UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811‑21321

(Exact name of registrant as specified in charter)

60 State Street, Boston, MA 02109

(Address of principal executive offices) (ZIP code)

Christopher J. Kelley, Amundi Asset Management, Inc.,

60 State Street, Boston, MA 02109

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 742‑7825

Date of fiscal year end: April 30, 2024

Date of reporting period: May 1, 2023 through April 30, 2024

Form N‑CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e‑1 under the Investment Company Act of 1940 (17 CFR 270.30e‑1). The Commission may use the information provided on Form N‑CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N‑CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N‑CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORT TO STOCKHOLDERS.

Pioneer Municipal High Income Fund, Inc.

Annual Report | April 30, 2024

| Ticker Symbol: MHI |

Table of Contents

1Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

Portfolio Management Discussion | 4/30/24

In the following interview, John (Jake) Crosby van Roden III* and Prakash Vadlamani* discuss the factors that affected the performance of the Pioneer Municipal High Income Fund, Inc. during the 12-month period ended April 30, 2024. Mr. van Roden, Managing Director and Director of Municipals and a portfolio manager at Amundi Asset Management US, Inc. (“Amundi US”), and Mr. Vadlamani, Senior Vice President, Senior Credit Analyst and associate portfolio manager at Amundi US, are responsible for the day-to-day management of the Fund.

| Q | How did the Fund perform during the 12-month period ended April 30, 2024? |

| A | Pioneer Municipal High Income Fund, Inc. returned -0.02% at net asset value (NAV) and 0.95% at market price during the 12-month period ended April 30, 2024. During the same 12-month period, the Fund’s benchmarks, the Bloomberg US Municipal High Yield Bond Index and the Bloomberg Municipal Bond Index, returned 6.63% and 2.08% at NAV, respectively. The Bloomberg US Municipal High Yield Bond Index is an unmanaged measure of the performance of lower rated municipal bonds, while the Bloomberg Municipal Bond Index is an unmanaged measure of the performance of investment-grade municipal bonds. Unlike the Fund, the two indices do not use leverage. While the use of leverage increases investment opportunity, it also increases investment risk. |

| During the same 12-month period, the average return at NAV of the 24 closed end funds in Morningstar’s Closed End High Yield Municipal category (which may or may not be leveraged) was -0.62%, and the average return at market price of the closed-end funds within the same Morningstar category was 0.96%. | |

| The shares of the Fund were selling at a 12.83% discount to NAV on April 30, 2024. Comparatively, the shares of the Fund were selling at a 13.67% discount to NAV on April 30, 2023. On |

| * | Mr. van Roden and Mr. Vadlamani became portfolio managers of the Fund effective February 28, 2024. |

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/242

| April 30, 2024, the standardized 30-day SEC yield of the Fund’s shares was 2.93%**. | |

| Q | Which of your investment strategies or individual portfolio holdings contributed positively to performance during the 12-month period ended April 30, 2024? |

| A | In sector terms, the portfolio’s positioning in the education, Tobacco Master Settlement Agreement (MSA) and housing sectors contributed positively to the Fund’s relative returns during the 12-month period. |

| Individual holdings of Puerto Rico municipal securities, specifically general obligation debt contributed positively to the Fund’s benchmark-relative returns as strong investor demand drove spreads tighter. Additionally, the water and sewer sectors also, contributed positively to the Fund’s benchmark-relative returns. | |

| The reduction in the Fund’s total managed assets financed by leverage in February 2024 helped relative returns, as the income component of the Fund’s total return improved. In addition, the Fund was able to divest lower yielding securities during the deleveraging process. | |

| Q | Which investment strategies or individual portfolio holdings detracted from the Fund’s benchmark-relative performance results during the 12-month period ended April 30, 2024? |

| A | Interest expense relating to the Fund’s employment of leverage detracted from the Fund’s benchmark relative returns during the first ten months of the 12-month period, due to a significant increase in short term interest rates. The interest expense on the leverage exceeded the aggregate yield of the Fund’s portfolio during that period. Subsequently, the Fund reduced the amount of its total managed assets financed by leverage, which had a positive impact on net portfolio income. |

| ** | The 30-day SEC yield is a standardized formula that is based on the hypothetical annualized earning power (investment income only) of the Fund’s portfolio securities during the period indicated. |

3Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| On a security selection basis, overweight allocations to Tobacco MSA bonds issued in New York and Ohio detracted from the Fund’s relative performance during the 12-month period. | |

| During the 12-month period, we made the decision to divest from a rural California municipal bond. This bond was under-performing as it failed to meet bond covenant requirements, resulting in distressed pricing and adversely affecting the Fund’s benchmark-relative return. | |

| Q | Did the Fund’s distributions*** to stockholders change during the 12-month period ended April 30, 2024? |

| A | Yes, the Fund’s monthly distribution rate changed a few times during the period. There was a decrease from $0.0375 cents per share/per month to $0.0325 cents per share/per month, announced on May 15, 2023 and paid on May 31, 2023. There was a second decrease from $0.0325 cents per share/per month to $0.0275 cents per share/per month, announced on August 17, 2023 and paid on August 31, 2023. The monthly distribution rate then remained unchanged, at $0.0275 per share/per month through February 2024. There was an increase from $0.0275 cents per share/per month to $0.0350 cents per share/per month, announced on March 14, 2024 and paid on March 28, 2024. The Fund’s distributions during the reporting period included returns of capital totaling $0.01 per share. The decrease in the Fund’s distribution rate was due to an increase in the cost of leverage incurred by the Fund, which reduced the amount of funds available for distribution. |

| Q | How did the level of leverage in the Fund change during the 12-month period ended April 30, 2024? |

| A | On April 30, 2024, 18.4% of the Fund’s total managed assets were financed by leverage obtained through the issuance of Variable Rate MuniFund Term Preferred Shares, compared with 35.8% of the Fund’s total managed assets financed by leverage at the start of the period on May 1, 2023. During the 12-month period, the Fund decreased the amount of leverage by a total of $79 million, to $50 million as of April 30, 2024. The reduction in the amount of the Fund’s leverage during the period was due to increased |

| *** | Distributions are not guaranteed. |

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/244

| borrowing costs and a decrease in the value of the Fund's total assets. The interest rate on the Fund's leverage increased by 108 basis points from April 30, 2023 to April 30, 2024. | |

| Q | Did the Fund have any exposure to derivatives during the 12-month period ended April 30, 2024? |

| A | Yes, we invested the Fund’s portfolio in interest rate futures contracts during the period, which were used to manage the duration during the Fund’s deleveraging. |

| Q | What is your investment outlook, and how is the Fund positioned heading into its new fiscal year? |

| A | We have continued to prefer investments in hospital-related issues, since the sector has historically had very low default rates. The revenue received by hospitals has remained diverse, coming from a combination of Medicare, Medicaid, private insurers, and self-payors. The Fund is also overweight to Tobacco MSA bonds, due in part to the fact that the sector has experienced a below market rate of default compared to other municipal sectors. Tobacco bond revenues have provided substantial funding for the advancement of public health and other similar programs to state and local governments that signed the tobacco MSA. |

| In addition, the Fund is slightly underweight relative to the benchmark to bonds issued by the Commonwealth of Puerto Rico. The Fund is underweight select sectors within the Puerto Rico tax-exempt market based on current valuation levels and the potential for elevated volatility. Sales tax collections are up 5.2% year-over-year for the Commonwealth. The increased revenue has supported fundamentals and has been driving spreads tighter for the issuer. | |

| The Fund is also underweight to state general obligation issues, which have tended to be sensitive to political considerations, as certain state governments may have lower flexibility to raise taxes due to constituents’ preferences, thus limiting their ability to increase revenues. | |

| We anticipate that the shifting interest-rate outlook will continue to impact near-term market performance, given the data |

5Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| dependent nature of US Federal Reserve System (Fed) policy. However, slowing consumer spending and decelerating activity in the housing market may indicate that the Fed is moving closer to the point at which it can conclude its monetary tightening cycle. If this turns out to be the case, we believe investors may turn their attention to the positive fundamental traits of the high yield municipal market, including its current low default rate and the continued decline in new-issue supply. We are also encouraged by the opportunities afforded by the compelling yields in the investment-grade municipal bond space. | |

| As is usually the case, headline news events have had a minimal effect on our day-to-day approach to managing the portfolio. Our goal is to invest the Fund in what we believe are fundamentally sound credits representing relative value opportunities, while maintaining an appropriate level of risk management. We also seek to avoid experiencing defaults in the Fund through our emphasis on fundamental research. We believe this steady, long term approach remains the most effective way to identify opportunities and to help minimize the risk associated with investing in the high-yield municipal market. |

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/246

Please refer to the Schedule of Investments on pages 15 - 23 for a full listing of Fund securities.

