0001160990falseN-CSR/AIn the event that the Common Shares to which this relates are sold to or through underwriters or dealer managers, a corresponding supplement will disclose the applicable sale load and/or commission.You will pay broker chargers if you direct your broker or the plan agent to sell your Common Shares that you acquired pursuant to a dividend reinvestment plan. You may also pay a pro rata share of brokerage commissions incurred in connection with open market purchase pursuant to the Fund’s Dividend Reinvestment Plan.The related supplement will disclose the estimated amount of offering expense, the offering price and the offering expenses borne by the Fund and indirectly by all of its Common Shareholders as a percentage of the offering price.Management fees include fees payable to the Investment Manager for advisory services and for supervisory, administrative and other services. The Fund pays for the advisory, supervisory and administrative services it requires under what is essentially an all-in fee structure. Pursuant to an investment management agreement, PIMCO is paid a Management Fee of 0.81% of the Fund’s average daily net assets (including daily net assets attributable to any preferred shares of the Fund that may be outstanding). The Fund (and not PIMCO) will be responsible for certain fees and expenses which are, reflected in the table above, that are not covered by the management fee under the investment management agreement. Please see Note 9, Fees and Expenses in the Notes to Financial Statements for an explanation of the management fee.Reflects the Fund’s use of leverage in the form of reverse repurchase agreements averaged over the fiscal year ended June 30, 2022, which represented 35.29% of the Fund’s total average managed assets (including assets attributable to reverse repurchase agreements), at an annual interest rate cost to the Fund of 0.47%, which is the weighted average interest rate cost during the fiscal year ended June 30, 2022. The actual amount of interest expense borne by the Fund will vary over time in accordance with the level of the Fund’s use of reverse repurchase agreements, dollar rolls and/or borrowings and variations in market interest rates. Borrowing expense is required to be treated as an expense of the Fund for accounting purposes. Any associated income or gains (or losses) realized from leverage obtained through such instruments is not reflected in the Annual Fund Operating Expenses table above, but would be reflected in the Fund’s performance results.Reflects the Fund’s outstanding Preferred Shares averaged over the fiscal year ended June 30, 2022, which represented 2.50% of the Fund’s total average managed assets (including the liquidation preference of outstanding Preferred Shares and assets attributable to reverse repurchase agreements), at an estimated annual dividend rate to the Fund of 0.39% (based on the weighted average Preferred Share dividend rate during the fiscal year ended June 30, 2022) and assumes the Fund will continue to pay Preferred Share dividends at the “maximum applicable rate” called for under the Fund’s Bylaws due to the ongoing failure of auctions for the ARPS. The actual dividend rate paid on the ARPS will vary over time in accordance with variations in market interest rates.Other expenses are estimated for the Fund’s fiscal year ending June 30, 2023.“Dividend Cost on Preferred Shares”, including distributions on Preferred Shares, and “Interest Payments on Borrowed Funds” are borne by the Fund separately from management fees paid to PIMCO. Excluding these expenses, Total Annual Fund Operating Expenses are 0.88%. Excluding only distributions on Preferred Shares of 0.02%, Total Annual Fund Operating Expenses are 1.22%.The example above should not be considered a representation of future expenses. Actual expenses may be higher or lower than those shown. The example assumes that the estimated Interest Payments on Borrowed Funds, Dividend Cost on Preferred Shares and Other Expenses set forth in the Annual Fund Operating Expenses table are accurate, that the rate listed under Total Annual Fund Operating Expenses remains the same each year and that all dividends and distributions are reinvested at NAV. Actual expenses may be greater or less than those assumed. Moreover, the Fund’s actual rate of return may be greater or less than the hypothetical 5% annual return shown in the example. The example does not include commissions or estimated offering expenses, which would cause the expenses shown in the example to increase.Fiscal year end changed from July 31st to June 30th.Unaudited. Information is presented in conformance with annual reporting requirements for funds that have filed a registration statement pursuant to General Instruction A.2 of Form N-2 (“Short Form N-2”).“Asset Coverage per Preferred Share” means the ratio that the value of the total assets of the Fund, less all liabilities and indebtedness not represented by ARPS, bears to the aggregate of the involuntary liquidation preference of ARPS, expressed as a dollar amount per ARPS.“Involuntary Liquidating Preference” means the amount to which a holder of ARPS would be entitled upon the involuntary liquidation of the Fund in preference to the Common Shareholders, expressed as a dollar amount per Preferred Share.The ARPS have no readily ascertainable market value. Auctions for the ARPS have failed since February 2008, there is currently no active trading market for the ARPS and the Fund is not able to reliably estimate what their value would be in a third-party market sale. The liquidation value of the ARPS represents its liquidation preference, which approximates fair value of the shares less any accumulated unpaid dividends. See Note 14, Auction-Rate Preferred Shares, in the notes to Financial Statements for more information.Such prices reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions.Effective April 1, 2022, the end of the Fund’s Fiscal year changed from July 31 to June 30 0001160990 2022-09-07 2022-09-07 0001160990 cik0001160990:CommonShareNetAssetValueMember 2020-05-01 2020-07-31 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2020-05-01 2020-07-31 0001160990 cik0001160990:ArpsMember 2020-07-31 2020-07-31 0001160990 cik0001160990:CommonSharesMember 2022-09-07 2022-09-07 0001160990 cik0001160990:CommonShareNetAssetValueMember 2022-04-01 2022-06-30 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2022-04-01 2022-06-30 0001160990 cik0001160990:CommonShareNetAssetValueMember 2021-11-01 2022-01-31 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2021-11-01 2022-01-31 0001160990 cik0001160990:CommonShareNetAssetValueMember 2021-08-01 2021-10-31 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2021-08-01 2021-10-31 0001160990 cik0001160990:CommonShareNetAssetValueMember 2021-05-01 2021-07-31 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2021-05-01 2021-07-31 0001160990 cik0001160990:CommonShareNetAssetValueMember 2020-11-01 2021-01-31 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2020-11-01 2021-01-31 0001160990 cik0001160990:CommonShareNetAssetValueMember 2020-08-01 2020-10-31 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2020-08-01 2020-10-31 0001160990 cik0001160990:CommonShareNetAssetValueMember 2020-02-01 2020-04-30 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2020-02-01 2020-04-30 0001160990 cik0001160990:CommonShareNetAssetValueMember 2019-11-01 2020-01-31 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2019-11-01 2020-01-31 0001160990 cik0001160990:CommonShareNetAssetValueMember 2019-08-01 2019-10-31 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2019-08-01 2019-10-31 0001160990 cik0001160990:ArpsMember 2021-08-01 2022-06-30 0001160990 cik0001160990:ArpsMember 2021-07-31 2021-07-31 0001160990 cik0001160990:ArpsMember 2019-07-31 2019-07-31 0001160990 cik0001160990:ArpsMember 2018-07-31 2018-07-31 0001160990 cik0001160990:ArpsMember 2017-07-31 2017-07-31 0001160990 cik0001160990:ArpsMember 2016-07-31 2016-07-31 0001160990 cik0001160990:ArpsMember 2014-11-01 2015-07-31 0001160990 cik0001160990:ArpsMember 2014-10-31 2014-10-31 0001160990 cik0001160990:ArpsMember 2013-10-31 2013-10-31 0001160990 cik0001160990:ArpsMember 2012-10-31 2012-10-31 0001160990 cik0001160990:ArpsMember 2011-10-31 2011-10-31 0001160990 cik0001160990:CommonShareNetAssetValueMember 2022-03-31 2022-03-31 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2022-03-31 2022-03-31 0001160990 cik0001160990:CommonShareNetAssetValueMember 2021-02-01 2021-04-30 0001160990 cik0001160990:PremiumDiscountNetAssetValueMember 2021-02-01 2021-04-30 xbrli:pure iso4217:USD xbrli:shares iso4217:USD xbrli:shares

