Exhibit 99.1

Tanzanian Royalty Exploration Corporation

Consolidated Financial Statements

For the years ended

August 31, 2017 and 2016

MANAGEMENT’S RESPONSIBILITY FOR FINANCIAL REPORTING

The accompanying consolidated financial statements of Tanzanian Royalty Exploration Corporation were prepared by management in accordance with International Financial Reporting Standards, as issued by the International Accounting Standards Board. Management acknowledges responsibility for the preparation and presentation of the consolidated financial statements, including responsibility for significant accounting judgments and estimates and the choice of accounting principles and methods that are appropriate to the Company’s circumstances. The significant accounting policies of the Company are summarized in Note 3 to the consolidated financial statements.

Management has established processes, which are in place to provide them with sufficient knowledge to support management representations that they have exercised reasonable diligence that (i) the consolidated financial statements do not contain any untrue statement of material fact or omit to state a material fact required to be stated or that is necessary to make a statement not misleading in light of the circumstances under which it is made, as of the date of and for the year presented by the consolidated financial statements and (ii) the consolidated financial statements fairly present in all material respects the financial condition and results of operations of the Company, as of the date of and for the year presented by the consolidated financial statements.

The Board of Directors is responsible for ensuring that management fulfills its financial reporting responsibilities and for reviewing and approving the consolidated financial statements together with other financial information. An Audit Committee assists the Board of Directors in fulfilling this responsibility. The Audit Committee meets with management to review the internal controls over the financial reporting process. The Audit Committee meets with management as well as with the independent auditors to review the consolidated financial statements and the auditors' report. The Audit Committee also reviews the Annual Report to ensure that the financial information reported therein is consistent with the information presented in the consolidated financial statements. The Audit Committee reports its findings to the Board of Directors for its consideration in approving the consolidated financial statements together with other financial information of the Company for issuance to the shareholders.

Management recognizes its responsibility for conducting the Company’s affairs in compliance with established financial standards, and applicable laws and regulations, and for maintaining proper standards of conduct for its activities.

| “Jeffrey R. Duval” | “Marco Guidi” | |

| Jeffrey R. Duval | Marco Guidi | |

| Acting Chief Executive Officer | Chief Financial Officer |

2

INDEPENDENT AUDITOR'S REPORT

To the Shareholders of Tanzanian Royalty Exploration Corporation:

We have audited the accompanying consolidated financial statements of Tanzanian Royalty Exploration Corporation, which comprise the consolidated statements of financial position as at August 31, 2017 and 2016, and the consolidated statements of comprehensive loss, changes in equity, and cash flow for the years then ended, and a summary of significant accounting policies and other explanatory information.

Management's Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with Canadian generally accepted auditing standards and the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of Tanzanian Royalty Exploration Corporation as at August 31, 2017 and 2016, and its financial performance and its cash flows for the years then ended in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board.

Emphasis of Matter

Without qualifying our opinion, we draw attention to Note 1 in the consolidated financial statements which describes certain conditions that indicate the existence of a material uncertainty that casts substantial doubt about Tanzanian Royalty Exploration Corporation's ability to continue as a going concern.

/s/ DMCL LLP

DALE MATHESON CARR-HILTON LABONTE LLP

CHARTERED PROFESSIONAL ACCOUNTANTS

Vancouver, Canada

November 27, 2017

3

MANAGEMENT’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

Management of the Company is responsible for establishing and maintaining adequate internal control over financial reporting for the Company as defined in Rule 13a-15(f) under the Securities and Exchange Act of 1934. Management of the Company is responsible for establishing and maintaining adequate internal control over financial reporting for the Company. The Company’s management, including our Chief Executive Officer and Chief Financial Officer, conducted an evaluation of the effectiveness of our internal control over financial reporting as of August 31, 2017. In making this assessment, the Company’s management used the criteria established in Internal Control – Integrated Framework, issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO 2013”). The Company’s management has completed their review and testing of the Company’s internal control over financial reporting and concluded that they are appropriately designed and operating effectively as of August 31, 2017.

4

Tanzanian Royalty Exploration

Corporation Consolidated Statements of Financial Position

(Expressed in Canadian Dollars)

| As at | August 31, 2017 | August 31, 2016 | ||||||

| Assets | ||||||||

| Current Assets | ||||||||

| Cash (Note 16) | $ | 1,011,293 | $ | 84,913 | ||||

| Other receivables (Note 12) | 329,008 | 254,389 | ||||||

| Inventory (Note 15) | 507,489 | 539,608 | ||||||

| Prepaid and other assets (Note 13) | 74,298 | 153,409 | ||||||

| 1,922,088 | 1,032,319 | |||||||

| Property, plant and equipment (Note 5) | 2,510,697 | 3,050,368 | ||||||

| Mineral properties and deferred exploration (Note 4) | 46,920,303 | 45,802,858 | ||||||

| $ | 51,353,088 | $ | 49,885,545 | |||||

| Liabilities | ||||||||

| Current Liabilities | ||||||||

| Trade, other payables and accrued liabilities (Note 14) | $ | 5,216,703 | $ | 4,827,508 | ||||

| Due to related parties (Note 9) | - | 86,000 | ||||||

| Leases payable (Note 5) | 56,631 | 370,103 | ||||||

| Convertible loan (Note 23) | 865,656 | 245,497 | ||||||

| Derivative in convertible loan (Note 23) | - | 108,000 | ||||||

| Gold bullion loans (Note 21) | 2,335,474 | 2,180,425 | ||||||

| Derivative in gold bullion loans (Note 21) | - | 5,051,000 | ||||||

| 8,474,464 | 12,868,533 | |||||||

| Warrant liability (Note 6) | 4,850,000 | 215,000 | ||||||

| Gold bullion loans (Note 21) | 1,059,524 | 941,406 | ||||||

| Asset Retirement Obligation (Note 19) | 715,057 | 704,123 | ||||||

| 15,099,045 | 14,729,062 | |||||||

| Shareholders’ equity | ||||||||

| Share capital (Note 6) | 125,174,377 | 122,380,723 | ||||||

| Share based payment reserve (Note 8) | 7,674,233 | 1,066,863 | ||||||

| Warrants reserve (Note 7) | 1,248,037 | 941,037 | ||||||

| Accumulated other comprehensive loss | (2,176,352 | ) | - | |||||

| Accumulated deficit | (96,566,577 | ) | (90,600,819 | ) | ||||

| Equity attributable to owners of the Company | 35,353,718 | 33,787,804 | ||||||

| Non-controlling interests (Note 20, 4(a)) | 900,325 | 1,368,679 | ||||||

| Total shareholders’ equity | 36,254,043 | 35,156,483 | ||||||

| $ | 51,353,088 | $ | 49,885,545 | |||||

Nature of operations and Going Concern (Note 1)

Segmented information (Note 17)

Commitments (Notes 4 and 18)

Events subsequent to the reporting period (Note 25)

The accompanying notes are an integral part of these consolidated financial statements

