UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________

FORM 10-K

________________________________________________

For the fiscal year ended December 31 , 2022

For the transition period from ________ to ________.

Commission file number 001-16797

________________________

(Exact name of registrant as specified in its charter)

________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices) (Zip Code)

(540 ) 362-4911

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol | Name of each exchange on which registered | ||||||||||||

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Registration S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of the last business day of the registrant’s most recently completed second fiscal quarter, July 16, 2022, the aggregate market value of common stock held by non-affiliates of the registrant was $11,302,276,702 , based on the last sales price on July 16, 2022, as reported by the New York Stock Exchange.

As of February 24, 2023, the number of shares of the registrant’s common stock outstanding was 59,273,781 shares.

Documents Incorporated by Reference:

| TABLE OF CONTENTS | |||||||||||

Page | |||||||||||

FORWARD-LOOKING STATEMENTS

Certain statements herein are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are usually identifiable by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “intend,” “likely,” “may,” “plan,” “position,” “possible,” “potential,” “probable,” “project,” “should,” “strategy,” “will,” or similar language. All statements other than statements of historical fact are forward-looking statements, including, but not limited to, statements about our strategic initiatives, operational plans and objectives, expectations for economic conditions and recovery and future business and financial performance, as well as statements regarding underlying assumptions related thereto. Forward-looking statements reflect our views based on historical results, current information and assumptions related to future developments. Except as may be required by law, we undertake no obligation to update any forward-looking statements made herein. Forward-looking statements are subject to a number of risks and uncertainties that could cause actual results to differ materially from those projected or implied by the forward-looking statements. They include, among others, factors related to the company’s leadership transition, the timing and implementation of strategic initiatives, including with respect to labor shortages or disruptions and the impact on our ability to complete store openings, deterioration of general macroeconomic conditions, the highly competitive nature of our industry, demand for our products and services, complexities in our inventory and supply chain and challenges with transforming and growing our business. Please refer to “Item 1A. Risk Factors” included in this report and other filings made by us with the Securities and Exchange Commission (“SEC”) for a description of these and other risks and uncertainties that could cause actual results to differ materially from those projected or implied by the forward-looking statements.

1

PART I

Item 1. Business.

Unless the context otherwise requires, “Advance,” “we,” “us,” “our,” and similar terms refer to Advance Auto Parts, Inc., its subsidiaries and their respective operations on a consolidated basis. Our fiscal year consists of 52 or 53 weeks ending on the Saturday closest to December 31st of each year. Our fiscal years ended December 31, 2022 (“2022”) and January 1, 2022 (“2021”) included fifty-two weeks of operations. Our fiscal year ended January 2, 2021 (“2020”) included fifty-three weeks of operations.

Overview

We are a leading automotive aftermarket parts provider in North America, serving both professional installers (“professional”) and “do-it-yourself” (“DIY”) customers, as well as independently owned operators. Our stores and branches offer a broad selection of brand names, original equipment manufacturer (“OEM”) and owned brand automotive replacement parts, accessories, batteries and maintenance items for domestic and imported cars, vans, sport utility vehicles and light and heavy duty trucks. As of December 31, 2022, we operated 4,770 total stores and 316 branches primarily under the trade names “Advance Auto Parts,” “Carquest” and “Worldpac.”

We were founded in 1929 as Advance Stores Company, Incorporated, and operated as a retailer of general merchandise until the 1980s. During the 1980s, we began targeting the sale of automotive parts and accessories to DIY customers. We initiated our professional delivery program in 1996 and have steadily increased our sales to professional customers since 2000. We have grown significantly as a result of strategic acquisitions, new store openings and comparable store sales growth. Advance Auto Parts, Inc., a Delaware corporation, was incorporated in 2001 in conjunction with the acquisition of Discount Auto Parts, Inc. In 2014, we acquired General Parts International, Inc. (“GPI”), a privately held company that was a leading distributor and supplier of original equipment and aftermarket automotive replacement products for professional markets operating under the Carquest and Worldpac trade names.

Stores and Branches

Key factors in selecting sites and market locations in which we operate include population, demographics, traffic count, vehicle profile, competitive landscape and the cost of real estate. During 2022, 144 stores and branches were opened and 30 were closed or consolidated, resulting in a total of 5,086 stores and branches as of December 31, 2022 compared with a total of 4,972 stores and branches as of January 1, 2022.

Through our integrated operating approach, we serve our professional and DIY customers through a variety of channels ranging from traditional “brick and mortar” store locations to self-service e-commerce sites. We believe we are better able to meet our customers’ needs by operating under several trade names, which are as follows:

Advance Auto Parts — Our 4,440 stores, inclusive of 328 hubs, as of December 31, 2022 are generally located in freestanding buildings with a focus on both professional and DIY customers. The average size of an Advance Auto Parts store is approximately 7,800 square feet. These stores carry a wide variety of products serving aftermarket auto part needs for both domestic and import vehicles. Our Advance Auto Parts stores carry a product offering of approximately 23,000 stock keeping units (“SKUs”), consisting of a custom mix of products based on each store’s unique market. Supplementing our stores’ inventory on-hand, less common SKUs are also available on a same-day or next-day basis from any of our larger hub stores.

Carquest — Our 330 stores as of December 31, 2022, including 148 stores in Canada, are generally located in freestanding buildings with a primary focus on professional customers, but also serve DIY customers. The average size of a Carquest store is approximately 7,300 square feet. These stores carry a wide variety of products serving the aftermarket auto part needs for both domestic and import vehicles with a product offering of approximately 25,000 SKUs. As of December 31, 2022, Carquest also serves 1,311 independently owned stores that operate under the Carquest name.

Worldpac — Our 316 branches, of which 135 are branded Autopart International (“AI”), as of December 31, 2022 principally serve professional customers utilizing an efficient and sophisticated online ordering and fulfillment system. Worldpac’s branches are generally larger than our other store locations, averaging approximately 18,400 square feet. Worldpac’s complete product offering includes over 285,000 SKUs for domestic and import vehicles and specializes in imported OEM parts. As part of our transformation efforts through December 31, 2022, we have converted all AI stores into the Worldpac technology format.

2

Store Development

The key factors used in selecting sites and market locations in which we operate include population, demographics, traffic count, vehicle profile, number and strength of competitors’ stores, and the cost of real estate. As of December 31, 2022, 4,915 stores and branches were located in 48 U.S. states and two U.S. territories, and 171 stores and branches were located in nine Canadian provinces.

We serve our stores and branches primarily from our principal corporate offices in Raleigh, NC and Roanoke, VA. We also maintain store support centers in Newark, CA and Norton, MA.

Our Products

The following table shows some of the types of products that we sell by major category:

| Parts & Batteries | Accessories & Chemicals | Engine Maintenance | ||||||

| Batteries and battery accessories | Air conditioning chemicals and accessories | Air filters | ||||||

| Belts and hoses | Air fresheners | Fuel and oil additives | ||||||

| Brakes and brake pads | Antifreeze and washer fluid | Fuel filters | ||||||

| Chassis parts | Electrical wire and fuses | Grease and lubricants | ||||||

| Climate control parts | Electronics | Motor oil | ||||||

| Clutches and drive shafts | Floor mats, seat covers and interior accessories | Oil filters | ||||||

| Engines and engine parts | Hand and specialty tools | Part cleaners and treatments | ||||||

| Exhaust systems and parts | Lighting | Transmission fluid | ||||||

| Hub assemblies | Performance parts | |||||||

| Ignition components and wire | Sealants, adhesives and compounds | |||||||

| Radiators and cooling parts | Tire repair accessories | |||||||

| Starters and alternators | Vent shades, mirrors and exterior accessories | |||||||

| Steering and alignment parts | Washes, waxes and cleaning supplies | |||||||

| Wiper blades | ||||||||

We provide our customers with quality products that are often offered at a good, better or best recommendation differentiated by price and quality. We accept customer returns for many new, core and warranty products. Customer returns have historically been immaterial.

