UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C.

20549

SCHEDULE 14A

PROXY STATEMENT PURSUANT TO SECTION 14(a)

OF THE

SECURITIES EXCHANGE ACT OF 1934

| Filed by the Registrant [X] | Filed by a Party other than the Registrant [ ] |

| Check the appropriate box: | |

| [X] | Preliminary Proxy Statement |

| [ ] | Confidential, for use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| [ ] | Definitive Proxy Statement |

| [ ] | Definitive Additional Materials |

| [ ] | Soliciting Material Under Rule 14a-12 |

CHINA SECURITY & SURVEILLANCE TECHNOLOGY,

INC.

(Name of Registrant as Specified in its Charter)

| Payment of Filing Fee (Check the appropriate box): | |

| [ ] | No fee required |

| [X] | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11(c)(1) |

| (1) |

Title of each class of securities to which transaction applies: | |

|

Common stock, par value $0.0001 per share of China Security & Surveillance Technology, Inc. (“common stock”) | ||

| (2) |

Aggregate number of securities to which transaction applies: | |

|

67,995,345 shares of common stock issued and outstanding as of July 22, 2011 (consisting of the 89,703,773 shares of common stock outstanding as of July 22, 2011 minus 21,708,428 shares held by Guoshen Tu, certain management members of the registrant and their respective affiliates (the “Rollover Shares”)*), and 12,864 shares of common stock underlying outstanding warrants as of July 22, 2011 with an exercise price below $6.50 per share. | ||

|

* The Rollover Shares are being contributed to Rightmark Holdings Limited immediately prior to the consummation of the merger. | ||

| (3) |

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11(c)(1) and the Securities and Exchange Commission Fee Rate Advisory #5 for Fiscal Year 2011 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

|

The proposed maximum aggregate value of the transaction for purposes of calculating the filing fee is $441,991,611. The maximum aggregate value of the transaction was calculated based upon the sum of (1) 67,995,345 shares of common stock issued and outstanding as of July 22, 2011 (consisting of the 89,703,773 shares of common stock outstanding as of July 22, 2011 minus the Rollover Shares) multiplied by $6.50 per share and (2) the product of 12,864 shares of common stock underlying outstanding warrants as of July 22, 2011 multiplied by $1.70 per share (which is the difference between the $6.50 per share merger consideration and the exercise price of $4.80 per share). The filing fee equals the product of $0.0001161 multiplied by the maximum aggregate value of the transaction. |

| (4) |

Proposed maximum aggregate value of transaction: $441,991,611 | |

| (5) |

Total fee paid: $51,329 |

| [ ] |

Fee paid previously with preliminary materials. |

| [X] |

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. |

| (1) |

Amount Previously Paid: $521.85 | |

| (2) |

Form, Schedule or Registration Statement No.: Form S-3 | |

| (3) |

Filing party: China Security & Surveillance Technology, Inc. | |

| (4) |

Date Filed: March 10, 2010 |

PRELIMINARY PROXY MATERIAL SUBJECT TO COMPLETION

![]()

August [ ], 2011

To the Stockholders of China Security & Surveillance Technology, Inc.:

You are cordially invited to attend an annual meeting of stockholders of China Security & Surveillance Technology, Inc., a Delaware corporation (the “Company,” “we,” “us” or “our”) to be held at 10:00 a.m. local time, on September 14, 2011, at the Company’s office at 13/F, Shenzhen Special Zone Press Tower, Shennan Road, Futian District, Shenzhen 518034, the People's Republic of China.

At the annual meeting, you will be asked to consider and vote upon a proposal to adopt an Amended and Restated Agreement and Plan of Merger, dated as of May 3, 2011 (the “merger agreement”), among the Company, Rightmark Holdings Limited, a British Virgin Islands company (“Parent”), Rightmark Merger Sub Limited, a Delaware corporation and a wholly owned subsidiary of Parent (“Merger Sub”), and solely for the purposes of Section 6.15 therein, Mr. Guoshen Tu (“Mr. Tu”), the Chairman and Chief Executive Officer of the Company. Under the terms of the merger agreement, Merger Sub will be merged with and into the Company (the “merger”), with the Company surviving the merger as a wholly owned subsidiary of Parent. Parent and Merger Sub were formed and are beneficially owned by Mr. Tu.

If the merger is completed, each share of Company common stock, other than as provided below, will be converted into the right to receive $6.50 in cash, without interest. We refer to this amount as the “per share merger consideration.” The following shares of Company common stock will not be converted into the right to receive the per share merger consideration in connection with the merger: (a) shares owned by Parent or Merger Sub, (b) shares contributed to Parent by the Rollover Stockholders (as defined below) immediately prior to the effective time of the merger and (c) shares owned by stockholders who have exercised, perfected and not withdrawn a demand for, or lost the right to, appraisal rights under the Delaware General Corporation Law.

The merger agreement provides that, each share of Company common stock that, immediately prior to the effective time of the merger, is subject to vesting and/or forfeiture restrictions under the equity incentive plan adopted by the board of directors of the Company on February 7, 2007 and subsequently amended in February 2010 shall become fully vested immediately prior to the effective time, and each such share shall be treated as a share of Company common stock.

At the effective time, each warrant to purchase shares of Company common stock issued that is outstanding at the effective time shall be canceled and, in exchange therefor, the surviving corporation shall pay to each former holder of any such canceled warrant immediately following the effective time an amount in cash (without interest) equal to the product of (i) the excess of the per share merger consideration over the exercise price per share of Company common stock of such warrant and (ii) the number of shares of Company common stock subject to such warrant; provided, that if the exercise price per share of Company common stock of any such warrant is equal to or greater than the per share merger consideration, such warrant shall be canceled without any cash payment being made in respect thereof. See “The Merger Agreement—Treatment of Common Stock, Restricted Shares and Company Warrants” beginning on page 67 for additional information.

A special committee of our board of directors, consisting entirely of independent directors, reviewed and considered the terms and conditions of the merger agreement and the transactions contemplated by the merger agreement, including the merger. The special committee unanimously determined that the merger agreement and the transactions contemplated by the merger agreement, including the merger, are advisable, fair to and in the best interests of the Company and its stockholders, and recommended that our board of directors approve and declare the advisability of the merger agreement and the transactions contemplated by the merger agreement, including the merger, and recommend that our stockholders adopt the merger agreement. Our board of directors, after careful consideration and acting on the unanimous recommendation of the special committee, deemed it advisable and in the best interests of the Company and our stockholders that the Company enter into the merger agreement, determined that the merger agreement and the transactions contemplated by the merger agreement, including the merger, are advisable, fair to and in the best interests of the Company and its stockholders and recommended that our stockholders adopt the merger agreement at the annual meeting. Our board of directors recommends that you vote “FOR” the proposal to adopt the merger agreement.

The merger cannot be completed unless the merger agreement is adopted by (i) stockholders holding at least a majority of the outstanding shares of Company common stock at the close of business, New York time, on the record date and (ii) stockholders holding at least a majority of the outstanding shares of the Company’s common stock at the close of business, New York time, on the record date, other than shares owned, directly or indirectly, by Parent, Merger Sub, Rollover Stockholders or any of their respective affiliates. More information about the merger is contained in the accompanying proxy statement and copy of the Amended and Restated Agreement and Plan of Merger is attached thereto as Annex A.

In considering the recommendation of the special committee and the board of directors, you should be aware that some of the Company’s directors and officers have interests in the merger that are different from, or in addition to, the interests of our stockholders generally. Mr. Tu, the Chairman and Chief Executive Officer of the Company, and Wing Khai Yap (also known as Terence Yap), the Chief Financial Officer and a director of the Company, Lizhong Wang, Zhongxin Xie, Lingfeng Xiong, Li Fang, Ying Zhang, Zhiming Wu, Daobin Sang, Guohui Cao, Po Kwai Chow, Yang Zhao, Yujuan Guan, Zhuo Gong, Xihong Dai, Qiaomin Wu, Kaicheng Cheng, Lei Wang and Xiaosheng Tong, each of whom is a member of the Company’s management team or the nominee of a member of the Company's management team (collectively, the “Rollover Stockholders”), beneficially own approximately 24.20% of the total number of outstanding shares of Company common stock. The Rollover Stockholders are parties to the rollover agreement described in the accompanying proxy statement and have agreed with Parent to contribute to Parent the shares of Company common stock owned by them in exchange for equity securities of Intelligent One Limited, a British Virgin Islands company (“Intelligent One”), that beneficially owns all of the share capital of Parent, immediately prior to the completion of the merger, or, if agreed between Parent and a Rollover Stockholder, in exchange for an amount in cash equal to $6.50 per share multiplied by the number of shares of Company common stock held by such Rollover Stockholder. The accompanying proxy statement includes additional information regarding certain interests of the Company’s directors and officers that may be different from, or in addition to, the interests of our stockholders generally.

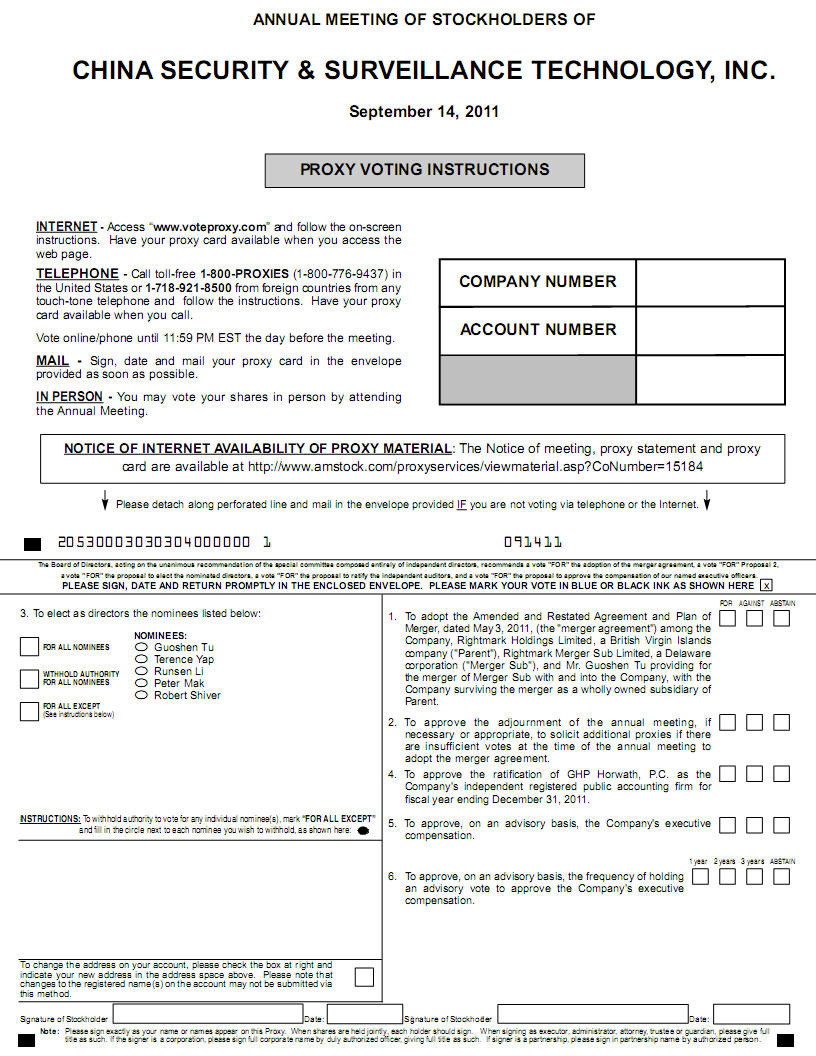

Also as part of the annual meeting, you are being asked to vote upon (1) the election of five persons to the board of directors of the Company; (2) the ratification of the selection by our Audit Committee of GHP Horwath, P.C. as the Company’s independent registered public accounting firm for the fiscal year ending December 31, 2011; (3) the approval, on an advisory basis, of executive compensation; (4) approval, on an advisory basis, of the frequency of holding an advisory vote on executive compensation; and (5) such other business as may properly come before the meeting or any adjournment thereof.

We encourage you to read the accompanying proxy statement in its entirety because it explains the proposed merger, the documents related to the merger and other related matters.

Regardless of the number of shares of Company common stock you own, your vote is important. The failure to vote will have the same effect as a vote against the proposal to adopt the merger agreement.

Whether or not you plan to attend the annual meeting, please take the time to submit a proxy by following the instructions on your proxy card as soon as possible. If your shares of Company common stock are held in an account at a broker, dealer, commercial bank, trust company or other nominee, you should instruct your broker, dealer, commercial bank, trust company or other nominee how to vote in accordance with the voting instruction form furnished by your broker, dealer, commercial bank, trust company or other nominee.

We appreciate your continued support of the Company.

Sincerely,

Guoshen Tu

Chairman of the Board

and Chief Executive Officer

The merger has not been approved or disapproved by the Securities and Exchange Commission or any state securities commission. Neither the Securities and Exchange Commission nor any state securities commission has passed upon the merits or fairness of the merger or upon the adequacy or accuracy of the information contained in this document or the accompanying proxy statement. Any representation to the contrary is a criminal offense.

The accompanying proxy statement is dated August [ ], 2011 and is first being mailed to stockholders on or about August [ ], 2011.

![]()

CHINA SECURITY & SURVEILLANCE TECHNOLOGY, INC.

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON SEPTEMBER 14, 2011

NOTICE IS HEREBY GIVEN that the annual meeting of stockholders of China Security & Surveillance Technology, Inc. (the “Company,” “we,” “us” or “our”) will be held at 10:00 a.m., local time, on September 14, 2011, at the Company’s office at 13/F, Shenzhen Special Zone Press Tower, Shennan Road, Futian District, Shenzhen 518034, the People's Republic of China, for the following purposes:

| 1. |

To adopt the Amended and Restated Agreement and Plan of Merger, dated as of May 3, 2011 (the “merger agreement”), with Rightmark Holdings Limited, a British Virgin Islands company (“Parent”), Rightmark Merger Sub Limited, a Delaware corporation and a wholly owned subsidiary of Parent (“Merger Sub”), and, solely for the purposes of Section 6.15 therein, Mr. Guoshen Tu, the Chairman and Chief Executive Officer of the Company, providing for the merger of Merger Sub with and into the Company (the “merger”), with the Company surviving the merger as a wholly owned subsidiary of Parent. Parent and Merger Sub were formed and are beneficially owned by Mr. Guoshen Tu; | |

| 2. |

To approve the adjournment of the annual meeting, if necessary or appropriate, to solicit additional proxies if there are insufficient votes at the time of the annual meeting to adopt the merger agreement; | |

| 3. |

To elect five persons to the board of directors of the Company; | |

| 4. |

To ratify the selection by our Audit Committee of GHP Horwath, P.C. as the Company’s independent registered public accounting firm for the fiscal year ending December 31, 2011; | |

| 5. |

To have an advisory vote on executive compensation; | |

| 6. |

To have an advisory vote on the frequency of holding an advisory vote on executive compensation; and | |

| 7. |

To transact such other business as may properly come before the annual meeting or any adjournment thereof. |

For more information about the merger and the other transactions contemplated by the merger agreement, please review the accompanying proxy statement and the merger agreement attached thereto as Annex A.

A special committee of our board of directors, consisting entirely of independent directors, reviewed and considered the terms and conditions of the merger agreement and the transactions contemplated by the merger agreement, including the merger. The special committee unanimously determined that the merger agreement and the transactions contemplated by the merger agreement, including the merger, are advisable, fair to and in the best interests of the Company and its stockholders, and recommended that our board of directors approve and declare the advisability of the merger agreement and the transactions contemplated by the merger agreement, including the merger, and recommend that our stockholders adopt the merger agreement. Our board of directors, acting on the unanimous recommendation of the special committee, deemed it advisable and in the best interests of the Company and our stockholders that the Company enter into the merger agreement, determined that the merger agreement and the transactions contemplated by the merger agreement, including the merger, are advisable, fair to and in the best interests of the Company and its stockholders and recommended that our stockholders adopt the merger agreement at the annual meeting. Our board of directors recommends that you vote “FOR” the proposal to adopt the merger agreement.

Guoshen Tu, the Chairman and Chief Executive Officer of the Company, and Wing Khai Yap (Terence), the Chief Financial Officer and a director of the Company, Lizhong Wang, Zhongxin Xie, Lingfeng Xiong, Li Fang, Ying Zhang, Zhiming Wu, Daobin Sang, Guohui Cao, Po Kwai Chow, Yang Zhao, Yujuan Guan, Zhuo Gong, Xihong Dai, Qiaomin Wu, Kaicheng Cheng, Lei Wang and Xiaosheng Tong, each a member of the Company’s management team or the nominee of a member of the Company’s management team (collectively, the “Rollover Stockholders”) beneficially own approximately 24.20% of the total number of outstanding shares of Company common stock. The Rollover Stockholders are parties to the rollover agreement described in the accompanying proxy statement and have agreed with Parent to contribute to Parent shares of Company common stock owned by them in exchange for equity securities of Intelligent One Limited, a British Virgin Islands company (“Intelligent One”), that beneficially owns all of the share capital of Parent, immediately prior to the completion of the merger or, if agreed between Parent and a Rollover Stockholder, in exchange for an amount in cash equal to $6.50 per share multiplied by the number of shares of Company common stock held by such Rollover Stockholder.

Only stockholders of record at the close of business, New York time, on August 5, 2011 are entitled to notice of and to vote at the annual meeting and at any and all adjournments or postponements thereof.

The adoption of the merger agreement requires the affirmative vote of (i) stockholders holding at least a majority of the outstanding shares of Company common stock at the close of business, New York time, on the record date and (ii) stockholders holding at least a majority of the outstanding shares of the Company’s common stock at the close of business, New York time, on the record date, other than shares owned, directly or indirectly, by Parent, Merger Sub, the Rollover Stockholders or any of their respective affiliates. The approval of the adjournment of the annual meeting requires the affirmative vote of the holders of at least a majority of the shares of the Company common stock present and entitled to vote at the annual meeting as of the record date, whether or not a quorum is present.

Regardless of the number of shares of Company common stock you own, your vote is important. The failure to vote will have the same effect as a vote against the proposal to adopt the merger agreement.

Whether or not you plan to attend the annual meeting, please take the time to submit a proxy by following the instructions on your proxy card as soon as possible. If your shares of Company common stock are held in an account at a broker, dealer, commercial bank, trust company or other nominee, you should instruct your broker, dealer, commercial bank, trust company or other nominee how to vote in accordance with the voting instruction form furnished by your broker, dealer, commercial bank, trust company or other nominee.

Company stockholders who do not vote in favor of adoption of the merger agreement will have the right to seek appraisal and receive the fair value of their shares in lieu of receiving the per share merger consideration if the merger closes but only if they perfect their appraisal rights by complying with the required procedures under Delaware law, which are summarized in the accompanying proxy statement.

If you plan to attend the annual meeting, please note that you may be asked to present valid photo identification, such as a driver’s license or passport. If you wish to attend the annual meeting and your shares of Company common stock are held in an account at a broker, dealer, commercial bank, trust company or other nominee (i.e., in “street name”), you will need to bring a copy of your voting instruction card or statement reflecting your share ownership as of the record date.

By Order of the Board of Directors,

Samuel Lo

Corporate

Secretary

Shenzhen, China

August [ ], 2011

Important Notice of Internet Availability

This proxy statement, the Notice of Annual Meeting of Stockholders, and a form of the Proxy Card for the annual meeting to be held on September 14, 2011 are available free of charge at www.myproxyonline.com/CSR.

YOUR VOTE IS IMPORTANT

WHETHER OR NOT YOU PLAN TO ATTEND THE ANNUAL MEETING IN PERSON, YOU ARE ENCOURAGED TO VOTE AS SOON AS POSSIBLE. YOU MAY VOTE YOUR SHARES OF COMPANY COMMON STOCK BY TELEPHONE, OVER THE INTERNET, OR IF YOU RECEIVED A PAPER COPY OF THE PROXY CARD, BY SIGNING AND DATING IT AND RETURNING IT PROMPTLY. VOTING BY PROXY WILL NOT PREVENT YOU FROM ATTENDING THE MEETING AND VOTING IN PERSON IF YOU SO DESIRE.

SUMMARY VOTING INSTRUCTIONS

Ensure that your shares of Company common stock can be voted at the annual meeting by submitting your proxy or contacting your broker, dealer, commercial bank, trust company or other nominee.

If your shares of Company common stock are registered in the name of a broker, dealer, commercial bank, trust company or other nominee: check the voting instruction card forwarded by your broker, dealer, commercial bank, trust company or other nominee to see which voting options are available or contact your broker, dealer, commercial bank, trust company or other nominee in order to obtain directions as to how to ensure that your shares of Company common stock are voted at the annual meeting.

If your shares of Company common stock are registered in your name: submit your proxy as soon as possible by telephone, via the Internet or by signing, dating and returning the enclosed proxy card in the enclosed postage-paid envelope, so that your shares of Company common stock can be voted at the annual meeting.

Instructions regarding telephone and Internet voting are included on the proxy card.

The failure to vote will have the same effect as a vote against the proposal to adopt the merger agreement. If you sign, date and mail your proxy card without indicating how you wish to vote, your proxy will be voted in favor of the proposal to adopt the merger agreement and the proposal to adjourn the annual meeting, if necessary and appropriate, to solicit additional proxies.

If you have any questions, require assistance with voting your proxy card, or need additional copies of proxy material, please call our Corporate Secretary at (+86) 755-8351-0888.

TABLE OF CONTENTS

| Page | |

| PROXY STATEMENT | 1 |

| SUMMARY TERM SHEET RELATED TO THE MERGER | 1 |

| QUESTIONS AND ANSWERS ABOUT THE ANNUAL MEETING AND THE MERGER | 12 |

| SPECIAL FACTORS RELATING TO THE MERGER | 18 |

|

The Parties |

18 |

|

Overview of the Transaction |

21 |

|

Management and Board of Directors of the Surviving Corporation |

22 |

|

Background of the Merger |

23 |

|

Purposes and Reasons of Our Board of Directors and Special Committee for the Merger |

30 |

|

Recommendation of Our Board of Directors and Special Committee; Reasons for Recommending the Adoption of the Merger Agreement; Fairness of the Merger |

31 |

|

Opinion of Imperial Capital, Financial Advisor to the Special Committee |

38 |

|

Purposes and Reasons of the Tu Parties for the Merger |

44 |

|

Positions of the Tu Parties Regarding the Fairness of the Merger |

44 |

|

Certain Effects of the Merger |

48 |

|

Effects on the Company if Merger is not Completed |

49 |

|

Plans for the Company |

50 |

|

Prospective Financial Information |

50 |

|

Financing of the Merger |

52 |

|

Limited Guaranty |

53 |

|

Limitation on Remedies |

53 |

|

Interests of the Company’s Directors and Officers in the Merger |

54 |

|

Relationship Between Us and the Tu Parties |

55 |

|

Dividends |

56 |

|

Determination of the Per Share Merger Consideration |

56 |

|

Regulatory Matters |

56 |

i

|

Fees and Expenses |

56 |

|

Material United States Federal Income Tax Consequences |

56 |

|

Material PRC Tax Consequences |

58 |

|

Delisting and Deregistration of the Company Common Stock |

59 |

|

Litigation Relating to the Merger and Other Legal Proceedings |

59 |

| THE ANNUAL MEETING | 61 |

|

Date, Time and Place |

61 |

|

Purpose of the Annual meeting |

61 |

|

Recommendation of Our Board of Directors and Special Committee |

61 |

|

Record Date; Stockholders Entitled to Vote; Quorum |

62 |

|

Vote Required |

62 |

|

Stock Ownership and Interests of Certain Persons |

63 |

|

Voting Procedures |

63 |

|

Other Business |

64 |

|

Revocation of Proxies |

64 |

|

Rights of Stockholders Who Object to the Merger |

65 |

|

Solicitation of Proxies |

65 |

|

Assistance |

65 |

| PROPOSAL ONE — ADOPTION OF THE MERGER AGREEMENT | 66 |

| THE MERGER AGREEMENT | 66 |

|

Explanatory Note Regarding the Merger Agreement |

66 |

|

Effects of the Merger; Directors and Officers; Certificate of Incorporation; Bylaws |

66 |

|

Closing and Effective Time of the Merger |

66 |

|

Treatment of Common Stock, Restricted Stock and Company Warrants |

67 |

|

Exchange and Payment Procedures |

67 |

|

Representations and Warranties |

68 |

|

Conduct of Business Prior to Closing |

72 |

|

Parent Forbearance |

73 |

|

Access to Information |

73 |

|

Alternative Takeover Proposals |

73 |

ii

|

Indemnification; Directors’ and Officers’ Insurance |

75 |

|

Financing |

76 |

|

No Knowledge of Inaccuracies |

77 |

|

Employee Matters |

77 |

|

Conditions to the Merger |

77 |

|

Termination |

78 |

|

Termination Fees and Reimbursement of Expenses |

79 |

|

Fees and Expenses |

80 |

|

Remedies |

80 |

|

Amendment; Waiver of Conditions |

80 |

| COMMON STOCK OWNERSHIP OF MANAGEMENT AND CERTAIN BENEFICIAL OWNERS | 80 |

|

Changes in Control |

82 |

|

Securities Authorized for Issuances under Equity Compensation Plans |

82 |

| COMMON STOCK TRANSACTION INFORMATION | 83 |

|

Purchases by Company |

83 |

|

Prior Public Offerings |

83 |

| APPRAISAL RIGHTS | 83 |

| SELECTED FINANCIAL INFORMATION | 87 |

|

Selected Historical Financial Information |

87 |

|

Ratio of Earnings to Fixed Charges |

87 |

|

Net Book Value per Share of Company Common Stock |

87 |

| MARKET PRICE AND DIVIDEND INFORMATION | 88 |

| PROPOSAL TWO—ADJOURNMENT OR POSTPONEMENT OF THE ANNUAL MEETING | 88 |

| PROPOSAL THREE—ELECTION OF DIRECTORS | 89 |

|

Director Selection |

89 |

|

Information Concerning Nominees and Incumbent Directors and Executive Officers |

90 |

|

General Information |

91 |

| CORPORATE GOVERNANCE | 92 |

iii

|

Corporate Governance Guidelines |

92 |

|

The Board and Committees of the Board |

92 |

|

Governance Structure |

92 |

|

The Board’s Role in Risk Oversight |

93 |

|

Independent Directors |

93 |

|

Audit Committee |

94 |

|

Compensation Committee |

95 |

|

Nominating and Governance Committee |

96 |

|

Material Changes to Director Nomination Procedures |

96 |

|

Board, Committee and Annual Meeting Attendance |

96 |

|

Amended and Restated Code of Ethics |

97 |

|

Communication with Directors or Non-Management Directors |

97 |

|

Report of the Audit Committee |

97 |

| EXECUTIVE COMPENSATION | 98 |

|

Compensation Discussion and Analysis |

98 |

|

Objectives of Our Executive Compensation Program |

98 |

|

How Executive Compensation is Determined |

99 |

|

The Key Elements of Our Executive Compensation Program |

101 |

|

Other Benefits |

102 |

|

Change in Control and Employment Agreements |

102 |

|

Compensation Committee Report |

102 |

|

Compensation Policies |

102 |

|

Summary Compensation Table |

103 |

|

Grants of Plan-Based Awards |

103 |

|

Outstanding Equity Awards at Fiscal Year End |

104 |

|

Option Exercises and Stock Vested |

104 |

|

Employment Agreements |

104 |

|

Potential Payments Upon Termination of Employment or Change of Control |

104 |

iv

|

Non-Management Directors’ Compensation |

105 |

|

Compensation Committee Interlocks and Insider Participation |

106 |

| CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS | 106 |

|

Transactions with Related Persons |

106 |

|

Policies and Procedures for Review, Approval or Ratification of Transactions with Related Persons |

106 |

| PROPOSAL FOUR—RATIFICATION OF SELECTION OF INDEPENDENT AUDITORS | 107 |

|

Independent Registered Public Accounting Firm’s Fees |

107 |

|

Pre-Approval Policies and Procedures |

108 |

| PROPOSAL FIVE—ADVISORY VOTE ON EXECUTIVE COMPENSATION | 108 |

| PROPOSAL SIX—ADVISORY VOTE ON THE FREQUENCY OF | 108 |

| AN ADVISORY VOTE ON EXECUTIVE COMPENSATION | |

| STOCKHOLDER PROPOSALS AND NOMINATIONS | 109 |

| CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS | 110 |

| WHERE YOU CAN FIND MORE INFORMATION | 110 |

| ANNEX A: MERGER AGREEMENT | A-1 |

| ANNEX B: FINANCIAL ADVISOR OPINION | B-1 |

| ANNEX C: DELAWARE GENERAL CORPORATION LAW SECTION 262 | C-1 |

v

CHINA SECURITY & SURVEILLANCE TECHNOLOGY, INC.

ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON SEPTEMBER 14, 2011

PROXY STATEMENT

This proxy statement contains information related to an annual meeting of stockholders of China Security & Surveillance Technology, Inc. (the “Company,” “we,” “us” or “our”) which will be held at 10:00 a.m., local time, on September 14, 2011, at the Company’s office at 13/F, Shenzhen Special Zone Press Tower, Shennan Road, Futian District, Shenzhen 518034, the People's Republic of China, and any adjournments or postponements thereof. We are furnishing this proxy statement to stockholders of China Security & Surveillance Technology, Inc. as part of the solicitation of proxies by the Company’s board of directors for use at the annual meeting. This proxy statement is dated August [ ], 2011 and is first being mailed to stockholders on or about August [ ], 2011.

SUMMARY TERM SHEET RELATED TO THE MERGER

This summary term sheet highlights selected information in this proxy statement regarding the merger and may not contain all of the information about the merger that is important to you. We have included page references in parentheses to direct you to more complete descriptions of the topics presented in this summary term sheet. You should carefully read this proxy statement in its entirety, including the annexes and the other documents to which we have referred you, for a more complete understanding of the matters being considered at the annual meeting. You may obtain without charge copies of documents incorporated by reference into this proxy statement by following the instructions under “Where You Can Find More Information” beginning on page 110. In this proxy statement, the terms “we,” “us,” “our,” “CSST” and the “Company” refer to China Security & Surveillance Technology, Inc. and its subsidiaries. We refer to Intelligent One Limited as “Intelligent One,” Whitehorse Technology Limited as “Whitehorse,” Rightmark Holdings Limited as “Parent” and Rightmark Merger Sub Limited as “Merger Sub.” We refer to Wing Khai Yap (Terence), Lizhong Wang, Zhongxin Xie, Lingfeng Xiong, Li Fang, Ying Zhang, Zhiming Wu, Daobin Sang, Guohui Cao, Po Kwai Chow, Yang Zhao, Yujuan Guan, Zhuo Gong, Xihong Dai, Qiaomin Wu, Kaicheng Cheng, Lei Wang and Xiaosheng Tong, each of whom is a member of the Company’s management or the nominee of a member of the Company’s management team, and together with Guoshen Tu (“Mr. Tu”), as the “Rollover Stockholders” and Parent, Merger Sub, Intelligent One, Whitehorse and the Rollover Stockholders, collectively as the “Tu Parties.” When we refer to the “merger agreement” we mean either the Agreement and Plan of Merger, dated as of April 20, 2011, or the Amended and Restated Agreement and Plan of Merger, dated as of May 3, 2011, as applicable, each among the Company, Parent, Merger Sub and Mr. Tu (solely for the purposes of Section 6.15 therein).

The Parties (page 18)

China Security & Surveillance Technology, Inc. is a leading integrated surveillance and safety solutions provider in China. Through its indirect Chinese subsidiaries, the Company is primarily engaged in the manufacturing, distributing, installing and servicing of surveillance and safety products, systems and services, and developing surveillance and safety related software in China. Both Parent and Merger Sub were formed for the sole purpose of entering into the merger agreement and consummating the transactions contemplated by the merger agreement. Both Parent and Merger Sub were formed and are beneficially owned by Mr. Tu.

Mr. Tu, the Chairman and Chief Executive Officer of the Company, beneficially owns approximately 20.9% of the total number of outstanding shares of Company common stock.

The Rollover Stockholders, including Mr. Tu, beneficially own approximately 24.20% of the total number of outstanding shares of Company common stock. The Rollover Stockholders have agreed with Parent to contribute to Parent the shares of Company common stock owned by them (the “Rollover Shares”) in exchange for equity securities of Intelligent One immediately prior to the completion of the merger pursuant to a letter agreement (the “rollover agreement”) or, if and to the extent, agreed between Parent and a Rollover Stockholder, in exchange for an amount in cash equal to $6.50 per share multiplied by the number of the relevant Rollover Shares.

Overview of the Transaction (page 21)

The Company, Parent, Merger Sub and Mr. Tu entered into the merger agreement on April 20, 2011, as amended and restated by the merger agreement entered into by the parties on May 3, 2011. Under the terms of the merger agreement, Merger Sub will be merged with and into the Company, with the Company surviving the merger as a wholly owned subsidiary of Parent (the “merger”). The Company, as the surviving corporation, will continue to do business under the name “China Security & Surveillance Technology, Inc.” following the merger. Both Parent and Merger Sub were formed and are beneficially owned by Mr. Tu. The following will occur in connection with the merger:

-

each share of Company common stock issued and outstanding immediately prior to the merger (other than shares owned by Parent, Merger Sub and their affiliates, the Rollover Stockholders and holders of the Dissenting Shares (as such term is defined in this proxy statement)) will be converted into the right to receive the per share merger consideration, as described below;

-

each share of Company common stock that, immediately prior to the effective time of the merger, is subject to vesting and/or forfeiture restrictions under the equity incentive plan adopted by the board of directors of the Company on February 7, 2007 and subsequently amended in February 2010 shall become fully vested immediately prior to the effective time, and each such share shall be treated as a share of Company common stock;

-

each warrant to purchase shares of Company common stock issued that is outstanding at the effective time shall be canceled and, in exchange therefor, the surviving corporation shall pay to each former holder of any such canceled warrant immediately following the effective time an amount in cash (without interest) equal to the product of (i) the excess of the per share merger consideration over the exercise price per share of Company common stock of such warrant and (ii) the number of shares of Company common stock subject to such warrant; provided, that if the exercise price per share of Company common stock of any such warrant is equal to or greater than the per share merger consideration, such warrant shall be canceled without any cash payment being made in respect thereof. See “The Merger Agreement—Treatment of Common Stock, Restricted Shares and Company Warrants” beginning on page 67 for additional information; and

-

all shares of Company common stock so converted will, at the closing of the merger, be canceled, and each holder of a certificate (or evidence of shares in book-entry form) representing any shares of Company common stock shall cease to have any rights with respect thereto, except the right to receive the per share merger consideration upon surrender of such certificate (if such shares are certificated).

Following and as a result of the merger:

-

Company stockholders (other than the Rollover Stockholders) will no longer have any interest in, and will no longer be stockholders of, the Company, and will not participate in any of the Company’s future earnings or growth;

-

shares of Company common stock will no longer be listed on the New York Stock Exchange (“NYSE”) or NASDAQ Dubai, and price quotations with respect to shares of Company common stock in the public market will no longer be available; and

-

the registration of shares of Company common stock under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) will be terminated.

2

The Annual Meeting (page 61)

The annual meeting will be held at 10:00 a.m., local time, on September 14, 2011, at the Company’s office at 13/F, Shenzhen Special Zone Press Tower, Shennan Road, Futian District, Shenzhen 518034, the People's Republic of China. At the annual meeting, you will be asked to, among other things, adopt the merger agreement. See “Questions and Answers About the Annual Meeting and the Merger” for additional information on the annual meeting, including how to vote your shares of Company common stock.

Stockholders Entitled to Vote; Vote Required to Adopt the Merger Agreement (page 62)

You may vote at the annual meeting if you owned any shares of Company common stock at the close of business, New York time, on August 5, 2011, the record date for the annual meeting. On that date, there were 89,716,630 shares of Company common stock outstanding and entitled to vote at the annual meeting. You may cast one vote for each share of Company common stock that you owned on that date. Adoption of the merger agreement requires the affirmative vote of (i) stockholders holding at least a majority of the outstanding shares of the Company’s common stock at the close of business, New York time, on the record date and (ii) stockholders holding at least a majority of the outstanding shares of the Company’s common stock at the close of business, New York time, on the record date other than shares owned, directly or indirectly, by Parent, Merger Sub, the Rollover Stockholders or any of their respective affiliates. Given that 89,716,630 shares of Company common stock are outstanding on the record date, at least 34,004,102 shares of Company common stock owned by unaffiliated stockholders must be voted in favor of the proposal to adopt the merger agreement in order for the proposal to be approved pursuant to the approval requirement set forth in (ii). See “The Annual Meeting” beginning on page 61 for additional information.

Merger Consideration (page 67)

If the merger is completed, each share of Company common stock, other than as provided below, will be converted into the right to receive $6.50 in cash, without interest. We refer to this amount as the “per share merger consideration.” Common stock owned by Parent or Merger Sub and shares of Company common stock contributed to Parent by the Rollover Stockholders will be canceled without payment of per share merger consideration. Shares of Company common stock owned by stockholders who have exercised, perfected and not withdrawn a demand for, or lost the right to, appraisal rights under the Delaware General Corporation Law (“DGCL”) will be canceled without payment of per share merger consideration and such stockholders will instead be entitled to appraisal rights under the DGCL.

A paying agent will send written instructions for surrendering your certificates representing shares of Company common stock (if your shares of Company common stock are certificated) and obtaining the per share merger consideration after we have completed the merger. Do not return your stock certificates with your proxy card and do not forward your stock certificates to the paying agent prior to receipt of the written instructions. If you hold uncertificated shares of Company common stock (i.e., you hold your shares in book-form entry), you will automatically receive your per share merger consideration as soon as practicable after the effective time of the merger without any further action required on your part. See “The Merger Agreement—Treatment of Common Stock, Restricted Shares and Company Warrants” and “The Merger Agreement—Exchange and Payment Procedures” beginning on page 67 for additional information.

Treatment of Restricted Stock and Company Warrants (page 67)

The merger agreement provides that, each share of Company common stock that, immediately prior to the effective time of the merger, is subject to vesting and/or forfeiture restrictions under the equity incentive plan adopted by the board of directors of the Company on February 7, 2007 and subsequently amended in February 2010 shall become fully vested immediately prior to the effective time, and each such share shall be treated as a share of Company common stock.

At the effective time, each warrant to purchase shares of Company common stock issued that is outstanding at the effective time shall be canceled and, in exchange therefor, the surviving corporation shall pay to each former holder of any such canceled warrant immediately following the effective time an amount in cash (without interest) equal to the product of (i) the excess of the per share merger consideration over the exercise price per share of Company common stock of such warrant and (ii) the number of shares of Company common stock subject to such warrant; provided, that if the exercise price per share of Company common stock of any such warrant is equal to or greater than the per share merger consideration, such warrant shall be canceled without any cash payment being made in respect thereof. See “The Merger Agreement—Treatment of Common Stock, Restricted Shares and Company Warrants” beginning on page 67 for additional information.

3

Recommendation of Our Board of Directors and Special Committee; Reasons for Recommending the Adoption of the Merger Agreement; Fairness of the Merger (page 31)

Our board of directors, after careful consideration and acting on the unanimous recommendation of the special committee composed entirely of independent directors, recommends that you vote “FOR” the proposal to adopt the merger agreement and “FOR” the proposal to approve the adjournment of the annual meeting, if necessary or appropriate, to solicit additional proxies if there are insufficient votes at the time of the annual meeting to adopt the merger agreement. Our board of directors and the special committee believe that the merger is fair to our stockholders. For a discussion of the material factors considered by our board of directors and the special committee in determining to recommend the adoption of the merger agreement and in determining that the merger is fair to our stockholders, see “Special Factors Relating to the Merger—Purposes and Reasons of Our Board of Directors and Special Committee for the Merger” beginning on page 30 and “Special Factors Relating to the Merger—Recommendation of Our Board of Directors and Special Committee; Reasons for Recommending the Adoption of the Merger Agreement; Fairness of the Merger” beginning on page 31 for additional information.

Positions of the Tu Parties Regarding the Fairness of the Merger (page 44)

Each of the Tu Parties believes that the merger is fair to our stockholders, other than the Rollover Stockholders. Their belief is based upon the factors discussed under the captions, “Special Factors Relating to the Merger—Positions of the Tu Parties Regarding the Fairness of the Merger” beginning on page 44, “Special Factors Relating to the Merger—Purposes and Reasons of Our Board of Directors and Special Committee for the Merger” beginning on page 30 and “Special Factors Relating to the Merger—Recommendation of Our Board of Directors and Special Committee; Reasons for Recommending the Adoption of the Merger Agreement; Fairness of the Merger” beginning on page 31.

Opinion of Imperial Capital, Financial Advisor to the Special Committee (page 38)

In connection with the merger, the special committee received a written opinion from Imperial Capital, LLC (“Imperial Capital”), financial advisor to the special committee, as to the fairness, from a financial point of view and as of the date of its opinion, of the per share merger consideration to be received by the holders of the Company common stock (other than Parent, Merger Sub and their affiliates, holders of the Dissenting Shares and the Rollover Stockholders (as each such term is defined in this proxy statement)). The full text of Imperial Capital’s written opinion, dated May 3, 2011, is attached to this proxy statement as Annex B. Holders of Company common stock are encouraged to read this opinion carefully in its entirety for a description of the assumptions made, procedures followed, matters considered and limitations on the review undertaken. Imperial Capital’s opinion was provided to the special committee in connection with, and for the purposes of, its evaluation of the per share merger consideration from a financial point of view, does not address the merits of the underlying decision by the Company to engage in the merger or the relative merits of any alternatives discussed by the special committee and the board of directors of the Company, does not constitute an opinion with respect to the Company’s underlying business decision to effect the merger, any legal, tax or accounting issues concerning the merger, or any terms of the merger (other than the per share merger consideration) and does not constitute a recommendation as to any vote or action the Company or any stockholders of the Company should take in connection with the merger or any aspect thereof.

For a more complete description of Imperial Capital’s opinion, see “Special Factors Relating to the Merger—Opinion of Imperial Capital, Financial Advisor to the Special Committee” beginning on page 38 for additional information. See also Annex B to this proxy statement.

Financing of the Merger (page 52)

Parent estimates that the total amount of funds required to complete the merger and related transactions, including payment of fees and expenses in connection with the merger, is anticipated to be approximately $594,975,018. This amount is expected to be provided through a combination of rollover financing from the Rollover Stockholders totaling approximately $141,104,782, and debt financing of up to $500 million. See “Special Factors Relating to the Merger—Financing of the Merger” beginning on page 52 for additional information.

4

Limited Guaranty (page 53)

Mr. Tu has agreed to guarantee the obligations of Parent under the merger agreement to pay, under certain circumstances, a reverse termination fee and reimburse certain expenses. See “Special Factors Relating to the Merger—Limited Guaranty” beginning on page 53 for additional information.

Rollover Agreement (page 53)

Pursuant to a rollover agreement, at or prior to the effective time of the merger, the Rollover Stockholders will contribute to Parent an aggregate amount of 21,708,428 shares of Company common stock beneficially owned by them in exchange for equity securities of Intelligent One or, if agreed between Parent and a Rollover Stockholder, in exchange for an amount in cash equal to $6.50 per share multiplied by the number of the relevant Rollover Shares. See “Special Factors Relating to the Merger—Financing of the Merger—Rollover Financing” beginning on page 53 for additional information.

Interests of the Company’s Directors and Officers in the Merger (page 54)

When considering the recommendation of our board of directors in favor of the adoption of the merger agreement, you should be aware that the members of our board of directors and certain of our officers have interests in the merger in addition to their interests as our stockholders generally. These interests may be different from, or in addition to, your interests as our stockholders. These interests include acceleration of vesting of their restricted stock, the ownership of equity interests in Parent by Mr. Tu, the rollover arrangement, compensation to members of special committee and the maintenance of indemnification rights and insurance coverage. The members of our board of directors were aware of these additional interests, and considered them, when they approved the merger agreement, the merger and the other transactions contemplated by the merger agreement.

Conditions to the Merger (page 77)

The respective obligations of each of the Company, Parent and Merger Sub to consummate the merger are subject to the satisfaction or waiver of certain conditions. For a more detailed description of these conditions, please see “The Merger Agreement—Conditions to the Merger” beginning on page 77.

Regulatory Matters (page 56)

The Company does not believe that any material federal, national, provincial, local or state, whether domestic or foreign, regulatory approvals, filings or notices are required in connection with the merger other than the approvals, filings or notices required under the U.S. federal securities laws and the filing of a certificate of merger with the Secretary of State of the State of Delaware with respect to the merger.

Alternative Takeover Proposals (page 73)

Until 11:59 p.m. New York City time on July 2, 2011 the Company is permitted to:

-

initiate, solicit and encourage any inquiry or the making of takeover proposals from third parties, including through public disclosure or by providing third parties non-public information pursuant to acceptable confidentiality agreements (provided that the Company promptly make such information available to Parent if not previously made available to Parent); and

-

enter into and maintain discussions or negotiations with any person with respect to any takeover proposal, or otherwise cooperate with or assist such inquiries, proposals, discussions or negotiations.

From and after 12:00 a.m. New York City time on July 3, 2011, the Company is required to immediately cease any discussions or negotiations with any persons that may be ongoing with respect to any takeover proposals, except as may relate to excluded parties (as defined below). From and after 12:00 a.m. New York City time on July 3, 2011 until the effective time or, if earlier, the termination of the merger agreement, the Company will not:

5

-

initiate, solicit, knowingly encourage or knowingly induce the making of takeover proposals from third parties;

-

provide any material non-public information to a third party in connection with a takeover proposal; or

-

engage in discussions or negotiations with any third party concerning a takeover proposal

Notwithstanding the foregoing, the Company may continue to engage in the activities permitted during the period prior to 11:59 p.m. New York City time on July 2, 2011 described above with an excluded party. In this proxy statement, we refer to any person that has submitted a takeover proposal after the execution of the merger agreement and prior to 11:59 p.m. New York City time on July 2, 2011 that the board of directors and the special committee determine in good faith (after consultation with its financial and legal advisors) constitutes or would reasonably be expected to result in a superior proposal as an “excluded party”; provided, however, that such person will cease to be an excluded party at such time as the takeover proposal made by such person is withdrawn, is terminated or expires, or the board of directors and the special committee determine in good faith (after consultation with its financial and legal advisors) ceases to constitute or ceases to be reasonably likely to lead to a superior proposal.

Prior to the time the Company’s stockholders adopt the merger agreement, if the Company receives an unsolicited takeover proposal from a third party that the special committee determines in good faith (after consultation with its financial and legal advisors) could result in a superior proposal, the Company may:

-

furnish information to such party pursuant to an acceptable confidentiality agreement; and

-

engage in discussions or negotiations with such party.

From and after 12:00 a.m. New York City time on July 3, 2011, the Company must advise Parent within 48 hours, orally and then in writing as promptly as practicable, of any takeover proposal, any initial request for non-public information and any initial request for discussions or negotiations related to a takeover proposal, received after 12:00 a.m. New York City time on July 3, 2011. In connection with such notice, Company must also provide the material terms and conditions and the identity of the third party make the takeover proposal or request. The Company must also keep Parent reasonably informed in all material respects of the status and details of such takeover proposal or request received after 12:00 a.m. New York City time on July 3, 2011.

The board of directors of the Company cannot effect a “change of recommendation” (as defined in “The Merger Agreement—Alternative Takeover Proposals”) or allow the Company to execute or enter into, any “Company acquisition agreement” (as defined in “The Merger Agreement—Alternative Takeover Proposals”) related to any takeover proposal. Notwithstanding the foregoing, at any time prior to the receipt of the requisite stockholder approvals of the merger, (x) if the special committee determines in good faith (after consultation with the Company’s outside legal advisors) that the failure to do so could likely be inconsistent with its fiduciary duties, then the board of directors of the Company, acting upon the recommendation of the special committee, may make a change of recommendation; and (y) if the board of directors of the Company determines in good faith (after consultation with the Company’s outside financial and legal advisors) that a takeover proposal constitutes a superior proposal, then the Company may make a change of recommendation, enter into a Company acquisition agreement with respect to such superior proposal and/or terminate the merger agreement.

The Company is not entitled to effect a change of recommendation or terminate the merger agreement unless (i) the Company has provided written notice at least three business days in advance to Parent and Merger Sub advising Parent that the board of directors of the Company intends to make a change of recommendation or enter into a Company acquisition agreement and specifying the reasons for the proposed action and, if a change of recommendation is being made as a result of a superior proposal, the terms and conditions of such takeover proposal (including the identity of the third party making the takeover proposal and any related financing materials) and (ii) with respect to a takeover proposal received on or after 12:00 a.m. New York City time on July 3, 2011, in addition to providing a written notice of a superior proposal to Parent, during the three business day period following Parent’s and Merger Sub’s receipt of such written notice, the Company will negotiate with Parent and Merger Sub in good faith (if Parent and Merger Sub desire to negotiate) to make such adjustments in the terms and conditions of the merger agreement and the facility agreement entered into between Parent and China Development Bank Hong Kong Branch (“CDB”), Parent’s lender, so that such superior proposal no longer constitutes a superior proposal, and following the end of the three business day period, the board of directors of the Company and the special committee will have determined in good faith, taking into account any changes to the merger agreement and the facility agreement proposed by Parent and Merger Sub, that the takeover proposal giving rise to such written notice continues to be a superior proposal. Any material amendment to the financial terms or any other material amendment of such superior proposal will require a new written notice and the Company will be required to comply again with the procedures in this paragraph.

6

The Company is not restricted from issuing a “stop, look and listen” communication pursuant to Rule 14d-9(f) promulgated under the Exchange Act or taking or disclosing to its stockholders any position contemplated by Rule 14e-2(a) or Rule 14d-9 promulgated under the Exchange Act or from making any other disclosure to its stockholders to comply with applicable law.

The Company has the right to reimburse the reasonable out-of-pocket expenses of any person who has submitted a takeover proposal prior to the receipt of the requisite stockholder approvals of the merger, if (i) the special committee determines in good faith that such takeover proposal constitutes a superior proposal and intends to change its recommendation, (ii) in response to the intended change of recommendation, Parent revises the terms and conditions of the merger agreement and (iii) the Company does not change its recommendation with respect to such a takeover proposal because the special committee determines that the takeover proposal submitted by such person no longer constitutes a superior proposal in consideration of the revisions to the merger agreement submitted by Parent.

As used in this proxy statement, the following terms shall have the following meanings:

The term “takeover proposal” means any proposal or offer made by any third party to purchase or otherwise acquire (A) beneficial ownership (as defined under section 13(d) of the Exchange Act) of 20% or more of any class of equity securities of the Company pursuant to a merger, consolidation or other business combination, sale of shares of capital stock, tender offer, exchange offer or similar transaction or (B) any one or more assets or businesses of the Company that constitute 20% or more of the revenues or assets of the Company.

The term “superior proposal” means a written takeover proposal (provided that for purposes of this definition, references to “20%” in the definition of takeover proposal shall be deemed to be references to “50%”) on terms which the board of directors of the Company and special committee determines in good faith (after consultation with the Company’s outside legal and financial advisors) to be more favorable to the Company’s stockholders from a financial point of view than the terms of the merger agreement (taking into account such factors as the board of directors of the Company deems appropriate including any changes to the terms of the merger agreement proposed by Parent) and to be reasonably capable of being consummated on the terms proposed.

Termination of the Merger Agreement (page 78)

The merger agreement may be terminated at any time prior to the consummation of the merger, whether before or after requisite stockholder approvals of the merger have been obtained:

by mutual written agreement of the Company and Parent;

by either of the Company or Parent, if:

-

any governmental entity has issued a final order, injunction or decree permanently enjoining or otherwise prohibiting consummation of the merger; provided, that this termination right is not available to a party if the failure of such party to fulfill any of its obligations under the merger agreement is the primary cause or material contributing factor to the denial of such approval, or issuance of such final order, injunction or decree;

7

-

the merger is not completed by April 20, 2012 (the “termination date”), provided that this termination right will not be available to a party if the failure to consummate the merger on or before the termination date was primarily due to the breach or failure of such party to fulfill any of its obligations under the merger agreement; or

-

our stockholders do not adopt the merger agreement at the annual meeting or any adjournment or postponement thereof.

by the Company:

-

if Parent or Merger Sub has breached any of its representations, warranties, covenants or agreements under the merger agreement, such that the corresponding condition to closing would not be satisfied and such breach or inaccuracy cannot be cured or if curable, is not cured by Parent or Merger Sub within 30 business days after written notice of such breach or if earlier, by the termination date, provided that this termination right is not available to the Company if a material breach of the merger agreement by the Company is the primary cause or material contributing factor to the failure of such condition to be satisfied;

-

if the Company enters into a Company acquisition agreement relating to a superior proposal and has complied with the requirements described under “The Merger Agreement—Alternative Takeover Proposals,” and concurrently with such termination, the Company pays the termination fee described under “The Merger Agreement—Termination Fees and Reimbursement of Expenses”;

-

if all of the closing conditions are otherwise satisfied but Parent and Merger Sub fail to close within two business days following the date the closing should have occurred, the Company has notified Parent in writing that it is ready to close and the Company has given Parent written notice of at least one business day of its intention to terminate the merger agreement; or

-

for any reason on or prior to May 4, 2011;

by Parent, if:

-

if the Company has breached any of its representations, warranties, covenants or agreements under the merger agreement, such that the corresponding condition to closing would not be satisfied and such breach or inaccuracy cannot be cured or if curable, is not cured by the Company within 30 business days after written notice of such breach, or if earlier, by the termination date, provided that this termination right is not available to Parent if a material breach of the merger agreement by Parent or Merger Sub is the primary cause or material contributing factor to the failure of such condition to be satisfied; or

-

the board of directors of the Company has made and not withdrawn a change of recommendation.

Termination Fees and Reimbursement of Expenses (page 79)

The Company is required to pay Parent a termination fee of $5.0 million and fees and expenses incurred by Parent of up to $1.0 million in the event the merger agreement is terminated by the Company in order to enter into a Company acquisition agreement relating to a superior proposal in connection with a takeover proposal received on or prior to 11:59 p.m. New York City time on July 2, 2011.

The Company is required to pay Parent a termination fee of $10.0 million in the event the merger agreement is terminated:

-

by the Company in order to enter into a Company acquisition agreement for a superior proposal in connection with a takeover proposal received on or after 12:00 a.m. New York City time on July 3, 2011;

8

-

by Parent or the Company due to (a)(i) a failure of either the Company or Parent to consummate the merger by the termination date or (ii) a failure by the Company to obtain the requisite stockholder approvals of the merger and (b) on or after the signing of the merger agreement but prior to the date of the stockholders’ meeting, a third party makes a takeover proposal which is publicly disclosed and not withdrawn and (c) within 12 months following such termination, the Company consummates or enters into a transaction with respect to such takeover proposal;

-

by Parent because the board of directors of the Company has made and not withdrawn a change of recommendation or has proposed to publicly announce its intention make such change of recommendation; or

-

the board of directors of the Company has adopted, approved or recommended or proposes publicly to adopt, approve or recommend an alternative transaction proposal.

Parent is required to pay the Company a reverse termination fee of $20.0 million in the event the merger agreement is terminated by the Company:

-

due to a breach by Parent or Merger Sub of any of their representations, warranties, covenants or agreements set forth in the merger agreement; or

-

if all of the closing conditions are otherwise satisfied but Parent and Merger Sub fail to close within two business days following the date the closing should have occurred, the Company has notified Parent in writing that it is ready to close and the Company has given Parent written notice of at least one business day of its intention to terminate the merger agreement.

Remedies (page 80)

Subject to any equitable remedies the Company may be entitled to, our right to receive payment under certain circumstances specified in the merger agreement of a reverse termination fee of $20.0 million in connection with the merger from Parent or Merger Sub is our sole and exclusive remedy for any loss or damage suffered as a result of the failure of the merger to be consummated or for a breach or failure to perform under the merger agreement or otherwise. Upon payment of such reverse termination fee, Parent, its subsidiaries and their respective representatives will have no further liability under the merger agreement.

Subject to any equitable remedies Parent or Merger Sub may be entitled to, Parent’s and Merger Sub’s right to receive payment under certain circumstances specified in the merger agreement of either (i) a termination fee of $10.0 million or (ii) a termination fee of $5.0 million plus Parent’s and Merger Sub’s out-of-pocket costs and expenses (up to $1.0 million) incurred in connection with the merger from us is the sole and exclusive remedy of Parent and Merger Sub against us for any loss or damage suffered as a result of the failure of the merger to be consummated or for a breach or failure to perform under the merger agreement or otherwise and upon payment of such amount, the Company, its subsidiaries and their respective representatives will have no further liability under the merger agreement.

The Company, Parent and Merger Sub are entitled to an injunction or injunctions to prevent breaches of the merger agreement and to enforce specifically the terms and provisions thereof, in addition to any other remedies under the merger agreement. The Company is not entitled to receive both a grant of specific performance that results in the consummation of the merger and payment of all or any portion of the reverse termination fee.

Appraisal Rights (page 83)

If the merger is consummated, persons who are stockholders of the Company will have certain rights under Delaware law to dissent and demand appraisal of, and payment in cash of the fair value of, their shares of Company common stock (“Dissenting Shares”). Any shares of Company common stock held by a person who does not vote in favor of adoption of the merger agreement, demands appraisal of such shares of Company common stock and complies with the applicable provisions of Delaware law will not be converted into the right to receive the per share merger consideration. Such appraisal rights, if the statutory procedures were complied with, will lead to a judicial determination of the fair value (excluding any element of value arising from the accomplishment or expectation of the merger) required to be paid in cash to such dissenting stockholders for their shares of Company common stock. The value so determined could be more or less than, or the same as, per share merger consideration.

9

You should read “Appraisal Rights” beginning on page 83 for a more complete discussion of the appraisal rights in relation to the merger as well as Annex C which contains a full text of the applicable Delaware statute.

Litigation Relating to the Merger and Other Legal Proceedings (page 59)

The Company, certain officers of the Company, the members of the board of directors and Merger Sub are named as defendants in purported class action lawsuits brought by stockholders of the Company. The lawsuits allege, among other things, that the members of the board of directors breached their fiduciary duties owed to the Company’s stockholders and seek, among other things, to enjoin the defendants from completing the merger on the agreed-upon terms.

One of the conditions to the closing of the merger is that no order, injunction or decree issued by any court or agency of competent jurisdiction or other law preventing or making illegal the consummation of the merger or any of the other transactions contemplated by the merger agreement shall be in effect. As such, if the plaintiffs are successful in obtaining an injunction prohibiting the defendants from completing the merger on the agreed-upon terms, then such injunction may prevent the merger from becoming effective, or from becoming effective within the expected time frame.

In September 2010, we were notified by the staff of the SEC that it had initiated a formal, nonpublic investigation of the Company (the “SEC Investigation”). On or around September 3, 2010 and March 29, 2011, we received two subpoenas from the SEC requesting the delivery of certain documents to the SEC. We are cooperating, and intend to continue to cooperate, with the SEC in connection with such investigation. Receipt of these subpoenas does not mean that the SEC has concluded that we or anyone else has violated the law. The investigation does not mean that the SEC has a negative opinion of any person, entity or security. It is not possible to predict the outcome of the investigation, including whether or when any proceedings might be initiated, when these matters may be resolved or what, if any, penalties or other remedies may be imposed.

Material United States Federal Income Tax Consequences (page 56)

The receipt of cash in exchange for Company common stock pursuant to the merger will be a taxable transaction for U.S. federal income tax purposes and may also be taxable under applicable state, local, foreign or other tax laws. In general a U.S. Holder (as defined under “Material United States Federal Income Tax Consequences”) of Company common stock will recognize gain or loss in an amount equal to the difference, if any, between the amount of cash received in the merger and the U.S. Holder’s adjusted tax basis in the shares of Company common stock. In general, a Non-U.S. Holder (as defined under “Material United States Federal Income Tax Consequences”) of shares of Company common stock will not be subject to U.S. federal income tax in respect of cash received in the merger, unless such Non-U.S. Holder has certain connections to the United States. Holders of Company common stock should consult their tax advisors to determine the particular tax consequences to them (including the application and effect of any state, local or foreign income and other tax laws) of the merger.

Material PRC Tax Consequences (page 58)

Under the PRC Enterprise Income Tax Law (the “EIT Law”), which took effect on January 1, 2008, enterprises established outside of China whose “de facto management bodies” are located in the People’s Republic of China (“PRC”) are considered “resident enterprises.” The implementation rules for the EIT Law define the “de facto management body” as an establishment that has substantial management and control over the business, personnel, accounts and properties of an enterprise. Although there has not been a definitive determination of the Company’s status by the PRC tax authorities, the Company does not believe that it should be considered a resident enterprise under the EIT Law or that the gain recognized on the receipt of cash for Company common stock should otherwise be subject to PRC tax to holders of such common stock that are not PRC residents. If, however, the PRC tax authorities were to determine that the Company should be considered a resident enterprise or that the receipt of cash for these securities should otherwise be subject to PRC tax, then gain recognized on the receipt of cash for Company common stock pursuant to the merger by holders of such securities who are not PRC residents could be treated as PRC-source income that would be subject to PRC tax at a rate of up to 10%. You should consult your own tax advisor for a full understanding of the tax consequences of the merger to you, including any PRC tax consequences.

10

Where You Can Find More Information (page 110)

You can find more information about the Company in the periodic reports and other information we file with the SEC. The information is available at the SEC’s public reference facilities and at the website maintained by the SEC at www.sec.gov. For a more detailed description of the additional information available, please see the section entitled “Where You Can Find More Information” beginning on page 110.

11

QUESTIONS AND ANSWERS ABOUT THE ANNUAL MEETING AND THE MERGER

| Q: |

When and where is the annual meeting of our stockholders? | |

| A: |

The annual meeting of stockholders will be held at 10:00 a.m., local time, on September 14, 2011, at the Company’s office at 13/F, Shenzhen Special Zone Press Tower, Shennan Road, Futian District, Shenzhen 518034, the People's Republic of China. | |

| Q: |

Why am I receiving this proxy statement? | |

| A: |

You are receiving this proxy statement in connection with the solicitation of proxies by the board of directors of the Company in favor of, among other things, the adoption of the merger agreement. On May 3, 2011, we entered into the merger agreement, with Parent, Merger Sub and Mr. Tu providing for the merger of Merger Sub with and into the Company, with the Company surviving the merger as a wholly owned subsidiary of Parent. After the merger, shares of the Company common stock will not be publicly traded. Parent and Merger Sub are beneficially owned by Mr. Tu, the Chairman and Chief Executive Officer of the Company. | |

| Q: |

What matters will be voted on at the annual meeting? | |

| A: |

You will be asked to consider and vote on the following proposals: | |

|

|

adoption of the merger agreement; | |

|

|

approval of the adjournment of the annual meeting, if necessary or appropriate, to solicit additional proxies if there are insufficient votes at the time of the annual meeting to adopt the merger agreement; | |

|

|

election of five persons to the board of directors of the Company; | |

|

|

ratification the selection by our Audit Committee of GHP Horwath, P.C. as the Company’s independent registered public accounting firm for the fiscal year ending December 31, 2011; | |

|

|

approval, on an advisory basis, of the executive compensation; | |

|

|

approval, on an advisory basis, of the frequency of holding an advisory vote on executive compensation; and | |

|

|

such other business as may properly come before the annual meeting or any adjournment thereof. | |

| Q: |

As a stockholder, what will I receive in the merger? | |

| A: |

If the merger is completed, you will be entitled to receive $6.50 in cash, without interest thereon, for each share of Company common stock that you own immediately prior to the effective time of the merger as described in the merger agreement. | |

|

See “Special Factors Relating to the Merger—Material United States Federal Income Tax Consequences” and “—Material PRC Tax Consequences” beginning on pages 56 and 58, respectively, for a more detailed description of the U.S. federal and PRC tax consequences of the merger. You should consult your own tax advisor for a full understanding of how the merger will affect your U.S. federal, state, local, PRC and/or other non-U.S. taxes. | ||

| Q: |

When will I receive the merger consideration for my shares of Company common stock? | |

| A: |

After the merger is completed, you will receive written instructions, including a letter of transmittal, that explain how to exchange your shares for the $6.50 per share merger consideration. When you properly complete and return the required documentation described in the written instructions, you will promptly receive from the paying agent payment of the merger consideration for your shares. | |

12

| Q: |