UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One) | |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017 | |

or | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to . | |

COMMISSION FILE NUMBER 001-31924

NELNET, INC.

(Exact name of registrant as specified in its charter)

NEBRASKA (State or other jurisdiction of incorporation or organization) | 84-0748903 (I.R.S. Employer Identification No.) |

121 SOUTH 13TH STREET, SUITE 100 LINCOLN, NEBRASKA (Address of principal executive offices) | 68508 (Zip Code) |

Registrant’s telephone number, including area code: (402) 458-2370

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

TITLE OF EACH CLASS: Class A Common Stock, Par Value $0.01 per Share

NAME OF EACH EXCHANGE ON WHICH REGISTERED: New York Stock Exchange

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [X] No [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. Large accelerated filer [X] Accelerated filer [ ]

Non-accelerated filer [ ] (Do not check if a smaller reporting company) Smaller reporting company [ ] Emerging growth company [ ]

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the registrant’s voting common stock held by non-affiliates of the registrant on June 30, 2017 (the last business day of the registrant’s most recently completed second fiscal quarter), based upon the closing sale price of the registrant’s Class A Common Stock on that date of $47.01 per share, was $1,027,524,695. For purposes of this calculation, the registrant’s directors, executive officers, and greater than 10 percent shareholders are deemed to be affiliates.

As of January 31, 2018, there were 29,343,603 and 11,468,587 shares of Class A Common Stock and Class B Common Stock, par value $0.01 per share, outstanding, respectively (excluding 11,317,364 shares of Class A Common Stock held by wholly owned subsidiaries).

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement to be filed for its 2018 Annual Meeting of Shareholders, scheduled to be held May 24, 2018, are incorporated by reference into Part III of this Form 10-K.

NELNET, INC.

FORM 10-K

TABLE OF CONTENTS

December 31, 2017

FORWARD-LOOKING AND CAUTIONARY STATEMENTS

This report contains forward-looking statements and information that are based on management's current expectations as of the date of this document. Statements that are not historical facts, including statements about the Company's plans and expectations for future financial condition, results of operations or economic performance, or that address management's plans and objectives for future operations, and statements that assume or are dependent upon future events, are forward-looking statements. The words “may,” “should,” “could,” “would,” “predict,” “potential,” “continue,” “expect,” “anticipate,” “future,” “intend,” “scheduled,” “plan,” “believe,” “estimate,” “assume,” “forecast,” “will,” and similar expressions, as well as statements in future tense, are intended to identify forward-looking statements.

The forward-looking statements are based on assumptions and analyses made by management in light of management's experience and its perception of historical trends, current conditions, expected future developments, and other factors that management believes are appropriate under the circumstances. These statements are subject to known and unknown risks, uncertainties, assumptions, and other factors that may cause the actual results and performance to be materially different from any future results or performance expressed or implied by such forward-looking statements. These factors include, among others, the risks and uncertainties set forth in “Risk Factors” and elsewhere in this report, and include such risks and uncertainties as:

• | loan portfolio risks such as interest rate basis and repricing risk resulting from the fact that the interest rate characteristics of the student loan assets do not match the interest rate characteristics of the funding for those assets, the risk of loss of floor income on certain student loans originated under the Federal Family Education Loan Program (the "FFEL Program" or "FFELP"), risks related to the use of derivatives to manage exposure to interest rate fluctuations, uncertainties regarding the expected benefits from purchased securitized and unsecuritized FFELP, private education, and consumer loans and initiatives to purchase additional FFELP, private education, and consumer loans, and risks from changes in levels of loan prepayment or default rates; |

• | financing and liquidity risks, including risks of changes in the general interest rate environment and in the securitization and other financing markets for loans, including adverse changes resulting from slower than expected payments on student loans in FFELP securitization trusts, which may increase the costs or limit the availability of financings necessary to purchase, refinance, or continue to hold student loans; |

• | risks from changes in the educational credit and services markets resulting from changes in applicable laws, regulations, and government programs and budgets, such as the expected decline over time in FFELP loan interest income and fee-based revenues due to the discontinuation of new FFELP loan originations in 2010 and potential government initiatives or legislative proposals to consolidate existing FFELP loans to the Federal Direct Loan Program or otherwise allow FFELP loans to be refinanced with Federal Direct Loan Program loans; |

• | the uncertain nature of the expected benefits from the acquisition of Great Lakes Educational Loan Services, Inc. ("Great Lakes") on February 7, 2018 and the ability to successfully integrate technology, shared services, and other activities and successfully maintain and increase allocated volumes of student loans serviced under existing and any future servicing contracts with the U.S. Department of Education (the "Department"), which current contract between the Company and the Department accounted for 21 percent of the Company's revenue in 2017, risks to the Company related to the Department's initiative to procure new contracts for federal student loan servicing, including the risk that the Company on a post-Great Lakes acquisition basis may not be awarded a contract, risks related to the development by the Company and Great Lakes of a new student loan servicing platform, including risks as to whether the expected benefits from the new platform will be realized, and risks related to the Company's ability to comply with agreements with third-party customers for the servicing of FFELP, Federal Direct Loan Program, and private education and consumer loans; |

• | risks related to a breach of or failure in the Company's operational or information systems or infrastructure, or those of third-party vendors, including cybersecurity risks related to the potential disclosure of confidential student loan borrower and other customer information; |

• | uncertainties inherent in forecasting future cash flows from student loan assets and related asset-backed securitizations; |

• | the uncertain nature of the expected benefits from the acquisition of ALLO Communications LLC on December 31, 2015 and the ability to integrate its communications operations and successfully expand its fiber network in existing service areas and additional communities and manage related construction risks; |

• | risks and uncertainties related to initiatives to pursue additional strategic investments and acquisitions, including investments and acquisitions that are intended to diversify the Company both within and outside of its historical core education-related businesses; and |

• | risks and uncertainties associated with litigation matters and with maintaining compliance with the extensive regulatory requirements applicable to the Company's businesses, reputational and other risks, including the risk of increased regulatory costs, resulting from the recent politicization of student loan servicing, and uncertainties inherent in the estimates and assumptions about future events that management is required to make in the preparation of the Company's consolidated financial statements. |

All forward-looking statements contained in this report are qualified by these cautionary statements and are made only as of the date of this document. Although the Company may from time to time voluntarily update or revise its prior forward-looking statements to reflect actual results or changes in the Company's expectations, the Company disclaims any commitment to do so except as required by securities laws.

2

PART I.

ITEM 1. BUSINESS

Overview

Nelnet, Inc. (the “Company”) is a diverse company with a focus on delivering education-related products and services and loan asset management. The largest operating businesses engage in student loan servicing, tuition payment processing and school information systems, and communications. A significant portion of the Company's revenue is net interest income earned on a portfolio of federally insured student loans. The Company also makes investments to further diversify the Company both within and outside of its historical core education-related businesses, including, but not limited to, investments in real estate and start-up ventures. Substantially all revenue from external customers is earned, and all long-lived assets are located, in the United States.

The Company was formed as a Nebraska corporation in 1978 to service federal student loans for two local banks. The Company built on this initial foundation as a servicer to become a leading originator, holder, and servicer of federal student loans, principally consisting of loans originated under the Federal Family Education Loan Program. A detailed description of the FFEL Program is included in Appendix A to this report.

The Health Care and Education Reconciliation Act of 2010 (the “Reconciliation Act of 2010”) discontinued new loan originations under the FFEL Program, effective July 1, 2010, and requires that all new federal student loan originations be made directly by the Department through the Federal Direct Loan Program. This law does not alter or affect the terms and conditions of existing FFELP loans.