SECURITIES AND EXCHANGE COMMISSION

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

Investment Company Act file number:

811-10555

PIMCO Corporate & Income Strategy Fund

(Exact name of registrant as specified in charter)

1633 Broadway, New York, NY 10019

(Address of principal executive offices)

Treasurer (Principal Financial & Accounting Officer)

650 Newport Center Drive, Newport Beach, CA 92660

(Name and address of agent for service)

Copies to:

Registrant’s telephone number, including area code: (844) 337-4626

Date of fiscal year end: June 30

Date of reporting period: June 30, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30e-1).

Annual Report

June 30, 2022

PIMCO Corporate & Income Opportunity Fund | PTY | NYSE

PIMCO Corporate & Income Strategy Fund | PCN | NYSE

PIMCO High Income Fund | PHK | NYSE

PIMCO Income Strategy Fund | PFL | NYSE

PIMCO Income Strategy Fund II | PFN | NYSE

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Page |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

2 |

|

|

|

|

| |

|

|

|

|

|

|

4 |

|

|

|

|

| |

|

|

|

|

|

|

23 |

|

|

|

|

| |

|

|

|

|

|

|

24 |

|

|

|

|

| |

|

|

|

|

|

|

28 |

|

|

|

|

| |

|

|

|

|

|

|

30 |

|

|

|

|

| |

|

|

|

|

|

|

32 |

|

|

|

|

| |

|

|

|

|

|

|

34 |

|

|

|

|

| |

|

|

|

|

|

|

100 |

|

|

|

|

| |

|

|

|

|

|

|

132 |

|

|

|

|

| |

|

|

|

|

|

|

133 |

|

|

|

|

| |

|

|

|

|

|

|

134 |

|

|

|

|

| |

|

|

|

|

|

|

135 |

|

|

|

|

| |

|

|

|

|

|

|

136 |

|

|

|

|

| |

|

|

|

|

|

|

138 |

|

|

|

|

| |

|

|

|

|

|

|

139 |

|

|

|

|

| |

|

|

|

|

|

|

140 |

|

|

|

|

| |

|

|

|

|

|

|

142 |

|

|

|

|

| |

|

|

|

|

|

|

143 |

|

|

|

|

| |

|

|

|

|

|

|

162 |

|

|

|

|

| |

|

|

|

|

|

|

192 |

|

|

|

|

| |

|

|

|

|

|

|

193 |

|

|

|

|

| |

|

|

|

|

|

|

194 |

|

|

|

|

| |

|

|

|

|

|

|

197 |

|

|

|

|

| |

|

|

|

|

|

|

201 |

|

|

|

|

| |

|

|

|

|

|

|

207 |

|

|

|

|

| |

|

|

|

|

|

|

208 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fund |

|

Fund

Summary |

|

|

Schedule of

Investments |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

8 |

|

|

|

36 |

|

|

|

|

| |

|

|

11 |

|

|

|

53 |

|

|

|

|

| |

|

|

14 |

|

|

|

65 |

|

|

|

|

| |

|

|

17 |

|

|

|

77 |

|

|

|

|

| |

|

|

20 |

|

|

|

88 |

|

|

|

|

|

|

Letter from the Chair of the Board & President |

|

|

|

|

Dear Shareholder,

We hope that you and your family are remaining safe and healthy during these challenging times. We continue to work tirelessly to navigate markets and manage the assets that you have entrusted with us. Following this letter is the PIMCO Closed-End Funds Annual Report, which covers the 12-month reporting period ended June 30, 2022.

1

On the subsequent pages, you will find specific details regarding investment results and a discussion of the factors that most affected performance during the reporting period.

For the 12-month reporting period ended June 30, 2022

The global economy continued to be affected by the COVID-19 pandemic (“COVID-19”) and its variants. Looking back, third quarter 2021 U.S. annualized gross domestic product (“GDP”) grew 2.3%. Economic activity accelerated during the fourth quarter, as GDP growth was 6.9%. However, the U.S. economy then experienced a setback, as first quarter 2022 GDP growth was -1.6%. Finally, the Commerce Department’s initial estimate for second quarter 2022 GDP growth — released after the reporting period ended — was -0.9%.

In the U.S., the Federal Reserve Board (the “Fed”) took several steps to tighten monetary policy to combat elevated inflation. The Fed reduced the monthly pace of its net asset purchases of Treasury securities and agency mortgage-backed securities in November 2021 and again in December. The Fed ended its monthly asset purchases in mid-March 2022. The Fed then raised the federal funds rate 0.25% to a range between 0.25% and 0.50% in March 2022, its first rate hike since 2018. The central bank then raised rates 0.50% in its May 2022 meeting and 0.75% in its June meeting. Finally, on July 27, 2022 — after the reporting period ended — the Fed raised rates 0.75%, to a range between 2.25% and 2.50%.

Economies outside the U.S. also continued to be impacted by the pandemic. The war in Ukraine and its repercussions also led to increased uncertainties around the world. In its April 2022 World Economic Outlook Update, the International Monetary Fund (“IMF”) said it expects U.S. gross domestic product (“GDP”) growth to be 3.7% in 2022, compared to 5.7% in 2021. Elsewhere, the IMF expects 2022 GDP to grow 2.8% in the eurozone (from 5.3% in 2021), 3.7% in the U.K. (from 7.4% in 2021) and 2.4% in Japan (from 1.6% in 2021).

Several other central banks began tightening monetary policy during the period. In December 2021, the Bank of England (the “BoE”) surprised the market and raised rates for the first time since COVID-19 began. The BoE again raised rates at its meetings in February, March, May and June 2022. The European Central Bank (the “ECB”) indicated that it intended to raise rates at its September 2022 meeting. Elsewhere, the Bank of Japan (the “BoJ”) maintained its loose monetary policy and appears likely to remain accommodative in the near future given the headwinds facing its economy.

