UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

[X] ANNUAL REPORT UNDER SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15 (d) OF THE EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission file number:

Boston Carriers, Inc.

(Name of Registrant as specified in its charter)

| Republic of the Marshall Islands | 65-1011679 |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

18 Nap. Zerva Str., 166 75 Glyfada, Greece

(Address of principal executive offices)

+30 2130165708

(Registrant’s telephone number)

Securities registered pursuant to Section 12(b) of the Exchange Act: None

Securities registered pursuant to Section 12(g) of the Exchange Act:

Common Stock

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the issuer is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes [ ] No [X]

Indicate by check mark if the issuer (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if there is no disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained in this form, and no disclosure will be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, a non-accelerated filer, or a smaller reporting company, See the definition of "large accelerated filer," "accelerated filer" and "smaller reporting company in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated file | [ ] | Smaller reporting company | [X] |

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The Company’s revenues for the year ended December 31, 2015 were $264,625.

At the end of the registrant’s most recently completed second quarter, the aggregate market value of the common shares held by non-affiliates of the registrant (based on a closing price of $0.0037 per share was $545,750).

The number of the registrant's common shares outstanding as of March 30, 2016 was 147,500,000.

| PART I | ||

| ITEM 1. | Business | 1 |

| ITEM 1A. | Risk Factors | 9 |

| ITEM 2. | Properties | 23 |

| ITEM 3. | Legal Proceedings | 24 |

| ITEM 4. | Mine Safety Disclosures | 24 |

| PART II | 25 | |

| ITEM 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchase of Equity Securities | 25 |

| ITEM 6. | Selected Financial Data | 26 |

| ITEM 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 26 |

| ITEM 7A | Quantitative and Qualitative Disclosures About Market Risk | 32 |

| ITEM 8. | Financial Statements | 32 |

| ITEM 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 32 |

| ITEM 9A. | Controls and Procedures | 32 |

| ITEM 9B. | Other Information | 33 |

| PART III | 34 | |

| ITEM 10. | Directors, Executive Officers, and Corporate Governance | 34 |

| ITEM 11. | Executive Compensation | 36 |

| ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 37 |

| ITEM 13. | Certain Relationships and Related Transactions, and Director Independence | 38 |

| ITEM 14. | Principal Accounting Fees and Services | 39 |

| PART IV | 40 | |

| ITEM 15. | Exhibits, Lists and Reports on Form 8-K | 40 |

PART I.

Item 1. DESCRIPTION OF THE BUSINESS

THE COMPANY – background and summary

Overview of the Company and its Prior Strategies

The Company was incorporated in Florida on July 31, 2001. On September 21, 2001, the Company was acquired by Pla.Net.Com, Inc., a Nevada public, non-reporting corporation (“Issuer”). Issuer was considered a shell at the time of the transaction and therefore the acquisition was treated as a reverse merger. Contemporaneously, Issuer changed its name to Inpatient Clinical Solutions, Inc. In April 2012, Issuer changed its name to Integrated Inpatient Solutions, Inc. which survives today as the Company.

From September 2001 until March 19, 2012 we operated as a provider of hospitalist services in the southeastern Florida market. Hospitalist medicine is organized around the admission and care of patients in facilities such as acute care hospitals. During that time we focused on providing, managing and coordinating the care of hospitalized patients. As of March 2012, we provided hospitalist services to a range of health plans, hospital clients, medical groups, and community physicians at 26 acute care hospitals. The Company also provided a non-material level of services at a number of nursing homes in the market.

Effective March 19, 2012 we sold substantially all of our assets relating to our hospitalist business (the “Assets”) pursuant to an Asset Purchase Agreement with InPatient Consultants of Florida, Inc. and Hospitalist Services of Florida, Inc. (collectively, the "Acquirors”). Following consummation of the transaction, and through March 2013 the Company continued providing health care services in the South Florida market. We have completed the process of winding down that aspect of our business.

After the sale of our Assets, Management came to believe that the best opportunity to maximize shareholder value was to explore options in other industries as well as continuing to explore opportunities in the health care industry. Having investigated potential opportunities in various industries, management launched an interior design business.

Our interior design business targeted cost conscious individuals. The business operated under the trade name Integrated Interior Design. We earned revenues from providing decorator services, which were billed on hourly and per diem rates. The business operated in South Florida and we intended to expand regionally and nationally. The business provided interior design, interior staging, accompanied shopping, paint color selection, architectural drawing and other services. Subsequent to the end of the fiscal year discussed in this report we have begun the process of winding down that aspect of our business.

Additionally, on August 26, 2014 we entered into a Share Exchange Agreement pursuant to which the Company agreed to acquire all of the outstanding capital stock of Integrated Timeshare Solutions, Inc. (“ITS”) in exchange for our newly issued common shares. Accordingly, as a result of the exchange ITS became a wholly owned subsidiary of the Company. ITS was established on July 2, 2014 as a real estate consulting firm specializing in timeshare liquidation and mortgage relief. We commenced operations in that area industry upon consummation of the acquisition. As of this date, however, we have discontinued the operations of this subsidiary.

On December 31, 2015, we entered into an Asset Purchase Agreement pursuant to which we agreed to acquire all of the assets and liabilities of Boston Carriers LTD, a corporation organized under the laws of the Republic of the Marshall Islands (“Boston Carriers”) in exchange for newly issued shares of the Company’s Series B Preferred Shares, $0.0001 par value per share (the “Series B Preferred Shares”), which were issued to the former sole shareholder of Boston Carriers (the “Exchange”). Included in the assets acquired was all outstanding stock in Poseidon Navigation Corp. a corporation organized under the laws of the Republic of the Marshall Islands (“Poseidon”). Accordingly, as a result of the Exchange, Poseidon is now a wholly owned subsidiary of the Company. In connection with the execution of the Purchase Agreement, we filed a Certificate of Designations with the Secretary of State of the State of Nevada regarding the creation of the Series B Preferred Shares and an aggregate of 1,850,000 Series B Preferred Shares were issued to the former Boston Carriers shareholder.

The Series B Preferred Shares will automatically convert, with no action by the holders thereof, into common shares of the Corporation at a rate of 1,000 common shares for each Series B Preferred Share, on the date that is five (5) business days following the distribution by the Corporation of a cash dividend to the shareholders of its common shares of all amounts received by the Corporation as a refund to the Corporation from the United States Internal Revenue Service in connection with the Corporation's 2014 federal tax return less a maximum of $20,000 which would solely be used to pay the Corporation’s obligation under a settlement agreement relating to the Strong v. Strong lawsuit (the "Dividend"). The Series B Preferred Shares are not participating shares and prior to conversion the holders thereof shall not receive any dividend or other distribution from the Corporation and no portion of the Dividend will be distributed for the benefit of the holders of Series B Preferred Shares. Prior to conversion, however, the holders of Series B Preferred Shares shall be entitled to vote on all matters on which holders of common shares are entitled to vote and shall vote as if such Series B Preferred Shares had converted, provided however, that the holders of Series B Preferred Shares shall not be entitled to vote on any matter which would amend the terms of and restrictions on the Series B Preferred Shares.

