0001493152-17-003997.txt : 20170417

0001493152-17-003997.hdr.sgml : 20170417

20170417154218

ACCESSION NUMBER: 0001493152-17-003997

CONFORMED SUBMISSION TYPE: 10-K

PUBLIC DOCUMENT COUNT: 71

CONFORMED PERIOD OF REPORT: 20161231

FILED AS OF DATE: 20170417

DATE AS OF CHANGE: 20170417

FILER:

COMPANY DATA:

COMPANY CONFORMED NAME: KIWA BIO-TECH PRODUCTS GROUP CORP

CENTRAL INDEX KEY: 0001159275

STANDARD INDUSTRIAL CLASSIFICATION: AGRICULTURE CHEMICALS [2870]

IRS NUMBER: 870448400

STATE OF INCORPORATION: DE

FISCAL YEAR END: 1231

FILING VALUES:

FORM TYPE: 10-K

SEC ACT: 1934 Act

SEC FILE NUMBER: 000-33167

FILM NUMBER: 17764515

BUSINESS ADDRESS:

STREET 1: 310 N. INDIAN HILL BOULEVARD

STREET 2: SUITE 702

CITY: CLAREMONT

STATE: CA

ZIP: 91711

BUSINESS PHONE: 626-715-5855

MAIL ADDRESS:

STREET 1: 310 N. INDIAN HILL BOULEVARD

STREET 2: SUITE 702

CITY: CLAREMONT

STATE: CA

ZIP: 91711

FORMER COMPANY:

FORMER CONFORMED NAME: TINTIC GOLD MINING CO

DATE OF NAME CHANGE: 20010918

10-K

1

form10-k.htm

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

[X]

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended December 31, 2016

OR

[ ]

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the Transition Period from ______ to ______

Commission

File Number: 000-33167

KIWA

BIO-TECH PRODUCTS GROUP CORPORATION

(Exact

name of registrant as specified in its charter)

Nevada

77-0632186

(State

or other jurisdiction of

incorporation or organization)

(I.R.S.

Employer

Identification No.)

310

N. Indian Hill Blvd., #702

Claremont,

California 91711

(Address

of principal executive offices)

(626)

715-5855

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to

Section 12(b) of the Act:

Securities

registered pursuant to

Section

12(g) of the Act:

(Title

of Each Class)

None

Common

Stock, $0.001 par value

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. [ ]

Yes [X] No

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. [ ]

Yes [X] No

Indicate

by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports),

and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate

by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the

preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [X] Yes [ ]

No

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not

be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference

in Part III of this Form 10-K or any amendment to this Form 10-K. [ ] Yes [X] No

Indicate

by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller

reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act.

Large

accelerated filer [ ]

Accelerated

filer [ ]

Non-accelerated

filer [ ]

Smaller

reporting company [X]

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). [ ] Yes [X]

No

The

aggregate market value of voting and non-voting common stock held by non-affiliates of the registrant, based upon the closing

bid quotation for the registrant’s common stock, as reported on the OTC Markets Group, Inc., as of June 30, 2016, the last

business day of the registrant’s most recently completed second fiscal quarter, was approximately $3,557,238 (based on the

closing sale price of the common stock as reported by the OTC QB) on June 30, 2016.

The

number of shares of registrant’s common stock outstanding as of April 17, 2017 was 9,798,981.

On

one or more occasions, we may make forward-looking statements in this Annual Report on Form 10-K regarding our assumptions, projections,

expectations, targets, intentions or beliefs about future events. Words or phrases such as “anticipates,” “may,”

“will,” “should,” “believes,” “estimates,” “expects,” “intends,”

“plans,” “predicts,” “projects,” “targets,” “will likely result,”

“will continue” or similar expressions identify forward-looking statements. These forward-looking statements are only

our predictions and involve numerous assumptions, risks and uncertainties, including, but not limited to those listed below and

those business risks and factors described elsewhere in this report and our other Securities and Exchange Commission filings.

We

undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future

events or otherwise. However, your attention is directed to any further disclosures made on related subjects in our subsequent

annual and periodic reports filed with the Securities and Exchange Commission on Forms 10-K, 10-Q and 8-K and Proxy Statements

on Schedule 14A.

References

herein to “we,” “us,” “our” or “the Company” refer to Kiwa Bio-Tech Products Group

Corporation and its wholly-owned and majority-owned subsidiaries unless the context specifically states or implies otherwise.

ITEM

1. Business

The

Company

1.

Organizational History

We

are the result of a share exchange transaction completed in March 2004 between the shareholders of Tintic Gold Mining Company

(“Tintic”), a corporation originally incorporated in the state of Utah on June 14, 1933 to perform mining operations

in Utah, and the shareholders of Kiwa Bio-Tech Products Group Ltd. (“Kiwa BVI”), a company originally organized under

the laws of the British Virgin Islands on June 5, 2002. The share exchange resulted in a change of control of Tintic, with former

Kiwa BVI stockholders owning approximately 89% of Tintic on a fully diluted basis and Kiwa BVI surviving as a wholly-owned subsidiary

of Tintic. Subsequent to the share exchange transaction, Tintic changed its name to Kiwa Bio-Tech Products Group Corporation.

On July 21, 2004, we completed our reincorporation in the State of Delaware. On March 8, 2017, we completed our reincorporation

in the State of Nevada.

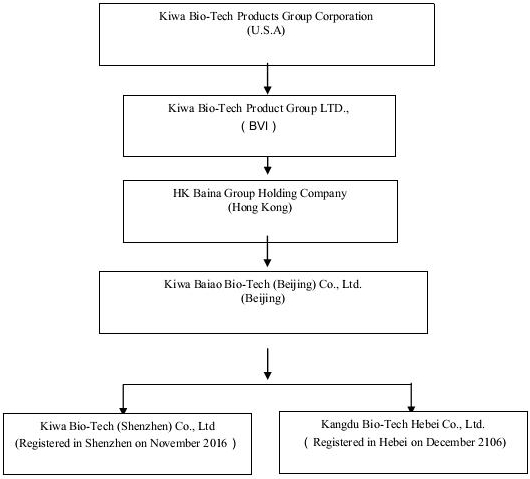

The

Company operates through a series of subsidiaries in the Peoples Republic of China as detailed in the following Organizational

Chart. The Company had previously operated its business through its subsidiaries Kiwa Bio-Tech Products (Shandong) Co., Ltd. (“Kiwa

Shandong”) and Tianjin Kiwa Feed Co., Ltd. (“Kiwa Tianjin”). Kiwa Tianjin has been dissolved since July 11,

2012. On February 11, 2017, the Company entered an Equity Transfer Agreement with Dian Shi Cheng Jing (Beijing) Technology Co.

(“Transferee”) to transfer all of shareholders’ right, title and interest in Kiwa Shandong to the Transferee

for USD $1.00. Currently, the completion of transfer is under the government processing.

3

2.

Overview of Business

We

develop, manufacture, distribute and market innovative, cost-effective and environmentally safe bio-technological products for

agriculture. Our products are designed to enhance the quality of human life by increasing the value, quality and productivity

of crops and decreasing the negative environmental impact of chemicals and other wastes.

4

Bio-fertilizers

We

have developed six bio-fertilizer products with bacillus species (“bacillus spp”) and/or photosynthetic bacteria as

core ingredients. Some of our products contain ingredients of both photosynthesis and bacillus bacteria. Bacillus spp is a species

of bacteria that interacts with plants and promotes biological processes. It is highly effective for promoting plant growth, enhancing

yield, improving quality and elevating resistances. Photosynthetic bacteria are a group of green and purple bacteria. Bacterial

photosynthesis differs from green plant photosynthesis in that bacterial photosynthesis occurs in an anaerobic environment and

does not produce oxygen. Photosynthetic bacteria can enhance the photosynthetic capacity of green plants by increasing the utilization

of sunlight, which helps keep the photosynthetic process at a vigorous level, enhances the capacity of plants to transform inorganic

materials to organic products, and boosts overall plant health and productivity.

