Commission file number

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

FORM

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EX- CHANGE ACT OF 1934 |

OR

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended |

OR

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to |

OR

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EX- CHANGE ACT OF 1934 |

Date of event requiring this shell company report .. . . . . . . . . . . . . . . . . . .

(Exact name of Registrant as specified in its charter and translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Chief Executive Officer

Telephone:

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol |

Name of each exchange on which registered | ||

| N/A | N/A | N/A |

Securities registered or to be registered pursuant to Section 12(g) of the Act: American Depositary Shares, each representing 600 Ordinary Shares.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. There were Ordinary Shares outstanding as of June 30, 2023.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes

☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | Accelerated filer ☐ | ||

| Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.”

☐ Yes

☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

☐ Yes ☒

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐ Yes ☒ No

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☐ |

International Accounting Standards Board ☒ |

Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

TABLE OF CONTENTS

| i |

| ii |

INTRODUCTION

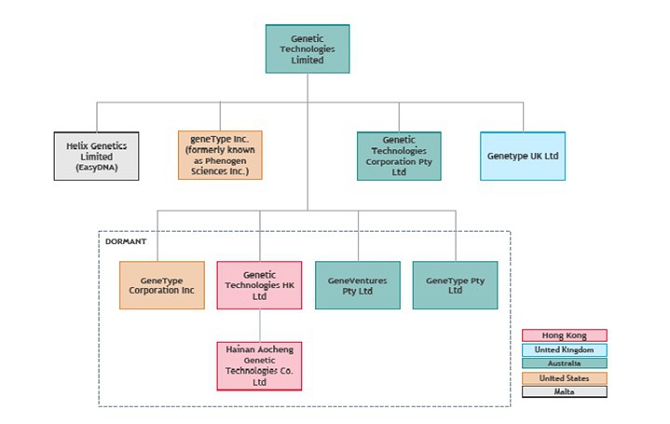

In this Annual Report, the “Company,” “Genetic Technologies”, “GTG”, “the Group”, “we,” “us” and “our” refer to Genetic Technologies Limited and its consolidated subsidiaries.

Our consolidated financial statements are set out beginning on page F-1 of this Annual Report (refer to Item 18 “Financial Statements”).

References to the “ADSs” are to our ADSs described in Item 12.D “American Depositary Shares” and references to the “Ordinary Shares” are to our Ordinary Shares described in Item 10.

Our fiscal year ends on June 30 and references in this Annual Report to any specific fiscal year are to the twelve-month period ended on June 30 of such year.

FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements that involve risks and uncertainties. We use words such as “anticipates”, “believes”, “plans”, “expects”, “future”, “intends” and similar expressions to identify such forward-looking statements. This Annual Report also contains forward-looking statements attributed to certain third parties relating to their estimates regarding the growth of Genetic Technologies and related markets and spending. You should not place undue reliance on these forward-looking statements, which apply only as of the date of this Annual Report. Our actual results could differ materially from those anticipated in these forward- looking statements for many reasons, including the risks faced by us described below under the caption “Risk Factors” and elsewhere in this Annual Report.

Although we believe that the expectations reflected in such forward-looking statements are reasonable at this time, we can give no assurance that such expectations will prove to be correct. Given these uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. Important factors that could cause actual results to differ materially from our expectations are contained in cautionary statements in this Annual Report including, without limitation, in conjunction with the forward-looking statements included in this Annual Report and specifically under Item 3.D “Risk Factors”.

All subsequent written and oral forward-looking statements attributable to us are expressly qualified in their entirety by reference to these cautionary statements.

AUSTRALIAN DISCLOSURE REQUIREMENTS

Our ordinary shares are primarily quoted on the Australian Securities Exchange (“ASX”) in addition to our listing of our ADSs on the NASDAQ Global Select Market. As part of our ASX listing, we are required to comply with various disclosure requirements as set out under the Australian Corporations Act 2001 and the ASX Listing Rules. Information furnished under the sub-heading “Australian Disclosure Requirements” is intended to comply with ASX listing and Corporations Act 2001 disclosure requirements and is not intended to fulfill information required by this Annual report on Form 20-F.

ENFORCEMENT OF LIABILITIES AND SERVICE OF PROCESS

We are incorporated under the laws of Western Australia in the Commonwealth of Australia. All of our directors and executive officers, and any experts named in this Annual Report, reside outside the U.S. Substantially all of our assets, our directors’ and executive officers’ assets and such experts’ assets are located outside the U.S. As a result, it may not be possible for investors to affect service of process within the U.S. upon us or our directors, executive officers or such experts, or to enforce against them or us in U.S. courts, judgments obtained in U.S. courts based upon the civil liability provisions of the federal securities laws of the U.S. In addition, we have been advised by our Australian solicitors that there is doubt that the courts of Australia will enforce against us, our directors, executive officers and experts named herein, judgments obtained in the U.S. based upon the civil liability provisions of the federal securities laws of the U.S. or will enter judgments in original actions brought in Australian courts based upon the federal securities laws of the U.S.

| iii |

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

Item 3.A Reserved

Item 3.B Capitalisation and Indebtedness

Not applicable.

Item 3.C Reasons for the Offer and Use of Proceeds

Not applicable.

Item 3.D Risk Factors

Before you purchase our ADSs, you should be aware that there are risks, including those described below. You should consider carefully these risk factors together with all of the other information contained elsewhere in this Annual Report before you decide to purchase our ADSs.

Risk Factor Summary

Risk Related to our Business

| ● | A variety of risks associated with commercializing our products and product candidates internationally could materially adversely affect our business. |

| ● | Our Company has a history of incurring losses. |

| ● | We may not be successful in transitioning from our existing product portfolio to our next generation of risk assessment tests, and our newly developed approach to marketing and distribution of such products may not generate revenues. |

| ● | Our products may never achieve significant market acceptance. |

| ● | We face additional risks as a result of the EasyDNA and AffinityDNA acquisitions and may be unable to integrate our businesses successfully and realize the anticipated synergies and related benefits of these acquisitions or do so within the anticipated time frame. |

| ● | Failure to demonstrate the clinical utility of our products could have a material adverse effect on our financial condition and results of operations. |

| ● | If our competitors develop superior products, our operations and financial condition could be affected. |

| ● | We have important relationships with external parties over whom we have limited control. |

| ● | We may be subject to liability and our insurance may not be sufficient to cover damages. |

| ● | Security breaches, privacy issues, loss of data and other incidents could compromise sensitive or personal information related to our business or prevent us from accessing critical information and expose us to liability, which could adversely affect our business and our reputation. |

| ● | We use potentially hazardous materials, chemicals and patient samples in our business and any disputes relating to improper handling, storage or disposal of these materials could be time consuming and costly. |

