EXHIBIT 99.1

REGISTRANT’S ANNUAL INFORMATION FORM FOR THE FISCAL YEAR ENDED

DECEMBER 31, 2014.

ANNUAL INFORMATION FORM

March 25, 2015

MAG Silver Corp.

Suite 770 – 800 West Pender Street

Vancouver, BC, Canada V6C 2V6

An additional copy of this Annual Information Form for the

year ended December 31, 2014 may be obtained upon request

from the Corporate Secretary of MAG Silver Corp. at the above

address or from the company’s web site - www.magsilver.com.

|

1

Table of Contents

|

INTRODUCTORY NOTES

|

3

|

|

Date of Information

|

3

|

|

Cautionary Statement on Forward-Looking Information

|

3

|

|

Currency and Exchange Rates

|

6

|

|

Metric Equivalents

|

7

|

|

Financial Data in this AIF

|

7

|

|

Defined Terms

|

7

|

|

Cautionary Statement Regarding Non-IFRS Measures

|

7

|

|

CORPORATE STRUCTURE

|

8

|

|

Intercorporate Relationships

|

8

|

|

GENERAL DEVELOPMENT OF THE BUSINESS

|

10

|

|

Three Year History

|

10

|

|

DESCRIPTION OF THE BUSINESS

|

18

|

|

General

|

18

|

|

Principal Markets

|

18

|

|

Adjacent Property Disclosure

|

18

|

|

Cautionary Note to Investors Concerning Estimates of Mineral Resources

|

18

|

|

Technical Information

|

19

|

|

Passive Foreign Investment Company

|

19

|

|

Employees

|

19

|

|

Competitive Conditions

|

19

|

|

Economic Dependence

|

20

|

|

CARRYING ON BUSINESS IN MEXICO

|

20

|

|

RISK FACTORS

|

24

|

|

MINERAL PROJECTS

|

43

|

|

DIVIDENDS

|

58

|

|

DESCRIPTION OF CAPITAL STRUCTURE

|

58

|

|

Common Shares

|

58

|

|

Shareholder Rights Plan

|

59

|

|

MARKET FOR SECURITIES

|

59

|

|

Trading Price and Volume

|

59

|

|

Prior Sales

|

60

|

|

DIRECTORS AND OFFICERS

|

60

|

|

Name, Occupation and Security Holding

|

60

|

|

Cease Trade Orders, Bankruptcies, Penalties or Sanctions

|

63

|

|

Conflicts of Interest

|

64

|

|

Audit Committee

|

65

|

|

Compensation Committee

|

67

|

|

Corporate Governance and Nomination Committee

|

67

|

|

Disclosure Committee

|

68

|

|

Finance Committee

|

68

|

|

LEGAL PROCEEDINGS AND REGULATORY ACTIONS

|

68

|

|

INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS

|

69

|

|

TRANSFER AGENTS AND REGISTRARS

|

70

|

|

MATERIAL CONTRACTS

|

70

|

|

INTERESTS OF EXPERTS

|

70

|

|

ADDITIONAL INFORMATION

|

71

|

|

Schedule “A”

|

72

|

|

Schedule “B”

|

78

|

2

INTRODUCTORY NOTES

In this Annual Information Form (“AIF”), unless the context otherwise dictates, “we”, “MAG” or the “Company” refers to MAG Silver Corp. and its subsidiaries.

Date of Information

All information in this AIF is as of December 31, 2014 unless otherwise indicated.

Documents Incorporated By Reference

The information provided in this AIF is supplemented by disclosure contained in the documents listed below which are incorporated by reference into this AIF. These documents must be read together with this AIF. The documents listed below are not contained within, nor attached to this document. The documents may be accessed by the reader at the following locations:

|

Type of Document

|

Effective Date /

Period Ended

|

Date Filed /

Posted

|

Document name which may be viewed at the SEDAR website at www.sedar.com

|

|

|

Amended and Restated Technical Report on the Mineral Resource Update for the Juanicipio Joint Venture, Zacatecas State, Mexico

|

June 12, 2014

(Amended June 30, 2014)

|

July 3, 2014

|

Technical Report (43-101) – English Qualification Certificate(s) and Consent(s)

|

|

|

Technical Report on the Upper Manto Deposit, Chihuahua, Mexico

|

November 14, 2012

|

November 16, 2012

|

Technical Report (43-101) – English Qualification Certificate(s) and Consent(s)

|

Cautionary Statement on Forward-Looking Information

This AIF and the documents incorporated by reference herein contain forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of Canadian securities laws. Such forward-looking statements and information include, but are not limited to:

|

|

·

|

the future price of silver, gold, lead and zinc;

|

|

|

·

|

the estimation of mineral resources;

|

|

|

·

|

preliminary economic estimates relating to the Juanicipio Project (as defined herein);

|

|

|

·

|

estimates of the time and amount of future silver, gold, lead and zinc production for specific operations;

|

|

|

·

|

estimated future exploration and development expenditures and other expenses for specific operations;

|

|

|

·

|

permitting time lines;

|

|

|

·

|

the Company’s expectations regarding impairments of mineral properties;

|

|

|

·

|

the Company’s expectations regarding its negotiations with the Ejido to obtain surface access to the Cinco de Mayo project;

|

3

|

|

·

|

the anticipated timing of an updated technical report for Minera Juanicipio (as defined herein);

|

|

|

·

|

the anticipated timing of a formal ‘production decision’ at Minera Juanicipio (as defined herein);

|

|

|

·

|

the Company’s expectations regarding the sufficiency of its capital resources and requirements for additional capital;

|

|

|

·

|

litigation risks;

|

|

|

·

|

currency fluctuations; and

|

|

|

·

|

environmental risks and reclamation cost.

|

When used in this AIF, any statements that express or involve discussions with respect to predictions, beliefs, plans, projections, objectives, assumptions or future events of performance (often but not always using words or phrases such as “anticipate”, “believe”, “estimate”, “expect”, “intend”, “plan”, “strategy”, “goals”, “objectives”, “project”, “potential” or variations thereof or stating that certain actions, events, or results “may”, “could”, “would”, “might” or “will” be taken, occur, or be achieved, or the negative of any of these terms and similar expressions), as they relate to the Company or management, are intended to identify forward-looking statements and information. Such statements reflect the Company’s current views with respect to future events and are subject to certain known and unknown risks, uncertainties and assumptions.

Many factors could cause actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements and information, including, among others:

|

|

·

|

the potential for no commercially mineable deposits due to the speculative nature of the Company’s business;

|

|

|

·

|

none of the properties in which the Company has an interest having any mineral reserves;

|

|

|

·

|

the Company’s properties are primarily in the exploration stage, and most exploration projects do not result in commercially mineable deposits;

|

|

|

·

|

estimates of mineral resources being based on interpretation and assumptions which are inherently imprecise;

|

|

|

·

|

no guarantee of surface rights for the Company’s mineral properties;

|

|

|

·

|

no guarantee of the Company’s ability to obtain all necessary licenses and permits that may be required to carry out exploration and development of its mineral properties and business activities;

|

|

|

·

|

risks related to all of the properties in which the Company has an interest being located in Mexico;

|

|

|

·

|

the effect of global economic and political instability on the Company’s business;

|

|

|

·

|

risks related to the Company’s ability to finance substantial expenditures required for commercial operations on its mineral properties;

|

|

|

·

|

the Company’s history of losses and no revenues from operations;

|

|

|

·

|

risks related to the Company’s ability to arrange additional financing, and possible loss of the Company’s interests in its properties due to a lack of adequate funding;

|

|

|

·

|

risks related to the development of the ramp decline to access and confirm mineralization at the Juanicipio Project, particularly, Minera Juanicipio not yet having made a formal “production decision”, and no guarantee that the financial results and the contemplated development timeline will be consistent with the Technical Report (as defined herein);

|

|

|

·

|

risks relating to the capital requirements for the Juanicipio Project and the timeline to production;

|

|

|

·

|

risks related to title, challenge to title, or potential title disputes regarding the Company’s mineral properties;

|

4

|

|

·

|

risks related to the Company being a minority shareholder of Minera Juanicipio;

|

|

|

·

|

risks related to disputes with joint venture partners;

|

|

|

·

|

risks related to the influence of the Company’s significant shareholders over the direction of the Company’s business;

|

|

|

·

|

the potential for legal proceedings to be brought against the Company;

|

|

|

·

|

risks related to environmental regulations;

|

|

|

·

|

the highly competitive nature of mineral exploration industry;

|

|

|

·

|

risks related to equipment shortages, access restrictions and lack of infrastructure;

|

|

|

·

|

the Company’s dependence upon key personnel, some of whom may not have entered into written agreements with the Company, and other qualified management;

|

|

|

·

|

the Company’s dependence on certain service providers (Minera Cascabel S.A. de C.V. (“Cascabel”) and IMDEX Inc. (“IMDEX”)) to supervise operations in Mexico;

|

|

|

·

|

risks related to directors being, or becoming, associated with other natural resource companies which may give rise to conflicts of interest;

|

|

|

·

|

currency fluctuations (particularly the C$/US$ and US$/Mexican Peso exchange rates) and inflationary pressures;

|

|

|

·

|

risks related to mining operations generally;

|

|

|

·

|

risks related to fluctuation of mineral prices and marketability;

|

|

|

·

|

the Company being subject to anti-corruption laws, human rights laws, and Mexican foreign investment and income tax laws;

|

|

|

·

|

the Company being subject to Canadian disclosure practices concerning its mineral resources which allow for more disclosure than is permitted for domestic U.S. reporting companies;

|

|

|

·

|

risks related to maintaining adequate internal control over financial reporting;

|

|

|

·

|

funding and property commitments that may result in dilution to the Company’s shareholders;

|

|

|

·

|

the volatility of the price of the Company’s Common Shares;

|

|

|

·

|

the uncertainty of maintaining a liquid trading market for the Company’s Common Shares;

|

|

|

·

|

of the Company being a “passive foreign investment company” which may have adverse U.S. federal income tax consequences for U.S. shareholders;

|

|

|

·

|

the difficulty of U.S. litigants effecting service of process or enforcing any judgments against the Company, as the Company, its principals and assets are located outside of the United States;

|

|

|

·

|

all of the Company’s assets being located outside of Canada;

|

|

|

·

|

risks related to the decrease of the market price of the Common Shares if the Company’s shareholders sell substantial amounts of Common Shares;

|

|

|

·

|

risks related to dilution to existing shareholders if stock options are exercised; and

|

|

|

·

|

the history of the Company with respect to not paying dividends and anticipation of not paying dividends in the foreseeable future.

|

Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described herein. This list is not exhaustive of the factors that may affect any of the Company’s forward-looking statements and information. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements of the Company or other future events or conditions may differ materially from those reflected in the forward-looking statements and information due to a variety of risks, uncertainties and other factors, including without limitation, those referred to in this AIF under the heading “Risk Factors” and documents incorporated by reference herein. The Company’s forward-looking statements and information are based on the reasonable beliefs, expectations and opinions of management on the date the statements are made and, other than as required by applicable securities laws, the Company does not assume any obligation to update forward-looking statements and information if circumstances or management’s beliefs, expectations or opinions should change. For the reasons set forth above, investors should not attribute undue certainty to or place undue reliance on forward-looking statements and information.

5

Currency and Exchange Rates

All dollar amounts referred to in this AIF are expressed in United States dollars (“US$”) except where indicated otherwise. The Company’s accounts are based on a US$ functional currency and are reported in a US$ presentation currency. All references to “dollars” are “$” are to US$ except where indicated otherwise. All references to “pesos” are to Mexican pesos. The Company incurs expenditures primarily in US$, and to a lessor extent in Canadian dollars (“C$”), and pesos.

The following table sets forth the rate of exchange for the C$ expressed in US$ in effect at the end of the periods indicated, the average of exchange rates in effect on the last day of each month during such periods, and the high and low exchange rates during such periods based on the noon rate of exchange as reported by the Bank of Canada for conversion of Canadian dollars into United States dollars:

|

Canadian dollars, as expressed in US dollars

|

Year Ended December 31

|

||

|

2014

|

2013

|

2012

|

|

|

Rate at end of period

|

$0.8620

|

$0.9402

|

$1.0051

|

|

Average rate for period

|

$0.9030

|

$0.9666

|

$1.0012

|

|

High for period

|

$0.9422

|

$1.0164

|

$1.0299

|

|

Low for period

|

$0.8589

|

$0.9348

|

$0.9599

|

The noon rate of exchange on March 25, 2015 as reported by the Bank of Canada for the conversion of Canadian dollars into United States dollars was C$1.00 equals US$0.7992.

The following table sets forth the rate of exchange for the Mexican Peso expressed in US$ in effect at the end of the periods indicated, the average of exchange rates in effect on the last day of each month during such periods, and the high and low exchange rates during such periods based on the exchange rate published by Banco de Mexico in the Official Journal of the Federation to settle liabilities denominated in foreign currency payable in Mexico, for conversion of Mexican Pesos into United States dollars (“Official Closing Rate”):

6

|

Mexican pesos, as expressed in US dollars

|

Year Ended December 31

|

||

|

2014

|

2013

|

2012

|

|

|

Rate at end of period

|

$0.0679

|

$0.0765

|

$0.0770

|

|

Average rate for period

|

$0.0748

|

$0.0779

|

$0.0760

|

|

High for period

|

$0.0778

|

$0.0835

|

$0.0792

|

|

Low for period

|

$0.0676

|

$0.0744

|

$0.0695

|

The Official Closing Rate of exchange on March 25, 2015 as reported by the Banco de Mexico for the conversion of Mexican Pesos into United States dollars was $1.00 Pesos equals US$0.0670.

Metric Equivalents

For ease of reference, the following factors for converting Imperial measurements into metric equivalents are provided:

|

To convert from Imperial

|

To metric

|

Multiply by

|

|

Acres

|

Hectares

|

0.404686

|

|

Tons

|

Tonnes

|

0.907185

|

|

Troy Ounces/ton (“opt”)

|

Grams/Tonne (“g/t”)

|

34.2857

|

Financial Data in this AIF

Financial information reported in this AIF is in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

Defined Terms

A glossary of certain terms used in this AIF is attached as Schedule “B”. Terms used and not defined in this AIF that are defined in National Instrument 51-102 - Continuous Disclosure Obligations shall bear that definition. Other definitions are set out in National Instrument 14-101 - Definitions.

Cautionary Statement Regarding Non-IFRS Measures

This AIF includes certain terms or performance measures commonly used in the mining industry that are not defined under IFRS, including cash cost per ounce of silver. These terms and measures do not have a standardized meaning prescribed by IFRS. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Non-IFRS measures should be read in conjunction with the Company’s financial statements.

7

CORPORATE STRUCTURE

MAG Silver Corp. was originally incorporated under the Company Act (British Columbia) on April 21, 1999 under the name “583882 B.C. Ltd.”. On June 28, 1999, in anticipation of becoming a capital pool company, the Company changed its name to “Mega Capital Investments Inc.” On April 22, 2003, the Company changed its name to “MAG Silver Corp.” to reflect its new business upon the completion of its qualifying transaction on the TSX Venture Exchange. Effective March 29, 2004, the Company Act (British Columbia) was replaced by the Business Corporations Act (British Columbia). Accordingly, on July 27, 2005, the Company transitioned under the Business Corporations Act (British Columbia) and adopted new articles and concurrently increased its authorized capital from 1,000,000,000 Common Shares to an unlimited number of Common Shares without par value and an unlimited number of Preferred Shares without par value.

The Company’s head office is located at Suite 770, 800 West Pender Street, Vancouver, British Columbia, Canada, V6C 2V6. The Company’s registered office is located at 2600 – 595 Burrard Street, Vancouver, British Columbia Canada, V7X 1L3.

Intercorporate Relationships

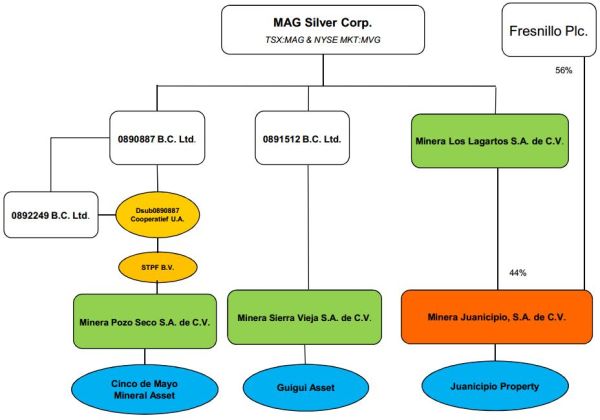

The Company is the registered owner of 99.99% of the issued Class I shares of Minera Los Lagartos, S.A. DE C. V. (“Lagartos”), a corporation incorporated under the laws of Mexico. The remaining 0.01% of the issued Class I shares of Lagartos are held by Dan MacInnis, a director of the Company. The Company effectively has 100% beneficial ownership of Lagartos. The registered and records office of Lagartos is located at Paseo de Los Tamarindos 60, Bosques de Las Lomas, 05120 Mexico, D.F., Mexico.

Lagartos is the registered owner of a 44% interest in Minera Juanicipio, S.A. DE C.V. (“Minera Juanicipio”), and Fresnillo plc (“Fresnillo”), a London Stock Exchange listed company that is controlled by Industrias Peñoles, S.A. DE C.V. (“Peñoles”), holds the remaining 56% interest in Minera Juanicipio. In December 2007, Lagartos and Peñoles established Minera Juanicipio to hold and operate all mineral and surface rights related to the Juanicipio property located in Zacatecas State, Mexico. Minera Juanicipio is governed by a shareholders agreement dated October 10, 2005 (the “Shareholders Agreement”). Pursuant to the Shareholders Agreement each shareholder is to provide funding to Minera Juanicipio pro rata to its interest in Minera Juanicipio, with Fresnillo contributing 56% and MAG, through Lagartos, contributing 44% (the “Juanicipio Joint Venture”). See more detail at “Description of the Business – The Juanicipio Property” below. The registered and records office of Minera Juanicipio is located at Moliere 222- 4th Floor, Los Morales-Palmas, C.P. 11540, México, D.F.

On October 18, 2010 the Company internally restructured its Mexican property holdings. Two new Mexican subsidiaries were created, Minera Pozo Seco S.A. de C.V. (“Minera Pozo Seco”) and Minera Sierra Vieja S.A. de C.V., (“Sierra Vieja”), and properties with common attributes were grouped together in order to provide the Company with more flexibility in managing its properties. The Cinco de Mayo Property was transferred to Minera Pozo Seco, and Guigui and various other properties and property option interests held at the time were transferred to Sierra Vieja. The Lagartos properties and its 44% interest in Minera Juanicipio remain in Lagartos. See Exhibit I below.

The Company, through various subsidiaries (as detailed in Exhibit 1 below), is the beneficial owner of 99.99% of the issued Class I shares of both Minera Pozo Seco and Sierra Vieja. The remaining 0.01% of the issued Class I shares of each of Minera Pozo Seco and Sierra Vieja are held by Dan MacInnis, a director of the Company. The Company effectively has 100% beneficial ownership of both Minera Pozo Seco and Sierra Vieja. The registered and records office of each is located at Paseo de Los Tamarindos No. 60, 3rd floor, Colonia Bosques de Las Lomas, 05120 Mexico, Federal District, Mexico.

8

Exhibit 1: Corporate structure as at December 31, 2014:

The following table lists the subsidiaries of the Company and a company in which MAG holds a significant interest, together with the jurisdiction of incorporation and the direct or indirect percentage ownership by the Company of each such subsidiary:

|

Name

|

Percentage of Ownership

|

Jurisdiction of Organization

|

|

Minera Los Lagartos, S.A. DE C.V.

|

100%(1)

|

Mexican Republic

|

|

Minera Juanicipio, S.A. DE C.V.

|

44%(2)

|

Mexican Republic

|

|

0890887 B.C. Ltd.

|

100%(3)

|

Canada

|

|

0891512 B.C. Ltd.

|

100%(3)

|

Canada

|

|

0892249 B.C. Ltd.

|

100%(3)

|

Canada

|

|

DSUB0890887 Cooperatief U.A.

|

100%(4)

|

Netherlands

|

|

STPF B.V.

|

100%(5)

|

Netherlands

|

|

Minera Pozo Seco S.A. DE C.V.

|

100%(6)

|

Mexico

|

|

Minera Sierra Vieja S.A. DE C.V.

|

100%(6)

|

Mexico

|

9

Notes:

|

(1)

|

On October 9, 2005 the assets of Lexington Capital Group Inc., previously a subsidiary of the Company, were merged with Lagartos, so that all of the Company’s interests in the Juanicipio claim were held by Lagartos.

|

|

(2)

|

44% interest is owned by Lagartos, which in turn is wholly owned by the Company.

|

|

(3)

|

0890887 B.C. Ltd., 0892249 B.C. Ltd., and 0891512 B.C. Ltd. were incorporated on September 21, 2010, September 28, 2010, and October 6, 2010, respectively and are wholly owned by the Company.

|

|

(4)

|

DSUB0890887 Cooperatief U.A. was incorporated on October 11, 2010 in the jurisdiction of the Netherlands, and is wholly owned by 0890887 B.C. Ltd. and 0892249 B.C. Ltd.

|

|

(5)

|

STPF B.V. was acquired by DSUB0890887 Cooperatief U.A. on October 12, 2010.

|

|

(6)

|

Minera Pozo Seco and Sierra Vieja were incorporated in Mexico on September 27, 2010.

|

GENERAL DEVELOPMENT OF THE BUSINESS

MAG is a company based in Vancouver, British Columbia, Canada focused on the acquisition, exploration and development of district scale projects located in the Mexican Silver Belt. The Company’s Common Shares trade on the Toronto Stock Exchange (“TSX”) under the symbol MAG and on the NYSE MKT LLC (formerly NYSE.A) under the symbol MVG. The Company is a “reporting issuer” in the Provinces of British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, Nova Scotia, New Brunswick, Prince Edward Island and Newfoundland and Labrador and is a reporting “foreign issuer” in the United States of America.

The Company’s two material properties at the date of this AIF are its 44% joint venture interest in the Juanicipio property (where underground development is ongoing) and the 100% owned Cinco de Mayo Property (which hosts the Upper Manto Ag-Au-Zn-Pb Deposit and the Pegaso discovery). The Juanicipio property is the most advanced and has been the most significant valuation factor for the Company. Although a formal production decision has not been made at Minera Juanicipio, on October 28, 2013, underground development commenced on the Juanicipio property, and has been ongoing since then, and along with exploration drilling on the property. The Company’s share of Juanicipio exploration and development costs are funded primarily through its 44% interest in Minera Juanicipio, and to a lesser extent, costs are incurred directly by MAG related to direct project oversight of the ramp development, and of the field and drilling programs executed on the Juanicipio property. Exploration and drilling on Cinco de Mayo and on the Company’s other properties is managed directly by MAG, through contracted service providers in Mexico (drilling companies, assay companies, etc.) as the Company has no direct employees in Mexico. All the work is overseen and supervised at industry market rates, by Cascabel and IMDEX, related companies to MAG (see “INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS” below).

Three Year History

Year Ended December 31, 2012

In September 2012, the Company closed a brokered private placement for 3,526,210 common shares of the Company at a price of C$9.40 per share for gross proceeds of $33,451,321. The intended use the net proceeds from the offering ($31,286,353) was to fund its share of the 2012 approved permitting and underground development program for Juanicipio (see “Juanicipio Property” below), for the exploration advancement of Cinco de Mayo and its other properties, and for general corporate purposes.

10

In 2012, costs were incurred dealing and negotiating with a dissident group of MAG shareholders which collectively held approximately 9.76% of MAG's outstanding shares at the time. The Company ultimately reached an agreement with the group on September 4, 2012 whereby MAG agreed to nominate Richard Clark and Peter Barnes for election to the board at the annual and special meeting (“Annual Meeting”) of shareholders held on October 5, 2012. At the Annual Meeting, Mr. Clark and Mr. Barnes along with seven of the existing members of MAG's board were elected.

Operational highlights of 2012 include the following summary.

Juanicipio Property

During the year ended December 31, 2012, the Company independently incurred project oversight expenditures on the Juanicipio property of $879,851, and advanced an additional $3,697,760 to Minera Juanicipio with respect to its proportionate 44% share of joint venture expenditures.

Updated Preliminary Economic Assessment (“UPEA”)

In June 2012, the Company announced the results of an updated Preliminary Economic Assessment undertaken by AMC Mining Consultants (Canada) Ltd. (“AMC”) and a NI 43-101 technical report, entitled “Technical Report for Minera Juanicipio S.A. de C.V.” documenting the economic assessment, was filed on SEDAR on July 16, 2012 (“UPEA”). The UPEA was expected to provide an important catalyst for Minera Juanicipio and open a pathway for the next step in its development, and has formed the basis for the start of the underground development (see “Year ended December 31, 2013” below). The UPEA has since been superceded and replaced by the Technical Report in respect of the Juanicipio Project dated June 12, 2014 (see below).

Underground Development Program

With the completion of the UPEA, MAG and Fresnillo had a framework on which the joint venture Technical Committee could build upon for the continued advancement of the Juanicipio Project. On August 15, 2012, the Company announced that the board of directors of Minera Juanicipio had approved an initial development budget covering mine permitting, surface preparation and the commencement of the first 2,500 metres of underground decline development. The proposed work plan is based on recommendations provided to Minera Juanicipio in the UPEA. (and those recommendations are also contained in the June 12, 2014 Technical Report which subsequently superceded the UPEA and is described in detail below).

The development program is being managed by Fresnillo as operators of the Joint Venture. See “Risks Related to the Development of the Juanicipio Project” below.

Cinco de Mayo Property

During the year ended December 31, 2012, the Company incurred exploration and evaluation expenditures at the Cinco de Mayo Property in connection with approximately 33 thousand metres of drilling in 54 holes. Overall, the 2012 drilling demonstrated that mineralization is continuous from the Jose Manto through the Bridge Zone to Cinco Ridge, which is now collectively referred to as the “Upper Manto” to differentiate it from mineralization hit at depth in the “Pegaso Zone.”

11

Hole CM12-431: The Pegaso Zone

In mid-June 2012, exploration hole CM12-431 drilled deep beneath the overlap zone between the Bridge Zone and the Jose Manto, cut four significant sulphide intervals within a 300 metre wide skarn and marble zone. The largest and deepest interval was 61 metres of high-grade massive sulphides that lies behind (to the southwest of) the structures that host the Upper Manto mineralization. This is an entirely new mineralization zone named the “Pegaso Zone,” which shows all of the hallmarks of being a near-source part of the Carbonate Replacement Deposit (“CRD”) system that MAG has been systematically seeking at Cinco de Mayo. The Company believes that the mineralization in the upper intercepts of hole CM12-431 may connect to the high-grade silver-lead-zinc mineralization in the 4 kilometre long Upper Manto, indicating that continuous mineralization exists from 125 to 900 metres vertical depth.

Upper Manto Inferred Mineral Resource

In October 2012, the Company announced that Roscoe Postle Associates (“RPA”) completed the first independent Mineral Resource estimate for the Upper Manto (Bridge Zone/Jose Manto). Inferred Mineral Resources are estimated to be 12.45 million tonnes at 132 g/t (3.9 opt) silver, 0.24 g/t gold, 2.86% lead and 6.47% zinc (9.33% lead plus zinc). An economic cut-off grade set at a net smelter return (“NSR”) of US$100 per tonne was applied as the base case for this initial resource estimate. The NI 43-101 Technical Report, entitled “Technical Report on the Upper Manto Deposit, Chihuahua, Mexico” was filed on SEDAR on November 16, 2012.

Overall, the near-surface Upper Manto mineralization appears higher in silver and lead than the deeper Pegaso Zone mineralization which is richer in zinc, copper and gold. The combined vertical metals and alteration zoning and broadening of mineralization is typical in CRD systems worldwide and strongly indicates that the source intrusion is being approached. The overall strength and style of mineralization and alteration further indicate that this source zone may be very large. The strongest mineralization has been found within the overlap zone between the fault slices that host the shallow Jose Manto and the Bridge Zone, suggesting that this structurally complex zone acted as a major conduit for mineralizing fluids and perhaps intrusive emplacement. The degree of mineralization seen so far indicates that the source intrusion could be surrounded by very large-scale mineralization.

“Soil Use Change Permit” and surface access

As of May, 2012, exploration drilling permits in Mexico require a “Soil Use Change Permit,” reflecting conversion of land from agricultural to industrial use. These permits incorporate verification of mining concession title, compliance with environmental norms, and surface access permissions. During the latter part of 2012, the Company was in the process of negotiating ordinary course surface access permissions with the Ejido Benito Juarez (the “Ejido”) as the final component in the application for the necessary Soil Use Change Permits. The Company had previously purchased 41 specific rights relating to relevant areas of the Cinco de Mayo project area from the Ejido members, who along with the Federal Agrarian Authority had ratified the purchase. The Company was awaiting formal title transfer of the surface rights, when certain members of the Ejido challenged the purchase, claiming the 41 rights purchased represented a 41/421 undivided interest in the Ejido owned surface rights , rather than rights to exclusive areas of the property.

12

The Company had anticipated obtaining the requisite access permission and final permit approval early in 2013. However, on November 17, 2012 at what the Company believes was an illegally constituted meeting, the Ejido voted to expel MAG from its Cinco de Mayo Property and establish a 100 year mining moratorium over Northern Chihuahua. The Company noted that it has been advised by its Mexican legal advisors that the Ejido Assembly has no ability in law to impose a ban on mining. Several Ejido members challenged the meeting on the grounds that proper notice was not given, key signatures required to properly call the meeting were fraudulent, and that the vote taken at the meeting was fraught with irregularities, including a significant number of votes being cast by unverified proxies. A court hearing was scheduled for the first quarter of 2013. MAG expected that the meeting and the illegal resolutions would be nullified, at which time, the Company planned to ask government officials to oversee a new assembly meeting of the Ejido to ensure that the necessary procedural and governance rules would be respected and the vote properly conducted.

Permission of the Ejido assembly is required to obtain surface access, and although there is no certainty that a new vote would produce a favourable outcome for the Company, MAG believes that the opposition group and its supporters do not represent the will of the majority of the 421 voting members of the Ejido (or of the 12,000 other citizens in the project area).

Year Ended December 31, 2013

The Company’s exploration and evaluation activity on its own 100% owned properties was minimal in the year ended December 31, 2013. Since April 2013 there has been significant volatility and a negative trend in the market prices for silver, gold and various base metals. In addition, poor market conditions have recently prevailed, making equity funding for exploration projects challenging. Given these prevailing market conditions and the desire to preserve cash for core projects, management determined that some of the Company’s non-core assets should be abandoned and written off. In the year ended December 31, 2013, the Lagartos Properties, specifically the “Lagartos NW,” “Largartos SE” and “Lagartos V” claims were written off, along with the 100% owned Lorena and Nuevo Mundo claims and their respective concessions were either not renewed in the year or will not be renewed going forward. The Mojina property was also considered impaired, and the option earn in agreement was terminated and its associated exploration and evaluation costs were written off.

During the year ended December 31, 2013, the Company entered into an option agreement with Canasil Resources Inc. (“Canasil”) whereby the Company can earn up to a 70% interest in Canasil's 14,719 hectare Salamandra property located in Durango State, Mexico. The Company paid C$150,000 upon signing the agreement, and to earn an initial 55% interest in the property, the Company must make additional cash payments to Canasil of C$600,000 over a period of four years, and complete C$5,500,000 in exploration expenditures over the same period, including a minimum committed first year work expenditure of C$1,000,000 and 3,000 metres of drilling. Upon earning its 55% interest, the Company may elect to earn a further 15% interest by producing either a feasibility study or spending an additional C$20,000,000 over a further four year period. A portion of the property is subject to a 2% NSR royalty, half of which may be purchased from the holder for $1,000,000.

Although Mr. Dan MacInnis will remain as an integral member of the board of directors, Mr. MacInnis announced his retirement as President and CEO of the Company, effective October 14, 2013. Mr. George Paspalas, who has held senior management positions at Silver Standard, Placer Dome, and most recently CEO of Aurizon Mines Ltd., was appointed as the successor on October 15, 2013. Mr. Paspalas brings a wealth of technical, operating and capital market experience to the Company, as it transitions itself to the next level of project development.

13

Juanicipio Property

Minera Juanicipio began the development permitting process in the fall of 2012 with the expectation of commencing the underground decline development in the first half of 2013. However, due to development permitting delays resulting from the recent Mexican government changeover, the start of the decline development was unavoidably delayed. On October 28, 2013, Minera Juanicipio commenced the underground development at the Juanicipio project. The initiation of underground work followed a year of engineering, hydrological and environmental studies in support of required permits. With the portal area preparation complete, a continuous miner started excavating the uppermost part of the access decline ramp.

Infill drilling - Valdecañas Vein

The Minera Juanicipio development budget proposed infill drilling on a maximum of 75 metre centres along the Valdecañas Vein, designed to convert inferred mineral resources to indicated mineral resources. To December 31, 2013, a total 40 infill holes had been completed by Minera Juanicipio, with 6 holes left in the infill drill program to be completed in 2014. The results were as expected showing the typical metal zoning of Fresnillo-style veins in the district.

2013 Exploration Program

The 2013 exploration budget for Minera Juanicipio included 13,033 metres of drilling to explore for additional veins and to delineate the high grade ore shoot emerging on the Juanicipio Vein. However, permitting for some of the areas where exploration drilling was planned took longer than expected and the majority of drilling in 2013 was ultimately concentrated on infill drilling on the Valdecañas Vein (see above). Infill drilling designed to convert inferred mineral resources to indicated mineral resources, is part of the development budget , and is excluded from the 2013 exploration budget.

Cinco de Mayo Property

No drilling or active exploration was undertaken on the Company’s 100% owned Cinco de Mayo Project in 2013. The Company has been in the process of negotiating a renewed surface access agreement with the local Ejido, since it was asked to vacate the property in November 2012 at what the Company maintains was an illegally constituted Ejido Assembly (see “Soil Use Change Permit” and surface access above in “Year Ended December 31, 2012”). In the year ended December 31, 2013, the principal focus of work has been in preparation for these negotiations and has included meetings with Chihuahua State, Municipal, and Mexican Federal authorities and Community Public Relations and legal advisors in Mexico. This process was protracted due to the political transition period as the new party and Presidency assumed operation of the Mexican government in December 2012, coupled with Municipal elections held in July 2013.

Various Ejido members legally challenged the November 2012 Assembly meeting, on the grounds that proper notice was not given, key signatures required to properly call the meeting were fraudulent, and that the vote taken at the meeting was fraught with irregularities, including a significant number of votes being cast by unverified proxies. A court hearing was held on February 6, 2013 in Chihuahua where the ejiditarios calling for the meeting to be declared illegal presented their evidence. The opponents who had organized the illegal meeting failed to appear in court on time and their testimony was dismissed by the judge. The judge ordered the Ejido administration to provide original documents for the meeting, which they failed to provide, so the judge declared their participation ended. As a result of back log of rulings, the judge’s formal ruling had still not been rendered as at year end, but was issued in February 2014 (see “Year Ended December 31, 2014” below).

14

Year Ended December 31, 2014

On July 16, 2014, the Company closed a bought deal public financing and issued 7,712,000 common shares, including 392,000 commons shares issued on partial exercise of the over-allotment option, at C$10.25 per share, for gross proceeds of $73,376,306 (C$79,048,000). On August 18, 2014, the underwriters exercised the balance of the over-allotment in full and issued an additional 706,000 shares at C$10.25 for additional gross proceeds of $6,640,819 (C$7,236,500) bringing total gross proceeds to $80,017,125 (C$86,284,500). As the net proceeds to the Company (C$80,974,635) were received in Canadian dollars, and as the Company funds the majority of its operations in US dollars, 95% of the net proceeds were immediately (upon closings) converted to US$, at a US$/C$ exchange rate of 0.9273. As outlined in the offering documents, the majority of the funds raised are designated for the Juanicipio project, with the balance for working capital and general corporate purposes. As at December 31, 2014, the Company had working capital of $87,033,742 including cash of $86,280,385.

Operational highlights of 2014 include the following summary.

Juanicipio Property

For the year ended December 31, 2014, the Company’s total combined expenditures on the Juanicipio property amounted to $4,738,177, and included $4,378,000 for its 44% share of cash advances, and a further $360,177 expended directly by the Company on project oversight and on an updated independent resource estimate.

On May 27, 2014 the Company announced an updated independent Mineral Resource estimate for the Juanicipio Property completed by RPA. The updated estimate reflects the results of 40 infill holes drilled in 2012 and 2013, and is based on drill results available as of December 31, 2013. The new estimate demonstrates a conversion of previously classified Inferred Resources into the Indicated category and reports a deep lower grade resource separately. An amended and restated NI 43-101 technical report documenting the updated Mineral Resource estimate and including enhanced cautionary language was filed on SEDAR on July 3, 2014 (the “Technical Report”) – see “Mineral Projects” section below.

As part of the Technical Report, RPA reviewed the 2012 UPEA carried out by AMC Mining Consultants (Canada) Ltd. and believes that it remains a reasonable representation of the property’s economic potential. The results of the 2012 UPEA are included in the Technical Report.

The economic analysis in the Technical Report is preliminary in nature and is based, in part, on Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the PEA will be realized.

The underground work to the end of 2014 has included mine permitting, surface preparation, the commencement of the first 2,500 metres of underground decline development, and infill drilling on the Valdecañas Vein. The majority of the infill drilling was completed in 2013, with the results to December 31, 2013 included in the updated Mineral Resource estimate above. In 2014, the initial ramp decline was advanced primarily utilizing a continuous miner until March 2014, when the contractor hired by Fresnillo to construct the ramp decline on behalf of Minera Juanicipio, received its full explosives permit from the Mexican Ministry of Defense. The development of the ramp decline then advanced from March to December, 2014, with conventional drill and blast cycles as well as with the continuous miner, depending on ground conditions. The continuous miner was retired in mid-December, 2014 and the ramp is now advancing exclusively with drilling and blasting. Late in 2014, based on actual conditions and geotechnical drill holes, it appears that the near-surface zone of variable rock quality has been passed and that the expected better rock quality zone has now been reached.

15

Cinco de Mayo Property

No drilling was undertaken on the Cinco de Mayo property in 2014 as the Company remains in the process of negotiating a renewed surface access agreement with the local Ejido, since it was asked to vacate the property in November 2012 at what the Company maintains was an illegally constituted Ejido Assembly (see ““Soil Use Change Permit” and surface access” above in the Year Ended December 31, 2012). Various Ejido members had legally challenged the Assembly meeting on the grounds that proper notice was not given, key signatures required to properly call the meeting were fraudulent, and that the vote taken at the meeting was fraught with irregularities, including a significant number of votes being cast by unverified proxies. MAG had expected that the Assembly and the resolutions passed would be nullified by the Fifth Unified Agrarian Tribunal (“the Tribunal”), but the Company was notified during the first quarter of 2014 that the Tribunal had rejected the Ejido challenge. The ruling was made on narrow technical grounds and did not speak to the merits of the actions of the Assembly. The Tribunal did note that a new vote of a majority of Ejido members can revoke the actions of the challenged Assembly at any time. The Company has been advised that an appeal of the ruling, based on failure of the Tribunal to consider broader requirements of the Agrarian Law, was promptly filed with the Mexican Supreme Court by the same Ejido members. It was expected that the appeal would have been considered by Courts in the latter half of 2014, but to date it has not, nor has a date for a hearing been set. The Company has no input or involvement in the appeal process, as it is Ejido members who have filed the appeal.

In the year ended December 31, 2014, the principal focus of work on the Cinco de Mayo property has been in preparation for and related to negotiations with the local Ejido which has included meetings with State and Federal authorities, several legal advisors, and Community Relations advisors in Mexico.

While no assurances can be given, MAG is continuing the negotiation process with the intent of arriving at a settlement agreement that would be fully supported at a properly constituted Assembly. Although there is no certainty that a new vote would produce a favourable outcome for the Company, MAG believes that the opposition group and its supporters do not represent the will of the majority of the 421 voting members of the Ejido (or of the 12,000 other citizens in the project area).

MAG believes that the access issue will be overcome, and that the requisite authorizations to complete its submission for the Soil use Change Permit will be obtained in due course. However, the overall timeline to successful resolution is not determinable at this time, and will depend upon various factors including but not limited to: the ability of the Company to arrive at a settlement agreement that would be fully supported by the majority of the Ejido; and, the ability of the Ejido to conduct a properly constituted Assembly meeting, with quorum, and favourable outcome.

16

Current Fiscal Year (Subsequent to December 31, 2014)

MAG continues to work with Fresnillo to progress the Juanicipio Property in accordance with the recommendations of the 2012 UPEA/2014 Technical Report, and the Company continues the negotiation process with the local Ejido to renew its surface rights access on the Cinco de Mayo Property.

Juanicipio Property

Along with some detailed engineering work, the ramp advancement and the associated underground mine infrastructure, continues to be the primary development activity ongoing at Juanicipio. The ramp is now advancing exclusively with drilling and blasting, and it appears that the near-surface zone of variable rock quality has been passed and that the expected better rock quality zone has now been reached. As a result, the ramp decline development has seen a sustained improvement in the advance rate, and subsequent to the year end, the 1 kilometre ramp advancement milestone was passed.

In addition to the Juanicipio underground development, exploration work continues by Minera Juanicipio to seek new veins and trace structures and veins in neighbouring parts of the district onto the Minera Juanicipio joint venture ground. Exploration targets for 2015 were identified at an onsite exploration day in December attended by exploration teams from both MAG and Fresnillo.

Subsequent to the year end on January 8, 2015, the Company advanced $2.2 million to Minera Juanicipio, representing its 44% share of a $4.9 million cash call for expenditures through April 2015. Currently one drill rig is on site and additional rigs will be used for exploration drilling once a series of holes being drilled for bulk metallurgical samples are completed.

Cinco de Mayo Property

No drilling or active exploration is being carried out on the Cinco de Mayo Project as the Company continues the process of negotiating a renewed surface access agreement with the local Ejido. The Company remains willing to work with the Ejido and the greater community to define a comprehensive Corporate Social Responsibility Program (“CSR”) to coincide with the next phases of our exploration activity. MAG’s goal is to continue its working relationship and ensure the Ejido and the greater community benefit from the expected successes and growth at Cinco de Mayo.

The overall timeline to successful resolution and renewed surface access is not determinable at this time, and will depend upon various factors including but not limited to: the ability of the Company to arrive at a settlement agreement that would be fully supported by the majority of the Ejido; and, the ability of the Ejido to conduct a properly constituted Assembly meeting, with quorum, and favourable outcome.

For more information on the Company’s progress and intentions for its material properties please refer to the “Mineral Projects” section below.

17

DESCRIPTION OF THE BUSINESS

General

The Company is in the mineral acquisition, exploration and development business. The Company is in the exploration and development stage and there is no assurance that a commercially viable mineral deposit exists on any of our properties. Further exploration will be required before a final evaluation as to the economic and legal feasibility of any of the Company’s properties is determined. Even if the Company completes its exploration program and is successful in identifying a mineral deposit, it will have to spend substantial funds on further drilling and engineering studies before it will know if it has a commercially viable mineral deposit or reserve.

Principal Markets

The Company is a reporting issuer in the Provinces of British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, Nova Scotia, New Brunswick, Prince Edward Island and Newfoundland and Labrador and is a reporting “foreign issuer” in the United States of America.

The Company’s Common Shares were listed and posted for trading on the TSX Venture Exchange (formerly CDNX) on April 19, 2000 under the symbol “MGA”. Concurrent with the Company’s name change to MAG Silver Corp. on April 22, 2003, the trading symbol was changed to “MAG”. On July 9, 2007, the Company’s Common Shares were listed on the American Stock Exchange (now the NYSE MKT LLC) under the symbol “MVG”. On October 5, 2007, the Company delisted from the TSX Venture Exchange concurrent with its listing on the TSX, with the Company’s Common Shares continuing to trade under the symbol “MAG”.

Adjacent Property Disclosure

The staff of the United States Securities and Exchange Commission (the “SEC”) take the position that mining and mineral exploration companies, in their filings with the SEC, should describe only those mineral deposits that the companies themselves can economically and legally extract or produce. This AIF contains information regarding adjacent properties on which we have no right to explore or mine, and is considered by management to be of material importance to the Company and its land holdings in the area. Investors are cautioned that mineral deposits on adjacent properties do not necessarily indicate and certainly do not prove the existence, nature or extent of mineral deposits on our properties.

Cautionary Note to Investors Concerning Estimates of Mineral Resources

This AIF uses the terms "Indicated Mineral Resources" and “Inferred Mineral Resources”. MAG advises investors that although these terms comply with Canadian reporting standards under NI 43-101, the SEC does not recognize these terms and U.S. companies are generally not permitted to disclose resources in documents that they file with the SEC. Furthermore, disclosure of “contained ounces” is permitted under Canadian regulations; however, the SEC permits issuers to report mineralization that does not constitute “reserves” by SEC standards only as in place tonnage and grade without reference to unit measures.

Investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into reserves. In addition, "Inferred Mineral Resources" have a great amount of uncertainty as to their existence, and economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resources will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources are considered too speculative geologically to have the economic considerations applied to them to enable them to be categorized as mineral resources and, accordingly, may not form the basis of feasibility or pre-feasibility studies, or economic studies except for a Preliminary Economic Assessment as defined under NI 43-101. Investors are cautioned not to assume that part or all of an Inferred Mineral Resource exists, or is economically or legally mineable indicated and inferred mineral resources that are not mineral resources do not have demonstrated economic viability.

18

Technical Information

Unless otherwise indicated, scientific or technical information in this AIF is based on information prepared by employees of MAG or its joint venture partners, as applicable, under the supervision of, or that has been reviewed and approved by, Dr. Peter Megaw, Ph.D., C.P.G., who is a “Qualified Person” as defined in NI 43-101. A “Qualified Person” means an individual who is an engineer or geoscientist with at least five years of experience in mineral exploration, mine development or operation or mineral project assessment, or any combination of these, has experience relevant to the subject matter of the mineral project, and is a member in good standing of a professional association.

Passive Foreign Investment Company

The Company believes it is a Passive Foreign Investment Company (“PFIC”), as that term is defined in Section 1297 of the Internal Revenue Code of 1986, as amended, and believes it will be a PFIC for the foreseeable future. Consequently, this classification may result in adverse tax consequences for U.S. holders of the Company’s Common Shares. For an explanation of these effects on taxation, U.S. shareholders and prospective U.S. holders of the Company’s Common Shares are encouraged to consult their own tax advisers.

Employees

The Company’s business is administered from its head office in Vancouver, British Columbia, Canada. As of December 31, 2014, the Company had eight full time employees (excluding directors), and no part time employees.

Specialized Skill and Knowledge

Many aspects of MAG’s business require specialized skill and knowledge. Such skills and knowledge include the areas of geology, engineering, accounting and mine planning. MAG has found that it has been able to locate and retain such employees when needed.

Competitive Conditions

Competition in the mineral exploration and production industry is intense. The Company competes with a number of large, established mining companies with greater financial resources and technical facilities, for the acquisition and development of mineral concessions, claims, leases and other interests, as well as for the recruitment and retention of qualified employees and consultants and the equipment required to continue the Company’s exploration activities.

19

Economic Dependence

The Juanicipio property, in which the Company owns a 44% joint venture interest, is considered one of the two material properties of the Company, and of all of the Company’s properties, the Juanicipio property is the most advanced and has been the most important valuation factor for the Company. The Company’s interest in the Juanicipio property is held through its indirect 44% ownership of Minera Juanicipio, and is governed by the terms of the Shareholders Agreement with Fresnillo.

The terms of the Shareholders Agreement governing the operation of Minera Juanicipio provide effective control to Fresnillo over many of the activities of Minera Juanicipio, as Fresnillo holds a majority (56%) of the shares of Minera Juanicipio. While a limited number of decisions of the shareholders or the directors of Minera Juanicipio require a special majority of 60%, and in one instance 75%, giving the Company an effective veto over any such decisions, the Company is a minority shareholder of Minera Juanicipio and is dependent on Fresnillo to manage the affairs of Minera Juanicipio in compliance with the Shareholders Agreement, the Articles of Minera Juanicipio and applicable law. The Shareholders Agreement also calls for adjustments to the interests of the shareholders in Minera Juanicipio where either shareholder fails to fund cash calls within certain specified periods. If the Company fails to fund cash calls, it risks having its interest reduced, may lose its effective veto power over certain decisions and ultimately could have its interest in Minera Juanicipio diluted entirely.

Please consult the Company's public filings at www.sedar.com and www.sec.gov for further, more detailed information concerning these matters.

CARRYING ON BUSINESS IN MEXICO

The Company’s property interests are located in Mexico. A summary of the regulatory regime material to the business and affairs of the Company is provided below.

Mining Regulations

The exploration and exploitation of minerals in Mexico may be carried out by Mexican citizens or Mexican companies incorporated under Mexican law by means of obtaining concessions (currently covering exploration and exploitation). Concessions are granted by the Mexican federal government for a period of fifty years from the date of their recording in the Public Registry of Mining. The term of mining concessions previously issued by the Mexican federal government (for exploration and/or exploitation) was automatically extended by the enactment of the 2006 amendments to the Mexican Mining Law. Likewise, due to such amendments, the holders of mining concessions for exploration were automatically authorized to carry out not only exploration work, but also exploitation works.

Holders of concessions may, within the five years prior to the expiration of such concessions, apply for their renewal for the same period of time. Failure to apply prior to the expiration of the term of the concession will result in termination of the concession. Concessions are subject to annual work requirements and payment of mining duties which are assessed and levied on a semi-annual basis. Such concessions may be transferred or assigned by their holders, but such transfers or assignments must comply with the requirements established by the Mexican Mining Law and be registered before the Public Registry of Mining in order to be valid against third parties.

Although the Law of Foreign Investment provides that mineral concessions may also be obtained by foreign citizens or foreign corporations, the Mexican Mining Law provides that such concessions may only be granted to Mexican citizens or Mexican corporations. Thus, foreign citizens or corporations may only obtain mineral concessions through the establishment of a subsidiary in Mexico. Foreign investment in Mexican companies must comply with certain requirements set forth in the Law of Foreign Investment.

20

The Mexican Mining Law does not require payment of finder’s fees or royalties to the Government, except for: i) a mining royalty fee of 7.5% and the 0.5% extraordinary governmental fee on precious metals, (see below “Income Tax – New Tax Regime Effective January 1, 2014); and ii) a discovery premium or economic consideration in connection with claims or allotments contracted directly from the Mexican Geological Service that have been awarded pursuant to a public bid process. None of the property interests held by Lagartos, Minera Pozo Seco or Sierra Vieja are under such fee regimes at the present time. However, holders of mining concessions are required to pay mining concession fees which are assessed and levied on a semi-annual basis, and that increase over time the longer the concessions are held.

Foreign Investment Regulation

Foreign investment regulation in Mexico is primarily governed by the Law of Foreign Investment and its Regulations. Foreign investment of up to 100% in Mexican mining companies is freely permitted. Companies with foreign investment in their capital stock must be registered with the National Registry of Foreign Investment which is maintained by the Ministry of Economy, and file certain reports and notices, including an annual report with respect to the operations carried out during the preceding fiscal year which is necessary in order to renew their certificate of recordation with such Registry.

Environmental Regulations

Mexico has federal, state and municipal laws and regulations relating to the protection of the environment and natural resources (“Environmental Laws”), including laws and regulations concerning water pollution, air pollution, noise pollution, hazardous substances and forest protection. The main federal Environmental Law in Mexico is the Ley General del Equilibrio Ecológico y la Protección al Ambiente (the “General Law of Ecological Balance and Environmental Protection” or the “General Law”), pursuant to which general environmental rules and policies have been promulgated addressing air pollution, hazardous substances and environmental impact among various others.

Another federal law particularly relevant for the mining sector is the Ley General para la Gestión Integral de los Residuos (the “General Law for Integrated Waste Management”) and its regulations the Reglamento de la Ley General para la Prevención y Gestión Integral de los Residuos (the “Regulations to the General Law for Integrated Waste Prevention and Management”), which regulate the generation, handling, transportation, storage and final disposal of hazardous waste, as well as the import and export of hazardous materials and hazardous wastes, and assign liability for ownership and possession of contaminated sites and for contaminating activities. The Ley General de Desarrollo Forestal Sustentable and its regulations (the “Forestry Protection Laws”) are also relevant, as they address reforestation obligations and compensation measures on projects which may have a deforestation impact, which may include mining projects.

On June 7, 2013, the Ley Federal de Responsabilidad Ambiental (Federal Law of Environmental Liability) was enacted, under which any person or entity that directly or indirectly (for action or omission) causes damage to the environment, will be held liable and obliged to: i) repair the damage, or in the event that such repair is not possible; ii) pay compensatory damages, subject to a corresponding judicial, administrative or criminal proceeding.

21

Applicable Environmental Laws contemplate the creation and regulation of Natural Protected Areas (Areas Naturales Protegidas) which along with Ecological Ordinance Programs (Programas de Ordenamiento Ecológico) constitute two of the main instruments that will regulate the use of land in the areas within their jurisdiction, including restrictions on certain activities and sectors, such as the mining sector.

In addition, there are a series of “Mexican Official Norms” which are technical standards issued by competent regulatory authorities, pursuant to the Ley General de Metrología y Normalización and to other laws that include the aforementioned Environmental Laws, which establish standards relating to air emissions, waste water discharges, the generation, handling and disposal of hazardous wastes (including specific Mexican Official Norms for the handling of mining tailings, which are considered mining hazardous wastes) and noise control, among others. There are Mexican Official Norms regarding soil contamination (mainly with total petroleum hydrocarbons and heavy metals) and waste management (the “Ecological Standards”). Of particular importance to the mining sector are Mexican Official Norms NOM-120-SEMARNAT-2011 regulating environmental protection of mining activities in certain zones, and NOM-141-SEMARNAT-2003 which addresses certain aspects of tailings (jales de minería) from mining activities, among other Ecological Standards applicable to mining activities.

The Secretaría de Medio Ambiente y Recursos Naturales (the “Ministry of the Environment and Natural Resources” or “SEMARNAT”, for its initials in Spanish) is the federal agency in charge of establishing and overseeing environmental regulation at the federal level, including the General Law and federal statutes and the Environmental Laws, as well as the Ecological Standards. On enforcement matters the SEMARNAT acts mainly through the “Procuraduría Federal de Protección al Ambiente” (the “Federal Bureau of Environmental Protection” or “PROFEPA”, for its initials in Spanish) and in certain cases through other governmental entities under its control, such as the Comisión Nacional del Agua (or National Water Commission).

Environmental Laws also regulate environmental protection in the mining industry in Mexico. In order to comply with these laws, a series of permits, licenses and authorizations must be obtained by a concession holder during the exploration and exploitation stages of a mining project. Generally, these permits and authorizations are issued on a timely basis after the completion of an application and the fulfillment of the necessary requirements by a concession holder. Additionally, periodic reporting of hazardous wastes and federal air emissions and federal waste water discharges to Federal authorities is required under the Environmental Laws. To the best of the Company’s knowledge, all of the Company’s property interests are currently in compliance with the Environmental Laws.

In the exploration stage, the cost of complying with such Environmental Laws is included in the exploration budget. Until such time as the Company conducts larger more invasive procedures, such as trenching or bulk sampling, there is only nominal cost associated with compliance with the Environmental Laws. The Company’s programs are not yet sufficiently advanced to allow an estimate of the future cost of such environmental compliance.

Currency

The official monetary unit of Mexico is the Mexican peso. The currency exchange rate freely floats and the country has no currency exchange restrictions. Nevertheless, following the devaluation of the Mexican peso in December, 1994, uncertainties continue with respect to the financial situation of Mexico. See “Description of the Business - Risk Factors”, specifically those risk factors dealing with currency fluctuation and inflation.

22

The following table presents a five-year history of the average annual exchange rates to convert one United States dollar into Mexican pesos, calculated by using the average of the exchange rates on the last day of each month during the given year.

|

Year

|

Average Exchange Rate (Mxn peso/US$)

|

|

2014

|

13.3609

|

|

2013

|

12.8411

|

|

2012

|

13.1657

|

|

2011

|

12.4804

|

|

2010

|

12.6555

|

Value Added Tax (“VAT”) also known as “IVA”

In Mexico, VAT is charged on the sale of goods, rendering of services, lease of goods and importation of goods and services at a rate of 16% percent. Exports and other specified items may be subject to a 0% rate. Proprietors selling goods or services must collect VAT on behalf of the government. Goods or services purchased incur a credit for VAT paid. The resulting net VAT is then remitted to, or collected from, the Government of Mexico through a formalized filing process. The Company has traditionally held a VAT receivable balance due to the expenditures it incurs whereby VAT is paid to the vendor or service provider. Collections of these receivables from the Government of Mexico often take months and sometimes years to recover.

Income Tax – New Tax Regime Effective January 1, 2014

The Mexican Senate approved Tax Reform changes in Mexico that became effective January 1, 2014, that in part, adversely affect operating mining companies in Mexico. The changes affecting the Mexican mining industry include: the elimination of a planned reduction in the corporate tax rate from 30% to 28% by 2015 (corporate tax rate will remain 30% indefinitely); a mining royalty fee of 7.5% on income before tax, depreciation, and interest; an extraordinary governmental fee on precious metals, including gold and silver, of 0.5% of gross revenues; and, changes affecting the timing of various expense deductions for tax purposes. Should the tax reform changes remain in place once Minera Juanicipio or any of the Company’s other properties are in production, it will be subjected to this tax regime. However, various industry lobbying and challenges are expected over the next several years, and possible tax planning opportunities may exist to reduce the impact of the tax changes. Managements’ initial assessment of the tax reform changes is that they will not have an impact on the viability of the Juanicipio project.

Under the new tax regime, mining concession holders that fail to develop mining works in accordance with the Mining Law, during a consecutive two year period within the first eleven years of the term of the concession, will pay on a semi-annual basis an additional mining fee equivalent to 50% to the maximum current mining duty. If the failure to carry out works remains unchanged, starting on the twelfth year, the additional fee will be doubled.

An additional component of the Mexican tax reform also includes a 10% dividend tax, to be withheld on all dividends paid to foreign residents of Mexico. With the existing Canadian-Mexico tax treaties, this dividend tax rate will be reduced to 5%. Prior to the tax reform, there was no dividend withholding tax on dividends paid from Mexico to Canadian corporations out of tax paid earnings.

Other general tax amendments are referred to in the “Mexican Foreign Investment and Income Tax Laws apply to the Company” Section.

23

RISK FACTORS

The exploration, development and mining of natural resources are highly speculative in nature and are subject to significant risks. The risk factors noted below do not necessarily comprise all those faced by the Company. Additional risks and uncertainties not presently known to the Company or that the Company currently considers immaterial may also impair the business, operations and future prospects of the Company. If any of the following risks actually occur, the business of the Company may be harmed and its financial condition and results of operations may suffer significantly, along with a possible significant decline in the value and/or share price of the Company’s publicly traded stock.

The Company’s securities should be considered a highly speculative investment and investors should carefully consider all of the information disclosed in the Company’s Canadian and U.S. regulatory filings prior to making an investment in the Company. Without limiting the foregoing, the following risk factors should be given special consideration when evaluating an investment in the Company’s securities.

Risks Relating to the Company’s Business Operations

Mineral exploration and development is a highly speculative business and most exploration projects do not result in the discovery of commercially mineable deposits.

Exploration for minerals is a highly speculative venture necessarily involving substantial risk. The expenditures made by the Company described herein may not result in discoveries of commercial quantities of minerals. The failure to find an economic mineral deposit on any of the Company’s exploration concessions will have a negative effect on the Company.

None of the properties in which the Company has an interest has any mineral reserves.