During the reporting period, short- and long-term U.S. Treasury yields moved sharply higher. The yield on the benchmark 10-year U.S. Treasury note was 2.98% on June 30, 2022, versus 1.45% on June 30, 2021. The Bloomberg Global Treasury Index (USD Hedged), which tracks fixed-rate, local currency government debt of investment grade countries, including developed and emerging markets, returned -7.91%. Meanwhile, the Bloomberg Global Aggregate Credit Index (USD Hedged), a widely used index of global investment grade credit bonds, returned -12.75%. Riskier fixed income asset classes, including high yield corporate bonds and emerging market debt, were also weak. The ICE BofAML Developed Markets High Yield Constrained Index (USD Hedged), a widely used index of below-investment-grade bonds, returned -12.85%, whereas emerging market external debt, as represented by the JPMorgan Emerging Markets Bond Index (EMBI) Global (USD Hedged), returned -19.25%. Emerging market local bonds, as represented by the JPMorgan Government Bond Index-Emerging Markets Global Diversified Index (Unhedged), returned -19.28%.

1

Please note that the Funds’ fiscal year ends were recently changed to June 30; therefore, the reporting period covered is from August 1, 2021 — June 30, 2022. Please see the Notes to Financial Statements for further detail.

Amid periods of volatility, global equities generally posted weak results during the reporting period as economic and geopolitical concerns weighed on investor sentiment. U.S. equities, as represented by the S&P 500 Index, returned

-10.62%.

Global equities, as represented by the MSCI World Index, returned -14.34%, while emerging market equities, as measured by the MSCI Emerging Markets Index, returned -25.28%. Meanwhile, Japanese equities, as represented by the Nikkei 225 Index (in JPY), returned -8.33% and European equities, as represented by the MSCI Europe Index (in EUR), returned -6.54%.

Commodity prices were volatile and generated mixed returns. Brent crude oil, which was approximately $75 a barrel at the start of the reporting period, rose to roughly $112 a barrel at the end of June 2022. We believe the oil-price increase was driven by supply shortages and stronger demand due to economic re-openings as COVID-19 restrictions eased. Repercussions from the war in Ukraine also contributed to higher oil prices. In terms of other commodities prices, copper declined, whereas gold rose during the period.

Finally, there were also periods of volatility in the foreign exchange markets. We believe this was due to several factors, including economic growth expectations and changing central bank monetary policies, as well as rising inflation, COVID-19 variants and geopolitical events. The U.S. dollar strengthened against several major currencies. For example, during the reporting period, the U.S. dollar returned 11.59%, 11.95% and 18.13% versus the euro, the British pound and the Japanese yen, respectively.

Thank you for the assets you have placed with us. We deeply value your trust, and we will continue to work diligently to meet your broad investment needs. For any questions regarding your PIMCO Closed-End Funds investments, please contact your financial adviser, or call the Funds’ shareholder servicing agent at (844) 33-PIMCO. We also invite you to visit our website at pimco.com to learn more about our global viewpoints.

Sincerely,

|

|

|

|

|

|

|

|

|

|

|

Deborah A. DeCotis |

|

Eric D. Johnson |

Chair of the Board of Trustees |

|

President |

Past performance is no guarantee of future results. Unless otherwise noted, index returns reflect the reinvestment of income distributions and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an unmanaged index.

|

|

|

|

|

Important Information About the Funds |

|

|

|

|

Information regarding each Fund’s principal investment strategies, principal risks and risk management strategies, the effects of each Fund’s leverage, and each Fund’s fundamental investment restrictions, including a summary of certain changes thereto during the most recent fiscal year, can be found within the relevant sections of this report. Please refer to the Table of Contents for further information.

We believe that bond funds have an important role to play in a well-diversified investment portfolio. It is important to note, however, that in an environment where interest rates may trend upward, rising rates would negatively impact the performance of most bond funds, and fixed-income securities and other instruments held by a Fund are likely to decrease in value. A wide variety of factors can cause interest rates or yields of U.S. Treasury securities (or yields of other types of bonds) to rise (e.g., central bank monetary policies, inflation rates, general economic conditions, etc.). In addition, changes in interest rates can be sudden and unpredictable, and there is no guarantee that Fund management will anticipate such movement accurately. A Fund may lose money as a result of movements in interest rates.

As of the date of this report, interest rates in the United States and many parts of the world, including certain European countries, are ascending from historically low levels. Thus, bond funds currently face a heightened level of risk associated with rising interest rates and/or bond yields. This could be driven by a variety of factors, including but not limited to central bank monetary policies, changing inflation or real growth rates, general economic conditions, increasing bond issuances or reduced market demand for low yielding investments. Further, while bond markets have steadily grown over the past three decades, dealer inventories of corporate bonds are near historic lows in relation to market size. As a result, there has been a significant reduction in the ability of dealers to “make markets”.

Bond funds and individual bonds with a longer duration (a measure used to determine the sensitivity of a security’s price to changes in interest rates) tend to be more sensitive to changes in interest rates, usually making them more volatile than securities or funds with shorter durations. All of the factors mentioned above, individually or collectively, could lead to increased volatility and/or lower liquidity in the fixed income markets or negatively impact a Fund’s performance or cause a Fund to incur losses.

A Fund may enter into opposite sides of multiple interest rate swaps or other derivatives with respect to the same underlying reference instrument (e.g., a 10-year U.S. treasury) that have different effective dates with respect to interest accrual time periods also for the principal purpose of generating distributable gains (characterized as ordinary income for tax purposes) that are not part of a Fund’s duration or yield curve management strategies. In such a “paired swap transaction”, a

Fund would generally enter into one or more interest rate swap agreements whereby a Fund agrees to make regular payments starting at the time the Fund enters into the agreements equal to a floating interest rate in return for payments equal to a fixed interest rate (the “initial leg”). A Fund would also enter into one or more interest rate swap agreements on the same underlying instrument, but take the opposite position (i.e., in this example, a Fund would make regular payments equal to a fixed interest rate in return for receiving payments equal to a floating interest rate) with respect to a contract whereby the payment obligations do not commence until a date following the commencement of the initial leg (the “forward leg”).

A Fund may engage in investment strategies, including those that employ the use of paired swaps transactions, the use of interest rate swaps to seek to capitalize on differences between short-term and long-term interest rates and other derivatives transactions, to, among other things, seek to generate current, distributable income, even if such strategies could potentially result in declines in the Fund’s net asset value (“NAV”). A Fund’s income and gain-generating strategies, including certain derivatives strategies, may generate current income and gains taxable as ordinary income sufficient to support monthly distributions even in situations when a Fund has experienced a decline in net assets due to, for example, adverse changes in the broad U.S. or non-U.S. equity markets or a Fund’s debt investments, or arising from its use of derivatives. For instance, a portion of a Fund’s monthly distributions may be sourced from paired swap transactions utilized to produce current distributable ordinary income for tax purposes on the initial leg, with a substantial possibility that a Fund will later realize a corresponding capital loss and potential decline in its NAV with respect to the forward leg (to the extent there are not corresponding offsetting capital gains being generated from other sources). Because some or all of these transactions may generate capital losses without corresponding offsetting capital gains, portions of a Fund’s distributions recognized as ordinary income for tax purposes (such as from paired swap transactions) may be economically similar to a taxable return of capital when considered together with such capital losses.

