Filed pursuant to Rule 424(b)(5)

Securities Act File No. 333-229337

PROSPECTUS SUPPLEMENT

(to Prospectus dated May 13, 2020)

$70,000,000

![]()

Oxford Square Capital Corp.

5.50% Notes due 2028

Our investment objective is to maximize our portfolio’s total return. Our primary current focus is to seek an attractive risk-adjusted total return by investing primarily in corporate debt securities and collateralized loan obligation (“CLO”) structured finance investments that own corporate debt securities. CLO investments may also include warehouse facilities, which are financing structures intended to aggregate loans that may be used to form the basis of a traditional CLO vehicle. We may also invest in publicly traded debt and/or equity securities. We operate as a closed-end, non-diversified management investment company and have elected to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). The portfolio companies in which we invest, however, will generally be considered below investment grade, and their debt securities may in turn be referred to as “junk.” A portion of our investment portfolio may consist of debt investments for which issuers are not required to make significant principal payments until the maturity of the senior loans, which could result in a substantial loss to us if such issuers are unable to refinance or repay their debt at maturity. In addition, many of the debt securities we hold typically contain interest reset provisions that may make it more difficult for a borrower to repay the loan, heightening the risk that we may lose all or part of our investment.

We are offering $70.0 million in aggregate principal amount of 5.50% notes due 2028, which we refer to as the “Notes.” The Notes will mature on July 31, 2028. We will pay interest on the Notes on January 31, April 30, July 31 and October 31 of each year, beginning on July 31, 2021. We may redeem the Notes in whole or in part at any time, or from time to time, on or after May 31, 2024, at the redemption price of par, plus accrued interest, as discussed under the caption “Description of the Notes — Optional Redemption” in this prospectus supplement. The Notes will be issued in minimum denominations of $25 and integral multiples of $25 in excess thereof.

The Notes will be our direct unsecured obligations and rank pari passu, which means equal to, all outstanding and future unsecured unsubordinated indebtedness issued by us, including our 6.50% Unsecured Notes due 2024 (the “6.50% Unsecured Notes”) and our 6.25% Unsecured Notes due 2026 (the “6.25% Unsecured Notes”), of which we had $64.4 million and $44.8 million outstanding, respectively, as of March 31, 2021. Because the Notes will not be secured by any of our assets, they will be effectively subordinated to all of our existing and future secured indebtedness (including indebtedness that is initially unsecured to which we subsequently grant security), to the extent of the value of the assets securing such indebtedness. The Notes will be structurally subordinated to all existing and future indebtedness and other obligations of any of our subsidiaries, CLO vehicles in which we hold an equity interest and financing vehicles since the Notes are obligations exclusively of Oxford Square Capital Corp. and not of any of our subsidiaries. The Notes will not be required to be guaranteed by any subsidiary we may acquire or create in the future. In any liquidation, dissolution, bankruptcy or other similar proceeding, the holders of any of our existing or future secured indebtedness may assert rights against the assets pledged to secure that indebtedness in order to receive full payment of their indebtedness before the assets may be used to pay other creditors, including the holders of the Notes, and any assets of our subsidiaries will not be directly available to satisfy the claims of our creditors, including holders of the Notes.

The Notes will also rank pari passu, which means equal to, our general liabilities. In total, these general liabilities were approximately $13.6 million as of March 31, 2021. We currently do not have outstanding debt that is subordinated to the Notes and do not currently intend to issue indebtedness that expressly provides that it is subordinated to the Notes. Therefore, the Notes will not be senior to any indebtedness or obligations.

We intend to list the Notes on the NASDAQ Global Select Market and we expect trading to commence thereon within 30 days of the original issue date under the trading symbol “OXSQG.” The Notes are expected to trade “flat.” This means that purchasers will not pay, and sellers will not receive, any accrued and unpaid interest on the Notes that is not included in the trading price. Currently, there is no public market for the Notes and there can be no assurance that one will develop.

Please read this prospectus supplement, the accompanying prospectus, and the documents incorporated by reference into this prospectus supplement and the accompanying prospectus before investing in the Notes, and keep each for future reference. This prospectus supplement, the accompanying prospectus, and the documents incorporated by reference into this prospectus supplement and the accompanying prospectus contain important information about us that a prospective investor should know before investing in the Notes. We are required to file annual, quarterly and current reports, proxy statements, and other information about us with the SEC. This information is available free of charge by contacting us by mail at 8 Sound Shore Drive, Suite 255, Greenwich, CT 06830, by telephone at (203) 983-5275 or on our website at http://www.oxfordsquarecapital.com. The SEC also maintains a website at http://www.sec.gov that contains such information. Information contained on our website is not incorporated by reference into this prospectus supplement or the accompanying prospectus, and you should not consider that information to be part of this prospectus supplement or the accompanying prospectus, except documents incorporated by reference into this prospectus supplement or the accompanying prospectus.

Investing in the Notes involves a high degree of risk and should be considered speculative. For more information regarding the risks you should consider, including the risk of leverage, please see “Supplementary Risk Factors” beginning on page S-18 of this prospectus supplement and “Risk Factors” on page 14 of the accompanying prospectus and under similar headings in the documents that are incorporated by reference into this prospectus supplement and the accompanying prospectus.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or determined if either this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters have agreed to purchase the Notes from us at 96.875% of the aggregate principal amount of the Notes (resulting in $67,812,500 in aggregate proceeds to us, before deducting expenses payable by us). The underwriters propose to offer the Notes for sale, from time to time, in one or more negotiated transactions, at prices that may be different than par. These sales may occur at market prices prevailing at the time of sale, at prices related to such prevailing market prices or at prices negotiated by the joint book-running managers or with approval from the joint book-running managers.

|

Per Note |

Total |

|||||

|

Public offering price |

$ |

25.00 |

$ |

70,000,000 |

||

|

Underwriting discount (sales load) |

$ |

0.78125 |

$ |

2,187,500 |

||

|

Proceeds to us before expenses(1) |

$ |

24.21875 |

$ |

67,812,500 |

||

____________

(1) We estimate that we will incur approximately $250,000 in offering expenses in connection with this offering. See “Underwriting.”

The underwriters may exercise an option to purchase up to an additional $10.5 million total aggregate principal amount of Notes offered hereby, within 30 days of the date of this prospectus supplement. If this option is exercised in full, the total public offering price will be $80,500,000, the total underwriting discount (sales load) paid by us will be $2,515,625, and total proceeds, before expenses, will be $77,984,375.

THE NOTES ARE NOT DEPOSITS OR OTHER OBLIGATIONS OF A BANK AND ARE NOT INSURED BY THE FEDERAL DEPOSIT INSURANCE CORPORATION OR ANY OTHER GOVERNMENT AGENCY.

Delivery of the Notes in book-entry form only through The Depository Trust Company will be made on or about May 20, 2021.

|

Joint Book-Running Managers |

||||

|

Ladenburg Thalmann |

B. Riley Securities |

William Blair |

||

|

Lead Managers |

|

Compass Point |

Incapital |

National Securities Corporation |

The date of this prospectus supplement is May 13, 2021

TABLE OF CONTENTS

PROSPECTUS SUPPLEMENT

|

Page |

||

|

S-ii |

||

|

S-1 |

||

|

S-10 |

||

|

S-16 |

||

|

S-18 |

||

|

S-22 |

||

|

S-23 |

||

|

S-24 |

||

|

S-35 |

||

|

S-39 |

||

|

S-43 |

||

|

S-43 |

||

|

S-43 |

||

|

S-44 |

PROSPECTUS

|

1 |

||

|

9 |

||

|

12 |

||

|

14 |

||

|

15 |

||

|

17 |

||

|

18 |

||

|

21 |

||

|

22 |

||

|

31 |

||

|

33 |

||

|

36 |

||

|

43 |

||

|

44 |

||

|

50 |

||

|

51 |

||

|

51 |

||

|

58 |

||

|

59 |

||

|

61 |

||

|

62 |

||

|

77 |

||

|

79 |

||

|

CUSTODIAN, TRANSFER AND DISTRIBUTION PAYING AGENT AND REGISTRAR |

79 |

|

|

79 |

||

|

79 |

||

|

79 |

||

|

80 |

S-i

ABOUT THIS PROSPECTUS SUPPLEMENT

We have filed a registration statement on Form N-2 (File No. 333-229337) utilizing a shelf registration process relating to the securities described in this prospectus supplement, which registration statement was declared effective on May 13, 2020.

