SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(A) OF THE

SECURITIES EXCHANGE ACT OF 1934

(AMENDMENT NO. )

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| x | Definitive Additional Materials | |

| ¨ | Soliciting Material Pursuant to Section 240.14a-12 | |

W. R. BERKLEY CORPORATION

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

Commencing on May 9, 2013, W. R. Berkley Corporation sent the following communication to certain of its stockholders.

W. R. BERKLEY CORPORATION

475 Steamboat Road

Greenwich, Connecticut 06830

Supplemental Information Regarding Proposals No. 1 & No. 2

Election of Directors and

Non-Binding Advisory Vote on Named Executive Officer Compensation

May 9, 2013

Executive Summary:

| • | The Board believes that the Company’s consistent long-term superior performance supports the compensation of its CEO and firmly disagrees that there is a disconnect between pay and performance. |

| • | The Board is comfortable that Mr. Berkley’s pledging of shares does not create a significant risk of a forced sale given his substantial resources, including $465 million of unpledged shares. |

| • | Mr. Berkley has maintained his significant ownership stake for more than forty years, and the Board believes that it would be wrong to create a policy that might encourage Mr. Berkley to sell shares. |

| • | The Board believes that the directors nominated for re-election have exercised proper business judgment and risk management oversight and deserve to be re-elected. |

W. R. Berkley Corporation has always managed its business for the long-term benefit of its stockholders. To that end, we strongly believe that key employees should be long-term holders of our shares to the greatest extent possible. Given these views and our historical outstanding returns, we are disappointed that two proxy advisory firms have issued voting recommendations against certain proposals contained in our 2013 proxy statement.

One firm, Glass Lewis & Co. (“Glass Lewis”), has recommended that its clients vote “FOR” the election of each of our nominees for director and “AGAINST” the say-on-pay proposal, while another firm, ISS Proxy Advisory Services (“ISS”), has recommended that its clients vote “AGAINST” both of these proposals. We are taking this opportunity to address matters raised by Glass Lewis and ISS.

We strongly believe that the five nominees for director should be re-elected and that the Company’s executive compensation program directly links pay with performance, and we urge you to vote “FOR” both Proposals No. 1 and No. 2.

Election of Directors

As noted above, Glass Lewis has recommended that its clients vote “FOR” the election of each of the Company’s nominees for director. ISS, however, has recommended votes against all director nominees due to their view that the pledging of a significant number of shares of the Company’s common stock by its founder, Chairman of the Board and Chief Executive Officer, William R. Berkley, raises “concern regarding the board’s risk oversight” due to the potential for margin calls on the shares or for use as part of a personal hedging strategy. The Board of Directors vehemently disagrees with the ISS analysis and conclusion.

Mr. Berkley is widely regarded as one of the most distinguished leaders of the insurance industry. Since the Company’s formation in 1967, Mr. Berkley has provided the Company with strategic leadership, bringing to the Board of Directors deep and comprehensive knowledge of, and experience with, the Company and all facets of the insurance and reinsurance businesses. Mr. Berkley has managed the enterprise with the singular vision of optimizing risk-adjusted returns for the benefit of stockholders.

Absent from the ISS analysis is the fact that Mr. Berkley has not sold a share of stock in more than forty years (other than in connection with cashless exercises of stock options, or to cover taxes on vested restricted stock units (“RSUs”) from time to time). Mr. Berkley has pledged shares from time to time since he founded the Company as collateral for lines of credit in order to have liquidity precisely because he did not want to reduce his significant ownership stake. In addition, he owns 10,885,169 shares (with a current market value greater than $460 million) that are not pledged. Since the founding of the Company, through many market cycles including the recent financial crisis, he has never been required to sell any shares. Mr. Berkley’s pledged shares are not designed to shift or hedge any economic risk associated with his ownership of the Company’s shares. In fact, the Company’s senior officers, as well as the presidents and chief

2

financial officers of the Company’s subsidiaries, are prohibited from engaging in hedging and other derivative transactions with respect to the Company’s common stock. In 2013, the Company adopted restrictions on pledging whereby shares used in fulfillment of stock ownership guidelines may not be pledged or otherwise encumbered. In addition, mandatorily deferred RSUs cannot be pledged.

Notably, at the completion of the Company’s initial public offering in November 1973, Mr. Berkley beneficially owned shares representing approximately 23.8% of the Company. Thus, a large portion of the stock owned by Mr. Berkley is founder’s shares that Mr. Berkley purchased and has owned for more than forty years. In fact, while Mr. Berkley has maintained his ownership percentage in the Company, in recent years he has reduced the amount pledged by over 19%, from 18.36 million shares at March 22, 2011 to the current 14.85 million shares pledged.