Our Customers

Our professional customers consist primarily of customers for whom we deliver products from our store or branch locations to their places of business, including garages, service stations and auto dealers. Our professional sales represented approximately 59%, 58% and 57% of our sales in 2022, 2021 and 2020. We also serve 1,311 independently owned Carquest stores with shipments directly from our distribution centers. Our DIY customers are primarily served through our stores, but can also order online to pick up merchandise at a conveniently located store or have their purchases shipped directly to them. Except where prohibited, we also provide a variety of services at our stores free of charge to our customers, including:

•Battery and wiper installation;

•Check engine light scanning;

•Electrical system testing, including batteries, starters and alternators;

•Oil and battery recycling; and

•Loaner tool programs.

We also serve our customers online at www.AdvanceAutoParts.com or on our Advance Mobile App. Our professional customers can conveniently place their orders electronically, including through MyAdvance.com and Technet, by phone or in-store, and we deliver products from our stores or branch locations to their places of business.

3

Supply Chain

Our supply chain consists of a network of distribution centers, hubs, stores, and branches that enable us to provide same-day or next-day availability to our customers. As of December 31, 2022, we operated 50 distribution centers, ranging in size from approximately 57,000 to 943,000 square feet with total square footage of approximately 12.6 million, including one distribution center dedicated to reclamations. In 2022, we closed distribution centers in Riverside, California and Anchorage, Alaska.

Merchandise, Marketing and Advertising

In 2022, we purchased merchandise from over 1,400 vendors, with no single vendor accounting for more than 10% of purchases. Our purchasing strategy involves negotiating agreements to purchase merchandise over a specified period of time along with other provisions, including pricing, rebates, volume and payment terms.

Our merchandising strategy is to carry a broad selection of high quality and reputable brand name automotive parts and accessories that we believe will appeal to our professional customers and also generate DIY customer traffic. Some of our brands include Bosch®, Castrol®, Dayco®, Denso®, Fram®, Gates®, Meguiar’sTM, Mobil 1TM, Moog®, Monroe®, NGK®, Prestone®, Purolator®, Trico® and Wagner®. In addition to these branded products, we stock a wide selection of high-quality owned brand products with a goal of appealing to value-conscious customers. These categories of merchandise include chemicals, interior automotive accessories, batteries and parts under various owned brand names such as Autopart International®, Carquest®, DieHard®, Driveworks® and Wearever®. For the DieHard® brand, we own the right to sell batteries and to extend the DieHard® brand into other automotive and vehicular categories. We granted the seller an exclusive royalty-free, perpetual license to develop, market and sell DieHard® branded products in certain non-automotive categories.

Our marketing and advertising program is designed to drive brand awareness, consideration by consumers and omnichannel traffic by position in the aftermarket auto parts category. We strive to exceed our customers’ expectations end-to-end through a comprehensive online and in-store pick up experience, extensive parts assortment, quality brands, experienced parts professionals, professional programs that are designed to build loyalty with our customers and our DIY customer loyalty program. Our DIY campaign was developed around a multi-channel communications plan that brings together radio, television, digital marketing, social media, sponsorships, store execution, public relations and Speed Perks (our customer loyalty program).

Seasonality

Our business is somewhat seasonal in nature, with the highest sales usually occurring in the spring and summer months. In addition, our business can be affected by weather conditions. While unusually heavy precipitation tends to soften sales as elective maintenance is deferred during such periods, extremely hot or cold weather tends to enhance sales by causing automotive parts to fail at an accelerated rate. Our fourth quarter is generally our most volatile as weather and spending trade-offs typically influence our professional and DIY sales.

Human Capital Management

We believe our People are Our Best Part, and we have adopted six Cultural Beliefs to help us foster a culture that fully engages our team members with our business: Speak Up, Be Accountable, Take Action, Move Forward, Grow Talent and Champion Inclusion. Our Cultural Belief of Grow Talent highlights the importance to us of developing our team members in their careers, and we seek to not only recruit the best talent, but also retain and promote the best talent. Through another Cultural Belief, Champion Inclusion, we seek to fully leverage the ideas and talents of all our team members in caring for our customers and each other. We encourage our team members to Speak Up and promote their engagement through a variety of programs and networks within our organization.

As of December 31, 2022, we employed approximately 40,000 full-time team members and approximately 27,000 part-time team members. Our workforce consisted of 82% of our team members employed in store-level operations, 13% in distribution and 5% in our corporate offices. As of December 31, 2022, approximately 2% of our team members were represented by labor unions.

Additional information about our human capital resources can be found in our Corporate Sustainability and Social Report, which is available on our website. Our Corporate Sustainability and Social Report is not, and will not be deemed to be, a part of this Annual Report on Form 10-K or incorporated by reference into any of our other filings with the Securities and Exchange Commission (“SEC”).

4

Intellectual Property

We own a number of trade names, service marks and trademarks, including “Advance Auto Parts®,” “Advance Same Day®,” “Autopart International®,” “Carquest®,” “CARQUEST Technical Institute®,” “DieHard®,” “DriverSide®,” “MotoLogic®,” “MotoShop®,” “speedDIAL®,” “TECH-NET Professional Auto Service®” and “Worldpac®” for use in connection with the automotive parts business. In addition, we own and have registered a number of trademarks for our owned brands. We believe that these trade names, service marks and trademarks are important to our merchandising strategy. We do not know of any infringing uses that would materially affect the use of these trade names and trademarks and we actively defend and enforce them.

Competition

We operate in both the professional and DIY markets of the automotive aftermarket industry. Our primary competitors are (i) both national and regional chains of automotive parts stores, including AutoZone, Inc., NAPA, O’Reilly Automotive, Inc., The Pep Boys-Manny, Moe & Jack and Auto Plus (formerly Uni-Select USA, Inc.), (ii) internet-based retailers, (iii) discount stores and mass merchandisers that carry automotive products, (iv) wholesalers or jobbers stores, including those associated with national parts distributors or associations, (v) independently owned stores and (vi) automobile dealers that supply parts. We believe that chains of automotive parts stores that, like us, have multiple locations in one or more markets, have competitive advantages in customer service, marketing, inventory selection, purchasing and distribution compared with independent retailers and jobbers that are not part of a chain or associated with other retailers or jobbers. The principal methods of competition in our business include brand recognition, customer service, product offerings, availability, quality, service with speed, price and store location.