Classifications of the Funds’ portfolio holdings in this report are made according to financial reporting standards. The classification of a particular portfolio holding as shown in the Allocation Breakdown and Schedule of Investments sections of this report may differ from the classification used for the Funds’ compliance calculations, including those used in the Funds’ prospectus, investment objectives, regulatory, and other investment limitations and policies, which may be based on different asset class, sector or geographical classifications. Each Fund is separately monitored for compliance with respect to prospectus and regulatory requirements.

The geographical classification of foreign

(non-U.S.)

securities in this report, if any, are classified by the country of incorporation of a holding. In certain instances, a security’s country of incorporation may be different from its country of economic exposure.

Beginning in January 2020, global financial markets have experienced and may continue to experience significant volatility resulting from the spread of a novel coronavirus known as

COVID-19.

The outbreak of

COVID-19

has resulted in travel and border restrictions, quarantines, supply chain disruptions, lower consumer demand and general market uncertainty. The effects of

COVID-19

have and may continue to adversely affect the global economy, the economies of certain nations and individual issuers, all of which may negatively impact the Funds’ performance. In addition,

COVID-19

and governmental responses to

COVID-19

may negatively impact the capabilities of the Funds’ service providers and disrupt the Funds’ operations.

The United States’ enforcement of restrictions on U.S. investments in certain issuers and tariffs on goods from other countries, each with a focus on China, has contributed to international trade tensions and may impact portfolio securities.

The United Kingdom’s withdrawal from the European Union may impact Fund returns. The withdrawal may cause substantial volatility in foreign exchange markets, lead to weakness in the exchange rate of the British pound, result in a sustained period of market uncertainty, and destabilize some or all of the other European Union member countries and/or the Eurozone.

The Funds may invest in certain instruments that rely in some fashion upon the London Interbank Offered Rate (“LIBOR”). LIBOR is an average interest rate, determined by the ICE Benchmark Administration, that banks charge one another for the use of short-term money. The United Kingdom’s Financial Conduct Authority, which regulates LIBOR, has announced plans to ultimately phase out the use of LIBOR. The transition may result in a reduction in the value of certain instruments held by a Fund or a reduction in the effectiveness of related Fund transactions such as hedges. There remains uncertainty regarding future utilization of LIBOR and the nature of any replacement rate (e.g., the Secured Overnight Financing Rate, which is intended to replace U.S. dollar LIBOR and measures the cost of overnight borrowings through repurchase agreement transactions collateralized with U.S. Treasury securities). Any potential effects of the transition away from LIBOR on a Fund or on certain instruments in which a Fund invests can be difficult to ascertain, and they may vary depending on a variety of factors. The transition may also result in a reduction in the value of certain instruments held by a Fund or a reduction in the effectiveness of related Fund transactions such as hedges. Any such effects of the transition away from LIBOR, as well as other unforeseen effects, could result in losses to a Fund.

The common shares of the Funds trade on the New York Stock Exchange. As with any stock, the price of a Fund’s common shares will fluctuate with market conditions and other factors. If you sell your common shares of a Fund, the price received may be more or less than your original investment. Shares of

closed-end

management investment companies, such as the Funds, frequently trade at a discount from their NAV and may trade at a price that is less than the initial offering price and/or the NAV of such shares. Further, if a Fund’s shares trade at a price that is more than the initial offering price and/or the NAV of such shares, including at a substantial premium and/or for an extended period of time, there is no assurance that any such premium will be sustained for any period of time and will not decrease, or that the shares will not trade at a discount to NAV thereafter.

On each applicable Fund Summary page in this Shareholder Report, the Average Annual Total Return table measures performance assuming that any dividend and capital gain distributions were reinvested. Total return is calculated by determining the percentage change in NAV or market price (as applicable) in the specified period. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions. Total return for a period of more than one year represents the average annual total return. Performance at market price will differ from results at NAV. Although market price returns tend to reflect investment results over time, during shorter periods returns at market price can also be influenced by factors such as changing views about a Fund, market conditions, supply and demand for the Fund’s shares, or changes in the Fund’s dividends. Performance shown is net of fees and expenses. Historical NAV performance for a Fund may have been positively impacted by fee waivers or expense limitations in place during some or all of the periods shown, if applicable. Future performance (including total return or yield) and distributions may be negatively impacted by the expiration or reduction of any such fee waivers or expense limitations.

The dividend rate that a Fund pays on its common shares may vary as portfolio and market conditions change, and will depend on a number of factors, including without limit the amount of a Fund’s undistributed net investment income and net short- and long-term capital gains, as well as the costs of any leverage obtained by a Fund. As portfolio and market conditions change, the rate of distributions on the common shares and a Fund’s dividend policy could change. There can be no assurance that a change in market conditions or other factors will not result in a change in a Fund distribution rate or that the rate will be sustainable in the future.

|

|

|

|

|

Important Information About the Funds |

|

|

|

|

The following table discloses the inception date and diversification status of each Fund:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| PIMCO Corporate & Income Opportunity Fund |

|

|

|

|

|

|

12/27/02 |

|

|

|

Diversified |

|

| PIMCO Corporate & Income Strategy Fund |

|

|

|

|

|

|

12/21/01 |

|

|

|

Diversified |

|

| PIMCO High Income Fund |

|

|

|

|

|

|

04/30/03 |

|

|

|

Diversified |

|

| PIMCO Income Strategy Fund |

|

|

|

|

|

|

08/29/03 |

|

|

|

Diversified |

|

| PIMCO Income Strategy Fund II |

|

|

|

|

|

|

10/29/04 |

|

|

|

Diversified |

|

An investment in a Fund is not a bank deposit and is not guaranteed or insured by the Federal Deposit Insurance Corporation or any other government agency. It is possible to lose money on investments in the Funds.

The Trustees are responsible generally for overseeing the management of the Funds. The Trustees authorize the Funds to enter into service agreements with Pacific Investment Management Company LLC (“PIMCO”) and other service providers in order to provide, and in some cases authorize service providers to procure through other parties, necessary or desirable services on behalf of the Funds. Shareholders are not parties to or third-party beneficiaries of such service agreements. Neither a Fund’s prospectus or Statement of Additional Information (“SAI”), any press release or shareholder report, any contracts filed as exhibits to a Fund’s registration statement, nor any other communications, disclosure documents or regulatory filings (including this report) from or on behalf of a Fund creates a contract between or among any shareholders of a Fund, on the one hand, and the Fund, a service provider to the Fund, and/or the Trustees or officers of the Fund, on the other hand.

The Trustees (or the Funds and their officers, service providers or other delegates acting under authority of the Trustees) may amend its most recent prospectus or use a new prospectus or SAI with respect to a Fund, adopt and disclose new or amended policies and other changes in press releases and shareholder reports and/or amend, file and/or issue any other communications, disclosure documents or regulatory filings, and may amend or enter into any contracts to which a Fund is a party, and interpret the investment objective(s), policies, restrictions and contractual provisions applicable to any Fund, without shareholder input or approval, except in circumstances in which shareholder approval is specifically required by law (such as changes to fundamental investment policies) or where a shareholder approval requirement was specifically disclosed in a Fund’s then-current prospectus, SAI or shareholder report and is otherwise still in effect.

PIMCO has adopted written proxy voting policies and procedures (“Proxy Policy”) as required by Rule

206(4)-6

under the Investment Advisers Act of 1940, as amended. The Proxy Policy has been adopted

by the Funds as the policies and procedures that PIMCO will use when voting proxies on behalf of the Funds. A description of the policies and procedures that PIMCO uses to vote proxies relating to portfolio securities of each Fund, and information about how each Fund voted proxies relating to portfolio securities held during the most recent twelve-month period ended June 30th, are available without charge, upon request, by calling the Funds at (844)

33-PIMCO,

on the Funds’ website at www.pimco.com, and on the Securities and Exchange Commission’s (“SEC”) website at www.sec.gov.

The Funds file portfolio holdings information with the SEC on

Form N-PORT

within 60 days of the end of each fiscal quarter. The Funds’ complete schedules of securities holdings as of the end of each fiscal quarter will be made available to the public on the SEC’s website at www.sec.gov and on PIMCO’s website at www.pimco.com, and will be made available, upon request, by calling PIMCO at (844)

33-PIMCO.

SEC rules allow shareholder reports to be delivered to investors by providing access to such reports online free of charge and by mailing a notice that the report is electronically available. Investors may elect to receive all reports in paper free of charge by contacting their financial intermediary or, if invested directly with a Fund, investors can inform the Fund by calling (844) 33-PIMCO. Any election to receive reports in paper will apply to all funds held with the fund complex if invested directly with a Fund or to all funds held in the investor’s account if invested through a financial intermediary, such as a broker-dealer or bank.

In April 2020, the SEC adopted amended rules modifying the registration, communications, and offering processes for registered

closed-end

funds and interval funds. Among other things, the amendments: (1) permit qualifying

closed-end

funds to use a short-form registration statement to offer securities in eligible transactions and certain funds to qualify as Well Known Seasoned Issuers; (2) permit interval funds to pay registration fees based on net issuance of shares in a manner similar to mutual funds; (3) require

closed-end

funds and interval funds to include additional disclosures in their annual reports; and (4) require certain information to be filed in interactive data format. The new rules have phased compliance dates, with some requirements having already taken effect and others requiring compliance as late as February 1, 2023.

In October 2020, the SEC adopted a rule related to the use of derivatives, short sales, reverse repurchase agreements and certain other transactions by registered investment companies that rescinds and withdraws the guidance of the SEC and its staff regarding asset segregation and cover transactions that was applicable to the Funds as of the date of this report. Subject to certain exceptions, the rule requires funds that trade derivatives and other transactions that create future payment or delivery obligations to comply with a value-at-risk

leverage limit and certain derivatives risk management program and reporting requirements. These requirements may limit the ability of the Funds to use derivatives and reverse repurchase agreements and similar financing transactions as part of their investment strategies and may increase the cost of the Funds’ investments and cost of doing business, which could adversely affect investors. The rule went into effect on February 19, 2021. The compliance date for the new rule and related recordkeeping requirements is August 19, 2022.

In October 2020, the SEC adopted a rule regarding the ability of a fund to invest in other funds. The rule allows a fund to acquire shares of another fund in excess of certain limitations currently imposed by the Investment Company Act of 1940 (the “Act”) without obtaining individual exemptive relief from the SEC, subject to certain conditions. The rule also includes the rescission of certain exemptive relief from the SEC and guidance from the SEC staff for funds to invest in other funds. The effective date for the rule was January 19, 2021, and the compliance date for the rule was January 19, 2022.

In December 2020, the SEC adopted a rule addressing fair valuation of fund investments. The new rule sets forth requirements for good faith determinations of fair value as well as for the performance of fair value determinations, including related oversight and reporting obligations. The new rule also defines “readily available market quotations” for purposes of the definition of “value” under the Act, and the SEC noted that this definition will apply in all contexts under the Act. The effective date for the rule was March 8, 2021. The compliance date for the new rule and the associated recordkeeping requirements is September 8, 2022.

In May 2022, the SEC proposed amendments to a current rule governing fund naming conventions. In general, the current rule requires funds with certain types of names to adopt a policy to invest at least 80% of their assets in the type of investment suggested by the name. The proposed amendments would expand the scope of the current rule in a number of ways that would result in an expansion of the types of fund names that would require the fund to adopt an 80% investment policy under the rule. Additionally, the proposed amendments would modify the circumstances under which a fund may deviate from its 80% investment policy and address the use and valuation of derivatives instruments for purposes of the rule. The proposal’s impact on the Funds will not be known unless and until any final rulemaking is adopted.

In May 2022, the SEC proposed a framework that would require certain registered funds (such as the Funds) to disclose their environmental, social, and governance (“ESG”) investing practices. Among other things, the proposed requirements would mandate that funds meeting three pre-defined classifications (

, integrated, ESG focused and/or

impact funds) provide prospectus and shareholder report disclosure related to the ESG factors, criteria and processes used in managing the fund. The proposal’s impact on the Funds will not be known unless and until any final rulemaking is adopted.

PIMCO Corporate & Income Opportunity Fund

Cumulative Returns Through June 30, 2022

$10,000 invested at the end of the month when the Fund commenced operations.

