Management Discussion & Analysis

Management Discussion & Analysis Management of Algonquin Power & Utilities Corp. (“AQN” or the “Company” or the “Corporation”) has prepared the following discussion and analysis to provide information to assist its securityholders’ understanding of the financial results for the three and six months ended June 30, 2023. This Management Discussion & Analysis (“MD&A”) should be read in conjunction with AQN’s unaudited interim consolidated financial statements for the three and six months ended June 30, 2023 and 2022. This MD&A should also be read in conjunction with AQN's annual consolidated financial statements for the years ended December 31, 2022 and 2021. This material is available on SEDAR at www.sedar.com, on EDGAR at www.sec.gov/edgar, and on the AQN website at www.AlgonquinPowerandUtilities.com. Additional information about AQN, including the most recent Annual Information Form (“AIF”), can be found on SEDAR at www.sedar.com and on EDGAR at www.sec.gov/edgar.

Unless otherwise indicated, financial information provided for the three and six months ended June 30, 2023 and 2022 has been prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”). As a result, the Company's financial information may not be comparable with financial information of other Canadian companies that provide financial information on another basis.

All monetary amounts are in U.S. dollars, except where otherwise noted. We denote any amounts denominated in Canadian dollars with "C$" immediately prior to the stated amount.

Capitalized terms used herein and not otherwise defined have the meanings assigned to them in the Company's most recent AIF.

Unless noted otherwise, this MD&A is based on information available to management as of August 10, 2023.

Contents

| Caution Concerning Forward-Looking Statements and Forward-Looking Information | |||||

| Caution Concerning Non-GAAP Measures | |||||

| Overview and Business Strategy | |||||

| Significant Updates | |||||

| 2023 Second Quarter Results From Operations | |||||

| 2023 Year-to-Date Results from Operations | |||||

| 2023 Second Quarter and Year-to-Date Net Earnings Summary | |||||

| 2023 Second Quarter and Year-to-Date Adjusted EBITDA Summary | |||||

| Regulated Services Group | |||||

| Renewable Energy Group | |||||

| AQN: Corporate and Other Expenses | |||||

| Non-GAAP Financial Measures | |||||

| Summary of Property, Plant and Equipment Expenditures | |||||

| Liquidity and Capital Reserves | |||||

| Share-Based Compensation Plans | |||||

| Related Party Transactions | |||||

| Enterprise Risk Management | |||||

| Quarterly Financial Information | |||||

| Disclosure Controls and Procedures | |||||

| Critical Accounting Estimates and Policies | |||||

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 1 | ||||

Caution Concerning Forward-Looking Statements and Forward-Looking Information

This document may contain statements that constitute "forward-looking information" within the meaning of applicable securities laws in each of the provinces and territories of Canada and the respective policies, regulations and rules under such laws or "forward-looking statements" within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 (collectively, “forward-looking information”). The words "aims", “anticipates”, “believes”, “budget”, “could”, “estimates”, “expects”, “forecasts”, “intends”, “may”, “might”, “plans”, “projects”, “schedule”, “should”, “will”, “would”, "seeks", "strives", "targets" (and grammatical variations of such terms) and similar expressions are often intended to identify forward-looking information, although not all forward-looking information contains these identifying words. Specific forward-looking information in this document includes, but is not limited to, statements relating to: expected future growth, earnings and results of operations; the sale of the Renewable Energy Group and the anticipated impact thereof on the Corporation; liquidity, capital resources and operational requirements; sources of funding, including adequacy and availability of credit facilities, cash flows from operations, capital markets financing, and asset recycling or asset sales initiatives; ongoing and planned acquisitions, dispositions, projects, initiatives or other transactions, including expectations regarding timing, costs, proceeds, financing, results, ownership structures, regulatory matters, in-service dates and completion dates; financing plans, including the Company's expectation that it will not undertake any new common equity financing through the end of 2024; expectations regarding future macroeconomic conditions; expectations regarding the Company's corporate development activities and the results thereof; the expected redemption of the Company's remaining outstanding Series C preferred shares on or before August 11, 2023; expectations regarding regulatory hearings, motions, filings, appeals and approvals, including rate reviews, and the timing, impacts and outcomes thereof; expected future generation, capacity and production of the Company’s energy facilities; expectations regarding future capital investments, including expected timing, investment plans, sources of funds and impacts; expectations regarding the outcome of legal claims and disputes; strategy and goals; dividends to shareholders, including expectations regarding the sustainability thereof and the Company's ability to achieve its targeted annual dividend payout ratio; expectations regarding future "greening the fleet" initiatives; credit ratings and equity credit from rating agencies; expectations regarding debt repayment and refinancing; the future impact on the Company of actual or proposed laws, regulations and rules; the expected impact of changes in customer usage on the Regulated Services Group’s revenue; accounting estimates; interest rates, including the anticipated effect of an increase thereof; the implementation of new technology systems and infrastructure, including the expected timing thereof; financing costs; and currency exchange rates. All forward-looking information is given pursuant to the “safe harbour” provisions of applicable securities legislation.

The forecasts and projections that make up the forward-looking information contained herein are based on certain factors or assumptions which include, but are not limited to: the receipt of applicable regulatory approvals and requested rate decisions; the absence of material adverse regulatory decisions being received and the expectation of regulatory stability; the absence of any material equipment breakdown or failure; availability of financing (including tax equity financing and self-monetization transactions for U.S. federal tax credits) on commercially reasonable terms and the stability of credit ratings of the Corporation and its subsidiaries; the absence of unexpected material liabilities or uninsured losses; the continued availability of commodity supplies and stability of commodity prices; the absence of interest rate increases or significant currency exchange rate fluctuations; the absence of significant operational, financial or supply chain disruptions or liability, including relating to import controls and tariffs; the continued ability to maintain systems and facilities to ensure their continued performance; the absence of a severe and prolonged downturn in general economic, credit, social or market conditions; the successful and timely development and construction of new projects; the closing of pending acquisitions substantially in accordance with the expected timing for such acquisitions; the absence of capital project or financing cost overruns; sufficient liquidity and capital resources; the continuation of long term weather patterns and trends; the absence of significant counterparty defaults; the continued competitiveness of electricity pricing when compared with alternative sources of energy; the realization of the anticipated benefits of the Corporation’s acquisitions and joint ventures; the absence of a change in applicable laws, political conditions, public policies and directions by governments materially negatively affecting the Corporation; the ability to obtain and maintain licenses and permits; maintenance of adequate insurance coverage; the absence of material fluctuations in market energy prices; the absence of material disputes with taxation authorities or changes to applicable tax laws; continued maintenance of information technology infrastructure and the absence of a material breach of cybersecurity; the successful implementation of new information technology systems and infrastructure; favourable relations with external stakeholders; favourable labour relations; that the Corporation will be able to successfully integrate newly acquired entities, and the absence of any material adverse changes to such entities prior to closing; the absence of undisclosed liabilities of entities being acquired; that such entities will maintain constructive regulatory relationships with applicable regulatory authorities; the ability of the Corporation to retain key personnel of acquired entities and the value of such employees; no adverse developments in the business and affairs of the sellers during the period when transitional services are provided to the Corporation in connection with any acquisition; the ability of the Corporation to satisfy its liabilities and meet its debt service obligations following completion of any acquisition; and the ability of the Corporation to successfully execute future “greening the fleet” initiatives; and the ability of the Corporation to effect a sale of the Renewable Energy Group and realize the anticipated benefits therefrom.

The forward-looking information contained herein is subject to risks, uncertainties and other factors that could cause actual results to differ materially from historical results or results anticipated by the forward-looking information. Factors which

