CONFIDENTIAL TREATMENT

OFFICE LEASE

RODICK EQUITIES INC.

(Landlord)

- and -

FLUIDIGM CANADA INC.

(Tenant)

- and -

FLUIDIGM CORPORATION

(Indemnifier)

SUITES 400 AND 401

ON THE FOURTH FLOOR OF THE OFFICE COMPONENT

AND A PORTION OF THE WAREHOUSE COMPONENT

1380 RODICK ROAD

MARKHAM, ONTARIO

Rentable Area: approximately 41,145 square feet

Date: August 17, 2015

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

I N D E X

ARTICLE I ‑ FUNDAMENTAL PROVISIONS

1.1 Landlord 5

1.2 Tenant 5

1.3 Building 5

1.4 Premises 5

1.5 Term 5

1.6 Basic Rent 6

1.7 Additional Rent 7

1.8 Deposit 7

1.9 Rent Commencement Date 7

1.10 Indemnifier 7

1.11 Fundamental Provisions 7

ARTICLE II ‑ PREMISES

2.1 Lease 8

2.2 Use: 8

2.3 Rules and Regulations: 8

2.4 Observance of Law: 9

2.5 No Waste or Nuisance: 9

2.6 Common Areas: 9

2.7 Easements: 10

2.8 Covenants of Landlord and Tenant: 10

ARTICLE III ‑ TERM ‑ POSSESSION

3.1 Term: 10

3.2 Tenant Fixturing: 10

3.3 Delay in Possession: 11

3.4 Surrender: 11

3.5 Overholding: 11

3.6 Effect of Termination: 11

3.7 Acceptance of Premises: 11

3.8 Demolition: Intentionally Deleted 11

3.9 Relocation: Intentionally Deleted 11

ARTICLE IV ‑ RENT

4.1 Payment: 12

4.2 Basic Rent: 12

4.3 Deposit: 12

4.4 Proportionate Share of Realty Taxes and Operating Costs: 13

4.5 Utilities ‑ Light Fixtures: 14

4.6 Additional Services: 14

4.7 General Provisions: 15

1

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

ARTICLE V ‑ TAXES

5.1 Taxes Payable by the Landlord: 15

5.2 Business and Other Taxes Payable by the Tenant: 16

5.3 Contesting Taxes: 16

5.4 Alternate Methods of Taxation: 16

ARTICLE VI ‑ MAINTENANCE, REPAIRS AND ALTERATIONS

6.1 General Statement: 16

6.2 Responsibility of Tenant: 16

6.3 Tenant Not Responsible: 17

6.4 Responsibility of Landlord: 17

6.5 Inspection, Entry and Notice: 17

6.6 Notify the Landlord: 18

6.7 Alterations or Improvements: 18

6.8 Removal and Restoration: 20

6.9 External Changes: 21

6.10 Trade Fixtures: 21

6.11 Tenant's Signs: 22

6.12 Directory Board: 23

6.13 Landlord's Signs: 23

6.14 Environmental Provisions: 23

6.15 Landlord's Alterations: 29

ARTICLE VII ‑ STANDARD SERVICES

7.1 Heating and Air‑Conditioning: 29

7.2 Cleaning: 30

7.3 Elevators: 31

7.4 Security and Information: 31

7.5 Utilities: 31

7.6 Interruption or Delay of Services: 31

7.7 Public Policy: 32

ARTICLE VIII ‑ ASSIGNMENT AND SUBLETTING

8.1 Assignment, Subletting: 32

8.2 Landlord's Consent: 33

8.3 Requests for Consent: 33

8.4 Assignment by Landlord: 34

8.5 Liability of Tenant after Transfers: 34

ARTICLE IX ‑ INSURANCE AND INDEMNIFICATION

9.1 Tenant's Insurance: 34

9.2 Policy Requirements: 35

9.3 Proof of Insurance: 36

9.4 Failure to Maintain: 36

9.5 Damage to Leasehold Improvements: 36

9.6 Increase in Insurance Premiums/Cancellation: 36

2

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

9.7 Landlord's Insurance: 37

9.8 Non‑Liability for Loss, Injury or Damage: 37

9.9 Indemnification of the Landlord: 37

9.10 Extension of Rights and Remedies: 38

ARTICLE X ‑ DAMAGE

10.1 Damage to Premises: 38

10.2 Damage to the Building: 39

10.3 Architect's Certificate: 40

ARTICLE XI ‑ UNAVOIDABLE DELAY

11.1 Unavoidable Delay: 41

ARTICLE XII ‑ LANDLORD'S REMEDIES

12.1 Landlord May Perform Tenant's Covenants: 41

12.2 Re‑Entry: 41

12.3 Right to Distrain: 45

12.4 Landlord May Follow Chattels: 45

12.5 Rights Cumulative: 45

12.6 Acceptance of Rent Non‑Waiver: 45

ARTICLE XIII ‑ STATUS STATEMENT, ATTORNMENT AND SUBORDINATION

13.1 Certification: 44

13.2 Attornment: 44

13.3 Subordination: 44

13.4 Rights of Mortgagees: 45

ARTICLE XIV ‑ MISCELLANEOUS

14.1 Joint and Several Liability: 45

14.2 Landlord and Tenant Relationship: 45

14.3 Planning Act: 45

14.4 No Waiver: 45

14.5 Expropriation: 46

14.6 Notice: 46

14.7 Net Lease: 47

14.8 Non Merger: 47

14.9 Lease Entire Agreement: 48

14.10 Registration: 48

14.11 Name of Building: 48

14.12 Governing Law: 48

14.13 Survival of Tenant's Covenants: 48

14.14 Quiet Enjoyment: 48

14.15 Binding on Successors: 49

14.16 Limitation on Use: 49

3

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

14.17 Corporate Ownership: 49

14.18 Assignment and Subletting: 49

14.19 Several Liability: 49

14.20 Time of the Essence: 49

14.21 Counterparts: 49

ARTICLE XV ‑ DEFINITIONS ‑ INTERPRETATION

15.1 Definitions: 50

15.2 Interpretation: 59

SCHEDULE "A" - LEGAL DESCRIPTION

SCHEDULE "B" - FLOOR PLAN OF THE OFFICE PREMISES

SCHEDULE "B-1" - FLOOR PLAN OF THE WAREHOUSE PREMISES

SCHEDULE "C" - LANDLORD’S & TENANT’S WORK

SCHEDULE "C1"- DEMOLITION PLANS

SCHEDULE "D" - RULES AND REGULATIONS

SCHEDULE "E" - SPECIAL PROVISIONS

SCHEDULE "F" - FLOOR PLAN SHOWING THE FOURTH FLOOR ROFO SPACE

SCHEDULE "G"- FLOOR PLAN SHOWING WAREHOUSE ROFO SPACE

SCHEDULE "H" - CONTAMINANTS LIST

SCHEDULE "I" - INDEMNITY AGREEMENT

4

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

THIS LEASE is made the 17th day of August, 2015

between the Landlord, Tenant and Indemnifier, if any, listed below.

ARTICLE I ‑ FUNDAMENTAL PROVISIONS

1.1 Landlord:

RODICK EQUITIES INC., a company incorporated under the laws of the Province of Ontario and having a mailing address for the purposes of this Lease at 40 University Avenue, Suite 1200, Toronto, Ontario M5J 1T1.

1.2 Tenant:

FLUIDIGM CANADA INC.