Allocation Breakdown as of June 30, 2022

|

|

|

|

|

| |

|

|

42.5% |

|

| |

|

Loan Participations and Assignments |

|

|

26.0% |

|

| |

|

| |

|

|

6.8% |

|

| |

|

Non-Agency Mortgage-Backed Securities |

|

|

5.8% |

|

| |

|

| |

|

|

5.5% |

|

| |

|

| |

|

|

4.0% |

|

| |

|

| |

|

|

2.2% |

|

| |

|

| |

|

|

1.6% |

|

| |

|

| |

|

|

1.6% |

|

| |

|

Real Estate Investment Trusts |

|

|

1.4% |

|

| |

|

| |

|

|

1.2% |

|

| |

|

| |

|

|

1.2% |

|

| |

|

| |

|

|

0.2% |

|

|

|

% of Investments, at value. |

|

|

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average Annual Total Return (1) for the period ended June 30, 2022 |

|

| |

|

|

|

|

|

| |

|

|

|

1 Year |

|

|

5 Year |

|

|

10 Year |

|

|

Commencement

of Operations

(12/27/02) |

|

|

|

|

Market Price |

|

|

(30.68)% |

|

|

|

4.21% |

|

|

|

8.08% |

|

|

|

11.54% |

|

|

|

|

NAV |

|

|

(13.53)% |

|

|

|

5.97% |

|

|

|

10.47% |

|

|

|

12.28% |

|

|

|

|

ICE BofAML US High Yield Index |

|

|

(12.66)% |

|

|

|

1.95% |

|

|

|

4.40% |

|

|

|

7.13% |

|

All Fund returns are net of fees and expenses and include applicable fee waivers and/or expense limitations. Absent any applicable fee waivers and/or expense limitations, performance would have been lower and there can be no assurance that any such waivers or limitations will continue in the future.

Average annual total return since 12/31/2002.

The average annual total returns shown above have been restated from previous reports to shareholders to align with the Fund’s change from a July 31 to a June 30 fiscal year end. For the period August 1, 2021 through June 30, 2022, the Fund’s total return was

-33.71%

and

-14.19%

on a market price and NAV basis, respectfully.

It is not possible to invest directly in an unmanaged index.

|

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. The NAV presented may differ from the NAV reported for the same period in other Fund materials. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

|

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The index is not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

|

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or market price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (‘‘ROC’’) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be made on Form 1099 DIV sent to shareholders each January. |

|

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

Fund Information (as of June 30, 2022)

(1)

|

|

|

|

|

| |

|

|

$12.51 |

|

| |

|

| |

|

|

$11.21 |

|

| |

|

Premium/(Discount) to NAV |

|

|

11.60% |

|

| |

|

Market Price Distribution Rate (2) |

|

|

11.40% |

|

| |

|

| |

|

|

12.72% |

|

| |

|

Total Effective Leverage (3) |

|

|

47.93% |

|

Investment Objective and Strategy Overview

PIMCO Corporate & Income Opportunity Fund’s investment objective is to seek maximum total return through a combination of current income and capital appreciation.

The following affected performance (on a gross basis) during the reporting period:

| » |

|

Short interest rate positioning, especially in the intermediate and long end of the curve, contributed to absolute performance, as rates increased. |

| » |

|

Exposure to select corporate special situation positions contributed to absolute performance, as select issuers posted positive returns. |

| » |

|

Security selection in asset backed securities, most notably student loans, contributed to absolute performance, as select securities posted positive returns. |

| » |

|

Exposure to corporate credit detracted from absolute performance, as the asset class posted negative returns. |

| » |

|

Exposure to emerging market debt detracted from absolute performance, as the asset class posted negative returns. |

| » |

|

Exposure to municipal debt detracted from absolute performance, as the asset class posted negative returns. |

|

|

|

|

|

| |

|

Market and Net Asset Value Information |

|

|

The following table, presented in conformance with annual reporting requirements for funds that have filed a Short Form N-2, sets forth, for each of the periods indicated, the high and low closing market prices of the Fund’s Common Shares on the NYSE, the high and low NAV per Common Share and the high and low premium/discount to NAV per Common Share. See Note 3, Investment Valuation and Fair Value Measurements in the Notes to Financial Statements for information as to how the Fund’s NAV is determined.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Common share market price (1) |

|

|

Common share

net asset value |

|

|

Premium (discount) as

a % of net asset value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Quarter ended June 30, 2022 |

|

$ |

15.84 |

|

|

$ |

12.51 |

|

|

$ |

13.21 |

|

|

$ |

11.21 |

|

|

|

22.65% |

|

|

|

9.48% |

|

| Period ended March 31, 2022 (2) |

|

$ |

16.08 |

|

|

$ |

13.48 |

|

|

$ |

13.86 |

|

|

$ |

12.61 |

|

|

|

16.55% |

|

|

|

6.65% |

|

| Quarter ended January 31, 2022 |

|

$ |

18.54 |

|

|

$ |

15.53 |

|

|

$ |

14.33 |

|

|

$ |

13.78 |

|

|

|

30.70% |

|

|

|

12.70% |

|

| Quarter ended October 31, 2021 |

|

$ |

21.66 |

|

|

$ |

17.94 |

|

|

$ |

14.52 |

|

|

$ |

14.15 |

|

|

|

52.21% |

|

|

|

24.79% |

|

| Quarter ended July 31, 2021 |

|

$ |

20.59 |

|

|

$ |

18.04 |

|

|

$ |

14.52 |

|

|

$ |

14.14 |

|

|

|

43.09% |

|

|

|

27.58% |

|

| Quarter ended April 30, 2021 |

|

$ |

18.98 |

|

|

$ |

17.78 |

|

|

$ |

14.42 |

|

|

$ |

14.04 |

|

|

|

32.63% |

|

|

|

25.17% |

|

| Quarter ended January 31, 2021 |

|

$ |

18.05 |

|

|

$ |

16.31 |

|

|

$ |

14.22 |

|

|

$ |

12.73 |

|

|

|

29.50% |

|

|

|

25.71% |

|

| Quarter ended October 31, 2020 |

|

$ |

16.84 |

|

|

$ |

15.35 |

|

|

$ |

12.82 |

|

|

$ |

12.43 |

|

|

|

31.36% |

|

|

|

23.49% |

|

| Quarter ended July 31, 2020 |

|

$ |

16.36 |

|

|

$ |

13.61 |

|

|

$ |

12.42 |

|

|

$ |

11.16 |

|

|

|

34.65% |

|

|

|

21.74% |

|

| Quarter ended April 30, 2020 |

|

$ |

19.68 |

|

|

$ |

10.44 |

|

|

$ |

14.98 |

|

|

$ |

10.58 |

|

|

|

32.23% |

|

|

|

(8.98)% |

|

| Quarter ended January 31, 2020 |

|

$ |

19.61 |

|

|

$ |

18.35 |

|

|

$ |

14.80 |

|

|

$ |

14.07 |

|

|

|

32.50% |

|

|

|

28.70% |

|

| Quarter ended October 31, 2019 |

|

$ |

18.73 |

|

|

$ |

17.02 |

|

|

$ |

14.64 |

|

|

$ |

14.04 |

|

|

|

31.36% |

|

|

|

21.23% |

|

|

Such prices reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions. |

|

Effective April 1, 2022, the end of the Fund’s Fiscal year changed from July 31 to June 30 |

The following information is presented in conformance with annual reporting requirements for funds that have filed a Short Form N-2.

The following table is intended to assist investors in understanding the fees and expenses (annualized) that an investor in Common Shares of the Fund would bear, directly or indirectly, as a result of an offering. The table reflects the use of leverage attributable to the Fund’s outstanding Preferred Shares and reverse repurchase agreements averaged over the fiscal year ended June 30, 2022 in an amount equal to 41.67% of the Fund’s total average managed assets (including assets attributable to such leverage), and shows Fund expenses as a percentage of net assets attributable to Common Shares. The percentage above does not reflect the Fund’s use of other forms of economic leverage, such as credit default swaps or other derivative instruments. The table and example below are based on the Fund’s capital structure as of June 30, 2022. The extent of the Fund’s assets attributable to leverage following an offering, and the Fund’s associated expenses, are likely to vary (perhaps significantly) from these assumptions.

Shareholder Transaction Expense

|

|

|

|

|

|

|

|

|

|

|

|

Sales load (as a percentage of offering price) (1) |

|

|

|

|

|

|

[ ]% |

|

| |

|

|

Offering Expenses Borne by Common Shareholders (as a percentage of offering price) (2) |

|

|

|

|

|

|

[ ]% |

|

| |

|

|

Dividend Reinvestment Plan Fees (3) |

|

|

|

|

|

|

None |

|

|

In the event that the Common Shares to which this relates are sold to or through underwriters or dealer managers, a corresponding supplement will disclose the applicable sale load and/or commission. |

|

The related supplement will disclose the estimated amount of offering expense, the offering price and the offering expenses borne by the Fund and indirectly by all of its Common Shareholders as a percentage of the offering price. |

|

You will pay broker chargers if you direct your broker or the plan agent to sell your Common Shares that you acquired pursuant to a dividend reinvestment plan. You may also pay a pro rata share of brokerage commissions incurred in connection with open market purchase pursuant to the Fund’s Dividend Reinvestment Plan. |

Annual Fund Operating Expenses

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Percentage of

Net Assets Attributable to

Common Shares (reflecting

leverage attributable to

ARPS and reverse

repurchase agreements) |

|

| |

|

|

| |

|

|

|

|

|

|

0.74% |

|

| |

|

|

Dividend Cost on Preferred Shares (2) |

|

|

|

|

|

|

0.07% |

|

| |

|

|

Interest Payments on Borrowed Funds (3) |

|

|

|

|

|

|

0.36% |

|

| |

|

|

| |

|

|

|

|

|

|

0.03% |

|

| |

|

|

Total Annual Fund Operating Expenses (5) |

|

|

|

|

|

|

|

|

|

Management fees include fees payable to the Investment Manager for advisory services and for supervisory, administrative and other services. The Fund pays for the advisory, supervisory and administrative services it requires under what is essentially an all-in fee structure. Pursuant to an investment management agreement, PIMCO is paid a Management Fee of 0.65% of the Fund’s average daily net assets (including daily net assets attributable to any preferred shares of the Fund that may be |

| |

outstanding). The Fund (and not PIMCO) will be responsible for certain fees and expenses which are, reflected in the table above, that are not covered by the management fee under the investment management agreement. Please see Note 9, Fees and Expenses in the Notes to Financial Statements for an explanation of the management fee. |

|

Reflects the Fund’s outstanding Preferred Shares averaged over the fiscal year ended June 30, 2022, which represented 7.82% of the Fund’s total average managed assets (including the liquidation preference of outstanding Preferred Shares and assets attributable to reverse repurchase agreements), at an estimated annual dividend rate to the Fund of 0.48% (based on the weighted average Preferred Share dividend rate during the fiscal year ended June 30, 2022) and assumes the Fund will continue to pay Preferred Share dividends at the “maximum applicable rate” called for under the Fund’s Bylaws due to the ongoing failure of auctions for the ARPS. The actual dividend rate paid on the ARPS will vary over time in accordance with variations in market interest rates. |

|

Reflects the Fund’s use of leverage in the form of reverse repurchase agreements averaged over the fiscal year ended June 30, 2022, which represented 33.85% of the Fund’s total average managed assets (including assets attributable to reverse repurchase agreements), at an annual interest rate cost to the Fund of 0.49%, which is the weighted average interest rate cost during the fiscal year ended June 30, 2022. The actual amount of interest expense borne by the Fund will vary over time in accordance with the level of the Fund’s use of reverse repurchase agreements, dollar rolls and/or borrowings and variations in market interest rates. Borrowing expense is required to be treated as an expense of the Fund for accounting purposes. Any associated income or gains (or losses) realized from leverage obtained through such instruments is not reflected in the Annual Fund Operating Expenses table above, but would be reflected in the Fund’s performance results. |

|

Other expenses are estimated for the Fund’s fiscal year ending June 30, 2023. |

|

“Dividend Cost on Preferred Shares”, including distributions on Preferred Shares, and “Interest Payments on Borrowed Funds” are borne by the Fund separately from management fees paid to PIMCO. Excluding these expenses, Total Annual Fund Operating Expenses are 0.77%. Excluding only distributions on Preferred Shares of 0.07%, Total Annual Fund Operating Expenses are 1.13%. |

The following example illustrates the expenses that you would pay on a $1,000 investment in Common Shares of the Fund, assuming (1) that the Fund’s net assets do not increase or decrease, (2) that the Fund incurs total annual expenses of 1.20% of net assets attributable to Common Shares in years 1 through 10 (assuming assets attributable to Preferred Shares and reverse repurchase agreements representing 41.67% of the Fund’s total managed assets) and (3) a 5% annual return

(1):

|

The example above should not be considered a representation of future expenses. Actual expenses may be higher or lower than those shown. The example assumes that the estimated Interest Payments on Borrowed Funds, Dividend Cost on Preferred Shares and Other Expenses set forth in the Annual Fund Operating Expenses table are accurate, that the rate listed under Total Annual Fund Operating Expenses remains the same each year and that all dividends and distributions are reinvested at NAV. Actual expenses may be greater or less than those assumed. Moreover, the Fund’s actual rate of return may be greater or less than the hypothetical 5% annual return shown in the example. The example does not include commissions or estimated offering expenses, which would cause the expenses shown in the example to increase. |

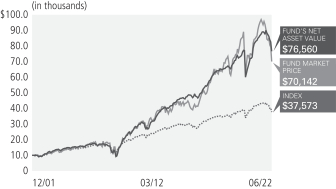

PIMCO Corporate & Income Strategy Fund

Cumulative Returns Through June 30, 2022

$10,000 invested at the end of the month when the Fund commenced operations.

