UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________________

FORM

(Mark One)

For the fiscal year ended

or

_____________________________________________

Commission file number:

(Exact name of registrant as specified in its charter)

|

||||

State or other jurisdiction of incorporation or organization |

|

I.R.S. Employer Identification No. |

||

|

|

|

||

|

||||

Address of principal executive offices |

|

Zip Code |

||

Registrant’s telephone number, including area code: (

_____________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act:

None

_____________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

|

Accelerated filer |

|

☐ |

|

☒ |

|

|

Smaller reporting company |

|

||

|

|

|

|

|

Emerging growth company |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☐ No

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No

As of June 30, 2023, the aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant was approximately $

As of February 21, 2024, there were

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement in connection with the registrant’s annual meeting of stockholders, scheduled to be held in June 2024, are incorporated by reference in Part III of this report. Except as expressly incorporated by reference, such proxy statement shall not be deemed to be part of this report.

STANDARD BIOTOOLS INC.

FISCAL YEAR 2023

FORM 10-K

ANNUAL REPORT

TABLE OF CONTENTS

|

|

|

|

Page |

PART I |

|

|

|

|

ITEM 1. |

|

|

1 |

|

ITEM 1A. |

|

|

24 |

|

ITEM 1B. |

|

|

58 |

|

ITEM 1C. |

|

|

58 |

|

ITEM 2. |

|

|

59 |

|

ITEM 3. |

|

|

60 |

|

ITEM 4. |

|

|

60 |

|

|

|

|

|

|

PART II |

|

|

|

|

|

|

|

|

|

ITEM 5. |

|

|

61 |

|

ITEM 6. |

|

|

61 |

|

ITEM 7. |

|

Management's Discussion and Analysis of Financial Condition and Results of Operations |

|

62 |

ITEM 7A. |

|

|

71 |

|

ITEM 8. |

|

|

72 |

|

ITEM 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosures |

|

105 |

ITEM 9A. |

|

|

105 |

|

ITEM 9B. |

|

|

105 |

|

ITEM 9C |

|

Disclosures Regarding Foreign Jurisdictions that Prevent Inspections |

|

105 |

|

|

|

|

|

PART III |

|

|

|

|

|

|

|

|

|

ITEM 10. |

|

|

106 |

|

ITEM 11. |

|

|

106 |

|

ITEM 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

106 |

ITEM 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

106 |

ITEM 14. |

|

|

106 |

|

|

|

|

|

|

PART IV |

|

|

|

|

|

|

|

|

|

ITEM 15. |

|

|

107 |

|

ITEM 16. |

|

|

107 |

|

|

|

|

|

|

|

108 |

|||

|

117 |

|||

i

Special Note Regarding Forward-looking Statements and Industry Data

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that are based on our management’s beliefs and assumptions and on information currently available to our management. The forward-looking statements are contained principally in the sections entitled “Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements include information concerning our possible or assumed future cash flow, revenue, sources of revenue and results of operations, cost of product revenue and product margin, operating and other expenses, unit sales and the selling prices of our products, business strategies, financing plans, expansion of our business, investments to expand our customer base, plans for our products, competitive position, industry environment, potential growth opportunities, market growth expectations, the effects of competition, our planned use of the proceeds from the Bridge Loans and Private Placement Issuance described herein, cost structure optimization, acceleration of growth, potential merger and acquisition (M&A) activity and restructuring plans (including expense reduction activities involving potential subleasing and talent relocation plans, modifications to the scope of the company’s proteomic and genomics businesses and discontinuing of certain product lines) and our expectations regarding the benefits and integration of acquired businesses and/or products (including in connection with our merger with SomaLogic, Inc. in January 2024). Forward-looking statements include statements that are not historical facts and can be identified by terms such as “anticipates,” “believes,” “could,” “seeks,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts, “projects,” “should,” “will,” “would,” or similar expressions and the negatives of those terms.

Forward-looking statements involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. We discuss these risks in greater detail in the section entitled “Risk Factors” and elsewhere in this Annual Report on Form 10-K. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

Forward-looking statements represent our management’s beliefs and assumptions only as of the date of this Annual Report on Form 10-K. Except as required by law, we assume no obligation to update these forward-looking statements, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future. You should read this Annual Report on Form 10-K completely and with the understanding that our actual future results may be materially different from what we expect.

This Annual Report on Form 10-K also contains estimates, projections and other information concerning our industry, our business, and the markets for certain of our products, including data regarding the estimated size of those markets. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties and actual events, or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained this industry, business, market, and other data from reports, research surveys, studies, and similar data prepared by market research firms and other third parties, industry, medical and general publications, government data, and similar sources.

Standard BioTools, the Standard BioTools logo, Fluidigm®, the Fluidigm logo, 48.Atlas™, Access Array™, Advanta™, Advanta EASE™, Atlas™, Biomark™, “Bringing new insights to life”™, C1™, Callisto™, Cell-ID™, CyTOF®, CyTOF XT™, the CyTOF XT logo, D3™, Delta Gene™, Direct™, Digital Array™, Dynamic Array™, EP1™, EQ™, FC1™, Flex Six™, Flow Conductor™, FluiDesign™, Helios™, High-Precision 96.96 Genotyping™, HTI™, Hyperion™, Hyperion+™, IMC™, Imaging Mass Cytometry™, Immune Profiling Assay™, Juno™, Maxpar®, MCD™, MSL®, Nanoflex™, Open App™, Pathsetter™, Polaris™, qdPCR 37K™, Script Builder™, Script Hub™, Singular™, SNP Trace™, SNP Type™, “Unleashing tools to accelerate breakthroughs in human health”™, X9™ Real Time PCR System, Xgrade™, SomaLogic®, SomaScan®, SOMAmer®, SomaSignal®, Power by SomaLogic™, DataDelve™, and CardioDM are trademarks or registered trademarks of Standard BioTools Inc. or its affiliates in the United States and/or other countries. Other service marks, trademarks and trade names referred to in this Annual Report on Form 10-K are the property of their respective owners.

Unless the context requires otherwise, references in this Annual Report on Form 10-K to “Standard BioTools,” the “Company,” “we,” “us,” and “our” refer to Standard BioTools Inc. and its subsidiaries.

