As filed with the Securities

and Exchange Commission on August 5, 2022

Registration Nos. 333-265964 and

333-265964-01

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM SF-3

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

FIRST

NATIONAL MASTER NOTE TRUST

(Issuing entity in respect of the Notes)

FIRST

NATIONAL FUNDING LLC

(Depositor)

(Exact name of registrant as specified in its charter)

| Nebraska | 02-0598125 | |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

Commission File Number

of depositor: 333-265964-01

Central Index Key Number of depositor: 0001171040

FIRST

NATIONAL FUNDING LLC

(Exact name of depositor as specified in its charter)

Central Index Key Number of sponsor: 0000036644

FIRST

NATIONAL BANK OF OMAHA

(Exact name of sponsor as specified in its charter)

1620 Dodge Street

Stop Code 3271

Omaha, Nebraska 68197

(402) 341-0500

(Address, including ZIP code, and telephone number,

including area code, of registrant’s principal executive offices)

Lori L. Niemeyer

First National Bank of Omaha

1620 Dodge Street

Stop Code 3271

Omaha, Nebraska 68197

(402) 341-0500

(Name, address, including

ZIP code, and telephone number,

including area code, of agent for service)

COPIES TO:

| Mark A. Ellis H. Dale Dixon Kutak Rock LLP 1650 Farnam Street Omaha, Nebraska 68102-2186 (402) 346-6000 |

Lori L. Niemeyer First National Bank of Omaha 1620 Dodge Street, Stop Code 33271 Omaha, Nebraska 68197 (402) 341-0500 |

Kenneth P. Marin 1270 Avenue of the Americas |

Approximate date of commencement of proposed sale to the public: From time to time after this Registration Statement becomes effective as determined by market conditions.

If any of the securities being registered on this Form SF-3 are to be offered pursuant to Rule 415 under the Securities Act of 1933, check the following box: x

If this Form SF-3 is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form SF-3 is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(A) OF THE SECURITIES ACT OF 1933 OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SAID SECTION 8(A), MAY DETERMINE.

The information in this prospectus is not complete and may be amended. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated [•][•], 20[•]

Prospectus dated [•][•], 20[•]

First

National Master Note Trust

Issuing Entity

(CIK: 0001396730)

| First National Funding LLC | First National Bank of Omaha |

|

Depositor (CIK: 0001171040) |

Sponsor, Originator, Bank and Servicer (CIK: 0000036644) |

|

$[•] Class A Series 20[•]-[•] Asset Backed Notes | |

|

Class A Notes | ||

| Principal amount | $[•] | |

| Interest rate | [[insert floating rate benchmark] [other indices limited exclusively to interest rate] plus]* [•]% per year [(determined as described in this prospectus), with a minimum interest rate of 0.00%] | |

| Interest payment dates | monthly on the [15th], beginning [•] [•], 20[•] | |

| Expected principal payment date | [•][•], 20[•] | |

| Final maturity date | [•][•], 20[•] | |

| Price to public | $[•] (or [•]%) | |

| Underwriting discount | $[•] (or [•]%) | |

|

Proceeds to issuing entity |

$[•] (or [•]%) | |

| *[Note: The interest rate for the Class A Series 20[•]-[•] notes will be based on [insert floating rate benchmark (other than LIBOR-based rate)] [other indices limited exclusively to interest rates; provided that no notes will be issued with interest accruing based on LIBOR. The prospectus for such floating rate notes will disclose the terms of the applicable benchmark index.] | ||

[The issuing entity will also issue $[•] Class B notes and $[•] Class C notes as part of Series 20[•]-[•].] Only the Class A notes are offered hereby.

[The issuing entity may offer and sell Class A notes having an aggregate initial principal amount that is either greater or less than the amount shown above. In that event, the initial principal amount of each Class of notes and the spread account amount will be proportionately increased or decreased.]

Each class of notes benefits from credit enhancement in the form of subordination of any junior classes of notes and, for the benefit of the Class C notes, a spread account.

[[The Series [201 ]- [•] notes][The Class [•] notes] will have the benefit of an interest rate swap provided by [Name of Interest Rate Swap Counterparty], as the interest rate swap counterparty.]

The notes will be paid from the issuing entity’s assets consisting primarily of receivables in a portfolio of VISA® and MasterCard® revolving credit card accounts owned by First National Bank of Omaha.

We expect to issue your series of notes in book-entry form on or about [•][•], 20[•].

You should consider carefully the risk factors beginning on page 21 in this prospectus.

A note is not a deposit and neither the notes nor the underlying accounts or receivables are insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency. The notes are obligations of First National Master Note Trust only and are not obligations of First National Funding LLC, First National Bank of Omaha or any other person.

Neither the Securities and Exchange Commission nor any state securities commission has approved these notes or determined that this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

Underwriters

| [•] | [•] |

[•]

[•][•], 20[•]

Notice About Information Presented In This Prospectus

We (First National Funding LLC) provide information to you about the notes in this prospectus, which provides (a) a description of the specific terms that apply to your series of notes, including:

| • | the terms, including interest rates, for each class; |

| • | the timing of interest and principal payments; |

| • | information about the receivables; |

| • | information about credit enhancement, if any, for each class; |

| • | the ratings for each class being offered; and |

| • | the method for selling the notes, |

and (b) general information, some of which may not apply to your series of notes.

You should rely only on the information provided in this prospectus, including the information incorporated by reference. We have not authorized anyone to provide you with different information. We are not offering the notes in any state where the offer is not permitted.

We include cross references in the prospectus to captions in the prospectus where you can find further related discussions. The following Table of Contents provides the pages on which these captions are located.

This prospectus uses defined terms. You can find a glossary of those terms under the caption “Glossary of Terms for Prospectus” beginning on page 154 of this prospectus.

Volcker Rule Considerations

The issuing entity is not now, and immediately following the issuance of the Series 20[•]-[•] notes on the closing date will not be, an “investment company” within the meaning of the Investment Company Act of 1940, as amended (the “Investment Company Act”). In making this determination, on the date of this prospectus and immediately following the issuance of the Series 20[•]-[•] notes on the closing date, the issuing entity will be relying on an exemption from registration set forth in Rule 3a-7 under the Investment Company Act, although the issuing entity may be entitled to rely on other statutory or regulatory exclusions and exemptions under the Investment Company Act as of the date of this prospectus, on the closing date or in the future. The issuing entity is structured so as not to constitute a “covered fund” for the purposes of the regulations adopted under Section 13 of the Bank Holding Company Act of 1956, commonly referred to as the “Volcker Rule.”

[Notice to Residents of the United Kingdom

This prospectus may only be communicated or caused to be communicated in the United Kingdom to persons having professional experience in matters relating to investments and qualifying as investment professionals under Article 19(5) (Investment Professionals) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “Order”) or to persons falling within Article 49(2)(A) to (D) (high net worth companies, unincorporated associations, etc.) of the Order or to any other person to whom this prospectus may otherwise lawfully be communicated or caused to be communicated (all such persons together being referred to as “Relevant Persons”).

Neither this prospectus nor the notes are or will be available to persons in the United Kingdom who are not Relevant Persons and this prospectus must not be acted on or relied on by persons in the United Kingdom who are not Relevant Persons. Any investment or investment activity to which this prospectus relates is available in the United Kingdom only to Relevant Persons and will be engaged in only with Relevant Persons in the United Kingdom. The communication of this prospectus to any person in the United Kingdom who is not a Relevant Person is unauthorized and may contravene the Financial Services and Markets Act 2000, as amended (the “FSMA”).]

[Notice to Residents of the European Economic Area

The notes are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the European Economic Area (“EEA”). For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of Directive 2014/65/EU, as amended (“MiFID II”); or (ii) a customer within the meaning of Directive (EU) 2016/97, where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II; or (iii) not a qualified investor as defined in Directive 2003/71/EC, as amended or superseded. Consequently, no key information document required by Regulation (EU) No 1286/2014 (the “PRIIPs Regulation”) for offering or selling the notes or otherwise making them available to retail investors in the EEA has been prepared and therefore offering or selling the notes or otherwise making them available to any retail investor in the EEA may be unlawful under the PRIIPs Regulation.]

[EU Due Diligence and Risk Retention Rules Considerations

Article 5 of Regulation (EU) 2017/2402 of the European Parliament and of the Council of December 12, 2017 (the “EU Securitization Regulation”) places certain conditions on investments in securitizations (as defined in the EU Securitization Regulation) by “institutional investors,” defined to include (a) a credit institution or an investment firm as defined in and for purposes of Regulation (EU) No. 575/2013, as amended, known as the Capital Requirements Regulation (the “CRR”), (b) an insurance undertaking or a reinsurance undertaking as defined in Directive 2009/138/EC, as amended, known as Solvency II, (c) an alternative investment fund manager (AIFM) as defined in Directive 2011/61/EU that manages or markets alternative investment funds in the European Union, (d) an undertaking for collective investment in transferable securities (UCITS) management company, as defined in Directive 2009/65/EC, as amended, known as the UCITS Directive, or an internally managed UCITS, which is an investment company that is authorized in accordance with that Directive and has not designated such a management company for its management, and (e) with certain exceptions, an institution for occupational retirement provision (IORP) falling within the scope of Directive (EU) 2016/2341, or an investment manager or an authorized entity appointed by such an institution for occupational retirement provision as provided in that Directive. Pursuant to Article 14 of the CRR, those conditions also apply to investments by certain consolidated affiliates, wherever established or located, of institutions regulated under the CRR. The EU Securitization Regulation has direct effect in member states of the European Union (the “EU”) and is to be implemented by national legislation in other countries in the EEA.

Under the terms and conditions of a risk retention agreement for the Class A notes that the bank will enter into with the depositor and the issuing entity, with reference to Articles 5 and 6 of the EU Securitization Regulation, together with any relevant regulatory technical standards adopted by the European Commission and any guidance published by the European Union supervisory authorities with respect thereto or to precedent legislation (together, “EU delegated regulations and guidance”), each as in effect and applicable on the date of the issuance of the Class A notes (referred to, collectively, as the “EU due diligence and risk retention rules”), the bank will covenant and agree that:

(i) as “originator”, within the meaning of Article 2(3)(a) of the EU Securitization Regulation, for the purposes of those EU due diligence and risk retention rules, it currently retains, and on an ongoing basis will retain, a material net economic interest that is not less than five per cent of the nominal value of the securitized exposures (measured at origination), in a form that is intended to qualify as an originator’s interest as provided in option (b) of Article 6(3) of the EU Securitization Regulation, by indirectly holding all the membership interest in the depositor, which in turn holds all or part of the transferor interest;

(ii) it will not change the retention option or the method of calculating its net economic interest in the securitized exposures while the Class A notes are outstanding, except under exceptional circumstances in accordance with the EU Securitization Regulation (as supplemented by applicable EU delegated regulations and guidance);

| ii |

(iii) it will not (and will not permit the depositor or any of its other affiliates) to allow the retained interest to be subject to any credit risk mitigation, short position or other hedge or to be sold if, as a result, the bank would not retain a material net economic interest in an amount that is not less than five per cent of the nominal value of the securitized exposures, except to the extent permitted in accordance with Article 6(1) of the EU Securitization Regulation (as supplemented by applicable EU delegated regulations and guidance); and

(iv) it will provide ongoing confirmation of its continued compliance with its obligations in clauses (i) and (iii) in this paragraph in or concurrently with the delivery of each distribution repot of the issuing entity on Form 10-D relating to the Class A notes.

The bank is not subject to the EU due diligence and risk retention rules or other provisions of the EU Securitization Regulation and, other than as set forward in the risk retention agreement (as summarized in the previous paragraph), the bank does not undertake any further action to comply with (or to enable affected investors to comply) with the EU due diligence and risk retention rules or other provisions of the EU Securitization Regulation, including the delivery of any information beyond that contained in each distribution report of the issuing entity on Form 10-D relating to the Class A notes. Accordingly, none of First National Bank of Omaha, First National Funding LLC, First National Master Note Trust, Wilmington Trust Company, U.S. Bank Trust Company, National Association, any of the underwriters, or any of their respective affiliates makes any representations or gives any assurance that the matters set forth in the previous paragraph and the information given in this prospectus or pursuant to the transaction documents are or will be sufficient for compliance by affected Class A noteholders with the requirements and the criteria set out in the EU due diligence and risk retention rules. Failure by affected Class A noteholders to comply with one or more of the requirements set forth in the EU due diligence and risk retention rules may result, among other things, in the imposition of a penalty regulatory capital charge through additional risk weights levied in respect of the Class A notes acquired by the applicable Class A noteholders that are subject to the EU due diligence and risk retention rules, or the imposition of other regulatory sanctions. Prospective Class A noteholders are responsible for analyzing their own regulatory position and are advised to consult with their own advisors regarding the suitability of the Class A notes for investment and compliance with the applicable EU due diligence and risk retention rules. U.S. Bank Trust Company, National Association shall have no responsibility to monitor compliance with, calculate, provide, or otherwise make available information or documents required by the EU Securitization Regulation or any other rules or regulations regarding risk retention. U.S. Bank Trust Company, National Association shall not be charged with knowledge of such rules and shall not be liable to any party for a violation of such rules now or hereafter in effect.]

[UK Due Diligence and Risk Retention Rules Considerations

Article 5 of Regulation (EU) 2017/2402 of the European Parliament and of the Council of December 12, 2017 as enacted into the laws of the United Kingdom pursuant to the European Union (Withdrawal) Act 2018 (the “UK Securitization Regulation”) places certain conditions on investments in securitizations (as defined in the UK Securitization Regulation) by “institutional investors,” requiring such investors to carry out due diligence where they hold an exposure to a securitization.

Under the terms and conditions of a risk retention agreement for the Class A notes that the bank will enter into with the depositor and the issuing entity, with reference to Articles 5 and 6 of the UK Securitization Regulation, together with any relevant regulatory technical standards adopted by the European Commission prior to 1 January 2021 or by the UK, and any guidance published by the European Union supervisory authorities published prior to 1 January 2021 (where such guidance is to be interpreted in light of the United Kingdom's exit from the EU pursuant to relevant guidance issued by the Financial Conduct Authority (the “FCA”)) or by the FCA with respect thereto or to precedent legislation (together, “UK delegated regulations and guidance”), each as in effect and applicable on the date of the issuance of the Class A notes (referred to, collectively, as the “UK due diligence and risk retention rules”), the bank will covenant and agree that:

(i) as “originator”, within the meaning of Article 2(3)(a) of the UK Securitization Regulation, for the purposes of those UK due diligence and risk retention rules, it currently retains, and on an ongoing basis will retain, a material net economic interest that is not less than five per cent of the nominal value of the securitized exposures (measured at origination), in a form that is intended to qualify as an originator’s interest as provided in option (b) of Article 6(3) of the UK Securitization Regulation, by indirectly holding all the membership interest in the depositor, which in turn holds all or part of the transferor interest;

| iii |

(ii) it will not change the retention option or the method of calculating its net economic interest in the securitized exposures while the Class A notes are outstanding, except under exceptional circumstances in accordance with the UK Securitization Regulation (as supplemented by applicable UK delegated regulations and guidance);

(iii) it will not (and will not permit the depositor or any of its other affiliates) to allow the retained interest to be subject to any credit risk mitigation, short position or other hedge or to be sold if, as a result, the bank would not retain a material net economic interest in an amount that is not less than five per cent of the nominal value of the securitized exposures, except to the extent permitted in accordance with Article 6(1) of the UK Securitization Regulation (as supplemented by applicable UK delegated regulations and guidance); and

(iv) it will provide ongoing confirmation of its continued compliance with its obligations in clauses (i) and (iii) in this paragraph in or concurrently with the delivery of each distribution repot of the issuing entity on Form 10-D relating to the Class A notes.

The bank is not subject to the UK due diligence and risk retention rules or other provisions of the UK Securitization Regulation and, other than as set forward in the risk retention agreement (as summarized in the previous paragraph), the bank does not undertake any further action to comply with (or to enable affected investors to comply) with the UK due diligence and risk retention rules or other provisions of the UK Securitization Regulation, including the delivery of any information beyond that contained in each distribution report of the issuing entity on Form 10-D relating to the Class A notes. Accordingly, none of First National Bank of Omaha, First National Funding LLC, First National Master Note Trust, Wilmington Trust Company, U.S. Bank Trust Company, National Association, any of the underwriters, or any of their respective affiliates makes any representations or gives any assurance that the matters set forth in the previous paragraph and the information given in this prospectus or pursuant to the transaction documents are or will be sufficient for compliance by affected Class A noteholders with the requirements and the criteria set out in the UK due diligence and risk retention rules. Failure by affected Class A noteholders to comply with one or more of the requirements set forth in the UK due diligence and risk retention rules may result, among other things, in the imposition of a penalty regulatory capital charge through additional risk weights levied in respect of the Class A notes acquired by the applicable Class A noteholders that are subject to the UK due diligence and risk retention rules, or the imposition of other regulatory sanctions. Prospective Class A noteholders are responsible for analyzing their own regulatory position and are advised to consult with their own advisors regarding the suitability of the Class A notes for investment and compliance with the applicable UK due diligence and risk retention rules. U.S. Bank Trust Company, National Association shall have no responsibility to monitor compliance with, calculate, provide, or otherwise make available information or documents required by the UK Securitization Regulation or any other rules or regulations regarding risk retention. U.S. Bank Trust Company, National Association shall not be charged with knowledge of such rules and shall not be liable to any party for a violation of such rules now or hereafter in effect.]

Compliance with Registration Requirements

We confirm that we have reasonable grounds to believe that we have met the registrant requirements set forth in General Instruction I.A.1 to Form SF-3, as in effect on the shelf eligibility determination date, as of such date. The term “shelf eligibility determination date” refers to either (i) the initial filing of the Form SF-3 shelf registration statement of which this prospectus forms a part or (ii) the ninetieth day after the end of our most recent fiscal year, whichever is the most recent to have occurred prior to date of this prospectus.

| iv |

TABLE OF CONTENTS

| 2 |

| 3 |

| 4 |

Summary: Overview of Transactions

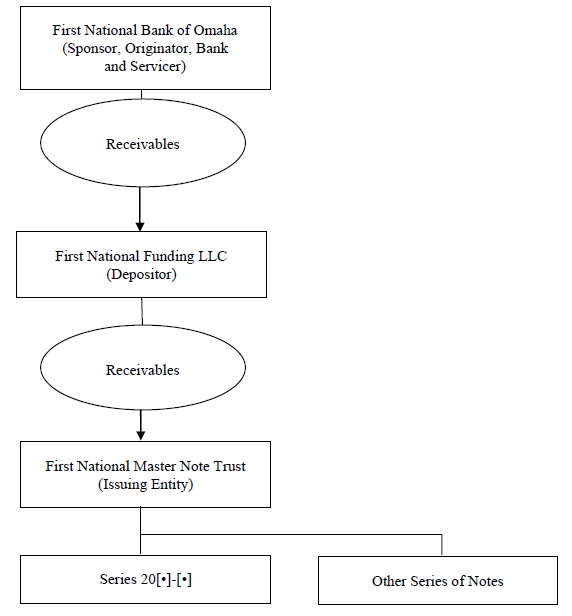

Each series of notes will be issued by First National Master Note Trust and will include one or more classes of notes, representing debt of the issuing entity. Each series of notes may differ as to timing and priority of distributions, allocations of losses, interest rates, the amount of distributions in respect of principal and interest and credit enhancement. We, First National Funding LLC, will disclose the details of these timing, priority and other matters in a prospectus for each series.

We refer to First National Master Note Trust as the trust or the issuing entity. The trust is a statutory trust created under the laws of the State of Delaware and pursuant to a trust agreement dated as of October 16, 2002, between us and Wilmington Trust Company, as owner trustee, which has been amended and restated, in its entirety, by a first amended and restated trust agreement dated as of December 20, 2012 and by a second amended and restated trust agreement dated as of September 23, 2016. For the purposes of this prospectus, all references to the trust agreement mean the second amended and restated trust agreement.

Each series of notes will be issued pursuant to an indenture supplement to the master indenture. The trust and The Bank of New York, as indenture trustee, entered into the master indenture on October 24, 2002. The master indenture was amended on November 17, 2003 and amended and restated, in its entirety, by a first amended and restated master indenture dated as of December 20, 2012, between the trust and The Bank of New York Mellon Trust Company, N.A., (formerly known as The Bank of New York Trust Company, N.A.), as successor indenture trustee to The Bank of New York. The first amended and restated master indenture was amended and restated, in its entirety, by a second amended and restated master indenture dated as of September 23, 2016, between the trust and U.S. Bank National Association, as successor indenture trustee to The Bank of New York Mellon Trust Company, N.A. U.S. Bank Trust Company, National Association became the successor indenture trustee under the master indenture, effective May 1, 2022. We refer to the master indenture as the indenture. For the purposes of this prospectus, all references to the indenture mean the second amended and restated master indenture.

The primary assets of the trust are credit card receivables arising in VISA® and MasterCard® 1 revolving credit card accounts that have been transferred directly or indirectly by First National Bank of Omaha or one of its affiliates to First Bankcard Master Credit Card Trust or the trust. Hereafter we sometimes refer to First National Bank of Omaha as the bank. The credit card receivables have been either originated by the bank or one of its affiliates or have been acquired by the bank from third-party financial institutions.

Prior to December 18, 2008, the bank transferred receivables directly or indirectly to First Bankcard Master Credit Card Trust. The trust held a collateral certificate issued by First Bankcard Master Credit Card Trust and evidencing an undivided interest in the receivables held thereby. On December 18, 2008, with all outstanding investor certificates issued by First Bankcard Master Credit Card Trust (other than the collateral certificate) retired, we exercised our option to terminate First Bankcard Master Credit Card Trust.

First Bankcard Master Credit Card Trust was formed under Nebraska law by the bank in 1995 under a pooling and servicing agreement. The trustee for First Bankcard Master Credit Card Trust was The Bank of New York Mellon Trust Company, N.A. Under the pooling and servicing agreement, the bank, in its capacity as transferor, designated some eligible accounts from its portfolio of VISA and MasterCard credit card accounts and transferred the receivables in those accounts to First Bankcard Master Credit Card Trust. For a period from December 31, 1995 through September 30, 2000, First National Bank South Dakota, an affiliate of First National Bank of Omaha, was the owner of some or all of the credit card accounts and the transferor or a co-transferor under the pooling and servicing agreement. Effective October 1, 2000, the credit card accounts were transferred to First National Bank of Omaha, which then again became the sole transferor under the pooling and servicing agreement.

The transactions described above were implemented, in part, through amendments to the pooling and servicing agreement.

1 VISA® and MasterCard® are federally registered servicemarks of VISA U.S.A., Inc. and MasterCard International Inc., respectively.

The applicable transferor or co-transferor that was party to the pooling and servicing agreement continued to transfer additional receivables generated in those accounts, and from time to time designated additional accounts, to First Bankcard Master Credit Card Trust until the October 2002 amendment to the pooling and servicing agreement. The amendment, among other things, designated us as the transferor replacing the bank. At the same time, we entered into a receivables purchase agreement with the bank whereby the bank designated some eligible accounts to us and transferred the receivables created in the accounts after the date of the agreement to us. Under the receivables purchase agreement, the bank will, from time to time, designate additional accounts to us and transfer additional receivables to us and will also occasionally remove accounts previously designated. Under the amended pooling and servicing agreement, in our capacity as transferor, we transferred all receivables sold to us by the bank under the receivables purchase agreement dated October 24, 2002 to the trust and designated to the trust all accounts designated to us by the bank. The receivables purchase agreement was amended and restated, in its entirety, by a first amended and restated receivables purchase agreement on December 20, 2012 and the first amended and restated receivables purchase agreement has been amended and restated, in its entirety, by a second amended and restated receivables purchase agreement on September 23, 2016. For the purposes of this prospectus, all references to the receivables purchase agreement mean the second amended and restated receivables purchase agreement.

First Bankcard Master Credit Card Trust issued a collateral certificate representing an interest in the receivables and the other assets of First Bankcard Master Credit Card Trust to us. We transferred the collateral certificate to the issuing entity, and the issuing entity transferred the collateral certificate to the indenture trustee as collateral for the notes issued by the trust. The collateral certificate was the initial primary asset of the trust.

Upon the termination of First Bankcard Master Credit Card Trust, we and the trustee transferred all of our right, title and interest in and to the receivables and other assets of First Bankcard Master Credit Card Trust to the indenture trustee, as the assignee of the collateral certificate. Upon its receipt of the assets of First Bankcard Master Credit Card Trust, the indenture trustee surrendered the collateral certificate to the registrar and paying agent under the pooling and servicing agreement for cancellation. All of the respective obligations of the servicer, the trustee and us under the pooling and servicing agreement and the collateral series supplement, respectively, were terminated on December 18, 2008 except for certain obligations of the servicer and us that expressly survive the termination of the pooling and servicing agreement and the collateral series supplement. See “Description of the Notes—Matters Regarding the Depositor and the Servicer” in this prospectus.

The bank will continue to own the accounts that are designated to the trust.

The notes will represent the right to payments from a portion of collections on the credit card receivables held by the trust.

In addition, a portion of certain fees payable by VISA and MasterCard to the bank, which are attributable to cardholder charges for merchandise and services, known as interchange, will be treated as collections of finance charge receivables.

All new receivables generated in the designated accounts will be automatically transferred to the trust. The total amount of receivables held by the trust will fluctuate daily as new receivables are generated and payments are received on existing receivables.

The bank continues to service the receivables that are transferred to the trust pursuant to a transfer and servicing agreement dated October 24, 2002, among us, the bank, as servicer and the trust. On December 20, 2012, the transfer and servicing agreement was amended and restated, in its entirety, by a first amended and restated transfer and servicing agreement and on September 23, 2016, the first amended and restated transfer and servicing agreement was amended and restated, in its entirety, by the second amended and restated transfer and servicing agreement. For the purposes of this prospectus, all references to the transfer and servicing agreement mean the second amended and restated transfer and servicing agreement.

In addition, the bank acts as the trust’s administrator pursuant to an administration agreement dated October 24, 2002, between the bank and the trust. On December 20, 2012, the administration agreement was amended and restated, in its entirety, by a first amended and restated administration agreement and on September 23, 2016, the first amended and restated trust agreement was amended and restated, in its entirety, by a second amended and restated administration agreement. For the purposes of this prospectus, all references to the administration agreement mean the second amended and restated administration agreement.

2

The trust has granted a security interest in the receivables and its other assets to the indenture trustee for the benefit of the noteholders and any credit enhancement provider.

| Issuing Entity/Trust: | First National Master Note Trust |

| Depositor/Securitizer: | First National Funding LLC |

| Sponsor/Originator/Bank/Servicer: | First National Bank of Omaha |

| Administrator: | First National Bank of Omaha |

| Indenture Trustee: | U.S. Bank Trust Company, National Association |

| Owner Trustee: | Wilmington Trust Company |

| Asset Representations Reviewer: | FTI Consulting, Inc. |

| [Derivative Counterparty:] | [Name of counterparty] |

| Expected Closing Date: | [•][•], 20[•] |

| Clearance and Settlement: | DTC/Clearstream/Euroclear |

| Servicing Fee Rate: | [2]% per annum |

| Initial Collateral Amount: | $[•] |

| Primary Assets of the Issuing Entity: | Receivables originated in VISA® and MasterCard® revolving credit card accounts owned by First National Bank of Omaha. |

| Offered Notes: | The Class A notes are offered by this prospectus. |

| Series 20[•]-[•] | ||||||||

| Class | Amount | % of Series 20[•]-[•] notes | ||||||

| Class A notes | $ | [•] | [•] | % | ||||

| Class B notes | [•] | [•] | % | |||||

| Class C notes | [•] | [•] | % | |||||

| Total | $ | [•] | 100.00 | % | ||||

3

| Class A | ||

| Initial Principal Amount: | $[•] | |

| Anticipated Ratings: | We expect the offered notes to receive credit ratings from at least two nationally recognized statistical rating organizations hired by the sponsor to rate the offered notes. Hereinafter we refer to each nationally recognized statistical rating organization hired by the sponsor to provide a credit rating on the offered notes as a “Hired Agency” and, collectively, as the “Hired Agencies.” | |

| Credit Enhancement: | subordination of Class B and Class C notes | |

| Interest Rate: | [[Benchmark] plus]2 [•]% per year[, with a minimum interest rate of 0.00%] (or, for the first interest period from and including the closing date through but excluding [•][•], 20[•]). See “Description of Series Provisions—Interest Payments” in this prospectus for a description of [how [Benchmark] will be determined and] the calculation of interest on the Class A notes. | |

| Interest Accrual Method: | [30][actual]/360 | |

| Distribution Dates: | [15th] day of each month, or if that day is not a business day, the next business day | |

| First Distribution Date: | [•][•], 20[•] | |

| Commencement of Accumulation Period (subject to adjustment): | [•][•], 20[•] | |

| Expected Principal Payment Date: | [•][•], 20[•] | |

| Final Maturity Date: | [•][•], 20[•] | |

| ERISA Eligibility: | Yes, subject to important considerations described under “ERISA Considerations” in this prospectus. | |

| Debt for United States Federal Income Tax Purposes: | Yes, subject to important considerations described under “Federal Income Tax Consequences” in this prospectus. |

2 [Note: The interest rate for the Class A Series 20[•]-[•] notes will be based on [insert floating rate benchmark (other than LIBOR-based rate)] [other indices limited exclusively to interest rates; provided that no notes will be issued with interest accruing based on LIBOR. The prospectus for such floating rate notes will disclose the terms of the applicable benchmark index.]

4

This summary is a simplified presentation of the major structural components of Series 20[•]-[•]. It does not contain all of the information that you need to consider in making your investment decision. You should carefully read this entire document before you purchase any notes.

5

The notes will be issued by First National Master Note Trust, a Delaware statutory trust, which is referred to in this prospectus as the issuing entity or the trust. The notes will be issued under an indenture supplement to the indenture, each between the issuing entity and the indenture trustee.

The indenture trustee is U.S. Bank Trust Company, National Association.

Asset Representations Reviewer

FTI Consulting, Inc., a Maryland corporation, is the asset representations reviewer. For additional information about the asset representations reviewer, see “Asset Representations Reviewer” in this prospectus.

The notes are secured by a pool of receivables that arise under First National Bank of Omaha’s VISA and MasterCard revolving credit card accounts and other assets that the issuer has pledged as collateral for all series of notes issued by the issuing entity under the indenture. The amount of collateral allocated to support your series of notes is equal to the collateral amount for your series. For a description of the collateral amount relating to your series of notes, see “—Allocations of Collections and Losses” in this prospectus.

The bank has designated eligible accounts from its portfolio of VISA and MasterCard credit card accounts and has transferred the receivables in those accounts either directly to First Bankcard Master Credit Card Trust or to us. On December 18, 2008, First Bankcard Master Credit Card Trust was terminated and the receivables in the accounts that were originally transferred by the bank to First Bankcard Master Credit Card Trust were transferred to the trust. We transfer the receivables sold to us by the bank to the trust under the transfer and servicing agreement. We refer to the accounts that have been designated as trust accounts, as the trust portfolio.

The receivables in the trust portfolio as of [•][•], 20[•] were approximately as follows:

| • | total receivables: $[•]; |

| • | principal receivables: $[•][, which amount excludes $[•] of principal receivables treated as finance charge collections through the discount option]; |

| • | finance charge receivables: $[•][, which amount includes $[•] of principal receivables treated as finance charge collections through the discount option]; and |

| • | total accounts designated to the trust: [•]. |

[On [•][•], 20[•], approximately [•] additional accounts with total receivables of approximately $[•] were designated to the trust.]

As of [•][•], 20[•],

| • | The accounts designated for the trust portfolio had an average principal receivable balance of $[•] and an average credit limit of $[•]; |

| • | The percentage of the aggregate total receivable balance to the aggregate total credit limit was [•]%; and |

| • | The average age of the accounts was approximately [•] months. |

6

Addition of Assets to the Trust

When an account has been designated as a trust account, First National Bank of Omaha (sometimes referred to hereinafter as to the bank) continues to own the account, but we buy all receivables existing at the time of designation or created later and transfer them to the trust. The bank has the option to designate additional accounts, which must meet the criteria for eligible accounts described in the definition of “Eligible Account” in the “Glossary of Terms for Prospectus” in this prospectus, to be included as trust accounts from time to time. If the volume of additional accounts designated exceeds specified periodic limitations, then additional new accounts can only be designated if the Rating Agency Condition is satisfied.

See “Description of the Notes—Addition of Trust Assets” in this prospectus for a more detailed description of these and other limitations on our ability to designate additional accounts. In addition, the bank is required to designate additional accounts as trust accounts if the amount of principal receivables held by the trust falls below a specified minimum or if the average transferor interest falls below the minimum transferor interest for any monthly period, as more fully described in “Description of the Notes—Addition of Trust Assets” in this prospectus.

Removal of Assets from the Trust

Optional Removals

We have the right to remove accounts from the list of designated accounts and to require the reassignment to us or our designee of all receivables in the removed accounts under two circumstances. First, we may remove accounts and reassign the receivables in the removed accounts to us or our designee provided the removal will not cause a pay-out event to occur for any series and the Rating Agency Condition is satisfied. Second, we may remove accounts and reassign the receivables in the removed accounts to a third party to the extent the removed accounts arose pursuant to a private-label, agent bank, co-branding or other similar contractual arrangement with such third party and the contractual arrangement, by its terms, gives such third party the right to repurchase the accounts upon the cancellation of the arrangement or the expiration of the arrangement without renewal and such third party exercises its right to repurchase the accounts. See “Description of the Notes—Removal of Accounts” and “Risk Factors—Changes in, or termination of, a material co-branding or agent bank arrangement may affect the performance of the trust receivables and cardholder usage and, consequently, the timing and amount of payments on your series” in this prospectus.

Required Removals

We are required to accept a reassignment of receivables from the trust if either we, the servicer, a responsible officer of the owner trustee or the indenture trustee discover that the receivables did not satisfy eligibility requirements in some material respect at the time that we transferred them to the trust, and the ineligibility results in a charge-off or an impairment of the trust’s rights in the receivables or their proceeds. Except under limited circumstances, there will be a 60 day cure period. Similarly, the servicer will be required to purchase receivables from the trust if the servicer fails to satisfy any of its obligations in connection with the transferred receivables or trust accounts and such failure results in a material impairment of the receivables or subjects their proceeds to a conflicting lien. These reassignment and purchase obligations and applicable cure periods are more fully described in “Description of the Notes—Representations and Warranties” and “Description of the Notes—Servicer’s Representations, Warranties and Covenants” in this prospectus.

We have performed a review of the receivables in the trust portfolio and the disclosure required to be included in this prospectus relating to Item 1111 of Regulation AB. This review was designed and effected to provide us with reasonable assurance that the disclosure relating to the receivables in this prospectus is accurate in all material respects. For additional information, see “Annex I: Review of Pool Asset Disclosure” included at the end of this prospectus.

7

Other Claims on the Receivables

Other Series of Notes

The trust has issued other series of notes and may issue other series of notes from time to time in the future. A summary of the series of notes expected to be outstanding on the closing date is in “Annex II: Other Securities Outstanding” included at the end of this prospectus. Neither you nor any other noteholder will have the right to consent to the issuance of future series of notes.

No new series of notes may be issued unless we satisfy the conditions described in “Description of the Notes—New Issuances of Notes” in this prospectus, including that:

| • | the Rating Agency Condition is satisfied; |

| • | we certify, based on facts known to the certifying officer, that the new issuance will not cause a pay-out event or an event of default or materially and adversely affect the amount or timing of distributions to be made to any series or class of noteholders; |

| • | after giving effect to the new issuance, the transferor interest will not be less than the required minimum transferor interest and the aggregate principal receivables will not be less than the required minimum aggregate principal receivables; and |

| • | delivery of an opinion with respect to certain tax matters. |

The Transferor Interest

We own the interest, called the transferor interest, in the receivables and the other assets of the trust not supporting your series or any other series of notes. The transferor interest does not provide credit enhancement for your series or any other series. We are required to maintain a minimum transferor interest. For a description of how the transferor interest and the minimum transferor interest are calculated, see the definitions of “Transferor Interest” and “Minimum Transferor Interest” in “Glossary of Terms for Prospectus” in this prospectus.

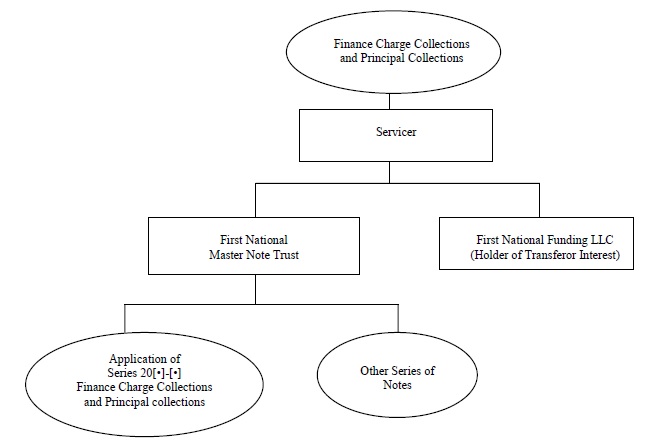

Allocations of Collections and Losses

Your notes represent the right to payments from a portion of the collections on the receivables . See the diagram on page 18, which summarizes the application of finance charge collections and principal collections by the servicer. The servicer will also allocate to your series a portion of defaulted receivables and will also allocate a portion of the dilution on the receivables to your series if the dilution is not offset by the amount of the Transferor Interest and the depositor fails to comply with its obligation to reimburse the trust for the dilution. Dilution means any reduction to the principal balances of receivables made by the servicer because of merchandise returns or any other reason except losses or payments.

The portion of collections, defaulted receivables and uncovered dilution allocated to your series will be based mainly upon the ratio of the amount of collateral for your series to the sum of the total amount of principal receivables in the trust and any balance in the trust’s excess funding account. The way this ratio is calculated will vary during each of three periods that may apply to your notes:

| • | The revolving period, which will begin on the closing date and end when either of the other two periods begins. |

| • | The accumulation period, which is scheduled to begin on [•][•], 20[•] and to end on [•][•], 20[•]. However, if a pay-out event occurs before the accumulation period begins, there will be no accumulation period and a rapid amortization period will begin. Unless a pay-out event occurs during the accumulation period, the accumulation period will end upon the Series Termination Date. If a pay-out event occurs during the accumulation period, the accumulation period will end, and a rapid amortization period will begin. Under some circumstances, the beginning of the accumulation period may be delayed, or if it has already begun, may be suspended. During this delay or upon the suspension of the accumulation period, the revolving period shall continue or resume, as appropriate. Throughout the accumulation period we will accumulate collections of principal receivables for later distribution to you. |

8

| • | The rapid amortization period, which will only occur if one or more adverse events, known as pay-out events, occurs and will continue until the Series Termination Date. |

For most purposes, the collateral amount used in determining these ratios will be measured as of and will be reset no less frequently than at the end of each month. There are exceptions, as follows.

For allocations of finance charge collections during the rapid amortization period, the collateral amount as of the end of the revolving period or, if applicable, the end of the accumulation period will be used. For allocations of principal collections during the accumulation period or the rapid amortization period, the collateral amount at the end of the revolving period will be used. We may request a decrease in the amount used, provided that the Series Rating Agency Condition is satisfied.

The collateral amount for your series is:

| • | the original principal amount of the notes, minus |

| • | principal payments on the notes (except payments made from the spread account) and the balance held in the principal accumulation account for principal payments, minus |

| • | the amount of any principal collections reallocated to cover interest and servicing payments for your series to the extent not reimbursed from finance charge collections and investment earnings allocated to your series, minus |

| • | your series’ share of defaults and uncovered dilution to the extent not reimbursed from finance charge collections and investment earnings allocated to your series. |

A reduction to the collateral amount because of reallocated principal collections or defaults or uncovered dilution will be reversed to the extent that your series has available finance charge collections and investment earnings in future periods. If a reduction to the collateral amount because of reallocated principal collections or defaults or uncovered dilution is not reversed, not all of the principal for your series of notes may be paid.

Subject to some limitations, we may elect to treat up to 4% of the principal receivables in the trust as finance charge receivables for purposes of the allocations described in this prospectus. We may from time to time, and subject to some limitations, increase, reduce or eliminate the percentage used for this purpose. This percentage will initially be zero.

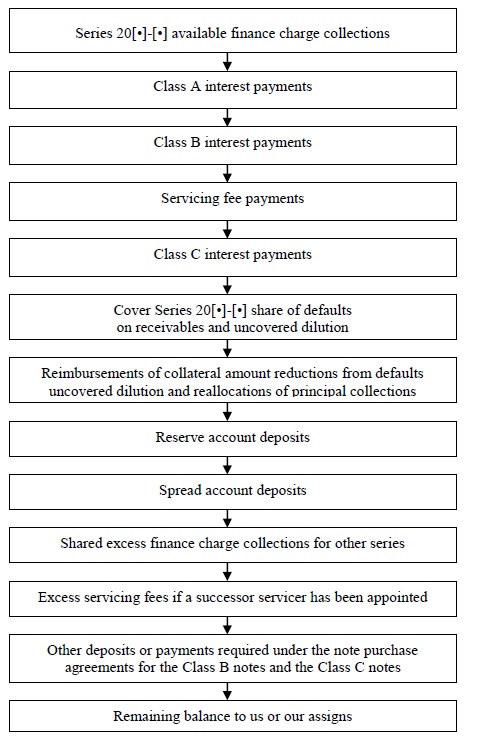

Application of Finance Charge Collections

Collections of finance charge receivables allocated to your series during each month will be applied in the following order of priority:

| • | to pay interest on the Class A notes; |

| • | to pay interest on the Class B notes; |

| • | to pay servicing fees for your series; |

9

| • | to pay interest on the Class C notes; |

| • | to cover your series’ share of defaulted receivables and uncovered dilution for the prior calendar month; |

| • | to reinstate any prior reductions in your series collateral amount on account of defaulted receivables, uncovered dilution or reallocated principal collections, in each case that have not been reimbursed; |

| • | in limited circumstances, to make deposits into a reserve account; |

| • | to make deposits, if required, into the spread account; |

| • | to other series that share excess finance charge collections with Series 20[•]-[•]; |

| • | following a servicer default and the appointment of a successor servicer, to pay to the successor servicer any excess servicing fees; |

| • | to make other deposits or payments required under note purchase agreements for Class B notes and Class C notes; and |

| • | any remaining balance to us or our assigns. |

With respect to outstanding series of variable funding notes that share excess finance charge collections with your series of notes, the holders of such outstanding series of variable funding notes are not entitled to distributions from the available finance charge collections allocated to your series of notes, except to the extent of any excess finance charge collections shared with such outstanding series of variable funding notes.

The above application of finance charge collections allocated to your series is summarized in the diagram on page 19.

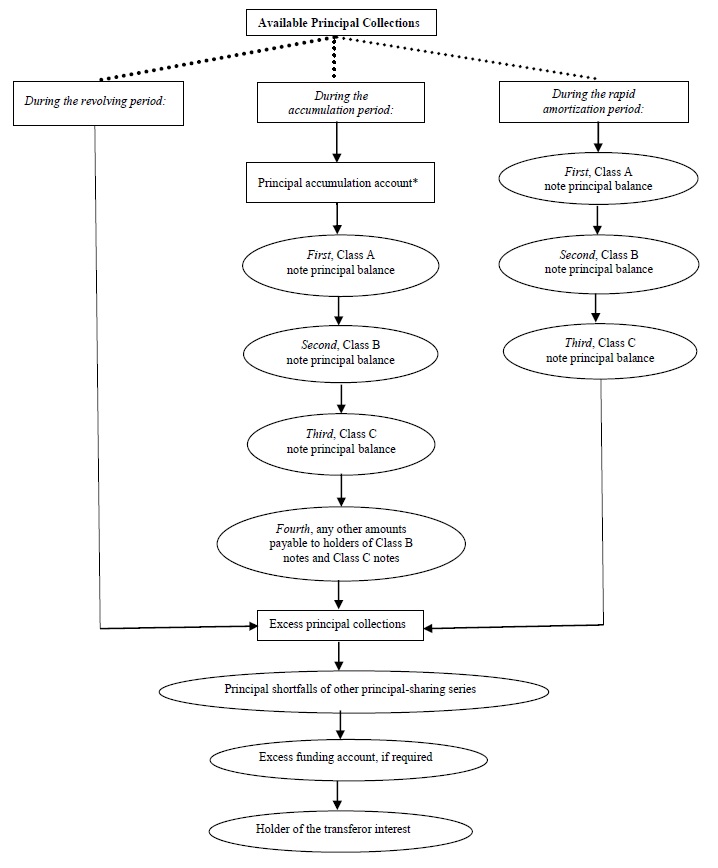

Application of Principal Collections

The issuing entity will apply your series’ share of collections of principal receivables each month as follows:

Revolving Period

During the revolving period, no principal will be paid or accumulated in a trust account for you.

Accumulation Period

During the accumulation period, your series’ share of principal collections will be deposited in a trust account, up to a specified controlled accumulation amount on each distribution date. Amounts on deposit in that account will be paid, first, to the Class A noteholders until the Class A notes are paid in full, then to the Class B noteholders until the Class B notes are paid in full, and then to the Class C noteholders until the Class C notes are paid in full, on the expected principal payment date for the notes, unless a pay-out event occurs. If a pay-out event does not occur, the accumulation period will end on the Series Termination Date.

Rapid Amortization Period

A rapid amortization period for your series will start if a pay-out event occurs. The pay-out events for your series are described under “—Pay-out events” below and “Description of Series Provisions—Pay-out events” in this prospectus. During the rapid amortization period, your series’ share of principal collections will be paid monthly—without any limitation based on the controlled accumulation amount—first to the Class A noteholders, then to the Class B noteholders and then to the Class C noteholders, in each case until the Series Termination Date.

10

Reallocation of Principal Collections

During any of the above periods, principal collections allocated to your series may be reallocated, if necessary, to make required payments of interest on the Class A notes and the Class B notes and monthly servicing fee payments that are not made from your series’ share of finance charge collections, other amounts treated as finance charge collections and excess finance charge collections available from other series that share with your series. This reallocation is one of the ways that the more senior classes of notes obtain the benefit of subordination, as described in the next section of this summary. The amount of reallocated principal collections is limited by the amount of available subordination.

Shared Principal Collections

At all times, collections of principal receivables allocated to your series that are not needed for payments on your series will first be made available to other series, second, deposited in the excess funding account if needed and third, paid to us or our assigns. See “Description of the Notes—Shared Principal Collections” in this prospectus.

With respect to outstanding series of variable funding notes that share excess principal collections with your series of notes, the holders of such outstanding series of variable funding notes are not entitled to distributions from the collections of principal receivables allocated to your series of notes, except to the extent of any excess principal collections shared with such outstanding series of variable funding notes.

The above applications of principal collections allocated to your series are summarized in the diagram on page 20.

Credit enhancement for your series includes subordination and, for the Class C noteholders, a spread account, each as described below. Credit enhancement for your series is for the benefit of your series only, and you are not entitled to the benefits of credit enhancement available to other series.

[Identify any credit enhancement referenced in Item 1114(b) of Regulation AB, and briefly describe what protection or support is provided by the enhancement. To the extent applicable, describe any enhancement provider referenced in Item 1114(b) of Regulation AB.]

Subordination

Credit enhancement for the Class A notes includes the subordination of the Class B notes and the Class C notes.

Credit enhancement for the Class B notes includes the subordination of the Class C notes.

Subordination serves as credit enhancement in the following way. The more subordinated, or junior, classes of notes will not receive payment of interest or principal until required payments have been made to the more senior classes. As a result, subordinated classes will absorb any shortfalls in collections or deterioration in the collateral for the notes prior to senior classes.

Spread Account

Credit enhancement is also available to the Class C noteholders in the form of a spread account. [The spread account will be funded with an initial deposit on the closing date.] [The spread account will not be funded with an initial deposit on the closing date.] The trust will make monthly deposits into the spread account from finance charge collections allocated to your series and excess finance charge collections allocated to your series to the extent the spread account is not funded to the required level. The required level will be adjusted based on the performance of the receivables.

11

If payments of principal and finance charge collections available to the Class C notes are insufficient to pay the principal and interest due on the Class C notes, the indenture trustee will use the funds on deposit in the spread account, if any, to make up the shortfall. Under certain conditions, after the payment of the principal of the Class C notes in full, the remaining funds on deposit in the spread account, if any, may be used to make up a principal shortfall to the Class A notes and then to the Class B notes, in that order of priority. See “Description of Series Provisions—Spread Account; Required Spread Account Amount” in this prospectus.

[Identify any derivative instrument referenced in Item 1115 of Regulation AB, and briefly describe what protection or support is provided by the derivative instrument. Identify any enhancement provider referenced in Item 1115 of Regulation AB.]

The issuing entity will begin to repay the principal of the notes before the expected principal payment date if a pay-out event occurs. A pay-out event will occur if the finance charge collections on the receivables are too low or if defaults are too high. The minimum yield that must be available for your series in any month, referred to as the base rate, is the annualized percentage equivalent of (x) the sum of the interest payable on the Series 20[•]-[•] notes for the related interest period, plus your series’ share of the servicing fee for the related calendar month divided by (y) the collateral amount of your series plus amounts on deposit in the principal accumulation account. If the average portfolio yield for your series, calculated as described in the following sentence, for any three consecutive calendar months is less than the average base rate for your series for the same three consecutive calendar months, a pay-out event will occur.

The portfolio yield for your series for any calendar month will equal the annualized percentage equivalent of:

| • | the amount of finance charge collections and other amounts treated as finance charge collections allocated to your series for that calendar month, excluding amounts withdrawn from the spread account and excess finance charge collections allocated to your series, unless the Hired Agencies consent to excess finance charge collections allocated to your series being included in the calculation of portfolio yield, net of the amount of defaulted principal receivables and uncovered dilution allocated to your series for that calendar month, divided by |

| • | the sum of the collateral amount for your series and amounts on deposit in the principal accumulation account, each as of the first day of that calendar month. |

The other pay-out events are:

| • | Our failure to make required payments or deposits or material failure to perform other obligations, subject to applicable grace periods; |

| • | Material inaccuracies in our representations and warranties, subject to applicable grace periods; |

| • | Any Series 20[•]-[•] notes are not paid in full on the expected principal payment date; |

| • | Bankruptcy, insolvency or similar events relating to us or the bank; |

| • | Our failure to designate receivables arising in additional accounts to the trust as required, subject to a grace period; provided that no pay-out event will occur if we reduce the invested amount of a variable funding note issued by the issuing entity, and after such reduction the Transferor Interest is not less than the Minimum Transferor Interest and the Aggregate Principal Receivables are not less than the Minimum Aggregate Principal Receivables; |

12

| • | Material servicer defaults; |

| • | Our inability to transfer receivables to the trust or the bank’s inability to transfer receivables to us; |

| • | The issuing entity becomes subject to regulation as an “investment company” under the Investment Company Act of 1940; or |

| • | An event of default occurs for the Series 20[•]-[•] notes and their final maturity date is accelerated. |

See “Description of Series Provisions—Pay-out events” in this prospectus for a more detailed description of the pay-out events.

The Series 20[•]-[•] notes are subject to events of default described under “The Indenture—Events of Default; Rights upon Event of Default” in this prospectus. These include, among other things, the failure to pay interest for 35 days after it is due or to pay principal when it is due on the final maturity date.

In the case of an event of default involving bankruptcy, insolvency or similar events relating to the issuing entity, the principal amount of the Series 20[•]-[•] notes automatically will become immediately due and payable. If any other event of default occurs and continues with respect to the Series 20[•]-[•] notes, the indenture trustee or holders of more than 50% of the then-outstanding principal balance of the Series 20[•]-[•] notes may declare the principal amount of the Series 20[•]-[•] notes to be immediately due and payable. These declarations may be rescinded by holders of more than 50% of the then-outstanding principal balance of the Series 20[•]-[•] notes if the related event of default has been cured, subject to the conditions described under “The Indenture— Events of Default; Rights upon Event of Default” in this prospectus.

After an event of default and the acceleration of the notes, collections allocated to Series 20[•]-[•] and the series’ share of funds on deposit in the collection account and the excess funding account will be applied to pay principal of and interest on the Series 20[•]-[•] notes to the extent permitted by law. If the indenture trustee sells a portion of the receivables (subject to certain conditions) or otherwise collects money or property on behalf of the holders of the Series 20[•]-[•] notes, that money or property will be applied first to pay any amounts owed to the indenture trustee pursuant to the indenture and then, to make payments on the Series 20[•]-[•] notes.

To the extent the indenture trustee sells a portion of receivables, the amount of principal receivables and related finance charge collections that may be sold by the indenture trustee is limited to an amount equal to the collateral amount of the Series 20[•]-[•] notes. Following such sale and the application of the sale proceeds, amounts then held in the Collection Account, the Excess Funding Account and any series accounts for the Series 20[•]-[•] notes and amounts available under any credit enhancement relating to the Series 20[•]-[•] notes pursuant to the indenture, the Series 20[•]-[•] notes will no longer be entitled to any allocation of collections or other property constituting the collateral of the trust under the indenture.

Amounts in the spread account will be available to pay interest payments on the Class C notes, and upon the earlier to occur of the final maturity date, the date the outstanding principal balances of Class A notes and Class B notes are reduced to zero or an event of default and acceleration of the Series 20[•]-[•] these amounts will be used to fund any shortfall in principal payments on the Class C notes.

If the Series 20[•]-[•] notes are accelerated or the issuing entity fails to pay the principal of the Series 20[•]-[•] notes on the final maturity date, subject to the conditions described in this prospectus under “The Indenture—Events of Default; Rights upon Event of Default”, the indenture trustee may, if legally permitted, cause the trust to sell (1) principal receivables in an amount equal to the collateral amount for Series 20[•]-[•] and (2) the related finance charge receivables.

13

At the option of the servicer, we will purchase your notes when the outstanding principal amount for your series has been reduced to 10% or less of the initial principal amount. See “Description of the Notes—Final Payment of Principal” in this prospectus. The servicer will give the indenture trustee at least thirty days’ prior written notice of the date on which the servicer intends to direct us to make an optional redemption.

The servicer for the trust is First National Bank of Omaha. First National Bank of Omaha, as servicer, receives a fee for its servicing activities. The share of the servicing fee allocable to Series 20[•]-[•] for each transfer date will be equal to one-twelfth of the product of (a) [2]% and (b) the collateral amount for Series 20[•]-[•] on the last day of the prior monthly period. However, the servicing fee for the first monthly period will be based on the number of days from the closing date through and including [•] [•], 20[•] and will be approximately $[•]. If First National Bank of Omaha is the servicer or the indenture trustee is the successor servicer, three quarters of the monthly servicing fee will be payable only to the extent of interchange allocated to the Series 20[•]-[•] notes. Following a servicer default and the appointment of a successor servicer, the successor servicer will be entitled to receive excess servicing fees for each month in an amount equal to one-twelfth of the excess of the market rate servicing fee percentage, as determined by the indenture trustee, over [2]%. In addition, if the indenture trustee is the successor servicer, the excess servicing fee will include any base servicing fee amounts not paid due to shortfalls. The servicing fee allocable to Series 20[•]-[•] for each transfer date will be paid from your series’ share of collections of finance charge receivables as described in “—Application of Finance Charge Collections” above and in “Description of Series Provisions—Application of Finance Charge Collections” below.

Fees and Expenses for Asset Review

The asset representations reviewer will be entitled to a one-time upfront fee and an annual fee. Payment of the asset representation reviewer’s fees will be made by the servicer from its own funds. The annual fee does not include the fees and expenses of the asset representations reviewer in connection with an asset review. With respect to each asset review, the asset representations reviewer will be entitled to receive a fee for the asset review, plus its out of pocket expenses (including travel and legal expenses) incurred in connection with the asset review. Payment of the fee and expenses relating to asset reviews will be made by the servicer from its own funds.

Subject to important considerations described under “Federal Income Tax Consequences” in this prospectus, Kutak Rock LLP as special federal tax counsel to the issuing entity, is of the opinion that under existing law the offered notes will be characterized as debt for federal income tax purposes and that the issuing entity will not be classified as an association or constitute a publicly traded partnership taxable as a corporation for U.S. federal income tax purposes. By your acceptance of an offered note, you will agree to treat your offered notes as debt for federal, state and local income and franchise tax purposes. See “Federal Income Tax Consequences” in this prospectus for additional information concerning the application of federal income tax laws.

Subject to important considerations described under “ERISA Considerations” in this prospectus, the Class A notes are eligible for purchase by persons investing assets of employee benefit plans or individual retirement accounts. If you are contemplating purchasing the Series 20[•]-[•] notes on behalf of or with plan assets of any plan or account, we suggest that you consult with counsel regarding whether the purchase or holding of the Series 20[•]-[•] notes could give rise to a transaction prohibited or not otherwise permissible under Title I of the Employee Retirement Income Security Act of 1974, as amended (“ERISA”) or Section 4975 of the Internal Revenue Code of 1986, as amended (the “Code”) or other applicable state law. Each purchaser that purchases a note offered hereunder will be deemed to represent and warrant that either (i) it is not acquiring the note with assets of (or on behalf of) a benefit plan or any other plan that is subject to Title I of ERISA or Section 4975 of the Code, any entity deemed to hold “plan assets” of either of the foregoing or any plan that is subject to any law that is substantially similar to the fiduciary responsibility or prohibited transaction provisions of Title I of ERISA or Section 4975 of the Code, or (ii) its purchase, holding and disposition of the note will not result in a non-exempt prohibited transaction under ERISA, Section 4975 of the Code or any substantially similar applicable law. See “ERISA Considerations” in this prospectus.

14

Investment in the Series 20[·]-[·] notes involves significant risks, most of which could result in accelerated, delayed or reduced payments on your notes. We have summarized these risks below and described them more fully under the heading “Risk Factors”, beginning on page 21 below. You should consider these risks carefully.

Business Risks Relating to the Bank’s Credit Card Business

The COVID-19 pandemic has reduced cardholder use, and the extent to which the pandemic and measures taken in response to the pandemic could materially and adversely impact cardholder use, payment patterns and the performance of the credit card receivables in the future and, consequently, the timing and amount of collections will depend on future developments, which are highly uncertain and difficult to predict.

The bank faces risks related to its operational, technological and organizational infrastructure that could affect its business and operations, including the ability to service its credit card accounts, originate credit card accounts, or generate new receivables.

In the event of the theft, loss or misuse of information, including as a result of cyber-attack, the bank could suffer damage to its reputation and disruptions to its credit card servicing, origination of credit card accounts and generation of new receivables.

Climate change manifesting as physical or transition risks could adversely affect the bank’s credit card business and cardholders.

High concentrations in a geographic area could affect the collection rate on the receivables.

The bank may change the terms and conditions of the accounts in a way that reduces collections.

Payment and origination patterns of receivables, finance charge rates and credit card usage could reduce collections.

Changes in, or termination of, a material co-branding or agent bank arrangement may affect the performance of the trust’s receivables and cardholder usage.

Some customers may provide information that is not accurate or intentionally false during the underwriting process.

The underwriting and risk management efforts of the bank may not be effective.

Insolvency and Security Interest Risks

If a conservator or receiver were appointed for First National Bank of Omaha, or if we become a debtor in a bankruptcy case, delays or reductions in payment of your notes could occur.

Some liens would be given priority over your notes which could cause delayed or reduced payments.

Other Legal and Regulatory Risks

Regulatory risk could result in losses.

Current and proposed regulation and legislation relating to consumer protection laws may impede collection efforts or reduce collections or restrict the manner in which the bank may conduct its activities.

Financial regulatory reform legislation could have a significant impact on us, the issuing entity and the bank.

Enforcement actions taken by the Consumer Financial Protection Bureau and the OCC may adversely impact the bank.

The bank, the transferor and the issuing entity could be named as defendants in litigation, resulting in increased expenses and greater risk of loss on your notes.

The application of the Servicemembers Civil Relief Act or the Military Lending Act may lead to delays in payment or losses on your notes.

Federal tax legislative proposals could impact your investment.

[Certain EEA and United Kingdom regulated investors are subject to EU or United Kingdom (as applicable) risk retention and due diligence requirements applicable to the Class A notes.]

15

Transaction Structure Risks

The interest rate terms of the receivables and those of the notes may differ.

[The Series 20[·]-[·] notes’ interest rate being based on the [Benchmark] may impact the liquidity of the Series 20[·]-[·] notes.]

[Negative [Benchmark] would reduce the rate of interest on your notes.]

An increase in the initial principal amount of the notes may dilute your voting rights.

Variations in cardholder payment patterns may result in reduced payment of principal or receipt of payment of principal earlier or later than expected.

Allocations of charged-off receivables or uncovered dilution could reduce payments to you.

Limited remedies for breaches of representations could reduce or delay payments.

Addition of assets to the trust may affect credit quality and lessen the trust’s ability to make payments to you.

Other series of notes may have different terms that may affect the timing and amount of payments to you.

The bank may, from time to time, use the proceeds from the sale of variable funding notes to fund growth in the bank’s balance sheet.

The servicer may temporarily commingle collections on the receivables.

Recharacterization of principal receivables would reduce principal receivables and may require the addition of new receivables.

We may assign our obligations as depositor and the bank may assign its obligations as servicer.

Payments on your notes may be delayed, reduced or otherwise adversely affected if the servicer fails to perform its servicing obligations.

It may be difficult to find a suitable successor servicer if the bank ceases to act as servicer.

The objective of the asset representations review process is to independently identify noncompliance with a representation or warranty concerning the receivables, but no assurances can be given as to its effectiveness.

The certification provided by the chief executive officer of the transferor does not guarantee the securitization will produce expected cash flows at the time and in the amounts to service scheduled payments of interest and the ultimate payment of principal on the offered notes in accordance with their terms as described in this prospectus.

General Risk Factors

It may not be possible to find investors to purchase your notes.

You may not be able to reinvest any proceeds from an optional redemption or the occurrence of a pay-out event or event of default in a comparable security.

The ratings for the Class A notes are limited in scope, may not continue to be issued, and do not consider the suitability of an investment in the Class A notes for you.

It is possible that other credit rating agencies not hired by the sponsor may provide an unsolicited rating that differs from (or is lower than) the ratings provided by the Hired Agencies.

16