Filed Pursuant To Rule 433

Registration No. 333-217785

April 27, 2018

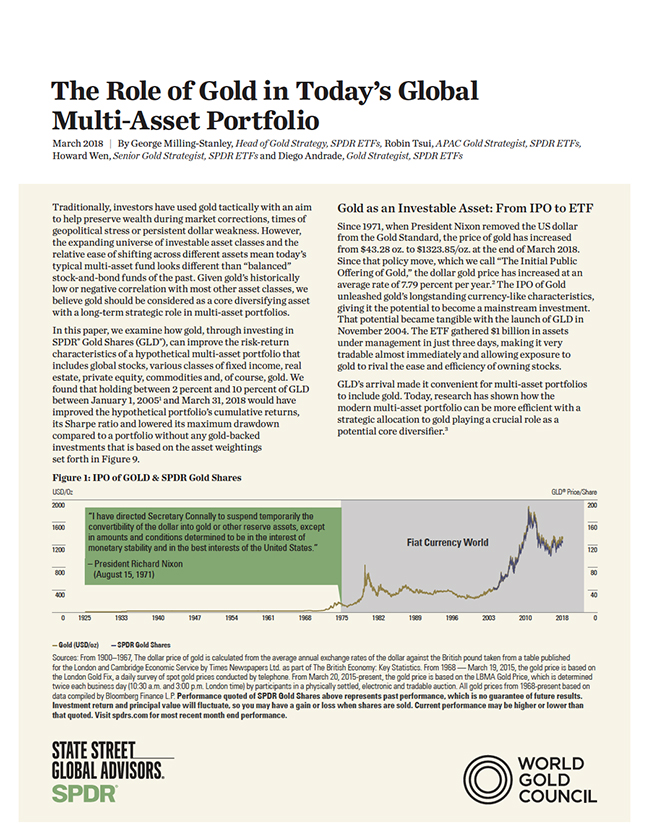

The Role of Gold in Today’s Global Multi-Asset Portfolio March 2018 | By George Milling-Stanley, Head of Gold Strategy, SPDR ETFs, Robin Tsui, APAC Gold Strategist, SPDR ETFs, Howard Wen, Senior Gold Strategist, SPDR ETFs and Diego Andrade, Gold Strategist, SPDR ETFs Traditionally, investors have used gold tactically with an aim to help preserve wealth during market corrections, times of geopolitical stress or persistent dollar weakness. However, the expanding universe of investable asset classes and the relative ease of shifting across different assets mean today’s typical multi-asset fund looks different than “balanced” stock-and-bond funds of the past. Given gold’s historically low or negative correlation with most other asset classes, we believe gold should be considered as a core diversifying asset with a long-term strategic role in multi-asset portfolios. In this paper, we examine how gold, through investing in SPDR® Gold Shares (GLD®), can improve the risk-return characteristics of a hypothetical multi-asset portfolio that includes global stocks, various classes of fixed income, real estate, private equity, commodities and, of course, gold. We found that holding between 2 percent and 10 percent of GLD between January 1, 20051 and March 31, 2018 would have improved the hypothetical portfolio’s cumulative returns, its Sharpe ratio and lowered its maximum drawdown compared to a portfolio without any gold-backed investments that is based on the asset weightings set forth in Figure 9. Figure 1: IPO of GOLD & SPDR Gold Shares Gold as an Investable Asset: From IPO to ETF Since 1971, when President Nixon removed the US dollar from the Gold Standard, the price of gold has increased from $43.28 oz. to $1323.85/oz. at the end of March 2018. Since that policy move, which we call “The Initial Public Offering of Gold,” the dollar gold price has increased at an average rate of 7.79 percent per year.2 The IPO of Gold unleashed gold’s longstanding currency-like characteristics, giving it the potential to become a mainstream investment. That potential became tangible with the launch of GLD in November 2004. The ETF gathered $1 billion in assets under management in just three days, making it very tradable almost immediately and allowing exposure to gold to rival the ease and efficiency of owning stocks. GLD’s arrival made it convenient for multi-asset portfolios to include gold. Today, research has shown how the modern multi-asset portfolio can be more efficient with a strategic allocation to gold playing a crucial role as a potential core diversifier.3 — Gold (USD/oz) — SPDR Gold Shares Sources: From 1900–1967, The dollar price of gold is calculated from the average annual exchange rates of the dollar against the British pound taken from a table published for the London and Cambridge Economic Service by Times Newspapers Ltd. as part of The British Economy: Key Statistics. From 1968 — March 19, 2015, the gold price is based on the London Gold Fix, a daily survey of spot gold prices conducted by telephone. From March 20, 2015-present, the gold price is based on the LBMA Gold Price, which is determined twice each business day (10:30 a.m. and 3:00 p.m. London time) by participants in a physically settled, electronic and tradable auction. All gold prices from 1968-present based on data compiled by Bloomberg Finance L.P. Performance quoted of SPDR Gold Shares above represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, so you may have a gain or loss when shares are sold. Current performance may be higher or lower than that quoted. Visit spdrs.com for most recent month end performance.