1.3 Building:

1380 Rodick Road, Markham, Ontario, situate upon the lands described in Schedule "A" of this Lease.

1.4 Premises (Section 2.1)

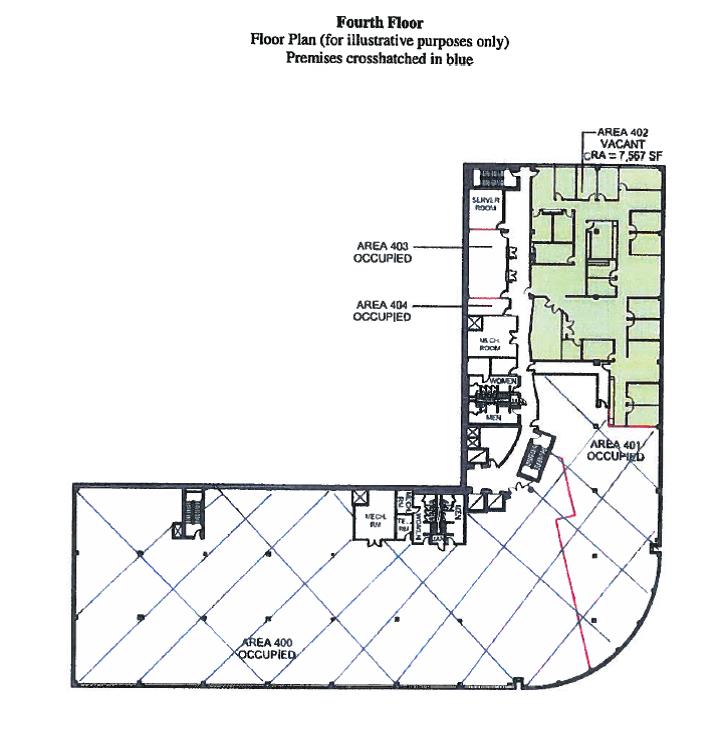

An aggregate area of approximately forty-one thousand, one hundred and forty-five (41,145) square feet in the Building, comprised of: (i) the Office Premises, cross hatched in blue on Schedule "B" of this Lease, designated as Suites 400 and 401, located on the fourth floor of the Office Component and having a Rentable Area of thirty thousand and nineteen (30,019) square feet; and (ii) the Warehouse Premises cross hatched in blue on Schedule “B-1” of this Lease, located on the ground floor, in the Warehouse Component, comprised of a Rentable Area of approximately eleven thousand, one hundred and twenty-six (11,126) square feet. The Rentable Area of the Office Premises includes a Proportionate Share of Common Areas of the Building. The Office Premises has been measured in accordance with BOMA. The Warehouse Premises shall be measured by the Landlord’s space planner in accordance with BOMA / SIOR 2009 Method B and all Rents will be adjusted to reflect the actual Rentable Area, retroactively if necessary. Except as otherwise specifically set out herein, the Office Premises and the Warehouse Premises are hereinafter collectively referred to herein as the “Premises”.

1.5 Term: (Section 3.1)

Ten (10) years having a Term Commencement Date of April 1, 2016 and ending March 31, 2026.

5

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

1.6 Basic Rent: (Section 4.2)

The Tenant will, throughout the Term, pay to the Landlord or to the Manager as the Landlord directs, at its head office, or at any other place designated by the Landlord or the Manager, as the case may be, in Canadian funds, without demand and without deduction, abatement, set-off or compensation as Basic Rent, as follows:

(A) Office Premises Basic Rent

(i) during the period from and including April 1, 2016 to and including March 31, 2021, the annual sum of [*****] ($[*****]) payable in equal consecutive monthly instalments of [*****] ($[*****]) each in advance on the first day of each calendar month during the aforesaid period based on an annual rate of [*****] ($[*****]) per square foot of the Rentable Area of the Office Premises;

(ii) during the period from and including April 1, 2021 to and including March 31 2023, the annual sum of [*****] ($[*****]) payable in equal consecutive monthly instalments of [*****] ($[*****]) each in advance on the first day of each calendar month during the aforesaid period based on an annual rate of [*****] ($[*****]) per square foot of the Rentable Area of the Office Premises; and

(iii) during the period from and including April 1, 2023 to and including March 31, 2026, the annual sum of [*****] ($[*****]) payable in equal consecutive monthly instalments of [*****] ($[*****]) each in advance on the first day of each calendar month during the aforesaid period based on an annual rate of [*****] ($[*****]) per square foot of the Rentable Area of the Office Premises.

(B) Warehouse Premises Basic Rent

(i)during the period from and including April 1, 2016 to and including March 31, 2021, the annual sum of [*****] ($[*****]) payable in equal consecutive monthly instalments of [*****] ($[*****]) each, in advance, on the first day of each calendar month, during the aforesaid period based on an annual rate of [*****] ($[*****]) per square foot of the Rentable Area of the Warehouse Premises; and

(ii) during the period from and including April 1, 2021 to and including March 31, 2026, the annual sum of [*****] ($[*****]) payable in equal consecutive monthly instalments of [*****] ($[*****]) each, in advance, on the first day of each calendar month, during the aforesaid period based on an annual rate of [*****] ($[*****]) per square foot of the Rentable Area of the Warehouse Premises.

6

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

1.7 Additional Rent:

The following additional payments are due as rent payable as of and from the Rent Commencement Date:

(a) Proportionate Share of Realty Taxes and Operating Costs (Section 4.4)

(b) Utilities for Premises (Section 4.5)

(c) Additional Services, if any (Section 4.6)

1.8 Deposit:

The Landlord acknowledges that the Tenant has deposited the sum of [*****] ($[*****]), with CBRE Limited, to be applied as provided in Section 4.3 hereof.

1.9 Rent Commencement Date: (Section 4.1)

All Rent payments will commence April 1, 2016.

1.10 Indemnifier:

To induce the Landlord to enter into this Lease, Fluidigm Corporation, will, jointly and severally, indemnify the Landlord with respect to the Tenant’s observance and performance of its obligations under this Lease. The Indemnifier will execute the Landlord’s standard form of Indemnity Agreement, attached hereto as Schedule “I”, upon terms reasonably acceptable to both parties, concurrently with the execution of this Lease.

1.11 Fundamental Provisions:

Each reference in this Lease to any of the Fundamental Provisions listed above shall be read as having the same dates, quantities and other meanings as specified in this Article I. Certain words and phrases recurring throughout this Lease have defined meanings as set out in Article 15, unless the subject matter or context requires otherwise.

ARTICLE II ‑ PREMISES

2.1 Lease:

In consideration of the Rent to be paid, the Landlord hereby leases to the Tenant the premises cross hatched in blue on Schedule "B" and Schedule “B-1”of this Lease, (the "Premises") described in Section 1.4 hereof, together with the rights and privileges as contained in this Lease, and the Tenant hereby

7

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

leases and accepts the Premises from the Landlord, to have and to hold during the Term, subject to the terms, covenants and conditions set out in this Lease. The area of the Premises will be measured by the Landlord, and the Rent will be adjusted in accordance with the certified area. The Landlord will advise the Tenant in writing of the area measurement, and the parties agree to be bound thereby.

2.2 Use:

The Tenant covenants to use: (i) the Office Premises for general office and administrative purposes and as a facility for research and testing of bio-analytical instruments and reagents for the Tenant’s business; and (ii) the Warehouse Premises for general distribution and warehousing activities, and the testing, development, production and manufacturing of bio-analytical instruments and reagents for the Tenant’s business. The Tenant shall use the Premises in compliance with all applicable laws, including without limitation, the bylaws and applicable zoning of the municipality in which the Premises is located. The Premises shall not be used for any other purpose or business. The Premises shall only be used in accordance with the standards of a first-class office building of similar age and in a similar location, and subject in any event to the limitations on use set forth in Section 14.16 hereof. The use, storage, handling, mixing, or disposal of any items used, researched, tested, manufactured, produced, developed or disposed in or from the Office Premises and Warehouse Premises (as the case may be) shall be conducted in accordance with all Environmental Laws. The Tenant shall indemnify Landlord and the Landlord Beneficiaries for all costs and expenses related to, arising out of or based upon any act, event, condition or circumstance resulting in any Contaminants in, at, above, on or migrating from the Premises by the Tenant or by the Tenant’s Parties.

The Tenant shall take possession of the Premises no later than the Term Commencement Date, unless the Landlord otherwise consents in writing, which consent shall not be unreasonably withheld.

2.3 Rules and Regulations:

The Tenant covenants to abide by the Rules and Regulations as set out in Schedule "D" annexed hereto, and to cause those for whom it is responsible to observe such Rules and Regulations. The Landlord, acting reasonably, may make changes to the Rules and Regulations from time to time, provided that the Landlord shall not be liable in any way for either a failure to enforce such observance, or a failure on the part of other tenants to so observe.

