UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-21413

Name of Fund: BlackRock Floating Rate Income Strategies Fund, Inc. (FRA)

Fund Address: 100 Bellevue Parkway, Wilmington, DE 19809

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock Floating

Rate Income Strategies Fund, Inc., 55 East 52nd Street, New York, NY 10055

Registrant’s telephone number, including area code: (800) 882-0052, Option 4

Date of fiscal year end: 08/31/2019

Date of reporting period: 08/31/2019

Item 1 – Report to Stockholders

AUGUST 31, 2019

| ANNUAL REPORT |

|

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA)

BlackRock Limited Duration Income Trust (BLW)

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of each Fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from BlackRock or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive all future reports in paper free of charge. If you hold accounts directly with BlackRock, you can call Computershare at (800) 699-1236 to request that you continue receiving paper copies of your shareholder reports. If you hold accounts through a financial intermediary, you can follow the instructions included with this disclosure, if applicable, or contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. Please note that not all financial intermediaries may offer this service. Your election to receive reports in paper will apply to all funds advised by BlackRock Advisors, LLC or its affiliates, or all funds held with your financial intermediary, as applicable.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive electronic delivery of shareholder reports and other communications by contacting your financial intermediary, if you hold accounts through a financial intermediary. Please note that not all financial intermediaries may offer this service.

| Not FDIC Insured • May Lose Value • No Bank Guarantee |

Supplemental Information

On September 5, 2019, the Funds, acting pursuant to a U.S. Securities and Exchange Commission (“SEC”) exemptive order and with the approval of each Fund’s Board of Directors (the “Board”), each adopted a managed distribution plan, consistent with its investment objectives and policies to support a level distribution of income, capital gains and/or return of capital (the “Plan”). In accordance with the Plans, starting in October 2019, FRA will distribute a fixed amount of $0.0788 per share on a monthly basis and BLW will distribute a fixed amount of $0.0981 per share on a monthly basis.

The fixed amounts distributed per share are subject to change at the discretion of each Fund’s Board. Under its Plan, each Fund will distribute all available investment income to its shareholders as required by the Internal Revenue Code of 1986, as amended (the “Code”). If sufficient income (inclusive of net investment income and short-term capital gains) is not earned on a monthly basis, the Funds will distribute long-term capital gains and/or return of capital to shareholders in order to maintain a level distribution. Each monthly distribution to shareholders is expected to be at the fixed amount established by the Board; however, each Fund may make additional distributions from time to time, including additional capital gain distributions at the end of the taxable year, if required to meet requirements imposed by the Code and/or the Investment Company Act of 1940, as amended (the “1940 Act”).

Shareholders should not draw any conclusions about each Fund’s investment performance from the amount of these distributions or from the terms of the Plan. Each Fund’s total return performance is presented in its financial highlights table.

The Board may amend, suspend or terminate a Fund’s Plan at any time without prior notice to the Fund’s shareholders if it deems such actions to be in the best interests of the Fund or its shareholders. The suspension or termination of the Plan could have the effect of creating a trading discount (if the Fund’s stock is trading at or above net asset value) or widening an existing trading discount. The Funds are subject to risks that could have an adverse impact on their ability to maintain level distributions. Examples of potential risks include, but are not limited to, economic downturns impacting the markets, changes in interest rates, decreased market volatility, companies suspending or decreasing corporate dividend distributions and changes in the Code.

The amounts and sources of distributions reported will be estimates and will be provided to you pursuant to regulatory requirements and will not be provided for tax reporting purposes. The actual amounts and sources for tax reporting purposes will depend upon each Fund’s investment experience during its fiscal year and may be subject to changes based on tax regulations. Each Fund will provide a Form 1099-DIV each calendar year that will tell you how to report these distributions for U.S. federal income tax purposes.

| 2 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| THIS PAGE IS NOT PART OF YOUR FUND REPORT | 3 |

| Page | ||||

| 2 | ||||

| 3 | ||||

| Annual Report: |

||||

| 5 | ||||

| 11 | ||||

| 11 | ||||

| Financial Statements |

||||

| 12 | ||||

| 56 | ||||

| 57 | ||||

| 58 | ||||

| 59 | ||||

| 61 | ||||

| 63 | ||||

| 76 | ||||

| 76 | ||||

| 77 | ||||

| 81 | ||||

| 82 | ||||

| 85 | ||||

| 87 | ||||

| 4 |

| Fund Summary as of August 31, 2019 | BlackRock Floating Rate Income Strategies Fund, Inc. |

Fund Overview

BlackRock Floating Rate Income Strategies Fund, Inc.’s (FRA) (the “Fund”) investment objective is to provide shareholders with high current income and such preservation of capital as is consistent with investment in a diversified, leveraged portfolio consisting primarily of floating rate debt securities and instruments. The Fund seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its managed assets in floating rate debt securities, including floating or variable rate debt securities that pay interest at rates that adjust whenever a specified interest rate changes and/or which reset on predetermined dates (such as the last day of a month or calendar quarter). The Fund invests a substantial portion of its investments in floating rate debt securities consisting of secured or unsecured senior floating rate loans that are rated below investment grade at the time of investment or, if unrated, are considered by the investment adviser to be of comparable quality. The Fund may invest directly in floating rate debt securities or synthetically through the use of derivatives.

No assurance can be given that the Fund’s investment objective will be achieved.

Fund Information

| Symbol on New York Stock Exchange (“NYSE”) |

FRA | |

| Initial Offering Date |

October 31, 2003 | |

| Current Distribution Rate on Closing Market Price as of August 31, 2019 ($12.46)(a) |

6.69% | |

| Current Monthly Distribution per Common Share(b) |

$0.0695 | |

| Current Annualized Distribution per Common Share(b) |

$0.8340 | |

| Leverage as of August 31, 2019(c) |

28% |

| (a) | Current Distribution Rate on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. The current distribution rate may consist of income, net realized gains and/or a return of capital. Past performance does not guarantee future results. |

| (b) | The monthly distribution per Common Share, declared on October 1, 2019, was increased to $0.0788 per share. The current distribution rate on closing market price, current monthly distribution per Common Share, and current annualized distribution per Common Share do not reflect the new distribution rate. The new distribution rate is not constant and is subject to change in the future. |

| (c) | Represents bank borrowings outstanding as a percentage of total managed assets, which is the total assets of the Fund (including any assets attributable to borrowings) minus the sum of liabilities (other than borrowings representing financial leverage). Does not reflect derivatives or other instruments that may give rise to economic leverage. For a discussion of leveraging techniques utilized by the Fund, please see The Benefits and Risks of Leveraging and Derivative Financial Instruments on page 10. |

