vornado Realty Trust, Series M, 5.25%

|

1,499,400

(b)

|

|

92,925

|

Vornado Realty Trust, Series N, 5.25%

|

1,319,535

(a)(b)

|

|

9,143

|

Vornado Realty Trust, Series O, 4.45%

|

109,076

(b)

|

|

|

|

9,695,995

|

|

Real Estate Management & Development 10.4%

|

||

|

50,000

|

Brookfield Property Partners LP, Series A, 5.75%

|

490,000

(b)

|

|

35,581

|

DigitalBridge Group, Inc., Series H, 7.13%

|

764,991

(a)(b)

|

|

358,166

|

DigitalBridge Group, Inc., Series I, 7.15%

|

7,525,068

(a)(b)

|

|

288,350

|

DigitalBridge Group, Inc., Series J, 7.13%

|

6,014,981

(a)(b)

|

|

|

|

14,795,040

|

|

Regional Malls 0.0%(c)

|

||

|

46,942

|

Pennsylvania Real Estate Investment Trust, Series C, 7.20%

|

13,848

*(b)

|

|

Self Storage 7.8%

|

||

|

10,100

|

National Storage Affiliates Trust, Series A, 6.00%

|

211,191

(b)

|

|

31,050

|

Public Storage, Series H, 5.60%

|

689,000

(b)

|

|

29,000

|

Public Storage, Series I, 4.88%

|

570,140

(b)

|

|

33,176

|

Public Storage, Series J, 4.70%

|

610,770

(a)(b)

|

|

102,000

|

Public Storage, Series K, 4.75%

|

1,906,380

(a)(b)

|

|

80,793

|

Public Storage, Series L, 4.63%

|

1,494,670

(a)(b)

|

|

31,700

|

Public Storage, Series M, 4.13%

|

520,197

(a)(b)

|

|

25,000

|

Public Storage, Series O, 3.90%

|

386,250

(a)(b)

|

|

118,790

|

Public Storage, Series P, 4.00%

|

1,875,694

(a)(b)

|

|

19,775

|

Public Storage, Series Q, 3.95%

|

305,524

(b)

|

|

154,200

|

Public Storage, Series S, 4.10%

|

2,490,330

(a)(b)

|

|

|

|

11,060,146

|

|

Shopping Centers 5.8%

|

||

|

30,813

|

Cedar Realty Trust, Inc., Series C, 6.50%

|

316,450

(b)

|

|

55,600

|

Federal Realty Investment Trust, Series C, 5.00%

|

1,106,440

(b)

|

|

23,369

|

Kimco Realty Corp., Series L, 5.13%

|

448,685

(b)

|

|

56,425

|

Kimco Realty Corp., Series M, 5.25%

|

1,129,064

(a)(b)

|

|

9,000

|

Regency Centers Corp., Series A, 6.25%

|

207,540

(b)

|

|

122,250

|

Regency Centers Corp., Series B, 5.88%

|

2,636,932

(b)

|

|

58,523

|

Saul Centers, Inc., Series E, 6.00%

|

1,188,017

(a)(b)

|

|

62,945

|

SITE Centers Corp., Series A, 6.38%

|

1,251,976

(a)(b)

|

|

|

|

8,285,104

|

|

Single Family Homes 2.5%

|

||

|

165,620

|

American Homes 4 Rent, Series G, 5.88%

|

3,534,331

(a)(b)

|

|

Specialty 0.5%

|

||

|

36,008

|

EPR Properties, Series G, 5.75%

|

649,224

(a)(b)

|

|

|

||

|

Total Preferred Stocks (Cost $90,157,408)

|

68,827,117

|

|

See Notes to Financial Statements

9

Schedule of Investments Real Estate Securities Income Fund Inc.^ (cont’d)

|

Number of Units

|

Value

|

|

|

Master Limited Partnerships and Limited Partnerships 1.1%

|

||

|

Real Estate Management & Development 1.1%

|

||

|

129,388

|

Brookfield Property Preferred LP, 6.25% (Cost $3,122,153)

|

$1,552,656

|

|

Number of Shares

|

|

|

|

|

||

|

|

||

|

Short-Term Investments 0.7%

|

||

|

Investment Companies 0.7%

|

||

|

991,323

|

State Street Institutional U.S. Government Money Market Fund Premier Class,

5.30%(d) (Cost $991,323)

|

991,323

|

|

Total Investments 135.1% (Cost

$225,699,034)

|

191,987,797

|

|

|

Liabilities Less Other Assets (35.1)%

|

(49,869,550

)

|

|

|

Net Assets Applicable to Common

Stockholders 100.0%

|

$142,118,247

|

|

|

*

|

Non-income producing security.

|

|

(a)

|

All or a portion of this security is pledged with the custodian in connection with the Fund's

loans payable

outstanding.

|

|

(b)

|

Perpetual security. Perpetual securities have no stated maturity date, but they may be

called/redeemed by

the issuer.

|

|

(c)

|

Represents less than 0.05% of net assets of the Fund.

|

|

(d)

|

Represents 7-day effective yield as of October 31, 2023.