| ● | Our industry is subject to rapidly changing technology and new and increasing amounts of scientific data related to genes and genetic variants and their role in disease. |

| ● | We depend on the collaborative efforts of our academic and corporate partners for research, development and commercialization of our products. A breach by our partners of their obligations, or the termination of the relationship, could deprive us of valuable resources and require additional investment of time and money. |

| ● | If our sole laboratory facility becomes inoperable, we may be unable to perform our tests and our business will be harmed. |

| ● | The loss of key members of our senior management team or our inability to attract and retain highly skilled scientists, clinicians and salespeople could adversely affect our business. |

| 1 |

| ● | Changes in the way that the Food & Drug Administration (FDA) regulates our tests could result in the delay or additional expense in offering our tests and tests that we may develop in the future. |

| ● | Our business could be harmed from the loss or suspension of a license or imposition of a fine or penalties under, or future changes in, or changing interpretations of, Clinical Laboratory Improvements Amendments (CLIA) or state laboratory licensing laws to which we are subject. |

| ● | Failure to establish and comply with appropriate quality standards to assure that the highest level of quality is observed in the performance of our testing services and in the design, manufacture and marketing of our products could adversely affect the results of our operations and adversely impact our reputation. |

| ● | We could be adversely affected by violations of the Foreign Corrupt Practices Act (FCPA) and other worldwide anti-bribery laws. |

| ● | If we fail to maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results or prevent fraud. |

| ● | Failure to comply with health information privacy laws, including Health Insurance Portability and Accountability Act of 1996 (HIPAA) or other U.S. federal or state health information privacy and security laws, as applicable, may negatively impact our business. |

| ● | If we or our partners fail to comply with the complex federal, state, local and foreign laws and regulations to the extent that apply to our business, we could suffer severe consequences that could materially and adversely affect our operating results and financial condition. |

| ● | A failure to comply with any of federal or state laws to the extent such are applicable to our business, particularly laws related to the elimination of healthcare fraud, may adversely impact our business. |

| ● | We face risks associated with currency exchange rate fluctuations, which could adversely affect our operating results. |

| ● | Government regulation of genetic research or testing may adversely affect the demand for our services and impair our business and operations. |

| ● | Failure in our information technology systems could significantly increase testing turn-around times or impact on the billing processes or otherwise disrupt our operations. |

| ● | Any significant disruption in service on our website or in our computer or logistics systems, whether due to a failure with our information technology systems or that of a third-party vendor, could harm our reputation and may result in a loss of customers. |

| ● | Breaches of network or information technology, natural disasters or terrorist attacks could have an adverse impact on our business. |

| ● | Ethical and other concerns surrounding the use of genetic information may reduce the demand for our services. |

| ● | Risks associated with our intellectual property. |

| ● | We rely heavily upon patents and proprietary technology that may fail to protect our business. |

| ● | We may face difficulties in certain jurisdictions in protecting our intellectual property rights, which may diminish the value of our intellectual property rights in those jurisdictions. |

| ● | Our operations may be adversely affected by the effects of extreme weather conditions or other interruptions in the timely transportation of specimens. |

| ● | Our Consumer Initiated Testing (CIT) Platform will expose us to various risks. |

| ● | Discontinuation or recalls of existing testing products or our customers using new technologies to perform their own tests could adversely affect our business. |

| ● | The Polygenic Risk Score (PRS) test may not be able to obtain necessary regulatory clearance, and therefore we may not generate any revenue. |

| ● | If the PRS test is required to obtain and maintain FDA approvals, it will be subject to continuing governmental regulations and additional foreign regulations. |

| ● | Declining general economic or business conditions may have a negative impact on our business. |

Risk Related to our Securities

| ● | Our ADSs may be delisted from the NASDAQ Capital Market. |

| ● | Our stock price is volatile and can fluctuate significantly based on events not in our control and general industry conditions. As a result, the value of your investment may decline significantly. |

| ● | The fact that we do not expect to pay cash dividends may lead to decreased prices for our stock. |

| ● | You may have difficulty in effecting service of legal process and enforcing judgments against us and our management. |

| 2 |

| ● | Because we are not required to provide you with the same information as an issuer of securities based in the United States, you may not be afforded the same protection or information you would have if you had invested in a public corporation based in the United States. |

| ● | As a foreign private issuer, we are permitted to adopt certain home country practices in relation to corporate governance matters that differ significantly from Nasdaq corporate governance listing standards and these practices may afford less protection to shareholders than they would enjoy if we complied fully with Nasdaq corporate governance listing standards. |

| ● | As a result of being a U.S. public company, we are subject to additional regulatory compliance requirements, including Section 404, and if we fail to maintain an effective system of internal controls, we may not be able to accurately report our financial results or prevent fraud. |

| ● | We will incur significant costs as a result of operating as a company with ADSs that are publicly traded in the United States, and our management will be required to devote substantial time to new compliance initiatives. |

| ● | The dual listing of our ordinary shares and the ADSs may negatively impact the liquidity and value of the ADSs. |

| ● | Australian takeover laws may discourage takeover offers being made for us or may discourage the acquisition of a significant position in our ordinary shares or ADSs. |

| ● | Our Constitution and Australian laws and regulations applicable to us may adversely affect our ability to take actions that could be beneficial to our shareholders. |

| ● | A lack of significant liquidity for our ADSs may negatively affect your ability to resell our securities. |

| ● | In certain circumstances, holders of ADSs may have limited rights relative to holders of Ordinary Shares. |

Risk Related to Taxation

| ● | We may be classified as a passive foreign investment company, which could result in adverse U.S. federal income tax consequences for U.S. holders. |

| ● | If a United States person is treated as owning at least 10% of our ordinary shares, such holder may be subject to adverse U.S. federal income tax consequences. |

| ● | Changes to tax laws could materially adversely affect our company and reduce net returns to our shareholders. |

| ● | Tax authorities may disagree with our positions and conclusions regarding certain tax positions, resulting in unanticipated costs, taxes or non-realization of expected benefits. |

Risks Related to our Business

A variety of risks associated with commercializing our products and product candidates internationally could materially adversely affect our business.