5

Tanzanian Royalty Exploration Corporation

Consolidated Statements of Comprehensive Loss

(Expressed in Canadian Dollars)

| Year ended August 31, | 2017 | 2016 | ||||||

| Administrative expenses | ||||||||

| Depreciation (Note 5) | $ | 421,983 | $ | 478,699 | ||||

| Consulting (Note 9) | 805,943 | 432,316 | ||||||

| Directors’ fees (Note 9) | 186,826 | 285,188 | ||||||

| Office and general | 197,457 | 246,938 | ||||||

| Shareholder information | 476,285 | 249,645 | ||||||

| Professional fees (Note 9) | 754,738 | 387,177 | ||||||

| Salaries and benefits (Note 6) | 458,700 | 623,716 | ||||||

| Share based payments (Note 6) | 1,772,663 | (38,996 | ) | |||||

| Travel and accommodation | 31,267 | 61,681 | ||||||

| (5,105,862 | ) | (2,726,364 | ) | |||||

| Other income (expenses) | ||||||||

| Foreign exchange gain | 161,593 | 111,352 | ||||||

| Interest, net | (22,528 | ) | (26,054 | ) | ||||

| Interest accretion (Note 21 and 23) | (725,696 | ) | (1,028,568 | ) | ||||

| Accretion on asset retirement obligation (Note 19) | (10,934 | ) | (24,123 | ) | ||||

| Finance costs (Note 22) | (347,418 | ) | (262,213 | ) | ||||

| Exploration costs | (53,194 | ) | (197,683 | ) | ||||

| Change in value of derivative liability (Notes 21 and 23) | - | (3,905,000 | ) | |||||

| Interest on leases (Note 5) | (24,362 | ) | (76,847 | ) | ||||

| Gain on disposal of property, plant and equipment | 2,030 | 34,476 | ||||||

| Loss on shares issued for settlement of debt (Note 9 and 21) | (141,108 | ) | (172,467 | ) | ||||

| Change in value of warrant liability (Note 6) | - | (946,600 | ) | |||||

| Write off of mineral properties and deferred exploration costs (Note 4) | (124,717 | ) | (3,516,268 | ) | ||||

| Withholding tax costs | (41,916 | ) | (45,543 | ) | ||||

| Net loss | $ | (6,434,112 | ) | $ | (12,781,902 | ) | ||

| Other comprehensive loss | ||||||||

| Foreign currency translation | (2,176,352 | ) | - | |||||

| Comprehensive loss | $ | (8,610,464 | ) | $ | (12,781,902 | ) | ||

| Loss attributable to: | ||||||||

| Parent | (5,965,758 | ) | (12,629,864 | ) | ||||

| Non-controlling interests | (468,354 | ) | (152,038 | ) | ||||

| $ | (6,434,112 | ) | $ | (12,781,902 | ) | |||

| Comprehensive loss attributable to: | ||||||||

| Parent | (7,983,689 | ) | (12,629,864 | ) | ||||

| Non-controlling interests | (626,775 | ) | - | |||||

| $ | (8,610,464 | ) | $ | (12,781,902 | ) | |||

| Loss per share – basic and diluted attributable to Parent | $ | (0.05 | ) | $ | (0.12 | ) | ||

| Weighted average # of shares outstanding – basic and diluted | 117,699,647 | 108,200,190 | ||||||

The accompanying notes are an integral part of these consolidated financial statements

6

Tanzanian Royalty Exploration Corporation

Consolidated Statements of Changes in Equity

(Expressed in Canadian Dollars)

| Share Capital | Reserves | |||||||||||||||||||||||||||||||||||

| Number of Shares | Amount | Share based payments | Warrants | Accumulated other comprehensive income | Accumulated deficit | Owner's equity | Non-controlling interests | Total equity | ||||||||||||||||||||||||||||

| Balance at September 1, 2015 | 107,853,554 | $ | 120,532,634 | $ | 1,048,757 | $ | 941,037 | $ | - | $ | (77,970,955 | ) | $ | 44,551,473 | $ | 1,520,717 | $ | 46,072,190 | ||||||||||||||||||

| Issued pursuant to Restricted Share Unit ("RSU") Plan (Note 6) | 50,000 | 120,500 | (120,500 | ) | - | - | - | - | - | - | ||||||||||||||||||||||||||

| Shares issued for interest on gold loans (Note 21) | 536,137 | 372,130 | - | - | - | - | 372,130 | - | 372,130 | |||||||||||||||||||||||||||

| Shares issued as financing fee for gold loan facility (Note 21) | 320,543 | 477,609 | - | - | - | - | 477,609 | - | 477,609 | |||||||||||||||||||||||||||

| Shares issued for services | 75,000 | 26,250 | - | - | - | - | 26,250 | - | 26,250 | |||||||||||||||||||||||||||

| Exercise of warrants | 233,258 | 851,600 | - | - | - | - | 851,600 | - | 851,600 | |||||||||||||||||||||||||||

| Share based compensation | - | 471,799 | - | - | - | 471,799 | - | 471,799 | ||||||||||||||||||||||||||||

| RSU shares forfeited (Note 6) | - | (333,193 | ) | - | - | - | (333,193 | ) | - | (333,193 | ) | |||||||||||||||||||||||||

| Total comprehensive loss for the year | - | - | - | - | (12,629,864 | ) | (12,629,864 | ) | (152,038 | ) | (12,781,902 | ) | ||||||||||||||||||||||||

| Balance at August 31, 2016 | 109,068,492 | $ | 122,380,723 | $ | 1,066,863 | $ | 941,037 | $ | - | $ | (90,600,819 | ) | $ | 33,787,804 | $ | 1,368,679 | $ | 35,156,483 | ||||||||||||||||||

| Issued for private placement, net of issuance costs | 7,197,543 | 5,589,501 | - | - | - | - | 5,589,501 | - | 5,589,501 | |||||||||||||||||||||||||||

| Warrants issued on private placement | (6,592,000 | ) | - | - | - | - | (6,592,000 | ) | - | (6,592,000 | ) | |||||||||||||||||||||||||

| Agent warrants issued on private placement | (92,000 | ) | - | 92,000 | - | - | - | - | - | |||||||||||||||||||||||||||

| Issued pursuant to Restricted Share Unit ("RSU") Plan (Note 6) | 695,991 | 1,040,990 | (1,040,990 | ) | - | - | - | - | - | - | ||||||||||||||||||||||||||

| Shares issued for interest on gold loans (Note 21) | 814,089 | 542,447 | - | - | - | - | 542,447 | - | 542,447 | |||||||||||||||||||||||||||

| Issued for settlement of leases (Note 5) | 458,329 | 288,747 | - | - | - | - | 288,747 | - | 288,747 | |||||||||||||||||||||||||||

| Issued for settlement of amounts due to related parties (Note 9) | 187,321 | 131,998 | - | - | - | - | 131,998 | - | 131,998 | |||||||||||||||||||||||||||

| Issued for settlement of convertible loans (Note 23) | 83,333 | 49,166 | - | - | - | - | 49,166 | - | 49,166 | |||||||||||||||||||||||||||

| Shares issued as financing fee for convertible loans (Note 23) | 132,577 | 92,805 | - | - | - | - | 92,805 | - | 92,805 | |||||||||||||||||||||||||||

| Exercise of warrants | 3,146,944 | 1,742,000 | - | - | - | - | 1,742,000 | - | 1,742,000 | |||||||||||||||||||||||||||

| Conversion component of convertible loans (Note 23) | - | 625,000 | - | - | - | 625,000 | - | 625,000 | ||||||||||||||||||||||||||||

| Reversal of warrant liability upon change of functional currency to USD | - | - | 215,000 | - | - | 215,000 | - | 215,000 | ||||||||||||||||||||||||||||

| Reversal of derivative in gold bullion loans upon change of functional currency to USD | - | 5,051,000 | - | - | - | 5,051,000 | - | 5,051,000 | ||||||||||||||||||||||||||||

| Reversal of derivative in gold convertible loans upon change of functional currency to USD | - | 108,000 | - | - | - | 108,000 | - | 108,000 | ||||||||||||||||||||||||||||