2.4 Observance of Law:

The Tenant is responsible at all times to comply with and to keep the Premises, the Leasehold Improvements and Trade Fixtures, and to otherwise conduct its business, in accordance with the requirements of all applicable laws, directions, rules, regulations or codes of the Landlord and every governmental authority having jurisdiction and of any insurer by which the Landlord or the Tenant is insured and affecting the operation, condition, maintenance, use or occupation of the Premises and Trade Fixtures or the making of any repair or alteration including, without limitation, compliance with each Environmental Law and, to the extent known by the Tenant, any agreements with adjoining owners and or third parties affecting the Premises and the Building. The Tenant shall not allow or cause any act

8

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

or omission to occur in or about the Premises which may result in an illegal use or causes any breach of or non-compliance with such laws, directions, rules, regulations and codes. If, due to the Tenant's acts, omissions or use of the Premises, repairs, alterations or improvements to the Premises or the Building are necessary to comply with any of the foregoing or with the requirements of insurance carriers, the Tenant will pay the entire cost thereof.

2.5 No Waste or Nuisance:

The Tenant shall not commit or permit any waste or damage to the Premises or the Building, or commit or permit anything which may disturb the quiet enjoyment of any occupant of the Building or which may interfere with the operation of the Building. The Tenant will not cause or permit any nuisance or hazard in or about the Premises and Tenant will not permit the unlawful storage of any Contaminant or any unlawful Discharge in or about the Premises or the Building and will keep the Premises free of unlawful Contaminants, debris, trash, rodents, vermin and anything of a dangerous, noxious or offensive nature or which could create a fire hazard (through undue load on electrical circuits or otherwise) or undue vibration, heat or any noxious or strong noises or odours or anything which may disturb the enjoyment of the Building and the Common Areas by customers and other tenants of the Building. The Tenant shall ensure that its Leasehold Improvements, Trade Fixtures or other equipment do not disrupt, adversely affect, or interfere with providers of telecommunication services in the Building or with any other tenant’s or occupant’s use or operation of communications, computer or other equipment or facilities in the Building; and should such disruption, adverse effect or interference occur, the Tenant shall immediately cease operation of the relevant facilities or equipment until the problem is corrected. Without limiting the generality of the foregoing: (a) the Tenant shall not use or permit the use of any equipment or device such as, without limitation, loudspeakers, stereos, public address systems, sound amplifiers, radios, televisions or VCR's which is in any manner audible or visible outside of the Premises; and (b) no noxious or strong odours shall be allowed to permeate outside the Premises; and (c) no boot trays or other items may be placed outside the Premises; in each case without the prior written consent of the Landlord which may be arbitrarily withheld or withdrawn on 24 hours’ written notice to the Tenant.

2.6 Common Areas:

The Landlord agrees that the Tenant, in common with all others entitled thereto including the general public in concourse areas, may use and have access through the Common Areas for their intended purposes during Normal Business Hours and in accordance with the Rules and Regulations only; provided however, that in an emergency or in the case of the Landlord making repairs, the Landlord may temporarily close or restrict the use of any part of the Common Areas, although the Landlord shall, in such instances, endeavour not to prevent access to the Premises.

2.7 Easements:

The Tenant acknowledges that the Landlord and any persons authorized by the Landlord may, after delivery of at least forty-eight (48) hours’ prior written notice to the Tenant (except in the case of an emergency real or apprehended in which case no notice shall be required), install, maintain and repair pipes, wires and other conduits or facilities through the Common Areas and the Premises. Any

9

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

such installing, maintaining and repairing shall be done as quickly as possible and in a manner that will minimize inconvenience to the Tenant.

2.8 Covenants of Landlord and Tenant:

The Landlord covenants to observe and perform all of the terms and conditions to be observed and performed by the Landlord under this Lease. The Tenant covenants to promptly pay the Rent when due under this Lease, and to observe and perform all of the terms and conditions to be observed and performed by the Tenant under this Lease.

ARTICLE III ‑ TERM ‑ POSSESSION

3.1 Term:

This Lease shall be for the Term set out in Section 1.5 unless earlier terminated as provided in this Lease, and nothing hereafter contained in this Article III shall postpone the Term Commencement Date, or extend the Term.

3.2 Tenant Fixturing:

Provided the Lease has been executed by the Tenant on or before August 17, 2015 in a form acceptable to the Landlord, the Tenant will be given access to the Office Premises, on an “as is” basis, for the purpose of construction of its Leasehold Improvements, fixturing the Office Premises and carrying on the Tenant’s business, within three (3) Business Days of the execution of this Lease by both parties and receipt of the Tenant’s certificates of insurance, to and including the day immediately preceding the Term Commencement Date (the “Fixturing Period”).

Provided the Lease has been executed by the Tenant on or before August 17, 2015 in a form acceptable to the Landlord, the Tenant will be granted possession of the Warehouse Premises on the later of: (i) the date the Landlord’s Work in respect of the Warehouse Premises is sufficiently complete or (ii) October 31, 2015, to and including the day immediately preceding the Term Commencement Date (the “Warehouse Fixturing Period”).

The Tenant’s occupation of the Office Premises and Warehouse Premises during the Fixturing Period and Warehouse Fixturing Period (as the case maybe) will be governed by all terms and conditions of this Lease, [*****].

3.3 Delay in Possession:

Should the Tenant be delayed by fault of the Landlord in taking possession of the Premises on the Term Commencement Date, then and only then shall the payment of Rent be postponed for the same number of days that the Tenant is so delayed in taking possession of the Premises. The Tenant hereby acknowledges and agrees that such postponement of the payment of Rent shall be in full settlement for any claims it might have against the Landlord for being delayed in its taking possession of the Premises.

10

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

3.4 Surrender:

The Tenant shall surrender possession of the Premises upon termination of this Lease by expiration of the Term or operation of the terms hereof.

3.5 Overholding:

If the Tenant remains in possession of the Premises following termination of this Lease by expiration of the Term or operation of the terms hereof, with or without objection by the Landlord, and without any written agreement otherwise providing, the Tenant shall be deemed to be a monthly tenant upon the same terms and conditions as are contained in this Lease except as to the Term, and except as to Basic Rent which shall be equal to [*****]. This provision shall not authorize the Tenant to so overhold where the Landlord has objected. Notwithstanding the foregoing, the Tenant shall be permitted upon the Landlord’s written permission to hold over its occupancy of the Premises beyond the expiration of the Term, [*****] for a period of [*****].

3.6 Effect of Termination:

The expiry or termination of this Lease whether by elapse of time or by the exercise of any right of either the Landlord or the Tenant pursuant to this Lease shall be without prejudice to the right of the Landlord to recover arrears of rent and the right of each party to recover damages for an antecedent default by the other.

3.7 Acceptance of Premises:

Taking possession of all or any portion of the Premises by the Tenant will be conclusive evidence as against the Tenant that the Premises or such portion thereof are in satisfactory condition on the date of taking possession, subject only to latent defects and to those deficiencies (if any) listed in writing in a notice delivered by the Tenant to the Landlord not more than ten (10 thirty (30) days after the later of the date of taking possession and the Term Commencement Date.

3.8 Demolition: Intentionally Deleted

Notwithstanding any other provision of this Lease, the Landlord may terminate the Lease at any time during the Term if the Landlord decides to demolish, alter or renovate the Building. The Landlord will give the Tenant not less than six months notice of termination of the Lease pursuant to this provision. The six months' notice specified above need not expire at the end of any year or at the end of any month, and if the day fixed for termination of the Lease expires on some day other than the last day of a month, the Rent for such month shall be apportioned on a per diem basis for the broken period.

