Document | | | | | | | | | | | |

Table of Contents | |

| Management’s Discussion and Analysis | |

| 1. | HIGHLIGHTS | |

| 2. | INTRODUCTION | |

| 3. | ABOUT CAE | |

| 3.1 | Who we are | |

| 3.2 | Our mission | |

| 3.3 | Our vision | |

| 3.4 | Our strategy | |

| 3.5 | Our operations | |

| 4. | FOREIGN EXCHANGE | |

| 5. | CONSOLIDATED RESULTS | |

| 5.1 | Results from operations – fourth quarter of fiscal 2024 | |

| 5.2 | Results from operations – fiscal 2024 | |

| 5.3 | Restructuring, integration and acquisition costs | |

| 5.4 | Impairment of goodwill | |

| | 5.5 | Consolidated adjusted orders and adjusted backlog | |

| 6. | RESULTS BY SEGMENT | |

| 6.1 | Civil Aviation | |

| 6.2 | Defense and Security | |

| | | |

| 7. | CONSOLIDATED CASH MOVEMENTS AND LIQUIDITY | |

| 7.1 | Consolidated cash movements | |

| 7.2 | Sources of liquidity | |

| 7.3 | Government participation | |

| 7.4 | Contingencies and commitments | |

| 8. | CONSOLIDATED FINANCIAL POSITION | |

| 8.1 | Consolidated capital employed | |

| | | |

| 8.2 | Off balance sheet arrangements | |

| 8.3 | Financial instruments | |

| 9. | DISCONTINUED OPERATIONS | |

| | |

| | |

| 10. | BUSINESS RISK AND UNCERTAINTY | |

| 10.1 | Strategic risks | |

| 10.2 | Operational risks | |

| 10.3 | Cybersecurity risks | |

| 10.4 | Talent risks | |

| 10.5 | Financial risks | |

| 10.6 | Legal and regulatory risks | |

| 10.7 | Environmental, social & governance risks | |

| 10.8 | Reputational risks | |

| 10.9 | Technological risks | |

| 11. | RELATED PARTY TRANSACTIONS | |

| 12. | NON-IFRS AND OTHER FINANCIAL MEASURES AND SUPPLEMENTARY NON-FINANCIAL INFORMATION | |

| 12.1 | Non-IFRS and other financial measure definitions | |

| 12.2 | Supplementary non-financial information definitions | |

| 12.3 | Non-IFRS measure reconciliations | |

| 13. | CHANGES IN ACCOUNTING POLICIES | |

| 13.1 | New and amended standards adopted | |

| 13.2 | New and amended standards not yet adopted | |

| 13.3 | Use of judgements, estimates and assumptions | |

| 14. | INTERNAL CONTROL OVER FINANCIAL REPORTING | |

| | | |

| | | |

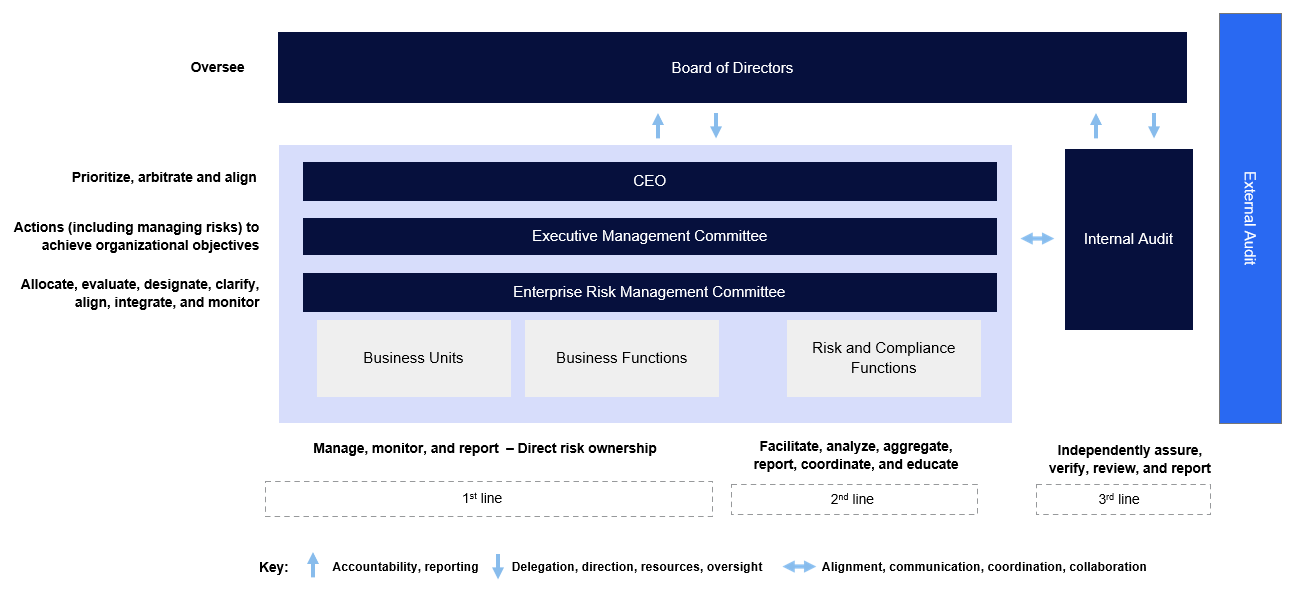

| 15. | OVERSIGHT ROLE OF AUDIT COMMITTEE AND BOARD OF DIRECTORS | |

| 16. | ADDITIONAL INFORMATION | |

| 17. | SELECTED FINANCIAL INFORMATION | |

| |

| |

| |

| |

Management’s Discussion and Analysis

for the fourth quarter and year ended March 31, 2024

1. HIGHLIGHTS

RE-BASELINING OF THE DEFENSE AND SECURITY BUSINESS, DEFENSE AND SECURITY IMPAIRMENTS AND ACCELERATED RISK RECOGNITION ON LEGACY CONTRACTS

On May 21, 2024, we announced a re-baselining of our Defense and Security business along with impairments and unfavourable contract adjustments related to eight previously identified fixed-price legacy contracts (the Legacy Contracts, as defined in Section 6.2 “Defense and Security” of this MD&A). In the fourth quarter of fiscal 2024, we recorded a $568.0 million non-cash impairment of Defense and Security goodwill and $90.3 million in unfavourable contract profit adjustments as a result of accelerated risk recognition on the Legacy Contracts. We also recorded a $35.7 million impairment of related technology and other non-financial assets which are principally related to the Legacy Contracts.

DISCONTINUED OPERATIONS AND RECLASSIFICATION OF COMPARATIVE FIGURES

On February 16, 2024, we announced the closing of the sale of our Healthcare business. In accordance with the requirements of IFRS 5, Non-current Assets Held for Sale and Discontinued Operations, the Healthcare segment is presented as discontinued operations. Consequently, the comparative consolidated income statement and consolidated statement of comprehensive income are reclassified as if the operation had been discontinued from the beginning of the comparative year. Unless otherwise indicated, results are presented on a continuing operations basis.

OTHER HIGHLIGHTS

On May 21, 2024, we announced that our Board of Directors approved, subject to the approval of the Toronto Stock Exchange (TSX), the re-establishment of a normal course issuer bid (NCIB). The NCIB is expected to commence shortly after regulatory approvals are obtained. The common shares that may be repurchased under such program over a period of approximately one year will represent up to 5 percent of the issued and outstanding common shares. The establishment of the program and the timing and amount of any purchases under the program is subject to regulatory approvals.

On May 21, 2024, we announced the appointment of Nick Leontidis to the new position of Chief Operating Officer (COO) as part of a senior leadership reorganization to further strengthen our execution capabilities and drive additional synergies between our Defense and Security business and Civil Aviation business. Mr. Leontidis was previously CAE’s Group President, Civil Aviation. As COO, he will have overall responsibility for both of CAE’s Civil and Defense business segments.