Our

bacillus bacteria based fertilizers are protected by patents. In 2004, we acquired patent no. ZL 93101635.5 entitled “Highly

Effective Composite Bacteria for Enhancing Yield and the Related Methodology for Manufacturing” from China Agricultural

University (“CAU”) for the aggregate purchase of $480,411, consisting of $60,411 in cash and 5,000 shares of our common

stock, valued at $84.00 per share (aggregate value of $420,000). Our photosynthetic bacteria based fertilizers are also protected

by trade secret laws.

The

patent acquired from CAU covers six different species of bacillus which have been tested as bio-fertilizers to enhance yield and

plant health. The production methods of the six species are also patented. The patent has expired on February 19, 2013.There are

no limitations under this agreement on our exclusive use of the patent. Pursuant to our agreement with CAU, the University agreed

to provide research and technology support services at no additional cost to us in the event we decide to use the patent to produce

commercial products. These research and technology support services include: (1) furnishing faculty or graduate-level researchers

to help bacteria culturing, sampling, testing, trial production and production formula adjustment; (2) providing production technology

and procedures to turn the products into powder form while keeping live required bacteria in the products; (3) establishing quality

standards and quality control systems; (4) providing testing and research support for us to obtain necessary sale permits from

the Chinese government; and (5) cooperation in developing derivative products.

On

January 5, 2011, the State Intellectual Property Office of the PRC (“Intellectual Property Office”) granted Kiwa two

Certificates of Patent of Invention for (1) “A cucumber dedicated composite anti-continuous cropping effect probiotics and

their specific strains with related application” with patent number of “ZL 2008 1 0144492.6”; and (2) “Cotton

dedicated composite anti-continuous cropping effect probiotics and their special strains with related application” with

patent number of “ZL 2008 1 0144491.1” These two patents have been developed by Kiwa-CAU R&D Center. These two

patents will expire on August 5, 2028. These two patents can be used to develop specific environment-friendly bio-fertilizer.

We

have obtained five fertilizer registration certificates from the Chinese government - four covering our bacillus bacteria fertilizer

and one covering our photosynthetic bacteria fertilizer. The five registration certificates are: (1) Microorganism Microbial Inoculum

Fertilizer Registration Certificate issued by the PRC Ministry of Agriculture; (2) Photosynthetic Bacteria Fertilizer Registration

Certificate issued by the PRC Ministry of Agriculture; (3) Amino Acid Foliar Fomular Fertilizer Registration Certificate issued

by the PRC Ministry of Agriculture; (4) Organic Fertilizer Registration Certificate issued by Agriculture Department of Shandong

Province; and (5) Organic Matter-Decomposing Inoculants Registration Certificate issued by the PRC Ministry of Agriculture on

February 16, 2008. Protected by these five fertilizer registration certificates and five trademarks under the names of “KANGTAN”

(Chinese translation name for Kiwa), “ZHIGUANGYOU,” “PUGUANGFU,” “JINWA” and “KANGGUAN,”

we have developed six series of bio-fertilizer products with bacillus spp and/or photosynthetic bacteria as core ingredients.

Valid period of fertilizer registration certificates is five years and may be extended for another five years upon application

from the owner of fertilizer registration certificates. The Company has determined to re-apply the Fertilizer Registration Certificate

issued by the PRC Ministry of Agriculture.

5

Kiwa-CAU

Research and Development Center

In

July 2006, we established a new research center with CAU which is known as Kiwa-CAU Bio-Tech Research & Development Center

(the “Kiwa-CAU R&D Center”). Pursuant to an agreement between CAU and Kiwa Shandong dated November 14, 2006, Kiwa

agreed to contribute RMB 1 million (approximately $160,000) each year to fund research at Kiwa-CAU R&D Center. Under the above

agreement, the Kiwa-CAU R&D Center is responsible for fulfilling the overall research-and-development functions of Kiwa Shandong,

including: (1) development of new technologies and new products (which will be shared by Kiwa and CAU); (2) subsequent perfection

of existing product-related technologies; and (3) training quality-control personnel and technicians and technical support for

marketing activities. The Company has spent $224,704 and $178,388 for its research and development activities during the years

ended December 31, 2016 and 2015, respectively. The costs incurred by Company’s research and development activities are

not borne directly by customers.

During

fiscal 2014, Kiwa-CAU R&D Center had successfully isolated several strains of endophytic bacillus from plants. A number of

strains had been observed to have the capability of boosting crop yield and dispelling chemical pesticide residual from soil.

These strains could be used for developing not only new biological preparation but also environmental protection preparation.

Pursuant

to the agreement on joint incorporation of the research and development center between CAU and Kiwa dated November 14, 2006, Kiwa

agreed to invest RMB 1 million (approximately $160,000) each year to fund research at the R&D Center. The term of this agreement

was ten years starting from July 1, 2006. Prof. Qi Wang, who became one of our directors in July 2007, has acted as the Director

of Kiwa-CAU R&D Center since July 2006. The Company has negotiated a follow-up Cooperation Agreement for the technologies

with China Agricultural University.

On

November 5, 2015, the Company signed a strategic cooperation agreement (the “Agreement”) with China Academy of Agricultural

Science (“CAAS”)’s Institute of Agricultural Resources & Regional Planning (“IARRP”) and Institute

of Agricultural Economy & Development (“IAED”). Pursuant to the Agreement, the Company will form a strategic partnership

with the two institutes and establish an “International Cooperation Platform for Internet and Safe Agricultural Products”.

To fund the cooperation platform’s R&D activities, the Company will provide RMB 1 million (approximately $160,000) per

year to the Spatial Agriculture Planning Method & Applications Innovation Team that belongs to the Institutes. The term of

the Agreement is for three years beginning November 20, 2015. Prof. Yong Chang Wu, the authorized representative of IARRP,

CAAS, is also one of the Company’s directors effective since November 20, 2015 until March 13, 2017.

On

February 23, 2017, the Company agreed to a strategic relationship with ETS (Tianjin) Biological Science and Technology Development

Co., Ltd. (“ETS”). The partnership will include the deployment and strategic use of ETS biotechnology to produce of

bio-fertilizers for use in both China and internationally. Kiwa and ETS, together with the certain Chinese government departments,

will work together to enhance China’s microbial fertilizer industry standards and China’s food safety industry chain

standards. The parties will work together on the development of microbial technology and products in agriculture, environmental

protection, soil management and other fields. Relying on the Chinese Academy of Sciences, ETS Environmental and Agricultural Microbial

Technology Research Center and biotechnology project research results, Kiwa has introduced the ETS core technology to complete

bio-fertilizer upgrading, transformation and to develop new product lines. In order to meet the growing global consumer demand

to increase food supply and develop sustainable farming we are applying sustainable use of biotechnology and the use of biotechnology

products to replace chemical products, which will strengthen environmental protection and promote international cooperation. As

a result of strict management of many agricultural chemicals, such chemicals will continue to be abandoned, resulting is a growing

demand for bio-fertilizers. It has been widely accepted that the application of ETS biotechnology facilitates agricultural sustainability

and helps to protect the soil and improve grain output. The technology focuses on keeping soil healthy by restoring healthy microbes

that are naturally present in healthy soils. As the technology gains worldwide recognition, it is imperative to popularize bio-fertilizer

in developing countries to fulfill the needs of growing populations and promote environmentally friendly agriculture. Through

the cooperation of Kiwa and ETS, the parties aim to enhance the usage of the bio-fertilizers in China. The cooperation will bring

technological transformation and support for Kiwa to improve its existing manufacturing techniques. Kiwa and ETS will also collaborate

to establish a comprehensive platform for producing, supplying, and marketing in China. Ultimately, Kiwa would look to introduce

these products to the international market, including the United States.

6

Other

On

November 30, 2015, we entered into an acquisition agreement (the “Agreement”) with the shareholders of Caber Holdings

LTD, whose Chinese name is Hong Kong Baina Group Co., Ltd, located in Hong Kong (“Baina Hong Kong”), and Oriental

Baina Co. Ltd. (hereinafter referred to as “Baina Beijing”), Baina Hong Kong’s wholly-owned subsidiary in Beijing,

China. As a result of this Agreement, Kiwa renamed Baina Beijing to Kiwa Baiao Bio-Tech (Beijing) Co., Ltd., which replaced Kiwa

Bio-Tech (Shandong) Co., Ltd (“Kiwa Shandong”) to operate Kiwa’s bio-fertilizer market expansion and become

Kiwa’s platform for future acquisitions of new agricultural-related projects in China. In accordance with the terms of the

Agreement, Kiwa agreed to pay US$30,000 to the Baina Hong Kong Shareholders for the acquisition of 100% of the equity of Baina

Hong Kong. The Company paid RMB 220,000 (approximately $34,000) for the acquisition. The acquisition was completed on January

7, 2016. Both Baina Hong Kong and Baina Beijing had no activities before the acquisition date and had no assets and liabilities.

Thereafter,

Baina Beijing formed two new subsidiaries—Kiwa Bio-Tech (Shenzhen) Co., Ltd (Registered in Shenzhen on November 2016); Kangdu

Bio-Tech Hebei Co., Ltd. (Registered in Hebei on December 2106) to operate in specific markets in China.

On

December 17, 2015, we entered into a distribution agreement (the “Agreement”) with Kangtan Gerui (Beijing) Bio-Tech

Co., Ltd. (“Gerui”) and formally awarded Gerui a right to sell and distribute the Company’s fertilizer products

in 3 major agricultural regions of China— Hainan Province, Hunan Province and Xinjiang Autonomous Region. The Company’s

Research and Development department has been conducting application experiments in Hainan and Hunan Provinces since August 2015,

in accordance with the market requirements. The experiment data indicates that the Company’s fertilizer products have fulfilled

the requirements of reduction of content of heavy metals in soil and improved crop yield. Gerui was founded in Beijing in April

2015 and relies on the sales network of China’s Supply and Marketing Cooperatives system. Currently, the Company and Gerui

do not hold any interest in each other; however, a collaboration and integration may take place in the future. The term of the

Agreement is for a period of three years commencing December 17, 2015. In September 2016, Kiwa Baiao Bio-Tech (Beijing) Co., Ltd

obtained a fertilizer sales permit from the Chinese government and began to sale the products directly to customers in those 3

major agricultural regions. In September 2016, Kiwa Baiao Bio-Tech

(Beijing) Co., Ltd obtained a fertilizer sales permit from the Chinese government and began to sale the products directly to customers

in those 3 major agricultural regions.

7

On

February 27, 2017, the Company signed a strategic cooperation agreement with the Beijing Zhongpin Agricultural Science and Technology

Development Center (“Zhongpin Center”). Zhongpin Center is the Chinese Agricultural Science and Technology Innovation

and Development Committee’s executive implementation agency (referred to as the Agricultural Science and Technology Commission).

The Agricultural Science and Technology Commission is set up by the Chinese Central Government for the construction of the National

Ecological Security Agriculture Industrial Chain standardization system. This includes the establishment of National Ecology Safe

Agricultural Industrial Parks to build China’s Ecological Security and Agricultural Industrial in an orderly business environment,

including completion of the National Soil Remediation Program and governance of the various government functions of the institutions.

Through the guidance and support by the Zhongpin Center, Kiwa will participate and be involved in China’s National Soil

Remediation Program and construction of the National Ecological Security Agriculture Industrial Chain Standardization System’s

operation and process.

ITEM

1A. Risk Factors

Smaller

reporting companies are not required to provide the information required by this item.

8

ITEM

1B. Unresolved Staff Comments

None.

ITEM

2. Properties

In

June 2002, Kiwa Shandong entered into an agreement with Zoucheng Municipal Government granting us the use of at least 15.7 acres

in Shandong Province, China at no cost for 10 years to construct a manufacturing facility. Under the agreement, we have the option

to pay a fee of approximately RMB 480,000 (approximately $78,155) per acre for the land use right at the expiration of the 10-year

period. We may not transfer or pledge the temporary land use right. In the same agreement, we have also committed to invest approximately

$18 million to $24 million for developing the manufacturing and research facilities in Zoucheng, Shandong Province. On February

11, 2017 Kiwa Bio-Tech Products (Shandong) entered an Equity Transfer Agreement with Dian Shi Cheng Jing (Beijing) Technology

Co. (“Transferee”) to transfer all of shareholders’ right, title and interest in Kiwa Shandong to the Transferee

for USD $1.00. Currently, the completion of transfer is under the government processing.

ITEM

3. Legal Proceedings

None.

ITEM

4. Mine Safety Disclosures

Not

applicable.

Part

II

ITEM

5. Market for Registrants’ Common Equity, Related Stockholder Matters and Issuer Purchasers of Equity Securities

Market

Information

The

Company’s common stock has been quoted on the OTCQB under the symbol “KWBT” since March 30, 2004.

The

following table sets forth the high and low bid quotations per share of our common stock as reported on the OTCQB for the periods

indicated. The high and low bid quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may

not necessarily represent actual transactions. All prices are adjusted to reflect the Company’s one for 200 reverse split

which went effective January 28, 2016.

Fiscal

Year 2016

High

Low

First

Quarter

$

2.24

$

0.20

Second

Quarter

$

1.98

$

1.30

Third

Quarter

$

1.65

$

0.62

Fourth

Quarter

$

1.43

$

0.80

Fiscal

Year 2015

High

Low

First

Quarter

$

1.47

$

0.12

Second

Quarter

$

0.44

$

0.02

Third

Quarter

$

0.32

$

0.12

Fourth

Quarter

$

0.70

$

0.12

Holders

As

of December 31, 2016, there were approximately 461 shareholders of record of our common shares.

Dividend

Policy

We

have not paid any dividends on our common shares since our inception and do not anticipate that dividends will be paid at any

time in the immediate future.

Equity

Compensation Plan Information

The

information required by Item 5 regarding securities authorized for issuance under equity compensation plans is included in Item

12 of this report.

9

Recent

Sales of Unregistered Securities

The

following is a list of securities issued for cash or converted with debentures or as stock compensation to consultants during

the period from January 1, 2016 through April 14, 2017, which were not registered under the Securities Act:

Name

of Purchaser

Issue

Date

Security

Shares

Consideration

YVONNE

WANG

3/24/16

Common

240,000

Debenture

Conversion

WEI

LI

3/24/16

Common

2,900,000

Debenture

Conversion

MARK

E. CRONE

3/25/16

Common

1,000

Legal

Fees

ZENG

MIN QING

5/24/16

Common

125,000

Stock

Purchase

CHENG

TZU-YUN

5/24/16

Common

50,000

Stock

Purchase

ZHIMING

ZHU

5/24/16

Common

45,000

Stock

Purchase

HANG

ZHAO

7/20/16

Common

20,000

Stock

Purchase

SHIWEI

XIE

7/20/16

Common

10,000

Stock

Purchase

XIAOQIANG

YU

7/20/16

Common

30,000

Stock

Purchase

HANG

ZHAO

8/10/16

Common

20,000

Stock

Purchase

XIAOQIANG

YU

8/10/16

Common

10,000

Stock

Purchase

XIANGRON

CHEN

8/10/16

Common

40,000

Stock

Purchase

JIMMY

ZHOU

8/24/16

Common

101,947

Consultant

Fees

WEIHONG

SHAN

10/6/16

Common

150,000

Stock

Purchase

LIFENG

LIU

10/6/16

Common

100,000

Stock

Purchase

ZHENPING

LI

10/6/16

Common

100,000

Stock

Purchase

QI

JIANG

10/6/16

Common

550,000

Stock

Purchase

LEI

HOU

10/6/16

Common

100,000

Stock

Purchase

BING

ZHANG

10/6/16

Common

150,000

Stock

Purchase

DEMEI

YANG

10/6/16

Common

150,000

Stock

Purchase

WSMG

ADVISORS, INC.