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 2 | ||||

could cause results or events to differ materially from current expectations include, but are not limited to: changes in general economic, credit, social or market conditions; changes in customer energy usage patterns and energy demand; reductions in the liquidity of energy markets; global climate change; the incurrence of environmental liabilities; natural disasters, diseases, pandemics, public health emergencies and other force majeure events and the collateral consequences thereof, including the disruption of economic activity, volatility in capital and credit markets and legislative and regulatory responses; critical equipment breakdown or failure; supply chain disruptions; the imposition of import controls or tariffs; the failure of information technology infrastructure and other cybersecurity measures to protect against data, privacy and cybersecurity breaches; failure to successfully implement, and cost overruns and delays in connection with, new information technology systems and infrastructure; physical security breach; the loss of key personnel and/or labour disruptions; seasonal fluctuations and variability in weather conditions and natural resource availability; reductions in demand for electricity, natural gas and water due to developments in technology; reliance on transmission systems owned and operated by third parties; issues arising with respect to land use rights and access to the Corporation’s facilities; terrorist attacks; fluctuations in commodity and energy prices; capital expenditures; reliance on subsidiaries; the incurrence of an uninsured loss; a credit rating downgrade; an increase in financing costs or limits on access to credit and capital markets; inflation; increases and fluctuations in interest rates and failure to manage exposure to credit and financial instrument risk; currency exchange rate fluctuations; restricted financial flexibility due to covenants in existing credit agreements; an inability to refinance maturing debt on favourable terms; disputes with taxation authorities or changes to applicable tax laws; failure to identify, acquire, develop or timely place in service projects to maximize the value of tax credits; requirement for greater than expected contributions to post-employment benefit plans; default by a counterparty; inaccurate assumptions, judgments and/or estimates with respect to asset retirement obligations; failure to maintain required regulatory authorizations; changes in, or failure to comply with, applicable laws and regulations; failure of compliance programs; failure to identify attractive acquisition or development candidates necessary to pursue the Corporation’s growth strategy; failure to dispose of assets (at all or at a competitive price) to fund the Company’s operations and growth plans; delays and cost overruns in the design and construction of projects; loss of key customers; failure to complete or realize the anticipated benefits of acquisitions or joint ventures; Atlantica (as defined herein) or a third party joint venture partner acting in a manner contrary to the Corporation’s interests; a drop in the market value of Atlantica's ordinary shares; facilities being condemned or otherwise taken by governmental entities; increased external stakeholder activism adverse to the Corporation’s interests; fluctuations in the price and liquidity of the Corporation’s common shares and the Corporation's other securities; impact of significant demands placed on the Corporation as a result of pending acquisitions or growth strategies; potential undisclosed liabilities of any entities being acquired by the Corporation; uncertainty regarding the length of time required to complete pending acquisitions; the failure to implement the Corporation’s strategic objectives or achieve expected benefits relating to acquisitions, dispositions or other initiatives, including with respect to the intended sale of the Renewable Energy Group; the possibility of adverse reactions or changes in business relationships or relationships with employees resulting from the announcement or completion of the intended sale of the Renewable Energy Group; risks relating to the diversion of the Board’s (as defined herein) or management’s attention in connection with the intended sale of the Renewable Energy Group; indebtedness of any entity being acquired by the Corporation; unanticipated expenses and/or cash payments as a result of change of control and/or termination provisions in purchase or sale agreements; and the reliance on third parties for certain transitional services following the completion of an acquisition. Although the Corporation has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking information, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. Some of these and other factors are discussed in more detail under the heading Enterprise Risk Management in this MD&A and in the Corporation’s MD&A for the three and twelve months ended December 31, 2022 (the “Annual MD&A”), and under the heading Enterprise Risk Factors in the Corporation's most recent AIF.

Forward-looking information contained herein (including any financial outlook) is provided for the purposes of assisting the reader in understanding the Corporation and its business, operations, risks, financial performance, financial position and cash flows as at and for the periods indicated and to present information about management’s current expectations and plans relating to the future, and the reader is cautioned that such information may not be appropriate for other purposes. Forward-looking information contained herein is made as of the date of this document and based on the plans, beliefs, estimates, projections, expectations, opinions and assumptions of management on the date hereof. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such forward-looking information. Accordingly, readers should not place undue reliance on forward-looking information. While subsequent events and developments may cause the Corporation’s views to change, the Corporation disclaims any obligation to update any forward-looking information or to explain any material difference between subsequent actual events and such forward-looking information, except to the extent required by applicable law. All forward-looking information contained herein is qualified by these cautionary statements.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |||||

Caution Concerning Non-GAAP Measures

AQN uses a number of financial measures to assess the performance of its business lines. Some measures are calculated in accordance with U.S. GAAP, while other measures do not have a standardized meaning under U.S. GAAP. These non-GAAP measures include non-GAAP financial measures and non-GAAP ratios, each as defined in Canadian National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. AQN’s method of calculating these measures may differ from methods used by other companies and therefore may not be comparable to similar measures presented by other companies.

The terms “Adjusted Net Earnings”, “Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization” (“Adjusted EBITDA”), “Adjusted Funds from Operations”, "Net Energy Sales", "Net Utility Sales" and "Divisional Operating Profit", which are used throughout this MD&A, are non-GAAP financial measures. An explanation of each of these non-GAAP financial measures is set out below and a reconciliation to the most directly comparable U.S. GAAP measure, in each case, can be found in this MD&A. In addition, “Adjusted Net Earnings” is presented throughout this MD&A on a per common share basis. Adjusted Net Earnings per common share is a non-GAAP ratio and is calculated by dividing Adjusted Net Earnings by the weighted average number of common shares outstanding during the applicable period.

AQN does not provide reconciliations for forward-looking non-GAAP financial measures as AQN is unable to provide a meaningful or accurate calculation or estimation of reconciling items and the information is not available without unreasonable effort. This is due to the inherent difficulty of forecasting the timing or amount of various events that have not yet occurred, are out of AQN’s control and/or cannot be reasonably predicted, and that would impact the most directly comparable forward-looking U.S. GAAP financial measure. For these same reasons, AQN is unable to address the probable significance of the unavailable information. Forward-looking non-GAAP financial measures may vary materially from the corresponding U.S. GAAP financial measures.

The compositions of Adjusted EBITDA, Adjusted Net Earnings, Adjusted Funds from Operations, and Divisional Operating Profit have been changed from those previously disclosed in the Annual MD&A to exclude gains and losses on disposition of assets. This change was made as gains and losses on disposition of assets are no longer used by management to evaluate the operating performance of the Company. Comparative figures for these metrics have been adjusted for the new compositions.

Adjusted EBITDA

Adjusted EBITDA is a non-GAAP financial measure used by many investors to compare companies on the basis of ability to generate cash from operations. AQN uses these calculations to monitor the amount of cash generated by AQN. AQN uses Adjusted EBITDA to assess the operating performance of AQN without the effects of (as applicable): depreciation and amortization expense, income tax expense or recoveries, acquisition and transition costs (including costs related to the strategic review of the Renewable Energy Group), certain litigation expenses, interest expense, gain or loss on derivative financial instruments, write down of intangibles and property, plant and equipment, earnings attributable to non-controlling interests exclusive of Hypothetical Liquidation at Book Value ("HLBV") income (which represents the value of net tax attributes earned in the period from electricity generated by certain of its U.S. wind power and U.S. solar generation facilities), non-service pension and post-employment costs, cost related to tax equity financing, costs related to management succession and executive retirement, costs related to prior period adjustments due to changes in tax law, costs related to condemnation proceedings, gain or loss on foreign exchange, earnings or loss from discontinued operations, changes in value of investments carried at fair value, gains and losses on disposition of assets, and other typically non-recurring or unusual items. AQN adjusts for these factors as they may be non-cash, unusual in nature and are not factors used by management for evaluating the operating performance of the Company. AQN believes that presentation of this measure will enhance an investor’s understanding of AQN’s operating performance. Adjusted EBITDA is not intended to be representative of cash provided by operating activities or results of operations determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of Adjusted EBITDA to net earnings, see Non-GAAP Financial Measures starting on page 33 of this MD&A.

Adjusted Net Earnings

Adjusted Net Earnings is a non-GAAP financial measure used by many investors to compare net earnings from operations without the effects of certain volatile primarily non-cash items that generally have no current economic impact or items such as acquisition expenses or certain litigation expenses that are viewed as not directly related to a company’s operating performance. AQN uses Adjusted Net Earnings to assess its performance without the effects of (as applicable): gains or losses on foreign exchange, foreign exchange forward contracts, interest rate swaps, acquisition and transition costs (including costs related to the strategic review of the Renewable Energy Group), one-time costs of arranging tax equity financing, certain litigation expenses and write down of intangibles and property, plant and equipment, earnings or loss from discontinued operations, unrealized mark-to-market revaluation impacts, costs related to management succession and executive retirement, costs related to prior period adjustments due to changes in tax law, costs related to condemnation proceedings, changes in value of investments carried at fair value, gains and losses on disposition of assets, and other typically non-recurring or unusual items as these are not reflective of the performance of the underlying business of AQN.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 4 | ||||

AQN believes that analysis and presentation of net earnings or loss on this basis will enhance an investor’s understanding of the operating performance of its businesses. Adjusted Net Earnings is not intended to be representative of net earnings or loss determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of Adjusted Net Earnings to net earnings, see Non-GAAP Financial Measures starting on page 34 of this MD&A.

Adjusted Funds from Operations

Adjusted Funds from Operations is a non-GAAP financial measure used by investors to compare cash provided by operating activities without the effects of certain volatile items that generally have no current economic impact or items such as acquisition expenses that are viewed as not directly related to a company’s operating performance. AQN uses Adjusted Funds from Operations to assess its performance without the effects of (as applicable): changes in working capital balances, acquisition and transition costs, certain litigation expenses, cash provided by or used in discontinued operations, cash provided by disposition of assets and other typically non-recurring items affecting cash from operations as these are not reflective of the long-term performance of the underlying businesses of AQN. AQN believes that analysis and presentation of funds from operations on this basis will enhance an investor’s understanding of the operating performance of its businesses. Adjusted Funds from Operations is not intended to be representative of cash provided by operating activities as determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of Adjusted Funds from Operations to cash provided by operating activities, see Non-GAAP Financial Measures starting on page 35 of this MD&A.

Net Energy Sales

Net Energy Sales is a non-GAAP financial measure used by investors to identify revenue after commodity costs used to generate revenue where such revenue generally increases or decreases in response to increases or decreases in the cost of the commodity used to produce that revenue. AQN uses Net Energy Sales to assess its revenues without the effects of fluctuating commodity costs as such costs are predominantly passed through either directly or indirectly in the rates that are charged to customers. AQN believes that analysis and presentation of Net Energy Sales on this basis will enhance an investor’s understanding of the revenue generation of the Renewable Energy Group. It is not intended to be representative of revenue as determined in accordance with U.S. GAAP. For a reconciliation of Net Energy Sales to revenue, see Renewable Energy Group - 2023 Second Quarter and Year-to-Date Renewable Energy Group Operating Results on page 28 of this MD&A.

Net Utility Sales

Net Utility Sales is a non-GAAP financial measure used by investors to identify utility revenue after commodity costs, either water, natural gas or electricity, where these commodity costs are generally included as a pass through in rates to its utility customers. AQN uses Net Utility Sales to assess its utility revenues without the effects of fluctuating commodity costs as such costs are predominantly passed through and paid for by utility customers. AQN believes that analysis and presentation of Net Utility Sales on this basis will enhance an investor’s understanding of the revenue generation of the Regulated Services Group. It is not intended to be representative of revenue as determined in accordance with U.S. GAAP. For a reconciliation of Net Utility Sales to revenue, see Regulated Services Group - 2023 Second Quarter and Year-to-Date Regulated Services Group Operating Results on page 19 of this MD&A.

Divisional Operating Profit

Divisional Operating Profit is a non-GAAP financial measure. AQN uses Divisional Operating Profit to assess the operating performance of its business groups without the effects of (as applicable): depreciation and amortization expense, corporate administrative expenses, income tax expense or recoveries, acquisition costs, certain litigation expenses, interest expense, gain or loss on derivative financial instruments, write down of intangibles and property, plant and equipment, gain or loss on foreign exchange, earnings or loss from discontinued operations (excluding the sale of assets in the course of normal operations), non-service pension and post-employment costs, gains and losses on disposition of assets, and other typically non-recurring or unusual items. AQN adjusts for these factors as they may be non-cash, unusual in nature and are not factors used by management for evaluating the operating performance of the divisional units. Divisional Operating Profit is calculated inclusive of interest, dividend and equity income earned from indirect investments, and HLBV income. AQN believes that presentation of this measure will enhance an investor’s understanding of AQN’s divisional operating performance. Divisional Operating Profit is not intended to be representative of cash provided by operating activities or results of operations determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of Divisional Operating Profit to revenue for AQN's main business units, see Regulated Services Group - 2023 Second Quarter and Year-to-Date Regulated Services Group Operating Results on page 19 and Renewable Energy Group - 2023 Second Quarter and Year-to-Date Renewable Energy Group Operating Results on page 28 of this MD&A.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |||||

Overview and Business Strategy

AQN is incorporated under the Canada Business Corporations Act. AQN owns and operates a diversified portfolio of regulated and non-regulated generation, distribution, and transmission assets which are expected to deliver predictable earnings and cash flows. Through its activities, the Company aims to drive growth in earnings and cash flows to support a sustainable dividend and share price appreciation. AQN strives to achieve these results while also seeking to maintain a business risk profile consistent with its BBB flat investment grade credit ratings and a strong focus on Environmental, Social and Governance factors.

AQN's current quarterly dividend to shareholders is $0.1085 per common share, or $0.4340 per common share on an annualized basis. AQN believes that, on a long-term basis, its targeted annual dividend payout will allow for both a return on investment for shareholders and retention of cash within AQN to partially fund growth opportunities. Changes in the level of dividends paid by AQN are at the discretion of AQN’s Board of Directors (the “Board”), with dividend levels being reviewed periodically by the Board in the context of AQN’s financial performance and growth prospects.

AQN’s operations are organized across two primary business units consisting of: the Regulated Services Group, which primarily owns and operates a portfolio of regulated assets in the United States, Canada, Bermuda and Chile; and the Renewable Energy Group, which primarily operates a diversified portfolio of owned renewable generation assets.

On May 11, 2023, the Company announced that the Board had initiated a strategic review of the Renewable Energy Group. To oversee the strategic review process, the Board formed a Strategic Review Committee, comprised of directors Chris Huskilson (Chair), Amee Chande and Dan Goldberg. On August 10, 2023, the Company announced that it will pursue a sale of the Renewable Energy Group.

Summary Structure of the Business

The following chart depicts, in summary form, AQN’s key businesses. A more detailed description of AQN’s organizational structure can be found in the most recent AIF.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 6 | ||||

Regulated Services Group

The Regulated Services Group operates a diversified portfolio of regulated utility systems located in the United States, Canada, Bermuda and Chile serving approximately 1,256,000 customer connections as at June 30, 2023 (using an average of 2.5 customers per connection, this translates into approximately 3,140,000 customers). The Regulated Services Group seeks to provide safe, high quality, and reliable services to its customers and to deliver stable and predictable earnings to AQN. In addition to encouraging and supporting organic growth within its service territories, the Regulated Services Group may seek to deliver long-term growth through accretive acquisitions of additional utility systems and pursuing "greening the fleet" opportunities.

The Regulated Services Group's regulated electrical distribution utility systems and related generation assets are located in the U.S. States of California, New Hampshire, Missouri, Kansas, Oklahoma, and Arkansas, as well as in Bermuda, which together served approximately 309,000 electric customer connections as at June 30, 2023. The group also owns and operates generating assets with a gross capacity of approximately 2.0 GW and has investments in generating assets with approximately 0.3 GW of net generation capacity.

The Regulated Services Group's regulated water distribution and wastewater collection utility systems are located in the U.S. States of Arizona, Arkansas, California, Illinois, Missouri, New York, and Texas as well as in Chile which together served approximately 571,000 customer connections as at June 30, 2023.

The Regulated Services Group's regulated natural gas distribution utility systems are located in the U.S. States of Georgia, Illinois, Iowa, Massachusetts, New Hampshire, Missouri, and New York, and in the Canadian Province of New Brunswick, which together served approximately 376,000 natural gas customer connections as at June 30, 2023.

Below is a breakdown of the Regulated Services Group’s Revenue by geographic area for the six months ended June 30, 2023.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |||||

Renewable Energy Group

The Renewable Energy Group generates and sells electrical energy produced by its diverse portfolio of renewable power generation and clean power generation facilities primarily located across the United States and Canada. The Renewable Energy Group seeks to deliver growth through new power generation projects and complementary projects, such as energy storage.

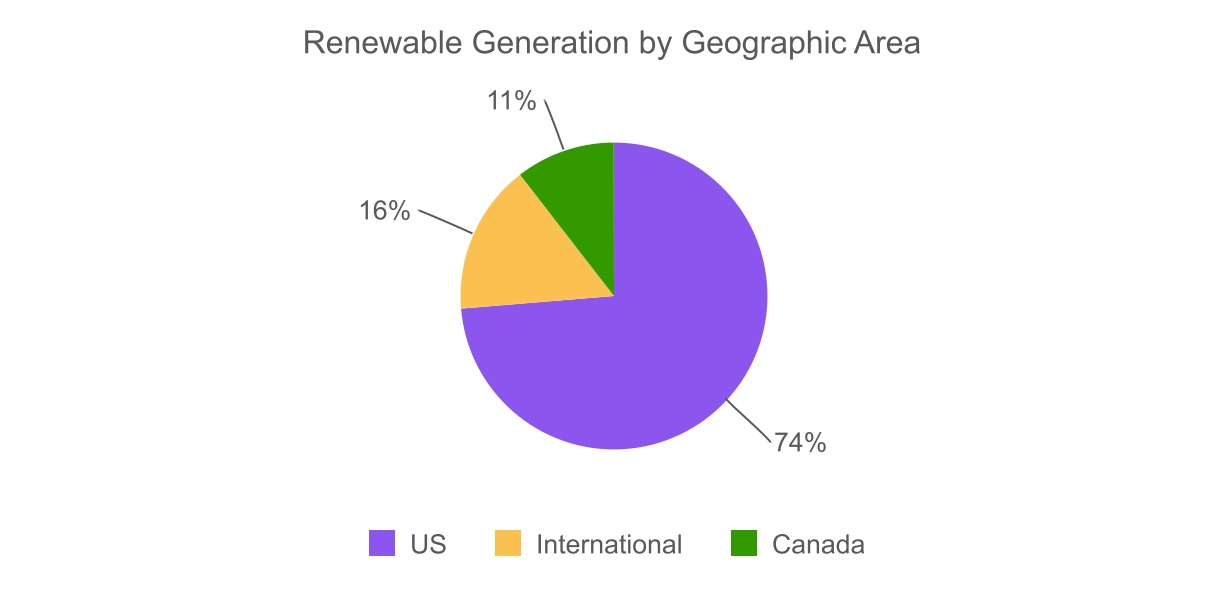

The Renewable Energy Group has a controlling interest in hydroelectric, wind, solar, renewable natural gas ("RNG") and thermal facilities with a combined gross generating capacity of approximately 2.5 GW and a net generating capacity (attributable to the Renewable Energy Group) of approximately 2.2 GW. Approximately 81% of the electrical output is sold pursuant to long term contractual arrangements which as of June 30, 2023 had a production-weighted average remaining contract life of approximately 10 years.

In addition to the assets in which the Renewable Energy Group has a controlling interest, the Renewable Energy Group has investments in generating assets with approximately 1.5 GW of net generating capacity, which includes the Company’s 51% interest in the Texas Coastal Wind Facilities (as defined herein) and approximately 42% interest in Atlantica Sustainable Infrastructure plc (“Atlantica”). Atlantica owns and operates a portfolio of international clean energy and water infrastructure assets under long term contracts with a Cash Available for Distribution weighted average remaining contract life of approximately 13 years as of June 30, 2023. Of the generating assets that the Renewable Energy Group has an interest in, the Renewable Energy Group operates assets with a net generating capacity of 2.7 GW.

Below is a breakdown of the Renewable Energy Group’s generating capacity by geographic area as of June 30, 2023, which was comprised of net generating capacity of facilities owned and operated and net generating capacity of investments, including the Company’s 51% interest in the Texas Coastal Wind Facilities and approximately 42% interest in Atlantica.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |||||

Significant Updates

Operating Results

AQN's operating results relative to the same period last year are as follows:

| (all dollar amounts in $ millions except per share information) | Three months ended June 30 | ||||||||||||||||

| 2023 | 2022 | Change | |||||||||||||||

| Net loss attributable to shareholders | $(253.2) | $(33.4) | (658)% | ||||||||||||||

Adjusted Net Earnings1 | $56.2 | $109.6 | (49)% | ||||||||||||||

Adjusted EBITDA1 | $277.7 | $289.2 | (4)% | ||||||||||||||

| Net loss per common share | $(0.37) | $(0.05) | (640)% | ||||||||||||||

Adjusted Net Earnings per common share1 | $0.08 | $0.16 | (50)% | ||||||||||||||

| 1 | See Caution Concerning Non-GAAP Measures. | ||||

CEO Succession

Effective August 10, 2023, Chris Huskilson, a member of the Board since 2020, was appointed Interim Chief Executive Officer of AQN. He succeeds Arun Banksota, who stepped down as President and Chief Executive Officer of AQN and as a member of the Board effective August 10, 2023.

The Board has engaged a nationally recognized search firm to commence a search process to identify a permanent Chief Executive Officer.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 9 | ||||

2023 Second Quarter Results From Operations

Key Financial Information | Three months ended June 30 | ||||||||||

| (all dollar amounts in $ millions except per share information) | 2023 | 2022 | |||||||||

| Revenue | $ | 627.9 | $ | 619.4 | |||||||

| Net loss attributable to shareholders | (253.2) | (33.4) | |||||||||

| Cash provided by operating activities | 261.4 | 135.3 | |||||||||

Adjusted Net Earnings1 | 56.2 | 109.6 | |||||||||

Adjusted EBITDA1 | 277.7 | 289.2 | |||||||||

Adjusted Funds from Operations1 | 154.2 | 180.3 | |||||||||

| Dividends declared to common shareholders | 75.4 | 122.6 | |||||||||

| Weighted average number of common shares outstanding | 687,761,648 | 674,742,897 | |||||||||

| Per share | |||||||||||

| Basic net loss | $ | (0.37) | $ | (0.05) | |||||||

| Diluted net loss | $ | (0.37) | $ | (0.05) | |||||||

Adjusted Net Earnings1 | $ | 0.08 | $ | 0.16 | |||||||

| Dividends declared to common shareholders | $ | 0.11 | $ | 0.18 | |||||||

| 1 | See Caution Concerning Non-GAAP Measures. | ||||

For the three months ended June 30, 2023, AQN reported basic net loss per common share of $0.37 as compared to basic net loss per common share of $0.05 during the same period in 2022, a decrease of $0.32. This decrease was primarily driven by:

•the decrease in value of investments carried at fair value of $167.9 million primarily related to the Company's investment in Atlantica; and

•impairment of assets and other losses of $43.8 million incurred as a result of the termination of the stock purchase agreement regarding the acquisition of Kentucky Power Company and AEP Kentucky Transmission Company, Inc. (the "Kentucky Power Impairment").

For the three months ended June 30, 2023, AQN reported Adjusted Net Earnings per common share of $0.08 as compared to $0.16 per common share during the same period in 2022, a decrease of $0.08 (see Caution Concerning Non-GAAP Measures). Adjusted Net Earnings decreased by $53.4 million year over year (see Caution Concerning Non-GAAP Measures). This decrease was primarily driven by:

•a decrease of $17.6 million in the Renewable Energy Group's operating profit primarily as a result wind facilities generating 75.1% of Long Term Average Resource ("LTAR") which represents a 22.0% decrease compared to the same period in 2022;

•a decrease of $14.0 million in the Renewable Energy Group's HLBV income as a result of the end of production tax credit ("PTC") eligibility on projects commissioned in 2012;

•an increase in earnings attributable to minority interest, exclusive of HLBV, of $12.9 million primarily due to the Company's sale in the fourth quarter of 2022 of a 49% ownership interest in the Odell, Deerfield and Sugar Creek Wind Facilities;

•an increase in interest expense of $25.1 million, driven by higher interest rates as well as increased borrowings to support growth initiatives;

•an increase in depreciation expense of $5.9 million driven by additional capital invested by the Company; and

•an increase in administrative expenses of $5.6 million due to timing, foreign exchange, inflation and increased headcount to support growth initiatives; partially offset by

•an increase of $28.5 million in the Regulated Services Group's operating profit primarily due to implementation of new rates.

For the three months ended June 30, 2023, AQN experienced an average exchange rate of Canadian to U.S. dollars of approximately 0.7445 as compared to 0.7834 in the same period in 2022, and an average exchange rate of Chilean pesos to U.S. dollars of approximately 0.0012 for the three months ended June 30, 2023 as compared to 0.0012 for the same period in 2022. As such, any year over year variance in revenue or expenses, in local currency, at any of AQN’s Canadian and Chilean entities is affected by a change in the average exchange rate upon conversion to AQN’s reporting currency.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 10 | ||||

For the three months ended June 30, 2023, AQN reported total revenue of $627.9 million as compared to $619.4 million during the same period in 2022, an increase of $8.5 million or 1.4%. The major factors impacting AQN’s revenue in the three months ended June 30, 2023 as compared to the same period in 2022 are as follows:

| (all dollar amounts in $ millions) | Three months ended June 30 | ||||

| Comparative Prior Period Revenue | $ | 619.4 | |||

| REGULATED SERVICES GROUP | |||||

| Existing Facilities | |||||

Electricity: Decrease is primarily due to one-time insurance proceeds for the Neosho Ridge Facility received in 2022 and unfavourable weather at the Empire Electric System. | (17.2) | ||||

Natural Gas: Decrease is primarily due to lower pass through commodity costs. | (15.6) | ||||

| Water: Increase is primarily due to the inflationary rate increase mechanism at the Suralis Water System (formerly called the ESSAL Water System) and organic growth at the Litchfield Park and Gold Canyon Water Systems. | 5.0 | ||||

| Other: | (0.7) | ||||

| (28.5) | |||||

| Rate Reviews | |||||

| Electricity: Increase is primarily due to the implementation of new rates at the CalPeco Electric System with recoupment to the first quarter of 2022, as well as the implementation of new rates at the Empire, Bermuda Electric Light Company ("BELCO") and Granite State Electric Systems. | 50.1 | ||||

| Natural Gas: Increase is primarily due to the implementation of new rates at the EnergyNorth, New Brunswick, Peach State, St. Lawrence and Empire Gas Systems. | 2.6 | ||||

| Water: Increase is due to the implementation of new rates at the Park Water System. | 1.5 | ||||

| 54.2 | |||||

| Foreign Exchange | 1.1 | ||||

| RENEWABLE ENERGY GROUP | |||||

| Existing Facilities | |||||

| Hydro: Decrease is primarily driven by lower retail sales in the Maritimes Region, and lower production for the Ontario and Quebec regions. | (2.1) | ||||

| Wind CA: Decrease is primarily due to lower production across the majority of the Canadian wind facilities. | (2.7) | ||||

| Wind U.S.: Decrease is primarily due to lower production across all U.S. wind facilities. | (7.4) | ||||

| Solar: Decrease is primarily driven by lower energy capture prices at the Altavista and Great Bay II Solar Facilities. | (1.2) | ||||

| Thermal: Decrease is primarily driven by unfavourable energy market pricing at the Windsor Locks Thermal Facility along with lower production at the Sanger Thermal Facility. | (4.2) | ||||

| Other: | (0.3) | ||||

| (17.9) | |||||

| New Facilities | |||||

| Other: Increase is primarily driven by Blue Hill Wind Facility (achieved full commercial operations (“COD”). | 1.0 | ||||

| 1.0 | |||||

| Foreign Exchange | (1.4) | ||||

| Current Period Revenue | $ | 627.9 | |||

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |||||

2023 Year-to-Date Results From Operations

Key Financial Information | Six months ended June 30 | ||||||||||

| (all dollar amounts in $ millions except per share information) | 2023 | 2022 | |||||||||

| Revenue | $ | 1,406.5 | $ | 1,352.6 | |||||||

| Net earnings attributable to shareholders | 16.9 | 57.6 | |||||||||

| Cash provided by operating activities | 294.7 | 301.6 | |||||||||

Adjusted Net Earnings1 | 176.0 | 250.7 | |||||||||

Adjusted EBITDA1 | 618.7 | 619.4 | |||||||||

Adjusted Funds from Operations1 | 367.8 | 400.6 | |||||||||

| Dividends declared to common shareholders | 150.8 | 238.2 | |||||||||

| Weighted average number of common shares outstanding | 687,727,579 | 674,720,319 | |||||||||

| Per share | |||||||||||

| Basic net earnings | $ | 0.02 | $ | 0.08 | |||||||

| Diluted net earnings | $ | 0.02 | $ | 0.08 | |||||||

Adjusted Net Earnings1 | $ | 0.25 | $ | 0.36 | |||||||

| Dividends declared to common shareholders | $ | 0.22 | $ | 0.35 | |||||||

| 1 | See Caution Concerning Non-GAAP Measures. | ||||

For the six months ended June 30, 2023, AQN reported basic net earnings per common share of $0.02 as compared to basic net earnings per common share of $0.08 during the same period in 2022, a decrease of $0.06. This loss was primarily driven by:

•a decrease in the value of investments carried at fair value of $52.0 million primarily related to the Company's investment in Atlantica; and

•the Kentucky Power Impairment of $46.5 million.

For the six months ended June 30, 2023, AQN reported Adjusted Net Earnings per common share of $0.25 as compared to $0.36 per common share during the same period in 2022, a decrease of $0.12 (see Caution Concerning Non-GAAP Measures). Adjusted Net Earnings decreased by $74.7 million year over year (see Caution Concerning Non-GAAP Measures),primarily due to:

•a decrease of $16.8 million in the Renewable Energy Group's operating profit primarily as a result wind facilities generating 84.5% of LTAR which represents a 10.8% decrease compared to the same period in 2022;

•a decrease of $26.4 million in the Renewable Energy Group's HLBV income as a result of the end of PTC eligibility on projects commissioned in 2012;

•an increase in earnings attributable to minority interest, exclusive of HLBV, of $23.2 million primarily due to the Company's sale in the fourth quarter of 2022 of a 49% ownership interest in the Odell, Deerfield and Sugar Creek Wind Facilities;

•an increase in interest expense of $49.1 million, driven by higher interest rates as well as increased borrowings to support growth initiatives;

•an increase in depreciation expense of $7.6 million driven by additional capital invested by the Company; and

•an increase in administrative expenses of $5.9 million due to timing, foreign exchange, inflation and increased headcount to support growth initiatives; partially offset by

•an increase of $52.5 million in the Regulated Services Group's operating profit primarily due to implementation of new rates.

For the six months ended June 30, 2023, AQN experienced an average exchange rate of Canadian to U.S. dollars of approximately 0.7421 as compared to 0.7865 in the same period in 2022, and an average exchange rate of Chilean pesos to U.S. dollars of approximately 0.0012 for the six months ended June 30, 2023 as compared to 0.0011 for the same period in 2022. As such, any year-over-year variance in revenue or expenses, in local currency, at any of AQN’s Canadian and Chilean entities is affected by a change in the average exchange rate upon conversion to AQN’s reporting currency.

For the six months ended June 30, 2023, AQN reported total revenue of $1,406.5 million as compared to $1,352.6 million during the same period in 2022, an increase of $53.9 million or 4.0%. The major factors resulting in the increase in AQN revenue for the six months ended June 30, 2023 as compared to the same period in 2022 are as follows:

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 12 | ||||

| (all dollar amounts in $ millions) | Six months ended June 30 | ||||

| Comparative Prior Period Revenue | $ | 1,352.6 | |||

| REGULATED SERVICES GROUP | |||||

| Existing Facilities | |||||

| Electricity: Increase is primarily due to higher pass through commodity costs at the Granite State Electric System, partially offset by one-time insurance proceeds for the Neosho Ridge Facility received in 2022. | 4.4 | ||||

Natural Gas: Decrease is primarily due to lower pass through commodity costs. | (10.9) | ||||

| Water: Increase is primarily due to the inflationary rate increase mechanism at the Suralis Water System and organic growth at the Litchfield Park and Gold Canyon Water Systems. | 9.7 | ||||

| Other: | (0.4) | ||||

| 2.8 | |||||

| Rate Reviews | |||||

| Electricity: Increase is primarily due to the implementation of new rates at the CalPeco Electric System with recoupment to the first quarter of 2022, as well as the implementation of new rates at the Empire, BELCO and Granite State Electric Systems. | 62.4 | ||||

| Natural Gas: Increase is primarily due to the implementation of new rates at the EnergyNorth, New Brunswick, Peach State, St. Lawrence and Empire Gas Systems. | 5.0 | ||||

| Water: Increase is due to the implementation of new rates at the Park Water System with one-time revenues from a recoupment to the third quarter of 2022. | 6.1 | ||||

| 73.5 | |||||

| Foreign Exchange | 1.1 | ||||

| RENEWABLE ENERGY GROUP | |||||

| Existing Facilities | |||||

| Hydro: Decrease is primarily driven by lower retail sales in the Maritimes Region. | (3.1) | ||||

| Wind CA: Decrease is primarily due to lower production across all Canadian wind facilities. | (5.0) | ||||

| Wind U.S.: Decrease is primarily due to lower production across the U.S. wind facilities. | (3.4) | ||||

| Solar: Decrease is primarily driven by lower energy capture prices at the Altavista and Great Bay II Solar Facilities. | (2.5) | ||||

| Thermal: Decrease is primarily driven by unfavourable energy market pricing at the Windsor Locks Thermal Facility along with lower production at the Sanger Thermal Facility. | (7.7) | ||||

| Other: | (1.1) | ||||

| (22.8) | |||||

| New Facilities | |||||

| Other: Increase is primarily driven by the Blue Hill Wind Facility (achieved COD in April 2022). | 2.4 | ||||

| 2.4 | |||||

| Foreign Exchange | (3.1) | ||||

| Current Period Revenue | $ | 1,406.5 | |||

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |||||

2023 Second Quarter and Year-to-Date Net Earnings Summary

Net loss attributable to shareholders for the three months ended June 30, 2023 totaled $253.2 million as compared to net loss attributable to shareholders of $33.4 million during the same period in 2022, a decrease of $219.8 million or 658.1%. Net earnings attributable to shareholders for the six months ended June 30, 2023 totaled $16.9 million as compared to net earnings attributable to shareholders of $57.6 million during the same period in 2022, a decrease of $40.7 million or 70.7%. The following table outlines the changes to net earnings (loss) attributable to shareholders for the three and six months ended June 30, 2023 as compared to the same periods in 2022. A more detailed analysis of these factors can be found under AQN: Corporate and Other Expenses.

| Change in net earnings (loss) attributable to shareholders | Three months ended | Six months ended | |||||||||

| June 30 | June 30 | ||||||||||

| (all dollar amounts in $ millions) | 2023 | 2023 | |||||||||

| Net earnings (loss) attributable to shareholders - Prior Period Balance | $ | (33.4) | $ | 57.6 | |||||||

Adjusted EBITDA1 | (11.5) | (0.7) | |||||||||

| Net earnings attributable to the non-controlling interest, exclusive of HLBV | (12.9) | (23.2) | |||||||||

| Income tax recovery | 33.2 | 17.9 | |||||||||

| Interest expense | (25.1) | (49.1) | |||||||||

| Other net losses | (31.7) | (30.4) | |||||||||

| Unrealized loss on energy derivatives included in revenue | 2.6 | 3.2 | |||||||||

| Pension and post-employment non-service costs | (3.0) | (5.5) | |||||||||

| Change in value of investments carried at fair value | (167.9) | 52.0 | |||||||||

| Gain on derivative financial instruments | 4.3 | 5.8 | |||||||||

| Foreign exchange | (1.9) | (3.1) | |||||||||

| Depreciation and amortization | (5.9) | (7.6) | |||||||||

| Net earnings (loss) attributable to shareholders - Current Period Balance | $ | (253.2) | $ | 16.9 | |||||||

| Change in Net Earnings (loss) ($) | $ | (219.8) | $ | (40.7) | |||||||

| Change in Net Earnings (loss) (%) | (658.1) | % | (70.7) | % | |||||||

| 1 | See Caution Concerning Non-GAAP Measures. | ||||

During the three months ended June 30, 2023, cash provided by operating activities totaled $261.4 million as compared to $135.3 million during the same period in 2022, an increase of $126.1 million primarily as a result of changes in working capital items. During the three months ended June 30, 2023, Adjusted Funds from Operations totaled $154.2 million as compared to Adjusted Funds from Operations of $180.3 million during the same period in 2022, a decrease of $26.1 million (see Caution Concerning Non-GAAP Measures).

During the three months ended June 30, 2023, Adjusted EBITDA totaled $277.7 million as compared to $289.2 million during the same period in 2022, a decrease of $11.5 million or 4.0% (see Caution Concerning Non-GAAP Measures). A more detailed analysis of this variance is presented within the reconciliation of Adjusted EBITDA to net earnings set out below under Non-GAAP Financial Measures.

During the six months ended June 30, 2023, cash provided by operating activities totaled $294.7 million as compared to $301.6 million during the same period in 2022, a decrease of $6.9 million primarily as a result of changes in working capital items. During the six months ended June 30, 2023, Adjusted Funds from Operations totaled $367.8 million as compared to Adjusted Funds from Operations of $400.6 million during the same period in 2022, a decrease of $32.8 million (see Caution Concerning Non-GAAP Measures).

During the six months ended June 30, 2023, Adjusted EBITDA totaled $618.7 million as compared to $619.4 million during the same period in 2022, a decrease of $0.7 million or 0.1% (see Caution Concerning Non-GAAP Measures). A more detailed analysis of this variance is presented within the reconciliation of Adjusted EBITDA to net earnings set out below under Non-GAAP Financial Measures.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 14 | ||||

2023 Second Quarter and Year-to-Date Adjusted EBITDA Summary

Adjusted EBITDA (see Caution Concerning Non-GAAP Measures) for the three months ended June 30, 2023 totaled $277.7 million as compared to $289.2 million during the same period in 2022, a decrease of $11.5 million or 4.0%. Adjusted EBITDA for the six months ended June 30, 2023 totaled $618.7 million as compared to $619.4 million during the same period in 2022, a decrease of $0.7 million or 0.1%. The breakdown of Adjusted EBITDA by the Company's main business units and a summary of changes are shown below.

| Three months ended | Six months ended | ||||||||||||||||||||||

Adjusted EBITDA1 by business units | June 30 | June 30 | |||||||||||||||||||||

| (all dollar amounts in $ millions) | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||

Divisional Operating Profit for Regulated Services Group1 | $ | 214.4 | $ | 185.9 | $ | 469.7 | $ | 417.2 | |||||||||||||||

Divisional Operating Profit for Renewable Energy Group1 | 90.6 | 122.2 | 197.0 | 240.2 | |||||||||||||||||||

| Administrative Expenses | (25.7) | (20.1) | (43.5) | (37.6) | |||||||||||||||||||

| Other Income & Expenses | (1.6) | 1.2 | (4.5) | (0.4) | |||||||||||||||||||

Total AQN Adjusted EBITDA1 | $ | 277.7 | $ | 289.2 | $ | 618.7 | $ | 619.4 | |||||||||||||||

Change in Adjusted EBITDA1 ($) | $ | (11.5) | $ | (0.7) | |||||||||||||||||||

Change in Adjusted EBITDA1 (%) | (4.0) | % | (0.1) | % | |||||||||||||||||||

Change in Adjusted EBITDA1 Breakdown | Three months ended June 30, 2023 | |||||||||||||

| (all dollar amounts in $ millions) | Regulated Services | Renewable Energy | Corporate | Total | ||||||||||

| Prior period balances | $ | 185.9 | $ | 122.2 | $ | (18.9) | $ | 289.2 | ||||||

| Existing Facilities and Investments | 3.3 | (30.5) | (2.8) | (30.0) | ||||||||||

| New Facilities and Investments | — | (0.1) | — | (0.1) | ||||||||||

| Rate Reviews | 24.5 | — | — | 24.5 | ||||||||||

| Foreign Exchange Impact | 0.7 | (1.0) | — | (0.3) | ||||||||||

| Administrative Expenses | — | — | (5.6) | (5.6) | ||||||||||

| Total change during the period | $ | 28.5 | $ | (31.6) | $ | (8.4) | $ | (11.5) | ||||||

| Current period balances | $ | 214.4 | $ | 90.6 | $ | (27.3) | $ | 277.7 | ||||||

Change in Adjusted EBITDA1 Breakdown | Six months ended June 30, 2023 | |||||||||||||

| (all dollar amounts in $ millions) | Regulated Services | Renewable Energy | Corporate | Total | ||||||||||

| Prior period balances | $ | 417.2 | $ | 240.2 | $ | (38.0) | $ | 619.4 | ||||||

| Existing Facilities and Investments | 8.3 | (40.7) | (4.1) | (36.5) | ||||||||||

| New Facilities and Investments | — | 0.3 | — | 0.3 | ||||||||||

| Rate Reviews | 43.8 | — | — | 43.8 | ||||||||||

| Foreign Exchange Impact | 0.4 | (2.8) | — | (2.4) | ||||||||||

| Administrative Expenses | — | — | (5.9) | (5.9) | ||||||||||

| Total change during the period | $ | 52.5 | $ | (43.2) | $ | (10.0) | $ | (0.7) | ||||||

| Current period balances | $ | 469.7 | $ | 197.0 | $ | (48.0) | $ | 618.7 | ||||||

| 1 | See Caution Concerning Non-GAAP Measures. | ||||

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 15 | ||||

REGULATED SERVICES GROUP

The Regulated Services Group operates rate-regulated utilities that as of June 30, 2023 provided distribution services to approximately 1,256,000 customer connections in the electric, natural gas, and water and wastewater sectors which is an increase of approximately 17,000 customer connections as compared to June 30, 2022.

The Regulated Services Group seeks to grow its business organically and through business development activities while using prudent acquisition criteria. The Regulated Services Group believes that its business results are maximized by building constructive regulatory and customer relationships, and enhancing customer connections in the communities in which it operates.

| Utility System Type | As at June 30 | ||||||||||||||||||||||

| 2023 | 2022 | ||||||||||||||||||||||

| (all dollar amounts in $ millions) | Assets | Net Utility Sales1 | Total Customer Connections2 | Assets | Net Utility Sales1 | Total Customer Connections2 | |||||||||||||||||

| Electricity | 5,065.8 | 418.5 | 309,000 | 4,848.8 | 373.0 | 307,000 | |||||||||||||||||

| Natural Gas | 1,753.9 | 206.8 | 376,000 | 1,611.9 | 200.9 | 370,000 | |||||||||||||||||

| Water and Wastewater | 1,651.7 | 175.6 | 571,000 | 1,404.3 | 162.2 | 562,000 | |||||||||||||||||

| Other | 286.0 | 28.2 | 311.8 | 27.5 | |||||||||||||||||||

| Total | $ | 8,757.4 | $ | 829.1 | 1,256,000 | $ | 8,176.8 | $ | 763.6 | 1,239,000 | |||||||||||||

| Accumulated Deferred Income Taxes Liability | $ | 722.3 | $ | 650.7 | |||||||||||||||||||

| 1 | Net Utility Sales for the six months ended June 30, 2023 and 2022. See Caution Concerning Non-GAAP Measures. | ||||

| 2 | Total Customer Connections represents the sum of all active and vacant customer connections. | ||||

The Regulated Services Group aggregates the performance of its utility operations by utility system type – electricity, natural gas, and water and wastewater systems.

The electric distribution systems are comprised of regulated electrical distribution utility systems and served approximately 309,000 customer connections in the U.S. States of California, New Hampshire, Missouri, Kansas, Oklahoma and Arkansas and in Bermuda as at June 30, 2023.

The natural gas distribution systems are comprised of regulated natural gas distribution utility systems and served approximately 376,000 customer connections located in the U.S. States of New Hampshire, Illinois, Iowa, Missouri, Georgia, Massachusetts and New York and in the Canadian Province of New Brunswick as at June 30, 2023.

The water and wastewater distribution systems are comprised of regulated water distribution and wastewater collection utility systems and served approximately 571,000 customer connections located in the U.S. States of Arkansas, Arizona, California, Illinois, Missouri, New York, and Texas, and in Chile as at June 30, 2023.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 16 | ||||

2023 Second Quarter and Year-to-Date Usage Results

| Electric Distribution Systems | Three months ended June 30 | Six months ended June 30 | |||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Average Active Electric Customer Connections For The Period | |||||||||||||||||||||||

| Residential | 262,700 | 261,800 | 261800 | 262,500 | 261,700 | ||||||||||||||||||

| Commercial and industrial | 42,700 | 42,400 | 42,600 | 42,300 | |||||||||||||||||||

| Total Average Active Electric Customer Connections For The Period | 305,400 | 304,200 | 305,100 | 304,000 | |||||||||||||||||||

| Customer Usage (GW-hrs) | |||||||||||||||||||||||

| Residential | 574.1 | 596.6 | 1,329.2 | 1,441.5 | |||||||||||||||||||

| Commercial and industrial | 918.9 | 948.5 | 1,842.3 | 1,864.4 | |||||||||||||||||||

| Total Customer Usage (GW-hrs) | 1,493.0 | 1,545.1 | 3,171.5 | 3,305.9 | |||||||||||||||||||

For the three months ended June 30, 2023, the electric distribution systems' usage totaled 1,493.0 GW-hrs as compared to 1,545.1 GW-hrs for the same period in 2022, a decrease of 52.1 GW-hrs or 3.4%. The decrease in electricity consumption is primarily due to colder weather at the Empire Electric System.

For the six months ended June 30, 2023, the electric distribution systems' usage totaled 3,171.5 GW-hrs as compared to 3,305.9 GW-hrs for the same period in 2022, a decrease of 134.4 GW-hrs or 4.1%. The decrease in electricity consumption is primarily due to warmer winter weather at the Empire Electric System.

Approximately 47% of the Regulated Services Group's electric distribution systems' revenues are not expected to be impacted by changes in customer usage, as they are subject to volumetric decoupling or represent fixed fee billings.

| Natural Gas Distribution Systems | Three months ended June 30 | Six months ended June 30 | |||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Average Active Natural Gas Customer Connections For The Period | |||||||||||||||||||||||

| Residential | 330,500 | 319,700 | 330,700 | 321,100 | |||||||||||||||||||

| Commercial and industrial | 41,100 | 38,500 | 41,100 | 38,900 | |||||||||||||||||||

| Total Average Active Natural Gas Customer Connections For The Period | 371,600 | 358,200 | 371,800 | 360,000 | |||||||||||||||||||

| Customer Usage (MMBTU) | |||||||||||||||||||||||

| Residential | 3,184,000 | 3,079,000 | 13,215,000 | 14,222,000 | |||||||||||||||||||

| Commercial and industrial | 4,196,000 | 3,655,000 | 12,910,000 | 12,534,000 | |||||||||||||||||||

| Total Customer Usage (MMBTU) | 7,380,000 | 6,734,000 | 26,125,000 | 26,756,000 | |||||||||||||||||||

For the three months ended June 30, 2023, usage at the natural gas distribution systems totaled 7,380,000 MMBTU as compared to 6,734,000 MMBTU during the same period in 2022, an increase of 646,000 MMBTU, or 9.6%. The increase in customer usage was primarily due to colder weather at the EnergyNorth Gas System.

For the six months ended June 30, 2023, usage at the natural gas distribution systems totaled 26,125,000 MMBTU as compared to 26,756,000 MMBTU during the same period in 2022, a decrease of 631,000 MMBTU, or 2.4%. The decrease in customer usage was primarily due to warmer weather at the Mid-States and New England Gas Systems.

Approximately 86% of the Regulated Services Group's gas distribution systems' revenues are not expected to be impacted by changes in customer usage, as they are subject to volumetric decoupling or represent fixed fee billings.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 17 | ||||

| Water and Wastewater Distribution Systems | Three months ended June 30 | Six months ended June 30 | |||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Average Active Customer Connections For The Period | |||||||||||||||||||||||

| Wastewater customer connections | 50,800 | 47,700 | 50,900 | 47,700 | |||||||||||||||||||

| Water distribution customer connections | 508,400 | 501,800 | 508,500 | 498,500 | |||||||||||||||||||

| Total Average Active Customer Connections For The Period | 559,200 | 549,500 | 559,400 | 546,200 | |||||||||||||||||||

| Gallons Provided (millions of gallons) | |||||||||||||||||||||||

| Wastewater treated | 840 | 812 | 1,635 | 1,590 | |||||||||||||||||||

| Water provided | 10,070 | 10,010 | 18,577 | 18,628 | |||||||||||||||||||

| Total Gallons Provided (millions of gallons) | 10,910 | 10,822 | 20,212 | 20,218 | |||||||||||||||||||

For the three months ended June 30, 2023, the water and wastewater distribution systems provided approximately 10,070 million gallons of water to customers and treated approximately 840 million gallons of wastewater. This is compared to 10,010 million gallons of water provided and 812 million gallons of wastewater treated during the same period in 2022, an increase in total gallons provided of 60 million or 0.6% and an increase in total gallons treated of 28 million or 3.4% This increase in water provided is primarily due to lower precipitation at the New York Water System and the increase in water treated is primarily due to customer growth at the Litchfield Park and Rio Rico Water Systems.

For the six months ended June 30, 2023, the water and wastewater distribution systems provided approximately 18,577 million gallons of water to customers and treated approximately 1,635 million gallons of wastewater. This is compared to 18,628 million gallons of water provided and 1,590 million gallons of wastewater treated during the same period in 2022, a decrease in total gallons provided of 51 million or 0.3% and an increase in total gallons treated of 45 million or 2.8% This decrease in water provided is due to higher precipitation at the Park Water System and the increase in water treated is primarily due to customer growth at the Litchfield Park and Rio Rico Water Systems.

Approximately 50% of the Regulated Services Group's water and wastewater distribution systems' revenues are not expected to be impacted by changes in customer usage, as they are subject to volumetric decoupling or represent fixed fee billings.

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | |||||

2023 Second Quarter and Year-to-Date Regulated Services Group Operating Results

| Three months ended | Six months ended | ||||||||||||||||||||||

| June 30 | June 30 | ||||||||||||||||||||||

| (all dollar amounts in $ millions) | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||

| Revenue | |||||||||||||||||||||||

| Regulated electricity distribution | $ | 326.8 | $ | 295.6 | $ | 642.4 | $ | 576.3 | |||||||||||||||

| Less: Regulated electricity purchased | (98.3) | (104.1) | (223.9) | (203.3) | |||||||||||||||||||

Net Utility Sales - electricity1 | 228.5 | 191.5 | 418.5 | 373.0 | |||||||||||||||||||

| Regulated gas distribution | 109.5 | 121.9 | 380.7 | 385.3 | |||||||||||||||||||

| Less: Regulated gas purchased | (36.2) | (51.8) | (173.9) | (184.4) | |||||||||||||||||||

Net Utility Sales - natural gas1 | 73.3 | 70.1 | 206.8 | 200.9 | |||||||||||||||||||

| Regulated water reclamation and distribution | 95.9 | 89.6 | 183.3 | 168.3 | |||||||||||||||||||

| Less: Regulated water purchased | (3.8) | (3.4) | (7.7) | (6.1) | |||||||||||||||||||

Net Utility Sales - water reclamation and distribution1 | 92.1 | 86.2 | 175.6 | 162.2 | |||||||||||||||||||

Other revenue2 | 14.2 | 12.6 | 28.2 | 27.5 | |||||||||||||||||||

Net Utility Sales1,3 | 408.1 | 360.4 | 829.1 | 763.6 | |||||||||||||||||||

| Operating expenses | (213.9) | (179.3) | (401.3) | (363.7) | |||||||||||||||||||

| Other income | 9.4 | 5.3 | 19.7 | 9.8 | |||||||||||||||||||

HLBV4 | 10.8 | (0.5) | 22.2 | 7.5 | |||||||||||||||||||

Divisional Operating Profit1,5 | $ | 214.4 | $ | 185.9 | $ | 469.7 | $ | 417.2 | |||||||||||||||

| 1 | See Caution Concerning Non-GAAP Measures. | ||||

| 2 | See Note 18 in the unaudited interim consolidated financial statements. | ||||

| 3 | This table contains a reconciliation of Net Utility Sales to revenue. The relevant sections of the table are derived from and should be read in conjunction with the unaudited consolidated statement of operations and Note 18 in the unaudited interim consolidated financial statements, “Segmented Information”. This supplementary disclosure is intended to more fully explain disclosures related to Net Utility Sales and provides additional information related to the operating performance of the Regulated Services Group. Investors are cautioned that Net Utility Sales should not be construed as an alternative to revenue. | ||||

| 4 | HLBV income represents the value of net tax attributes monetized by the Regulated Services Group in the period at the Luning and Turquoise Solar Facilities and the Neosho Ridge, Kings Point and North Fork Ridge Wind Facilities. | ||||

| 5 | This table contains a reconciliation of Divisional Operating Profit to revenue for the Regulated Services Group. The relevant sections of the table are derived from and should be read in conjunction with the unaudited consolidated statement of operations and Note 18 in the unaudited interim consolidated financial statements, “Segmented Information”. This supplementary disclosure is intended to more fully explain disclosures related to Divisional Operating Profit and provides additional information related to the operating performance of the Regulated Services Group. Investors are cautioned that Divisional Operating Profit should not be construed as an alternative to revenue. | ||||

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 19 | ||||

2023 Second Quarter Operating Results

For the three months ended June 30, 2023, the Regulated Services Group reported revenue of $532.2 million (i.e., $326.8 million of regulated electricity distribution, $109.5 million of regulated gas distribution and $95.9 million of regulated water reclamation and distribution) as compared to revenue of $507.1 million in the comparable period in the prior year (i.e., $295.6 million of regulated electricity distribution, $121.9 million of regulated gas distribution and $89.6 million of regulated water reclamation and distribution).

For the three months ended June 30, 2023, the Regulated Services Group reported a Divisional Operating Profit (excluding corporate administration expenses) of $214.4 million as compared to $185.9 million for the comparable period in the prior year (see Caution Concerning Non-GAAP Measures).

Highlights of the changes are summarized in the following table:

| (all dollar amounts in $ millions) | Three months ended June 30 | ||||

Prior Period Divisional Operating Profit1 | $ | 185.9 | |||

| Existing Facilities | |||||

| Electricity: Increase is primarily due higher HLBV of approximately $12.0 million income at the Neosho Ridge Wind Facility partially offset by unfavourable weather of approximately $11.0 million at the Empire Electric System. | 2.2 | ||||

| Gas: Decrease is primarily due to higher operating expenses. | (2.0) | ||||

| Water: Decrease is driven by lower revenue related to the removal of the decoupling mechanism at the Park Water System causing seasonality in 2023 not encountered in 2022 partially offset by organic growth at the Litchfield Park and Gold Canyon Water Systems. | (1.1) | ||||

| Other: Increase is driven by higher interest income on regulatory asset accounts. | 4.2 | ||||

| 3.3 | |||||

| Rate Reviews | |||||

Electricity: Increase is primarily due to the implementation of new rates at the CalPeco Electric System with recoupment to the first quarter of 2022 of approximately $11.2 million, as well as the implementation of new rates at the Empire, BELCO and Granite State Electric Systems. | 20.4 | ||||

| Gas: Increase is primarily due to the implementation of new rates at the EnergyNorth, New Brunswick, Peach State, St. Lawrence and Empire Gas Systems. | 2.6 | ||||

| Water: Increase is due to the implementation of new rates at the Park Water System. | 1.5 | ||||

| 24.5 | |||||

| Foreign Exchange | 0.7 | ||||

Current Period Divisional Operating Profit1 | $ | 214.4 | |||

| 1 | See Caution Concerning Non-GAAP Measures. | ||||

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 20 | ||||

2023 Year-to-Date Operating Results

For the six months ended June 30, 2023, the Regulated Services Group reported revenue of $1,206.4 million (comprised of $642.4 million of regulated electricity distribution revenue, $380.7 million of regulated natural gas distribution revenue and $183.3 million of regulated water reclamation and distribution revenue) as compared to revenue of $1,129.9 million in the same period in the prior year (comprised of $576.3 million of regulated electricity distribution revenue, $385.3 million of regulated natural gas distribution revenue and $168.3 million of regulated water reclamation and distribution revenue).

For the six months ended June 30, 2023, the Regulated Services Group reported a Divisional Operating Profit (excluding corporate administration expenses) of $469.7 million as compared to $417.2 million in the comparable period in the prior year (see Caution Concerning Non-GAAP Measures).

Highlights of the changes are summarized in the following table:

| (all dollar amounts in $ millions) | Six months ended June 30 | ||||

Prior Period Divisional Operating Profit1 | $ | 417.2 | |||

| Existing Facilities | |||||

| Electricity: Increase is primarily due higher HLBV of approximately $12.0 million income at the Neosho Ridge Wind Facility partially offset by unfavourable weather and higher operating expenses of approximately $12.0 million at the Empire Electric System, leading to no change period over period. | — | ||||

| Natural Gas: Decrease is primarily due to higher operating costs. | (3.0) | ||||

| Water: Increase is primarily due to organic growth at the Litchfield Park and Gold Canyon Water Systems. | 1.2 | ||||

| Other: Increase is primarily due to increased carrying charges on regulatory assets. | 10.1 | ||||

| 8.3 | |||||

| Rate Reviews | |||||

| Electricity: Increase is primarily due to the implementation of new rates at the CalPeco Electric System with recoupment to the first quarter of 2022, as well as the implementation of new rates at the Empire, BELCO and Granite State Electric Systems. | 32.7 | ||||

| Natural Gas: Increase is primarily due to the implementation of new rates at the EnergyNorth, New Brunswick, Peach State, St. Lawrence and Empire Gas Systems. | 5.0 | ||||

| Water: Increase is due to the implementation of new rates at the Park Water System with one-time revenues from a recoupment to the third quarter of 2022. | 6.1 | ||||

| 43.8 | |||||

| Foreign Exchange | 0.4 | ||||

Current Period Divisional Operating Profit1 | $ | 469.7 | |||

| 1 | See Caution Concerning Non-GAAP Measures. | ||||

| Algonquin Power & Utilities Corp. - Management Discussion & Analysis | 21 | ||||

Regulatory Proceedings

The following table summarizes the major regulatory proceedings currently underway or completed or effective in 2023 within the Regulated Services Group.

| Utility | Jurisdiction | Regulatory Proceeding Type | Rate Request (millions) | Current Status | ||||||||||||||||

| Completed Rate Reviews | ||||||||||||||||||||

| BELCO | Bermuda | General Rate Case ("GRC") | $34.8 | On September 30, 2021, BELCO filed its revenue allowance application in which it requested a $34.8 million increase for 2022 and a $6.1 million increase for 2023. On March 18, 2022, the Regulatory Authority (“RA”) approved an annual increase of $22.8 million, for a revenue allowance of $224.1 million for 2022 and $226.2 million for 2023. The RA authorized a 7.16% rate of return, comprised of a 62% equity and an 8.92% return on equity (“ROE”). In April 2022, BELCO filed an appeal in the Supreme Court of Bermuda challenging the decisions made by the RA through the recent Retail Tariff Review. A hearing on the appeal occurred in May 2023 and a judgment is expected in the second half of 2023. | ||||||||||||||||

| New Brunswick Gas | Canada | GRC | -$3.9 | On November 22, 2021, filed its 2022 general rate application for a revenue decrease based on the Energy & Utilities Board's decision authorizing a capital structure of 45% equity and an ROE of 8.5%. In January 2022, New Brunswick Gas appealed the Energy & Utilities Board's cost of capital decision. In May 2022, the Energy & Utilities Board issued a partial decision approving a decrease in annual revenues of $1.0 million to become effective in July 2022. In June 2022, the Court of Appeal found in favour of New Brunswick Gas and remanded the cost of capital case back to the Energy & Utilities Board. On December 22, 2022 the Energy & Utilities Board issued a Final Order and approved an annual revenue increase of $1.3 million based on an ROE of 9.8%. New rates became effective January 1, 2023. | ||||||||||||||||

| Apple Valley Water System | California | GRC | $2.9 | On July 2, 2021, filed an application requesting revenue increases of $2.9 million for 2022, $2.1 million for 2023, and $2.3 million for 2024 based on an ROE of 9.4% and on a 57% equity capital structure. The California Public Utilities Commission ("CPUC") Public Advocates Office issued its report in January 2022. Rebuttal testimony was filed in February 2022 and a hearing was held in March 2022. On February 3, 2023, the Commission issued a Final Order authorizing an annual revenue increase of $1.5 million. New rates became effective in March 2023 retroactive to July 1, 2022. | ||||||||||||||||