Effective as of March 21, 2016, we changed our jurisdiction of incorporation from the State of Nevada to the Republic of the Marshall Islands (the “Reincorporation”), following approval by the Company’s board of directors on February 29, 2016 and written consent from the holder of a majority of the voting power of the Company dated February 29, 2016 (the “Written Consent”). Pursuant to the same approvals and consents, the Company’s name changed effective March 21, 2016 to Boston Carriers Inc. (the “Name Change”). The Company submitted information regarding the Reincorporation and the Name Change to the Financial Industry Regulatory Authority (“FINRA”) on March 2, 2016 and requested that the Company be assigned a new stock symbol effective March 21, 2016. We have not yet received assignment of the new symbol from FINRA.

In connection with the Reincorporation, we filed Articles of Conversion with the State of Nevada and Articles of Domestication with the Republic of the Marshall Islands as well as Articles of Incorporation with the Republic of the Marshall Islands (the “MI Articles”).

Due to the Reincorporation, the rights of the Company’s shareholders is now governed by the Business Corporations Act of the Marshall Islands, the MI Articles of Incorporation and new bylaws which were contemporaneously approved by our Board of Directors. As a Marshall Islands corporation following the Reincorporation, we are deemed to be the same continuing entity as the Nevada corporation prior to the Reincorporation. As such, we continue to possess all of the rights, privileges and powers we previously had, all of our property and all of our debts, liabilities and obligations, including all contractual obligations, and we continue with the same business, assets, liabilities, headquarters, officers and directors as immediately prior to the Reincorporation.

Upon effectiveness of the Reincorporation, all of our issued and outstanding common shares automatically converted into issued and outstanding common shares of the Marshall Islands Company without any action on the part of our shareholders. In the same manner, all of our issued and outstanding preferred shares automatically converted into issued and outstanding preferred shares of the Marshall Islands Company holding identical rights as the pre-existing preferred shares without any action on the part of the Company’s shareholders. In order to more accurately reflect their relative rights, as part of the Reincorporation, we renamed the prior Series B Preferred Shares as Series A Preferred Shares and renamed our previously existing Convertible Redeemable Preferred Shares as Series B Preferred Shares.

Our principal executive offices are located at 18 Nap. Zerva Str., 166 75 Glyfada, Greece and our telephone number is +30 2130165708. The company does not yet operate a website about its current operations. Previously the company operated a website at http://www.integratedinteriordesigns.com. Information contained on or accessed through our website or any other website does not constitute a part of this prospectus.

Our Current Business

Industry Overview

All the information and data presented in this section, including the analysis of the various sectors of the dry bulk shipping industry has been provided by Clarcksons. The statistical and graphical information contained herein is drawn from its database. In connection therewith, Clarcksons has advised that: (1) certain information in Clarcksons database is derived from estimates or subjective judgments; (2) the information in the databases of other maritime data collection agencies may differ from the information in Clarcksons database; and (3) while Clarcksons has taken reasonable care in the compilation of the statistical and graphical information and believes it to be accurate and correct, data compilation is subject to limited audit and validation procedures.

Seaborne cargo is broadly categorized as either dry or liquid cargo. Dry cargo includes dry bulk cargo, container cargo, non-container cargo and other cargo. Liquid cargo includes crude oil, refined petroleum products, vegetable oils, gases and chemicals.

Ocean going vessels represent the most efficient and often the only means of transporting large volumes of basic commodities and finished products over long distances. In general, the supply of, and demand for, seaborne transportation capacity are the primary drivers of charter rates and values for all vessels. Due to the larger volume of cargo they ship, their reliance on a few key commodities and long-haul routes among a small number of ports, larger vessels exhibit higher charter rate and vessel value volatility compared to smaller vessels. Vessel values primarily reflect prevailing and expected future charter rates, and are also influenced by factors such as the age of the vessel, the shipyard of its construction and its specifications.

During extended periods of high charter rates, vessel values tend to appreciate. Conversely, during periods where rates have declined, such as the period we are currently in, vessel values tend to decline. Historically, the relationship between incremental supply and demand has varied among different types of vessels, because the drivers of demand for each type of vessel are different and are not always subject to the same factors. This means that at any one time different types of vessels, such as tankers and dry bulk carriers, may be in differing stages of their respective

supply and demand cycle.

Dry bulk cargo comprises approximately 39% of total seaborne trade. Dry bulk cargo is any form of cargo that is shipped in bulk and can be loaded and unloaded in its original, unadulterated and unpackaged state. Common dry bulk cargoes include steel, grains (soybean, wheat, etc.), cement and lumber. Less directly visible, but often in large quantities, are iron ore and metallurgic coal (the two primary raw materials used in producing steel), thermal coal (used in power plants for electric generation) and fertilizers (used in farming). For statistical purposes, dry bulk cargoes are commonly categorized into major or minor bulks. The major bulks category consists of iron ore, coal and grains. The minor bulks category includes, but is not limited to, fabricated steel, steel scrap, fertilizers, lumber, cement and minerals. These raw materials are typically poured or lifted into a ship’s hold without the aid of additional pallets or other packaging materials.

Dry bulk carriers play an important role in connecting the resource extraction points, such as mines and farms, and end users, such as steel mills and food processors. Due to the increasingly global supply chain and changing demand patterns for different raw materials, dry bulk freighters provide the most cost effective means of completing the supply chain as compared to other transportation methods such as air, rail or truck transportation. Shipping is beneficial relative to other modes of transportation due to the larger economies of scale, especially considering the massive capacity of bulk freighters, and their ability to serve destinations with limited existing infrastructure. Additionally, the majority of the supply centers are either at a great distance or separated by vast bodies of water from the main demand centers, making waterborne transportation the only effective means of movement in most cases.

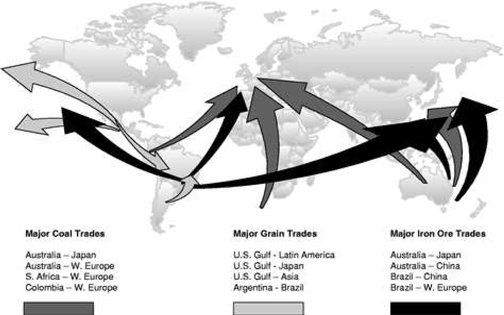

Major Dry Bulk Seaborne Trades

Dry Bulk Shipping Demand

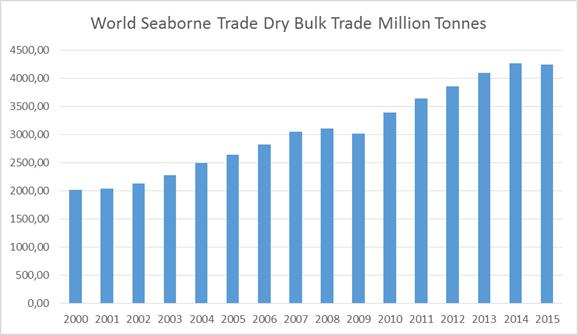

Dry bulk trade is influenced by the underlying demand for the dry bulk commodities which, in turn, is influenced by the level of worldwide economic activity. Generally, growth in GDP and industrial production correlate with peaks in demand for marine dry bulk transportation services. The following chart demonstrates the change in world dry bulk trade between 2000 and 2015 (Source Clarcksons).

