Exhibit 99.1

letter to shareholders

As we left 2012, the value of TransAlta’s shares had fallen by 28 per cent over the year and the market value of equity fell by approximately 19 per cent. Although we have seen some improvement since January 2013, the 2012 results were not at all what we wanted or what we intend to produce for our shareholders.

Despite these results, 2012 was a year of progress for TransAlta as we repositioned the company for growth and worked to preserve significant value for shareholders going forward. Some of the highlights of our 2012 accomplishments include:

|

I spent a lot of time over the last few years ensuring our operations team is ready to take full accountability for delivering the base business. My focus now is on growing and understanding what customers want and need so that we can expand our market share.

|

· Achieving fleet adjusted availability of 90 per cent, a level that is well above the North American Electric Reliability Corporation average availability for plants of our age and size,

· Achieving first quartile safety performance with an incident frequency rate of 0.89,

· Signing a significant cornerstone contract with Puget Sound Energy for output from Centralia Thermal, as well as reducing plant cash costs to ensure Centralia Thermal can compete in an environment of low natural gas and power prices,

· Creating a strategic partnership with MidAmerican Energy Holdings Company (MidAmerican) for natural gas-fired generation development in Canada,

· Acquiring the Solomon power station in Western Australia, adding 125 MW of contracted power to the portfolio and moving us closer to our goal of having 600 MW of behind-the-fence generation in Western Australia by 2015,

· Completing our three-year reinvestment program in our coal fleet and setting it up for solid operations until its end of life,

· Winning two significant force majeure claims, one on our Sundance Units 1 and 2, and one on Sundance 3, both of which validated TransAlta’s strong operating practices,

· Uprating our Keephills Units 1 and 2,

· Raising over $1 billion in new capital in the form of preferred shares, common equity, and long-term debt to strengthen the balance sheet, repay short-term debt, and finance the New Richmond wind farm and the acquisition of Solomon in Australia,

· Starting the life extension of our hydro fleet through investing $22 million in a new penstock for the Pocaterra hydro plant,

· Signing 115 MW of new commercial and industrial contracts and renewing 85 per cent of expiring contracts, bringing the total number of direct customers to just over 500 MW – a goal that was accomplished two years ahead of schedule, and

· Realigning the company to ensure a focus on operations and growth while eliminating duplication and cost, which is expected to generate approximately $25 million to $30 million in benefits on an annualized basis.

External events also added value to the company, particularly the federal government’s September announcement of the final greenhouse gas (GHG) regulations. As a result of changes in the rules from what was previously proposed, our coal plants can now serve Albertans for an average of 43 years, 3.5 years longer than before. This greatly enhances the value of these assets and provides significant benefits to electricity consumers in the province

|

TransAlta Corporation | 2012 Annual Report |

|

letter to shareholders

We also had a number of difficult challenges in 2012, including:

· The arbitration panel did not agree with TransAlta’s assesment that Sundance 1 and 2 should be economically destroyed. As a result, we had to invest $190 million to rebuild the boilers on both units. We continue to believe that the spirit of the legislation governing the PPAs is meant to ensure that shareholders receive a reasonable rate of return, and that being forced to invest significant capital dollars to keep a PPA intact is unwarranted, despite the ruling of the panel. We will continue to work to ensure that our PPA plants earn reasonable returns through to the end of their PPA terms.

· Our Energy Trading business generated only $3 million in gross margin, the lowest level in its 17-year history and one year after achieving an all-time high. This volatility is unacceptable for the size of our company and we have refocused our strategies to return back to the basics and deliver more consistent results in the range of $40 million to $60 million of gross margin year after year.

· The return of Sundance Units 1 and 2 to the market makes it prudent to delay our plans for Sundance Unit 7. We will continue to advance this investment in 2013, moving forward with permitting efforts as we believe the unit will be needed in the 2018 time frame.

· Lower power pricing in the Pacific Northwest and Alberta markets. Low natural gas prices translate directly into lower power prices, especially in the Pacific Northwest. Above-normal water conditions for the second consecutive year also put downside pressure on spot market power prices due to the large amount of hydro generation and storage in the region. These factors reduced revenues from our Centralia plant.