3.9 Relocation: Intentionally Deleted

If at any time during the Term the Landlord requires possession of the Premises in order to carry out or complete any alterations to the Building or the Common Areas provided for in Section 6.15, Landlord,

11

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

on not less than 3 months' notice to the Tenant, may require the Tenant to vacate the Premises on the date specified in such notice and relocate into other premises in the Building. The lease insofar as it relates to the Premises shall terminate on such specified date. Such other premises shall be comparable in all material respects to the Premises and shall be available for occupancy not later than 6 months after the date that the Tenant is required to vacate the Premises. The Landlord shall pay all direct costs of preparing such other premises for occupation by the Tenant and of relocating the Tenant and all Tenant property therein. The Landlord shall not be liable for any other or any consequential costs, damages or losses of the Tenant. From and after the specified vacating date such other premises shall be deemed to be the Premises for all purposes of this Lease and such rent as is affected by a change in area shall be adjusted so that the same rent per square foot per annum shall be payable with respect to such other premises as had been payable with respect to the premises from which the Tenant has relocated.

ARTICLE IV ‑ RENT

4.1 Payment:

From and after the Rent Commencement Date, the Tenant shall pay to the Landlord the Basic Rent and the Additional Rent as set out in this Lease.

4.2 Basic Rent:

The Tenant shall pay Basic Rent in the amount set out in Section 1.6, which shall be payable without demand in advance in equal consecutive monthly instalments on the first of each month commencing on the Rent Commencement Date. Rent is subject to adjustment upon certification of the Rentable Area of the Premises.

4.3 Deposit:

The Landlord acknowledges that the Tenant has paid the following amounts, in trust, to CBRE Limited, the Landlord’s broker:

(A) Office Premises

(a) | Rental Deposit - The sum of [*****] ($[*****]) (the “Rental Deposit”). The Rental Deposit shall be held, without interest, and applied against first months’ Rent with respect to the Office Premises, (Basic Rent, Tenant’s Proportionate Share of Operating Costs, Realty Taxes, Premises hydro and HST) as it first falls due and payable by the Tenant under this Lease; and |

(b) | Security Deposit - The sum of [*****] ($[*****])equal to the last months’ Rent with respect to the Office Premises (Basic Rent, Tenant’s Proportionate Share of Operating Costs, Realty Taxes, Premises hydro and HST), (the “Security Deposit”), which shall be held, by the Landlord, without interest, and applied against the Tenant’s faithful performance of its |

12

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

obligations under this Lease and, if not applied to remedy a default, returned to the Tenant within thirty (30) days after the expiry of this Lease or any extension thereof.

(B) | Warehouse Premises |

(a) | Rental Deposit - the sum of [*****] ($[*****]) (the “Warehouse Rental Deposit”), which will be held, without interest, and applied on account of the first month’s Rent with respect to the Warehouse Premises (Basic Rent, Tenant’s Proportionate Share of Operating Costs, Realty Taxes, and HST) as it first falls due and payable by the Tenant under this Lease; and |

(b) | Security Deposit - the sum of [*****]($[*****]) (the “Warehouse Security Deposit”) equal to the last months’ Rent with respect to the Warehouse Premises (Basic Rent, Tenant’s Proportionate Share of Operating Costs, Realty Taxes, and HST), which will be held, without interest, by the Landlord as security against the Tenant’s faithful performance of its obligations under this Lease and if not applied to remedy a default, shall be returned to the Tenant within thirty (30) days after the expiry of this Lease or any extension thereof. |

4.4 Proportionate Share of Realty Taxes and Operating Costs:

(a) | The Tenant shall pay to the Landlord its Proportionate Share of Realty Taxes and Operating Costs commencing on the Rent Commencement Date. The Tenant will also pay a share of all Realty Taxes levied, assessed or allocated by the Landlord in respect to the Common Areas, if applicable. On or before the Term Commencement Date and the commencement of any Fiscal Period in which the Term falls, the Landlord shall estimate the Realty Taxes and Operating Costs and the Tenant's Proportionate Share thereof. The Tenant shall pay to the Landlord in equal monthly instalments in advance on the first day of each month a sum on account of its Proportionate Share of Realty Taxes and Operating Costs based on the Landlord's estimates. |

(b) | The Landlord may from time to time re‑estimate the amount of projected Realty Taxes and Operating Costs for the then current Fiscal Period and re‑estimate the Tenant's Proportionate Share thereof for the remainder of the Fiscal Period and the Tenant shall change its monthly instalments to conform with the revised estimates. |

(c) | After the end of each Fiscal Period the Landlord shall determine the actual Tenant's Proportionate Share of Realty Taxes and Operating Costs and the difference between such actual determination and the amount already billed to the Tenant in instalments. If the aggregate of the Tenant's instalments for the Fiscal Period in question was less than the actual determination, then the Tenant shall pay the difference to the Landlord forthwith, or if the aggregate of such instalments was more than the actual determination, the Landlord shall credit the difference to the Tenant's rental account. |

13

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

4.5 Utilities ‑ Light Fixtures:

(a) | Except where the Tenant is purchasing Utilities directly from a supplier, the Tenant shall pay to the Landlord the cost of Utilities supplied to the Premises commencing on the Rent Commencement Date, as reasonably determined by the Landlord, and billed monthly, in advance. The amount of such cost shall be based on the Landlord's reasonable estimates for the quantities of Utilities supplied multiplied by the average unit costs to the Landlord for such utilities. The Tenant shall if requested by the Landlord or may, if it desires, install at the Tenant's own expense meters to measure the amount of any utilities supplied, and the Landlord shall employ the resulting metered quantities in lieu of estimated consumption. The Tenant shall also pay to the Landlord the cost of cleaning, maintaining and servicing all electric light fixtures in the Premises, including the cost of replacing light bulbs, tubes, starters and ballasts. |

Landlord will install, at the Tenant’s cost and expense, check meters to measure the Tenant’s hydro consumption in the Office Premises and Warehouse Premises, the cost of which at Tenant’s option, may be subtracted from the Tenant’s Allowance for Tenant’s Leasehold Improvements or shall be payable to the Landlord as Additional Rent under this Lease, prior to the Term Commencement Date, upon written demand.

(b) | Where the Tenant is purchasing utilities directly from a supplier, it shall only deal with such suppliers that have obtained a license or other form of approval from the Landlord to run service for such utility through the Building. |

4.6 Additional Services:

(a) | The Tenant may from time to time request Additional Services from the Landlord and the Tenant shall pay to the Landlord, the Landlord's charge for such Additional Services, payable forthwith upon receipt of the Landlord's invoice therefor. |

(b) | The Tenant shall not install in the Premises, without the Landlord's prior written consent, equipment (including telephone equipment) which generates sufficient heat to affect the temperature otherwise maintained in the Premises by the air conditioning system as normally operated. The Landlord may install supplementary air conditioning units, facilities or services in the Premises, or modify its air conditioning system, as may in the Landlord's reasonable opinion be required to maintain proper temperature levels, and the Tenant shall pay the Landlord within ten (10) days of receipt of any invoice for the cost thereof, including, without limitation, installation, operation and maintenance expenses, plus 15% of such cost to cover the Landlord's costs of administration. |

(c) | If the Landlord shall from time to time reasonably determine that the use of electricity or any other utility or service in the Premises is disproportionate to the use of other tenants in the Building the Landlord may adjust the Tenant's share of the cost thereof from a date reasonably determined by the Landlord to take equitable account of the disproportionate use and may separately charge the Tenant for such excess cost, plus 15% of such excess cost to cover the Landlord's costs of administration. At the Landlord's request, the Tenant shall install and |

14

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

maintain at the Tenant's expense metering devices for checking the use of any such utility or service in the Premises. In all cases the Tenant shall reimburse the Landlord in the same manner in which the Landlord is charged including any demand or energy charges.

