Use these links to rapidly review the document

PANDORA MEDIA, INC. FORM 10-K TABLE OF CONTENTS

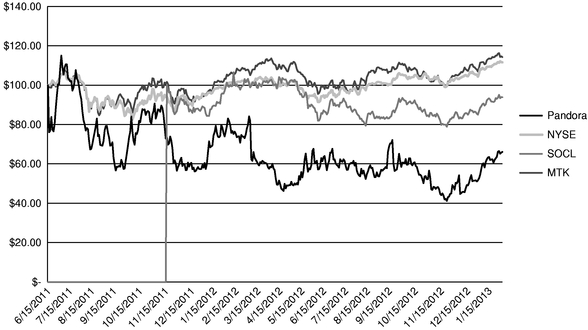

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the Fiscal Year ended January 31, 2013 |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission File Number: 001-35198

Pandora Media, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

94-3352630 (I.R.S. Employer Identification No.) |

|

2101 Webster Street, Suite 1650 Oakland, CA (Address of principal executive offices) |

94612 (Zip Code) |

(510) 451-4100

(Registrant's telephone number, including area code)

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common stock, $0.0001 par value | The New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by a check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the voting common stock held by non-affiliates of the registrant as of July 31, 2012(the last business day of the registrant's most recently completed second quarter), based on the closing price of such stock on The New York Stock Exchange on such date was approximately $725 million. This calculation excludes the shares of common stock held by executive officers, directors and stockholders whose ownership exceeds 5% outstanding at July 31, 2012. This calculation does not reflect a determination that such persons are affiliates for any other purposes.

On March 13, 2013 the registrant had 172,896,461 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Definitive Proxy Statement relating to its 2013 annual meeting of stockholders, to be filed subsequent to the date hereof, are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated. Such Definitive Proxy Statement will be filed with the Securities and Exchange Commission not later than 120 days after the conclusion of the registrant's fiscal year ended January 31, 2013. Except with respect to information specifically incorporated by reference in this Annual Report on Form 10-K, the Definitive Proxy Statement is not deemed to be filed as part of this Annual Report on Form 10-K.

PANDORA MEDIA, INC.

FORM 10-K

TABLE OF CONTENTS

1

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS AND INDUSTRY DATA

This Annual Report on Form 10-K contains "forward-looking statements" that involve substantial risks and uncertainties. The statements contained in this Annual Report on Form 10-K that are not purely historical are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), including, but not limited to, statements regarding our expectations, beliefs, intentions, strategies, future operations, future financial position, future revenue, projected expenses and plans and objectives of management. In some cases, you can identify forward-looking statements by terms such as "anticipate," "believe," "estimate," "expect," "intend," "may," "might," "plan," "project," "will," "would," "should," "could," "can," "predict," "potential," "continue," "objective," or the negative of these terms, and similar expressions intended to identify forward-looking statements. However, not all forward-looking statements contain these identifying words. These forward-looking statements reflect our current views about future events and involve known risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievement to be materially different from those expressed or implied by the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those identified below, and those discussed in the section titled "Risk Factors" included in this Annual Report on Form 10-K. Furthermore, such forward-looking statements speak only as of the date of this report. Except as required by law, we undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date of such statements. We qualify all of our forward-looking statements by these cautionary statements. In addition, the industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors including those described in the section entitled "Risk Factors." These and other factors could cause our results to differ materially from those expressed in this Annual Report on Form 10-K.

Some of the industry and market data contained in this Annual Report on Form 10-K are based on independent industry publications, including those generated by Triton Digital Media or "Triton" and International Data Corporation or "IDC" or other publicly available information. This information involves a number of assumptions and limitations. Although we believe that each source is reliable as of its respective date, we have not independently verified the accuracy or completeness of this information.

As used herein, "Pandora," the "Company," "we," "our," and similar terms refer to Pandora Media, Inc., unless the context indicates otherwise.

"Pandora" and other trademarks of ours appearing in this report are our property. This report contains additional trade names and trademarks of other companies. We do not intend our use or display of other companies' trade names or trademarks to imply an endorsement or sponsorship of us by such companies, or any relationship with any of these companies.

Overview

Pandora is the leader in internet radio in the United States, offering a personalized experience for each of our listeners. We have pioneered a new form of radio—one that uses intrinsic qualities of music to initially create stations and then adapts playlists in real-time based on the individual feedback of each listener. As of January 31, 2013, we had approximately 175 million registered users, which we define as the total number of accounts that have been created for our service at period end. As of January 31, 2013 approximately 140 million registered users have accessed Pandora through smartphones and tablets. For the fiscal year ended January 31, 2013, we streamed 14.01 billion hours of radio and as of January 31, 2013, we had 65.6 million active users during the prior 30 day period. According to a December 2012 report by Triton, we have more than a 70% share of internet radio

2

among the top 20 stations and networks in the United States. Since we launched our free, advertising-supported radio service in 2005 our listeners have created over 4.0 billion stations.

In June 2012, we entered into or activated agreements which allow Pandora to launch in New Zealand, Australia and the territories associated with the two countries. The arrangements with PPNZ Music Licensing Limited, which represents recording artists and record companies, and APRA/AMCOS, which represents songwriters, composers and publishers, have not had a material effect on our results of operations to date.

Our Service

Unlike traditional radio stations that broadcast the same content at the same time to all of their listeners, we enable each of our listeners to create up to 100 personalized stations. The Music Genome Project and our playlist generating algorithms power our ability to predict listener music preferences, play music content suited to the tastes of each individual listener and introduce listeners to music they will love. When a listener enters a single song, artist or genre to start a station—a process we call seeding—the Pandora service instantly generates a station that plays music we think that listener will enjoy. Based on listener reactions to the songs we pick, we further tailor the station to match the listener's preferences.

We currently provide the Pandora service through two models:

- •

- Free Service. Our free service is advertising-based and

allows listeners access to our music and comedy catalogs and personalized playlist generating system for free across all of our delivery platforms. In September 2011, we effectively eliminated the

40 hour per month listening cap on desktop and laptop computers by increasing the cap to 320 hours of listening per month, which almost none of our listeners exceed. We have the right to

assess a $0.99 fee to listeners who exceed the new cap, but this has not generated, and is not expected to generate any meaningful revenue. In fiscal years 2010, 2011 and 2012 listeners on other

platforms had access to unlimited hours of free music and comedy. Starting in March 2013, we instituted a 40 hour per month listening cap on mobile and other connected devices. Listeners who

reach this limit may continue to use our ad supported service on these devices by paying $0.99 for the remainder of the month, may listen to our ad supported service on their desktop or laptop

computers, or may purchase annual or monthly Pandora One subscriptions for $36 per year or approximately $4 per month, respectively.

- •

- Pandora One. Pandora One currently eliminates all external advertising from any device used to access our service. Pandora One allows unlimited listening time and provides access to higher quality 192 kbps audio on supported devices. In fiscal years 2011, 2012 and 2013, subscription services and other revenue accounted for approximately 13%, 13% and 12%, respectively, of our total revenue.

Beyond song delivery, listeners can discover more about the music they hear by researching song lyrics, reading the history of their favorite artists, viewing artist photos and buying albums and songs from Amazon or iTunes. Our service also incorporates community social networking features. Listeners can create and customize personal listener profile pages to connect with other listeners. Our music feed feature enables a real-time, centralized stream for listeners to view the music that their social connections are experiencing and to provide and receive recommendations for songs, albums and artists. Listeners can also share their stations across other social media outlets and through email by using our share feature or by distributing our individualized station URLs. In addition, our website is integrated with Facebook's instant personalization capability, allowing our listeners to share their stations and music preferences with their Facebook friends and enabling us to make additional music recommendations. In October 2012, we announced the redesign of our mobile listener interface,

3

Pandora 4.0, on both IOS and Android smartphones which included expanding listening functionality, artist pages, personal music profiles and sharing capabilities.

Distribution and Partnerships

One key element of our strategy is to make the Pandora service available everywhere that there is internet connectivity. To this end, we make the Pandora service available through a variety of distribution channels. In addition to streaming our service to traditional computers, we have developed Pandora mobile device applications or "apps" for smartphones such as Android, Blackberry and the iPhone, and for tablets including the iPad, Android tablets, and Amazon Kindle Fire tablets. We distribute those mobile apps free to listeners via app stores. Pandora is now available on more than 1,000 integrations, including automobiles, automotive aftermarket devices and consumer electronic devices. In the consumer electronics space, more than 760 consumer electronics devices from third-party distribution partners such as Samsung, Roku and DirecTV make Pandora available in the home. Many automotive partners, including Alpine Electronics, Audiovox, Clarion, JVC, Kenwood, Pioneer Sony, incorporate our application into aftermarket radios. We have also developed relationships with major automobile manufacturers and are currently available on vehicle models sold by Acura, BMW, Buick, Cadillac, Chevrolet, Ford, GMC, Honda, Hyundai, Lexus, Lincoln, Mazda, Mercedes-Benz, MINI, Nissan, Scion, Suzuki and Toyota. Additionally, Chrysler, Infiniti and Kia have publicly announced their plans to offer Pandora integration on future vehicles. Holden Ltd., a subsidiary of General Motors, has also launched the first in-car system in Australia to offer full compatibility with Pandora. Under the arrangements, we receive no financial compensation and recognize no revenue from these automotive distribution partners.

Advertising

We generate revenue primarily from advertising. In fiscal 2011, 2012 and 2013, advertising revenue accounted for approximately 87%, 87% and 88% of our total revenue, respectively, and we expect that advertising will comprise a substantial majority of revenue for the foreseeable future.

We offer a comprehensive suite of display, audio and video advertising products across our traditional computer, mobile and connected device platforms. Our advertising products allow both national and local advertisers to target and connect with listeners based on attributes including age, gender, zip code and content preferences, and we provide analytics for our advertisers detailing campaign performance.

- •

- Display Advertising. Our display products offer

advertisers opportunities to maximize exposure to our listeners through our desktop and mobile service interfaces, which are divided between our tuner containing our player and "now playing"

information, and the information space surrounding our tuner. Our display ads include industry standard banner ads of various sizes and placements depending on platform and listener interaction.

- •

- Audio Advertising. Our audio advertising products allow

custom audio messages to be delivered between songs during short ad interludes. Audio ads are available across all of our delivery platforms. On supported platforms, the audio ads can be accompanied

by display ads to further enhance advertisers' messages.

- •

- Video Advertising. Our video advertising products allow delivery of rich branded messages to further engage listeners through in-banner click-initiated videos, videos that automatically play when a listener changes stations or skips a song and opt-in videos that pause the music and cover the tuner.

Our advertising strategy focuses on developing our core suite of display, audio and video advertising products and marketing these products to advertisers for delivery across traditional

4

computer, mobile and other connected device platforms such as automobiles and consumer electronics. We believe that our ability to run multi-platform ad campaigns enables advertisers to deliver their advertising messages to listeners anytime and anywhere they enjoy music and comedy, providing a unique advertising opportunity that is central to our achieving and sustaining profitability. As listenership on our mobile platforms has grown more rapidly than on our other platforms, we have sought to improve our advertising products for the mobile environment to better enable us to develop and market multi-platform advertising solutions. For example, our introduction of audio ads was driven by the growth of mobile listenership. In addition, our banner advertising products for display on mobile devices include standard banner ads displayed on the Pandora app "now-playing" screen, "welcome" screen banners which are the first to display upon launch of the app, and other multi-functional banners of different shapes and sizes. Further, advertisers can create "drag-and-drop" stations where listeners select among branded icons and drag and drop the selected icon to automatically launch a station. We have also incorporated rich media touch screen initiated functionality, or "tap-to" technology, to enhance connections between our mobile listeners and advertisers. "Tap-to" technology allows mobile listeners to expand banner ads, launch videos, receive advertiser emails, dial advertiser phone numbers, download applications and access links to advertiser websites, offering increased listener and advertiser engagement.

Our display, audio and video advertising products can be designed and modified by us and advertisers to create advertising campaigns tailored across all of our high volume delivery platforms to fit specific advertiser needs. For example, our advertisers can create custom "branded" stations from our music library that can be accessed by our listeners, as well as engage listeners by allowing them to personalize the branded stations through listener-controlled variables.

Sales and Marketing

We organize our sales force into multiple teams that are each focused on selling advertising across our traditional computer, mobile and other connected device platforms. Teams are located in our Oakland, California headquarters, in regional sales offices in Chicago, Illinois; Santa Monica, California; and New York, New York and local sales offices throughout the country.

Our marketing team is charged with amplifying Pandora's brand message to grow awareness and drive listening hours. We organize the marketing team into three groups focused on communications, marketing analytics, and brand marketing.

Our Technologies

Music Genome Project

The Music Genome Project is the foundation of our personalized playlist generating system and has been built by our music analysts to select songs tailored to an individual's music tastes. The Music Genome Project database was developed one song at a time, by evaluating and cataloging each song's particular attributes. Our music catalog currently consists of over 1,000,000 uniquely analyzed songs from over 100,000 artists, spanning over 500 genres and sub-genres ranging from classical, jazz, rock, pop and hip hop to post punk, Celtic and flamenco. Our musical catalog includes both well-known and little-known music and incorporates listener suggestions and independent submissions. Music is assessed on the basis of value to our catalog and we do not accept money or any form of consideration from artists or their representatives for inclusion in the Music Genome Project.

Once we select music to become part of our catalog, our music analysts genotype it by examining up to 450 attributes including objectively observable metrics such as tone and tempo, as well as subjective characteristics, such as lyrics, vocal texture and emotional intensity. We employ rigorous hiring and training standards for selecting our music analysts, who typically have four-year degrees in

5

music theory, composition or performance, and we provide them with intensive training in the Music Genome Project's precise methodology.

Comedy Genome Project

Our Comedy Genome Project leverages similar technology to the technology underlying the Music Genome Project, allowing a listener to choose a favorite comedian or a genre as a seed to start a station and then give feedback to personalize that station. Our comedy collection includes content from more than 1,500 comedians with more than 20,000 tracks.

Our Other Core Innovations

In addition to the Music Genome Project, we have developed other proprietary technologies to improve delivery of the Pandora service, enhance the listener experience and expand our reach. Our other core innovations include:

Playlist Generating Algorithms. We have developed complex algorithms that determine which songs play and in what order on each personalized station. Developed since 2004, these algorithms combine the Music Genome Project with the individual and collective feedback we receive from our listeners in order to deliver a personalized listening experience.

Pandora User Experience. We have invested in ways to enable our listeners to play music they love as quickly as possible. To this end, we have developed a number of innovative approaches, including our autocomplete station creation feature, which predicts and generates a list of the most likely musical starting points as a listener begins to enter a favorite station, song or artist.

Pandora Streaming Network. We have developed our own infrastructure for streaming music content to a diverse network of devices and destinations. Our streaming network is hosted from Pandora owned and operated infrastructure in data centers across the country. This network has allowed us to deliver a high quality streaming experience to a broad collection of devices at significant cost savings relative to outsourced third-party solutions.

Pandora Mobile Streaming. We have designed a sophisticated system for streaming music content to mobile devices. This system involves a combination of music coding programs that are optimized for mobile devices as well as algorithms designed to address the intricacies of reliable delivery over diverse mobile network technologies. For example, these algorithms are designed to maintain a continuous stream to a listener even in circumstances where the mobile data network may be unreliable.

Automotive Protocol. We have developed an automotive protocol to facilitate increased availability of the Pandora service in automobiles. Through the automotive protocol, automobile manufacturers, their suppliers and makers of aftermarket audio systems can easily connect dash-mounted interface elements to the Pandora app running on a smartphone. This allows us to deliver the Pandora service to listeners via their existing smartphone, while leveraging the automobile itself for application command, display and control functionalities.

Pandora API. As part of our effort to make the Pandora service available everywhere our listeners want it, we have developed an application programming interface, which we call the Pandora API. Through our partnerships with manufacturers of consumer electronics products, we have used this technology to bring the Pandora experience to connected devices throughout the home.

6

Competition

Competition for Listeners

We compete for the time and attention of our listeners with other content providers on the basis of a number of factors, including quality of experience, relevance, acceptance and diversity of content, ease of use, price, accessibility, perceptions of ad load, brand awareness and reputation. We also compete for listeners on the basis of our presence and visibility as compared with other providers that deliver content through the internet, mobile devices and consumer products. We believe that we compete favorably on these factors. For additional details on risks related to competition for listeners, please refer to the section entitled "Risk Factors."

We offer our service at no cost or through a low cost subscription plan through web, mobile and consumer electronic platforms however, many of our current and potential future competitors enjoy substantial competitive advantages, such as greater name recognition, longer operating histories and larger marketing budgets, as well as substantially greater financial, technical and other resources.

Our competitors include:

Other Radio Providers. We compete for listeners with broadcast radio providers, including terrestrial radio providers such as Clear Channel and CBS and satellite radio providers such as Sirius XM. Many broadcast radio companies own large numbers of radio stations or other media properties. Many terrestrial radio stations have begun broadcasting digital signals, which provide high quality audio transmission. In addition, unlike participants in the emerging internet radio market, terrestrial and satellite radio providers, as aggregate entities of their subsidiary providers, generally enjoy larger established audiences and longer operating histories. Broadcast and satellite radio companies enjoy a significant cost advantage because they pay a much lower percentage of revenue for transmissions of sound recordings. Broadcast radio pays no royalties for its terrestrial use of sound recordings, and satellite radio pays only 9% of revenue for its satellite transmissions of sound recordings. By contrast, Pandora incurred content acquisition costs representing 55.9% of revenue for our internet transmissions of sound recordings during the fiscal year ending January 31, 2013. We also compete directly with other emerging non-interactive online radio providers such as CBS's Last.fm, Clear Channel's iheartradio and Slacker Personal Radio. We could face additional competition if known incumbents in the digital media space choose to enter the internet radio market.

Other Audio Entertainment Providers. We face competition from providers of interactive on-demand audio content and pre-recorded entertainment, such as Apple's iTunes Music Store, RDIO, Rhapsody, Spotify, and Amazon that allow listeners to select the audio content that they stream or purchase. This interactive on-demand content, is accessible in automobiles and homes, using portable players, mobile phones and other wireless devices. The audio entertainment marketplace continues to rapidly evolve, providing our listeners with a growing number of alternatives and new media platforms.

Other Forms of Media. We compete for the time and attention of our listeners with providers of other forms of in-home and mobile entertainment. To the extent existing or potential listeners choose to watch cable television, stream video from on-demand services such as Hulu, VEVO or YouTube or play interactive video games on their home-entertainment system, computer or mobile phone rather than listen to the Pandora service, these content services pose a competitive threat.

Competition for Advertisers

We compete with other content providers for a share of our advertising customers' overall marketing budgets. We compete on the basis of a number of factors, including perceived return on investment, effectiveness and relevance of our advertising products, pricing structure and ability to deliver large volumes or precise types of ads to targeted demographics. We believe that our ability to

7

deliver targeted and relevant ads across a wide range of platforms allows us to compete favorably on the basis of these factors and justify a long-term profitable pricing structure. However, the market for online advertising solutions is intensely competitive and rapidly changing, and with the introduction of new technologies and market entrants, we expect competition to intensify in the future. For additional details on risks related to competition for advertisers, please refer to the section entitled "Risk Factors."

Our competitors include:

Other Internet Companies. The market for online advertising is becoming increasingly competitive as advertisers are allocating increasing amounts of their overall marketing budgets to web-based advertising. We compete for online advertisers with other internet companies, including major internet portals, search engine companies and social media sites. Large internet companies with greater brand recognition, such as Facebook, Google, MSN and Yahoo! have large direct sales staffs, substantial proprietary advertising technology and extensive web traffic and consequently enjoy significant competitive advantages.

Broadcast Radio. Terrestrial broadcast and to a lesser extent satellite radio are significant sources of competition for advertising dollars. These radio providers deliver ads across platforms that are more familiar to traditional advertisers than the internet might be. Advertisers may be reluctant to migrate advertising dollars to our internet-based platform.

Other Traditional Media Providers. We compete for advertising dollars with other traditional media companies in television and print, such as ABC, CBS, FOX and NBC, cable television channel providers, national newspapers such as The New York Times and the Wall Street Journal and some regional newspapers. These traditional outlets present us with a number of competitive challenges in attracting advertisers, including large established audiences, longer operating histories, greater brand recognition and a growing presence on the internet.

Content, Copyrights and Royalties

To secure the rights to stream music content over the internet, we must obtain licenses from, and pay royalties to, copyright owners of both sound recordings and musical compositions. These royalty and licensing arrangements strongly influence our business operations. We stream spoken word comedy content, for which the underlying literary works are not currently entitled to eligibility for licensing by any performing rights organization for the United States. Rather, pursuant to industry-wide custom and practice, this content is performed absent a specific license from any such performing rights organization. We do, however, obtain licenses to stream the sound recordings of comedy content under federal statutory licenses as more fully described under the section captioned "Sound Recordings" below, which in some instances we have opted to augment with direct agreements with the licensors of such sound recordings.

Sound Recordings

Our largest royalty expense arises from our use of sound recordings. We obtain performance rights licenses and pay performance rights royalties to the copyright owners of sound recordings, typically performing artists and recording companies, pursuant to the Digital Millennium Copyright Act of 1998, (the "DMCA"). Under federal statutory licenses created by the Digital Performance Right in Sound Recordings Act of 1995, (the "DPRA"), and DMCA, we are permitted to stream any lawfully released sound recordings and to make reproductions of these recordings on our computer servers, without having to separately negotiate and obtain direct licenses with each individual copyright owner. These statutory licenses are granted to us on the condition that we operate in compliance with the rules of statutory licenses and pay the applicable royalty rates to SoundExchange, the non-profit organization

8

designated by the Copyright Royalty Board, or CRB, to collect and distribute royalties under these statutory licenses. We believe we are not an "interactive service" as defined in the U.S. Copyright Act of 1976 (the "U.S. Copyright Act"). As a non-interactive service, we are not allowed to stream a particular song "on-demand" and are otherwise obliged to limit the ways in which we stream music to our listeners. As such we are required, among other things, to restrict the number of songs that are played on a particular station from a particular artist or album within certain time periods.

The rates we pay to SoundExchange for non-interactive streaming of sound recordings pursuant to these licenses are privately negotiated or set by the CRB. In 2007, the CRB set royalty rates for non-interactive, online streaming of music that were extremely high. In response to the lobbying efforts of internet webcasters, including Pandora, Congress passed the Webcaster Settlement Acts of 2008 and 2009, which permitted webcasters to negotiate alternative royalty rates directly with SoundExchange outside of the scope of the CRB process. In July 2009, certain webcasters reached a settlement agreement with SoundExchange establishing a royalty structure more favorable to us that by its terms will apply through 2015. This settlement agreement is commonly known as the "Pureplay Settlement." Once the rates and terms of the Pureplay Settlement came into effect in July 2009, any qualifying commercial webcaster could elect to avail itself of those rates and terms by filing an initial notice, followed by annual notices, of election with SoundExchange through 2015. In July 2009, we elected to be subject to the Pureplay Settlement and timely filed notices of election with SoundExchange for 2010, 2011, 2012 and 2013. We currently intend to continue to make such elections through 2015.

The table below sets forth the per performance rates for the calendar years 2012 to 2015 (1) as established by the CRB, which we have opted not to pay, (2) under the Pureplay Settlement applicable to our non-subscription, ad-supported service and (3) under the Pureplay Settlement applicable to our subscription service.

Year

|

CRB Rate | Pureplay Rate (non-subscription)* |

Pureplay Rate (subscription) |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

2012 |

$ | 0.00210 | $ | 0.00110 | $ | 0.00200 | ||||

2013 |

0.00210 | 0.00120 | 0.00220 | |||||||

2014 |

0.00230 | 0.00130 | 0.00230 | |||||||

2015 |

0.00230 | 0.00140 | 0.00250 | |||||||

- *

- The rate applicable to our non-subscription service is the greater of the per performance rates set forth in this column or 25% of our U.S. gross revenue.

As reflected in the table above, we currently pay per-performance rates for streaming of sound recordings via our Pandora One subscription service that are higher than the per-performance rates for our free, non-subscription service. As a result, we may incur higher royalty expenses to SoundExchange for a listener that subscribes to Pandora One as compared to a listener that uses our free, non-subscription service, even if both listeners listen for the same amount of time.

Proceedings to establish rates that will be applicable to our service after 2015, known as Webcasting IV proceedings, are expected to commence in January 2014. While we did not participate in the prior proceedings to establish royalty rates for non-interactive webcasting services, we currently expect to participate in the Webcasting IV proceedings. At that time, webcasters, including us, will have the opportunity to enter into voluntary settlement negotiations with SoundExchange, and failing that, will participate in formal hearings before the CRB to establish rates.

We believe that our participation in the Webcasting IV proceedings as a mature player in an industry that will have evolved significantly since the prior proceedings may enhance our ability to negotiate rates on economically favorable terms. However, if we are unable to successfully negotiate rates for the 2016-2020 period, we will be forced to litigate those rates before the CRB. Any such litigation would be costly, and the outcome of such litigation would be uncertain. If the Webcasting IV

9

proceedings establish rates applicable to us that represent incremental increases in the per performance rates set forth as "CRB Rates" in the table above for the 2016-2020 period and there is no percentage of revenue option available to us, then our content acquisition costs could substantially increase, which could materially and adversely affect our operating results. For additional details on risks related to the rate-setting process, please refer to the section entitled "Risk Factors." We are unable to estimate the direct and indirect costs of participating in the Webcaster IV proceedings, but we expect those costs to be significant.

The existing laws and regulations governing performance royalties applicable to commercial webcasters are subject to change. For example, there is no guarantee that the royalty structure that emerged from the Pureplay Settlement will be available upon its expiration. In addition, performers and owners of sound recordings are seeking compensation for the public performance of sound recordings from terrestrial broadcasters who are not currently required to pay royalties for non-subscription broadcast transmissions. If these performers and owners are successful, terrestrial radio broadcasters will, for the first time, be subject to payment of sound recording performance royalties, a development that could potentially have a positive impact on our ability to compete with terrestrial radio broadcasters. Further, the Copyright Office has issued a report with respect to whether sound recordings released in the United States prior to January 1972 (the time at which federal copyright protection was first afforded to sound recordings), should be covered under federal copyright law. The report recommended that federal copyright protection should apply to sound recordings fixed before February 15, 1972. It proposed special provisions to address issues such as copyright ownership, term of protection, termination of transfers and copyright registration. We do not expect any potential resulting legislation to have a material impact on our business, financial condition or results of operations. We are not aware of any other proposed or pending changes to laws and regulations relating to performance royalties applicable to commercial webcasters such as us.

Musical Works

We also incur royalty expenses from our use of musical works embodied in sound recordings, with respect to which we must obtain public performance licenses and pay performance rights royalties to copyright owners of those musical works (typically, songwriters and music publishers) or their agents. Copyright owners of musical works most often rely on intermediaries known as performance rights organizations to negotiate so-called "blanket" licenses with copyright users, collect royalties under such licenses and distribute them to copyright owners. We have obtained public performance licenses from, and pay license fees to, the three major performance rights organizations in the United States: the American Society of Composers, Authors and Publishers, or ASCAP, Broadcast Music, Inc., or BMI and SESAC, Inc., or SESAC.

We currently operate under a final agreement with SESAC, which automatically renews yearly, but is subject to termination by either party in accordance with its terms at the end of each yearly term. The SESAC rate is subject to small annual increases. There is no guarantee that the license and associated royalty rate available to us now with respect to SESAC will be available to us in the future.

In 2012, we elected to terminate our prior agreement with BMI effective as of December 31, 2012 because we believed the royalty rates sought by BMI were excessive. Notwithstanding our termination of this BMI agreement, the musical works administered by BMI are licensed to us pursuant to the provisions of a consent decree which BMI entered into with the U.S. Department of Justice. Rates to be paid to BMI can be set, in the absence of a negotiated agreement, by the rate court established pursuant to such consent decree in the U.S. District Court for the Southern District of New York. The rates to be paid to BMI may be adjusted retroactively, either by mutual agreement or order of the rate court.

10

In 2010, we elected to terminate our prior agreement with ASCAP as of December 31, 2010 because we believed that the royalty rates sought by ASCAP were excessive. Notwithstanding our termination of this ASCAP agreement, the musical works administered by ASCAP are licensed to us pursuant to the provisions of a consent decree which ASCAP entered into with the U.S. Department of Justice. Rates to be paid to ASCAP can be set, in the absence of a negotiated settlement, by the rate court established pursuant to such consent decree in the U.S. District Court for the Southern District of New York. In September 2011, we changed the method we used to calculate royalties due to ASCAP following the execution of an interim arrangement for the period commencing January 1, 2011, pending a final determination of new rates. The rates to be paid to ASCAP may be adjusted retroactively, either by mutual agreement or order of the rate court. In November 2012, we filed a petition in the rate court to determine final, reasonable rates and terms with ASCAP. Rate court proceedings could take years to complete, could be very costly, and there are no guarantees that the rate court will establish royalty rates more favorable to us than those we previously paid pursuant to our terminated agreement with ASCAP or those we pay pursuant to our interim arrangement with ASCAP.

We also obtain licenses directly from music publishers. In May 2011, EMI Music Publishing, or EMI, announced its decision to withdraw from ASCAP certain portions of its musical works catalog that ASCAP had been administering on its behalf. As a result, ASCAP may no longer be able to license those musical works, and new media licensees, such as Pandora, who were previously able to secure licenses from ASCAP for those musical works, may now have to enter into direct licensing arrangements with EMI. In March 2012, we entered into a licensing agreement with EMI covering the public performance of the EMI musical works purportedly withdrawn from the ASCAP repertory.

In late 2012, Sony ATV Music Publishing or Sony ATV, which led a consortium in the acquisition of EMI in June 2012, announced its intention to withdraw from ASCAP and BMI certain portions of its musical works catalog that ASCAP and BMI had been administering on its behalf. As a result, ASCAP and BMI may no longer be able to license those musical works, and new media licensees, such as Pandora, who were previously able to secure licenses from ASCAP and BMI for those musical works, may now have to enter into direct licensing arrangements with Sony ATV. In January 2013, we entered into a licensing agreement with Sony ATV and EMI covering the public performance of the works purportedly withdrawn from ASCAP and BMI.

Other music publishers have signaled their intent to withdraw from ASCAP and BMI all or a portion of the musical works catalogs that ASCAP and BMI administer on their behalf. It is unclear whether other music publishers will be able to withdraw their catalogs from ASCAP or BMI and, if so, what specific effect those withdrawals will have on us.

Non-U.S. Licensing Regimes

In addition to the copyright and licensing arrangements described above for our use of sound recordings and musical compositions in the United States, other countries have various copyright and licensing regimes, including in some cases performance-rights organizations and copyright collection societies from which licenses must be obtained. We have obtained licenses to operate in Australia and New Zealand for the communication of sound recordings and the musical compositions embodied in those sound recordings. As yet, we have not identified economically suitable licensing arrangements in other countries.

Government Regulation

As a company conducting business on the internet, we are subject to a number of foreign and domestic laws and regulations relating to consumer protection, information security, data protection and privacy, among other things. Many of these laws and regulations are still evolving and could be interpreted in ways that could harm our business. In the area of information security and data

11

protection, the laws in several states require companies to implement specific information security controls to protect certain types of information. Likewise, all but a few states have laws in place requiring companies to notify users if there is a security breach that compromises certain categories of their information. Any failure on our part to comply with these laws may subject us to significant liabilities.

We are also subject to federal and state laws regarding privacy of listener data. Our privacy policy and terms of use describe our practices concerning the use, transmission and disclosure of listener information and are posted on our website. Any failure to comply with our posted privacy policy or privacy-related laws and regulations could result in proceedings against us by governmental authorities or others, which could harm our business. Further, any failure by us to adequately protect the privacy or security of our listeners' information could result in a loss of confidence in our service among existing and potential listeners, and ultimately, in a loss of listeners and advertising customers, which could adversely affect our business.

Intellectual Property

Our success depends upon our ability to protect our technologies and intellectual property. To accomplish this, we rely on a combination of intellectual property rights, including trade secrets, patents, copyrights, trademarks, contractual restrictions, technological measures and other methods. We enter into confidentiality and proprietary rights agreements with our employees, consultants and business partners, and we control access to and distribution of our proprietary information.

We have three patents that have been issued in the United States and we continue to pursue additional patent protection, both in the United States and abroad where appropriate and cost effective.

Our registered trademarks in the United States include "Pandora," the "Music Genome Project," and "QUICKMIX," in addition to a number of Pandora logos. "Pandora" is also registered in Australia, Canada, Chile, the European Union, Israel, Korea, Mexico, New Zealand, Switzerland, and other countries. "Music Genome Project" is also registered in Australia, China, and New Zealand. "QUICKMIX" is also registered in China. We have pending trademark applications in the United States and in certain other countries, including applications for Pandora logos.

We are the registrant of the internet domain name for our website, pandora.com, as well as pandora.co.in, pandora.co.uk, pandora.co.nz and pandora.de, among others. We own rights to proprietary processes and trade secrets, including those underlying the Pandora service.

In addition to the foregoing protections, we generally control access to and use of our proprietary software and other confidential information through the use of internal and external controls, including contractual protections with employees, contractors, customers and partners.

Customer Concentration

No single customer accounted for 10% or more of our total revenues in fiscal 2011, 2012 or 2013.

Seasonality

Our results may reflect the effects of some seasonal trends in listener behavior due to increased internet usage and sales of media-streaming devices during certain vacation and holiday periods. For example, we expect to experience increased usage during the fourth quarter of each calendar year due to the holiday season, and in the first quarter of each calendar year due to increased use of media-streaming devices received as gifts during the holiday season. We may also experience higher advertising sales during the fourth quarter of each calendar year due to greater advertiser demand during the holiday season and lower advertising sales in the first quarter of the following year due to

12

reduced advertiser demand. See the section entitled "Quarterly Trends" in Item 7 of this Annual Report on Form 10-K for a more complete description of the seasonality of our financial results.

Employees

As of January 31, 2013, we had approximately 740 employees. None of our employees are covered by collective bargaining agreements, and we consider our relations with our employees to be good.

Corporate and Available Information

We were incorporated as a California corporation in January 2000 and reincorporated as a Delaware corporation in December 2010. Our principal executive offices are located at 2101 Webster Street, Suite 1650, Oakland, California 94612 and our telephone number is (510) 451-4100. Our website is located at www.pandora.com and our Investor Relations website is located at investor.pandora.com.

We have a January 31 fiscal year end. Accordingly, in this Annual Report on Form 10-K, all references to a fiscal year refer to the 12 months ended January 31 of such year, and references to the first, second, third and fourth fiscal quarters refer to the three months ended April 30, July 31, October 31 and January 31, respectively.

We file reports with the Securities and Exchange Commission ("SEC"), including Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any other filings required by the SEC. We make available on our Investor Relations website, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to those reports, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The information on our website is not incorporated by reference into this Annual Report on Form 10-K or in any other report or document we file with the SEC.

The public may read and copy any materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site (http://www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

The risks and uncertainties set forth below, as well as other factors described elsewhere in this Annual Report on Form 10-K or in other filings by the Company with the SEC, could adversely affect the Company's business, financial condition, results of operations and the trading price of our common stock. Additional risks and uncertainties that are not currently known to the Company or that are not currently believed by the Company to be material may also harm the Company's business operations and financial results. Because of the following factors, as well as other factors affecting the Company's financial condition and operating results, past financial performance should not be considered to be a reliable indicator of future performance, and investors should not use historical trends to anticipate results or trends in future periods.

Risks Related to Our Business

Internet radio is an emerging market, which makes it difficult to evaluate our current business and future prospects.

Internet radio is an emerging market and our current business and future prospects are difficult to evaluate. The market for internet radio has undergone rapid and dramatic changes in its relatively short history and is subject to significant challenges. As a result, the future revenue and income

13

potential of our business is uncertain. You should consider our business and prospects in light of the risks and difficulties we encounter in this new and rapidly evolving market, which risks and difficulties include, among others:

- •

- our relatively new, evolving and unproven business model;

- •

- our ability to retain our current listenership, build our listener base and increase listener hours;

- •

- our ability to effectively monetize listener hours, particularly with respect to listener hours on mobile devices, by

growing our sales of advertising inventory created from growing listener hours and developing compelling ad product solutions that successfully deliver advertisers' messages across the range of our

delivery platforms while maintaining our listener experience in continually evolving markets;

- •

- our ability to attract new advertisers, retain existing advertisers and prove to advertisers that our advertising platform

is effective enough to justify a pricing structure that is profitable for us;

- •

- our ability to maintain relationships with makers of mobile devices, consumer electronic products and automobiles; and

- •

- our operation under an evolving music industry licensing structure including statutory and compulsory licenses that may change or cease to exist, which in turn may result in a significant increase in our operating expenses.

Failure to successfully address these risks and difficulties, and other challenges associated with operating in a new and emerging market, could inhibit the implementation of our business plan, significantly harm our financial condition, operating results and liquidity and prevent us from achieving or sustaining profitability.

We have incurred significant operating losses in the past and may not be able to generate sufficient revenue to be profitable.

Since our inception in 2000, we have incurred significant net operating losses and, as of January 31, 2013, we had an accumulated deficit of $139.6 million. A key element of our strategy is to increase the number of listeners and listener hours to increase our market penetration, including the number of listener hours on mobile and other connected devices, such as automobiles and consumer electronics. However, as our number of listener hours increases, the royalties we pay for content acquisition also increase. We have not in the past generated, and may not in the future generate, sufficient revenue from the sale of advertising and subscriptions to offset our expenses. While we have generated revenue from our advertising products at a rate that exceeds the growth in listener hours in certain fiscal years for traditional computers and for the fiscal year ending January 31, 2013 for mobile and other connected devices, to date we have not been able to grow our total advertising revenue at a rate that exceeds the growth in our listener hours. Part of the challenge that we face in increasing sales to monetize inventory generated by mobile devices is that radio advertising has traditionally attracted primarily local advertisers and we are still at an early stage of building our sales capability and penetrating local advertising markets. In addition, to the extent that our listener base on mobile platforms may skew to different demographics than we have historically sold on our traditional computer platform, we must identify such demographics and convince advertisers of the capabilities of mobile advertising to maximize advertising inventory utilization across our multi-platform ad campaigns.

If we cannot successfully earn revenue at a rate that exceeds the operational costs associated with increased listener hours, we may not be able to achieve or sustain profitability. In addition, we expect to invest heavily in our operations to support anticipated future growth. As a result of these factors, we expect to continue to incur annual losses on a U.S. GAAP basis in the near term.

14

Our revenue increased rapidly in each of the fiscal years ended January 31, 2007 through January 31, 2013; however, we expect our revenue growth rate to decline in the future as a result of a variety of factors, including increased competition and the maturation of our business, and we cannot assure you that our revenue will continue to grow or will not decline. You should not consider our historical revenue growth or operating expenses as indicative of our future performance. If our revenue growth rate declines or our operating expenses exceed our expectations, our financial performance will be adversely affected. Further, if our future growth and operating performance fail to meet investor or analyst expectations, it could have a materially negative effect on our stock price.

In addition, in our efforts to increase revenue as the number of listener hours has grown, we have expanded and expect to continue to expand our sales force. If our hiring of additional sales personnel does not result in a sufficient increase in revenue, the cost of this additional headcount will not be offset, which would harm our operating results and financial condition.

Our failure to convince advertisers of the benefits of our service in the future could harm our business.

For our fiscal year ended January 31, 2013 we derived 88% of our revenue from the sale of advertising and expect to continue to derive a substantial majority of our revenue from the sale of advertising in the future. Our ability to attract and retain advertisers, and ultimately to sell our advertising inventory to generate advertising revenue, depends on a number of factors, including:

- •

- increasing the number of listener hours;

- •

- keeping pace with changes in technology and our competitors;

- •

- competing effectively for advertising dollars from other online marketing and media companies;

- •

- penetrating the market for local radio advertising;

- •

- demonstrating the value of advertisements to reach targeted audiences across all of our delivery platforms, including the

value of mobile digital advertising;

- •

- continuing to develop and diversify our advertisement platform, which currently includes delivery of display, audio and

video advertising products through multiple delivery channels, including traditional computers, mobile and other connected devices, including automobiles; and

- •

- coping with ad blocking technologies that have been developed and are likely to continue to be developed that can block the display of our ads.

Our agreements with advertisers are generally short term or may be terminated at any time by the advertiser. Advertisers that are spending only a small amount of their overall advertising budget on our service may view advertising with us as experimental and unproven and may leave us for competing alternatives at any time. We may never succeed in capturing a greater share of our advertisers' core advertising spending, particularly if we are unable to achieve the scale and market penetration necessary to demonstrate the effectiveness of our advertising platforms, or if our advertising model proves ineffective or not competitive when compared to alternatives. Failure to demonstrate the value of our service would result in reduced spending by, or loss of, existing or potential future advertisers, which would materially harm our revenue and business.

Advertising on mobile devices, such as smartphones, is an emerging phenomenon, and if we are unable to increase revenue from our advertising products delivered to mobile devices, our results of operations will be materially adversely affected.

Our number of listener hours on mobile devices has surpassed listener hours on traditional computers, and we expect that this trend will continue. Our mobile listenership has experienced significant growth since we introduced the first mobile version of our service in May 2007. Listener

15

hours on mobile devices and other connected devices constituted approximately 5%, 26%, 54%, 69% and 77% of our total listener hours for fiscal years 2009, 2010, 2011, 2012 and 2013, respectively. We expect this growth to continue, though at a less rapid pace. Digital advertising on mobile devices is an emerging phenomenon, and the percentage of advertising spending allocated to digital advertising on mobile devices is lower than that allocated to traditional online advertising. According to IDC, the percentage of U.S. advertising spending allocated to advertising on mobile devices was less than 1% in 2010, compared to 13% for all online advertising. We must therefore convince advertisers of the capabilities of mobile digital advertising opportunities so that they migrate their advertising spend toward demographics and ad solutions that more effectively utilize mobile inventory. Our cost of content acquisition, or royalty fees for public performances is currently calculated on the same basis whether a listening hour is consumed on a traditional computer or a mobile device. To date, we have not been able to generate revenue from our advertising products delivered to mobile and other connected devices, such as automobiles and consumer electronics, as effectively as we have for our advertising products served on traditional computers.

Radio advertising has traditionally attracted primarily local advertisers, and we are still at an early stage of building our sales capability to penetrate local advertising markets, which we view as a key challenge in monetizing our listener hours, including listener hours on mobile and other connected devices. In addition, while a substantial amount of our revenue has traditionally been derived from display ads, some display ads may not be currently optimized for use on certain mobile or other connected devices. For example, standard display ads may not be well-suited for use on smartphones due to the size of the device screen and may not be appropriate for smartphones connected to or integrated in automobiles due to safety considerations. Further, some display ads may not be optimized to take advantage of the multimedia capabilities of connected devices. By contrast, audio ads are better-suited for delivery on smartphones connected to or installed in automobiles and across mobile and connected device platforms and video ads can be optimized for a variety of platforms. However, our audio and video advertising products are relatively new and have not been as widely accepted by advertisers as our traditional display ads. In addition, the introduction of audio advertising places us in more direct competition with terrestrial radio, as many advertisers that purchase audio ads focus their spending on terrestrial radio stations who traditionally have strong connections with local advertisers.

We have plans that, that if successfully implemented, would increase our number of listener hours on mobile and other connected devices, including efforts to expand the reach of our service by making it available on an increasing number of devices, such as smartphones and devices connected to or installed in automobiles. In order to effectively monetize such increased listener hours, we must, among other things, convince advertisers to migrate spending to nascent advertising markets, penetrate local advertising markets and develop compelling ad product solutions. We cannot assure you that we will be able to effectively monetize inventory generated by listeners using mobile and connected devices, or the time frame on which we may do so.

If our efforts to attract prospective listeners and to retain existing listeners are not successful, our growth prospects and revenue will be adversely affected.

Our ability to grow our business and generate advertising revenue depends on retaining and expanding our listener base and increasing listener hours. We must convince prospective listeners of the benefits of our service and existing listeners of the continuing value of our service. The more listener hours we stream, the more ad inventory we have to sell. Further, growth in our listener base increases the size of demographic pools targeted by advertisers, which improves our ability to deliver advertising in a manner that maximizes our advertising customers' return on investment and, ultimately, to demonstrate the effectiveness of our advertising solutions and justify a pricing structure that is profitable for us. If we fail to grow our listener base and listener hours, particularly in key

16

demographics such as young adults, we will be unable to grow advertising revenue, and our business will be materially and adversely affected.

Our ability to increase the number of our listeners and listener hours will depend on effectively addressing a number of challenges. We may fail to do so. Some of these challenges include:

- •

- providing listeners with a consistent high quality, user-friendly and personalized experience;

- •

- continuing to build our catalogs of music and comedy content that our listeners enjoy;

- •

- continuing to innovate and keep pace with changes in technology and our competitors; and

- •

- maintaining and building our relationships with makers of consumer products such as mobile devices, other consumer electronic products and automobiles to make our service available through their products.

In addition, we have historically relied heavily on the success of viral marketing to expand consumer awareness of our service. If we are unable to maintain or increase the efficacy of our viral marketing strategy, or if we otherwise decide to expand the reach of our marketing through use of more costly marketing campaigns, we may experience an increase in marketing expenses, which could have an adverse effect on our results of operations. We cannot assure you that we will be successful in maintaining or expanding our listener base and failure to do so would materially reduce our revenue and adversely affect our business, operating results and financial condition.

Further, although we use our number of registered users and our number of active users as indicators of our brand awareness and the growth of our business, the number of registered users and number of active users exceeds the number of unique individuals who register for, or actively use, our service. We define registered users as the total number of accounts that have been created for our service and we define active users as the number of distinct registered users that have requested audio from our servers within the trailing 30 days from the end of each calendar month. To establish an account, a person does not need to provide personally unique information. For this reason a person may have multiple accounts. If the number of actual listeners does not result in an increase in listener hours, then our business may not grow as quickly as we expect, which may harm our business, operating results and financial condition.

We have experienced rapid growth in both listener hours and advertising revenue. We do not expect to be able to sustain these growth rates in the future and our business and operating results may suffer.

We have experienced rapid growth rates in both listener hours and advertising revenue as a result of our growth strategy to commit substantial financial, operational and technical resources to build the Company. As we grow larger and increase our listener base and usage, we expect it will become increasingly difficult to maintain the rate of growth we currently experience. Slower growth could negatively impact our stock price, our ability to hire and retain employees or harm our business in other ways.

If we fail to effectively manage our growth, our business and operating results may suffer.

Our rapid growth has placed, and will continue to place, significant demands on our management and our operational and financial infrastructure. In order to attain and maintain profitability, we will need to recruit, integrate and retain skilled and experienced sales personnel who can demonstrate our value proposition to advertisers and increase the monetization of listener hours, particularly on mobile devices, by developing relationships with both national and local advertisers to convince them to migrate advertising spending to online and mobile digital advertising markets and utilize our advertising product solutions. Continued growth could also strain our ability to maintain reliable service levels for our listeners, effectively monetize our listener hours, develop and improve our operational, financial

17

and management controls, enhance our reporting systems and procedures and recruit, train and retain highly skilled personnel. If our systems do not evolve to meet the increased demands placed on us by an increasing number of advertisers, we may also be unable to meet our obligations under advertising agreements with respect to the timing of our delivery of advertising or other performance obligations. As our operations grow in size, scope and complexity, we will need to improve and upgrade our systems and infrastructure, which will require significant expenditures and allocation of valuable management resources. If we fail to maintain the necessary level of discipline and efficiency and allocate limited resources effectively in our organization as it grows, our business, operating results and financial condition may suffer.

We face and will continue to face competition for both listener hours and advertising spending.

We compete with other content providers for listener hours.

We compete for the time and attention of our listeners with other content providers on the basis of a number of factors, including quality of experience, relevance, acceptance and diversity of content, ease of use, price, accessibility, perception of ad load, brand awareness and reputation.

Many of our competitors may leverage their existing infrastructure, brand recognition and content collections to augment their services by offering competing internet radio features to provide listeners with more comprehensive music service delivery choices. We face increasing competition for listeners from a growing variety of businesses that deliver audio media content through mobile phones and other wireless devices.

Our competitors include terrestrial radio, satellite radio, and online radio. Terrestrial radio providers such as CBS and Clear Channel offer their content for free, are well-established and accessible to listeners and offer content, such as news, sports, traffic, weather and talk that we currently do not offer. In addition, many terrestrial radio stations have begun broadcasting digital signals, which provide high quality audio transmission.

Satellite radio providers, such as Sirius XM, may offer extensive and oftentimes exclusive news, comedy, sports and talk content, national signal coverage, and long established automobile integration. In addition, terrestrial radio pays no royalties for its use of sound recordings and satellite radio pays a much lower percentage of revenue, currently 9.0%, than internet radio providers for use of sound recordings, giving broadcast and satellite radio companies a significant cost advantage.

Other online radio providers may offer more extensive content libraries than we offer and some may be accessed internationally.

We also compete with providers of on-demand audio media and entertainment which are purchased or available for free and playable on mobile devices, automobiles and in the home. These forms of media may be purchased, downloaded and owned such as iTunes audio files, MP3s, CDs, or accessed from subscription or free online on-demand offerings by music providers such as RDIO, Spotify, and Rhapsody or content streams from other online services such as Hulu, VEVO, turntable fm and YouTube. We believe that companies with a combination of financial resources, technical expertise and digital media experience also pose a significant threat of developing competing internet radio and digital audio entertainment technologies in the future. In particular, if known incumbents in the digital media space such as Amazon, Apple, Facebook or Google choose to offer competing services, they may devote greater resources than we have available, have a more accelerated time frame for deployment and leverage their existing user base and proprietary technologies to provide products and services that our listeners and advertisers may view as superior. Our current and future competitors may have more well-established brand recognition, more established relationships with consumer product manufacturers, greater financial, technical, and other resources, more sophisticated technologies or more experience in the markets in which we compete.

18

We also compete for listeners on the basis of our presence and visibility as compared with other businesses and software that deliver audio and other content through the internet, mobile devices and consumer products. We face significant competition for listeners from companies promoting their own digital music and content online or through application stores, including several large, well-funded and seasoned participants in the digital media market. Search engines, such as Google, and mobile device application stores, such as the iTunes Store, rank responses to search queries based on the popularity of a website or mobile application, as well as other factors that are outside of our control. Additionally, mobile device application stores often offer users the ability to browse applications by various criteria, such as the number of downloads in a given time period, the length of time since a mobile app was released or updated, or the category in which the application is placed. The websites and mobile applications of our competitors may rank higher than our website and our Pandora app, and our app may be difficult to locate in mobile device application stores, which could draw potential listeners away from our service and toward those of our competitors. In addition, our competitors' products may be pre-loaded into consumer electronics products or automobiles, creating an initial visibility advantage. If we are unable to compete successfully for listeners against other digital media providers by maintaining and increasing our presence and visibility online, in application stores and in consumer electronics products and automobiles, our listener hours may fail to increase as expected or decline and our advertising sales may suffer.

To compete effectively, we must continue to invest significant resources in the development of our service to enhance the user experience of our listeners. There can be no assurance that we will be able to compete successfully for listeners in the future against existing or new competitors, and failure to do so could result in loss of existing or potential listeners, reduced revenue, increased marketing expenses or diminished brand strength, any of which could harm our business.

We compete for advertising spending with other content providers.

We compete for a share of advertisers' overall marketing budgets with other content providers on a variety of factors including perceived return on investment, effectiveness and relevance of our advertising products, pricing structure and ability to deliver large volumes or precise types of ads to targeted demographics.

We face significant competition for advertising dollars from terrestrial and, to a lesser extent, satellite radio providers. As many of the advertisers we target have traditionally advertised on terrestrial radio and have less experience with internet radio providers, they may be reluctant to spend for advertising on traditional computers, mobile or other connected device platforms. In addition, terrestrial radio providers as well as other traditional media companies in television and print, such as broadcast television networks such as ABC, CBS, FOX and NBC, cable television channel providers, national newspapers such as the New York Times and the Wall Street Journal and some regional newspapers, enjoy a number of competitive advantages over us in attracting advertisers, including large established audiences, longer operating histories, greater brand recognition and a growing presence on the internet.

Although advertisers are allocating an increasing amount of their overall marketing budgets to web and mobile-based ads, such spending lags behind growth in internet and mobile usage, and the market for online and mobile advertising is intensely competitive. As a result, we also compete for advertisers with a range of internet companies, including major internet portals, search engine companies and social media sites. Large internet companies with greater brand recognition, such as Facebook, Google, MSN and Yahoo! have significant numbers of direct sales personnel and substantial proprietary advertising inventory and web traffic that provide a significant competitive advantage and have a significant impact on pricing for internet advertising and web traffic. The trend toward consolidation among online marketing and media companies may also affect pricing and availability of advertising inventory.

19

In order to compete successfully for advertisers against new and existing competitors, we must continue to invest resources in developing and diversifying our advertisement platform, harnessing listener data and ultimately proving the effectiveness and relevance of our advertising products. Failure to compete successfully against our current or future competitors could result in loss of current or potential advertisers or a reduced share of our advertisers' overall marketing budget, which could adversely affect our pricing and margins, lower our revenue, increase our research and development and marketing expenses and prevent us from achieving or maintaining profitability.

Our ability to increase the number of our listeners will depend in part on our ability to establish and maintain relationships with automakers, automotive suppliers and consumer electronics manufacturers with products that integrate our service.