As a result of the Reconciliation Act of 2010, the Company no longer originates new FFELP loans. However, a significant portion of the Company's income continues to be derived from its existing FFELP student loan portfolio. As of December 31, 2017, the Company had a $21.8 billion loan portfolio, consisting primarily of FFELP loans, that management anticipates will amortize over the next approximately 20 years and has a weighted average remaining life of 7.5 years. Interest income on the Company's existing FFELP loan portfolio will decline over time as the portfolio is paid down. However, since July 1, 2010, which is the effective date on and after which no new loans can be originated under the FFEL Program, the Company has purchased $21.4 billion of FFELP loans from other FFELP loan holders looking to adjust their FFELP businesses. The Company believes there may be additional opportunities to purchase FFELP portfolios to generate incremental earnings and cash flow. However, since all FFELP loans will eventually run off, a key objective of the Company is to reposition the Company for the post-FFELP environment.

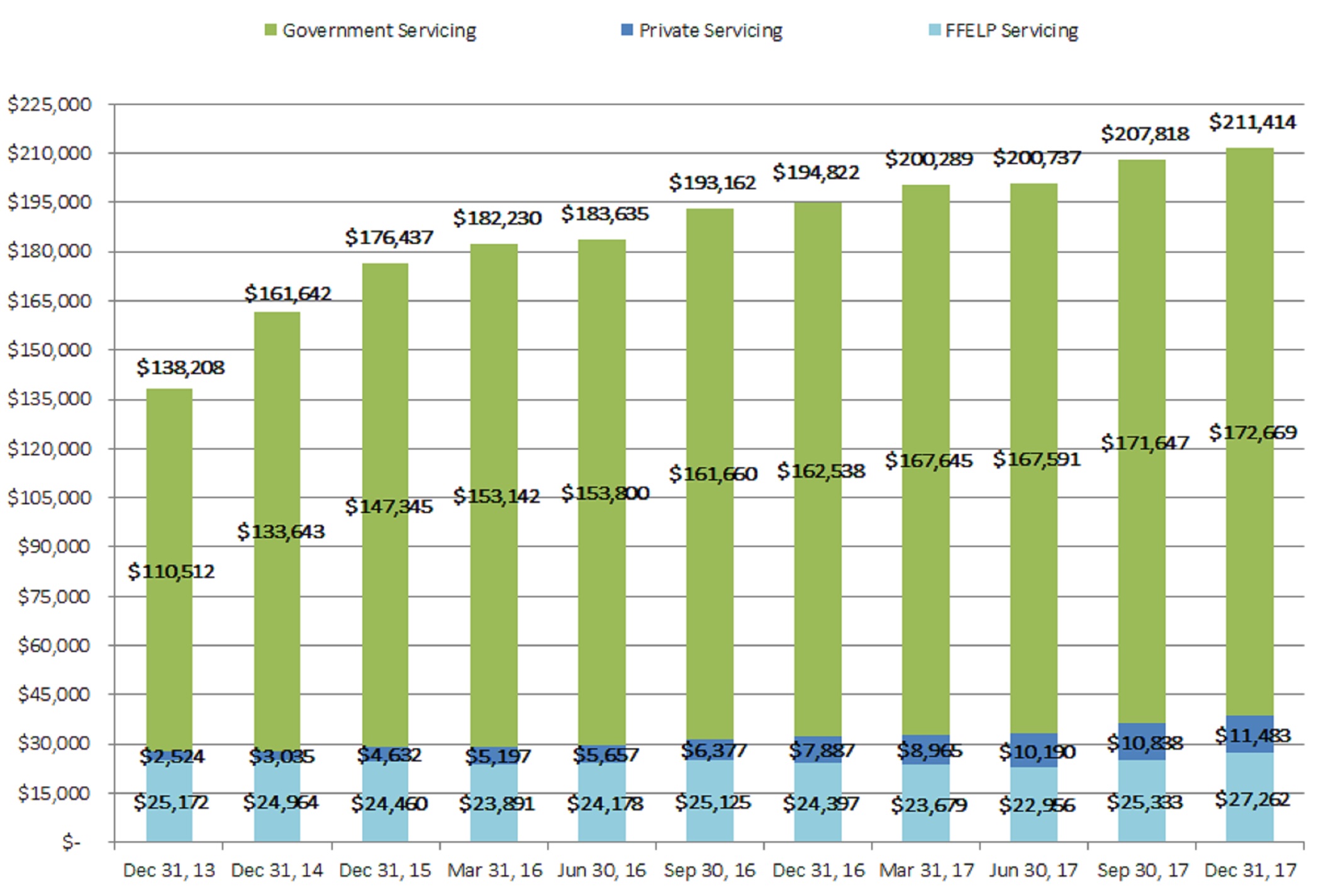

To reduce its reliance on interest income on student loans, the Company has expanded its services and products. This expansion has been accomplished through internal growth and innovation as well as business acquisitions. In addition, in 2009, the Company began servicing federally owned student loans for the Department. As of December 31, 2017, the Company was servicing $172.7 billion of student loans for 5.9 million borrowers on behalf of the Department.

Recent Developments

On February 7, 2018, the Company acquired 100 percent of the outstanding stock of Great Lakes for a purchase price of $150.0 million in cash. Nelnet Servicing, LLC (“Nelnet Servicing”), a subsidiary of the Company, and Great Lakes are two of the four large private sector companies (referred to as Title IV Additional Servicers, or “TIVAS”) that have student loan servicing contracts awarded by the Department in June 2009 to provide servicing for loans owned by the Department.

Going forward, Great Lakes and the Company will continue to service their respective government-owned portfolios on behalf of the Department, while maintaining their distinct brands, independent servicing operations, and teams. Likewise, each entity will continue to compete for new student loan volume under its respective existing contract with the Department. Nelnet will integrate technology, as well as shared services and other activities, to become more efficient and effective in meeting borrower needs.

Headquartered in Madison, Wisconsin, Great Lakes has approximately 1,800 employees and as of December 31, 2017, Great Lakes was servicing $224.4 billion in government-owned student loans for 7.5 million borrowers, $10.7 billion in FFELP loans for almost 479,000 borrowers, and $8.5 billion in private education and consumer loans for over 415,000 borrowers.

The operating results of Great Lakes will be included in the Company's Loan Systems and Servicing operating segment beginning February 7, 2018.

3

Operating Segments

The Company has four reportable operating segments summarized below.

Loan Systems and Servicing

• | Referred to as Nelnet Diversified Solutions (“NDS”) |

• | Focuses on student loan servicing, consumer loan origination and servicing, student loan servicing-related technology solutions, and outsourcing services for lenders and other entities |

• | Includes the brands Nelnet Loan Servicing, Firstmark Services, GreatNet Solutions, and Proxi |

Tuition Payment Processing and Campus Commerce

• | Referred to as Nelnet Business Solutions (“NBS”) |

• | Focuses on tuition payment plans and billings, financial needs assessment services, online payment and refund processing, school information system software, payment technologies, and professional development and educational instruction services |

• | Includes the brands FACTS Management, Nelnet Campus Commerce, RenWeb, PaymentSpring, and FACTS Education Solutions |

Communications

• | Includes the operations of ALLO Communications LLC ("ALLO") |

• | Focuses on providing fiber optic service directly to homes and businesses for internet, broadband, telephone, and television services |

Asset Generation and Management

• | Includes the acquisition and management of the Company's student and other loan assets |

Segment Operating Results

The Company's reportable operating segments are defined by the products and services they offer or the types of customers they serve, and they reflect the manner in which financial information is currently evaluated by management. The Company includes separate financial information about its reportable segments, including revenues, net income or loss, and total assets for each of the Company's reportable segments, for the last three fiscal years in note 15 of the notes to consolidated financial statements included in this report. For segment reporting purposes, business activities and operating segments that are not reportable are combined and included in "Corporate and Other Activities."