Allocation Breakdown as of June 30, 2022

|

|

|

|

|

| |

|

|

40.1% |

|

| |

|

Loan Participations and Assignments |

|

|

20.7% |

|

| |

|

| |

|

|

8.9% |

|

| |

|

Non-Agency Mortgage-Backed Securities |

|

|

6.7% |

|

| |

|

| |

|

|

6.7% |

|

| |

|

| |

|

|

4.8% |

|

| |

|

| |

|

|

2.9% |

|

| |

|

| |

|

|

2.5% |

|

| |

|

Real Estate Investment Trusts |

|

|

1.7% |

|

| |

|

| |

|

|

1.6% |

|

| |

|

| |

|

|

1.6% |

|

| |

|

| |

|

|

1.5% |

|

| |

|

| |

|

|

0.3% |

|

|

|

% of Investments, at value. |

|

|

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average Annual Total Return (1) for the period ended June 30, 2022 |

|

| |

|

|

|

|

|

| |

|

|

|

1 Year |

|

|

5 Year |

|

|

10 Year |

|

|

Commencement

of Operations

(12/21/01) |

|

|

|

|

Market Price |

|

|

(26.25)% |

|

|

|

2.27% |

|

|

|

7.50% |

|

|

|

9.95% |

|

|

|

|

NAV |

|

|

(11.66)% |

|

|

|

4.47% |

|

|

|

8.87% |

|

|

|

10.42% |

|

|

|

|

ICE BofAML US High Yield Index |

|

|

(12.66)% |

|

|

|

1.95% |

|

|

|

4.40% |

|

|

|

6.67% |

|

All Fund returns are net of fees and expenses and include applicable fee waivers and/or expense limitations. Absent any applicable fee waivers and/or expense limitations, performance would have been lower and there can be no assurance that any such waivers or limitations will continue in the future.

Average annual total return since 12/31/2001.

The average annual total returns shown above have been restated from previous reports to shareholders to align with the Fund’s change from a July 31 to a June 30 fiscal year end. For the period August 1, 2021 through June 30, 2022, the Fund’s total return was

-27.59%

and

-12.65%

on a market price and NAV basis, respectfully.

It is not possible to invest directly in an unmanaged index.

|

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. The NAV presented may differ from the NAV reported for the same period in other Fund materials. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

|

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The index is not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

|

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or market price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (‘‘ROC’’) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be made on Form 1099 DIV sent to shareholders each January. |

|

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

Fund Information (as of June 30, 2022)

(1)

|

|

|

|

|

| |

|

|

$12.65 |

|

| |

|

| |

|

|

$11.60 |

|

| |

|

Premium/(Discount) to NAV |

|

|

9.05% |

|

| |

|

Market Price Distribution Rate (2) |

|

|

10.67% |

|

| |

|

| |

|

|

11.64% |

|

| |

|

Total Effective Leverage (3) |

|

|

39.08% |

|

Investment Objective and Strategy Overview

PIMCO Corporate & Income Strategy Fund’s primary investment objective is to seek high current income, with secondary objectives of capital preservation and appreciation.

The following affected performance (on a gross basis) during the reporting period:

| » |

|

Exposure to select corporate special situation positions contributed to absolute performance, as select issuers posted positive returns. |

| » |

|

Short interest rate positioning, especially in the intermediate and long end of the curve, contributed to absolute performance, as rates increased. |

| » |

|

Security selection in asset backed securities, most notably student loans, contributed to absolute performance, as select securities posted positive returns. |

| » |

|

Exposure to corporate credit detracted from absolute performance, as the asset class posted negative returns. |

| » |

|

Exposure to emerging market debt detracted from absolute performance, as the asset class posted negative returns. |

| » |

|

Exposure to municipal debt detracted from absolute performance, as the asset class posted negative returns. |

|

|

|

|

|

| |

|

Market and Net Asset Value Information |

|

|

The following table, presented in conformance with annual reporting requirements for funds that have filed a Short Form N-2, sets forth, for each of the periods indicated, the high and low closing market prices of the Fund’s Common Shares on the NYSE, the high and low NAV per Common Share and the high and low premium/discount to NAV per Common Share. See Note 3, Investment Valuation and Fair Value Measurements in the Notes to Financial Statements for information as to how the Fund’s NAV is determined.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Common share market price (1) |

|

|

Common share

net asset value |

|

|

Premium (discount) as

a % of net asset value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Quarter ended June 30, 2022 |

|

$ |

16.02 |

|

|

$ |

12.39 |

|

|

$ |

13.43 |

|

|

$ |

11.60 |

|

|

|

19.29% |

|

|

|

4.38% |

|

| Period ended March 31, 2022 (2) |

|

$ |

16.19 |

|

|

$ |

14.18 |

|

|

$ |

14.02 |

|

|

$ |

13.08 |

|

|

|

18.29% |

|

|

|

8.16% |

|

| Quarter ended January 31, 2022 |

|

$ |

18.78 |

|

|

$ |

15.44 |

|

|

$ |

14.53 |

|

|

$ |

13.97 |

|

|

|

29.34% |

|

|

|

10.04% |

|

| Quarter ended October 31, 2021 |

|

$ |

19.43 |

|

|

$ |

17.63 |

|

|

$ |

14.68 |

|

|

$ |

14.36 |

|

|

|

34.93% |

|

|

|

20.84% |

|

| Quarter ended July 31, 2021 |

|

$ |

18.99 |

|

|

$ |

17.24 |

|

|

$ |

14.56 |

|

|

$ |

14.27 |

|

|

|

30.99% |

|

|

|

20.81% |

|

| Quarter ended April 30, 2021 |

|

$ |

18.03 |

|

|

$ |

16.93 |

|

|

$ |

14.53 |

|

|

$ |

14.22 |

|

|

|

24.86% |

|

|

|

18.64% |

|

| Quarter ended January 31, 2021 |

|

$ |

17.36 |

|

|

$ |

15.68 |

|

|

$ |

14.39 |

|

|

$ |

13.02 |

|

|

|

23.42% |

|

|

|

18.56% |

|

| Quarter ended October 31, 2020 |

|

$ |

16.37 |

|

|

$ |

15.22 |

|

|

$ |

13.10 |

|

|

$ |

12.75 |

|

|

|

27.76% |

|

|

|

16.99% |

|

| Quarter ended July 31, 2020 |

|

$ |

16.74 |

|

|

$ |

14.25 |

|

|

$ |

12.74 |

|

|

$ |

11.57 |

|

|

|

33.92% |

|

|

|

19.50% |

|

| Quarter ended April 30, 2020 |

|

$ |

20.20 |

|

|

$ |

9.98 |

|

|

$ |

15.04 |

|

|

$ |

11.01 |

|

|

|

35.12% |

|

|

|

(16.35)% |

|

| Quarter ended January 31, 2020 |

|

$ |

19.86 |

|

|

$ |

18.58 |

|

|

$ |

14.90 |

|

|

$ |

14.40 |

|

|

|

35.33% |

|

|

|

26.44% |

|

| Quarter ended October 31, 2019 |

|

$ |

19.10 |

|

|

$ |

16.40 |

|

|

$ |

14.95 |

|

|

$ |

14.43 |

|

|

|

31.54% |

|

|

|

13.49% |

|

|

Such prices reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions. |

|