Financially, all of this translated into delivering $776 million dollars in funds from operations. This is slightly below what we delivered in 2011, despite the pressure on Centralia gross margins due to low power prices and below average results from our Energy Trading business. This level of funds allows us to pay the dividend and reinvest in our current fleet. In terms of the balance sheet, we were very focused on ensuring we maintained our investment grade ratings, and therefore took a number of steps in this regard including issuing preferred shares and common equity, introducing the Premium DividendTM Reinvestment Program, contracting our assets, and reducing costs.

As we look forward into 2013 and beyond, we see both opportunities and challenges.

My focus for 2013 will be overseeing TransAlta’s growth and development. I have spent a lot of time over the last few years ensuring our operations team is ready to take full accountability for delivering the base business they are. My focus now is on growing and continuing to expand our direct customer business. This will dominate how I spend my time in 2013.

In 2012, our realignment allowed us to define our resources more clearly between base operations and growth. Excellence in operations is a given for TransAlta and it underpins our overall strategy. Our performance is first quartile and our fleet availability continues to outperform North American averages. In 2013, the team will continue to implement best-in-class practices for safety, work management, and management of change. Their dedication to a workplace that is both safe and productive is reflected in our performance in 2012, and by the end of next year we will be able to report even greater progress on our costs and quality initiatives.

|

TransAlta Corporation | 2012 Annual Report |

letter to shareholders

In terms of growth, we have excellent teams in place in all of our key markets, and we see tremendous opportunities within them all. The partnership with MidAmerican will allow us to pursue more opportunities than in the past. Our goal is to add between $40 million and $60 million of EBITDA from new growth every year going forward. We are now well positioned to do this.

The upcoming year will also be a big year for our Energy Trading and Marketing team. They have done a terrific job attracting new customers to TransAlta and they will continue that effort. In 2013, their goal is to attract another 600 MW of customers to our business. Our move away from exclusively focusing on wholesale marketing to more direct relationships with wholesale and commercial customers here in Alberta is deliberate. They will return trading back to its historical profitability of $40 million to $60 million in gross margins, which will give us that additional value-added in support of the dividend, our sustaining capital program, and new growth investments.

As always, opportunities can only come with a strong team that is motivated to make the right decisions in both the long and short term. I have spent a significant amount of time with my team and the Human Resources Committee to design a compensation structure that better aligns our incentive pay to achievements in delivering strong funds from operations, free cash flow, and availability. Medium-term incentive pay is aligned to growth in cash flow per share, free cash flow, and total shareholder returns.

I fundamentally believe that we can never lose sight of how financial incentives motivate employees. As we implement this new system in 2013, our staff at TransAlta will have a very clear understanding of how together they can make decisions that will be consistent with short-term and long-term shareholder value creation. The new incentive system – along with our strength in internal communications, our dedication to an open and transparent culture, our commitment to the professional growth of management, technical, and front line staff, and our insistence on a business-centric approach to decision making – will ensure that your team will be one of the strongest in the industry.

Overall, TransAlta’s management team worked tremendously hard this past year. The results may not yet be properly reflected in our share price, but their accomplishments contribute to both preserving and growing the future value of TransAlta. I would like to personally thank each member of the team for all they have done. They are more than ready for what 2013 has to bring.

In closing, I would also like to thank the members of our Board of Directors for their patience, guidance, insights and hard work throughout 2012. The Board has your interests at heart by consistently demanding that we take personal accountability for improving our performance. For that I am grateful. I also appreciate the time, counsel, and encouragement that our Chair, Ambassador Gordon Giffin, has given me this year as we’ve navigated through a very full schedule. Finally, many thanks to both the employees who continue to build their careers here and the employees that we had to say goodbye to in November. Your loyalty, dedication, and spirit make it an honour to represent TransAlta as CEO.

Sincerely,

Dawn Farrell

President and Chief Executive Officer

February 27, 2013

|

TransAlta Corporation | 2012 Annual Report |

|

message from the chair

|

|

The past year presented many challenges for TransAlta. Some, such as depressed natural gas prices leading to low power prices, are factors your company cannot directly affect. Others, such as regulatory and public policy impacting our business, were addressed by management with commitment and insight. Senior management, led by Dawn Farrell, along with your Board, believes that TransAlta is continuing to develop a solid platform, in challenging times, to succeed going forward.

|

TransAlta is continuing to diversify the fuel and the geography of its generating fleet, while being innovative and prudent relative to the regulatory regime applicable to its historic coal-fired assets. Dawn Farrell has aligned company management to respond to this new-paradigm era for power generation. The executive team and dedicated employees throughout the organization are focused on building a 21st-century power generator that is sensitive to environmental concerns, committed to efficiently serving its markets, and intent on enhancing shareholder value.