4.7 General Provisions:

(a) | No Delay in Payment of Rent: Nothing contained in this Lease shall suspend or delay the payment of any money at the time it becomes due and payable. The Tenant agrees that the Landlord may, at its option, apply any sums received against any amounts due and payable under this Lease in such manner as the Landlord sees fit. |

(b) | Interest on Arrears: If any amount of Rent is in arrears it shall bear interest at the Interest Rate. |

(c) | Partial Periods: If the Rent Commencement Date is any day other than the first day of a calendar month, or if the Term ends on a day other than the last day of a calendar month, then Basic Rent and Additional Rent, as the case may be, will be adjusted for the months affected, pro rata based on a 365 day year. |

(d) | Estimated Amounts: Where the Landlord estimates or re‑estimates the costs of Realty Taxes, Operating Costs and the amount of Utilities supplied, it shall do so acting reasonably and shall provide the Tenant with statements of such estimates in reasonable detail. |

(e) | Audited Statement: Invoices for the actual determination of the Tenant's Proportionate Share of Operating Costs shall be accompanied by an audited statement of such Operating Costs. |

(f) | General: All amounts payable by the Tenant to the Landlord pursuant to this Lease shall be deemed to be Rent. The Tenant agrees to pay all Rent together with Rental Taxes, if applicable, in advance on the first day of each month without deduction or abatement, except as expressly provided in this Lease, and without set‑off, and where payments due have been invoiced, such amounts shall be paid within ten (10) days of delivery of such invoice. All Rent shall be paid in lawful money of Canada. |

ARTICLE V ‑ TAXES

5.1 Taxes Payable by the Landlord:

The Landlord shall pay before delinquency all Realty Taxes. The Landlord covenants that at all appropriate times it shall declare itself a public school supporter for purposes of determining the amounts of any Realty Taxes payable.

15

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

5.2 Business and Other Taxes Payable by the Tenant:

The Tenant shall pay before delinquency all business taxes, and any other taxes, charges, rates, duties and assessments levied, rated, imposed, charged or assessed against or in respect of any use or occupancy of the Premises or in respect of the personal property, Leasehold Improvements, Trade Fixtures, fixtures and facilities of the Tenant or the business or income of the Tenant on or from the Premises. The Tenant shall pay to the Landlord any increase or incremental amount of Realty Taxes or other taxes which the Landlord, acting reasonably, has determined to be attributable to an act by the Tenant (for example declaring itself a separate school supporter) or attributable to the Leasehold Improvements and Trade Fixtures.

5.3 Contesting Taxes:

(a) | The Tenant may, at its expense, appeal or contest the taxes, assessments and other amounts payable as described in Section 5.2 hereof, but such appeal or contest shall be limited to the assessment of the Premises alone and not to any other part of the Building or the Lands provided it first gives the Landlord written notice of its intention to do so, and consults with the Landlord, and obtains the Landlord's prior written approval, which shall not be unreasonably withheld. |

(b) | The Landlord reserves the right to appeal or contest any taxes payable by the Landlord. |

5.4 Alternate Methods of Taxation:

If, during the Term, the method of taxation shall be altered, so that the whole or any part of the Realty Taxes now levied, on real estate and improvements are levied wholly or partially as a capital levy or on the rents received or reserved or otherwise, or if any new or other tax, assessment, levy, imposition or charge in lieu thereof, shall be imposed upon the Landlord, related in any way to the Building, the Lands or the income therefrom, then all such taxes, assessments, levies, impositions and charges shall be included when determining the Realty Taxes. If, during the Term, the method of taxation shall be altered, so that the whole or any part of the business taxes formerly payable in respect of any use or occupancy of the Premises is merged into a comprehensive realty tax, the Landlord shall have the right to allocate and collect such component of the comprehensive realty tax (as would have been formerly business taxes) in the manner or on the same basis as would have been employed.

ARTICLE VI ‑ MAINTENANCE, REPAIRS AND ALTERATIONS

6.1 General Statement:

The Landlord and Tenant agree to carry out their respective responsibilities for maintenance and repair as detailed in this Lease in accordance with general standards for comparable office buildings in the City of Markham, of similar age and in a similar location.

6.2 Responsibility of Tenant:

Without notice or demand from the Landlord, the Tenant shall:

16

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

(a) | Maintain and keep in a good state of repair and in good appearance compatible with the Building, the Premises including the interior faces of any demising walls and permanent building walls, columns and covers for heating units along the exterior walls. |

(b) | Maintain and keep in a good state of repair, the Leasehold Improvements, the Trade Fixtures and any signage, or other fixtures, attachments or installations in any part of the Building permitted by this Lease to be installed by or on behalf of the Tenant, whether or not located in the Premises. |

(c) | Keep the Premises in a clean and tidy condition, and not permit wastepaper, garbage, ashes, waste or objectionable material to accumulate thereon or in or about the Building, other than in areas designated by the Landlord. |

(d) | Repair all damage in the Premises resulting from any misuse, excessive use or installation, alteration, or removal of Leasehold Improvements, Trade Fixtures, fixtures, furnishings or equipment. |

6.3 Tenant Not Responsible:

Notwithstanding Section 6.2 hereof, the Tenant shall not be responsible for:

(a) | Reasonable wear and tear. which does not affect the proper use and enjoyment of the Premises. |

(b) | The obligations of the Landlord as set out in Section 6.4 hereof. |

6.4 Responsibility of Landlord:

The Landlord shall maintain and keep in a good state of repair:

(a) | The Building structure, roof, and permanent building walls (except for interior faces facing into the Premises). |

(b) | Equipment installed by the Landlord to heat, ventilate, and air-condition the Building. |

(c) | Systems installed by the Landlord for the distribution of Utilities. |

(d) | The Common Areas including the elevators. |

(e) | The Landlord's Improvements in the Premises. |

6.5 Inspection, Entry and Notice:

(a) | The Landlord, or its agents, may, from time to time, acting reasonably and where practical in a manner that will not substantially disrupt the Tenant's business, after delivery of |

17

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

at least forty-eight (48) hours’ prior written notice to the Tenant (except in the case of an emergency real or apprehended in which case no notice shall be required), enter the Premises and inspect the state of maintenance, repair and decoration, and after twenty-four (24) hours’ upon reasonable prior notice to the Tenant, show the Premises to prospective purchasers, tenants and existing or prospective Mortgagees.

(b) | The Landlord may give written notice to the Tenant requiring it to perform in accordance with Section 6.2 hereof, and the Tenant shall rectify any failure to perform within the time period set out in Section 12.1 hereof. Should the Tenant fail to commence such remedy within the allotted time, or having so commenced, fail to diligently continue such remedy to conclusion, the Landlord may carry out such remedy without further notice to the Tenant, and charge the Tenant for such remedy as if it were an Additional Service requested by the Tenant. |

(c) | If the Tenant is not present to open and permit any entry into the Premises when for any reason an entry shall be necessary in the case of emergency, the Landlord or its agents may, using reasonable force, enter the same without rendering the Landlord or such agents liable therefor, and without affecting the obligations and covenants of Tenant under this Lease. |

(d) | Nothing in this Lease shall make the Landlord liable for any actions, notices or inspections as described in this Section 6.5, nor is the Landlord required to inspect the Premises, give notice to the Tenant (except as otherwise specifically provided in this Lease) or carry out remedies on the Tenant's behalf, nor is the Landlord under any obligation for the care, maintenance or repair of the Premises, except as specifically provided in this Lease. |

6.6 Notify the Landlord:

The Tenant covenants to immediately notify the Landlord of any defect, damage or malfunction affecting the Premises or other parts of the Building of which the Tenant is aware.

6.7 Alterations or Improvements:

(a) | Following approval by the Landlord, the Tenant shall install its initial Leasehold Improvements and Trade Fixtures in accordance with the provisions of Schedule "C" annexed hereto and the "Design Criteria Manual" (if applicable) prepared by the Landlord and provided to the Tenant. |

(b) | Following installation of such initial Leasehold Improvements, and Trade Fixtures the Tenant shall not make any alterations, repairs, changes, replacements, additions, installations or improvements (the "Alterations") to any part of the Premises or Leasehold Improvements and Trade Fixtures without the Landlord's prior written approval, which approval shall not be unreasonably withheld, unless the Alteration may affect a structural part of the Building or may affect the mechanical, electrical, communications, air control or other basic systems of the Building or the capacities thereof, in which instance the Landlord's approval may be arbitrarily withheld. The Tenant shall submit to the Landlord details of any proposed work, including complete working drawings and specifications prepared by qualified designers and conforming to good engineering practice. |

18

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

(c) | The installation of all Leasehold Improvements shall: |

‑ be performed expeditiously and at the sole risk and expense of the Tenant;

‑ be performed by competent workmen whose labour union affiliations, if any, are compatible with others employed by the Landlord and its contractors, and who will not interfere with work being performed by the Landlord;

‑ be performed in a good and workmanlike manner and only in accordance with the drawings and specifications which the Landlord has approved; and

‑ be performed in compliance with the applicable requirements of all Authorities, evidence of which shall be provided to the Landlord, and be subject to the supervision and direction of the Landlord.

(d) | Any Leasehold Improvements made by the Tenant without the prior written consent of the Landlord or which are not in accordance with the drawings and specifications approved by the Landlord shall, if requested by the Landlord, be promptly removed by the Tenant at the Tenant's expense, and the Premises shall be restored to their previous condition. |

(e) | The Tenant shall reimburse the Landlord for the cost of technical evaluation of the Tenant's plans and specifications and shall revise such plans and specifications, as the Landlord deems necessary. |

(f) | In carrying out any Alterations or Leasehold Improvements in the Premises, the Tenant, at its expense, shall pay to the Landlord with respect to such work the cost to the Landlord of all Utilities supplied to the Premises with respect to such work and the cost of any Additional Services including the cost of any necessary cutting or patching or repairing of any damage to the Building or the Premises, any cost to the Landlord of removing refuse, cleaning, hoisting of materials and any other costs of the Landlord which can be reasonably allocated as a direct expense relating to the conduct of such work. |

(g) | If a request is made by the Tenant with respect to Alterations which may affect the structure or matters which affect the mechanical, electrical, communications, air control or other basic systems of the Building or the capacities thereof, which is approved by the Landlord, the Landlord may require that such work be designed by consultants designated by it and that it be performed by the Landlord or its contractors. If the Landlord or its contractors perform such work, it shall be at the Tenant's expense in an amount equal to the Landlord's total cost of such work or the contract price therefor plus ten (10%) percent, payable following completion upon demand. Notwithstanding the foregoing, if the Tenant requests the Landlord to alter or install any Leasehold Improvements or Trade Fixtures such work will be considered as an Additional Service. |

(h) | No Leasehold Improvements by or on behalf of the Tenant shall be permitted which may adversely affect the condition or operation of the Building or any of its systems or the Premises or diminish the value thereof or restrict or reduce the Landlord's coverage for municipal zoning purposes. |

19

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

(i) | During the construction and installation of Leasehold Improvements the Tenant shall keep the Building clean from any debris related thereto, and in any event after construction is completed the Tenant shall do an adequate "first clean" to the Premises. |

(j) | The Tenant shall promptly pay all its contractors and suppliers and shall do all things necessary to prevent a lien attaching to the Lands or Building and should any such lien be made or filed, the Tenant shall discharge or vacate such lien immediately. If the Tenant shall fail to discharge or vacate any lien, then in addition to any other right or remedy of the Landlord, the Landlord may discharge or vacate the lien by paying into Court the amount required by statute to be paid to obtain a discharge, and the amount so paid by the Landlord together with all costs and expenses including solicitor's fees (on a solicitor and his client basis) incurred in connection therewith shall be due and payable by the Tenant to the Landlord on demand together with interest at the Interest Rate, calculated from the date of payment by the Landlord until all of such amounts have been paid by the Tenant to the Landlord. |

6.8 Removal and Restoration:

(a) | The Leasehold Improvements shall immediately upon installation become the property of the Landlord without compensation to the Tenant. |

(b) | Unless the Landlord by notice in writing requests otherwise, the Tenant shall at its expense, at the end of the Term or earlier termination of this Lease, remove all (or part, as designated by the Landlord) of the Leasehold Improvements, and, subject only to reasonable wear and tear, restore the Premises to the base building standard with the basic systems of the Building, including the reconstruction necessary to reinstate the Premises original structure in the event structural changes were undertaken. |

Upon the expiration or earlier termination of the Lease, the Tenant:

(A) shall surrender the Premises in the condition and state of repair in which the Tenant is required to maintain the Premises, reasonable wear and tear excepted;

(B) shall remove all of its trade fixtures, trade equipment, furniture, workstations, security systems, personal property, hazardous substances, chemicals, Contaminants, and contamination; and

(C) | shall not be required to remove any Leasehold Improvements from the Premises, other than those: |

(i)specified by the Landlord in writing at the time Landlord gave its consent to their installation.

(ii)Non-Standard Leasehold Improvements (as defined below) that the Landlord may require to be removed. The term “Non-Standard Leasehold Improvements” means, but shall not be limited to: generators, computer rooms and/or any other raised-floor environments; staircases; laboratory

20

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

rooms; non-standard heating, ventilating and air conditioning systems installed for the specific use of the Premises; custom lighting and electrical installations; dry-wall ceilings; telecommunication equipment (including all cabling, wiring, and conduits which have been installed by or on behalf of the Tenant); safes, vaults, fume hoods, clean rooms, argon storage tanks (including any necessary accessories, such as by way of example, piping, the 12 foot by 13 foot concrete pad, concrete bollards and fencing), exhaust fans, roof penetrations, air makeup units, showers, wash stations, water lines, and ducting for the Tenant’s specific use; or

(iii) installed by or on behalf of the Tenant without the Landlord’s prior consent; and

(D) | shall be required to restore the tbar ceiling grid and ceiling tiles which were removed from the office portion of the Warehouse Premises, at the Tenant’s request, in accordance with the Landlord’s Work. |

The Tenant must repair any damage caused to the Premises or the Building by the removal of the items described in paragraph (B) above and, in the case of paragraphs (C) and (D) above, restore the applicable part of the Premises to the condition they were in prior to the relevant installation or removal, reasonable wear and tear excepted.

(c) | Any damage to the Premises or to the Building caused by the installation or removal by the Tenant or by others on its behalf of Leasehold Improvements or trade fixtures shall be repaired forthwith by the Tenant at its expense (except that in the case of damage to areas outside of the Premises or to any structural or base building system or component, such repairs shall be made by the Landlord at the Tenant’s expense). |

6.9 External Changes:

The Tenant agrees that it shall not erect, affix or attach to any roof, exterior walls or surfaces of the Building any antennae, sign or fixture of any kind, nor shall it make any opening in or alteration to the roof, walls, or structure of the Premises, or install in the Premises or Building free standing air‑conditioning units, without the prior written consent of the Landlord which may be arbitrarily withheld.

6.10 Trade Fixtures:

The Tenant may, at the end of the Term, if not in default, remove its Trade Fixtures, and the Tenant shall, in the case of every installation or removal of Trade Fixtures, make good any damage caused to the Premises or the Building by such installation or removal. Any Trade Fixtures removed during the Term will be contemporaneously replaced with Trade Fixtures of equal or better quality. Any Trade Fixtures and equipment belonging to the Tenant, if not removed at the termination or expiry of this Lease, shall, if the Landlord so elects, be deemed abandoned and become the property of the Landlord without

21

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

compensation to the Tenant. If the Landlord shall not so elect, the Landlord may remove such Trade Fixtures from the Premises and store them at the Tenant's risk and expense and the Tenant shall save the Landlord harmless from all damage to the Premises caused by such removal, whether by the Tenant or by the Landlord.

6.11 Tenant's Signs:

The Tenant shall not at any time cause or permit any sign, picture, advertisement, notice, lettering, flag, decoration or direction (hereinafter collectively called "Signs") to be painted, displayed, inscribed, placed, affixed or maintained within the Premises and visible outside the Premises or in or on any windows or the exterior of the Premises (including glass demising walls facing onto Common Areas), nor anywhere else on or in the Building, without the prior and continuous consent of the Landlord which consent may, with respect to proposed signage on the main floor of the Building, or which can be seen from outside the Premises, be arbitrarily withheld, but otherwise shall not be unreasonably withheld, provided that the copy and style of any Signs shall be consistent with the first-class nature of the Building and in accordance with the Landlord's sign criteria. No hand-written signs will be permitted. The Landlord may at any time prescribe a uniform pattern of identification signs for tenants to be placed on the outside of the Premises and other premises. Any breach by the Tenant of this provision may be immediately rectified by the Landlord at the Tenant's expense and in this connection, the Landlord shall be entitled to enter the Premises and remove any Signs contravening this provision and charge the Tenant the costs thereof, and same shall not constitute a re-entry under this Lease and the Landlord shall not be liable for any damages caused thereby, whether or not arising from its own negligence.

Notwithstanding the foregoing, the Landlord will, at the expense of the Tenant, supply and install: (a) a sign bearing the name of the Tenant which will be located on or near the entrance door of the Office Premises; (b) identification and/or directional signage on the floor the Tenant’s Office Premises are located; (c) one entry in the Building directory board (if any) located in the Building lobby; and (d) one sign between the two elevator doors near the warehouse entrance.

Notwithstanding the foregoing, provided the Tenant is Fluidigm Canada Inc., is itself in occupation of all of the Premises initially leased to Tenant under this Lease, and is not and has not been in default of any provision of this Lease, then Tenant shall be entitled to install at its sole cost and expense, including all costs associated with, maintenance, repair and restoration thereof, a sign on the top fascia of one (1) side of the Building, in an area to be mutually agreed upon by the Landlord and Tenant. Said signage shall be of a design and quality appropriate to the image of the Building, in keeping with the architectural integrity of the Building, and shall be subject to the prior written approval of Landlord of its design and specifications. All costs of maintaining this signage, including, without limitation, all costs of electricity consumed by the sign, will be paid for by Tenant to Landlord upon receipt of an invoice therefor, with Tenant’s next installment of monthly Rent, as an item of Additional Rent. Tenant’s insurance coverage shall include the sign. Such signage shall be in conformance with the building code, zoning by-laws and the regulations of any other bodies having jurisdiction and Tenant shall obtain, at its sole expense, all necessary permits and approvals. At the earlier of (i) expiration or earlier termination of the Lease, and any renewal or extension thereof, or (ii) the date upon which Tenant ceases to occupy the entirety of the Premises initially leased to it under this Lease, if requested by the Landlord in writing, Tenant shall, at its sole cost and expense, remove all such signage from the Building and make good any

22

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

damage caused thereby. If required by Landlord, the installation and removal of the sign shall be performed by Landlord’s contractors at Tenant’s cost which cost shall be payable as an item of Additional Rent with the next monthly installment of Additional Rent.

6.12 Directory Board:

The Landlord may erect and maintain (as an Operating Cost) a directory board in the main lobby of the Building which shall indicate the name of the Tenant and the location of the Premises within the Building. The Tenant shall pay the Landlord's cost of changes thereto, and any other signage with respect to the Premises. Should sufficient space exist on the directory board, the Landlord may provide to the Tenant, at the Tenant's expense, additional entries as requested. The directory board shall be for identification only and not for advertising. The Landlord's acceptance of any name for listing on the directory board will not be deemed, nor will it substitute for, the Landlord's consent, as required by this Lease, to any sublease, assignment or other occupancy of the Premises.

6.13 Landlord's Signs:

In addition to the Landlord's right to install general information and direction signs in and about the Building as would be customary for comparable office building in the City of Markham, the Landlord shall have the right at any time to place upon the Building a notice of reasonable dimensions, reasonably placed so as not to interfere with the Tenant's business, stating that the Building is for sale, or that areas of the Building are for lease, as the case may be, and at any time during the last six (6) months of the Term, that the Premises are for rent and the Tenant shall not remove such notices or signs.

6.14 Environmental Provisions:

(a) | Notwithstanding any other provision of this Lease, the Tenant and the Tenant’s Parties shall fully comply with all Environmental Laws applicable to the Premises, Building and Lands and the Tenant's use and occupation thereof, including but not limited to the delivery, handling and disposal of Contaminants on the Premises, Lands and or Building, in the care, custody and or control of the Tenant and or the Tenant’s Parties. |

(b) | If the Landlord or Tenant, and or the Tenant’s Parties, receives an order, notice or directive under an Environmental Law (“Offence”), and or is convicted of an Offence, which relates to Contaminants, and or Contaminant Activities at the Premises, Lands or the Building, and such Offence is not rectified in accordance with Environmental Laws, forthwith, by the Tenant, then the Landlord shall have the option, at its sole discretion, to: |

(i) | take reasonable steps to remedy such Offence, at the sole cost and expense of the Tenant, and such costs incurred by the Landlord shall be deemed to be Rent under this Lease and shall be immediately due and owing by the Tenant to the Landlord upon receipt of an invoice for same delivered to the Tenant from the Landlord; or |

23

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

(ii) | if the Offence has an adverse impact on the Premises, Building or Lands, terminate this Lease, in the event the Tenant is unable or unwilling to remedy the Offence, as set out in the first paragraph of (ib) above, forthwith by notice in writing, and the Landlord shall not be liable for any losses or damages of any kind however caused arising out of such termination, and the Tenant shall indemnify, defend with counsel, and hold Landlord and the Landlord Beneficiaries, harmless from and against any and all claims, damages, costs, expenses and liabilities arising out of any attempt by the Landlord to remedy such Offence, and this indemnity shall survive the termination of the Lease, for the period of time allowable in law. |

(c) | The Tenant shall obtain and comply with the terms of all licenses, certificates of approval, permits, orders, directives and other requirements under applicable Environmental Law for the safe and lawful conduct of its business at or from the Premises, Buildings and Lands. |

(d) | The Tenant will not use pesticides in the Premises or the Building unless the Tenant has first obtained prior written consent from the Landlord to do so and has obtained all necessary permits or approvals required under applicable Environmental Law. |

(e) | The Tenant, and the Tenant’s Parties, shall not cause or allow any Contaminant to be used, generated, transported, stored, discharged, spilled, emitted to air or disposed of on, under, above or about, or transported to or from, the Building, Lands, the Common Areas and or the Premises (collectively the " Contaminant Activities") except in strict compliance, at the Tenant's expense, with all applicable Environmental Laws and the reasonable requirements of the Landlord, and using all necessary and appropriate precautions which a cautious, diligent and prudent operator would exercise. |

(f) | The Landlord shall not be liable to the Tenant for any Contaminant Activities conducted or permitted by the Tenant or the Tenant’s Parties in or about the Building, the Common Areas, Lands and or the Premises during the Term and any extensions and or renewals thereof, however caused, whether or not consented to by the Landlord. The Tenant, shall indemnify, defend with counsel, and hold the Landlord and those for whom the Landlord is responsible in law and contract harmless from and against any claims, damages, costs, expenses and or liabilities arising out of any and all such Contaminant Activities conducted or permitted by the Tenant, and the Tenant’s Parties (including without limitation the full amount of all legal and consultants’ fees and expenses and the costs of removal, treatment, storage and disposal of Contaminants and remediation of the Premises and any adjacent property), and this indemnity shall survive the termination of the Lease, for the period of time allowable in law. |

(g) | The Tenant shall immediately notify the Landlord both by telephone and in writing of any actual, alleged or suspected Discharge and the Landlord, its representatives and employees may enter the Premises at any time during the Term to inspect the Tenant's compliance herewith. |

(h) | The Tenant shall also be responsible for proper disposal of all Contaminants and other materials which require special disposal measures, including oil, kitchen waste and grease. |

24

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

The Tenant shall also, if required by the Landlord, refrigerate all garbage, such that it does not constitute a nuisance or health hazard. The Tenant will store and dispose of all of its waste in a lawful manner. In particular, the Tenant will use the garbage collection service provided by the Landlord only to dispose of solid waste (which is not Hazardous Waste) which can lawfully be transported to, and dumped at, a landfill site without requiring payment of surcharges or penalties, and will use the sewers only to dispose of liquid waste (which is not Hazardous Waste) which may be lawfully, and in full compliance with all applicable Environmental Laws, discharged into the municipal sewer. All other wastes shall be disposed of by the Tenant, at its sole cost and expense, at least once every month, using a properly licensed waste hauler, to take away all or part of the Tenant's waste to an appropriately licensed landfill. The Tenant acknowledges and agrees that regardless of whether the waste hauler is retained by the Landlord or the Tenant, the Tenant, and not the Landlord, shall be deemed to be the generator of the Tenant's waste.

(i) | Where the Landlord provides separate waste collection facilities for different types of non-hazardous waste, the Tenant will separate such waste and will deliver each such waste to the appropriate facility. If contamination of such separated waste occurs as a result of Tenant's failure to comply with the foregoing sentence, the Tenant will indemnify the Landlord for all damages, loss, expense and costs incurred by the Landlord with respect to such contamination, together with an administration fee equal to fifteen (15%) percent twenty per cent (20%) of such costs. The Tenant shall comply with any non-hazardous waste reduction work plan prepared by Landlord from time to time (if any), at Tenant's cost. The Tenant shall comply with all reasonable requirements imposed by Landlord with respect to the implementation of a system for the storage, disposal, and separation of non-hazardous waste at the Building as contemplated by this Section 6.14. |

(j) | The Tenant will not authorize, cause or permit a Discharge except in accordance with Environmental Law. |

(k) | The Tenant will fully comply with all orders of an Authority which may be directed to the Landlord or the Tenant and which relate to the Premises or the Building in relation to the Premises, including orders to provide financial assurance, to perform studies, to improve pollution control, to remove waste, to conduct investigations or to prepare or perform an environmental cleanup of the Premises or the Building. Should an order or direction of an Authority be issued to the Landlord or the Tenant, requiring the Landlord or the Tenant to do anything in relation to an environmental problem caused or contributed to by the Tenant, the Tenant will, upon receipt of written notice from the Landlord, satisfy the requirements of the order or direction at the Tenant's expense. |

(l) | If the Tenant fails or refuses to promptly and fully satisfy the requirements of an order or direction referred to in this Section, or if, in the Landlord's opinion the Tenant is not competent to satisfy the requirements of the order or direction, the Landlord may elect in writing (but is not obligated) to satisfy the whole or any part of the requirements of the order or direction at the Tenant's expense. |

25

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

(m) | If the Tenant fails or refuses to promptly and fully satisfy the requirements of any such order or direction the Landlord will have the option, at its sole discretion, to terminate this Lease forthwith by notice in writing, and Landlord will not be liable for any losses or damages of any kind however caused arising out of such termination. |

(n) | Commercial building materials commonly include the use or presence of Contaminants. The Landlord has policies, procedures and programs in place to manage Contaminants known to be present within the Building in accordance with Environmental Laws. The Landlord will take reasonable steps to abate or remove known Contaminants that are in the Landlord’s care, custody and or control and as required by Environmental Laws or deemed necessary by the Landlord. In the event the Tenant undertakes construction during the Fixturing Period, the Warehouse Fixturing Period and/or throughout the Term, the Landlord will provide to the Tenant a designated substances survey prior to the commencement of such construction activities. Additionally, the Landlord will provide any available asbestos containing material information, as it pertains to the Tenant’s occupancy in the Building. |

(o) | The Tenant shall not be liable for Contaminants which do not comply with applicable Environmental Laws and which (i) are present, or discharged, released or otherwise placed at the Premises, Building or Lands or which migrated to the Premises, Building or Lands from other lands, and (ii) were not brought upon, stored, kept, used, introduced or Discharged by the Tenant and or the Tenant’s Parties or otherwise caused, contributed to or made worse by the Tenant and or the Tenant’s Parties, be it before or after the Commencement Date or the end of the Term, but this shall not preclude the Landlord from including in Operating Costs any expenses or costs that pertain to Contaminants at the Building or Lands in Operating Costs except as expressly precluded under the definition of “Operating Costs” in Article XV of this Lease.. |

(p) | The Tenant and the Tenant’s Parties shall not bring or allow to be present in the Premises any Contaminants, other than those Contaminants, if any, which the Tenant requires for the proper operation of its business operations in the Premises, being those listed on Schedule "H". The Tenant shall notify the Landlord in writing of any proposed changes to Schedule "H" (including without limitation, the volume of the items listed on Schedule “H”). If Landlord objects to any such change, Landlord shall make commercially reasonable efforts to provide Tenant with written notice of its objection to any such change within ten (10) Business Days of receipt of Tenant’s written notice, which objection(s) shall be made only upon a reasonable basis. Failure of the Landlord to deliver notice to the Tenant within such ten (10) Business Day period advising of the Landlord’s objection shall not be deemed to be an acceptance by the Landlord of the Tenant's proposed changes to Schedule “H”. Within 20 days of being requested to do so by the Landlord, the Tenant shall provide the Landlord with a written statement describing: |

(i) the procedures used by the Tenant to contain and handle such Contaminants; and

(ii) the procedures used by the Tenant to contain and deal with spills of Contaminants.

26

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT

(q) | Tenant shall ensure that, at all times during the Term, and any extensions thereof, Landlord is in receipt of a copy of the Tenant’s emergency preparedness plans prepared by the Tenant in connection with the use of the Premises which include references to, or which require the involvement of other tenants in the Building. |

6.14A | Tenant’s Responsibility |

(a) | The Tenant shall be solely responsible and liable for any clean-up and remediation required by the Landlord or any Authority having jurisdiction of any Contaminants which the Tenant, the Tenant's Parties or any Transferee caused or allowed to be Discharged, released onto or into the air, the Premises, the Building, other lands and/or the groundwater or surface waters under or on the Lands or any other lands. Upon the occurrence of any such Discharge, the Tenant shall immediately give prompt written notice to the Landlord and take all steps necessary to remedy the situation giving rise to such Discharge. |

(b) | If any such clean-up or remediation is required in accordance with section 6.14A (a), the Tenant shall, at its sole cost, prepare all necessary studies, plans and proposals and submit them to the Landlord for approval, provide all bonds and other security required by any lawful Authorities and carry out the work required. In carrying out such work, the Tenant shall keep the Landlord fully informed of the progress of the work. The Landlord may, in its sole discretion, elect to carry out all such work, or any part of it, and, if the Landlord does so, the Tenant shall pay for all costs in connection therewith, together with an administrative fee equal to 15% of such costs, within 15 days of written demand being made by the Landlord. |

(c) | All Contaminants brought or allowed onto the Premises, Building or Lands during the Term, or any extensions thereof, by the Tenant, the Tenant's Parties or a Transferee shall, despite any other provision of this Lease to the contrary and any expiry, termination or disclaimer of this Lease, be and remain the property and sole responsibility of the Tenant regardless of the degree or manner of affixation of such Contaminants to the Premises. In addition, and at the option of the Landlord, anything contaminated by such Contaminants shall become the property of the Tenant. This affirmation of the Tenant’s interest in the Contaminants or the goods containing the Contaminants shall not, however, prohibit the Landlord from dealing with such material as otherwise provided in this Lease. |

(d) | If the Tenant is required by any applicable Environmental Laws to maintain environmental and operating documents and records, including, without limitation, permits and licenses (collectively, "Environmental Records"), the Tenant shall maintain all requisite Environmental Records in accordance with all applicable Environmental Laws. The Landlord may inspect all Environmental Records at any time during Term on forty-eight (48) 24 hours' prior written notice, but no prior notice shall be required in the case of an emergency, real or apprehended. |

The Tenant shall promptly notify the Landlord in writing of:

(i) | any notice or investigation by any Authority alleging non-compliance or a possible violation of or with respect to any Environmental Laws in connection with operations or activities in the Premises; |

(ii) | any charges laid by any Authority alleging non-compliance or a violation by the Tenant, the Tenant's Parties or a Transferee of any Environmental Laws; |

27

[*****] | Confidential Information has been omitted and filed separately with the Securities and Exchange Commission. Confidential treatment has been requested with respect to this omitted information. |

CONFIDENTIAL TREATMENT