This document is in two parts. The first part is the prospectus supplement, which describes the terms of this offering of Notes and also adds to and updates information contained in the accompanying prospectus. The second part is the accompanying prospectus, which gives more general information and disclosure. To the extent the information contained in this prospectus supplement differs from or is additional to the information contained in the accompanying prospectus, you should rely only on the information contained in this prospectus supplement and the documents incorporated by reference herein. Please carefully read and consider all of the information contained in this prospectus supplement and the accompanying prospectus, including the information described under the headings “Incorporation of Certain Information by Reference,” “Where You Can Find Additional Information,” and “Supplementary Risk Factors” in this prospectus supplement and under the headings “Incorporation of Certain Information by Reference,” “Where You Can Find Additional Information,” and “Risk Factors” included in the accompanying prospectus, respectively, before investing in our Notes.

Neither we nor Ladenburg Thalmann & Co. Inc. has authorized any dealer, salesman or other person to give any information or to make any representation other than those contained in or incorporated by reference into this prospectus supplement or the accompanying prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. This prospectus supplement and the accompanying prospectus do not constitute an offer to sell or a solicitation of any offer to buy any security other than the Notes, nor do they constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction or to any person to whom it is unlawful to make such an offer or solicitation in such jurisdiction. The information contained in or incorporated by reference into this prospectus supplement and the accompanying prospectus is accurate as of their respective dates or such earlier date as indicated therein. Our financial condition, results of operations and prospects may have changed since those dates. To the extent required by law, we will amend or supplement the information contained in or incorporated by reference into this prospectus supplement and the accompanying prospectus to reflect any material changes subsequent to the date of this prospectus supplement and the accompanying prospectus and prior to the completion of any offering pursuant to this prospectus supplement and the accompanying prospectus.

S-ii

The following summary contains basic information about the offering of our Notes included elsewhere, or incorporated by reference, in this prospectus supplement and the accompanying prospectus. It is not complete and may not contain all the information that is important to you. For a more complete understanding of the offering of our Notes pursuant to this prospectus supplement, we encourage you to read this entire prospectus supplement and the accompanying prospectus, including the documents incorporated by reference herein or therein, as well as the documents to which we have referred in this prospectus supplement and the accompanying prospectus. Together, these documents describe the specific terms of the Notes we are offering. You should carefully read “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 of our most recent Annual Report on Form 10-K, and in Part 1, Item 2 of our most recent Quarterly Report on Form 10-Q for more information and the sections entitled “Risk Factors,” “Business,” “Incorporation of Certain Information by Reference” and our financial statements included in the accompanying prospectus and “Supplementary Risk Factors” and “Incorporation of Certain Information by Reference” in this prospectus supplement.

Except where the context requires otherwise, the terms “OXSQ,” “Company,” “we,” “us” and “our” refer to Oxford Square Capital Corp.; “Oxford Square Management” refers to Oxford Square Management, LLC; and “Oxford Funds” refers to Oxford Funds, LLC.

Overview

We are a closed-end, non-diversified management investment company that has elected to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). We have elected to be treated for tax purposes as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”) beginning with our 2003 taxable year. Our investment objective is to maximize our portfolio’s total return. Our primary current focus is to seek an attractive risk-adjusted total return by investing primarily in corporate debt securities and collateralized loan obligation (“CLO”) structured finance investments that own corporate debt securities. CLO investments may also include warehouse facilities, which are early-stage CLO vehicles intended to aggregate loans that may be used to form the basis of a traditional CLO vehicle. We may also invest in publicly traded debt and/or equity securities. As a BDC, we may not acquire any asset other than “qualifying assets” unless, at the time we make the acquisition, the value of our qualifying assets represents at least 70% of the value of our total assets.

We generally expect to invest between $5.0 million and $25.0 million in each of our portfolio investments, although this investment size may vary as the size of our capital base changes and market conditions warrant. We invest in both fixed and variable interest rate structures. We expect that our investment portfolio will be diversified among many investments with few investments exceeding 5% of the total portfolio.

Our capital is generally used by our corporate borrowers to finance organic growth, acquisitions, recapitalizations and working capital. Our investment decisions are based on extensive analysis of potential portfolio companies’ business operations supported by an in-depth understanding of the quality of their recurring revenues and cash flow, variability of costs and the inherent value of their assets, including proprietary intangible assets and intellectual property. In making our CLO investments, we consider the indenture structure for that vehicle, its operating characteristics and compliance with its various indenture provisions, as well as its corporate loan-based collateral pool.

Our corporate debt investments will vary, and we seek to invest across a wide range of different industries. Many of these companies have financial backing provided by other financial or strategic sponsors at the time we make an investment. The portfolio companies in which we invest, however, will generally be considered below investment grade, and their debt securities may in turn be referred to as “junk.” Our investment portfolio will likely continue to consist of debt investments for which issuers are not required to make significant principal payments until the maturity of the senior loans, which could result in a substantial loss to us if such issuers are unable to refinance or repay their debt at maturity.

We also purchase portions of equity and junior debt tranches of CLO vehicles. Substantially all the CLO vehicles in which we may invest would be deemed to be investment companies under the 1940 Act but for the exceptions set forth in section 3(c)(1) or section 3(c)(7). Other than CLO vehicles, we do not intend to invest, and we would be limited to 15% of our net assets if we did invest, in any types of entities that rely on the exceptions set forth in section 3(c)(1) or section 3(c)(7) of the 1940 Act. Structurally, CLO vehicles are entities that are formed

S-1

to originate and manage a portfolio of loans. The loans within the CLO vehicle are limited to loans which meet established credit criteria and are subject to concentration limitations to limit a CLO vehicle’s exposure to a single credit. A CLO vehicle is formed by raising various classes or “tranches” of debt (with the most senior tranches being rated “AAA” to the most junior tranches typically being rated “BB” or “B”) and equity. The tranches of CLO vehicles rated “BB” or “B” may be referred to as “junk.” The equity of a CLO vehicle is generally required to absorb the CLO’s losses before any of the CLO’s other tranches, yet it also has the lowest level of payment priority among the CLO’s tranches; therefore, the equity is typically the riskiest of CLO investments. We primarily focus on investing in the junior tranches and the equity of CLO vehicles. The CLO vehicles which we focus on are collateralized primarily by senior secured loans made to companies whose debt is unrated or is rated below investment grade, and generally have very little or no direct exposure to real estate, mortgage loans or to pools of consumer-based debt, such as credit card receivables or auto loans. However, there can be no assurance that the collateral securing such senior secured loans would satisfy all the unpaid principal and interest of our investment in the CLO vehicle in the event of default and the junior tranches, especially the equity tranches, of CLO vehicles are the last tranches to be paid, if at all, in the event of a default. Our investment strategy may also include warehouse facilities, which are early-stage CLO vehicles intended to aggregate loans that may be used to form the basis of a traditional CLO vehicle.

We have historically borrowed funds to make investments and may continue to do so. As a result, we are exposed to the risks of leverage, which may be considered a speculative investment technique. Borrowings, also known as leverage, magnify the potential for gain and loss on amounts invested and therefore increase the risks associated with investing in our securities. In addition, the costs associated with our borrowings, including any increase in the advisory fee payable to our investment adviser, Oxford Square Management, will be borne by our common stockholders.

The total fair value of our investment portfolio was approximately $320.6 million and $294.7 million as of March 31, 2021, and December 31, 2020, respectively. The increase in the value of investments during the three month period ended March 31, 2021, was due primarily to net unrealized appreciation on our investment portfolio of approximately $31.0 million (which incorporates reductions to CLO equity cost value of $6.0 million) and $32.9 million of investments acquired, which was partially offset by $16.4 million of debt repayments, $1.8 million of sales of investments and realized losses of $14.1 million.