Environmental and Other Regulatory Matters

We are subject to various federal, state and local laws and governmental regulations relating to the operation of our business, including those governing collection, transportation and recycling of automotive lead-acid batteries, used motor oil and other recyclable items and ownership and operation of real property. We sell products containing hazardous materials as part of our business. In addition, our customers may bring automotive lead-acid batteries, used motor oil or other recyclable items onto our properties. We currently provide collection and recycling programs for used lead-acid batteries, used oil and other recyclable items at a majority of our stores as a service to our customers. Pursuant to agreements with third-party vendors, lead-acid batteries, used motor oil and other recyclable items are collected by our team members, deposited onto pallets or into vendor supplied containers and stored by us until collected by the third-party vendors for recycling or proper disposal. The terms of our contracts with third-party vendors require that they are in compliance with all applicable laws and regulations. Our third-party vendors who arrange for the removal, disposal, treatment or other handling of hazardous or toxic substances may be liable for the costs of removal or remediation at any affected disposal, treatment or other site affected by such substances. Based on our experience, we do not believe that there are any material environmental costs associated with the current business practice of accepting lead-acid batteries, used oil and other recyclable items as these costs are borne by the respective third-party vendors.

We own and lease real property. Under various environmental laws and regulations, a current or previous owner or operator of real property may be liable for the cost of removal or remediation of hazardous or toxic substances on, under or in such property. These laws often impose joint and several liability and may be imposed without regard to whether the owner or operator knew of, or was responsible for, the release of such hazardous or toxic substances. Other environmental laws and common law principles also could be used to impose liability for releases of hazardous materials into the environment or work place, and third parties may seek recovery from owners or operators of real properties for personal injury or property damage associated with exposure to released hazardous substances. From time to time, we receive notices from the U.S. Environmental Protection Agency and state environmental authorities indicating that there may be contamination on properties we own, lease or operate or may have owned, leased or operated in the past or on adjacent properties for which we may be responsible. Compliance with these laws and regulations and clean-up of released hazardous substances have not had, and do not anticipate to have, a material impact on our operations.

We are also subject to numerous regulations including those related to labor and employment, discrimination, anti-bribery/anti-corruption, product quality and safety standards, data privacy and taxes. Compliance with any such laws and regulations has not had a material adverse effect on our operations to date. For more information, see the following disclosures in “Part I. Item 1A. Risk Factors” elsewhere in this report.

5

Available Information

Our Internet address is www.AdvanceAutoParts.com. Our website and the information contained therein or linked thereto are not part of this Annual Report on Form 10-K for 2022. We make available free of charge through our Investor Relations website, located at ir.advanceautoparts.com, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements, registration statements and amendments to those reports filed or furnished pursuant to the Securities Exchange Act of 1934 (“Exchange Act”) as soon as reasonably practicable after we electronically file such materials with, or furnish them to the SEC. The SEC maintains a website that contains reports, proxy statements and other information regarding issuers that file electronically with the SEC. These materials may be obtained electronically by accessing the SEC’s website at www.sec.gov.

6

Item 1A. Risk Factors.

You should consider carefully the risks and uncertainties described below together with the other information included in this Annual Report on Form 10-K, including without limitation our consolidated financial statements and related notes thereto and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations - Critical Accounting Policies”. The occurrence of any of the following risks could materially adversely affect our business, financial condition, results of operations, cash flows and future prospects, which could in turn materially affect the price of our common stock.

Risks Related to Our Operations and Growth Strategy

If we are unable to successfully implement our business strategy, our business, financial condition, results of operations and cash flows could be adversely affected.

We have identified several initiatives as part of our business strategy to increase sales, expand margins, drive accelerated growth and deliver top quartile results relative total shareholder return. We are currently making and expect to continue to make significant investments to pursue our strategic initiatives. If we are unable to implement our strategic initiatives efficiently and effectively, our business, financial condition, results of operations and cash flows could be adversely affected. We could also be adversely affected if we have not appropriately prioritized and balanced our initiatives or if we are unable to effectively manage change throughout our organization. Implementing strategic initiatives could disrupt or reduce the efficiency of our operations and may not provide the anticipated benefits, or may provide them on a delayed schedule or at a higher cost. These risks increase when significant changes are undertaken.

If we are unable to successfully implement our growth strategy, keep existing store locations or open new locations in desirable places on favorable terms, it could adversely affect our business, financial condition, results of operations and cash flows.

We intend to continue to expand the markets we serve as part of our growth strategy, which may include opening new stores or branches, as well as expansion of our online business. We may also grow our business through strategic acquisitions. As we expand our market presence, it becomes more critical that we have consistent and effective execution across all of our locations and brands. There is uncertainty about the profitability of newly opened locations, including whether newly opened stores will harm the profitability or comparable store sales of existing locations. The newly opened and existing locations’ profitability will depend on the competition we face as well as our ability to properly stock, market and price the products desired by customers in these markets. The actual number and format of any new locations to be opened and the success of our growth strategy will depend on a number of factors, including, among other things:

•the availability of desirable locations;

•the negotiation of acceptable lease or purchase terms for new locations;

•the availability of financial resources, including access to capital at cost-effective interest rates;

•our ability to expand our online offerings and sales; and

•our ability to manage the expansion and to hire, train and retain qualified team members.

We compete with other retailers and businesses for suitable locations for our stores. Local land use and zoning regulations, environmental regulations and other regulatory requirements may impact our ability to find suitable locations and influence the cost of constructing, renovating and operating our stores. In addition, real estate, zoning, construction and other delays may adversely affect store openings and renovations and increase our costs. For example, during 2021 through 2022 we experienced significant delays associated with our planned opening of new locations in California, primarily as a result of permitting challenges, and such delays increased our costs and resulted in significant lost sales opportunities. Further, changing local demographics at existing store locations may adversely affect revenue and profitability levels at those stores. The termination or expiration of leases at existing store locations may adversely affect us if the renewal terms of those leases are unacceptable to us and we are forced to close or relocate stores. If we determine to close or relocate a store subject to a lease, we may remain obligated under the applicable lease for the balance of the lease term. In addition to potentially incurring costs related to lease obligations, we may also incur employee-related severance or other facility closure costs for stores that are closed or relocated.

7

Omnichannel growth in our business is complex and if we are unable to successfully maintain a relevant omnichannel experience for our customers, our sales and results of operations could be adversely impacted.

Our business has become increasingly omnichannel as we strive to deliver a seamless shopping experience to our customers through both online and in-store shopping experiences. Operating an e-commerce platform is a complex undertaking and exposes us to risks and difficulties frequently experienced by internet-based businesses, including risks related to our ability to attract and retain customers on a cost-effective basis and our ability to operate, support, expand and develop our internet operations, website, mobile applications and software and other related operational systems. Continuing to improve our e-commerce platform involves substantial investment of capital and resources, increasing supply chain and distribution capabilities, attracting, developing and retaining qualified personnel with relevant subject matter expertise and effectively managing and improving the customer experience. Omnichannel and e-commerce retail are competitive and evolving environments. Insufficient, untimely or inadequately prioritized or ineffectively implemented investments could significantly impact our profitability and growth and affect our ability to attract new customers, as well as maintain our existing ones.

Enhancing the customer experience through omnichannel programs such as buy-online-pickup-in-store, new or expanded delivery options, the ability to shop through a mobile application or other similar programs depends in part on the effectiveness of our inventory management processes and systems, the effectiveness of our merchandising strategy and mix, our supply chain and distribution capabilities, and the timing and effectiveness of our marketing activities, particularly our promotions. Costs associated with implementing omnichannel initiatives may be higher than expected, and the initiatives may not result in increased sales, including same store sales, customer traffic, customer loyalty or other anticipated results. Website downtime and other technology disruptions in our e-commerce platform, including interruptions due to cyber-related issues or natural disasters, as well as supply and distribution delays and other related issues may affect the successful operation of our e-commerce platform. If we are not able to successfully operate or improve our e-commerce platform and omnichannel business, we may not be able to provide a relevant shopping experience or improve customer traffic, sales or margins, and our reputation, operations, financial condition, results of operations and cash flows could be materially adversely affected.

If we are unable to successfully integrate future acquisitions into our existing operations or implement joint ventures or other strategic relationships, it could adversely affect our business, financial condition, results of operations and cash flows.

We expect to continue to make strategic acquisitions and enter into strategic relationships as an element of our growth strategy. Acquisitions, joint ventures and other strategic relationships involve certain risks that could cause our growth and profitability to differ from our expectations. The success of these acquisitions and relationships depends on a number of factors, including but not limited to:

•our ability to continue to identify and acquire suitable targets or strategic partners, or to acquire additional companies or enter into strategic relationships, at favorable prices and/or with favorable terms;

•our ability to obtain the full benefits envisioned by strategic transactions or relationships;

•the risk that management’s attention may be distracted;

•our ability to attract and retain key personnel;

•our ability to successfully integrate the operations and systems of the acquired companies, and to achieve the strategic, operational, financial or other anticipated synergies of the acquisition or other transaction or relationship;

•the performance of our strategic partners;

•significant transaction or integration costs that may not be offset by the synergies or other benefits achieved in the near term or at all;

•additional operational risks, such as those associated with doing business internationally or expanding operations into new territories, geographies or channels, that may become applicable to us; and

•loss contingencies that we may assume or become subject to, whether known or unknown, of acquired companies, which could relate to past, present or future facts, events, circumstances or occurrences.

8

If we experience difficulties implementing various information systems, our ability to conduct our business could be negatively impacted.

We are dependent on information systems to facilitate the day-to-day operations of the business and to produce timely, accurate and reliable information on financial and operational results. We are in the process of implementing and updating various information systems. These implementations will require significant investment of human and financial resources, and we may experience significant delays, increased costs and other difficulties with these projects. Any significant disruption or deficiency in the design and implementation of these information systems could adversely affect our ability to process orders, ship products, send invoices and track payments, fulfill contractual obligations or otherwise operate our business. While we have invested meaningful resources in planning, project management and training, additional and significant implementation issues may arise as we integrate onto these new information systems that may disrupt our operations and negatively impact our business, financial condition, results of operations, cash flows and internal controls structure.

If we are unable to maintain adequate supply chain capacity and improve supply chain efficiency, we will not be able to expand our business, which could adversely affect our business, financial condition, results of operations and cash flows.

Our store inventories are primarily replenished by shipments from our network of distribution centers, warehouses and hub stores. As we expand our market presence, we will need to increase efficiency and maintain adequate capacity of our supply chain network in order to achieve the business goal of reducing inventory costs while improving availability and movement of goods throughout our supply chain to meet consumer product needs and channel preferences. We continue to streamline and optimize our supply chain network and systems. If our investments in our supply chain do not provide the anticipated benefits, we could experience sub-optimal inventory levels, inventory availability or increases in our costs, which could adversely affect our business, financial condition, results of operations and cash flows.

We are dependent on our suppliers to supply us with products that comply with safety and quality standards at competitive prices.

We are dependent on our vendors continuing to supply us with quality products on payment terms that are favorable to us. If our merchandise offerings do not meet our customers’ expectations regarding safety, innovation and quality, we could experience lost sales, increased costs and exposure to legal and reputational risk. Our suppliers are subject to applicable product safety laws, and we are dependent on them to ensure that the products we buy comply with all safety and quality standards. We have also established standards for product safety and quality and workplace standards that we require all our suppliers to meet. We do not condone human trafficking, forced labor, child labor, harassment or abuse of any kind, and we expect our suppliers to operate within these same principles. Our ability to find qualified suppliers who can supply products in a timely and efficient manner that meet our standards can be challenging. Events that give rise to actual, potential or perceived product safety concerns could expose us to government enforcement action and private litigation and result in costly product recalls and other liabilities. Suppliers may also fail to invest adequately in design, production or distribution facilities, may reduce their customer incentives, advertising and promotional activities or change their pricing policies. To the extent our suppliers are subject to additional government regulation of their product design and/or manufacturing processes, the cost of the merchandise we purchase may rise. In addition, negative customer perceptions regarding the safety or quality of the products we sell could cause our customers to seek alternative sources for their needs, resulting in lost sales. In those circumstances, it may be difficult and costly for us to regain the confidence of our customers.

Our reliance on suppliers, including freight carriers and other third parties in our global supply chain, subjects us to various risks and uncertainties which could adversely affect our financial results.

We source the products we sell from a wide variety of domestic and international suppliers, and place significant reliance upon various third parties to transport, store and distribute those products to our distribution centers, stores and customers. Our financial results depend on us securing acceptable terms with our suppliers for, among other things, the price of merchandise we purchase from them, funding for various forms of promotional programs, payment terms and provisions covering returns and factory warranties. To varying degrees, our suppliers may be able to leverage their competitive advantages - for example, their financial strength, the strength of their brand with customers, their own stores or online channels or their relationships with other retailers - to our commercial disadvantage. Generally, our ability to negotiate favorable terms with our suppliers is more difficult with suppliers for whom our purchases represent a smaller proportion of their total revenues, consequently impacting our profitability from such vendor relationships. If we encounter any of these issues with our suppliers, our business, financial condition, results of operations and cash flows could be adversely impacted.

9

In addition, our suppliers, including those within our global supply chain, are impacted by global conditions that in turn may impact our ability to source merchandise at competitive prices or timely supply product at levels adequate to meet consumer demand. For example, the recent surges in consumer demand, shortages of raw materials and disruptions to the global supply chain resulting from lack of carrier capacity, labor shortages, port congestion and/or closures, amongst other factors, have negatively impacted costs and inventory availability and may continue to have a negative impact on future results and profitability. As suppliers increase prices charged to us for products, including transportation and distribution, as a result of these or other factors, it may negatively impact our results. If we experience transitions or changeover with any of our significant vendors, or if they experience financial difficulties or otherwise are unable to deliver merchandise to us on a timely basis, or at all, we could have product shortages in our stores that could adversely affect customers’ perceptions of us and cause us to lose customers and sales.

We depend on the services of many qualified executives and other team members, whom we may not be able to attract, develop and retain.

Our success, to a significant extent, depends on the continued engagement, services and experience of our executives and other team members. We may not be able to retain our current executives and other key team members or attract and retain additional qualified executives and team members who may be needed in the future. Our ability to attract, develop and retain an adequate number of qualified team members depends on factors such as employee morale, our reputation, competition from other employers, availability of qualified personnel, our ability to offer competitive compensation and benefit packages and our ability to maintain a safe working environment. For example, during 2021 and 2022, we experienced unusually low availability of workers, which we believe was primarily attributable to COVID-19-pandemic-related factors, and in turn has created increased competition in labor markets. Disruptions and heightened competition may increase our costs, impact our ability to serve customers and otherwise affect our business operations. We also believe our future success will depend in part upon our ability to attract and retain highly skilled personnel for whom the market is highly competitive, particularly for individuals with certain types of technical skills. Failure to recruit or retain qualified employees may impair our efficiency and effectiveness and our ability to pursue growth opportunities. Additionally, turnover in executive or other key positions can disrupt progress in implementing business strategies, result in a loss of institutional knowledge, cause other team members to take on substantially more responsibility which results in greater workload demands and diverting attention away from key areas of the business, or otherwise negatively impact our growth prospects or future operating results. In February 2023, our President and Chief Executive Officer informed our Board of his intention to retire from his position at the end of the year. Leadership transitions can be inherently difficult to manage, and uncertainty regarding future leadership at our organization or inadequate transition of our Chief Executive Officer may increase the risk of turnover in executive or other key positions, negatively impact our ability to recruit and retain talent, cause disruption to our business or hinder our planning, execution and future performance.

We operate in a competitive labor market and there is a risk that market increases in compensation could have an adverse effect on our profitability. Market or government regulated increases to employee hourly wage rates, along with our ability to implement corresponding adjustments within our labor model and wage rates, could have a significant impact to the profitability of our business. In addition, approximately 2% of our team members are represented by unions. If these team members were to engage in a strike, work stoppage, or other slowdown, or if the terms and conditions in labor agreements were renegotiated, we could experience a disruption in our operations and higher ongoing labor costs. If we fail or are unable to maintain competitive compensation, our customer service and execution levels could suffer by reason of a declining quality of our workforce, which could adversely affect our business, financial condition, results of operations and cash flows.

Because we are involved in litigation from time to time, and are subject to numerous laws and governmental regulations, we could incur substantial judgments, fines, legal fees and other costs.

We are sometimes the subject of complaints or litigation, which may include class action litigation from customers, team members or others for various actions. From time to time, we are involved in litigation involving claims related to, among other things, breach of contract, tortious conduct, employment, discrimination, breach of laws or regulations (including The Americans With Disabilities Act), payment of wages, exposure to asbestos or potentially hazardous product, real estate and product defects. The damages sought against us in some of these litigation proceedings are substantial. Although we maintain liability insurance for some litigation claims, if one or more of the claims were to greatly exceed our insurance coverage limits or if our insurance policies do not cover a claim, this could have a material adverse effect on our business, financial condition, results of operations and cash flows. For instance, we are subject to numerous lawsuits alleging injury as a result of exposure to asbestos-containing products (see Note 13. Contingencies, of the Notes to the Consolidated Financial Statements included herein).

10

We are subject to numerous federal, state and local laws and governmental regulations relating to, among other things, environmental protection, product quality and safety standards, building and zoning requirements, labor and employment, discrimination, anti-bribery/anti-corruption, data privacy and income taxes. Compliance with existing and future laws and regulations could increase the cost of doing business and adversely affect our results of operations. If we fail to comply with existing or future laws or regulations, we may be subject to governmental or judicial fines or sanctions while incurring substantial legal fees and costs as well as reputational risk. In addition, our capital and operating expenses could increase due to remediation measures that may be required if we are found to be noncompliant with any existing or future laws or regulations.

We work diligently to maintain the privacy and security of our customers, suppliers, team members and business information and the functioning of our computer systems, website and other online offerings. In the event of a security breach or other cyber security incident, we could experience adverse operational effects or interruptions and/or become subject to legal or regulatory proceedings, any of which could lead to damage to our reputation in the marketplace and substantial costs.

The nature of our business requires us to receive, retain and transmit certain personally identifiable information about our customers, suppliers and team members, some of which is entrusted to third-party service providers. While we have taken and continue to undertake significant steps to protect such personally identifiable information and other confidential information and to protect the functioning of our computer systems, website and other online offerings, a compromise of our data security systems or those of businesses we interact with could result in information related to our customers, suppliers, team members or business being obtained by unauthorized persons or adverse operational effects or interruptions, which could have a material adverse effect on our business, financial condition, results of operations and cash flows. We develop, maintain and update processes and systems in an effort to try to prevent this from occurring, but these actions are costly and require constant, ongoing attention as technologies change, privacy and information security regulations change, and efforts to overcome security measures by bad actors continue to become ever more sophisticated. The cost of complying with stricter and more complex data privacy (such as the California Consumer Privacy Act, which grants expanded rights to access and delete personal information and opt out of certain personal information sharing), data collection and information security laws and standards could also be significant to us. Such laws and standards may also increase our responsibility and liability in relation to personal data that we process, and we may be required to put in place additional mechanisms ensuring compliance with privacy laws and regulations.

Despite our efforts, our security measures may be breached in the future due to a cyber attack, computer malware viruses, exploitation of hardware and software vulnerabilities, team member error, malfeasance, fraudulent inducement (including so-called “social engineering” attacks and “phishing” scams) or other acts. While we have experienced threats to our data and systems, including phishing attacks, to date we are not aware that we have experienced a material cyber-security breach that has in any manner hindered our operational capabilities or resulted in a known data breach. Unauthorized parties may in the future obtain access to our data or the data of our customers, suppliers or team members or may otherwise cause damage to or interfere with our equipment, our data and/or our network including our supply chain. While we maintain insurance coverage that may, subject to policy terms and conditions, cover certain aspects of cyber risks, such insurance coverage may be insufficient to cover losses in any particular situation. Any breach, damage to or interference with our equipment or our network, or unauthorized access in the future could result in significant operational difficulties including legal and financial exposure and damage to our reputation that could potentially have an adverse effect on our business. While we also seek to obtain assurances that others we interact with will protect confidential information, there is always the risk that the confidentiality or accessibility of data held or utilized by others may be compromised. If a compromise of our data security or function of our computer systems or website were to occur, it could have a material adverse effect on our operating results and financial condition and possibly subject us to additional legal, regulatory and operating costs and damage our reputation in the marketplace.

Business interruptions may negatively impact our store hours, operability of our computer systems and the availability and cost of merchandise, which may adversely impact our sales and profitability.

Hurricanes, tornadoes, earthquakes or other natural disasters, war or acts of terrorism, public health issues or pandemics or the threat of any of these incidents or others, may have a negative impact on our ability to obtain merchandise to sell in our stores, result in certain of our stores being closed for an extended period of time, negatively affect the lives of our customers or team members, or otherwise negatively impact our operations. Some of our merchandise is imported from other countries. If imported goods become difficult or impossible to import into the United States due to business interruption (including regulation of exporting or importing), and if we cannot obtain such merchandise from other sources at similar costs and without an adverse delay, our sales and profit margins may be negatively affected.

In the event that commercial transportation, including the global shipping industry, is curtailed or substantially delayed, our business may be adversely impacted as we may have difficulty receiving merchandise from our suppliers and/or transporting it to our stores.

11

Terrorist attacks, warfare, geopolitical unrest, or uncertainty or insurrection involving any oil producing country could result in an abrupt increase in the price of crude oil, gasoline and diesel fuel. Such price increases would increase the cost of doing business for us and our suppliers, and also negatively impact our customers’ disposable income, causing an adverse impact on our business, sales, profit margins and results of operations.

We rely extensively on our computer systems and the systems of our business partners to manage inventory, process transactions and report results. These systems are subject to damage or interruption due to various reasons such as power outages, telecommunication failures, computer viruses, security breaches, malicious cyber attacks and catastrophic events or occasional system breakdowns related to ordinary use or wear and tear. If our computer systems or those of our business partners fail, we may experience loss of critical data and interruptions or delays in our ability to process transactions and manage inventory. Any significant business interruptions may make it difficult or impossible to continue operations, and any disaster recovery or crisis management plans we may employ may not suffice in any particular situation to avoid a significant adverse impact to our business, financial condition and our results of operations.

Risks Related to Our Industry and the Business Environment

If overall demand for the products we sell declines, our business, financial condition, results of operations and cash flows will suffer. Decreased demand could also negatively impact our stock price.

Overall demand for products we sell depends on many factors and may decrease due to any number of reasons, including:

•a decrease in the total number of vehicles on the road or in the number of annual miles driven or significant increase in the use of ride sharing services, because fewer vehicles means less maintenance and repairs, and lower vehicle mileage, which decreases the need for maintenance and repair;

•the economy, because as consumers reduce their discretionary spending by deferring vehicle maintenance or repair, sales may decline and as new car purchases increase, the number of cars requiring maintenance and repair may decrease;

•the weather, because milder weather conditions may lower the failure rates of automobile parts while extended periods of rain and winter precipitation may cause our customers to defer elective maintenance and repair of their vehicles; additionally, overall climate changes could create greater variability in weather events, which may result in greater volatility for our business, or lead to other significant weather conditions that could impact our business;

•the average duration of vehicle manufacturer warranties and average age of vehicles driven, because newer cars typically require fewer repairs and will be repaired by the manufacturers’ dealer networks using dealer parts pursuant to warranties (which have gradually increased in duration and/or mileage expiration over the recent past), while vehicles that are seven years old and older are generally no longer covered under manufacturers’ warranties and tend to need more maintenance and repair;

•an increase in internet-based retailers, because potentially favorable prices and ease of use of purchasing parts via other websites on the internet may decrease the need for customers to visit and purchase their aftermarket parts from our physical stores and may cause fewer customers to order aftermarket parts on our website;

•technological advances, including the rate of adoption of electric vehicles, hybrid vehicles, ride sharing services, alternative modes of transportation, autonomously driven vehicles and future legislation related thereto, and the increase in the quality of vehicles manufactured, because vehicles that need less frequent maintenance or have lower part failure rates will require less frequent repairs using aftermarket parts and, in the case of electric and hybrid vehicles, do not require or require less frequent oil changes; and

•the refusal of vehicle manufacturers to make available diagnostic, repair and maintenance information to the automotive aftermarket industry that our professional and DIY customers require to diagnose, repair and maintain their vehicles, because this may force consumers to have a majority of diagnostic work, repairs and maintenance performed by the vehicle manufacturers’ dealer networks.

We may be adversely affected by legal, regulatory or market responses regarding technological adaptation in the automotive industry.

Policy makers in the U.S. may enact legislative or regulatory proposals that would impose mandatory requirements on greenhouse gas emissions and encourage more rapid adoption of vehicles that minimize emissions. Such laws, if enacted, are likely to impact our business in a number of ways. For example, significant increases in fuel economy requirements, new federal or state restrictions on emissions of carbon dioxide or new federal or state incentive programs that may be imposed on vehicles and automobile fuels could adversely affect annual miles driven, purchases of used vehicles that are likely to have a higher need for maintenance and repair, or the relevancy of the products we sell to new vehicles coming into production. We

12

may not be able to accurately predict, prepare for and respond to new kinds of technological innovations with respect to electric vehicles and other technologies that minimize emissions. Additionally, compliance with any new or more stringent laws or regulations, or stricter interpretations of existing laws, could require additional expenditures by us or our suppliers. Our inability to appropriately respond to such changes, adapt our business to meet evolving demands or innovate to remain competitive could adversely impact our business, financial condition, results of operations or cash flows.

If we are unable to compete successfully against other companies in the automotive aftermarket industry, we may lose customers and market share and our revenues may decline.

The sale of automotive parts, accessories and maintenance items is highly competitive and influenced by a number of factors, including name recognition, location, price, quality, product availability and customer service. We compete in both the professional and DIY categories of the automotive aftermarket industry, primarily with: (i) national and regional chains of automotive parts stores, (ii) internet-based retailers, (iii) discount stores and mass merchandisers that carry automotive products, (iv) wholesalers or jobbers stores, including those associated with national parts distributors or associations, (v) independently owned stores and (vi) automobile dealers that supply parts. These competitors and the level of competition vary by market. Some of our competitors may possess advantages over us in certain markets we share, including with respect to the level of marketing activities, number of stores, store locations, store layouts, operating histories, name recognition, established customer bases, vendor relationships, prices and product warranties. Internet-based retailers may possess cost advantages over us due to lower overhead costs, time and travel savings and ability to price competitively. In order to compete favorably, we may need to increase delivery speeds and incur higher shipping costs or lower prices, which would adversely impact our financial results. Consolidation among our competitors could enhance their market share and financial position, provide them with the ability to achieve better purchasing terms and allow them to provide more competitive prices to customers for whom we compete.

In addition, our reputation is critical to our continued success. Customers are increasingly shopping, reading reviews and comparing products and prices online. If we fail to maintain high standards for, or receive negative publicity (whether through social media or traditional media channels) relating to, product safety and quality, as well as our integrity and reputation, we could lose customers to our competition. The products we sell are brands of our vendors and our owned brands. If the perceived quality or value of the brands we sell declines in the perception of our customers, our results of operations could be negatively affected.

Competition may require us to reduce our prices below our normal selling prices or increase our promotional spending, which could lower our revenue and profitability. Competitive disadvantages may also prevent us from introducing new product lines, require us to discontinue current product offerings, or change some of our current operating strategies. If we do not have the resources, expertise and consistent execution, or otherwise fail to develop successful strategies, to address these potential competitive disadvantages, we may lose customers and market share, our revenues and profit margins may decline and we may be less profitable or potentially unprofitable.

Our inventory and ability to meet customer expectations may be adversely impacted by factors out of our control.

For the portion of our inventory manufactured and/or sourced outside the United States, geopolitical changes, changes in trade regulations or tariff rates, currency fluctuations, work stoppages, labor strikes, port delays, civil unrest, natural disasters, pandemics and other factors beyond our control may increase the cost of items we purchase or create shortages that could have a material adverse effect on our sales and profitability. In addition, unanticipated changes in consumer preferences or any unforeseen hurdles in meeting our customers’ needs for automotive products (particularly parts availability) in a timely manner could undermine our business strategy.

Deterioration of general macroeconomic conditions, including unemployment, inflation or deflation, consumer debt levels, and/or high fuel and energy costs, could have a negative impact on our business, financial condition, results of operations and cash flows due to impacts on our suppliers, customers and operating results.

Our business depends on developing and maintaining close relationships with our suppliers and on our suppliers’ ability and willingness to sell quality products to us at favorable prices and terms. Many factors outside our control may harm these relationships and the ability or willingness of these suppliers to sell us products on favorable terms. Such factors include a general decline in the economy and economic conditions and prolonged recessionary conditions. These events could negatively affect our suppliers’ operations and make it difficult for them to obtain the credit lines or loans necessary to finance their operations in the short-term or long-term and meet our product requirements. Financial or operational difficulties that some of our suppliers may face could also increase the cost of the products we purchase from them or our ability to source products from them. We might not be able to pass our increased costs onto our customers. If our suppliers fail to develop new products, we may not be able to meet the demands of our customers and our results of operations could be negatively affected.

13

In addition, the trend towards consolidation among automotive parts suppliers as well as the off-shoring of manufacturing capacity to foreign countries may disrupt or end our relationship with certain suppliers, and could lead to less competition and result in higher prices. We could also be negatively impacted by suppliers who might experience bankruptcies, work stoppages, labor strikes, changes in foreign or domestic trade policies, changes in tariff rates or other interruptions to or difficulties in the manufacture or supply of the products we purchase from them.

Deterioration in macroeconomic conditions or an increase in fuel costs or proposed or additional tariffs may have a negative impact on our customers’ net worth, financial resources, disposable income or willingness or ability to pay for accessories, maintenance or repairs for their vehicles, resulting in lower sales. An increase in fuel costs may also reduce the overall number of miles driven by our customers resulting in fewer parts failures and a reduced need for elective maintenance.

Rising energy prices also directly impact our operating and product costs, including our store, supply chain, professional delivery, utility and product acquisition costs.

Risks Related to Our Common Stock and Financial Condition

The market price of our common stock may be volatile and could expose us to securities class action litigation.

The stock market and the price of our common stock may be subject to wide fluctuations based upon general economic and market conditions. Downturns in the stock market may cause the price of our common stock to decline. The market price of our stock may also be affected by our ability to meet analysts’ expectations. Failure to meet such expectations, even slightly, could have an adverse effect on the price of our common stock. In the past, following periods of volatility in the market price of a company’s securities, securities class action litigation has often been instituted against such a company. Such litigation could result in substantial costs and a diversion of our attention and resources, which could have an adverse effect on our business. For example, in February 2018, following a significant decline in the price of our common stock, a putative class action was commenced against us. The settlement agreement received final approval by the court in June 2022 and was fully paid by our insurance carriers (see “Note 13. Contingencies” of this Annual Report on Form 10-K).

The amount and frequency of our share repurchases and dividend payments may fluctuate.

The amount, timing and execution of our share repurchase program may fluctuate based on our priorities for the use of cash for other purposes such as operational spending, capital spending, acquisitions or repayment of debt. Changes in operational results, cash flows, tax laws and our share price could also impact our share repurchase program and other capital activities. For example, in August 2022, Congress enacted the Inflation Reduction Act of 2022, which instituted, among other things, a 1% excise tax on certain corporate share repurchases beginning on January 1, 2023. Additionally, decisions to return capital to stockholders, including through our repurchase program or the issuance of dividends on our common stock, remain subject to determination of our Board of Directors that any such activity is in the best interests of our stockholders and is in compliance with all applicable laws and contractual obligations.

Our level of indebtedness, a downgrade in our credit ratings or a deterioration in global credit markets could limit the cash flow available for operations and could adversely affect our ability to service our debt or obtain additional financing.

Our level of indebtedness could restrict our operations and make it more difficult for us to satisfy our debt obligations. For example, our level of indebtedness could, among other things:

•affect our liquidity by limiting our ability to obtain additional financing for working capital;

•limit our ability to obtain financing for capital expenditures and acquisitions or make any available financing more costly;

•require us to dedicate all or a substantial portion of our cash flow to service our debt, which would reduce funds available for other business purposes, such as capital expenditures, dividends or acquisitions;

•limit our flexibility in planning for or reacting to changes in the markets in which we compete;

•place us at a competitive disadvantage relative to our competitors who may have less indebtedness;

•render us more vulnerable to general adverse economic and industry conditions; and

•make it more difficult for us to satisfy our financial obligations.

The indentures governing our senior unsecured notes and credit agreement governing our credit facilities contain financial and other restrictive covenants. Our failure to comply with those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of all of our debt, including such notes.

14

In addition, our overall credit rating may be negatively impacted by deteriorating and uncertain credit markets or other factors that may or may not be within our control. The interest rates on our revolving credit facility are linked directly to our credit ratings and the interest rates on future debt we issue or incur likely would be affected by our credit ratings in effect at the time such debt is issued or incurred. Accordingly, any negative impact on our credit ratings would likely result in higher interest rates and interest expense on any borrowings under our revolving credit facility and less favorable terms on our other operating and financing arrangements, including additional debt we may issue or incur in the future. In addition, it could reduce the attractiveness of certain vendor payment programs whereby third-party institutions finance arrangements to our vendors based on our credit rating, which could result in increased working capital requirements.

Conditions and events in the global credit market could have a material adverse effect on our access to short- and long-term borrowings to finance our operations and the terms and cost of that debt. It is possible that one or more of the banks that provide us with financing under our revolving credit facility may fail to honor the terms of our existing credit facility or be financially unable to provide the unused credit as a result of significant deterioration in such bank’s financial condition. An inability to obtain sufficient financing at cost-effective rates could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

The following table summarizes the location, ownership status and total square footage of space utilized for distribution centers, principal corporate offices and retail stores and branches as of December 31, 2022:

Square Footage (in thousands) | ||||||||||||||||||||

| Location | Leased | Owned | ||||||||||||||||||

| Distribution centers | 50 locations in 31 U.S. states and four Canadian provinces | 7,951 | 4,648 | |||||||||||||||||

| Principal corporate offices: | ||||||||||||||||||||

| Raleigh, NC | Raleigh, NC | 245 | — | |||||||||||||||||

| Roanoke, VA | Roanoke, VA | 265 | — | |||||||||||||||||

| Stores and branches | 4,915 stores and branches in 48 U.S. states and two U.S. territories and 171 stores and branches in nine Canadian provinces | 36,302 | 6,289 | |||||||||||||||||

Item 3. Legal Proceedings.

Refer to discussion in Note 13. Contingencies, of the Notes to the Consolidated Financial Statements included herein for information relating to legal proceedings.

Item 4. Mine Safety Disclosures.

Not applicable.

15

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is listed on the New York Stock Exchange under the symbol “AAP.”

As of February 24, 2023, there were 375 holders of record of our common stock, which does not include the number of beneficial owners whose shares were represented by security position listings.

The following table sets forth information with respect to repurchases of our common stock for the fourth quarter ended December 31, 2022:

| Period | Total Number of Shares Purchased (1) | Average Price Paid per Share (1) | Total Number of Shares Purchased as Part of Publicly Announced Programs | Maximum Dollar Value that May Yet Be Purchased Under the Programs (in thousands) (2) | ||||||||||||||||||||||

| October 9, 2022 to November 5, 2022 | 441,926 | $ | 169.71 | 441,762 | $ | 947,339 | ||||||||||||||||||||

| November 6, 2022 to December 3, 2022 | 5,741 | $ | 151.79 | — | $ | 947,339 | ||||||||||||||||||||

| December 4, 2022 to December 31, 2022 | 2 | $ | 140.90 | — | $ | 947,339 | ||||||||||||||||||||

| Total | 447,669 | $ | 169.54 | 441,762 | ||||||||||||||||||||||

(1)The aggregate cost of repurchasing shares in connection with the net settlement of shares issued as a result of the vesting of restricted stock units was $0.9 million, or an average price of $151.78 per share, during the twelve weeks ended December 31, 2022.

(2)On February 8, 2022, our Board of Directors authorized an additional $1 billion to the existing share repurchase program. This authorization is incremental to the $1.7 billion that was previously authorized by our Board of Directors.

16

Stock Price Performance

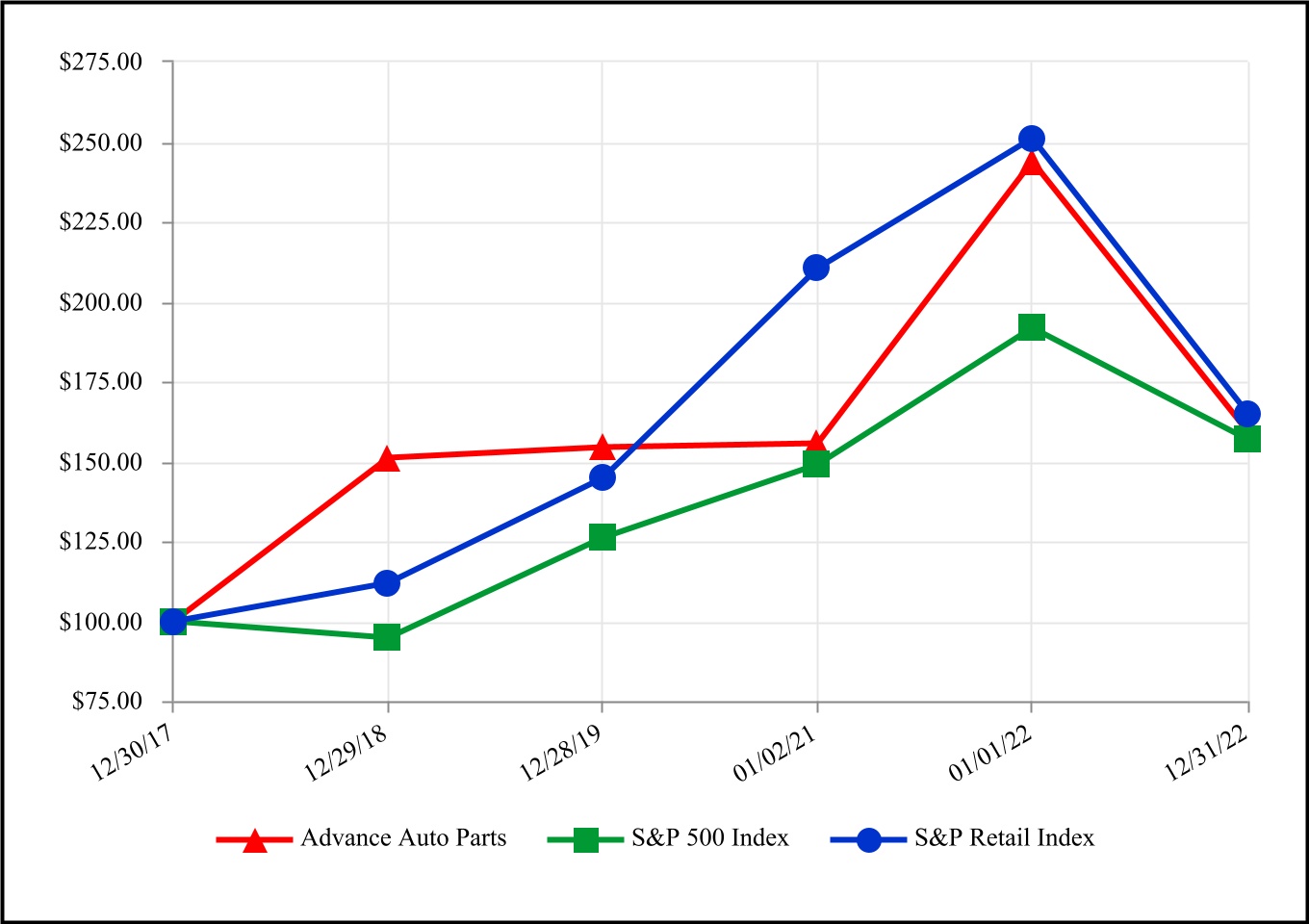

The following graph shows a comparison of the cumulative total return on our common stock, the Standard & Poor’s (“S&P”) 500 Index and the S&P’s Retail Index. The graph assumes that the value of an investment in our common stock and in each such index was $100 on December 30, 2017, and that any dividends have been reinvested. The comparison in the graph below is based solely on historical data and is not intended to forecast the possible future performance of our common stock.

COMPARISON OF CUMULATIVE TOTAL RETURN AMONG

ADVANCE AUTO PARTS, INC., S&P 500 INDEX

AND S&P RETAIL INDEX

| Company/Index | December 30, 2017 | December 29, 2018 | December 28, 2019 | January 2, 2021 | January 1, 2022 | December 31, 2022 | ||||||||||||||||||||||||||||||||

| Advance Auto Parts | $ | 100.00 | $ | 151.06 | $ | 154.32 | $ | 155.68 | $ | 243.72 | $ | 159.22 | ||||||||||||||||||||||||||

| S&P 500 Index | $ | 100.00 | $ | 94.80 | $ | 126.06 | $ | 148.85 | $ | 191.58 | $ | 156.88 | ||||||||||||||||||||||||||

| S&P Retail Index | $ | 100.00 | $ | 112.04 | $ | 144.71 | $ | 210.44 | $ | 251.08 | $ | 165.00 | ||||||||||||||||||||||||||

17

Item 6. [Reserved]

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion and analysis of financial condition and results of operations should be read in conjunction with our consolidated historical financial statements and the notes to those statements that appear elsewhere in this report. Our discussion contains forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of a number of factors, including those set forth under the section titled “Part 1. Item 1A. Risk Factors” elsewhere in this report. The discussion of our financial condition and changes in our results of operations, liquidity and capital resources for the fiscal year ended January 1, 2022 (“2021”) compared with the fiscal year ended January 2, 2021 (“2020”) has been omitted from this Form 10-K, but are included in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” of our Form 10-K for 2021, filed with the Securities and Exchange Commission (“SEC”) on February 15, 2022. Amounts are presented in thousands, except per share data, unless otherwise stated.

Management Overview

Net sales increased 1.4% during the fifty-two weeks ended December 31, 2022 (“2022”) compared with 2021, driven by improvements in strategic pricing and growth in both new store openings and sales to professional customers, partially offset by declines in DIY customer sales and units sold. Category growth was led by batteries, fluids and chemicals and motor oil.

We generated Diluted earnings per share (“Diluted EPS”) of $8.27 during 2022 compared with $9.55 in 2021. When adjusted for the following non-operational items, our Adjusted diluted earnings per share (“Adjusted EPS”) in 2022 was $13.04 compared with $12.02 in 2021:

| Year Ended | |||||||||||

| December 31, 2022 | January 1, 2022 | ||||||||||

Last-in, first-out (“LIFO”) impacts | $ | 3.85 | $ | 1.42 | |||||||

| Transformation expenses | $ | 0.49 | $ | 0.73 | |||||||

| General Parts International, Inc. (“GPI”) amortization of acquired intangible assets | $ | 0.34 | $ | 0.32 | |||||||

| Other adjustments | $ | 0.09 | $ | — | |||||||

Refer to “Reconciliation of Non-GAAP Financial Measures” for a definition and reconciliation of Adjusted EPS and other non-GAAP measures to the most directly comparable financial measures calculated and presented in accordance with U.S. GAAP.

A high-level summary of our financial results and other highlights from 2022 includes:

•Net sales during 2022 were $11.2 billion, an increase of 1.4% compared with 2021, driven by improvements in strategic pricing and growth in both new stores openings and sales to our professional customers, partially offset by declines in DIY customer sales and units sold.

•Gross profit margin for 2022 was 44.5% of Net sales, a decrease of 33 basis points compared with 2021. This decrease was primarily due to inflationary product costs, including the impact of LIFO related expenses, and unfavorable channel mix, primarily offset by improvements in strategic pricing and product mix.