Loan Systems and Servicing

The primary service offerings of this operating segment include:

• | Servicing federally-owned student loans for the Department |

• | Servicing FFELP loans |

• | Originating and servicing private education and consumer loans |

• | Providing student loan servicing software and other information technology products and services |

• | Providing outsourced services including call center, processing, and marketing services |

In addition, this segment provided servicing, outsourcing services, and collection services to two FFELP guaranty agencies. The contract with one agency expired on October 31, 2015, and was not renewed. The remaining guaranty agency customer exited the FFELP guaranty business at the end of its contract term on June 30, 2016. After the expiration of this contract, the Company has no remaining guaranty revenue.

As of December 31, 2017, the Company serviced $211.4 billion of student loans for 7.8 million borrowers. See Part II, Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations - Loan Systems and Servicing Operating Segment - Results of Operations - Student Loan Servicing Volumes" for additional information related to the Company's servicing volume.

4

Servicing federally-owned student loans for the Department

As previously discussed, the Company is one of four large private sector companies, or TIVAS, awarded a student loan servicing contract by the Department in June 2009 to provide additional servicing capacity for loans owned by the Department. These loans include Federal Direct Loan Program loans originated directly by the Department and FFEL Program loans purchased by the Department. Under the servicing contract, the Company earns a monthly fee from the Department for each unique borrower who has loans owned by the Department and serviced by the Company. The amount paid per each unique borrower is dependent on the status of the borrower (e.g., in school or in repayment). As of December 31, 2017, the Company was servicing $172.7 billion of student loans for 5.9 million borrowers under its contract with the Department. The Department is the Company's largest customer, representing 21 percent of the Company's revenue in 2017.

The servicing contract with the Department is currently scheduled to expire on June 16, 2019. In April 2016, the Department announced a new contract procurement process to acquire a single servicing platform to manage all student loans owned by the Department. In May 2016, Nelnet Servicing and Great Lakes submitted a joint response to the procurement as part of their GreatNet Solutions, LLC ("GreatNet") joint venture created to respond to the contract solicitation process and to provide services under a new contract in the event that the Department selects it for a contract award.

On August 1, 2017, the Department canceled the prior procurement process. On February 20, 2018, the Department’s Office of Federal Student Aid ("FSA") released information regarding a new contract procurement process. The contract solicitation process is divided into two phases. Responses for Phase One are due on April 6, 2018. The contract solicitation requests responses from interested vendors for nine components, including:

• | Component A: Enterprise-wide digital platform and related middleware |

• | Component B: Enterprise-wide contact center platform, customer relationship management (CRM), and related middleware |

• | Component C: Solution 3.0 (core processing, related middleware, and rules engine) |

• | Component D: Solution 2.0 (core processing, related middleware, and rules engine) |

• | Component E: Solution 3.0 business process operations |

• | Component F: Solution 2.0 business process operations |

• | Component G: Enterprise-wide data management platform |

• | Component H: Enterprise-wide identity and access management (IAM) |

• | Component I: Cybersecurity and data protection |

The solicitation indicates Component C (Solution 3.0) is anticipated to be tailored for new customers and Component D (Solution 2.0) is anticipated to serve as the primary environment for FSA’s existing customers. After Solution 3.0 is deployed, FSA will determine the best distribution of loans between Solution 2.0 and Solution 3.0. In addition, more than one business process solution may be selected for Components E and F.

Vendors may provide a response for an individual, multiple, or all components. The Company intends to respond to Phase One of the solicitation.

The Department also has contracts with 31 not-for-profit ("NFP") entities to service student loans, although five NFP servicers currently service the volume allocated to these 31 entities. One NFP servicer exited the Federal Direct Loan Program servicing business in August 2016. The Company licenses its remote-hosted servicing software to three of the five NFP servicers.

New loan volume was historically allocated by the Department among the four TIVAS based on certain performance metrics established by the Department beginning in 2010. The Department currently allocates new loan volume among the TIVAS and NFP servicers based on the following performance metrics:

• | Two metrics measure the satisfaction among separate customer groups, including borrowers (35 percent) and Federal Student Aid personnel who work with the servicers (5 percent). |

• | Three metrics measure the success of keeping borrowers in an on-time repayment status and helping borrowers avoid default as reflected by the percentage of borrowers in current repayment status (30 percent), percentage of borrowers more than 90 days but fewer than 271 days delinquent (15 percent), and percentage of borrowers over 270 days and fewer than 361 days delinquent (15 percent). The loans are evaluated in 15 different loan portfolio stratifications to account for differences in portfolios. |

5

The allocation of ongoing volume is determined twice each year based on the performance of each servicer in relation to the other servicers. Quarterly results are compiled for each servicer. The average of the September and December quarter-end results are used to allocate volume for the period from March 1 to August 31, and the average of the March and June quarter-end results are used to allocate volume for the period from September 1 to February month end, of each year.

The following table shows the Company's rankings and percent of new volume allocated to the Company since the inception of the Department's allocations of new loan volume based on performance metrics methodologies under this contract:

Initial Metrics (a) | Revised Metrics, NFPs received 25% of volume (b) | Current Metrics (Common Metrics for TIVAS and NFPs) | ||||||||||||||||||||

Performance Evaluation Period | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | |||||||||||

Defaulted borrower # | 4 | 4 | 1 | 1 | 2 | Borrower survey | 2 | 2 | 1 | 4 | 2 | 2 | ||||||||||

Defaulted borrower $ | 4 | 4 | 1 | 1 | 2 | FSA survey | 2 | 2 | 2 | 4 | 4 | 3 | ||||||||||

Borrower survey | 4 | 4 | 3 | 2 | 2 | Current repay % | 4 | 4 | 10 | 3 | 7 | 6 | ||||||||||

School survey | 2 | 2 | 2 | 3 | 2 | 91-270 Repay % | 4 | 4 | 10 | 6 | 7 | 7 | ||||||||||

FSA survey | 3 | 3 | 3 | 3 | 4 | 271-360 Repay % | 4 | 4 | 10 | 9 | 7 | 8 | ||||||||||

Overall ranking | 4 | 4 | 1 | 1 | 2 | 4 | 4 | 8 | 5 | 5 | 4 | |||||||||||

Allocation | 16% | 16% | 30% | 30% | 26% | 14% | 13% | 8% | 12% | 11% | 11% | |||||||||||

Allocation period | August 15, 2010 - August 14, 2011 | August 15, 2011 - August 14, 2012 | August 15, 2012 - August 14, 2013 | August 15, 2013 - August 14, 2014 | August 15, 2014 - February 28, 2015 | March 1, 2015 - August 31, 2015 | September 1, 2015 - February 29, 2016 | March 1, 2016 - June 30, 2016 | July 1, 2016 - February 28, 2017 | March 1, 2017 - August 31, 2017 | September 1, 2017 - February 28, 2018 | |||||||||||

(a) | During the first five years of the servicing contract, the Department allocated 100 percent of new loan volume among the four TIVAS based on the following performance metrics: |