As Chair, I assure you that your Board is engaged and an active partner with management in charting the course for this new era of providing power to markets in North America and Australia. We are not daunted by the challenges and we welcome the opportunity to apply creativity and vision to the future growth of TransAlta. We will continue our practice of employing top governance practices, prudent capital allocation, and industry-leading safety performance, all the while remembering our duty to you, the shareholder.

I look forward to speaking with all of you at our annual meeting.

Sincerely,

Ambassador Gordon D. Giffin

Chairman of the Board

February 27, 2013

|

TransAlta Corporation | 2012 Annual Report |

plant summary

|

|

|

|

|

|

|

|

|

Net capacity |

|

|

|

|

|

|

|

As of |

|

|

|

Capacity |

|

Ownership |

|

ownership |

|

|

|

Revenue |

|

Contract |

|

February 8, 2013 |

|

Facility |

|

(MW)1 |

|

(%) |

|

interest (MW)1 |

|

Fuel |

|

source |

|

expiry date |

|

Western Canada |

|

Sundance, AB2,3 |

|

2,141 |

|

100% |

|

2,141 |

|

Coal |

|

Alberta PPA/Merchant4 |

|

2020 |

|

39 Facilities |

|

Keephills, AB5 |

|

792 |

|

100% |

|

792 |

|

Coal |

|

Alberta PPA/Merchant5 |

|

2020 |

|

|

|

Genesee 3, AB |

|

466 |

|

50% |

|

233 |

|

Coal |

|

Merchant |

|

- |

|

|

|

Keephills 3, AB |

|

450 |

|

50% |

|

225 |

|

Coal |

|

Merchant |

|

- |

|

|

|

Sheerness, AB |

|

780 |

|

25% |

|

195 |

|

Coal |

|

Alberta PPA |

|

2020 |

|

|

|

Poplar Creek, AB |

|

356 |

|

100% |

|

356 |

|

Gas |

|

LTC/Merchant |

|

2024 |

|

|

|

Fort Saskatchewan, AB |

|

118 |

|

30% |

|

35 |

|

Gas |

|

LTC |

|

2019 |

|

|

|

Brazeau, AB |

|

355 |

|

100% |

|

355 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Big Horn, AB |

|

120 |

|

100% |

|

120 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Spray, AB |

|

103 |

|

100% |

|

103 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Ghost, AB |

|

51 |

|

100% |

|

51 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Rundle, AB |

|

50 |

|

100% |

|

50 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Cascade, AB |

|

36 |

|

100% |

|

36 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Kananaskis, AB |

|

19 |

|

100% |

|

19 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Bearspaw, AB |

|

17 |

|

100% |

|

17 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Pocaterra, AB |

|

15 |

|

100% |

|

15 |

|

Hydro |

|

Alberta PPA |

|

2013 |

|

|

|

Horseshoe, AB |

|

14 |

|

100% |

|

14 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Barrier, AB |

|

13 |

|

100% |

|

13 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Taylor Hydro, AB |

|

13 |

|

100% |

|

13 |

|

Hydro |

|

Merchant |

|

- |

|

|

|

Interlakes, AB |

|

5 |

|

100% |

|

5 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Belly River, AB |

|

3 |

|

100% |

|

3 |

|

Hydro |

|

Merchant |

|

- |

|

|

|

Three Sisters, AB |

|

3 |

|

100% |

|

3 |

|

Hydro |

|

Alberta PPA |

|

2020 |

|

|

|

Waterton, AB |