See “Business” in Part I, Item 1 in our most recent Annual Report on Form 10-K for additional information about us and our investment adviser, Oxford Square Management.

6.50% Unsecured Notes

On April 12, 2017, we completed an underwritten public offering of approximately $64.4 million in aggregate principal amount of our 6.50% Unsecured Notes. The 6.50% Unsecured Notes mature on March 30, 2024, and may be redeemed in whole or in part at any time or from time to time at our option on or after March 30, 2020. The 6.50% Unsecured Notes bear interest at a rate of 6.50% per year payable quarterly on March 30, June 30, September 30, and December 30 of each year. The 6.50% Unsecured Notes are listed on the NASDAQ Global Select Market under the trading symbol “OXSQL.”

6.25% Unsecured Notes

On April 3, 2019, we completed an underwritten public offering of approximately $44.8 million in aggregate principal amount of our 6.25% Unsecured Notes. The 6.25% Unsecured Notes mature on April 30, 2026, and may be redeemed in whole or in part at any time or from time to time at our option on or after April 30, 2022. The 6.25% Unsecured Notes bear interest at a rate of 6.25% per year payable quarterly on January 31, April 30, July 31 and October 31 of each year. The 6.25% Unsecured Notes are listed on the NASDAQ Global Select Market under the trading symbol “OXSQZ.”

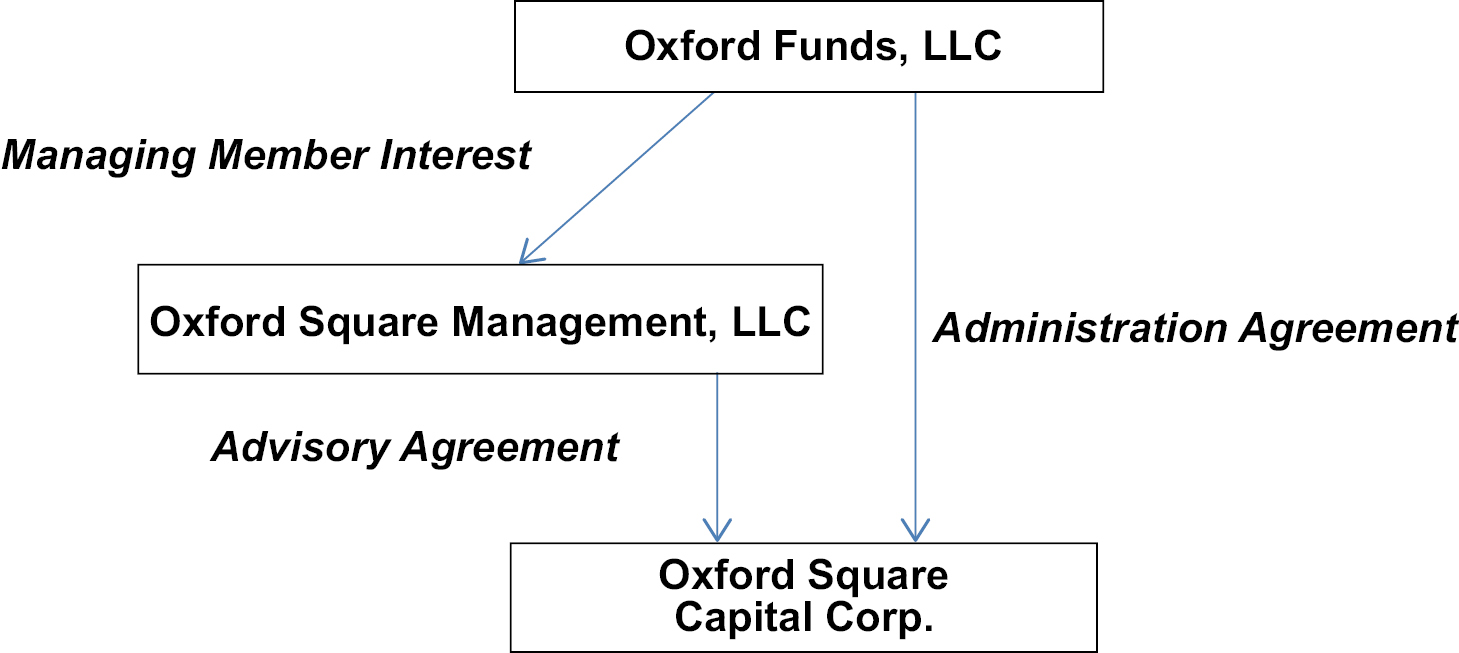

Organizational and Regulatory Structure

Our investment activities are managed by Oxford Square Management. Oxford Square Management is an investment adviser registered under the Investment Advisers Act of 1940, as amended, or the “Advisers Act.” Oxford Square Management is owned by Oxford Funds, its managing member, and Charles M. Royce, a member of our Board of Directors who holds a minority, non-controlling interest in Oxford Square Management. Jonathan H. Cohen, our Chief Executive Officer, and Saul B. Rosenthal, our President and Chief Operating Officer, directly or indirectly

S-2

own or control all of the outstanding equity interests of Oxford Funds. Under the investment advisory agreement, or the “Investment Advisory Agreement,” we have agreed to pay Oxford Square Management an annual base management fee based on our gross assets as well as an incentive fee based on our performance.

We were founded in July 2003 and completed an initial public offering of shares of our common stock in November 2003. We are a Maryland corporation and a closed-end, non-diversified management investment company that has elected to be regulated as a BDC under the 1940 Act. As a BDC, we are required to meet certain regulatory tests, including the requirement to invest at least 70% of our total assets in eligible portfolio companies. For more information, see Item 1. Business — Regulation as a Business Development Company” in our most recent Annual Report on Form 10-K. In addition, we have elected to be treated for U.S. federal income tax purposes, and intend to qualify annually, as a RIC.

Set forth below is a chart detailing our current organizational structure.

Our Corporate Information

Our headquarters are located at 8 Sound Shore Drive, Suite 255 Greenwich, Connecticut and our telephone number is (203) 983-5275.

Market Overview and Opportunity

The broader corporate loan and CLO equity market exhibited volatility in 2020. Significant weakness during the first quarter of 2020 was followed by significant strength during the remainder of the year. During the first quarter of 2020, the S&P/LSTA Leveraged Loan Index decreased from a price of 96.72% at the end of December 2019 to 82.85% at the end of March 2020. During this period, lower credit quality loans significantly underperformed higher credit quality loans. The S&P/LSTA Leveraged Loan Index ended the year at a price of 96.19%, with lower credit quality loans outperforming higher credit quality loans during the period of March 2020 through December 2020. For the full year, BB rated loan prices decreased 0.72%, B rated loan prices increased 0.67%, and CCC rated loan prices increased 5.46%. We believe that the significant volatility of the loan market during 2020 was driven by the negative impact of the COVID-19 pandemic on the global economic outlook and individual loan issuers followed by improvement in this outlook over the course of 2020. We believe that while the U.S. loan market has stabilized, conditions continue to exhibit weakness versus the end of 2019 as exhibited by an increase in default rates to 3.8% at the end of 2020 versus 1.4% at the end of 2019. This environment may allow corporate loan and CLO managers to buy performing loan assets in the secondary market at discounts to par, which may build CLO asset value and spread over time, ultimately accruing to the benefit of CLO equity. Moreover, as we execute our corporate loan strategy of focusing primarily on smaller broadly syndicated loans, narrowly syndicated loans and private deals, through purchases in both the primary and secondary markets, we remain mindful of maintaining overall portfolio liquidity. We believe this strategy allows us to maintain corporate debt investments which have sufficient liquidity in order to take advantage of market opportunities.

S-3

Competitive Advantages

We believe that we are well positioned to provide financing to corporate borrowers and structured finance vehicles that, in turn, provide capital to corporate borrowers for the following reasons:

• Expertise in credit analysis and monitoring investments; and

• Established transaction sourcing network.