PART I

ITEM 1. BUSINESS

Overview

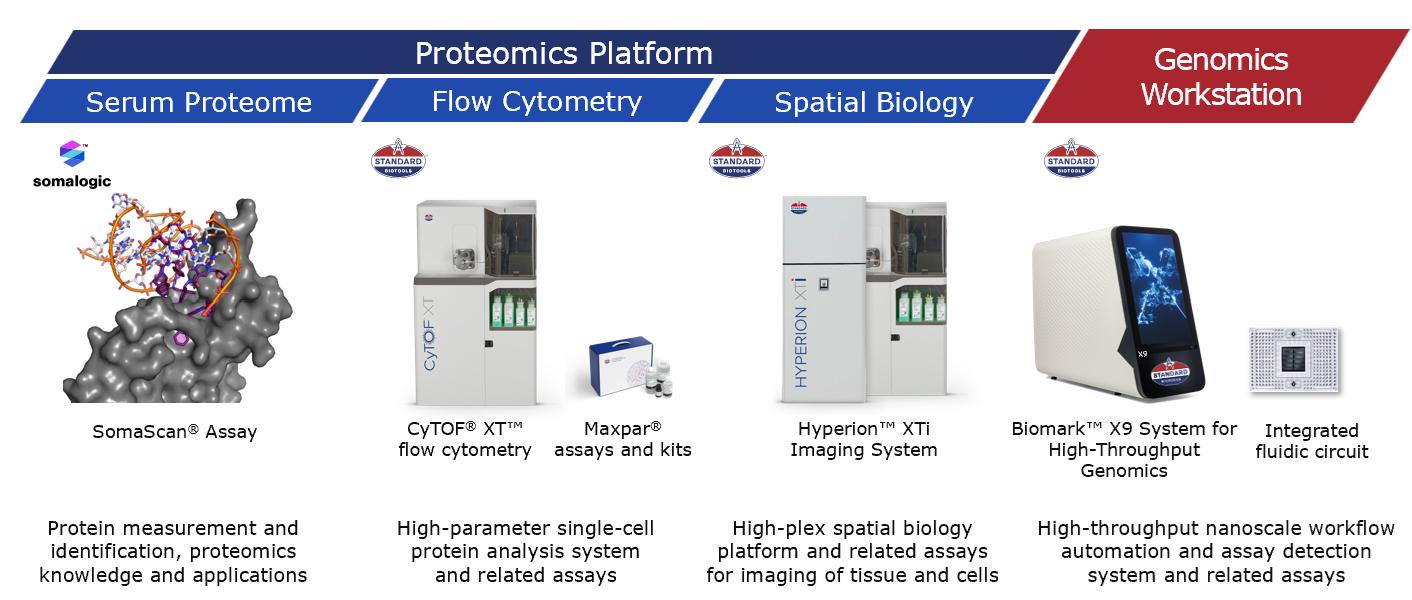

Standard BioTools Inc. is driven by a bold purpose – unleashing tools to accelerate breakthroughs in human health. We develop, manufacture and sell technologies that help biomedical researchers in their search for developing medicines faster and better. Our tools provide insights in health and disease using our proprietary mass cytometry and microfluidics technologies, which serve applications in proteomics and genomics, respectively.

Within proteomics our mass cytometry technology is embodied in two analytical platforms: flow cytometry and tissue imaging or spatial biology. Our flow cytometry systems (Helios™ and CyTOF XT) deeply profile cell phenotype and function. Referenced by more than 2,200 peer-reviewed publications around the world, our CyTOF technology has set a new standard in human immune profiling with our proprietary digital readout. Our spatial biology systems (Hyperion™ Imaging System and Hyperion+TM Imaging System) enable highly multiplexed protein biomarker detection at a single cellular level in tissues and tumors while still preserving tissue architecture and cellular morphology information and without any autofluorescence artifacts by using our Imaging Mass Cytometry™ (IMC™) technology.

Within genomics, our microfluidics technology with our proprietary Integrated Fluidic Circuits (IFCs) provides high throughput and automated workflows for quantitative polymerase chain reaction (PCR), gene expression, copy number variation analysis, and next-generation sequencing (NGS) library preparation. These automated systems are used to detect somatic and genomic variations from a range of different sample types which provide cost efficiencies, flexibility and proven analytical performance that customers need to meet the increasing demands of molecular biomarker analysis for diagnostics and research applications.

On January 5, 2024, we completed the merger (the Merger) with SomaLogic, Inc. (SomaLogic), creating a leading provider of differentiated multi-omics tools for research.

Strategic Investment Transaction and Business Restructuring

On April 1, 2022, our stockholders approved the closing of a private placement of preferred stock to Casdin Private Growth Equity Fund II, L.P. and Casdin Partners Master Fund, L.P. (collectively, Casdin) and Viking Global Opportunities Illiquid Investments Sub-Master LP and Viking Global Opportunities Drawdown (Aggregator) LP (collectively, Viking and together with Casdin, the Purchasers). On the closing date, April 4, 2022, we sold an aggregate of $225.0 million worth, and converted $25.0 million of previously issued bridge loans (the Bridge Loans), into shares of Series B-1 Convertible Preferred Stock and Series B-2 Convertible Preferred Stock pursuant to separate Series B Convertible Preferred Stock Purchase Agreements, dated and effective as of January 23, 2022, with each of the Purchasers (the Private Placement Issuance). The $250.0 million proceeds from the Bridge Loans and Private Placement Issuance are being used for working capital and general corporate purposes. On the closing date, the stockholders also approved the name change of our company to “Standard BioTools Inc.”

In connection with the closing of the private placement, Dr. Michael Egholm was appointed President and Chief Executive Officer and Alex Kim as Chief Operating Officer of the Company. Between April 2022 and today, Mr. Egholm has rebuilt our entire executive leadership team, assembling a team of disciplined operators that we believe can execute our vision to become a diversified leader in life sciences tools. Collectively, the Standard BioTools executive leadership team has over 140 years of combined life sciences experience. We have also reconstituted our board of directors since early 2022, adding significant life sciences operating, technology and capital markets expertise. In only seven quarters since the initiation of our restructuring plans in April 2022, our new management has significantly improved our legacy business performance, as demonstrated by the results of the fiscal year ended December 31, 2023 during which revenues increased 9% year-to-year (including over 40% growth in instrument revenue), gross margins expanded by more than 25% year-to-year, operating expenses declined by approximately 17% year-to-year, and operating cash burn declined by 53% year-to-year.

Merger With SomaLogic, Inc.

On January 5, 2024, we completed the Merger with SomaLogic and Martis Merger Sub, Inc., a Delaware corporation and direct wholly owned subsidiary of the Company (Merger Sub), pursuant to which, at the effective time of the Merger (the Effective Time), among other matters, Merger Sub merged with and into SomaLogic, with SomaLogic surviving as a wholly owned subsidiary of the Company. Upon the terms and subject to the conditions set forth in that certain Agreement and Plan of Merger, dated as of October 4,

1

2023, by and between the Company, SomaLogic and Merger Sub (the Merger Agreement), at the Effective Time, each share of SomaLogic common stock, par value $0.0001 per share (SomaLogic Common Stock), converted into the right to receive 1.11 shares (the Exchange Ratio) of the Company’s common stock, par value $0.001 per share.

SomaLogic is catalyzing drug research and development and biomarker identification as a global leader in proteomics technology. With a single 55 microliter plasma or serum sample, SomaLogic can run 11,000 protein measurements, covering more than a third of the approximately 20,000 proteins in the human body and twice as many as other proteomic platforms. For more than 20 years SomaLogic has supported pharmaceutical companies, and academic and contract research organizations who rely on SomaLogic’s protein detection and analysis technologies to fuel drug, disease, and treatment discoveries in such areas as oncology, diabetes, and cardiovascular, liver and metabolic diseases.

The combination of Standard BioTools and SomaLogic represents an opportunity for the combined company to leverage this operational expertise and discipline to achieve cost synergies for the combined company and to create new revenue opportunities with the combined platform, which we believe will inure to the benefit of our customers and create long-term value for the combined company’s stockholders.

Including expected acquired cash and investments, the combined company had a balance of approximately $565.5 million of cash, cash equivalents, short-term investments and restricted cash at December 31, 2023, which amount includes SomaLogic’s unaudited cash, cash equivalents and short-term investments of $449.8 million as of December 31, 2023. For the year ended December 31, 2023, the combined company had pro forma revenue of $192.4 million, which amount includes SomaLogic’s unaudited 2023 revenue of $86.1 million. The preliminary combined company cash and revenue included in this Form 10-K has been prepared by, and is the responsibility of, Standard BioTools’ management. PricewaterhouseCoopers LLP has not audited, reviewed, examined, compiled, nor applied agreed-upon procedures with respect to the preliminary financial data. Accordingly, PricewaterhouseCoopers LLP does not express an opinion or any other form of assurance with respect thereto.