FINANCIAL

FOURTH QUARTER OF FISCAL 2024

| | | | | | | | | | | | | | | | | | | | | | | |

| (amounts in millions, except per share amounts, adjusted ROCE and book-to-sales ratio) | | Q4-2024 | | Q4-2023 | Variance $ | Variance % |

| Performance | | | | | | | |

| Revenue | $ | 1,126.3 | | $ | 1,197.4 | | $ | (71.1) | | (6 | %) |

| Operating (loss) income | $ | (533.0) | | $ | 178.3 | | $ | (711.3) | | (399 | %) |

| Adjusted segment operating income1 | $ | 125.7 | | $ | 193.4 | | $ | (67.7) | | (35 | %) |

| Net (loss) income attributable to equity holders of the Company | $ | (504.7) | | $ | 93.6 | | $ | (598.3) | | (639 | %) |

| Basic and diluted earnings per share (EPS) – continuing operations | $ | (1.58) | | $ | 0.29 | | $ | (1.87) | | (645 | %) |

| | | | | | | |

| Basic and diluted EPS – discontinued operations | $ | 0.06 | | $ | 0.02 | | $ | 0.04 | | 200 | % |

| | | | | | | |

Adjusted EPS1 | $ | 0.12 | | $ | 0.33 | | $ | (0.21) | | (64 | %) |

| Net cash provided by operating activities | $ | 215.2 | | $ | 180.6 | | $ | 34.6 | | 19 | % |

Free cash flow1 | $ | 191.1 | | $ | 147.6 | | $ | 43.5 | | 29 | % |

| Liquidity and Capital Structure | | | | | | | |

Capital employed1 | $ | 7,216.8 | | $ | 7,621.4 | | $ | (404.6) | | (5 | %) |

| | | | | | | |

Adjusted return on capital employed (ROCE)1 | % | 5.9 | | % | 5.6 | | | | |

| Total debt | $ | 3,074.3 | | $ | 3,250.1 | | $ | (175.8) | | (5 | %) |

Net debt1 | $ | 2,914.2 | | $ | 3,032.5 | | $ | (118.3) | | (4 | %) |

| Growth | | | | | | | |

Adjusted order intake1 | $ | 1,550.5 | | $ | 1,406.2 | | $ | 144.3 | | 10 | % |

Adjusted backlog1 | $ | 12,183.9 | | $ | 10,796.4 | | $ | 1,387.5 | | 13 | % |

Book-to-sales ratio1 | | 1.38 | | | 1.17 | | | | |

| Book-to-sales ratio for the last 12 months | | 1.15 | | | 1.21 | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

1 Non-IFRS financial measure, non-IFRS ratio, capital management measure, or supplementary financial measure. Refer to Section 12.1 “Non-IFRS and other financial measure definitions" and Section 12.3 "Non-IFRS measure reconciliations” of this MD&A for the definitions and reconciliations of these measures to the most directly comparable measure under IFRS.

CAE Financial Report 2024 I 1

Management’s Discussion and Analysis

FISCAL 2024

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | |

| (amounts in millions, except per share amounts) | | FY2024 | | FY2023 | Variance $ | Variance % |

| Performance | | | | | | | |

| Revenue | $ | 4,282.8 | | $ | 4,010.6 | | $ | 272.2 | | 7 | % |

| Operating (loss) income | $ | (185.4) | | $ | 466.0 | | $ | (651.4) | | (140 | %) |

| Adjusted segment operating income | $ | 549.7 | | $ | 538.4 | | $ | 11.3 | | 2 | % |

| Net (loss) income attributable to equity holders of the Company | $ | (325.3) | | $ | 220.6 | | $ | (545.9) | | (247 | %) |

| Basic and diluted EPS – continuing operations | $ | (1.02) | | $ | 0.69 | | $ | (1.71) | | (248 | %) |

| | | | | | | |

| Basic and diluted EPS – discontinued operations | $ | 0.07 | | $ | 0.01 | | $ | 0.06 | | 600 | % |

| | | | | | | |

| Adjusted EPS | $ | 0.87 | | $ | 0.87 | | $ | — | | — | % |

| Net cash provided by operating activities | $ | 566.9 | | $ | 408.4 | | $ | 158.5 | | 39 | % |

| Free cash flow | $ | 418.2 | | $ | 333.1 | | $ | 85.1 | | 26 | % |

2. INTRODUCTION

In this management’s discussion and analysis (MD&A), we, us, our, CAE and Company refer to CAE Inc. and its subsidiaries. Unless we have indicated otherwise:

–This year and 2024 mean the fiscal year ending March 31, 2024;

–Last year, prior year and a year ago mean the fiscal year ended March 31, 2023;

–Dollar amounts are in Canadian dollars.

This MD&A was prepared as of May 27, 2024. It is intended to enhance the understanding of our annual consolidated financial statements and notes for the year ended March 31, 2024 and should therefore be read in conjunction with this document. We have prepared it to help you understand our business, performance and financial condition for the year ended March 31, 2024. Except as otherwise indicated, all financial information has been reported in accordance with IFRS Accounting Standards (IFRS), as issued by the International Accounting Standards Board (IASB). All quarterly information disclosed in the MD&A is based on unaudited figures.

The MD&A provides you with a view of CAE as seen through the eyes of management and helps you understand the Company from a variety of perspectives:

–Our mission;

–Our vision;

–Our strategy;

–Our operations;

–Foreign exchange;

–Consolidated results;

–Results by segment;

–Consolidated cash movements and liquidity;

–Consolidated financial position;

–Discontinued operations;

–Business risk and uncertainty;

–Related party transactions;

–Non-IFRS and other financial measures and supplementary non-financial information;

–Changes in accounting policies;

–Internal control over financial reporting;

–Oversight role of Audit Committee and Board of Directors (the Board).

You will find our most recent financial report and Annual Information Form (AIF) on our website (www.cae.com), SEDAR+ (www.sedarplus.ca) and EDGAR (www.sec.gov). Holders of CAE’s securities may also request a printed copy of the Company’s consolidated financial statements and MD&A free of charge by contacting Investor Relations (investor.relations@cae.com).

NON-IFRS AND OTHER FINANCIAL MEASURES

This MD&A includes non-IFRS financial measures, non-IFRS ratios, capital management measures and supplementary financial measures. These measures are not standardized financial measures prescribed under IFRS and therefore should not be confused with, or used as an alternative for, performance measures calculated according to IFRS. Furthermore, these measures should not be compared with similarly titled measures provided or used by other issuers. Management believes that these measures provide additional insight into our operating performance and trends and facilitate comparisons across reporting periods.

2 I CAE Financial Report 2024

Management’s Discussion and Analysis

Performance Measures

–Gross profit margin (or gross profit as a % of revenue);

–Operating income margin (or operating income as a % of revenue);

–Adjusted segment operating income or loss;

–Adjusted segment operating income margin (or adjusted segment operating income as a % of revenue);

–Adjusted effective tax rate;

–Adjusted net income or loss;

–Adjusted earnings or loss per share (EPS);

–EBITDA and Adjusted EBITDA;

–Free cash flow.

Liquidity and Capital Structure Measures

–Non-cash working capital;

–Capital employed;

–Adjusted return on capital employed (ROCE);

–Net debt;

–Net debt-to-capital;

–Net debt-to-EBITDA and net debt-to-adjusted EBITDA;

–Maintenance and growth capital expenditures.

Growth Measures

–Adjusted order intake;

–Adjusted backlog;

–Book-to-sales ratio.

Definitions of all non-IFRS and other financial measures are provided in Section 12.1 “Non-IFRS and other financial measure definitions” of this MD&A to give the reader a better understanding of the indicators used by management. In addition, when applicable, we provide a quantitative reconciliation of the non-IFRS and other financial measures to the most directly comparable measure under IFRS. Refer to Section 12.1 “Non-IFRS and other financial measure definitions” for references to where these reconciliations are provided.

ABOUT MATERIAL INFORMATION

This MD&A includes the information we believe is material to investors after considering all circumstances, including potential market sensitivity. We consider something to be material if:

–It results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares; or

–It is likely that a reasonable investor would consider the information to be important in making an investment decision.

CAUTION REGARDING FORWARD-LOOKING STATEMENTS

This MD&A includes forward-looking statements about our activities, events and developments that we expect to or anticipate may occur in the future including, for example, statements about our vision, strategies, market trends and outlook, future revenues, earnings, cash flow growth, profit trends, growth capital spending, expansions and new initiatives, including initiatives that pertain to environmental, social and governance (ESG) matters, financial obligations, available liquidities, expected sales, general economic and political outlook, inflation trends, prospects and trends of an industry, expected annual recurring cost savings from operational excellence programs, our management of the supply chain, estimated addressable markets, demands for CAE’s products and services, our access to capital resources, our financial position, the expected accretion in various financial metrics, the expected capital returns to shareholders, our business outlook, business opportunities, objectives, development, plans, growth strategies and other strategic priorities, and our competitive and leadership position in our markets, the expansion of our market shares, CAE's ability and preparedness to respond to demand for new technologies, the sustainability of our operations, our ability to retire the Legacy Contracts (as defined in Section 6.2 “Defense and Security” of this MD&A) as expected and to manage and mitigate the risks associated therewith, the impact of the retirement of the Legacy Contracts and other statements that are not historical facts. Since forward-looking statements and information relate to future events or future performance and reflect current expectations or beliefs regarding future events, they are typically identified by words such as “anticipate”, “believe”, “could”, “estimate”, “expect”, “intend”, “likely”, “may”, “plan”, “seek”, “should”, “will”, “strategy”, “future” or the negative thereof or other variations thereon suggesting future outcomes or statements regarding an outlook. All such statements constitute "forward-looking statements" within the meaning of applicable Canadian securities legislation and “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. By their nature, forward‑looking statements require us to make assumptions and are subject to inherent risks and uncertainties associated with our business which may cause actual results in future periods to differ materially from results indicated in forward‑looking statements. While these statements are based on management’s expectations and assumptions regarding historical trends, current conditions and expected future developments, as well as other factors that we believe are reasonable and appropriate in the circumstances, readers are cautioned not to place undue reliance on these forward-looking statements as there is a risk that they may not be accurate.

CAE Financial Report 2024 I 3

Management’s Discussion and Analysis

Important risks that could cause such differences include, but are not limited to, strategic risks, such as geopolitical uncertainty, global economic conditions, competitive business environment, original equipment manufacturer (OEM) leverage and encroachment, inflation, international scope of our business, level and timing of defence spending, constraints within the civil aviation industry, our ability to penetrate new markets, research and development (R&D) activities, evolving standards and technology innovation and disruption, length of sales cycle, business development and awarding of new contracts, strategic partnerships and long-term contracts, risk that we cannot assure investors that we will effectively manage our growth, estimates of market opportunity and competing priorities; operational risks, such as supply chain disruptions, program management and execution, mergers and acquisitions, business continuity, subcontractors, fixed price and long-term supply contracts, our continued reliance on certain parties and information, and health and safety; cybersecurity risks; talent risks, such as recruitment, development and retention, ability to attract, recruit and retain key personnel and management, corporate culture and labour relations; financial risks, such as availability of capital, customer credit risk, foreign exchange, effectiveness of internal controls over financial reporting, liquidity risk, interest rate volatility, returns to shareholders, shareholder activism, estimates used in accounting, impairment risk, pension plan funding, indebtedness, acquisition and integration costs, sales of additional common shares, market price and volatility of our common shares, seasonality, taxation matters and adjusted backlog; legal and regulatory risks, such as data rights and governance, U.S. foreign ownership, control or influence mitigation measures, compliance with laws and regulations, insurance coverage potential gaps, product-related liabilities, environmental laws and regulations, government audits and investigations, protection of our intellectual property and brand, third-party intellectual property, foreign private issuer status, and enforceability of civil liabilities against our directors and officers; ESG risks, such as extreme climate events and the impact of natural or other disasters (including effects of climate change) and more acute scrutiny and perception gaps regarding ESG matters; reputational risks; and technological risks, such as information technology (IT) and reliance on third-party providers for information technology systems and infrastructure management. The foregoing list is not exhaustive and other unknown or unpredictable factors could also have a material adverse effect on the performance or results of CAE. Additionally, differences could arise because of events announced or completed after the date of this MD&A. You will find more information about the risks and uncertainties affecting our business in Section 10 “Business risk and uncertainty” of this MD&A. Readers are cautioned that any of the disclosed risks could have a material adverse effect on CAE’s forward-looking statements. Readers are also cautioned that the risks described above and elsewhere in this MD&A are not necessarily the only ones we face; additional risks and uncertainties that are presently unknown to us or that we may currently deem immaterial may adversely affect our business.

Except as required by law, we disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise. The forward-looking information and statements contained in this MD&A are expressly qualified by this cautionary statement.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based on information available to us as of the date of this MD&A. While we believe that information provides a reasonable basis for these statements, that information may be limited or incomplete. Our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely on these statements.

MATERIAL ASSUMPTIONS

The forward-looking statements set out in this MD&A are based on certain assumptions including, without limitation: the prevailing market conditions, geopolitical instability, the customer receptivity to our training and operational support solutions, the accuracy of our estimates of addressable markets and market opportunity, the realization of anticipated annual recurring cost savings and other intended benefits from restructuring initiatives and operational excellence programs, the ability to respond to anticipated inflationary pressures and our ability to pass along rising costs through increased prices, the actual impact to supply, production levels, and costs from global supply chain logistics challenges, the stability of foreign exchange rates, the ability to hedge exposures to fluctuations in interest rates and foreign exchange rates, the availability of borrowings to be drawn down under, and the utilization, of one or more of our senior credit agreements, our available liquidity from cash and cash equivalents, undrawn amounts on our revolving credit facility, the balance available under our receivable purchase facility, the assumption that our cash flows from operations and continued access to debt funding will be sufficient to meet financial requirements in the foreseeable future, access to expected capital resources within anticipated timeframes, no material financial, operational or competitive consequences from changes in regulations affecting our business, our ability to retain and attract new business, our ability to effectively execute and retire the Legacy Contracts while managing the risks associated therewith, and our ability to complete the integration of the AirCentre business and the separation of the CAE Healthcare business within the anticipated time periods and at the expected cost levels. Air travel is a major driver for CAE's business and management relies on analysis from the International Air Transport Association (IATA) to inform its assumptions about the rate and profile of recovery in its key civil aviation market. Accordingly, the assumptions outlined in this MD&A and, consequently, the forward-looking statements based on such assumptions, may turn out to be inaccurate. For additional information, including with respect to other assumptions underlying the forward-looking statements made in this MD&A, refer to Section 10 “Business risk and uncertainty” of this MD&A.

4 I CAE Financial Report 2024

Management’s Discussion and Analysis

3. ABOUT CAE

3.1 Who we are

At CAE, we equip people in critical roles with the expertise and solutions to create a safer world. As a technology company, we digitalize the physical world, deploying software-based simulation training and critical operations support solutions. Above all else, we empower pilots, cabin crew, maintenance technicians, airlines, business aviation operators and defence and security forces to perform at their best every day and when the stakes are the highest. Around the globe, we’re everywhere customers need us to be with approximately 13,000 employees in more than 240 sites and training locations in over 40 countries. CAE represents more than 75 years of industry firsts–the highest-fidelity flight and mission simulators as well as training programs powered by digital technologies. We embed sustainability in everything we do. Today and tomorrow, we’ll make sure our customers are ready for the moments that matter.

CAE’s common shares are listed on the Toronto and New York stock exchanges (TSX / NYSE) under the symbol CAE.

3.2 Our mission

To lead at the frontier of digital immersion with high-tech training and operational support solutions to make the world a safer place.

3.3 Our vision

To be the worldwide partner of choice in civil aviation and defence and security by revolutionizing our customers’ training and critical operations with digitally immersive solutions to elevate safety, efficiency and readiness.

3.4 Our strategy

CAE’s four strategic pillars

There are four fundamental pillars that underpin our strategy and investment thesis:

–Efficient growth;

–Technology and market leadership;

–Revolutionizing training and critical operations;

–Skills and culture.

Efficient growth

Our business features a high degree of recurring revenues due to the underlying characteristics of our technology-enabled solutions and regulatory requirements across our markets. We seek to maximize the benefits of our strong competitive position to deliver premium growth and profitability through a focus on operational rigour, cost optimization, capital efficiency, and a disciplined approach to pursuing organic and inorganic growth.

Technology and market leadership

We have a rich and long-dated history of customer centricity, innovation and delivering state-of-the-art technology solutions that define the forefront of the industries we operate in. As a result, we constantly seek new ways to enhance the performance of our customers by fostering a culture of continuous improvement and innovation. This drives technology leadership, deeper customer partnerships, and new customer development, enabling us to capitalize on the ample headroom in our large, growing addressable markets.

Revolutionizing training and critical operations

We are a global leader in the application of training, digital immersion, critical operations, and modelling and simulation technologies. We seek to use data-driven applications and advanced analytics to produce measurable and demonstrated outcomes in our markets. The efficacy of our technology solutions enables customized, collaborative, and multi-domain offerings. Furthermore, our technologies are deployed with a focus on driving sustainability.

Skills and culture

Our core values are innovation, integrity, empowerment, excellence and One CAE. We employ these values across a diverse global team to drive a unique social impact. We seek to create an employee experience and environment that values teamwork, professional growth, and engagement. As a result, our employees across the globe share a passion to prepare our customers for the moments that matter.

CAE Financial Report 2024 I 5

Management’s Discussion and Analysis

3.5 Our operations

Our operations are managed through two segments:

–Civil Aviation – We provide comprehensive training solutions for flight, cabin, maintenance and ground personnel in commercial, business and helicopter aviation, a complete range of flight simulation training devices, ab initio pilot training and crew sourcing services, as well as aircraft flight operations solutions. The civil aviation market includes major commercial airlines, regional airlines, business aircraft operators, civil helicopter operators, aircraft manufacturers, third-party training centres, flight training organizations, maintenance, repair and overhaul organizations (MRO) and aircraft finance leasing companies;

–Defense and Security – We are a global training and simulation provider delivering scalable, platform-independent solutions that enable and enhance force readiness and security. The defence and security market includes defence forces, OEMs, government agencies and public safety organizations worldwide.

On February 16, 2024, we announced the closing of the sale of CAE’s Healthcare business. The Healthcare segment is presented as discontinued operations and you will find more details in Section 9 “Discontinued operations” of this MD&A.

CIVIL AVIATION MARKET

We have the unique capability and global scale to address the total lifecycle needs of the professional pilot, from cadet to captain, with our comprehensive aviation training solutions. We are the world’s largest provider of civil aviation training services. Our deep industry experience and thought leadership, large installed base, strong relationships and reputation as a trusted partner enable us to access a broader share of the market than any other company in our industry. We provide aviation training services in more than 35 countries and through our broad global network of approximately 70 sites, we serve all sectors of civil aviation including airlines and other commercial, business and helicopter aviation operators.

Among our thousands of customers, we have long-term training centre operations, training services agreements and joint ventures with approximately 50 major airlines and aircraft operators around the world. Our range of training solutions includes product and service offerings for pilots, cabin crew and aircraft maintenance technicians, training centre operations, curriculum development, courseware solutions and consulting services. We currently manage 343 full-flight simulators (FFSs), including those operating in our joint ventures. We offer industry-leading technology, and we are shaping the future of training through innovations such as our next generation training systems, including CAE Real-time Insights and Standardized Evaluations (CAE Rise), which improves training quality, objectivity and efficiency through the integration of untapped flight and simulator data-driven insights into training. In the development of new pilots, we operate the largest ab initio flight training network in the world and have approximately 20 cadet training programs globally. With our CAE flight operation solutions, we have further strengthened our position as a technology leader, complementing our flight simulator and training solutions while increasing our total addressable market.

Quality, fidelity, reliability and innovation are hallmarks of the CAE brand in flight simulation and we are the world leader in the development of civil flight simulators. We continuously innovate our processes and lead the market in the design, manufacture and integration of civil FFSs for major and regional commercial airlines, business aircraft operators, third-party training centres and OEMs. For example, as we are entering a new era of aviation with Advanced Air Mobility (AAM), disruptive aerospace companies are building new aircraft types from the ground up. This will create a large demand for trained professional pilots to safely fly both passengers and cargo across markets. CAE has already partnered with five electric vertical takeoff and landing (eVTOL) developers in order to support the evolution of this new industry. We are positioned to develop the pilot workforce of the future and ensure safe introduction of eVTOL operations by leveraging our technologies and expertise in aviation safety.

We have established a wealth of experience in developing first‑to‑market simulators for more than 35 types of aircraft models. Our flight simulation equipment, including FFSs, are designed to meet the rigorous demands of their long and active service lives, often spanning several decades of continuous use. Our global reach enables us to provide best-in-class support services such as real-time, remote monitoring and enables us to leverage our extensive worldwide network of spare parts and service teams.

We believe the Civil Aviation segment is positioned as a gateway in a highly regulated, secular growth market, with an addressable market estimated at approximately $6.5 billion, and headroom for growth.

Market drivers

Demand for training and flight operations solutions in the civil aviation market is driven by the following:

–Pilot and maintenance training and industry regulations;

–Safety and efficiency imperatives of commercial airlines and business aircraft operators;

–Expected long-term secular global growth in air travel;

–Expected long-term growth, including new aircraft deliveries and renewal of the active fleet of commercial and business aircraft;

–Demand for trained aviation professionals;

–Complexity of flight operations solutions;

–Emergence of the newer market for advanced air mobility.

6 I CAE Financial Report 2024

Management’s Discussion and Analysis

Pilot and maintenance training and industry regulations

Civil aviation training is a largely recurring business driven by a highly-regulated environment through global and domestic standards for pilot licensing and certification, amongst other regulatory requirements. These recurring training requirements are mandatory and are regulated by national and international aviation regulatory authorities such as the International Civil Aviation Organization (ICAO), European Aviation Safety Agency (EASA) and the U.S. Federal Aviation Administration (FAA).

In recent years, pilot certification processes and regulatory requirements have become increasingly stringent. Simulation-based pilot certification training is taking on a greater role internationally with the Multi-Crew Pilot License, with the Airline Transport Pilot certification requirements in the U.S. and with Upset Prevention and Recovery Training requirements mandated by both EASA and the FAA.

Safety and efficiency imperatives of commercial airlines and business aircraft operators

The commercial airline industry is competitive, requiring operators to continuously pursue operational excellence and efficiency initiatives to achieve satisfactory returns while continuing to maintain the highest safety standards and the confidence of air travelers. Airlines are finding it increasingly more effective to seek expertise in training from trusted partners such as CAE to address growing efficiency gaps, pilot capability gaps, evolving regulatory and training environments, and on-going aircraft programs. Additionally, CAE offers business jet pilots one of the most advanced, respected and accessible training programs in the industry, covering a wide spectrum of business aircrafts. Partnering with CAE gives immediate access to a world-wide fleet of simulators, courses, programs and instruction capabilities, and allows them flexibility in pursuing fleet training options that suit their business.

Our pilot training system, CAE Rise, is well positioned to elevate the pilot training experience. This system enables instructors to deliver training in accordance with airlines’ Standard Operating Procedures and enables instructors to objectively assess pilot competencies using live data during training sessions. Furthermore, CAE Rise augments instructors’ capability to identify pilot proficiency gaps and evolve airline training programs to the most advanced aviation safety standards, including Advanced Qualification Program and Evidence Based Training methodologies.

Expected long-term secular global growth in air travel

The secular growth in air travel results in long-term demand for flight, cabin, maintenance and ground personnel, which in turn drives demand for training and flight operations solutions.

In commercial aviation, as per the International Air Transport Association (IATA), global air passenger demand, measured by revenue passenger-kilometers (RPKs), has shown a strong increase of 37% for calendar 2023 compared to calendar 2022. For the first three months of calendar 2024, worldwide passenger traffic increased by 17% compared to the first three months of calendar 2023. Passenger traffic in Asia grew by 31%, while in Europe and North America it increased by 11% and 7% respectively over the same period.

Air cargo has seen a slight reduction in demand in recent months, with cargo tonne-kilometers down 2% for calendar 2023 compared to calendar 2022. For the first three months of calendar 2024, cargo tonne-kilometers increased by 13% compared to the first three months of calendar 2023.

In business aviation, the recovery post-COVID has been very strong, reaching a historical peak in calendar 2021. Both the FAA and Eurocontrol, the European Organisation for the Safety of Air Navigation, have shown a decrease in flight activity in the last year. The activity remains above the calendar 2019 average for both FAA and EASA. The FAA has shown a decrease of 4% in the total number of business jet flights, remaining at 12% above calendar 2019 levels, which includes all domestic and international flights over the past 12 months. The European business jet market has declined; according to Eurocontrol, the total number of business aviation flights in Europe have decreased by 6% over the same period, remaining stable with calendar 2019 levels.

Additionally, high inflation, the continuing military hostilities in Ukraine, the war between Hamas and Israel, and industry supply chain issues are causing disruptions to our Civil operations.

Expected long-term growth, including new aircraft deliveries and renewal of the active fleet of commercial and business aircraft

As an integrated training solutions provider, our long-term growth is closely tied to the active commercial and business aircraft fleet. Both commercial and business aviation fleets are expected to grow over the next decade, with significant backlogs reported by all OEMs. Short and medium-term growth in aircraft fleets may experience pressure as OEMs face supply, capacity, and certification challenges in delivering aircraft.

Major business jet OEMs are continuing with plans to introduce a variety of new aircraft models in the upcoming years including Dassault's Falcon 10X and the Bombardier Global 8000.

Our business aviation training network, comprehensive suite of training programs, key long-term OEM partnerships and ongoing network investments, position us well to effectively address the training demand arising from the entry-into-service of these new aircraft programs.

Our strong competitive moat in the aviation market, as defined by our extensive global training network, best-in-class instructors, comprehensive training programs and strength in training partnerships with airlines and business aircraft operators, allows us to effectively address training needs that arise from a growing active fleet of aircraft.

CAE Financial Report 2024 I 7

Management’s Discussion and Analysis

We are well positioned to leverage our technology leadership and expertise, including CAE 7000XR Series FFSs, CAE 400XR, 500XR, and 600XR Series Flight Training Devices and CAE Simfinity™ ground school solutions, in delivering training equipment solutions that address the growing training needs of airlines, business jet operators, helicopter operators and now AAM.

Demand for trained aviation professionals

Demand for trained aviation professionals is driven by air traffic growth, pilot retirements and by the number of aircraft deliveries. The expansion of global economies and operator aircraft fleets have resulted in demand for qualified aviation professionals to support the expected growth of the commercial and business aviation markets. We are well positioned in the training products and services market to address operators’ training requirements.

In June 2023, we released our 2023 Aviation Talent Forecast in which we estimated a global requirement of 1.3 million new aviation professionals over the next ten years to sustain growth in the civil aviation industry and support mandatory retirements. In the commercial aviation domain, the projections show demand for 1.2 million new aviation professionals, including 252,000 pilots, 328,000 maintenance technicians and 599,000 cabin crew professionals. The business aviation segment anticipates 106,000 professionals comprising 32,000 pilots and 74,000 maintenance technicians. Furthermore, we expect additional demand for new professionals in the emerging AAM sector with the future entry-into-service of eVTOL aircraft.

Complexity of flight operations solutions

Airlines need to closely manage their operations which come with daily challenges. To help optimize these operations, we offer a suite of flight service products. This suite of products provides solutions for flight operations including training management, crew management, flight management, airport management, in-flight services management and operations control. These products enable optimized management for schedule disruptions and allows for maximized resources for all personnel and aircrafts.

The benefits for our flight management solution include reduced fuel and carbon emissions for both regular and irregular operations. Our crew and airport management solution decreases disruption related crew costs and improved staff utilization. Finally, our movement management solution decreases delay and cancellation costs for airlines.

Emergence of the newer market for advanced air mobility

AAM and the developing eVTOL aircraft are emerging into a new era of aviation. We look at this new industry as a potential new avenue for pilot training. This technology is expected to promote community acceptance, instill confidence in the public, influence regulators to implement rules and policies that will stimulate growth, and ensure safety in this emerging industry.

DEFENSE AND SECURITY MARKET

Defense and Security addresses the critical needs of its customers operating in complex environments. The ever-changing global landscape requires the U.S. and its allies to prepare for the possibility of near-peer threats across multi‑domain operations in air, land, sea, space and cyber. Aligned with the priorities of U.S. and allied national defence strategies, we leverage our core training and simulation expertise with advanced digital technologies to deliver innovative and scalable solutions that address military training modernization and enhanced mission support requirements.

Our customers depend on synthetic training and next-generation situational awareness to ensure mission success through planning, preparation, and analysis in complex, multi-domain environments. Leveraging our global training system, we work with the military, government, and industry to deliver tailored solutions at the pace and point of need. From mixed-reality task training devices to high‑fidelity full‑mission simulators and aircrews to maintenance technicians, we support more than 85 different platforms across more than 145 sites and all domains. Our extensive suite of simulation-based technologies coupled with advanced capabilities like biometrics, real-time feedback, artificial intelligence (AI) and adaptive rehearsal scenarios enhances training to deliver scalable and integrated solutions to critical personnel.

Utilizing the strength and expertise that spans our global business, our solutions range from turnkey training centres to tailored live, virtual, and constructive solutions at government-owned locations. We are everywhere our customers need us to be with a global network and local expertise to deliver training efficacy at all proficiency levels. At the CAE Dothan Training Center in Alabama, U.S. Army fixed-wing candidates enter initial training, while the U.S. Air Force (USAF) initial entry training is maintained at CAE’s Pueblo Training Center in Colorado. Outside of the U.S., we provide basic and advanced flight training at NATO Flight Training Centres across multiple sites in Canada. Leveraging our expertise and strategic partnerships, we also support training in Europe with the International Flight Training School in Italy, a joint venture with Leonardo, along with providing ab initio training for the German Air Force at CAE’s Bremen Training Centre in Germany and a site in Montpellier, France.

8 I CAE Financial Report 2024

Management’s Discussion and Analysis

As a collaborative partner with industry and government, we enhance customer readiness and mitigate challenges to enable rapid modernization. New generational platforms and programs are rapidly transforming global training and require adaptive approaches to advance defence force readiness. We are essential team members for generational programs like Canada’s Future Aircrew Training (FAcT) through SkyAlyne, our joint venture with KF Aerospace, the MQ-9B SkyGuardian® Remotely Piloted Aircraft Systems (RPAS) with General Atomics Aeronautical Systems, Inc. as well as the Bell Textron’s tiltrotor aircraft for the U.S. Army Future Long Range Assault Aircraft. We continue to create opportunities through partnerships with Lockheed Martin on global C-130 training solutions, Boeing to support mission-critical platforms like the P-8 and CH-47 and our position as the Authorized Training Provider for Bombardier’s Global 6500 for the High Accuracy Detection and Exploitation System. Increasing complexities of contracts and systems drive the industry toward collaboration as we continue to leverage our strategic relationships and culture of innovation to meet the ever-changing market landscape.

The mission readiness of defence and security forces requires connecting customers, platforms and locations in a secured multi‑domain environment for training and rehearsal. A real-time enterprise network, like the USAF Simulators Common Architecture Requirements and Standards (SCARS), is critical in enhancing operational test and training infrastructure and supporting distributed mission training and multi-domain operations. We lead the integration and standardization of aircraft simulators on SCARS to operate and train together in a strict cyber secure environment. Leveraging our expertise on SCARS and other programs like Flight School Training Support Services for the U.S. Army, and the Platforms and Systems Training Contract for the Royal Australian Navy, we address the vast complexity and scale of digital environments, empower decision-makers at every level and advance the rigor of data‑driven capabilities and assessments so that our customers stay ahead of the evolving security landscapes.

We believe the Defense and Security segment is positioned as a strategic partner to achieve transformational digital training solutions, next-generation situational awareness, and multi-domain operations. We estimate our addressable defence market across all five domains to be approximately US$22.7 billion.

Market drivers

Demand for training and operational support solutions in the defence and security markets is driven by the following:

–Continued increase in defence spending as a reflection of heightened global tensions;

–Expected stable demand on enduring platforms and increased opportunities on next-generation systems and technology;

–Maximization of efficiencies through outsourced training and support services;

–Increased competition straining military aviation recruitment, training and retention;

–Demand for integrated network training systems to support multi-domain conflict;

–Expanded utilization of synthetic environments to support efficacy, reduce costs and lower environmental impact.

Continued increase in defence spending as a reflection of heightened global tensions

According to the Stockholm International Peace Research Institute, global military expenditures increased by 6.8% in 2023, reaching US$2.4 trillion. The immediate challenges posed by geopolitical instability and near-peer threats across multi‑domain operations will continue to drive expected increases in defence budgets. Economic headwinds and a potential need to reverse current levels of deficit spending could impact global defence; however, training is fundamental to achieving and maintaining mission readiness and budget pressures will push more training into the cost-effective virtual environment, thus creating increased opportunities for our products, services and digital capabilities.

Expected stable demand on enduring platforms and increased opportunities on next-generation systems and technology

We generate a high degree of recurring business from our strong position on enduring platforms, including long-term service contracts. Defence forces in mature markets maximize the use of their existing platforms through upgrades, updates, and life extension programs of existing assets, creating opportunities for simulator upgrades and training support services. In addition, substantial demand for enduring platforms such as the C-130, P-8, F-16, C295, MH-60R, NH90 and MQ-9 in global defence markets requires new training systems and services. Opportunities continue to expand as defence forces prepare for next-generation platforms, and the ever-increasing interaction and teaming of manned and unmanned systems. Our global reach with critical defence customers in key regions, as well as strategic relationships with OEM provider including Boeing, Lockheed Martin and Bell Textron uniquely position us to support next-generation platforms, and enable the efficient transition from current to future state training.

Maximization of efficiencies through outsourced training and support services

Another driver for our expertise and capabilities is the efficiency gained by our customers from outsourcing training and support services. Defence forces and governments continue to find ways to maximize efficiency and enhance readiness, which includes allowing active‑duty personnel to focus on operational requirements. There has been a growing trend among defence forces to consider outsourcing a variety of training and operational support services. We expect this trend to continue, which aligns directly with our strategy to grow long‑term, recurring services business. We believe governments will increasingly look to industry for training and operational support solutions to achieve faster delivery, lower capital investment requirements, and desired readiness levels.

Increased competition straining military aviation recruitment, training and retention

High demand from the civil commercial and business aviation sector has impacted the recruitment, training and retention of military pilots. The challenge has led to defence forces looking at numerous initiatives to address the potential pilot shortage, including modernization efforts and initiatives related explicitly to training innovation, such as the U.S. Air Force Pilot Training Transformation project and Canada's FAcT program. Defence forces are considering outsourcing instructor pilot positions and adopting new technologies that help make pilot training more effective and efficient to increase throughput, creating opportunities for our products, services and solutions.

CAE Financial Report 2024 I 9

Management’s Discussion and Analysis

Demand for integrated network training systems to support multi-domain conflict

The shift in the nature of the geopolitical environment and the pivot to preparing for a near‑peer adversary, combined with limited personnel and budget pressures, have prompted defence forces globally to outsource the development, management and delivery of training systems required to support today’s complex environments. Increasingly, defence forces are considering a more integrated and holistic approach to training across all domains – air, land, sea, space and cyber. Defence forces are seeking to maximize commonality for increased efficiencies, cost savings, integration and immersive training across multi-domain operations. As a training systems integrator, we leverage our leadership experience on programs like the USAF SCARS, to address the enterprise training network and deliver comprehensive solutions that enhance operational test and training infrastructure and support distributed mission training and multi‑domain operations.

Expanded utilization of synthetic environments to support efficacy, reduce costs and lower environmental impact

One of the underlying drivers for our expertise and capabilities is the increasing use of synthetic training throughout the defence community. More defence forces and governments are adopting synthetic environments for a greater percentage of their overall approach to improve training effectiveness, reduce operational demands on platforms, lower risks in training and significantly lower costs. Additional benefits of synthetic training mitigate our customers’ environmental impact by providing a safer form of multi-domain training with a significant reduction in the carbon footprint compared to live training in a real environment. At the same time, these digitally immersive synthetic environments, when combined with AI and cloud computing, can provide a tool for planning, course of action analysis, and mission support.

4. FOREIGN EXCHANGE

We report all dollar amounts in Canadian dollars. We value assets, liabilities and transactions that are measured in foreign currencies using various exchange rates as required by IFRS.

The tables below show the variations of the closing and average exchange rates for the three main currencies in which we operate.

We used the closing foreign exchange rates below to value our assets, liabilities and adjusted backlog in Canadian dollars at the end of each of the following periods:

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | Increase / |

| | | 2024 | | | 2023 | | | (decrease) |

| U.S. dollar (US$ or USD) | | 1.35 | | | 1.35 | | | — | % |

| Euro (€ or EUR) | | 1.46 | | | 1.47 | | | (1 | %) |

| British pound (£ or GBP) | | 1.71 | | | 1.67 | | | 2 | % |

We used the average quarterly and yearly foreign exchange rates below to value our revenues and expenses throughout the following periods:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Increase / | | | | | | Increase / |

| | Q4-2024 | | Q4-2023 | | (decrease) | | FY2024 | | FY2023 | | (decrease) |

| U.S. dollar (US$ or USD) | 1.35 | | | 1.35 | | | — | % | | 1.35 | | | 1.32 | | | 2 | % |

| Euro (€ or EUR) | 1.46 | | | 1.45 | | | 1 | % | | 1.46 | | | 1.38 | | | 6 | % |

| British pound (£ or GBP) | 1.71 | | | 1.64 | | | 4 | % | | 1.69 | | | 1.59 | | | 6 | % |

For fiscal 2024, the effect of translating the results of our foreign operations into Canadian dollars resulted in an increase in revenue of $80.7 million and an increase in adjusted segment operating income of $8.9 million, when compared to fiscal 2023. We calculated this by translating the current year’s foreign currency revenue and net income of our foreign operations using the average monthly exchange rates from the previous year and comparing these adjusted amounts to our current year reported results. You will find more details about our foreign exchange exposure and hedging strategies in Section 10 "Business risk and uncertainty" of this MD&A. A sensitivity analysis for foreign currency risk is included in Note 30 of our consolidated financial statements.

10 I CAE Financial Report 2024

Management’s Discussion and Analysis

5. CONSOLIDATED RESULTS

5.1 Results from operations – fourth quarter of fiscal 2024

| | | | | | | | | | | | | | | | | | | | |

| (amounts in millions, except per share amounts) | | Q4-2024 | Q3-2024 | Q2-2024 | Q1-2024 | Q4-2023 |

| Continuing operations | | | | | | |

| Revenue | $ | 1,126.3 | | 1,094.5 | | 1,050.0 | | 1,012.0 | | 1,197.4 | |

| Cost of sales | $ | 844.8 | | 791.9 | | 765.3 | | 726.3 | | 860.6 | |

| Gross profit | $ | 281.5 | | 302.6 | | 284.7 | | 285.7 | | 336.8 | |

As a % of revenue2 | % | 25.0 | | 27.6 | | 27.1 | | 28.2 | | 28.1 | |

| Research and development expenses | $ | 41.7 | | 38.1 | | 33.3 | | 36.7 | | 37.8 | |

| Selling, general and administrative expenses | $ | 138.1 | | 140.9 | | 132.3 | | 123.7 | | 134.2 | |

| Other (gains) and losses | $ | 36.3 | | (4.8) | | (2.2) | | (1.4) | | (9.3) | |

| After-tax share in profit of equity accounted investees | $ | (24.6) | | (16.7) | | (14.3) | | (16.6) | | (19.3) | |

| | | | | | |

| | | | | | |

| Restructuring, integration and acquisition costs | $ | 55.0 | | 23.5 | | 37.9 | | 15.0 | | 15.1 | |

| Impairment of goodwill | $ | 568.0 | | — | | — | | — | | — | |

| Operating (loss) income | $ | (533.0) | | 121.6 | | 97.7 | | 128.3 | | 178.3 | |

As a % of revenue2 | % | — | | 11.1 | | 9.3 | | 12.7 | | 14.9 | |

| | | | | | |

| | | | | | |

| Finance expense – net | $ | 52.4 | | 52.4 | | 47.1 | | 53.1 | | 50.4 | |

| (Loss) earnings before income taxes | $ | (585.4) | | 69.2 | | 50.6 | | 75.2 | | 127.9 | |

| Income tax (recovery) expense | $ | (80.6) | | 8.2 | | (8.3) | | 7.9 | | 30.8 | |

| As a % of earnings before income taxes | | | | | | |

| (effective tax rate) | % | 14 | | 12 | | (16) | | 11 | | 24 | |

| Net (loss) income from continuing operations | $ | (504.8) | | 61.0 | | 58.9 | | 67.3 | | 97.1 | |

| Net income (loss) from discontinued operations | $ | 20.5 | | (1.9) | | 2.2 | | 0.5 | | 4.8 | |

| Net (loss) income | $ | (484.3) | | 59.1 | | 61.1 | | 67.8 | | 101.9 | |

| Attributable to: | | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Equity holders of the Company | $ | (484.2) | | 56.5 | | 58.4 | | 65.3 | | 98.4 | |

| Non-controlling interests | $ | (0.1) | | 2.6 | | 2.7 | | 2.5 | | 3.5 | |

| | $ | (484.3) | | 59.1 | | 61.1 | | 67.8 | | 101.9 | |

| EPS attributable to equity holders of the Company | | | | |

| Basic and diluted – continuing operations | $ | (1.58) | | 0.18 | | 0.17 | | 0.20 | | 0.29 | |

| Basic and diluted – discontinued operations | $ | 0.06 | | (0.01) | | 0.01 | | — | | 0.02 | |

| | | | | | |

Adjusted segment operating income2 | $ | 125.7 | | 145.1 | | 135.6 | | 143.3 | | 193.4 | |

Adjusted net income2 | $ | 38.7 | | 76.6 | | 85.2 | | 76.3 | | 106.1 | |

Adjusted EPS2 | $ | 0.12 | | 0.24 | | 0.26 | | 0.24 | | 0.33 | |

Revenue was 6% lower compared to the fourth quarter of fiscal 2023

Revenue was $1,126.3 million this quarter, $71.1 million or 6% lower than the fourth quarter of fiscal 2023. Revenue variances by segment were as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| (amounts in millions) | | | | | | |

| Three months ended March 31 | | 2024 | | 2023 | Variance $ | Variance % |

| Civil Aviation | $ | 700.8 | | $ | 661.4 | | $ | 39.4 | | 6 | % |

| Defense and Security | | 425.5 | | | 536.0 | | | (110.5) | | (21 | %) |

| Revenue | $ | 1,126.3 | | $ | 1,197.4 | | $ | (71.1) | | (6 | %) |

You will find more details in Section 6 "Results by segment" of this MD&A.

2 Non-IFRS financial measure, non-IFRS ratio, capital management measure, or supplementary financial measure. Refer to Section 12.1 “Non-IFRS and other financial measure definitions" and Section 12.3 "Non-IFRS measure reconciliations” of this MD&A for the definitions and reconciliations of these measures to the most directly comparable measure under IFRS.

CAE Financial Report 2024 I 11

Management’s Discussion and Analysis

Gross profit was 16% lower compared to the fourth quarter of fiscal 2023

Gross profit was $281.5 million this quarter (25.0% of revenue) compared to $336.8 million (28.1% of revenue) in the fourth quarter of fiscal 2023. The decrease in gross profit and gross profit margin compared to the fourth quarter of fiscal 2023 was mainly due to the impact of unfavourable profit adjustments of $90.3 million recorded this quarter related to the Legacy Contracts in Defense and Security, partially offset by higher revenue recognized in Civil Aviation.

Operating loss was $533.0 million this quarter, a decrease of $711.3 million compared to the fourth quarter of fiscal 2023

Operating loss was $533.0 million this quarter compared to an operating income of $178.3 million (14.9% of revenue) in the fourth quarter of fiscal 2023. Operating income (loss) variances by segment were as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| (amounts in millions) | | | | | | |

| Three months ended March 31 | | 2024 | | 2023 | Variance $ | Variance % |

| Civil Aviation | $ | 147.0 | | $ | 149.3 | | $ | (2.3) | | (2 | %) |

| Defense and Security | | (680.0) | | | 29.0 | | | (709.0) | | (2,445 | %) |

| Operating (loss) income | $ | (533.0) | | $ | 178.3 | | $ | (711.3) | | (399 | %) |

You will find more details in Section 6 "Results by segment" of this MD&A.

Adjusted segment operating income was 35% lower compared to the fourth quarter of fiscal 2023

Adjusted segment operating income was $125.7 million this quarter (11.2% of revenue) compared to $193.4 million (16.2% of revenue) in the fourth quarter of fiscal 2023. Adjusted segment operating income (loss) variances by segment were as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| (amounts in millions) | | | | | | |

| Three months ended March 31 | | 2024 | | 2023 | Variance $ | Variance % |

| Civil Aviation | $ | 191.4 | | $ | 162.9 | | $ | 28.5 | | 17 | % |

| Defense and Security | | (65.7) | | | 30.5 | | | (96.2) | | (315 | %) |

| Adjusted segment operating income | $ | 125.7 | | $ | 193.4 | | $ | (67.7) | | (35 | %) |

You will find more details in Section 6 "Results by segment" of this MD&A.

Finance expense - net was 4% higher compared to the fourth quarter of fiscal 2023

Finance expense - net was $52.4 million this quarter, compared to $50.4 million in the fourth quarter of fiscal 2023. The increase was mainly due to higher finance expense on lease liabilities.

Effective tax rate was 14% this quarter

Income tax recovery this quarter amounted to $80.6 million, representing an effective tax rate of 14%, compared to an income tax expense of $30.8 million for the fourth quarter of fiscal 2023, representing an effective tax rate of 24%. The adjusted effective tax rate3 on our adjusted net income was 47% this quarter compared to 23% in the fourth quarter of fiscal 2023. The increase in the adjusted effective tax rate was mainly attributable to the derecognition of tax assets previously recorded in Europe partially offset by the change in the mix of income from various jurisdictions.

Net income from discontinued operations was $20.5 million this quarter

Net income from discontinued operations was $20.5 million this quarter compared to $4.8 million in the fourth quarter of fiscal 2023. The increase compared to the fourth quarter of fiscal 2023 was mainly attributable to the after-tax gain on disposal of discontinued operations of $16.5 million in relation to the sale of the Healthcare business.

You will find more details in Section 9 “Discontinued operations” of this MD&A.

3 Non-IFRS financial measure, non-IFRS ratio, capital management measure, or supplementary financial measure. Refer to Section 12.1 “Non-IFRS and other financial measure definitions" and Section 12.3 "Non-IFRS measure reconciliations” of this MD&A for the definitions and reconciliations of these measures to the most directly comparable measure under IFRS.

12 I CAE Financial Report 2024

Management’s Discussion and Analysis

5.2 Results from operations – fiscal 2024

| | | | | | | | | | | |

| (amounts in millions, except per share amounts) | | FY2024 | FY2023 |

| Continuing operations | | | |

| Revenue | $ | 4,282.8 | | 4,010.6 | |

| Cost of sales | $ | 3,128.3 | | 2,927.1 | |

| Gross profit | $ | 1,154.5 | | 1,083.5 | |

As a % of revenue | % | 27.0 | | 27.0 | |

| Research and development expenses | $ | 149.8 | | 129.0 | |

| Selling, general and administrative expenses | $ | 535.0 | | 501.5 | |

| Other (gains) and losses | $ | 27.9 | | (22.4) | |

| After-tax share in profit of equity accounted investees | $ | (72.2) | | (53.2) | |

| | | |

| | | |

| Restructuring, integration and acquisition costs | $ | 131.4 | | 62.6 | |

| Impairment of goodwill | $ | 568.0 | | — | |

| Operating (loss) income | $ | (185.4) | | 466.0 | |

As a % of revenue | % | — | | 11.6 | |

| | | |

| | | |

| Finance expense – net | $ | 205.0 | | 173.6 | |

| (Loss) earnings before income taxes | $ | (390.4) | | 292.4 | |

| Income tax (recovery) expense | $ | (72.8) | | 62.6 | |

| As a % of earnings before income taxes (effective tax rate) | % | 19 | | 21 | |

| Net (loss) income from continuing operations | $ | (317.6) | | 229.8 | |

| Net income from discontinued operations | $ | 21.3 | | 2.1 | |

| Net (loss) income | $ | (296.3) | | 231.9 | |

| Attributable to: | | | |

| | | |

| | | |

| | | |

| Equity holders of the Company | $ | (304.0) | | 222.7 | |

| Non-controlling interests | $ | 7.7 | | 9.2 | |

| | $ | (296.3) | | 231.9 | |

| EPS attributable to equity holders of the Company | |

| Basic and diluted – continuing operations | $ | (1.02) | | 0.69 | |

| | | |

| | | |

| Basic and diluted – discontinued operations | $ | 0.07 | | 0.01 | |

| | | |

| | | |

| Adjusted segment operating income | $ | 549.7 | | 538.4 | |

| Adjusted net income | $ | 276.8 | | 275.9 | |

| Adjusted EPS | $ | 0.87 | | 0.87 | |

Revenue was 7% higher compared to last year

Revenue was $4,282.8 million this year, $272.2 million or 7% higher than last year. Revenue variances by segment were as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| (amounts in millions) | | | | | | |

| Years ended March 31 | | 2024 | | 2023 | Variance $ | Variance % |

| Civil Aviation | $ | 2,435.8 | | $ | 2,166.4 | | $ | 269.4 | | 12 | % |

| Defense and Security | | 1,847.0 | | | 1,844.2 | | | 2.8 | | — | % |

| Revenue | $ | 4,282.8 | | $ | 4,010.6 | | $ | 272.2 | | 7 | % |

You will find more details in Section 6 "Results by segment" of this MD&A.

Gross profit was 7% higher compared to last year

Gross profit was $1,154.5 million this year (27.0% of revenue) compared to $1,083.5 million (27.0% of revenue) last year. The increase in gross profit compared to last year was mainly due to higher revenue recognized in Civil Aviation, partially offset by the impact of unfavourable profit adjustments on contracts recorded in the current and prior year, specifically $90.3 million related to the Legacy Contracts recorded in the fourth quarter of fiscal 2024, compared to $28.9 million recorded on two U.S. programs in the first quarter of fiscal 2023.

CAE Financial Report 2024 I 13

Management’s Discussion and Analysis

Operating loss was $185.4 million this year, a decrease of $651.4 million compared to last year

Operating loss was $185.4 million this year compared to an operating income of $466.0 million (11.6% of revenue) last year. Operating income (loss) variances by segment were as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| (amounts in millions) | | | | | | |

| Years ended March 31 | | 2024 | | 2023 | Variance $ | Variance % |

| Civil Aviation | $ | 442.0 | | $ | 430.3 | | $ | 11.7 | | 3 | % |

| Defense and Security | | (627.4) | | | 35.7 | | | (663.1) | | (1,857 | %) |

| Operating (loss) income | $ | (185.4) | | $ | 466.0 | | $ | (651.4) | | (140 | %) |

You will find more details in Section 6 "Results by segment" of this MD&A.

Adjusted segment operating income was 2% higher compared to last year

Adjusted segment operating income was $549.7 million this year (12.8% of revenue) compared to $538.4 million (13.4% of revenue) last year. Adjusted segment operating income variances by segment were as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| (amounts in millions) | | | | | | |

| Years ended March 31 | | 2024 | | 2023 | Variance $ | Variance % |

| Civil Aviation | $ | 548.9 | | $ | 485.3 | | $ | 63.6 | | 13 | % |

| Defense and Security | | 0.8 | | | 53.1 | | | (52.3) | | (98 | %) |

| Adjusted segment operating income | $ | 549.7 | | $ | 538.4 | | $ | 11.3 | | 2 | % |

You will find more details in Section 6 "Results by segment" of this MD&A.

Finance expense - net was $31.4 million higher than last year

| | | | | |

| | FY2023 to |

| (amounts in millions) | FY2024 |

| Finance expense - net, prior period | $ | 173.6 | |

| Change in finance expense from the prior period: | |

| Increase in finance expense on long-term debt (other than lease liabilities) | $ | 18.8 | |

| Increase in finance expense on lease liabilities | 9.2 | |

| Decrease in finance expense on royalty obligations | (0.6) | |

| Increase in other finance expense | 7.2 | |

| Decrease in borrowing costs capitalized | 0.9 | |

| Increase in finance expense from the prior period | $ | 35.5 | |

| Change in finance income from the prior period: | |

| Increase in interest income on loans and finance lease contracts | $ | (0.7) | |

| Increase in other finance income | (3.4) | |

| Increase in finance income from the prior period | $ | (4.1) | |

| Finance expense - net, current period | $ | 205.0 | |

Net finance expense was $205.0 million, $31.4 million higher compared to the same period last year. The increase was mainly due to higher finance expense on long-term debt from an increased level of borrowing and higher variable interest rates and higher finance expense on lease liabilities in support of training network expansions.

Effective tax rate was 19% this year

Income tax recovery this year amounted to $72.8 million, representing an effective tax rate of 19%, compared to an income tax expense of $62.6 million for the same period last year, representing an effective tax rate of 21%. The adjusted effective tax rate on our adjusted net income was 17% this year compared to 22% last year. The decrease in the adjusted effective tax rate was mainly attributable to the change in the mix of income from various jurisdictions, the recognition of previously unrecognized deferred tax assets in relation to the statutory combination of certain foreign operations and an income tax benefit resulting from the tax court decision in the first quarter of fiscal 2024, partially offset by the derecognition of tax assets previously recorded in Europe.

Net income from discontinued operations was $21.3 million this year

Net income from discontinued operations was $21.3 million this year, $19.2 million higher compared to the same period last year. The increase was mainly due to the after-tax gain on disposal of discontinued operations of $16.5 million incurred in the fourth quarter of fiscal 2024 in relation to the sale of the Healthcare business.

You will find more details in Section 9 “Discontinued operations” of this MD&A.

14 I CAE Financial Report 2024

Management’s Discussion and Analysis

5.3 Restructuring, integration and acquisition costs

| | | | | | | | | | | | | | | | | | | | | | | |

| FY2024 | | FY2023 | | Q4-2024 | | Q4-2023 |

| Integration and acquisition costs | $ | 79.9 | | | $ | 65.8 | | | $ | 15.0 | | | $ | 14.8 | |

Severances and other employee related costs | 31.2 | | | 2.0 | | | 19.7 | | | 0.3 | |

Impairment of non-financial assets - net | 19.2 | | | 1.8 | | | 19.2 | | | — | |

Other costs | 1.1 | | | 2.8 | | | 1.1 | | | — | |

| Impairment reversal of non-financial assets following their | | | | | | | |

repurposing and optimization | — | | | (9.8) | | | — | | | — | |

Total restructuring, integration and acquisition costs | $ | 131.4 | | | $ | 62.6 | | | $ | 55.0 | | | $ | 15.1 | |

On February 16, 2024, concurrent with the sale of our Healthcare business, we announced that we will further streamline our operating model and portfolio, optimize our cost structure and create efficiencies. For the year ended March 31, 2024, costs related to this restructuring program totalled $39.3 million and included $15.8 million of severances and other employee related costs and $16.8 million of impairment of intangible assets related to the termination of certain product offerings within the Civil Aviation segment. We expect to record approximately $10 million of additional restructuring expenses over the next two quarters.

For the year ended March 31, 2024, restructuring, integration and acquisition costs associated with the fiscal 2022 acquisition of AirCentre amounted to $76.8 million (2023 – $48.9 million) and those related to the fiscal 2022 acquisition of L3H MT amounted to $12.9 million (2023 – $17.6 million).

The ongoing integration costs associated with the AirCentre acquisition relate mainly to IT infrastructure migration and integration and are expected to be substantially complete by mid fiscal 2025. While a significant portion of the integration costs associated with the L3H MT acquisition were incurred by the end of fiscal 2023, additional integration costs were incurred in fiscal 2024 following the completion of IT infrastructure and systems integration and structural organizational changes.

For the year ended March 31, 2023, restructuring, integration and acquisition costs include gains on the reversal of impairment of an intangible asset of $6.8 million in the Defense and Security segment and property, plant and equipment of $3.0 million in the Civil Aviation segment, following their repurposing and optimization and new customer contracts and opportunities.

5.4 Impairment of goodwill

We performed the annual impairment test for goodwill during the fourth quarter of fiscal 2024. We determined the recoverable amount of each of our cash generating units (CGUs) based on fair value less costs of disposal calculations using a discounted cash flow model. The recoverable amount of each CGU is calculated using estimated cash flows derived from our five-year strategic plan as approved by the Board of Directors. The cash flows are based on expectations of market growth, industry reports and trends, and past performance. Cash flows subsequent to the five‑year period were extrapolated using a constant terminal value growth rate of 2%, which is consistent with forecasts included in industry reports specific to the industry in which each CGU operates. The discount rates used to calculate the recoverable amounts reflect each CGUs’ specific risks and market conditions, including the market view of risk for each CGU, and range from 9.0% to 10.9%.

In fiscal 2024, the assumptions used in determining the recoverable amount of the Defense and Security CGU using the discounted cash flow model, including expected revenue growth, margin projections and the discount rate, were impacted by the general economic headwinds and the re-baselining of the Defense and Security business resulting in the delayed recovery and growth of the CGU. As a result of the impairment test performed, we recorded a goodwill impairment charge of $568.0 million. The recoverable amount of the Defense and Security CGU after the impairment, based on the fair value less costs of disposal calculation, was $2.1 billion.

Variations in assumptions and estimates, particularly in the expected revenue growth, margin projections and the discount rate could have a significant impact on fair value. For the Defense and Security CGU, a decrease of 1% in expected revenue growth would have resulted in an additional impairment of approximately $85 million, a decrease of 1% in margin projections would have resulted in an additional impairment of approximately $190 million, and an increase of 1% in the discount rate of 10.9% would have resulted in an additional impairment of approximately $245 million.

No impairment charge was identified for the CGUs included in the Civil Aviation segment. A decrease of 1% in expected revenue growth, a decrease of 1% in margin projections, or an increase of 1% in the discount rate would not have resulted in an impairment charge for any of the Civil Aviation CGUs.

You will find more details in Note 14 of our consolidated financial statements.

CAE Financial Report 2024 I 15

Management’s Discussion and Analysis

5.5 Consolidated adjusted orders and adjusted backlog

Adjusted backlog4 13% higher compared to last year

| | | | | | | | |

| (amounts in millions) | FY2024 | FY2023 |

Obligated backlog4, beginning of period | $ | 8,961.9 | | $ | 7,871.4 | |

| + adjusted order intake | 4,937.4 | | 4,856.4 | |

- revenue | (4,282.8) | | (4,010.6) | |

+ / - adjustments | (101.2) | | 244.7 | |

| Obligated backlog, end of period | $ | 9,515.3 | | $ | 8,961.9 | |

Joint venture backlog4 (all obligated) | 464.1 | | 300.2 | |

Unfunded backlog and options4 | 2,204.5 | | 1,534.3 | |

| Adjusted backlog | $ | 12,183.9 | | $ | 10,796.4 | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

Fiscal 2024 adjustments were mainly due to contract cancellations and contract amendments, partially offset by foreign exchange movements.

The book-to-sales ratio for the quarter was 1.38x. The ratio for the last 12 months was 1.15x.

In fiscal 2024, $935.7 million was added to the unfunded backlog and $623.9 million was transferred to obligated backlog.

You will find more details in Section 6 "Results by segment" of this MD&A.

6. RESULTS BY SEGMENT

We manage our business and report our results in two segments:

–Civil Aviation;

–Defense and Security.

The method used for the allocation of assets jointly used by the operating segments and costs and liabilities jointly incurred (mostly corporate costs) between operating segments is based on the level of utilization when determinable and measurable, otherwise the allocation is based on a proportion of each segment’s cost of sales and revenue.