| Share based compensation - RSU | - | 262,931 | - | - | - | 262,931 | - | 262,931 | ||||||||||||||||||||||||||||

| Share based compensation - Stock options | - | 1,725,000 | - | - | - | 1,725,000 | - | 1,725,000 | ||||||||||||||||||||||||||||

| RSU shares forfeited (Note 6) | - | (123,571 | ) | - | - | - | (123,571 | ) | - | (123,571 | ) | |||||||||||||||||||||||||

| Exchange on translation of foreign subsidiaries | - | - | - | (2,176,352 | ) | - | (2,176,352 | ) | - | (2,176,352 | ) | |||||||||||||||||||||||||

| Total comprehensive loss for the year | - | - | - | - | (5,965,758 | ) | (5,965,758 | ) | (468,354 | ) | (6,434,112 | ) | ||||||||||||||||||||||||

| Balance at August 31, 2017 | 121,784,619 | $ | 125,174,377 | $ | 7,674,233 | $ | 1,248,037 | $ | (2,176,352 | ) | $ | (96,566,577 | ) | $ | 35,353,718 | $ | 900,325 | $ | 36,254,043 | |||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements

7

Tanzanian Royalty Exploration Corporation

Consolidated Statements of Cash Flow

(Expressed in Canadian Dollars)

| Year ended August 31, | 2017 | 2016 | ||||||

| Operating | ||||||||

| Net loss | $ | (6,434,112 | ) | $ | (12,781,902 | ) | ||

| Adjustments to reconcile net loss to cash flow from operating activities: | ||||||||

| Depreciation | 421,984 | 478,699 | ||||||

| Change in value of warrant liability | - | 946,600 | ||||||

| Change in value of derivative liability | - | 3,905,000 | ||||||

| Write-off of mineral properties and deferred exploration costs | 124,717 | 3,516,268 | ||||||

| Share based payments | 1,772,663 | (38,996 | ) | |||||

| Accretion on asset retirement obligation | 10,934 | 24,123 | ||||||

| Interest accretion | 725,696 | 1,036,303 | ||||||

| Foreign exchange | (384,216 | ) | 7,906 | |||||

| Shares issued for payment of interest on bullion loans | 429,426 | 174,076 | ||||||

| Loss on shares issued for settlement of debt | 141,108 | 172,467 | ||||||

| Gain on sale of property, plant and equipment | (2,030 | ) | (34,476 | ) | ||||

| Shares issued for services | - | 26,250 | ||||||

| Cash interest paid | - | (50,926 | ) | |||||

| Non cash directors’ fees | 75,200 | 157,813 | ||||||

| Net change in non-cash operating working capital items: | ||||||||

| Other receivables | (74,619 | ) | (38,217 | ) | ||||

| Inventory | 32,119 | (52,033 | ) | |||||

| Prepaid expenses | 79,111 | (72,566 | ) | |||||

| Trade, other payables and accrued liabilities | (1,201,470 | ) | 709,116 | |||||

| Cash used in operations | (4,283,489 | ) | (1,914,495 | ) | ||||

| Investing | ||||||||

| Mineral properties and exploration expenditures, net of recoveries | (1,568,614 | ) | (688,296 | ) | ||||

| Property, plant and equipment, net of proceeds from sale | 13,803 | (88,339 | ) | |||||

| Cash used in investing activities | (1,554,811 | ) | (776,635 | ) | ||||

| Financing | ||||||||

| Loans (repayment) of loans from related parties | (32,686 | ) | 133,632 | |||||

| Interest on leases | 25,872 | - | ||||||

| Repayment of leases | - | (75,530 | ) | |||||

| Proceeds from gold bullion loan | - | 1,729,000 | ||||||

| Proceeds from convertible loan | 1,181,993 | 221,115 | ||||||

| Cash provided by financing activities | 6,764,680 | 2,008,217 | ||||||

| Net increase (decrease) in cash and cash equivalents | 926,380 | (682,913 | ) | |||||

| Cash and cash equivalents, beginning of year | 84,913 | 767,826 | ||||||

| Cash and cash equivalents, end of year | $ | 1,011,293 | $ | 84,913 | ||||

The accompanying notes are an integral part of these consolidated financial statements

8

Tanzanian Royalty Exploration Corporation

Consolidated Statements of Cash Flow

(Expressed in Canadian Dollars)

| Supplementary information: | 2017 | 2016 | ||||||

| Non-cash transactions: | ||||||||

| Share based payments capitalized to mineral properties | $ | 16,497 | $ | 18,733 | ||||

| Shares issued pursuant to RSU plan | 1,040,990 | 120,500 | ||||||

| Shares issued for interest on gold loans | 542,447 | 372,130 | ||||||

| Exercise of warrants – cashless exercise | 1,742,000 | 851,600 | ||||||

| Shares issued for finders’ fee on gold bullion loan | - | 477,609 | ||||||

| Shares issued as financing fee for convertible loans | 92,805 | - |

The accompanying notes are an integral part of these consolidated financial statements

9

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 1. | Nature of Operations and Going Concern |

The Company was originally incorporated under the corporate name “424547 Alberta Ltd.” in the Province of Alberta on July 5, 1990, under the Business Corporations Act (Alberta). The name was changed to “Tan Range Exploration Corporation” on August 13, 1991. The name of the Company was again changed to “Tanzanian Royalty Exploration Corporation” (“TREC” or the “Company”) on February 28, 2006. The address of the Company’s registered office is 22 Adelaide Street West, Suite 3400, Toronto, Ontario M5H 4E3 Canada. The Company’s principal business activity is in the exploration and development of mineral property interests. The Company’s mineral properties are located in United Republic of Tanzania (“Tanzania”).

The Company is in the process of exploring and evaluating its mineral properties. The business of exploring and mining for minerals involves a high degree of risk. The underlying value of the mineral properties is dependent upon the existence and economic recovery of mineral resources and reserves, the ability to raise long-term financing to complete the development of the properties, government policies and regulations, and upon future profitable production or, alternatively, upon the Company’s ability to dispose of its interest on an advantageous basis; all of which are uncertain.

The amounts shown as mineral properties and deferred expenditures represent costs incurred to date, less amounts amortized and/or written off, and do not necessarily represent present or future values. The underlying value of the mineral properties is entirely dependent on the existence of economically recoverable reserves, securing and maintaining title and beneficial interest, the ability of the Company to obtain the necessary financing to complete development, and future profitable production.

At August 31, 2017 the Company had a working capital deficiency of $6,552,376 (August 31, 2016 – $11,836,214 working capital deficiency), had not yet achieved profitable operations, has accumulated losses of $96,566,577 (August 31, 2016 – $90,600,819) and expects to incur further losses in the development of its business. The Company will require additional financing in order to conduct its planned work programs on mineral properties, meet its ongoing levels of corporate overhead and discharge its future liabilities as they come due.

The Company’s current funding sources and taking into account the working capital position and capital requirements at August 31, 2017, indicate the existence of a material uncertainty that raises substantial doubt about the Company’s ability to continue as a going concern and is dependent on the Company raising additional debt or equity financing. The Company must obtain additional funding in order to continue development and construction of the Buckreef Project. The Company is continuing to pursue additional financing to fund the construction of the Buckreef Project and additional projects. Whilst the Company has been successful in obtaining financing in the past, there is no assurance that such additional funding and/or project financing will be obtained or obtained on commercially favourable terms.

These consolidated financial statements do not give effect to any adjustment which would be necessary should the Company be unable to continue as a going concern and, therefore, be required to realize its assets and discharge its liabilities in other than the normal course of business and at amounts different from those reflected in the consolidated financial statements.

10

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 2. | Basis of Preparation |

2.1 Statement of compliance

The Company’s consolidated financial statements, including comparatives, have been prepared in accordance with and using accounting policies in full compliance with the International Financial Reporting Standards (“IFRS”) and International Accounting Standards (“IAS”) issued by the International Accounting Standards Board (“IASB”) and Interpretations of the International Financial Reporting Interpretations Committee (“IFRIC”), effective for the Company’s reporting for the year ended August 31, 2017.

These consolidated financial statements were approved and authorized by the Board of Directors of the Company on November 27, 2017.

2.2 Basis of presentation

The consolidated financial statements of the Company as at and for the years ended August 31, 2017 and 2016 comprise of the Company and its subsidiaries (together referred to as the “Company” or “Group”).

The consolidated financial statements have been prepared on the historical cost basis except for certain financial instruments, which are measured at fair value, as explained in the accounting policies set out in note 3.

| 2.3 | Adoption of new and revised standards and interpretations |

New standards and interpretations adopted

The Company applies, for the first time, certain standards and amendments that require restatement of previous financial statements. These include IAS 1 Presentation of Financial Statements, IAS 16 Property Plant and Equipment, IAS 38 Intangible Assets and IFRS 11 Joint Arrangements. The nature and effect of these changes are disclosed below.

Several other new standards and amendments apply for the first time in 2016. However, they

did not impact the consolidated financial statements of the Company.

The nature and impact of each new standard/amendment is described below:

| • | In December 2014, the IASB issued amendments to IAS 1 – Presentation of Financial Statements (“IAS 1”) to improve the effectiveness of presentation and disclosure in financial reports with the objective of reducing immaterial note disclosure. The amendments are effective for annual periods beginning on or after January 1, 2016 with early adoption permitted. The adoption of the standard has not had an impact on the Company’s financial statements. |

| • | IAS 16 Property Plant and Equipment and IAS 38 Intangible Assets – The amendment is applied retrospectively and clarifies in IAS 16 and IAS 38 that the asset may be revalued by reference to observable data on either the gross or net carrying amount. In addition, the accumulated depreciation or amortization is the difference between the gross and carrying amounts of the asset. The policy became effective for annual periods starting after, or on January 1, 2016. The adoption of the standard has not had an impact on the Company’s financial statements. |

11

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 2. | Basis of Preparation (continued) |

| 2.3 | Adoption of new and revised standards and interpretations (continued) |

New standards and interpretations adopted (continued)

| • | Amendments to IFRS 11 Joint Arrangements - The amendments to IFRS 11 require that a joint operator accounting for the acquisition of an interest in a joint operation, in which the activity of the joint operation constitutes a business must apply the relevant IFRS 3 principles for business combinations accounting. The amendments also clarify that a previously held interest in a joint operation is not re-measured on the acquisition of an additional interest in the same joint operation while joint control is retained. In addition, a scope exclusion has been added to IFRS 11 to specify that the amendments do not apply when the parties sharing joint control, including the reporting entity, are under common control of the same ultimate controlling party. The amendments apply to both the acquisition of the initial interest in a joint operation and the acquisition of any additional interests in the same joint operation and are prospectively effective for annual periods beginning on or after January 1, 2016, with early adoption permitted. The adoption of the standard has not had an impact on the Company’s financial statements. |

| • | IAS 38 - Intangible Assets (“IAS 38”) and IAS 16 – Property, Plant and Equipment (“IAS 16”), were amended in May 2014 to introduce a rebuttable presumption that the use of revenue-based amortization methods is inappropriate. The amendments are effective for annual periods beginning on or after January 1, 2016. The adoption of the standard has not had an impact on the Company’s financial statements. |

New standards and interpretations to be adopted in future

At the date of authorization of these Financial Statements, the IASB and IFRIC has issued the following new and revised Standards and Interpretations which are not yet effective for the relevant reporting periods and which the Company has not early adopted these standards, amendments and interpretations. However, the Company is currently assessing what impact the application of these standards or amendments will have on the consolidated financial statements of the Company.

• IFRS 9 Financial Instruments. IFRS 9 covers the classification and measurement, impairment and hedge accounting of financial assets and financial liabilities and the effective date is for annual periods on or after January 1, 2018, with earlier application permitted. The Company is assessing the impact of adopting IFRS 9 but does not expect it will have a significant impact on its consolidated financial statements. Amendments to IFRS 9 also provide relief from the requirement to restate comparative financial statements for the effect of applying IFRS 9. Instead, additional transition disclosures will be required to help investors understand the effect that the initial application of IFRS 9 has on the classification and measurement of financial instruments.

| • | IFRS 15 Revenue from Contracts with Customers. In May 2014, the IASB issued IFRS 15, Revenue from Contracts with Customers. IFRS 15 specifies how and when to recognize revenue as well as requires entities to provide users of financial statements with more informative, relevant disclosures. The standard supersedes IAS 18, Revenue, IAS 11, Construction Contracts, and a number of revenue-related interpretations. Application of the standard is mandatory for all IFRS reporters and it applies to nearly all contracts with customers: the main exceptions are leases, financial instruments and insurance contracts. IFRS 15 must be applied in an entity’s first annual IFRS financial statements for periods beginning on or after January 1, 2018. Application of the standard is mandatory and early adoption is permitted. The Company has not yet determined the impact of the amendments on the Company’s financial statements. |

12

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 2. | Basis of Preparation (continued) |

| 2.4 | Adoption of new and revised standards and interpretations (continued) |

New standards and interpretations to be adopted in future (continued)

| • | IFRS 16 - In 2016, the IASB issued IFRS 16, Leases (“IFRS 16”), replacing IAS 17, Leases and related interpretations. The standard introduces a single on-balance sheet recognition and measurement model for lessees, eliminating the distinction between operating and finance leases. Lessors continue to classify leases as finance and operating leases. IFRS 16 becomes effective for annual periods beginning on or after January 1, 2019, and is to be applied retrospectively. Early adoption is permitted if IFRS 15, Revenue from Contracts with Customers (“IFRS 15”) has been adopted. The Company is assessing the impact of the amendments on the Company’s financial statements, but does not anticipate that the impact will be significant. |

| 2.5 | Change in functional currency |

The functional currency of the Company and each of its subsidiaries is the U.S. dollar. The consolidated financial statements are presented in Canadian Dollars which is the Company’s presentation currency.

The Company changed its functional currency from the Canadian dollar (“CAD”) to the U.S. dollar (“USD”) as of September 1, 2016. The change in functional currency coincides with the September 1, 2016 closing of the first tranche of the USD unit private placement as described in note 6. Considering the Company’s business activities, which have changed over the years to being comprised primarily of USD expenditures as well as the Company now receiving most of its financing through USD denominated financings, management determined that the functional currency of the Company changed to the USD.

As a result, translation adjustments for prior periods were not removed from equity and the translated amounts for nonmonetary assets at the end of the prior period become the accounting basis for those assets in the period of the change and subsequent periods. These changes have been accounted for prospectively.

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions or valuation where items are re-measured. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at period-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognized in the statement of comprehensive loss.

The operation’s assets and liabilities are translated to the presentation currency at the closing rate as at the date of the consolidated statements of financial position, and revenue and expenses are translated using the rate as at the time of the transaction. All exchange differences resulting from the translation are recognized in other comprehensive income.

13

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 3. | Summary of Significant Accounting Policies |

3.1 Basis of consolidation

The consolidated financial statements include the financial statements of the Company and its controlled subsidiaries: Tanzania American International Development Corporation 2000 Limited (“Tanzam”), Tancan Mining Co. Limited (“Tancan”), Buckreef Gold Company Ltd. (“Buckreef”), and Northwestern Base Metals Company Limited (“NWBM”). Control is achieved when the Company has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

Subsidiaries are consolidated from the date of acquisition, being the date on which the Company obtains control, and continued to be consolidated until the date when such control ceases. The financial statements of the subsidiaries are prepared for the same reporting period as the parent company, using consistent accounting policies.

The consolidated financial statements of the Company set out the assets, liabilities, expenses, and cash flows of the Corporation and its subsidiaries, namely:

| Ownership interest as at August 31, | ||||||||||||||

| Country of incorporation | 2017 | 2016 | ||||||||||||

| Tanzam | Tanzania | 100 | % | 100 | % | |||||||||

| Tancan | Tanzania | 100 | % | 100 | % | |||||||||

| Buckreef | Tanzania | 55 | % | 55 | % | |||||||||

| NWBM | Tanzania | 75 | % | 75 | % | |||||||||

All inter-company transactions, balances, income and expenses are eliminated in full on consolidation.

Non-controlling interests in the net assets of consolidated subsidiaries are identified separately from the Company’s equity therein. Total comprehensive income within a subsidiary is attributed to the non-controlling interest even if it results in a negative balance.

3.2 Mineral properties

All direct costs related to the acquisition and exploration and development of specific properties are capitalized as incurred. If a property is brought into commercial production, these costs will be amortized against the income generated from the property. If a property is abandoned, sold or impaired, an appropriate charge will be made to the statement of comprehensive loss at the date of such impairment. Discretionary option payments arising on the acquisition of mining properties are only recognized when paid. Amounts received from other parties to earn an interest in the Company's mining properties are applied as a reduction of the mining property and deferred exploration and development costs until all capitalized costs are recovered at which time additional reimbursements are recorded in the statement of comprehensive loss, except for administrative reimbursements which are credited to operations.

Consequential revenue from the sale of metals, extracted during the Company's test mining activities, is recognized on the date the mineral concentrate level is agreed upon by the Company and customer, as this coincides with the transfer of title, the risk of ownership, the determination of the amount due under the terms of settlement contracts the Company has with its customer, and collection is reasonably assured. Revenues from properties earned prior to the commercial production stage are deducted from capitalized costs.

The amounts shown for mining claims and related deferred costs represent costs incurred to date, less amounts expensed or written off, reimbursements and revenue, and do not necessarily reflect present or future values of the particular properties. The recoverability of these costs is dependent upon discovery of economically recoverable reserves and future production or proceeds from the disposition thereof.

14

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 3. | Summary of Significant Accounting Policies (continued) |

The Company reviews the carrying value of a mineral exploration property when events or changes in circumstances indicate that the carrying value may not be recoverable. If the carrying value of the property exceeds its fair value, the property will be written down to fair value with the provision charged against operations in the year of impairment. An impairment is also recorded when management determines that it will discontinue exploration or development on a property or when exploration rights or permits expire.

Ownership in mineral properties involves certain risks due to the difficulties in determining the validity of certain claims as well as the potential for problems arising from the frequently ambiguous conveyance history characteristic of many mineral interests. The Company has investigated the ownership of its mineral properties and, to the best of its knowledge, ownership of its interests are in good standing.

Capitalized mineral property exploration costs are those directly attributable costs related to the search for, and evaluation of mineral resources that are incurred after the Company has obtained legal rights to explore a mineral property and before the technical feasibility and commercial viability of a mineral reserve are demonstrable. Any cost incurred prior to obtaining the legal right to explore a mineral property are expensed as incurred. Field overhead costs directly related to exploration are capitalized and allocated to mineral properties explored. All other overhead and administration costs are expensed as incurred.

Once an economically viable reserve has been determined for a property and a decision has been made to proceed with development has been approved, acquisition, exploration and development costs previously capitalized to the mineral property are first tested for impairment and then classified as property, plant and equipment under construction.

3.3 Property, plant and equipment

Property, plant and equipment (“PPE”) are stated at cost less accumulated depreciation and accumulated impairment losses. The cost of an item of PPE consists of the purchase price, any costs directly attributable to bringing the asset to the location and condition necessary for its intended use and an initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located.

Depreciation is provided at rates calculated to write off the cost of PPE, less their estimated residual value, using the declining balance method over the following expected useful lives:

| Assets | Rate | |||

| Machinery and equipment | 20% to 30 | % | ||

| Automotive | 30 | % | ||

| Computer equipment | 30 | % | ||

| Drilling equipment and automotive equipment | 6.67 | % | ||

| Leasehold improvements | 20 | % | ||

| Heap leach pads | 20 | % | ||

An item of PPE is derecognized upon disposal, when held for sale or when no future economic benefits are expected to arise from the continued use of the asset. Any gain or loss arising on disposal of the asset, determined as the difference between the net disposal proceeds and the carrying amount of the asset, is recognized in the consolidated statement of comprehensive loss.

Assets under construction are capitalized as construction-in-progress. The cost of construction-in-progress comprises of its purchase price and any costs directly attributable to bringing it into working condition for its intended use. Such cost includes the cost of replacing part of the plant and equipment and borrowing costs for long-term construction projects if the recognition criteria are met. Construction-in-progress assets are not depreciated until it is completed and available for use.

15

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 3. | Summary of Significant Accounting Policies (continued) |

The Company conducts an annual assessment of the residual balances, useful lives and depreciation methods being used for PPE and any changes arising from the assessment are applied by the Company prospectively.

Where an item of plant and equipment comprises major components with different useful lives, the components are accounted for as separate items of plant and equipment. Expenditures incurred to replace a component of an item of property, plant and equipment that is accounted for separately, including major inspection and overhaul expenditures are capitalized.

3.4 Decommissioning, restoration and similar liabilities (“Asset retirement obligation” or “ARO”)

The Company recognizes liabilities for statutory, contractual, constructive or legal obligations, including those associated with the reclamation of mineral properties and PPE, when those obligations result from the acquisition, construction, development or normal operation of the Company’s assets. Initially, a liability for an asset retirement obligation is recognized at its fair value in the period in which it is incurred. Upon initial recognition of the liability, the corresponding asset retirement obligation is added to the carrying amount of the related asset and the cost is amortized as an expense over the economic life of the asset using the declining balance method. Following the initial recognition of the asset retirement obligation, the carrying amount of the liability is increased for the passage of time and adjusted for changes to the current market-based discount rate, and adjusted for changes to the amount or timing of the underlying cash flows needed to settle the obligation.

3.5 Share based payments

Share based payment transactions

Employees (including directors and senior executives) of the Company receive a portion of their remuneration in the form of share based payment transactions, whereby employees render services as consideration for equity instruments (“equity-settled transactions”).

In situations where equity instruments are issued and some or all of the goods or services received by the entity as consideration cannot be specifically identified, they are measured at fair value of the share-based payment.

Equity settled transactions

The costs of equity settled transactions with employees are measured by reference to the fair value at the date on which they are granted.

The costs of equity-settled transactions are recognized, together with a corresponding increase in equity, over the period in which the performance and/or service conditions are fulfilled, ending on the date on which the relevant employees become fully entitled to the award (“the vesting date”). The cumulative expense is recognized for equity-settled transactions at each reporting date until the vesting date reflects the Company’s best estimate of the number of equity instruments that will ultimately vest. The profit or loss charge or credit for a period represents the movement in cumulative expense recognized as at the beginning and end of that period and the corresponding amount is represented in share based payment reserve.