The disclosures in this Item 1 of this Annual Report on Form 10-K (the Annual Report) under the heading “Business” speak to the combined company subsequent to the Merger unless otherwise noted. However, the financial results described herein relate, except as otherwise expressly noted herein, to Standard BioTools on a standalone basis without to giving effect to Merger and, accordingly, do not include the results of SomaLogic. Future filings, beginning with our Quarterly Report on Form 10-Q for the fiscal quarter ending March 31, 2024, will reflect the results of the combined company.

Strategy

Our new leadership team has identified three strategic priorities: revenue growth, improving operating discipline through the Standard BioTools Business Systems (SBS) and strategic capital allocation.

Revenue Growth

One of our top priorities is to grow our instrument, consumables and service revenue. We have established new growth strategies for our product lines, returning our business to growth in 2023. This growth has been driven by over 40% increase in instrument revenue, led by new placements of our Hyperion XTi Imaging System, which we launched in April 2023. Importantly, we believe growth in instrument placements is a leading indicator. And while we expect to see continued variability in quarter-to-quarter instrument placements, the growing installed base expands future consumables and service pull-through, which are significant drivers of both revenue and margin growth.

We continue to invest in research and development (R&D) to create and launch new products and have adopted best practice approaches to improve our lead generation and funnel management growth, among other things.

Improving Operating Discipline Through SBS

Our second priority is to improve our operating discipline through the implementation of SBS. We are leveraging SBS with a set of organizing principles, rigorous standard work processes, and a continuous improvement mindset to build more efficient operations and commercial execution and reduce costs.

Following the closing of our private placement described above, we implemented a phased restructuring plan designed to improve efficiencies, expand gross margins, reduce operating costs and better align our workforce with the current needs of our business.

Key highlights of our restructuring initiatives have included:

2

Strategic Capital Allocation

Our third priority is strategic capital allocation. We are actively pursuing business development opportunities in the life sciences industry with consolidation and synergies expected to be a key growth driver to sustain the longer-term value proposition of the Company. The merger with SomaLogic is our latest step forward toward unlocking value in a highly fragmented market through scale, diversification and operational expertise.

Market Opportunity

We participate in growing and emerging market segments within the broader proteomics and genomics markets.

Proteomics

The market for proteomics is broadly defined as instruments, consumables and reagents, software, and services for all technologies used in the identification of proteins. Proteins perform a vast array of functions within living organisms, including catalyzing metabolic reactions, replicating DNA, signaling response to stimuli and transporting molecules from one location to another. The proteome varies and is dynamic. Every cell in an individual organism has the same set of genes, but the set of proteins produced in different tissues differ from one another and are dependent on gene expression. Protein analysis is required to profile and understand cellular function as well as the interaction in tissues and other complex microenvironments. Within the proteomics market, we focus on Flow Cytometry and Spatial Biology.

Flow Cytometry is a method to detect and measure physical and chemical characteristics of cells or particles. With our CyTOF technology, we focus in a smaller sub-segment of Flow Cytometry for high-parameter analysis defined as greater than 20 parameters.

Spatial Biology, which itself is a sub-segment of the broader Tissue Image Analysis market that includes immunohistochemistry and in-situ hybridization, is the study of single cells in its spatial context to understand the role of heterogeneity in cell function and assess complex phenotypes and tumor-immune interactions in the tissue and tumor microenvironment.

3

Genomics

The market for genomics is broadly defined as instruments, consumables and reagents, software, and services for all technologies used in the identification of genes (DNA, RNA) and their function. The hereditary material or nucleic acid of an organism is often referred to as its genome, the protein-encoding regions of which are commonly known as genes. Analysis of variations in genomes, genes and gene activity in and between organisms can provide insights into their health and functioning.

Within the genomics market, we focus on two sub-segments: qPCR analysis and NGS library preparation.

There are several forms of genetic analysis in use today, including genotyping, gene expression analysis and NGS:

OEM Markets

We also utilize our proprietary microfluidics technology to collaborate with OEM providers to pursue market opportunities outside our core markets. These OEM markets are highly varied, and we believe represent significant expansion opportunities for our technology.

Products

We market life science tools, including preparatory and analytical instruments, consumables, and software for single cell proteomics analysis via mass cytometry and tissue imaging, and protein detection and analysis technologies and services for genomics analysis via real-time PCR and NGS library preparation.

4

Throughout 2022 and 2023, we have greatly enhanced our proteomics offerings through continuous quality improvements and targeting of our flagship flow cytometry instrument, the CyTOF XT™ System, and the commercial release of our third-generation imaging solution for spatial biology, the Hyperion XTi™ Imaging System.

We have begun to more clearly distinguish the technological and workflow advantages of our flow cytometry solution. The CyTOF XT is the only technology that can do a high number of both extra cellular markers and intra cellular markers. The ability to do both at the same time allows our customers to gain biological insights that would otherwise go unnoticed using competing technologies.

Since the commercial launch of the Hyperion XTi™ Imaging System in the second quarter of 2023, the system’s market-leading data quality and throughput continue to be very well-received, and we believe early customer feedback suggests that it is the strongest contender in the emerging field of spatial biology for translational research.

In addition, at the end of 2022, we completed the strategic repositioning of our microfluidics, or genomics, business, consolidating the portfolio to a single commercially available instrument, the Biomark X9, which combines the functionality of the Juno and the Biomark HD with improved workflow and performance. The Juno and Biomark HD are still available to legacy customers under certain circumstances. We continued to deliver the Signature Q100 microfluidics platform to our OEM collaborator, Olink Holding AB.

As discussed above, on January 5, 2024, we completed the Merger with SomaLogic, a global leader in proteomics technology. With a single 55 microliter plasma or serum sample, SomaLogic can run 11,000 protein measurements, covering more than a third of the approximately 20,000 proteins in the human body and twice as many as other proteomic platforms. For more than 20 years, SomaLogic has supported pharmaceutical companies, and academic and contract research organizations who rely on SomaLogic’s protein detection and analysis technologies to fuel drug, disease and treatment discoveries in such areas as oncology, diabetes, and cardiovascular, liver and metabolic diseases.

Standard BioTools offers a comprehensive suite of multi-omics technologies.

Our primary instrument offerings are summarized in the table below:

Product |

|

Product Description |

|

Applications |

Single Cell Proteomics |

|

|

|

|

|

|

|

|

|

Analytical Systems: |

|

|

|

|

|

|

|

|

|

CyTOF XT™ System |

|

The CyTOF XT mass cytometry system performs highly automated high-parameter (>50) single-cell analysis using antibodies conjugated to metal isotopes. |

|

Flow Cytometry |

|

|

|

|

|

Hyperion XTi™ Imaging System |

|

Our third-generation spatial biology instrument, the Hyperion XTi™ Imaging System brings together |

|

Tissue Imaging |

5

Product |

|

Product Description |

|

Applications |

|

|

imaging capability with proven high-parameter mass cytometry technology to enable the simultaneous detection of up to 40 protein markers in the spatial context of the tissue microenvironment. |

|

|

|

|

|

|

|

Genomics |

|

|

|

|

|

|

|

|

|

Analytical and Preparatory Instruments: |

|

|

||

|

|

|

|

|

X9TM Real-Time PCR System |

|

Real-time PCR analytical instrument, including pre-processing steps for microfluidics-based workflows using IFCs. |

|

Real-time PCR analysis |

|

|

|

|

|

BiomarkTM HD System |

|

Real-time PCR analytical instrument for microfluidics-based workflows using prepared IFCs. |

|

Real-time PCR analysis |

|

|

|

|

|

IFC Controllers (HX, MX, and RX) |

|

Each controller is designed to work with specific IFC formats: (i) IFC Controller MX- for priming and loading the 48.48 Dynamic ArrayTM IFC, the 12.765 Digital ArrayTM, IFC, the 48.770 Digital Array IFC, and qdPCR 37KTM , (ii) IFC Controller HX- for priming and loading the Flex SixTM Gene Expression IFC and Flex Six Genotyping IFC, 96.96 Dynamic Array IFC, (iii) IFC Controller RX- for loading the 192.24 Gene Expression IFC, 192.24 Genotyping IFC, and the 24.192 Dynamic Array IFC for gene expression. |

|

Real-time PCR analysis |

|

|

|

|

|

Integrated Fluidic Circuits

Our IFCs incorporate several different types of technology that together enable us to use multi-layer soft lithography (MSL) technology to rapidly design and deploy new microfluidic applications with state-of-the-art commercial manufacturing processes. The first level of our IFC technology is a library of components that perform basic microfluidic functions, such as pumps, mixers, single-cell capture chambers, separation columns, control logic, and reaction chambers. The second level of our IFC technology comprises the architectures we have designed to exploit our ability to conduct thousands of reactions on a single IFC. The third level of our IFC technology involves the interaction of our IFCs with the actual laboratory environment.

