Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 20-F

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from to

Commission file number 1-31517

(Exact Name of Registrant as Specified in Its Charter)

China Telecom Corporation Limited

(Translation of Registrant’s Name into English)

People’s Republic of China

(Jurisdiction of Incorporation or Organization)

31 Jinrong Street, Xicheng District

Beijing, People’s Republic of China 100033

(Address of Principal Executive Offices)

Ms. Wong Yuk Har, Rebecca

China Telecom Corporation Limited

38/F, Everbright Centre

108 Gloucester Road

Wanchai, Hong Kong

Email: rebecca.wong@chinatelecom-h.com

Telephone: (+852) 2582 5819

Fax: (+852) 2157 0010

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange On Which Registered | |

| American depositary shares H shares, par value RMB1.00 per share |

New York Stock Exchange, Inc. New York Stock Exchange, Inc.* |

| * | Not for trading, but only in connection with the listing on the New York Stock Exchange, Inc. of American depositary shares, each representing 100 H shares. |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of December 31, 2017, 67,054,958,321 domestic shares and 13,877,410,000 H shares, par value RMB1.00 per share, were issued and outstanding. H shares are ordinary shares of the Company listed on The Stock Exchange of Hong Kong Limited.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ☒ Accelerated Filer ☐ Non-Accelerated Filer ☐ Emerging Growth Company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification After April 5, 2012. |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing.

U.S. GAAP ☐

International Financial Reporting Standards as issued by the International Accounting Standards Board ☒

Other ☐

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐

Table of Contents

CHINA TELECOM CORPORATION LIMITED

TABLE OF CONTENTS

| Page | ||||||

| - 2 - | ||||||

| Item 1. |

- 2 - | |||||

| Item 2. |

- 2 - | |||||

| Item 3. |

- 2 - | |||||

| Item 4. |

- 17 - | |||||

| Item 4A. |

- 43 - | |||||

| Item 5. |

- 43 - | |||||

| Item 6. |

- 59 - | |||||

| Item 7. |

- 69 - | |||||

| Item 8. |

- 77 - | |||||

| Item 9. |

- 77 - | |||||

| Item 10. |

- 78 - | |||||

| Item 11. |

- 88 - | |||||

| Item 12. |

- 93 - | |||||

| - 93 - | ||||||

| Item 13. |

- 93 - | |||||

| Item 14. |

Material Modifications to the Rights of Security Holders and Use of Proceeds |

- 94 - | ||||

| Item 15. |

- 94 - | |||||

| Item 16A. |

- 96 - | |||||

| Item 16B. |

- 96 - | |||||

| Item 16C. |

- 96 - | |||||

| Item 16D. |

- 96 - | |||||

| Item 16E. |

Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

- 96 - | ||||

| Item 16F. |

- 96 - | |||||

| Item 16G. |

- 97 - | |||||

| Item 16H. |

- 98 - | |||||

| Item 17. |

- 98 - | |||||

| Item 18. |

- 98 - | |||||

| Item 19. |

- 98 - | |||||

Table of Contents

FORWARD-LOOKING STATEMENTS

This annual report contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. These forward-looking statements are, by their nature, subject to significant risks and uncertainties, and include, without limitation, statements relating to:

| • | our business and operating strategies and our ability to successfully execute these strategies; |

| • | our network expansion and capital expenditure plans; |

| • | our operations and business prospects; |

| • | the expected benefit of any acquisitions or other strategic transactions; |

| • | our financial condition and results of operations; |

| • | the expected impact of new services on our business, financial condition and results of operations; |

| • | the future prospects of and our ability to integrate acquired businesses and assets; |

| • | the industry regulatory environment as well as the industry outlook generally; and |

| • | future developments in the telecommunications industry in the People’s Republic of China, or the PRC. |

The words “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “seek,” “will,” “would” and similar expressions, as they relate to us, are intended to identify a number of these forward-looking statements.

These forward-looking statements are subject to risks, uncertainties and assumptions, some of which are beyond our control. In addition, these forward-looking statements reflect our current views with respect to future events and are not a guarantee of future performance. We are under no obligation to update these forward-looking statements and do not intend to do so. Actual results may differ materially from the information contained in the forward-looking statements as a result of a number of factors, including, without limitation, the following:

| • | any changes in the regulations or policies of the Ministry of Industry and Information Technology (prior to March 2008, the Ministry of Information Industry, or the MII), or the MIIT, and other relevant government authorities relating to, among other matters: |

| • | the granting and approval of licenses; |

| • | tariff or network speed policies; |

| • | interconnection and settlement arrangements; |

| • | capital investment priorities; |

| • | the provision of telephone and other telecommunications services to rural areas in the PRC; |

| • | the convergence of television broadcast, telecommunications and Internet access networks, or three-network convergence; and |

| • | spectrum and numbering resources allocation; |

| • | the effects of competition on the demand for and price of our services; |

| • | any potential further restructuring or consolidation of the PRC telecommunications industry; |

| • | changes in the PRC telecommunications industry as a result of the issuance of the fourth generation mobile telecommunications, or 4G, licenses by the MIIT; |

| • | the development of new technologies and applications or services affecting the PRC telecommunications industry and our current and future business; |

| • | changes in political, economic, legal and social conditions in the PRC, including changes in the PRC government’s specific policies with respect to foreign investment in and entry by foreign companies into the PRC telecommunications industry, economic growth, inflation, foreign exchange and the availability of credit; |

- 1 -

Table of Contents

| • | results and effects of any investigation by the relevant PRC regulatory authorities; and |

| • | the development of our mobile business is dependent on the Tower Company. |

Please also see “D. Risk Factors” under Item 3.

CERTAIN DEFINITIONS AND CONVENTIONS

As used in this annual report, references to “us,” “we,” the “Company,” “our Company” and “China Telecom” are to China Telecom Corporation Limited and its consolidated subsidiaries except where we make clear that the term means China Telecom Corporation Limited or a particular subsidiary or business group only. References to matters relating to our H shares or American depositary shares, or ADSs, or matters of corporate governance are to the H shares, ADSs and corporate governance of China Telecom Corporation Limited. All references to “China Telecom Group” are to China Telecommunications Corporation, our controlling shareholder. Unless the context otherwise requires, these references include all of its subsidiaries, including us and our subsidiaries. Unless otherwise indicated, references to and statements regarding China and the PRC in this annual report do not apply to Hong Kong Special Administrative Region, Macau Special Administrative Region or Taiwan.

| Item 1. | Identity of Directors, Senior Management and Advisers. |

Not applicable.

| Item 2. | Offer Statistics and Expected Timetable. |

Not applicable.

| Item 3. | Key Information. |

| A. | Selected Financial Data |

The following table presents our selected financial data. The selected consolidated statements of financial position data as of December 31, 2016 and 2017, and the selected consolidated statements of comprehensive income (except for earnings per ADS) and consolidated cash flow data for the years ended December 31, 2015, 2016 and 2017, are derived from our audited consolidated financial statements included elsewhere in this annual report, and should be read in conjunction with those consolidated financial statements. The selected consolidated statements of financial position data as of December 31, 2013, 2014 and 2015 and the selected consolidated statements of comprehensive income (except for earnings per ADS) and consolidated cash flow data for the years ended December 31, 2013 and 2014 are derived from our consolidated financial statements which are not included in this annual report. Our consolidated financial statements are prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board.