|

3 |

|

100% |

|

3 |

|

Hydro |

|

Merchant |

|

- |

|

|

|

St. Mary, AB |

|

2 |

|

100% |

|

2 |

|

Hydro |

|

Merchant |

|

- |

|

|

|

Upper Mamquam, BC |

|

25 |

|

100% |

|

25 |

|

Hydro |

|

LTC |

|

2025 |

|

|

|

Pingston, BC |

|

45 |

|

50% |

|

23 |

|

Hydro |

|

LTC |

|

2023 |

|

|

|

Bone Creek, BC |

|

19 |

|

100% |

|

19 |

|

Hydro |

|

LTC |

|

2031 |

|

|

|

Akolkolex, BC |

|

10 |

|

100% |

|

10 |

|

Hydro |

|

LTC |

|

2015 |

|

|

|

Summerview 1, AB |

|

70 |

|

100% |

|

70 |

|

Wind |

|

Merchant |

|

- |

|

|

|

Summerview 2, AB |

|

66 |

|

100% |

|

66 |

|

Wind |

|

Merchant |

|

- |

|

|

|

Ardenville, AB |

|

69 |

|

100% |

|

69 |

|

Wind |

|

Merchant |

|

- |

|

|

|

Blue Trail, AB |

|

66 |

|

100% |

|

66 |

|

Wind |

|

Merchant |

|

- |

|

|

|

Castle River, AB6 |

|

44 |

|

100% |

|

44 |

|

Wind |

|

Merchant |

|

- |

|

|

|

McBride Lake, AB |

|

75 |

|

50% |

|

38 |

|

Wind |

|

LTC |

|

2023 |

|

|

|

Soderglen, AB |

|

71 |

|

50% |

|

35 |

|

Wind |

|

Merchant |

|

- |

|

|

|

Cowley Ridge, AB |

|

21 |

|

100% |

|

21 |

|

Wind |

|

Merchant |

|

- |

|

|

|

Cowley North, AB |

|

20 |

|

100% |

|

20 |

|

Wind |

|

Merchant |

|

- |

|

|

|

Sinnott, AB |

|

7 |

|

100% |

|

7 |

|

Wind |

|

Merchant |

|

- |

|

|

|

Macleod Flats, AB |

|

3 |

|

100% |

|

3 |

|

Wind |

|

Merchant |

|

- |

|

Total Western Canada |

|

|

|

6,536 |

|

|

|

5,315 |

|

|

|

|

|

|

|

Eastern Canada |

|

Sarnia, ON |

|

506 |

|

100% |

|

506 |

|

Gas |

|

LTC |

|

2022-2025 |

|

14 Facilities |

|

Mississauga, ON |

|

108 |

|

50% |

|

54 |

|

Gas |

|

LTC |

|

2017 |

|

|

|

Ottawa, ON |

|

68 |

|

50% |

|

34 |

|

Gas |

|

LTC |

|

2012 |

|

|

|

Windsor, ON |

|

68 |

|

50% |

|

34 |

|

Gas |

|

LTC/Merchant |

|

2016 |

|

|

|

Ragged Chute, ON |

|

7 |

|

100% |

|

7 |

|

Hydro |

|

Merchant |

|

- |

|

|

|

Misema, ON |

|

3 |

|

100% |

|

3 |

|

Hydro |

|

LTC |

|

2027 |

|

|

|

Galetta, ON |

|

2 |

|

100% |

|

2 |

|

Hydro |

|

LTC |

|

2031 |

|

|

|

Appleton, ON |

|

1 |

|

100% |

|

1 |

|

Hydro |

|

LTC |

|

2031 |

|

|

|

Moose Rapids, ON |

|

1 |

|

100% |

|

1 |

|

Hydro |

|

LTC |

|

2031 |

|

|

|

Melancthon, ON |

|

200 |

|

100% |

|

200 |

|

Wind |

|

LTC |

|

2026-2028 |

|

|

|

Wolfe Island, ON |

|

198 |

|

100% |

|

198 |

|

Wind |

|

LTC |

|

2029 |

|

|

|

Kent Hills, NB |

|

150 |

|

83% |

|

125 |

|

Wind |

|

LTC |

|

2033-2035 |

|

|

|

Le Nordais, QC |

|

99 |

|

100% |

|

99 |

|

Wind |

|

LTC |

|

2033 |

|

|

|

New Richmond, QC7 |

|

68 |

|

100% |

|

68 |

|

Wind |

|

Quebec PPA |

|

2032 |

|

Total Eastern Canada |

|

|

|

1,479 |

|

|

|

1,332 |

|

|

|

|

|

|

|

United States |

|

Centralia Thermal, WA |

|

1,340 |

|

100% |

|

1,340 |

|

Coal |

|

Merchant |

|

- |

|

17 Facilities |

|

Centralia Gas, WA |

|

248 |

|

100% |

|

248 |

|

Gas |

|

Merchant |

|

- |

|

|

|