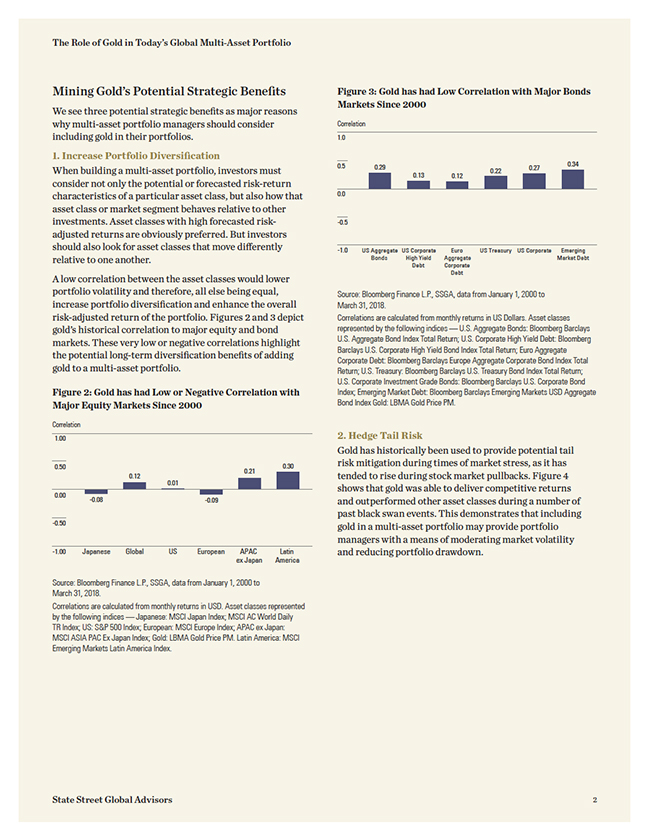

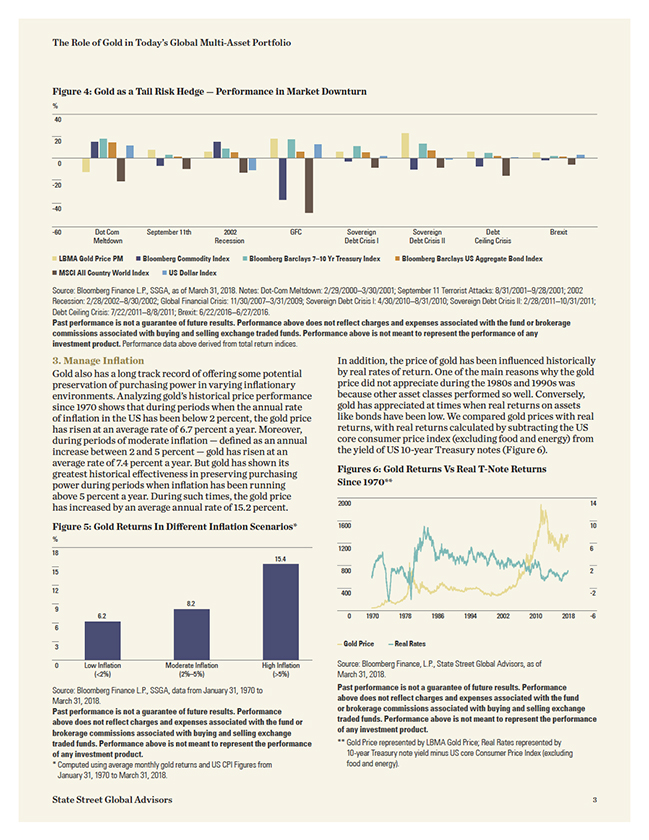

The Role of Gold in Today’s Global Multi-Asset Portfolio Mining Gold’s Potential Strategic Benefits We see three potential strategic benefits as major reasons why multi-asset portfolio managers should consider including gold in their portfolios. 1. Increase Portfolio Diversification When building a multi-asset portfolio, investors must consider not only the potential or forecasted risk-return characteristics of a particular asset class, but also how that asset class or market segment behaves relative to other investments. Asset classes with high forecasted risk-adjusted returns are obviously preferred. But investors should also look for asset classes that move differently relative to one another. A low correlation between the asset classes would lower portfolio volatility and therefore, all else being equal, increase portfolio diversification and enhance the overall risk-adjusted return of the portfolio. Figures 2 and 3 depict gold’s historical correlation to major equity and bond markets. These very low or negative correlations highlight the potential long-term diversification benefits of adding gold to a multi-asset portfolio. Figure 2: Gold has had Low or Negative Correlation with Major Equity Markets Since 2000 Correlation 1.00 Source: Bloomberg Finance L.P., SSGA, data from January 1, 2000 to March 31, 2018. Correlations are calculated from monthly returns in USD. Asset classes represented by the following indices — Japanese: MSCI Japan Index; MSCI AC World Daily TR Index; US: S&P 500 Index; European: MSCI Europe Index; APAC ex Japan: MSCI ASIA PAC Ex Japan Index; Gold: LBMA Gold Price PM. Latin America: MSCI Emerging Markets Latin America Index. Figure 3: Gold has had Low Correlation with Major Bonds Markets Since 2000 Correlation 1.0 Source: Bloomberg Finance L.P., SSGA, data from January 1, 2000 to March 31, 2018. Correlations are calculated from monthly returns in US Dollars. Asset classes represented by the following indices — U.S. Aggregate Bonds: Bloomberg Barclays U.S. Aggregate Bond Index Total Return; U.S. Corporate High Yield Debt: Bloomberg Barclays U.S. Corporate High Yield Bond Index Total Return; Euro Aggregate Corporate Debt: Bloomberg Barclays Europe Aggregate Corporate Bond Index Total Return; U.S. Treasury: Bloomberg Barclays U.S. Treasury Bond Index Total Return; U.S. Corporate Investment Grade Bonds: Bloomberg Barclays U.S. Corporate Bond Index; Emerging Market Debt: Bloomberg Barclays Emerging Markets USD Aggregate Bond Index Gold: LBMA Gold Price PM. 2. Hedge Tail Risk Gold has historically been used to provide potential tail risk mitigation during times of market stress, as it has tended to rise during stock market pullbacks. Figure 4 shows that gold was able to deliver competitive returns and outperformed other asset classes during a number of past black swan events. This demonstrates that including gold in a multi-asset portfolio may provide portfolio managers with a means of moderating market volatility and reducing portfolio drawdown. State Street Global Advisors 2

The Role of Gold in Today’s Global Multi-Asset Portfolio Figure 4: Gold as a Tail Risk Hedge — Performance in Market Downturn Source: Bloomberg Finance L.P., SSGA, as of March 31, 2018. Notes: Dot-Com Meltdown: 2/29/2000–3/30/2001; September 11 Terrorist Attacks: 8/31/2001–9/28/2001; 2002 Recession: 2/28/2002–8/30/2002; Global Financial Crisis: 11/30/2007–3/31/2009; Sovereign Debt Crisis I: 4/30/2010–8/31/2010; Sovereign Debt Crisis II: 2/28/2011–10/31/2011; Debt Ceiling Crisis: 7/22/2011–8/8/2011; Brexit: 6/22/2016–6/27/2016. Past performance is not a guarantee of future results. Performance above does not reflect charges and expenses associated with the fund or brokerage commissions associated with buying and selling exchange traded funds. Performance above is not meant to represent the performance of any investment product. Performance data above derived from total return indices. 3. Manage Inflation Gold also has a long track record of offering some potential preservation of purchasing power in varying inflationary environments. Analyzing gold’s historical price performance since 1970 shows that during periods when the annual rate of inflation in the US has been below 2 percent, the gold price has risen at an average rate of 6.7 percent a year. Moreover, during periods of moderate inflation — defined as an annual increase between 2 and 5 percent — gold has risen at an average rate of 7.4 percent a year. But gold has shown its greatest historical effectiveness in preserving purchasing power during periods when inflation has been running above 5 percent a year. During such times, the gold price has increased by an average annual rate of 15.2 percent. Figure 5: Gold Returns In Different Inflation Scenarios* In addition, the price of gold has been influenced historically by real rates of return. One of the main reasons why the gold price did not appreciate during the 1980s and 1990s was because other asset classes performed so well. Conversely, gold has appreciated at times when real returns on assets like bonds have been low. We compared gold prices with real returns, with real returns calculated by subtracting the US core consumer price index (excluding food and energy) from the yield of US 10-year Treasury notes (Figure 6). Figures 6: Gold Returns Vs Real T-Note Returns Since 1970** Source: Bloomberg Finance, L.P., State Street Global Advisors, as of March 31, 2018. Source: Bloomberg Finance L.P., SSGA, data from January 31, 1970 to March 31, 2018. Past performance is not a guarantee of future results. Performance above does not reflect charges and expenses associated with the fund or brokerage commissions associated with buying and selling exchange traded funds. Performance above is not meant to represent the performance of any investment product. Computed using average monthly gold returns and US CPI Figures from January 31, 1970 to March 31, 2018. Past performance is not a guarantee of future results. Performance above does not reflect charges and expenses associated with the fund or brokerage commissions associated with buying and selling exchange traded funds. Performance above is not meant to represent the performance of any investment product. Gold Price represented by LBMA Gold Price; Real Rates represented by 10-year Treasury note yield minus US core Consumer Price Index (excluding food and energy). State Street Global Advisors 3

