UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended: December 31, 2013

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ______________to ______________

Commission File Number 000-50155

NF ENERGY SAVING CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

|

Delaware

|

|

02-0563302

|

|

(State of Incorporation)

|

|

(I.R.S. Employer ID Number)

|

|

|

|

|

|

3106, Tower C, 390 Qingnian Avenue, Heping District

|

|

|

|

Shenyang, P. R. China

|

|

110015

|

|

(Address of Principal Executive Offices)

|

|

(Zip Code)

|

(8624) 2560-9775

(Issuer’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

|

Name of Each Exchange on Which Registered

|

|

Common stock, $0.001 par value

|

|

The NASDAQ Stock Market

|

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "accelerated filer", "large accelerated filer", and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check One):

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

Non-accelerated filer ¨

|

smaller reporting company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.).

Yes ¨ No x

As of June 28, 2013, the aggregate market value of the common equity held by non-affiliates of the registrant was $1,865,259 based on the price of $0.639 per share which the registrant’s common stock was last sold.

As of March 11, 2014, there were 5,619,147 shares of the registrant’s common stock outstanding.

NF ENERGY SAVING CORPORATION

FORM 10-K

TABLE OF CONTENTS

|

|

|

Page

|

|

|

|

No.

|

|

PART I

|

|

|

|

Item 1

|

Business

|

2

|

|

Item 1A

|

Risk Factors

|

17

|

|

Item 1B

|

Unresolved Staff Comments

|

30

|

|

Item 2

|

Properties

|

30

|

|

Item 3

|

Legal Proceedings

|

30

|

|

Item 4

|

Mine Safety Disclosure

|

30

|

|

PART II

|

|

|

|

Item 5

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

31

|

|

Item 6

|

Selected Financial Data

|

32

|

|

Item 7

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

32

|

|

Item 7A

|

Quantitative and Qualitative Disclosures About Market Risk

|

46

|

|

Item 8

|

Financial Statements and supplementary data

|

46

|

|

Item 9

|

Changes In and Disagreements With Accountants on Accounting and Financial Disclosure

|

47

|

|

Item 9A

|

Controls and Procedures

|

47

|

|

Item 9B

|

Other Information

|

49

|

|

PART III

|

|

|

|

Item 10

|

Directors, Executive Officers and Corporate Governance

|

49

|

|

Item 11

|

Executive Compensation

|

54

|

|

Item 12

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

55

|

|

Item 13

|

Certain Relationships and Related Transactions, and Director Independence

|

56

|

|

Item 14

|

Principal Accountant Fees and Services

|

57

|

|

PART IV

|

|

|

|

Item 15

|

Exhibits and Financial Statement Schedules

|

59

|

| 1 | ||

PART I

ITEM 1. BUSINESS

The Company

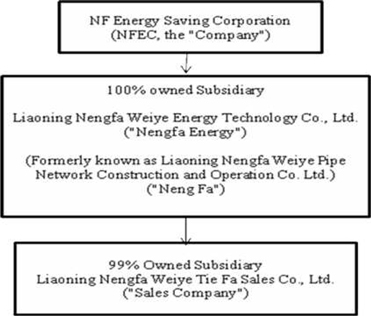

As used herein the terms “we”, “us”, “our,” “NFEC” and the “Company” means, NF Energy Saving Corporation, a Delaware corporation, formerly known as NF Energy Saving Corporation of America, Diagnostic Corporation of America, Global Broadcast Group, Inc., and Galli Process, Inc. These terms also include our subsidiaries, Liaoning Nengfa Weiye Energy Technology Company Ltd., a corporation organized and existing under the laws of the Peoples’ Republic of China (“PRC”), and Liaoning Nengfa Weiye Tie Fa Sales Co., Ltd., a limited liability corporation organized and existing under the laws of the PRC.

NF Energy Saving Corporation was incorporated under the laws of the State of Delaware under the name of Galli Process, Inc. on October 31, 2000 for the purpose of seeking and consummating a merger or acquisition with a business entity organized as a private corporation, partnership, or sole proprietorship. On December 31, 2001, Galli Process, Inc. became a majority owned subsidiary of City View TV, Inc., a Florida corporation (“City View”). On February 7, 2002, Galli Process, Inc. changed its name to Global Broadcast Group, Inc. On March 1, 2002, City View merged into Global Broadcast Group, Inc., which was the surviving entity. On November 12, 2004, the Company changed its name to Diagnostic Corporation of America. On March 15, 2007, we changed our name to NF Energy Saving Corporation of America, and on August 24, 2009, the Company further changed its name to NF Energy Saving Corporation, in both instances to more accurately reflect our business after the Plan of Exchange (see below). Our principal place of business is 3106, Tower C, 390 Qingnian Avenue, Heping District, Shenyang, P. R. China 110015. Our telephone number is (8624) 2560-9775.

On November 15, 2006, we executed a Plan of Exchange (“Plan of Exchange”), among the Company, Liaoning Nengfa Weiye Pipe Network Construction and Operation Co. Ltd. (“Nengfa”), the shareholders of Nengfa (the "Nengfa Shareholders") and Gang Li, our Chairman and Chief Executive Officer (“Mr. Li”). At the closing of the Plan of Exchange, which occurred on November 30, 2006, we issued to the Nengfa Shareholders 12,000,000 shares of our common stock, or 89.4% of our then outstanding common stock, in exchange for all of the shares of capital stock of Nengfa owned by the Nengfa Shareholders. Immediately upon the closing, Nengfa became our 100% owned subsidiary, and the Company adopted and implemented the business plan of Nengfa.

On September 5, 2007, we established a new sales company, Liaoning Nengfa Weiye TieFa Sales Co., Ltd. (“Sales Company”). Sales Company is a subsidiary, which is 99% owned by Liaoning Nengfa Weiye Energy Technology Company Ltd. Sales Company engages in the sales and marketing of flow control equipment and products in PRC. On August, 2013, "Sales Company" is not longer in existence because of no obviously increase incurred in transaction. Currently, the Company is in the process of the de-registration process with the local authority.

| 2 | ||

On January 31, 2008, to better reflect our energy technology business, we changed the name of Nengfa to Liaoning Nengfa Weiye Energy Technology Company Ltd. (“Nengfa Energy”). Nengfa Energy’s area of business includes research and development, processing, manufacturing, marketing and distribution of energy saving flow control equipment; manufacturing, marketing and distribution of energy equipment, wind power equipment and fittings; energy saving technical reconstruction; and energy saving technology consulting services.

On August 26, 2009, the Company completed a 3 to 1 reverse share split of its common stock. As a result, the total number of shares of outstanding common stock changed from 39,872,704 pre-split to 13,291,387 post-split shares.

On September 15, 2010 the Company completed a 2.5 to 1 reverse share split of its common stock, the total number of shares of outstanding common stock changed from 13,315,486 pre-split to 5,326,501 post-split shares.

On October 4, 2010 our common stock commenced trading on the Nasdaq Global Market. On March 7, 2012, and upon approval by NASDAQ, our common stock transferred from the Nasdaq Global Market to the Nasdaq Capital Market, Our common stock trades on the Nasdaq Stock Market under the ticker symbol “NFEC”.

The structure of our corporate organization is as follows:

Business Description

NFEC is dedicated to energy efficiency enhancement in two fields: (1) manufacturing large diameter energy efficient intelligent flow control systems for thermal and nuclear power generation plants, major national and regional water supply projects and municipal water, gas and heat supply pipeline networks; and (2) energy saving technology consulting, optimization design services, energy saving reconstruction of pipeline networks and contractual energy management services for China’s electric power, petrochemical, coal, metallurgy, construction, and municipal infrastructure industries.

| 3 | ||

NFEC has received many awards and honors from China's regulators, professional associations and renowned international organizations, including the ISO 9001:2008 certification from Det Norske Veritas Management System, the Liaoning Provincial Government's Award of Innovative Enterprise with Best Investment Return Potentials, the Special Industrial Contribution Award of the ESCO Committee of China Energy Conservation Association, and the “Contract-abiding and credit enterprise” Award by the Liaoning State Local administrative bureau for industry and commerce. NFEC was awarded of “Hi-tech enterprise” by Liaoning Technology bureau in 2013.

NFEC enjoys a reputation as a leader and dedicated energy saving company in China for over 15 years. Its professional capacity as a provider of energy services is officially certified by China’s National Development and Reform Commission (NDRC). It has been a corporate member on the Board of the ESCO Committee of China Energy Conservation Association and a founding member of China Standardization and Technical Consortium for Energy Conservation and Emission.

As a certified energy service provider, NFEC is entitled to various tax breaks and energy saving awards created by Chinese governments at national, provincial and local levels. The major tax incentives by the central government include a two-year corporate income tax exemption plus a three-year reduction of corporation income tax for all energy performance based, profit sharing energy service projects. The government policy also incentivizes NFEC's clients with tax refunds on goods and properties of the energy saving projects when NFEC transfers to them at the end of the energy service contracts.

The current principal development focus of NFEC is to complete the on-going construction project of the new manufacturing facility which will triple the Company's capacity to produce large intelligent flow control systems and to provide our Company with more advanced technology to supply high grade energy efficient and safety reliant products for high end markets such as super critical power generation plants.

Our corporate goal is to maintain our established position as a leading provider of energy efficiency flow control systems, a cutting edge innovator with clean energy and energy efficiency technologies, and a total energy efficiency solution and service provider dedicated to maximum returns to our investors, partners, clients and environment.

Products and Services

Our products and services include the manufacturing and sales of energy-saving flow control equipment, energy saving technology consulting, optimization design services, energy saving reconstruction of pipeline networks and contractual energy management services for China’s electric power, water power, petrochemical, coal, metallurgy, construction, and municipal infrastructure development industries. Examples of contracts entered into by the Company or its subsidiaries are:

| 4 | ||

|

|

·

|

In 2007, Nengfa Energy received contracts for our products and services to be used in three sub-sections of the prominent “South to North Water Transfer and Supply Project." The subsections were completed and passed inspection in 2008.

|

|

|

|

|

|

|

·

|

In 2008, the Company received flow control equipment contracts from seven cities in Liaoning Province for their water supply systems.

|

|

|

|

|

|

|

·

|

In 2009, the Company was awarded several flow control equipment supply contracts, including one for the Xijiang diversion project of Guangdong Province, and one for Phase 1 of Guangdong Yuedian Huilai Power Plant.

|

|

|

|

|

|

|

·

|

In 2010, the Company received contracts for our products and services to be used in over 50 companies, including Chongqing Water Turbine Company, Chongqing Fangneng Electricity Power Company, Zhejiang Zheneng Jiahua Electricity Power Co. Ltd, and Shaoxing Binhai Thermal Power Company, and a project contract with a Fuxin inner-Mongolian county.

|

|

|

|

|

|

|

·

|

In 2011, the Company received contracts for our products, including from Jiangsu Changshu Electricity Power Ltd, India RODA Supercritical Coal Fired Power Station, India KAWAI Supercritical Coal Fired Power Station, Zhejiang Zheneng Zhongmei Zhoushan Coal and Electricity Company, Shenzhen Qinglinjing Water diversion project, Chongqing Yunneng Electricity Power Ltd, and Shenyang Mining Machinery Ltd.

|

|

|

|

|

|

|

·

|

In 2012, the Company received contracts from Beijing South to North Water Diversion Operation and Management Center, Shanxi Kegong Longsheng technology Ltd, Huaihu Coal Ltd, Chongqing Water-Turbine Ltd, Shenergy Company Limited, Shanghai Qingcaosha City-Environment Project (South Branch Project), Luanhe Power station of China Guodian Corporation ,Qiangui power Ltd , Guizhou Province, Guihang Nenghuan refrigeration engineering Ltd, Shanghai City , Electric power construction corporation (Zambia’s project) , Shandong Province; Lu Electric International Trading corporation, and Shandong Province ( Philippines project).

|

|

|

|

In 2013, the Company received contracts from Zheneng Zhenhai Gas Thermal power Ltd; Chongqing Water Turbine Factory Ltd; Chongqing Wanliu power Ltd; Dalian Petrochemical Company of Petro of China ; China National Electric Power Engineering Ltd ; Xinyu Iron and Steel Ltd; Shandong Electric Power Corporation; Jiajie Gas-fired Cogeneration Branch of Shanxi New Energy Industry Group; and the Amedyan Power Ltd of State Grid.

|

Production and Sales of Energy Saving Flow Control Equipment

The Company’s current principal business is the production and sales of energy-saving flow control equipment, and intelligent flow control equipment. This business currently accounts for the majority of the Company’s revenues.

Pipeline transport is one of the basic modes of transportation together with rail transport, road transport, air transport and water transport. Water, gas, oil, and heat rely on various kinds of pipelines and pipe networks to be transported to end users. In the case of water pipelines, such systems are also used for public health and safety, and waste and flood control.

| 5 | ||

The key to the efficiency and energy conservation of the pipeline transportation process is the valve and the flow control equipment. Having unique technology in this field, the Company has obtained four patents and holds fourteen utilization model patents in China for flow control devices, especially in the area of the bidirectional seal zero revelation installation system with its special characteristics. Using valves of this type can result in reduced energy consumption by 20% for customers compared to traditional valves. The reduced energy consumption thereby increases the efficiency of the pipeline system. It is widely used in the fields of electric power, hydro power, petroleum, and natural gas. The Company’s super intelligent flow-control device was awarded “Number One Energy Saving Valve of China” by the Chinese Energy Conservation Association. Our products currently are exported to the United States, Russia, Turkey, Japan, South Korea, Vietnam, India, Iraq, and Afghanistan.

Once the Company’s new manufacturing facility is completed, the newly installed numerical controlled machines will allow the Company to manufacture and process technologically advanced flow control equipment with greater precision. This should enable the Company to expand its markets into and new high precision energy related equipment.

Because improved manufacturing and use of sophisticated technologies are important revenue drivers for the Company and represent an important part of its energy efficiency focus, the Company will continue to develop comprehensive energy conservation and energy reduction equipment and services, and to pursue research development and improved manufacturing of flow control and clean energy related equipment.

Energy Saving Reconstruction Projects

1. Energy Efficiency Retrofitting Projects on Industrial Boilers and Furnaces

Our business also focuses on the reconstruction of various industrial boiler/furnace systems with the objective of modernization and improvement in the overall efficiency of existing systems. Efficiency can be expressed in several ways, such as lower operating costs, reduced energy consumption, recapture of by-products which can be used for other purposes, and pollution reduction.

China’s industrial boilers and furnaces are used mainly in the iron and steel, metallurgy, building materials, machinery manufacturing, chemical industry and other similar energy consumption industries. Their energy consumption accounts for about 10% of China’s total energy consumption. It is estimated that as many as half of the enterprises have outdated technology and equipment, and experience a significant waste of energy. Using our existing technology, we can reconstruct the boiler’s or furnace’s structure, its heat source system, combustion system, and control system, and thereby both improve the overall efficiency of the system and yield important conservation and pollution control benefits.

| 6 | ||

One of the most important opportunities for the Company is to undertake projects that refurbish or reconstruct industrial boilers and create cogeneration opportunities for coal fired boilers. It is estimated that as many as 95% of the industrial boilers in China are coal fired. These types of industrial boilers are very inefficient because: most industrial coal burning boilers use traditional traveling grate boilers, only a small portion of the coal fired boilers are equipped with advanced technology, such as the pulverized coal combustion or circulating fluidized bed. Due to their low combustion and thermal efficiency, the traditional coal fired boilers emit more CO2 and NOx, and the boilers are typically at or beyond their estimated useful life. Overall, it is estimated that these types of boilers are operating at about 60-70% of their efficiency, which is about 20% below that of international best practice. The inefficiency, in part, results from their use of mixed sizes of coal particles in layer combustion. Among these types of boilers, about 60% of them are clockwise rotation boilers. The use of the differing sizes of the coal particles results in a highly inefficient combustion, due to the poor ventilation for the effective combustion and the accumulation of dust which chokes the combustion. Therefore, the coal is not totally burned and there is a loss of potential energy. The current methods of coal feed to the boilers and the current combustion cannot solve this problem. Given the large quantities of these types of industrial boilers, approximately 0.3~0.4 million sets of traveling grate boilers currently are in-use, the Company sees a significant opportunity to focus on boiler transformation technology and projects.

The Company’s solution is to redesign and reconstruct elements of an existing boiler or boiler system to improve its overall performance and increase its optimization rates. This is done in a number of different ways, such as the following:

a) Boilers using a pulverized coal fired or a clockwise rotation chain grate system can be refitted with a circulating fluidized bed combustion technology. This change has the benefit of allowing the boiler to use a lower grade of coal but improve the thermal efficiency. The ash from the fluidized bed combustion system can be used in building materials, which is a valuable by-product and reduces pollution output.

b) The control system of a boiler can be either reconstructed or modified to improve the operations of the unit and system.

c) The coal feed system of a boiler system can be altered to provide more efficient coal layer arrangement according to different volume and nature of the coal , with the effect that the boiler will fully combust the coal. This improves the operating cost and fuel optimization.

d) Another change that can be made to boilers is to improve the ventilation system by adding the right amount of fresh air and increase the turbulence based on computer aided calculation, which can result in increased fuel combustion efficiency and hence reducing the operating costs.

e) One of the most important improvements that the Company seeks to introduce into existing and new boiler systems are methods to reclaim discharged water. The Company designs recovery equipment which permits recovery of significant amounts of the waste water used in a traditional boiler. This recovery can also improve the capture of pollutants by the boiler system.

| 7 | ||

f) A boiler’s heat recovery can be improved, whether it is coal, natural gas or petroleum fueled. By-product heat can be used in a number of different ways, such as to create steam for other uses or localized heating of the factory. The capture and use of the residual heat reduces its emission into the atmosphere thereby reducing heat pollution. This can be an additional source of income or help reduce operating costs and pollution.

The Company is capable of designing and introducing steam thermal systems into existing systems with the effect of recovering the condensed water, eliminating the leakage losses due to faulty or worn steam trap valves and improving the heat preservation systems.

2. Motor Drive Reconstruction

In China, motor drive systems use about two thirds of the total electricity consumption of the country. About 90% of these motors are AC asynchronous motors. Nengfa Energy redesigns such systems to convert them so that they can be used for variable load fans and pumps through frequency conversion and speed regulation technology. Nengfa Energy focuses on the reconstruction and energy conservation of the fans of power station boilers, industrial furnaces and kilns, and the energy-saving pumps in the cold/hot water pipe system. As we analyze the whole industrial reconstruction projects, we can also provide power conservation reconstruction in solid material conveyor systems used in the mining, metallurgy, iron and steel industries.

It is estimated that approximately 12% of China’s electric power consumption is for lighting. As one of the most important energy-saving projects, the Chinese government plans to distribute 150 million energy-saving lamps throughout the country during the "Eleventh Five Year Plan" period through a fiscal subsidy in an effort to replace inefficient incandescent lamps and other lighting products. The government also plans to reduce the consumption of power by changing the use of lighting through a rational distribution of public lighting, improving the quality of power consumption and introducing on-demand controls.

3. Energy-Saving and Reconstruction of Steam Heat Energy System

As a high quality source of secondary energy, steam is widely used in petroleum, petrochemical, chemical, paper making, brewing, tobacco, steel, pharmaceutical, packaging, machinery, and electronics among other industries. The total energy efficiency of steam is directly determined by the system’s energy efficiency. The characteristics of the steam and condensation system are highly complex, due to factors such as the need for a condensation traps and vacuum breakers, the damage from water hammer, corrosion of the heat exchanger and leakage, condensation, pollution and purification, steam consumption’s imbalance in winter and summer, steam consumption’s mismatching between high and low pressures, the flash steam problem, and steam leakage. For a long time, due to the irrationality of system design, the complexity of the system itself, the negligence of owners, the imprecision of management, and the deficiency of maintenance, the overall energy efficiency of steam systems in China is very low. Therefore, the Company believes there is a significant opportunity for energy savings in steam systems:

| 8 | ||

1) Approximately 0.5 billion tons of standard coal is consumed annually, which is more than 1/3 of the total national consumption of fossil fuels.

2) The overall energy efficiency of steam systems in China is only approximately 30%, which is 25% lower than well developed countries.

3) The annual energy waste due to the low energy efficiency of steam systems is approximately 120 million tce, which is estimated to be worth over 120 billion RMB.

4) The annual waste due to inefficient transportation and distribution of steam systems is approximately 180 million tce.

5) Of the more than 1 million traps being used in steam systems in China, 60% of them have above average leakage, 30% of them have serious leakage, and only less than 10% work normally. The waste due to trap leakage is significant.

6) Current condensation systems are generally designed in such a way as to be inappropriate to the system, resulting in the average recovery rate being less than 30% thus; causing large waste of heat energy and water.

Working with energy saving experts in steam systems in China, the Company has built a steam system department. This department has an R&D and design team, which can provide energy conservation solutions for efficient and the long lasting energy saving results. Under normal conditions, the reduction of steam energy cost is generally between 10% and 25%.

Our energy conservation solutions improve energy efficiency in steam systems in five principal ways, covering the entire process of the steam and condensation system: steam generation, steam transportation and distribution, steam consumption, and condensation recovery and condensation purification.

1) Steam generation stage

Our energy saving measures include: using the boiler’s long-term stable heat sink resources to fully absorb low temperature waste heat and reduce fuel consumption; correctly designing the generator in order to reduce the steam consumption of the deoxygenizing process and increasing the efficiency of the boiler; controlling boiler blowdown and fully utilizing the waste heat of blowdown water; adjusting the steam load with steam accumulator; and improving the quality of steam.

| 9 | ||

2) Steam transportation and distribution stage

Our energy saving measures include: designing the most economical flow speed of steam, reducing leakage, draining condensation correctly, filtering dirt and debris, reducing pressure drop loss, improving steam quality, and avoiding water hammer. The most serious problems to be addressed are water hammer, big drops in steam pressure, high steam humidity and low steam quality caused by errors in the design of the condensation trapping system.

3) Steam consumption stage

In this stage, we improve the energy efficiency of the steam system by studying the difference in details between designed and actual steam consumption of each heat exchanger, and looking for the root causes of excessive energy consumption; consuming lower pressure steam as far as possible when meeting the process's demands; equipping the system with a vacuum breaker and air valve in beehive heat exchangers; designing a condensation trapping system correctly to avoid waterlogging; controlling temperatures automatically in the heating process; installing a separator for steam and vaporous water in the inlet of important equipment to ensure steam quality; optimizing the condensation pipe system according to the residual pressure of each heat exchanger; and enhancing daily inspection and maintenance.

4) Condensation recovery stage

In this stage, we improve steam efficiency by optimizing the overall condensation piping system and deploying decentralized, cutting-edge pressure pump recovery technology; comprehensive treatment on flash steam; comprehensive utilization of heat sink resources; and limit water hammer. The key to optimizing the overall condensation piping system is to identify different condensations according to the residual pressure as “strong”, “mainstream” and “weak”, thus minimizing the mutual interference between different residual pressures.

5) Condensation purification stage

The Company’s “solvent impregnated resin oil desorption technology” can separate emulsified oil molecules and dissolved oil molecules from high temperature condensation directly through the resin’s lipophilicity and hydrophobicity. Before separation, “emulsification breaking”, “capturing” and “enriching” are completed automatically. When the oil molecules adsorbed in the face of the resin reaches a certain saturation level, the enriched oil will be separated from the resin as large oil-drops through the flow impact of condensation water inside the tank. After separation the oil-drops float into an oil-water separator and the off-oil resin will start to work automatically. In the oil-water separator the oils will separate from water automatically.

| 10 | ||

Nengfa Energy’s condensation iron deprivation technology is called “Powder Ion Exchange Resin Coverage and Filtration Technology”.. We utilize this technology to separate excessive metal oxides, colloids and iron ion (Fe3+ & Fe2+) from high temperature condensation. The technical principles are filtration, adsorption, and ion replacement; the processes are film formation, operating, toggling, back-washing and film formation again.

We estimate the energy saving market for steam systems is very large in China. We believe the annual consumption of steam systems is approximately 0.5 billion tce. The overall energy efficiency of steam systems in China is only approximately 30%, which is 25% lower than well developed countries. The annual energy waste due to low energy efficiency of steam systems is approximately 120 million tce, which is worth over 120 billion RMB. If all the energy saving projects in steam systems were operated under a EPC (Energy Performance Contract) model, and the average profit were to equal three years of energy-saved we estimate, the value of the energy-saving market for steam system in China would be approximately 360 billion RMB.

Patents and Technology

Nengfa Energy currently has been issued four invention patents and has applied for fourteen utility model patents in the PRC. We will strive to maintain the innovation of our products in order to maintain our leading position in the market.

The invention patents include the following:

1. Processing technology of butterfly valve seal (ZL2006 1 0152644.8), which expires on September 26, 2026;

2. Butterfly valve body dynamic seal ring pointing device (ZL2007 1 0159250.X), which expires on December 28, 2027;

3. The closing and locking equipment for valves (ZL2009 1 0011939.7), which expires on June 11, 2029; and

4. Valve body active seal circle position monitor equipment (ZL2009 2 0014504.3), which expires on July 21, 2030.

The utility model patents that we have applied for include the following:

5. An energy-saving heat-sink used in heating (ZL2008 2 0218146.3), with an application date of September 23, 2008

6. A device used in energy-saving boiler combustion (ZL2008 2 0218145.9) , with an application date of September 23, 2008;

| 11 | ||

7. Butterfly valve sealing ring instruction device (ZL2007 2 0185293.0) , with an application date of December 12, 2007;

8. Butterfly valve with block for opening butterfly plate (ZL2007 2 0185289.4), with an application date of December 12, 2007;

9. Piston flow-adjusting valve with removable piston sealing ring (ZL2007 2 0185288.X), with an application date of December 12, 2007;

10. J-shapes large dimension butterfly valve hard sealing ring (ZL2007 2 0185292.6), with an application date of December 12, 2007;

11. Composite valve sealing ring (ZL2007 2 0185290.7), with an application date of December 12, 2007;

12. Multi-level buffering full oriented valve fuel tank (ZL2007 2 0185287.5), with an application date of December 12, 2007;

13. Fluid control valve on-off speed control device (ZL2007 2 0185286.0), with an application date of December 12, 2007;

14. T-shaped large dimension butterfly valve rubber sealing ring (ZL2007 2 0185291.1), with an application date of December 12, 2007;

15. Butterfly valve with butterfly plate adjusting device (ZL2008 2 0231340.5), with an application date of September 23, 2008;

16. Two-way sealed butterfly valve (ZL 2009 2 0014504.3), with an application date of June 11, 2009;

17. Energy-saving electric valve (ZL2011 2 0393230.0) with an application date of October 14,2011; and

18. Radial fixed valve seal butterfly valve (ZL2011 2 0393135.0) with an application date of October 14, 2011.

In addition to the patent protection that we seek, we also rely on the confidentiality of our operations, proprietary know-how and business secrets. Although we do not have formal agreements with our employees, we do consider our employees’ work to be proprietary and owned by the Company. Where necessary, we will take steps to protect our intellectual property interests under the laws of the PRC. There can be no assurance that we will be able to enforce our rights if they are improperly taken by our employees or adopted by our competitors outside of sanctioned use and royalty agreements with the Company.

Certain of our service offerings will not be patentable or otherwise be capable of being registered as intellectual property. Therefore, the Company will rely solely on such services being proprietary. As such the Company will have to rely on the services being more advanced or better than its competitors’ offerings or rely on trade secret laws and protections. Such protections in the PRC are considered rather weak and are difficult if not impossible to enforce. Consequently, it may be possible for our competitors to obtain our information and to copy, adopt or adapt our methods, services and technical aspects to their own business with no assurance that we will be able to prevent them from using the intellectual property in competition with us.

| 12 | ||

The Company does not have any significant trademarks in use at this time. As our business develops, we will consider the advantage of developing specific trademarks for our products and services and have registered those marks with the PRC government authorities for their protection.

Markets and Customers

The South-North Water Diversion Project is a multi-decade project undertaken by the Chinese government to better utilize water resources available to China. Part of this massive project was brought forward to provide additional water supply for the 2008 Olympics in Beijing. While the main task is to divert water from the Yangtze River in the south to the Yellow River and Hai River in the north, other spin-off plans are also included. Among these, a plan calling for the capture and diversion of water from Brahmaputra River, located in Yarlung Zangbo Grand Canal north of India, has been under study for years. This is because the heavily industrialized Northern China has a much lower rainfall and its rivers are running at reduced rates as demand increases for industrial water and general population usage. For example, the Yellow River and Hai River have experienced significant flow reduction and at times during certain years have been dry.

Currently, the Grand Canal parallel to the eastern coast is being upgraded, as the Eastern route for diverting water to the North. Water from the Yangtze River will be drawn into the canal in Jiangdu City, where a giant 400 m³/s. pumping station was built in the 1980s, and will then be fed uphill by pumping stations along the Grand Canal and through a tunnel under the Yellow River, from where it can flow downhill to reservoirs near Tianjin. Construction on the eastern route officially began in December 2002 and completed in 2012 which results in the citizens of Tianjin City who enable to use the water derived from Yangtze River.

The central route for the water diversion project is from Danjiangkou Reservoir on the Han River, a tributary of the Yangtze River, to Beijing. This route is built on the North China Plain and, once the Yellow River has been crossed, water can flow all the way to Beijing by gravity. The main engineering challenge is to build a tunnel under the Yellow River. Construction on the central route began in 2004. In 2008 the 307 km-long northern stretch of the central route was completed at a cost of $2 billion. Water in that stretch of the canal does not yet come from the Han River, but from various reservoirs in Hebei Province south of Beijing. Farmers and industries in Hebei have had to cut back their water consumption to allow for water to be transferred to Beijing. The whole project was initially expected to be completed around 2010; however, this has recently been pushed back to 2014 to allow for more environmental protection elements to be built into the system. A major difficulty in completion of the central route has been the resettlement of approximately 250,000 persons around Danjiangkou Reservoir and along the route. Another consideration that has to be accommodated in the implementation of the central route is the effect of removing approximately one third of the water from Han River and the effect of that reduction on the environment and other users that currently depend on the Han River. One long-term plan to reduce the effect on the Han River basin is to build another canal to divert water from the Three Gorges Dam to Danjiangkou Reservoir.

| 13 | ||

The western route for the water diversion project is to divert water from the headwaters of the Yangtze River into the headwaters of the Yellow River. In order to move the water through the drainage divide between these rivers, huge dams and long tunnels need to be built to cross the Tibetan-Qinghai and Western Yunnan Plateaus. The feasibility of this route is still under study and this part of the project will not start anytime soon.

To date, the Company has participated in the water diversion project by being a supplier of flow control equipment for various parts of the water flow infrastructure, with contract value over $3.05 million for four phases of the project. And as part of providing that equipment, the Company has also provided design and related services. The contracts related to this project accounted for 9.5% of total revenues in 2013. In the newly released Twelfth Five Year Plan announced by Chinese government, the fixed asset investment in hydro and water diversion projects will be increased dramatically in the next 5 to 10 years. The expected investment is 4 trillion RMB in 10 years, with annual average investment of 400 billion RMB.

In addition to the water diversion project, the Company also supplies flow control equipment and related equipment to the power generation industry (thermal power plants and hydroelectric power plants). Customers in these market segments are well-established, larger state and private corporations.

In connection with its work on the water diversion project and some of the power plant projects, the Company has a preferred provider agreement with Nengfa Weiye Tieling Valve Joint Stock Co., Ltd. (“Tieling Valve”) under which Nengfa Energy is the preferred provider of the valves and other related flow control equipment that Tieling Valve requires in its own work on the water diversion project. The agreement is in the manner of a right of first refusal whereby Tieling Valve is obliged to offer supply opportunities to Nengfa Energy within its scope of product offerings and expertise, but Tieling Valve is not prohibited from developing other supply arrangements. Tieling Valve and Nengfa Energy have agreed to cooperate to develop and market their respective technologies, equipment, products and services for their respective and mutual benefit, and will work together to examine and expand their respective businesses. Under the agreement, each party retains full right to their respective intellectual property. The agreement terminates in 2016, but by its terms will automatically extend for additional one year terms unless notice of termination is given by one party to the other at least six months prior to the then termination date.

The Company will focus its marketing to the wind power generation and the boiler/furnace industry through participation in and addressing government organizations and industry associations related to energy conservation and emission reduction. Marketing will also focus on equipment suppliers and end-users such as the larger and medium sized high energy consumption enterprises that provide or use the kinds of products and services that the Company currently offers or plans to offer. The focus will not only be to sell the products and services, but also to learn of the customer’s needs so that the Company can develop and adapt its products and services to the needs of its customer base. Another important aspect of the marketing strategy will be to participate directly in the consulting and reconstruction services of energy conservation projects organized by government agencies. Nevertheless, the Company plans to continue to participate in the bidding process for government projects, in an effort to enhance its market position.

| 14 | ||

The Company’s marketing and sales strategy also relies on the use of exclusive agents throughout China who act as marketing agents and after sale service providers. The Company currently has 23 exclusive distributing agents national wide. At certain times each year, the Company provides and organizes training sessions for these agents and their personnel. These sessions provide the Company with a valuable opportunity to gather feedback and to foster an exchange of technical ideas. These agents have agreements with the Company to sell NF flow control equipment and systems. The Company evaluates the performance of these exclusive agents annually, based on how well they achieve the annual sales target established by the Company. The Company typically will terminate its agreement with those agents that miss the sales targets for two consecutive years without good reasons.

Raw Materials

The major raw materials for our production are pig iron, steel, copper, and plastic. We source our materials locally in China. Nengfa Energy is located in Liaoning Province which is China’s largest production base for iron and steel. We have stable long term supply arrangements for our principal raw material suppliers based on long standing business relationships. Since we are located close to the supplies of many of our essential raw materials, we enjoy price and transportation cost advantages over our competitors and competing users. Through our advanced technology and our management of raw materials, we are able to manage and improve our consumption rates of the raw materials we use in production, which results in lower operating expense and extension of our inventories.

Regulatory Compliance

The products are subject to regulatory standards and enforcement codes which typically require that these products meet stringent performance criteria. Standards are established by industry testing and certification organizations such as the Ministry of Industry and Information Technology of China, the American Society of Mechanical Engineers (A.S.M.E.), the Canadian Standards Association (C.S.A.), the Japanese Standards Association (J.S.A.), the International Association of Plumbing and Mechanical Officials (I.A.P.M.O.), Factory Mutual (F.M.), and Underwriters Laboratory (U.L.). These standards are incorporated into state and municipal plumbing and heating, building and fire protection codes in China.

We maintain stringent quality control and testing procedures at our manufacturing facility in order to manufacture products in compliance with code requirements. Our production management is certified to conform to the ISO 9001 standards by the Det Norske Veritas Management System.

| 15 | ||

Competition

We think that the valve products of the Company place it in a leading position in the super diameter energy efficient flow control system in China. The Company has an extensive competitive advantage compared to Chinese domestic manufactures in this field. Other manufactures that are focusing on the development of different products may enter into this field. Our potential competitor in this field is China Valve Technology.

In the other areas of the Company’s business, there are many different competitors with differing focuses and strengths. To some extent, boilers and furnaces are specialized to particular industries and output requirements. This specialization engenders specialization in the design, manufacture and installation of new equipment and retrofit solutions. Therefore, there are many engineering and manufacturing companies that focus on certain types of boilers and furnaces resulting in a relatively fragmented market for these services. The same is true for the retrofit and reconstruction of other industrial systems for improved energy efficiency, as well as for the localized projects for energy conservation and biomass utilization, and similar projects. Therefore, the competition that the Company faces tends to be localized companies with no dominant players at this time.

The utilization of biomass energy is matured in China. Although the technology is widely used in China, it is still at a stage of individual household build gas digesters, rather with a large scale piped gas supply system. The county-city level gas supply project the Company concentrates on will generate a local area monopoly business operation. There is no direct competition in short term.

We plan to compete based on our ability to address a wide spectrum of solutions in our various market areas. We believe our competitive advantages result from our patented technologies, our strategic relationships with engineering companies, our marketing and our business relationships. We plan to continue to expand these aspects of our business to further grow our core businesses and provide solutions for the energy savings and green energy projects. We intend to participate actively in the government sponsored projects and government contracting.

Research and Development

The research and development expenses are to develop new products or new production technologies. The research and development expenses include the materials and labor costs, application fees for patents and significant improvements to existing products. We incurred $79,450 and $50,207 of research and development expenses in 2103 and 2012, respectively.

Employees

As of December 31, 2013, there were 221 employees including 30 technical staff working in our subsidiaries located in China. We believe we have a good relationship with our employees.

| 16 | ||

Others

Our internet website address is http://www.nfenergy.com. Through our website, we make available, free of charge, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports, proxy statement and registration statements, and all of our insider Section 16 reports, as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission, or SEC. These SEC reports can be accessed through the “Investors” section of our website.

ITEM 1A. RISK FACTORS

Investors should carefully consider the following risk factors, in addition to other information included in this annual report, in evaluating NF Energy Saving Corporation and our business. If any of the following risks occur, our business, financial condition and operating results could be materially adversely affected.

Risks Related to Our Business

We are subject to the risks of any growing enterprise, any one of which could limit our growth and our product and market development.

Our operating history makes it difficult to predict how our businesses will develop and where the Company will find success. This is especially true in respect of our expansion into areas other than flow valve technology and their design, sales and installation. Accordingly, we face all of the risks and uncertainties encountered by companies in similar stages of development, such as: (i) uncertain and continued market acceptance for our product extensions and our services; (ii) the evolving nature of the wind energy equipment industry in the PRC, where significant consolidation may occur, leading to the formation of companies which may be better able to compete with us than is currently the case; (iii) the fragmented nature of the boiler and furnace business which may limit our ability to penetrate the market and provide comprehensive solutions on a sufficiently wide basis to make the business profitable; (iv) changing competitive conditions, technological advances or customer preferences could adversely effect the sales of our products or services; (v) maintaining our competitive position in the PRC and competing with Chinese and international companies, many of which have longer operating histories and greater financial resources than us; (vi) continuing to offer commercially successful products to attract and retain a larger base of direct customers and ultimate users; (vii) maintaining effective control of our costs and expenses; and (viii) retaining our management and skilled technical staff and recruiting additional key employees.

If we are not able to meet the challenges of building our businesses and managing our growth, the likely result will be slower growth, lower margins, additional operational costs and lower income.

| 17 | ||

We may be unable to generate sufficient cash flow from operations or obtain financing in the future to support our operations and expansion.

Having access to sufficient operating funds and capital funds for expansion will affect our ability to execute our business plan. We finance our business mainly through internally generated funds, short-term bank loans and, from time to time, selling equity securities to raise additional capital. There is no guarantee that we will always have internal funds available for our future development or that we will be able to raise capital from investor financing and loans granted by investors and financial institutions in the future. In addition, there may be delays in the process of selling our securities, which may require us to cut back on our operations or expansion activities. Our access to debt or equity financing depends on the investors’ and banks’ willingness to lend to and invest in us, our financial condition and on general conditions in the capital markets. We may not be able to secure additional sources of financing on commercially acceptable terms, if at all. Any shortfall in our cash flow and capital needs may result in our having to curtail our business plans or have an adverse effect on our financial condition.

We believe that we need to raise additional capital for the expansionary elements of our business plan, which financing may not be available or available on terms favorable to us.

During the next phase of our business development, as we complete Phase II of our new manufacturing facility and continue our planned expansion into manufacture of energy-saving equipment and other aspects of the energy savings industry, including steam energy, we believe that we will need to raise additional capital from outside sources during the next year or two. We cannot be certain that we will be able to obtain additional financing on favorable terms, if at all. One possible impediment to raising capital is the tightening credit policies of the Chinese banks and the continued effects of tightening in the global credit markets as a result of the recent economic financial crisis. If we cannot raise additional capital on acceptable terms, we may not be able to develop or enhance our products or services, take advantage of future opportunities or respond to competitive pressures or unanticipated requirements. We cannot be sure that we will be able to secure all the financing we will require, or that it will be available on favorable terms. If we are unable to obtain any necessary additional financing, we will be required to substantially curtail our approach to implementing our business objectives. Additional financing may be debt, equity or a combination of debt and equity. If equity is used, it could result in significant dilution to our shareholders.

Efforts to protect our intellectual property rights and to defend against claims against us can increase our costs and will not always succeed. Any failures could adversely affect our sales and results of operations or restrict our ability to conduct our business.

Intellectual property rights are important to many aspects of our business. We actively pursue patent protection in our flow valve business, and we expect to pursue intellectual property rights in our other business endeavors as we develop unique solutions to business demands. We, however, may be unable to obtain protection for our intellectual property. Even if protection is obtained, competitors may raise legal challenges to our rights or illegally infringe on our rights, including through means that may be difficult to prevent, detect or defend. In addition, because of the rapid pace of technological change and the confidentiality of patent applications in some jurisdictions, competitors may be issued patents from applications that were unknown to us prior to issuance. The patents of others could reduce the value of our commercial or pipeline of products or, to the extent they cover key technologies on which we have unknowingly relied, require that we seek to obtain licenses at a financial cost to us or cease using the technology, no matter how valuable the patents may be to our business. We cannot assure you we would be able to obtain such licenses on acceptable terms. Also, litigation may be necessary to enforce our intellectual property rights, protect our trade secrets or determine the validity and scope of our and the proprietary rights of others. There is a risk that the outcome of such litigation will not be in our favor. Such litigation may be costly and may divert management attention as well as expend other resources which could otherwise have been devoted to our business. An adverse determination in any such litigation will impair our intellectual property rights and may harm our business, prospects and reputation. In addition, we have no insurance coverage against litigation costs and would have to bear all costs arising from such litigation to the extent we are unable to recover such costs from other parties. The occurrence of any of the foregoing may harm our business, results of operations and financial condition.

| 18 | ||

Finally, implementation of PRC intellectual property-related laws has historically been limited, primarily because of ambiguities in the PRC laws and difficulties in enforcement. Accordingly, intellectual property rights and confidentiality protections in China may not be as effective as in the United States or other countries, which increases the risk that we may not be able to adequately protect our intellectual property.

For aspects of our business we rely on strategic relationships, and there is no assurance that we will be able to renew these arrangements.

We have several strategic relationships which provide us with access to technology and provide us with a competitive advantage. These include the relationships with Shanghai Electric Co., LTD., Sichuan Eastern Electric Co., LTD, Harbin Electric Co., LTD, China Datang Corporation, China Huadian Group, China Huaneng Group and China Guodian Group. There is no guarantee that any of these agreements and arrangements will provide the benefits that we hope will result or that the relationships will be renewed on substantially similar terms or at all. Moreover, there is no assurance that any steps we have already taken or might take in the future will ensure the successful renewal of any or all our rights or the granting of further new rights or that the terms of any renewals would not be significantly less favorable to us than the terms of our current agreements. The loss of such arrangements or diminution of the rights may have an adverse impact on our business development, including product offerings, research and development and competitive position.

We derive a substantial part of our revenues from several major customers, therefore if we lose any of these customers or they reduce the amount of business they do with us in the future, our revenues may be affected

Our largest customer, Nengfa Weiye Tieling Valve Joint Stock Co. Ltd, accounted for 71% of our revenues for the years ended December 31, 2013 Our second largest customer, Yangzhou power equipment Co. Ltd accounted for 5% of our revenue in the year ended December 31, 2013. As of December 31, 2013, these two customers accounted for 76% in our total revenue. These customers may not maintain the same volume of business with us in the future. If we lose any of these customers or they reduce the amount of business they do with us, our revenues may be materially and adversely affected. Although we have a strategic partnership with our second largest customer and a preferred provider agreement with our largest customer, there can be no assurance that these customers will continue to provide the current level of demand or will not seek to modify or terminate their respective agreements.

| 19 | ||

Our technology may not satisfy the changing needs of our customers.

With any technology, including the technology of our current and proposed products, there are risks that the technology may not successfully address our customers' needs. Certain of our product offerings in relation to the wind energy equipment will be new for the Company. While we have already established successful relationships with our customers, their needs may change or vary. This may affect the ability of our present or proposed products to address all of our customers' ultimate technology needs in an economically feasible manner.

We may not be able to keep pace with rapid technological changes and competition in our industry.

While we believe that we have hired or engaged personnel and outside consultants who have the experience and ability necessary to keep pace with advances in technology, and while we continue to seek out and develop "next generation" technology through our research and development efforts, there is no guarantee that we will be able to keep pace with technological developments and market demands in this evolving industry and market. In addition, our industry is competitive in various aspects. Although we believe that we have developed strategic relationships to best penetrate the China market, we face competition from other manufacturers of products similar to our products and services. Some of these companies have significant advantages over us with respect to their products, marketing and services, and their financial resources and customer relationships.

We may experience high accounts receivable balances from time to time, which may have an adverse effect on our operating profitability and cash flow and financing needs.

Although we generally have a 90 to 180 day accounts receivable period, if our customers extend the period in which they pay, we will experience a reduced cash flow, which could have an adverse effect on our ability to fund our operations and growth. One result may be that we will have to obtain outside financing and our operating expense will increase. Extension of the accounts receivable period may also result in reduced collections, which will adversely affect our operations and profitability.

| 20 | ||

To the extent that we depend on government projects, our business is dependent on government policy and, to some extent, government funding and government contracts.

Although we do not characterize our business as a government contractor, some aspects of our business are indirectly dependent on government policy, government funding, and government contracts. For example, the South to North Water Diversion Project is largely a government funded project, and our customers are contractors with the government. Similarly, our energy-saving projects and adjustments of our products and services are dependent on the policies issued by the government. As a consequence, it is possible that our requirements based on the products and services to be provided will be diminished resulting in a decrease in our revenue. Much of the pollution control and green industries are dependent on government policy to implement societal improvements. Our business has a number of aspects that are dependent on the government and our products, services and revenues are dependent on policies that can change if the government officials determine to redirect attention and investment to other aspects of society and industrial development.

Additionally, as a number of our customers are dependent on the government for their revenues through the provision of products and services on government contracts or government funded projects, there may be delays in our receiving payment for our products and services.

Fluctuation in the availability and cost of our raw materials may have an adverse effect on our operations and results of operations.

A portion of the inventory of raw materials and parts may be affected by fluctuations in the availability of the items and the price. Such things may include steel, electronic components, power systems, paints and welding rods. We do not generally have long term supply contracts with our suppliers, but rely on long standing relationships. To the extent that we are not able to obtain the required materials and parts necessary to enable us to fabricate our products, or we are required to pay more for such items, then there could be an adverse effect on our operations and our results of operations.

We may be unable to effectively manage our growth.

As we expand our business into several different areas of energy savings and green industry, we will need to manage our growth effectively, which may entail devising and effectively implementing business plans, training and managing our growing workforce, managing our costs, and implementing adequate control in our reporting systems in a timely manner. We may not be able to successfully manage our growth. Our failure to do so could affect our success in executing our business plan and adversely affect our revenues, profitability and results of operations.

| 21 | ||

If we fail to successfully manage our planned expansion of operations, our growth prospects will be diminished and our operating expenses could exceed budgeted amounts.

Our ability to offer our products and services in an evolving market and in different markets requires effective planning and management process. This rapid growth places significant demand on our managerial and operational resources and our internal training capabilities. In addition, we plan to increase our total work force. This growth will place a substantial burden on our management team. To manage growth effectively, we must implement and improve our operational, financial and other systems, procedures and controls on a timely basis and expand, train and manage our workforce, particularly our sales and marketing and support organizations. We cannot be certain that our systems, procedures and controls will be adequate to support our current or future operations or that our management will be able to handle such expansion and still achieve the execution necessary to meet our growth expectations. Failure to manage our growth effectively could diminish our growth prospects and could result in lost opportunities as well as operating expenses exceeding the amount budgeted.

If we fail to establish and maintain an effective system of internal control, we may not be able to report our financial results accurately or to prevent fraud. Any inability to report and file our financial results accurately and timely could harm our business and adversely impact the trading price of our common stock.

We are required to establish and maintain internal controls over financial reporting, disclosure controls, and to comply with other requirements of the Sarbanes-Oxley Act and the rules promulgated by the SEC thereunder. Our management, including our Chief Executive Officer and Chief Financial Officer, cannot guarantee that our internal controls and disclosure controls will prevent all possible errors or all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. In addition, the design of a control system must reflect the fact that there are resource constraints and the benefit of controls must be relative to their costs. Because of the inherent limitations in all control systems, no system of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty and that breakdowns can occur because of simple error or mistake. Further, controls can be circumvented by individual acts of some persons, by collusion of two or more persons, or by management override of the controls. The design of any system of controls also is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Over time, a control may become inadequate because of changes in conditions or the degree of compliance with policies or procedures may deteriorate. Because of inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and may not be detected.

Our operations are vulnerable to natural disasters or other events.

Our operating income may be reduced by natural disasters, in locations where we own and/or operate significant manufacturing facilities or are working on significant projects. Some types of losses, such as from earthquake, severe winter storms and environmental hazards, may be either uninsurable or too expensive to justify insuring against. Should an uninsured loss or a loss in excess of insured limits occur, we could lose all or a portion of the capital we have invested in any particular property, as well as any anticipated future revenue from such property.

| 22 | ||

Our products may contain defects, which could adversely affect our reputation and cause us to incur significant costs.

Despite numerous testing and quality controls, defects may be found in existing or new products. Any such defects could cause us to incur significant return and exchange costs, re-engineering costs, divert the attention of our engineering personnel from product development efforts, and cause significant customer relations and business reputation problems. Any such defects could force us to undertake a product recall program, which could cause us to incur significant expenses and could harm our reputation and that of our products. If we deliver products with defects, our credibility and the market acceptance and sales of our products could be harmed.

Our business could be subject to environmental liabilities.

We use certain hazardous substances in our operations. Currently we do not anticipate any material adverse effect on our business, revenues or results of operations, as a result of compliance with Chinese environmental laws and regulations. However, the risk of environmental liability and charges associated with maintaining compliance with environmental laws is inherent in the nature of our business, and there is no assurance that material environmental liabilities and compliance charges will not arise in the future.

We have limited business insurance coverage in China

The insurance industry in China is still at an early stage of development. Insurance companies in China offer limited business insurance products. As a result, we do not have any business liability or disruption insurance coverage for our operations in China. Any business disruption, litigation or natural disaster might result in substantial costs and diversion of resources.

Because our funds are held in banks in the PRC that do not provide insurance, the failure of any bank in which we deposit our funds could affect our ability to continue in business.

Banks and other financial institutions in the PRC do not provide insurance for funds held on deposit. A portion of our assets are in the form of cash deposited with banks in the PRC, and in the event of a bank failure, we may not have access to our funds on deposit. Depending upon the amount of money we maintain in a bank that fails, our inability to have access to our cash could impair our operations, and, if we are not able to access funds to pay our suppliers, employees and other creditors, we may be unable to continue in business.

| 23 | ||

We substantially depend on a few key personnel who, if not retained, could cause declines in productivity and operational results and loss of our strategic guidance, all of which would diminish our business prospects and value to investors.

Our success depends to a large extent upon the continued service of a few executive officers and key employees, including, Mr. Gang Li, our Chairman, Chief Executive Officer and President. The loss of the services of one or more of our key employees would have an adverse effect on us and our PRC operating subsidiaries, as these individuals play a significant role in developing and executing our overall business plan and maintaining customer relationships and proprietary technology systems. While none of our key personnel is irreplaceable, the loss of the services of any of these individuals would be disruptive to our business. We believe that our overall future success depends in large part upon our ability to attract and retain highly skilled managerial and marketing personnel. There is no assurance that we will be successful in attracting and retaining such personnel on terms acceptable to the Company or the employee. Inadequate personnel will limit our growth, and will be seen as a detriment to our prospects, leading potentially to a loss in value for investors.

We are controlled by a small group of our existing stockholders, whose interests may differ from other stockholders.

Our Chairman, Chief Executive Officer and President, Mr. Gang Li, beneficially owns approximately 36.16% of the outstanding shares of our common stock and is our largest single stockholder. Together with, Ms Lihua Wang, who is our Chief Financial Officer, they own 45.2% of the outstanding shares of our common stock. Accordingly these stockholders acting together will have significant influence in determining the outcome of any corporate transaction or other matter submitted to the stockholders for approval, including mergers, consolidations, the sale of all or substantially all of our assets, election of directors and other significant corporate actions. They will also have significant influence in preventing or causing a change in control. In addition, without the consent of these stockholders, we may be prevented from entering into certain transactions which may be beneficial to our other stockholders. The interests of these stockholders may differ from the interests of the other stockholders.

We are responsible for the indemnification of our officers and directors.

Delaware law and our Bylaws provide for the indemnification of our directors, officers, employees, and agents, under certain circumstances, against costs and expenses incurred by them in any litigation to which they become a party arising from their association with or activities on our behalf. Consequently, we may be required to expend substantial funds to satisfy these indemnity obligations. Any payment in respect of these indemnification rights could have an adverse effect on our cash flow and our results of operations.

If we fail to implement effective internal controls required by the Sarbanes-Oxley Act of 2002, or remedy any material weaknesses in our internal controls that we may identify, such failure could result in material misstatements in our financial statements, cause investors to lose confidence in our reported financial information and have a negative effect on the trading price of our common stock.

Section 404 of the Sarbanes-Oxley Act of 2002 requires management of public companies to develop and implement internal controls over financial reporting and evaluate the effectiveness thereof. A material weakness is a deficiency or a combination of deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of our annual interim financial statement will not be prevented or detected on a timely basis. Due to the Company’s limited resources, the Company does not have accounting personnel with extensive experience in maintaining books and records and preparing financial statements in accordance with US GAAP which could lead to untimely identification and resolution of accounting matters inherent in the Company’s financial transactions in accordance with US GAAP.

| 24 | ||

Any failure to complete our assessment of our internal controls over financial reporting, to remediate any material weaknesses that we may identify, including the one identified above, or to implement new or improved controls, could harm our operating results, cause us to fail to meet our reporting obligations or result in material misstatements in our financial statements. Inadequate disclosure controls and procedures and internal controls over financial reporting could also cause investors to lose confidence in our public disclosures and reported financial information, which could have a negative effect on the trading price of our common stock.

The inability to inspect may prevent the PCAOB from regularly evaluating our auditor’s audits and its quality control procedures since our auditors come from Hong Kong rather than United States.

Public company auditors are required by law to undergo regular Public Company Accounting Oversight Board, or PCAOB, inspections to assess their compliance with U.S. law and professional standards in connection with their audits of public company financial statements filed with the SEC. Due to the position taken by the authorities in China, the PCAOB was prevented from conducting inspections of certain registered firms in Hong Kong to the extent that their audit clients had operations in China.

The inability of the PCAOB to conduct inspections of auditors in the PRC makes it more difficult to evaluate the effectiveness of our independent registered public accounting firm’s audit procedures or quality control procedures as compared to auditors outside of the PRC that are subject to PCAOB inspections, which could cause investors and potential investors in our stock to lose confidence in our audit procedures and reported financial information and the quality of our financial statements.