Expertise in credit analysis and monitoring investments

While our investment focus is on middle-market companies, we have invested, and in the future will likely continue to invest, in larger and smaller companies and in other investment structures on an opportunistic basis, including CLO investment vehicles. We believe our experience in analyzing middle-market companies and CLO investment structures, as detailed in the biographies of Oxford Square Management’s senior investment professionals, affords us a sustainable competitive advantage over lenders with limited experience in investing in these markets. In particular, we have expertise in evaluating the investment merits of middle-market companies as well as the structural features of CLO investments, and monitoring the credit risk of such investments after closing until full repayment.

• Jonathan H. Cohen, our Chief Executive Officer, has more than 25 years of experience in debt and equity research and investment. Mr. Cohen has also served as Chief Executive Officer and a Director of Oxford Lane Capital Corp. (NasdaqGS: OXLC), a registered closed-end fund, and as Chief Executive Officer of its investment adviser, Oxford Lane Management, LLC, or “Oxford Lane Management,” since 2010. Since 2015 and 2018, respectively, Mr. Cohen has also served as Chief Executive Officer of Oxford Bridge Management, LLC, or “Oxford Bridge Management,” the investment adviser to Oxford Bridge, LLC and Oxford Bridge II, LLC (collectively, the “Oxford Bridge Funds”), and Oxford Gate Management, LLC, or “Oxford Gate Management,” the investment adviser to Oxford Gate Master Fund, LLC, Oxford Gate, LLC and Oxford Gate (Bermuda), LLC (collectively, the “Oxford Gate Funds”). The Oxford Bridge Funds and the Oxford Gate Funds are private investment funds. Previously, Mr. Cohen managed technology equity research groups at Wit Capital, Merrill Lynch, UBS and Smith Barney. Mr. Cohen is a member of the Board of Trustees of Connecticut College. Mr. Cohen received a B.A. in Economics from Connecticut College and an M.B.A. from Columbia University.

• Saul B. Rosenthal, our President and Chief Operating Officer, has more than 20 years of experience in the capital markets, with a focus on middle-market transactions. In addition, Mr. Rosenthal has served as President and a Director of Oxford Lane Capital Corp. (NasdaqGS: OXLC), a registered closed-end fund, and as President of Oxford Lane Management, since 2010. Mr. Rosenthal has also served as President of Oxford Bridge Management, the investment adviser to the Oxford Bridge Funds and Oxford Gate Management, the investment adviser to the Oxford Gate Funds, since 2015 and 2018, respectively. Mr. Rosenthal was previously an attorney at the law firm of Shearman & Sterling LLP. Mr. Rosenthal serves on the board of the National Museum of Mathematics. Mr. Rosenthal received a B.S., magna cum laude, from the Wharton School of the University of Pennsylvania, a J.D. from Columbia University Law School, where he was a Harlan Fiske Stone Scholar, and a LL.M. (Taxation) from New York University School of Law.

• Darryl Monasebian is the Executive Vice President and head of risk and portfolio management of Oxford Square Management, and also holds those same positions at Oxford Lane Management, the investment adviser to Oxford Lane Capital Corp., Oxford Bridge Management, the investment adviser to the Oxford Bridge Funds and Oxford Gate Management, the investment adviser to the Oxford Gate Funds. Prior to joining Oxford Square Management, Mr. Monasebian was a director in the Merchant Banking Group at BNP Paribas, and prior to that he was a director at Swiss Bank Corporation and a senior account officer at Citibank. He began his business career at Metropolitan Life Insurance Company as an investment analyst in the Corporate Investments Department. Mr. Monasebian received a B.S. in Management Science/Operations Research from Case Western Reserve University and a Masters of Business Administration from Boston University’s Graduate School of Management.

S-4

• Debdeep Maji is a Senior Managing Director of Oxford Square Management, and also holds the same position at Oxford Lane Management, the investment adviser to Oxford Lane Capital Corp., at Oxford Bridge Management, the investment adviser to the Oxford Bridge Funds and Oxford Gate Management, the investment adviser to the Oxford Gate Funds. Mr. Maji graduated from the Jerome Fisher Program in Management and Technology at the University of Pennsylvania where he received a Bachelor of Science degree in Economics from the Wharton School (and was designated a Joseph Wharton Scholar) and a Bachelor of Applied Science from the School of Engineering.

• Kevin Yonon is a Managing Director of Oxford Square Management, and also holds the same position at Oxford Lane Management, the investment adviser to Oxford Lane Capital Corp., at Oxford Bridge Management, the investment adviser to the Oxford Bridge Funds and Oxford Gate Management, the investment adviser to the Oxford Gate Funds. Previously, Mr.Yonon was an Associate at Deutsche Bank Securities and prior to that he was an Analyst at Blackstone Mezzanine Partners. Before joining Blackstone, he worked as an Analyst at Merrill Lynch in the Mergers & Acquisitions group. Mr.Yonon received a B.S. in Economics with concentrations in Finance and Accounting from the Wharton School at the University of Pennsylvania, where he graduated magna cum laude, and an M.B.A. from the Harvard Business School.

Established deal sourcing network

Through the investment professionals of Oxford Square Management, we have extensive contacts and sources from which to generate investment opportunities. These contacts and sources include private equity funds, companies, brokers and bankers. We believe that senior professionals of Oxford Square Management have developed strong relationships within the investment community over their years within the banking, investment management and equity research fields.

Advisory Fee

General Terms

We pay Oxford Square Management an advisory fee for its services under the Investment Advisory Agreement consisting of a base advisory fee (the “Base Fee”) and two types of incentive fees.

The Base Fee is payable quarterly in arrears, calculated based on a percentage of the average value of our gross assets at the end of the two most recently completed calendar quarters, and appropriately prorated for any partial quarter.

The incentive fees are commonly referred to as the “income incentive fee” and the “capital gains incentive fee,” with the first fee payable quarterly in arrears and the second fee payable in arrears at the end of each calendar year.

• The first fee, which we refer to as the “Net Investment Income Incentive Fee,” is determined by reference to the Company’s “Pre-Incentive Fee Net Investment Income” (as defined below). Given that this incentive fee is payable without regard to any gain, loss or unrealized depreciation that may occur during the quarter, Oxford Square Management’s incentive fee may be payable notwithstanding a decline in net asset value that quarter.

• The second fee, which we refer to as the “Capital Gains Incentive Fee,” equals 20% of our “Incentive Fee Capital Gains,” which consists of our realized capital gains for each calendar year, computed net of all realized capital losses and unrealized capital depreciation for that calendar year. For accounting purposes under U.S. generally accepted accounting principles, the Capital Gains Incentive Fee is based on a hypothetical liquidation of the Company. In such a calculation, in order to reflect the theoretical Capital Gains Incentive Fee that would have been payable for a given period as if all unrealized gains were realized, we will accrue a Capital Gains Incentive Fee based upon net realized gains and unrealized depreciation for that calendar year (in accordance with the terms of the Investment Advisory Agreement), plus unrealized appreciation on investments held at the end of the period. It should be noted that a fee so calculated and accrued would not necessarily be payable under the Investment Advisory

S-5

Agreement, and may never be paid based upon the computation of Capital Gains Incentive Fees in subsequent periods. Amounts paid under the Investment Advisory Agreement will be consistent with the formula in the Investment Advisory Agreement.

The cost of both the Base Fee payable to Oxford Square Management and any incentive fees earned by Oxford Square Management are ultimately borne by our common stockholders.

Calculation of Fees under the Investment Advisory Agreement and 2016 Fee Waiver

The Investment Advisory Agreement specifies the calculation of the advisory fee payable thereunder, as described in greater detail below. However, Oxford Square Management unilaterally determined to waive, under certain circumstances, part of its total fees payable under the Investment Advisory Agreement, pursuant to a fee waiver letter effective April1, 2016 (the “2016 Fee Waiver”).

