Exhibit 1.1

ANNUAL INFORMATION FORM

(Except as otherwise noted the

information herein is given

as at December 31, 2011)

March 22, 2012

TABLE OF CONTENTS

Page

|

1

|

|

|

CONVERSIONS

|

1

|

|

DEFINITIONS

|

1

|

|

GLOSSARY OF TECHNICAL TERMS

|

4

|

|

CURRENCY

|

7

|

|

FORWARD-LOOKING INFORMATION

|

8

|

|

SHARE CONSOLIDATION

|

10

|

|

SONDE RESOURCES CORP.

|

11

|

|

GENERAL DEVELOPMENT OF THE BUSINESS

|

12

|

|

DESCRIPTION OF THE BUSINESS

|

16

|

|

PRINCIPAL PROPERTIES

|

17

|

|

STATEMENT OF RESERVES DATA AND OTHER OIL AND GAS INFORMATION

|

18

|

|

CONTINGENT RESOURCES

|

27

|

|

RISK FACTORS

|

29

|

|

INDUSTRY CONDITIONS

|

38

|

|

DIVIDENDS

|

38

|

|

DESCRIPTION OF SHARE CAPITAL

|

40

|

|

MARKET FOR SECURITIES

|

41

|

|

PRIOR SALES

|

42

|

|

ESCROWED SECURITIES

|

42

|

|

DIRECTORS AND OFFICERS

|

43

|

|

AUDIT COMMITTEE

|

45

|

|

LEGAL AND REGULATORY PROCEEDINGS

|

46

|

|

INTERESTS OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS

|

47

|

|

TRANSFER AGENT AND REGISTRAR

|

47

|

|

MATERIAL CONTRACTS

|

47

|

|

INTERESTS OF EXPERTS

|

47

|

|

ADDITIONAL INFORMATION

|

48

|

|

APPENDIX "A" REPORT ON RESERVES DATA BY INDEPENDENT QUALIFIED RESERVES EVALUATOR OR AUDITOR

|

A1

|

|

APPENDIX "B" REPORT OF MANAGEMENT AND DIRECTORS ON OIL AND GAS DISCLOSURE

|

B1

|

|

APPENDIX "C" CHARTER OF THE AUDIT COMMITTEE OF SONDE RESOURCES CORP.

|

C1

|

- i -

ABBREVIATIONS

In this Annual Information Form, the following abbreviations have the meanings set forth below.

|

Oil, Natural Gas Liquids and Natural Gas

|

||

|

bbl

|

barrel

|

|

|

Mbbl

|

thousand barrels

|

|

|

MMbbl

|

million barrels

|

|

|

bbl/d

|

barrel or barrels per day

|

|

|

Mcf

|

thousand cubic feet

|

|

|

MMcf

|

million cubic feet

|

|

|

Mcf/d

|

thousand cubic feet per day

|

|

|

MMcf/d

|

million cubic feet per day

|

|

|

Bcf

|

billion cubic feet

|

|

|

MMBtu

|

million British Thermal Units

|

|

|

Other

|

||

|

AECO

|

a natural gas storage facility located at Suffield, Alberta

|

|

|

API

|

American Petroleum Institute

|

|

|

°API

|

an indication of the specific gravity of crude oil measured on the API gravity scale. Liquid petroleum with a specified gravity of 28 °API or higher is generally referred to as light crude oil

|

|

|

BOE

|

barrel of oil equivalent of natural gas and crude oil on the basis of 1 BOE for 6 Mcf of natural gas. BOEs may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 Mcf to 1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead

|

|

|

BOE/d

|

barrels of oil equivalent per day

|

|

|

m3

|

cubic metres

|

|

|

MBOE

|

1,000 barrels of oil equivalent

|

|

|

M$

|

thousands of dollars

|

|

|

WTI

|

West Texas Intermediate, the reference price paid in U.S. dollars at Cushing, Oklahoma for crude oil of standard grade

|

|

|

3D

|

three dimensional seismic

|

|

CONVERSIONS

The following table sets forth certain conversions between Standard Imperial Units and the International System of Units (or metric units).

|

To Convert From

|

To

|

Multiply By

|

||

|

Mcf

|

1,000 m3 of gas

|

0.028

|

||

|

1,000 m3 of gas

|

Mcf

|

35.493

|

||

|

bbl

|

m3 of oil

|

0.158

|

||

|

m3 of oil

|

bbl

|

6.290

|

||

|

feet

|

metres

|

0.305

|

||

|

metres

|

feet

|

3.281

|

||

|

miles

|

kilometres

|

1.609

|

||

|

kilometres

|

miles

|

0.621

|

||

|

acres

|

hectares

|

0.405

|

||

|

hectares

|

acres

|

2.471

|

||

|

GJ

|

MMBtu

|

0.950

|

DEFINITIONS

In this Annual Information Form, the following words and phrases have the meanings specified below, unless the context otherwise requires.

- 2 -

"ABCA" means the Business Corporations Act (Alberta), including the regulations promulgated thereunder, as amended from time to time.

"Best estimate" is considered to be the best estimate of the quantity that will actually be recovered. It is equally likely that the actual remaining quantities recovered will be greater or less than the best estimate. If probabilistic methods are used, there should be at least a 50 percent probability that the quantity actually recovered will equal or exceed the best estimate.

"BG" means BG International Limited, a wholly-owned subsidiary of BG Group PLC.

"BG Sale Agreement" means the Sale Agreement dated June 30, 2009 between the Company and BG in respect of the purchase of a 45% interest in Block 5(c) by BG.

"Block 5(c)" means the "Intrepid" Block 5(c), covering approximately 32,383 hectares (80,041 acres) located approximately 97 kilometres (60 miles) off the east coast of Trinidad in the Columbus Basin as described in and subject to the terms of the PSC.

"Board" means the board of directors of the Company.

"CCAA" means the Companies' Creditors Arrangement Act, including the regulations promulgated thereunder, as amended from time to time.

"CCAA Proceedings" means the proceedings commenced by the Company, Canadian Superior Trinidad and Tobago Limited (now Sonde Resources Trinidad and Tobago Limited) and Seeker under the CCAA pursuant to an order of the Court dated March 5, 2009.

"Challenger" means Challenger Energy Corp.

"Challenger CCAA Proceedings" means the proceedings commenced by Challenger and Challenger Energy Trinidad and Tobago Ltd. under the CCAA pursuant to an order of the Court dated February 27, 2009.

"Crown Lands" means leases granted by a Canadian Provincial authority.

"COGE Handbook" means the Canadian Oil and Gas Evaluation Handbook.

"Common Shares" means the common shares in the capital of the Company.

"Company" or "Sonde" means Sonde Resources Corp. and all of its subsidiaries, unless the context otherwise requires.

"Court" means the Court of Queen's Bench of Alberta.

"EPSA" means the Exploration and Production Sharing Agreement dated August 27, 2008 between the Company and Joint Oil.

"ETAP" means Entreprise Tunisienne d'Activities Petrolicres.

"Federal Plan" means the Framework as amended by the Update.

"Framework" means the 'Regulatory Framework for Air Emissions' paper released by the Government of Canada on April 26, 2007.

"GLJ" means GLJ Petroleum Consultants Ltd.

"GLJ Report" means the report dated February 23, 2012 prepared by GLJ evaluating the oil, NGL and natural gas reserves attributable to the properties of the Company effective December 31, 2011.

"High estimate" is considered to be an optimistic estimate of the quantity that will actually be recovered. It is unlikely that the actual remaining quantities recovered will exceed the high estimate. If probabilistic methods are

- 3 -

used, there should be at least a 10 percent probability that the quantity actually recovered will equal or exceed the high estimate.

"Joint Oil" means the Joint Exploration, Production, and Petroleum Services Company that is owned equally by the Tunisian government via ETAP and the Libyan government via Libya Oil Holdings.

"Joint Oil Block" means the area covering approximately 310,799 hectares (768,000 acres) located approximately 121 kilometres (75 miles) offshore the Mediterranean Gulf of Gabes as described in and subject to the terms of the EPSA.

"Joint Oil Block JOA" means the joint operating agreement dated July 5, 2010 between the Company and Sahara in respect of the Joint Oil Block.

"LNG Project" means the proposed development of a LNG regasification project in U.S. federal waters offshore New Jersey.

"Mariner Block" means the "Mariner" Block, covering approximately 11,246 hectares (27,790 acres) located approximately 9 kilometres (5.6 miles) northeast of Sable Island, offshore Nova Scotia as described in and subject to the terms of the Mariner Exploration License 2409.

"MG Block" means the "Mayaro/Guayaguayare" Block, covering approximately 23,522 hectares (58,080 acres) located approximately 6.4 kilometres (4 miles) off the east coast of Trinidad in the Columbus Basin as described in and subject to the terms of the Exploration and Production License.

"NI 51-101" means National Instrument 51-101, Standards of Disclosure for Oil and Gas Activities.

"NI 51-102" means National Instrument 51-102, Continuous Disclosure Obligations.

"Niko" means Niko Resources Ltd.

"Niko Sale Agreement" means the Sale Agreement dated December 21, 2010 between the Company and Niko in respect of the purchase of the Company’s interests in Block 5(c) and the assumption of certain liabilities in respect of the MG Block by Niko.

"NYSE Amex" means NYSE Amex LLC.

"OPEC" means the Organization of the Petroleum Exporting Countries.

"Options" means the options to acquire Common Shares issued under the stock option plan of the Company.

"Preferred Shares" means the preferred shares in the capital of the Company.

"PSC" means the Production Sharing Contract dated July 20, 2005 between the Company and the Government of the Republic of Trinidad and Tobago in respect of Block 5(c).

"Rights Plan" means the shareholder rights plan of the Company.

"Rights Plan Agreement" means the Shareholder Rights Plan Agreement dated June 3, 2010 between the Company and Valiant Trust Company.

"SEC" means the United States Securities and Exchange Commission.

"Seeker" means Seeker Petroleum Ltd.

"Series A Preferred Shares" means the Series A, 5% U.S. cumulative redeemable preferred shares in the capital of the Company.

"Series B Preferred Shares" means the Series B, 5% U.S. cumulative redeemable preferred shares in the capital of the Company.

"Shareholders" means the holders of Common Shares and "Shareholder" means any one of them.

- 4 -

"Swap Agreement" means the "Mariner" Block Swap Agreement dated August 27, 2008 between the Company and Joint Oil in respect of the Mariner Block.

"TSX" means the Toronto Stock Exchange.

“UN” means the United Nations.

"Update" means the 'Turning the Corner: Regulatory Framework for Industrial Greenhouse Gas Emissions' paper released by the Government of Canada on March 10, 2008.

"U.S." or "United States" means the United States of America, its territories and possessions, any state of the United States, and the District of Columbia.

"West Coast" means West Coast Opportunity Fund, LLC.

"Zarat Field" means a portion of the Joint Oil Block surrounding the Zarat North 1 well, combined with an adjacent license owned by a third party.

GLOSSARY OF TECHNICAL TERMS

In this Annual Information Form, the following technical terms and acronyms have the meanings specified below.

"CBM" means coal based methane.

"contingent resources" are those quantities of crude oil and natural gas estimated, as of a given date, to be potentially recoverable from known accumulations using established technology or technology under development, but which are not currently considered to be commercially recoverable due to one or more contingencies. The contingencies that prevent the classification of reserves are economic, legal and political. There is no certainty that it will be commercially viable to produce any portion of the contingent resources.

"crude oil" or "oil" as described in the COGE Handbook means a mixture consisting mainly of pentanes and heavier hydrocarbons that exists in the liquid phase in reservoirs and remains liquid at atmospheric pressure and temperature. Crude oil may contain small amounts of sulphur and other non-hydrocarbons but does not include liquids obtained from the processing of natural gas.

"development costs" means costs incurred to obtain access to reserves and to provide facilities for extracting, treating, gathering and storing the oil and gas from the reserves. More specifically, development costs, including applicable operating costs of support equipment and facilities and other costs of development activities, are costs incurred to:

|

(a)

|

gain access to and prepare well locations for drilling, including surveying well locations for the purpose of determining specific development drilling sites, clearing ground, draining, road building, and relocating public roads, gas lines and power lines, to the extent necessary in developing the reserves;

|

|

(b)

|

drill and equip development wells, development type stratigraphic test wells and service wells, including the costs of platforms and of well equipment such as casing, tubing, pumping equipment and the wellhead assembly;

|

|

(c)

|

acquire, construct and install production facilities such as flow lines, separators, treaters, heaters, manifolds, measuring devices and production storage tanks, natural gas cycling and processing plants, and central utility and waste disposal systems; and

|

|

(d)

|

provide improved recovery systems.

|

"developed non-producing reserves" are those reserves that either have not been on production, or have previously been on production, but are shut-in, and the date of resumption of production is unknown.

- 5 -

"developed producing reserves" are those reserves that are expected to be recovered from completion intervals open at the time of the estimate. These reserves may be currently producing or, if shut-in, they must have previously been on production, and the date of resumption of production must be known with reasonable certainty.

"development well" means a well drilled inside the established limits of an oil or gas reservoir, or in close proximity to the edge of the reservoir, to the depth of a stratigraphic horizon known to be productive.

"exploration costs" means costs incurred in identifying areas that may warrant examination and in examining specific areas that are considered to have prospects that may contain oil and gas reserves, including costs of drilling exploratory wells and exploratory type stratigraphic test wells. Exploration costs may be incurred both before acquiring the related property (sometimes referred to in part as "prospecting costs") and after acquiring the property. Exploration costs, which include applicable operating costs of support equipment and facilities and other costs of exploration activities, are:

|

(a)

|

costs of topographical, geochemical, geological and geophysical studies, rights of access to properties to conduct those studies, and salaries and other expenses of geologists, geophysical crews and others conducting those studies (collectively sometimes referred to as "geological and geophysical costs");

|

|

(b)

|

costs of carrying and retaining unproved properties, such as delay rentals, taxes (other than income and capital taxes) on properties, legal costs for title defence, and the maintenance of land and lease records;

|

|

(c)

|

dry hole contributions and bottom hole contributions;

|

|

(d)

|

costs of drilling and equipping exploratory wells; and

|

|

(e)

|

costs of drilling exploratory type stratigraphic test wells.

|

"exploratory well" means a well that is not a development well, a service well or a stratigraphic test well.

"field" means a defined geographical area consisting of one or more pools.

"future net revenue" means the estimated net amount to be received with respect to the development and production of reserves (including synthetic oil, coal bed methane and other non-conventional reserves) estimated using constant prices or forecast prices and costs.

"future prices and costs" means future prices and costs that are:

|

(a)

|

generally accepted as being a reasonable outlook of the future;

|

|

(b)

|

if, and only to the extent that, there are fixed or presently determinable future prices or costs to which the Company is legally bound by a contractual or other obligation to supply a physical product, including those for an extension period of a contract that is likely to be extended, those prices or costs rather than the prices and costs referred to in paragraph (a).

|

“GHG” means greenhouse gas.

"gross" means:

|

(a)

|

in relation to the Company's interest in production or reserves, its "company gross reserves", which are its working interest (operating or non-operating) share before deduction of royalties and without including any royalty interests of the Company;

|

|

(b)

|

in relation to wells, the total number of wells in which the Company has an interest; and

|

|

(c)

|

in relation to properties, the total area of properties in which the Company has an interest.

|

"LNG" means liquefied natural gas.

- 6 -

"natural gas" as described in the COGE Handbook, means a mixture of lighter hydrocarbons that exist either in the gaseous phase or in solution in crude oil in reservoirs but are gaseous at atmospheric conditions. Natural gas may contain sulphur or other non-hydrocarbon compounds.

"natural gas liquids" or "NGL" as described in the COGE Handbook, means those hydrocarbon components that can be recovered from natural gas as liquids including, but not limited to, ethane, propane, butanes, pentanes plus, condensate and small quantities of non-hydrocarbons.

"net" means:

|

(a)

|

in relation to the Company's interest in production or reserves its working interest (operating or non-operating) share after deduction of royalty obligations, plus its royalty interests in production or reserves;

|

|

(b)

|

in relation to the Company's interest in wells, the number of wells obtained by aggregating the Company's working interest in each of its gross wells; and

|

|

(c)

|

in relation to the Company's interest in a property, the total area in which the Company has an interest multiplied by the working interest owned by the Company.

|

"non-associated gas" means an accumulation of natural gas in a reservoir where there is no crude oil.

"operating costs" or "production costs" means costs incurred to operate and maintain wells and related equipment and facilities, including applicable operating costs of support equipment and facilities and other costs of operating and maintaining those wells and related equipment and facilities.

"possible reserves" are those additional reserves that are less certain to be recovered than probable reserves. It is unlikely that the actual remaining quantities recovered will exceed the sum of the estimated proved plus probable plus possible reserves.

"probable reserves" are those additional reserves that are less certain to be recovered than proved reserves. It is equally likely that the actual remaining quantities recovered will be greater or less than the sum of the estimated proved plus probable reserves.

"production" means the cumulative quantity of petroleum that has been recovered at a given date.

"property" includes:

|

(a)

|

fee ownership or a lease, concession, agreement, permit, license or other interest representing the right to extract oil or gas subject to such terms as may be imposed by the conveyance of that interest;

|

|

(b)

|

royalty interests, production payments payable in oil or gas, and other non-operating interests in properties operated by others; and

|

|

(c)

|

an agreement with a foreign government or authority under which the Company participates in the operation of properties or otherwise serves as "producer" of the underlying reserves (in contrast to being an independent purchaser, broker, dealer or importer).

|

but does not include supply agreements, or contracts that represent a right to purchase, rather than extract, oil or gas.

"proved property" means a property or part of a property to which reserves have been specifically attributed.

"proved reserves" are those reserves that can be estimated with a high degree of certainty to be recoverable. It is likely that the actual remaining quantities recovered will exceed the estimated proved reserves.

"reserves" are estimated remaining quantities of oil and natural gas and related substances anticipated to be recoverable from known accumulations, from a given date forward, based on: (a) analysis of drilling, geological, geophysical, and engineering data; (b) the use of established technology; and (c) specified economic conditions, which are generally accepted as being reasonable and shall be disclosed. Reserves are classified according to the degree of certainty associated with the estimates.

- 7 -

"reservoir" means a porous and permeable subsurface rock formation that contains a separate accumulation of petroleum that is confined by impermeable rock or water barriers and is characterized by a single pressure system.

"service well" means a well drilled or completed for the purpose of supporting production in an existing field. Wells in this class are drilled for the following specific purposes: gas injection (natural gas, propane, butane or flue gas), water injection, steam injection, air injection, salt-water disposal, water supply for injection, observation, or injection for combustion.

"undeveloped reserves" are those reserves expected to be recovered from known accumulations where a significant expenditure (e.g., when compared to the cost of drilling a well) is required to render them capable of production. They must fully meet the requirements of the reserves classification (proved, probable, possible) to which they are assigned. In multi-well pools, it may be appropriate to allocate total pool reserves between the developed and undeveloped categories or to sub-divide the developed reserves for the pool between developed producing and developed non-producing. This allocation should be based on the estimator's assessment as to the reserves that will be recovered from specific wells, facilities and completion intervals in the pool and their respective development and production status.

"unproved property" means a property or part of a property to which no reserves have been specifically attributed.

"well abandonment costs" means costs of abandoning a well (net of salvage value) and of disconnecting the well from the surface gathering system. They do not include costs of abandoning the gathering system or reclaiming the well site.

Certain other terms used herein but not defined herein are defined in NI 51-101 and, unless the context otherwise requires, shall have the same meanings herein as in NI 51-101.

CURRENCY

All dollar amounts set forth in this Annual Information Form are expressed in Canadian dollars, except where otherwise indicated. References to Canadian dollars or "$" are to the currency of Canada and references to U.S. dollars or "US$" are to the currency of the United States.

The following table sets forth: (i) the exchange rate in effect at the end of each of the periods indicated; (ii) the average of exchange rates in effect on the first business day of each month during such periods; and (iii) the high and low exchange rates during each such periods, in each case based on the Bank of Canada noon buying rate for one Canadian dollar as expressed in U.S. dollars.

|

Year ended December 31

|

|||

|

2011

|

2010

|

2009

|

|

|

Rate at end of period

|

US$0.9833

|

US$1.0054

|

US$0.9564

|

|

Average rate during period

|

US$1.0111

|

US$0.9674

|

US$0.8757

|

|

High

|

US$0.9480

|

US$0.9278

|

US$0.9748

|

|

Low

|

US$1.0607

|

US$1.0054

|

US$0.7698

|

- 8 -

FORWARD-LOOKING INFORMATION

Certain information included in this Annual Information Form and the documents incorporated by reference herein constitutes forward-looking information under applicable securities legislation. Such forward-looking information is provided for the purpose of providing information about management's current expectations and plans relating to the future. Readers are cautioned that reliance on such information may not be appropriate for other purposes, such as making investment decisions. Forward-looking information typically contains statements with words such as "anticipate", "believe", "expect", "plan", "intend", "estimate", "propose", "project" or similar words suggesting future outcomes or statements regarding an outlook. Forward-looking information in this Annual Information Form and the documents incorporated by reference herein include, but is not limited to, information with respect to:

|

·

|

volume and product mix of the Company's oil and gas production;

|

|

·

|

future oil and gas prices and interest rates in respect of the Company's commodity risk management programs;

|

|

·

|

future liquidity, creditworthiness and financial capacity;

|

|

·

|

volumes and estimated value of the Company's oil and gas reserves and volumes of the Company’s contingent resources;

|

|

·

|

planned exploration and development activities;

|

|

·

|

future results from operations and operating metrics;

|

|

·

|

the life of each of the Company's reserves;

|

|

·

|

future interest rates;

|

|

·

|

future costs, expenses and royalty rates;

|

|

·

|

future development, exploration and other expenditures;

|

|

·

|

the amount and timing of future asset retirement obligations;

|

|

·

|

the Company's tax pools; and

|

|

·

|

source of funding for future exploration development activities.

|

Furthermore, information relating to "reserves" and “resources” are deemed to be forward-looking information, as it involves the implied assessment, based on certain estimates and assumptions, that the reserves and resources described can be recovered and profitable in the future. The assumptions relating to the reserves of the Company are discussed under "Statement of Reserves Data and Other Oil and Gas Information".

Forward-looking information is based on a number of factors and assumptions which have been used to develop such information but which may prove to be incorrect. Although the Company believes that the expectations reflected in such forward-looking information are reasonable, undue reliance should not be placed on forward-looking information because the Company can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified in this Annual Information Form and the documents incorporated by reference herein, assumptions have been made regarding and are implicit in, among other things:

|

·

|

the ability of the Company to receive approval by Joint Oil and implement a plan of development for the Joint Oil Block;

|

|

·

|

entering into a utilization agreement for the Zarat Field;

|

|

·

|

the ability of the Company to obtain financing on acceptable terms and the outcome of financing alternatives in North Africa;

|

|

·

|

field production rates and decline rates;

|

- 9 -

|

·

|

the ability of the Company to secure adequate product transportation and natural gas processing facilities;

|

|

·

|

the impact of increasing competition in or near the Company's properties;

|

|

·

|

the timely receipt of any required regulatory approvals;

|

|

·

|

the ability of the Company to hire and retain qualified management, equipment and services in a timely and cost efficient manner to develop its business;

|

|

·

|

the Company's ability to operate the properties in a safe, efficient and effective manner;

|

|

·

|

the ability to replace and expand oil and natural gas reserves through acquisition, development of exploration;

|

|

·

|

the timing and costs of pipeline, storage and facility construction and expansion;

|

|

·

|

future oil and natural gas prices;

|

|

·

|

currency, exchange and interest rates;

|

|

·

|

the regulatory framework regarding royalties, taxes and environmental matters; and

|

|

·

|

the ability of the Company to successfully market its oil and natural gas products.

|

Readers are cautioned that the foregoing list is not exhaustive of all factors and assumptions which have been used.

By its nature, forward-looking information is subject to a number of risks and uncertainties, which could cause actual results or other expectations to differ materially from those anticipated, including those material risks set forth under "Risk Factors" in this Annual Information Form, "Risk Management" in the financial statements of the Company for the year ended December 31, 2011 and "Risk Management" and "Risk Assessment" in the management discussion and analysis of the Company for the year ended December 31, 2011. The Company is exposed to a number of operational risks inherent in exploiting, developing, producing and marketing crude oil and natural gas. These risks include but are not limited to:

|

·

|

the unsettled and volatile political and security situations in Libya and Tunisia;

|

|

·

|

the outcome of financing alternatives in North Africa;

|

|

·

|

sufficient liquidity for future operations;

|

|

·

|

cost of capital risk to carry out the Company's operations;

|

|

·

|

economic risk of finding and producing reserves at a reasonable cost;

|

|

·

|

reliance on reserve estimates for the year as well as on acquisitions;

|

|

·

|

financial risk of marketing reserves at an acceptable price given market conditions;

|

|

·

|

fluctuations in commodity prices, foreign exchange and interest rates;

|

|

·

|

operational matters related to non-operated properties;

|

|

·

|

delays in business operations, pipeline or facility restrictions, blowouts;

|

|

·

|

debt service and indebtedness may affect the market price of the Common Shares;

|

|

·

|

the continued availability of adequate debt and equity financing and cash flow to fund planned expenditures;

|

|

·

|

unforeseen title defects;

|

|

·

|

aboriginal land claims;

|

- 10 -

|

·

|

increased competition and the lack of availability of qualified personnel or management;

|

|

·

|

loss of key personnel;

|

|

·

|

ability to attract key personnel;

|

|

·

|

uncertainty of government policy changes;

|

|

·

|

the risk of carrying out operations with minimal environmental impact;

|

|

·

|

operational hazards and availability of insurance;

|

|

·

|

industry conditions including changes in laws and regulations including the adoption of new environmental laws and regulations and changes in how they are interpreted and enforced;

|

|

·

|

general economic, market and business conditions;

|

|

·

|

competitive action by other companies;

|

|

·

|

the ability of suppliers to meet commitments;

|

|

·

|

stock market volatility;

|

|

·

|

obtaining required approvals of regulatory authorities; and

|

|

·

|

creditworthiness of counterparties.

|

The forward-looking information contained in this Annual Information Form and the documents incorporated by reference herein are made as of the date of such documents and the Company undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, except as required by applicable securities laws. The forward-looking information contained in this Annual Information Form and the documents incorporated by reference herein are expressly qualified by this cautionary statement.

SHARE CONSOLIDATION

On June 3, 2010, the Company consolidated the Common Shares on a five-for-one basis. As such, unless otherwise specifically stated, information contained herein in respect of the Company's share capital which is: (i) as of a date that is prior to June 3, 2010, is presented on a pre-consolidation basis; and (ii) as of a date that is on or after June 3, 2010, is presented on a post-consolidation basis.

- 11 -

SONDE RESOURCES CORP.

General

The Company was incorporated pursuant to the provisions of the ABCA as "297272 Alberta Ltd." on March 21, 1983. Subsequently, the articles of the Company have been amended as follows:

|

·

|

on April 17, 1993 to change the name of the Company to "KapaIua Gold Mines Ltd." and to remove the private company restrictions;

|

|

·

|

on November 16, 1993 to change the name of the Company to "Prize-Energy Inc." and to consolidate the issued and outstanding Common Shares on a one-for-five basis;

|

|

·

|

on January 19, 1999 to permit the appointment of additional directors between annual meetings of Shareholders and to restate the articles in a consolidated form;

|

|

·

|

on August 24, 2000 to change the name of the Company to "Canadian Superior Energy Inc." and to consolidate the issued and outstanding Common Shares on a one-for-two basis;

|

|

·

|

on January 31, 2006 to add the Series A Preferred Shares to the authorized share capital of the Company;

|

|

·

|

on February 3, 2010 to add the Series B Preferred Shares to the authorized share capital of the Company; and

|

|

·

|

on June 3, 2010 to change the name of the Company to "Sonde Resources Corp." and to consolidate the issued and outstanding Common Shares on a one-for-five basis.

|

The Company is a reporting issuer, or the equivalent, in the provinces of British Columbia, Alberta, Saskatchewan, Ontario, Quebec, Manitoba, Nova Scotia and Newfoundland. The Common Shares are listed and posted for trading on the TSX and the NYSE Amex (the successor exchange to the American Stock Exchange) under the symbol "SOQ".

The head office of the Company is located at 3200, 500 – 4th Avenue S.W., Calgary, Alberta, T2P 2V6 and its registered office is located at 3700, 400 – 3rd Avenue S.W., Calgary, Alberta, T2P 4H2. In addition, the Company has offices located in Drumheller, Alberta, and Gammarth, Tunis, Tunisia. In 2011, the Company closed its offices in Jersey City, New Jersey and St. Clair, Port of Spain, Trinidad and Tobago.

- 12 -

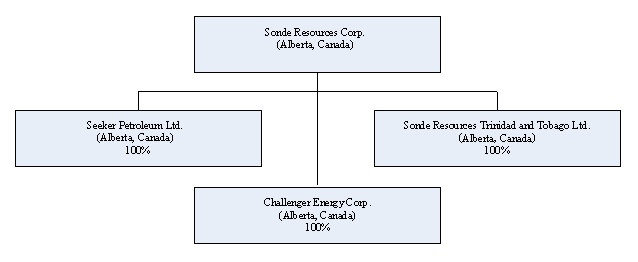

Inter-Corporate Relationships

The percentage of votes attaching to all voting securities of the material subsidiaries beneficially owned, or controlled or directed, directly or indirectly, by the Company as at December 31, 2011, as well as the jurisdiction where the subsidiary was incorporated, continued, formed or organized, as the case may be, is set forth below.

Effective January 1, 2012, the Company amalgamated Seeker Petroleum Ltd., Sonde Resources Trinidad and Tobago Ltd. and Challenger Energy Corp. into Sonde Resources Corp., transferring all assets and obligations of the wholly-owned subsidiaries to the parent company. As a result, the Company no longer has any material subsidiaries.

Reorganizations

In September 2009 the Company completed its financial restructuring and emerged from protection under the CCAA. The Court issued its final approval order for the implementation of the plan of arrangement pursuant to the CCAA Proceedings and the Challenger CCAA Proceedings on September 15, 2009. The plan of arrangement resulted in the acquisition by the Company of Challenger by plan of arrangement pursuant to section 192 of the Canada Business Corporations Act and the sale of a 45% interest in Block 5(c). The Company retained a 25% interest in Block 5(c) following the plan of arrangement, as well as oil and gas assets in Westeren Canada, the East Coast (Mariner Block) and North Africa (Joint Oil Block) and a 100% intereset in its LNG project in the United States. The Company issued approximately 27.4 million shares in connection with its acquisition of Challenger.

Aside from the CCAA Proceedings, the Challenger CCAA Proceedings and the amalgamation of Seeker, Sonde Resources Trinidad and Tobago Ltd. and Challenger into the Company, there have been no reorganizations of the Company or its subsidiaries within the three most recently completed financial years.

GENERAL DEVELOPMENT OF THE BUSINESS

General

The Company is engaged in the exploration for, and acquisition, development and production of, petroleum and natural gas with operations in Western Canada and North Africa. See "Statement of Reserves Data and Other Oil and Gas Information." The Company also reviews new drilling opportunities and potential acquisitions, both domestic and international, to supplement its exploration and development activities.

Three Year History

The following is a description of the general development of the business of the Company over the last three financial years. For a description of the business of the Company, see "Description of the Business".

- 13 -

2009

From February 2009 through September 2009, the Company and Challenger were involved in CCAA Proceedings and the Challenger CCA Proceedings, respectively. The Company emerged from CCAA protection on September 15, 2009.

On February 10, 2009, the Company announced its proposal to monetize a 25% or larger interest in Block 5(c) and its related discoveries, subject to acceptable terms and conditions, and subject to all required approvals.

On February 17, 2009, the Company received a demand letter from Canadian Western Bank for repayment of all amounts outstanding under the Company's $45.0 million credit facility with Canadian Western Bank by February 23, 2009.

On February 23, 2009, the Company advised that it had reached an accommodation with Canadian Western Bank whereby the demand for repayment of all amounts outstanding under the Company's credit facility with Canadian Western Bank was extended to February 27, 2009 (further extended on March 2, 2009 to March 12, 2009). The credit facility had been permanently reduced the previous week from $45.0 million to $37.5 million with a payment of approximately $7.5 million made to Canadian Western Bank by the Company from the sale of certain Western Canadian properties.

On March 3, 2009, the Company announced the successful flow testing of the "Endeavour" well, the third well drilled by the Company offshore Trinidad on Block 5(c).

On April 24, 2009, Messrs. Noval and Coolen ceased to be the Executive Chairman of the Board and the President, Chief Executive Officer and Chief Operating Officer of Corporation, respectively. Jake Harp was appointed Interim Chairman of the Board.

On April 30, 2009, Leif Snethun was appointed as the Chief Operating Officer of the Company.

On June 30, 2009, the Company entered into the BG Sale Agreement with respect of the purchase of its 45% interest in Block 5(c) by BG.

On September 9, 2009, the annual and special meeting of the Shareholders was held at which time the Shareholders approved the an arrangement involving the Company, Challenger and the shareholders of Challenger that provided for the acquisition of Challenger by the Company. In addition, at the meeting Shareholders elected Messrs. Brittain, Chronister, Funk, Roach, Turnbull and Watkins as directors.

On September 14, 2009, Marvin Chronister was appointed as the Chairman of the Board.

On September 15, 2009, the Company paid all amounts outstanding including accrued interest owed on its $37.5 million credit facility with Canadian Western Bank and obtained a new $25.0 million demand revolving credit facility with National Bank of Canada.

On September 15, 2009, pursuant to the CCAA Proceedings, the Company acquired Challenger, by way of a plan of arrangement, for consideration of approximately $77.8 million, including assumed net debt of approximately $54.4 million. Approximately 27,728,346 Common Shares were issued in exchange for all of the issued and outstanding common shares of Challenger. The Company also assumed 9,925,000 outstanding share purchase warrants of Challenger which were exercisable at a proportionally adjusted exercise price for Common Shares based on the same exchange ratio by which the Common Shares were issued for common shares of Challenger under the arrangement. All Challenger Share purchase warrants assumed by the Company have expired or were exercised.

On October 28, 2009, National Bank of Canada increased the Company's demand revolving credit facility from $25.0 million to $40.0 million. The credit facility is subject to its next scheduled review in April 2012.

On December 21, 2009, the Company announced that due to the current industry environment and market conditions, the Company allowed the Mayflower Exploration License 2406 and the Marauder Exploration License 2415, both offshore Nova Scotia, to lapse in favour of focusing on Trinidad and Tobago, Western Canada and North Africa. The Company extended the Mariner Exploration License 2409 until December 31, 2010.

- 14 -

2010

On January 18, 2010, James H.T. Riddell was appointed as a member of the Board.

On January 19, 2010, the Company completed a private placement of 114,424,238 Common Shares at a price of $0.52 per Common Share for gross proceeds of approximately $59.5 million.

On February 3, 2010, the Company converted the entire issued and outstanding Series A Preferred Shares in the aggregate principal amount of US$15,000,000 owned by West Coast for an equal number of Series B Preferred Shares and 2,500,000 Common Share purchase warrants. Each Common Share purchase warrant entitles West Coast to purchase a Common Share until December 31, 2011 at a price of US$0.65 per Common Share. For a description of the Series A Preferred Shares and the Series B Preferred Shares, see "Description of Share Capital - Series A Preferred Shares" and "Description of Share Capital - Series B Preferred Shares". For more information with respect to the conversion of the Series A Preferred Shares, see the Material Change Report of the Company dated February 4, 2010, a copy of which is available on SEDAR at www.sedar.com and is incorporated by reference herein.

On July 5, 2010, the Company and Sahara finalized the Joint Oil Block JOA. In addition, the two parties entered into a clarification agreement which, among other matters, gave Sahara until September 15, 2010 to pay its share of costs, plus interest, incurred after April 1, 2010. Sahara's failure to pay its share of costs, plus interest, when due would constitute a default under the terms of the Joint Oil Block JOA.

On September 16, 2010, the Company, as operator under the Joint Oil Block JOA, issued a Notice of Default to Sahara due to Sahara's failure to pay when due its share of joint account expenses associated with the Joint Oil Block. Under the terms of the Joint Oil Block JOA, a formal default period began five business days after issuance of that notice and Sahara had until October 15, 2010, to pay all outstanding joint account expenses associated with its 50% working interest in the Joint Oil Block.

On September 24, 2010, Robb Thompson resigned as the Chief Financial Officer of the Company.

On October 20, 2010, the Company announced that Sahara had failed to cure its default under the Joint Oil Block JOA and that the Company was therefore exercising its option to require that Sahara completely withdraw from the Joint Oil Block, thereby forfeiting its 50% working interest to the Company. In response, Sahara filed for creditor protection under the Bankruptcy and Insolvency Act (Canada), with the intention of making a proposal to its creditors (including the Company).

On October 21, 2010 Messrs. Schanck, Dirks and Barkwell were appointed the President and Chief Executive Officer, Chief Operating Officer, and Interim Chief Financial Officer of the Company, respectively.

On November 21, 2010, the Company announced that the Court had ruled in the Company's favour, dismissing the creditor protection previously afforded Sahara and lifting the stay protecting Sahara. As a result, Sahara was notified that Sonde was exercising its option to require that Sahara completely withdraw from the Joint Oil Block, thereby forfeiting its 50% working interest to the Company.

On December 15, 2010, Jack W. Schanck was appointed as a member of the Board.

On December 21, 2010, the Company entered into the Niko Sale Agreement with respect to the purchase of its interests in Block 5(c) by Niko for an aggregate purchase price of US$87.5 million, to be satisfied at closing by the payment of US$75.5 million in cash and the assumption of the Company's US$12.0 million liability under the performance guarantee provided for in the MG Block. A US$20 million debenture was provided by the Company to support the deposit made by Niko in the event that the Niko Sale is not completed. BG waived it’s right of first refusal with respect to the Niko Sale. The transaction closed on June 23, 2011, and the Company received an additional US$1.5 million in purchase price adjustments. The Company ceased all operations in Trinidad and Tobago and completely exited the country effective September 30, 2011. For additional details refer to the Material Change Report of the Company dated December 29, 2010, a copy of which is available on SEDAR at www.sedar.com and is incorporated by reference herein.

In December 2010, the Mariner Exploration License 2409, its remaining asset in Eastern Canada, expired. As a result, Joint Oil had the right to put back and sell the overriding royalty to the Company for US$12.5 million. This

- 15 -

right, which is referred to as the Mariner Swap Agreement, was exercised by Joint Oil in August 2011. The Company made a payment of US$12.5 million on January 15, 2012. Prior to the payment, the Company confirmed that the EPSA remains in full force and effect.

2011

On January 11, 2011, the Company announced the successful drilling and production testing of its 100% working interest in the Zarat North -1 well on the Joint Oil Block. The well has been temporarily abandoned while the Company evaluates the recoverable reserve scenarios, development options and cost estimates for the field's development.

On February 24, 2011, the Company announced that it had sold its subsidiary, Liberty Natural Gas LLC, which owned a 100% working interest in the LNG Project to an entity related to West Face Capital Inc. for US$1.0 million and an entitlement to receive a deferred cash consideration of US$12.5 million payable upon Liberty Natural Gas LLC's first successful gas delivery. The sale had an effective date of February 22, 2011.

On April 5, 2011, W. Gordon Lancaster was appointed as a member of the Board and Chairman of the Audit Committee.

On May 25, 2011, Kurt A. Nelson was appointed as Chief Financial Officer.

On June 8, 2011, the Company declared Force Majeure on the Joint Oil Block because of UN sanctions adopted by the UN Security Council and Canada that prevented the Company from fulfilling its obligations under the EPSA.

On June 23, 2011, the Company completed the sale of its interests in Block 5(c) and the assumption of certain liabilities in respect of the MG Block through the Niko Sale Agreement for gross proceeds of US$75.5 million plus purchase price adjustments of US1.5 million.

On September 23, 2011, the Company completed the acquisition of a block of producing and non-producing assets in Drumheller from a third party, which includes the bulk of producing interests in the Mannville “I” oil pool not previously owned by the Company for an aggregate purchase price of $6.3 million.

On October 5, 2011, the Company lifted the Force Majeure Declaration on the Joint Oil Block as a result a result of the Government of Canada and the United Nations repealing their unilateral sanctions against Libya on September 22, 2011.

On November 23, 2011, the Company appointed Toufic Nassif as President of Sonde North Africa.

On December 30, 2011, the Company redeemed all 150,000 outstanding Series “B” Preferred Shares for an aggregate amount of US$15,186,987.

On January 1, 2012, the Company amalgamated Seeker Petroleum Ltd., Challenger Energy Corp. and Sonde Resources Trinidad and Tobago Ltd. into Sonde Resources Corp.

On January 15, 2012, the Company received a one year extension on the first phase of the exploration period on the Joint Oil Block until December 23, 2013. In addition, Sonde paid to Joint Oil US$12.5 million pursuant to the Mariner Swap Agreement.

On February 8, 2012, the Company completed the sale of 26,240 gross undeveloped acres (24,383 net acres) in its Kaybob Duvernay play in Alberta for aggregate proceeds of $75 million. The sale resulted in a net gain of approximately $73 million.

Significant Acquisitions

The Company did not complete any significant acquisitions during the year ended December 31, 2011 for which disclosure was required under Part 8 of NI 51-102.

- 16 -

DESCRIPTION OF THE BUSINESS

General

The Company is engaged in the exploration for, and acquisition, development and production of, petroleum and natural gas with operations in Western Canada and North Africa. See "Statement of Reserves Data and Other Oil and Gas Information." The Company also reviews new drilling opportunities and potential acquisitions, both domestic and international, to supplement its exploration and development activities.

Competitive Conditions

The oil and natural gas industry is intensely competitive in all its phases. The Company competes with numerous other participants in the search for, and the acquisition of, oil and natural gas properties and in the marketing of oil and natural gas. The Company's competitors include resource companies which have greater financial resources, staff and facilities than those of the Company. Competitive factors in the distribution and marketing of oil and natural gas include price and methods and reliability of delivery. The Company believes that its competitive position is equivalent to that of other oil and gas issuers of similar size and at a similar stage of development. See "Risk Factors - Competition".

Cycles

The development of oil and gas reserves is dependent on access to areas where exploration and production is to be conducted. Seasonal weather variations, including freeze-up and break-up, affect access in certain circumstances.

Environmental Protection

The oil and gas industry is subject to environmental regulations pursuant to applicable legislation. Such legislation provides for restrictions and prohibitions on release or emission of various substances produced in association with certain oil and gas industry operations, and requires that well and facility sites be abandoned and reclaimed to the satisfaction of environmental authorities. As at December 31, 2011, the Company had recorded an obligation on its statement of financial position of $26.3 million for the costs of decommissioning its oil and gas assets. The Company maintains an insurance program consistent with industry practice to protect against losses due to accidental destruction of assets, well blowouts, pollution and other operating accidents or disruptions. The Company also has operational and emergency response procedures and safety and environmental programs in place to reduce potential loss exposure. No assurance can be given that the application of environmental laws to the business and operations of the Company will not result in a curtailment of production or a material increase in the costs of production, development or exploration activities or otherwise adversely affect the Company's financial condition, results of operations or prospects. See "Risk Factors – Environmental Risks" and "Industry Conditions".

Employees

The Company has a total of 34 full-time employees and consultants in the Calgary office, with nine employees in its Drumheller, Alberta office, two consultants in its Tunis office and one consultant in Houston.

Foreign Operations

In addition to its Canadian operations, the Company is engaged in the exploration for oil and natural gas in offshore North Africa. International oil and gas operations are subject to inherent risks and uncertainties which are beyond the control of the Company, particularly those associated with exploring for, and developing, economic quantities of hydrocarbons, volatile commodity prices, political risks, foreign exchange rates, issues relating to global supply and demand, government regulations, and environmental matters. The Company's international exploration ventures may entail certain political and technical business risks. The Company's strategy is to mitigate such risks by aligning itself with partners and engaging personnel and consultants that have international experience. See "Risk Factors - Foreign Political and Security Issues", "Risk Factors - Foreign Operations", "Risk Factors - Foreign Legal Systems" and "Risk Factors - Foreign Currency Rates".

- 17 -

Social or Environmental Policies

The health and safety of employees, contractors and the public, as well as the protection of the environment, is of utmost importance to the Company. To this end, the Company has instituted health and safety policies and programs and endeavors to conduct its operations in a manner that will minimize both adverse effects and consequences of emergency situations by:

|

·

|

complying with government regulations and standards, particularly relating to the environment, health and safety;

|

|

·

|

conducting operations consistent with industry codes, practices and guidelines;

|

|

·

|

ensuring prompt, effective response and repair to emergency situations and environmental incidents;

|

|

·

|

providing training to employees and contractors to ensure compliance with corporate safety and environmental rules and procedures; and

|

|

·

|

communicating openly with members of the public regarding its activities.

|

The Company believes that all employees have a vital role in achieving excellence in environmental, health and safety performance. This is best achieved through careful planning and the support and active participation of everyone involved.

PRINCIPAL PROPERTIES

A summary description of the Company's major producing and exploration properties is set out below. References to gross volumes refer to total production. References to net volumes refer to the Company's working interest share before the deduction of royalties payable to others.

Western Canada

The Company derives all of its production and cash flow from operations in Western Canada. The Company’s Western Canadian oil and gas assets are primarily high working interest properties that are geographically concentrated in southern and west-central Alberta, the most significant being the Company’s Southern Alberta cash generating unit (“CGU”) (or Greater Drumheller, Alberta area), which accounts for approximately 80% of the Company’s production. The balance of production largely comes from the Kaybob/Windfall and Boundary Lake/Eaglesham areas in west-central Alberta, with minor production in north-eastern British Columbia.

At December 31, 2011, the Company held 416,796 gross / 297,623 net acres in Western Canada the majority of which is operated by the Company. At March 23, 2012, the Company held 380,362 gross / 268,120 net acres in Western Canada as adjusted for the February 8, 2012, 26,420 gross / 24,383 net sale of interests in the Kaybob Duvernay play in Alberta and subsequent purchases.

Drumheller

Drumheller contains a wide variety of low-moderate risk operated development opportunities for oil, Cretaceous tight gas sands, and Cretaceous CBM, vertically-stacked on a concentrated, high working interest land position. Of particular importance are operated positions in six oil pools, the largest of which are the Mannville “I” pool (lower Cretaceous Ellerslie sandstone) and the Michichi Detrital pool (lower Cretaceous Detrital sandstone). The Company’s plan was to drill three horizontal wells (03-04-29-19, 03-05-29-19 and 14-14-029-19) to test the crest of the structure, a pressure depleted area and the fringe of the pool. The results were not as expected but Sonde continues to evaluate new lift technology to enhance the total liquids production. At the same time, the Company acquired the remaining working interest in the Mannville “I” pool as well as other assets in the Drumheller area. This will allow a water flood of the Mannville “I” pool to potentially increase oil recovery. The Company subsequently drilled two additional wells in the Drumheller area (16-20-029-14 and 02-19-31-19), both horizontal wells. Two wells (3-17-31-17, horizontal and 13-16-03-17 vertical) were drilled at Michichi (Drumheller)

- 18 -

and two minor wells drilled by a partner at (13-33-34-20 and 09-33-34-20. Production in the fourth quarter averaged 2,911 boepd.

In addition, the Company owns numerous locations in the form of both producing and suspended vertical wells that hold potential for re-development of existing zones and development of new, principally shallower non-producing zones. The Company plans to continue its work-over and re-development program targeting the Cretaceous Ellerslie, Glauconitic and Viking formations in these locations during 2012.

Kaybob/Windfall

With success in recent lease sales Sonde added acreage in the Ante Creek North area, Sonde owns 38,920 gross (38,920 net) high potential acres in the rapidly expanding Duvernay play. The Company is actively working to permit its inaugural drilling program and anticipates drilling in late 2012. In addition to the Duvernay, Sonde has 38,453 gross (38,453-net) acres of Montney rights at Waskahigan and Ante Creek North, near recently announced high-rate horizontal wells drilled by competitors. Sonde has been engaged in joint venture discussions with several industry and financial partners to provide financial leverage and risk-mitigation in the early phases of these plays.

International

Offshore North Africa (Tunisia and Libya)

The Company acquired the Exploration and Production Sharing Agreement for the 768,000 acre Joint Oil Block, offshore Tunisia and Libya, on August 27, 2008. The exploration work commitment for the first phase (four years) of the seven year exploration period includes three exploration wells, 500 square kilometres (311 square miles) of 3D seismic and one appraisal well. The Company holds a 100% working interest in the concession.

The appraisal well obligation was satisfied by drilling the Zarat North-1, which was temporarily abandoned on January 11, 2011 while the Company evaluates the recoverable reserve scenarios, development options and cost estimates for the field’s development. The well was the third drilled on the large Zarat anticlinal feature, following two wells drilled by Marathon in 1992 and 1994, respectively. It encountered 240 net feet of gas/condensate and oil pay in the Eocene El Gueria limestone, with oil/water and gas/oil contacts at the same structural elevation found in the Marathon wells. Tested in three separate intervals, the Zarat North-1 flowed at sustained rates averaging eight MMcf/d of natural gas plus 750 bbl/d of condensate. The Company is currently evaluating the commercial development potential of the Zarat Field, as well as negotiating a unitization agreement with the owners of an adjacent concession. On December 21, 2011, the Company commenced the shooting of 512 square kilometres of 3D seismic around two potential exploration well locations in accordance with the requirements of the EPSA and completed the shoot in January 2012. On January 12, 2012, the Company received notice from Joint Oil extending the first phase of the exploration period one year, until December 23, 2013, subject to securing the services of a drilling rig and agreeing to a plan of development. On January 30, 2012, the Company announced that it began an initiative to identify and evaluate alternatives to finance the Company’s remaining North Africa obligations.

STATEMENT OF RESERVES DATA AND OTHER OIL AND GAS INFORMATION

GLJ prepared the GLJ Report in accordance with NI 51-101. The GLJ Report evaluated, as at December 31, 2011, the oil, NGL and natural gas reserves attributable to the properties of the Company. All of the Company's reserves are located in the Canadian provinces of Alberta and British Columbia. No reserves have been attributed to the Joint Oil Block in North Africa.

The tables below are summaries of the oil, NGL and natural gas reserves of the Company and the net present value of future net revenue attributable to such reserves as summarized in the GLJ Report based on forecast price and cost assumptions. The tables summarize the data contained in the GLJ Report and as a result may contain slightly different numbers than such report due to rounding. Also due to rounding, certain columns may not add exactly.

The net present value of future net revenue attributable to the Company's reserves is stated without provision for interest costs and general and administrative costs, but after providing for estimated royalties, production costs, development costs, other income, future capital expenditures and well abandonment costs for only those wells assigned reserves by GLJ. It should not be assumed that the undiscounted or discounted net present value of future

- 19 -

net revenue attributable to the Company's reserves estimated by GLJ represent the fair market value of those reserves. Other assumptions and qualifications relating to costs, prices for future production and other matters are summarized herein. The recovery and reserve estimates of the Company's oil, NGL and natural gas reserves provided herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Actual reserves may be greater than or less than the estimates provided herein.

The values shown for income taxes and future net revenue after income taxes were calculated on a stand-alone basis in the GLJ Report. The values shown may not be representative of future income tax obligations, applicable tax horizon or after tax valuation.

The GLJ Report is based on certain factual data supplied by the Company and GLJ's opinions of reasonable practice in the industry. The extent and character of ownership and all factual data pertaining to the Company's petroleum properties and contracts (except for certain information residing in the public domain) were supplied by the Company to GLJ and accepted without any further investigation. GLJ accepted this data as presented and neither title searches nor field inspections were conducted.

Summary of Oil and Gas Reserves

|

Gross Reserves

|

Net Reserves

|

|||||

|

Light and Medium Crude Oil

|

NGLs

|

Natural Gas

|

Light and Medium Crude Oil

|

NGLs

|

Natural Gas

|

|

|

Reserve Category

|

Mbbl

|

Mbbl

|

MMcf

|

Mbbl

|

Mbbl

|

MMcf

|

|

Proved

|

||||||

|

Developed Producing

|

1,059

|

368

|

22,457

|

945

|

247

|

20,192

|

|

Developed Non-Producing

|

25

|

48

|

3,012

|

21

|

33

|

2,674

|

|

Undeveloped

|

0

|

0

|

2,823

|

0

|

0

|

2,615

|

|

Total Proved

|

1,085

|

416

|

28,292

|

966

|

280

|

25,482

|

|

Probable

|

899

|

190

|

13,266

|

747

|

127

|

11,720

|

|

Total Proved Plus Probable

|

1,984

|

606

|

41,518

|

1,713

|

407

|

37,202

|

Summary of Net Present Value of Future Net Revenue

|

Before Future Income Tax Expenses and Discounted at (%/year)

|

|||||

|

0%

|

5%

|

10%

|

15%

|

20%

|

|

|

Reserve Category

|

(M$)

|

(M$)

|

(M$)

|

(M$)

|

(M$)

|

|

Proved

|

|||||

|

Developed Producing

|

107,035

|

84,779

|

70,564

|

60,749

|

53,576

|

|

Developed Non-Producing

|

8,789

|

6,362

|

5,017

|

4,141

|

3,511

|

|

Undeveloped

|

4,403

|

2,767

|

1,738

|

1,074

|

637

|

|

Total Proved

|

120,227

|

93,908

|

77,318

|

65,964

|

57,724

|

|

Probable

|

83,222

|

52,499

|

36,287

|

26,706

|

20,554

|

|

Total Proved Plus Probable

|

203,448

|

146,407

|

113,605

|

92,670

|

78,278

|

- 20 -

|

After Future Income Tax Expenses and Discounted at (%/year)

|

|||||

|

0%

|

5%

|

10%

|

15%

|

20%

|

|

|

Reserve Category

|

(M$)

|

(M$)

|

(M$)

|

(M$)

|

(M$)

|

|

Proved

|

|||||

|

Developed Producing

|

107,035

|

84,779

|

70,564

|

60,749

|

53,576

|

|

Developed Non-Producing

|

8,789

|

6,362

|

5,017

|

4,141

|

3,511

|

|

Undeveloped

|

4,403

|

2,767

|

1,738

|

1,074

|

637

|

|

Total Proved

|

120,227

|

93,908

|

77,318

|

65,964

|

57,724

|

|

Probable

|

83,222

|

52,499

|

36,287

|

26,706

|

20,554

|

|

Total Proved Plus Probable

|

203,448

|

146,407

|

113,605

|

92,670

|

78,278

|

Total Future Net Revenue (Undiscounted)

|

Revenue

|

Royalties

|

Operating Costs

|

Development Costs

|

Abandonment and Reclamation Costs

|

Future Net Revenue Before Future Income Tax Expenses

|

Future Income Tax Expenses

|

Future Net Revenue After Future Income Taxes Expenses

|

|

|

Reserve Category

|

(M$)

|

(M$)

|

(M$)

|

(M$)

|

(M$)

|

(M$)

|

(M$)

|

(M$)

|

|

Total Proved

|

285,240

|

32,264

|

118,509

|

6,466

|

7,773

|

120,227

|

-

|

120,227

|

|

Total Proved Plus Probable

|

480,186

|

60,541

|

196,050

|

10,998

|

9,149

|

203,448

|

-

|

203,448

|

Future Net Revenue By Production Group

|

Future Net Revenue Before

Future Income Tax Expenses and Discounted at 10%/year(1)

|

Unit Value Before Future Income Tax Expenses and Discounted at 10%/year

|

|

|

Reserve Category and Product Group

|

(M$)

|

($/BOE)

|

|

Total Proved

|

||

|

Light and Medium Crude Oil

|

37,961

|

29.75

|

|

Associated Gas and Non-Associated Gas

|

37,725

|

10.12

|

|

Non-Conventional Oil and Gas Activities (CBM)

|

1,632

|

3.34

|

|

Total

|

77,318

|

14.08

|

|

Total Proved Plus Probable

|

||

|

Light and Medium Crude Oil

|

57,001

|

25.48

|

|

Associated Gas and Non-Associated Gas

|

52,673

|

10.18

|

|

Non-Conventional Oil and Gas Activities (CBM)

|

3,931

|

4.33

|

|

Total

|

113,605

|

13.65

|

Note:

|

(1)

|

Other revenue and costs not related to a specific production group have been allocated proportionately to production groups.

|

- 21 -

Summary of Pricing, Exchange Rate and Inflation Rate Assumptions

GLJ employed the following pricing, exchange rate and inflation rate assumptions as of December 31, 2011 in estimating the Company's reserves data, using forecast prices and costs.

|

Alberta NGLs

|

|||||||||||||||

|

Bank of Canada Average Noon Ex-change Rate

|

NYMEX WTI Near Month Futures Contract Crude Oil at Cushing Oklahoma

|

ICE BRENT Near Month Futures Contract Crude Oil FOB North Sea

|

Light Sweet Crude Oil (40 API, 0.3%S) at Edmonton

|

Bow River Crude Oil Stream Quality at Hardisty

|

Lloyd Blend Crude Oil Stream Quality at Hardisty

|

WCS Crude Oil Stream Quality at Hardisty

|

Heavy Crude Oil Proxy (12 API) at Hardisty

|

Light Crude Oil (35 API, 1.2 %S) at Cromer

|

Medium Crude Oil (29 API, 2.0%S) at Cromer

|

Spec Ethane

|

Edmonton Propane

|

Edmonton Butane

|

Edmonton Pentanes Plus

|

||

|

Year

|

Infla-

tion

%

|

$US/$

|

$US/bbl

|

$US/bbl

|

$/bbl

|

$/bbl

|

$/bbl

|

$/bbl

|

$/bbl

|

$/bbl

|

$/bbl

|

$/bbl

|

$/bbl

|

$/bbl

|

$/bbl

|

|

2012

|

2

|

0.98

|

97.00

|

105.00

|

97.96

|

83.27

|

81.31

|

81.61

|

72.37

|

93.06

|

90.12

|

11.46

|

58.78

|

76.41

|

107.76

|

|

2013

|

2

|

0.98

|

100.00

|

105.00

|

101.02

|

84.35

|

82.33

|

82.63

|

73.60

|

94.96

|

92.94

|

13.67

|

60.61

|

78.80

|

108.09

|

|

2014

|

2

|

0.98

|

100.00

|

102.00

|

101.02

|

84.35

|

82.33

|

82.63

|

74.51

|

93.95

|

91.93

|

15.26

|

60.61

|

78.80

|

105.06

|

|

2015

|

2

|

0.98

|

100.00

|

100.00

|

101.02

|

84.35

|

82.33

|

82.63

|

74.51

|

93.95

|

91.93

|

16.85

|

60.61

|

78.80

|

105.06

|

|

2016

|

2

|

0.98

|

100.00

|

100.00

|

101.02

|

84.35

|

82.33

|

82.63

|

74.51

|

93.95

|

91.93

|

18.43

|

60.61

|

78.80

|

105.06

|

|

2017

|

2

|

0.98

|

100.00

|

100.00

|

101.02

|

84.35

|

82.33

|

82.63

|

74.51

|

93.95

|

91.93

|

20.02

|

60.61

|

78.80

|

105.06

|

|

2018

|

2

|

0.98

|

101.35

|

101.35

|

102.40

|

85.50

|

83.45

|

83.75

|

74.54

|

95.23

|

93.18

|

20.84

|

61.44

|

79.87

|

106.49

|

|

2019

|

2

|

0.98

|

103.38

|

103.38

|

104.47

|

87.23

|

85.14

|

85.44

|

77.09

|

97.16

|

95.07

|

21.25

|

62.68

|

81.49

|

108.65

|

|

2020

|

2

|

0.98

|

105.45

|

105.45

|

106.58

|

89.00

|

86.86

|

87.16

|

78.67

|

99.12

|

96.99

|

21.70

|

63.95

|

83.13

|

110.84

|

|

2021

|

2

|

0.98

|

107.56

|

107.56

|

108.73

|

90.79

|

88.62

|

88.92

|

80.28

|

101.12

|

98.95

|

22.14

|

65.24

|

84.81

|

113.08

|

|

2022+

|

2

|

0.98

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

+2.0%/yr

|

|

Year

|

Alberta Plant Gate

|

Saskatchewan Plant Gate

|

British Columbia

|

|||||||||||

|

Henry Hub NYMEX

Near Month Contract

|