All investments are subject to risk, including the possible loss of principal. In the past several years, financial markets have experienced increased volatility and heightened uncertainty. The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict including Russia’s military invasion of Ukraine, sanctions against Russia, other nations or individuals or companies and possible countermeasures, market disruptions caused by tariffs, trade disputes or other government actions, or adverse investor sentiment. These conditions may continue, recur, worsen or spread.

Investments in high-yield or lower-rated securities are subject to greater-than-average risk.

The Fund may invest in securities of issuers that are in default or that are in bankruptcy.

A portion of income may be subject to state, federal, and/or alternative minimum tax. Capital gains, if any, are subject to a capital gains tax.

When interest rates rise, the prices of debt securities held by the Fund will generally fall. Conversely, when interest rates fall the prices of debt securities held by the Fund generally will rise. A general rise in interest rates could adversely affect the price and liquidity of fixed income securities.

The value of municipal securities can be adversely affected by changes in financial condition of municipal issuers, lower revenues, and regulatory and political developments. By concentrating in municipal securities, the Fund is more susceptible to adverse economic, political or regulatory developments than is a portfolio that invests more broadly.

Investments in the Fund are subject to possible loss due to the financial failure of the issuers of the underlying securities and the issuers’ inability to meet their debt obligations.

The Fund may invest up to 20% of its total assets in illiquid securities. Illiquid securities may be difficult to dispose of at a price reflective of their value at the times when the Fund believes it is desirable to do so, and the market price of illiquid securities is generally more volatile than that of more liquid securities. Illiquid securities are also more difficult to value and investment of the Fund’s assets in illiquid securities may restrict the Fund’s ability to take advantage of market opportunities.

7Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

The Fund currently uses leverage through the issuance of preferred shares. Leverage creates significant risks, including the risk that the Fund’s incremental income or capital appreciation for investments purchased with the proceeds of leverage will not be sufficient to cover the cost of the leverage, which may adversely affect the return for the holders of common shares.

The Fund is required to maintain certain regulatory, rating agency and other asset coverage requirements in connection with its outstanding preferred shares. In order to maintain required asset coverage levels, the Fund may be required to alter the composition of its investment portfolio or take other actions, such as redeeming preferred shares with the proceeds from portfolio transactions, at what might be inopportune times in the market. Such actions could reduce the net earnings or returns to holders of the Fund’s common shares over time, which is likely to result in a decrease in the market value of the Fund’s shares.

These risks may increase share price volatility.

Any information in this stockholder report regarding market or economic trends or the factors influencing the Fund’s historical or future performance are statements of opinion as of the date of this report. Past performance is no guarantee of future results.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/248

Portfolio Summary | 4/30/24

Portfolio Diversification

(As a percentage of total investments)*

Portfolio Maturity

(As a percentage of total investments)*

9Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

State Diversification

(As a percentage of total investments)*

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2410

Portfolio Summary | 4/30/24 (continued)

10 Largest Holdings

| (As a percentage of total investments)* | ||

| 1. | Buckeye Tobacco Settlement Financing Authority, Senior Class 2, Series B-2, 5.00%, 6/1/55 | 4.56% |

| 2. | New York Transportation Development Corp., Delta Airlines Inc-LaGuardia, 5.00%, 10/1/40 | 4.44 |

| 3. | Puerto Rico Commonwealth Aqueduct ∓ Sewer Authority, Series A, 5.00%, 7/1/47 (144A) | 3.80 |

| 4. | Arkansas Development Finance Authority, Green Bond, 5.45%, 9/1/52 | 3.77 |

| 5. | Brookhaven Development Authority, Children's Healthcare Of Atlanta, Inc., Series A, 4.00%, 7/1/44 | 3.63 |

| 6. | Iowa Finance Authority, Alcoa Inc. Projects, 4.75%, 8/1/42 | 3.48 |

| 7. | Massachusetts Development Finance Agency, WGBH Educational Foundation, Series A, 5.75%, 1/1/42 (AMBAC Insured) | 3.32 |

| 8. | Puerto Rico Sales Tax Financing Corp. Sales Tax Revenue, Series A1, 5.00%, 7/1/58 | 3.07 |

| 9. | City of Houston Airport System Revenue, 4.00%, 7/15/41 | 2.79 |

| 10. | Metropolitan Transportation Authority, Green Bond, Series C-1, 4.75%, 11/15/45 | 2.35 |

* Excludes short-term investments and all derivative contracts except for options purchased. The Fund is actively managed, and current holdings may be different. The holdings listed should not be considered recommendations to buy or sell any securities.

† Amount rounds to less than 0.1%.

11Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

Market Value per Common Share^

| 4/30/24 | 4/30/23 | |

| Market Value | $ |

$ |

| Discount | ( |

( |

Net Asset Value per Common Share^

| 4/30/24 | 4/30/23 | |

| Net Asset Value | $ |

$ |

Distributions per Common Share

| Net Investment Income |

Short-Term Capital Gains |

Long-Term Capital Gains |

Tax Return of Capital | |

| 5/1/23 – 4/30/24 | $0.3461 | $— | $— | $0.0124 |

Yields

| 4/30/24 | 4/30/23 | |

| 30-Day SEC Yield | 2.93% | 4.50% |

The data shown above represents past performance, which is no guarantee of future results.

^ Net asset value and market value are published daily on the Fund’s website at www.amundi.com/us.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2412

Performance Update | 4/30/24

Investment Returns

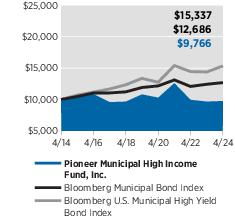

The mountain chart on the right shows the change in market value, including reinvestment of dividends and distributions, of a $10,000 investment made in common shares of Pioneer Municipal High Income Fund, Inc. during the periods shown, compared to that of the Bloomberg Municipal Bond Index and Bloomberg U.S. Municipal High Yield Bond Index.

Call 1-800-710-0935 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

Performance data shown represents past performance. Past performance is no guarantee of future results. Investment return and market price will fluctuate, and your shares may trade below NAV due to such factors as interest rate changes and the perceived credit quality of borrowers.

Total investment return does not reflect broker sales charges or commissions. All performance is for common shares of the Fund.

Shares of closed-end funds, unlike open-end funds, are not continuously offered. There is a one-time public offering and, once issued, shares of closed-end funds are bought and sold in the open market through a stock exchange and frequently trade at prices lower than their NAV. NAV per common share is total assets less total liabilities, which include preferred shares or borrowings, as applicable, divided by the number of common shares outstanding.

When NAV is lower than market price, dividends are assumed to be reinvested at the greater of NAV or 95% of the market price. When NAV is higher, dividends are assumed to be reinvested at prices obtained through open-market purchases under the Fund’s dividend reinvestment plan.

The performance table and graph do not reflect the deduction of fees and taxes that a stockholder would pay on Fund distributions or the sale of Fund shares. Had these fees and taxes been reflected, performance would have been lower.

The Bloomberg Municipal Bond Index is an unmanaged, broad measure of the municipal bond market. The Bloomberg U.S. Municipal High Yield Bond Index is unmanaged, totals over $26 billion in market value and maintains over 1,300 securities. Municipal bonds in this index have the following requirements: maturities of one year or greater, sub investment grade (below Baa or non-rated), fixed coupon rate, issued after 12/31/90, deal size over $20 million,

13Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

Performance Update | 4/30/24

maturity size of at least $3 million. Indices are unmanaged and their returns assume reinvestment of dividends and do not reflect any fees or expenses. The indices do not use leverage. It is not possible to invest directly in an index.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2414

Schedule of Investments | 4/30/24

| Principal Amount USD ($) |

Value | |||||

| UNAFFILIATED ISSUERS — 120.2% | ||||||

| Municipal Bonds — 119.8% of Net Assets(a) | ||||||

| Arizona — 0.9% | ||||||

| 2,220,000 | Industrial Development Authority of the City of Phoenix, 3rd ∓ Indian School Assisted Living Project, 5.40%, 10/1/36 | $ 1,972,470 | ||||

| Total Arizona | $1,972,470 | |||||

| Arkansas — 4.5% | ||||||

| 10,200,000 | Arkansas Development Finance Authority, Green Bond, 5.45%, 9/1/52 | $ 10,050,162 | ||||

| Total Arkansas | $10,050,162 | |||||

| California — 5.9% | ||||||

| 2,500,000 | Bay Area Toll Authority, Series F-2, 2.60%, 4/1/56 | $ 1,571,225 | ||||

| 530,000 | California County Tobacco Securitization Agency, Series B-1, 5.00%, 6/1/49 | 538,671 | ||||

| 10,000,000(b) | California County Tobacco Securitization Agency, Capital Appreciation, Stanislaus County, Subordinated, Series A, 6/1/46 | 2,621,500 | ||||

| 750,000 | California Municipal Finance Authority, Westside Neighborhood School Project, Series A, 6.375%, 6/15/64 (144A) | 768,487 | ||||

| 1,400,000 | California Statewide Communities Development Authority, Lancer Plaza Project, 5.625%, 11/1/33 | 1,401,176 | ||||

| 2,000,000 | California Statewide Communities Development Authority, Loma Linda University Medical Center, 5.50%, 12/1/58 (144A) | 2,037,800 | ||||

| 4,000,000 | San Diego County Regional Airport Authority, Series B, 5.25%, 7/1/58 | 4,195,440 | ||||

| Total California | $13,134,299 | |||||

| Colorado — 2.5% | ||||||

| 1,000,000 | Aerotropolis Regional Transportation Authority, 4.375%, 12/1/52 | $ 818,630 | ||||

| 2,450,000 | Dominion Water ∓ Sanitation District, 5.875%, 12/1/52 | 2,404,038 | ||||

| 2,500,000 | Nine Mile Metropolitan District, 5.125%, 12/1/40 | 2,419,625 | ||||

| Total Colorado | $5,642,293 | |||||

| Connecticut — 1.5% | ||||||

| 3,280,000 | Mohegan Tribal Finance Authority, 7.00%, 2/1/45 (144A) | $ 3,286,101 | ||||

| Total Connecticut | $3,286,101 | |||||

The accompanying notes are an integral part of these financial statements.

15Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| Principal Amount USD ($) |

Value | |||||

| District of Columbia — 3.8% | ||||||

| 5,825,000 | District of Columbia Tobacco Settlement Financing Corp., Asset-Backed, 6.75%, 5/15/40 | $ 6,018,739 | ||||

| 10,000,000(b) | District of Columbia Tobacco Settlement Financing Corp., Capital Appreciation, Asset-Backed, Series A, 6/15/46 | 2,355,400 | ||||

| Total District of Columbia | $8,374,139 | |||||

| Florida — 4.9% | ||||||

| 3,220,000 | City of Tampa, Hospital Revenue Bonds (H. Lee Moffit Cancer Center Project), Series B, 4.00%, 7/1/45 | $ 2,944,787 | ||||

| 5,000,000 | County of Miami-Dade, Water ∓ Sewer System Revenue, Series A, 4.00%, 10/1/44 | 4,764,000 | ||||

| 2,000,000 | Florida Development Finance Corp., Brightline Florida Passenger Rail Project, 5.50%, 7/1/53 | 2,079,980 | ||||

| 1,000,000(c) | Florida Development Finance Corp., Brightline Florida Passenger Rail Project, 12.00%, 7/15/32 (144A) | 1,028,490 | ||||

| Total Florida | $10,817,257 | |||||

| Georgia — 4.4% | ||||||

| 10,000,000 | Brookhaven Development Authority, Children's Healthcare Of Atlanta, Inc., Series A, 4.00%, 7/1/44 | $ 9,689,300 | ||||

| Total Georgia | $9,689,300 | |||||

| Idaho — 2.3% | ||||||

| 5,000,000 | Power County Industrial Development Corp., FMC Corp. Project, 6.45%, 8/1/32 | $ 5,014,050 | ||||

| Total Idaho | $5,014,050 | |||||

| Illinois — 6.6% | ||||||

| 2,000,000(d) | Chicago Board of Education, Series A, 5.00%, 12/1/47 | $ 2,007,560 | ||||

| 2,000,000(d) | Chicago Board of Education, Series H, 5.00%, 12/1/46 | 1,960,400 | ||||

| 704,519(b)(e) | Illinois Finance Authority, Cabs Clare Oaks Project, Series B-1, 11/15/52 | 42,271 | ||||

| 1,116,010(c)(e) | Illinois Finance Authority, Clare Oaks Project, Series A-3, 4.00%, 11/15/52 | 725,406 | ||||

| 3,500,000 | Illinois Finance Authority, The Admiral at the Lake Project, 5.25%, 5/15/42 | 2,729,265 | ||||

| 4,000,000 | Illinois Finance Authority, The Admiral at the Lake Project, 5.50%, 5/15/54 | 2,892,400 | ||||

| 915,000 | Illinois Housing Development Authority, Series B, 2.15%, 10/1/41 (GNMA FNMA FHLMC COLL Insured) | 627,965 | ||||

| 2,000,000 | Metropolitan Pier ∓ Exposition Authority, McCormick Place Expansion, 4.00%, 6/15/50 | 1,796,300 | ||||

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2416

Schedule of Investments | 4/30/24 (continued)

| Principal Amount USD ($) |

Value | |||||

| Illinois — (continued) | ||||||

| 1,205,000 | Metropolitan Pier ∓ Exposition Authority, McCormick Place Expansion, 5.00%, 6/15/57 | $ 1,212,929 | ||||

| 695,000(e) | Southwestern Illinois Development Authority, Village of Sauget Project, 5.625%, 11/1/26 | 521,250 | ||||

| Total Illinois | $14,515,746 | |||||

| Indiana — 1.8% | ||||||

| 2,000,000 | City of Evansville, Silver Birch Evansville Project, 5.45%, 1/1/38 | $ 1,760,220 | ||||

| 1,500,000 | City of Mishawaka, Silver Birch Mishawaka Project, 5.375%, 1/1/38 (144A) | 1,272,915 | ||||

| 1,000,000 | Indiana Finance Authority, Multipurpose Educational Facilities, Avondale Meadows Academy Project, 5.375%, 7/1/47 | 949,100 | ||||

| Total Indiana | $3,982,235 | |||||

| Iowa — 4.2% | ||||||

| 9,675,000 | Iowa Finance Authority, Alcoa Inc. Projects, 4.75%, 8/1/42 | $ 9,285,871 | ||||

| Total Iowa | $9,285,871 | |||||

| Maine — 1.2% | ||||||

| 3,000,000 | Maine Health ∓ Higher Educational Facilities Authority, Series A, 4.00%, 7/1/50 | $ 2,734,140 | ||||

| Total Maine | $2,734,140 | |||||

| Maryland — 1.0% | ||||||

| 3,000,000 | Maryland State Transportation Authority, Series A, 3.00%, 7/1/47 | $ 2,260,500 | ||||

| Total Maryland | $2,260,500 | |||||

| Massachusetts — 7.3% | ||||||

| 2,500,000 | Massachusetts Development Finance Agency, Series A, 5.00%, 7/1/44 | $ 2,379,325 | ||||

| 3,000,000 | Massachusetts Development Finance Agency, Lowell General Hospital, Series G, 5.00%, 7/1/44 | 2,914,260 | ||||

| 7,100,000 | Massachusetts Development Finance Agency, WGBH Educational Foundation, Series A, 5.75%, 1/1/42 (AMBAC Insured) | 8,837,015 | ||||

| 2,270,000(d) | Town of Millbury, 4.00%, 8/15/51 | 2,051,830 | ||||

| Total Massachusetts | $16,182,430 | |||||

| Michigan — 0.4% | ||||||

| 990,000 | David Ellis Academy-West, 5.25%, 6/1/45 | $ 897,653 | ||||

| Total Michigan | $897,653 | |||||

The accompanying notes are an integral part of these financial statements.

17Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| Principal Amount USD ($) |

Value | |||||

| Minnesota — 0.4% | ||||||

| 1,000,000 | City of Ham Lake, DaVinci Academy, Series A, 5.00%, 7/1/47 | $ 912,590 | ||||

| Total Minnesota | $912,590 | |||||

| Montana — 0.0%† | ||||||

| 1,600,000(e) | Two Rivers Authority, 7.375%, 11/1/27 | $ 64,000 | ||||

| Total Montana | $64,000 | |||||

| New Hampshire — 2.9% | ||||||

| 6,000,000 | New Hampshire Health and Education Facilities Authority Act, Series A, 5.00%, 8/1/59 (BAM-TCRS Insured) | $ 6,222,780 | ||||

| 375,000 | New Hampshire Health and Education Facilities Authority Act, Catholic Medical Centre, 3.75%, 7/1/40 | 281,993 | ||||

| Total New Hampshire | $6,504,773 | |||||

| New Jersey — 1.4% | ||||||

| 2,200,000 | New Jersey Economic Development Authority, Continental Airlines, 5.75%, 9/15/27 | $ 2,204,004 | ||||

| 1,000,000 | New Jersey Economic Development Authority, Marion P. Thomas Charter School, Inc., Project, Series A, 5.375%, 10/1/50 (144A) | 899,690 | ||||

| Total New Jersey | $3,103,694 | |||||

| New Mexico — 1.1% | ||||||

| 2,540,000(c) | County of Otero, Otero County Jail Project, Certificate Participation, 9.00%, 4/1/28 | $ 2,400,300 | ||||

| Total New Mexico | $2,400,300 | |||||

| New York — 18.9% | ||||||

| 2,000,000 | Erie Tobacco Asset Securitization Corp., Asset-Backed, Series A, 5.00%, 6/1/45 | $ 1,876,440 | ||||

| 6,175,000 | Metropolitan Transportation Authority, Green Bond, Series C-1, 4.75%, 11/15/45 | 6,260,462 | ||||

| 2,000,000 | Metropolitan Transportation Authority, Green Bond, Series C-1, 5.25%, 11/15/55 | 2,068,560 | ||||

| 2,000,000 | Metropolitan Transportation Authority, Green Bond, Series D-2, 4.00%, 11/15/48 | 1,794,420 | ||||

| 3,000,000 | Metropolitan Transportation Authority, Green Bond, Series E, 4.00%, 11/15/45 | 2,781,900 | ||||

| 2,500,000 | New York Counties Tobacco Trust IV, Settlement pass through, Series A, 5.00%, 6/1/45 | 2,288,775 | ||||

| 2,000,000 | New York State Housing Finance Agency, Sustainability Bonds, Series D-1, 4.20%, 11/1/52 (SONYMA FHA 542c Insured) | 1,824,880 | ||||

| 2,500,000 | New York Transportation Development Corp., Series A, 5.25%, 1/1/50 | 2,488,675 | ||||

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2418

Schedule of Investments | 4/30/24 (continued)

| Principal Amount USD ($) |

Value | |||||

| New York — (continued) | ||||||

| 11,330,000 | New York Transportation Development Corp., Delta Airlines Inc-LaGuardia, 5.00%, 10/1/40 | $ 11,828,067 | ||||

| 1,750,000 | New York Transportation Development Corp., Green Bond, 5.375%, 6/30/60 | 1,827,350 | ||||

| 340,000 | Suffolk Regional Off-Track Betting Co., 5.75%, 12/1/44 | 345,797 | ||||

| 1,000,000 | Suffolk Regional Off-Track Betting Co., 6.00%, 12/1/53 | 1,010,000 | ||||

| 2,500,000 | Triborough Bridge ∓ Tunnel Authority Sales Tax Revenue, Series A-1, 5.25%, 5/15/59 | 2,702,325 | ||||

| 2,148,177 | Westchester County Healthcare Corp., Series A, 5.00%, 11/1/44 | 2,041,885 | ||||

| 1,000,000 | Westchester County Local Development Corp., Purchase Senior Learning Community, 4.50%, 7/1/56 (144A) | 827,090 | ||||

| Total New York | $41,966,626 | |||||

| Ohio — 6.6% | ||||||

| 13,375,000 | Buckeye Tobacco Settlement Financing Authority, Senior Class 2, Series B-2, 5.00%, 6/1/55 | $ 12,162,289 | ||||

| 1,000,000 | Ohio Housing Finance Agency, Sanctuary Springboro Project, 5.45%, 1/1/38 (144A) | 819,790 | ||||

| 1,540,000 | State of Ohio, 5.00%, 12/31/39 | 1,548,039 | ||||

| Total Ohio | $14,530,118 | |||||

| Oregon — 1.6% | ||||||

| 5,000,000 | Oregon Health ∓ Science University, Green Bond, Series A, 3.00%, 7/1/51 | $ 3,573,200 | ||||

| Total Oregon | $3,573,200 | |||||

| Pennsylvania — 6.2% | ||||||

| 5,000,000 | Montgomery County Higher Education and Health Authority, Thomas Jefferson University, Series B, 4.00%, 5/1/52 | $ 4,434,500 | ||||

| 3,500,000 | Montgomery County Higher Education and Health Authority, Thomas Jefferson University, Series B, 5.00%, 5/1/57 | 3,537,940 | ||||

| 4,335,000 | Pennsylvania Higher Educational Facilities Authority, University of Pennsylvania, 4.00%, 8/15/49 | 4,103,815 | ||||

| 500,000 | Philadelphia Authority for Industrial Development, 5.50%, 6/1/49 (144A) | 455,525 | ||||

The accompanying notes are an integral part of these financial statements.

19Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| Principal Amount USD ($) |

Value | |||||

| Pennsylvania — (continued) | ||||||

| 1,000,000 | Philadelphia Authority for Industrial Development, Global Leadership Academy Charter School Project, Series A, 5.00%, 11/15/50 | $ 822,800 | ||||

| 460,000 | Philadelphia Authority for Industrial Development, Greater Philadelphia Health Action, Inc., Project, Series A, 6.625%, 6/1/50 | 433,729 | ||||

| Total Pennsylvania | $13,788,309 | |||||

| Puerto Rico — 13.8% | ||||||

| 5,267,777(d) | Commonwealth of Puerto Rico, Restructured Series A-1, 4.00%, 7/1/41 | $ 4,901,087 | ||||

| 3,000,000(d) | Commonwealth of Puerto Rico, Restructured Series A-1, 4.00%, 7/1/46 | 2,704,920 | ||||

| 2,000,000 | GDB Debt Recovery Authority of Puerto Rico, 7.50%, 8/20/40 | 1,925,000 | ||||

| 10,000,000 | Puerto Rico Commonwealth Aqueduct ∓ Sewer Authority, Series A, 5.00%, 7/1/47 (144A) | 10,121,900 | ||||

| 1,000,000(e) | Puerto Rico Electric Power Authority, Series AAA, 5.25%, 7/1/24 | 262,500 | ||||

| 2,500,000 | Puerto Rico Sales Tax Financing Corp. Sales Tax Revenue, Series 2, 4.784%, 7/1/58 | 2,443,750 | ||||

| 8,191,000 | Puerto Rico Sales Tax Financing Corp. Sales Tax Revenue, Series A1, 5.00%, 7/1/58 | 8,172,570 | ||||

| Total Puerto Rico | $30,531,727 | |||||

| Rhode Island — 1.1% | ||||||

| 5,900,000(e) | Central Falls Detention Facility Corp., 7.25%, 7/15/35 | $ 2,360,000 | ||||

| Total Rhode Island | $2,360,000 | |||||

| Texas — 4.6% | ||||||

| 500,000 | Arlington Higher Education Finance Corp., 5.45%, 3/1/49 (144A) | $ 519,085 | ||||

| 1,000,000 | Arlington Higher Education Finance Corp., Universal Academy, Series A, 7.00%, 3/1/34 | 1,001,480 | ||||

| 8,000,000 | City of Houston Airport System Revenue, 4.00%, 7/15/41 | 7,436,160 | ||||

| 1,500,000 | New Hope Cultural Education Facilities Finance Corp., Sanctuary LTC Project, Series A-1, 5.50%, 1/1/57 | 1,231,215 | ||||

| 3,960,000(e) | Sanger Industrial Development Corp., Texas Pellets Project, Series B, 8.00%, 7/1/38 | 396 | ||||

| Total Texas | $10,188,336 | |||||

| Virginia — 7.0% | ||||||

| 2,700,000 | Tobacco Settlement Financing Corp., Series A-1, 6.706%, 6/1/46 | $ 2,300,292 | ||||

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2420

Schedule of Investments | 4/30/24 (continued)

| Principal Amount USD ($) |

Value | |||||

| Virginia — (continued) | ||||||

| 2,000,000 | Virginia Small Business Financing Authority, Senior Lien, 5.00%, 12/31/42 | $ 2,052,600 | ||||

| 1,000,000 | Virginia Small Business Financing Authority, Senior Lien, 5.00%, 12/31/47 | 968,460 | ||||

| 1,000,000 | Virginia Small Business Financing Authority, Senior Lien 95 Express Lanes LLC Project, 4.00%, 1/1/48 | 870,290 | ||||

| 3,500,000 | Virginia Small Business Financing Authority, Transform 66-P3 Project, 5.00%, 12/31/49 | 3,357,060 | ||||

| 6,100,000 | Virginia Small Business Financing Authority, Transform 66-P3 Project, 5.00%, 12/31/56 | 5,944,450 | ||||

| Total Virginia | $15,493,152 | |||||

| Wisconsin — 1.0% | ||||||

| 1,500,000 | Public Finance Authority, Gardner Webb University, 5.00%, 7/1/31 (144A) | $ 1,552,770 | ||||

| 750,000 | Public Finance Authority, Roseman University Health Sciences Project, 5.875%, 4/1/45 | 756,330 | ||||

| Total Wisconsin | $2,309,100 | |||||

| Total Municipal Bonds (Cost $274,775,499) |

$265,564,571 | |||||

| U.S. Government and Agency Obligations — 0.4% of Net Assets |

||||||

| 1,000,000(b) | U.S. Treasury Bills, 5/21/24 | $ 997,072 | ||||

| Total U.S. Government and Agency Obligations (Cost $997,065) |

$997,072 | |||||

| TOTAL INVESTMENTS IN UNAFFILIATED ISSUERS — 120.2% (Cost $275,772,564) |

$266,561,643 | |||||

| OTHER ASSETS AND LIABILITIES — (20.2)% | $(44,805,665) | |||||

| net assets applicable to common stockholders — 100.0% | $221,755,978 | |||||

| AMBAC | Ambac Assurance Corporation. |

| BAM | Build America Mutual Assurance Company. |

| COLL | Collateral. |

| FHA 542c | Federal Housing Administration Section 542c. |

| FHLMC | Federal Home Loan Mortgage Corporation. |

| FNMA | Federal National Mortgage Association. |

| GNMA | Government National Mortgage Association. |

| SONYMA | State of New York Mortgage Agency. |

The accompanying notes are an integral part of these financial statements.

21Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| TCRS | Transferable Custodial Receipts. |

| (144A) | The resale of such security is exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may be resold normally to qualified institutional buyers. At April 30, 2024, the value of these securities amounted to $23,589,643, or 10.6% of net assets applicable to common stockholders. |

| (a) | Consists of Revenue Bonds unless otherwise indicated. |

| (b) | Security issued with a zero coupon. Income is recognized through accretion of discount. |

| (c) | The interest rate is subject to change periodically. The interest rate and/or reference index and spread shown at April 30, 2024. |

| (d) | Represents a General Obligation Bond. |

| (e) | Security is in default. |

| † | Amount rounds to less than 0.1%. |

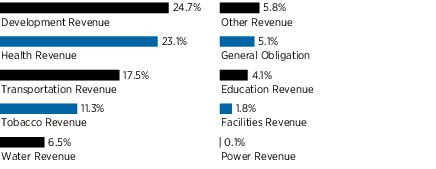

The concentration of investments as a percentage of total investments by type of obligation/market sector is as follows:

| Revenue Bonds: | |

| Development Revenue | 24.7% |

| Health Revenue | 23.1 |

| Transportation Revenue | 17.5 |

| Tobacco Revenue | 11.3 |

| Water Revenue | 6.5 |

| Other Revenue | 5.8 |

| Education Revenue | 4.1 |

| Facilities Revenue | 1.8 |

| Power Revenue | 0.1 |

| 94.9% | |

| General Obligation Bonds: | 5.1% |

| 100.0% |

FUTURES CONTRACTS

FIXED INCOME INDEX FUTURES CONTRACTS

FIXED INCOME INDEX FUTURES CONTRACTS

| Number of Contracts Long |

Description | Expiration Date |

Notional Amount |

Market Value |

Unrealized (Depreciation) |

| 87 | U.S. Long Bond (CBT) | 6/18/24 | $10,354,590 | $9,901,688 | $(452,902) |

| TOTAL FUTURES CONTRACTS | $10,354,590 | $9,901,688 | $(452,902) | ||

| CBT | Chicago Board of Trade. | ||||

Purchases and sales of securities (excluding short-term investments) for the year ended April 30, 2024, aggregated $109,921,228 and $190,753,444, respectively.

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2422

Schedule of Investments | 4/30/24 (continued)

At April 30, 2024, the net unrealized depreciation on investments based on cost for federal tax purposes of $274,923,869 was as follows:

| Aggregate gross unrealized appreciation for all investments in which there is an excess of value over tax cost | $10,913,782 |

| Aggregate gross unrealized depreciation for all investments in which there is an excess of tax cost over value | (19,276,008) |

| Net unrealized depreciation | $(8,362,226) |

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels below.

| Level 1 | – | unadjusted quoted prices in active markets for identical securities. |

| Level 2 | – | other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risks, etc.). See Notes to Financial Statements — Note 1A. |

| Level 3 | – | significant unobservable inputs (including the Adviser’s own assumptions in determining fair value of investments). See Notes to Financial Statements — Note 1A. |

The following is a summary of the inputs used as of April 30, 2024 in valuing the Fund’s investments:

| Level 1 | Level 2 | Level 3 | Total | |

| Municipal Bonds | $— | $265,564,571 | $— | $265,564,571 |

| U.S. Government and Agency Obligations | — | 997,072 | — | 997,072 |

| Total Investments in Securities | $— | $266,561,643 | $— | $266,561,643 |

| Other Financial Instruments | ||||

| Variable Rate MuniFund Term Preferred Shares(a) | $— | $(50,000,000) | $— | $(50,000,000) |

| Net unrealized depreciation on futures contracts | (452,902) | — | — | (452,902) |

| Total Other Financial Instruments | $(452,902) | $(50,000,000) | $— | $(50,452,902) |

| (a) | The Fund may hold liabilities in which the fair value approximates the carrying amount for financial statement purposes. |

During the year ended April 30, 2024, there were no transfers in or out of Level 3.

The accompanying notes are an integral part of these financial statements.

23Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

Statement of Assets and Liabilities | 4/30/24

| ASSETS: | |

| Investments in unaffiliated issuers, at value (cost $275,772,564) | $266,561,643 |

| Cash | 3,707,961 |

| Futures collateral | 398,906 |

| Due from broker for futures | 67,969 |

| Distribution paid in advance | 796,997 |

| Receivables — | |

| Investment securities sold | 926,232 |

| Interest | 4,140,389 |

| Other assets | 104 |

| Total assets | $276,600,201 |

| LIABILITIES: | |

| Variable Rate MuniFund Term Preferred Shares* | $50,000,000 |

| Payables — | |

| Investment securities purchased | 3,775,940 |

| Distributions | 796,997 |

| Directors’ fees | 889 |

| Variation margin for futures contracts | 67,969 |

| Management fees | 22,264 |

| Administrative expenses | 24,055 |

| Accrued expenses | 156,109 |

| Total liabilities | $54,844,223 |

| NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS: | |

| Paid-in capital | $299,230,912 |

| Distributable earnings (loss) | (77,474,934) |

| Net assets | $221,755,978 |

| NET ASSET VALUE PER COMMON SHARE: | |

| No par value | |

| Based on $221,755,978/22,771,349 common shares | $9.74 |

* $100,000 liquidation value per share applicable to 500 shares.

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2424

Statement of Operations FOR THE YEAR ENDED 4/30/24

| INVESTMENT INCOME: | ||

| Interest from unaffiliated issuers | $17,169,260 | |

| Total Investment Income | $17,169,260 | |

| EXPENSES: | ||

| Management fees | $1,984,692 | |

| Administrative expenses | 90,521 | |

| Transfer agent fees | 18,723 | |

| Stockholder communications expense | 70,698 | |

| Custodian fees | 3,226 | |

| Professional fees | 410,185 | |

| Printing expense | 14,388 | |

| Officers’ and Directors’ fees | 15,332 | |

| Insurance expense | 8,809 | |

| Interest expense | 6,323,520 | |

| Miscellaneous | 243,634 | |

| Total expenses | $9,183,728 | |

| Net investment income | $7,985,532 | |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | ||

| Net realized gain (loss) on: | ||

| Reimbursement by the Adviser | $223,759 | |

| Investments in unaffiliated issuers | (24,361,627) | |

| Futures contracts | (755,613) | $(24,893,481) |

| Change in net unrealized appreciation (depreciation) on: | ||

| Investments in unaffiliated issuers | $15,720,657 | |

| Futures contracts | (452,902) | $15,267,755 |

| Net realized and unrealized gain (loss) on investments | $(9,625,726) | |

| Net decrease in net assets resulting from operations | $(1,640,194) |

The accompanying notes are an integral part of these financial statements.

25Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

Statements of Changes in Net Assets

| Year Ended 4/30/24 |

Year Ended 4/30/23 | |

| FROM OPERATIONS: | ||

| Net investment income (loss) | $7,985,532 | $9,182,035 |

| Net realized gain (loss) on investments | (24,893,481) | (17,025,390) |

| Change in net unrealized appreciation (depreciation) on investments | 15,267,755 | 2,971,984 |

| Net decrease in net assets resulting from operations | $(1,640,194) | $(4,871,371) |

| DISTRIBUTIONS TO COMMON STOCKHOLDERS: | ||

| ($0.35 and $0.46 per share, respectively) | $(7,880,612) | $(10,370,270) |

| Tax Return Of Capital To Common Stockholders: | ||

| ($0.01 and $0.06 per share, respectively) | $(282,917) | $(1,482,217) |

| Total distributions to common stockholders | $(8,163,529) | $(11,852,487) |

| Net decrease in net assets applicable to common stockholders | $(9,803,723) | $(16,723,858) |

| NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS: | ||

| Beginning of year | $231,559,701 | $248,283,559 |

| End of year | $221,755,978 | $231,559,701 |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2426

Statement of Cash Flows FOR THE YEAR ENDED 4/30/24

| Cash Flows From Operating Activities | |

| Net decrease in net assets resulting from operations | $(1,640,194) |

| Adjustments to reconcile net decrease in net assets resulting from operations to net cash and restricted cash from operating activities: | |

| Purchases of investment securities | $(106,145,288) |

| Proceeds from disposition and maturity of investment securities | 190,051,827 |

| Net purchases of short term investments | (671,427) |

| Net accretion and amortization of discount/premium on investment securities | (551,048) |

| Reimbursement by the Adviser | (223,759) |

| Net realized loss on investments in unaffiliated issuers | 24,361,627 |

| Change in unrealized appreciation on investments in unaffiliated issuers | (15,720,657) |

| Increase in due from broker for futures | (67,969) |

| Decrease in interest receivable | 1,509,777 |

| Decrease in due from affiliates | 1,719 |

| Decrease in distributions paid in advance | 56,929 |

| Decrease in other assets | 1,341 |

| Increase in variation margin for futures contracts | 67,969 |

| Decrease in management fees payable | (7,293) |

| Decrease in directors’ fees payable | (592) |

| Increase in administrative expenses payable | 5,910 |

| Increase in accrued expenses payable | 51,552 |

| Net cash and restricted cash from operating activities | $91,080,424 |

| Cash Flows Used In Financing Activities: | |

| VMTP Shares Redeemed | (79,000,000) |

| Distributions to stockholders | (8,220,458) |

| Net cash flows used in financing activities | $(87,220,458) |

| NET INCREASE (DECREASE) IN CASH AND RESTRICTED CASH | $3,859,966 |

| Cash and Restricted Cash: | |

| Beginning of year* | $246,901 |

| End of year* | $4,106,867 |

| Cash Flow Information: | |

| Cash paid for interest | $6,323,520 |

| * | The following table provides a reconciliation of cash and restricted cash reported within the Statement of Assets and Liabilities that sum to the total of the same such amounts shown in the Statement of Cash Flows: |

| Year Ended 4/30/24 |

Year Ended 4/30/23 | |

| Cash | $3,707,961 | $246,901 |

| Restricted cash | 398,906 | — |

| Total cash and restricted cash shown in the Statement of Cash Flows | $4,106,867 | $246,901 |

The accompanying notes are an integral part of these financial statements

27Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

Financial Highlights

| Year Ended 4/30/24 |

Year Ended 4/30/23 |

Year Ended 4/30/22 |

Year Ended 4/30/21 |

Year Ended 4/30/20 | |

| Per Share Operating Performance | |||||

| Net asset value, beginning of period | $10.17 | $10.90 | $13.14 | $12.31 | $12.65 |

| Increase (decrease) from investment operations:(a) | |||||

| Net investment income (loss)(b) | $0.35 | $0.40 | $0.53 | $0.55 | $0.55 |

| Net realized and unrealized gain (loss) on investments | (0.42) | (0.61) | (2.29) | 0.87 | (0.32) |

| Net increase (decrease) from investment operations | $(0.07) | $(0.21) | $(1.76) | $1.42 | $0.23 |

| Distributions to stockholders: | |||||

| Net investment income and previously undistributed net investment income | $(0.35) | $(0.46)* | $(0.48) | $(0.59)* | $(0.57)* |

| Tax return of capital | (0.01) | (0.06) | — | — | — |

| Total distributions | $(0.36) | $(0.52) | $(0.48) | $(0.59) | $(0.57) |

| Net increase (decrease) in net asset value | $(0.43) | $(0.73) | $(2.24) | $0.83 | $(0.34) |

| Net asset value, end of period | $9.74 | $10.17 | $10.90 | $13.14 | $12.31 |

| Market value, end of period | $8.49 | $8.78 | $9.57 | $12.61 | $10.82 |

| Total return at net asset value(c) | (0.02)%(d) | (1.17)% | (13.64)% | 12.04% | 2.00%(e) |

| Total return at market value(c) | 0.95% | (2.82)% | (20.99)% | 22.33% | (4.77)% |

| Ratios to average net assets of common stockholders: | |||||

| Total expenses plus interest expense(f)(g) | 4.16% | 3.15% | 1.56% | 1.62% | 2.13% |

| Net investment income | 3.61% | 3.95% | 4.15% | 4.22% | 4.24% |

| Portfolio turnover rate | 35% | 60% | 11% | 10% | 17% |

| Net assets of common stockholders, end of period (in thousands) | $221,756 | $231,560 | $248,284 | $299,280 | $280,258 |

| Preferred shares outstanding (in thousands)(h)(i)(j)(k) | $50,000 | $129,000 | $145,000 | $145,000 | $125,000 |

| Asset coverage per preferred share, end of period | $543,512 | $279,504 | $271,230 | $306,399 | $324,229 |

| Average market value per preferred share(l) | $100,000 | $100,000 | $100,000 | $100,000 | $100,000 |

| Liquidation value, including interest expense payable, per preferred share | $100,000 | $100,000 | $100,000 | $99,999 | $100,023 |

| * | The amount of distributions made to stockholders during the year were in excess of the net investment income earned by the Fund during the year. The Fund has accumulated undistributed net investment income which is part of the Fund’s net asset value (“NAV”). A portion of the accumulated net investment income was distributed to stockholders during the year. A decrease in distributions may have a negative effect on the market value of the Fund’s shares. |

| (a) | The per common share data presented above is based upon the average common shares outstanding for the periods presented. |

| (b) | Beginning April 30, 2020, distribution payments to preferred stockholders are included as a component of net investment income. |

The accompanying notes are an integral part of these financial statements.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2428

Financial Highlights (continued)

| (c) | Total investment return is calculated assuming a purchase of common shares at the current net asset value or market value on the first day and a sale at the current net asset value or market value on the last day of the periods reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment return does not reflect brokerage commissions. Past performance is not a guarantee of future results. |

| (d) | For the year ended April 30, 2024, the Fund's total return includes a reimbursement by the Adviser (see Notes to the Financial Statements-Note 1B). If the Fund had not been reimbursed by the Adviser the total return would have been (0.12)%. |

| (e) | If the Fund had not recognized gains in settlement of class action lawsuits during the year ended April 30, 2020, the total return would have been 1.73%. |

| (f) | Includes interest expense of 2.86%, 1.94%, 0.45%, 0.47%, and 1.10%, respectively. |

| (g) | Prior to April 30, 2020, the expense ratios do not reflect the effect of distribution payments to preferred stockholders. |

| (h) | The Fund redeemed 635 Variable Rate MuniFund Term Preferred Shares, with a liquidation preference of $100,000 per share, on February 29, 2024. |

| (i) | The Fund redeemed 155 Variable Rate MuniFund Term Preferred Shares, with a liquidation preference of $100,000 per share, on October 11, 2023. |

| (j) | The Fund redeemed 160 Variable Rate MuniFund Term Preferred Shares, with a liquidation preference of $100,000 per share, on November 14, 2022. |

| (k) | The Fund issued 200 Variable Rate MuniFund Term Preferred Shares, with a liquidation preference of $100,000 per share, on February 16, 2021. |

| (l) | Market value is redemption value without an active market. |

The accompanying notes are an integral part of these financial statements.

29Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

Notes to Financial Statements | 4/30/24

1. Organization and Significant Accounting Policies

Pioneer Municipal High Income Fund, Inc. (the “Fund”) is organized as a Maryland corporation. Prior to April 21, 2021, the Fund was organized as a Delaware statutory trust. On April 21, 2021, the Fund redomiciled to a Maryland corporation through a statutory merger of the predecessor Delaware statutory trust with and into a newly-established Maryland corporation formed for the purpose of effecting the redomiciling. The Fund was originally organized on March 13, 2003. Prior to commencing operations on July 21, 2003, the Fund had no operations other than matters relating to its organization and registration as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the "1940 Act"). The investment objective of the Fund is to seek a high level of current income exempt from regular federal income tax, and the Fund may, as a secondary objective, also seek capital appreciation to the extent that it is consistent with its primary investment objective.

Amundi Asset Management US, Inc., an indirect, wholly owned subsidiary of Amundi and Amundi’s wholly owned subsidiary, Amundi USA, Inc., serves as the Fund’s investment adviser (the “Adviser”).

The Fund is required to comply with Rule 18f-4 under the 1940 Act, which governs the use of derivatives by registered investment companies. Rule 18f-4 permits funds to enter into derivatives transactions (as defined in Rule 18f-4) and certain other transactions notwithstanding the restrictions on the issuance of “senior securities” under Section 18 of the 1940 Act. Rule 18f-4 requires a fund to establish and maintain a comprehensive derivatives risk management program, appoint a derivatives risk manager and comply with a relative or absolute limit on fund leverage risk calculated based on value-at-risk (“VaR”), unless the fund uses derivatives in only a limited manner (a "limited derivatives user"). The Fund is currently a limited derivatives user for purposes of Rule 18f-4.

The Fund is an investment company and follows investment company accounting and reporting guidance under U.S. Generally Accepted Accounting Principles (“U.S. GAAP”). U.S. GAAP requires the management of the Fund to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of income, expenses and gain or loss on investments during the reporting period. Actual results could differ from those estimates.

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2430

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements:

| A. | Security Valuation |

| The net asset value of the Fund is computed once daily, on each day the New York Stock Exchange (“NYSE”) is open, as of the close of regular trading on the NYSE. | |

| Fixed income securities are valued by using prices supplied by independent pricing services, which consider such factors as market prices, market events, quotations from one or more brokers, Treasury spreads, yields, maturities and ratings, or may use a pricing matrix or other fair value methods or techniques to provide an estimated value of the security or instrument. A pricing matrix is a means of valuing a debt security on the basis of current market prices for other debt securities, historical trading patterns in the market for fixed income securities and/or other factors. Non-U.S. debt securities that are listed on an exchange will be valued at the bid price obtained from an independent third party pricing service. When independent third party pricing services are unable to supply prices, or when prices or market quotations are considered to be unreliable, the value of that security may be determined using quotations from one or more broker-dealers. | |

| Futures contracts are generally valued at the closing settlement price established by the exchange on which they are traded. | |

| Securities for which independent pricing services or broker-dealers are unable to supply prices or for which market prices and/or quotations are not readily available or are considered to be unreliable are valued by a fair valuation team comprised of certain personnel of the Adviser. The Adviser is designated as the valuation designee for the Fund pursuant to Rule 2a-5 under the 1940 Act. The Adviser’s fair valuation team is responsible for monitoring developments that may impact fair valued securities. | |

| Inputs used when applying fair value methods to value a security may include credit ratings, the financial condition of the company, current market conditions and comparable securities. The Adviser may use fair value methods if it is determined that a significant event has occurred after the close of the exchange or market on which the security trades and prior to the determination of the Fund’s net asset value. Examples of a significant event might include political or economic news, corporate restructurings, natural disasters, terrorist activity or trading |

31Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| halts. Thus, the valuation of the Fund’s securities may differ significantly from exchange prices, and such differences could be material. | |

| B. | Investment Income and Transactions |

| Interest income, including interest on income-bearing cash accounts, is recorded on the accrual basis. Dividend and interest income are reported net of unrecoverable foreign taxes withheld at the applicable country rates and net of income accrued on defaulted securities. | |

| Discounts and premiums on purchase prices of debt securities are accreted or amortized, respectively, daily, into interest income on an effective yield to maturity basis with a corresponding increase or decrease in the cost basis of the security. Premiums and discounts related to certain mortgage-backed securities are amortized or accreted in proportion to the monthly paydowns. | |

| Interest and dividend income payable by delivery of additional shares is reclassified as PIK (payment-in-kind) income upon receipt and is included in interest and dividend income, respectively. | |

| Security transactions are recorded as of trade date. Gains and losses on sales of investments are calculated on the identified cost method for both financial reporting and federal income tax purposes. | |

| During the year ended April 30, 2024, the Fund realized a loss of $223,759 due to an operational error. The Adviser voluntarily reimbursed the Fund for this loss, which is reflected on the Statement of Operations as Reimbursement by the Adviser. | |

| C. | Federal Income Taxes |

| It is the Fund’s policy to comply with the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute all of its net taxable income and net realized capital gains, if any, to its stockholders. Therefore, no provision for federal income taxes is required. As of April 30, 2024, the Fund did not accrue any interest or penalties with respect to uncertain tax positions, which, if applicable, would be recorded as an income tax expense on the Statement of Operations. Tax returns filed within the prior three years remain subject to examination by federal and state tax authorities. | |

| The amount and character of income and capital gain distributions to stockholders are determined in accordance with federal income tax rules, which may differ from U.S. GAAP. Distributions in excess of net investment income or net realized gains are temporary over distributions |

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2432

| for financial statement purposes resulting from differences in the recognition or classification of income or distributions for financial statement and tax purposes. Capital accounts within the financial statements are adjusted for permanent book/tax differences to reflect tax character, but are not adjusted for temporary differences. | |

| At April 30, 2024, the Fund was permitted to carry forward indefinitely $5,368,173 of short-term losses and $62,947,538 of long-term losses. | |

| The tax character of distributions paid during the years ended April 30, 2024 and April 30, 2023, was as follows: |

| 2024 | 2023 | |

| Distributions paid from: | ||

| Tax-exempt income | $13,790,979 | $14,653,673 |

| Ordinary income | 413,153 | 239,797 |

| Tax return of capital | 282,917 | 1,482,217 |

| Total | $14,487,049 | $16,375,687 |

The following shows the components of distributable earnings (losses) on a federal income tax basis at April 30, 2024:

| 2024 | |

| Distributable earnings/(losses): | |

| Capital loss carryforward | $(68,315,711) |

| Other book/tax temporary differences | (796,997) |

| Net unrealized depreciation | (8,362,226) |

| Total | $(77,474,934) |

The difference between book-basis and tax-basis unrealized depreciation is primarily attributable to the tax adjustments relating to wash sales, the book/tax differences in the accrual of income on securities in default, and discounts on fixed income securities.

| D. | Automatic Dividend Reinvestment Plan |

| All stockholders whose shares are registered in their own names automatically participate in the Automatic Dividend Reinvestment Plan (the “Plan”), under which participants receive all dividends and capital gain distributions (collectively, dividends) in full and fractional shares of the Fund in lieu of cash. Stockholders may elect not to participate in the Plan. Stockholders not participating in the Plan receive all dividends and capital gain distributions in cash. Participation in the Plan is completely voluntary and may be terminated or resumed at any time without penalty by notifying Equiniti Trust Company, the agent for stockholders in administering the Plan (the “Plan Agent”), in writing prior to any |

33Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| dividend record date; otherwise such termination or resumption will be effective with respect to any subsequently declared dividend or other distribution. | |

| If a stockholder’s shares are held in the name of a brokerage firm, bank or other nominee, the stockholder can ask the firm or nominee to participate in the Plan on the stockholder’s behalf. If the firm or nominee does not offer the Plan, dividends will be paid in cash to the stockholder of record. A firm or nominee may reinvest a stockholder’s cash dividends in shares of the Fund on terms that differ from the terms of the Plan. | |

| Whenever the Fund declares a dividend on shares payable in cash, participants in the Plan will receive the equivalent in shares acquired by the Plan Agent either (i) through receipt of additional unissued but authorized shares from the Fund or (ii) by purchase of outstanding shares on the New York Stock Exchange or elsewhere. If, on the payment date for any dividend, the net asset value per share is equal to or less than the market price per share plus estimated brokerage trading fees (market premium), the Plan Agent will invest the dividend amount in newly issued shares. The number of newly issued shares to be credited to each account will be determined by dividing the dollar amount of the dividend by the net asset value per share on the date the shares are issued, provided that the maximum discount from the then current market price per share on the date of issuance does not exceed 5%. If, on the payment date for any dividend, the net asset value per share is greater than the market value (market discount), the Plan Agent will invest the dividend amount in shares acquired in open-market purchases. There are no brokerage charges with respect to newly issued shares. However, each participant will pay a pro rata share of brokerage trading fees incurred with respect to the Plan Agent’s open-market purchases. Participating in the Plan does not relieve stockholders from any federal, state or local taxes which may be due on dividends paid in any taxable year. Stockholders holding Plan shares in a brokerage account may be able to transfer the shares to another broker and continue to participate in the Plan. | |

| E. | Risks |

| The value of securities held by the Fund may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political or regulatory conditions, recessions, the spread of infectious illness or other public health issues, inflation, changes in interest rates, armed conflict such as between Russia and Ukraine or in the Middle East, sanctions against Russia, |

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2434

| other nations or individuals or companies and possible countermeasures, lack of liquidity in the bond markets or adverse investor sentiment. In the past several years, financial markets have experienced increased volatility, depressed valuations, decreased liquidity and heightened uncertainty. These conditions may continue, recur, worsen or spread. Inflation and interest rates have increased and may rise further. These circumstances could adversely affect the value and liquidity of the Fund’s investments and negatively impact the Fund’s performance. | |

| The long-term impact of the COVID-19 pandemic and its subsequent variants on economies, markets, industries and individual issuers, are not known. Some sectors of the economy and individual issuers have experienced or may experience particularly large losses. Periods of extreme volatility in the financial markets, reduced liquidity of many instruments, increased government debt, inflation, and disruptions to supply chains, consumer demand and employee availability, may continue for some time. Following Russia’s invasion of Ukraine, Russian securities lost all, or nearly all, their market value. Other securities or markets could be similarly affected by past or future political, geopolitical or other events or conditions. | |

| Governments and central banks, including the U.S. Federal Reserve, have taken extraordinary and unprecedented actions to support local and global economies and the financial markets. These actions have resulted in significant expansion of public debt, including in the U.S. The consequences of high public debt, including its future impact on the economy and securities markets, may not be known for some time. | |

| The U.S. and other countries are periodically involved in disputes over trade and other matters, which may result in tariffs, investment restrictions and adverse impacts on affected companies and securities. For example, the U.S. has imposed tariffs and other trade barriers on Chinese exports, has restricted sales of certain categories of goods to China, and has established barriers to investments in China. Trade disputes may adversely affect the economies of the U.S. and its trading partners, as well as companies directly or indirectly affected and financial markets generally. If the political climate between the U.S. and China does not improve or continues to deteriorate, if China were to attempt unification of Taiwan by force, or if other geopolitical conflicts develop or get worse, economies, markets and individual securities may be severely affected both regionally and globally, and the value of the Fund’s assets may go down. |

35Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| At times, the Fund’s investments may represent industries or industry sectors that are interrelated or have common risks, making the Fund more susceptible to any economic, political, or regulatory developments or other risks affecting those industries and sectors. | |

| Under normal circumstances, the Fund will invest substantially all of its assets in municipal securities. The municipal bond market can be susceptible to unusual volatility, particularly for lower-rated and unrated securities. Liquidity can be reduced unpredictably in response to overall economic conditions or credit tightening. Municipal issuers may be adversely affected by rising health care costs, increasing unfunded pension liabilities, and by the phasing out of federal programs providing financial support. Unfavorable conditions and developments relating to projects financed with municipal securities can result in lower revenues to issuers of municipal securities, potentially resulting in defaults. Issuers often depend on revenues from these projects to make principal and interest payments. The value of municipal securities can also be adversely affected by changes in the financial condition of one or more individual municipal issuers or insurers of municipal issuers, regulatory and political developments, tax law changes or other legislative actions, and by uncertainties and public perceptions concerning these and other factors. Municipal securities may be more susceptible to down-grades or defaults during recessions or similar periods of economic stress. Financial difficulties of municipal issuers may continue or get worse, particularly in the event of economic or market turmoil or a recession. To the extent the Fund invests significantly in a single state (including California and Massachusetts), city, territory (including Puerto Rico), or region, or in securities the payments on which are dependent upon a single project or source of revenues, or that relate to a sector or industry, including health care facilities, education, transportation, special revenues and pollution control, the Fund will be more susceptible to associated risks and developments. | |

| The Fund invests in below investment grade (high yield) municipal securities. Debt securities rated below investment grade are commonly referred to as “junk bonds” and are considered speculative with respect to the issuer’s capacity to pay interest and repay principal. These securities involve greater risk of loss, are subject to greater price volatility, and may be less liquid and more difficult to value, especially during periods of economic uncertainty or change, than higher rated debt securities. | |

| The market prices of the Fund’s fixed income securities may fluctuate significantly when interest rates change. The value of your investment will generally go down when interest rates rise. A rise in rates tends to |

Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/2436

| have a greater impact on the prices of longer term or duration securities. For example, if interest rates increase by 1%, the value of a Fund’s portfolio with a portfolio duration of ten years would be expected to decrease by 10%, all other things being equal. In recent years interest rates and credit spreads in the U.S. have been at historic lows. The U.S. Federal Reserve has raised certain interest rates, and interest rates may continue to go up. A general rise in interest rates could adversely affect the price and liquidity of fixed income securities. The maturity of a security may be significantly longer than its effective duration. A security’s maturity and other features may be more relevant than its effective duration in determining the security’s sensitivity to other factors affecting the issuer or markets generally, such as changes in credit quality or in the yield premium that the market may establish for certain types of securities (sometimes called “credit spread”). In general, the longer its maturity the more a security may be susceptible to these factors. When the credit spread for a fixed income security goes up, or “widens”, the value of the security will generally go down. | |

| If an issuer or guarantor of a security held by the Fund or a counterparty to a financial contract with the Fund defaults on its obligation to pay principal and/or interest, has its credit rating downgraded or is perceived to be less creditworthy, or the credit quality or value of any underlying assets declines, the value of your investment will typically decline. Changes in actual or perceived creditworthiness may occur quickly. The Fund could be delayed or hindered in its enforcement of rights against an issuer, guarantor or counterparty. | |

| With the increased use of technologies such as the Internet to conduct business, the Fund is susceptible to operational, information security and related risks. While the Fund’s Adviser has established business continuity plans in the event of, and risk management systems to prevent, limit or mitigate, such cyber-attacks, there are inherent limitations in such plans and systems, including the possibility that certain risks have not been identified. Furthermore, the Fund cannot control the cybersecurity plans and systems put in place by service providers to the Fund such as the Fund’s custodian and accounting agent, and the Fund’s transfer agent. In addition, many beneficial owners of Fund shares hold them through accounts at broker-dealers, retirement platforms and other financial market participants over which neither the Fund nor the Adviser exercises control. Each of these may in turn rely on service providers to them, which are also subject to the risk of cyber-attacks. Cybersecurity failures or breaches at the Adviser or the Fund’s service providers or intermediaries have the ability to cause disruptions and impact business operations, potentially resulting in |

37Pioneer Municipal High Income Fund, Inc. | Annual Report | 4/30/24

| financial losses, interference with the Fund’s ability to calculate its net asset value, impediments to trading, the inability of Fund stockholders to effect share purchases or sales or receive distributions, loss of or unauthorized access to private stockholder information and violations of applicable privacy and other laws, regulatory fines, penalties, reputational damage, or additional compliance costs. Such costs and losses may not be covered under any insurance. In addition, maintaining vigilance against cyber-attacks may involve substantial costs over time, and system enhancements may themselves be subject to cyber-attacks. | |

| F. | Statement of Cash Flows |

| Information on financial transactions which have been settled through the receipt or disbursement of cash or restricted cash is presented in the Statement of Cash Flows. Cash as presented in the Fund’s Statement of Assets and Liabilities includes cash on hand at the Fund’s custodian bank and does not include any short-term investments. As of and for the year ended April 30, 2024, the Fund had restricted cash in the form of futures collateral on the Statement of Assets and Liabilities. | |

| G. | Futures Contracts |

| The Fund may enter into futures transactions in order to attempt to hedge against changes in interest rates, securities prices and currency exchange rates or to seek to increase total return. Futures contracts are types of derivatives. | |

| All futures contracts entered into by the Fund are traded on a futures exchange. Upon entering into a futures contract, the Fund is required to deposit with a broker an amount of cash or securities equal to the minimum “initial margin” requirements of the associated futures exchange. The amount of cash deposited with the broker as collateral at April 30, 2024 is recorded as “Futures collateral” on the Statement of Assets and Liabilities. | |

| Subsequent payments for futures contracts (“variation margin”) are paid or received by the Fund, depending on the daily fluctuation in the value of the contracts, and are recorded by the Fund as unrealized appreciation or depreciation. Cash received from or paid to the broker related to previous margin movement is held in a segregated account at the broker and is recorded as either “Due from broker for futures” or “Due to broker for futures” on the Statement of Assets and Liabilities. When the contract is closed, the Fund realizes a gain or loss equal to the difference between the opening and closing value of the contract as well as any fluctuation in foreign currency exchange rates where applicable. Futures contracts are subject to market risk, interest rate risk and currency |