The Investment Advisory Agreement provides for a series of calculations to be used in determining the Base Fee and Net Investment Income Incentive Fee payable to Oxford Square Management. The 2016 Fee Waiver operates by providing for a second series of calculations to be run alongside the calculations of the Base Fee and Net Investment Income Incentive Fee under the Investment Advisory Agreement. In the event that the second set of calculations produces a higher combined Base Fee and Net Investment Income Incentive Fee for any quarterly period, those combined fees are set to the original (lower) level, calculated pursuant to the Investment Advisory Agreement. In the event that the second set of calculations produces lower combined Base Fee and Net Investment Income Incentive Fee for that quarterly period, those lower combined fees are adopted for that quarterly period. In either case, the lower level of combined fees is used for that quarter, and, accordingly, the advisory fee payable to Oxford Square Management can only be reduced, and never increased, as a result of the 2016 Fee Waiver.

Calculation of Fees under the Investment Advisory Agreement. Under the Investment Advisory Agreement, and without applying the 2016 Fee Waiver, the total advisory fee would be calculated as follows:

1) Base Fee: The Base Fee is calculated at an annual rate of 2.00% of our gross assets, and appropriately adjusted for any equity or debt capital raises, repurchases or redemptions during the current calendar quarter.

2) Net Investment Income Incentive Fee: The Net Investment Income Incentive Fee is calculated based on our “Pre-Incentive Fee Net Investment Income” for the immediately preceding calendar quarter.

a. For this purpose, “Pre-Incentive Fee Net Investment Income” means interest income, dividend income and any other income (including any other fees, such as commitment, origination, structuring, diligence and consulting fees or other fees that we receive from portfolio companies) accrued during the calendar quarter minus our operating expenses for the quarter (including the Base Fee, expenses payable under our administration agreement, and any interest expense and dividends paid on any issued and outstanding preferred stock, but excluding the incentive fee). Pre-Incentive Fee Net Investment Income includes, in the case of investments with a deferred interest feature (such as original issue discount, debt instruments with payment-in-kind (“PIK”) interest, and zero coupon securities), accrued income that we have not yet received in cash. Pre-Incentive Fee Net Investment Income does not include any realized capital gains, realized capital losses or unrealized capital appreciation or depreciation.

b. Pre-Incentive Fee Net Investment Income, expressed as a rate of return on the value of our net assets at the end of the immediately preceding calendar quarter, is compared to one-fourth of an annual “hurdle rate.” The annual hurdle rate is determined as of the immediately preceding December 31st by adding 5.0% to the interest rate then payable on the most recently issued five-year U.S. Treasury Notes, up to a maximum annual hurdle rate of 10.0%. The annual hurdle rates for the 2020, 2019 and 2018 calendar years, calculated as of December 31, were approximately 6.69%, 7.51%, and 7.20%, respectively, under the terms of the Investment Advisory Agreement. Our net investment income (to the extent not distributed to our shareholders) used to calculate the Net Investment Income Incentive Fee was also included in the amount of our gross assets used to calculate the 2.00% Base Fee.

S-6

c. The operation of the incentive fee with respect to our Pre-Incentive Fee Net Investment Income for each quarter is as follows:

i. no incentive fee was payable to Oxford Square Management in any calendar quarter in which our Pre-Incentive Fee Net Investment Income did not exceed one fourth of the annual hurdle rate (approximately 6.69% for the 2020 calendar year).

ii. 20% of the amount of our Pre-Incentive Fee Net Investment Income, if any, that exceeds one-fourth of the annual hurdle rate (approximately 6.69% for the 2020 calendar year) in any calendar quarter was payable to Oxford Square Management (i.e., once the hurdle rate is reached, 20% of all Pre-Incentive Fee Net Investment Income thereafter was allocated to Oxford Square Management).

3) Capital Gains Incentive Fee. The “Capital Gains Incentive Fee,” is determined as described above.

For more information about the calculation of the advisory fee under the Investment Advisory Agreement prior to effectiveness of the 2016 Fee Waiver, refer to our Annual Report on Form 10-K for the fiscal year ended December 31, 2016.

Calculation of Fees under the 2016 Fee Waiver. Following the effectiveness of the 2016 Fee Waiver, a second set of calculations is applied each quarter, and, if (and only if) those calculations result in a lower total advisory fee (i.e., the combination of the Base Fee and any incentive fees), they are used to calculate the total advisory fee payable to Oxford Square Management for a particular quarter. No individual element of those calculations is applicable by itself — only the totality of those calculations is considered. Generally, and as described in greater detail below, under the second set of calculations provided for by the 2016 Fee Waiver:

1) Base Fee:

a. The calculation of the Base Fee component is reduced from 2.00% to 1.50%; and

b. No Base Fee is calculated on funds received in connection with any capital raises until the funds are invested.

2) Net Investment Income Incentive Fee:

a. The calculation of our Net Investment Income Incentive Fee is revised to include a Total Return Requirement (as defined below). Under the Total Return Requirement, we are only required to pay Oxford Square Management a Net Investment Income Incentive Fee if 20% of the “cumulative net increase in net assets resulting from operations” (as defined below) — during the calendar quarter for which such fees are being calculated and the eleven (11) preceding quarters — is greater than the cumulative Net Investment Income Incentive Fees accrued and/or paid over for the same period, even when our net investment income exceeds the minimum return to our stockholders required to be achieved before Oxford Square Management is entitled to receive a Net Investment Income Incentive Fee (which minimum return is commonly referred to as the “preferred return” or “hurdle rate”);

b. The calculation of our Net Investment Income Incentive Fee incorporates a “catch-up” provision that provides that Oxford Square Management will receive 100% of our net investment income with respect to that portion of such net investment income, if any, that exceeds the preferred return but is less than 2.1875% quarterly (8.75% annualized) and 20% of any net investment income thereafter; and

c. The hurdle rate used to calculate the Net Investment Income Incentive Fee is changed from a variable rate, based on the five-year U.S. Treasury note plus 5.00% (with a maximum of 10%), to a fixed rate of 7.00%.

S-7

More specifically, for the purpose of calculating the amount of total advisory fees (if any) to be waived during a particular calendar quarter, the Base Fee and Net Investment Income Incentive Fee are calculated as follows under the 2016 Fee Waiver:

1) Base Fee: The Base Fee is calculated at an annual rate of 1.50%, adjusted pro rata for any share issuances, debt issuances, repurchases or redemptions during the current calendar quarter; provided, however, that no Base Fee is payable on the cash proceeds received by us in connection with any share or debt issuances until such proceeds have been invested in accordance with our investment objectives. The Base Fee for any partial month or quarter is pro-rated.

2) Net Investment Income Incentive Fee: The Income Incentive Fee is calculated based on the amount by which (x) the “Pre-Incentive Fee Net Investment Income” (as defined below) for the calendar quarter exceeds (y) the “Preferred Return Amount” (as defined below) for the calendar quarter.

a. A “Preferred Return Amount” is calculated on a quarterly basis by multiplying 1.75% by the Company’s net asset value at the end of the immediately preceding calendar quarter.

b. The Net Investment Income Incentive Fee is then calculated as follows:

(i) no Net Investment Income Incentive Fee is payable to Oxford Square Management in any calendar quarter in which the “Pre-Incentive Fee Net Investment Income” does not exceed the “Preferred Return Amount”;

(ii) 100% of the “Pre-Incentive Fee Net Investment Income” for such quarter, if any, that exceeds the “Preferred Return Amount” but is less than or equal to a “Catch-Up Amount” determined on a quarterly basis by multiplying 2.1875% by OXSQ’s net asset value at the end of such calendar quarter; and

(iii) for any quarter in which the “Pre-Incentive Fee Net Investment Income” exceeds the “Catch-Up Amount,” the Net Investment Income Incentive Fee will be calculated at the rate of 20% of the amount of the “Pre-Incentive Fee Net Investment Income” for such quarter.

c. There is no accumulation of amounts from quarter to quarter for the “Preferred Return Amount,” and accordingly there is no claw back of amounts previously paid to Oxford Square Management if the “Pre-Incentive Fee Net Investment Income” for subsequent quarters is below the quarterly “Preferred Return Amount”.

d. The calculation of the Company’s Net Investment Income Incentive Fee is subject to a total return requirement (the “Total Return Requirement”) that provides that a Net Investment Income Incentive Fee will not be payable to Oxford Square Management except to the extent 20% of the “cumulative net increase in net assets resulting from operations” (which is the amount, if positive, of the sum of the “Pre-Incentive Fee Net Investment Income,” realized gains and losses and unrealized appreciation and depreciation) during the calendar quarter for which such fees are being calculated and the eleven (11) preceding quarters exceeds the cumulative Net Investment Income Incentive Fees accrued and/or paid for such eleven (11) preceding quarters.