We, or our licensing partners, may seek regulatory approval for our products or product candidates in multiple jurisdictions, accordingly, we expect that we will be subject to additional risks for our products and product candidates related to operating in foreign countries if we obtain the necessary approvals, including:

| ● | differing regulatory requirements in foreign countries; |

| ● | the potential for so-called parallel importing, when a local seller, faced with high or higher local prices, opts to import goods from a foreign market (with low or lower prices) rather than buying them locally; |

| ● | unexpected changes in tariffs, trade barriers, price and exchange controls and other regulatory requirements; |

| ● | economic weakness, including inflation, or political instability in particular foreign economies and markets; |

| ● | compliance with tax, employment, immigration and labor laws for employees living or traveling abroad; |

| ● | foreign taxes, including withholding of payroll taxes; |

| ● | foreign currency fluctuations, which could result in increased operating expenses and reduced revenues, and other obligations incident to doing business in another country; |

| ● | difficulties staffing and managing foreign operations; |

| ● | workforce uncertainty in countries where labor unrest is more common than in Australia or the U.S.; |

| ● | challenges enforcing our contractual and intellectual property rights, especially in those foreign countries that do not respect and protect intellectual property rights to the same extent as in Australia or the U.S.; |

| ● | production shortages resulting from any events affecting raw material supply or manufacturing capabilities abroad; and |

| ● | business interruptions resulting from geo-political actions, including war and terrorism. |

These and other risks associated with our or our licensing partners’ international operations may materially adversely affect our ability to attain or maintain profitable operations.

| 3 |

Our Company has a history of incurring losses.

We have incurred operating losses in every year since the year ended June 30, 2011. As at June 30, 2023, the Company had accumulated losses of A$156,715,687 and the extent of any future losses and whether or not the Company can generate profits in future years remains uncertain. The Company currently does not generate sufficient revenue to cover its operating expenses. We expect our capital outlays and operating expenditures to remain constant for the foreseeable future as we continue to focus on R&D and new product development, IP creation and the introduction of predictive genetic testing products. If we fail to generate sufficient revenue and eventually become profitable, or if we are unable to fund our continuing losses by raising additional financing when required, our shareholders could lose all or part of their investments.

We may not be successful in expanding our revenues, and therefore improving operational profitability, of the recently acquired EasyDNA and AffinityDNA businesses or achieve significant commercial sales of the portfolio to our next generation of geneType risk assessment tests.

Although GTG have recently achieved a significant increase in product revenues, which are largely attributable to the recently acquired EasyDNA and AffinityDNA businesses and the Company has recently developed, launched and marketed our geneType Multi- risk test, we believe that our future success is dependent upon our ability to grow revenues from our existing product offerings and to successfully introduce and sell our newly developed products including our innovative hereditary breast and ovarian cancer test, due for launch in financial year 2024. Although we believe that we now have world class products that are poised to be an important part of making predictive genetic testing a mainstream healthcare activity, we may not be successful in transitioning from our existing products to these products, and there can be no assurance that the demand for these new products will develop. Furthermore, we plan to introduce our new products to healthcare providers through a global network of distribution partners instead of through our own sales force. Although we believe that we are building worthwhile sales and distribution relationships with experienced distribution firms, there can be no assurance that we will be able to enter into distribution arrangements on terms satisfactory to us, and that our marketing strategy will be successful and result in significant revenues.

Our products may never achieve significant market acceptance.

We may expend substantial funds and management effort on the development and marketing of our predictive genetic testing products with no assurance that we will be successful in selling our products or services. Our ability to enter into distribution arrangements to successfully sell our molecular risk assessment and predictive genetic testing products and services will depend significantly on the perception that our products and services can reduce patient risk and improve medical outcomes, and that our products and services are superior to existing tests. Our business could also be adversely affected if we expend money without any return.

We face additional risks as a result of the EasyDNA and AffinityDNA acquisitions. We may be unable to integrate our businesses successfully and realize the anticipated synergies and related benefits of these acquisitions or do so within our anticipated timeframes. Including:

| ● | difficulties in integrating and managing the combined operations of EasyDNA and AffinityDNA, and realizing the anticipated economic, operational, and other benefits in a timely manner, which could result in substantial costs and delays or other operational, technical, or financial problems; |

| ● | disruptions to the EasyDNA and AffinityDNA businesses and their operations and relationships with service providers and other third parties; |

| ● | loss of key employees of EasyDNA and AffinityDNA and other challenges associated with integrating new employees into our culture, as well as reputational harm if integration is not successful; |

| ● | diversion of management time and focus from operating our business to addressing the EasyDNA and AffnityDNA operations integration challenges; |

| ● | diversion of significant resources from the ongoing development of our existing products, services, and operations; |

| ● | failure to successfully realize our intended business strategy; |

| ● | increase in the operating losses that we expect to incur in future periods; |

| ● | regulatory complexities of integrating or managing the combined operations or expanding into other industries or parts of the healthcare industry; |

| ● | regulatory developments or enforcement trends focusing on corporate practice of medicine; |

| ● | greater than anticipated costs related to the integration of the EasyDNA and AffinityDNA businesses and operations; |

| ● | increase in compliance and related costs associated with the addition of a regulated business; |

| 4 |

| ● | responsibility for the liabilities of EasyDNA and AffinityDNA, including those that were not disclosed to us or exceed our estimates, as well as, without limitation, liabilities arising out of their failure to maintain effective data protection and privacy practices controls and comply with applicable regulations; and |

| ● | potential accounting charges to the extent intangibles recorded in connection with the EasyDNA and AffinityDNA acquisitions, such as goodwill, trademarks, client relationships, or intellectual property, are later determined to be impaired and written down in value. |

Failure to demonstrate the clinical utility of our geneType products could have a material adverse effect on our financial condition and results of operations.

The Company believes that its current GeneType risk assessment tests, along with the pipeline of new tests for additional disease indications under development have the capacity to transform health outcomes for entire populations. However, it is critical for the Company to demonstrate the clinical utility of its new products at scale. Clinical utility is the usefulness of a test for clinical practice. If the Company is unable to demonstrate clinical utility, or if the data is deemed insufficient to validate utility, there may be insufficient demand for the Company’s products.

If our competitors develop superior products, our operations and financial condition could be affected.

We are currently subject to increased competition from biotechnology and diagnostic companies, academic and research institutions and government or other publicly-funded agencies that are pursuing products and services which are substantially similar to our molecular risk assessment testing products, or which otherwise address the needs of our customers and potential customers.

Our competitors in the predictive genetic testing and assessment market include private and public sector enterprises located in Australia, the U.S. and elsewhere. Many of the organizations competing with us are much larger and have more ready access to needed resources. In particular, they would have greater experience in the areas of finance, research and development, manufacturing, marketing, sales, distribution, technical and regulatory matters than we do. In addition, many of the larger current and potential competitors have already established name / brand recognition and more extensive collaborative relationships.