The selected financial data reflect the acquisitions and divestment in 2013, the establishment of new subsidiaries in 2014, the tower assets disposal in 2015, the disposal of Chengdu E-store Technology Co., Ltd., or E-Store, the establishment of Tianyi Capital Holding Co., Ltd., or Tianyi Capital, and the acquisitions of the satellite communications business and Shaanxi Zhonghe Hengtai Insurance Agent Limited, or Zhonghe Hengtai, in 2017 described under “Item 4. Information on the Company—A. History and Development of the Company—Changes in Our Corporate Organization in 2013”, “—Changes in Our Corporate Organization in 2014”, “—Establishment of the Tower Company and the Disposal and Lease of the Telecommunications Towers”, “—Disposal of E-store and Establishment of Tianyi Capital”, “—Our Acquisition from China Telecom Group of the Satellite Communications Business” and “—Our Acquisition from China Telecom Group of Zhonghe Hengtai.”

On December 15, 2017, we and China Telecom Satellite Communication Co., Ltd., a wholly owned subsidiary of China Telecom Group, entered into an acquisition agreement, pursuant to which we agreed to purchase from China Telecom Satellite Communication Co., Ltd. the satellite communications business for a consideration of RMB70 million. We expect to settle the consideration in full in the second quarter of 2018. On December 20, 2017, we, through E-surfing Pay Co., Ltd., entered into an acquisition agreement with Shaanxi Communications Services Company Limited, or Shaanxi Comservice, which is ultimately controlled by China Telecom Group, to acquire 100% of equity interest in Zhonghe Hengtai from Shaanxi Comservice for a consideration of RMB17 million. Zhonghe Hengtai primarily engages in insurance agency business in the PRC. The consideration had been settled in full by March 23, 2018.

- 2 -

Table of Contents

Because we and the acquired satellite communications business and Zhonghe Hengtai were under the common control of China Telecom Group, our acquisitions of the satellite communications business and Zhonghe Hengtai were accounted for as a combination of entities under common control in a manner similar to a pooling-of interests. Accordingly, the assets and liabilities of the acquired satellite communications business and Zhonghe Hengtai have been accounted for at historical amounts and our consolidated financial statements for periods prior to the respective acquisitions have been restated to include the financial position and results of operations of the acquired satellite communications business and Zhonghe Hengtai on a combined basis. The considerations for the acquisition of the acquired satellite communications business and Zhonghe Hengtai were accounted for as an equity transaction in the consolidated statement of changes in equity.

| As of or for the year ended December 31, | ||||||||||||||||||||||||

| 2013 RMB | 2014 RMB | 2015 RMB | 2016 RMB | 2017 RMB | 2017 US$ | |||||||||||||||||||

| (restated)(1) | (restated)(1) | (restated)(1) | (restated)(1) | |||||||||||||||||||||

| (in millions, except share numbers and per share and per ADS data) | ||||||||||||||||||||||||

| Consolidated Statements of Comprehensive Income Data: |

||||||||||||||||||||||||

| Operating revenues |

321,817 | 324,755 | 331,517 | 352,534 | 366,229 | 56,288 | ||||||||||||||||||

| Operating expenses |

(294,349 | ) | (296,239 | ) | (305,070 | ) | (325,314 | ) | (339,009 | ) | (52,105 | ) | ||||||||||||

| Operating income |

27,468 | 28,516 | 26,447 | 27,220 | 27,220 | 4,184 | ||||||||||||||||||

| Earnings before income tax |

23,088 | 23,265 | 26,698 | 24,116 | 24,953 | 3,835 | ||||||||||||||||||

| Income tax |

(5,422 | ) | (5,498 | ) | (6,552 | ) | (5,993 | ) | (6,192 | ) | (952 | ) | ||||||||||||

| Profit attributable to equity holders of the Company |

17,545 | 17,688 | 20,058 | 18,018 | 18,617 | 2,861 | ||||||||||||||||||

| Basic earnings per share(2) |

0.22 | 0.22 | 0.25 | 0.22 | 0.23 | 0.04 | ||||||||||||||||||

| Basic earnings per ADS(2) |

21.68 | 21.86 | 24.78 | 22.26 | 23.00 | 3.54 | ||||||||||||||||||

| Cash dividends declared per share |

0.08 | 0.08 | 0.08 | 0.09 | 0.09 | 0.01 | ||||||||||||||||||

| As of or for the year ended December 31, | ||||||||||||||||||||||||

| 2013 RMB | 2014 RMB | 2015 RMB | 2016 RMB | 2017 RMB | 2017 US$ | |||||||||||||||||||

| (restated)(1) | (restated)(1) | (restated)(1) | (restated)(1) | |||||||||||||||||||||

| (in millions, except share numbers and per share and per ADS data) | ||||||||||||||||||||||||

| Consolidated Statements of Financial Position Data: |

||||||||||||||||||||||||

| Cash and cash equivalents |

16,070 | 20,436 | 31,869 | 24,617 | 19,410 | 2,983 | ||||||||||||||||||

| Accounts receivable, net |

20,111 | 21,756 | 21,190 | 21,465 | 22,096 | 3,396 | ||||||||||||||||||

| Total current assets |

52,933 | 59,782 | 78,267 | 74,134 | 71,550 | 10,997 | ||||||||||||||||||

| Property, plant and equipment, net |

374,354 | 372,898 | 374,004 | 389,671 | 406,257 | 62,441 | ||||||||||||||||||

| Total assets |

543,414 | 561,537 | 629,747 | 652,558 | 661,194 | 101,624 | ||||||||||||||||||

| Short-term debt |

27,687 | 43,976 | 51,636 | 40,780 | 54,558 | 8,385 | ||||||||||||||||||

| Current portion of long-term debt and payable |

20,072 | 82 | 84 | 62,276 | 1,146 | 176 | ||||||||||||||||||

| Accounts payable |

81,159 | 88,587 | 118,128 | 122,493 | 119,321 | 18,339 | ||||||||||||||||||

| Total current liabilities |

200,246 | 206,553 | 256,074 | 319,133 | 275,408 | 42,329 | ||||||||||||||||||

| Long-term debt and payable |

62,617 | 62,494 | 64,830 | 9,370 | 48,596 | 7,469 | ||||||||||||||||||

| Deferred revenues (including current portion) |

2,431 | 1,858 | 2,482 | 3,558 | 3,061 | 470 | ||||||||||||||||||

| Total liabilities |

264,723 | 271,394 | 324,957 | 336,210 | 334,497 | 51,411 | ||||||||||||||||||

| Equity attributable to equity holders of the Company |

277,768 | 289,218 | 303,823 | 315,377 | 325,867 | 50,085 | ||||||||||||||||||

| Consolidated Cash Flow Data: |

||||||||||||||||||||||||

| Net cash generated from operating activities |

88,354 | 96,412 | 108,755 | 101,135 | 96,502 | 14,832 | ||||||||||||||||||

| Net cash used in investing activities(3) |

(107,951 | ) | (81,715 | ) | (102,255 | ) | (99,043 | ) | (85,263 | ) | (13,105 | ) | ||||||||||||

| Capital expenditures(3) |

(70,924 | ) | (80,280 | ) | (101,903 | ) | (96,678 | ) | (87,334 | ) | (13,423 | ) | ||||||||||||

| Net cash generated from / (used in) financing activities |

5,637 | (10,327 | ) | 4,809 | (9,555 | ) | (16,147 | ) | (2,482 | ) | ||||||||||||||

| (1) | Certain comparative financial data prior to January 1, 2017 presented herein have been restated as a result of the acquisitions of the satellite communications business and Zhonghe Hengtai from China Telecom Group. See Note 1 to our audited consolidated financial statements included elsewhere in this annual report for further details. |

| (2) | The basic earnings per share have been calculated based on the respective net profit attributable to equity holders of the Company in 2013, 2014, 2015, 2016 and 2017 and the weighted average number of shares in issue during each of the relevant years of 80,932,368,321 shares. Basic earnings per ADS have been computed as if all of our issued and outstanding shares, including domestic shares and H shares, are represented by ADSs during each of the years presented. Each ADS represents 100 H shares. |

| (3) | Capital expenditures are part of and not an addition to net cash used in investing activities. |

- 3 -

Table of Contents

Pursuant to the shareholders’ approval at the annual general meeting held on May 23, 2017, a final dividend of RMB7,530 million (RMB0.093043 per share equivalent to HK$0.105 per share, pre-tax) for the year ended December 31, 2016 was declared, all of which has been fully paid. Pursuant to a resolution passed at the Directors’ meeting on March 28, 2018, a final dividend of approximately RMB7,518 million (RMB0.092888 per share equivalent to HK$0.115 per share, pre-tax) for the year ended December 31, 2017 was proposed for shareholders’ approval at the forthcoming annual general meeting.