3) Capital Gains Incentive Fee. The second part of the incentive fee, the “Capital Gains Incentive Fee,” is determined as described above.

Summary Risk Factors

The value of our assets, as well as the market price of our securities, will fluctuate. Our investments may be risky, and you may lose all or part of your investment in us. Investing in our securities, including the Notes, involves significant risks. For a further discussion of these risk factors, please see “Supplementary Risk Factors” beginning on page S-18 of this prospectus supplement and “Risk Factors” beginning on page 14 of the accompanying prospectus.

S-8

Risks Relating to the Notes

• The Notes will be unsecured and therefore will be effectively subordinated to any secured indebtedness we have incurred or may incur in the future and rank pari passu with, which means equal to, all outstanding and future unsecured unsubordinated indebtedness issued by us and our general liabilities.

• The Notes will be structurally subordinated to the indebtedness and other liabilities of our subsidiaries, if any.

• The indenture under which the Notes will be issued contains limited protection for holders of the Notes.

• The price you pay for the Notes may be higher than the prices paid by other investors.

• There is no existing trading market for the Notes, and, even if NASDAQ approves the listing of the Notes, an active trading market for the Notes may not develop, which could limit your ability to sell the Notes or the market price of the Notes.

• We may choose to redeem the Notes when prevailing interest rates are relatively low.

• If we default on our obligations to pay our other indebtedness, we may not be able to make payments on the Notes.

• A downgrade, suspension or withdrawal of the credit rating assigned by a rating agency to us or our securities, if any, could cause the liquidity or market value of the Notes to decline significantly.

Risks Relating to Our Investments

• Our investment portfolio may be concentrated in a limited number of portfolio companies, which will subject us to a risk of significant loss if any of these companies defaults on its obligations under any of its debt securities that we hold or if the sectors in which we invest experience a market downturn.

• The lack of liquidity in our investments may adversely affect our business.

• Because we generally do not hold controlling equity interests in our portfolio companies, we may not be in a position to exercise control over our portfolio companies or to prevent decisions by the managements of our portfolio companies that could decrease the value of our investments.

• Our financial results may be affected adversely if one or more of our significant equity or junior debt investments in a CLO vehicle defaults on its payment obligations or fails to perform as we expect or if the market price fluctuates significantly in such illiquid investments.

Risks Relating to Our Business and Structure

Our business is subject to numerous risks, as described in the section titled “Supplementary Risk Factors” in this prospectus supplement, the section titled “Risk Factors” in the accompanying prospectus (beginning on page 14 thereof) and under similar headings in the documents that are incorporated by reference into this prospectus supplement and the accompanying prospectus, including the section titled “Risk Factors” included in our most recent Annual Report on Form 10-K. Please refer to these filings and documents for additional discussion of factors you should carefully consider before investing in our Notes.

Recent Developments

On May 3, 2021 we were notified that one of our portfolio companies failed to make a required first lien interest payment to holders of its first lien debt. We estimate the amount of that payment to us would have been approximately $250,000. We note that in the first quarter of 2021 we recognized approximately $311,000 of revenue associated with our investment in this portfolio company (which represented approximately 6.5% of our net investment income for that period). We can offer no assurance as to the prospect for the receipt or recognition of revenue associated with our investment or repayment of the investment upon maturity, default or otherwise in this portfolio company in the future. We have been informed that the first lien lenders are currently negotiating a forbearance agreement with this portfolio company, which could prohibit payments to us for a specified period of time.

S-9

SPECIFIC TERMS OF THE NOTES AND THE OFFERING

|

Issuer |

Oxford Square Capital Corp. |

|

|

Title of the Securities |

5.50% Notes due 2028 |

|

|

Initial aggregate principal amount being offered |

|

|

|

Option to purchase additional shares |

The underwriters may also purchase from us from time to time up to an additional $10.5 million aggregate principal amount of Notes within 30 days of the date of this prospectus supplement. |

|

|

Issue price |

$25.00, subject to variable price reoffer. The underwriters propose to offer the Notes for sale, from time to time, in one or more negotiated transactions, at prices that may be different than par. These sales may occur at market prices prevailing at the time of sale, at prices related to such prevailing market prices or at prices negotiated by the joint book-running managers or with approval from the joint book-running managers. |

|

|

Principal payable at maturity |

100% of the aggregate principal amount; the principal amount of each Note will be payable on its stated maturity date at the office of the Trustee, Paying Agent, and Registrar for the Notes or at such other office in New York, New York as we may designate. |

|

|

Type of note |

Fixed rate note |

|

|

Private Rating of the Notes |

BBB from Egan-Jones Ratings Company. An explanation of the significance of ratings may be obtained from the rating agency. Generally, rating agencies base their ratings on such material and information, and such of their own investigations, studies and assumptions, as they deem appropriate. The rating of the Notes should be evaluated independently from similar ratings of other securities. A credit rating of a security is paid for by the issuer and is not a recommendation to buy, sell or hold securities and may be subject to review, revision, suspension, reduction or withdrawal at any time by the assigning rating agency. See “Risk Factors — A downgrade, suspension or withdrawal of the credit rating assigned by a rating agency to us or our securities, if any, could cause the liquidity or market value of the Notes to decline significantly”. |

|

|

Listing |

We intend to list the Notes on the Nasdaq Global Select Market, within 30 days of the original issue date under the trading symbol “OXSQG.” |

|

|

Interest Rate |

5.50% per year |

|

|

Day count basis |

360-day year of twelve 30-day months |

|

|

Original issue date |

May 20, 2021 |

|

|

Stated maturity date |

July 31, 2028 |

|

|

Date interest starts accruing |

May 20, 2021 |

|

|

Interest payment dates |

Every January 31, April 30, July 31, and October 31, beginning July 31, 2021. If an interest payment date falls on a non-business day, the applicable interest payment will be made on the next business day and no additional interest will accrue as a result of such delayed payment. |

|

|

Interest periods |

The initial interest period will be the period from and including May 20, 2021, to, but excluding, the initial interest payment date, and the subsequent interest periods will be the periods from and including an interest payment date to, but excluding, the next interest payment date or the stated maturity date, as the case may be. |

S-10

|

Regular record dates for interest |

January 15, April 15, July 15 and October 15, beginning July 15, 2021. |

|

|

Specified Currency |

U.S. dollars |

|

|

Place of Payment |

New York City and/or such other places that may be specified in the indenture or a notice to holders |

|

|

Ranking of Notes |

The Notes will be our direct unsecured obligations and will rank: |

|

|

• pari passu with, which means equal to, all outstanding and future unsecured unsubordinated indebtedness issued by us, including our 6.50% Unsecured Notes and our 6.25% Unsecured Notes, of which we had $64.4 million and $44.8 million outstanding, respectively, as of March 31, 2021. The Notes will also rank pari passu with, which means equal to, our general liabilities, which consist of trade and other payables, including any outstanding dividend payable, base and incentive management fees payable, interest and debt fees payable, vendor payables and accrued expenses such as auditor fees, legal fees, director fees, etc. In total, these general liabilities were approximately $13.6 million as of March 31, 2021. |

||

|

• senior to any of our future indebtedness that expressly provides it is subordinated to the Notes. We currently do not have outstanding debt that is subordinated to the Notes and do not currently intend to issue indebtedness that expressly provides that it is subordinated to the Notes. Therefore, the Notes will not be senior to any indebtedness or obligations. |

||

|

• effectively subordinated to all of our existing and future secured indebtedness (including indebtedness that is initially unsecured to which we subsequently grant security), to the extent of the value of the assets securing such indebtedness. In any liquidation, dissolution, bankruptcy or other similar proceeding, the holders of any of our existing or future secured indebtedness may assert rights against the assets pledged to secure that indebtedness in order to receive full payment of their indebtedness before the assets may be used to pay other creditors, including the holders of the Notes, and any assets of our subsidiaries will not be directly available to satisfy the claims of our creditors, including holders of the Notes. Currently, we do not have any secured indebtedness at the Oxford Square Capital Corp. level. |

||

|

• structurally subordinated to all existing and future indebtedness and other obligations of any of the Company’s subsidiaries, CLO vehicles in which we hold an equity interest and financing vehicles since the Notes are obligations exclusively of Oxford Square Capital Corp. and not of any of our subsidiaries. Structural subordination means that creditors of a parent entity are subordinate to creditors of a subsidiary entity with respect to the subsidiary’s assets. |