|

See Notes to Financial Statements

10

Schedule of Investments Real Estate Securities Income Fund Inc.^ (cont’d)

The following is a summary, categorized by Level (see Note A of the Notes to Financial Statements), of inputs used to value the Fund’s investments as of

October 31, 2023:

|

Asset Valuation Inputs

|

Level 1

|

Level 2

|

Level 3(a)

|

Total

|

|

Investments:

|

|

|

|

|

|

Common Stocks#

|

$120,616,701

|

$—

|

$—

|

$120,616,701

|

|

Preferred Stocks

|

|

|

|

|

|

Office

|

3,494,045

|

6,201,950

|

—

|

9,695,995

|

|

Other Preferred Stocks#

|

59,131,122

|

—

|

—

|

59,131,122

|

|

Total Preferred Stocks

|

62,625,167

|

6,201,950

|

—

|

68,827,117

|

|

Master Limited Partnerships and Limited Partnerships#

|

1,552,656

|

—

|

—

|

1,552,656

|

|

Short-Term Investments

|

—

|

991,323

|

—

|

991,323

|

|

Total Investments

|

$184,794,524

|

$7,193,273

|

$—

|

$191,987,797

|

|

#

|

The Schedule of Investments provides information on the industry or sector

categorization.

|

|

(a)

|

The following is a reconciliation between the beginning and ending balances

of investments in which

significant unobservable inputs (Level 3) were used in determining value:

|

|

(000's

omitted)

|

Beginning

balance as

of 11/1/2022

|

Accrued

discounts/

(premiums)

|

Realized

gain/(loss)

|

Change

in unrealized

appreciation/

(depreciation)

|

Purchases

|

Sales

|

Transfers

into

Level 3

|

Transfers

out of

Level 3

|

Balance

as of

10/31/2023

|

Net change in

unrealized

appreciation/

(depreciation)

from

investments

still held as of

10/31/2023

|

|

Investments in Securities:

|

||||||||||

|

Preferred Stocks(1)

|

$6,367

|

$—

|

$—

|

$(165

)

|

$—

|

$—

|

$—

|

$(6,202

)

|

$—

|

$—

|

|

Total

|

$6,367

|

$—

|

$—

|

$(165

)

|

$—

|

$—

|

$—

|

$(6,202

)

|

$—

|

$—

|

|

(1) At the beginning of the year, these securities were valued in accordance with procedures approved by

the valuation designee. The Fund held no Level 3 investments at October 31, 2023.

|

||||||||||

^

A balance indicated with a "—", reflects either a zero balance or an amount that rounds to less than 1.

See Notes to Financial Statements

11

Statement of Assets and Liabilities

Neuberger Berman

|

|

Real Estate

Securities Income

Fund Inc.

|

|

|

October 31, 2023

|

|

Assets

|

|

|

Investments in securities, at value* (Note

A)—see Schedule of Investments:

|

|

|

Unaffiliated issuers(a)

|

$191,987,797

|

|

Dividends and interest receivable

|

249,419

|

|

Prepaid offering costs (Note A)

|

350,024

|

|

Prepaid expenses and other assets

|

3,357

|

|

Total Assets

|

192,590,597

|

|

Liabilities

|

|

|

Loans payable (Note A)

|

50,000,000

|

|

Distributions payable—common stock

|

59,985

|

|

Payable to investment manager (Note B)

|

102,023

|

|

Payable to administrator (Note B)

|

42,510

|

|

Payable to directors

|

3,367

|

|

Interest payable (Note A)

|

139,248

|

|

Other accrued expenses and payables

|

125,037

|

|

Total Liabilities

|

50,472,170

|

|

Net Assets applicable to Common Stockholders

|

$142,118,427

|

|

Net Assets applicable to Common Stockholders consist of:

|

|

|

Paid-in capital—common stock

|

$199,459,993

|

|

Total distributable earnings/(losses)

|

(57,341,566

)

|

|

Net Assets applicable to Common Stockholders

|

$142,118,427

|

|

Shares of Common Stock Outstanding ($0.0001 par value; 999,978,880 shares

authorized)

|

47,455,806

|

|

Net Asset Value Per Share of Common Stock Outstanding

|

$2.99

|

|

*Cost of Investments:

|

|

|

(a) Unaffiliated issuers

|

$225,699,034

|

|

|

See Notes to Financial Statements

12

Statement of Operations

Neuberger Berman

|

|

Real Estate

Securities Income

Fund Inc.

|

|

|

For the Fiscal

Year Ended

October 31,

2023

|

|

Investment Income:

|

|

|

Income (Note A):

|

|

|

Dividend income—unaffiliated issuers

|

$9,699,277

|

|

Interest and other income—unaffiliated issuers

|

298,691

|

|

Foreign taxes withheld

|

(6,872

)

|

|

Total income

|

$9,991,096

|

|

Expenses:

|

|

|

Investment management fees (Note B)

|

1,329,636

|

|

Administration fees (Note B)

|

554,015

|

|

Audit fees

|

50,710

|

|

Custodian and accounting fees

|

47,655

|

|

Insurance

|

6,498

|

|

Legal fees

|

149,864

|

|

Stockholder reports

|

51,724

|

|

Stock exchange listing fees

|

7,132

|

|

Stock transfer agent fees

|

15,621

|

|

Directors' fees and expenses

|

49,235

|

|

Interest

|

2,585,139

|

|

Miscellaneous and other fees

|

8,745

|

|

Total expenses

|

4,855,974

|

|

Net investment income/(loss)

|

$5,135,122

|

|

Realized and Unrealized Gain/(Loss) on Investments (Note A):

|

|

|

Net realized gain/(loss) on:

|

|

|

Transactions in investment securities of unaffiliated issuers

|

(4,443,388

)

|

|

Change in net unrealized appreciation/(depreciation) in

value of:

|

|

|

Investment securities of unaffiliated issuers

|

(1,931,362

)

|

|

Net gain/(loss) on investments

|

(6,374,750

)

|

|

Net increase/(decrease) in net assets applicable to Common Stockholders

resulting from operations

|

$(1,239,628

)

|

See Notes to Financial Statements

13

Statements of Changes in Net Assets

Neuberger Berman

|

|

Real Estate Securities

Income Fund Inc.

|

|

|

|

Fiscal Year Ended

|

Fiscal Year Ended

|

|

|

October 31, 2023

|

October 31, 2022

|

|

Increase/(Decrease) in Net Assets Applicable to Common Stockholders:

|

|

|

|

From Operations (Note A):

|

|

|

|

Net investment income/(loss)

|

$5,135,122

|

$4,229,355

|

|

Net realized gain/(loss) on investments

|

(4,443,388

)

|

5,661,644

|

|

Change in net unrealized appreciation/(depreciation) of investments

|

(1,931,362

)

|

(80,085,703

)

|

|

Net increase/(decrease) in net assets applicable to Common Stockholders resulting from

operations

|

(1,239,628

)

|

(70,194,704

)

|

|

Distributions to Common Stockholders From (Note A):

|

|

|

|

Distributable earnings

|

(5,116,490

)

|

(5,899,759

)

|

|

Tax return of capital

|

(12,650,964

)

|

(11,864,748

)

|

|

Total distributions to Common Stockholders

|

(17,767,454

)

|

(17,764,507

)

|

|

From Capital Share Transactions (Note D):

|

|

|

|

Proceeds from reinvestment of dividends and distributions

|

—

|

61,655

|

|

Net Increase/(Decrease) in Net Assets Applicable to Common

Stockholders

|

(19,007,082

)

|

(87,897,556

)

|

|

Net Assets Applicable to Common Stockholders:

|

|

|

|

Beginning of year

|

161,125,509

|

249,023,065

|

|

End of year

|

$142,118,427

|

$161,125,509

|

See Notes to Financial Statements

14

Statement of Cash Flows

Neuberger Berman

|

|

Real Estate

Securities Income

Fund Inc.

|

|

|

For the

Fiscal Year Ended

October 31, 2023

|

|

Increase/(Decrease) in cash:

|

|

|

Cash flows from operating activities:

|

|

|

Net decrease in net assets applicable to Common Stockholders resulting from operations

|

$(1,239,628

)

|

|

Adjustments to reconcile net increase in net assets applicable to Common Stockholders

resulting from

operations to net cash provided by operating activities:

|

|

|

Changes in assets and liabilities:

|

|

|

Purchase of investment securities

|

(14,778,883

)

|

|

Proceeds from disposition of investment securities

|

36,648,970

|

|

Purchase/sale of short-term investment securities, net

|

926,846

|

|

Increase in prepaid offering costs

|

(350,024

)

|

|

Decrease in dividends and interest receivable

|

10,294

|

|

Decrease in prepaid expenses and other assets

|

2,311

|

|

Decrease in receivable for securities sold

|

185,683

|

|

Increase in interest payable

|

43,926

|

|

Decrease in payable to investment manager

|

(14,746

)

|

|

Decrease in payable to directors

|

(9,884

)

|

|

Decrease in payable to administrator

|

(6,144

)

|

|

Decrease in other accrued expenses and payables

|

(23,692

)

|

|

Unrealized depreciation on investment securities of unaffiliated issuers

|

1,931,362

|

|

Net realized loss from transactions in investment securities of unaffiliated issuers

|

4,443,388

|

|

Net cash provided by (used in) operating activities

|

$27,769,779

|

|

Cash flows from financing activities:

|

|

|

Cash distributions paid on common stock

|

(17,769,779

)

|

|

Cash disbursements from repayment of loan

|

(10,000,000

)

|

|

Net cash provided by (used in) financing activities

|

$(27,769,779

)

|

|

Net increase/(decrease) in cash

|

—

|

|

Cash:

|

|

|

Cash and restricted cash at beginning of year

|

—

|

|

Cash and restricted cash at end of year

|

$—

|

|

Supplemental disclosure

|

|

|

Cash paid for interest

|

$2,541,213

|

See Notes to Financial Statements

15

Notes to Financial Statements Real Estate Securities Income Fund Inc.

Note A—Summary of Significant Accounting Policies:

1

General: Neuberger Berman

Real Estate Securities Income Fund Inc. (the "Fund") was organized as a Maryland corporation on August 28, 2003 as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the

"1940 Act"). Under the 1940 Act, the status of a fund that was registered as non-diversified may,

under certain circumstances, change to that of a diversified fund. The Fund is currently a diversified fund. The Fund’s Board of Directors (the "Board") may classify or re-classify any unissued shares of capital stock into one or more classes of preferred stock without the approval of stockholders.

A balance indicated with a "—", reflects either a zero balance or a balance that rounds to less than 1.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of

the Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") Topic 946 "Financial Services—Investment Companies."

The preparation of financial statements in accordance with U.S. generally accepted accounting principles ("GAAP")

requires Management to make estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates.

2

Portfolio valuation: In

accordance with ASC 820 "Fair Value Measurement" ("ASC 820"), all investments held by the Fund are carried at the value that Management believes the Fund would receive upon selling an investment in an orderly transaction to an

independent buyer in the principal or most advantageous market for the investment under current market conditions. Various inputs, including the volume and level of activity for the asset or liability in the market, are considered

in valuing the Fund's investments, some of which are discussed below. At times, Management may need to apply significant judgment to value investments in accordance with ASC 820.

ASC 820 established a three-tier hierarchy of inputs to create a classification of value measurements for disclosure

purposes. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below.

•

Level 1 – unadjusted quoted prices in active markets for identical investments

•

Level 2 – other observable inputs (including quoted prices for similar investments, interest rates,

prepayment speeds, credit risk, amortized cost, etc.)

•

Level 3 – unobservable inputs (including the Fund's own assumptions in determining the fair value of

investments)

The inputs or methodology used for valuing an investment are not necessarily an indication of the risk associated with

investing in those securities.

The value of the Fund’s investments in equity securities, master limited partnerships and limited partnerships, and

certain preferred stocks, for which market quotations are available, is generally determined by Management by obtaining valuations from independent pricing services based on the latest sale price quoted on a principal exchange or market

for that security (Level 1 inputs). Securities traded primarily on the NASDAQ Stock Market are

normally valued at the NASDAQ Official Closing Price ("NOCP") provided by NASDAQ each business day. The NOCP is the most recently reported price as of 4:00:02 p.m., Eastern Time, unless that price is outside the range of the "inside"

bid and asked prices (i.e., the bid and asked prices that dealers quote to each other when trading for their own accounts); in that case, NASDAQ will adjust the price to equal the inside bid or asked price, whichever is closer. Because

of delays in reporting trades, the NOCP may not be based on the price of the last trade to occur before the market closes. If there is no sale of a security on a particular day, the independent pricing services may value the security

based on market quotations. The value of certain preferred stock is determined by Management by obtaining

16

valuations from independent pricing services which are based on market information which may include benchmark yields, reported trades,

broker/dealer quotes, issuer spreads, benchmark securities, bids, offers, and reference data, such as market research publications, when available (generally Level 2 inputs).

Management has developed a process to periodically review information provided by independent pricing services for all

types of securities.

Investments in non-exchange traded investment companies are valued using the respective fund’s daily calculated net

asset value ("NAV") per share (Level 2 inputs), when available.

If a valuation is not available from an independent pricing service, or if Management has reason to believe that the

valuation received does not represent the amount the Fund might reasonably expect to receive on a current sale in an orderly transaction, Management seeks to obtain quotations from brokers or dealers (generally considered Level 2 or

Level 3 inputs depending on the number of quotes available). If such quotations are not available, the security is valued using methods Management has approved in the good-faith belief that the resulting valuation will reflect the fair

value of the security. Pursuant to Rule 2a-5 under the 1940 Act, the Board designated Management as the Fund's valuation designee. As the Fund's valuation designee, Management is responsible for determining fair value in good faith for

all Fund investments. Inputs and assumptions considered in determining fair value of a security based on Level 2 or Level 3 inputs may include, but are not limited to, the type of security; the initial cost of the security; the

existence of any contractual restrictions on the security’s disposition; the price and extent of public trading in similar securities of the issuer or of comparable companies; quotations or evaluated prices from broker-dealers or

pricing services; information obtained from the issuer and analysts; an analysis of the company’s or issuer’s financial statements; an evaluation of the inputs that influence the issuer and the market(s) in which the security is

purchased and sold.

Fair value prices are necessarily estimates, and there is no assurance that such a price will be at or close to the

price at which the security is next quoted or traded.

3

Securities transactions and investment income: Securities transactions are recorded on trade date for financial reporting purposes. Dividend income is recorded on the ex-dividend date. Non-cash dividends included in dividend income, if any, are recorded at

the fair market value of the securities received. Interest income, including accretion of discount (adjusted for original issue discount, where applicable), if any, is recorded on the accrual basis. Realized gains and losses from

securities transactions are recorded on the basis of identified cost and stated separately in the Statement of Operations. Included in net realized gain/(loss) on investments are proceeds from the settlement of class action

litigation(s) in which certain of the Funds participated as a class member. The amount of such proceeds for the year ended October 31, 2023, was $141,519.

4

Income tax information: It

is the policy of the Fund to continue to qualify for treatment as a regulated investment company ("RIC") by complying with the requirements of the U.S. Internal Revenue Code applicable to RICs and to distribute substantially all of

its net investment income and net realized capital gains to its stockholders. To the extent the Fund distributes substantially all of its net investment income and net realized capital gains to stockholders, no federal income or

excise tax provision is required.

ASC 740 "Income Taxes" sets forth a minimum threshold for financial statement recognition of a tax position taken, or

expected to be taken, in a tax return. The Fund recognizes interest and penalties, if any, related to unrecognized tax positions as an income tax expense in the Statement of Operations. The Fund is subject to examination by U.S. federal

and state tax authorities for returns filed for the tax years for which the applicable statutes of limitations have not yet expired. Management has analyzed the Fund's tax positions taken or expected to be taken on federal and state

income tax returns for all open tax years (the current and the prior three tax years) and has concluded that no provision for income tax is required in the Fund's financial statements.

For federal income tax purposes, the estimated cost of investments held at October 31, 2023 was $229,947,248. The

estimated gross unrealized appreciation was $13,069,471 and estimated gross unrealized depreciation was $51,028,922 resulting in net unrealized depreciation in value of investments of $37,959,451 based on cost for U.S. federal income

tax purposes.

17

Income distributions and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

These differences are primarily due to differing treatments of income and gains on various investment securities held by the Fund, timing differences and differing characterization of distributions made by the Fund.

Any permanent differences resulting from different book and tax treatment are reclassified at year-end and have no

impact on net income, NAV or NAV per share of common stock of the Fund. For the year ended October 31, 2023, the Fund recorded permanent reclassifications primarily related to prior year true up adjustment on real estate investment

trusts ("REITs"). For the year ended October 31, 2023, the Fund recorded the following permanent reclassifications:

|

|

Paid-in Capital

|

Total Distributable

Earnings/(Losses)

|

|

|

$35,828

|

$(35,828

)

|

The tax character of distributions paid during the years ended October 31, 2023, and October 31, 2022, was as follows:

|

|

Distributions Paid From:

|

|||||||

|

|

Ordinary

Income

|

Long-Term

Capital Gain

|

Return of

Capital

|

Total

|

||||

|

|

2023

|

2022

|

2023

|

2022

|

2023

|

2022

|

2023

|

2022

|

|

|

$5,116,490

|

$5,899,759

|

$—

|

$—

|

$12,650,964

|

$11,864,748

|

$17,767,454

|

$17,764,507

|

|

|

|

|

|

|

|

|

|

|

As of October 31, 2023, the components of distributable earnings (accumulated losses) on a U.S. federal income tax basis

were as follows:

|

|

Undistributed

Ordinary

Income

|

Undistributed

Long-Term

Capital Gain

|

Unrealized

Appreciation/

(Depreciation)

|

Loss

Carryforwards

and Deferrals

|

Other

Temporary

Differences

|

Total

|

|

|

$—

|

$—

|

$(37,959,451

)

|

$(19,249,923

)

|

$(132,192

)

|

$(57,341,566

)

|

The temporary differences between book basis and tax basis distributable earnings are primarily due to timing

differences of fund level distributions, losses disallowed and/or recognized on wash sales and tax adjustments related to partnerships.

To the extent the Fund’s net realized capital gains, if any, can be offset by capital loss carryforwards, it is the

policy of the Fund not to distribute such gains. Capital loss carryforward rules allow for RICs to carry forward capital losses indefinitely and to retain the character of capital loss carryforwards as short-term or long-term. As

determined at October 31, 2023, the Fund had unused capital loss carryforwards available for federal income tax purposes to offset future net realized capital gains, if any, as follows:

|

Capital Loss Carryforwards

|

|

|

Long-Term

|

Short-Term

|

|

$15,374,367

|

$3,875,556

|

5

Foreign taxes: Foreign

taxes withheld, if any, represent amounts withheld by foreign tax authorities, net of refunds recoverable.

6

Distributions to common stockholders: The Fund earns income, net of expenses, daily on its investments. It is the policy of the Fund to declare and pay monthly distributions to common stockholders. The Fund has adopted a policy to pay common

stockholders a stable monthly distribution. The Fund’s ability to satisfy its policy will depend on a number of factors, including the amount and stability of income received from its investments, the availability of capital gains,

interest paid on any borrowings and the level of other Fund fees and expenses. In an effort to maintain a stable distribution amount, the Fund may pay distributions consisting of net investment income, net realized gains and paid-in

capital. There is no assurance that the

18

Fund will always be able to pay distributions of a particular size, or that distributions will consist solely of net investment income

and net realized capital gains. The composition of the Fund’s distributions for the calendar year 2023 will be reported to Fund stockholders on IRS Form 1099-DIV. The Fund may pay distributions in excess of those required by its stable

distribution policy to avoid excise tax or to satisfy the requirements of Subchapter M of the Internal Revenue Code. Distributions to common stockholders are recorded on the ex-date. Net realized capital gains, if any, will be offset to

the extent of any available capital loss carryforwards. Any such offset will not reduce the level of the stable monthly distribution paid by the Fund.

The Fund invests a significant portion of its assets in securities issued by real estate companies, including REITs. The

distributions received from REITs are generally composed of income, capital gains, and/or return of REIT capital, but the REITs do not report this information to the Fund until the following calendar year. At October 31, 2023, the Fund

estimated these amounts for the period January 1, 2023 to October 31, 2023 within the financial statements because the 2023 information is not available from the REITs until after the Fund's fiscal year-end. All estimates are based upon

REIT information sources available to the Fund together with actual IRS Forms 1099-DIV received to date. For the year ended October 31, 2023, the character of distributions paid to stockholders of the Fund, if any, disclosed within the

Statements of Changes in Net Assets was based on estimates made at that time. Based on past experience it is possible that a portion of the Fund’s distributions during the current fiscal year, if any, will be considered tax return of

capital, but the actual amount of the tax return of capital, if any, is not determinable until after the Fund’s fiscal year-end. After calendar year-end, when the Fund learns the nature of the distributions paid by REITs during that

year, distributions previously identified as income may be re-characterized as return of capital and/or capital gain. After all applicable REITs have informed the Fund of the actual breakdown of distributions paid to the Fund during its

fiscal year, estimates previously recorded are adjusted to reflect actual results. As a result, the composition of the Fund’s distributions as reported herein may differ from the final composition determined after calendar year-end and

reported to Fund stockholders on IRS Form 1099-DIV.

On October 31, 2023, the Fund declared a monthly distribution to common stockholders in the amount of $0.0312 per share,

payable on November 30, 2023 to stockholders of record on November 15, 2023, with an ex-date of November 14, 2023. Subsequent to October 31, 2023, the Fund declared a monthly distribution on November 30, 2023 to common stockholders in

the amount of $0.0312 per share, payable on December 29, 2023 to stockholders of record on December 15, 2023, with an ex-date of December 14, 2023.

7

Expense allocation: Certain

expenses are applicable to multiple funds within the complex of related investment companies. Expenses directly attributable to the Fund are charged to the Fund. Expenses borne by the complex of related investment companies, which

includes open-end and closed-end investment companies for which NBIA serves as investment manager, that are not directly attributable to a particular investment company (e.g., the Fund) are allocated among the Fund and the other

investment companies or series thereof in the complex on the basis of relative net assets, except where a more appropriate allocation of expenses to each of the investment companies or series thereof in the complex can otherwise be

made fairly.

8

Financial leverage: In

September 2014, the Fund entered into a $125 million secured, committed five-year credit facility (the "Old Facility") with State Street Bank and Trust Company ("State Street"). Under the Old Facility, State Street made a Term Loan

of $75 million and committed to making revolving LIBOR Loans and Base Rate Loans of up to $50 million.

In September 2019, the Fund amended and extended the Old Facility and reduced the size of the Old Facility to $100

million (as so amended and extended, the "Current Facility"). Under the Current Facility, in 2019 State Street made a 3-year Term Loan of $30 million due September 2022 and a 5-year Term Loan of $30 million due September 2024 and

committed to making revolving LIBOR Loans and Base Rate Loans of up to $40 million. In March 2020, the Fund repaid the $30 million 3-year Term Loan due September 2022. After the repayment, the amount of the Fund's outstanding fixed-rate

borrowings under the Current Facility was reduced to $30 million, consisting of the 5-year Term Loan due September 2024. In November 2021, the Fund amended the Current Facility to increase the total commitment amount under the revolving

credit

19

facility from $40 million to $70 million. In December 2022, the Fund amended the Current Facility to address the discontinuation of

certain LIBOR-based interest rates and provide for the commitment to make revolving SOFR Loans.

Under the Current Facility, interest on the 5-year Term Loan is charged at a fixed rate of 2.96% and is payable on the

first day of each calendar quarter. Interest on SOFR Loans is charged at an adjusted SOFR rate and is payable (i) on the last day of the interest period in effect, (ii) in the event such interest period shall exceed three months, on the

last day of each three month interval during such interest period and (iii) the termination date. Interest on Base Rate Loans is charged at a rate equal to the highest of (i) Term SOFR; (ii) the Overnight Bank Funding Rate; and (iii)

the federal funds rate as in effect on that day, plus a spread, and is payable (i) with respect to interest accrued during a calendar month, on the fifteenth day of the immediately succeeding calendar month, and (ii) with respect to all

accrued and unpaid interest, on the termination date.

During the year ended October 31, 2023, the average principal balance outstanding and average annualized interest rate

under the Current Facility were $59,616,438 and 4.30%, respectively. At October 31, 2023, the principal balance outstanding under the Current Facility was $50 million, consisting of the $30 million 5-year Term Loan and $20 million

outstanding under the revolving credit facility.

The Fund pays a commitment fee in arrears based on the unused portion of the revolving commitment amount under the

Current Facility. This fee is included in the Interest expense line item that is reflected in the Statement of Operations. Under the terms of the Current Facility, the Fund is required to satisfy certain collateral requirements and

maintain a certain level of net assets.

9

Concentration of risk:

Under normal market conditions, the Fund’s investments will be concentrated in income producing common equity securities, preferred securities, convertible securities and non-convertible debt securities issued by companies deriving

the majority of their revenue from the ownership, construction, financing, management and/or sale of commercial, industrial, and/or residential real estate. The value and/or price of the Fund’s common stock may fluctuate more due to

economic, legal, cultural, geopolitical or technological developments affecting the United States real estate industry, or a segment of the United States real estate industry in which the Fund owns a substantial position, than would

the stock of a fund not concentrated in the real estate industry.

10

Securities lending: The

Fund, using State Street as its lending agent, may loan securities to qualified brokers and dealers in exchange for negotiated lender’s fees. These fees, if any, would be disclosed within the Statement of Operations under the

caption "Income from securities loaned-net" and are net of expenses retained by State Street as compensation for its services as lending agent.

The initial collateral received by the Fund at the beginning of each transaction shall have a value equal to at least

102% of the prior day’s market value of the loaned securities (105% in the case of international securities). Collateral in the form of cash and/or securities issued or guaranteed by the U.S. government or its agencies, equivalent to at

least 100% of the market value of securities, is maintained at all times. Thereafter, the value of the collateral is monitored on a daily basis, and collateral is moved daily between a counterparty and the Fund until the close of the

transaction. Cash collateral is generally invested in a money market fund registered under the 1940 Act that is managed by an affiliate of State Street and is included in the Statement of Assets and Liabilities under the caption

"Investments in securities, at value-Unaffiliated issuers". The total value of securities received as collateral for securities on loan is included in a footnote following the Schedule of Investments, but is not included within the

Statement of Assets and Liabilities because the receiving Fund does not have the right to sell or repledge the securities received as collateral. The risks associated with lending portfolio securities include, but are not limited to,

possible delays in receiving additional collateral or in the recovery of the loaned securities. Any increase or decrease in the fair value of the securities loaned and any interest earned or dividends paid or owed on those securities

during the term of the loan would accrue to the Fund.

During the year ended October 31, 2023, the Fund did not participate in securities lending.

11

Indemnifications: Like many

other companies, the Fund’s organizational documents provide that its officers ("Officers") and directors ("Directors") are indemnified against certain liabilities arising out of the

20

performance of their duties to the Fund. In addition, both in some of its principal service contracts and in the normal course of its

business, the Fund enters into contracts that provide indemnifications to other parties for certain types of losses or liabilities. The Fund’s maximum exposure under these arrangements is unknown as this could involve future claims

against the Fund.

12

Shelf Registration Statement: The Fund has filed a registration statement with the SEC, which became effective on March 14, 2023, authorizing the Fund to issue up to $150,000,000 of additional shares of common stock through one or more offerings (the

"Shelf Registration Statement"). Under the Shelf Registration Statement, the Fund, subject to market conditions, may raise additional equity capital by issuing additional shares of common stock from time to time in varying amounts

and by different offering methods. The Fund is not required to issue shares of its common stock pursuant to the Shelf Registration Statement and may choose not to do so. As of October 31, 2023, the Fund has not yet sold any shares

of common stock pursuant to the Shelf Registration Statement.

Costs incurred by the Fund in connection with the initial Shelf Registration Statement are recorded as a prepaid asset

and included in "Prepaid offering costs" in the Statement of Assets and Liabilities.

Note B—Investment Management Fees, Administration Fees, and Other Transactions with Affiliates:

The Fund retains NBIA as its investment manager under a Management Agreement. For such investment management services,

the Fund pays NBIA an investment management fee at an annual rate of 0.60% of the Fund's average daily Managed Assets. Managed Assets equal the total assets of the Fund, less liabilities other than the aggregate indebtedness entered

into for purposes of leverage.

The Fund retains NBIA as its administrator under an Administration Agreement. The Fund pays NBIA an administration fee

at an annual rate of 0.25% of its average daily Managed Assets under this agreement. Additionally, NBIA retains State Street as its sub-administrator under a Sub-Administration Agreement. NBIA pays State Street a fee for all services

received under the Sub-Administration Agreement.

Note C—Securities Transactions:

During the year ended October 31, 2023, there were purchase and sale transactions of long-term securities of $15,583,906

and $33,778,741, respectively.

During the year ended October 31, 2023, no brokerage commissions on securities transactions were paid to affiliated

brokers.

Note D—Capital:

Transactions in shares of common stock for the years ended October 31, 2023, and October 31, 2022, were as follows:

|

For the Year Ended October 31, 2023

|

For the Year Ended October 31, 2022

|

||

|

Stock Issued on

Reinvestment of

Dividends

and Distributions

|

Net Increase/

(Decrease)

In Common Stock

Outstanding

|

Stock Issued on

Reinvestment of

Dividends

and Distributions

|

Net Increase/

(Decrease)

In Common Stock

Outstanding

|

|

—

|

—

|

13,492

|

13,492

|

Note E—Recent Accounting Pronouncements:

In December 2022, the FASB issued Accounting Standards Update No. 2022-06, "Reference Rate Reform (Topic 848)" ("ASU

2022-06"), which is an update to Accounting Standards Update No. 2021-01, "Reference Rate Reform (Topic 848)" ("ASU 2021-01") and defers the sunset date for applying the reference rate reform relief in Topic 848. ASU 2021-01 is an

update of ASU 2020-04, which is in response

21

to concerns about structural risks of interbank offered rates, and particularly the risk of cessation of LIBOR. Regulators have

undertaken reference rate reform initiatives to identify alternative reference rates that are more observable or transaction based and less susceptible to manipulation. ASU 2020-04 provides optional guidance for a limited period of time

to ease the potential burden in accounting for (or recognizing the effects of) reference rate reform on financial reporting. ASU 2020-04 is elective and applies to all entities, subject to meeting certain criteria, that have contracts,

hedging relationships, and other transactions that reference LIBOR or another reference rate expected to be discontinued because of reference rate reform. The ASU 2021-01 update clarifies that certain optional expedients and exceptions

in Topic 848 for contract modifications and hedge accounting apply to derivatives that are affected by the discounting transition. The amendments in this update are effective immediately through December 31, 2024, for all entities.

Management is currently evaluating the implications, if any, of the additional requirements and its impact on the Fund's financial statements.

In June 2022, FASB issued Accounting Standards Update No. 2022-03, "Fair Value Measurement of Equity Securities Subject

to Contractual Sale Restrictions" ("ASU 2022-03"). ASU 2022-03 clarifies the guidance in ASC 820, related to the measurement of the fair value of an equity security subject to contractual sale restrictions, where it eliminates the

ability to apply a discount to the fair value of these securities, and introduces disclosure requirements related to such equity securities. The guidance is effective for fiscal years, and interim periods within those fiscal years,

beginning after December 15, 2023, and allows for early adoption. Management is currently evaluating the impact of applying this update.

22

Financial Highlights

Real Estate Securities Income Fund Inc.

The following table includes selected data for a share of common stock outstanding throughout each period and other performance

information derived from the Financial Statements. Amounts that do not round to $0.01 or $(0.01) per share are presented as $0.00 or $(0.00), respectively. Ratios that do not round to 0.01% or (0.01)% are presented as 0.00% or (0.00)%,

respectively. A "—" indicates that the line item was not applicable in the corresponding period.

|

|

Year Ended October 31,

|

||||

|

|

2023

|

2022

|

2021

|

2020

|

2019

|

|

Common Stock Net Asset Value, Beginning of Year

|

$3.40

|

$5.25

|

$3.89

|

$5.88

|

$5.06

|

|

Income/(Loss) From Investment Operations Applicable to

Common

Stockholders:

|

|

|

|

|

|

|

Net Investment Income/(Loss)a

|

0.11

|

0.09

|

0.13

|

0.11

|

0.22

|

|

Net Gains or (Losses) on Securities (both realized and unrealized)

|

(0.15

)

|

(1.57

)

|

1.62

|

(1.62

)

|

1.08

|

|

Total From Investment Operations Applicable to Common

Stockholders

|

(0.04

)

|

(1.48

)

|

1.75

|

(1.51

)

|

1.30

|

|

Less Distributions to Common Stockholders From:

|

|

|

|

|

|

|

Net Investment Income

|

(0.10

)

|

(0.12

)

|

(0.15

)

|

(0.15

)

|

(0.21

)

|

|

Tax Return of Capital

|

(0.27

)

|

(0.25

)

|

(0.24

)

|

(0.33

)

|

(0.27

)

|

|

Total Distributions to Common Stockholders

|

(0.37

)

|

(0.37

)

|

(0.39

)

|

(0.48

)

|

(0.48

)

|

|

Common Stock Net Asset Value, End of Year

|

$2.99

|

$3.40

|

$5.25

|

$3.89

|

$5.88

|

|

Common Stock Market Value, End of Year

|

$2.59

|

$3.36

|

$5.02

|

$3.70

|

$5.58

|

|

Total Return, Common Stock Net Asset Valueb

|

(0.92

)%c

|

(29.49

)%

|

46.70

%c

|

(25.65

)%

|

27.80

%

|

|

Total Return, Common Stock Market Valueb

|

(13.15

)%c

|

(27.12

)%

|

47.48

%c

|

(25.48

)%

|

30.85

%

|

|

Supplemental Data/Ratios

|

|

|

|

|

|

|

Net Assets Applicable to Common Stockholders, End of Year (in millions)

|

$142.1

|

$161.1

|

$249.0

|

$184.5

|

$278.8

|

|

Ratios are Calculated Using Average Net Assets Applicable to

Common Stockholders

|

|

|

|

|

|

|

Ratio of Gross Expensesd

|

3.00

%

|

2.06

%

|

1.69

%

|

2.16

%

|

2.75

%

|

|

Ratio of Net Expensesd

|

3.00

%

|

2.06

%

|

1.69

%

|

2.16

%

|

2.75

%

|

|