If Mr. Berkley did what is customarily done by most executives, he would have regularly sold Company shares to diversify his holdings. The ISS analysis ignores that consideration. The typical stock holding requirement for CEOs of 5 to 10 times base compensation is far exceeded by Mr. Berkley’s significant ownership, even excluding his pledged shares. The Board of Directors and the Compensation Committee believe that barring any pledging of shares would have the undesirable effect of encouraging regular sales of stock, rather than having Mr. Berkley maintain his significant ownership level, which best aligns his interests with our stockholders.

Through his demonstrated actions for over forty years, Mr. Berkley has sought and has instilled an ownership mentality at the Company, whereby key employees own a piece of the business for a prolonged period. Selling of shares is either discouraged or in some cases restricted due to the terms of equity grants (e.g., RSUs awarded to all NEOs and seventy-plus key employees are mandatorily deferred after vesting until separation from service from the Company). The business is managed under the premise that the closest possible alignment between the interests of stockholders and employees is to have employees’ compensation tied to the Company’s long-term performance. The Company does not just want its employees to think like owners, it wants them to be owners. In addition, the Company’s stock retention guideline requires directors to hold shares granted to them as director compensation until such time as he or she no longer serves as a member of the Board.

The Board of Directors and the Compensation Committee both believe that Mr. Berkley’s actions exhibit the highest commitment to stockholders. Mr. Berkley’s decades-long holding of

3

his shares demonstrates his unwavering commitment to the Company and its future. The Board and the Compensation Committee are comfortable that, due to Mr. Berkley’s overall financial position (including the substantial unpledged shares he owns), his pledging of a portion of his shares does not create a significant risk of a forced sale. By ignoring the benefits of having a founding stockholder who maintains significant holdings, ISS’ policy unfairly penalizes Mr. Berkley and the Company and seemingly encourages transactions that are not in the best interest of stockholders. Moreover, the issue of Mr. Berkley’s pledged holdings has never come up as a concern during any conversation the Company has had with any investor at any time.

We further note that our Compensation Committee has specific responsibility for the risk oversight of our executive compensation policies and practices. As discussed in our proxy statement, this includes our policies regarding stock ownership requirements and restrictions on hedging and the pledging of our shares. The Compensation Committee has concluded that the risks arising from the Company’s compensation policies and practices for its employees are not reasonably likely to have a material adverse effect on the Company.

In addition, we note that the five directors standing for re-election have been directors for at least seven years, with one a director since 1998 and three directors since 2001. They have successfully guided the Company through difficult economic times and continue to be vital to its success. We believe it would be a disservice to the Company and its stockholders to not re-elect these longstanding directors.

We strongly urge you to vote “FOR” each nominee for director in Proposal No. 1.

Say-on-Pay

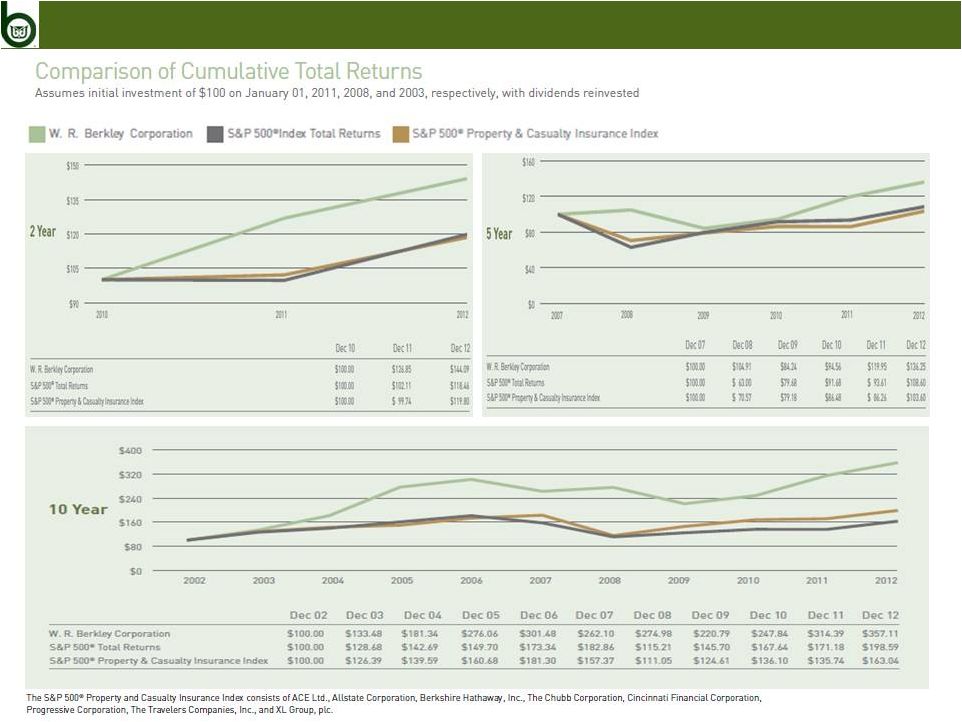

The Company’s strategy is predicated on achieving the highest long-term performance for our stockholders. Particularly in a volatile and cyclical industry such as insurance, the Company seeks to optimize risk-adjusted returns over the long-term. And in fact, under the leadership of Mr. Berkley, the Company has been successful in maintaining low volatility and significant risk mitigation. The Company’s annualized total shareholder return, defined as the change in the Company’s stock price plus reinvestment of dividends, was 13.6% over the past ten years, compared to 7.1% for the S&P 500 Index over the same period. In addition, the Company’s five-year volatility of earnings was lower than nearly 90% of our peer companies.

4

The Company’s compensation programs are specifically designed to emphasize and reward such long-term performance, while discouraging risky actions – such as managing to quarterly or even annual EPS numbers - that provide short-term benefits to the detriment of longer-term performance or risk exposure. Thus, the appropriate measurement period is not one year, or even three or five years, but seven to ten years – which better captures insurance cycles. We note, however, that the Company did outperform the peer companies used by ISS and Glass Lewis over 3-, 5- and 10-year periods. All of our compensation elements are designed to help achieve our objective of sustained long-term performance. We note the following:

| • | Mr. Berkley’s base salary is relatively low compared to the base salaries of CEOs at peer companies and has not been increased since 2000; |

| • | Discretion in annual bonus determination, which gives the Compensation Committee the flexibility to assess the totality of the Company’s performance over the long run as well as the short run, particularly during periods of volatility, and discourages short-term actions by executives. No matter how sophisticated an incentive formula may be, using only objective targets may drive actions that are not in the best interests of the Company or its stockholders. Pre-set goals can quickly become irrelevant as market conditions change. Executives could have a financial incentive to do exactly the wrong thing in light of such changing circumstances. We believe that any effort to assess performance using a simple pre-set formula could encourage decision-making that is not aligned with stockholders’ interests; |

| • | Strong long-term incentive program with features that are stricter than what are typical at most companies, including longer performance and vesting periods. In particular: |

| • | Long-Term Incentive Plan (“LTIP”) performance is measured over five years, not the three-year cycle that is more common at other companies; |

| • | In order to attain a maximum payout under the LTIP, book value per share (which was chosen because of its strong correlation to growth in market value in the insurance industry) must grow by 15 percent annually. This is a high bar for performance, compared to the historical experience at most insurance companies; |

5

| • | RSUs vest only after the end of five years and then are mandatorily deferred until separation; and |

| • | Approximately 50% of the long-term incentive value is linked to specific performance goals (growth in book value), while the balance is linked to stock price performance over the executive’s full career. Therefore, we believe long-term incentive compensation is 100% performance-based and linked to stockholder value. |

The Compensation Committee recognizes that Mr. Berkley is well paid and firmly believes that the level of compensation is justified due to his steadfast commitment to the Company and its stockholders as well as his exemplary individual performance. The Company has consistently been a high performer in many ways (please see accompanying charts). The most recent 10 percent increase in Mr. Berkley’s 2012 annual incentive compensation award is consistent with the 30 percent increase in the Company’s net income per share and a 20 percent improvement in return on equity over 2011.

We would also like to point out that there are two components of Mr. Berkley’s compensation considered by the advisory firms that artificially increased pay reported for last year. These include a change in pension value of approximately $9.2 million as well as dividend equivalents paid on mandatorily deferred RSUs of approximately $1.6 million. The change in pension value is due primarily to a change in interest rates (as no additional pension accrual was earned), and the dividend equivalents are due to the structure of the mandatory deferral feature of our RSUs and should not be attributable to 2012. Therefore, these amounts should have been excluded for purposes of comparison to the peer companies.

We continue to believe that there is clear alignment between the Company’s demonstrated long-term performance and its pay practices.

While the suggestions of proxy advisory firms may be well-intentioned, rigidly applying the “one size fits all” rules of outsiders, who have an imperfect understanding of the Company and the industry in which it operates, is no substitute for the considered business judgment of the Board of Directors of the Company.

We urge you to vote “FOR” Proposal No. 2.

6

Your vote is important to us, and we appreciate your ongoing support.

We would strongly encourage investor feedback and are available to speak with any of our interested stockholders. If any further information is needed or to discuss any points, please contact:

| Karen A. Horvath , VP External Financial Communications | khorvath@wrberkley.com | (203) 629-3040 | ||

| Eugene G. Ballard, SVP – Chief Financial Officer | eballard@wrberkley.com | (203) 629-3030 | ||

| Ira S. Lederman, SVP – General Counsel & Secretary | ilederman@wrberkley.com | (203) 629-3021 | ||

7

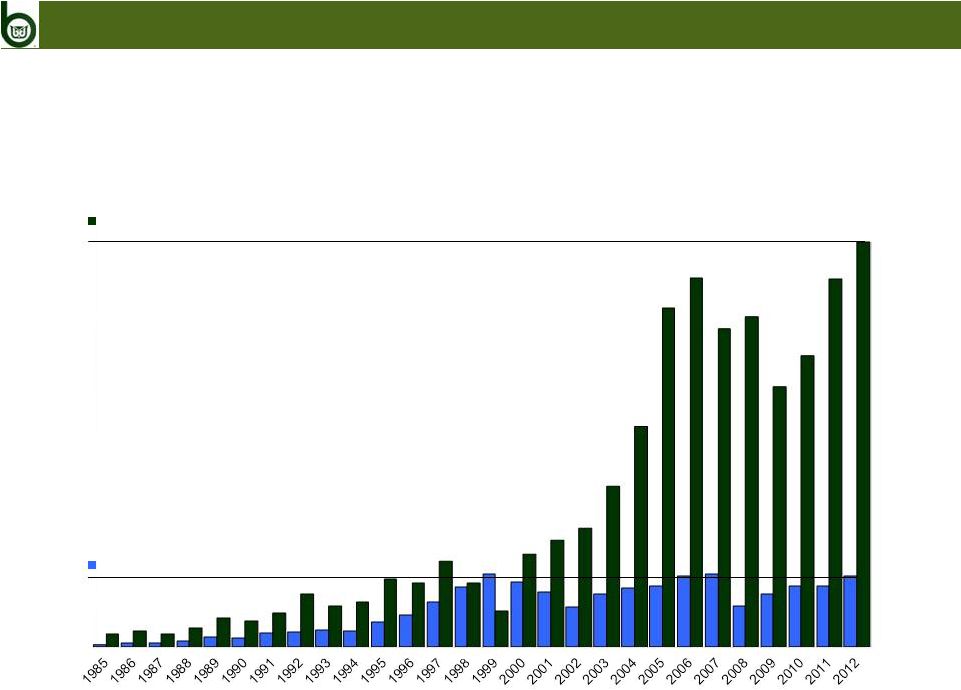

W. R.

Berkley Corporation’s cumulative stock performance has significantly W.

R. Berkley Corporation’s cumulative stock performance has significantly

out-performed the S&P 500

out-performed the S&P 500

®

®

8

Cumulative

Growth: 4,288%

753%

W. R. Berkley Corporation

S&P 500

®

RELATIVE

STOCK

PRICE

PERFORMANCE

W.

R.

Berkley

Corporation

vs.

S&P

500

® |

9

|

Commencing May 9, 2013, W. R. Berkley Corporation sent the following communication to all of its employees

Sent on behalf of William R. Berkley

Every year at W. R. Berkley Corporation’s annual meeting, stockholders vote on important matters. Most of the voting takes place before the meeting, through proxy voting. Voting by proxy allows stockholders to vote on issues that will be considered at the meeting, without actually attending the meeting in person.

If you hold shares as a registered stockholder, as a beneficial stockholder or as a participant in the 401(k) plan, voting your shares is an important way to take an active role in the overall governance of our Company.

Every vote counts. Every vote matters. All stockholders – including employees – are encouraged to voice their opinion by voting their shares. The Company’s Board of Directors has recommended a vote “FOR” each of the proposals on the ballot.

Voting by proxy began on April 8th and continues until 11:59 p.m. ET on May 20th, in advance of the annual meeting on May 21st.

Proxy materials have been sent to you either electronically or through postal mail, based on preferences on file with your bank or brokerage firm. In either case, you may vote by following the instructions in the materials you receive. If you do not receive proxy materials, please contact your bank or broker, or Bruce Weiser at W. R. Berkley Corporation if you have not yet received proxy materials or require additional assistance.

Your vote is important.

10