Instrumentation and Software

Our mass cytometry instrumentation technology includes a custom-designed inductively coupled plasma ion source, ion-optical and vacuum systems, and instrument control electronics. With our CyTOF systems, individual cells are atomized, ionized, and extracted. A time-of-flight mass analyzer separates atomic ions of different mass-to-charge ratios, providing information on temporal distribution of ions. Our Imaging Mass Cytometry systems combine mass cytometry technology with imaging capability to enable simultaneous interrogation of up to 50 protein markers in the spatial context of the tissue microenvironment. Our systems have the ability to utilize up to 135 channels to detect additional parameters to meet future market needs.

Our microfluidics-based X9 Real-Time PCR system includes our custom thermal cycler, a sophisticated fluorescence imaging system, and on-board scripting and protocol control software, and utilizes our IFC technology for a wide range automated genomics applications.

We also offer specialized software to manage and analyze the unusually large amounts of data produced by our systems. We offer Cytobank, our cloud-based platform of analytical tools, FCS Express7 Flow, and Maxpar Pathsetter data analysis packages for use with the CyTOF systems. For our Imaging Mass Cytometry platform, Hyperion, we offer various state of the art software packages to enable data analysis from basic to translational research: CyTOF Software 7.0, MCD Viewer, histoCAT, Visiopharm Phenomap and Indica Lab Halo. Our bioinformatic toolset, the Singular software, facilitates the analysis and visualization of single-cell gene expression data. More recently, we extended the scope of the toolset to include DNA analysis tools.

6

Assays and Reagents

We manufacture over 800 metal-conjugated antibodies for use with our mass cytometry and Imaging Mass Cytometry instruments to allow detection of up to 48 protein targets simultaneously in a single cell for a total of more than 50 detected cellular parameters. Our metal-conjugated antibodies are manufactured using metal-chelating polymers, which are produced using proprietary polymerization processes and subsequent post-polymerization modifications.

Our genotyping and single nucleotide polymorphism type (SNP Type) assay products consist of assay design and custom content delivery systems for gene expression and genotyping, respectively. These offerings provide low-cost alternatives to other available chemistries and allow customers to use IFCs in more flexible ways with validated assays for their targets of interest.

SomaLogic® Offerings and Applications

Effective with the closing of our Merger on January 5, 2024, our SomaLogic offering consists primarily of a service model whereby we receive samples (including from pharmaceutical, biotechnology or academic clients), perform the SomaScan® assay, and subsequently use bioinformatics and analytics to further refine the collected data and deliver the results back to the customer.

SomaScan® Assay

As of January 5, 2024, the SomaScan® assay measures approximately 11,000 protein targets in a single sample. The SomaScan® assay is designed to have breadth (or number of proteins measured), precision, specificity, dynamic range, depth (or lower limits of detection), and throughput. SomaScan® assay customers can also gain access to individual SOMAmer® reagents for a wide range of follow-up studies, which is a feature we consider to be a unique addition to our research services in comparison to the offerings of other proteomic platforms. The SomaScan 11K Platform is the largest proteomics offering available on the market.

SomaScan® Certified Sites

The SomaScan Certified Sites program allows global pharmaceutical and biotech companies, academic and core labs, and government research institutions to run our industry leading proteomics platform on site with the same precision, robustness, and reproducibility seen in our assay services facility. Certified Sites run the assay on the same equipment as in the SomaLogic Assay Service facility utilizing a reagent based kit. As of January 4, 2024, we had 17 Certified Sites, utilizing the SomaScan Assay kits.

SomaSignal™ Tests

As of January 5, 2024, we had 15 SomaSignal™ tests currently available for use as laboratory developed tests (LDTs) under our CLIA certification, with several more in various stages of development. As of January 5, 2024, we had 29 RUO tests primarily targeting clinical trial applications, such as characterizing and monitoring patients through the clinical trial cycle. We believe our SomaSignal™ tests will provide health systems and national health services with a leading-edge scientific tool set to allocate resources, risk stratify both populations and individual patients and personalize therapy.

SOMAmer® Reagents

Customers have been granted licenses to use a limited subset of our SOMAmer® reagents and to access to our Systematic Evolution of Ligands by Exponential enrichment (“SELEX”) technology in three ways: (i) through the transfer of individual reagents that have been developed by SomaLogic, (ii) through the transfer of custom reagents developed by SomaLogic on behalf of a customer, and (iii) through the development of custom reagents by a customer after receiving a license to perform the SELEX process and to use the subsequently developed reagents. An example of the commercial use of SOMAmer® reagents by a licensee of SomaLogic is the inclusion of SOMAmer® reagent-based inhibitors of thermophilic enzymes, such as polymerases used in a product category offered by certain biotechnology companies referred to as “hot-start” PCR amplification.

7

Customers

We sell our instruments and consumables for research use only (RUO) to leading academic research institutions, translational research and medicine centers, cancer centers, clinical research laboratories, and biopharmaceutical, biotechnology, and plant and animal research companies. One genomics customer accounted for 10% and 11% of our total revenue for the years ended December 31, 2023 and 2022, respectively.

Marketing, Sales, Service and Support

We distribute our systems through our direct sales force and support organizations located in North America, Europe, and Asia-Pacific, and through distributors or sales agents in European, Latin American, Middle Eastern, and Asia-Pacific countries. Our sales and marketing efforts are targeted at laboratory directors and principal investigators at leading academic, translational research, healthcare consortiums, and biopharmaceutical companies who need reliable life science automation solutions to power their disease research with the goal of providing actionable insights.

Our sales process often involves numerous interactions and demonstrations with multiple people within an organization. Some potential customers conduct in-depth evaluations of the system, including running experiments on our system and competing systems. In addition, in most countries, sales to academic or governmental institutions require participation in a tender process involving preparation of extensive documentation and a lengthy review process. As a result of these factors and the budget cycles of our customers, our sales cycle, the time from initial contact with a customer to our receipt of a purchase order, can often be 12 months or longer.

Manufacturing

Our manufacturing operations are located in Singapore and Canada. Our facility in Singapore manufactures IFCs and assemblies of microfluidics instruments. In 2022, assembly of microfluidics instruments was insourced to our Singapore facility to reduce cost and improve product quality. All of our IFCs for commercial sale and some IFCs for our research and development purposes are also fabricated at our Singapore facility. Our mass cytometry instruments and reagents for commercial sale, as well as for internal research and development purposes, are manufactured at our facility in Canada. Our genomics reagent manufacturing was transferred from South San Francisco to Markham, Canada in late 2022.

Additionally, in connection with the Merger we acquired additional manufacturing operations in Boulder, Colorado. Our facility in Boulder manufactures reagents, SomaScan® assay kits, and other consumables used to run SomaScan® assays.

We rely on a limited number of suppliers for certain components and materials used in our products. Key components in Standard BioTools legacy products and SomaLogic products are supplied by sole or limited source suppliers. The loss of a single or sole source supplier would require significant time and effort to locate and qualify an alternative source of supply, if at all, and could adversely impact our business. For additional information, please refer to “Item 1A. Risk Factors.”

Laboratory Operations

We perform all of our SomaSignalTM tests in our laboratory facility located in Boulder, Colorado. Our laboratory is certified under the Clinical Laboratory Improvement Amendments of 1988 (CLIA) and accredited by the College of American Pathologists (CAP). Our laboratory is certified for performance of high-complexity testing by the Centers for Medicare & Medicaid Services (CMS) in accordance with the Clinical Laboratory Improvement Amendments of 1988 (CLIA) and is licensed by certain other states requiring out-of-state licensure including California, Maryland, Pennsylvania and Rhode Island.

We believe that our existing laboratory facility is adequate to meet our business needs for at least the next 12 months and that additional laboratory space will be available on commercially reasonable terms, if required.

Quality Assurance

Our quality assurance function oversees the quality of our laboratory operations. We have established oversight for systems implementation and maintenance procedures, document control processes, supplier qualification, preventive or corrective actions and employee training processes that we believe achieves excellence in operations. We continuously monitor and improve our processes and procedures and believe this high-quality service leads to customer satisfaction and retention.

8

Research and Development

We have assembled experienced research and development teams at our South San Francisco, California, Markham, Ontario, Canada, and Singapore locations and have the scientific, engineering, software, bioinformatic, and process talent that we believe is required to grow our business.

The largest components of our current research and development efforts are in the areas of new products, new applications and new content. We launched our Hyperion Imaging System in October 2017. The Hyperion Imaging System provides spatial resolution of protein expression in complex tissue samples at the single-cell level, quantitative measurement using metal isotope tags, and analysis of up to 40 proteins, while having 135 channels available. We also developed metal-labeled antibodies compatible with formalin fixed paraffin embedded tissue samples, to be used with the Hyperion Imaging System. In 2022 we launched the Hyperion+ Imaging System, our second-generation imaging platform.

In 2019, we launched the Maxpar Direct Immune Profiling Assay, a sample-to-answer workflow for comprehensive human immune profiling for use with our CyTOF systems, which puts pre-titrated antibodies in dry format in a single tube, with automated software that provides data analysis in as few as five minutes. This assay is reproducible from site-to-site and lot-to-lot, which is important for translational and pharma/biotech research work. We have collaborated with industry partners to enable workflows and software for the Hyperion and CyTOF systems. Also in 2019, we added seven new metal antibody labels, becoming the first company to enable 50-plex cytometry panels, and launched three Imaging Mass Cytometry panel kits as well as CyTOF Software v7.0, an updated CyTOF software application.

In May 2021, we launched the new, fourth generation cell suspension mass cytometry system, CyTOF XT. Its main features include automation of sample introduction and acquisition, and lower cost of ownership and enhanced performance in resolution of cell populations. The system enables storage of pelleted samples in the cooled autosampler, automated resuspension of pellets, and addition of beads standards.

We also invest significantly in research and development efforts to expand our microfluidics applications. For example, we continue to develop and commercialize various panel sets for use with our systems. In 2017, we successfully launched the Advanta™ Immuno-Oncology Gene Expression Assay, which is a 170-gene expression qPCR assay that enables profiling of tumor immunobiology and new biomarker identification. In 2019, we launched the Advanta™ RNA-Seq NGS Library Prep Kit. Designed to drive significant improvement in the RNA-seq workflow, the Advanta RNA-Seq NGS Library Prep Kit together with the Juno™ system delivers an integrated solution for automated, cost-efficient NGS library prep. In 2020, we expanded our microfluidics franchise to develop products for the COVID-19 testing marketplace and we launched the AdvantaDx SARS-CoV-2 RT-PCR assay. These COVID-19 related products were discontinued in 2022.

In 2022, we launched the X9 Real Time PCR System: a next-generation system platform that integrates all the features of all our legacy platforms into one ultra-compact footprint with a simple-to-operate user interface. In addition, we secured significant development collaborations, including for development of OEM systems using our microfluidics technology.

The second component of our research and development effort is to continuously develop new manufacturing processes and test methods to drive down manufacturing costs, increase manufacturing throughput, widen fabrication process capability, and support new microfluidic devices and designs.

Additionally, in connection with the Merger we acquired research and development facilities in Boulder, Colorado and La Jolla, California. These facilities are focused on the discovery of protein biomarkers and the development of slow off-rate modified aptamers (SOMAmers®), which are modified nucleic acid-based protein binding reagents that are specific for their cognate proteins. The facility in La Jolla is specifically focused on creating small-mid plex solutions for SOMAmer® technology that will enable SomaLogic products to serve additional market segments.

We expect some synergies to be achieved in research and development activities as the combined company shares certain resources; however, the research and development efforts of SomaLogic and Standard BioTools will continue to operate independently for the foreseeable future, with primarily the same teams that were in place prior to the Merger.

Competition

The life science markets are highly competitive and expected to grow more competitive with the increasing knowledge gained from ongoing research and development. We believe that the principal competitive factors in our target markets include quality of product, cost of capital equipment and supplies; reputation among customers; innovation in product offerings; flexibility and ease of use; accuracy

9

and reproducibility of results; competition for human resources; and compatibility with existing laboratory processes, tools, and methods.

We compete with both established and development stage life science companies that design, manufacture, and market instruments for gene expression analysis, genotyping, other nucleic acid detection, protein expression analysis, imaging, and additional applications. In addition, a number of other companies and academic groups are in the process of developing novel technologies for life science markets. Many of our competitors enjoy several competitive advantages over us, including significantly greater name recognition; greater financial and human resources; broader product lines and product packages; larger sales forces and e-commerce channels; larger and more geographically dispersed customer support organizations; substantial intellectual property portfolios; larger and more established customer bases and relationships; greater resources dedicated to marketing efforts; better established and larger scale manufacturing capability; and greater resources and longer experience in research and development. For additional information, please refer to “Item 1A. Risk Factors.”

To successfully compete with existing products and future technologies, we need to demonstrate to potential customers that the performance of our technologies and products, the solutions we provide our customers, as well as our customer support capabilities, are superior to those of our competitors.

Intellectual Property

Patents

We have developed a portfolio of issued patents and patent applications directed towards commercial products and technologies in development. As of December 31, 2023, we owned or licensed approximately 400 patents and had over 175 pending patent applications worldwide. Our utility patents have expiration dates ranging up to year 2039, and our design patents have expiration dates ranging up to year 2047.

As of December 31, 2023, SomaLogic owned or licensed more than 660 patents and had approximately 435 pending patent applications worldwide. SomaLogic's utility patents have expiration dates ranging up to year 2043.

License Agreements

We have entered into licenses for technologies from various companies and academic institutions.

Genomics Technologies. Our core genomics technology originated at the California Institute of Technology (Caltech) in the laboratory of Professor Stephen Quake, who is a co-founder of Fluidigm (now Standard BioTools Inc.). We license genomics technology from Caltech, Harvard University, and Caliper Life Sciences, Inc. (Caliper), now a PerkinElmer company.

Proteomics. Some of the intellectual property rights covering our mass cytometry products were subject to a license agreement (the Original License Agreement) between Fluidigm Canada Inc. (now Standard BioTools Canada Inc.), and PerkinElmer Health Sciences, Inc. (PerkinElmer). Under the Original License Agreement, Fluidigm Canada Inc, received an exclusive, royalty bearing, worldwide license to certain patents owned by PerkinElmer in the field of inductively coupled plasma (ICP)-based proteomics, including the analysis of elemental tagged materials in connection therewith (the Patents), and a non-exclusive license for reagents outside the field of ICP-based mass cytometry. In November 2015, we entered into a patent purchase agreement with PerkinElmer pursuant to which we purchased the Patents for a purchase price of $6.5 million and a patent assignment agreement pursuant to which PerkinElmer transferred and assigned to us all rights, title, privileges, and interest in and to the Patents and the Original License Agreement. Accordingly, we have no further financial obligations to PerkinElmer under the Original License Agreement. Contemporaneously with the purchase of the Patents, we entered into a license agreement with PerkinElmer pursuant to which we granted PerkinElmer a worldwide, non-exclusive, fully paid-up license to the Patents in fields other than (i) ICP-based mass analysis of atomic elements associated with a

10

biological material, including any elements that are unnaturally bound, directly or indirectly, to such biological material (Mass Analysis) and (ii) the development, design, manufacture, and use of equipment or associated reagents for such Mass Analysis. The license will terminate on the last expiration date of the Patents, currently expected to be in November 2026, unless earlier terminated pursuant to the terms of the license agreement.

InstruNor AS. In January 2020, we completed the acquisition of InstruNor AS (InstruNor) for $7.2 million, including $5.2 million in cash and $2.0 million in stock. InstruNor provided automated sample preparation solutions for proteomics and flow cytometry instrument markets and became part of Standard BioTools Inc.’s proteomics business. Included in this acquisition were certain intellectual property portfolio assets comprised of patents and/or patent applications directed to various aspects of automated cell pretreatment instruments. The expiration dates for the issued patents in this patent portfolio extended to March 2033. We recognized a $3.5 million impairment charge on InstruNor’s developed technology intangible asset in the second quarter of 2022 related to our discontinued Flow Conductor product line.

Any loss, termination, or adverse modification of our licensed intellectual property rights could have a material adverse effect on our business, operating results, and financial condition. For additional information, please refer to “Item 1A. Risk Factors.”

Other

In addition to pursuing patents and licenses on key technologies, we have taken steps to protect our intellectual property and proprietary technology by entering into confidentiality agreements and intellectual property assignment agreements with our employees, consultants, OEM counterparties and collaborators and, when needed, our advisers.

Government Regulation

We are subject to a variety of laws and regulations in the United States, the European Union and other countries. The level and scope of the regulation varies depending on the country or defined economic region, but may include, among other things, the research, development, testing, clinical trials, manufacture, storage, recordkeeping, marketing authorization, labeling, safety, efficacy, packaging, advertising, promotion and commercial sales and distribution, of many of our products.

Clinical Laboratory Improvement Amendments of 1988

We are required to hold certain federal, state and local licenses, certifications and permits to operate our clinical laboratory facility in Boulder, Colorado, including the performance of certain diagnostic assays. Under CLIA, we are required to hold a certificate applicable to the categories of laboratory tests we perform and to comply with standards applicable to our operations, including test processes, personnel, facilities administration, equipment maintenance, recordkeeping, quality systems and proficiency testing. We must maintain CLIA certification to be eligible to bill for diagnostic services provided to Medicare beneficiaries. Many commercial third-party payors also require CLIA certification as a condition of payment.

Our Boulder facility holds a current CLIA certificate. To renew our CLIA certificate, we are subject to survey and inspection every two years to assess compliance with program standards. We elect to participate in the accreditation program of CAP. CMS has deemed CAP standards to be equally or more stringent than CLIA regulations and has approved CAP as a recognized accrediting organization. Inspection by CAP is performed in lieu of inspection by CMS for CAP-accredited laboratories. Because we are accredited by the CAP Laboratory Accreditation Program, we are deemed to also comply with CLIA. The regulatory and compliance standards applicable to the testing we perform may change over time, and any such changes could have a material effect on our business.

Penalties for non-compliance with CLIA or CAP requirements include suspension, limitation or revocation of the laboratory’s CLIA or CAP certificate, as well as a directed plan of correction, state on-site monitoring, civil money penalties, civil injunctive suit or criminal penalties, as applicable.

State Laboratory Licensing

Our Boulder facility also holds a state license issued by the Colorado Department of Public Health and Environment (CDPHE). Colorado law and regulations establish standards for the day-to-day operation of a clinical laboratory, including the training and skills required of laboratory personnel and quality control.

Federal Oversight of Laboratory Developed Tests and Certain Devices

11

The laws and regulations governing the marketing of diagnostic products are evolving, extremely complex, and in many instances, there are no significant regulatory or judicial interpretations of these laws and regulations. We perform our diagnostic tests like the SomaSignal™ assays in our Boulder, Colorado CLIA-certified and CAP-accredited clinical laboratory, and we believe such tests are primarily regulated under CLIA, as administered by CMS, as well as by applicable state laws, as described above. The FDA regulates any diagnostic tests that meet the definition of a medical device, except under specific, narrow circumstances. The Federal Food, Drug and Cosmetic Act (FDCA) defines a medical device as "an instrument, apparatus, implement, machine, contrivance, implant, in vitro reagent, or other similar or related article, including a component part, or accessory, which is, among other things: intended for use in the diagnosis of disease or other conditions, or in the cure, mitigation, treatment, or prevention of disease, in man or other animals and which does not achieve its primary intended purposes through chemical action within or on the body of man or other animals and which is not dependent upon being metabolized for the achievement of any of its primary intended purposes." By this definition, in vitro reagents and diagnostic tests are considered medical devices. Specifically, the FDA defines an in vitro diagnostic test (IVD), as "reagents, instruments, and systems intended for use in the diagnosis of disease or other conditions, including a determination of the state of health, in order to cure, mitigate, treat, or prevent disease or its sequelae." Therefore, the FDA generally considers diagnostic testing products like ours to be IVDs subject to the agency's regulatory requirements.

Among other things, pursuant to the FDCA and its implementing regulations, the FDA regulates the research, testing, manufacturing, safety, labeling, storage, recordkeeping, pre-market clearance or approval, marketing and promotion and sales and distribution of medical devices, including IVDs, in the United States to ensure that medical products distributed domestically are safe and effective for their intended uses. In addition, the FDA regulates the export of medical devices manufactured in the United States to international markets. Many of the instruments, reagents, kits or other consumable products used within our laboratory facility are regulated as medical devices and therefore must comply with FDA quality system regulations and certain other device requirements. We have policies and procedures in place to ensure that we source such materials from suppliers that are in compliance with any applicable medical device regulatory requirements.

The FDCA classifies medical devices into one of three categories based on the risks associated with the device and the level of control necessary to provide reasonable assurance of safety and effectiveness. Devices deemed by the FDA to pose the greatest risk, such as life-sustaining, life-supporting or implantable devices or devices deemed not substantially equivalent to a previously 510(k) cleared device, are categorized as class III. These devices typically require submission and approval of a premarket approval application (PMA). Devices deemed to pose lower risk are categorized as either class I or II. For most class II devices, a manufacturer must submit to the FDA a 510(k) premarket notification submission requesting clearance of the device for commercial distribution in the United States. However, some low-risk class II devices are exempted from this requirement. When a 510(k) premarket notification submission is required, the manufacturer must submit to the FDA a premarket notification submission demonstrating that the device is "substantially equivalent" to a predicate device, which is: (i) a device that was legally marketed prior to May 28, 1976, for which PMA approval is not required, (ii) a legally marketed device that has been reclassified from class III to class II or class I, or (iii) another legally marketed, similar device that has been cleared through the 510(k) clearance process. Class II devices may also be subject to special controls such as performance standards, post-market surveillance, FDA guidelines, or particularized labeling. Most class I devices are exempt from 510(k) premarket notification requirements, but like class II and III devices, are subject to general controls, such as registration and listing, quality system, labeling, and reporting requirements.

After the FDA permits a device to enter commercial distribution, numerous regulatory requirements apply. These include: the Quality System Regulation, which requires manufacturers to follow elaborate design, testing, control, documentation and other quality assurance procedures during the manufacturing process; labeling regulations; the FDA’s general prohibition against promoting products for unapproved or "off-label" uses; and the medical device reporting regulation, which requires that manufacturers report to the FDA if their device may have caused or contributed to a death or serious injury or malfunctioned in a way that would likely cause or contribute to a death or serious injury if the malfunction were to recur. The FDA has broad post-market and regulatory and enforcement powers. Failure to comply with the applicable U.S. medical device regulatory requirements could result in, among other things, warning letters, fines, injunctions, consent decrees, civil penalties, repairs, replacements, refunds, recalls or seizures of products, total or partial suspension of production, the FDA’s refusal to grant future premarket clearances or approvals, withdrawals or suspensions of current product applications, and criminal prosecution.

In February 2022, we were granted an Emergency Use Authorization (EUA) for our the Advanta Dx COVID-19 EASE Assay, which was authorized for the qualitative detection of nucleic acid from SARS-CoV-2 in nasopharyngeal swab, oropharyngeal swab, mid-turbinate nasal swab, and anterior nasal swab specimens from individuals suspected of COVID-19 by their healthcare provider. Subsequently, in February 2023, the FDA granted our request to withdraw the EUA for our Advanta Dx SARS-CoV-2 RT-PCR Assay. We submitted our request to withdraw such EUA as we had discontinued commercial distribution of the product.

Although the FDA has statutory authority to assure that medical devices, including IVDs, are safe and effective for their intended uses, the FDA has generally exercised its enforcement discretion and not enforced applicable device regulations with respect to IVDs that are

12

designed, manufactured and used within a single high-complexity CLIA-certified laboratory. Such tests are referred to as LDTs. We believe that the SomaSignalTMassays we offer for clinical diagnostic use are LDTs, as are our near-term pipeline candidate tests intended for clinical diagnostic use. However, in October 2023, the FDA issued a proposed rule aimed at regulating LDTs under the current medical device framework and proposing to phase out its existing enforcement discretion policy for this category of diagnostic tests; the public comment period ended in early December 2023. The proposal envisions that the LDT enforcement policy phase-out process would occur in gradual stages over a total period of four years, with pre-market approval applications for high-risk tests to be submitted by the 3.5-year mark, although more details are expected to be provided with the upcoming final rule. The likelihood of the FDA finalizing the proposed rule in April 2024 (as is currently projected), as well as potential litigation challenging the agency’s authority to take such action, is uncertain at this time. Affected stakeholders continue to press for a comprehensive legislative solution to create a harmonized paradigm for oversight of LDTs by both the FDA and CMS, instead of implementation of the proposed FDA administrative action, which may be disruptive to the industry and to patient access to certain diagnostic tests.

Even though we presently commercialize some of our SomaSignalTM tests as LDTs, the FDA may disagree that such tests are within the scope of its current enforcement discretion criteria for LDTs, or our SomaSignalTM tests may in the future become subject to more onerous regulation by the FDA. For several years, members of Congress have been working with stakeholders on a possible bill to regulate in vitro clinical tests including LDTs. For example, as drafted and re-introduced for consideration in the 118th Congress, legislation called the Verifying Accurate, Leading-edge IVCT Development (VALID Act), has been garnering bipartisan and bicameral support. The VALID Act would codify into law the term "in vitro clinical test" (IVCT) to create a new medical product category separate from medical devices that includes products currently regulated as IVDs as well as LDTs. The VALID Act would also create a new system for labs and hospitals to use to submit their tests electronically to the FDA for approval, which is aimed at reducing the amount of time it takes for the agency to approve such tests, and establish a new program to expedite the development of diagnostic tests that can be used to address a current unmet need for patients.

It is unclear whether the VALID Act would be passed by Congress in its current form or signed into law by the President. If the FDA finalizes its position on regulation of LDTs through the ongoing notice-and-comment rulemaking process or the VALID Act or other federal legislation is passed reforming the government’s regulation of LDTs, or alternatively, if the FDA disagrees with our assessment that our SomaSignalTMassays intended for clinical diagnostic use fall within the definition of an LDT, we could, for the first time, be subject to enforcement of regulatory requirements such as registration and listing requirements, medical device reporting requirements and quality control requirements. Any new legislation or FDA regulations affecting LDTs may result in increased regulatory burdens on our ability to continue marketing our tests and to develop and introduce new tests in the future. Additionally, if and when the FDA begins to actively enforce its premarket submission regulations with respect to LDTs generally or our SomaSignalTM tests in particular, whether as a result of new legislative authority or culmination of the current notice-and-comment rulemaking process, we may be required to obtain premarket clearance for our SomaSignalTM assays intended for clinical diagnostic use under Section 510(k) of the FDCA or approval of a PMA. The process for submitting a 510(k) premarket notification and receiving FDA clearance usually takes from three to 12 months, but it can take significantly longer and clearance is never guaranteed. The process for submitting and obtaining FDA approval of a PMA generally takes from one to three years or even longer and approval is not guaranteed. PMA approval typically requires extensive clinical data and can be significantly longer, more expensive and more uncertain than the 510(k) clearance process. If premarket review is required for some or all of our tests, the FDA could require that we stop selling our products pending clearance or approval and conduct clinical testing prior to making submissions to the FDA to obtain premarket clearance or approval. The FDA could also require that we label our SomaSignalTM tests as investigational or limit the labeling claims we are permitted to make.

Regulation of Clinical Trials

We may in the future conduct research studies for our SomaSignalTMtests intended for clinical diagnostic use and our other assays in development that involve clinical investigators and human subjects (or stored specimens from human subjects) at sites in the United States. We may need to conduct additional clinical trials for the SomaSignalTM tests for clinical use, as well as other tests we may offer in the future, to drive test adoption in the marketplace and reimbursement. Should we not be able to perform these studies, or should their results not provide clinically meaningful data and value for clinicians, adoption of our tests could be impaired and we may not be able to obtain reimbursement for them.

The conduct of clinical trials is also subject to extensive federal and institutional regulations intended to assure that the data and reported results are credible and accurate and that the rights, safety, and welfare of study participants are protected. Most studies involving human participants must be reviewed and approved by, and conducted under the auspices of, a duly-constituted institutional review board (IRB), which is a multi-disciplinary committee responsible for reviewing and evaluating the risks and benefits of a clinical trial for participating subjects and monitoring the trial on an ongoing basis. Companies sponsoring the clinical trials and investigators also must comply with, as applicable, regulations, guidelines and IRB requirements for obtaining informed consent from the study subjects, following the protocol and investigational plan, adequately monitoring the clinical trial, and timely reporting of adverse events. The sponsoring

13

company or the IRB may suspend or terminate a clinical trial at any time on various grounds, including a finding that the subjects are being exposed to an unacceptable health risk. In addition, trials involving human subjects often require significant time and cash resources to complete and are subject to a high degree of risk, including risks of experiencing delays, failing to complete the trial or obtaining unexpected or negative results.

Laboratory Technology for Research Use Only

Our proteomics, genomics, and analytical instruments, reagents, and other consumables are currently intended for, labeled and sold for research use only (RUO) applications, and we sell them to academic institutions, life sciences and clinical research laboratories that conduct research, and biopharmaceutical and biotechnology companies for non-clinical and non-diagnostic purposes. In addition, the SomaLogic offerings, other than the SomaSignalTM assays intended for clinical diagnostic use, are intended and offered for RUO applications. Such products are not intended or promoted for use in clinical practice in the diagnosis of disease or other conditions. Accordingly, they are not subject to pre- and post-market controls for medical devices by the FDA, with the exception that we must comply with the agency’s regulations relating to the labeling of IVDs intended for RUO applications. In accordance with such regulations, our RUO products are labeled, “For Research Use Only. Not for use in diagnostic procedures.”

The FDA’s final guidance document “Distribution of In Vitro Diagnostic Products Labeled for Research Use Only or Investigational Use Only” (the RUO/IUO Guidance), provides the FDA’s thinking on when IVDs are properly labeled for RUO or for IUO. The RUO/IUO Guidance explains that merely including a labeling statement that the product is for research purposes only will not necessarily render the device exempt from the FDA’s clearance, approval, or other regulatory requirements if the totality of circumstances surrounding the distribution of the product indicate that the manufacturer knows its product is being used by customers for clinical diagnostic uses or that the manufacturer intends such uses. These circumstances may include, among other things, written or verbal marketing claims regarding a product’s performance in clinical diagnostic applications, a manufacturer’s provision of technical support for clinical validation or clinical applications of the product, or solicitation of business from clinical laboratories, all of which FDA may consider evidence of intended uses that conflict with RUO/IUO labeling. In the future, certain of our products or related applications could become subject to regulation as medical devices by the FDA. If we are required to submit our products for pre-market review by the FDA, we may be required to delay marketing and commercialization while we obtain pre-market clearance or approval from the FDA. There would be no assurance that we could ever obtain such clearance or approval.

In some cases, our customers may, on their own initiative and without consulting us, use our RUO-labeled products in their own LDTs or in other FDA-regulated products for clinical diagnostic use.

Advertising of Laboratory Technologies and Services

Whether our proteomics or genomics technologies or our laboratory assays are not regulated by FDA, regulated as class I or class II devices, or subject to enforcement discretion with respect to FDA’s device requirements, advertising for such services and products is subject to federal truth-in-advertising laws enforced by the Federal Trade Commission (FTC), as well as comparable state consumer protection laws. Under the Federal Trade Commission Act (FTC Act), the FTC is empowered, among other things, to (a) prevent unfair methods of competition and unfair or deceptive acts or practices in or affecting commerce; (b) seek monetary redress and other relief for conduct injurious to consumers; and (c) gather and compile information and conduct investigations relating to the organization, business, practices, and management of entities engaged in commerce. The FTC has very broad enforcement authority, and failure to abide by the substantive requirements of the FTC Act and other consumer protection laws can result in administrative or judicial penalties, including civil penalties, injunctions affecting the manner in which we would be able to market services or products in the future, or criminal prosecution.

Federal and State Anti-Kickback Laws

The Federal Anti-Kickback Statute makes it a felony for a person or entity, including a clinical laboratory, to knowingly and willfully offer, pay, solicit or receive any remuneration, directly or indirectly, overtly or covertly, in cash or in kind, in order to induce or in return for the referral of an individual for the furnishing of, or the recommending or arranging for the furnishing of, purchasing, leasing, ordering or arranging for or recommending purchasing, leasing or ordering of any item or service that is reimbursable in whole or in part, under any federal healthcare program. A person or entity does not need to have actual knowledge of the statute or specific intent to violate it in order to have committed a violation. Courts have broadly interpreted the scope of the Anti-Kickback Statute and generally have held that the statute may be violated if merely one purpose of a payment arrangement is to induce referrals.

14

In addition to statutory exceptions to the Anti-Kickback Statute, regulations provide for a number of safe harbors. If an arrangement meets the provisions of a safe harbor or exception, it is deemed not to violate the Anti-Kickback Statute, and the parties are immune from prosecution. An arrangement must fully comply with each element of an applicable safe harbor in order to qualify for protection.

Failure to meet the requirements of an exception or a safe harbor does not render an arrangement illegal. Rather, the government may evaluate such arrangements on a case-by-case basis, taking into account all facts and circumstances.

A violation of the Anti-Kickback Statute may result in imprisonment for up to ten years and significant fines for each violation and additional administrative civil money penalties, plus up to three times the amount of the remuneration paid. Convictions under the Anti-Kickback Statute result in mandatory exclusion from federal healthcare programs for a minimum of five years. In addition, a violation of the Anti-Kickback Statute can serve as the basis of liability under the federal False Claims Act, which is discussed in greater detail below.

Although the Anti-Kickback Statute applies only to items and services reimbursable under any federal healthcare program, a number of states, including California, have passed statutes substantially similar to the Anti-Kickback Statute that apply to all third-party payors, including commercial insurers, and, in some states, to patients without insurance. The California Attorney General and courts have interpreted the California anti-kickback and fee-splitting laws in substantially the same way as the courts have interpreted the Anti-Kickback Statute. Penalties under such state laws include imprisonment and significant monetary fines.

In addition, in October 2018, the Eliminating Kickbacks in Recovery Act of 2018 (EKRA) was enacted as part of the Substance Use-Disorder Prevention that Promotes Opioid Recovery and Treatment for Patients and Communities Act. EKRA is an all-payor anti-kickback law that makes it a criminal offense to pay any remuneration to induce referrals to, or in exchange for, patients using the services of a recovery home, a substance use clinical treatment facility, or laboratory. However, unlike the Anti-Kickback Statute, EKRA is not limited to services covered by federal healthcare programs but applies more broadly to services covered by “healthcare benefit programs,” including commercial third-party payors. Although EKRA apparently was intended to reach patient brokering and similar arrangements to induce patronage of substance use recovery and treatment, the language in EKRA is broadly written. Further, certain of EKRA’s exceptions are inconsistent with the Anti-Kickback Statute and regulations. EKRA permits the U.S. Department of Justice to issue regulations clarifying EKRA’s exceptions or adding additional exceptions, but such regulations have not yet been issued.

Other Federal and State Healthcare Laws

In addition to the requirements discussed above, several other healthcare fraud and abuse laws could have an effect on our business. For example, federal law permits the Office of Inspector General for the Department of Health and Human Services (HHS-OIG) to exclude an individual or entity from Medicare or Medicaid for charging federal healthcare programs, including Medicare or Medicaid, substantially in excess of its usual charges for its items or services absent a finding of good cause. The terms “usual charge” and “substantially in excess” are subject to varying interpretations, and the HHS OIG has withdrawn multiple versions of a proposed rule intended to implement the statute.

The federal False Claims Act prohibits, among other things, a person from knowingly presenting, or causing to be presented, a false or fraudulent claim for payment to the federal government. In addition to actions initiated by the government itself, the statute authorizes actions to be brought on behalf of the federal government by a private party having knowledge of the alleged fraud pursuant to its qui tam provisions. Because the complaint in a qui tam action is initially filed under seal, the action may be pending for some time before the defendant is even aware of the action. Regardless of whether the government intervenes in the action, the relator, if successful, will receive a percentage of the recovery. In addition, providers and suppliers must report and return any overpayments received from the Medicare and Medicaid programs within 60 days of identification, and failure to identify and return such overpayments exposes the provider or supplier to federal False Claims Act liability. Violation of the federal False Claims Act may result payment of up to three times the actual damages sustained by the government, plus significant per-claim civil penalties, as well as mandatory exclusion from government healthcare programs. Several states, including California, have enacted comparable false claims laws that may apply regardless of payor.