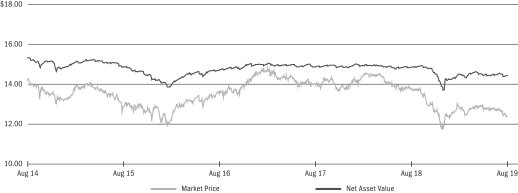

Market Price and Net Asset Value Per Share Summary

| 08/31/19 | 08/31/18 |

Change | High | Low | ||||||||||||||||

| Market Price |

$ | 12.46 | $ | 13.80 | (9.71 | )% | $ | 13.85 | $ | 11.63 | ||||||||||

| Net Asset Value |

14.49 | 14.92 | (2.88 | ) | 14.98 | 13.75 | ||||||||||||||

Market Price and Net Asset Value History For the Past Five Years

| FUND SUMMARY | 5 |

| Fund Summary as of August 31, 2019 (continued) | BlackRock Floating Rate Income Strategies Fund, Inc. |

Performance and Portfolio Management Commentary

Returns for the period ended August 31, 2019 were as follows:

| Average Annual Total Returns | ||||||||||||

| 1 Year | 3 Years | 5 Years | ||||||||||

| Fund at NAV(a)(b) |

3.94 | % | 5.38 | % | 4.80 | % | ||||||

| Fund at Market Price(a)(b) |

(3.37 | ) | 2.77 | 3.23 | ||||||||

| S&P/LSTA Leveraged Loan Index(c) |

3.33 | 4.66 | 3.76 | |||||||||

| (a) | All returns reflect reinvestment of dividends and/or distributions at actual reinvestment prices. Performance results reflect the Fund’s use of leverage. |

| (b) | The Fund’s discount to NAV widened during the period, which accounts for the difference between performance based on market price and performance based on NAV. |

| (c) | An unmanaged market value-weighted index (the “Reference Benchmark”) designed to measure the performance of the U.S. leveraged loan market based upon market weightings, spreads and interest payments. |

Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles.

Past performance is not indicative of future results.

The following discussion relates to the Fund’s absolute performance based on NAV:

What factors influenced performance?

The largest absolute sector contributors to Fund performance included floating rate loan interests (“bank loans”) held within technology, consumer cyclical services and health care. The Fund’s B-rated positions were the largest contributors, followed by BB-rated positions. Importantly, returns for all ratings segments CCC and above were positive over the period. From an asset allocation perspective, indexed loan positions were additive as well.

The oil field services, banking and independent energy sectors were the largest detractors. In terms of rating categories, nonrated/other positions were the only detractors.

Describe recent portfolio activity.

Sector allocations were largely unchanged over the 12 months, although single-name relative positioning was arguably more important to portfolio performance. The investment adviser has been an active user of liquid products within the loan market, recently adding total return swaps to the portfolio.

From a credit quality standpoint, the portfolio remained concentrated on the B- and BB-rated segments of the bank loan market, while maintaining a much smaller allocation to CCC-rated risk. The investment adviser reduced the Fund’s CCC-rated exposure throughout the period.

Describe portfolio positioning at period end

The Fund’s largest allocation at period end was to B-rated loans, with a focus on higher quality segments within that rating category. The Fund had very little exposure to the CCC-rated component of the loan market. Also reflecting a focus on relative quality, the Fund had a clear preference for loans with spreads in the 200-300 basis point (2%-3%) range over the London InterBank Offered Rate reference rate as opposed to positions with spreads of 400 or more basis points. The largest sector positions included technology, health care and consumer cyclical services. The Fund had a preference for larger loan tranches of $1 billion or more. From a vintage perspective, the Fund had a cautious stance on transactions initiated since 2017, given the arguably more aggressive lending standards and weaker protections for loan holders seen in recent years.

The Fund’s top five issuer-level positions comprised approximately 8% of the portfolio. The largest overweights included Clear Channel Outdoor Holdings, Inc. (media & entertainment), Sedgwick Claims Management Services, Inc. (financial other) and Infor US, Inc. (technology).

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| 6 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Fund Summary as of August 31, 2019 (continued) | BlackRock Floating Rate Income Strategies Fund, Inc. |

Overview of the Fund’s Total Investments

| FUND SUMMARY | 7 |

| Fund Summary as of August 31, 2019 | BlackRock Limited Duration Income Trust |

Fund Overview

BlackRock Limited Duration Income Trust’s (BLW) (the “Fund”) investment objective is to provide current income and capital appreciation. The Fund seeks to achieve its investment objective by investing primarily in three distinct asset classes:

| • | intermediate duration, investment grade corporate bonds, mortgage-related securities, asset-backed securities and U.S. Government and agency securities; |

| • | senior, secured floating rate loans made to corporate and other business entities; and |

| • | U.S. dollar-denominated securities of U.S. and non-U.S. issuers rated below investment grade at the time of investment or unrated and deemed by the investment adviser to be of comparable quality and, to a limited extent, non-U.S. dollar denominated securities of non-U.S. issuers rated below investment grade or unrated and deemed by the investment adviser to be of comparable quality. |

The Fund’s portfolio normally has an average portfolio duration of less than five years (including the effect of anticipated leverage), although it may be longer from time to time depending on market conditions. The Fund may invest directly in securities or synthetically through the use of derivatives.

No assurance can be given that the Fund’s investment objective will be achieved.

Fund Information

| Symbol on NYSE |

BLW | |

| Initial Offering Date |

July 30, 2003 | |

| Current Distribution Rate on Closing Market Price as of August 31, 2019 ($15.44)(a) |

6.18% | |

| Current Monthly Distribution per Common Share(b) |

$0.0795 | |

| Current Annualized Distribution per Common Share(b) |

$0.9540 | |

| Leverage as of August 31, 2019(c) |

25% |

| (a) | Current Distribution Rate on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. The current distribution rate may consist of income, net realized gains and/or a return of capital. Past performance does not guarantee future results. |

| (b) | The monthly distribution per Common Share, declared on October 1, 2019, was increased to $0.0981 per share. The current distribution rate on closing market price, current monthly distribution per Common Share, and current annualized distribution per Common Share do not reflect the new distribution rate. The new distribution rate is not constant and is subject to change in the future. |

| (c) | Represents reverse repurchase agreements outstanding as a percentage of total managed assets, which is the total assets of the Fund (including any assets attributable to borrowing) minus the sum of liabilities (other than borrowings representing financial leverage). Does not reflect derivatives or other instruments that may give rise to economic leverage. For a discussion of leveraging techniques utilized by the Fund, please see The Benefits and Risks of Leveraging and Derivative Financial Instruments on page 10. |

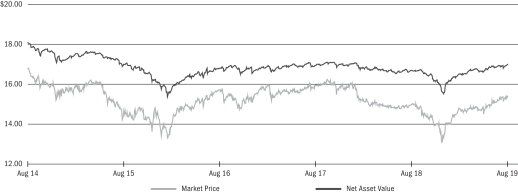

Market Price and Net Asset Value Per Share Summary

| 08/31/19 | 08/31/18 |

Change | High | Low | ||||||||||||||||

| Market Price |

$ | 15.44 | $ | 15.06 | 2.52 | % | $ | 15.53 | $ | 13.00 | ||||||||||

| Net Asset Value |

17.03 | 16.71 | 1.92 | 17.03 | 15.57 | |||||||||||||||

Market Price and Net Asset Value History For the Past Five Years

| 8 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Fund Summary as of August 31, 2019 (continued) | BlackRock Limited Duration Income Trust |

Performance and Portfolio Management Commentary

Returns for the period ended August 31, 2019 were as follows:

| Average Annual Total Returns | ||||||||||||

| 1 Year | 3 Years | 5 Years | ||||||||||

| Fund at NAV(a)(b) |

8.77 | % | 7.58 | % | 6.50 | % | ||||||

| Fund at Market Price(a)(b) |

9.41 | 6.49 | 6.01 | |||||||||

| Reference Benchmark(c) |

5.25 | 4.44 | 3.63 | |||||||||

| Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index(d) |

6.56 | 6.17 | 4.86 | |||||||||

| S&P/LSTA Leveraged Loan Index(e) |

3.33 | 4.66 | 3.76 | |||||||||

| BATS S Benchmark(f) |

5.75 | 2.44 | 2.21 | |||||||||

| (a) | All returns reflect reinvestment of dividends and/or distributions at actual reinvestment prices. Performance results reflect the Fund’s use of leverage. |

| (b) | The Fund’s discount to NAV narrowed during the period, which accounts for the difference between performance based on market price and performance based on NAV. |

| (c) | The Reference Benchmark is comprised of the Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index (33.33%), the S&P/LSTA Leveraged Loan Index (33.33%), and the BATS S Benchmark (33.34%). The Reference Benchmark’s index content and weightings may have varied over past periods. |

| (d) | An unmanaged index comprised of issuers that meet the following criteria: at least $150 million par value outstanding; maximum credit rating of Ba1; at least one year to maturity; and no issuer represents more than 2% of the index. |

| (e) | An unmanaged market value-weighted index designed to measure the performance of the U.S. leveraged loan market based upon market weightings, spreads and interest payments. |

| (f) | A composite index comprised of Bloomberg Barclays ABS 1-3 Year AAA Rated ex Home Equity Index, Bloomberg Barclays Corporate 1-5 year Index, Bloomberg Barclays CMBS Investment Grade 1-3.5 Yr. Index, Bloomberg Barclays MBS 15 Yr Index and Bloomberg Barclays Credit Ex-Corporate 1-5 Yr Index. |

Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles.

Past performance is not indicative of future results.

The following discussion relates to the Fund’s absolute performance based on NAV:

What factors influenced performance?

Positive contributions to the Fund’s performance over the period came from allocations to credit sensitive areas of the market including high yield corporate bonds, investment grade corporate bonds and floating rate loan interests (“bank loans”). Exposure to sovereign bonds and commercial mortgage-backed securities (“CMBS”) also added to the Fund’s return, as did the Fund’s currency exposures.

The largest detractors from the Fund’s performance came from its positioning within municipal bonds, equities and cash.

The Fund held derivatives during the period, including Treasury futures, currency forwards, currency options, interest rate swaps and credit default swaps. Derivative securities were employed primarily to adjust duration (sensitivity to interest rate changes) and yield curve exposure, as well as to manage credit and currency risk. Currency forwards were used to provide the portfolio with active currency exposure. The Fund’s use of derivatives contributed positively to Fund performance during the period.

Describe recent portfolio activity.

During the reporting period, the Fund’s defensive posture was maintained. The Fund had a slight increase in foreign currency exposure from 0.4% to 0.9%, and an increase in its U.S. Treasury position from 0% to 3%. Over the period, the Fund trimmed its asset-backed securities (“ABS”) position from 11.4% to 5%, and reduced its CMBS position from 6.5% to 1%.

Describe portfolio positioning at period end.

At period end, the Fund maintained a diversified exposure to non-government spread sectors including high yield corporate bonds, senior bank loans, investment grade corporate bonds, CMBS, ABS, agency and non-agency residential mortgage-backed securities, emerging market debt and foreign sovereign debt.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| FUND SUMMARY | 9 |

| Fund Summary as of August 31, 2019 (continued) | BlackRock Limited Duration Income Trust |

Overview of the Fund’s Total Investments

| 10 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

The Benefits and Risks of Leveraging

The Funds may utilize leverage to seek to enhance the distribution rate on, and net asset value (“NAV”) of, their common shares (“Common Shares”). However, there is no guarantee that these objectives can be achieved in all interest rate environments.

In general, the concept of leveraging is based on the premise that the financing cost of leverage, which is based on short-term interest rates, is normally lower than the income earned by a Fund on its longer-term portfolio investments purchased with the proceeds from leverage. To the extent that the total assets of the Funds (including the assets obtained from leverage) are invested in higher-yielding portfolio investments, the Funds’ shareholders benefit from the incremental net income. The interest earned on securities purchased with the proceeds from leverage (after paying the leverage costs) is paid to shareholders in the form of dividends, and the value of these portfolio holdings (less the leverage liability) is reflected in the per share NAV.

To illustrate these concepts, assume a Fund’s capitalization is $100 million and it utilizes leverage for an additional $30 million, creating a total value of $130 million available for investment in longer-term income securities. If prevailing short-term interest rates are 3% and longer-term interest rates are 6%, the yield curve has a strongly positive slope. In this case, a Fund’s financing costs on the $30 million of proceeds obtained from leverage are based on the lower short-term interest rates. At the same time, the securities purchased by a Fund with the proceeds from leverage earn income based on longer-term interest rates. In this case, a Fund’s financing cost of leverage is significantly lower than the income earned on a Fund’s longer-term investments acquired from such leverage proceeds, and therefore the holders of Common Shares (“Common Shareholders”) are the beneficiaries of the incremental net income.

However, in order to benefit shareholders, the return on assets purchased with leverage proceeds must exceed the ongoing costs associated with the leverage. If interest and other costs of leverage exceed the Funds’ return on assets purchased with leverage proceeds, income to shareholders is lower than if the Funds had not used leverage. Furthermore, the value of the Funds’ portfolio investments generally varies inversely with the direction of long-term interest rates, although other factors can influence the value of portfolio investments. In contrast, the value of the Funds’ obligations under their respective leverage arrangements generally does not fluctuate in relation to interest rates. As a result, changes in interest rates can influence the Funds’ NAVs positively or negatively. Changes in the future direction of interest rates are very difficult to predict accurately, and there is no assurance that the Funds’ intended leveraging strategy will be successful.

The use of leverage also generally causes greater changes in each Fund’s NAV, market price and dividend rates than comparable portfolios without leverage. In a declining market, leverage is likely to cause a greater decline in the NAV and market price of a Fund’s shares than if the Fund were not leveraged. In addition, each Fund may be required to sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of leverage instruments, which may cause the Fund to incur losses. The use of leverage may limit a Fund’s ability to invest in certain types of securities or use certain types of hedging strategies. Each Fund incurs expenses in connection with the use of leverage, all of which are borne by shareholders and may reduce income to the shareholders. Moreover, to the extent the calculation of the Funds’ investment advisory fees includes assets purchased with the proceeds of leverage, the investment advisory fees payable to the Funds’ investment adviser will be higher than if the Funds did not use leverage.

Each Fund may utilize leverage through a credit facility or reverse repurchase agreements as described in the Notes to Financial Statements.

Under the Investment Company Act of 1940, as amended (the “1940 Act”), each Fund is permitted to issue debt up to 331⁄3% of its total managed assets. A Fund may voluntarily elect to limit its leverage to less than the maximum amount permitted under the 1940 Act. In addition, a Fund may also be subject to certain asset coverage, leverage or portfolio composition requirements imposed by its credit facility, which may be more stringent than those imposed by the 1940 Act.

If a Fund segregates or designates on its books and records cash or liquid assets having a value not less than the value of a Fund’s obligations under the reverse repurchase agreements (including accrued interest) then such transaction is not considered a senior security and is not subject to the foregoing limitations and requirements imposed by the 1940 Act.

Derivative Financial Instruments

The Funds may invest in various derivative financial instruments. These instruments are used to obtain exposure to a security, commodity, index, market, and/or other assets without owning or taking physical custody of securities, commodities and/or other referenced assets or to manage market, equity, credit, interest rate, foreign currency exchange rate, commodity and/or other risks. Derivative financial instruments may give rise to a form of economic leverage and involve risks, including the imperfect correlation between the value of a derivative financial instrument and the underlying asset, possible default of the counterparty to the transaction or illiquidity of the instrument. The Funds’ successful use of a derivative financial instrument depends on the investment adviser’s ability to predict pertinent market movements accurately, which cannot be assured. The use of these instruments may result in losses greater than if they had not been used, may limit the amount of appreciation a Fund can realize on an investment and/or may result in lower distributions paid to shareholders. The Funds’ investments in these instruments, if any, are discussed in detail in the Notes to Financial Statements.

| THE BENEFITS AND RISKS OF LEVERAGING / DERIVATIVE FINANCIAL INSTRUMENTS | 11 |

|

August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) (Percentages shown are based on Net Assets) |

| 12 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 13 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) (Percentages shown are based on Net Assets) |

| 14 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 15 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) (Percentages shown are based on Net Assets) |

| 16 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 17 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) (Percentages shown are based on Net Assets) |

| 18 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 19 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) (Percentages shown are based on Net Assets) |

During the year ended August 31, 2019, investments in issuers considered to be an affiliate/affiliates of the Fund for purposes of Section 2(a)(3) of the Investment Company Act of 1940, as amended, and/or related parties of the Fund were as follows:

| Affiliate | Shares Held at 08/31/18 |

Shares Purchased |

Shares Sold |

Shares Held at 08/31/19 |

Value at 08/31/19 |

Income | Net Realized Gain (Loss) (a) |

Change in Unrealized Appreciation (Depreciation) |

||||||||||||||||||||||||

| BlackRock Liquidity Funds, T-Fund, Institutional Class(b) |

155,382 | — | (155,382 | )(c) | — | $ | — | $ | 38,562 | $ | — | $ | — | |||||||||||||||||||

| iShares iBoxx USD High Yield Corporate Bond ETF(b) |

— | 46,500 | (46,500 | ) | — | — | — | 27,274 | — | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| $ | — | $ | 38,562 | $ | 27,274 | $ | — | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| (a) | Includes net capital gain distributions, if applicable. |

| (b) | As of period end, the entity is no longer held by the Fund. |

| (c) | Represents net shares sold. |

Derivative Financial Instruments Outstanding as of Period End

Forward Foreign Currency Exchange Contracts

| Currency Purchased |

Currency Sold |

Counterparty | Settlement Date | Unrealized Appreciation (Depreciation) |

||||||||||||||||

| USD | 5,112,331 | EUR | 4,575,000 | Goldman Sachs International | 09/05/19 | $ | 83,800 | |||||||||||||

| USD | 2,289,368 | GBP | 1,876,000 | BNP Paribas S.A. | 09/05/19 | 6,555 | ||||||||||||||

| USD | 5,029,406 | EUR | 4,563,000 | State Street Bank and Trust Co. | 10/03/19 | 2,937 | ||||||||||||||

| USD | 2,287,362 | GBP | 1,873,000 | Standard Chartered Bank | 10/03/19 | 5,329 | ||||||||||||||

|

|

|

|||||||||||||||||||

| 98,621 | ||||||||||||||||||||

|

|

|

|||||||||||||||||||

| EUR | 4,563,000 | USD | 5,018,173 | State Street Bank and Trust Co. | 09/05/19 | (2,832 | ) | |||||||||||||

| GBP | 1,873,000 | USD | 2,284,493 | Standard Chartered Bank | 09/05/19 | (5,331 | ) | |||||||||||||

|

|

|

|||||||||||||||||||

| (8,163 | ) | |||||||||||||||||||

|

|

|

|||||||||||||||||||

| Net Unrealized Appreciation | $ | 90,458 | ||||||||||||||||||

|

|

|

|||||||||||||||||||

Exchange-Traded Options Purchased

| Description | Number of Contracts |

Expiration Date |

Exercise Price |

Notional Amount (000) |

Value | |||||||||||||||||||

| Call | ||||||||||||||||||||||||

| SPDR S&P 500 ETF Trust |

170 | 09/20/19 | USD | 315.00 | USD | 4,972 | $ | 255 | ||||||||||||||||

| Put | ||||||||||||||||||||||||

| SPDR S&P 500 ETF Trust |

170 | 09/20/19 | USD | 270.00 | USD | 4,972 | 14,450 | |||||||||||||||||

|

|

|

|||||||||||||||||||||||

| $ | 14,705 | |||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||

| 20 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) |

Derivative Financial Instruments Categorized by Risk Exposure

As of period end, the fair values of derivative financial instruments located in the Statements of Assets and Liabilities were as follows:

| Commodity Contracts |

Credit Contracts |

Equity Contracts |

Foreign Currency Exchange Contracts |

Interest Rate Contracts |

Other Contracts |

Total | ||||||||||||||||||||||

| Assets — Derivative Financial Instruments |

||||||||||||||||||||||||||||

| Forward foreign currency exchange contracts |

||||||||||||||||||||||||||||

| Unrealized appreciation on forward foreign currency exchange contracts |

$ | — | $ | — | $ | — | $ | 98,621 | $ | — | $ | — | $ | 98,621 | ||||||||||||||

| Options purchased |

||||||||||||||||||||||||||||

| Investments at value — unaffiliated(a) |

— | — | 14,705 | — | — | — | 14,705 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| $ | — | $ | — | $ | 14,705 | $ | 98,621 | $ | — | $ | — | $ | 113,326 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Liabilities — Derivative Financial Instruments |

||||||||||||||||||||||||||||

| Forward foreign currency exchange contracts |

||||||||||||||||||||||||||||

| Unrealized depreciation on forward foreign currency exchange contracts |

$ | — | $ | — | $ | — | $ | 8,163 | $ | — | $ | — | $ | 8,163 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (a) | Includes options purchased at value as reported in the Schedule of Investments. |

For the year ended August 31, 2019, the effect of derivative financial instruments in the Statements of Operations was as follows:

| Commodity Contracts |

Credit Contracts |

Equity Contracts |

Foreign Currency Exchange Contracts |

Interest Rate Contracts |

Other Contracts |

Total | ||||||||||||||||||||||

| Net Realized Gain (Loss) from: |

||||||||||||||||||||||||||||

| Forward foreign currency exchange contracts |

$ | — | $ | — | $ | — | $ | 587,067 | $ | — | $ | — | $ | 587,067 | ||||||||||||||

| Swaps |

— | — | — | — | (610,309 | ) | — | (610,309 | ) | |||||||||||||||||||

| Options purchased(a) |

— | — | 124,969 | — | — | — | 124,969 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| $ | — | $ | — | $ | 124,969 | $ | 587,067 | $ | (610,309 | ) | $ | — | $ | 101,727 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net Change in Unrealized Appreciation (Depreciation) on: | ||||||||||||||||||||||||||||

| Forward foreign currency exchange contracts |

$ | — | $ | — | $ | — | $ | 36,256 | $ | — | $ | — | $ | 36,256 | ||||||||||||||

| Options purchased(b) |

— | — | 16,094 | — | — | — | 16,094 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| $ | — | $ | — | $ | 16,094 | $ | 36,256 | $ | — | $ | — | $ | 52,350 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (a) | Options purchased are included in net realized gain (loss) from investments. |

| (b) | Options purchased are included in net change in unrealized appreciation (depreciation) on investments. |

Average Quarterly Balances of Outstanding Derivative Financial Instruments

| Forward foreign currency exchange contracts: |

| |||

| Average amounts purchased — in USD |

$ | 14,824,361 | ||

| Average amounts sold — in USD |

$ | 7,390,708 | ||

| Options: |

| |||

| Average value of option contracts purchased |

$ | 14,234 | ||

| Total return swaps: |

| |||

| Average notional value |

$ | 5,043,500 | ||

For more information about the Fund’s investment risks regarding derivative financial instruments, refer to the Notes to Financial Statements.

| SCHEDULES OF INVESTMENTS | 21 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) |

Derivative Financial Instruments — Offsetting as of Period End

The Fund’s derivative assets and liabilities (by type) were as follows:

| Assets | Liabilities | |||||||

| Forward foreign currency exchange contracts |

$ | 98,621 | $ | 8,163 | ||||

| Options |

14,705 | (a) | — | |||||

|

|

|

|

|

|||||

| Total derivative assets and liabilities in the Statements of Assets and Liabilities |

$ | 113,326 | $ | 8,163 | ||||

| Derivatives not subject to a Master Netting Agreement or similar agreement (“MNA”) |

(14,705 | ) | — | |||||

|

|

|

|

|

|||||

| Total derivative assets and liabilities subject to an MNA |

$ | 98,621 | $ | 8,163 | ||||

|

|

|

|

|

|||||

| (a) | Includes options purchased at value which is included in Investments at value — unaffiliated in the Statements of Assets and Liabilities and reported in the Schedule of Investments. |

The following table presents the Fund’s derivative assets (and liabilities) by counterparty net of amounts available for offset under an MNA and net of the related collateral received (and pledged) by the Fund:

| Counterparty | Derivative Assets Subject to an MNA by Counterparty |

Derivatives Available for Offset (a) |

Non-cash Collateral Received |

Cash Collateral Received |

Net Amount of Derivative Assets (b) |

|||||||||||||||

| BNP Paribas S.A. |

$ | 6,555 | $ | — | $ | — | $ | — | $ | 6,555 | ||||||||||

| Goldman Sachs International |

83,800 | — | — | — | 83,800 | |||||||||||||||

| Standard Chartered Bank |

5,329 | (5,329 | ) | — | — | — | ||||||||||||||

| State Street Bank and Trust Co. |

2,937 | (2,832 | ) | — | — | 105 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | 98,621 | $ | (8,161 | ) | $ | — | $ | — | $ | 90,460 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Counterparty | Derivative Liabilities Subject to an MNA by Counterparty |

Derivatives Available for Offset (a) |

Non-cash Collateral Pledged |

Cash Collateral Pledged |

Net Amount of Derivative Liabilities (c) |

|||||||||||||||

| Standard Chartered Bank |

$ | 5,331 | $ | (5,329 | ) | $ | — | $ | — | $ | 2 | |||||||||

| State Street Bank and Trust Co. |

2,832 | (2,832 | ) | — | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| $ | 8,163 | $ | (8,161 | ) | $ | — | $ | — | $ | 2 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | The amount of derivatives available for offset is limited to the amount of derivative asset and/or liabilities that are subject to an MNA. |

| (b) | Net amount represents the net amount receivable from the counterparty in the event of default. |

| (c) | Net amount represents the net amount payable due to counterparty in the event of default. |

| 22 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Floating Rate Income Strategies Fund, Inc. (FRA) |

Fair Value Hierarchy as of Period End

Various inputs are used in determining the fair value of investments and derivative financial instruments. For information about the Fund’s policy regarding valuation of investments and derivative financial instruments, refer to the Notes to Financial Statements.

The following tables summarize the Fund’s investments categorized in the disclosure hierarchy:

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Assets: |

||||||||||||||||

| Investments: |

||||||||||||||||

| Long-Term Investments: |

| |||||||||||||||

| Common Stocks(a) |

$ | 401,285 | $ | 224 | $ | 564,703 | $ | 966,212 | ||||||||

| Corporate Bonds |

— | 7,466,475 | 875,355 | 8,341,830 | ||||||||||||

| Floating Rate Loan Interests |

— | 688,501,539 | 24,982,577 | 713,484,116 | ||||||||||||

| Investment Companies |

30,184,350 | — | — | 30,184,350 | ||||||||||||

| Warrants |

— | 593,757 | — | 593,757 | ||||||||||||

| Options Purchased |

14,705 | — | — | 14,705 | ||||||||||||

| Liabilities: |

||||||||||||||||

| Investments: |

||||||||||||||||

| Unfunded Floating Rate Loan Interest(b) |

— | (4,797 | ) | — | (4,797 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | 30,600,340 | $ | 696,557,198 | $ | 26,422,635 | $ | 753,580,173 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Derivative Financial Instruments(c) |

||||||||||||||||

| Assets: |

||||||||||||||||

| Forward foreign currency contracts |

$ | — | $ | 98,621 | $ | — | $ | 98,621 | ||||||||

| Liabilities: |

||||||||||||||||

| Forward foreign currency contracts |

— | (8,163 | ) | — | (8,163 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | — | $ | 90,458 | $ | — | $ | 90,458 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (a) | See above Schedule of Investments for values in each industry. |

| (b) | Unfunded floating rate loan interests are valued at the unrealized appreciation (depreciation) on the commitment. |

| (c) | Derivative financial instruments are forward foreign currency exchange contracts, which are valued at the unrealized appreciation (depreciation) on the instrument. |

The Fund may hold assets and/or liabilities in which the fair value approximates the carrying amount for financial statement purposes. As of period end, bank borrowings payable of $204,000,000 is categorized as Level 2 within the disclosure hierarchy.

A reconciliation of Level 3 investments is presented when the Fund had a significant amount of Level 3 investments at the beginning and/or end of the year in relation to net assets. The following table is a reconciliation of Level 3 investments for which significant unobservable inputs were used in determining fair value:

| Asset-Backed Securities |

Common Stocks |

Corporate Bonds |

Floating Rate Loan Interests |

Warrants | Options Purchased |

Total | ||||||||||||||||||||||

| Assets: |

||||||||||||||||||||||||||||

| Opening balance, as of August 31, 2018 |

$ | 2,698,550 | $ | 2,048,238 | $ | 2,892,436 | $ | 36,749,545 | $ | — | $ | — | $ | 44,388,769 | ||||||||||||||

| Transfers into Level 3(a) |

— | — | — | 10,346,533 | — | — | 10,346,533 | |||||||||||||||||||||

| Transfers out of Level 3(b) |

— | — | — | (13,160,490 | ) | — | — | (13,160,490 | ) | |||||||||||||||||||

| Accrued discounts/premiums |

— | — | 1,547 | 10,362 | — | — | 11,909 | |||||||||||||||||||||

| Net realized gain (loss) |

(39,405 | ) | 26,946 | (405,297 | ) | (1,312,262 | ) | (24 | ) | (43,022 | ) | (1,773,064 | ) | |||||||||||||||

| Net change in unrealized appreciation (depreciation)(c)(d) |

— | (1,291,122 | ) | (84,433 | ) | 702,387 | 24 | 43,022 | (630,122 | ) | ||||||||||||||||||

| Purchases |

— | 2,940,312 | 977,128 | 12,857,976 | — | — | 16,775,416 | |||||||||||||||||||||

| Sales |

(2,659,145 | ) | (3,159,671 | ) | (2,506,026 | ) | (21,211,474 | ) | — | — | (29,536,316 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Closing balance, as of August 31, 2019 |

$ | — | $ | 564,703 | $ | 875,355 | $ | 24,982,577 | $ | — | $ | — | $ | 26,422,635 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net change in unrealized appreciation (depreciation) on investments still held at August 31, 2019(d) |

$ | — | $ | (1,164,821 | ) | $ | 28,938 | $ | (343,249 | ) | $ | — | $ | — | $ | (1,479,132 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (a) | As of August 31, 2018 the Fund used observable inputs in determining the value of certain investments. As of August 31, 2019, the Fund used significant unobservable inputs in determining the value of the same investments. As a result, investments at beginning of period value were transferred from Level 2 to Level 3 in the disclosure hierarchy. |

| (b) | As of August 31, 2018, the Fund used significant unobservable inputs in determining the value of certain investments. As of August 31, 2019, the Fund used observable inputs in determining the value of the same investments. As a result, investments at beginning of period value were transferred from Level 3 to Level 2 in the disclosure hierarchy. |

| (c) | Included in the related change in unrealized appreciation (depreciation) in the Statements of Operations. |

| (d) | Any difference between net change in unrealized appreciation (depreciation) and net change in unrealized appreciation (depreciation) on investments still held at August 31, 2019 is generally due to investments no longer held or categorized as Level 3 at period end. |

The Fund’s investments that are categorized as Level 3 were valued utilizing third party pricing information without adjustment. Such valuations are based on unobservable inputs. A significant change in third party information could result in a significantly lower or higher value of such Level 3 investments.

See notes to financial statements.

| SCHEDULES OF INVESTMENTS | 23 |

| Schedule of Investments August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 24 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 25 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 26 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 27 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 28 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 29 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 30 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 31 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 32 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 33 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 34 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 35 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 36 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 37 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 38 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 39 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 40 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 41 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 42 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| SCHEDULES OF INVESTMENTS | 43 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) (Percentages shown are based on Net Assets) |

| 44 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) |

| (t) | During the year ended August 31, 2019, investments in issuers considered to be an affiliate/affiliates of the Fund for purposes of Section 2(a)(3) of the Investment Company Act of 1940, as amended, were as follows: |

| Affiliate | Shares Held at 08/31/18 |

Net Activity |

Shares Held at 08/31/19 |

Value at 08/31/19 |

Income | Net Realized Gain (Loss) (a) |

Change in Unrealized Appreciation (Depreciation) |

|||||||||||||||||||||

| BlackRock Liquidity Funds, T-Fund, Institutional Class |

180,494 | 3,508,414 | 3,688,908 | $ | 3,688,908 | $ | 171,752 | $ | — | $ | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| (a) | Includes net capital gain distributions, if applicable. |

Reverse Repurchase Agreements

| Counterparty | Interest Rate |

Trade Date |

Maturity Date (a) |

Face Value | Face Value Including Accrued Interest |

Type of Non-Cash Underlying Collateral |

Remaining Contractual Maturity of the Agreements (a) | |||||||||||||||||

| Deutsche Bank Securities, Inc. |

0.70 | % | 09/13/18 | Open | $ | 77,400 | $ | 78,032 | Corporate Bonds | Open/Demand | ||||||||||||||

| UBS Ltd. |

2.50 | 09/20/18 | Open | 3,026,213 | 3,104,121 | Foreign Agency Obligations | Open/Demand | |||||||||||||||||

| UBS Ltd. |

2.70 | 09/20/18 | Open | 746,250 | 766,892 | Corporate Bonds | Open/Demand | |||||||||||||||||

| UBS Ltd. |

2.70 | 09/20/18 | Open | 250,200 | 257,121 | Corporate Bonds | Open/Demand | |||||||||||||||||

| UBS Ltd. |

2.70 | 09/20/18 | Open | 362,780 | 372,815 | Corporate Bonds | Open/Demand | |||||||||||||||||

| UBS Ltd. |

2.70 | 09/20/18 | Open | 1,730,000 | 1,777,854 | Capital Trusts | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 10/09/18 | Open | 2,808,000 | 2,874,296 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 10/09/18 | Open | 256,000 | 262,044 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.65 | 10/09/18 | Open | 417,000 | 427,792 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.65 | 10/09/18 | Open | 496,000 | 508,837 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Deutsche Bank Securities, Inc. |