◦ | Two performance metrics measured the success of default prevention efforts as reflected by the percentage of borrowers (20 percent) and percentage of dollars (20 percent) in each servicer's portfolio that went into default. |

◦ | Three metrics measured the satisfaction among separate borrower groups, including borrowers (20 percent), financial aid personnel at postsecondary schools participating in federal student loan programs (20 percent), and Federal Student Aid and other federal agency personnel or contractors who worked with the servicers (20 percent). |

(b) | For these performance evaluation periods (6 and 7 in the above table), the numerical rankings are among the four TIVAS, since the NFPs received a fixed 25 percent of the overall new loan volume. Prior to these evaluation periods, the NFPs serviced loans for up to 100,000 borrower accounts and were not subject to allocations based on performance. |

Incremental revenue components earned by the Company from the Department (in addition to loan servicing revenues) include:

• | Administration of the Total and Permanent Disability (TPD) Discharge program. The Company processes applications for the TPD discharge program and is responsible for discharge, monitoring, and servicing TPD loans. Individuals who are totally and permanently disabled may qualify for a discharge of their federal student loans, and the Company processes applications under the program and receives a fee from the Department on a per application basis, as well as a monthly servicing fee during the monitoring period. The Company is the exclusive provider of this service to the Department. |

• | Origination of consolidation loans. Beginning in 2014, the Department implemented a process to outsource the origination of consolidation loans whereby each of the four TIVAS, and beginning in December 2017, each of the NFP servicers, receives Federal Direct Loan consolidation origination volume based on borrower choice. The Department pays the Company a fee for each completed consolidation loan application it processes. The Company services the consolidation volume it originates. |

Servicing FFELP loans

The Loan Systems and Servicing operating segment provides for the servicing of the Company's student loan portfolio and the portfolios of third parties. The loan servicing activities include loan conversion activities, application processing, borrower updates, customer service, payment processing, due diligence procedures, funds management reconciliations, and claim processing. These activities are performed internally for the Company's portfolio, in addition to generating external fee revenue when performed for third-party clients.

6

The Company's student loan servicing division uses proprietary systems to manage the servicing process. These systems provide for automated compliance with most of the federal student loan regulations adopted under Title IV of the Higher Education Act of 1965, as amended (the “Higher Education Act”).

The Company serviced FFELP loans on behalf of 29 third-party servicing customers as of December 31, 2017. The Company's FFELP servicing customers include national and regional banks, credit unions, and various state and nonprofit secondary markets. The majority of the Company's external FFELP loan servicing activities are performed under “life of loan” contracts. Life of loan contract servicing essentially provides that as long as the loan exists, the Company shall be the sole servicer of that loan; however, the agreement may contain “deconversion” provisions where, for a fee, the lender may move the loan to another servicer.

The discontinuation of new FFELP loan originations in July 2010 has caused and will continue to cause FFELP servicing revenue to decline as these loan portfolios are paid down. However, the Company believes there may be opportunities to service additional FFELP loan portfolios from current FFELP participants as the program winds down.

Originating and servicing private education and consumer loans

The Loan Systems and Servicing operating segment conducts origination and servicing activities for private education and consumer loans.

Private education loans are non-federal loans made to students or their families; as such, the loans are not issued or guaranteed by the federal government. These loans are used primarily to bridge the gap between the cost of higher education and the amount funded through financial aid, federal loans, or the borrowers' personal resources. Although similar in terms of activities and functions as FFELP loan servicing (i.e., application processing, disbursement processing, payment processing, customer service, statement distribution, and reporting), private education loan servicing activities are not required to comply with provisions of the Higher Education Act and may be more customized to individual client requirements.

The Company has invested in modernizing key technologies and services to position its consumer loan servicing business for the long-term, expanding services to include personal loan products and other consumer installment assets. Improvements allow for diversified products to be both originated and serviced with state-of-the-art application and servicing platforms to drive growth for the Company's client partners. Presenting a very wide market opportunity of new entrants and existing players, consumer lending is a key growth area. In both back-up servicing and full servicing partnerships, the Company is a valuable resource for consumer lenders and asset holders as it allows for leveraged economies of scale, high compliance, and secure service to client partners.

The Company serviced private education and consumer loans on behalf of 27 third-party servicing customers as of December 31, 2017. In addition, the Company provides back-up servicing arrangements to assist nine entities for more than 800,000 borrowers. For a monthly fee, these arrangements require a 30 to 90 day notice from a triggering event to transfer the customer's servicing volume to the Company's platform and becoming a full servicing customer.

Providing student loan servicing software and other information technology products and services

The Loan Systems and Servicing operating segment provides data center services and student loan servicing software for servicing private education and federal loans. These proprietary software systems are used internally by the Company and licensed to third-party student loan holders and servicers. These software systems have been adapted so they can be offered as hosted servicing software solutions that can be used by third parties to service various types of student loans, including Federal Direct Loan Program and FFEL Program loans. The Company earns a monthly fee from its remote hosting customers for each unique borrower on the Company's platform, with a minimum monthly charge for most contracts. As of December 31, 2017, 2.8 million borrowers were hosted on the Company's hosted servicing software solution platforms.

Providing outsourced services including call center, processing, and marketing services

The Company provides business process outsourcing specializing in contact center management. The contact center solutions and services include taking inbound calls, helping with outreach campaigns and sales, and interacting with customers through multi-channels.

7

Competition

The Company's scalable servicing platform allows it to provide compliant, efficient, and reliable service at a low cost, giving the Company a competitive advantage over others in the industry. The principal competitor for existing and prospective FFELP and private education loan servicing business is Navient Corporation ("Navient"). Navient is the largest for-profit provider of servicing functions. In contrast to its competitors, the Company has segmented its private education loan servicing on a distinct platform, created specifically to meet the needs of private education student loan borrowers, their families, the schools they attend, and the lenders who serve them. This ensures access to specialized teams with a dedicated focus on servicing these borrowers.

With the elimination of new loan originations under the FFEL Program, four servicers, including the Company, were named by the Department in 2009 as servicers of federally-owned loans. The three other servicers are Great Lakes (now owned by the Company), FedLoan Servicing (Pennsylvania Higher Education Assistance Agency ("PHEAA")), and Navient. In addition, the Department has contracts with 31 NFP entities to service student loans that are serviced by five prime NFP servicers. These NFP entities were authorized in 2012 to begin servicing loans for existing borrower accounts. While previously these entities have only serviced existing loans, beginning in the first quarter of 2015, they began to receive a portion of new borrower loan activity. The Company currently licenses its hosted servicing software to 3 prime NFP servicers that represent 13 NFP organizations. PHEAA is the only other TIVAS servicer offering a hosted Federal Direct Loan Program servicing solution to the NFP servicers.

The Company is one of the leaders in the development of servicing software for guaranty agencies, consumer loan programs, the Federal Direct Loan Program, and FFELP student loans. Many student loan lenders and servicers utilize the Company's software either directly or indirectly. The Company believes the investments it has made to scale its systems and to create a secure infrastructure to support the Department's servicing volume and requirements increase its competitive advantage as a long-term partner in the loan servicing market.

Tuition Payment Processing and Campus Commerce

The Company's Tuition Payment Processing and Campus Commerce operating segment provides products and services to help students and families manage the payment of education costs at all levels (K-12 and higher education). It also provides innovative education-focused technologies, services, and support solutions to help schools automate administrative processes and collect and process commerce data. The Company also provides to K-12 schools professional development and educational instruction services and provides payment technology and services for software platforms, businesses, and nonprofits beyond the K-12 and higher education space.