S-11

|

Except as described under the captions “Description of the Notes — Events of Default,” “— Other Covenants,” and “— Merger or Consolidation” in this prospectus supplement, the indenture does not contain any provisions that give you protection in the event we issue a large amount of debt or we are acquired by another entity. |

||

|

Denominations |

We will issue the Notes in denominations of $25 and integral multiples of $25 in excess thereof. |

|

|

Business Day |

Each Monday, Tuesday, Wednesday, Thursday and Friday that is not a day on which banking institutions in New York City are authorized or required by law or executive order to close. |

|

|

Optional redemptions |

The Notes may be redeemed in whole or in part at any time or from time to time at our option on or after May 31, 2024 upon not less than 30 days nor more than 60 days written notice by mail prior to the date fixed for redemption thereof, at a redemption price of 100% of the outstanding principal amount of the Notes to be redeemed plus accrued and unpaid interest payments otherwise payable thereon for the then-current quarterly interest period accrued to the date fixed for redemption. |

|

|

You may be prevented from exchanging or transferring the Notes when they are subject to redemption. In case any Notes are to be redeemed in part only, the redemption notice will provide that, upon surrender of such Note, you will receive, without a charge, a new Note or Notes of authorized denominations representing the principal amount of your remaining unredeemed Notes. |

||

|

Any exercise of our option to redeem the Notes will be done in compliance with the 1940 Act. |

||

|

If we redeem only some of the Notes, the Trustee or, with respect to global securities, The Depository Trust Company (“DTC”) will determine the method for selection of the particular Notes to be redeemed, in accordance with the indenture and the 1940 Act, and in accordance with the rules of any national securities exchange or quotation system on which the Notes are listed. Unless we default in payment of the redemption price, on and after the date of redemption, interest will cease to accrue on the Notes called for redemption. |

||

|

Sinking Fund |

The Notes will not be subject to any sinking fund (i.e., no amounts will be set aside by us to ensure repayment of the Notes at maturity). As a result, our ability to repay the Notes at maturity will depend on our financial condition on the date that we are required to repay the Notes. |

|

|

Repayment at option of Holders |

Holders will not have the option to have the Notes repaid prior to the stated maturity date. |

S-12

|

Defeasance |

The Notes are subject to defeasance by us. “Defeasance” means that, by depositing with a trustee an amount of cash and/or government securities sufficient to pay all principal and interest, if any, on the Notes when due and satisfying any additional conditions required under the indenture relating to the Notes, we will be deemed to have been discharged from our obligations under the Notes. |

|

|

Covenant defeasance |

The Notes are subject to covenant defeasance by us. In the event of a “covenant defeasance,” upon depositing such funds and satisfying similar conditions discussed below we would be released from the restrictive covenants under the indenture relating to the Notes. The consequences to the holders of the Notes is that, while they no longer benefit from the restrictive covenants under the indenture, and while the Notes may not be accelerated for any reason, the holders of Notes nonetheless are guaranteed to receive the principal and interest owed to them. |

|

|

Form of Notes |

The Notes will be represented by global securities that will be deposited and registered in the name of DTC or its nominee. This means that, except in limited circumstances, you will not receive certificates for the Notes. Beneficial interests in the Notes will be represented through book-entry accounts of financial institutions acting on behalf of beneficial owners as direct and indirect participants in DTC. Investors may elect to hold interests in the Notes through either DTC, if they are a participant, or indirectly through organizations that are participants in DTC. |

|

|

Trustee, Paying Agent, and Registrar |

U.S. Bank National Association |

|

|

Other covenants |

In addition to any covenants described elsewhere in this prospectus, the following covenants shall apply to the Notes: |

|

|

• We agree that for the period of time during which the Notes are outstanding, we will not violate (whether or not we are subject to) Section 18(a)(1)(A) as modified by such provisions of Section 61(a) of the 1940 Act as may be applicable to us from time to time or any successor provisions, but giving effect to any exemptive relief granted to us by the SEC. Currently, these provisions generally prohibit us from making additional borrowings, including through the issuance of additional debt or the sale of additional debt securities, unless our asset coverage, as defined in the 1940 Act, equals at least 150% immediately after such borrowings. See “Risk Factors — Regulations governing our operation as a BDC affect our ability to, and the way in which we raise additional capital, which may expose us to risks, including the typical risks associated with leverage” in the accompanying prospectus. |

S-13

|

• We agree that for the period of time during which the Notes are outstanding, we will not declare any dividend (except a dividend payable in our stock), or declare any other distribution, upon a class of our capital stock, or purchase any such capital stock, unless, in every such case, at the time of the declaration of any such dividend or distribution, or at the time of any such purchase, we have an asset coverage (as defined in the 1940 Act) of at least the threshold specified in Section 18(a)(1)(B) as modified by such provisions of Section 61(a) of the 1940 Act as may be applicable to us from time to time or any successor provisions thereto of the 1940 Act, as such obligation may be amended or superseded, after deducting the amount of such dividend, distribution or purchase price, as the case may be, and in each case giving effect to (i) any exemptive relief granted to us by the SEC, and (ii) any SEC no-action relief granted by the SEC to another BDC (or to us if we determine to seek such similar no-action or other relief) permitting the BDC to declare any cash dividend or distribution notwithstanding the prohibition contained in Section 18(a)(1)(B) as modified by such provisions of Section 61(a) of the 1940 Act as may be applicable to us from time to time, as such obligation may be amended or superseded, in order to maintain such BDC’s status as a regulated investment company under Subchapter M of the Code. |

||

|

• We agree that, if, at any time, we are not subject to the reporting requirements of Sections 13 or 15(d) of the Securities Exchange Act of 1934, or the Exchange Act, to file any periodic reports with the SEC, we agree to furnish to holders of the Notes and the Trustee, for the period of time during which the Notes are outstanding, our audited annual consolidated financial statements, within 90 days of our fiscal year end, and unaudited interim consolidated financial statements, within 45 days of our fiscal quarter end (other than our fourth fiscal quarter). All such financial statements will be prepared, in all material respects, in accordance with applicable United States generally accepted accounting principles. |

||

|

Events of Default |

You will have rights if an Event of Default occurs with respect to the Notes. |

|

|

The term “Event of Default” in respect of the Notes means any of the following: |

||

|

• We do not pay the principal (or premium, if any) of any Note when due. |

||

|

• We do not pay interest on any Note when due, and such default is not cured within 30 days. |

||

|

• We remain in breach of any other covenant with respect to the Notes for 60 days after we receive a written notice of default stating we are in breach. The notice must be sent by either the Trustee or holders of at least 25.0% of the principal amount of the Notes. |

S-14

|

• We file for bankruptcy or certain other events of bankruptcy, insolvency or reorganization occur and in the case of certain orders or decrees entered against us under any bankruptcy law, such order or decree remains undischarged or unstayed for a period of 60 days. |

||

|

• On the last business day of each of twenty-four consecutive calendar months, the Notes have an asset coverage, as defined in the 1940 Act, of less than 100% after giving effect to any exemptive relief granted to us by the SEC. |

||

|

Further Issuances |

We have the ability to issue additional debt securities under the indenture with terms different from the Notes and, without consent of the holders thereof, to reopen the Notes and issue additional Notes. If we issue additional debt securities, these additional debt securities could rank higher in priority of payment or have a lien or other security interest greater than that accorded to the holders of the Notes. |

|

|

Global Clearance and Settlement Procedures |

|

|

|

Use of Proceeds |

We estimate that the net proceeds we will receive from the sale of the Notes will be approximately $67,562,500 (or $77,734,375 if the underwriters exercise their option to purchase additional Notes in full), in each case based on the underwriters purchasing the Notes from us at 96.875% of the aggregate principal amount, after deducting underwriting discounts and commissions and estimated offering expenses payable by us. We intend to use the net proceeds from this offering to primarily fund investments in debt securities and CLO investments in accordance with our investment objective and for other general corporate purposes. |

S-15

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus supplement and the accompanying prospectus, including the documents incorporated by reference herein and therein, contain forward-looking statements that involve substantial risks and uncertainties. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about our company, our current and prospective portfolio investments, our industry, our beliefs, and our assumptions. Words such as “anticipates,” “expects,” “intends,” “plans,” “will,” “may,” “continue,” “believes,” “seeks,” “estimates,” “would,” “could,” “should,” “targets,” “projects,” and variations of these words and similar expressions are intended to identify forward-looking statements.