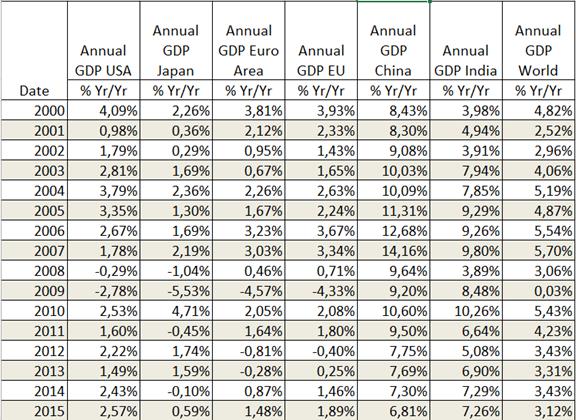

Historically, certain economies have acted as the primary drivers of dry bulk trade. In the 1990s, Japan was the driving force of increases in ton-miles, when buoyant Japanese industrial production stimulated demand for imported dry bulk commodities. More recently, China and, to a lesser extent, India have been the main drivers behind the recent increase in seaborne dry bulk trade, as high levels of economic growth have generated increased demand for imported raw materials. The following table illustrates the GDP growth rates of China and India compared to those of the United States, Europe, Japan and the world during the periods indicated (Source IMF).

Coal

Asia’s rapid industrial development has contributed to strong demand for coal. Coal is divided into two main categories: thermal (or steam) and coking (or metallurgical). Thermal coal is used mainly for power generation, whereas coking coal is used to produce coke to feed blast furnaces in the production of steel. Chinese and Indian electricity consumption has grown at a rapid pace. China is the second largest consumer of electricity in the world, even though generally highly populated developing economies have low per capita electricity consumption.

Expansion in air conditioned office and factory space, along with industrial use, has increased demand for electricity, of which nearly half is generated from coal-fired plants, thus increasing demand for thermal coal. In addition, Japan’s domestic nuclear power generating industry has suffered from safety problems in recent years, leading to increased demand for oil, gas and coal-fired power generation. Furthermore, the high cost of oil and gas has led to increasing development of coal-fired electricity plants around the world, especially in Asia. Future prospects are also heavily tied to the steel industry. Coking coal is of a higher quality than thermal coal (i.e., more carbon and fewer impurities) and its price is both higher and more volatile.

Increases in steam coal demand have been significant, as both developed and developing nations require increasing amounts of electric power. The main exporters of coal are Australia, South Africa, Russia, Indonesia, the United States, Colombia and Canada. The main importers of coal are Europe, Japan, South Korea, Taiwan, India and China. China has recently become a net importer of coal, and Indian imports have doubled in less than five years. Coal is transported primarily by Capesize, Panamax and Supramax vessels.

Iron Ore

Iron ore is used as a raw material for the production of steel, along with limestone and coking (or metallurgical) coal. Steel is the most important construction and engineering material in the world. Main importers are China, the European Union, Japan and South Korea. The main producers and exporters of iron ore are Australia and Brazil.

Chinese imports of iron ore have grown significantly due to increased steel production in the last few years and have been a major driving force in the dry bulk sector.

Chinese imports of iron ore have traditionally come primarily from Australia, Brazil and India. The shares of Indian and Brazilian imports into China have increased since 2000. Australia and Brazil together account for approximately two-thirds of global iron ore exports. Although both countries have seen strong demand from China, Australia continues to benefit the most from China’s increased demand for iron ore. India is also becoming a major exporter of iron ore. Unlike Australia and Brazil, which tend to export primarily in the larger Capesize vessels, much of India’s exports are shipped in smaller vessels.

Grains

Grains include wheat, coarse grains (corn, barley, oats, rye and sorghum) and oil seeds extracted from different crops, such as soybeans and cotton seeds. In general, wheat is used for human consumption while coarse grains are used as feed for liveShares. Oil seeds are used to manufacture vegetable oil for human consumption or for industrial use, while their protein-rich residue is used as food for liveShares.

Global grain production is dominated by the United States. Argentina is the second largest producer, followed by Canada and Australia. International trade in grains is dominated by four key exporting regions: North America, South America, Oceania and Europe (including the former Soviet Union). These regions collectively account for over 90% of global exports. In terms of imports, the Asia/Pacific region (excluding Japan) ranks first, followed by Latin America, Africa and the Middle East.

Historically, international grain trade volumes have fluctuated considerably as a result of regional weather conditions and the long history of grain price volatility and government interventionism. However, demand for wheat and coarse grains are fundamentally linked in the long-term to population growth and rising per capita income.

Minor Dry Bulks

The balance of dry bulk trade, minor dry bulks, can be subdivided into two types of cargo. The first type includes secondary dry bulks or free-flowing cargo, such as agricultural cargoes, bauxite and alumina, fertilizers and cement. The second type is neo-bulks, which include non-free flowing or part manufactured cargo that is principally forest products and steel products, including scrap.

Seasonality

Two of the three largest commodity drivers of the dry bulk industry, coal and grains, are affected by seasonal demand fluctuations. Thermal coal is linked to the energy markets and in general encounters upswings towards the end of the year in anticipation of the forthcoming winter period as power supply companies try to increase their Sharess, or during hot summer periods when increased electricity demand is required for air conditioning and refrigeration purposes. Grain production is also seasonal and is driven by the harvest cycle of the northern and southern hemispheres. However, with four nations and the European Union representing the largest grain producers (the United States, Canada and the European Union in the northern hemisphere and Argentina and Australia in the southern hemisphere), harvests and crops reach seaborne markets throughout the year. Taken as a whole, seasonal factors mean that the market for dry bulk vessels is often stronger during the winter months.

Dry Bulk Carrier Supply

The world dry bulk fleet is generally divided into six major categories, based on a vessel’s cargo carrying capacity. These categories consist of: Handysize, Handymax/Supramax, Panamax, Post Panamax, Capesize and Very Large Ore Carrier.

Dry Bulk Vessel Types and Sizes

| Cargo Type | Handysize | Handymax | Supramax | Panamax | Post Panamax/ Kamsarmax | Capesize | VLOC | |||||||||||||||||||

| Iron Ore | X | X | X | |||||||||||||||||||||||

| Coal | X | X | X | X | X | X | ||||||||||||||||||||

| Grains | X | X | X | X | X | |||||||||||||||||||||

| Alumina, Bauxite | X | X | X | X | X | |||||||||||||||||||||

| Steel Products | X | X | X | X | X | |||||||||||||||||||||

| Forest Products | X | X | X | |||||||||||||||||||||||

| Fertilizers | X | X | X | |||||||||||||||||||||||

| Minerals | X | X | X | |||||||||||||||||||||||

| Minor Bulks-Other | X | X |

The supply of dry bulk shipping capacity, which is measured by the amount of suitable vessel tonnage available to carry cargo, is determined by the size of the existing worldwide dry bulk fleet, the number of new vessels on order, the scrapping of older vessels and the number of vessels out of active service (i.e., laid up or otherwise not available for hire). In addition to prevailing and anticipated freight rates, factors that affect the rate of newbuilding, scrapping and laying-up include newbuilding prices, secondhand vessel values in relation to scrap prices, costs of bunkers and other voyage expenses, costs associated with classification society surveys, normal maintenance and insurance coverage, the efficiency and age profile of the existing fleets in the market and government and industry regulation of marine transportation practices.

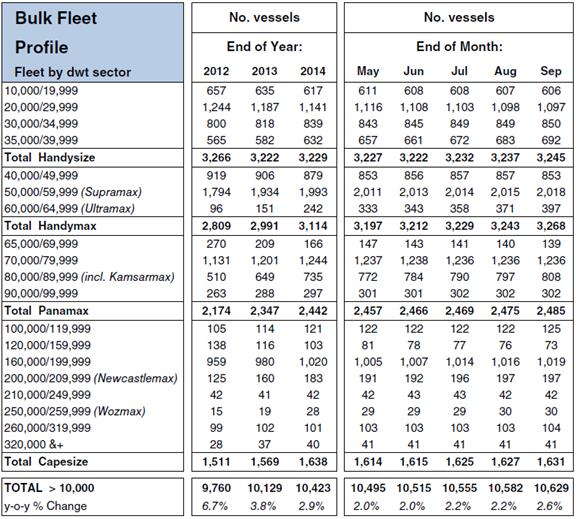

As of September, 2015, the world fleet of dry bulk vessels consisted of 10,629 vessels, totaling 1,547 million dwt in capacity. These figures are, however, based on pure dry bulk vessels and exclude a small number of combination vessels. The following table presents the world dry bulk vessel fleet by size as of September, 2015.

Current and Planned Operations

Through our wholly owned subsidiary, Poseidon Navigation Corp., a Marshall Islands corporation, we will own and operate a dry bulk vessel that transport iron ore, coal, grain, steel products, cement, alumina and other dry bulk cargoes internationally. We intend to grow our fleet through timely and selective acquisitions in a manner that we believe will provide an attractive return on equity and will be accretive to our earnings and cash flow based on anticipated market rates at the time of purchase. There is no guarantee however, that we will be able to find suitable vessels to purchase or that such vessels will provide an attractive return on equity or be accretive to our earnings and cash flow.

Competition

Demand for drybulk carriers fluctuates in line with the main patterns of trade of the major drybulk cargoes and varies according to changes in the supply and demand for these items. We compete with other owners of drybulk carriers in the Handymax/Supramax size sectors. Ownership of drybulk carriers is highly fragmented and is divided among approximately 1,600 independent drybulk carrier owners. We compete for charters on the basis of price, vessel location, size, age and condition of the vessel, as well as on our reputation as an owner and operator.

Employees

We currently employ only one full time person, our Chief Executive Officer.

Description Of Property

We do not own any real property or any interest in real property and does not invest in real property or have any policies with respect thereto as a part of its operations or otherwise.

We currently maintain our principal business at 18 Nap. Zerva Str. 16675 Glyfada, Greece which is provided to us on a rent free basis. We also lease space in Delray Beach, FL on a month to month basis for $450 per month plus tax. This office will be used by our Chief Executive Officer while he is in the United States and also by Osnah Bloom, former CEO of the Company who has been hired as a consultant to assist with the transition of the Company’s business. As our employee count grows we will relocate our principal business office to a larger location in Greece.

Legal Proceedings

We are not aware of any pending or threatened litigation against Boston Carriers that we expect will, individually or in the aggregate, have a material adverse effect on our business, financial condition, liquidity, or operating results. We cannot assure you that we will not be adversely affected in the future by legal proceedings.

In the ordinary course of the Company’s discontinued business in the health care industry, the Company became involved in lawsuits and legal proceedings involving claims of medical malpractice related to medical services provided by the Company’s affiliated physicians. The Company is currently involved in the settlement stages of one such matter.

Edra Schwartz as the Personal Representative of the Estate of Robert A. Schwartz, Deceased, v. Jason Strong, M.D., Aretha Nelson, M.D. and Inpatient Clinical Solutions, Inc. - This matter involves a 66 year old white male who developed a MRSA (methicillin-resistant staphylococcus aureus) infection following a craniotomy to remove a suspected meningioma. The matter alleges (1) Failure to properly interpret the brain MRIs preoperatively (this is directed at the radiologist preoperatively); and (2) Failure to diagnose a MRSA infection and brain abscess following the craniotomy on May 6, 2009. The patient died on September 24, 2009. The suit commenced October 18, 2011 and the case is pending in the circuit court of the 17 Judicial Circuit in and for Broward County, FL, Case # 11-10485. The claim is for unspecified monetary damages. The Company is defending this case vigorously and, while the claims for damages have not been quantified, the Company does not believe that a negative decision would have a material impact on the Company.

Additionally, in October 2015, the Company became involved in a potential legal settlement relating to a malpractice claim. The Company and the other parties have not entered into a settlement agreement. However, the Company anticipates that the amount will be covered by the tail malpractice insurance. The Company has accrued $25,000 for the deductible on the tail malpractice insurance as of December 31, 2015.

We are not aware of any other pending or threatened litigation against us that we expect will, individually or in the aggregate, have a material adverse effect on our business, financial condition, liquidity, or operating results. We cannot assure you that we will not be adversely affected in the future by legal proceedings.

Item 1A. RISK FACTORS

Our business is subject to numerous risks. We caution you that the following important factors, among others, could cause our actual results to differ materially from those expressed in forward-looking statements made by us or on our behalf in filings with the SEC, press releases, communications with investors and oral statements. Any or all of our forward-looking statements in this and in any other public statements we make may turn out to be wrong. They can be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties. Many factors mentioned in the discussion below will be important in determining future results. Consequently, no forward-looking statement can be guaranteed. Actual future results may vary materially from those anticipated in forward-looking statements. We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. You are advised, however, to consult any further disclosure we make in our reports filed with the SEC.

RISKS RELATED TO OUR BUSINESS

We have changed the focus of our business.

Previously our business operations were focused exclusively on the health care industry. Following the sale of the majority of our assets in 2012, management decided to pursue opportunities in the interior design industry and unsuccessfully attempted to enter the real estate consulting industry. Our management team did not have experience in the real estate consulting industry and has limited experience in the interior design industry. We have now discontinued the operations in the interior design industry and, following our acquisition of all of the assets of Boston Carriers, LTD have now entered into the dry bulk shipping business.

Our limited operating history in our current industry makes it difficult to evaluate our current business and future prospects.

We have only recently begun operating in the dry bulk shipping business. Previously we were involved in unrelated businesses. Therefore, we have a relatively limited operating history in executing our current business model. Our lack of operating history makes it difficult to evaluate our current business model and future prospects.

In light of the costs, uncertainties, delays and difficulties frequently encountered by companies in the early stages of development with limited operating history, there is a significant risk that we will not be able to implement or execute our current business plan, or demonstrate that our business plan is sound. If we cannot execute any one of the foregoing or similar matters relating to our operations, our business may fail.

We are dependent on the services of our Chief Executive Officer and the loss of his services would have a material adverse effect on our business.

We are highly dependent on the services of Antonios Bertsos, our Chief Executive Officer. Mr. Bertsos maintains responsibility for our overall corporate operational strategy. Mr. Bertsos has a strong background in dry bulk shipping. Mr. Bertsos is an integral part of our operations and the loss of his services would have a material adverse effect upon our business and prospects.

We are an “emerging growth company” under the JOBS Act of 2012 and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common shares less attractive to investors.

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012 (“JOBS Act”), and we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies (other than smaller reporting companies) that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act and reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements. We are also currently able to take advantage of these exemptions as a smaller reporting company. In addition, emerging growth companies are entitled to take advantage of exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. By comparison, smaller reporting companies (unless they are also emerging growth companies) are subject to the requirements of holding nonbinding advisory votes on executive compensation, and shareholder approval of any golden parachute payments not previously approved. We cannot predict if investors will find our common shares less attractive because we may rely on these exemptions. If some investors find our common shares less attractive as a result, there may be a less active trading market for our common shares and our share price may be more volatile.

Furthermore, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We are choosing to take advantage of the extended transition period for complying with new or revised accounting standards. As a result, our financial statements may not be comparable to those of companies that comply with public company effective dates.

We will remain an “emerging growth company” for up to five years, although we will lose that status sooner if our revenues exceed $1 billion, if we issue more than $1 billion in non-convertible debt in a three year period, or if the market value of our common shares that is held by non-affiliates exceeds $700 million as of any June 30.

Our status as an “emerging growth company” under the JOBS Act of 2012 may make it more difficult to raise capital as and when we need it.

Because of the exemptions from various reporting requirements provided to us as an “emerging growth company” and because we will have an extended transition period for complying with new or revised financial accounting standards, we may be less attractive to investors and it may be difficult for us to raise additional capital as and when we need it. Investors may be unable to compare our business with other companies in our industry if they believe that our financial accounting is not as transparent as other companies in our industry. If we are unable to raise additional capital as and when we need it, our financial condition and results of operations may be materially and adversely affected.

Risks relating to Our Industry

The seaborne transportation industry is cyclical and volatile.

The international seaborne transportation industry is both cyclical and volatile in terms of charter rates, vessel values and profitability. Fluctuations in charter rates result from changes in the supply and demand for vessel capacity and changes in the supply and demand for energy resources, commodities, semi-finished and finished consumer and industrial products internationally carried at sea. For example, the degree of charter hire rate volatility among different types of dry bulk vessels has varied widely. After reaching historical highs in mid-2008, charter hire rates for Supramax and Panamax dry bulk vessels reached near historically low levels at the end of 2008, and have since recovered to some extent but recently fallen again to historically low levels. Because from time to time we may charter some of our future vessels pursuant to short-term time charters or on the spot market, we may be exposed to changes in spot market and short-term charter rates for dry bulk vessels and such changes may affect our earnings and the value of our dry bulk vessels at any given time. The supply of and demand for shipping capacity strongly influences freight rates. The factors affecting the supply and demand for vessels are outside of our control, and the nature, timing and degree of changes in industry conditions are unpredictable.

Factors that influence demand for vessel capacity include:

| • | supply and demand for energy resources, commodities, semi-finished and finished consumer and industrial products; |

| • | changes in the production of energy resources, commodities, semi-finished and finished consumer and industrial products; |

| • | the location of regional and global production and manufacturing facilities; |

| • | the location of consuming regions for energy resources, commodities, semi-finished and finished consumer and industrial products; |

| • | the globalization of production and manufacturing; |

| • | global and regional economic and political conditions; |

| • | developments in international trade; |

| • | changes in seaborne and other transportation patterns, including the distance dry bulk cargo is transported by sea; |

| • | environmental and other regulatory developments; |

| • | currency exchange rates; and |

| • | weather. |

Factors that influence the supply of vessel capacity include:

| • | the number of newbuilding deliveries, which among other factors relates to the ability of shipyards to deliver newbuildings by contracted delivery dates and the ability of purchasers to finance such newbuildings; |

| • | the scrapping rate of older vessels; |

| • | vessel casualties; |

| • | the price of steel; |

| • | changes in environmental and other regulations that may limit the useful lives of vessels; |

| • | the number of vessels that are out of service; and |

| • | port or canal congestion. |

We anticipate that the future demand for our dry bulk vessels and charter rates will be dependent upon continued economic growth in the world’s economies including China and India, seasonal and regional changes in demand and changes to the capacity of the global dry bulk vessel fleet and the sources and supply of dry bulk cargo to be transported by sea. Adverse economic, political, social or other developments could negatively impact charter rates and therefore have a material adverse effect on our business, results of operations and ability to pay dividends.

The dry bulk vessel charter market remains significantly below its high in 2008.

The revenues, earnings and profitability of companies in our industry are affected by the charter rates that can be obtained in the market, which is volatile and has experienced significant declines since its highs in the middle of 2008. For example, the Baltic Dry Index, or BDI highest ever of 11,793 on May 20, 2008 is now to as low of 478 on December 30, 2015.

There remains considerable instability in the world economy.

We expect that a significant number of the port calls we expect our vessels to make will likely involve the loading or discharging of raw materials in ports in the Asia Pacific region, particularly China. As a result, a negative change in economic conditions in any Asia Pacific country, particularly China, Japan and, to some extent, India, can have a material adverse effect on our business, financial position and results of operations, as well as our future prospects, by reducing demand and, as a result, charter rates and affecting our ability to charter our vessels. In the recent past, China and India have had two of the world’s fastest growing economies in terms of gross domestic product and have been the main driving force behind increases in marine dry bulk trade and the demand for dry bulk vessels. If economic growth declines in China, Japan, India and other countries in the Asia Pacific region, we may face decreases in such dry bulk trade and demand. Moreover, a slowdown in the United States and Japanese economies or the economies of the European Union or certain Asian countries may adversely affect economic growth in China, India and elsewhere. Such an economic downturn in any of these countries could have a material adverse effect on our business, financial condition, results of operations and ability to pay dividends.

The international shipping industry and dry bulk market are highly competitive.

The shipping industry and dry bulk market are capital intensive and highly fragmented with many charterers, owners and operators of vessels and are characterized by intense competition. Competition arises primarily from other vessel owners, most of whom have substantially greater resources than we currently do. Although we believe that no single competitor has a dominant position in the markets in which we compete, the trend towards consolidation in the industry is creating an increasing number of global enterprises capable of competing in multiple markets, which may result in a greater competitive threat to us. Our competitors may be better positioned to devote greater resources to the development, promotion and employment of their businesses than we are. Competition for the transportation of cargo by sea is intense and depends on customer relationships, operating expertise, professional reputation, price, location, size, age, condition and the acceptability of the vessel and its operators to the charterers. Competition may increase in some or all of our principal markets, including with the entry of new competitors, who may operate larger fleets through consolidations or acquisitions and may be able to sustain lower charter rates and offer higher quality vessels than we are able to offer. We may not be able to continue to compete successfully or effectively with our competitors and our competitive position may be eroded in the future, which could have an adverse effect on our fleet utilization and, accordingly, business, financial condition, results of operations and ability to pay dividends.

There may be changes in the economic and political environment in China and China may adopt policies to regulate its economy.

The Chinese economy differs from the economies of most countries belonging to the Organization for Economic Cooperation and Development in respects such as structure, government involvement, level of development, growth rate, capital reinvestment, allocation of resources, rate of inflation and balance of payments position. Prior to 1978, the Chinese economy was a planned economy. Since 1978, increasing emphasis has been placed on the utilization of market forces in the development of the Chinese economy. Annual and five year State Plans are adopted by the Chinese government in connection with the development of the economy. Although state-owned enterprises still account for a substantial portion of the Chinese industrial output, in general, the Chinese government is reducing the level of direct control that it exercises over the economy through State Plans and other measures. There is an increasing level of freedom and autonomy in areas such as allocation of resources, production, pricing and management and a gradual shift in emphasis to a “market economy” and enterprise reform. Limited price reforms were undertaken, with the result that prices for certain commodities are principally determined by market forces. Many of the reforms are unprecedented or experimental and may be subject to revision, change or abolition based upon the outcome of such experiments. We cannot assure you that the Chinese government will continue to pursue a policy of economic reform.

The level of imports to and exports from China could be adversely affected by changes to these economic reforms by the Chinese government, as well as by changes in political, economic and social conditions or other relevant policies of the Chinese government, such as changes in laws, regulations or export and import restrictions, all of which could, adversely affect our business, operating results, financial condition and ability to pay dividends.

We depend on spot charters in volatile shipping markets.

We will charter our vessel on the spot charter market, and we may charter other vessels on the spot market in the future. Although dependence on spot charters is not unusual in the shipping industry, the spot charter market is highly competitive and spot charter rates may fluctuate significantly based upon available charters and the supply of and demand for seaborne shipping capacity. While our focus on the spot market may enable us to benefit if industry conditions strengthen, we must consistently procure spot charter business. Conversely, such dependence makes us vulnerable to declining market rates for spot charters and to the off-hire periods including ballast passages. Rates within the spot charter market are subject to volatile fluctuations while longer-term time charters provide income at pre-determined rates over more extended periods of time. There can be no assurance that we will be successful in keeping our vessels fully employed in these short-term markets or that future spot rates will be sufficient to enable the vessels to be operated profitably. A significant decrease in charter rates would affect value and adversely affect our profitability, cash flows and ability to pay dividends. We cannot give assurances that future available spot charters will enable us to operate our vessels profitably.

The dry bulk vessel capacity may be oversupplied.

The market supply of drybulk carriers has been increasing as a result of the delivery of numerous newbuilding orders over the last few years. Newbuildings have been delivered in significant numbers since the beginning of 2006 and, as of January 1, 2015, newbuilding orders had been placed for an aggregate of more than 22% of the existing global drybulk fleet, with deliveries expected during the next three years. Due to lack of financing many analysts expect significant cancellations and/or slippage of newbuilding orders. While vessel supply will continue to be affected by the delivery of new vessels and the removal of vessels from the global fleet, either through scrapping or accidental losses, an over-supply of dry bulk carrier capacity could exacerbate the recent decrease in charter rates or prolong the period during which low charter rates prevail. Currently, our vessel will be employed in the spot market where operations are at times unprofitable due the volatility associated with dry cargo freight rates. If market conditions persist or worsen we could have a material adverse effect on our business, results of operations, cash flows, financial condition and ability to pay dividends.

The market values of our vessel may decrease.

The market value of dry bulk vessels has generally experienced high volatility. The market prices for secondhand and newbuilding dry bulk vessels in the recent past have declined from historically high levels to low levels within a short period of time. The market value of any vessels we acquire may increase or decrease depending on a number of factors including:

| • | prevailing level of charter rates; |

| • | general economic and market conditions affecting the shipping industry; |

| • | competition from other shipping companies; |

| • | configurations, sizes and ages of vessels; |

| • | supply and demand for vessels; |

| • | other modes of transportation; |

| • | cost of newbuildings; |

| • | governmental or other regulations; and |

| • | technological advances. |

If the market value of our vessels declines, we may incur losses if we sell one or more of our vessels, to obtain additional financing, all of which would adversely affect our business and financial condition, results of operations and ability to pay dividends. If we sell any vessel at a time when vessel prices have fallen and before we have recorded an impairment adjustment to our financial statements, the sale may be at less than the vessel’s depreciated book value in our financial statements, resulting in a loss and a reduction in earnings.

Our revenues are subject to seasonal fluctuations.

Our fleet will consist of dry bulk vessels that operate in markets that have historically exhibited seasonal variations in demand and, as a result, in charter rates. This seasonality may result in quarter-to-quarter volatility in our operating results, which could affect the amount of dividends, if any, that we pay to our shareholders from quarter to quarter. The dry bulk sector is typically stronger in the fall and winter months in anticipation of increased consumption of coal and other raw materials in the northern hemisphere during the winter months. As a result, revenues from our dry bulk vessels not otherwise fixed on long term charters may be weaker during the quarters ended June 30 and September 30, and, conversely, we expect our revenues from our dry bulk vessels may be stronger in quarters ended December 31 and March 31. In addition, unpredictable weather patterns in these months tend to disrupt vessel scheduling and supplies of certain commodities. This seasonality could have a material adverse effect on our business, financial condition, results of operations and ability to pay dividends.

Our industry is subject to complex laws and regulations, including environmental regulations.

Our operations are subject to numerous laws and regulations in the form of international conventions and treaties, national, state and local laws and national and international regulations in force in the jurisdictions in which our vessels will operate or are registered, which can significantly affect the ownership and operation of our vessels. These requirements include but are not limited to: U.S. Oil Pollution Act 1990, as amended, which we refer to as OPA; International Convention for the Safety of Life at Sea, 1974, as amended, which we refer to as SOLAS; International Convention on Load Lines, 1966; International Convention for the Prevention of Pollution from Ships, 1973, as amended by the 1978 Protocol, which we refer to as MARPOL; International Convention on Civil Liability for Bunker Oil Pollution Damage, 2001, which we refer to as the Bunker Convention; International Convention on Liability and Compensation for Damage in Connection with the Carriage of Hazardous and Noxious Substances by Sea, 1996, as superseded by the 2010 Protocol, which we refer to as the HNS Convention; International Convention on Civil Liability for Oil Pollution Damage of 1969, as amended by the 1992 Protocol and further amended in 2000, which we refer to as the CLC; International Convention on the Establishment of an International Fund for Compensation for Oil Pollution Damage, 1971, as amended, which we refer to as the Fund Convention; and Marine Transportation Security Act of 2002, which we refer to as the MTSA.

Government regulation of vessels, particularly in the area of environmental requirements, can be expected to become more stringent in the future and could require us to incur significant capital expenditures on our vessels to keep them in compliance, or even to scrap or sell certain vessels altogether. Compliance with such laws, regulations and standards, where applicable, may require installation of costly equipment or operational changes and may affect the resale value or useful lives of our vessels. We may also incur additional costs in order to comply with other existing and future regulatory obligations, including, but not limited to, costs relating to air emissions, the management of ballast waters, maintenance and inspection, elimination of tin-based paint, development and implementation of emergency procedures and insurance coverage or other financial assurance of our ability to address pollution incidents. These costs could have a material adverse effect on our business, results of operations, cash flows and financial condition and our ability to pay dividends.

Additional conventions, laws and regulations may be adopted which could limit our ability to do business or increase the cost of our doing business and which may materially adversely affect our business, financial condition and results of operations. Because such conventions, laws and regulations are often revised, or the required additional measures for compliance are still under development, we cannot predict the ultimate cost of complying with such conventions, laws and regulations or the impact thereof on the resale prices or useful lives of our vessels. We are also required by various governmental and quasi-governmental agencies to obtain certain permits, licenses, certificates and financial assurances with respect to our operations.

These requirements can also affect the resale prices or useful lives of our vessels or require reductions in capacity, vessel modifications or operational changes or restrictions. Failure to comply with these requirements could lead to decreased availability or more costly insurance coverage for environmental matters or result in the denial of access to certain jurisdictional waters or ports, or detention in certain ports. Under local, national and foreign laws, as well as international treaties and conventions, we could incur material liabilities, including cleanup obligations and claims for natural resource, personal injury and property damages in the event that there is a release of petroleum or other hazardous materials from our vessels or otherwise in connection with our operations. Violations of, or liabilities under, environmental regulations can result in substantial penalties, fines and other sanctions, including, in certain instances, seizure or detention of our vessels. Events of this nature would have a material adverse effect on our business, financial condition and results of operations.

The operation of our vessels is affected by the requirements set forth in the ISM Code. The ISM Code requires shipowners, ship managers and bareboat charterers to develop and maintain an extensive “Safety Management System” that includes the adoption of a safety and environmental protection policy setting forth instructions and procedures for safe operation and describing procedures for dealing with emergencies. The failure of a shipowner or bareboat charterer to comply with the ISM Code may subject it to increased liability, may invalidate existing insurance or decrease available insurance coverage for the affected vessels and may result in a denial of access to, or detention in, certain ports.

Capital expenditures and other costs necessary to operate and maintain our vessels may increase.

Changes in safety or other equipment standards, as well as compliance with standards imposed by maritime self-regulatory organizations and customer requirements or competition, may require us to make additional expenditures. In order to satisfy these requirements, we may, from time to time, be required to take our vessels out of service for extended periods of time, with corresponding losses of revenues. In the future, market conditions may not justify these expenditures or enable us to operate some or all of our vessels profitably during the remainder of their economic lives.

There are inherent operational risks in the seaborne transportation industry and the costs associated with these risks, such as drydocking for vessel repairs, may be substantial.

The operation of any vessel includes risks such as mechanical failure, collision, fire, contact with floating objects, cargo or property loss or damage and business interruption due to political circumstances in foreign countries, piracy, terrorist attacks, armed hostilities and labor strikes. Such occurrences could result in death or injury to persons, loss of property or environmental damage, delays in the delivery of cargo, loss of revenues from or termination of charter contracts, governmental fines, penalties or restrictions on conducting business, higher insurance rates and damage to our reputation and customer relationships generally. In the past, political conflicts have also resulted in attacks on vessels, mining of waterways and other efforts to disrupt international shipping, particularly in the Arabian Gulf region. In addition, there is always the possibility of a marine disaster, including oil spills and other environmental damage.

If our vessels suffer damage, they may need to be repaired at a drydocking facility. The costs of drydocking repairs are unpredictable and may be substantial. We may have to pay drydocking costs that our insurance does not cover in full. The loss of earnings while these vessels are being repaired and repositioned, as well as the actual cost of these repairs, would decrease our earnings. In addition, space at drydocking facilities is sometimes limited and not all drydocking facilities are conveniently located. We may be unable to find space at a suitable drydocking facility or our vessels may be forced to travel to a drydocking facility that is not conveniently located to our vessels’ positions. The loss of earnings while these vessels are forced to wait for space or to steam to more distant drydocking facilities would decrease our earnings.

Our insurance may not be adequate to cover our losses that may result from our operations due to the inherent operational risks of the seaborne transportation industry.

We will carry insurance to protect us against most of the accident-related risks involved in the conduct of our business, including marine hull and machinery insurance, war risk insurance, protection and indemnity insurance, which includes pollution risks, crew insurance and war risk insurance. However, we may not be adequately insured to cover losses from our operational risks, which could have a material adverse effect on us. Additionally, our insurers may refuse to pay particular claims and our insurance may be voidable by the insurers if we take, or fail to take, certain action, such as failing to maintain certification of our vessels with applicable maritime regulatory organizations. Any significant uninsured or underinsured loss or liability could have a material adverse effect on our business, results of operations, cash flows and financial condition and our ability to pay dividends. It may also result in protracted legal litigation. In addition, we may not be able to obtain adequate insurance coverage at reasonable rates in the future during adverse insurance market conditions.

As a result of the September 11, 2001 terrorist attacks, the U.S. response to the attacks and related concern regarding terrorism, insurers have increased premiums and reduced or restricted coverage for losses caused by terrorist acts generally. Accordingly, premiums payable for terrorist coverage have increased substantially and the level of terrorist coverage has been significantly reduced.

In addition, we do not currently carry and may not carry loss-of-hire insurance, which covers the loss of revenue during extended vessel offhire periods, such as those that occur during an unscheduled drydocking due to damage to the vessel from accidents. Accordingly, any loss of a vessel or extended vessel off-hire, due to an accident or otherwise, could have a material adverse effect on our business, results of operations, financial condition and our ability to pay dividends.

We may be subject to funding calls by our protection and indemnity clubs, and our clubs may not have enough resources to cover claims made against them.

We are indemnified for legal liabilities incurred while operating our vessel through membership of protection and indemnity, or P&I, associations, otherwise known as P&I clubs. P&I clubs are mutual insurance clubs whose members must contribute to cover losses sustained by other club members. The objective of a P&I club is to provide mutual insurance based on the aggregate tonnage of a member’s vessels entered into the club. Claims are paid through the aggregate premiums of all members of the club, although members remain subject to calls for additional funds if the aggregate premiums are insufficient to cover claims submitted to the club. Claims submitted to the club may include those incurred by members of the club, as well as claims submitted by other P&I clubs with which our club has entered into interclub agreements. We cannot assure you that the P&I club to which we belong will remain viable or that we will not become subject to additional funding calls which could adversely affect us.

There are increased inspection procedures, tighter import and export controls and new security regulations.

International shipping is subject to various security and customs inspection and related procedures in countries of origin and destination and trans-shipment points. Inspection procedures can result in the seizure of the cargo and contents of our vessels, delays in the loading, offloading or delivery and the levying of customs duties, fines or other penalties against us.

It is possible that changes to inspection procedures could impose additional financial and legal obligations on us. Furthermore, changes to inspection procedures could also impose additional costs and obligations on our customers and may, in certain cases, render the shipment of certain types of cargo impractical. Any such changes or developments may have a material adverse effect on our business, financial condition, results of operations and our ability to pay dividends.

Rising fuel prices may adversely affect our profits.

While we currently have no charters under which we are bearing the cost of fuel (bunkers), fuel is a significant, if not the largest, expense if vessels are under voyage charter. Moreover, the cost of fuel will affect the profit we can earn on the spot market. Upon redelivery of vessels at the end of a time charter, we may be obliged to repurchase the fuel on board at prevailing market prices, which could be materially higher than fuel prices at the inception of the time charter period. As a result, an increase in the price of fuel may adversely affect our profitability. The price and supply of fuel is unpredictable and fluctuates based on events outside our control, including geopolitical events, supply and demand for oil and gas, actions by the Organization of the Petroleum Exporting Countries and other oil and gas producers, war and unrest in oil producing countries and regions, regional production patterns and environmental concerns. Further, fuel may become much more expensive in the future, which may reduce the profitability and competitiveness of our business versus other forms of transportation, such as truck or rail.

The operation of dry bulk vessels has certain unique operational risks.

The operation of certain vessel types, such as dry bulk vessels, has certain unique risks. With a dry bulk vessel, the cargo itself and its interaction with the vessel can be a risk factor. By their nature, dry bulk cargoes are often heavy, dense, easily shifted, and react badly to water exposure. In addition, dry bulk vessels are often subjected to battering during unloading operations with grabs, jackhammers (to pry encrusted cargoes out of the hold), and small bulldozers. This may cause damage to the vessel. Vessels damaged due to treatment during unloading procedures may be more susceptible to breach while at sea. Hull breaches in dry bulk vessels may lead to the flooding of the vessels holds. If a dry bulk vessel suffers flooding in its forward holds, the bulk cargo may become so dense and waterlogged that its pressure may buckle the vessels bulkheads leading to the loss of a vessel. If we are unable to adequately maintain our vessel we may be unable to prevent these events. Any of these circumstances or events could negatively impact our business, financial condition, results of operations and ability to pay dividends. In addition, the loss of any of our vessels could harm our reputation as a safe and reliable vessel owner and operator.

Maritime claimants could arrest our vessels, which would interrupt our business.

Crew members, suppliers of goods and services to a vessel, shippers of cargo and other parties may be entitled to a maritime lien against a vessel, or other assets of the relevant vessel-owning company, for unsatisfied debts, claims or damages. In many jurisdictions, a claimant may seek to obtain security for its claim by arresting a vessel through foreclosure proceedings. The arrest or attachment of one or more of our vessels, or other assets of the relevant vessel-owning company or companies, could cause us to default on a charter, breach covenants in our credit facility and loan agreement, interrupt our cash flow and require us to pay large sums of money to have the arrest or attachment lifted.

In addition, in some jurisdictions, such as South Africa, under the “sister ship” theory of liability, a claimant may arrest both the vessel which is subject to the claimant’s maritime lien and any “associated” vessel, which is any vessel owned or controlled by the same owner. Claimants could attempt to assert “sister ship” liability against one vessel in our fleet for claims relating to another of our vessels.

Governments could requisition our vessels during a period of war or emergency.

A government could requisition one or more of our vessels for title or for hire. Requisition for title occurs when a government takes control of a vessel and becomes the owner. Requisition for hire occurs when a government takes control of a vessel and effectively becomes the charterer at dictated charter rates. Generally, requisitions occur during a period of war or emergency, although governments may elect to requisition vessels in other circumstances. Even if we would be entitled to compensation in the event of a requisition of one or more of our vessels, the amount and timing of payment would be uncertain. Government requisition of one or more of our vessels may negatively impact our business, financial condition, results of operations and ability to pay dividends.

World events could affect our results of operations and financial condition.

Terrorist attacks such as the attacks on the United States on September 11, 2001, in London on July 7, 2005 and in Mumbai on November 26, 2008 and the continuing response of the United States and others to these attacks, as well as the threat of future terrorist attacks in the United States or elsewhere, continues to cause uncertainty in the world’s financial markets and may affect our business, operating results and financial condition. The continuing presence of United States and other armed forces in Iraq and Afghanistan may lead to additional acts of terrorism and armed conflict around the world, which may contribute to further economic instability in the global financial markets. These uncertainties could also adversely affect our ability to obtain additional financing on terms acceptable to us or at all. In the past, political conflicts have also resulted in attacks on vessels, mining of waterways and other efforts to disrupt international shipping, particularly in the Arabian Gulf region. Acts of terrorism have also affected vessels. Any of these occurrences could have a material adverse impact on our operating results, revenues, costs and ability to pay dividends.

Terrorist attacks on vessels, such as the October 2002 attack on the m.v. Limburg and the July 2010 alleged Al-Qaeda attack on the M. Star , both very large crude carriers not related to us, may in the future also negatively affect our operations and financial condition and directly impact our vessels or our customers. Future terrorist attacks could result in increased volatility and turmoil of the financial markets in the United States and globally. Any of these occurrences could have a material adverse impact on our operating results, revenues, costs and ability to pay dividends.

Acts of piracy on ocean-going vessels have recently increased in frequency.

Acts of piracy have historically affected ocean-going vessels trading in regions of the world such as the South China Sea and in the Gulf of Aden off the coast of Somalia. Throughout 2008 and 2009, the frequency of piracy incidents has increased significantly, particularly in the Gulf of Aden off the coast of Somalia. If these piracy attacks result in regions in which our vessels are deployed being characterized by insurers as “war risk” zones, as the Gulf of Aden temporarily was in May 2008, or Joint War Committee “war and strikes” listed areas, premiums payable for such coverage could increase significantly and such insurance coverage may be more difficult or impossible to obtain. In addition, crew costs, including employing onboard security guards, could increase in such circumstances. We may not be adequately insured to cover losses from these incidents, which could have a material adverse effect on us. In addition, detention hijacking as a result of an act of piracy against our vessel, or an increase in cost, or unavailability of insurance for our vessels, could have a material adverse impact on our business, financial condition, results of operations and ability to pay dividends.

Disruptions in world financial markets and the resulting governmental action in the United States and in other parts of the world could affect us.

The United States and other parts of the world are exhibiting deteriorating economic trends and have been in a recession. For example, the credit markets in the United States have experienced significant contraction, deleveraging and reduced liquidity, and the United States federal government and state governments have implemented and are considering a broad variety of governmental action and/or new regulation of the financial markets. Securities and futures markets and the credit markets are subject to comprehensive statutes, regulations and other requirements. The Securities and Exchange Commission, which we refer to as the SEC, other regulators, self-regulatory organizations and exchanges are authorized to take extraordinary actions in the event of market emergencies, and may effect changes in law or interpretations of existing laws.

A number of financial institutions have experienced serious financial difficulties and, in some cases, have entered bankruptcy proceedings or are in regulatory enforcement actions. The uncertainty surrounding the future of the credit markets in the United States and the rest of the world has resulted in reduced access to credit worldwide.

We face risks attendant to changes in economic environments, changes in interest rates and instability in the banking and securities markets around the world, among other factors. Major market disruptions and the current adverse changes in market conditions and regulatory climate in the United States and worldwide may adversely affect our business or impair our ability to borrow amounts under any future financial arrangements. We cannot predict how long the current market conditions will last. However, these recent and developing economic and governmental factors, together with the concurrent decline in charter rates and vessel values, may have a material adverse effect on our results of operations, financial condition, cash flows and ability to pay dividends.

Compliance with safety and other vessel requirements imposed by classification societies may be costly.

The hull and machinery of every commercial vessel must be certified as safe and seaworthy in accordance with applicable rules and regulations, and accordingly vessels must undergo regular surveys. If any vessel does not maintain its class and/or fails any annual survey, intermediate survey or special survey, the vessel will be unable to trade between ports and will be unemployable and this would negatively impact our revenues.

Vessels must undergo annual surveys, immediate surveys and special surveys. In lieu of a special survey, a vessel’s machinery may be on a continuous survey cycle, under which the machinery would be surveyed over a five-year period. Our vessels are on special survey cycles for hull inspection and continuous survey cycles for machinery inspection. Every vessel is also required to be drydocked every two to three years for inspection of its underwater parts.

If any vessel does not maintain its class and/or fails any annual, intermediate or special survey, the vessel may be unable to trade between ports and may be unemployable which could have a material adverse impact on our business, financial condition, results of operations and ability to pay dividends.

The smuggling of drugs or other contraband onto our vessels may lead to governmental claims against us.

We expect that our vessels will call at ports where smugglers may attempt to hide drugs and other contraband on vessels, with or without the knowledge of crew members. To the extent that our vessels are found with contraband, whether inside or attached to the hull of our vessel, and whether with or without the knowledge of any of our crew, we may face governmental or other regulatory claims that could have an adverse effect on our business, results of operations, cash flows, financial condition and ability to pay dividends.

Risks Related To Company’s Management and Key Personnel

We will depend upon key individuals who may terminate their employment or other relationship with us or Boston Carriers at any time, and Boston Carriers will need to hire additional qualified personnel which may be unavailable due to the necessity of unique skills and resources

Our success will depend to a significant degree upon the continued services of our sole officer, Mr. Antonios Bertsos (age 41).

We do not have “key person” life insurance for Mr. Bertsos. In addition, our success will depend on Boston Carrier’s ability to attract and retain other highly skilled personnel. Competition for qualified personnel is intense, and the process of hiring and integrating such qualified personnel is often lengthy. Boston Carriers may be unable to recruit such personnel on a timely basis, if at all. We have not entered into an employment agreement with Mr. Bertsos. Accordingly, Mr. Bertsos, will have the ability to resign from the Company and voluntarily terminate his employment at any time. The loss of the services of key personnel, or the inability to attract and retain additional qualified personnel, could result in delays to development or approval, loss of sales and diversion of management resources.

The common shares of the Company are considered “a penny stock” and may be difficult to trade.