Our competitive position in the molecular risk assessment and predictive testing area is based upon, amongst other things, our ability to:

| ● | continue to strengthen and maintain scientific credibility through the process of obtaining scientific validation through clinical trials supported by peer-reviewed publication in medical journals; |

| ● | create and maintain scientifically advanced technology and offer proprietary products and services; |

| ● | continue to strengthen and improve the messaging regarding the importance and value that our cancer risk assessment tests provide to patients and physicians; |

| ● | diversify our product offerings in disease types; |

| ● | obtain and maintain patent or other protection for our products and services; |

| ● | obtain and maintain required government approvals and other accreditations on a timely basis; and |

| ● | successfully market our products and services. |

If we are not successful in meeting these goals, our business could be adversely affected. Similarly, our competitors may succeed in developing technologies, products or services that are more effective than any that we are developing or that would render our technology, products and services obsolete, noncompetitive or uneconomical.

We have important relationships with external parties over whom we have limited control.

We have relationships with academic consultants, research collaborators at other institutions and other advisers who are not employed by us. Accordingly, we have limited control over their activities and can expect only limited amounts of their time to be dedicated to our activities. These persons may have consulting, employment or advisory arrangements with other entities that may conflict with or compete with their obligations to us. Our consultants typically sign agreements that provide for confidentiality of our proprietary information and results of studies. However, we may not be able to maintain the confidentiality of our technology, the dissemination of which could hurt our competitive position and results of operations. To the extent that our scientific consultants, collaborators or advisors develop inventions or processes that may be applicable to our proposed products, disputes may arise as to the ownership of the proprietary rights to such information, and we may not be successful with any dispute outcomes.

| 5 |

We may be subject to liability and our insurance may not be sufficient to cover damages.

Our business exposes us to potential liability risks that are inherent in the testing, manufacturing, marketing and sale of molecular risk assessment and predictive tests. The use of our products and product candidates, whether for clinical trials or commercial sale, may expose us to professional and product liability claims and possible adverse publicity. We may be subject to claims resulting from incorrect results of analysis of genetic variations or other screening tests performed using our products. Litigation of such claims could be costly. Further, if a court were to require us to pay damages to a plaintiff, the amount of such damages could be significant and severely damage our financial condition. Although we have public and product liability insurance coverage under broad form liability and professional indemnity policies, the level or breadth of our coverage may not be adequate to fully cover any potential liability claims. In addition, we may not be able to obtain additional liability coverage in the future at an acceptable cost. A successful claim or series of claims brought against us in excess of our insurance coverage and the effect of professional and/or product liability litigation upon the reputation and marketability of our technology and products, together with the diversion of the attention of key personnel, could negatively affect our business.

Security breaches, privacy issues, loss of data and other incidents could compromise sensitive or personal information related to our business or prevent us from accessing critical information and expose us to liability, which could adversely affect our business and our reputation.

In the ordinary course of our business, we collect and store sensitive data, including Protected Health Information, (PHI), personally identifiable information, genetic information, credit card information, intellectual property and proprietary business information owned or controlled by ourselves or our customers, payers and other parties. We manage and maintain our applications and data utilizing a combination of on-site systems, managed data center systems and cloud-based systems. We also communicate PHI and other sensitive patient data through our various customer tools and platforms. In addition to storing and transmitting sensitive data that is subject to multiple legal protections, these applications and data encompass a wide variety of business-critical information including research and development information, commercial information, and business and financial information. We face a number of risks relative to protecting this critical information, including loss of access risk, inappropriate disclosure, inappropriate modification, and the risk of our being unable to adequately monitor and modify our controls over our critical information. Any technical problems that may arise in connection with our data and systems, including those that are hosted by third-party providers, could result in interruptions to our business and operations or exposure to security vulnerabilities. These types of problems may be caused by a variety of factors, including infrastructure changes, intentional or accidental human actions or omissions, software errors, malware, viruses, security attacks, fraud, spikes in customer usage and denial of service issues. In addition, there has recently been a significant increase in ransomware and cyber security attacks related to the ongoing conflict between Russia and Ukraine, which could result in substantial harm to internal systems necessary for running our critical operations and revenue generating services.

The secure processing, storage, maintenance and transmission of this critical information are vital to our operations and business strategy, and we devote significant resources to protecting such information. Although we take what we believe to be reasonable and appropriate measures, including a formal, dedicated enterprise security program, to protect sensitive information from various compromises (including unauthorized access, disclosure, or modification or lack of availability), our information technology and infrastructure may be vulnerable to attacks by hackers or viruses or breached due to employee error, malfeasance or other disruptions. For example, we have been subject to phishing incidents in the past, and we may experience additional incidents in the future. Any such breach or interruption could compromise our networks, and the information stored therein could be accessed by unauthorized parties, altered, publicly disclosed, lost or stolen.

Unauthorized access, loss or dissemination could also disrupt our operations (including our ability to conduct our analyses, provide test results, bill payers or patients, process claims and appeals, provide customer assistance, conduct research and development activities, collect, process and prepare company financial information, provide information about our tests and other patient and physician education and outreach efforts through our website, and manage the administrative aspects of our business) and damage our reputation, any of which could adversely affect our business.

In addition to data security risks, we also face privacy risks. Should we actually violate, or be perceived to have violated, any privacy commitments we make to patients or consumers, we could be subject to a complaint from an affected individual or interested privacy regulator, such as the FTC, a state Attorney General, an EU Member State Data Protection Authority, or a data protection authority in another international jurisdiction. This risk is heightened given the sensitivity of the data we collect.

Any security compromise that causes an apparent privacy violation could also result in legal claims or proceedings; liability under federal, state, foreign, or multinational laws that regulate the privacy, security, or breach of personal information, such as but not limited to the Health Insurance Portability and Accountability Act of 1996, or HIPAA, as amended by the Health Information Technology for Economic and Clinical Health Act of 2009, or HITECH, state data security and data breach notification laws, the European Union’s General Data Protection Regulation, or GDPR, and the UK Data Protection Act of 2018; and related regulatory penalties. Penalties for failure to comply with a requirement of HIPAA or HITECH vary significantly, and, depending on the knowledge and culpability of the HIPAA-regulated entity, may include civil monetary penalties of up to US$1.5 million per calendar year for each provision of HIPAA that is violated. A person who knowingly obtains or discloses individually identifiable health information in violation of HIPAA may face a criminal penalty of up to US$50,000 and up to one-year imprisonment. The criminal penalties increase if the wrongful conduct involves false pretenses or the intent to sell, transfer or use identifiable health information for commercial advantage, personal gain or malicious harm. Penalties for unfair or deceptive acts or practices under the FTC Act or state Unfair and Deceptive Acts and Practices, or UDAP, statutes may also vary significantly.

| 6 |

There has been unprecedented activity in the development of data protection regulation around the world. As a result, the interpretation and application of consumer, health-related and data protection laws in the United States, Europe and elsewhere are often uncertain, contradictory and in flux. The GDPR took effect on May 25, 2018. The GDPR applies to any entity established in the EU as well as extraterritorially to any entity outside the EU that offers goods or services to, or monitors the behavior of, individuals who are located in the EU. The GDPR imposes strict requirements on controllers and processors of personal data, including enhanced protections for “special categories” of personal data, which includes sensitive information such as health and genetic information of data subjects. The GDPR also grants individuals various rights in relation to their personal data, including the rights of access, rectification, objection to certain processing and deletion. The GDPR provides an individual with an express right to seek legal remedies if the individual believes his or her rights have been violated. Failure to comply with the requirements of the GDPR or the related national data protection laws of the member states of the EU, which may deviate from or be more restrictive than the GDPR, may result in significant administrative fines issued by EU regulators. Maximum penalties for violations of the GDPR are capped at 20M euros or 4% of an organization’s annual global revenue, whichever is greater.

Additionally, the implementation of GDPR has led other jurisdictions to either amend or propose legislation to amend their existing data privacy and cybersecurity laws to resemble the requirements of GDPR. For example, on June 28, 2018, California adopted the California Consumer Privacy Act of 2018, or the CCPA. The CCPA regulates how certain for-profit businesses that meet one or more CCPA applicability thresholds collect, use, and disclose the personal information of consumers who reside in California. Among other things, the CCPA confers to California consumers the right to receive notice of the categories of personal information that will be collected by a business, how the business will use and share the personal information, and the third parties who will receive the personal information. The CCPA also confers rights to access, delete, or transfer personal information; and the right to receive equal service and pricing from a business after exercising a consumer right granted by the CCPA. In addition, the CCPA allows California consumers the right to opt out of the “sale” of their personal information, which the CCPA defines broadly as any disclosure of personal information to a third party in exchange for monetary or other valuable consideration. The CCPA also requires a business to implement reasonable security procedures to safeguard personal information against unauthorized access, use, or disclosure. The CCPA does not apply to PHI collected by certain parties subject to HIPAA, or to de-identified data as defined under HIPAA. The CCPA provides for civil penalties for violations, as well as a private right of action for certain data breaches resulting from a business’s failure to implement and maintain reasonable data security procedures that is expected to increase data breach litigation. On January 1, 2023, the California Privacy Rights Act, or CPRA, is scheduled to go into effect and will substantially amend the CCPA. The CPRA would, among other things, amend the CCPA to give California residents the ability to limit the use of their sensitive information, provide for penalties for CPRA violations concerning California residents under the age of 16, and establish a new California Privacy Protection Agency to implement and enforce the law.

Virginia, Colorado, and Utah have recently enacted similar privacy acts, and dozens of other states in the United States are currently considering similar consumer data privacy laws, which could impact our operations if enacted. Some observers have noted that the CCPA could mark the beginning of a trend toward more stringent privacy legislation in the United States, which could increase our potential liability and adversely affect our business, results of operations, and financial condition.

It is possible the GDPR, CCPA and other emerging United States and international data protection laws may be interpreted and applied in a manner that is inconsistent with our practices. If so, this could result in government-imposed fines or orders requiring that we change our practices, which could adversely affect our business. In addition, these privacy laws and regulations may differ from country to country and state to state, and our obligations under these laws and regulations vary based on the nature of our activities in the particular jurisdiction, such as whether we collect samples from individuals in the local jurisdiction, perform testing in the local jurisdiction, or process personal information regarding employees or other individuals in the local jurisdiction. Complying with these various laws and regulations could cause us to incur substantial costs or require us to change our business practices and compliance procedures in a manner adverse to our business. We can provide no assurance that we are or will remain in compliance with diverse privacy and data security requirements in all of the jurisdictions in which we do business. Failure to comply with privacy and data security requirements could result in a variety of consequences, including civil or criminal penalties, litigation, or damage to our reputation, any of which could have a material adverse effect on our business.

| 7 |

We use potentially hazardous materials, chemicals and patient samples in our business and any disputes relating to improper handling, storage or disposal of these materials could be time consuming and costly.

Our research and development, production and service activities involve the controlled use of hazardous laboratory materials and chemicals, including small quantities of acid and alcohol, and fluid (i.e. saliva, blood) as well as tissue samples from customers. We do not knowingly deal with infectious samples. We, our collaborators and service providers are subject to stringent Australian federal, state and local laws and regulations governing occupational health and safety standards, including those governing the use, storage, handling and disposal of these materials and certain waste products. However, we could be liable for accidental contamination or discharge or any resultant injury from hazardous materials, and conveyance, processing, and storage of and data on patient samples. If we, our collaborators or service providers fail to comply with applicable laws or regulations, we could be required to pay penalties or be held liable for any damages that result and this liability could exceed our financial resources. Further, future changes to environmental health and safety laws could cause us to incur additional expense or restrict our operations.

In addition, our collaborators and service providers may be working with these same types of hazardous materials, including hazardous chemicals, in connection with our collaborations. In the event of a lawsuit or investigation, we could be held responsible for any injury caused to persons or property by exposure to, or release of, these hazardous materials or customer samples that may contain infectious materials. The cost of this liability could exceed our resources. While we maintain broad form liability insurance coverage for these risks, the level or breadth of our coverage may not be adequate to fully cover potential liability claims.

Our industry is subject to rapidly changing technology and new and increasing amounts of scientific data related to genes and genetic variants and their role in disease.

Our failure to develop tests to keep pace with these changes could make us obsolete. In recent years, there have been numerous advances in methods used to analyze very large amounts of genomic information and the role of genetics and gene variants in disease and treatment therapies. Our industry has and will continue to be characterized by rapid technological change, increasingly larger amounts of data, frequent new testing service introductions and evolving industry standards, all of which could make our tests obsolete. Our future success will also depend on our ability to keep pace with the evolving needs of our customers on a timely and cost-effective basis and to pursue new market opportunities that develop as a result of technological and scientific advances. Our tests could become obsolete and our business adversely affected unless we continually update our offerings to reflect new scientific knowledge about genes and genetic variations and their role in diseases and treatment therapies.

We depend on the collaborative efforts of our academic and corporate partners for research, development and commercialization of our products. A breach by our partners of their obligations, or the termination of the relationship, could deprive us of valuable resources and require additional investment of time and money.

Our strategy for research, development and commercialization of our products has historically involved entering into various arrangements with academic, corporate partners and others. As a result, the success of our strategy depends, in part, upon the strength of those relationships and these outside parties undertaking their responsibilities and performing their tasks to the best of their ability and responding in a timely manner. Our collaborators may also be our competitors. We cannot necessarily control the amount and timing of resources that our collaborators devote to performing their contractual obligations and we have no certainty that these parties will perform their obligations as expected or that any revenue will be derived from these arrangements.

If our collaborators breach or terminate their agreement with us or otherwise fail to conduct their collaborative activities in a timely manner, the development or commercialization of the product candidate or research program under such collaborative arrangement may be delayed. If that is the case, we may be required to undertake unforeseen additional responsibilities or to devote unforeseen additional funds or other resources to such development or commercialization, or such development or commercialization could be terminated. The termination or cancellation of collaborative arrangements could adversely affect our financial condition, intellectual property position and general operations. In addition, disagreements between collaborators and us could lead to delays in the collaborative research, development, or commercialization of certain products or could require or result in formal legal process or arbitration for resolution. These consequences could be time-consuming and expensive and could have material adverse effects on the Company.

We rely upon scientific, technical and clinical data supplied by academic and corporate collaborators, licensors, licensees, independent contractors and others in the evaluation and development of potential therapeutic methods. There may be errors or omissions in this data that would materially adversely affect the development of these methods.

If our sole laboratory facility becomes inoperable, we may be unable to perform our tests and our business will be harmed.

We rely heavily upon our sole laboratory facilities in Melbourne, Australia, which has been certified under the U.S. CLIA. Our current lease of laboratory premises expires February 28, 2025. The facility and the equipment we use to perform our tests would be costly to replace and could require substantial lead time to repair or replace. If we were to lose our CLIA certification or other required certifications or licenses, or if the facility is harmed or rendered inoperable by natural or man-made disasters, including flooding and power outages, it will be difficult or impossible for us to perform our tests for some period of time. The inability to perform our tests or the backlog of tests that could develop if our facility is inoperable for even a short period of time may result in the loss of customers or harm our reputation, and we may be unable to regain those customers in the future.

| 8 |

If we no longer had our own facility and needed to rely on a third party to perform our tests, we could only use another facility with established state licensure and CLIA accreditation. We cannot assure you that we would be able to find another CLIA certified facility willing to comply with the required procedures, that this laboratory would be willing to perform the tests on commercially reasonable terms, or that it would be able to meet our quality standards. In order to establish a redundant clinical reference laboratory facility, we would have to spend considerable time and money securing adequate space, constructing the facility, recruiting and training employees, and establishing the additional operational and administrative infrastructure necessary to support a second facility. We may not be able, or it may take considerable time, to replicate our testing processes or results in a new facility. Additionally, any new clinical reference laboratory facility would be subject to certification under CLIA and licensing by several states, including California and New York, which could take a significant amount of time and result in delays in our ability to begin operations.

The loss of key members of our senior management team or our inability to attract and retain highly skilled scientists, clinicians and salespeople could adversely affect our business.

Our success depends largely on the skills, experience and performance of key members of our executive management team and others in key management positions. The efforts of each of these persons together will be critical as we continue to develop our technologies and testing processes, continue our international expansion and transition to a company with multiple commercialized products. If we were to lose one or more of these key employees, we may experience difficulties in competing effectively, developing our technologies and implementing our business strategies.

Our research and development programs and commercial laboratory operations depend on our ability to attract and retain highly skilled scientists and technicians, including licensed laboratory technicians, chemists, biostatisticians and engineers. We may not be able to attract or retain qualified scientists and technicians in the future due to the competition for qualified personnel among life science businesses. In addition, if there were to be a shortage of clinical laboratory scientists in coming years, this would make it more difficult to hire sufficient numbers of qualified personnel. We also face competition from universities and public and private research institutions in recruiting and retaining highly qualified scientific personnel. Our success also depends on our ability to attract and retain salespeople with extensive experience in oncology and have close relationships with medical oncologists, pathologists and other hospital personnel. We may have difficulties sourcing, recruiting or retaining qualified salespeople, which could cause delays or a decline in the rate of adoption of our tests. If we are not able to attract and retain the necessary personnel to accomplish our business objectives, we may experience constraints that could adversely affect our ability to support our research and development and sales programs.

Changes in the way that the FDA regulates our tests could result in the delay or additional expense in offering our tests and tests that we may develop in the future.

Historically, the U.S. Food and Drug Administration (“FDA”) has exercised enforcement discretion with respect to most Laboratory Developed Tests (“LDTs”) and has not required laboratories that furnish LDTs to comply with the agency’s requirements for medical devices (e.g., establishment registration, device listing, quality systems regulations, premarket clearance or premarket approval, and post-market controls). In recent years, however, the FDA publicly announced its intention to regulate certain LDTs and issued two draft guidance documents that set forth a proposed phased-in risk-based regulatory framework that would apply varying levels of FDA oversight to LDTs. However, these guidance documents were withdrawn at the end of the Obama administration and replaced by an informal discussion paper reflecting some of the feedback that FDA had received on LDT regulation. The FDA acknowledged that the discussion paper in January 2017 does not represent the formal position of the FDA and is not enforceable. Nevertheless, the FDA wanted to share its synthesis of the feedback that it had received in the hope that it might advance public discussion on future LDT oversight. Notwithstanding the discussion paper, the FDA continues to exercise enforcement discretion and may decide to regulate certain LDTs on a case-by-case basis at any time, which could result in delay or additional expense in offering our tests and tests that we may develop in the future.

As a matter of policy, the FDA generally does not review Direct-to-Consumer LDTs that are created and performed in a single laboratory, if they are offered to patients only when prescribed by a health care provider.

Legislative proposals addressing the FDA’s oversight of LDTs have been introduced in the current and previous Congresses, and we expect that new legislative proposals will be introduced from time-to-time. On May 17, 2022, the Senate Health, Education, Labor and Pensions (HELP) Committee released an FDA user fees reauthorization legislative package, which incorporates contents from the Verifying Accurate Leading-edge IVCT Development (VALID) Act that would establish a new category of in vitro clinical tests (IVCTs) comprised of traditional in vitro diagnostics and LDTs, and grant the FDA authority to review and approve them pre-market. Such arrangement increased the likelihood for Congress to pass a legislation that will give the FDA clear authority to regulate LDTs, but the eventual result is difficult to predict at this time.

If the FDA ultimately regulates certain LDTs, whether via final guidance, final regulation, or as instructed by Congress, our tests may be subject to certain additional regulatory requirements. Complying with the FDA’s requirements can be expensive, time-consuming, and subject us to significant or unanticipated delays. Insofar as we may be required to obtain premarket clearance or approval to perform or continue performing an LDT, we cannot assure you that we will be able to obtain such authorization. Even if we obtain regulatory clearance or approval where required, such authorization may not be for the intended uses that we believe are commercially attractive or are critical to the commercial success of our tests. As a result, the application of the FDA’s requirements to our tests could materially and adversely affect our business, financial condition, and results of operations.

| 9 |

Our business could be harmed from the loss or suspension of a license or imposition of a fine or penalties under, or future changes in, or changing interpretations of, CLIA or state laboratory licensing laws to which we are subject.

The clinical laboratory testing industry is subject to extensive federal and state regulation. The regulations implementing CLIA set out federal regulatory standards that apply to virtually all clinical laboratories operating in the U.S. (regardless of the location, size or type of laboratory), including those operated by physicians in their offices, by requiring that they be certified by the federal government or by a federally approved accreditation agency. CLIA is a U.S. federal law regulating clinical laboratories that perform testing on specimens derived from humans for the purpose of providing information for the diagnosis, prevention or treatment of disease. CLIA is intended to ensure the quality and reliability of clinical laboratories in the U.S. by mandating specific standards in the areas of personnel qualifications, administration, and participation in proficiency testing, patient test management, quality control, quality assurance and inspections.

Certain US States also require state laboratory licenses in order to test specimens received from patients residing in those states or requests received from ordering physicians in those states. We currently hold out-of-state laboratory licenses in California, New York, Maryland, Rhode Island, and Pennsylvania.

Further, CLIA does not pre-empt state law, which in some cases may be more stringent than federal law and require additional personnel qualifications, quality control, record maintenance and proficiency testing. The sanction for failure to comply with CLIA and state requirements may be suspension, revocation or limitation of a laboratory’s CLIA certificate, which is necessary to conduct business, as well as significant fines, civil and criminal penalties, the imposition of directed plan of correction, and on-site monitoring. If we were to be found out of compliance with CLIA program requirements and subjected to sanctions, our business and reputation could be harmed. Several states have similar laws, and we may be subject to similar penalties. If the CLIA certification of one laboratory owned by the Company is suspended or revoked that may preclude the Company from owning or operating any other CLIA regulated laboratory for two years. Further, even if it were possible for us to bring our laboratory back into compliance, we could incur significant expenses and potentially lose revenue in doing so.

We cannot assure you that applicable statutes and regulations will not be interpreted or applied by a prosecutorial, regulatory or judicial authority in a manner that would adversely affect our business. Potential sanctions for violation of these statutes and regulations include significant fines and the suspension or loss of various licenses, certificates and authorizations, which could have a material adverse effect on our business. In addition, compliance with future legislation could impose additional requirements on us, which may be costly.

Failure to establish and comply with appropriate quality standards to assure that the highest level of quality is observed in the performance of our testing services and in the design, manufacture and marketing of our products could adversely affect the results of our operations and adversely impact our reputation.

The provision of clinical testing services, and the design, manufacture and marketing of diagnostic products involve certain inherent risks. The services that we provide and the products that we design, manufacture and market are intended to provide information for healthcare providers in providing patient care. Therefore, users of our services and products may have a greater sensitivity to errors than the users of services or products that are intended for other purposes. Similarly, negligence in performing our services can lead to injury or other adverse events. We may be sued under common law, physician liability or other liability law for acts or omissions by our laboratory personnel. We are subject to the attendant risk of substantial damages awards and risk to our reputation.

We could be adversely affected by violations of the FCPA and other worldwide anti-bribery laws.

We are subject to the FCPA, which prohibits companies and their intermediaries from making payments in violation of law to non-U.S. government officials for the purpose of obtaining or retaining business or securing any other improper advantage. We are increasing our direct sales and operations personnel outside the United States, in which we have limited experience. We use a limited number of independent distributors to sell our tests internationally, which requires a high degree of vigilance in maintaining our policy against participation in corrupt activity, because these distributors could be deemed to be our agents, and we could be held responsible for their actions. Other U.S. companies in the medical device and pharmaceutical fields have faced criminal penalties under the FCPA for allowing their agents to deviate from appropriate practices in doing business with these individuals. We are also subject to similar anti- bribery laws in the jurisdictions in which we operate, including anti-bribery laws in Australia which also prohibits commercial bribery and makes it a crime for companies to fail to prevent bribery. These laws are complex and far-reaching in nature, and, as a result, we cannot assure you that we would not be required in the future to alter one or more of our practices to be in compliance with these laws or any changes in these laws or the interpretation thereof. Any violations of these laws, or allegations of such violations, could disrupt our operations, involve significant management distraction, involve significant costs and expenses, including legal fees, and could result in a material adverse effect on our business, prospects, financial condition or results of operations. We could also incur severe penalties, including criminal and civil penalties, disgorgement and other remedial measures.

| 10 |

If we fail to maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results or prevent fraud.

Effective internal controls over financial reporting are necessary for us to provide reliable financial reports and, together with adequate disclosure controls and procedures, are designed to prevent fraud. Any failure to design and implement an effective system of internal control may reveal deficiencies in our internal controls over financial reporting that are deemed to be material weaknesses. Ineffective internal controls could also cause investors to lose confidence in our reported financial information, which could have a negative effect on the trading price of the ADSs and our Ordinary Shares.

As of June 30, 2020, we had identified a material weakness in our internal control over financial reporting in relation to segregation of duties. Such material weakness was remedied as of June 30, 2021.

As of June 30, 2023, our Chief Executive Officer and Chief Financial Officer assessed the effectiveness of our internal control over financial reporting. We did not identify any material weakness in our internal control over financial reporting during the year. However, we cannot assure you that the measures we have taken to date, and actions we may take in the future, will be sufficient to prevent potential future material weaknesses.

Failure to comply with health information privacy laws, including HIPAA or other U.S. federal or state health information privacy and security laws, as applicable, may negatively impact our business.

Pursuant to the Health Insurance Portability and Accountability Act of 1996, or HIPAA, as amended by the Health Information Technology for Economic and Clinical Health Act of 2009, or HITECH, covered entities (including health plans, healthcare clearinghouses, and certain healthcare providers), as well as their respective “business associates” that create, receive, maintain or transmit individually identifiable health information for or on behalf of a covered entity, with respect to safeguarding the privacy, security and transmission of individually identifiable health information. Individuals and entities who are subject to HIPAA must comply with comprehensive privacy and security standards with respect to the use and disclosure of protected health information, as well as standards for electronic transactions, including specified transaction and code set rules. Under HITECH, HIPAA was expanded, including requirements to provide notification of certain identified data breaches, direct patient access to laboratory records, the extension of certain HIPAA privacy and security standards directly to business associates, and heightened penalties for noncompliance, and enforcement efforts. Failure to comply with HIPAA or other U.S. federal and state health information privacy and security laws, as applicable, could result in significant penalties

If we or our partners fail to comply with the complex federal, state, local and foreign laws and regulations to the extent that apply to our business, we could suffer severe consequences that could materially and adversely affect our operating results and financial condition.

Our operations are subject to extensive federal, state, local and foreign laws and regulations, all of which are subject to change. The U.S. laws and regulations that may apply to our business include, among other things:

| ● | CLIA, which requires that laboratories obtain certification from the federal government, and state licensure laws; |

| ● | FDA laws and regulations; |

| ● | HIPAA, which imposes comprehensive federal standards with respect to the privacy and security of protected health information and requirements for the use of certain standardized electronic transactions; amendments to HIPAA under HITECH, which strengthen and expand HIPAA privacy and security compliance requirements, increase penalties for violators, extend enforcement authority to state attorneys general and impose requirements for breach notification; |

| ● | state laws regulating genetic testing and protecting the privacy of genetic test results, as well as state laws protecting the privacy and security of health information and personal data and mandating reporting of breaches to affected individuals and state regulators; |

| ● | federal and state fraud and abuse laws, such as false claims and anti-kickback laws, and prohibitions on self-referral; |

| ● | Section 216 of the federal Protecting Access to Medicare Act of 2014 (“PAMA”), which requires applicable laboratories to report private payer data in a timely and accurate manner; |

| ● | state laws that impose reporting and other compliance-related requirements; and |

| ● | similar foreign laws and regulations that apply to us in the countries in which we operate. |

These laws and regulations are complex and are subject to interpretation by the courts and by government agencies. Our failure to comply could lead to significant administrative civil or criminal penalties, exclusion from participation in state and federal health care programs, imprisonment, disgorgement, and prohibitions or restrictions on our laboratory’s ability to provide or receive payment for our services. We believe that we are in material compliance with all statutory and regulatory requirements that apply to us, but there is a risk that one or more government agencies could take a contrary position, or that a private, party could file suit under the qui tam provisions of the federal False Claims Act or a similar state law. Such occurrences, regardless of their outcome, could damage our reputation and adversely affect important business relationships with third parties, including managed care organizations, and other private third-party payers.

| 11 |

A failure to comply with any of federal or state laws to the extent such are applicable to our business, particularly laws related to the elimination of healthcare fraud, may adversely impact our business.

The healthcare industry is subject to changing political, economic, and regulatory influences that may affect our business. During the past several years, the healthcare industry has been subject to an increase in governmental regulation and subject to potential disruption due to legislative initiatives and government regulation, as well as judicial interpretations thereof. While these regulations may not directly impact us or our offerings in every instance, they will affect the healthcare industry as a whole and may impact patient use of our services. We currently accept payments only from our customers not any third-party payers, such as government healthcare programs or health insurers. Because of this approach, we are not subject to many of the laws and regulations that impact many other participants in the healthcare industry.

If the government asserts broader regulatory control over companies like ours or if we determine that we will change our business model and accept payment from and/or participate in third-party payer programs, the complexity of our operations and our compliance obligations will materially increase. Failure to comply with any applicable federal, state, and local laws and regulations could have a material adverse effect on our business, financial condition, and results of operations.

While we seek to conduct our business in compliance with all applicable healthcare laws and regulations, regulatory or law enforcement authorities may not agree with our interpretation of these laws and regulations and may seek to enforce legal remedies or penalties against us for violations. Any action brought against us for violation of these or other laws or regulations, even if we successfully defend against it, could cause us to incur significant legal expenses and divert our management’s attention from the operation of our business. If our operations are found to be in violation of any of the federal, state, fraud and abuse or other healthcare laws and regulations that apply to us, we may be subject to penalties, including significant criminal, civil, and administrative penalties, damages and fines, disgorgement, additional reporting requirements and oversight, and imprisonment for individuals, as well as contractual damages and reputational harm. We could also be required to curtail or cease our operations. Any of the foregoing consequences could seriously harm our business and our financial results. From time to time we may need to change our operations, particularly pricing or billing practices, in response to changing interpretations of these laws and regulations or regulatory or judicial determinations with respect to these laws and regulations. These occurrences, regardless of their outcome, could damage our reputation and harm important business relationships that we have with healthcare providers, payers and others.

We face risks associated with currency exchange rate fluctuations, which could adversely affect our operating results.

We receive a portion of our revenues and pay a portion of our expenses in currencies other than the Australian dollar, such as the U.S. dollar, the Euro and the British pound. As a result, we are at risk for exchange rate fluctuations between such foreign currencies and the Australian dollar, which could affect the results of our operations. If the Australian dollar strengthens against foreign currencies, the translation of these foreign currency denominated transactions will result in decreased revenues and operating expenses. We may not be able to offset adverse foreign currency impact with increased revenues. Other than holding foreign currency bank accounts in which revenues from foreign currency denominated sales are held, offering a natural hedge against some foreign currency expenditures, we do not currently utilize other hedging strategies to mitigate foreign currency risk. Even if we were to implement hedging strategies to mitigate foreign currency risk, these strategies might not eliminate our total exposure to foreign exchange rate fluctuations and would involve costs and risks of their own, such as ongoing management time and expertise, external costs to implement the strategies and potential accounting implications.

Government regulation of genetic research or testing may adversely affect the demand for our services and impair our business and operations.

In addition to the regulatory framework governing healthcare, genetic research and testing has been the focus of public attention and regulatory scrutiny. From time to time, federal, state and/or local governments adopt regulations relating to the conduct of genetic research and genetic testing. In the future, these regulations could limit or restrict genetic research activities as well as genetic testing for research or clinical purposes. In addition, if such regulations are adopted, these regulations may be inconsistent with, or in conflict with, regulations adopted by other government bodies. Regulations relating to genetic research activities could adversely affect our ability to conduct our research and development activities. Regulations restricting genetic testing could adversely affect our ability to market and sell our products and services. Accordingly, any regulations of this nature could increase the costs of our operations or restrict our ability to conduct our testing business.

| 12 |

Failure in our information technology systems could significantly increase testing turn-around times or impact on the billing processes or otherwise disrupt our operations.

Our laboratory operations depend, in part, on the continued performance of our information technology systems. Our information technology systems are potentially vulnerable to physical or electronic break-ins, computer viruses and similar disruptions. Sustained system failures or interruption of our systems in our laboratory operations could disrupt our ability to process laboratory requisitions, perform testing, and provide test results in a timely manner and/or billing process. Failure of our information technology systems could adversely affect our business and financial condition.

Any significant disruption in service on our website or in our computer or logistics systems, whether due to a failure with our information technology systems or that of a third-party vendor, could harm our reputation and may result in a loss of customers.

Customers purchase and access our services through our websites. Our reputation and ability to attract, retain and serve our customers, patients, and members is dependent upon the reliable performance of our website, network infrastructure and content delivery processes. Interruptions in any of these systems, whether due to system failures, computer viruses or physical or electronic break-ins, could affect the security or availability of our website, including our databases, and prevent our customers, patients, and members from accessing and using our services.