2.75 | 11/15/18 | Open | 2,730,000 | 2,795,065 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.65 | 11/27/18 | Open | 839,000 | 857,630 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/11/18 | Open | 740,835 | 756,993 | Corporate Bonds | Open/Demand | |||||||||||||||||

| UBS Ltd. |

2.70 | 12/12/18 | Open | 250,582 | 255,937 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

1.50 | 12/14/18 | Open | 403,705 | 405,372 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

(1.75 | ) | 12/14/18 | Open | 101,640 | 100,453 | Corporate Bonds | Open/Demand | ||||||||||||||||

| Barclays Capital, Inc. |

2.25 | 12/14/18 | Open | 2,119,500 | 2,161,107 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 551,700 | 563,519 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 399,757 | 408,321 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 403,124 | 411,760 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 636,334 | 649,965 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 640,888 | 654,617 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 624,025 | 637,393 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 436,500 | 445,851 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 483,862 | 494,228 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 589,235 | 601,858 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 449,970 | 459,609 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/14/18 | Open | 442,531 | 452,011 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 160,000 | 163,026 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 3,148,000 | 3,207,541 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 771,000 | 785,583 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 908,000 | 925,174 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 866,000 | 882,379 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 2,522,000 | 2,569,701 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 1,357,000 | 1,382,666 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 6,371,000 | 6,491,500 | Capital Trusts | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 503,000 | 512,514 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 12/14/18 | Open | 908,000 | 931,500 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.65 | 12/14/18 | Open | 381,000 | 388,889 | Corporate Bonds | Open/Demand | |||||||||||||||||

| SCHEDULES OF INVESTMENTS | 45 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) |

Reverse Repurchase Agreements (continued)

| Counterparty | Interest Rate |

Trade Date |

Maturity Date (a) |

Face Value | Face Value Including Accrued Interest |

Type of Non-Cash Underlying Collateral |

Remaining Contractual Maturity of the Agreements (a) | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.65 | % | 12/14/18 | Open | $ | 2,927,000 | $ | 2,987,605 | Capital Trusts | Open/Demand | ||||||||||||||

| UBS Securities LLC |

2.70 | 12/18/18 | Open | 1,944,443 | 1,985,251 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

1.00 | 12/21/18 | Open | 245,265 | 247,217 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

1.70 | 12/24/18 | Open | 361,600 | 367,102 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 12/24/18 | Open | 38,070 | 38,860 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.25 | 01/08/19 | Open | 989,063 | 998,678 | Capital Trusts | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

1.80 | 01/16/19 | Open | 98,972 | 100,113 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

1.00 | 01/18/19 | Open | 192,965 | 194,155 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.40 | 01/18/19 | Open | 824,440 | 836,173 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.50 | 02/12/19 | Open | 527,217 | 534,539 | Capital Trusts | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.50 | 02/12/19 | Open | 382,826 | 388,143 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Credit Suisse Securities (USA) LLC |

2.15 | 02/26/19 | Open | 207,680 | 210,523 | Foreign Agency Obligations | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

0.75 | 03/04/19 | Open | 258,126 | 259,094 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.40 | 03/04/19 | Open | 242,685 | 245,597 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.60 | 03/04/19 | Open | 273,257 | 276,809 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.60 | 03/04/19 | Open | 441,559 | 447,300 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.60 | 03/04/19 | Open | 477,720 | 483,931 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.60 | 03/04/19 | Open | 659,311 | 667,882 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.60 | 03/04/19 | Open | 1,207,335 | 1,223,030 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.60 | 03/04/19 | Open | 383,152 | 388,133 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.60 | 03/04/19 | Open | 158,392 | 160,451 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 03/05/19 | Open | 474,881 | 481,965 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.50 | 03/11/19 | Open | 190,858 | 193,124 | Foreign Agency Obligations | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.80 | 03/26/19 | Open | 802,710 | 813,523 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.80 | 03/26/19 | Open | 691,437 | 700,693 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 03/29/19 | Open | 190,275 | 192,701 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.25 | 04/12/19 | Open | 781,750 | 790,051 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.25 | 04/12/19 | Open | 1,316,875 | 1,330,858 | Capital Trusts | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.25 | 04/12/19 | Open | 1,370,625 | 1,385,178 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.25 | 04/12/19 | Open | 1,552,845 | 1,569,333 | Capital Trusts | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.25 | 04/12/19 | Open | 1,259,375 | 1,272,747 | Capital Trusts | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.25 | 04/12/19 | Open | 2,272,050 | 2,296,175 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 04/12/19 | Open | 855,400 | 865,308 | Capital Trusts | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 04/12/19 | Open | 1,181,575 | 1,195,262 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 04/12/19 | Open | 2,340,000 | 2,367,105 | Capital Trusts | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 04/12/19 | Open | 1,345,075 | 1,360,655 | Capital Trusts | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 04/12/19 | Open | 1,089,108 | 1,101,723 | Capital Trusts | Open/Demand | |||||||||||||||||

| Goldman Sachs & Co LLC |

2.40 | 04/12/19 | Open | 1,354,175 | 1,366,994 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 04/18/19 | Open | 130,579 | 132,015 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.80 | 04/24/19 | Open | 307,440 | 310,800 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.65 | 04/29/19 | Open | 470,000 | 474,733 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.30 | 05/03/19 | Open | 286,877 | 289,510 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Credit Suisse Securities (USA) LLC |

2.25 | 05/07/19 | Open | 176,500 | 178,001 | Foreign Agency Obligations | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 05/13/19 | Open | 1,004,981 | 1,014,277 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 05/13/19 | Open | 869,535 | 877,578 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 05/13/19 | Open | 784,988 | 792,249 | Capital Trusts | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 05/15/19 | Open | 224,338 | 226,264 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.00 | 05/20/19 | Open | 106,080 | 106,839 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.40 | 05/24/19 | Open | 812,000 | 817,977 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Credit Suisse Securities (USA) LLC |

1.95 | 06/11/19 | Open | 210,250 | 211,409 | Foreign Agency Obligations | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

0.67 | 06/20/19 | Open | 10,912 | 10,938 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.36 | 06/21/19 | Open | 94,510 | 95,003 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.50 | 06/21/19 | Open | 369,922 | 372,172 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.51 | 06/21/19 | Open | 581,788 | 584,999 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.52 | 06/21/19 | Open | 219,794 | 221,011 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.64 | 06/21/19 | Open | 252,450 | 253,985 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.64 | 06/21/19 | Open | 2,421,969 | 2,435,384 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.65 | 06/21/19 | Open | 703,099 | 707,177 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.65 | 06/21/19 | Open | 2,902,500 | 2,919,334 | Capital Trusts | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.65 | 06/21/19 | Open | 1,483,125 | 1,491,727 | Capital Trusts | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.70 | 06/21/19 | Open | 838,189 | 843,285 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.70 | 06/21/19 | Open | 618,008 | 621,654 | Corporate Bonds | Open/Demand | |||||||||||||||||

| 46 | 2019 BLACKROCK ANNUAL REPORT TO SHAREHOLDERS |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) |

Reverse Repurchase Agreements (continued)

| Counterparty | Interest Rate |

Trade Date |

Maturity Date (a) |

Face Value | Face Value Including Accrued Interest |

Type of Non-Cash Underlying Collateral |

Remaining Contractual Maturity of the Agreements (a) | |||||||||||||||||

| BNP Paribas S.A. |

2.70 | % | 06/21/19 | Open | $ | 944,843 | $ | 950,417 | Corporate Bonds | Open/Demand | ||||||||||||||

| BNP Paribas S.A. |

2.70 | 06/21/19 | Open | 157,885 | 158,816 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.70 | 06/21/19 | Open | 130,975 | 131,716 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.72 | 06/21/19 | Open | 5,264,190 | 5,291,742 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.72 | 06/21/19 | Open | 531,644 | 534,802 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.79 | 06/21/19 | Open | 457,209 | 459,989 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.79 | 06/21/19 | Open | 1,351,565 | 1,359,674 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.79 | 06/21/19 | Open | 802,240 | 806,973 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.79 | 06/21/19 | Open | 226,187 | 227,563 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.79 | 06/21/19 | Open | 993,200 | 999,239 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.79 | 06/21/19 | Open | 292,777 | 294,558 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.79 | 06/21/19 | Open | 590,008 | 593,595 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.79 | 06/21/19 | Open | 1,015,728 | 1,021,903 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 1,776,250 | 1,785,748 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 98,375 | 98,901 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 993,431 | 998,744 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 535,575 | 538,439 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 392,531 | 394,630 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 1,455,000 | 1,462,781 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 465,000 | 467,487 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 2,364,675 | 2,377,320 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 263,312 | 264,721 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 285,937 | 287,467 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 1,218,544 | 1,225,060 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 430,650 | 432,953 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 1,452,506 | 1,460,274 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 370,781 | 372,764 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 843,750 | 848,262 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 162,350 | 163,218 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 134,925 | 135,646 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 343,350 | 345,186 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 1,434,125 | 1,441,794 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 1,493,888 | 1,501,876 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 654,063 | 657,560 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 1,528,788 | 1,536,963 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 407,531 | 409,711 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 154,635 | 155,462 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 256,275 | 257,645 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 386,250 | 388,315 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 288,562 | 290,106 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 680,231 | 683,869 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 229,125 | 230,350 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.54 | 06/21/19 | Open | 1,110,819 | 1,116,759 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.79 | 06/21/19 | Open | 275,224 | 276,696 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 06/26/19 | Open | 842,310 | 846,943 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 07/10/19 | Open | 608,130 | 610,816 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 07/10/19 | Open | 707,350 | 710,474 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 07/10/19 | Open | 587,400 | 589,994 | Corporate Bonds | Open/Demand | |||||||||||||||||

| RBC Capital Markets, LLC |

2.80 | 07/11/19 | Open | 255,780 | 256,885 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 07/12/19 | Open | 1,233,568 | 1,238,502 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 07/12/19 | Open | 1,066,051 | 1,070,582 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 07/16/19 | Open | 110,760 | 111,185 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.25 | 07/16/19 | Open | 457,464 | 458,925 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.30 | 07/16/19 | Open | 569,250 | 571,105 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.30 | 07/16/19 | Open | 795,150 | 797,741 | Corporate Bonds | Open/Demand | |||||||||||||||||

| BNP Paribas S.A. |

2.30 | 07/16/19 | Open | 334,051 | 335,140 | Corporate Bonds | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.26 | 07/17/19 | Open | 6,512,000 | 6,532,538 | U.S. Treasury Obligations | Open/Demand | |||||||||||||||||

| HSBC Securities (USA), Inc. |

2.26 | 07/17/19 | Open | 8,316,000 | 8,342,228 | U.S. Treasury Obligations | Open/Demand | |||||||||||||||||

| Citigroup Global Markets, Inc. |

1.75 | 07/19/19 | Open | 117,972 | 118,241 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.30 | 07/25/19 | Open | 179,000 | 179,515 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 07/26/19 | Open | 414,335 | 415,509 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 07/26/19 | Open | 331,380 | 332,319 | Corporate Bonds | Open/Demand | |||||||||||||||||

| SCHEDULES OF INVESTMENTS | 47 |

| Schedule of Investments (continued) August 31, 2019 |

BlackRock Limited Duration Income Trust (BLW) |

Reverse Repurchase Agreements (continued)

| Counterparty | Interest Rate |

Trade Date |

Maturity Date (a) |

Face Value | Face Value Including Accrued Interest |

Type of Non-Cash Underlying Collateral |

Remaining Contractual Maturity of the Agreements (a) | |||||||||||||||||

| RBC Capital Markets, LLC |

2.80 | % | 07/26/19 | Open | $ | 88,125 | $ | 88,379 | Corporate Bonds | Open/Demand | ||||||||||||||

| Barclays Capital, Inc. |

2.50 | 08/01/19 | Open | 1,333,745 | 1,336,801 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

2.50 | 08/07/19 | Open | 455,809 | 456,568 | Corporate Bonds | Open/Demand | |||||||||||||||||

| Barclays Capital, Inc. |

0.00 | 08/08/19 | Open | 168,937 | 168,939 | Corporate Bonds | Open/Demand | |||||||||||||||||

| TD Securities (USA) LLC |

2.33 | 08/12/19 | 9/12/19 | 4,492,000 | 4,497,524 | U.S. Government Sponsored Agency Securities | Up to 30 Days | |||||||||||||||||

| TD Securities (USA) LLC |

2.33 | 08/12/19 | 9/12/19 | 3,056,000 | 3,059,758 | U.S. Government Sponsored Agency Securities | Up to 30 Days | |||||||||||||||||

| Barclays Capital, Inc. |