10/6/16

Common

100,000

Consultant

Fees

EQUITIES.COM,

INC

10/6/16

Common

30,808

Consultant

Fees

GENG

LIU

10/19/16

Common

500,000

Consultant

Fees

LIXIN

TIAN

10/19/16

Common

500,000

Consultant

Fees

XU

LIU

10/19/16

Common

500,000

Consultant

Fees

QINGKE

XING

10/19/16

Common

60,000

Consultant

Fees

GROWTH

CIRCLE INC.

10/19/16

Common

20,000

Consultant

Fees

WILLIAM

FARRANCE

11/29/16

Common

125,000

Stock

Purchase

JUNWEI

ZHENG

3/3/17

Common

920,000

Stock

Purchase

YUAN

WANG

3/3/17

Common

80,000

Stock

Purchase

YUAN

WANG

3/3/17

Common

70,000

Consultant

Fees

ITEM

6. Selected Financial Data

Not

required.

ITEM

7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

This

Annual Report on Form 10-K for the fiscal year ended December 31, 2016 contains “forward-looking” statements within

the meaning of Section 21E of the Securities and Exchange Act of 1934, as amended, including statements that include the words

“believes,” “expects,” “anticipates,” or similar expressions. These forward-looking statements

include, among others, statements concerning our expectations regarding our working capital requirements, financing requirements,

business, growth prospects, competition and results of operations, and other statements of expectations, beliefs, future plans

and strategies, anticipated events or trends, and similar expressions concerning matters that are not historical facts. The forward-looking

statements in this Annual Report on Form 10-K for the fiscal year ended December 31, 2016 involve known and unknown risks, uncertainties

and other factors (described in “Business-Risk Factors” under Item 1) that could cause our actual results, performance

or achievements to differ materially from those expressed in or implied by the forward-looking statements contained herein.

Overview

The

Company took its present corporate form in March 2004 when the shareholders of Tintic Gold Mining Company, a Utah public corporation

(“Tintic”), entered into a share exchange transaction with the shareholders of Kiwa BVI, a privately-held British

Virgin Islands corporation that left the shareholders of Kiwa BVI owning a majority of Tintic and Kiwa BVI a wholly-owned subsidiary

of Tintic, see “Business - The Company” under Item 1. For accounting purposes this transaction was treated as an acquisition

of Tintic Gold Mining Company by Kiwa BVI in the form of a reverse triangular merger and a recapitalization of Kiwa BVI and its

wholly owned subsidiary, Kiwa Shandong. On July 21, 2004, we completed our reincorporation in the State of Delaware. On March

8, 2017, we completed our reincorporation in the State of Nevada.

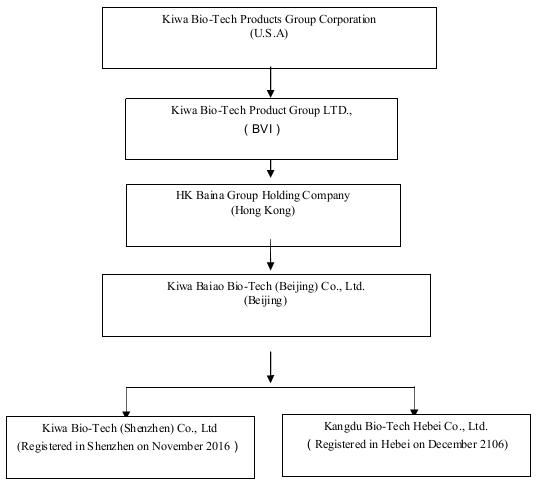

The

Company operates through a series of subsidiaries in the Peoples Republic of China as detailed in the Organizational Chart on

page 4, above. The Company had previously operated its business through its subsidiaries Kiwa Bio-Tech Products (Shandong) Co.,

Ltd. (“Kiwa Shandong”) and Tianjin Kiwa Feed Co., Ltd. (“Kiwa Tianjin”). Kiwa

Tianjin has been dissolved since July 11, 2012. On February 11, 2017, the Company entered an Equity Transfer Agreement with Dian

Shi Cheng Jing (Beijing) Technology Co. (“Transferee”) to transfer all of shareholders’ right, title and interest

in Kiwa Shandong to the Transferee for USD $1.00. Currently, the completion of transfer is under the government processing.

10

We

generated revenue in fiscal year 2016. We incurred a net income of $963,296 and a net loss $677,358 during fiscal 2016 and 2015,

respectively.

Due

to our limited revenues, we have relied on the proceeds from loans from both unrelated and related parties to provide the resources

necessary to fund the development of our business plan and operations. Our financing activities generated $1,053,358 and

$148,009 during fiscal 2016 and 2015, respectively. These funds are insufficient to execute our business plan as currently contemplated,

which may result in the risks described in “Risk Factors” under Item 1 - Business.

Going

Concern

The

consolidated financial statements have been prepared assuming that the Company will continue as a going concern, which contemplates

the realization of assets and the satisfaction of liabilities in the normal course of business.

As

of December 31, 2016, the Company’s current liabilities substantially exceeded its current assets by $5,729,622. Although

the company’s operations for the year ended December 31, 2016 resulted net income of $963,296, it had an accumulated deficit

of $19,489,400 and stockholders’ deficiency of $5,601,213 at December 31, 2016. These circumstances, among others, raise

substantial doubt about the Company’s ability to continue as a going concern. The financial statements do not include any

adjustments that might result from the outcome of this uncertainty. The financial statements also do not include any adjustments

relating to the recoverability and classification of recorded asset amounts, or amounts and classifications of liabilities that

might be necessary should the Company be unable to continue as a going concern.

The Company already raised additional fund

through equity financing and plans to raise additional funds from domestic and foreign banks and/or financial institutions to

increase working capital in order to meet capital demands. Please refer to Note 15 (Subsequent Evens) for additional information.

Trends

and Uncertainties in Regulation and Government Policy in China

Foreign

Exchange Policy Changes

China

is considering allowing its currency to be freely exchangeable for other major currencies. This change will result in greater

liquidity for revenues generated in Renminbi (“RMB”). We would benefit by having easier access to and greater flexibility

with capital generated in and held in the form of RMB. The majority of our assets are located in China and most of our earnings

are currently generated in China, and are therefore denominated in RMB. Changes in the RMB-U.S. Dollar exchange rate will impact

our reported results of operations and financial condition. In the event that RMB appreciates over the next year as compared to

the U.S. Dollar, our earnings will benefit from the appreciation of the RMB. However, if we have to use U.S. Dollars to invest

in our Chinese operations, we will suffer from the depreciation of U.S. Dollars against the RMB. On the other hand, if the value

of the RMB were to depreciate compared to the U.S. Dollar, then our reported earnings and financial condition would be adversely

affected when converted to U.S. Dollars.

On

July 21, 2005, the People’s Bank of China announced it would appreciate the RMB, increasing the RMB-U.S. Dollar exchange

rate from approximately US$1.00 = RMB 8.28 to approximately US$1.00 = RMB 8.11. So far the trend of such appreciation continues.

The exchange rate of U.S. Dollar against RMB on December 31, 2016 was US$1.00 = RMB 6.945.

Critical

Accounting Policies and Estimates

We

prepared our consolidated financial statements in accordance with accounting principles generally accepted in the United States

of America. The preparation of these financial statements requires the use of estimates and assumptions that affect the reported

amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements

and the reported amount of revenues and expenses during the reporting period. Management periodically evaluates the estimates

and judgments made. Management bases its estimates and judgments on historical experience and on various factors that are believed

to be reasonable under current circumstances. Actual results may differ from these estimates as a result of different assumptions

or conditions.

The

following critical accounting policies affect the more significant judgments and estimates used in the preparation of our consolidated

financial statements. In addition, you should refer to our accompanying audited balance sheets as of December 31, 2016 and 2015,

and the audited statements of comprehensive loss, equity movement and cash flows for the fiscal years ended December 31, 2016

and 2015, and the related notes thereto, for further discussion of our accounting policies.

Fair

value of warrants and options

We

have adopted ASC Topic 815, “Accounting for Derivative Instruments and Hedging Activities” to recognize warrants relating

to loans and warrants issued to consultants as compensation as derivative instruments in our consolidated financial statements.

11

We

also adopted ASC Topic 718, “Share Based Payment” to recognize options granted to employees as derivative instruments

in our consolidated financial statements.

We

calculate the fair value of the warrants and options using the Black-Scholes Model.

Income

Taxes

The

Company accounts for income taxes under the provisions of FASB ASC Topic 740, “Income Tax,” which requires recognition

of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the consolidated

financial statements or tax returns. Deferred tax assets and liabilities are recognized for the future tax consequence attributable

to the difference between the tax bases of assets and liabilities and their reported amounts in the financial statements. Deferred

tax assets and liabilities are measured using the enacted tax rate expected to apply to taxable income in the years in which those

temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in

tax rates is recognized in income in the period that includes the enactment date. The Company establishes a valuation when it

is more likely than not that the assets will not be recovered.

ASC

Topic 740.10.30 clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s financial statements

and prescribes a recognition threshold and measurement attribute for the financial statement recognition and measurement of a

tax position taken or expected to be taken in a tax return. ASC Topic 740.10.40 provides guidance on derecognition, classification,

interest and penalties, accounting in interim periods, disclosure, and transition. We have no material uncertain tax positions

for any of the reporting periods presented.

Major

Customers and Suppliers.

Bio-fertilizer

products

During

2016, the following were Kiwa’s major customers:

1.

Qingzhou City Agricultural Production Materials Co., Ltd. second wholesale department (11.3% of sales)

2.

Huarong County Yinfeng fertilizer industry LTD. (81% of sales)

During

2016, the following were Kiwa’s major suppliers:

1.

Weifang Druek Fertilizer Co., Ltd (92% of Subcontractor Production)

3.

Linshu Shangrun Color Printing Co., Ltd (Packing provider)

Results

of Operations

Net

Sales

Net

sales were $9,617,845 and $0 for the years ended December 31, 2016 and 2015, respectively.

Cost

of Sales

Cost

of sales was $7,672,451 and $0 for the years ended December 31, 2016 and 2015, respectively.

Gross

Profit/Loss

Gross

profit for fiscal 2016 was $1,945,394 compared to $0 for fiscal 2015.

Licensing

Revenue

Licensing

revenue totaled $786,329 for the year ended December 31, 2016.

General

and Administrative

General

and administrative expenses were $874,097 and $313,589 for the years ended December 31, 2016 and 2015, respectively, an increase

of $560,508 or 178%. General and administrative expenses include professional fees, officers’ compensation, depreciation

and amortization, salaries, travel and entertainment, rent, office expense and telephone expense etc.

12

Research

and Development

Research

and development expenses increased significantly by $45,445 or 25% to $224,433 for the year ended December 31, 2016, compared

to $178,988 for the prior comparable period. Research and development expense mainly consists of the expenses of maintaining Kiwa-CAU

R&D Center, which began operation in July 2006 (see “Business-Intellectual Property and Product Lines- Kiwa-CAU R&D

Center” under Item 1 in Part I). On November 5, 2015, the Company signed a strategic cooperation agreement (the “Agreement”)

with China Academy of Agricultural Science (“CAAS”)’s Institute of Agricultural Resources & Regional Planning

(“IARRP”) and Institute of Agricultural Economy & Development (“IAED”). Pursuant to the Agreement,

the Company will form a strategic partnership with the two institutes and establish an “International Cooperation Platform

for Internet and Safe Agricultural Products”. To fund the cooperation platform’s R&D activities, the Company will

provide RMB 1 million (approximately $160,000) per year to the Spatial Agriculture Planning Method & Applications Innovation

Team that belongs to the Institutes. During the years ended December 31, 2016 and 2015, the Company accrued $224,433

and $178,988 for research and development respectively.

Penalty

Expense

We

charged $77,575 and $72,512 of liquidated damages in connection with the 6% Notes to penalty expenses during the years ended December

31, 2016 and 2015, respectively. The increase of penalty expense was mainly due to accrued and unpaid interest on the 6% Notes.

Interest

Expenses

Net

interest expense was $112,977 and $112,629 in the fiscal years of 2016 and 2015, respectively, representing a increase

of $348 or 0.3%.

Net

Income & (Loss)

During

the fiscal year 2016, net income was $963,296, comparing with net loss $677,358 for the same period of 2015, representing an

increase of $1,640,654.

Comprehensive

Gain & (Loss)

Comprehensive

income increased by $1,446,652 from $(253,293) for fiscal 2015, as compared to $1,193,359 for the comparable year of 2016.

Liquidity

and Capital Resources

Since

inception of our ag-biotech business in 2002, we have relied on the proceeds from the sale of our equity securities and loans

from both unrelated and related parties to provide the resources necessary to fund our operations and the execution of our business

plan. During fiscal 2016 and 2015, we raised $1,053,358 and $148,009 in total from stock purchase agreements and related

party loans. To some extent, these advances improved our short-term liquidity. However, as of December 31, 2016, our current

liabilities substantially exceeded current assets by $5,729,622, reflecting a current ratio of 0.4451, whereas current

liabilities exceeded current assets by $11,103.261, reflecting a current ratio of 0.0043 as of December 31, 2015.

During the years ended December 31, 2016 and 2015, we did not issue any shares resulting from the conversion of principal of the

6% Notes into our common stock.

13

As

of December 31, 2016 and 2015, we had cash of $13,469 and $721, respectively. The change is outlined as follows:

During

the fiscal year of 2016, net cash used in our operating activities was $1,142,9741,

compared to $150,208 for the comparable period of 2015. Such cash was mainly used for maintaining operations of a public company

and working capital for our bio-fertilizer business.

During

the fiscal year of 2016, we incurred approximately $79,083 in investment activity, including $34,112 in acquiring a subsidiary.

During

the year ended December 31, 2016, we generated cash inflow for $1,053,358 from financing activities, compared to $148,009 of cash

inflow during the year ended December 31, 2015, from financing activities.

As

of December 31, 2016, we had an accumulated deficit of $19,489,400, down from $20,324,812 deficit at December 31, 2015, as a result

of a net income of $967,296 including $127,884 for statutory reserve for the year ended December 31, 2016 and compared to a net

loss of $677,358 for 2015.

We

still require additional working capital to accomplish our business objectives and to sustain our operations. Continuously, we

intend to raise additional capital through the issuance of debt or equity securities to fund the development of our planned business

operations, although there can be no assurance that we will be successful in obtaining this financing. The following factors,

among others, may significantly harm our ability to obtain required additional financing.

Given

the facts that:

(1)

Outstanding

6% Notes. As of December 31, 2016, the amount of outstanding 6% Notes was $150,250. The 6% Notes have been in default

since June 2009.

(2)

Outstanding

note payable of $360,000 as of December 31, 2016. This note has been in default since July 2007.

Contractual

Obligations

(1)

Operation of Kiwa-CAU R&D Center

Pursuant

to the agreement on joint incorporation of the research and development center between CAU and Kiwa Shandong dated November 14,

2006, Kiwa Shandong agrees to invest RMB 1 million (approximately $160,000) each year to fund research at the R&D Center.

The term of this agreement is ten years starting from July 1, 2006. Prof. Qi Wang, who became one of our directors in July 2007,

has acted as the Director of Kiwa-CAU R&D Center since July 2006.

(2)

Investment in manufacturing and research facilities in Zoucheng, Shandong Province in China

According

to the Project Agreement with Zoucheng Municipal Government in 2002, we have committed to investing approximately $18 million

to $24 million for developing the manufacturing and research facilities in Zoucheng, Shandong Province. As of December 31, 2016,

we had invested approximately $1.91 million for the project. On

February 11, 2017, the Company entered an Equity Transfer Agreement with Dian Shi Cheng Jing (Beijing) Technology Co. (“Transferee”)

to transfer all of shareholders’ right, title and interest in Kiwa Shandong to the Transferee for USD $1.00. Currently,

the completion of transfer is under the government processing.

14

(3)

Strategic cooperation with two institutes in China

On

November 5, 2015, the Company signed a strategic cooperation agreement (the “Agreement”) with China Academy of Agricultural

Science (“CAAS”)’s Institute of Agricultural Resources & Regional Planning (“IARRP”) and Institute

of Agricultural Economy & Development (“IAED”). Pursuant to the Agreement, the Company will form a strategic partnership

with the two institutes and establish an “International Cooperation Platform for Internet and Safe Agricultural Products”.

To fund the cooperation platform’s R&D activities, the Company will provide RMB 1 million (approximately $160,000) per

year to the Spatial Agriculture Planning Method & Applications Innovation Team that belongs to the Institutes. The term of

the Agreement is for three years beginning November 20, 2015.

(4)

Acquisition of Caber Holdings LTD (Hong Kong Baina Group Co. LTD) in China

On

November 30, 2015, we entered into an acquisition agreement (the “Agreement”) with the shareholders of Caber Holdings

LTD, whose Chinese name is Hong Kong Baina Group Co., Ltd, located in Hong Kong (“Baina Hong Kong”), and Oriental

Baina Co. Ltd. (hereinafter referred to as “Baina Beijing”), Baina Hong Kong’s wholly-owned subsidiary in Beijing,

China. When this acquisition is completed, Kiwa will rename Baina Beijing to Kiwa Baiao Bio-Tech (Beijing) Co., Ltd. Kiwa Baiao

Co. Ltd will replace Kiwa’s current subsidiary in China - Kiwa Bio-Tech (Shandong) Co., Ltd (“Kiwa Shandong”)

- to operate Kiwa’s bio-fertilizer market expansion and become Kiwa’s platform for future acquisitions of new agricultural-related

projects in China. In accordance with the terms of the Agreement, Kiwa agreed to pay US$30,000 to the Baina Hong Kong Shareholders

for the acquisition of 100% of the equity of Baina Hong Kong. As of December 31, 2015, the Company has paid RMB 220,000 (approximately

$34,000) for the acquisition. The acquisition was completed on January 7, 2016. Both Baina Hong Kong and Baina Beijing had no

activities before the acquisition date and had no assets and liabilities. Thereafter, Baina Beijing formed two new subsidiaries—Kiwa

Bio-Tech (Shenzhen) Co., Ltd (Registered in Shenzhen on November 2016); Kangdu Bio-Tech Hebei Co., Ltd. (Registered in Hebei on

December 2106) to operate in specific markets in China.

(5)

Distribution agreement with Kangtan Gerui Bio-Tech in China

On

December 17, 2015, Kiwa Bio-Tech Products Group Corporation (the “Company”) entered into a distribution agreement

(the “Agreement”) with Kangtan Gerui (Beijing) Bio-Tech Co., Ltd. (“Gerui”) and formally awarded Gerui

a right to sell and distribute the Company’s fertilizer products in 3 major agricultural regions of China— Hainan

Province, Hunan Province and Xinjiang Autonomous Region. The Company’s Research and Development department has been conducting

application experiments in Hainan and Hunan Provinces since August 2015, in accordance with the market requirements. The experiment

data indicates that the Company’s fertilizer products have fulfill the requirements of reduction of content of heavy metals

in soil and improve crop yield. Gerui was founded in Beijing in April 2015 and relies on the sales network of China’s Supply

and Marketing Cooperatives system. Currently, the Company and Gerui do not hold any interest in each other; however, a collaboration

and integration may take place in the future. The term of the Agreement is for a period of three years commencing December 17,

2015. In September 2016, Kiwa Baiao Bio-Tech (Beijing) Co., Ltd obtained a fertilizer sales permit from the Chinese government

and began to sale the products directly to customers in those 3 major agricultural regions.

(6)

Lease payments

(1)

On April 29, 2016, Kiwa Baiao Bio-Tech (Beijing) Co., Ltd. entered an office lease agreement with two-year team. Monthly lease

payment and building management fee totaled RMB 77,867 or approximately USD $11,622.

(2)

On November 11, 2017, Kiwa Baiao Bio-Tech (Beijing) Co., Ltd. entered an apartment lease agreement for its employees. The lease

term is one year with monthly lease payment of RMB 6,000 or approximately USD $896.

(3)

In March 1, 2017, Kiwa Bio-Tech (Shenzhen) Co., Ltd, a newly established subsidiary entered an office lease agreement with one-year

term. Monthly lease payment is RMB 29,000 or approximately of USD $4,320.

Off-Balance

Sheet Arrangements

At

December 31, 2016, we did not have any relationships with unconsolidated entities or financial partnerships, such as entities

often referred to as structured finance or special purpose entities, established for the purpose of facilitating off-balance sheet

arrangements or other contractually narrow or limited purposes. As such, we are not exposed to any financing, liquidity, market

or credit risk that could arise had we engaged in such relationships.

Recent

Accounting Pronouncements

See

Note 2 to the Consolidated Financial Statements under Item 8, Part II.

15

ITEM

7A. Quantitative and Qualitative Disclosures about Market Risk

Not

required.

ITEM

8. Financial Statements and Supplementary Data

The

full text of our audited consolidated financial statements as of December 31, 2016 and 2015 begins on page F-1 of this annual

report.

ITEM

9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

On

February 15, 2017, the Board of Directors of Kiwa Bio-Tech Products Group Corporation (“Kiwa” or “Company”)

decided to engage DYH & Co. as independent principal accountant and auditor to report on the Company’s financial statements

for the fiscal year ended December 31, 2016, including performing the required quarterly reviews.

In

conjunction with the new engagement, the Company has dismissed its former accountant, Paritz & Co., P.A., Hackensack, NJ (“Paritz”),

as the Company’s principal accountant effective February 22, 2016. Paritz has served the Company well since 2013. Under

Item 304 of Regulation S-K, the reason for the auditor change is dismissal, not resignation nor declining to stand for re-election.

During

the two most recent fiscal years and the interim period through the date of the dismissal, there were no disagreements with Paritz

on any matter of accounting principles or practices, financial statement disclosure or auditing scope or procedure, which disagreements,

if not resolved to Paritz’s satisfaction, would have caused Paritz to make reference to the subject matter of the disagreements

in connection with its reports.

ITEM

9A. Controls and Procedures

Disclosure

Controls and Procedures

Our

management, under the supervision and with the participation of our Chief Executive Officer (“CEO”) and Chief Financial

Officer (“CFO”), has evaluated the effectiveness of our disclosure controls and procedures as defined in SEC Rules

13a-15(e) and 15d-15(e) as of the end of the period covered by this Annual Report. Our disclosure controls and procedures are

designed to ensure that information required to be disclosed in the reports we file or submit under the Securities Exchange Act

of 1934 (“Exchange Act”) is recorded, processed, summarized, and reported within the time periods specified in the

SEC’s rules and forms, and that such information is accumulated and communicated to our management including our CEO and

CFO, to allow timely decisions regarding required disclosures. Based on their evaluation, our CEO and CFO have concluded that,

as of December 31, 2016, our disclosure controls and procedures were ineffective.

Management

Report on Internal Control over Financial Reporting

Our

management is responsible for establishing and maintaining adequate internal control over financial reporting, as such term is

defined in Exchange Act Rules 13a-15(f) and 15d-15(f). Our internal control over financial reporting was designed to provide reasonable

assurance to the Company’s management and board of directors regarding the preparation and fair presentation of published

consolidated financial statements. Internal control over financial reporting is promulgated under the Exchange Act as a process

designed by, or under the supervision of, the Company’s principal executive and principal financial officers and effected

by the Company’s board of directors, management and other personnel, to provide reasonable assurance regarding the reliability

of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted

accounting principles. Internal control over financial reporting, no matter how well designed, has inherent limitations and may

not prevent or detect misstatements. Therefore, even effective internal control over financial reporting can only provide reasonable

assurance with respect to the financial statement preparation and presentation.

Our

management has conducted, with the participation of our CEO and CFO, an assessment, including testing of the effectiveness, of

our internal control over financial reporting as of December 31, 2016. Management’s assessment of internal control over

financial reporting was conducted using the criteria in Internal Control over Financial Reporting - Guidance for Smaller Public

Companies issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”). Based on such evaluation,

management identified deficiencies that were determined to be a material weakness.

A

material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there

is a reasonable possibility that a material misstatement of the company’s annual or interim financial statements will not

be prevented or detected on a timely basis. Because of the material weakness described below, management concluded that our internal

control over financial reporting was ineffective as of December 31, 2016.

16

The

specific material weakness identified by the Company’s management as of December 31, 2016 is described as follows:

●

The

Company did not have sufficient and skilled accounting personnel with an appropriate level of technical accounting knowledge

and experience in the application of accounting principles generally accepted in the United States of America commensurate

with the Company’s financial reporting requirements, which resulted in a number of internal control deficiencies that

were identified as being significant. The Company’s management determined that the number and nature of these significant

deficiencies, when aggregated, constituted a material weakness.

●

The

Company lacks qualified resources to perform the internal audit functions properly. In addition, the scope and effectiveness

of the Company’s internal audit function are yet to be developed.

●

We

currently do not have an audit committee.

Remediation

Initiative

●

We

are committed to establishing the internal audit functions but due to limited qualified resources in the region, we were not

able to hire sufficient internal audit resources before the end of 2016. However, internally we established a central management

center to recruit more senior qualified people in order to improve our internal control procedures. Externally, we are looking

forward to engaging an accounting firm to assist the Company in improving the Company’s internal control system based

on COSO Framework.

●

We

intend to establish an audit committee of the board of directors as soon as practicable. We envision that the audit committee

will be primarily responsible for reviewing the services performed by our independent auditors, evaluating our accounting

policies and our system of internal controls.

Conclusion

Despite

the material weakness and deficiencies reported above, the Company’s management believes that its consolidated financial

statements included in this report fairly present in all material respects the Company’s financial condition, results of

operations and cash flows for the periods presented and that this report does not contain any untrue statement of a material fact

or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements

were made, not misleading with respect to the period covered by this report.

This

Annual Report does not include an attestation report of the Company’s registered public accounting firm regarding internal

control over financial reporting. Management’s report was not subject to attestation by the Company’s registered public

accounting firm pursuant to temporary rules of the SEC that permit the Company to provide only management’s report in this

Annual Report.

Changes

in Internal Control over Financial Reporting

There

were no changes in our internal control over financial reporting during the fiscal year ended December 31, 2016 that materially

affected, or are reasonably likely to materially affect, our internal control over financial reporting.

ITEM

9B. Other Information

None.

17

Part

III

ITEM

10. Directors, Executive Officers and Corporate Governance

Directors

and Executive Officers

Set

forth below are the names of our directors and executive officers, their ages, their offices with us, if any, their principal

occupations or employment for the past five years. The directors listed below will serve until the Company’s next annual

meeting of the stockholders:

Name

Age

Position

Director

Since

Yvonne

Wang

39

Acting

President, CEO and CFO and Director

2015

Feng

Li

28

Secretary

and Director

2015

Qi

Wang

49

Vice

President of Technology, Director

2007

Yong

Lin Song

Xiao

Qiang Yu

50

39

CTO,

Director of Technology and Director

Sales

and Marketing Director

2017

2016

Yvonne

Wang Ms. Wang became our Chairman in November 2015. She served as corporate Secretary from 2005 to 2015. Prior to 2005,

she served as an executive assistant and a manager of the Company’s U.S. office between April 2003 and September 2005. She

obtained her B.S. degree of Business Administration from University of Phoenix.

On

August 11, 2106 became Company’s acting president, CEO and CFO.

Feng

Li became our Secretary and a Director in 2015. From 2011- 2012, Ms. Li has served as an assistant project manager for

SCHSAsia, a boutique business consulting firm specializing in events and project management for overseas company wishing to expand

into the Asia Pacific arena. From 2012 until 2014, Ms. Li served as a campaigner for WildAid China Office, a non-profit organization

with focus on raising public awareness on wildlife and climate change related issues.

Qi

Wang became our Vice President - Technical on July 19, 2005 and was elected as one of our directors of the Company on

July 18, 2007. Prof. Wang has also acted as Director of Kiwa-CAU R&D Center since July 2006. Prof. Wang served as a Professor

and Advisor for Ph.D. students in the Department of Plant Pathology, China Agricultural University (“CAU”) since January

2005. Prior to that, he served as an assistant professor and lecturer of CAU since June 1997. He obtained his master degree and

Ph.D. in agricultural science from CAU in July 1994 and July 1997, respectively. Prof. Wang received his bachelor’s degree

of science from Inner Mongolia Agricultural University in July 1989. He is a committee member of various scientific institutes

in China, including the National Research and Application Center for Increasing-Yield Bacteria, Chinese Society of Plant Pathology,

Chinese Association of Animal Science and Veterinary Medicine. Prof. Wang’s unique expertise in the field of agriculture

offers significant knowledge and experience to the Board of Directors when making critical operational decisions.

Yong

Lin Song became our CTO and Director of Technology responsible for the Company’s R&D operations on March 2016

and as one of our directors of the Company on March 2017. Mr. Song is a senior agronomist at the Institute of Agricultural Resources

and Regional Planning, Chinese Academy of Agricultural Sciences. He has 29 years of experience in microbial R&D and technology

promotion and has led many national agricultural projects. In 2001, he was responsible for technological achievement transformation

and technology promotion of Agricultural Resources and Regional Planning, Chinese Academy of Agricultural Sciences. In 2009, he

served as deputy secretary general of the Chinese Society of Plant Nutrition and Fertilizer Science.

Xiao

Qiang Yu became our Sales and Marketing Director on June 2016 and is responsible for managing the overall marketing strategy

of Kiwa, which includes brand expansion, sale targets, strategic planning and corporate communications. Mr. Yu participated in

Chinese fertilizer market since 1999. Mr. Yu has over 15 years of marketing, management and strategy experience from two major

fertilizer companies in China.

18

Family

Relationships

There

are no family relationships among our directors or executive officers.

Involvement

in Certain Legal Proceedings

None

of our directors or executive officers has, during the past ten years:

(a)

Had

any bankruptcy petition filed by or against any business of which such person was a general partner or executive officer either

at the time of the bankruptcy or within two years prior to that time;

(b)

Been

convicted in a criminal proceeding or subject to a pending criminal proceeding;

(c)

Been

subject to any order, judgment, or decree, not subsequently reversed, suspended or vacated, of any court of competent jurisdiction

or any federal or state authority, permanently or temporarily enjoining, barring, suspending or otherwise limiting his involvement

in any type of business, securities, futures, commodities or banking activities; and

(d)

Been

found by a court of competent jurisdiction (in a civil action), the Securities and Exchange Commission or the Commodity Futures

Trading Commission to have violated a federal or state securities or commodities law, and the judgment has not been reversed,

suspended, or vacated.

Section

16(a) Beneficial Ownership Compliance

Section

16(a) of the Securities Exchange Act of 1934 requires our officers, directors and certain persons holding more than 10 percent

of a registered class of our common stock to file with the SEC initial reports of ownership and reports of changes in ownership

of our common stock. Officers, directors and certain other shareholders are required by the SEC to furnish the Company with copies

of all Section 16(a) forms they file. To the best of the Company’s knowledge, based solely upon a review of the copies of

such reports, the Company believes that all Section 16(a) filing requirements applicable to its officers, directors and certain

other shareholders were complied with during the fiscal year ended December 31, 2016.

Code

of Ethics

We

have adopted a Code of Business Conduct and Ethics (the “Code”) that is applicable to all employees, consultants and

members of the Board of Directors, including the Chief Executive Officer, Chief Financial Officer and Secretary. This Code embodies

our commitment to conduct business in accordance with the highest ethical standards and applicable laws, rules and regulations.

We will provide any person a copy of the Code, without charge, upon written request to the Company’s Secretary. Requests

should be addressed in writing to Ms. Yvonne Wang; 310 N. Indian Hill Blvd., #702 Claremont, California 91711.

Board

Composition; Audit Committee and Financial Expert

Our

Board of Directors is currently composed of four members: Yvonne Wang, Feng Li, Qi Wang and Yong Lin Song. All board actions require

the approval of a majority of the directors in attendance at a meeting at which a quorum is present.

19

We

currently do not have an audit committee. We intend, however, to establish an audit committee of the board of directors as soon

as practicable. We envision that the audit committee will be primarily responsible for reviewing the services performed by our

independent auditors, evaluating our accounting policies and our system of internal controls. Currently such functions are performed

by our Board of Directors.

The

Board does not have a “financial expert” as defined by SEC rules implementing Section 407 of the Sarbanes-Oxley Act.

Board

meetings and committees; annual meeting attendance.

During

fiscal year 2016, the Board of Directors did not have any meetings.

ITEM

11. Executive Compensation

We

currently have no Compensation Committee. The Board of Directors is currently performing the duties and responsibilities of Compensation

Committee. In addition, we have no formal compensation policy. We decide on our executives’ compensation based on average

compensation levels of similar companies in the U.S. or China, depending on consideration of many factors such as where the executive

works. Our Chief Executive Officer’s compensation is approved by the Board of Directors. Other named executive officers’

compensation are proposed by our Chief Executive Officer and approved by the Board of Directors.

Our

Stock Incentive Plan is administered by the Board of Directors. Any amendment to our Stock Incentive Plan requires majority approval

of the stockholders of the Company.

The

Company had no officers or directors whose total compensation during either 2016 or 2015 exceeded $100,000.

Currently,

the main forms of compensation provided to each of our executive officers are: (1) annual salary; (2) non-equity Incentive Plan;

and (3) the granting of incentive stock options subject to approval by our Board of Directors.

Summary

Compensation Table

Summary

Compensation Table

Name

and principal position

Year

Salary

($)

Bonus

($)

Stock

Awards ($)

Option

Awards ($)

Non-Equity

Incentive Plan Compensation ($)

Nonqualified

Deferred Compensation Earnings

($)

All

Other Compensation

($)

Total

($)

(a)

(b)

(c)

(d)

(e)

(f)

(g)

(h)

(i)

(j)

Yvonne

Wang,

2016

84,000

Nil

Nil

Nil

Nil

Nil

Nil

84,000

Acting

President, CEO and CFO

2015

51,000

Nil

Nil

Nil

Nil

Nil

Nil

51,000

Yong

Lin Song,

2016

29,828

Nil

Nil

Nil

Nil

Nil

Nil

29,828

CTO,

Director of Technology

2015

Nil

Nil

Nil

Nil

Nil

Nil

Nil

Nil

Xiao

Qiang Yu,

2016

30,259

Nil

Nil

Nil

Nil

Nil

Nil

30,259

Sales

and Marketing Director

2015

Nil

Nil

Nil

Nil

Nil

Nil

Nil

Nil

Employment

Contracts and Termination of Employment and Change of Control Arrangements

There

are no compensatory plans or arrangements with respect to a named executive officer that would result in payments or installments

in excess of $100,000 upon the resignation, retirement or other termination of such executive officer’s employment with

us or from a change-in-control.

20

Stock

Incentive Plan and Option Grants

2016

Stock Incentive Plan

On

March 8, 2017, pursuant to the consent of the holders of a majority of the votes entitled to be cast on the matter, were approved

of the Kiwa Bio-Tech Products Group Corporation 2016 Employee, Director and Consultant Stock Plan. The Plan is a key aspect of

our compensation program, designed to attract, retain, and motivate the highly qualified individuals required for our long-term

success.

No

options were granted under the Plan during 2016.

Option

Exercises and Stock Vested

No

stock options were exercised by any officers or directors during 2016 and 2015. We did not adjust or amend the exercise price

of any stock options previously awarded to any named executive officers during 2016 and 2015.

21

Director

Compensation for 2016

We

currently have no policy in effect for providing compensation to our directors for their services on our Board of Directors, and

did not compensate our directors in 2016 for services performed as directors.

ITEM

12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

The

following table sets forth as of April 7, 2017 certain information with respect to the beneficial ownership of our common stock

by (i) each of our executive officers, (ii) each person who is known by us to beneficially own more than 5% of our outstanding

common stock, and (iii) all of our directors and executive officers as a group. Percentage ownership is calculated based on 9,798,981

shares of our common stock and 500,000 shares of our Series A Preferred Stock outstanding as of April 7, 2017. None of the shares

listed below are issuable pursuant to stock options or warrants of the Company.

Title

of class

Name

and Address of Beneficial Ownership(1)

Amount

and Nature of Beneficial Owner (2)

Percentage

of class

Common

Stock

Yvonne

Wang

240,000

2.45

%

Common

Stock

Feng

Li (3)

1,965,326

20.06

%

Common

Stock

Qi

Wang

-

-

Common

Stock

Yong

Lin Song

-

-

Common

Stock

All

officers and directors as a group

2,205,326

22.51

%

Ser.

A Pref. Stock

Yvonne

Wang

250,000

50.00

%

Ser.

A Pref. Stock

Feng

Li

250,000

50.00

%

Ser.

A Pref. Stock

All

officers and directors as a group

500,000

100.00

%

5% Holders:

Common

Stock

Troniya

Industrial Incubator, Inc.

1,000,000

10.21

%

Common

Stock

Liu

Geng

500,000

5.10

%

Common

Stock

Liu

Xu

500,000

5.10

%

Common

Stock

Tian

Lixin

500,000

5.10

%

Common

Stock

Zheng

JunWei

920,000

9.39

%

Common

Stock

Wei

Li (3)

1,965,326

20.06

%

(1)

The

address for all holders is 310 N. Indian Hill Blvd, #702, Claremont, CA 91711.

(2)

In

determining beneficial ownership of our Common Stock and Series A Preferred Stock, the number of shares shown includes shares

which the beneficial owner may acquire upon exercise of debentures, warrants and options which may be acquired within 60 days.

Unless otherwise stated, each beneficial owner has sole power to vote and dispose of its shares.

(3)

Includes

61,784 shares of common stock held by All Star Technology, Inc., a British Virgin Islands international business company.

Feng Li’s father, Wei Li, exercises voting and investment control over the shares held by All Star Technology, Inc.

Wei Li is a principal stockholder of All Star Technology, Inc. and may be deemed to beneficially own such shares, but disclaims

beneficial ownership in such shares held by All Star Technology, Inc. except to the extent of his pecuniary interest therein.

Mr. Li has pledged all of his common stock of the Company as collateral security for the Company’s obligations under

certain 6% Convertible Notes owed by the Company.

22

Change

in Control

None.

ITEM

13. Certain Relationships and Related Transactions, and Director Independence

For

description of transactions with related parties, see Note 6 to Consolidated Financial Statements under Item 8 in Part II.

Under

the independence standard set forth in Rule 4200(a) (15) of the Market Place Rules of the Nasdaq Stock Market, which is the independence

standard that we have chosen to report under.

ITEM

14. Principal Accountant Fees and Services

Fees

Paid to Independent Public Accountants for 2016 and 2015.

Audit

Fees

All

of the services described below were approved by our board of directors prior to performance of such services. The board of directors