The forward-looking statements contained in this prospectus supplement and the accompanying prospectus, including the documents incorporated by reference herein and therein, involve risks and uncertainties, including statements as to:

• our future operating results, including our ability to achieve objectives as a result of the current COVID-19 pandemic;

• our business prospects and the prospects of our portfolio companies;

• the impact of investments that we expect to make;

• our contractual arrangements and relationships with third parties;

• the dependence of our future success on the general economy and its impact on the industries in which we invest and the impact of the COVID-19 pandemic thereon;

• the ability of our portfolio companies and CLO investments to achieve their objectives, including as a result of the COVID-19 pandemic;

• the valuation of our investments in portfolio companies and CLOs, particularly those having no liquid trading market, and the impact of the COVID-19 pandemic thereon;

• market conditions and our ability to access alternative debt markets and additional debt and equity capital, and the impact of the COVID-19 pandemic thereon;

• our expected financings and investments;

• the adequacy of our cash resources and working capital;

• the timing of cash flows, if any, from the operations of our portfolio companies and CLO investments and the impact of the COVID-19 pandemic thereon; and

• the ability of our investment adviser to locate suitable investments for us and monitor and administer our investments and the impact of the COVID-19 pandemic thereon.

These statements are not guarantees of future performance and are subject to risks, uncertainties, and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements, including without limitation:

• an economic downturn, including as a result of the COVID-19 pandemic, could impair our portfolio companies’ and CLO investments’ ability to continue to operate, which could lead to the loss of some or all of our investments in such portfolio companies and CLO investments;

• a contraction of available credit and/or an inability to access the equity markets, including as a result of the COVID-19 pandemic, could impair our lending and investment activities;

• interest rate volatility could adversely affect our results, particularly because we use leverage as part of our investment strategy;

S-16

• currency fluctuations could adversely affect the results of our investments in foreign companies, particularly to the extent that we receive payments denominated in foreign currency rather than U.S. dollars; and

• the risks, uncertainties and other factors we identify in Item 1A. — Risk Factors and elsewhere in our Annual Report on Form 10-K and in our filings with the SEC.

Although we believe that the assumptions on which these forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward-looking statements based on those assumptions also could be inaccurate. Important assumptions include our ability to originate new investments, certain margins and levels of profitability and the availability of additional capital. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this prospectus supplement or the accompanying prospectus should not be regarded as a representation by us that our plans and objectives will be achieved. These risks and uncertainties include those described or identified in “Supplementary Risk Factors” in this prospectus supplement and “Risk Factors” in the accompanying prospectus, and in our most recent Annual Report on Form 10-K, and in our most recent Quarterly Report on Form 10-Q. You should not place undue reliance on these forward-looking statements, which are based on information available to us as of the applicable dates of this prospectus supplement and the accompanying prospectus, including any documents incorporated by reference to this prospectus supplement or the accompanying prospectus, and while we believe such information forms, or will form, a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely on these statements.

However, we will update this prospectus supplement and the accompanying prospectus to reflect any material changes to the information contained herein.

S-17

Investing in our Notes involves a number of significant risks. You should carefully consider the risks described below, together with all of the risks and uncertainties described in the section titled “Risk Factors” in the accompanying prospectus, our most recent Annual Report on Form 10-K, our most recent Quarterly Report on Form 10-Q, which are or will be incorporated by reference into this prospectus supplement and the accompanying prospectus in their entirety, and other information in this prospectus supplement, the accompanying prospectus, the documents incorporated by reference in this prospectus supplement and the accompanying prospectus, and any free writing prospectus that we may authorize for use in connection with this offering. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties not presently known to us, or not presently deemed material by us, may also impair our operations and performance. If any of the following risks actually occur, our business, financial condition, results of operations and cash flows could be materially and adversely affected, and consequently, our ability to repay principal and pay interest on the Notes could be material affected. If that happens, our net asset value and the trading price of our securities could decline and you may lose all or part of your investment. Please also read carefully the section titled “Cautionary Statement Regarding Forward-Looking Statements” in this prospectus supplement.

RISKS RELATING TO THE NOTES

The Notes will be unsecured and therefore are effectively subordinated to any secured indebtedness we have incurred or may incur in the future and rank pari passu with, which means equal to, all outstanding and future unsecured unsubordinated indebtedness issued by us and our general liabilities.

The Notes will not be secured by any of our assets or any of the assets of our subsidiaries. As a result, the Notes will be effectively subordinated to all of our existing and future secured indebtedness (including indebtedness that is initially unsecured to which we subsequently grant security), to the extent of the value of the assets securing such indebtedness. In any liquidation, dissolution, bankruptcy or other similar proceeding, the holders of any of our existing or future secured indebtedness may assert rights against the assets pledged to secure that indebtedness in order to receive full payment of their indebtedness before the assets may be used to pay other creditors, including the holders of the Notes.

The Notes will rank pari passu with, which means equal to, all outstanding and future unsecured unsubordinated indebtedness issued by us, including our 6.50% Unsecured Notes and our 6.25% Unsecured Notes, of which we had $64.4 million and $44.8 million outstanding, respectively, as of March 31, 2021. The Notes will also rank pari passu with our general liabilities, which consist of trade and other payables, including any outstanding dividend payable, base and incentive management fees payable, interest and debt fees payable, vendor payables and accrued expenses such as auditor fees, legal fees, director fees, etc. In total, these general liabilities were approximately $13.6 million as of March 31, 2021.

The Notes will be structurally subordinated to the indebtedness and other liabilities of our subsidiaries, if any.

The Notes will be obligations exclusively of Oxford Square Capital Corp., will not be of any of our subsidiaries. The Notes are not required to be guaranteed by any subsidiary we may acquire or create in the future. Any assets of our subsidiaries will not be directly available to satisfy the claims of our creditors, including holders of the Notes. Except to the extent we are a creditor with recognized claims against any of our subsidiaries, all claims of creditors of our subsidiaries will have priority over our equity interests in such entities (and therefore the claims of our creditors, including holders of the Notes) with respect to the assets of such entities. Even if we are recognized as a creditor of one or more of these entities, our claims would still be effectively subordinated to any security interests in the assets of any such entity and to any indebtedness or other liabilities of any such entity senior to our claims. Consequently, the Notes will be structurally subordinated to all existing and future indebtedness and other liabilities of any of our subsidiaries, CLO vehicles in which we hold an equity interest and financing vehicles since the Notes are obligations exclusively of Oxford Square Capital Corp. and not of any of our subsidiaries. Structural subordination means that creditors of a parent entity are subordinate to creditors of a subsidiary entity with respect to the subsidiary’s assets.

S-18

The indenture under which the Notes are issued contains limited protection for holders of the Notes.

The indenture under which the Notes are issued offers limited protection to holders of the Notes. The terms of the indenture and the Notes do not restrict our or any of our subsidiaries’ ability to engage in, or otherwise be a party to, a variety of corporate transactions, circumstances or events that could have a material adverse impact on your investment in the Notes. In particular, the terms of the indenture and the Notes will not place any restrictions on our or any of our subsidiaries’ ability to: