Exhibit 99.1

Western

Alliance Reports Profit of $5.2 million for the First Quarter 2011

PHOENIX--(BUSINESS WIRE)--April 25, 2011--Western Alliance

Bancorporation (NYSE:WAL) announced today its financial results for the

first quarter 2011.

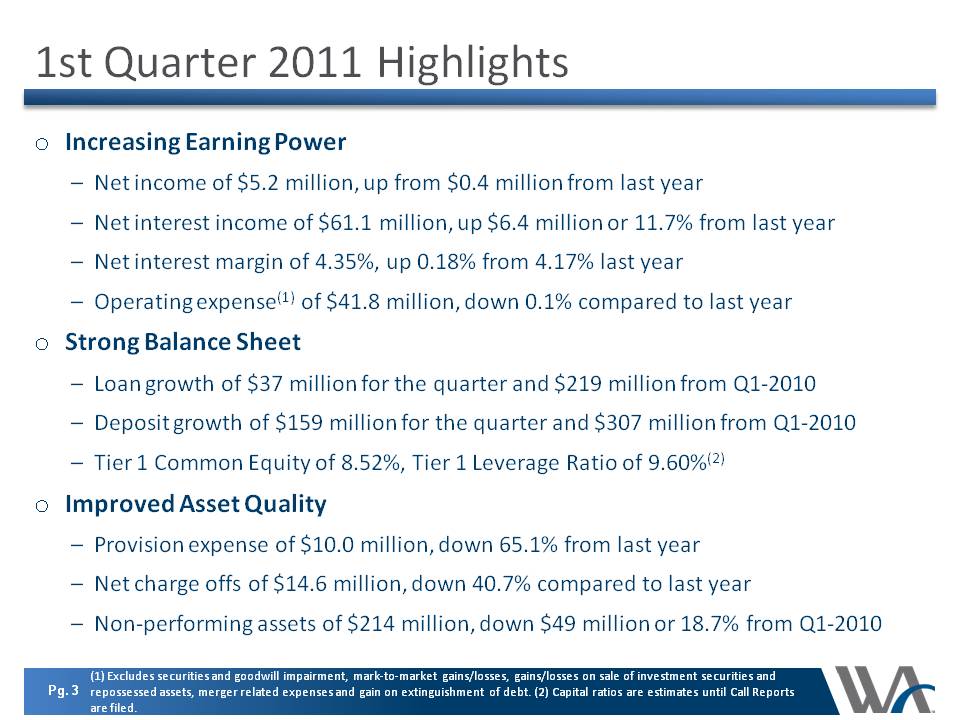

First Quarter 2011 Highlights:

-

Net income of $0.03 per common share, compared to net loss of $0.17

for the fourth quarter 2010 and $0.03 net loss for the first quarter

of 2010

-

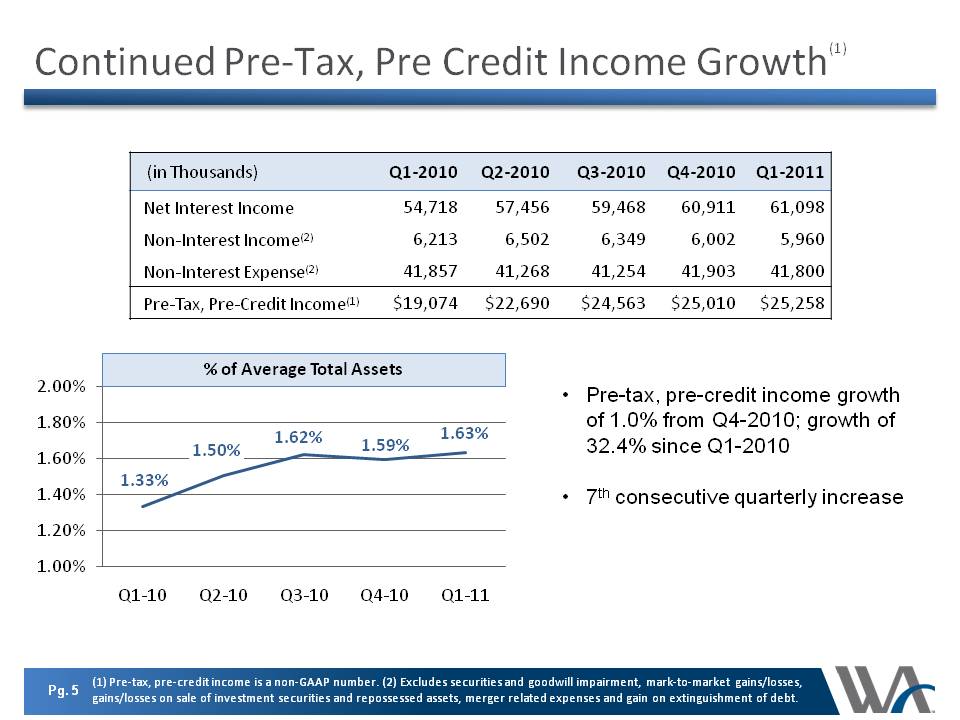

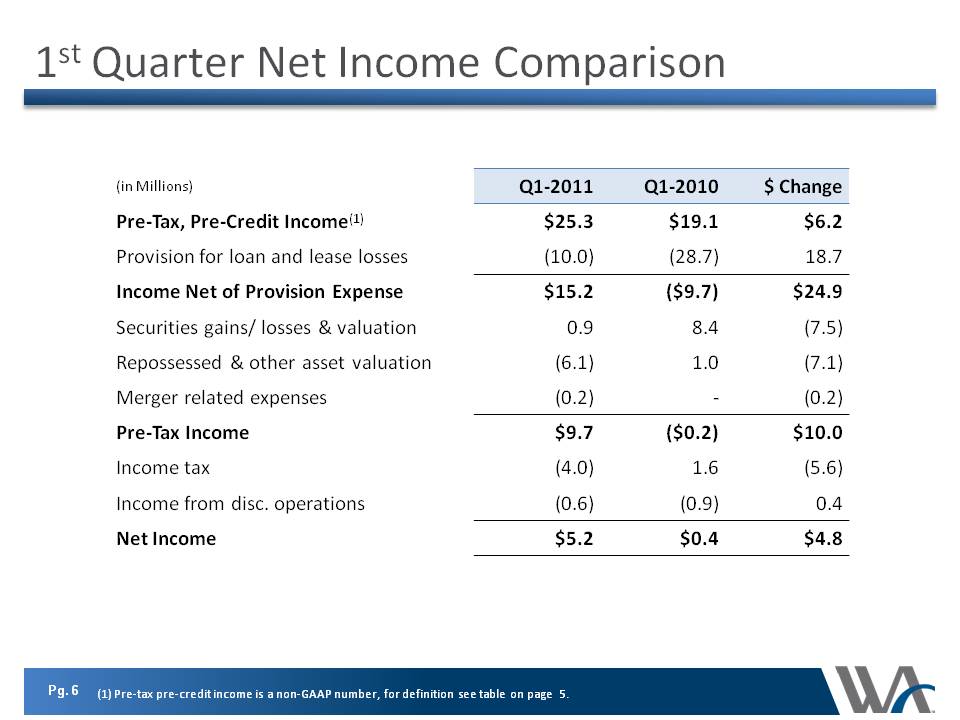

Pre-tax, pre-provision operating earnings of $25.3 million, up from

$25.0 million in fourth quarter 2010 and up 32.4% from $19.1 million

in first quarter 20101

-

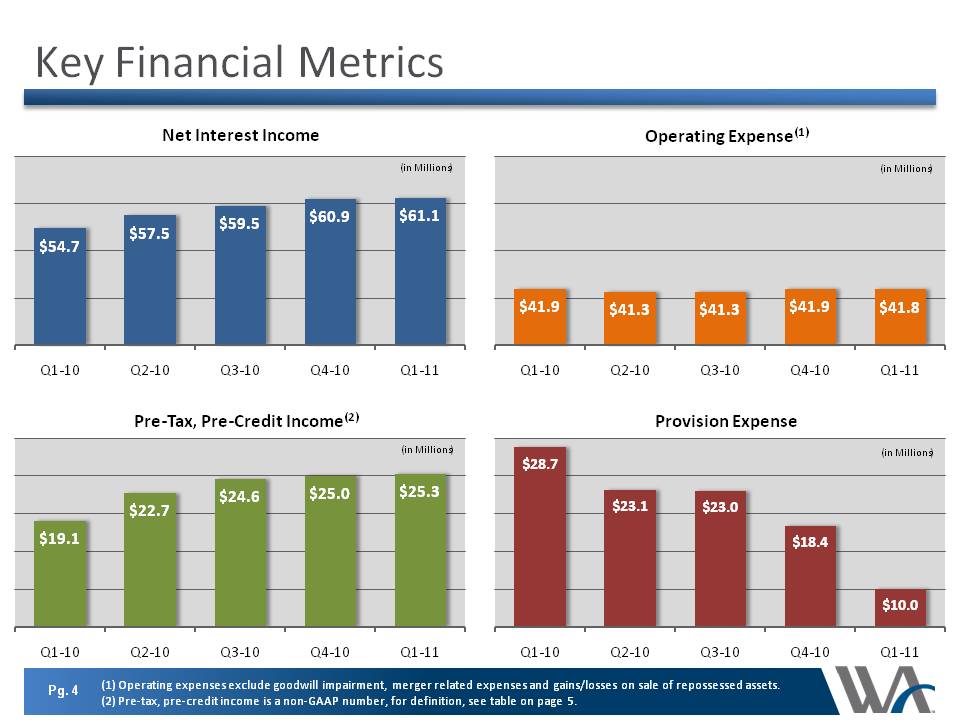

Record net interest income of $61.1 million, compared to $60.9 million

in prior quarter and $54.7 million in same quarter last year

-

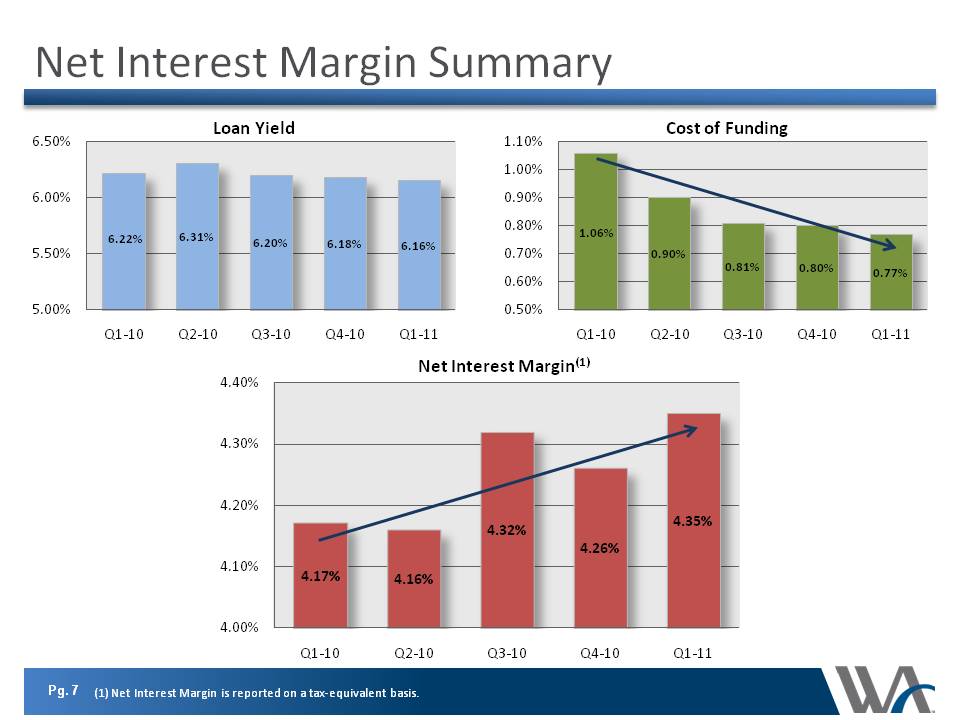

Net interest margin of 4.35%, compared to 4.26% in fourth quarter of

2010 and 4.17% in first quarter last year

-

Total loans of $4.28 billion, up $37 million from December 31, 2010

and up $219 million from March 31, 2010

-

Total deposits of $5.50 billion, up $159 million from December 31,

2010 and up $307 million from March 31, 2010

-

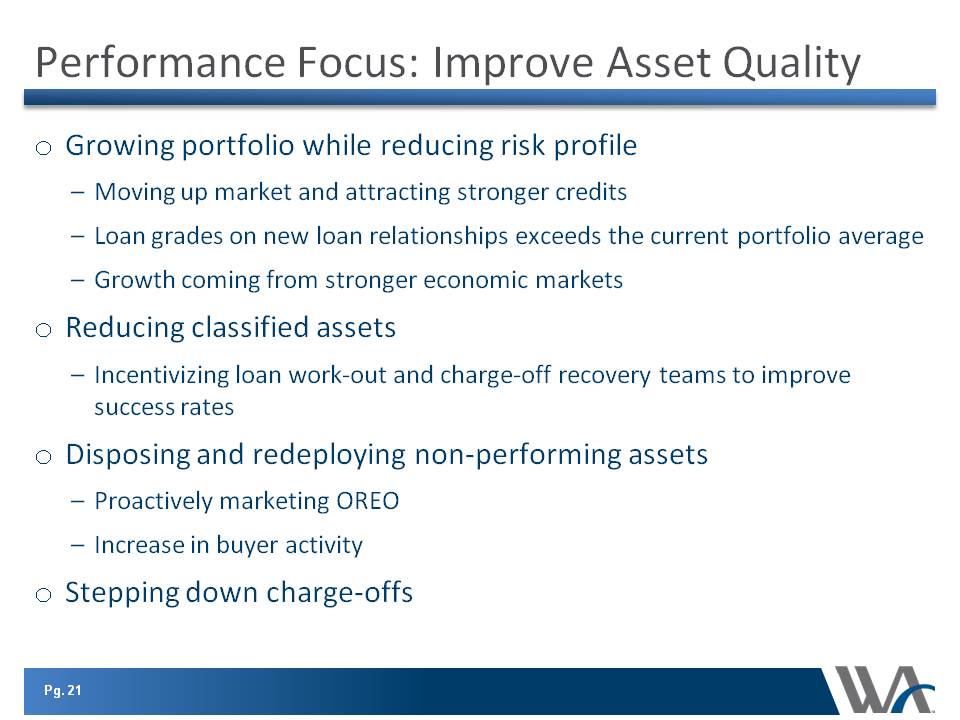

Nonperforming assets (nonaccrual loans and repossessed assets) of 3.3%

of total assets, compared to 3.6% in fourth quarter 2010 and 4.2% in

first quarter 2010

-

Total watch and classified loans (including nonaccrual) of $445

million at March 31, 2011, compared to $452 million at December 31,

2010 and $603 million at March 31, 2010

-

Provision for credit losses of $10.0 million, compared to $18.4

million in the fourth quarter 2010 and $28.7 million in first quarter

last year

-

Net loan charge-offs of $14.6 million, down from $15.9 million for the

fourth quarter 2010 and $24.6 million in first quarter last year

-

Net income of $5.2 million, including pre-tax loss on repossessed

asset valuations/sales of $6.1 million

-

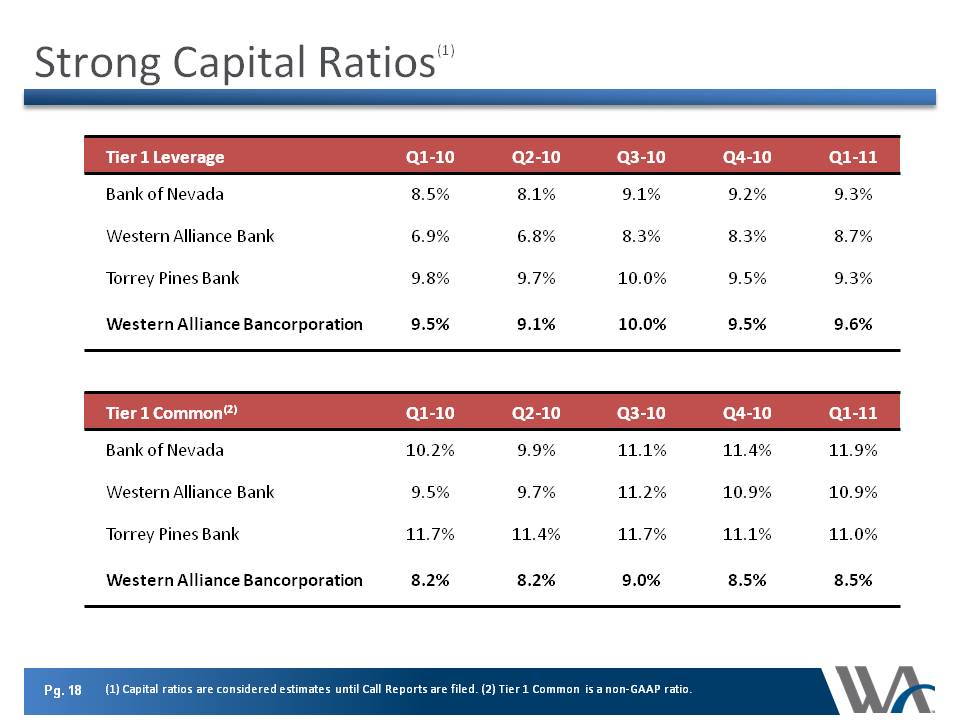

Tier I Leverage capital of 9.6% and Total Risk-Based Capital ratio of

13.2%, compared to 9.5% and 14.6% a year ago

Financial Performance

“I’m pleased with our strong start in 2011 with an increase in our top

line performance, driven by loan and deposit growth and an expanding

margin, and our bottom line performance through increased efficiency and

improved asset quality,” said Robert Sarver, Chairman and Chief

Executive Officer of Western Alliance Bancorporation. “For the first

time in three years, each of our operating units was profitable. We

continue to make important strides on multiple fronts simultaneously as

we achieve total loan growth while reducing higher risk construction and

land exposure, and growing our deposits while reducing our funding

costs. These successes demonstrate our continued progress toward

achieving our full operating potential.”

Ken Vecchione, President and Chief Operating Officer, added, “Western

Alliance continues to demonstrate predictability along with improving

credit metrics. Over the last several quarters our Company has shown

consistent loan growth, improving quarter-to-quarter net interest

income, expense discipline, increasing operating leverage, and strong

core profitability dynamics. Focus on our long-term objectives, adhering

to our straight-forward business model, and the improving backdrop of

credit quality help produce our best quarterly financial results since

2007.”

Western Alliance Bancorporation reported net income of $5.2 million in

the first quarter 2011, including a net loss from sales/valuation of

repossessed assets of $6.1 million and a loss on discontinued operations

net of tax of $0.6 million.

The Company reported net income per common share of $0.03 in the first

quarter 2011. The income included $0.05 loss from sales/valuations of

repossessed assets after tax and a net loss from discontinued affinity

credit card operations held for sale net of tax of $0.01.

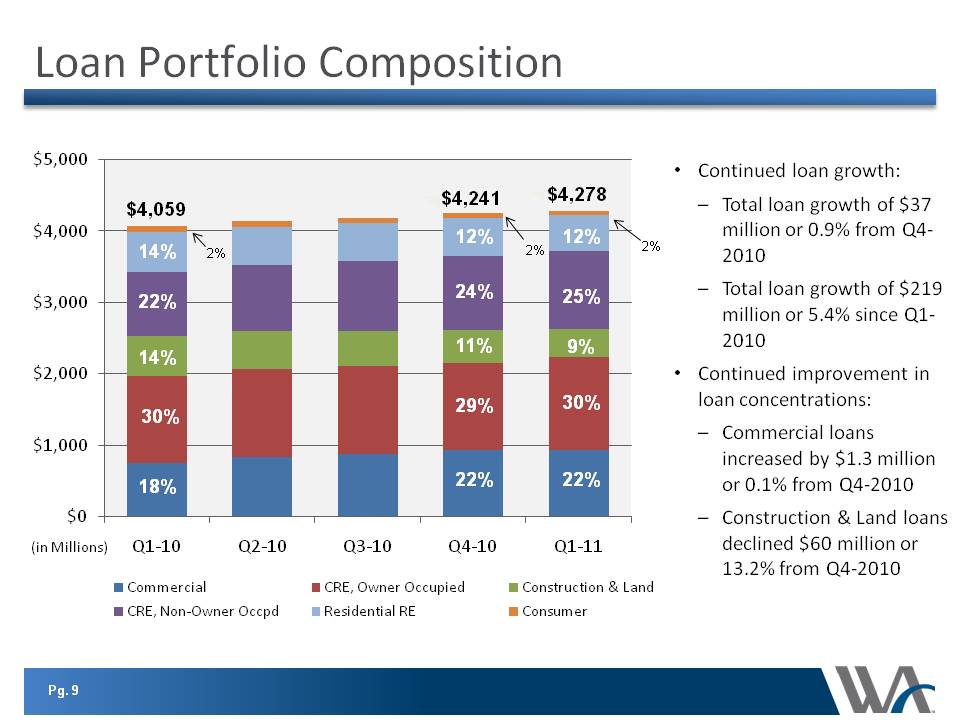

Total loans increased $37 million to $4.28 billion at March 31, 2011

from $4.24 billion on December 31, 2010. This increase was driven by

growth in commercial real estate loans and commercial leases; partially

offset by reductions in all other loan types. Geographically, loans

outstanding at our Las Vegas, Nevada affiliate decreased by $42 million

and increased by $79 million at our other affiliates. Loans increased

$219 million from March 31, 2010.

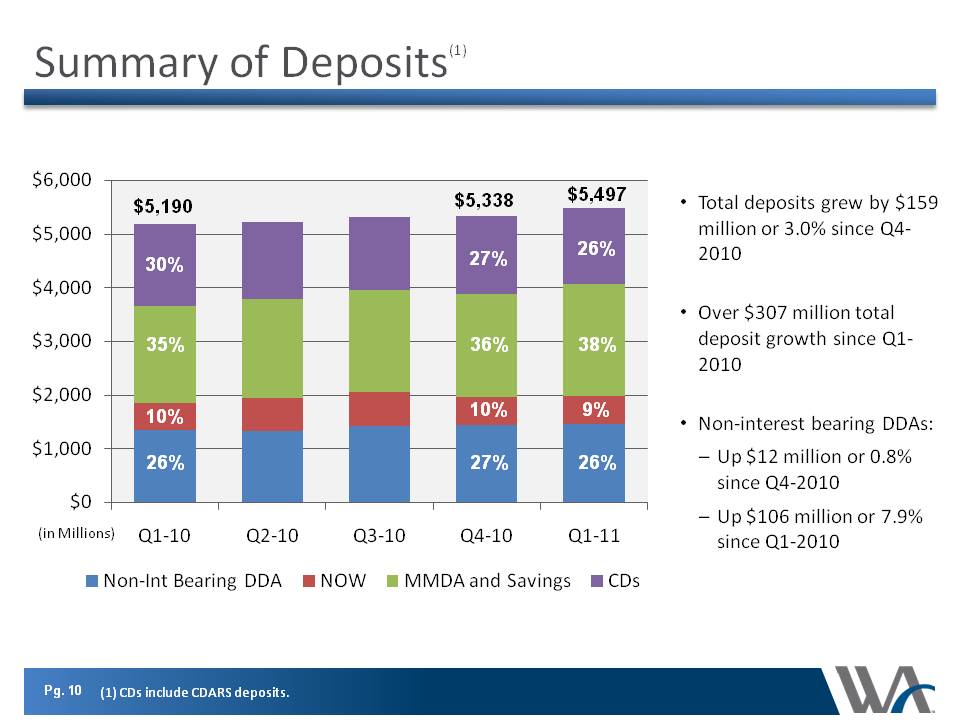

Total deposits increased $159 million to $5.50 billion at March 31, 2011

from $5.34 billion at December 31, 2010, with significant growth in

money market/savings accounts and, non-interest bearing demand deposits

offset by a decline in certificates of deposits and interest bearing

demand deposits. Deposits increased $307 million from March 31, 2010.

Income Statement

Net interest income increased slightly to $61.1 million in the first

quarter 2011 from $60.9 million in the fourth quarter 2010 and 11.7

percent compared to the first quarter 2010, propelled by reductions in

cost of funds. The net interest margin in the first quarter 2011 was

4.35 percent compared to 4.26 percent in the fourth quarter 2010 and

4.17 percent in the first quarter of 2010.

Operating non-interest income was $6.0 million for the first quarter

2011.1 This performance was a decrease from $6.2 million for

the same period in 2010 and the same as fourth quarter of 2010,

resulting from the disposition of the majority of our asset management

businesses.1

Net revenue was $67.1 million for the first quarter 2011, a slight

increase from $66.9 million for the fourth quarter of 2010 and 10.2

percent from net revenue of $60.9 million for the first quarter 2010.1

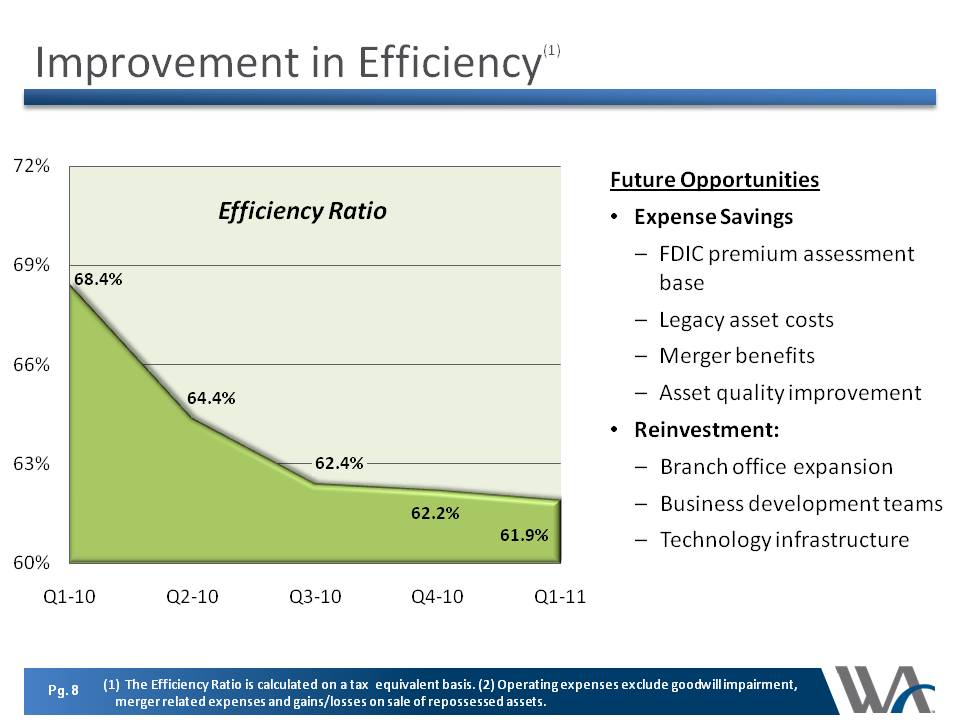

Operating non-interest expense was $41.8 million for the first quarter

2011, compared to $41.9 million for the fourth quarter of 2010 and the

same period in 2010.1 The operating efficiency ratio was 62

percent for the first quarter 2011, compared to 68 percent for the first

quarter 2010.1 The Company had 894 full-time equivalent

employees at March 31, 2011, compared to 948 one year ago.

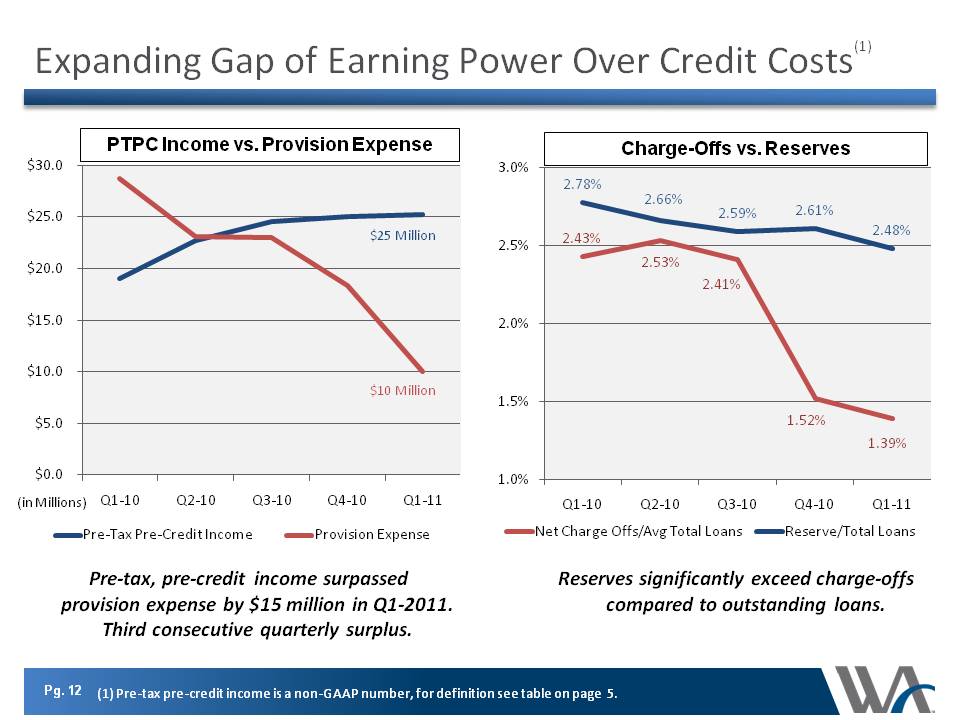

A key performance metric for the Company is its pre-tax, pre-provision

operating earnings, which it defines as net revenue less its operating

non-interest expense.1 For the first quarter 2011, the

Company’s performance was $25.3 million, compared to $25.0 million in

the fourth quarter 2010 and $19.1 million in the first quarter 2010.1

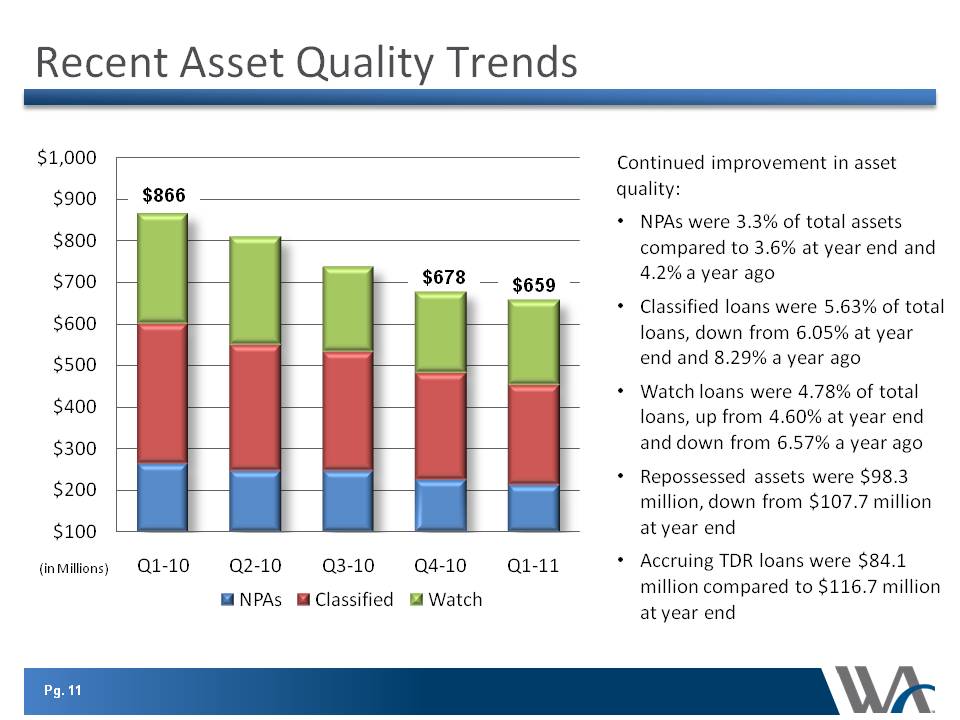

The provision for credit losses was $10.0 million for the first quarter

2011 compared to $18.4 million for the fourth quarter 2010 and $28.7

million for the first quarter 2010. Nonaccrual loans and repossessed

assets were $213 million or 3.3 percent of total assets at March 31,

2011, down from $225 million or 3.6 percent of total assets at December

31, 2010 and $254 million or 4.2 percent of total assets at March 31,

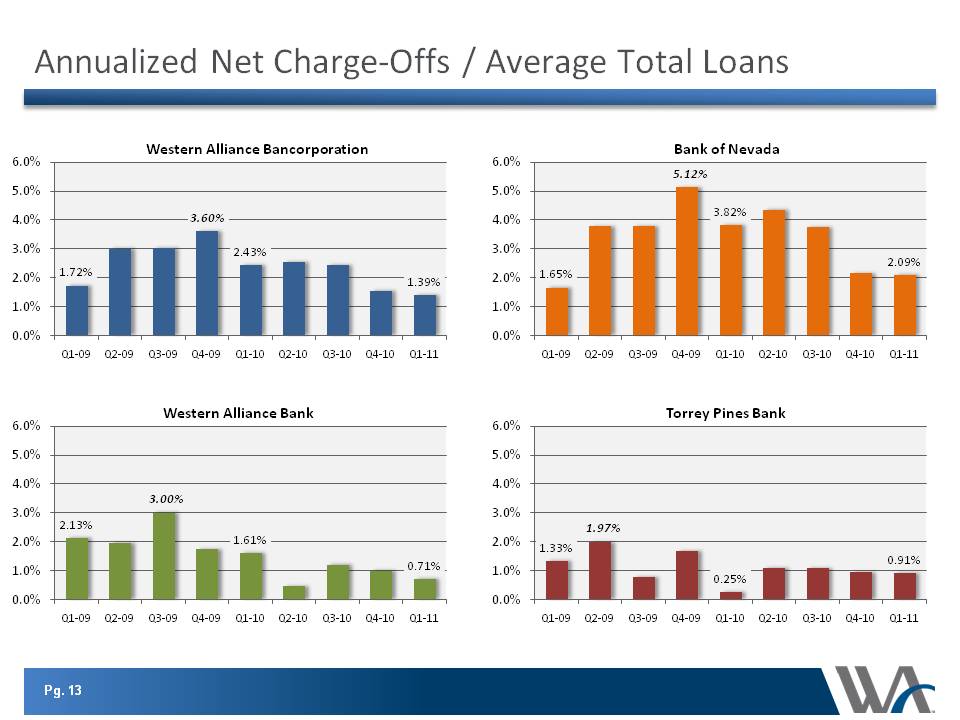

2010. Net loan charge-offs in the first quarter 2011 were $14.6 million

or 1.39 percent of average loans (annualized), down from $15.9 million

or 1.52 percent of average loans (annualized) for the fourth quarter

2010 and $24.6 million or 2.43% of average loans (annualized) for the

first quarter 2010. Loans past due 90 days and still accruing totaled

$1.1 million at March 31, 2011, down from $1.5 million at December 31,

2010 and down from $8.4 million at March 31, 2010. Loans past due 30-89

days totaled $30.7 million at quarter end, up from $18.2 million at

December 31, 2010 and down from $38.6 million at March 31, 2010.

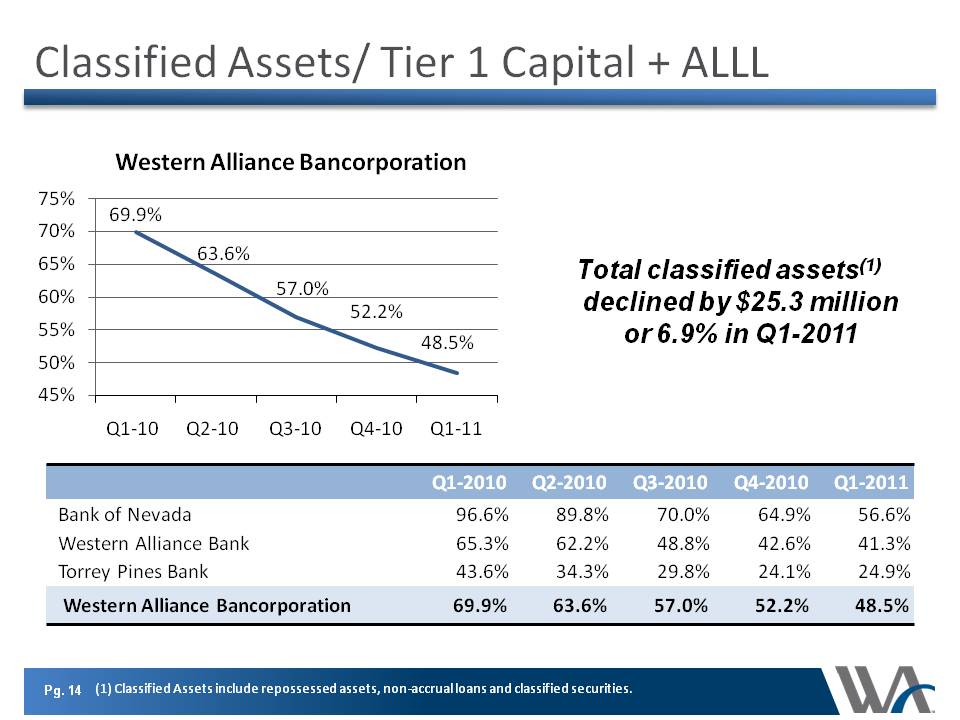

Classified assets to Tier I capital plus allowance for credit losses, a

common regulatory measure of asset quality, improved to 48 percent at

March 31, 2011 from 70 percent one year ago.1

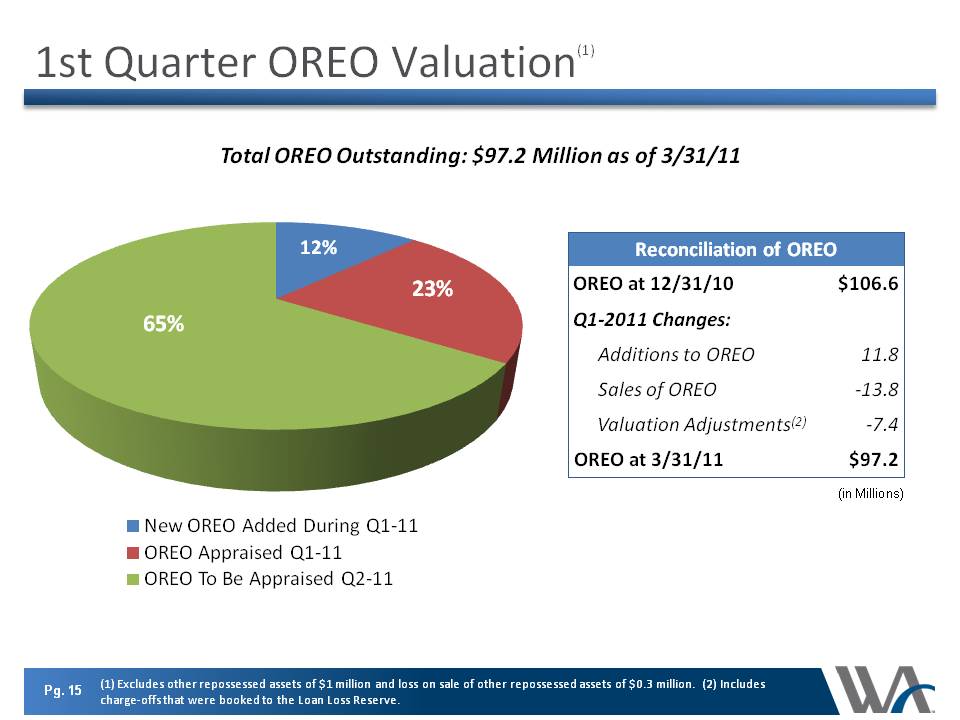

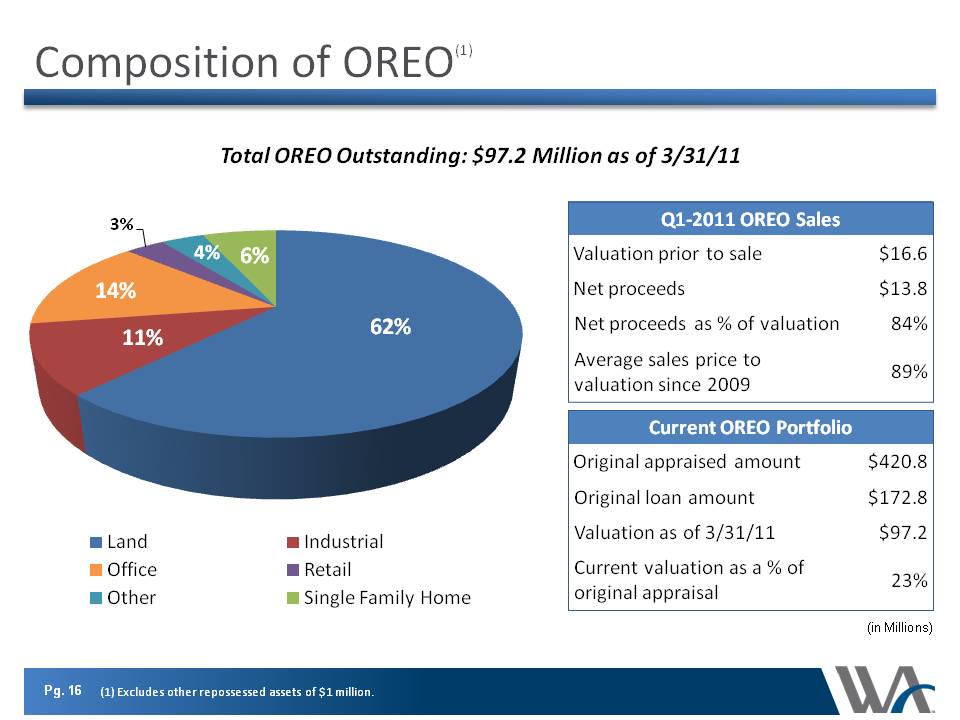

Net loss on sales and valuation of repossessed assets (primarily other

real estate) was $6.1 million for the first quarter 2011 compared to

$13.0 million in the prior quarter. At March 31, 2011, other repossessed

assets were valued at $98 million compared to $108 million at December

31, 2010.

During the first quarter 2011, the Company completed its consolidations

of its Alta Alliance Bank subsidiary into Torrey Pines Bank and its

First Independent Bank of Nevada subsidiary into Alliance Bank of

Arizona doing business as Western Alliance Bank and incurred $0.2

million in merger charges related to these transactions.

Balance Sheet

Gross loans totaled $4.28 billion at March 31, 2011, an increase of $37

million from December 31, 2010 and an increase of $219 million from

$4.06 billion at March 31, 2010. At March 31, 2011 the allowance for

credit losses was 2.48 percent of total loans down from 2.61 percent at

December 31, 2010 and 2.78 percent at March 31, 2010.

Deposits totaled $5.50 billion at March 31, 2011, an increase of $159

million from $5.34 billion at December 31, 2010 and an increase of $307

million from $5.19 billion at March 31, 2010.

Non-interest bearing deposits increased by $11.8 million to $1.46

billion at March 31, 2011 from December 31, 2010 and increased $106.3

million from $1.35 billion at March 31, 2010. Non-interest bearing

deposits comprised 26.5 percent of total deposits at March 31, 2011,

compared to 26 percent a year ago.

At March 31, 2011 the Company’s loans were 77.8 percent of deposits,

compared to 78.2 percent one year earlier and 79.4 percent at December

31, 2010.

Stockholders’ equity at March 31, 2011 was essentially flat at $601.6

million from $602.2 million at December 31, 2010. At March 31, 2011,

tangible common equity was 6.8 percent of tangible assets1

and total risk-based capital was 13.2 percent of risk-weighted assets.

Total assets increased 5 percent to $6.40 billion at March 31, 2011 from

$6.10 billion at March 31, 2010 and increased 3.4 percent from $6.19

billion at December 31, 2010.

Operating Unit Highlights

Bank of Nevada reported that loans declined $42 million during the first

quarter of 2011 and declined $141 million during the last 12 months to

$1.87 billion at March 31, 2011. Deposits increased slightly since

December 31, 2010 and increased $123 million over the last twelve months

to $2.39 billion. Net income for Bank of Nevada was $0.9 million during

the first quarter 2011, compared with net losses of $5.8 million for the

fourth quarter of 2010 and $3.0 million during the first quarter 2010.

Western Alliance Bank reported loan growth of $39 million during the

first quarter 2011 and an increase of $190 million during the last 12

months to $1.34 billion. Deposits increased $22 million in the first

quarter and decreased $18 million during the last 12 months to $1.69

billion. Net income for Western Alliance Bank was $4.9 million during

the first quarter 2011 compared with net income of $3.6 million during

the fourth quarter of 2010 and a net income of $1.1 million during the

first quarter 2010.

Torrey Pines Bank segment, which excludes discontinued operations,

reported that loans increased $40 million during the first quarter 2011

and increased $169 million during the last 12 months to $1.10 billion.

Deposits increased $135 million and $201 million to $1.42 billion during

the same periods, respectively. Net income for Torrey Pines Bank was

$4.0 million during the first quarter 2011 compared with net income of

$3.2 million for the fourth quarter of 2010 and net income of $0.5

million during the first quarter 2010.

Attached to this press release is summarized financial information for

the quarter ended March 31, 2011.

Conference Call and Webcast

Western Alliance Bancorporation will host a conference call and live

audio webcast to discuss its first quarter 2011 financial results at

12:00 p.m. ET on Monday, April 25, 2011. Participants may access the

call by dialing 1-866-843-0890 and using passcode: 1293839 or via live

audio webcast using the website link: http://www.talkpoint.com/viewer/starthere.asp?Pres=135049.

The webcast is also available via our website at www.westernalliancebancorp.com.

Participants should log in at least 15 minutes early to receive

instructions. The call will be recorded and made available for replay

after 2:00 p.m. ET, April 25, until 9 a.m. ET, May 9, by dialing

1-877-344-7529 and using the passcode: 449879.

About Western Alliance Bancorporation

Western Alliance Bancorporation is the parent company of Bank of Nevada,

Western Alliance Bank doing business as Alliance Bank of Arizona and

First Independent Bank, Torrey Pines Bank, and Shine Investment Advisory

Services. These dynamic organizations provide a broad array of deposit

and credit services to clients in Nevada, Arizona and California, and

investment services in Colorado. Staffed with experienced financial

professionals, these organizations deliver a broader product array and

larger credit capacity than community banks, yet are empowered to be

more responsive to customers' needs than larger institutions. Additional

investor information can be accessed on the Investor Relations page of

the company's website, www.westernalliancebancorp.com.

Cautionary Note Regarding Forward-Looking Statements

This release contains forward-looking statements that relate to

expectations, beliefs, projections, future plans and strategies,

anticipated events or trends and similar expressions concerning matters

that are not historical facts. The forward-looking statements contained

herein reflect our current views about future events and financial

performance and are subject to risks, uncertainties, assumptions and

changes in circumstances that may cause our actual results to differ

significantly from historical results and those expressed in any

forward-looking statement. Some factors that could cause actual results

to differ materially from historical or expected results include:

factors listed in the Form 10-K as filed with the Securities and

Exchange Commission; changes in general economic conditions, either

nationally or locally in the areas in which we conduct or will conduct

our business; inflation, interest rate, market and monetary

fluctuations; increases in competitive pressures among financial

institutions and businesses offering similar products and services;

higher defaults on our loan portfolio than we expect; changes in

management’s estimate of the adequacy of the allowance for credit

losses; legislative or regulatory changes or changes in accounting

principles, policies or guidelines; management’s estimates and

projections of interest rates and interest rate policy; the execution of

our business plan; and other factors affecting the financial services

industry generally or the banking industry in particular.

We do not intend and disclaim any duty or obligation to update or revise

any industry information or forward-looking statements set forth in this

press release to reflect new information, future events or otherwise.

This press release contains both financial measures based on accounting

principles generally accepted in the United States (“GAAP”) and non-GAAP

based financial measures, which are used where management believes it to

be helpful in understanding Western Alliance Bancorporation’s results of

operations or financial position. Where non-GAAP financial measures are

used, the comparable GAAP financial measure, as well as the

reconcilement to the comparable GAAP financial measure, can be found in

this press release. These disclosures should not be viewed as a

substitute for operating results determined in accordance with GAAP, nor

are they necessarily comparable to non-GAAP performance measures that

may be presented by other companies.

1 See Reconciliation of Non-GAAP Financial Measures beginning

on page 15

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Western Alliance Bancorporation and Subsidiaries

|

|

Summary Consolidated Financial Data

|

|

Unaudited

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

At or for the Three Months

|

|

|

|

|

|

|

|

|

Ended March 31,

|

|

|

|

|

|

|

|

|

2011

|

|

|

|

2010

|

|

|

|

Change %

|

|

|

|

|

|

|

|

|

(in thousands, except per share data)

|

|

|

Selected Balance Sheet Data:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(dollars in millions)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets

|

|

|

|

|

|

$

|

6,404.8

|

|

|

|

|

$

|

6,096.2

|

|

|

|

|

5.1

|

|

%

|

|

Loans, net of deferred fees

|

|

|

|

|

|

|

4,278.0

|

|

|

|

|

|

4,059.1

|

|

|

|

|

5.4

|

|

|

|

Securities and money market investments

|

|

|

|

|

|

|

1,319.6

|

|

|

|

|

|

781.1

|

|

|

|

|

68.9

|

|

|

|

Federal funds sold

|

|

|

|

|

|

|

-

|

|

|

|

|

|

2.4

|

|

|

|

|

(100.0

|

)

|

|

|

Total deposits

|

|

|

|

|

|

|

5,497.5

|

|

|

|

|

|

5,190.1

|

|

|

|

|

5.9

|

|

|

|

Borrowings

|

|

|

|

|

|

|

73.0

|

|

|

|

|

|

20.0

|

|

|

|

|

265.0

|

|

|

|

Junior subordinated and subordinated debt

|

|

|

|

|

|

|

43.0

|

|

|

|

|

|

102.3

|

|

|

|

|

(58.0

|

)

|

|

|

Stockholders' equity

|

|

|

|

|

|

|

601.6

|

|

|

|

|

|

575.7

|

|

|

|

|

4.5

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Income Statement Data:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(dollars in thousands)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest income

|

|

|

|

|

|

$

|

71,966

|

|

|

|

|

$

|

68,734

|

|

|

|

|

4.7

|

|

%

|

|

Interest expense

|

|

|

|

|

|

|

10,868

|

|

|

|

|

|

14,016

|

|

|

|

|

(22.5

|

)

|

|

|

Net interest income

|

|

|

|

|

|

|

61,098

|

|

|

|

|

|

54,718

|

|

|

|

|

11.7

|

|

|

|

Provision for loan losses

|

|

|

|

|

|

|

10,041

|

|

|

|

|

|

28,747

|

|

|

|

|

(65.1

|

)

|

|

|

Net interest income after provision for credit losses

|

|

|

|

|

|

|

51,057

|

|

|

|

|

|

25,971

|

|

|

|

|

96.6

|

|

|

|

Non-interest income

|

|

|

|

|

|

|

6,830

|

|

|

|

|

|

14,629

|

|

|

|

|

(53.3

|

)

|

|

|

Non-interest expense

|

|

|

|

|

|

|

48,146

|

|

|

|

|

|

40,843

|

|

|

|

|

17.9

|

|

|

|

Income (loss) from continuing operations before income taxes

|

|

|

|

|

|

|

9,741

|

|

|

|

|

|

(243

|

)

|

|

|

|

(4,108.6

|

)

|

|

|

Income tax expense (benefit)

|

|

|

|

|

|

|

4,029

|

|

|

|

|

|

(1,562

|

)

|

|

|

|

(357.9

|

)

|

|

|

Income from continuing operations

|

|

|

|

|

|

|

5,712

|

|

|

|

|

|

1,319

|

|

|

|

|

333.1

|

|

|

|

Loss on discontinued operations, net

|

|

|

|

|

|

|

(559

|

)

|

|

|

|

|

(935

|

)

|

|

|

|

(40.2

|

)

|

|

|

Net income

|

|

|

|

|

|

$

|

5,153

|

|

|

|

|

$

|

384

|

|

|

|

|

1,241.9

|

|

%

|

|

Diluted net income (loss) from continuing operations

|

|

|

|

|

|

$

|

0.04

|

|

|

|

|

$

|

(0.02

|

)

|

|

|

|

|

|

|

Diluted net loss from discontinued operations, net of tax

|

|

|

|

|

|

$

|

(0.01

|

)

|

|

|

|

$

|

(0.01

|

)

|

|

|

|

|

|

|

Diluted net income (loss) per common share

|

|

|

|

|

|

$

|

0.03

|

|

|

|

|

$

|

(0.03

|

)

|

|

|

|

(200.0

|

)

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common Share Data:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Diluted net income (loss) per common share

|

|

|

|

|

|

$

|

0.03

|

|

|

|

|

$

|

(0.03

|

)

|

|

|

|

(200.0

|

)

|

%

|

|

Book value per common share

|

|

|

|

|

|

$

|

5.72

|

|

|

|

|

$

|

6.12

|

|

|

|

|

(6.5

|

)

|

%

|

|

Tangible book value per share, net of tax (1)

|

|

|

|

|

|

$

|

5.30

|

|

|

|

|

$

|

5.62

|

|

|

|

|

(5.7

|

)

|

%

|

|

Average shares outstanding (in thousands):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

|

|

|

|

|

|

|

80,794

|

|

|

|

|

|

71,965

|

|

|

|

|

12.3

|

|

|

|

Diluted

|

|

|

|

|

|

|

81,103

|

|

|

|

|

|

71,965

|

|

|

|

|

12.7

|

|

|

|

Common shares outstanding

|

|

|

|

|

|

|

82,237

|

|

|

|

|

|

73,031

|

|

|

|

|

12.6

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) See Reconciliation of Non-GAAP Financial Measures

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Western Alliance Bancorporation and Subsidiaries

|

|

Summary Consolidated Financial Data (continued)

|

|

Unaudited

|

|

|

|

|

|

|

|

|

|

At or for the Three Months

|

|

|

|

|

|

|

|

|

Ended March 31,

|

|

|

|

|

|

|

|

|

2011

|

|

|

|

2010

|

|

|

|

Change %

|

|

|

|

|

|

|

|

|

(in thousands, except per share data)

|

|

|

Selected Performance Ratios:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average assets (1)

|

|

|

|

|

|

0.33

|

%

|

|

|

0.03

|

%

|

|

|

1,000.0

|

|

%

|

|

Return on average stockholders' equity (1)

|

|

|

|

|

|

3.41

|

|

|

|

0.27

|

|

|

|

1,163.0

|

|

|

|

Net interest margin (1)

|

|

|

|

|

|

4.35

|

|

|

|

4.17

|

|

|

|

4.3

|

|

|

|

Net interest spread

|

|

|

|

|

|

4.06

|

|

|

|

3.84

|

|

|

|

5.7

|

|

|

|

Efficiency ratio - tax equivalent basis (2)

|

|

|

|

|

|

61.89

|

|

|

|

68.42

|

|

|

|

(9.5

|

)

|

|

|

Loan to deposit ratio

|

|

|

|

|

|

77.82

|

|

|

|

78.21

|

|

|

|

(0.5

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital Ratios:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tangible equity (2)

|

|

|

|

|

|

8.8

|

%

|

|

|

8.8

|

%

|

|

|

0.4

|

|

%

|

|

Tangible common equity (2)

|

|

|

|

|

|

6.8

|

|

|

|

6.7

|

|

|

|

1.4

|

|

|

|

Tier one common equity (2)

|

|

|

|

|

|

8.5

|

|

|

|

8.2

|

|

|

|

3.5

|

|

|

|

Tier 1 Leverage ratio (3)

|

|

|

|

|

|

9.6

|

|

|

|

9.5

|

|

|

|

1.1

|

|

|

|

Tier 1 Risk Based Capital (3)

|

|

|

|

|

|

12.0

|

|

|

|

12.0

|

|

|

|

0.0

|

|

|

|

Total Risk Based Capital (3)

|

|

|

|

|

|

13.2

|

|

|

|

14.6

|

|

|

|

(9.6

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Asset Quality Ratios:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net charge-offs to average loans outstanding (1)

|

|

|

|

|

|

1.39

|

%

|

|

|

2.43

|

%

|

|

|

(42.8

|

)

|

%

|

|

Nonaccrual loans to gross loans

|

|

|

|

|

|

2.67

|

|

|

|

3.66

|

|

|

|

(27.0

|

)

|

|

|

Nonaccrual loans and repossessed assets to total assets

|

|

|

|

|

|

3.32

|

|

|

|

4.17

|

|

|

|

(20.4

|

)

|

|

|

Loans past due 90 days and still accruing to total loans

|

|

|

|

|

|

0.03

|

|

|

|

0.21

|

|

|

|

(85.7

|

)

|

|

|

Allowance for credit losses to loans

|

|

|

|

|

|

2.48

|

|

|

|

2.78

|

|

|

|

(10.8

|

)

|

|

|

Allowance for credit losses to nonaccrual loans

|

|

|

|

|

|

92.90

|

|

|

|

75.78

|

|

|

|

22.6

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) Annualized for the three month periods ended March 31, 2011 and

2010.

|

|

(2) See Reconciliation of Non-GAAP Financial Measures.

|

|

(3) Capital ratios are preliminary until Call Reports are filed.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Western Alliance Bancorporation and Subsidiaries

|

|

Condensed Consolidated Statements of Operations

|

|

Unaudited

|

|

|

|

|

|

Three Months Ended

|

|

|

|

|

|

|

|

March 31,

|

|

|

|

|

|

|

|

2011

|

|

|

|

|

|

2010

|

|

Interest income:

|

|

|

|

|

|

(dollars in thousands)

|

|

Loans

|

|

|

|

|

|

$

|

63,882

|

|

|

|

|

|

|

$

|

62,350

|

|

|

Investment securities

|

|

|

|

|

|

|

7,930

|

|

|

|

|

|

|

|

6,121

|

|

|

Federal funds sold and other

|

|

|

|

|

|

|

154

|

|

|

|

|

|

|

|

263

|

|

|

Total interest income

|

|

|

|

|

|

|

71,966

|

|

|

|

|

|

|

|

68,734

|

|

|

Interest expense:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposits

|

|

|

|

|

|

|

7,898

|

|

|

|

|

|

|

|

12,079

|

|

|

Customer repurchase agreements

|

|

|

|

|

|

|

86

|

|

|

|

|

|

|

|

284

|

|

|

Borrowings

|

|

|

|

|

|

|

2,182

|

|

|

|

|

|

|

|

449

|

|

|

Junior subordinated and subordinated debt

|

|

|

|

|

|

|

702

|

|

|

|

|

|

|

|

1,204

|

|

|

Total interest expense

|

|

|

|

|

|

|

10,868

|

|

|

|

|

|

|

|

14,016

|

|

|

Net interest income

|

|

|

|

|

|

|

61,098

|

|

|

|

|

|

|

|

54,718

|

|

|

Provision for credit losses

|

|

|

|

|

|

|

10,041

|

|

|

|

|

|

|

|

28,747

|

|

|

Net interest income after provision for credit losses

|

|

|

|

|

|

|

51,057

|

|

|

|

|

|

|

|

25,971

|

|

|

Non-interest income

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unrealized (losses) gains on assets/liabilities measured at fair

value,net

|

|

|

|

|

|

|

(509

|

)

|

|

|

|

|

|

|

301

|

|

|

Securities impairment charges

|

|

|

|

|

|

|

-

|

|

|

|

|

|

|

|

(103

|

)

|

|

Gains on sales of investment securities, net

|

|

|

|

|

|

|

1,379

|

|

|

|

|

|

|

|

8,218

|

|

|

Trust and investment advisory services

|

|

|

|

|

|

|

636

|

|

|

|

|

|

|

|

1,213

|

|

|

Service charges

|

|

|

|

|

|

|

2,284

|

|

|

|

|

|

|

|

2,197

|

|

|

Operating lease income

|

|

|

|

|

|

|

671

|

|

|

|

|

|

|

|

964

|

|

|

Bank owned life insurance

|

|

|

|

|

|

|

1,184

|

|

|

|

|

|

|

|

719

|

|

|

Other

|

|

|

|

|

|

|

1,185

|

|

|

|

|

|

|

|

1,120

|

|

|

|

|

|

|

|

|

|

6,830

|

|

|

|

|

|

|

|

14,629

|

|

|

Non-interest expenses:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Salaries and employee benefits

|

|

|

|

|

|

|

22,840

|

|

|

|

|

|

|

|

21,440

|

|

|

Occupancy

|

|

|

|

|

|

|

4,854

|

|

|

|

|

|

|

|

4,787

|

|

|

Insurance

|

|

|

|

|

|

|

3,863

|

|

|

|

|

|

|

|

3,492

|

|

|

Net loss on sales and valuations of repossessed assets

|

|

|

|

|

|

|

6,129

|

|

|

|

|

|

|

|

(1,014

|

)

|

|

Repossessed asset and loan expenses

|

|

|

|

|

|

|

2,122

|

|

|

|

|

|

|

|

2,364

|

|

|

Legal, professional and director's fees

|

|

|

|

|

|

|

1,366

|

|

|

|

|

|

|

|

1,868

|

|

|

Merger related expenses

|

|

|

|

|

|

|

217

|

|

|

|

|

|

|

|

-

|

|

|

Customer service

|

|

|

|

|

|

|

892

|

|

|

|

|

|

|

|

1,065

|

|

|

Intangible amortization

|

|

|

|

|

|

|

890

|

|

|

|

|

|

|

|

907

|

|

|

Marketing

|

|

|

|

|

|

|

1,157

|

|

|

|

|

|

|

|

1,156

|

|

|

Data Processing

|

|

|

|

|

|

|

848

|

|

|

|

|

|

|

|

791

|

|

|

Operating lease depreciation

|

|

|

|

|

|

|

421

|

|

|

|

|

|

|

|

689

|

|

|

Other

|

|

|

|

|

|

|

2,547

|

|

|

|

|

|

|

|

3,298

|

|

|

|

|

|

|

|

|

|

48,146

|

|

|

|

|

|

|

|

40,843

|

|

|

Income (loss) from continuing operations before income taxes

|

|

|

|

|

|

|

9,741

|

|

|

|

|

|

|

|

(243

|

)

|

|

Income tax expense (benefit)

|

|

|

|

|

|

|

4,029

|

|

|

|

|

|

|

|

(1,562

|

)

|

|

Income from continuing operations

|

|

|

|

|

|

|

5,712

|

|

|

|

|

|

|

|

1,319

|

|

|

Loss from discontinued operations net of tax benefit

|

|

|

|

|

|

|

(559

|

)

|

|

|

|

|

|

|

(935

|

)

|

|

Net income

|

|

|

|

|

|

|

5,153

|

|

|

|

|

|

|

|

384

|

|

|

Preferred stock dividends

|

|

|

|

|

|

|

1,750

|

|

|

|

|

|

|

|

1,750

|

|

|

Accretion on preferred stock discount

|

|

|

|

|

|

|

753

|

|

|

|

|

|

|

|

716

|

|

|

Net income (loss) available to common stockholders

|

|

|

|

|

|

$

|

2,650

|

|

|

|

|

|

|

$

|

(2,082

|

)

|

|

Diluted net income (loss) per share

|

|

|

|

|

|

$

|

0.03

|

|

|

|

|

|

|

$

|

(0.03

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Western Alliance Bancorporation and Subsidiaries

|

|

Five Quarter Condensed Consolidated Statements of Operations

|

|

Unaudited

|

|

|

|

Three Months Ended

|

|

|

|

|

|

March 31,

|

|

|

|

Dec. 31,

|

|

|

|

Sept. 30,

|

|

|

|

June 30,

|

|

|

|

March 31,

|

|

|

|

|

|

2011

|

|

|

|

2010

|

|

|

|

2010

|

|

|

|

2010

|

|

|

|

2010

|

|

Interest income:

|

|

|

|

(in thousands, except per share data)

|

|

Loans

|

|

|

|

$

|

63,882

|

|

|

|

|

$

|

64,985

|

|

|

|

|

$

|

64,273

|

|

|

|

|

$

|

64,201

|

|

|

|

|

$

|

62,350

|

|

|

Investment securities

|

|

|

|

|

7,930

|

|

|

|

|

|

7,054

|

|

|

|

|

|

6,047

|

|

|

|

|

|

5,327

|

|

|

|

|

|

6,121

|

|

|

Federal funds sold and other

|

|

|

|

|

154

|

|

|

|

|

|

335

|

|

|

|

|

|

385

|

|

|

|

|

|

472

|

|

|

|

|

|

263

|

|

|

Total interest income

|

|

|

|

|

71,966

|

|

|

|

|

|

72,374

|

|

|

|

|

|

70,705

|

|

|

|

|

|

70,000

|

|

|

|

|

|

68,734

|

|

|

Interest expense:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposits

|

|

|

|

|

7,898

|

|

|

|

|

|

8,652

|

|

|

|

|

|

9,531

|

|

|

|

|

|

11,067

|

|

|

|

|

|

12,079

|

|

|

Borrowings and customer repurchase agreements

|

|

|

|

|

2,268

|

|

|

|

|

|

2,097

|

|

|

|

|

|

970

|

|

|

|

|

|

483

|

|

|

|

|

|

733

|

|

|

Junior subordinated and subordinated debt

|

|

|

|

|

702

|

|

|

|

|

|

714

|

|

|

|

|

|

736

|

|

|

|

|

|

994

|

|

|

|

|

|

1,204

|

|

|

Total interest expense

|

|

|

|

|

10,868

|

|

|

|

|

|

11,463

|

|

|

|

|

|

11,237

|

|

|

|

|

|

12,544

|

|

|

|

|

|

14,016

|

|

|

Net interest income

|

|

|

|

|

61,098

|

|

|

|

|

|

60,911

|

|

|

|

|

|

59,468

|

|

|

|

|

|

57,456

|

|

|

|

|

|

54,718

|

|

|

Provision for credit losses

|

|

|

|

|

10,041

|

|

|

|

|

|

18,384

|

|

|

|

|

|

22,965

|

|

|

|

|

|

23,115

|

|

|

|

|

|

28,747

|

|

|

Net interest income after provision for credit losses

|

|

|

|

|

51,057

|

|

|

|

|

|

42,527

|

|

|

|

|

|

36,503

|

|

|

|

|

|

34,341

|

|

|

|

|

|

25,971

|

|

|

Non-interest income

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mark-to-market (losses) gains, net

|

|

|

|

|

(509

|

)

|

|

|

|

|

(6,710

|

)

|

|

|

|

|

(210

|

)

|

|

|

|

|

6,250

|

|

|

|

|

|

301

|

|

|

Gains on sales of investment securities, net

|

|

|

|

|

1,379

|

|

|

|

|

|

-

|

|

|

|

|

|

5,460

|

|

|

|

|

|

6,079

|

|

|

|

|

|

8,218

|

|

|

Gain on extinguishment of debt

|

|

|

|

|

-

|

|

|

|

|

|

-

|

|

|

|

|

|

-

|

|

|

|

|

|

3,000

|

|

|

|

|

|

-

|

|

|

Securities impairment charges

|

|

|

|

|

-

|

|

|

|

|

|

(12

|

)

|

|

|

|

|

-

|

|

|

|

|

|

(1,071

|

)

|

|

|

|

|

(103

|

)

|

|

Trust and investment advisory services

|

|

|

|

|

636

|

|

|

|

|

|

608

|

|

|

|

|

|

1,001

|

|

|

|

|

|

1,181

|

|

|

|

|

|

1,213

|

|

|

Service charges

|

|

|

|

|

2,284

|

|

|

|

|

|

2,177

|

|

|

|

|

|

2,276

|

|

|

|

|

|

2,319

|

|

|

|

|

|

2,197

|

|

|

Operating lease income

|

|

|

|

|

671

|

|

|

|

|

|

864

|

|

|

|

|

|

998

|

|

|

|

|

|

967

|

|

|

|

|

|

964

|

|

|

Bank owned life insurance

|

|

|

|

|

1,184

|

|

|

|

|

|

1,027

|

|

|

|

|

|

773

|

|

|

|

|

|

780

|

|

|

|

|

|

719

|

|

|

Other

|

|

|

|

|

1,185

|

|

|

|

|

|

1,326

|

|

|

|

|

|

1,869

|

|

|

|

|

|

1,255

|

|

|

|

|

|

1,120

|

|

|

|

|

|

|

|

6,830

|

|

|

|

|

|

(720

|

)

|

|

|

|

|

12,167

|

|

|

|

|

|

20,760

|

|

|

|

|

|

14,629

|

|

|

Non-interest expenses:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Salaries and employee benefits

|

|

|

|

|

22,840

|

|

|

|

|

|

21,125

|

|

|

|

|

|

21,860

|

|

|

|

|

|

22,161

|

|

|

|

|

|

21,440

|

|

|

Occupancy

|

|

|

|

|

4,854

|

|

|

|

|

|

5,075

|

|

|

|

|

|

4,890

|

|

|

|

|

|

4,828

|

|

|

|

|

|

4,787

|

|

|

Insurance

|

|

|

|

|

3,863

|

|

|

|

|

|

4,109

|

|

|

|

|

|

4,115

|

|

|

|

|

|

3,759

|

|

|

|

|

|

3,492

|

|

|

Repossessed asset and loan expenses

|

|

|

|

|

2,122

|

|

|

|

|

|

2,230

|

|

|

|

|

|

1,918

|

|

|

|

|

|

1,564

|

|

|

|

|

|

2,364

|

|

|

Net (gain) loss on sales and valuations of repossessed assets

|

|

|

|

|

6,129

|

|

|

|

|

|

12,991

|

|

|

|

|

|

4,855

|

|

|

|

|

|

11,994

|

|

|

|

|

|

(1,014

|

)

|

|

Legal, professional and director's fees

|

|

|

|

|

1,366

|

|

|

|

|

|

2,038

|

|

|

|

|

|

1,546

|

|

|

|

|

|

2,139

|

|

|

|

|

|

1,868

|

|

|

Marketing

|

|

|

|

|

1,157

|

|

|

|

|

|

982

|

|

|

|

|

|

878

|

|

|

|

|

|

1,045

|

|

|

|

|

|

1,156

|

|

|

Intangible amortization

|

|

|

|

|

890

|

|

|

|

|

|

889

|

|

|

|

|

|

901

|

|

|

|

|

|

907

|

|

|

|

|

|

907

|

|

|

Customer service

|

|

|

|

|

892

|

|

|

|

|

|

1,050

|

|

|

|

|

|

987

|

|

|

|

|

|

1,154

|

|

|

|

|

|

1,065

|

|

|

Data Processing

|

|

|

|

|

848

|

|

|

|

|

|

948

|

|

|

|

|

|

842

|

|

|

|

|

|

793

|

|

|

|

|

|

791

|

|

|

Operating lease depreciation

|

|

|

|

|

421

|

|

|

|

|

|

542

|

|

|

|

|

|

627

|

|

|

|

|

|

647

|

|

|

|

|

|

689

|

|

|

Merger related expense

|

|

|

|

|

217

|

|

|

|

|

|

1,651

|

|

|

|

|

|

-

|

|

|

|

|

|

-

|

|

|

|

|

|

-

|

|

|

Other

|

|

|

|

|

2,547

|

|

|

|

|

|

2,915

|

|

|

|

|

|

2,690

|

|

|

|

|

|

2,271

|

|

|

|

|

|

3,298

|

|

|

|

|

|

|

|

48,146

|

|

|

|

|

|

56,545

|

|

|

|

|

|

46,109

|

|

|

|

|

|

53,262

|

|

|

|

|

|

40,843

|

|

|

Income (loss) from continuing operations before income taxes

|

|

|

|

|

9,741

|

|

|

|

|

|

(14,738

|

)

|

|

|

|

|

2,561

|

|

|

|

|

|

1,839

|

|

|

|

|

|

(243

|

)

|

|

Income tax expense (benefit)

|

|

|

|

|

4,029

|

|

|

|

|

|

(4,580

|

)

|

|

|

|

|

(79

|

)

|

|

|

|

|

(190

|

)

|

|

|

|

|

(1,562

|

)

|

|

Income (loss) from continuing operations

|

|

|

|

$

|

5,712

|

|

|

|

|

$

|

(10,158

|

)

|

|

|

|

$

|

2,640

|

|

|

|

|

$

|

2,029

|

|

|

|

|

$

|

1,319

|

|

|

Loss from discontinued operations, net of tax

|

|

|

|

|

(559

|

)

|

|

|

|

|

(657

|

)

|

|

|

|

|

(631

|

)

|

|

|

|

|

(802

|

)

|

|

|

|

|

(935

|

)

|

|

Net income (loss)

|

|

|

|

$

|

5,153

|

|

|

|

|

$

|

(10,815

|

)

|

|

|

|

$

|

2,009

|

|

|

|

|

$

|

1,227

|

|

|

|

|

$

|

384

|

|

|

Preferred stock dividends

|

|

|

|

|

1,750

|

|

|

|

|

|

1,750

|

|

|

|

|

|

1,750

|

|

|

|

|

|

1,750

|

|

|

|

|

|

1,750

|

|

|

Accretion on preferred stock

|

|

|

|

|

753

|

|

|

|

|

|

734

|

|

|

|

|

|

716

|

|

|

|

|

|

716

|

|

|

|

|

|

716

|

|

|

Net Income (loss) available to common stockholders

|

|

|

|

$

|

2,650

|

|

|

|

|

$

|

(13,299

|

)

|

|

|

|

$

|

(457

|

)

|

|

|

|

$

|

(1,239

|

)

|

|

|

|

$

|

(2,082

|

)

|

|

Diluted net income (loss) per share

|

|

|

|

$

|

0.03

|

|

|

|

|

$

|

(0.17

|

)

|

|

|

|

$

|

(0.01

|

)

|

|

|

|

$

|

(0.02

|

)

|

|

|

|

$

|

(0.03

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Western Alliance Bancorporation and Subsidiaries

|

|

Five Quarter Condensed Consolidated Balance Sheets

|

|

Unaudited

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

March 31,

|

|

|

|

Dec. 31,

|

|

|

|

Sept. 30,

|

|

|

|

June 30,

|

|

|

|

March 31,

|

|

|

|

|

|

2011

|

|

|

|

2010

|

|

|

|

2010

|

|

|

|

2010

|

|

|

|

2010

|

|

Assets:

|

|

|

|

(in millions)

|

|

Cash and due from banks

|

|

|

|

$

|

363.3

|

|

|

|

|

$

|

215.8

|

|

|

|

|

$

|

615.0

|

|

|

|

|

$

|

560.6

|

|

|

|

|

$

|

827.6

|

|

|

Federal funds sold

|

|

|

|

|

-

|

|

|

|

|

|

0.9

|

|

|

|

|

|

1.0

|

|

|

|

|

|

-

|

|

|

|

|

|

2.4

|

|

|

Cash and cash equivalents

|

|

|

|

|

363.3

|

|

|

|

|

|

616.0

|

|

|

|

|

|

616.0

|

|

|

|

|

|

560.6

|

|

|

|

|

|

830.0

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Securities and money market investments

|

|

|

|

|

1,319.6

|

|

|

|

|

|

1,273.1

|

|

|

|

|

|

929.7

|

|

|

|

|

|

848.6

|

|

|

|

|

|

781.1

|

|

|

Loans:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commercial

|

|

|

|

|

935.9

|

|

|

|

|

|

934.6

|

|

|

|

|

|

876.8

|

|

|

|

|

|

832.8

|

|

|

|

|

|

757.9

|

|

|

Commercial real estate - owner occupied

|

|

|

|

|

1,299.5

|

|

|

|

|

|

1,223.1

|

|

|

|

|

|

1,227.7

|

|

|

|

|

|

1,234.1

|

|

|

|

|

|

1,209.3

|

|

|

Construction and land development

|

|

|

|

|

391.7

|

|

|

|

|

|

451.5

|

|

|

|

|

|

488.3

|

|

|

|

|

|

532.4

|

|

|

|

|

|

556.9

|

|

|

Commercial real estate - non-owner occupied

|

|

|

|

|

1,086.9

|

|

|

|

|

|

1,038.5

|

|

|

|

|

|

981.4

|

|

|

|

|

|

926.0

|

|

|

|

|

|

902.9

|

|

|

Residential real estate

|

|

|

|

|

504.5

|

|

|

|

|

|

527.3

|

|

|

|

|

|

533.6

|

|

|

|

|

|

536.1

|

|

|

|

|

|

560.2

|

|

|

Consumer

|

|

|

|

|

65.7

|

|

|

|

|

|

71.5

|

|

|

|

|

|

71.4

|

|

|

|

|

|

74.6

|

|

|

|

|

|

77.6

|

|

|

Deferred fees, net

|

|

|

|

|

(6.2

|

)

|

|

|

|

|

(6.0

|

)

|

|

|

|

|

(5.7

|

)

|

|

|

|

|

(6.0

|

)

|

|

|

|

|

(5.7

|

)

|

|

|

|

|

|

|

4,278.0

|

|

|

|

|

|

4,240.5

|

|

|

|

|

|

4,173.5

|

|

|

|

|

|

4,130.0

|

|

|

|

|

|

4,059.1

|

|

|

Allowance for credit losses

|

|

|

|

|

(106.1

|

)

|

|

|

|

|

(110.7

|

)

|

|

|

|

|

(108.2

|

)

|

|

|

|

|

(110.0

|

)

|

|

|

|

|

(112.7

|

)

|

|

Loans, net

|

|

|

|

|

4,171.9

|

|

|

|

|

|

4,129.8

|

|

|

|

|

|

4,065.3

|

|

|

|

|

|

4,020.0

|

|

|

|

|

|

3,946.4

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Premises and equipment, net

|

|

|

|

|

112.0

|

|

|

|

|

|

114.4

|

|

|

|

|

|

116.5

|

|

|

|

|

|

118.7

|

|

|

|

|

|

121.2

|

|

|

Other repossessed assets

|

|

|

|

|

98.3

|

|

|

|

|

|

107.7

|

|

|

|

|

|

110.1

|

|

|

|

|

|

104.4

|

|

|

|

|

|

105.6

|

|

|

Bank owned life insurance

|

|

|

|

|

131.0

|

|

|

|

|

|

129.8

|

|

|

|

|

|

94.8

|

|

|

|

|

|

94.0

|

|

|

|

|

|

93.2

|

|

|

Goodwill and other intangibles

|

|

|

|

|

38.4

|

|

|

|

|

|

39.3

|

|

|

|

|

|

40.2

|

|

|

|

|

|

41.3

|

|

|

|

|

|

42.2

|

|

|

Other assets

|

|

|

|

|

170.3

|

|

|

|

|

|

183.1

|

|

|

|

|

|

206.5

|

|

|

|

|

|

171.9

|

|

|

|

|

|

176.5

|

|

|

Total assets

|

|

|

|

$

|

6,404.8

|

|

|

|

|

$

|

6,193.9

|

|

|

|

|

$

|

6,179.1

|

|

|

|

|

$

|

5,959.5

|

|

|

|

|

$

|

6,096.2

|

|

|

Liabilities and Stockholders' Equity:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Liabilities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deposits:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-interest bearing demand deposits

|

|

|

|

$

|

1,455.1

|

|

|

|

|

$

|

1,443.3

|

|

|

|

|

$

|

1,421.7

|

|

|

|

|

$

|

1,330.4

|

|

|

|

|

$

|

1,348.7

|

|

|

Interest bearing

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Demand

|

|

|

|

|

521.2

|

|

|

|

|

|

523.8

|

|

|

|

|

|

645.4

|

|

|

|

|

|

611.4

|

|

|

|

|

|

510.2

|

|

|

Savings and money market

|

|

|

|

|

2,100.6

|

|

|

|

|

|

1,926.1

|

|

|

|

|

|

1,892.2

|

|

|

|

|

|

1,845.9

|

|

|

|

|

|

1,798.5

|

|

|

Time certificates

|

|

|

|

|

1,420.6

|

|

|

|

|

|

1,445.2

|

|

|

|

|

|

1,369.2

|

|

|

|

|

|

1,442.5

|

|

|

|

|

|

1,532.7

|

|

|

Total deposits

|

|

|

|

|

5,497.5

|

|

|

|

|

|

5,338.4

|

|

|

|

|

|

5,328.5

|

|

|

|

|

|

5,230.2

|

|

|

|

|

|

5,190.1

|

|

|

Customer repurchase agreements

|

|

|

|

|

163.4

|

|

|

|

|

|

109.4

|

|

|

|

|

|

86.8

|

|

|

|

|

|

87.1

|

|

|

|

|

|

169.1

|

|

|

Total customer funds

|

|

|

|

|

5,660.9

|

|

|

|

|

|

5,447.8

|

|

|

|

|

|

5,415.3

|

|

|

|

|

|

5,317.3

|

|

|

|

|

|

5,359.2

|

|

|

Borrowings

|

|

|

|

|

73.0

|

|

|

|

|

|

73.0

|

|

|

|

|

|

72.9

|

|

|

|

|

|

-

|

|

|

|

|

|

20.0

|

|

|

Junior subordinated and subordinated debt

|

|

|

|

|

43.0

|

|

|

|

|

|

43.0

|

|

|

|

|

|

36.3

|

|

|

|

|

|

36.3

|

|

|

|

|

|

102.3

|

|

|

Accrued interest payable and other liabilities

|

|

|

|

|

26.3

|

|

|

|

|

|

27.9

|

|

|

|

|

|

34.8

|

|

|

|

|

|

30.0

|

|

|

|

|

|

39.0

|

|

|

Total liabilities

|

|

|

|

|

5,803.2

|

|

|

|

|

|

5,591.7

|

|

|

|

|

|

5,559.3

|

|

|

|

|

|

5,383.6

|

|

|

|

|

|

5,520.5

|

|

|

Stockholders' Equity