The majority of this segment's customers are located in the United States; however, the Company has begun providing its products and services in Australia, New Zealand, and Southeast Asia, and currently believes there are opportunities to increase its customer base and revenues internationally.

See Part II, Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations - Tuition Payment Processing and Campus Commerce Operating Segment - Results of Operations" for a discussion of the seasonality of the business in this operating segment.

K-12

In the K-12 market, the Company offers tuition management services, assistance with financial needs assessment and donor management, school information systems, and professional development and education instruction services. The Company provides services for nearly 11,500 K-12 schools and serves 2.2 million families representing 3.2 million students.

The Company is the market leader in actively managed tuition payment plans and financial needs assessment services. Tuition management services include payment plan administration, incidental billing, accounts receivable management, and record keeping. K-12 educational institutions contract with the Company to administer deferred payment plans that allow families to make monthly payments generally over 6 to 12 months. The Company collects a fee from either the institution or the payer as an administration fee.

The Company's financial needs assessment service helps K-12 schools evaluate and determine the amount of financial aid to disburse to the families it serves. The Company's donor services allow schools to assess and deliver strategic fundraising solutions using the latest technology.

RenWeb provides school information systems to help schools automate administrative processes such as admissions, enrollment, scheduling, student billing, attendance, and grade book management. RenWeb's information systems software is sold as a

8

subscription service to schools. RenWeb also offers a streamlined, social, and fully integrated learning management system to enhance classroom instruction for both teachers and students. The combination of RenWeb’s school administration software, learning management system, and the Company’s tuition management and financial needs assessment services has significantly increased the value of the Company’s offerings in this area, allowing the Company to deliver a comprehensive suite of solutions to schools.

Under the brand FACTS Education Solutions, the Company provides customized professional development services for teachers and school leaders as well as instructional services for students experiencing academic challenges. These services provide continuous advance learning and professional development while helping private schools identify and attain equitable participation in federal education programs.

Higher Education

The Company offers two principal products to the higher education market: actively managed tuition payment plans, and campus commerce technologies and payment processing. The Company provides service for 970 colleges and universities worldwide and serves 7 million students and families.

Higher education institutions contract with the Company to administer actively managed payment plans that allow the student and family to make monthly payments on either a semester or annual basis. The Company collects a fee from the student or family as an administration fee.

The Company's suite of campus commerce solutions provides services that allow for families' electronic billing and payment of campus charges. Campus commerce includes cashiering for face-to-face transactions, campus-wide commerce management, and refunds management, among other activities. The Company earns revenue for e-billing, hosting and maintenance, credit card processing fees, and e-payment transaction fees, which are powered by the Company's secure payment processing systems.

The Company's campus commerce products are sold as a subscription service to colleges and universities. The systems process payments through the appropriate channels in the banking or credit card networks to make deposits into the client's bank account. The systems can be further deployed to other departments around campus as requested (e.g., application fees, alumni giving, parking, events, etc.).

Non-education services

Under the brand PaymentSpring, the Company has expanded its customer base to include both education and non-education customers. PaymentSpring offers payment services including electronic transfer and credit card processing, reporting, billing and invoicing, mobile and virtual terminal solutions, and specialized integrations to business software.

Competition

The Company is the largest provider of tuition management and financial needs assessment services to the private and faith-based K-12 market in the United States. Competitors include financial institutions, tuition management providers, financial needs assessment providers, accounting firms, and a myriad of software companies.

In the higher education market, the Company targets business offices at colleges and universities. In this market, the primary competition is limited to only a few campus commerce and tuition payment providers, as well as solutions developed in-house by colleges and universities.

The Company's principal competitive advantages are (i) the customer service it provides to institutions and consumers, (ii) the technology provided with the Company's service, and (iii) the Company's ability to integrate its technology with the institution clients and their third party service providers. The Company believes its clients select products primarily based on technology features, functionality, and the ability to integrate with other systems, but price and service also impact the selection process.

Communications

On December 31, 2015, the Company acquired the majority of the membership interests of ALLO. ALLO derives its revenue primarily from the sale of telecommunication services, including internet, broadband, telephone, and television services, to business and residential customers in Nebraska, and specializes in high-speed internet and broadband services available through its all-fiber network. ALLO currently serves the Scottsbluff, Gering, Bridgeport, North Platte, Ogallala, Alliance, and Lincoln communities in Nebraska. ALLO began providing services in Lincoln, Nebraska in September 2016, as part of a multi-year project

9

to pass substantially all commercial and residential properties in the community. In the fourth quarter of 2017, ALLO announced plans to expand its network to make services available in Hastings, Nebraska and Fort Morgan, Colorado. This will expand total households in ALLO’s current markets from 137,500 to over 152,000. In December 2017, the Fort Morgan city council approved a 40-year agreement with ALLO for ALLO to provide broadband service over a fiber network that the city will build and own, and ALLO will lease and operate to provide services to subscribers. ALLO plans to continue expansion to additional communities in Nebraska and Colorado over the next several years.

Internet, broadband, and television services

Internet, broadband, and television services include data and video products and services to residential and business subscribers. ALLO data services provide high-speed internet access over ALLO's all-fiber network at various symmetrical speeds up to 1 gigabit per second for residential customers, depending on the nature of the network facilities that are available, the level of service selected, and the geographic market availability. ALLO also offers a variety of data connectivity services for businesses, including Ethernet services capable of multiple connections over ALLO's fiber-based networks. ALLO's Internet Protocol Television Video ("IPTV") services range from limited basic service to advanced television, which includes several plans, each with hundreds of local, national, and music channels, including premium and pay-per-view channels, as well as video on demand service. Subscribers may also subscribe to ALLO's advanced video services, which consist of high definition television, digital video recorders (“DVR”), and/or a whole home DVR. ALLO's whole home DVR gives customers the ability to watch recorded shows on any television in the house, record multiple shows at one time, and utilize an intuitive on-screen guide and user interface.

ALLO expects that internet and broadband services will continue to increase as a more significant component of its overall services, and offset the anticipated decline in traditional residential telephone and television services.

Telephone services

Local calling services include a full suite of telephone services, including basic services, primary rate interface ("PRI"), and session initiation protocol ("SIP"). ALLO's service plans include options for voicemail and other enhanced custom calling features including hunting, caller ID, call forwarding, and call waiting, among others. Services are charged at a fixed monthly rate or can be bundled with selected services at a discounted rate. ALLO provides a hosted private branch exchange ("PBX") package, which utilizes a soft switch and allows the customer the flexibility of utilizing new telephone technology and features without investing in a new telephone system. The package bundles local service, calling features, and internet protocol (“IP”) business telephones.

Long-distance services include traditional domestic and international long distance, which enables customers to make calls that terminate outside their local calling area. These services also include toll-free calls and conference calling. ALLO offers a variety of long distance plans, including unlimited flat-rate calling plans, and offers a combination of subscription and usage fees.

Sales and marketing

The key components of ALLO's overall marketing strategy include:

• | Promoting the advantages of an all-fiber network connected directly to homes and businesses capable of delivering synchronous internet speeds of over one gigabit per second |

• | Building complete fiber communities by passing all homes and businesses within its network |

• | Organizing sales and marketing activities around consumer, enterprise, and carrier customers |

• | Positioning ALLO as a single point of contact for customers’ communications needs |

• | Providing customers with a broad array of internet, broadband, television, and telephone services and bundling these services whenever possible |

• | Providing excellent local customer service, including 24/7/365 customer support to coordinate installation of new services, repair, and maintenance functions |

• | Developing and delivering new services to meet evolving customer needs and market demands |

• | Utilizing proven modern technology to deliver services |

ALLO currently offers services through direct marketing, call centers, its website, communication centers, and commissioned sales representatives. ALLO markets its services both individually and as bundled services, including its triple-play offering of internet, television, and telephone services. By bundling service offerings, ALLO is able to offer and sell a more complete and competitive package of services, which simultaneously increases its margin per customer and adds value for the consumer. ALLO also believes that bundling leads to increased customer loyalty and retention.

10

Network architecture and technology

ALLO has made significant investments in its technologically advanced telecommunications networks. As a result, ALLO is able to deliver high-quality, reliable internet, broadband, telephone, and television services through fiber optics. ALLO's wide-ranging network and extensive use of fiber provide an easy reach into existing and new areas. By bringing the fiber network to the customer premises, ALLO can increase its service offerings, quality, and bandwidth services. ALLO's existing fiber network enables it to efficiently respond and adapt to changes in technology and is capable of supporting the rising customer demand for bandwidth in order to support the growing number of internet devices in the home. ALLO's all-fiber network enhances its operating efficiencies by facilitating new network and technology choices that provide for lower costs to operate. ALLO's networks are supported by an advanced digital telephone switch and IPTV service platform. The digital switch provides all local telephone customers with access to a full suite of telecommunication products, custom calling features, and value-added services. ALLO's fiber network utilizes fiber-to-the-premise (“FTTP”) networks to offer bundled residential and commercial services. ALLO leverages its high definition IPTV headend equipment to distribute content across its network, allowing it to provide a sharp video picture and to better manage costs of future channel additions and upgrades. ALLO's network provides substantially all of its marketable homes and businesses with bandwidth of 1 gigabit per second or more.

Growth strategy

As discussed previously, ALLO plans to increase its customer base with its superior all-fiber network by increasing its share in existing markets and entering additional markets currently served by carriers using traditional copper and coaxial cable in their telecommunications networks. Although the initial capital expenditures for most of these expansion efforts are expected to be significant, ALLO believes that its service delivery model will continue to generate customer demand sufficient to provide attractive returns on the capital investment. In addition, ALLO is focused on increasing revenues per customer by capitalizing on increased demand for bandwidth by commercial and residential customers.

Competition

Telecommunications businesses are highly competitive and continue to face increased competition as a result of technology changes and industry legislative and regulatory developments. ALLO faces actual or potential competition from many existing and emerging companies, including incumbent and competitive local telephone companies, long distance carriers and resellers, wireless companies, internet service providers ("ISPs"), satellite companies, cable television companies, and in some cases by new forms of providers who are able to offer competitive services through software applications, requiring a comparatively small initial investment. Due to consolidation and strategic alliances within the industry, ALLO cannot predict the number of competitors it will face at any given time. The wireless business has expanded significantly, causing many residential subscribers of traditional telephone services to discontinue those services and rely exclusively on wireless service. Consumers are finding individual television shows of interest to them through the internet and are watching content that is downloaded to their computers. Some providers, including television and cable television content owners, have initiated what are referred to as “over-the-top” services that deliver video content to televisions and computers over the internet. Over-the-top services can include episodes of highly-rated television series in their current broadcast seasons. They also can include content that is related to broadcast or sports content that ALLO carries, but that is distinct and may be available only through the alternative source. Finally, the transition to digital broadcast television has allowed many consumers to obtain high definition local broadcast television signals (including many network affiliates) over-the-air, using a simple antenna. Consumers can pursue each of these options without foregoing any of the other options. The incumbent telephone carriers in the markets ALLO serves enjoy certain business advantages, including size, financial resources, favorable regulatory position, a more diverse product mix, brand recognition, and connection to virtually all of ALLO's customers and potential customers. The largest cable operators also enjoy certain business advantages, including size, financial resources, ownership of or superior access to desirable programming and other content, a more diverse product mix, brand recognition, and first-in-the-field advantages with a customer base that generates positive cash flow for its operations. ALLO's competitors continue to add features and adopt aggressive pricing and packaging for services comparable to the services ALLO offers. Their success in selling some services competitive with ALLO's can lead to revenue erosion in other related areas. ALLO faces intense competition in its markets for long distance, internet access, and other ancillary services that are important to ALLO's business and to its growth strategy.

11

Asset Generation and Management

The Asset Generation and Management operating segment includes the acquisition, management, and ownership of the Company's loan assets, primarily its federally insured student loan portfolio. As of December 31, 2017, the Company's loan portfolio was $21.8 billion. The Company generates a substantial portion of its earnings from the spread, referred to as the Company's loan spread, between the yield it receives on its loan portfolio and the associated costs to finance such portfolio. See Part II, Item 7, “Management's Discussion and Analysis of Financial Condition and Results of Operations - Asset Generation and Management Operating Segment - Results of Operations - Loan Spread Analysis,” for further details related to the loan spread. The student loan assets are held in a series of education lending subsidiaries and associated securitization trusts designed specifically for this purpose. In addition to the loan spread earned on its portfolio, all costs and activity associated with managing the portfolio, such as servicing of the assets and debt maintenance, are included in this segment.

Loans consist of federally insured student loans, private education loans, and consumer loans. Federally insured student loans were originated under the FFEL Program. The Company's portfolio of federally insured student loans is subject to minimal credit risk, as these loans are guaranteed by the Department at levels ranging from 97 percent to 100 percent. Substantially all of the Company's loan portfolio (98.8 percent as of December 31, 2017) is federally insured. The Company's portfolio of private education loans is subject to credit risk similar to other consumer loan assets. In 2017, the Company began to purchase consumer loans.

The Higher Education Act regulates every aspect of the federally insured student loan program, including certain communications with borrowers, loan originations, and default aversion. Failure to service a student loan properly could jeopardize the guarantee on federal student loans. In the case of death, disability, or bankruptcy of the borrower, the guarantee covers 100 percent of the loan's principal and accrued interest.

FFELP loans are guaranteed by state agencies or nonprofit companies designated as guarantors, with the Department providing reinsurance to the guarantor. Guarantors are responsible for performing certain functions necessary to ensure the program's soundness and accountability. Generally, the guarantor is responsible for ensuring that loans are serviced in compliance with the requirements of the Higher Education Act. When a borrower defaults on a FFELP loan, the Company submits a claim to the guarantor, who provides reimbursements of principal and accrued interest, subject to the applicable risk share percentage.

Origination and acquisition

The Reconciliation Act of 2010 discontinued originations of new FFELP loans, effective July 1, 2010. However, the Company believes there will be ongoing opportunities to continue to purchase FFELP loan portfolios from current FFELP participants looking to adjust their FFELP businesses. For example, from July 1, 2010 through December 31, 2017, the Company purchased a total of $21.4 billion of FFELP student loans from various third parties. However, since all FFELP loans will eventually run off, a key objective of the Company is to reposition the Company for the post-FFELP environment. As such, the Company is actively expanding its private education and consumer loan portfolios. The Company's competition for the purchase of loan portfolios and residuals includes large banks, hedge funds, and other student loan finance companies.

Interest rate risk management

Since the Company generates a significant portion of its earnings from its loan spread, the interest rate sensitivity of the Company's balance sheet is very important to its operations. The current and future interest rate environment can and will affect the Company's interest income and net income. The effects on the Company's results of operations as a result of the changing interest rate environments are further outlined in Part II, Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations - Asset Generation and Management Operating Segment - Results of Operations - Loan Spread Analysis" and Part II, Item 7A, “Quantitative and Qualitative Disclosures About Market Risk - Interest Rate Risk.”

Corporate and Other Activities

Whitetail Rock Capital Management, LLC ("WRCM")

As of December 31, 2017, WRCM, the Company's SEC-registered investment advisor subsidiary, had $874.3 million in asset-backed security assets, consisting primarily of student loan asset-backed securities, under management for third-party customers. WRCM earns annual management fees of 25 basis points for assets under management and up to 50 percent of the gains from the sale of securities or securities being called prior to the full contractual maturity for which it provides advisory services. During 2017, WRCM traded almost $1.3 billion for their customers, generating $10.1 million in performance fees. Assuming assets under

12

management remain at their current levels, management fees should be relatively stable in future years. However, the Company currently anticipates that opportunities for WRCM to earn performance fees could be limited in future years.

Real estate and other investments

The Company makes investments to further diversify itself both within and outside of its historical core education-related businesses, including investments in real estate and start-up ventures. Recent real estate investments have been focused on the development of commercial properties in the Midwest, and particularly in Lincoln, Nebraska, where the Company is headquartered. These investments include projects for the development of properties in Lincoln’s east downtown Telegraph District, where a new facility for the Company’s student loan servicing operations is located, and a building in Lincoln’s Haymarket District that is the new headquarters of Hudl, an online video analysis and coaching tools software company for athletes of all levels. The Company is also a tenant at Hudl's headquarters. As of December 31, 2017, the total amount of real estate investments by the Company was $49.5 million. In addition, the Company has a total equity investment in Hudl of $51.8 million. David S. Graff, a member of the Company’s board of directors, is a co-founder, the chief executive officer, and a director of Hudl.

Regulation and Supervision

The Company's operating segments and industry partners are heavily regulated by federal and state government regulatory agencies. The following provides a summary of the more significant existing and proposed legislation and regulations affecting the Company. A failure to comply with these laws and regulations could subject the Company to substantial fines, penalties, and remedial and other costs, restrictions on business, and the loss of business. Regulations and supervision can change rapidly, and changes could alter the manner in which the Company operates and increase the Company's operating expenses as new or additional regulatory compliance requirements are addressed.

Loan Systems and Servicing

The Company's Loan Systems and Servicing operating segment, which services Federal Direct Loan Program, FFELP, and private education and consumer loans, is subject to federal and state consumer protection, privacy, and related laws and regulations. Some of the more significant federal laws and regulations include:

• | The Higher Education Act, which establishes financial responsibility and administrative capability that govern all third-party servicers of federally insured student loans |

• | The Telephone Consumer Protection Act (“TCPA”), which governs communication methods that may be used to contact customers |

• | The Truth-In-Lending Act and Regulation Z, which governs disclosures of credit terms to consumer borrowers |

• | The Fair Credit Reporting Act and Regulation V, which governs the use and provision of information to consumer reporting agencies |

• | The Equal Credit Opportunity Act and Regulation B, which prohibits discrimination on the basis of race, creed, or other prohibited factors in extending credit |

• | The Servicemembers Civil Relief Act (“SCRA”), which applies to all debts incurred prior to commencement of active military service and limits the amount of interest, including certain fees or charges that are related to the obligation or liability |

• | The Electronic Funds Transfer Act (“EFTA”) and Regulation E, which protects individual consumers engaged in electronic fund transfers (“EFTs”) |

• | The Gramm-Leach-Bliley Act (“GLBA”) and Regulation P, which governs a financial institution’s treatment of nonpublic personal information about consumers and requires that an institution, under certain circumstances, notify consumers about its privacy policies and practices |

• | Laws prohibiting unfair, deceptive, or abusive acts or practices |

• | Various laws, regulations, and standards that govern government contractors |

As a student loan servicer for the federal government and for financial institutions, including the Company’s FFELP student loan portfolio, the Company is subject to the Higher Education Act and related laws, rules, regulations, and policies. The Higher Education Act regulates every aspect of the federally insured student loan program. The Company has designed its servicing operations to comply with the Higher Education Act, and it regularly monitors the Company's operations to maintain compliance.

Under the TCPA, plaintiffs may seek actual monetary loss or damages of $500 per violation, whichever is greater, and courts may treble the damage award for willful or knowing violations. In addition, TCPA lawsuits have asserted putative class action claims.

13

The Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) established the Consumer Financial Protection Bureau (“CFPB”), which has broad authority to regulate a wide range of consumer financial products and services. The Company's student loan servicing business is subject to CFPB oversight authority.

In 2015, the CFPB conducted a public inquiry into student loan servicing practices throughout the industry and issued a report discussing public comments submitted in response to the inquiry, and suggesting a framework to improve borrower outcomes and reduce defaults, including the creation of consistent, industry-wide standards for the entire servicing market.

The CFPB has authority to draft new regulations implementing federal consumer financial protection laws, to enforce those laws and regulations, and to conduct examinations of the Company's operations to determine compliance. The CFPB’s authority includes the ability to assess financial penalties and fines and provide for restitution to consumers if it determines there have been violations of consumer financial protection laws. The CFPB also provides consumer financial education, tracks consumer complaints, requests data from industry participants, and promotes the availability of financial services to underserved consumers and communities. The CFPB has authority to prevent unfair, deceptive, or abusive acts or practices and to ensure that all consumers have access to fair, transparent, and competitive markets for consumer financial products and services. The CFPB’s scrutiny of financial services has impacted participants’ approach to their services, including how the Company interacts with consumers.

In addition, where a company has violated Title X of the Dodd-Frank Act or CFPB regulations implemented under Title X of the Dodd-Frank Act, the Dodd-Frank Act empowers state attorneys general and state regulators to bring civil actions to remedy violations of state law. Most states also have statutes that prohibit unfair and deceptive practices. To the extent states enact requirements that differ from federal standards or state officials and courts adopt interpretations of federal consumer laws that differ from those adopted by the CFPB under the Dodd-Frank Act, the Company's ability to offer the same products and services to consumers nationwide may be limited.

As a third-party service provider to financial institutions, the Company is subject to periodic examination by the Federal Financial Institutions Examination Council (“FFIEC”). FFIEC is a formal interagency body of the U.S. government empowered to prescribe uniform principles, standards, and report forms for the federal examination of financial institutions by the Federal Reserve Banks, the Federal Deposit Insurance Corporation ("FDIC"), and the CFPB, and to make recommendations to promote uniformity in the supervision of financial institutions.

Tuition Payment Processing and Campus Commerce

The Tuition Payment Processing and Campus Commerce operating segment provides tuition management services and school information software for K-12 schools and tuition management services and campus commerce solutions for higher education institutions. The Company also provides payments technologies and payment services for software platforms, businesses, and nonprofits beyond the K-12 and higher education space. As a service provider that takes payment instructions from institutions and their constituents and sends them to bank partners, the Company is directly or indirectly subject to a variety of federal and state laws and regulations. The Company's contracts with clients and bank partners require the Company to comply with these laws and regulations.

The Company's payment processing services are subject to the EFTA and Regulation E, which govern automatic deposits to and withdrawals from deposit accounts and customers’ rights and liabilities arising from the use of debit cards and certain other electronic banking services. The Company assists bank partners with fulfilling their compliance obligations pursuant to these requirements.

The Company's payment processing services are also subject to the National Automated Clearing House Association (“NACHA”) requirements, which include operating rules and sound risk management procedures to govern the use of the Automated Clearing House ("ACH") Network. These rules are used to ensure that the ACH Network is efficient, reliable, and secure for its members. Because the ACH Network uses a batch process, the importance of proper submissions by NACHA members is magnified.

The Company is also impacted by laws and regulations that affect the bankcard industry. The Company is registered with Visa, Mastercard, American Express, and the Discover Network as a service provider and is subject to their respective rules.

The Company's higher education institution clients are subject to the Family Educational Rights and Privacy Act (“FERPA”), which protects the privacy of student education records. The Company's higher education institution clients disclose certain non-directory information concerning their students to the Company, including contact information, student identification numbers, and the amount of students’ credit balances pursuant to one or more exceptions under FERPA. Additionally, as the Company is indirectly subject to FERPA, it may not permit the transfer of any personally identifiable information to another party other than in a manner in which an educational institution may properly disclose it. While the Company believes that it has adequate policies

14

and procedures in place to safeguard the privacy of such information, a breach of this prohibition could result in a five-year suspension of the Company's access to the related client’s records. The Company may also be subject to similar state laws and regulations that restrict higher education institutions from disclosing certain personally identifiable student information.

Some of the Company's K-12 and higher education institution clients choose to charge convenience fees to students, parents, or other payers who make online payments using a credit or debit card. Laws and regulations related to such fees vary from state to state and certain states have laws that to varying degrees prohibit the imposition of a surcharge on a cardholder who elects to use a credit or debit card in lieu of cash, check, or other means.

The Company's contracts with higher education institution clients also require the Company to comply with regulations promulgated by the Department regarding the handling of student financial aid funds received by institutions on behalf of their students under Title IV of the Higher Education Act. On October 30, 2015, the Department amended cash management and other regulations to ensure students have convenient access to their Title IV funds, do not incur unreasonable fees, and are not led to believe they must open a financial account to receive such funds.

Communications

The telecommunications business is subject to extensive federal, state, and local regulation. Under the Telecommunications Act of 1996 (“Telecommunications Act”), federal and state regulators share responsibility for implementing and enforcing statutes and regulations designed to encourage competition and to preserve and advance widely available, quality telephone service at affordable prices.

At the federal level, the Federal Communications Commission ("FCC") generally exercises jurisdiction over facilities and services of local exchange carriers to the extent they are used to provide, originate, or terminate interstate or international communications. The FCC has the authority to condition, modify, cancel, terminate, or revoke operating authority for failure to comply with applicable federal laws or FCC rules, regulations, and policies.

State regulatory commissions generally exercise jurisdiction over carriers’ facilities and services to the extent they are used to provide, originate, or terminate intrastate communications. In addition, municipalities and other local government agencies regulate the public rights-of-way necessary to install and operate networks.

The Communications Act of 1934 ("Communications Act") requires, among other things, that telecommunications carriers offer services at just and reasonable rates and on non-discriminatory terms and conditions. The 1996 amendments to the Communications Act, contained in the Telecommunications Act, dramatically changed, and likely will continue to change, the landscape of the telecommunications industry. The central aim of the Telecommunications Act is to open local telecommunications markets to competition while enhancing universal service. The Telecommunications Act imposes a number of interconnection and other requirements on all local communications providers. All telecommunications carriers have a duty to interconnect directly or indirectly with the facilities and equipment of other telecommunications carriers.

The State of Nebraska Public Services Commission dictates service requirements and fees that have required ALLO to obtain franchises from each incorporated municipality in which it operates. ALLO is also required to obtain permits for street opening and construction, or for operating franchises to install and expand fiber optic facilities. These permits or other licenses or agreements typically require the payment of fees.

ALLO's aerial and underground construction operations are subject to extensive laws and regulations relating to the maintenance of safe conditions in the workplace. ALLO could also be subject to potential liabilities in the event it causes a release of hazardous substances or other environmental damage resulting from underground objects it encounters.

Internet services

The provision of internet access services is not significantly regulated by either the FCC or the state commissions. However, the FCC has in recent years taken some steps toward the imposition of some controls on the provision of internet access, and has asserted that it has jurisdictional authority in some areas related to the promotion of an open internet. The extent of the FCC’s jurisdiction with respect to the internet has not been resolved, and the outcome could lead to increased costs for ALLO in connection with its provision of internet services, and could affect ALLO's ability to effectively compete.

As the internet has matured, it has become the subject of increasing regulatory interest. Congress and federal regulators have adopted a wide range of measures directly or potentially affecting internet use, including, for example, consumer privacy, copyright protections, defamation liability, taxation, obscenity, and unsolicited commercial email. ALLO's internet services are subject to

15

the Communications Assistance for Law Enforcement Act ("CALEA") requirements regarding law enforcement surveillance. Content owners are now seeking additional legal mechanisms to combat copyright infringement over the internet. Pending and future legislation in this area could adversely affect ALLO's operations as an ISP and relationship with internet customers. Additionally, the FCC and Congress are considering subjecting internet access services to the Universal Service funding requirements. These funding requirements could impose significant new costs on ALLO's high-speed internet service. Also, the FCC and some state regulatory commissions direct certain subsidies to telephone companies deploying broadband to areas deemed to be “unserved” or “underserved.” State and local governmental organizations have also adopted internet-related regulations. These various governmental jurisdictions are also considering additional regulations in these and other areas, such as privacy, pricing, service and product quality, and taxation. The adoption of new internet regulations or the adaptation of existing laws to the internet could adversely affect ALLO's business.

On June 12, 2015, the FCC Net Neutrality Order became effective. On December 14, 2017, the FCC voted to repeal the Open Internet Order and effectively the net neutrality rules. The previous rules prohibited ISPs from engaging in blocking, throttling, and paid prioritization, and transparency rules compelling the disclosure of network management policies were enhanced. The FCC was also granted the authority under the rules to hear complaints and take enforcement action if it determined that the interconnection activities of ISPs were not just and reasonable, or if ISPs failed to meet general obligations not to harm consumers or what are referred to as edge providers. The final version of the net neutrality repeal order restores the Federal Trade Commission's jurisdiction over broadband internet access services. The uncertainty around how the Federal Trade Commission will respond and challenges to the FCC repeal could limit ALLO’s ability to efficiently manage internet service and respond to operational and competitive challenges.

Although the FCC approved the repeal of Net Neutrality regulations, ALLO’s views on the consumer protection aspect of Net Neutrality remain intact. ALLO will continue to treat internet speeds and access as they were under Net Neutrality regulations.

Television services

Federal regulations currently restrict the prices that cable systems charge for the minimum level of television programming service, referred to as “basic service,” and associated equipment. All other television service offerings are now universally exempt from rate regulation. Although basic service rate regulation operates pursuant to a federal formula, local governments, commonly referred to as local franchising authorities, are primarily responsible for administering this regulation. The majority of ALLO's local franchising authorities have never been certified to regulate basic service cable rates (and order rate reductions and refunds), but they generally retain the right to do so (subject to potential regulatory limitations under state franchising laws), except in those specific communities facing “effective competition,” as defined under federal law. There have been frequent calls to impose expanded rate regulation on the cable industry. As a result of rapidly increasing cable programming costs, it is possible that Congress may adopt new constraints on the retail pricing or packaging of cable programming. Federal rate regulations currently include certain marketing restrictions that could affect ALLO's pricing and packaging of service tiers and equipment. As ALLO attempts to respond to a changing marketplace with competitive pricing practices, it may face regulations that impede its ability to compete.