No expense is recognized for awards that do not ultimately vest, except for awards where vesting is conditional upon a market condition, which are treated as vesting irrespective of whether or not the market condition is satisfied provided that all other performance and/or service conditions are satisfied.

16

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 3. | Summary of Significant Accounting Policies (continued) |

Where the terms of an equity-settled award are modified, the minimum expense recognized is the expense as if the terms had not been modified. An additional expense is recognized for any modification which increases the total fair value of the share-based payment arrangement, or is otherwise beneficial to the employee as measured at the date of modification.

The effect of outstanding options is considered in the computation of earnings per share, if dilutive.

3.6 Taxation

Income tax expense represents the sum of tax currently payable and deferred tax.

Current income tax

Current income tax assets and liabilities for the current and prior periods are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted by the date of the statement of financial position.

Deferred income tax

Deferred income tax is provided using the liability method on temporary differences at the date of the statement of financial position between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes.

Deferred income tax liabilities are recognized for all taxable temporary differences, except:

• where the deferred income tax liability arises from the initial recognition of goodwill or of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit nor taxable profit or loss; and

• in respect of taxable temporary differences associated with investments in subsidiaries, associates and interests in joint ventures, where the timing of the reversal of the temporary differences can be controlled and it is probable that the temporary differences will not reverse in the foreseeable future.

Deferred income tax assets are recognized for all deductible temporary differences, carry forward of unused tax credits and unused tax losses, to the extent that it is probable that taxable profit will be available against which the deductible temporary differences and the carry forward of unused tax credits and unused tax losses can be utilized except:

• where the deferred income tax asset relating to the deductible temporary difference arises from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit nor taxable profit or loss; and

• in respect of deductible temporary differences associated with investments in subsidiaries, associates and interests in joint ventures, deferred income tax assets are recognized only to the extent that it is probable that the temporary differences will reverse in the foreseeable future and taxable profit will be available against which the temporary differences can be utilized.

The carrying amount of deferred income tax assets is reviewed at each date of the statement of financial position and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred income tax asset to be utilized. Unrecognized deferred income tax assets are reassessed at each date of the statement of financial position and are recognized to the extent that it has become probable that future taxable profit will allow the deferred tax asset to be recovered.

17

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 3. | Summary of Significant Accounting Policies (continued) |

Deferred income tax assets and liabilities are measured at the tax rates that are expected to apply to the year when the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the date of the statement of financial position.

Deferred income tax relating to items recognized directly in equity is recognized in equity and not in the statement of comprehensive loss.

Deferred income tax assets and deferred income tax liabilities are offset if, and only if, a legally enforceable right exists to set off current tax assets against current tax liabilities and the deferred tax assets and liabilities relate to income taxes levied by the same taxation authority on either the same taxable entity or different taxable entities which intend to either settle current tax liabilities and assets on a net basis, or to realize the assets and settle the liabilities simultaneously, in each future period in which significant amounts of deferred tax assets or liabilities are expected to be settled or recovered.

Sales tax

Expenses and assets are recognized net of the amount of sales tax, except:

| • | When the sales tax incurred on a purchase of assets or services is not recoverable from the taxation authority, in which case the sales tax is recognised as part of the cost of acquisition of the asset or as part of the expense item, as applicable; or |

| • | When receivables and payables are stated with the amount of sales tax included. |

The net amount of sales tax recoverable from, or payable to, the taxation authority is included as part of receivables or payables in the statement of financial position.

3.7 Loss per share

The basic loss per share is computed by dividing the net loss by the weighted average number of common shares outstanding during the period. The diluted loss per share reflects the potential dilution of common share equivalents, such as outstanding restricted stock units and share purchase warrants, in the weighted average number of common shares outstanding during the year, if dilutive.

3.8 Financial assets

All financial assets are initially recorded at fair value and designated upon inception into one of the following four categories: held-to-maturity, available-for-sale, loans-and-receivables or at fair value through profit or loss (“FVTPL”). The Company initially recognizes loans and receivables on the date they are originated. All other financial assets are recognized on the trade date at which the Company becomes party to the contractual provisions of the instruments.

Subsequent to initial recognition, financial assets classified as FVTPL are measured at fair value with unrealized gains and losses recognized through earnings. The Company’s other financial assets are classified as FVTPL.

Financial assets classified as loans-and-receivables and held-to-maturity are measured at amortized cost. The Company’s cash and cash equivalents and trade and other receivables are classified as loans-and-receivables.

Subsequent to initial recognition, financial assets classified as available-for-sale are measured at fair value with unrealized gains and losses recognized in other comprehensive income (loss) except for losses in value that are considered other than temporary. During the periods presented, the Company has not classified any financial assets as available-for-sale.

18

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 3. | Summary of Significant Accounting Policies (continued) |

Transactions costs associated with FVTPL financial assets are expensed as incurred, while transaction costs associated with all other financial assets are included in the initial carrying amount of the asset.

The Company derecognizes a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in which substantially all the rights and rewards of ownership of the financial asset are transferred.

3.9 Financial liabilities

All financial liabilities are initially recorded at fair value and designated upon inception as FVTPL or other-financial-liabilities on the trade date at which the Company becomes party to the contractual provisions of the instrument.

Financial liabilities classified as other-financial-liabilities are initially recognized at fair value less directly attributable transaction costs. After initial recognition, other-financial-liabilities are subsequently measured at amortized cost using the effective interest method. The effective interest method is a method of calculating the amortized cost of a financial liability and of allocating interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments through the expected life of the financial liability, or, where appropriate, a shorter period. The Company’s trade and other payables and convertible debt are classified as other-financial-liabilities.

Financial liabilities classified as FVTPL include financial liabilities held for trading and financial liabilities designated upon initial recognition as FVTPL. Derivatives, including separated embedded derivatives are also classified as FVTPL unless they are designated as effective hedging instruments. Fair value changes on financial liabilities classified as FVTPL are recognized through the statement of comprehensive loss. At August 31, 2017 and 2016 the Company’s warrant liability and the derivative in gold bullion loans have been classified as FVTPL.

The Company derecognizes a financial liability when its contractual obligations are discharged or cancelled, as they expire.

3.10 Impairment of financial assets

The Company assesses at each date of the statement of financial position whether a financial asset is impaired.

Assets carried at amortized cost

If there is objective evidence that an impairment loss on assets carried at amortized cost has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows discounted at the financial asset’s original effective interest rate. The carrying amount of the asset is then reduced by the amount of the impairment. The amount of the loss is recognized in profit or loss.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized, the previously recognized impairment loss is reversed to the extent that the carrying value of the asset does not exceed what the amortized cost would have been had the impairment not been recognized. Any subsequent reversal of an impairment loss is recognized in profit or loss.

19

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 3. | Summary of Significant Accounting Policies (continued) |

In relation to trade receivables, a provision for impairment is made and an impairment loss is recognized in profit and loss when there is objective evidence (such as the probability of insolvency or significant financial difficulties of the debtor) that the Company will not be able to collect all of the amounts due under the original terms of the invoice. The carrying amount of the receivable is reduced through use of an allowance account. Impaired debts are written off against the allowance account when they are assessed as uncollectible.

Available-for-sale

If an available-for-sale asset is impaired, an amount comprising the difference between its cost and its current fair value, less any impairment loss previously recognized in profit or loss, is transferred from equity to profit or loss. Reversals in respect of equity instruments classified as available-for-sale are not recognized in profit or loss.

3.11 Impairment of non-financial assets

At each date of the statement of financial position, the Company reviews the carrying amounts of its tangible and intangible assets to determine whether there is an indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). Where it is not possible to estimate the recoverable amount of an individual asset, the Company estimates the recoverable amount of the cash-generating unit to which the assets belong.

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (or cash-generating unit) is reduced to its recoverable amount. An impairment loss is recognized immediately in the statement of comprehensive loss, unless the relevant asset is carried at a re-valued amount, in which case the impairment loss is treated as a revaluation decrease.

Where an impairment loss subsequently reverses, the carrying amount of the asset (cash-generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognized for the asset (or cash-generating unit) in prior years.

3.12 Cash and cash equivalents

Cash and cash equivalents in the statement of financial position comprise cash at banks and on hand, and short term deposits with an original maturity of three months or less, which are readily convertible into a known amount of cash.

3.13 Related party transactions

Parties are considered to be related if one party has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions. Parties are considered to be related if they are subject to common control or are controlled by parties that have significant influence over the entity. Related parties may be individuals or corporate entities. A transaction is considered to be a related party transaction when there is a transfer of resources or obligations between related parties. Related party transactions that are in the normal course of business and have commercial substance are measured at the exchange amount, being the amount agreed by the parties to the transaction.

20

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 3. | Summary of Significant Accounting Policies (continued) |

3.14 Foreign currency transactions

Functional and presentation currency

Items included in the financial statements of each of the Company’s entities are measured using the currency of the primary economic environment in which the entity operates (“the functional currency”). The functional currency of the Company and each of its subsidiaries is USD. The consolidated financial statements are presented in Canadian Dollars (“CDN”) which is the Company’s presentation currency.

Transactions and balances

Transactions in foreign currencies are initially recorded by the Company’s subsidiaries at their respective functional currency spot rates at the date the transaction first qualifies for recognition. Monetary assets and liabilities denominated in foreign currencies are translated at the functional currency spot rates of exchange at the reporting date.

Differences arising on settlement or translation of monetary items are recognised in profit or loss with the exception of monetary items that are designated as part of the hedge of the Company’s net investment in a foreign operation. These are recognised in OCI until the net investment is disposed of, at which time, the cumulative amount is reclassified to profit or loss. Tax charges and credits attributable to exchange differences on those monetary items are also recorded in OCI.

Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rates at the dates of the initial transactions. Non-monetary items measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value is determined. The gain or loss arising on translation of non-monetary items measured at fair value is treated in line with the recognition of the gain or loss on the change in fair value of the item (i.e., translation differences on items whose fair value gain or loss is recognised in OCI or profit or loss are also recognised in OCI or profit or loss, respectively).

Group companies

On consolidation, the assets and liabilities of foreign operations are translated into CDN at the rate of exchange prevailing at the reporting date and their statements of profit or loss are translated at exchange rates prevailing at the dates of the transactions. The exchange differences arising on translation for consolidation are recognized in OCI. On disposal of a foreign operation, the component of OCI relating to that particular foreign operation is reclassified to profit or loss.

3.15 Significant accounting judgments and estimates

The preparation of these consolidated financial statements requires management to make judgements and estimates and form assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and reported amounts of revenues and expenses during the reporting period. On an ongoing basis, management evaluates its judgements and estimates in relation to assets, liabilities, revenue and expenses. Management uses historical experience and various other factors it believes to be reasonable under the given circumstances as the basis for its judgements and estimates. Actual outcomes may differ from these estimates under different assumptions and conditions. The most significant estimates relate to the appropriate depreciation rate for property, plant and equipment, the valuation of warrant liability, the recoverability of accounts receivable, the valuation of deferred income tax amounts, impairment testing of mineral properties and deferred exploration and property, plant and equipment and the calculation of share-based payments. The most significant judgements relate to the recognition of deferred tax assets and liabilities and asset retirement obligations, the determination of the economic viability of a project or mineral property and the determination of functional currencies.

21

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 3. | Summary of Significant Accounting Policies (continued) |

3.16 Inventory

Stockpiled ore and consumables are physically measured or estimated and valued at the lower of cost or net realizable value. Net realizable value is the estimated future sales price of the product the entity expects to realize when the product is processed and sold, less estimated costs to complete production and bring the product to sale. Where the time value of money is material, these future prices and costs to complete are discounted.

Consumables are valued at the lower of cost or net realizable value. Any provision for obsolescence is determined by reference to specific items. A regular review is undertaken to determine the extent of any provision for obsolescence.

3.17 Borrowing costs

Borrowing costs directly attributable to the acquisition, construction or production of an asset that necessarily takes a substantial period of time to get ready for its intended use or sale are capitalized as part of the cost of the asset. All other borrowing costs are expensed in the period in which they occur. Borrowing costs consist of interest and other costs that an entity incurs in connection with the borrowing of funds.

| 4. | Mineral Properties |

The Company explores or acquires gold or other precious metal concessions through its own efforts or through the efforts of its subsidiaries. All of the Company’s concessions are located in Tanzania.

The Company’s mineral interests in Tanzania are initially held under prospecting licenses granted pursuant to the Mining Act, 2010 (Tanzania) for a period of up to four years, and are renewable two times for a period of up to two years each. Annual rental fees for prospecting licenses are based on the total area of the license measured in square kilometres, multiplied by USD$100/sq.km for the initial period, USD$150/sq.km for the first renewal and USD$200/sq.km for the second renewal. With each renewal at least 50% of the licensed area, if greater than 20 square kilometres, must be relinquished and if the Company wishes to keep the relinquished one-half portion, it must file a new application for the relinquished portion. There is also an initial one-time “preparation fee” of USD$500 per license. Upon renewal, there is a renewal fee of USD$300 per license.

Section 30 of the Mining Act states that the amount that is to be spent on prospecting operations is to be prescribed by Regulation.

| Period | Minimum expenditure (US$) | |

| Initial period (4 years) | $500 per sq km for annum | |

| First renewal (3 years) | $1,000 per sq km for annum | |

| Second renewal (2 years) | $2,000 per sq km for annum |

Certain of the Company’s prospecting licenses are currently being renewed.

The Company assessed the carrying value of mineral properties and deferred exploration costs as at August 31, 2017 and recorded a write-down of $124,717 during the year ended August 31, 2017 (2016 - $3,516,268).

22

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 4. | Mineral Properties (continued) |

The continuity of expenditures on mineral properties is as follows:

Buckreef (a) | Kigosi (b) | Itetemia (c) | Luhala (d) | Lunguya (e) | Total | |||||||||||||||||||

| Balance, September 1, 2015 | $ | 23,153,374 | $ | 12,208,394 | $ | 6,080,438 | $ | 3,354,062 | $ | 3,353,923 | $ | 48,150,191 | ||||||||||||

| Exploration expenditures: | ||||||||||||||||||||||||

| Camp, field supplies and travel | 386,911 | 23,354 | - | - | - | 410,265 | ||||||||||||||||||

| License fees and exploration and field overhead | 773,388 | 222,506 | 35,865 | 5,853 | - | 1,037,612 | ||||||||||||||||||

| Geological consulting and field wages | 261 | - | - | - | - | 261 | ||||||||||||||||||

| Geophysical and geochemical | - | - | - | - | - | - | ||||||||||||||||||

| Property acquisition costs | - | - | - | - | - | - | ||||||||||||||||||

| Trenching and drilling | - | - | - | - | - | - | ||||||||||||||||||

| Recoveries | (279,203 | ) | - | - | - | - | (279,203 | ) | ||||||||||||||||

| 881,357 | 245,860 | 35,865 | 5,853 | - | 1,168,935 | |||||||||||||||||||

| 24,034,731 | 12,454,254 | 6,116,303 | 3,359,915 | 3,353,923 | 49,319,126 | |||||||||||||||||||

| Write-offs | - | - | (153,588 | ) | (8,757 | ) | (3,353,923 | ) | (3,516,268 | ) | ||||||||||||||

| Balance, August 31, 2016 | $ | 24,034,731 | $ | 12,454,254 | $ | 5,962,715 | $ | 3,351,158 | $ | - | $ | 45,802,858 | ||||||||||||

| Exploration expenditures: | ||||||||||||||||||||||||

| Camp, field supplies and travel | 187,940 | 19,565 | - | - | - | 207,505 | ||||||||||||||||||

| License fees and exploration and field overhead | 2,527,005 | 67,942 | 17,738 | 5,988 | - | 2,618,673 | ||||||||||||||||||

| Geological consulting and field wages | 206,722 | - | - | - | - | 206,722 | ||||||||||||||||||

| Geophysical and geochemical | - | - | - | - | - | - | ||||||||||||||||||

| Property acquisition costs | 168,284 | - | - | - | - | 168,284 | ||||||||||||||||||

| Trenching and drilling | - | - | - | - | - | - | ||||||||||||||||||

| Recoveries | (25,408 | ) | - | - | - | - | (25,408 | ) | ||||||||||||||||

| Foreign exchange translation | (1,037,832 | ) | (513,491 | ) | (244,842 | ) | (137,449 | ) | - | (1,933,614 | ) | |||||||||||||

| 2,026,711 | (425,984 | ) | (227,104 | ) | (131,461 | ) | - | 1,242,162 | ||||||||||||||||

| 26,061,442 | 12,028,270 | 5,735,611 | 3,219,697 | - | 47,045,020 | |||||||||||||||||||

| Write-offs | - | (124,717 | ) | - | - | - | (124,717 | ) | ||||||||||||||||

| Balance, August 31, 2017 | $ | 26,061,442 | $ | 11,903,553 | $ | 5,735,611 | $ | 3,219,697 | $ | - | $ | 46,920,303 | ||||||||||||

23

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 4. | Mineral Properties (continued) |

(a) Buckreef Gold Project:

On December 21, 2010, the Company announced it was the successful bidder for the Buckreef Gold Mine Re-development Project in northern Tanzania (the “Buckreef Project”). Pursuant to the agreement dated December 16, 2010, the Company paid USD $3,000,000 to the State Mining Company (“Stamico”). On October 25, 2011, a Definitive Joint Venture Agreement was entered into with Stamico for the development of the Buckreef Gold Project. Through its wholly-owned subsidiary, Tanzam, the Company holds a 55% interest in the joint venture company, Buckreef Gold Company Limited, with Stamico holding the remaining 45%.

The Company has 100% control over all aspects of the joint venture. In accordance with the joint venture agreement, the Company has to arrange financing, incur expenditures, make all decisions and operate the mine in the future. The Company’s obligations and commitments include completing a preliminary economic assessment, feasibility study and mine development. Stamico’s involvement is to contribute the licences and rights to the property and receive a 45% interest in Buckreef Project.

The joint venture agreement contains an obligation clause regarding the commissioning date for the plant. The clause becomes effective only in the event the property is not brought into production before a specified future date which was originally estimated to be in December 2015. The Company shall be entitled to extend the date for one additional year:

i) for the extension year, on payment to Stamico of US$500,000;

ii) for the second extension year, on payment to Stamico of US$625,000; and

iii) for each subsequent extension year, on payment to Stamico of US$750,000.

The Company has received a request letter from Stamico regarding the status of the penalty payment and has responded that no penalty is due at this time. The Company has received a subsequent letter from Stamico regarding request for payment. It remains the Company’s position that no penalty is due at this time, but the Company and Stamico have been engaged in settlement discussions to resolve this issue, and a payment of $172,330 has been made in connection with the settlement discussions to be applied towards the amount owing with the remainder to be paid out of proceeds of production.

The Company has recognized a non-controlling interest (NCI) in respect of Stamico’s 45% interest in the Consolidated Financial Statements based on the initial payment by the Company to Stamico and will be adjusted based on annual exploration and related expenditures. Stamico has a free carried interest and does not contribute to exploration expenses.

There is a supervisory board made up of 4 directors of Tanzam and 3 directors of Stamico, whom are updated with periodic reports and review major decisions. Amounts paid to Stamico and subsequent expenditures on the property are capitalized under Mineral Properties or Inventories for costs directly related to the extraction and processing of ore and reported under Buckreef Gold Company Limited.

Force Majeure:

On February 5, 2016, the Company, through its subsidiary Tanzam provided notice of Force Majeure under its agreement with STAMICO. The notice of Force Majeure is based upon the invasion and forced occupation by several hundred illegal miners of the Company’s properties including the South Pit and other areas within the Buckreef site, thereby endangering the Company’s team and preventing Tanzam from continuing its mining operations.

24

Tanzanian Royalty Exploration Corporation

Notes to the Consolidated Financial Statements

For the Years Ended August 31, 2017 and 2016

| 4. | Mineral Properties (continued) |

(a) Buckreef Gold Project (continued):

Force Majeure (continued):

The Company was requested by the Deputy Minister of Energy and Minerals to provide an area of access for artisanal miners within 14 days of notice. The Company identified three potential areas with one to be designated for true artisanal mining, meaning without the use of mechanized mining equipment. Mining would not be allowed below the water table. The Company would also require artisanal miners to operate responsibly in accordance with Tanzanian mining and environmental law, and land and water requirements.

On the 15th day following notice, the occupation by illegal miners occurred as the Company refused to allow access to areas that represent a material portion of the deposit according to the Company’s NI 43-101 technical reports. The Company has communicated to both the Minister and the Deputy Minister, indicating its willingness to provide an area of access to legitimate artisanal miners.

On June 9th, 2016, Force Majeure was lifted.

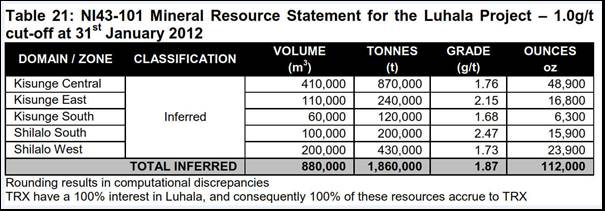

(b) Kigosi:

The Kigosi Project is principally located within the Kigosi Game Reserve controlled area. Through prospecting and mining option agreements, the Company has options to acquire interests in several Kigosi prospecting licenses. The Company has an agreement with Stamico providing Stamico a 15% carried interest in the Kigosi Project.

The Kigosi Mining License was granted by the Ministry of Energy and Minerals to Tanzam, (wholly owned subsidiary of Tanzanian Royalty). The official signing ceremony of the Kigosi Mining License was held in October 2013 and was attended by the Company and Ministry for Energy and Minerals representatives. The area remains subject to a Game Reserve Declaration Order. Upon repeal or amendment of that order by degazzeting the respective license by the Tanzanian Government, the Company will be legally entitled to exercise its rights under the Mineral Rights and Mining Licence.

During the year ended August 31, 2017, the Company decided to abandon certain licenses within the Kigosi project as they come up for renewal, as such, a write off of $124,717 was taken for these licenses related to the property (year ended August 31, 2016 - $nil).

(c) Itetemia Project: