UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

For the fiscal year ended March 31 , 2024

OR

Commission File Number: 1-33026

Commvault Systems, Inc.

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices, including zip code)

(732 ) 870-4000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

þ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ¨

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

As of September 30, 2023, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of voting and non-voting common stock held by non-affiliates of the registrant (based upon the closing price of the common stock as reported by The Nasdaq Stock Market) was approximately $2.9 billion.

As of May 9, 2024, there were 43,401,217 shares of the registrant’s common stock ($0.01 par value) outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

COMMVAULT SYSTEMS, INC.

FORM 10-K

FISCAL YEAR ENDED MARCH 31, 2024

TABLE OF CONTENTS

| Page | ||||||||

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 1C. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

2

FORWARD-LOOKING STATEMENTS

The discussion throughout this Annual Report on Form 10-K contains forward-looking statements. In some cases, you can identify these statements by our use of forward-looking words such as “may,” “will,” “should,” “anticipate,” “estimate,” “expect,” “plan,” “believe,” “predict,” “potential,” “project,” “intend,” “could,” “feel” or similar expressions. In particular, statements regarding our plans, strategies, prospects and expectations regarding our business are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). You should be aware that these statements and any other forward-looking statements in this document reflect only our expectations and are not guarantees of performance. These statements involve risks, uncertainties and assumptions. Many of these risks, uncertainties and assumptions are beyond our control and may cause actual results and performance to differ materially from our expectations. Important factors that could cause our actual results to be materially different from our expectations include the risks and uncertainties set forth under the heading “Risk Factors.” Accordingly, you should not place undue reliance on the forward-looking statements contained in this Annual Report on Form 10-K. These forward-looking statements speak only as of the date on which the statements were made. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

References in this Annual Report on Form 10-K to "Commvault," the "Company", "we," "our" or "us" refer to Commvault Systems, Inc., including as the context requires, its direct and indirect subsidiaries.

3

PART I

| Item 1. | Business | ||||

Company Overview

Incorporated in Delaware in 1996, Commvault Systems, Inc. provides its customers with a scalable platform that enhances customers' cyber resiliency by protecting their data in a world of increasing threats. We provide these products and services for their data across many types of environments, including on-premises, hybrid and multi-cloud. Our offerings are delivered via self-managed software, software-as-a-service ("SaaS"), integrated appliances, or managed by partners. Customers use our Commvault Cloud platform to protect themselves from threats like ransomware and recover their data efficiently.

With Commvault Cloud, customers have access to business-critical capabilities such as layered defenses to detect and minimize the impact of bad actors; automation to verify clean recovery points; and cloud-native capabilities to dedupe, scale, and as necessary, recover business. We believe in solving hard problems for our customers by enabling them to protect their data in a difficult world. Our comprehensive solutions address the critical aspects of modern cyber resiliency, from data security to data recovery, data governance and compliance in a flexible and scalable platform.

Products

Commvault helps customers protect their data and be cyber resilient in a hybrid multi-cloud environment. Commvault delivers a portfolio of products and services to effectively secure, quickly capture intelligence, and rapidly recover from ransomware attacks or any other threats. Our solutions create an intuitive cyber resilience experience across customer-managed enterprise software and SaaS-delivered cloud native solutions that mitigate data sprawl, facilitate cloud adoption, and help customers modernize and transform their enterprise IT environment.

We do this by offering unified visibility and management across the entire hybrid enterprise so our customers can secure and recover data from any location to any location. Our Commvault Cloud offerings are organized in the following packages – Operational Recovery, Autonomous Recovery and Cyber Recovery.

Operational Recovery includes Commvault’s leading backup and recovery capabilities which can be utilized across hybrid enterprise workloads. It includes features like Zero Trust Architecture and immutable storage to ensure critical data is protected and recoverable. This solution can be delivered as customer-managed software, as SaaS, or a mix of the two to meet the requirements of hybrid enterprises worldwide. It is designed to meet the needs of any size business protecting workloads across all locations, including hybrid environments such as on-premises and multiple cloud providers; physical servers; virtual machines (“VMs”); applications and databases; endpoint devices; and cloud applications. Operational Recovery provides backup, verifiable recovery, and cost-optimized cloud workload mobility, helping to ensure data availability and granular recovery, even across multiple clouds all managed with Commvault’s Command Center.

Autonomous Recovery aims to reduce recovery time, downtime, and costs by bringing automation and validation to Operational Recovery. Designed for automated disaster and cyber recovery use cases, Autonomous Recovery can deliver backup, replication, and disaster recovery for all workloads, on-premises, in the cloud, across multiple clouds, and in hybrid environments. It provides trusted recovery of data and applications, VMs, and containers, along with verifiable recoverability of replicas, cost-optimized cloud data mobility and resilience. Organizations can automatically failover applications to the secondary site in the event of a data incident and continue running without interruption.

Cyber Recovery offers the most comprehensive set of Commvault Cloud capabilities. Building on Operational and Autonomous Recovery Solutions, Cyber Recovery adds data backup and data validation capabilities which help organizations scan for risks, remediate issues, identify compromises in the backup data, and recover clean data at scale. This includes threat scanning to hunt for threats within backup data and cyber deception and threat detection to provide early warning of attacks. This enables organizations to minimize the impact of attacks and aims towards a fast recovery after a cyber incident.

In addition, Commvault provides customers with a variety of industry-leading offerings, including Cleanroom Recovery, HyperScale X, Air Gap Protect and Compliance.

Commvault Cloud’s Cleanroom Recovery is a resilience offering. Traditional isolated on-premises cleanrooms can be expensive to build and maintain, and incident response plans often go untested, increasing an

4

organization’s risk and recovery time objectives. Our Cleanroom Recovery solution empowers organizations to be ready to recover by providing a clean, isolated, and on-demand recovery location in the cloud, as well as the ability to regularly and proactively test their response plans and recover quickly.

Commvault HyperScale X is an intuitive, easy-to-deploy and scale-out, integrated data protection solution to help enterprises transition from legacy scale-up infrastructures to the hybrid cloud, container and virtualized environments. Its flexible architecture allows customers to get up, run quickly and scale while delivering comprehensive data protection for all workloads, including containers, VMs and databases, from a single, extensible platform. With HyperScale X, customers can leverage the entire Commvault portfolio, giving them access to all the features, functions, and industry-leading integration with applications, databases, public cloud environments, hypervisors, operating systems, NAS systems, and primary storage arrays, wherever the data resides. It is available as a fully integrated appliance or as a reference architecture depending on an organization’s requirements.

Commvault Cloud Air Gap Protect is the “easy button” to adopt secure and scalable cloud storage in minutes, supporting an organization's hybrid cloud strategy without the need for additional cloud expertise. It is an integrated, air-gapped cloud storage target that enables IT organizations to efficiently adopt cloud storage for Operational Recovery, HyperScale X or SaaS to ease digital transformation, save costs, reduce risk and scale. This minimizes IT complexities and allows customers to easily store, isolate, and secure data while providing the foundation for predictable costs and reduced overhead.

Commvault's Compliance is an add-on product that facilitates efficient compliance and aids in ensuring relevant legal data remains unaltered. It provides built-in reporting, auditing, and logging to help ensure data is not modified or deleted for legal and compliance purposes. It reduces the time and costs spent between IT and legal departments to expedite discovery and review.

Professional & Customer Support Services

Commvault offers a wide range of professional and customer support services to complement its product portfolio. We offer multiple levels of service that can be tailored to our customers’ needs.

Our services consist of:

•Real-Time Support. Customers have 24/7 access to support with our support staff available by phone for first responses and to manage resolutions. Our customers also have access to an online support database for help with troubleshooting and operational questions. Innovative use of web-based diagnostic tools provides problem analysis and resolution. Our comprehensive customer support includes “summary of findings” problem analysis, intelligent alerting and troubleshooting assistance.

•Broad Expertise. Our support engineers have extensive knowledge of complex applications, servers and networks. We proactively take ownership of the customer’s problem. We have also developed and maintain a knowledge library of storage systems and software products to further enable our support organization to quickly and effectively resolve customer problems.

•Global Operations. We offer our global customer support from physical locations around the world, which allows us to provide 24/7 support. Our cloud-based support system creates a virtual global support center combining these locations to allow for the fastest possible resolution times for customer incidents. We have designed our support infrastructure to scale with the increasing globalization of our customers.

•Customer Success Options. We offer various enhanced Customer Success options, including Enterprise Success Program ("ESP") offerings, to our software and SaaS customers. Our Customer Success offerings provide resources focused on proactively helping our customers achieve their goals and are aligned to their business initiatives. Our ESP provides additional industry technical experts who provide strategic guidance and advice to ensure our enterprise customers achieve their cyber resiliency objectives. The entire Customer Success program is centered around driving customer adoption, customer satisfaction and quick time to value.

5

•Technology Consulting Services. Our technical consultants ensure that customers’ data protection environment is designed for optimal results, configured quickly, and is easy to maintain. We offer architecture design; implementation; automation and orchestration; data migration; and health assessment services. In addition, we offer customers staff-augmentation options via resident support engineers to assist with rapid expert deployment and operation of the Commvault portfolio.

•Recovery Services. Commvault Readiness Solutions provide the resources and expertise to quickly accelerate returning to normal business operations through the proper design, implementation, administration, and support of our customers' data protection and cyber resilience environment.

•Education Services. We offer training content for learners at all levels, with basic, intermediate, and expert certifications available. We also provide a selection of self-paced online content for our products in our On-Demand Learning Library.

•Remote Managed Services. Commvault Remote Managed Services provide results-oriented data protection and cyber resilience to customers worldwide. Commvault experts provide secure, reliable, and cost-effective remote monitoring and management of our customers' data protection environment.

Customers

Our current customer base spans thousands of organizations across a variety of sizes, including large global enterprise companies, and small or mid-sized businesses and government agencies. We support customers in a range of industries, including banking, insurance and financial services, government, healthcare, pharmaceuticals and medical services, technology, legal, manufacturing, utilities and energy.

Strategic Relationships

An important element of Commvault’s strategy is to establish partnerships that support development, marketing, selling and implementation of our solutions. We believe that strategic and technology-based relationships with industry leaders are fundamental to our success. We have forged numerous relationships with software, hardware, cloud and cybersecurity partners to enhance our combined capabilities and to create the optimal combination of data and information management applications. We believe this approach enhances our ability to expand our product offerings and customer base and to enter new markets. We have established the following types of strategic relationships:

Alliance and Technology Partners. We maintain strategic sales, marketing and technology relationships with industry leaders to ensure that our products are integrated with, supported by and add value to our partners’ portfolios. Collaboration with these market leaders allows us to provide solutions that enable our customers to improve data and information management efficiency. We also maintain relationships with a broad range of industry operating system, application and infrastructure vendors to verify and demonstrate the interoperability of our portfolio with their equipment and technologies. We believe these partnerships enhance our position in the market and serve as an accelerator to sales.

Distributors, Value-Added Reseller, Systems Integrator, Corporate Reseller and Original Equipment Manufacturer Relationships. These partners either bundle our solutions together with their own products or resell our solutions independently.

To broaden our market coverage, we work closely with our global original equipment manufacturer ("OEM") partners, investing significant time and resources to deliver joint solutions incorporating Commvault solutions. These partners team with our technical, engineering, marketing and sales force to enhance integration, tuning, operational management, implementation and vision for solutions that are designed to meet current and future data protection and cyber resilience needs. Our alliance managers work directly with global OEM partners to design, deliver and support field activities that make it easier for customers to locate, learn about, and purchase these differentiated solutions.

Additionally, we have a non-exclusive distribution agreement with Arrow Enterprise Computing Solutions, Inc. ("Arrow"), a subsidiary of Arrow Electronics, Inc. Arrow's primary role is to enable a more efficient and effective distribution channel for our products and services by managing our reseller partners and leveraging their own industry experience. Sales generated through our distribution agreement with Arrow accounted for 36% of our total revenue in fiscal 2024 and 37% in fiscal 2023.

6

Service Provider Partners. Our solutions are the cyber resilience platform for many service providers, which provide cloud-based solutions to customers worldwide. As companies of all sizes and markets rapidly adopt cloud infrastructures for cost efficiencies, speed and agility, we remain committed to these strategic relationships to address this growing trend. Customers looking to move IT operations to the cloud depend on service providers to migrate, manage and protect their data and cloud infrastructures. We partner with a broad ecosystem of managed service providers and cloud partners to effectively deliver data protection-as-a-service solutions based on Commvault solutions across geographies, vertical markets and offerings.

Marketplace. During fiscal year 2024, we began selling our solutions via marketplace offerings which enable customers to purchase our solutions through online platforms, such as Microsoft, AWS or Google. The marketplace allows us to publish an offer which an end user can then purchase directly, or through the assistance of a partner.

Competition

The data protection and cyber resilience market is intensely competitive and highly fragmented. The principal competitive factors in our industry include product functionality, performance, integration, platform coverage, scalability, price, global sales infrastructure, technical support, branding and reputation. The ability of major system vendors to bundle solutions is also a significant competitive factor in our industry.

Our primary competitors in the data protection software applications market, each of which has one or more products that compete with a part of or our entire product suite, include Avepoint, Cohesity, Dell-EMC, Druva, IBM, Rubrik, Veeam, and Veritas.

Some of our competitors have greater financial resources and may have the ability to offer their products at lower prices than ours. In addition, some have greater name recognition, longer operating histories, substantially larger technical, sales, marketing and other global resources, and larger installed customer base with broader product offerings. As a result, these competitors can devote greater resources to the development, promotion, sale and support of their products than we can. Refer to our "Risk Factors" below.

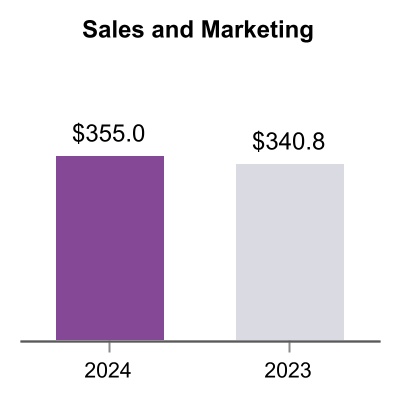

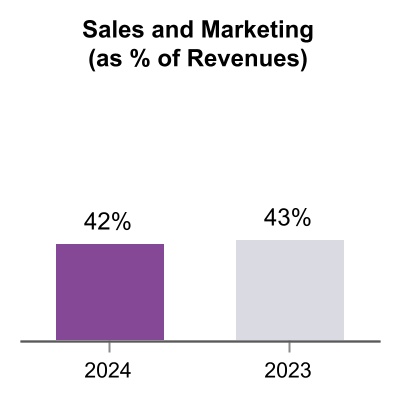

Sales and Marketing

We sell our cyber resilience solutions to businesses of all sizes and government agencies. We sell through our global direct sales force and partner channels.

We have a variety of marketing programs designed to create brand awareness and market recognition for our product offerings and sales lead generation. Our marketing efforts include sales campaigns, webinars, active participation at trade shows, technical conferences and seminars; advertising; content development and distribution; public relations; social media; industry analyst relations; publication of technical and educational articles in industry journals; sales training; and preparation of competitive analyses. In addition, our strategic partners augment our marketing and sales campaigns through seminars, trade shows, joint public relations and advertising campaigns. Our customers and strategic partners provide references and recommendations that we often feature in external marketing activities.

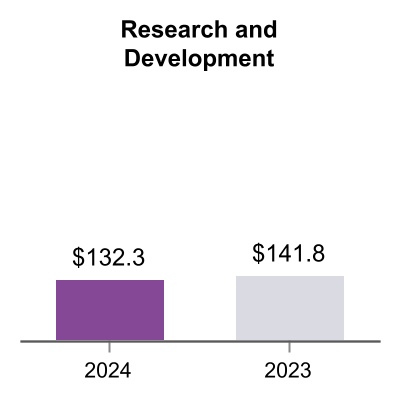

Research and Development

Our research and development organization is responsible for the design, development, testing and certification of our cyber resilience platform and solutions. Our engineering efforts support product development across all major operating systems, databases, applications, hyperscalers and network storage devices. A substantial amount of our development effort goes into certification, integration and support of our solutions to ensure interoperability with our strategic partners’ solutions. We have also made substantial investments in the automation of our product test and quality assurance laboratories.

Technology, Intellectual Property and Proprietary Rights

We believe our solutions are a major differentiator versus our competitors’ portfolios. Our Commvault Cloud platform powered by Metallic AI aims to deliver the highest security, most intelligence, and fastest recovery across on-premises, hybrid and multi-cloud environments. Our solutions’ unique features drive the performance, scale, TCO benefits and interoperability of our offerings. Such features include encryption, indexing and immutable recovery. Additional options enable content search and auditing features to support data discovery and compliance.

7

Our success and ability to compete depend on our continued development and protection of our solutions. We rely primarily on a combination of trade secret, patent, copyright and trademark laws, as well as contractual provisions, to establish and protect our intellectual property rights.

We patent our technical infrastructure and key usability and design concepts. Our software’s unique capabilities are covered by a robust portfolio of patents worldwide. Areas such as cyber resilience, data protection, security, transformation, insights, and compliance and governance, including our SaaS and HyperScale X solutions, are core to our competitive advantage. More than 1,400 patents have been issued to Commvault globally as a result of our strategic patenting. We also have established proprietary trademark rights in markets across the globe, and Commvault owns over 150 worldwide trademark registrations and pending registration applications. Refer to our “Risk Factors” below.

Government Regulations

The global legal environment of technology businesses is evolving rapidly and is often unclear. These topics include data privacy and security, pricing, advertising, taxation, economic sanctions, content regulation and intellectual property ownership and infringement.

We are subject to several local, state, federal and foreign laws and regulations regarding privacy and data protection. Regulators around the world have adopted or proposed limitations on, or requirements regarding, the collection, distribution, use, security and storage of personal information, payment card information or other confidential information of individuals, and the U.S. Federal Trade Commission and many state attorneys general are applying federal and state consumer protection laws to impose standards on the online collection, use and dissemination of data. In the event of a security breach, these laws may subject us to incident response, notice and remediation costs. Failure to safeguard data adequately or to destroy data securely could subject us to regulatory investigations or enforcement actions under applicable data security, unfair practices or consumer protection laws. The scope and interpretation of these laws could change, and the associated burdens and our compliance costs could increase in the future.

We are also subject to global laws and regulations that govern or restrict our business and activities in certain countries and with certain persons, including the U.S. Commerce Department’s Export Administration Regulations and economic and trade sanctions regulations maintained by OFAC, as well as anti-bribery and anti-corruption laws and regulations, including the FCPA and the U.K. Bribery Act.

People

Commvault aims to unlock potential in data, customers and our employees. To accomplish that, our employees are empowered to drive innovation and help our customers—by inspiring one another and working to make what’s already great, even greater—whether that’s product, process or team. As of March 31, 2024, we had 2,882 employees worldwide, of which approximately 40% were in the United States and 60% were located internationally.

We remain committed to providing employees with opportunities and resources that enable them to work successfully and creatively, while also investing in their professional and personal development. Throughout fiscal 2024, our employees participated in over 1,200 training programs, totaling more than 190,000 hours.

Diversity, Equity and Inclusion

At Commvault, we believe that diversity is a business imperative at the heart of our human capital management strategy. We not only drive the ability to be a best-in-class cyber resilience organization but also uphold our value in the marketplace by leading as an employer of choice.

We continue to elevate our employee engagement and belonging efforts which is the foundation of our approach. We have implemented an Employee Resource Group (“ERG”) operating model and have established five ERGs for cross-cultural learning, mentoring and relationship building across employees:

1.Women in Technology (WiT)

2.Multi-Culture

3.PRISM (LGBTQ+ & Allies)

4.VALOR (Veterans & Allies)

5.CapAbilities (Disability inclusion)

We also have two Employee Affinity Groups: Family Support Network and Environmental Group - VAST (Vaulters Advocating Sustainable Technology). Foundational to these engagement initiatives is our Courageous

8

Conversations program designed to foster difficult conversations in an open, safe and respectful manner. This program has become the hub for all diversity, equity and inclusion issues and related conversations, where employees and senior leaders share courageous life experiences related to bias and social injustice. Since its inception, we have hosted powerful sessions, each virtually, reaching our workforce around the globe.

We continue to be committed to securing the best talent with a concerted effort to expound on and build an inclusive and diverse pipeline of candidates. We are committed to providing an environment that fosters career growth, investing in the development, creativity and aspirational needs of all employees.

Employee Health, Safety and Wellness

Commvault values its people and their contribution to our company. In return for their contribution, we are committed to providing a corporate culture that is focused on the health, safety and well-being of our employees. We take a holistic approach to health and wellness to support the dynamic aspects of our employees’ lives, including their physical, social, emotional, family and financial well-being. We operate in accordance with applicable safety laws and procedures to ensure we provide a safe work environment for all.

Information about our Executive Officers

The following table presents information with respect to our executive officers as of May 9, 2024:

| Name | Age | Position | ||||||||||||

| Sanjay Mirchandani | 59 | President and Chief Executive Officer | ||||||||||||

| Gary Merrill | 49 | Chief Financial Officer | ||||||||||||

Sanjay Mirchandani has served as our President and Chief Executive Officer ("CEO") since February 2019. Prior to joining Commvault, Mr. Mirchandani served from September 2016 to January 2019 as the Chief Executive Officer of Puppet, Inc. (“Puppet”), an Oregon-based IT automation company. Mr. Mirchandani joined Puppet in May 2016 as President and Chief Operating Officer. Mr. Mirchandani brings a wealth of international business experience through his diverse well-rounded career in technology. Before joining Puppet, from October 2013 to April 2016, Mr. Mirchandani served as Corporate Senior Vice President and General Manager of Asia Pacific and Japan at VMware, Inc. and, from June 2006 to October 2013, Mr. Mirchandani held various senior leadership positions at EMC Corporation, including Chief Information Officer and leader of the Global Centers of Excellence. Prior to that, Mr. Mirchandani held various positions at Microsoft Corporation and Arthur Andersen LLP. Mr. Mirchandani has a Master of Business Administration degree from the University of Pittsburgh and a bachelor’s degree in mathematics from Drew University.

Gary Merrill has served as our Chief Financial Officer ("CFO") since July 2022. Prior to his current role, Mr. Merrill served as our Chief of Business Operations from April 2021 until June 2022. He also held the position of Vice President of Operations from April 2019 through March 2021 and from December 2012 to March 2019, served as Chief Accounting Officer. Prior to joining Commvault, Mr. Merrill held accounting management positions with several publicly traded companies. Mr. Merrill began his career with Arthur Anderson LLP in its audit practice. Mr. Merrill obtained his bachelor’s degree in accounting from Elizabethtown College.

Available Information

Our website is located at: www.commvault.com. On the Investor Relations section of the website, we post filings as soon as reasonably practicable after they are electronically filed with or furnished to the U.S. Securities and Exchange Commission ("SEC"), including: our Annual Reports on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K, our proxy statements related to our annual stockholders’ meetings and any amendment to those reports or statements filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. All such filings are available on the Investor Relations portion of our website free of charge. The contents of our website are not incorporated by reference into this Form 10-K or in any other report, statement or document we file with the SEC.

9

| Item 1A. | Risk Factors | ||||

You should consider each of the following factors as well as the other information in this Annual Report in evaluating our business and our prospects. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently consider immaterial may also impair our business operations. If any of the following risks actually occur, our business and financial results could be harmed. In that case, the trading price of our common stock could decline. You should also refer to the other information set forth in this Annual Report, including our financial statements and the related notes.

Risks Related to Our Business

Our industry is intensely competitive, and many of our competitors have greater financial, technical and sales and marketing resources and larger installed customer bases, which could enable them to compete more effectively than we do.

The cyber resiliency market is intensely competitive, highly fragmented and characterized by rapidly changing technology and evolving standards, changing customer requirements and frequent new product introductions. Competitors vary in size and in the scope and breadth of the products and services offered.

The principal competitive factors in our industry include product functionality and integration, platform coverage, ability to scale, price, worldwide sales infrastructure, global technical support, brand recognition and reputation. If we are unable to address these factors, our competitive position could weaken and we could experience a decline in revenues that could adversely affect our business.

It is also costly and time-consuming to change data management systems. Most of our new customers have installed data management systems, which gives an incumbent competitor an advantage in retaining a customer because the incumbent already understands the network infrastructure, user demands and information technology needs of the customer, and because some customers are reluctant to invest the time and money necessary to change vendors.

New competitors entering our markets can have a negative impact on our competitive positioning. In addition, we expect to encounter new competitors as we enter new markets. Furthermore, many of our existing competitors are broadening their operating systems platform coverage. We also expect increased competition from OEMs, including those we partner with, and from systems and network management companies, especially those that have historically focused on the mainframe computer market and have been making acquisitions and broadening their efforts to include data protection products. We expect that competition will increase as a result of future industry consolidation. Increased competition could harm our business by causing, among other things, price reductions of our products, reduced profitability and loss of market share.

We rely on indirect sales channels, such as value-added resellers, systems integrators, corporate resellers, distributors, OEMs, and marketplaces for the distribution of our solutions, and the failure of these channels to effectively sell our solutions could have a material adverse effect on our revenues and results of operations.

We rely significantly on our value-added resellers, systems integrators and corporate resellers, which we collectively refer to as resellers, for the marketing and distribution of our products and services. Resellers are our most significant distribution channel. However, our agreements with resellers are generally not exclusive, are generally renewable annually, typically do not contain minimum sales requirements and in many cases may be terminated by either party without cause. Many of our resellers carry data protection solutions that compete with ours. These resellers may give a higher priority to other software or SaaS applications, including those of our competitors, or may not continue to carry data protection solutions. If a number of resellers were to discontinue or reduce the sales of our products, or were to promote our competitors’ products in lieu of our own, it could have a material adverse effect on our future revenues. Events or occurrences of this nature could seriously harm our sales and results of operations. If we fail to manage our resellers successfully, there may be conflicts between resellers or they could fail to perform as we anticipate, including required compliance with the terms and obligations of our agreement, either of which could reduce our sales or impact our reputation in the market. In addition, we expect that a portion of our sales growth will depend upon our ability to identify and attract new resellers. Our competitors also use reseller arrangements and may be more successful in attracting reseller partners and could enter into exclusive relationships with resellers that make it difficult to expand our reseller network. Any failure on our part to maintain and/or expand our network of resellers could impair our ability to grow revenues in the future.

10

Some of our resellers may, either independently or jointly with our competitors, develop and market solutions that compete with our offerings. If this were to occur, these resellers might discontinue marketing and distributing our solutions. In addition, these resellers would have an advantage over us when marketing their competing products and related services because of their existing customer relationships. The occurrence of any of these events could have a material adverse effect on our revenues and results of operations.

In addition, we have a non-exclusive distribution agreement with Arrow pursuant to which Arrow’s primary role is to enable a more efficient and effective distribution channel for our solutions by managing our resellers and leveraging their own industry experience. Arrow accounted for approximately 36% of our total revenues for fiscal 2024 and 37% of our total revenues in both fiscal 2023 and fiscal 2022. If Arrow were to discontinue or reduce the sales of our solutions or if our agreement with Arrow was terminated, and if we were unable to take back the management of our reseller channel or find another distributor to replace Arrow, there could be a material adverse effect on our future business.

Our OEMs sell and integrate our solutions which represents a material portion of our revenues. We have no control over the shipping dates or volumes of systems these OEMs sell and they have no obligation to sell systems incorporating our solutions. They also have no obligation to recommend or offer our solutions exclusively or at all. They have no minimum sales requirements and can terminate our relationship at any time. These OEMs also could choose to develop their own data protection solutions. Our OEM partners compete with one another. If one of our OEM partners views our arrangement with another OEM as competing, it may decide to stop doing business with us. Any material decrease in the volume of sales generated by OEMs could have a material adverse effect on our revenues and results of operations in future periods.

We also sell our solutions via marketplace offerings which enable customers to purchase our solutions through online platforms, typically hosted by a cloud provider. The marketplace allows us to publish an offer which an end user can then purchase directly, or through the assistance of a partner. Similar to our resellers and OEMs, marketplace providers have no obligation to sell or recommend our solutions or offer our solutions exclusively or at all. Sales through the marketplace have not been material to date; however, we anticipate an increase in revenue through this channel. Failure to effectively compete in the marketplace could have a material adverse effect on our revenues and results of operations in future periods.

If the cost for maintenance and support agreements, or our term-based subscription licenses and SaaS arrangements, with our customers is not competitive in the market or if our customers do not renew their agreements either at all, or on terms that are less favorable to us, our business and financial performance might be adversely impacted.

Most of our support and maintenance agreements are for a one-year term and thereafter, we pursue renewal thereof. Historically, such renewals have represented a significant portion of our total revenue. If our customers do not renew their annual maintenance and support agreements either at all, or on terms that are less favorable to us, our business and financial performance might be adversely impacted.

Additionally, a significant amount of our revenues are from term-based software license and SaaS arrangements. The arrangements are typically one to three years in duration. If at the end of the initial term, customers elect to not renew, or they renew terms that are less favorable to us, our business and financial performance might be adversely impacted.

In periods of volatile economic conditions, our exposure to credit risk and payment delinquencies on our accounts receivable significantly increases.

Our outstanding accounts receivables are generally not secured. Our standard terms and conditions permit payment within a specified number of days following the receipt of our solution. Volatile economic conditions, including those related to the wars in Israel and Ukraine and the global response to the conflicts, the COVID-19 pandemic and its variants, or the financial instability of banking institutions could result in our customers and resellers facing liquidity concerns leading to them not being able to satisfy their payment obligations to us, which would have a material adverse effect on our financial condition, operating results and cash flows.

In addition, we have transitioned a more significant percentage of our revenue to subscription, or term-based, arrangements. In these arrangements, our customers may pay for solutions over a period of several years. Due to the potential for extended period of collection, we may be exposed to more significant credit risk.

11

We develop solutions that interoperate with certain products, operating systems and hardware developed by others, and if the developers of those operating systems and hardware do not cooperate with us or we are unable to devote the necessary resources so that our solutions interoperate with those systems, our development efforts may be delayed or foreclosed and our business and results of operations may be adversely affected.

Our solutions operate primarily on the Windows, UNIX, Linux and Novell Netware operating systems; used in conjunction with Microsoft SQL; and on hardware devices of numerous manufacturers. When new or updated versions of these operating systems, solution applications, and hardware devices are introduced, it is often necessary for us to develop updated versions of our solution applications so that they interoperate properly with these systems and devices. We may not accomplish these development efforts quickly or cost-effectively, and it is not clear what the relative growth rates of these operating systems and hardware will be.

We encounter long sales and implementation cycles, particularly for our larger customers, which could have an adverse effect on the size, timing and predictability of our revenues.

Potential or existing customers, particularly larger enterprise customers, generally commit significant resources to an evaluation of available solutions and require us to expend substantial time, effort and money educating them as to the value of our solutions. Sales often require an extensive education and marketing effort.

We could expend significant funds and resources during a sales cycle and ultimately fail to win the customer. Our sales cycle for all of our products and services is subject to significant risks and delays over which we have little or no control, including:

•our customers’ budgetary constraints;

•the timing of our customers’ budget cycles and approval processes;

•our customers’ willingness to replace their current solutions;

•our need to educate potential customers about the uses and benefits of our solutions; and

•the timing of the expiration of our customers’ current agreements for similar solutions.

If our sales cycles lengthen unexpectedly, they could adversely affect the timing of our revenues or increase costs, which may cause fluctuations in our quarterly revenues and results of operations. Finally, if we are unsuccessful in closing sales of our solutions after spending significant funds and management resources, our operating margins and results of operations could be adversely impacted, and the price of our common stock could decline.

We depend on growth in the data protection and cyber resiliency market, and lack of growth or contraction in this market could have a material adverse effect on our sales and financial condition.

Demand for data protection and cyber resilience solutions is linked to growth in the amount of data generated and stored, demand for data retention and management (whether as a result of regulatory requirements or otherwise) demand for and adoption of new backup devices and networking technologies, and ability to respond to and recover from data breaches in a secure environment. Because our solutions are concentrated within the data protection and cyber resiliency market, if the demand for backup and data protection solutions devices declines, our sales, profitability and financial condition would be materially adversely affected.

Furthermore, the data protection and cyber resiliency market is dynamic and evolving. Our future financial performance will depend in large part on continued growth in the number of organizations adopting data protection and cyber resilience solutions for their environments. The market for data protection and cyber resilience solutions may not continue to grow at historic rates, or at all. If this market fails to grow or grows more slowly than we currently anticipate, our sales and profitability could be adversely affected.

Our SaaS offerings require costly and continual infrastructure investments and if these investments do not yield the expected return, our business and financial performance might be adversely impacted.

In order to deliver our SaaS offerings via a cloud-based deployment, we have made and will continue to make capital investments and incur substantial costs to implement and maintain this business model. In addition, as we look to deliver new or different cloud-based services, we are making significant technology investments to deliver new capabilities and advance our software to deliver cloud-native customer experiences. Our revenues

12

related to SaaS offerings have increased in recent years. If there is a reduction in demand for these services caused by a lack of customer acceptance, technological challenges, weakening economic or political conditions, security or privacy concerns, inability to properly manage such services, competing technologies and products, decreases in corporate spending or otherwise, our financial results and competitive position could suffer. If these investments do not yield the expected return, or we are unable to decrease the cost of delivering our cloud services, our gross margins, overall financial results, business model and competitive position could suffer.

We rely on third-party hosting providers to deliver our SaaS offerings. Therefore, any disruption or interference with our use of these services could adversely affect our business.

Our use of third-party hosting facilities requires us to rely on the functionality and availability of the third parties’ services, as well as their data security, which despite our due diligence, may be or become inadequate. Our continued growth depends in part on the ability of our existing and potential customers to use and access our cloud services or our website to download our software within an acceptable amount of time. Third-party service providers operate platforms that we access, and we are vulnerable to their service interruptions. We may experience interruptions, delays, and outages in service and availability due to problems with our third-party service providers’ infrastructure. This infrastructure’s lack of availability could be due to many potential causes, including technical failures, power shortages, natural disasters, fraud, terrorism, or security attacks that we cannot predict or prevent. Such outages could trigger our service level agreements and the issuance of credits to our customers, which may impact our business and consolidated financial statements.

If we are unable to renew our agreements with our cloud service providers on commercially reasonable terms, an agreement is prematurely terminated, or we need to add new cloud services providers to increase capacity and uptime, we could experience interruptions, downtime, delays, and additional expenses related to transferring to and providing support for these new platforms. Any of the above circumstances or events may harm our reputation and brand, reduce our platforms’ availability or usage, and impair our ability to attract new users, any of which could adversely affect our business, financial condition, and results of operations.

We sell a backup appliance which integrates our solution with hardware. If we fail to accurately predict manufacturing requirements and manage our supply chain we could incur additional costs or experience manufacturing delays that could harm our business.

We generally provide forecasts of our requirements to our supply chain partners on a rolling basis. If our forecast exceeds our actual requirements, a supply chain partner may assess additional charges or we may incur costs for excess inventory they hold, each of which could negatively affect our gross margins. If our forecast is less than our actual requirements, the applicable supply chain partner may have insufficient time or components to produce or fulfill our solutions' requirements, which could delay or interrupt manufacturing of our products or fulfillment of orders for our solutions, and result in delays in shipments, customer dissatisfaction, and deferral or loss of revenue. If we fail to accurately predict our requirements, we may be unable to fulfill those orders or we may be required to record charges for excess inventory. Any of the foregoing could adversely affect our business, financial condition or results of operations.

Our complex solutions may contain undetected errors, which could adversely affect not only their performance but also our reputation and the acceptance of our solutions in the market.

Our complex solutions may contain undetected errors or failures, especially when they are made generally available or new versions are released. Despite extensive testing by us and customers, we have discovered errors in our solutions in the past and will do so in the future. As a result of past discovered errors, we experienced delays and lost revenues while we corrected those solutions. In addition, customers in the past have brought to our attention “bugs” in our software created by the customers’ unique operating environments, which are often characterized by a wide variety of both standard and non-standard configurations that make pre-release testing very difficult and time consuming. Although we have been able to fix these bugs in the past, we may not always be able to do so. Our solutions may also be subject to intentional attacks by viruses that seek to take advantage of these bugs, errors or other weaknesses. Any of these events may result in the loss of, or delay in, market acceptance of our solutions or damage to our reputation, which would seriously harm our sales, results of operations and financial condition.

Incorrect or improper implementation or use of our data security solutions could result in customer dissatisfaction and harm our business, financial condition, and results of operations.

13

Our products are deployed by our customers and partners in a wide variety of IT infrastructures, including large-scale, complex technology environments, and we believe our future success will depend, at least in part, on our ability to support such deployments. Implementations of our products may be technically complicated, and it may not be easy to maximize the value of our products without proper implementation, training, and support. Some of our customers have experienced difficulties implementing our products in the past and may experience implementation difficulties in the future. If our customers and partners are unable to implement our products successfully, perceptions of our products may be impaired, our reputation and brand may suffer, or customers may choose not to renew their subscriptions or purchase additional products from us.

Any failure by customers or partners to appropriately implement our products could result in customer dissatisfaction, impact the perceived reliability of our products, result in negative press coverage, negatively affect our reputation, and harm our business, financial condition, and results of operations.

We may not receive significant revenues from our current research and development efforts for several years, if at all.

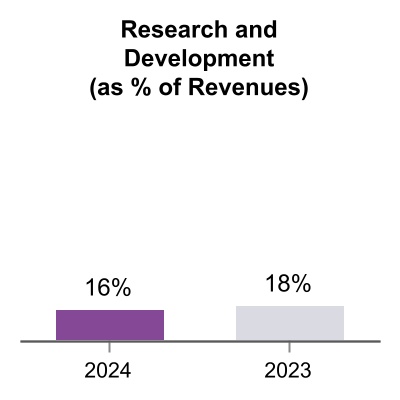

Developing software and technology is expensive, and the investment in product development may involve a long payback cycle. Our research and development expenses were $132.3 million, or 16% of our total revenues in fiscal 2024, $141.8 million, or 18% of our total revenues in fiscal 2023 and $153.6 million, or 20% of our total revenues in fiscal 2022. We believe that we must continue to dedicate a significant amount of resources to our research and development efforts to maintain our competitive position. However, we may not recognize significant revenues from these investments for several years, if at all.

Our ability to sell our solutions is highly dependent on the quality of our customer support and professional services, and failure to offer high quality customer support and professional services would have a material adverse effect on our sales and results of operations.

Our services include the assessment and design of solutions to meet our customers’ storage management requirements and the efficient installation and deployment of our software applications based on specified business objectives. Further, once our software applications are deployed, our customers depend on us to resolve issues relating to our software applications. A high level of service is critical for the successful marketing and sale of our software. If we or our partners do not effectively install or deploy our applications, or succeed in helping our customers quickly resolve post-deployment issues, it would adversely affect our ability to sell software products to existing customers and could harm our reputation with prospective customers. As a result, our failure to maintain high quality support and professional services would have a material adverse effect on our sales of software applications and results of operations.

We implemented a restructuring plan in fiscal 2024, which we cannot guarantee will achieve its intended results.

In fiscal 2024, we initiated a restructuring plan to enhance customer satisfaction, optimize operational efficiency, and align our customer experience functions with our strategic goals. We cannot guarantee the restructuring plan will achieve its intended results. Risks associated with this restructuring plan also include additional unexpected costs, adverse effects on employee morale and the failure to meet operation and growth targets due to the loss of key employees, any of which may impair our ability to achieve anticipated results of operations or otherwise harm our business.

We are subject to several local, state, federal and foreign laws and regulations regarding privacy and data protection, and any actual or perceived failure by us to comply with such laws and regulations could adversely affect our business.

We are currently subject, and may become further subject, to local, state, federal and foreign laws and regulations regarding the privacy and protection of personal data or other potentially sensitive information. In the United States, federal, state, and local governments have enacted numerous data privacy security laws, including data breach notification laws, data privacy laws, consumer protection laws, and other similar laws. For example, the California Consumer Privacy Act of 2018, as amended by the California Privacy Rights Act of 2020 (collectively, the "CCPA"), imposes obligations on certain businesses to provide specific disclosures in privacy notices and grants California residents certain rights related to their personal data. The CCPA imposes statutory fines for noncompliance (up to $7,500 per violation). Other states have enacted or proposed similar laws. These developments may increase legal risk and compliance costs for us and our customers.

14

Outside the United States, an increasing number of laws, regulations, and industry standards govern data privacy and security. For example, the European Union’s ("E.U.") General Data Protection Regulation ("E.U. GDPR"), and the United Kingdom’s ("U.K.") GDPR ("U.K. GDPR"), impose strict requirements for processing the personal data of individuals. Violations of these obligations carry significant potential consequences. For example, under the E.U. GDPR, government regulators may impose temporary or definitive bans on processing, as well as fines of up to €20 million or 4% of the annual global revenue, whichever is greater. Additionally, new and emerging data privacy regimes may be applicable in Asia, including India's Digital Personal Data Protection Act, China's Personal Information Protection Law, Japan's Act on the Protection of Personal Information, and Singapore's Personal Data Protection Act.

In addition, as a technology provider, our customers expect us to demonstrate compliance with current data privacy laws and further make contractual commitments and implement processes to enable the customer to comply with their own obligations under data privacy laws, and our actual or perceived inability to do so may adversely impact sales of our products and services, particularly to customers in highly regulated industries.

Our actual or perceived failure to comply with laws, regulations, contractual commitments, or other actual or asserted obligations, including certain industry standards, regarding personal information, or other confidential information of individuals could lead to costly legal action, brand and reputational damage, significant liability, inability to process data, and decreased demand for our services, which could adversely affect our business. In addition, any security breach that results in the release of, or unauthorized access to, personal information, or other confidential information of individuals could subject us to incident response, notice and remediation costs. Failure to safeguard data adequately or to destroy data securely could subject us to regulatory investigations or enforcement actions under applicable data security, unfair practices or consumer protection laws which could have an adverse effect on our business, financial condition or operating results. The scope and interpretation of these laws could change and the associated burdens and our compliance costs could increase in the future.

A portion of our revenue is generated by sales to government entities, which are subject to a number of challenges and risks.

Sales to global federal, state, and local governmental agencies account for a portion of our revenue, and we may in the future increase sales to government entities. This customer base experiences budgetary constraints or shifts in spending priorities regularly which may adversely affect sales of our solutions to government entities.

Selling to government entities can be highly competitive, expensive and time consuming, often requiring significant upfront time and expense without any assurance that we will successfully sell our solutions. Government entities may require contract terms that differ from our standard terms and conditions including termination rights favorable for the customer, audit rights, and maintenance of certain security clearances for facilities and employees which can entail administrative time and effort resulting in costs and delays. Government demand for our solutions may be more volatile as they are affected by stringent regulations, public sector budgetary cycles, funding authorizations, and the potential for funding reductions or delays, making the time to close such transactions more difficult to predict.

Changes in senior management or key personnel could cause disruption in the Company and have a material effect on our business.

We have had, and could have, changes in senior management which could be disruptive to management and operations of the Company and could have a material effect on our business, operating results and financial conditions. Turnover at the senior management level may create instability within the Company, which could impede the Company’s day-to-day operations. Such instability could impede our ability to fully implement our business plan and growth strategy, which would harm our business and prospects.

We rely on our key personnel to execute our existing business operations and identify and pursue new growth opportunities. The loss of key employees could result in significant disruptions to our business, and the integration and training of replacement personnel could be costly, time consuming, cause additional disruptions to our business and be unsuccessful.

We have engaged, and may continue to engage, in strategic acquisitions or transactions, which could have a material adverse effect on our business, results of operations, financial condition and cash flows.

15

Acquisitions involve a number of risks, including diversion of management’s attention, ability to finance the acquisition on attractive terms, failure to retain key personnel or valuable customers, legal liabilities, the need to amortize acquired intangible assets, and intellectual property ownership and infringement risks, any of which could have a material adverse effect on our business, results of operations, financial condition and cash flows. Any additional future acquisitions may also result in the incurrence of indebtedness or the issuance of additional equity securities.

We could also experience financial or other setbacks if transactions encounter unanticipated problems, including problems related to governmental approval, execution, integration or underperformance relative to prior expectations. Acquisitions may not result in long-term benefits to us or we may not be able to further develop the acquired business in the manner we anticipated.

Following the completion of acquisitions, we may have to rely on the seller to provide administrative and other support, including financial reporting and internal controls, and other transition services to the acquired business for a period of time. There can be no assurance that the seller will do so in a manner that is acceptable to us.

Actual or threatened public health crises could adversely affect our business in a material way.

As a global company, with employees and customers located around the world in a variety of industries, our performance may be impacted by public health crises, including the COVID-19 pandemic and its variants, which has caused global economic uncertainty. The emergence of a public health threat could pose the risk that our employees, partners, and customers may be prevented from conducting business activities at full capacity for an indefinite period, due to the spread of the disease or suggested or mandated by governmental authorities. Moreover, these conditions can affect the rate of information technology spending and may adversely affect our customers’ willingness to purchase our solutions, delay prospective customers’ purchasing decisions, reduce the value or duration of their contracts, cause our customers to request concessions including extended payment terms or better pricing, or affect attrition rates, all of which could adversely affect our future sales and operating results. The global spread of COVID-19 has created significant uncertainty, and economic disruption. We have undertaken measures to protect our employees, partners, and customers, including allowing our employees to work remotely; however, there can be no assurance that these measures will be sufficient or that we can implement them without adversely affecting our business operations.

Borrowing against our revolving credit facility could adversely affect our operations and financial results.

We have a $100 million revolving credit facility. As of March 31, 2024, there were no borrowings under the credit facility. If we were to borrow substantially against this facility the indebtedness could have adverse consequences, including:

•requiring us to devote a portion of our cash flow from operations to payments of indebtedness, which would reduce the availability of cash flow to fund working capital requirements, capital expenditures and other general purposes;

•limiting our flexibility in planning for, or reacting to, general adverse economic conditions or changes in our business and the industry in which we operate in;

•placing us at a competitive disadvantage compared to our competitors that have less debt; and

•limiting our ability to fund potential acquisitions.

The credit facility also contains financial maintenance covenants, including a leverage ratio and interest coverage ratio, and customary events of defaults. Failure to comply with these covenants could result in an event of default, which, if not cured or waived, could accelerate our repayment obligations. For further discussion on our revolving credit facility, see Note 16 of the notes to the consolidated financial statements.

16

Risks Related to our International Operations

If we are unable to effectively manage certain risks and challenges related to our India operations, our business could be harmed.

Our India operations are a key factor to our success. We believe that our significant presence in India provides certain important advantages for our business, such as direct access to a large pool of skilled professionals and assistance in growing our business internationally. However, it also creates certain risks that we must effectively manage. As of March 31, 2024, we had 1,037 employees located in India. Wage costs differentiate depending on regions throughout the world. Wages in India are increasing at a faster rate than in the many other countries, including the United States. These increases could result in us incurring increased costs for technical professionals and reduced margins. There is intense competition in India for skilled technical professionals, and we expect such competition to increase. As a result, we may be unable to cost-effectively retain our current employee base in India or hire additional new talent. In addition, India has experienced significant inflation, low growth in gross domestic product and shortages of foreign exchange. India also has experienced civil unrest and has been involved in conflicts with neighboring countries. The occurrence of any of these circumstances could result in disruptions to our India operations, which, if continued for an extended period of time, could have a material adverse effect on our business.

In recent years, India’s government has adopted policies that are designed to promote foreign investment, including significant tax incentives, relaxation of regulatory restrictions, liberalized import and export duties and preferential rules on foreign investment and repatriations. These policies may not continue. If we are unable to effectively manage any of the foregoing risks related to our India operations, our development efforts could be impaired, our growth could be slowed and our results of operations could be negatively impacted.

Volatility in the global economy could adversely impact our continued growth, results of operations and our ability to forecast future business.

As a global company, we have become increasingly subject to the risks arising from adverse changes in domestic and global economic and political conditions. Uncertainty in the macroeconomic environment and associated global economic conditions have resulted in volatility in credit, equity, debt and foreign currency markets.

These global economic conditions can result in slower economic activity, decreased consumer confidence, reduced corporate profits and capital spending, inflation, adverse business conditions and liquidity concerns. There has also been increased volatility in foreign exchange markets. These factors make it difficult for our customers, our vendors and us to accurately forecast and plan future business activities. These factors could cause customers to slow or defer spending on our solutions, which would delay and lengthen sales cycles and negatively affect our results of operations. If such conditions deteriorate or if the pace of economic recovery is slower or more uneven, our results of operations could be adversely affected, we may not be able to sustain the growth rates we have experienced recently, and we could fail to meet the expectations of stock analysts and investors, which could cause the price of our common stock to decline.

We continue to invest in our business internationally where there may be significant risks with overseas investments and growth prospects. Increased volatility or declines in the credit, equity, debt and foreign currency markets in these regions could cause delays in or cancellations of orders. Deterioration of economic conditions in the countries in which we do business could also cause slower or impaired collections on accounts receivable.

We may experience fluctuations in foreign currency exchange rates that could adversely impact our results of operations.

Our international sales are generally denominated in foreign currencies, and this revenue could be materially affected by currency fluctuations. Our primary exposure is to fluctuations in exchange rates for the U.S. dollar versus the Euro and, to a lesser extent, the Australian dollar, British pound sterling, Canadian dollar, Chinese yuan, Indian rupee, Korean won and Singapore dollar. Changes in currency exchange rates could adversely affect our reported revenues and could require us to reduce our prices to remain competitive in foreign markets, which could also have a material adverse effect on our results of operations. An unfavorable change in the exchange rate of foreign currencies against the U.S. dollar would result in lower revenues when translated into U.S. dollars, although operating expenditures would be lower as well.

In recent fiscal years, we have selectively hedged our exposure to changes in foreign currency exchange rates on the balance sheet. In the future, we may enter into additional foreign currency-based hedging contracts to

17

reduce our exposure to significant fluctuations in currency exchange rates on the balance sheet, although there can be no assurances that we will do so. However, as our international operations grow, or if dramatic fluctuations in foreign currency exchange rates continue or increase or if our hedging strategies become ineffective, the effect of changes in the foreign currency exchange rates could become material to revenue, operating expenses, and income.

Our international sales and operations are subject to factors that could have an adverse effect on our results of operations.

We have significant sales and services operations outside the United States and derive a substantial portion of our revenues from these operations. We generated approximately 48% and 47% of our revenues from outside the United States in fiscal 2024 and fiscal 2023, respectively. International revenue increased 9% in fiscal 2024 compared to fiscal 2023. Expansion of our international operations will require a significant amount of attention from our management and substantial financial resources and might require us to add qualified management in these markets.

In addition to facing risks similar to the risks faced by our domestic operations, our international operations are also subject to risks related to the differing legal, political, social and regulatory requirements and economic conditions of many countries, including:

•adverse effects in economic conditions in the countries in which we operate related specifically to the wars in Israel and Ukraine, the COVID-19 pandemic and the governmental regulations put in place as a result of the virus, and the financial instability of banking institutions;

•difficulties in staffing and managing our international operations;

•foreign countries may impose additional withholding taxes or otherwise tax our foreign income, impose tariffs or adopt other restrictions on foreign trade or investment, including currency exchange controls;

•difficulties in coordinating the activities of our geographically dispersed and culturally diverse operations;

•general economic conditions in the countries in which we operate, including seasonal reductions in business activity in the summer months in Europe and in other periods in other countries, could have an adverse effect on our earnings from operations in those countries;

•imposition of, or unexpected adverse changes in, foreign laws or regulatory requirements may occur, including those pertaining to sanctions, export restrictions, privacy and data protection, trade and employment restrictions and intellectual property protections;

•longer payment cycles for sales in foreign countries and difficulties in collecting accounts receivable;

•competition from local suppliers;

•greater risk of a failure of our employees and partners to comply with both U.S. and foreign laws, including antitrust regulations, the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act of 2010, and any trade regulations ensuring fair trade practices;

•costs and delays associated with developing solutions in multiple languages; and

•political unrest, war or acts of terrorism.

Our business in emerging markets requires us to respond to rapid changes in market conditions in those markets. Our overall success in international markets depends, in part, upon our ability to succeed in differing legal, regulatory, economic, social and political conditions. We may not continue to succeed in developing and implementing policies and strategies that will be effective in each location where we do business. The occurrence of any of the foregoing factors may have a material adverse effect on our business and results of operations.

18

Risks Related to Technology and Security

We may be subject to IT system failures, network disruptions, cybersecurity incidents and breaches in data security.

IT system failures, network disruptions, cybersecurity incidents and breaches of data security could disrupt our operations by causing delays or cancellation of customer orders, impeding the delivery of our solutions, negatively affecting customer support or professional services, preventing the processing of transactions and reporting of financial results, and disturbing our enterprise resource planning system. IT system failures, network disruptions, cybersecurity incidents and breaches of data security could also result in the unintentional disclosure of customer or our information as well as damage our reputation. There can be no assurance that a system failure, network disruption, cybersecurity incident or data security breach will not have a material adverse effect on our financial condition and operating results. Cybersecurity breaches or incidents and other exploited security vulnerabilities could subject us to significant costs and third-party liabilities, result in improper disclosure of data and violations of applicable privacy and other laws, require us to change our business practices, cause us to incur significant remediation costs, lead to loss of customer confidence in, or decreased use of our products and services, damage our reputation, divert the attention of management from the operation of our business, result in significant compensation or contractual penalties from us to our customers and their business partners as a result of losses to or claims by them, or expose us to litigation, regulatory investigations, and significant fines and penalties.

Bad actors regularly attempt to gain unauthorized access to our IT systems, and many such attempts are increasingly sophisticated. These attempts, which might be related to industrial, corporate or other espionage, criminal hackers or state-sponsored intrusions, include trying to covertly introduce malware or ransomware to our environments and impersonating authorized users.