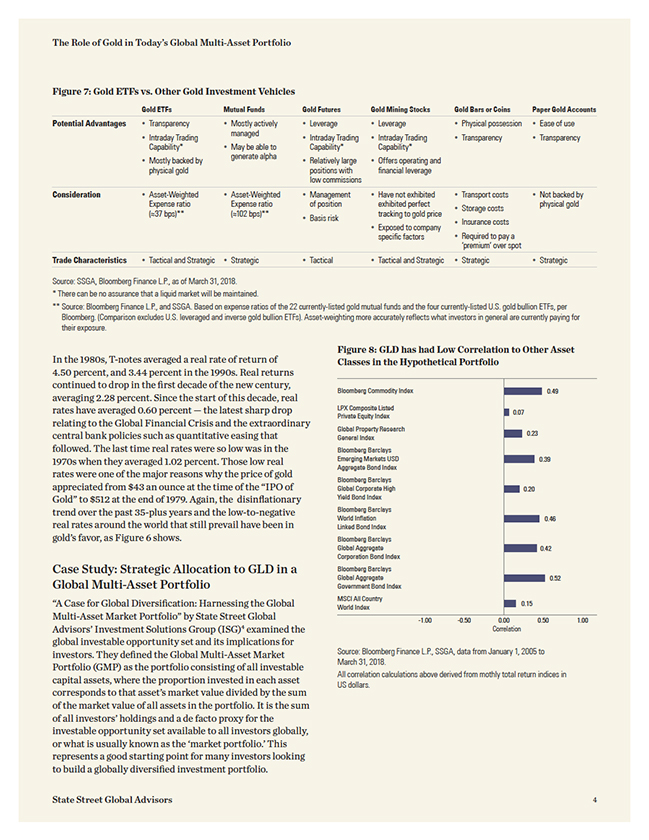

The Role of Gold in Today’s Global Multi-Asset Portfolio Figure 7: Gold ETFs vs. Other Gold Investment Vehicles Gold ETFs Mutual Funds Gold Futures Gold Mining Stocks Gold Bars or Coins Paper Gold Accounts Potential Advantages • Transparency • Intraday Trading Capability* • Mostly backed by physical gold Mostly actively managed May be able to generate alpha • Leverage • Leverage • Physical possession • Ease of use • Intraday Trading • Intraday Trading • Transparency • Transparency Capability* Capability* Relatively large• Offers operating and positions with financial leverage low commissions Consideration • Asset-Weighted • Asset-Weighted • Management Expense ratio Expense ratio of position (?37 bps)** (?102 bps)** • Basis risk Have not exhibited exhibited perfect tracking to gold price Exposed to company specific factors Transport costs Storage costs Insurance costs Required to pay a ‘premium’ over spot Not backed by physical gold Trade Characteristics • Tactical and Strategic • Strategic • Tactical • Tactical and Strategic • Strategic • Strategic Source: SSGA, Bloomberg Finance L.P., as of March 31, 2018. * There can be no assurance that a liquid market will be maintained. Source: Bloomberg Finance L.P., and SSGA. Based on expense ratios of the 22 currently-listed gold mutual funds and the four currently-listed U.S. gold bullion ETFs, per Bloomberg. (Comparison excludes U.S. leveraged and inverse gold bullion ETFs). Asset-weighting more accurately reflects what investors in general are currently paying for their exposure. In the 1980s, T-notes averaged a real rate of return of 4.50 percent, and 3.44 percent in the 1990s. Real returns continued to drop in the first decade of the new century, averaging 2.28 percent. Since the start of this decade, real rates have averaged 0.60 percent — the latest sharp drop relating to the Global Financial Crisis and the extraordinary central bank policies such as quantitative easing that followed. The last time real rates were so low was in the 1970s when they averaged 1.02 percent. Those low real rates were one of the major reasons why the price of gold appreciated from $43 an ounce at the time of the “IPO of Gold” to $512 at the end of 1979. Again, the disinflationary trend over the past 35-plus years and the low-to-negative real rates around the world that still prevail have been in gold’s favor, as Figure 6 shows. Case Study: Strategic Allocation to GLD in a Global Multi-Asset Portfolio “A Case for Global Diversification: Harnessing the Global Multi-Asset Market Portfolio” by State Street Global Advisors’ Investment Solutions Group (ISG)4 examined the global investable opportunity set and its implications for investors. They defined the Global Multi-Asset Market Portfolio (GMP) as the portfolio consisting of all investable capital assets, where the proportion invested in each asset corresponds to that asset’s market value divided by the sum of the market value of all assets in the portfolio. It is the sum of all investors’ holdings and a de facto proxy for the investable opportunity set available to all investors globally, or what is usually known as the ‘market portfolio.’ This represents a good starting point for many investors looking to build a globally diversified investment portfolio. Figure 8: GLD has had Low Correlation to Other Asset Classes in the Hypothetical Portfolio Source: Bloomberg Finance L.P., SSGA, data from January 1, 2005 to March 31, 2018. All correlation calculations above derived from mothly total return indices in US dollars. State Street Global Advisors 4

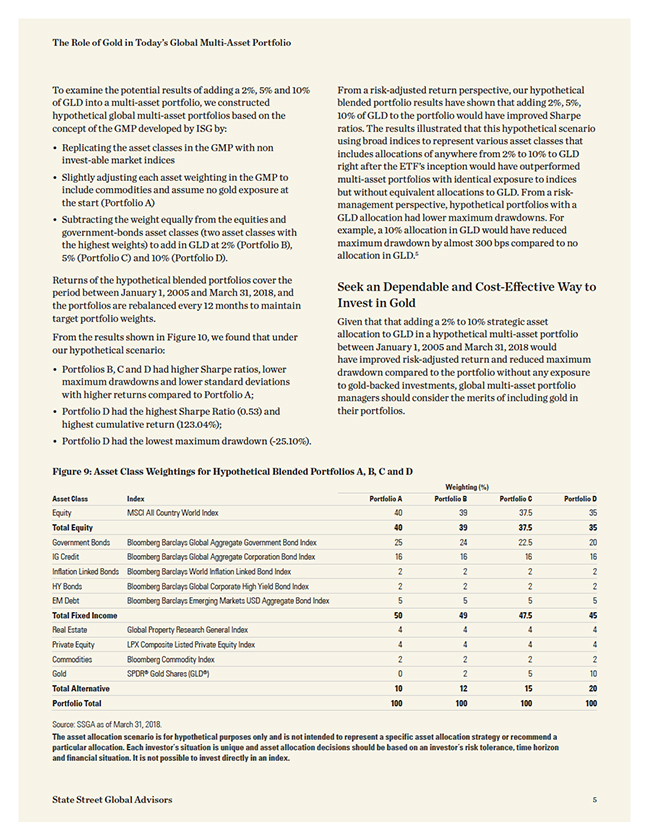

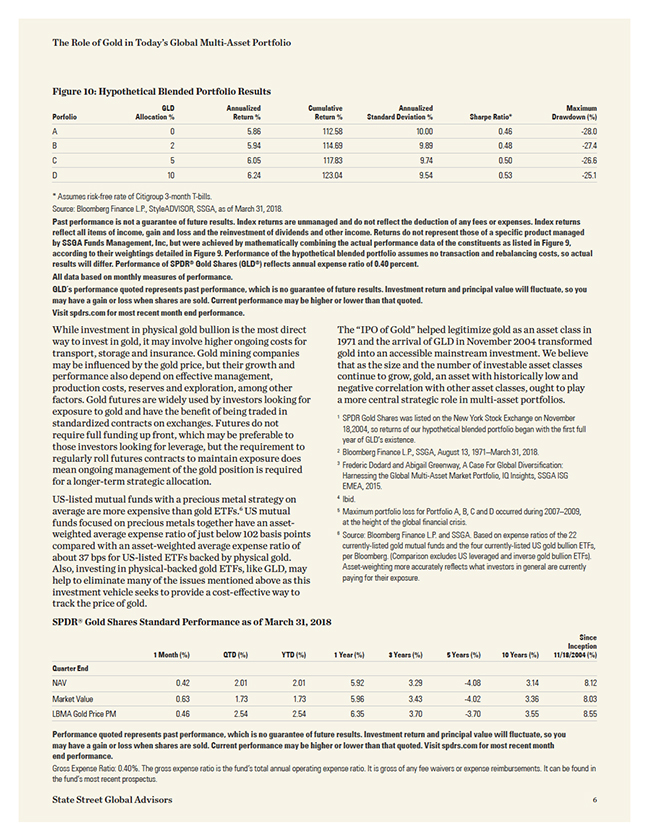

The Role of Gold in Today’s Global Multi-Asset Portfolio To examine the potential results of adding a 2%, 5% and 10% of GLD into a multi-asset portfolio, we constructed hypothetical global multi-asset portfolios based on the concept of the GMP developed by ISG by: Replicating the asset classes in the GMP with non invest-able market indices Slightly adjusting each asset weighting in the GMP to include commodities and assume no gold exposure at the start (Portfolio A) Subtracting the weight equally from the equities and government-bonds asset classes (two asset classes with the highest weights) to add in GLD at 2% (Portfolio B), 5% (Portfolio C) and 10% (Portfolio D). Returns of the hypothetical blended portfolios cover the period between January 1, 2005 and March 31, 2018, and the portfolios are rebalanced every 12 months to maintain target portfolio weights. From the results shown in Figure 10, we found that under our hypothetical scenario: Portfolios B, C and D had higher Sharpe ratios, lower maximum drawdowns and lower standard deviations with higher returns compared to Portfolio A; Portfolio D had the highest Sharpe Ratio (0.53) and highest cumulative return (123.04%); Portfolio D had the lowest maximum drawdown (-25.10%). From a risk-adjusted return perspective, our hypothetical blended portfolio results have shown that adding 2%, 5%, 10% of GLD to the portfolio would have improved Sharpe ratios. The results illustrated that this hypothetical scenario using broad indices to represent various asset classes that includes allocations of anywhere from 2% to 10% to GLD right after the ETF’s inception would have outperformed multi-asset portfolios with identical exposure to indices but without equivalent allocations to GLD. From a risk-management perspective, hypothetical portfolios with a GLD allocation had lower maximum drawdowns. For example, a 10% allocation in GLD would have reduced maximum drawdown by almost 300 bps compared to no allocation in GLD.5 Seek an Dependable and Cost-Effective Way to Invest in Gold Given that that adding a 2% to 10% strategic asset allocation to GLD in a hypothetical multi-asset portfolio between January 1, 2005 and March 31, 2018 would have improved risk-adjusted return and reduced maximum drawdown compared to the portfolio without any exposure to gold-backed investments, global multi-asset portfolio managers should consider the merits of including gold in their portfolios. Figure 9: Asset Class Weightings for Hypothetical Blended Portfolios A, B, C and D Weighting (%) Asset Class Index Portfolio A Portfolio B Portfolio C Portfolio D Equity MSCI All Country World Index 40 39 37.5 35 Total Equity 40 39 37.5 35 Government Bonds Bloomberg Barclays Global Aggregate Government Bond Index 25 24 22.5 20 IG Credit Bloomberg Barclays Global Aggregate Corporation Bond Index 16 16 16 16 Inflation Linked Bonds Bloomberg Barclays World Inflation Linked Bond Index 2 2 2 2 HY Bonds Bloomberg Barclays Global Corporate High Yield Bond Index 2 2 2 2 EM Debt Bloomberg Barclays Emerging Markets USD Aggregate Bond Index 5 5 5 5 Total Fixed Income 50 49 47.5 45 Real Estate Global Property Research General Index 4 4 4 4 Private Equity LPX Composite Listed Private Equity Index 4 4 4 4 Commodities Bloomberg Commodity Index 2 2 2 2 Gold SPDR® Gold Shares (GLD®) 0 2 5 10 Total Alternative 10 12 15 20 Portfolio Total 100 100 100 100 Source: SSGA as of March 31, 2018. The asset allocation scenario is for hypothetical purposes only and is not intended to represent a specific asset allocation strategy or recommend a particular allocation. Each investor’s situation is unique and asset allocation decisions should be based on an investor’s risk tolerance, time horizon and financial situation. It is not possible to invest directly in an index. State Street Global Advisors 5

The Role of Gold in Today’s Global Multi-Asset Portfolio Figure 10: Hypothetical Blended Portfolio Results GLD Annualized Cumulative Annualized Maximum Porfolio Allocation % Return % Return % Standard Deviation % Sharpe Ratio* Drawdown (%) A 0 5.86 112.58 10.00 0.46 -28.0 B 2 5.94 114.69 9.89 0.48 -27.4 C 5 6.05 117.83 9.74 0.50 -26.6 D 10 6.24 123.04 9.54 0.53 -25.1 * Assumes risk-free rate of Citigroup 3-month T-bills. Source: Bloomberg Finance L.P., StyleADVISOR, SSGA, as of March 31, 2018. Past performance is not a guarantee of future results. Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income. Returns do not represent those of a specific product managed by SSGA Funds Management, Inc, but were achieved by mathematically combining the actual performance data of the constituents as listed in Figure 9, according to their weightings detailed in Figure 9. Performance of the hypothetical blended portfolio assumes no transaction and rebalancing costs, so actual results will differ. Performance of SPDR® Gold Shares (GLD®) reflects annual expense ratio of 0.40 percent. All data based on monthly measures of performance. GLD’s performance quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, so you may have a gain or loss when shares are sold. Current performance may be higher or lower than that quoted. Visit spdrs.com for most recent month end performance. While investment in physical gold bullion is the most direct way to invest in gold, it may involve higher ongoing costs for transport, storage and insurance. Gold mining companies may be influenced by the gold price, but their growth and performance also depend on effective management, production costs, reserves and exploration, among other factors. Gold futures are widely used by investors looking for exposure to gold and have the benefit of being traded in standardized contracts on exchanges. Futures do not require full funding up front, which may be preferable to those investors looking for leverage, but the requirement to regularly roll futures contracts to maintain exposure does mean ongoing management of the gold position is required for a longer-term strategic allocation. US-listed mutual funds with a precious metal strategy on average are more expensive than gold ETFs.6 US mutual funds focused on precious metals together have an asset-weighted average expense ratio of just below 102 basis points compared with an asset-weighted average expense ratio of about 37 bps for US-listed ETFs backed by physical gold. Also, investing in physical-backed gold ETFs, like GLD, may help to eliminate many of the issues mentioned above as this investment vehicle seeks to provide a cost-effective way to track the price of gold. SPDR® Gold Shares Standard Performance as of March 31, 2018 The “IPO of Gold” helped legitimize gold as an asset class in 1971 and the arrival of GLD in November 2004 transformed gold into an accessible mainstream investment. We believe that as the size and the number of investable asset classes continue to grow, gold, an asset with historically low and negative correlation with other asset classes, ought to play a more central strategic role in multi-asset portfolios. SPDR Gold Shares was listed on the New York Stock Exchange on November 18,2004, so returns of our hypothetical blended portfolio began with the first full year of GLD’s existence. Bloomberg Finance L.P., SSGA, August 13, 1971–March 31, 2018. Frederic Dodard and Abigail Greenway, A Case For Global Diversification: Harnessing the Global Multi-Asset Market Portfolio, IQ Insights, SSGA ISG EMEA, 2015. Ibid. Maximum portfolio loss for Portfolio A, B, C and D occurred during 2007–2009, at the height of the global financial crisis. Source: Bloomberg Finance L.P. and SSGA. Based on expense ratios of the 22 currently-listed gold mutual funds and the four currently-listed US gold bullion ETFs, per Bloomberg. (Comparison excludes US leveraged and inverse gold bullion ETFs). Asset-weighting more accurately reflects what investors in general are currently paying for their exposure. Since Inception 1 Month (%) QTD (%) YTD (%) 1 Year (%) 3 Years (%) 5 Years (%) 10 Years (%) 11/18/2004 (%) Quarter End NAV 0.42 2.01 2.01 5.92 3.29 -4.08 3.14 8.12 Market Value 0.63 1.73 1.73 5.96 3.43 -4.02 3.36 8.03 LBMA Gold Price PM 0.46 2.54 2.54 6.35 3.70 -3.70 3.55 8.55 Performance quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, so you may have a gain or loss when shares are sold. Current performance may be higher or lower than that quoted. Visit spdrs.com for most recent month end performance. Gross Expense Ratio: 0.40%. The gross expense ratio is the fund’s total annual operating expense ratio. It is gross of any fee waivers or expense reimbursements. It can be found in the fund’s most recent prospectus. State Street Global Advisors 6

The Role of Gold in Today’s Global Multi-Asset Portfolio Glossary 10-Year U.S. Treasury Note A debt obligation issued by the US government that matures in 10 years. The debt pays interest at a fixed rate once every six months and pays the face value to the holder at maturity. Black Swan An event that is beyond what is normally in the realm of what is expected and is thus very difficult to foresee. The term was made popular by Nassim Nicholas Taleb, a finance professor and trader who has authored a number of books on uncertainty, including “The Black Swan,” a discussion on the impact of random events. Bloomberg Barclays Emerging Markets USD Aggregate Index A hard currency emerging markets debt benchmark that includes US dollar-denominated debt from sovereign, quasi-sovereign, and corporate issuers in the developing markets. Bloomberg Barclays Euro-Aggregate Corporate Bond Index A rules-based benchmark measuring investment grade, euro-denominated, fixed rate issued by corporations. Only bonds with a maturity of 1 year and above are eligible. Bloomberg Barclays Global Aggregate Corporate Bond Index A benchmark of global investment-grade, fixed-rate corporate debt. This multi-currency benchmark includes bonds from developed and emerging markets issuers within the industrial, utility and financial sectors. Bloomberg Barclays Global Aggregate Government Bond Index A benchmark that provides a broad-based measure of the global investment-grade fixed income markets, with a focus on Treasuries and government-related debt from both developed- and emerging-market issuers. Bloomberg Barclays Global Corporate High Yield Bond Index A multi-currency fixed-income benchmark of the global high yield debt market. The index represents the union of the US High Yield, the Pan-European High Yield, and Emerging Markets (EM) Hard Currency High Yield Indices. The high yield and emerging markets sub-components are mutually exclusive. Bloomberg Barclays World Inflation Linked Bond Index A fixed-income benchmark that measures the performance of investment grade, government inflation-linked debt from 12 different developed-market countries. Bloomberg Barclays U.S. Aggregate Bond Index A benchmark that provides a measure of the performance of the U.S. dollar denominated investment grade bond market. The “Agg” includes investment-grade government bonds, investment-grade corporate bonds, mortgage pass through securities, commercial mortgage backed securities and asset backed securities that are publicly for sale in the US. Bloomberg Barclays U.S. Corporate Bond Index A fixed-income benchmark that measures the investment-grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers. Bloomberg Barclays Emerging Markets USD Aggregate Index A hard currency emerging markets debt benchmark that includes US dollar-denominated debt from sovereign, quasi-sovereign, and corporate issuers in the developing markets. Bloomberg Barclays U.S. High Yield Corporate Bond Index The Barclays U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included. The index includes both corporate and non-corporate sectors. Bloomberg Barclays U.S. Treasury Bond Index A benchmark of US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index. Bloomberg Commodity Index A broadly diversified commodity price index distributed by Bloomberg Indexes that tracks 22 commodity futures and seven sectors. No one commodity can compose less than 2 percent or more than 15 percent of the index, and no sector can represent more than 33 percent of the index. Brexit An abbreviation of the term “British Exit” referring to the UK referendum on June 23, 2016 that resulted in the country’s decision to withdraw from the European Union. CPI, or Consumer Price Index A widely used measure of inflation at the consumer level that helps to evaluate changes in cost of living. Debt Ceiling Crisis A contentious debate in July 2011 regarding the maximum amount of money that the US government should be allowed to borrow. Congress did end up immediately raising the “debt ceiling” by $400 billion, from $14.3 trillion to $14.7 trillion, with the possibility of future increases included in the agreement as well, but the contentious nature of the debate led Standard and Poor’s to downgrade the US’credit rating from AAA to AA+, even though the U.S. did not default. Fiat Currency Currency that a government declares to be legal tender, but that it is not backed by a physical commodity. The value of fiat money is linked to supply and demand rather than the value of the material that the money is made of, such as gold or silver historically. Fiat money’s value is instead based solely on the faith and credit of the economy. Global Financial Crisis The economic crisis that occurred from 2007-2009 that is generally considered biggest economic challenge since the Great Depression of the 1930s. The GFC was triggered largely by the sub-prime mortgage crisis, which led to the collapse of systemically vital US investment banks such as Lehman Brothers. The crisis began with the collapse of two Bear Stearns hedge funds in June 2007, and the stabilization period began in late 2008 and continued until the end of 2009. Global Property Research General Index A broad-based global real estate benchmark that contains all listed real estate companies that conform to General Property Research’s index-qualification rules, bringing the number of index constituents to more than 650. The index’s inception date was Dec. 31 1983. Gold Standard A monetary standard under which the basic unit of currency is defined by a stated quantity of gold. In 1971 US President Richard Nixon ended the ability to convert US dollars into gold at the fixed price of $35 per ounce. LBMA Gold Price The LBMA Gold Price is determined twice each business day — 10:30 a.m. London time (i.e., the LBMA Gold Price AM) and 3:00 p.m. London time (i.e., the LBMA Gold Price PM) by the participants in a physically settled, electronic and tradable auction. LPX Composite Listed Private Equity Index A broad global listed private equity index whose number of constituents is not limited. The LPX Composite includes all major private equity companies listed on global stock exchanges that fulfils the index provider’s liquidity criteria. The index composition is well diversified across listed private equity categories, styles, regions and vintage years. The index has two versions: a price index (PI) and a total return index (TR) that includes all payouts. MSCI ACWI Index, or MSCI All Country World Index A free-float weighted global equity index that includes companies in 23 emerging market countries and 23 developed market countries and is designed to be a proxy for most of the investable equities universe around the world. Real Rate of Return The return realized on an investment, usually expressed annually as a percentage, which is adjusted to reflect the effects of inflation or other external factors, on the so-called nominal return. The real rate of return is calculated as follows: Real Rate of Return = Nominal Interest Rate — Inflation. Sharpe Ratio A measure for calculating risk-adjusted returns that has become the industry standard for such calculations. It was developed by Nobel laureate William F. Sharpe. The Sharpe ratio is the average return earned in excess of the risk-free rate per unit of volatility or total risk. The higher the Sharpe ratio the better. Sharpe Ratio A measure for calculating risk-adjusted returns that has become the industry standard for such calculations. It was developed by Nobel laureate William F. Sharpe. The Sharpe ratio is the average return earned in excess of the risk-free rate per unit of volatility or total risk. The higher the Sharpe ratio the better. State Street Global Advisors 7

The Role of Gold in Today’s Global Multi-Asset Portfolio Sovereign Debt Crisis A period of time beginning in 2008 when several European countries on the periphery of the Eurozone became unable to repay or refinance government debt or bail out banks without the assistance of the European Central Bank and the International Monetary Fund. It was brought to heel in July 2012 with the ECB’s pledge to save the euro and the Eurozone at all costs. While the crisis began with the collapse of Icelandic and Irish banks, it became largely focused on southern European countries — mainly Greece, but also Spain, Portugal and even Italy. Standard Deviation A statistical measure of volatility that quantifies the historical dispersion of a security, fund or index around an average. Investors use standard deviation to measure expected risk or volatility, and a higher standard deviation means the security has tended to show higher volatility or price swings in the past. As an example, for a normally distributed return series, about two-thirds of the time returns will be within 1 standard deviation of the average return. ssga.com Hypothetical Blended Portfolio Performance Methodology Returns do not represent those of a fund but were achieved by mathematically combining the actual performance data of MSCI AC World Daily TR Index, Bloomberg Barclays Global Aggregate Government Bond Index, Bloomberg Barclays Aggregate Global Corporate Bond Index, Bloomberg Barclays Emerging Markets Debt Index, Global Property Research General Index, S&P Listed Private Equity Index, Bloomberg Barclays World Inflation Linked Bond Index, Bloomberg Barclays Global Corporate High Yield Index, S&P GSCI Index, and SPDR® Gold Shares (GLD®) between January 1, 2005 and March 31, 2018. Each portfolio is re-balanced at the beginning of each year to maintain target portfolio weights. The performance assumes no transaction and rebalancing costs, so actual results will differ. Important Risk Information The views expressed in this material are the views of George Milling- Stanley, Robin Tsui, Howard Wen and Diego Andrade and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information provided does not constitute investment advice and it should not be relied on as such. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor. All material has been obtained from sources believed to be reliable. There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information. ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETFs’ net asset value. Brokerage commissions and ETF expenses will reduce returns. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress. There can be no assurance that a liquid market will be maintained for ETF shares. Commodities and commodity-index linked securities may be affected by changes in overall market movements, changes in interest rates, and other factors such as weather, disease, embargoes, or political and regulatory developments, as well as trading activity of speculators and arbitrageurs in the underlying commodities. Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. Foreign investments involve greater risks than U.S. investments, including political and economic risks and the risk of currency fluctuations, all of which may be magnified in emerging markets. State Street Global Advisors 8

The Role of Gold in Today’s Global Multi-Asset Portfolio Asset Allocation is a method of diversification which positions assets among major investment categories. Asset Allocation may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss. Diversification does not ensure a profit or guarantee against loss. Investments in small-sized companies may involve greater risks than in those of larger, better known companies. Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions. Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. International Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. Increase in real interest rates can cause the price of inflation-protected debt securities to decrease. Interest payments on inflation-protected debt securities can be unpredictable. Investing in high yield fixed income securities, otherwise known as junk bonds, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Investing in futures is highly risky. Futures positions are considered highly leveraged because the initial margins are significantly smaller than the cash value of the contracts. The smaller the value of the margin in comparison to the cash value of the futures contract, the higher the leverage. There are a number of risks associated with futures investing including but not limited to counterparty credit risk, currency risk, derivatives risk, foreign issuer exposure risk, sector concentration risk, leveraging and liquidity risks. Derivative investments may involve risks such as potential illiquidity of the markets and additional risk of loss of principal. The use of leverage, as part of the investment process, can multiply market movements into greater changes in an investment’s value, thus resulting in increased volatility of returns. Growth stocks may underperform stocks in other broad style categories (and the stock market as a whole) over any period of time and may shift in and out of favor with investors generally, sometimes rapidly. Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs. The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data. Investing in commodities entails significant risk and is not appropriate for all investors. Important risk information Investing involves risk, and you could lose money on an investment in GLD. ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETFs’ net asset value. Brokerage commissions and ETF expenses will reduce returns. Commodities and commodity-index linked securities may be affected by changes in overall market movements, changes in interest rates, and other factors such as weather, disease, embargoes, or political and regulatory developments, as well as trading activity of speculators and arbitrageurs in the underlying commodities. Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs. Diversification does not ensure a profit or guarantee against loss. Investing in commodities entails significant risk and is not appropriate for all investors. Important Information Relating to SPDR Gold Shares Trust (“GLD®”): The SPDR Gold Trust (“GLD”) has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents GLD has filed with the SEC for more complete information about GLD and this offering. Please see the GLD prospectus for a detailed discussion of the risks of investing in GLD shares. When distributed electronically, the GLD prospectus is available by clicking here. You may get these documents for free by visiting EDGAR on the SEC website at sec.gov or by visiting spdrgoldshares.com. Alternatively, the Trust or any authorized participant will arrange to send you the prospectus if you request it by calling 866.320.4053. GLD is not an investment company registered under the Investment Company Act of 1940 (the “1940 Act”) and is not subject to regulation under the Commodity Exchange Act of 1936 (the “CEA”). As a result, shareholders of the Trust do not have the protections associated with ownership of shares in an investment company registered under the 1940 Act or the protections afforded by the CEA. GLD shares trade like stocks, are subject to investment risk and will fluctuate in market value. The value of GLD shares relates directly to the value of the gold held by GLD (less its expenses), and fluctuations in the price of gold could materially and adversely affect an investment in the shares. The price received upon the sale of the shares, which trade at market price, may be more or less than the value of the gold represented by them. GLD does not generate any income, and as GLD regularly sells gold to pay for its ongoing expenses, the amount of gold represented by each Share will decline over time to that extent. The World Gold Council name and logo are a registered trademark and used with the permission of the World Gold Council pursuant to a license agreement. The World Gold Council in not responsible for the content of, and is not liable for the use of or reliance on, this material. World Gold Council is an affiliate of GLD’s sponsor. Standard & Poor’s®, S&P® and SPDR® are registered trademarks of Standard Poor’s Financial Services LLC, a division of S&P Global (S&P); Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones); and these trademarks have been licensed for use by S&P Dow Jones Indices LLC (SPDJI) and sublicensed for certain purposes by State Street Corporation. State Street Corporation’s financial products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates and third party licensors and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability in relation thereto. For more information, please contact the Marketing Agent for GLD: State Street Global Advisors Funds Distributors, LLC, One Iron Street, Boston MA 02210; T: +1 866 320 4053 spdrgoldshares.com State Street Global Advisors © 2018 State Street Corporation. All Rights Reserved. ID12798-1996883.3.1.NA.RTL 0418 Exp. Date: 07/31/20189

SPDR® GOLD TRUST has filed a registration statement (including a prospectus) with the SEC for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents the issuer has filed with the SEC for more complete information about the Trust and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the Trust or any Authorized Participant will arrange to send you the prospectus if you request it by calling toll free at 1-866-320-4053 or contacting State Street Global Advisors Funds Distributors, LLC, One Lincoln Street, Attn: SPDR® Gold Shares, 30th Floor, Boston, MA 02111.