Exchange Rate Information

Our business is primarily conducted in China and substantially all of our revenues are denominated in Renminbi. We present our historical consolidated financial statements in Renminbi. In addition, solely for the convenience of the reader, this annual report contains translations of certain Renminbi and Hong Kong dollar amounts into U.S. dollars at specific rates. For any date and period, the exchange rate refers to the exchange rate as set forth in the H.10 statistical release of the Federal Reserve Board. Unless otherwise indicated, conversions of Renminbi or Hong Kong dollars into U.S. dollars in this annual report are based on the exchange rate on December 29, 2017 (RMB6.5063 to US$1.00 and HK$7.8128 to US$1.00). We make no representation that any Renminbi or Hong Kong dollar amounts could have been, or could be, converted into U.S. dollars or vice versa, as the case may be, at any particular rate, the rates stated below, or at all. For a detailed explanation of the risk of currency rate fluctuations, please see “D. Risk Factors—Risks Relating to the People’s Republic of China— Fluctuation of the Renminbi could materially affect our financial condition, results of operations and cash flows.” under this Item. The PRC government imposes controls over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign exchange. Examples of such government regulations and restrictions are set forth in “Risk Factors—Risks Relating to the People’s Republic of China—Government control of currency conversion may adversely affect our financial condition.”

On April 20, 2018, the daily exchange rates reported by the Federal Reserve Board was RMB6.2945 to US$1.00 and HK$7.8448 to US$1.00. The following table sets forth additional information concerning exchange rates between Renminbi and U.S. dollars and between Hong Kong dollars and U.S. dollars for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we use in this annual report or will use in the preparation of our future periodic reports or any information to be provided to you.

| RMB per US$1.00 | HK$ per US$1.00 | |||||||||||||||||

| High | Low | High | Low | |||||||||||||||

| October 2017 |

6.6533 | 6.5712 | October 2017 | 7.8106 | 7.7996 | |||||||||||||

| November 2017 |

6.6385 | 6.5967 | November 2017 | 7.8118 | 7.7955 | |||||||||||||

| December 2017 |

6.6210 | 6.5063 | December 2017 | 7.8228 | 7.8050 | |||||||||||||

| January 2018 |

6.5263 | 6.2841 | January 2018 | 7.8230 | 7.8161 | |||||||||||||

| February 2018 |

6.3471 | 6.2649 | February 2018 | 7.8267 | 7.8183 | |||||||||||||

| March 2018 |

6.3565 | 6.2685 | March 2018 | 7.8486 | 7.8275 | |||||||||||||

| April 2018 (through April 20, 2018) |

6.3045 | 6.2655 | April 2018 (through April 20, 2018) | 7.8499 | 7.8448 | |||||||||||||

The following table sets forth the average exchange rates between Renminbi and U.S. dollars and between Hong Kong dollars and U.S. dollars for each of 2013, 2014, 2015, 2016 and 2017 calculated by averaging the exchange rates on the last day of each month during each of the relevant years.

Average Exchange Rate

| RMB per US$ 1.00 | HK$ per US$1.00 | |||||||

| 2013 | 6.1412 | 7.7565 | ||||||

| 2014 | 6.1704 | 7.7554 | ||||||

| 2015 | 6.2869 | 7.7519 | ||||||

| 2016 | 6.6549 | 7.7618 | ||||||

| 2017 | 6.7350 | 7.7950 | ||||||

| B. | Capitalization and Indebtedness |

Not applicable.

- 4 -

Table of Contents

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Risks Relating to Our Business

We face increasing competition, which may materially and adversely affect our business, financial condition and results of operations.

The telecommunications industry in the PRC is rapidly evolving.

After the industry restructuring in 2008, China Unicom (Hong Kong) Limited (formerly known as China Unicom Limited), or China Unicom, and our Company have full-service capabilities and compete with each other in both wireline and wireless telecommunications services. China Mobile Limited, or China Mobile, continues to be the leading provider of mobile telecommunications services in the PRC and competes with us in mobile telecommunications services and other telecommunications services.

In December 2013, each of China Mobile Communications Group Co., Ltd.(formerly known as China Mobile Communications Corporation), or China Mobile Group, China Telecom Group and China United Network Communications Group Company Limited, or Unicom Group, was granted the permit to provide 4G services based on LTE/Time Division Duplex standard, or TD-LTE, technologies nationwide. In February 2015, China Telecom Group and Unicom Group were granted the permit to provide 4G services based on Frequency Division Long Term Evolution standard, or LTE FDD, technologies nationwide. In April 2018, China Mobile Group was granted the permit to provide 4G services based on LTE FDD technologies pursuant to which China Mobile can develop mobile IoT and Industrial Internet services nationwide and LTE FDD services only in rural areas. We have been authorized by China Telecom Group to operate 4G business nationwide based on both TD-LTE technologies and LTE FDD technologies. We cannot assure you that: (i) our 4G services will deliver the quality and levels of services currently anticipated; (ii) we will be able to provide all planned 4G services or we will be able to provide such services on schedule; (iii) there will be sufficient demand for 4G services for us to deliver these services profitably; (iv) our competitors’ 4G, or newer technology based, services will not be more popular among potential subscribers; or (v) we will not encounter unexpected technological difficulties in providing 4G services. The failure of any of these possible developments to occur could impede our growth, which could have a material adverse effect on our business, financial condition and results of operations. We expect that the market competition will be further intensified as a result of our competitors obtaining permits and expanding their 4G services, which could materially and adversely affect our business and prospect.

Prior to December 2013, China Unicom, China Tietong Telecommunications Corporation, or China Railcom, which is a wholly-owned subsidiary of China Mobile Group, CITIC NETWORKS Co., Ltd., and our Company were the only operators licensed by the MIIT to provide fixed-line telecommunications services in China. In December 2013, China Mobile Group received permission from the MIIT to authorize China Mobile to operate fixed-line telecommunications businesses. In December 2015, China Mobile completed its acquisition from China Mobile Group of the fixed-line telecommunications businesses operated by China Railcom. In May 2016, China Radio and Television Network Co. Ltd. received license from the MIIT to operate fixed-line broadband business. The entry of China Mobile and China Radio and Television Network Co. Ltd. has intensified and may further intensify the competition in this sector, which could have a material adverse effect on our business.

We also face increasing competition from other competitors outside the telecommunications industry, in particular, from Internet services providers and mobile software and application developers, such as Over-the-Top messaging or voice services providers who offer contents and services on the Internet without their proprietary telecommunications network infrastructure. These competitors are competing with us in information and application or voice services. During the past few years, some of our traditional revenue contributors have experienced a slowdown in the growth rate or negative growth, primarily due to the alternative means of communication offered by these Over-the-Top messaging or voice services becoming increasingly popular among the consumers. Though the increasing popularity of these Over-the-Top messaging or voice services has generally contributed to the increase in our Internet data traffic and Internet services revenues during the past few years, we cannot assure you that our Internet data traffic and Internet services revenue will continue to increase in the future or such increase could fully offset the negative effect of these Over-the-Top services on our voice services or short message services, or SMS. In addition, we expect that competition from competitors outside the telecommunications industry will intensify and the strategic cooperation between these competitors and telecommunications operators may even reshape the competitive landscape of the telecommunications industry in which we operate. Though we strive to maintain our competitiveness through our comprehensive transformation and upgrades strategy, we may encounter difficulties and challenges in addressing changing consumer needs and responding to the evolving competitive landscape.

- 5 -

Table of Contents

In addition, the PRC government has taken various initiatives to encourage competition in the telecommunications industry, such as the three-network convergence policy and the policy encouraging private capital to enter the industry. For more details of the three-network convergence policy, please see “Item 4. Information on the Company – B. Business Overview – Regulatory and Related Matters – Three-Network Convergence Policy.” For a series of government measures to encourage private capital to invest in telecommunications services that could compete with our services, see “Item 4. Information on the Company – B. Business Overview – Competition.” In 2017, MIIT further opened up broadband access markets to private capital in nine provinces on a province-wide basis and an additional 50 pilot cities. As of December 31, 2017, 42 mobile virtual network operators had been approved by the MIIT to conduct resale business on a pilot basis, and there were a total of 62.21 million users of mobile virtual network. As a result, the competitive landscape in the PRC telecommunications industry may further diversify, causing more intensified competition.

Increasing competition from other existing telecommunications services providers, including China Mobile and China Unicom, as well as competition from new competitors, could materially and adversely affect our business and prospect by, among other factors, forcing us to lower our tariffs, reducing or reversing the growth of our customer base and reducing usage of our services. Any of these developments could materially and adversely affect our revenues and profitability. We cannot assure you that the increasingly competitive environment and any change in the competitive landscape of the telecommunications industry in the PRC would not have a material adverse effect on our business, financial condition or results of operations.

Our operations and further development of our mobile business is dependent on the Tower Company.

In July 2014, the Company, China United Network Communications Corporation Limited (“CUCL”) and China Mobile Communication Company Limited (“CMCL”) made the decision to jointly establish China Communications Facilities Services Corporation Limited (currently known as China Tower Corporation Limited, the “Tower Company”), and carried out the establishment of Tower Company and the transfer of certain tower assets. Upon completion of the transfer of tower assets by the Company to the Tower Company, the Company and the Tower Company entered into the Lease Agreement on July 8, 2016 that sets forth the pricing and related arrangements in relation to the lease of telecommunications towers and related assets (including both acquired towers and new towers). On February 1, 2018, the Company and the Tower Company entered into a supplemental agreement, effective from January 1, 2018, on the basis of the original Lease Agreement mainly to adjust the relevant pricing arrangement of tower products under the Lease Agreement. See “Item 4. Information on the Company—A. History and Development of the Company—Establishment of the Tower Company and the Disposal and Lease of the Telecommunications Towers”.

The Tower Company has been and will continue to be of significant importance to the operations and further development of our mobile business and our results of operations. Construction of new tower assets has been carried out by the Tower Company since the completion of the transfer of tower assets and, in principle, we expect the Tower Company will continue to carry out the construction of new tower assets in the future. Therefore, our mobile business has depended on and will continue to depend on the lease arrangement between us and the Tower Company. However, since we do not control the Tower Company, we cannot assure you that it will act in the best interests of us or the services of the Tower Company can sufficiently support our business needs and future plans.

The Lease Agreement, as may be further supplemented and amended from time to time, provides for pricing adjustment mechanism under which the fees may be further negotiated or agreed upon after considering effects of inflation, significant fluctuations in the real estate market or the steel price, many of which are beyond our control, and such pricing adjustment mechanism may result in a further adjustment of the fees charged to us by the Tower Company in the future. Furthermore, prior to the expiration of lease periods of individual towers, we have to negotiate with the Tower Company new leases of such tower, we cannot assure you that we will be able to enter into new leases at all or on favorable terms with the Tower Company. Due to our reliance on Tower Company for tower assets, if we fail to use the relevant tower assets at our desired locations and on terms and conditions that are favorable to us to maintain or expand our mobile network coverage, or if we cannot receive quality and stable services in a timely and economically viable manner from the Tower Company, the operations and further growth of our mobile business as well as our financial condition and results of operations may be materially and adversely affected.

Further, during 2016 and 2017, the SEC issued comment letters relating to the Company’s previously filed annual reports on Form 20-F for the fiscal years ended December 31, 2015 and 2016. The comment letters inquired mainly about the background, execution process, and accounting treatment in relation to the Company’s disposal and lease of telecommunications towers and related assets with the Tower Company. The Company responded to these comment letters and was notified by the SEC in its letter dated October 20, 2017 that it has completed its review of such previously filed annual reports of the Company. The SEC did not in its October 2017 letter require us to make any amendment to those previously filed annual reports. However, there is no assurance that the SEC will not issue comment letters on our disclosure relating to these and future transactions with the Tower Company.

- 6 -

Table of Contents

We will continue to be controlled by China Telecom Group, which could cause us to take actions that may conflict with the best interests of our other shareholders.

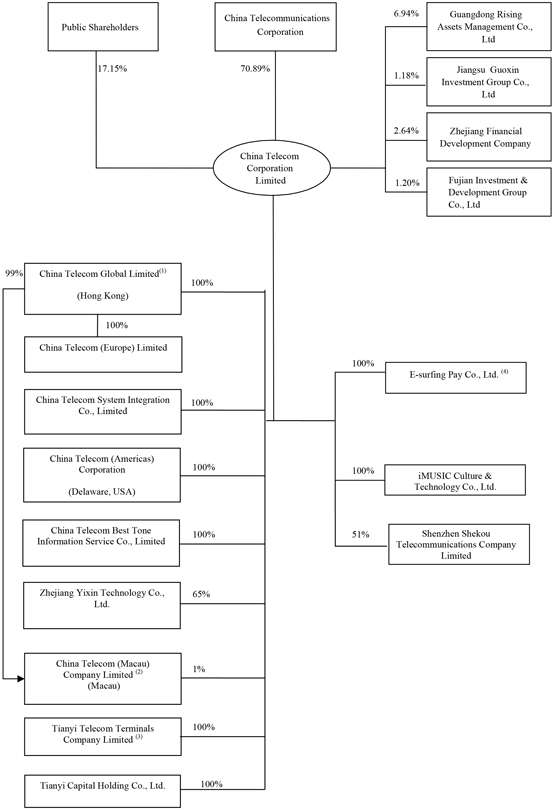

China Telecom Group, a state-owned enterprise owned by the State-owned Assets Supervision and Administration Commission of the State Council, or the SASAC, owned approximately 70.89% of our outstanding shares as of April 23, 2018. Accordingly, subject to our Articles of Association and applicable laws and regulations, China Telecom Group, as our controlling shareholder, will continue to be able to exercise significant influence over our management and policies by:

| • | controlling the election of our Directors and, in turn, indirectly controlling the selection of our senior management; |

| • | determining the timing and amount of our dividend payments; |

| • | approving our annual budgets; |

| • | deciding on increases or decreases in our share capital; |

| • | determining issuance of new securities; |

| • | approving mergers and acquisitions; and |

| • | amending our Articles of Association. |

The interests of China Telecom Group as our controlling shareholder could conflict with our interests or the interests of our other shareholders. As a result, China Telecom Group may take actions with respect to our business that may not be in our or our other shareholders’ best interests.

We depend on China Telecom Group and its other subsidiaries to provide certain services and facilities for which we currently have limited alternative sources of supply.

In addition to being our controlling shareholder, China Telecom Group, by itself and through its other subsidiaries, also provides us with services and facilities necessary for our business activities, including, but not limited to:

| • | use of international gateway facilities; |

| • | provision of services in areas outside our service regions necessary to enable us to provide end-to-end services to our customers; |

| • | use of certain inter-provincial optic fibers; and |

| • | lease of properties and assets. |

The interests of China Telecom Group and its other subsidiaries as providers of these services and facilities may conflict with our interests. We currently have limited alternative sources of supply for these services and facilities. Therefore, we have limited leverage in negotiating with China Telecom Group and its other subsidiaries over the terms for the provision of these services and facilities. Termination or adverse changes of the terms for the provisions of these services and facilities could materially and adversely affect our business, results of operations and financial condition. See “Item 4. Information on the Company—A. History and Development of the Company—Industry Restructuring and Our Acquisition of the CDMA Business in 2008” and “—Our Acquisition from China Telecom Group of the CDMA Network Assets and Associated Liabilities” and “Item 7. Major Shareholders and Related Party Transactions—B. Related Party Transactions” for a description of the services and facilities provided by China Telecom Group and its other subsidiaries.

- 7 -

Table of Contents

Since our services require interconnection with networks of other operators, disruption in interconnections with those networks could have a material adverse effect on our business and results of operations.

Under the relevant telecommunications regulations, telecommunications operators are required to interconnect with networks of other operators. China Telecom Group entered into interconnection settlement agreements with other telecommunications operators, including Unicom Group and China Mobile Group. We entered into an interconnection settlement agreement, as amended, with China Telecom Group, which allows our networks to interconnect with China Telecom Group’s networks as well as networks of the other telecommunications operators, with whom China Telecom Group had interconnection arrangements. The effective provision of our voice, Internet and other services requires interconnection between our networks and those of China Telecom Group, Unicom Group, China Mobile Group and other telecommunications operators. Any interruption in our interconnection with the networks of those operators or other international telecommunications carriers with which we interconnect due to technical or competitive reasons may affect our operations, service quality and customer satisfaction, and, in turn, our business and results of operations. In addition, any obstacles in existing interconnection arrangements and leased line agreements or any change in their terms, as a result of natural events, accidents, or for regulatory, technological, competitive or other reasons, could lead to temporary service disruptions and increased costs that may seriously jeopardize our operations and adversely affect our profitability and growth.

We may be unable to obtain sufficient financing to fund our capital requirements, which could limit our growth potential and prospects.

We believe that cash from operations, together with any necessary borrowings, will provide sufficient financial resources to meet our projected capital and other expenditure requirements. However, we may require additional funds to the extent we have underestimated our capital requirements or overestimated our future cash from operations. In addition, a significant feature of our business strategy is to transform our Company into a leading integrated intelligent information services provider, which may require additional capital resources. The cost of implementing new technologies, upgrading our networks, expanding capacity or acquisitions of businesses or assets may be significant. Furthermore, in order for us to effectively respond to technological changes and more intensive competition, we may need to make substantial investments in the future.

Financing may not be available to us on acceptable terms or at all. In addition, any future issuance of equity securities, including securities convertible or exchangeable into or that represent the right to receive equity securities, may require approval from the relevant government authorities. Our ability to obtain additional financing will depend on a number of factors, including:

| • | our future financial condition, results of operations and cash flows; |

| • | general market conditions for financing activities by telecommunications companies; and |

| • | economic, political and other conditions in the markets where we operate or plan to operate. |

We cannot assure you that we can obtain sufficient financing at commercially reasonable terms or at all. If adequate capital is not available on commercially reasonable terms, our growth potential and prospects could be materially and adversely affected. Furthermore, additional issuances of equity securities will result in dilution to our shareholders. Incurrence of debt would result in increased interest expense and could require us to agree to restrictive operating and financial covenants.

- 8 -

Table of Contents

If we are not able to respond successfully and cost-efficiently to technological or industry developments, our business may be materially and adversely affected.

The telecommunications market is characterized by rapid advancements in technology, evolving industry standards and changes in customer needs. We cannot assure you that we will be successful in responding to these developments. In addition, new services or technologies, such as mobile Internet, the three-network convergence, cloud computing and Internet of Things, may render our existing services or technologies less competitive. In the event we do take measures to respond to technological developments and changes in industry standards, the integration of new technology or industry standards or the upgrading of our networks may require substantial time, effort and capital investment. For example, we have begun to research and develop Software-Defined Networking (“SDN”) and Network Functions Virtualization (“NFV”) technologies so as to build a neat, swift, efficiently centralized and open network structure in order to provide visual network, free resource selection and self-service experience and to increase the flexibility of networks, the utilization rate of resources and the ability to provide services rapidly. However, the successful deployment and application of such cutting edge technologies depend on a number of factors, including the integration of legacy networks and cloud security related challenges. We cannot assure you that we will succeed in integrating these new technologies and industry standards or adapting our network and systems in a timely and cost-effective manner, or at all. Our inability to respond successfully and cost-efficiently to technological or industry developments may materially and adversely affect our business, results of operations and competitiveness.

Our ability to respond to technological developments in a cost-efficient manner may also be adversely affected by external factors, some of which are beyond our control. For example, the development in 5G technology is expected to have a major impact on our services. We have been engaged in standards formulation, network technology trial runs as well as planning of the application of 5G services towards commercialization. In addition, we have been taking the initiatives to explore and research on the feasibility study of collaborative development of 5G and 4G. We have devoted, and will continue to devote, substantial resources in the development of 5G technology. However, various details concerning 5G services are still uncertain, including the timing of the issuance of 5G permits, the frequency bands allocated to 5G services and relevant regulations. In addition, there is no assurance that we will be able to roll out 5G services in an economically viable manner to gain favorable market share based on reasonable commercial terms with business partners without undue delay. If we are unable to respond to these uncertainties, the expected benefits from our investment in development of 5G technology would not be fully realized or at all and such inability to respond to these uncertainties may materially and adversely affect our business in the future.

We face a number of risks relating to our Internet-related services.

We currently provide a range of Internet-related services, including dial-up and broadband Internet access, and Internet-related applications. We face a number of risks in providing these services.

Our network may be vulnerable to cyber attacks, including unauthorized access, computer viruses, denial of service and use of malicious software. Cyber attacks may cause equipment failures, loss of information, including confidential or otherwise protected information stored in our customers’ computer systems and mobile phone systems, failure or perceived failure to comply with applicable privacy, security, or data protection laws or regulations, as well as disruptions to our operations or our customers’ operations. We have devoted significant resources to network security, data security and other security measures to protect our systems and data, but we cannot assure you that the security measures we have implemented will not be circumvented or otherwise fail to protect the integrity of our network, including our mobile network. The economic costs to us to eliminate or alleviate cyber attacks could be significant and may be difficult to estimate or calculate because the loss may differ based on the identity and motive of the programmer or hacker, which are often difficult to identify. Eliminating computer viruses and other security problems may also require interruptions, delays or suspension of our services, reduce our customer satisfaction and cause us to incur costs. Cyber attacks may also subject us to litigations, liabilities for information loss, breach of confidentiality of private information, and/or reputational damage. While, to date, we have not been subject to cyber attacks which, individually or in the aggregate, have been material to our operations or financial condition, we cannot assure you that we will not experience them in the future. Due to the evolving nature of cybersecurity threats, the scope and impact of any future incident cannot be predicted. While we continually work to safeguard our systems and mitigate potential risks, there is no assurance that such actions will be sufficient to prevent cyber attacks or security breaches that manipulate or improperly use our systems or networks, compromise confidential or otherwise protected information, destroy or corrupt data, or otherwise disrupt our operations. The occurrence of such events could have a material adverse effect on our financial condition and results of operations.

- 9 -

Table of Contents

In addition, because we provide connections to the Internet and host websites for customers and develop Internet content and applications, we may be perceived as being associated with the content carried over our network or displayed on websites that we host. We cannot and do not screen all of this content and may face litigation claims due to a perceived association with this content. These types of claims have been brought against other providers of online services in the past. Regardless of the merits of the lawsuits, these types of claims can be costly to defend, divert management resources and attention, and may damage our reputation.

Revenues derived from our voice services may continue to decline, which may adversely affect our results of operations, financial condition and prospects.

Revenues from our voice services continued to decline during the past several years. Our revenues from voice services decreased by 10.8% from RMB78,661 million in 2015 to RMB70,185 million in 2016 and further decreased by 12.1% to RMB61,678 million in 2017. Percentage of revenues derived from our voice services out of our total operating revenues also continued to decrease, from 23.8% in 2015 to 19.9% in 2016 and 16.8% in 2017.

Of revenues from our voice services, revenues from wireline voice services decreased by 12.2% in 2016 compared to 2015 and further decreased by 14.3% in 2017 and the percentage of revenues derived from our wireline voice services out of our total operating revenues also continued to decrease, from 9.0% in 2015 to 7.4% in 2016 and 6.1% in 2017. This is primarily due to the fact that we continued to lose wireline telephone subscribers resulting from the increasing popularity of mobile voice services and other alternative means of communication, such as Over-the-Top messaging services. The number of our wireline telephone subscribers decreased by 5.6% at the end of 2016 compared to that at the end of 2015 and further decreased by 4.0% at the end of 2017.

Revenues from our mobile voice services decreased by 9.9% in 2016 compared to 2015 and further decreased by 10.8% in 2017 and the percentage of revenues derived from our mobile voice services out of our total operating revenues also continued to decrease, from 14.8% in 2015 to 12.5% in 2016 and 10.7% in 2017. In recent years, while the number of subscribers of our mobile services and mobile voice usage have continued to grow, due to the increasing popularity of alternative means of communication and the continued decrease in our tariffs for mobile voice services, revenues from our mobile voice services still continued to decrease.

We cannot assure you that we will be successful in slowing down the decline of our revenues generated from voice services. Migration from voice services to other alternative means of communication may further intensify and tariffs for voice services may further decrease in the future, which may affect the financial performance of our voice services and thus adversely affect our results of operations, financial condition and prospects as a whole.

We may suffer damage to our reputation due to communications fraud carried out on our network.

Communications fraud, in which a person defrauds another by means of telecommunications technologies including SMS, telephone, and Internet, poses a risk to us. If communications fraud is committed over our network, we may incur liability as a result of the inadequacy in our measures to prevent such fraud. On September 23, 2016, six departments including the Supreme People’s Court, the Supreme People’s Procuratorate, the Ministry of Public Security, the MIIT, the People’s Bank of China and the China Banking Regulatory Commission jointly released the Announcement on Preventing and Cracking Down on Telecom and Internet Frauds (关于防范和打击电信网络诈骗犯罪的通告) and the MIIT issued the Implementation Opinions on the Work of Further Prevention and Crack Down on Communications Fraud (关于进一步防范和打击通讯信息诈骗工作的实施意见) on November 7, 2016. We have implemented various measures to strengthen our management and control over sales and distribution channels, including full scale implementation of the compliance review of sales agencies. In addition, we have continued to implement and enhance real name registration and verification of customers by taking and storing the photo or video of customers when they conduct business with us either online or offline, strengthened management of new subscribers and maintained a whitelist of 400 telephone numbers, which are often registered by enterprise customers for marketing, technology support and aftersales services. We also have established an information security system to identify suspicious calls, text messages and software. We have formulated customer personal information collection and usage rules and procedures and have initiated awareness campaigns. However, there is no assurance that such measures will prevent communications fraud effectively. Communications fraud as a result of our failure in implementing the real name registration measure may result in claims being brought against us and may damage our reputation and could have an adverse effect on our business and results of operations.

- 10 -

Table of Contents

Risks Relating to the Telecommunications Industry in the PRC

The current and future government regulations and policies that extensively govern the telecommunications industry may limit our flexibility in responding to market conditions as well as competition, and may have a material adverse effect on our profitability and results of operation.

Our business is subject to extensive government regulation. The MIIT, which is the primary telecommunications industry regulator under the PRC’s State Council, regulates, among other things:

| • | industry policies and regulations; |

| • | licensing; |

| • | competition; |

| • | telecommunications resource allocation; |

| • | service standards; |

| • | technical standards; |

| • | tariff policies; |

| • | interconnection and settlement arrangements; |

| • | enforcement of industry regulations; |

| • | universal service obligations; |

| • | network information security; |

| • | network access license approval for telecom equipment and terminals; and |

| • | network construction plans. |

Other PRC governmental authorities also take part in regulating tariff policies, capital investment and foreign investment in the telecommunications industry. The regulatory framework within which we operate may constrain our ability to implement our business strategies and limit our flexibility to respond to market conditions.

For example, the PRC governmental authorities have promulgated various regulations, rules, guidance opinions and other directives regarding network speed upgrade and tariff reduction. On May 20, 2015, the office of the State Council promulgated the Guidance Opinions Regarding Expediting the Development of the High-Speed Broadband Network and Promoting the Speed Upgrade and Tariff Reduction, calling for the telecommunications operators to reduce the data tariffs. As a result, we carried out a series of measures, including launching the upgrade service in October 2015 which allowed handset data subscribers who subscribe to our monthly data packages to rollover the unused data remaining in the monthly packages to the next month. In addition, we ceased to charge handset subscribers domestic long distance and roaming fees on and from September 1, 2017. Meanwhile, we have significantly reduced the fees of international, Hong Kong, Macau and Taiwan long distance calls since May 1, 2017 and also have reduced the tariff of Internet dedicated line access for small and medium enterprises in 2017.

On March 5, 2018, the Government Work Report presented in the first plenary session of the 13th National People’s Congress of the PRC included certain policy requirements regarding network speed upgrade and tariff reduction, including requirements to: (i) increase efforts in implementing network speed upgrade and tariff reduction measures; (ii) achieve full coverage of high-speed broadband in cities and rural areas; (iii) expand the coverage of free Wifi Internet access in public areas; (iv) substantially reduce the tariffs of household broadband, corporate broadband and dedicated leased line; (v) cancel data roaming fee; and (vi) reduce mobile data tariff by at least 30% in 2018. We expect to roll out corresponding measures in due course to meet the policy requirements.

Though we strive to sustain our competitive advantages through various initiatives, our revenues and profitability may be negatively and materially affected by these requirements on network speed upgrade and tariff reduction. We may also have to devote substantial resources, incur significant expenses and make strategic adjustment of business and operation strategies in order to meet these requirements and maintain our competitive advantages. Failure to effectively respond to such evolving standards in a timely and cost-efficient manner may materially and adversely affect our business, financial condition and results of operations. In addition, we may face further policy requirements imposed by the PRC government on network speed upgrade and price adjustment in the future. Any such requirements could materially and adversely affect our revenues, profitability and results of operations.

- 11 -

Table of Contents

Moreover, on January 6, 2016, the MIIT issued the Guidance on the Wholesale Price Adjustments of Mobile Telecommunication Resale Business (关于移动通信转售业务批发价格调整的指导意见), pursuant to which the MIIT required that the wholesale price for resale of mobile telecommunications services should be lower than the per unit price (or package price) for similar services of the mobile networks operators. On December 1, 2016, the amended PRC Regulations on the Management of Radio Operation (中华人民共和国无线电管理条例) came into effect. The amended provision provided that a permit is required for using certain radio frequencies, which may be obtained through a bidding process or auctions. As such, we may incur additional costs in the future when we need to obtain the permit to use certain radio frequencies, such as the frequency bands for 5G, which will affect our cost structure. In addition, the PRC government has taken various initiatives and promulgated a number of regulations to encourage private capital to invest in the telecommunications industry, all of which have intensified, and are expected to continue to intensify, the competition in the telecommunications industry in the PRC. See “ – D. Risk Factors – Risks Relating to our Business – We face increasing competition, which may materially and adversely affect our business, financial condition and results of operations.”

The regulations and policies that govern the telecommunications industry in the PRC have experienced continuous changes in the past several years. Any significant future changes in regulations or policies that govern the telecommunications industry may have a material adverse effect on our business and operations.

The PRC government may require us, along with other providers in the PRC, to provide universal services with specified obligations, and we may not be compensated adequately for providing such services.

Under the Telecommunications Regulations promulgated by the State Council, telecommunications service providers in the PRC are required to fulfill universal service obligations in accordance with relevant regulations to be promulgated by the PRC government. The MIIT has the authority to delineate the scope of universal service obligations. The MIIT, together with other governmental authorities, is also responsible for formulating administrative rules relating to the establishment of a universal service fund and compensation schemes for universal services. The PRC government currently uses financial resources to compensate for the expenses incurred in the “Village to Village” and the “Broadband China” projects before the establishment of a universal service fund. See “Item 4. Information on the Company – B. Business Overview – Regulatory and Related Matters – Universal Services.” However, the compensation from the PRC government may not be sufficient to cover all of our expenses for providing the telecommunications services under the “Village to Village” and the “Broadband China” projects.

Under the Telecommunications Regulations, all PRC telecommunications operators shall provide universal services, and we expect to perform our duties thereunder accordingly. We may not be able to realize adequate return on investments for expanding networks to, and providing telecommunications services in, those economically less developed areas due to potentially higher capital expenditure requirements, lower usage by customers and lack of flexibility in setting our tariffs. If we are required to provide universal services with specified obligations without proper compensation by the government, our business and profitability may be adversely affected.

We have experienced incidents of executive misconduct in the past, which could adversely impact our reputation, our financial condition and results of operations as well as the trading price of our securities.

According to the information disclosed on the website of Communist Party of China Central Commission for Discipline Inspection, or the CCDI, and Ministry of Supervision of the PRC, or the MOS, on December 27, 2015, Mr. Chang Xiaobing, the former Chairman of Unicom Group and the then Chairman of China Telecom Group was under investigation by such authorities for suspected serious disciplinary violations. Mr. Chang was appointed as the chief executive officer of the Company on September 1, 2015 and the director and chairman of the Company on October 23, 2015. On December 30, 2015, Mr. Chang resigned from his positions as the executive director, chairman and chief executive officer of the Company with effect from the same date. Prior to his resignation, Mr. Chang had worked at the Company for four months. Mr. Chang was sentenced to six years of imprisonment over corruption charges in May 2017. According to the information disclosed on the website of the CCDI and the MOS on September 29, 2017, Mr. Zhen Caiji, the former Party Secretary and President of China Academy of Telecommunications Technology was expelled from the Communist Party of China and dismissed from public service for serious disciplinary violations and was under investigation of suspected criminal violations. Mr. Zhen was appointed as an executive vice president of the Company on November 4, 2016 and resigned from the position of executive vice president of the Company on May 22, 2017. Prior to his resignation, Mr. Zhen had worked at the Company for seven months. The investigation and trial conducted by the PRC authorities on Mr. Chang and Mr. Zhen may harm our reputation and adversely affect our financial condition and results of operations as well as the trading price of our securities.

- 12 -

Table of Contents

Risks Relating to the People’s Republic of China

Substantially all of our assets are located in the PRC and substantially all of our revenues are derived from our operations in the PRC. Accordingly, our results of operations and prospects are subject, to a significant extent, to the economic, political and legal developments in the PRC.

The PRC’s economic, political and social conditions, as well as government policies, could affect our business.

Substantially all of our business, assets and operations are located in the PRC. The PRC’s economy differs from the economies of most developed countries in many respects, including without limitation:

| • | government involvement; |

| • | level of development; |

| • | growth rate; |

| • | control of foreign exchange; and |

| • | allocation of resources. |

While the PRC’s economy has experienced significant growth in the past 30 years, growth has been uneven, both geographically and among various sectors of the economy. The PRC government has implemented various measures to encourage economic growth and guide the allocation of resources. Some of these measures benefit the overall economy of the PRC, but may also have a negative effect on us.

Economic developments in the PRC have a significant effect on our financial condition and results of operations. Although the PRC has been one of the world’s fastest growing economies in terms of GDP growth in the past 30 years, the economic growth of the PRC has experienced a marked slowdown in the past few years and may continue to slow down. For example, the GDP growth rate of the PRC decreased from 11.4% in 2007 to 6.9% in 2017. The PRC economy may continue to grow at a relatively slow pace in the next few years. There is no assurance that the GDP growth rate of the PRC will not further decline. A slowdown in economic growth could reduce business activities and demand for our services. The global economy may continue to deteriorate in the future and continue to have an adverse impact on the PRC economy. Any significant slowdown in the PRC economy could have a material adverse effect on the PRC telecommunications industry as well as our business and operations.

Government control of currency conversion may adversely affect our financial condition.

We receive substantially all of our revenues in Renminbi, which currently is not a freely convertible currency. A portion of these revenues must be converted into other currencies to meet our foreign currency obligations. These foreign currency-denominated obligations include:

| • | payment of interest and principal on foreign currency-denominated debt; |

| • | payment for equipment and materials purchased offshore; and |

| • | payment of dividends declared, if any, in respect of our H shares. |

Under the PRC’s existing foreign exchange regulations, we will be able to pay dividends in foreign currencies without prior approval from the State Administration of Foreign Exchange, or SAFE, by complying with certain procedural requirements. However, the PRC government may take measures at its discretion in the future to restrict access to foreign currencies for both current account transactions and capital account transactions. We may not be able to pay dividends in foreign currencies to our shareholders, including holders of our ADSs, if the PRC government restricts access to foreign currencies for current account transactions.

Foreign exchange transactions under our capital account, including but not limited to foreign currency-denominated borrowings from foreign banks, issuance of foreign currency-denominated debt securities, if any, and principal payments in respect of foreign currency-denominated obligations, continue to be subject to significant foreign exchange controls and require the approval of or registration with SAFE or certain banks designated by SAFE, as applicable. These limitations could affect our ability to obtain foreign exchange through debt or equity financing, or to obtain foreign exchange to meet our payment obligations under the debt securities, if any, or to obtain foreign exchange for capital expenditures.

- 13 -

Table of Contents

Fluctuation of the Renminbi could materially affect our financial condition, results of operations and cash flows.

We receive substantially all of our revenues, and our financial statements are presented, in Renminbi. The value of the Renminbi against U.S. dollar and other currencies fluctuates and is affected by, among other things, changes in the PRC’s and international political and economic conditions. Since 1994, the conversion of Renminbi into foreign currencies, including Hong Kong and U.S. dollars, has been based on rates set by the People’s Bank of China, which are set daily based on the previous business day’s inter-bank foreign exchange market rates and current exchange rates on the world financial markets. On July 21, 2005, the PRC government introduced a managed floating exchange rate system to allow the value of the Renminbi to fluctuate within a regulated band based on market supply and demand and by reference to a basket of currencies. In April 2012, the PRC government expanded the daily floating band of Renminbi trading prices against the U.S. dollar in the inter-bank spot foreign currency exchange market from 0.5% to 1.0%, which was further expanded to 2.0% in March 2014. Fluctuations in exchange rates may adversely affect the value, translated or converted into U.S. dollars or Hong Kong dollars, of our net assets, earnings and any declared dividends payable on our H shares in foreign currency terms. Our financial condition and results of operations may also be affected by changes in the value of certain currencies other than the Renminbi, in which our obligations are denominated. For further information on our foreign exchange risks and certain exchange rates, see “Item 3. Key Information—A. Selected Financial Data—Exchange Rate Information” and “Item 11. Quantitative and Qualitative Disclosures about Market Risk—Foreign Exchange Rate Risk.” We cannot assure you that any future movements in the exchange rate of the Renminbi against the U.S. dollar or other foreign currencies will not adversely affect our results of operations and financial condition.

The PRC legal system has inherent uncertainties that could limit the legal protections available to you.

We were incorporated under PRC laws and are governed by our Articles of Association. The PRC legal system is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. Since 1979, the PRC government has promulgated laws and regulations dealing with economic matters such as foreign investment, corporate organization and governance, commerce, taxation and trade. However, because these laws and regulations are relatively new, and because of the limited number of published cases and their non-binding nature, interpretation and enforcement of these laws and regulations involve uncertainties.

The ability of our shareholders to enforce their rights in respect of violations of corporate governance procedures may be limited. In this regard, our Articles of Association provide that most disputes between holders of H shares and our Company, directors, supervisors, officers or holders of domestic shares, arising out of our Articles of Association or the PRC Company Law and related regulations concerning the affairs of our Company, are to be resolved through arbitration by an arbitration tribunal in Hong Kong or the PRC, rather than by a court of law. Awards that are made by PRC arbitral authorities recognized under the Arbitration Ordinance of Hong Kong can be enforced in Hong Kong. Hong Kong arbitration awards are also enforceable in the PRC. However, to our knowledge, no action has been brought in the PRC by any holder of H shares to enforce an arbitral award, and we are uncertain as to the outcome of any action, if brought in the PRC to enforce an arbitral award made in favor of holders of H shares. See “Item 10. Additional Information—B. Memorandum and Articles of Association.”

To our knowledge, there has not been any published report of judicial enforcement in the PRC by holders of H shares of their rights under the Articles of Association of a PRC company or the PRC Company Law.

Unlike in the United States, the applicable PRC laws did not specifically allow shareholders to sue the directors, supervisors, senior management or other shareholders on behalf of the corporation to enforce a claim against such party or parties that the corporation has failed to enforce itself until January 1, 2006, when the amendments to the PRC Company Law passed on October 27, 2005 became effective. Although the amended PRC Company Law provides that shareholders, under certain circumstances, may sue the directors, supervisors and senior management on behalf of the company, no detailed implementation rules or judicial interpretations have been issued in this regard. In addition, our minority shareholders may not be able to enjoy protections to the same extent afforded to shareholders of companies incorporated under the state laws of the United States.

Although we will be subject to the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited (the “Listing Rules”) and the Hong Kong Codes on Takeovers and Mergers and Share Buy-backs (the “Codes”), the holders of H shares will not be able to bring actions on the basis of violations of the Listing Rules or the Codes, and must rely on the Hong Kong Stock Exchange and The Securities and Futures Commission of Hong Kong to enforce the Listing Rules or the Codes, as the case may be.

- 14 -

Table of Contents

You may experience difficulties in effecting service of legal process and enforcing judgments against us and our management.

We are a company incorporated under PRC laws, and substantially all of our assets and our subsidiaries are located in the PRC. In addition, most of our directors and officers reside within the PRC, and substantially all of the assets of our directors and officers are located within the PRC. As a result, it may not be possible to effect service of process within the United States or elsewhere outside the PRC upon most of our directors or officers, including with respect to matters arising under applicable laws and regulations. Moreover, our PRC counsel has advised us that the PRC does not have treaties providing for the reciprocal recognition and enforcement of judgments of courts with the United States, the United Kingdom or most other Western countries. Our Hong Kong counsel has also advised us that Hong Kong has no arrangement for the reciprocal enforcement of judgments with the United States.

As a result, recognition and enforcement in the PRC of judgments of a court in the United States and any of the other jurisdictions mentioned above in relation to any matter not subject to a binding arbitration provision may be difficult or impossible.

Holders of H shares may be subject to PRC taxation.

Under the Enterprise Income Tax Law of the PRC, or the EIT Law, and its implementing regulations, holders of our H shares or ADSs which are “non-resident enterprises” for the EIT Law’s purpose are subject to enterprise income tax at the rate of 10.0% with respect to dividends paid by us and income derived from sale of our H shares or ADSs, unless reduced under an applicable tax treaty. In addition, a resident enterprise, including a foreign enterprise whose “de facto management body” is located in the PRC, is not subject to any PRC income tax with respect to dividends paid to it by us. The capital gains realized by such resident enterprise are subject to the PRC enterprise income tax. Specifically, according to the Notice of the PRC State Administration of Taxation Concerning the Withholding Enterprise Income Tax on Dividend Distributed by PRC Resident Enterprises to Overseas Non-Resident Enterprise Holders of H shares issued in November 2008 and the Approval of the PRC State Administration of Taxation Concerning the Collection of Enterprise Income Tax on Dividend from B-shares Received by Non-Resident Enterprise issued in July 2009, when PRC resident enterprises distribute dividend to overseas non-resident enterprise holders of H shares for the year 2008 and the years thereafter, the 10.0% enterprise income tax will be withhold. The Company will withhold the 10.0% enterprise income tax when it pays dividend to holders of H shares or ADSs who are non-resident enterprises. See “Item 10. Additional Information—E. Taxation—People’s Republic of China.”

Furthermore, dividends paid by us to holders of our H shares or ADSs who are individuals outside the PRC are subject to a withholding tax of 20.0% unless reduced by an applicable tax treaty. For example, Hong Kong and Macau individual residents are subject to a withholding tax of 10.0% on dividends paid to them. In addition, gains realized by individuals upon the sale or other disposition of our H shares or ADSs are temporarily exempted from PRC capital gains tax. If the exemptions are withdrawn in the future, holders of our H shares or ADSs who are individuals may be required to pay PRC capital gains tax upon the sale or other disposition of our H shares. See “Item 10. Additional Information—E. Taxation— People’s Republic of China.”

Natural disasters and health hazards in the PRC may severely disrupt our business and operations and may have a material adverse effect on our financial condition and results of operations.