Power Resources, TX |

|

212 |

|

50% |

|

106 |

|

Gas |

|

Merchant |

|

- |

|

|

|

Saranac, NY |

|

240 |

|

37.5% |

|

90 |

|

Gas |

|

Merchant |

|

- |

|

|

|

Yuma, AZ |

|

50 |

|

50% |

|

25 |

|

Gas |

|

LTC |

|

2024 |

|

|

|

Imperial Valley, CA8 |

|

327 |

|

50% |

|

164 |

|

Geothermal |

|

LTC |

|

2016-2029 |

|

|

|

Wailuku, HI |

|

10 |

|

50% |

|

5 |

|

Hydro |

|

LTC |

|

2023 |

|

|

|

Skookumchuck, WA |

|

1 |

|

100% |

|

1 |

|

Hydro |

|

LTC |

|

2020 |

|

Total U.S. |

|

|

|

2,428 |

|

|

|

1,979 |

|

|

|

|

|

|

|

Australia |

|

Parkeston, WA |

|

110 |

|

50% |

|

55 |

|

Gas |

|

LTC |

|

2016 |

|

5 Facilities |

|

Southern Cross, WA9 |

|

245 |

|

100% |

|

245 |

|

Gas/Diesel |

|

LTC |

|

2013 |

|

|

|

Solomon Power Station10 |

|

125 |

|

100% |

|

125 |

|

Gas/Diesel |

|

LTC |

|

2028 |

|

Total Australia |

|

|

|

480 |

|

|

|

425 |

|

|

|

|

|

|

|

Total |

|

|

|

10,923 |

|

|

|

9,051 |

|

|

|

|

|

|

1 Megawatts are rounded to the nearest whole number.

2 Includes a 15 MW uprate on Sundance Unit 3; the resulting increased capacity will not be realized until the generator stator is replaced.

3 Includes Sundance A expected to be back in service in the fall of 2013 (560 MW).

4 Merchant capacity refers to uprates on Unit 4 (53 MW), Unit 5 (53 MW), and Unit 6 (44 MW).

5 Testing of the Keephills Unit 1 and Unit 2 uprates has been completed and it was determined that the actual capability of the uprates was less than originally anticipated. As a result we have adjusted the uprates to 13 MW, bringing the maximum capability of these units to 396 MW each.

6 Includes seven individual turbines at other locations.

7 Facilities currently under development.

8 Comprised of 10 facilities.

9 Comprised of four facilities.

10 This facility was acquired in September 2012 and was under construction for the remainder of 2012. The plant is expected to be fully commissioned in Q1 of 2013.

|

TransAlta Corporation | 2012 Annual Report |

|

| |

|

management’s discussion and analysis | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

table of contents |

|

|

|

|

|

|

|

|

|

|

|

Highlights |

8 |

|

Employee Share Ownership |

37 |

|

Summary of Results |

9 |

|

Employee Future Benefits |

37 |

|

Business Environment |

9 |

|

Statements of Cash Flows |

38 |

|

Strategy |

12 |

|

Liquidity and Capital Resources |

39 |

|

Capability to Deliver Results |

13 |

|

Unconsolidated Structured Entities or Arrangements |

40 |

|

Performance Metrics |

14 |

|

Climate Change and the Environment |

40 |

|

Results of Operations |

17 |

|

Forward Looking Statements |

43 |

|

Net Earnings Attributable to Common Shareholders |

17 |

|

2013 Outlook |

44 |

|

Significant Events |

19 |

|

Risk Management |

48 |

|

Discussion of Segmented Results |

24 |

|

Critical Accounting Policies and Estimates |

56 |

|

Net Interest Expense |

32 |

|

Future Accounting Changes |

61 |

|

Non-Controlling Interests |

32 |

|

Additional IFRS Measures |

63 |

|

Income Taxes |

32 |

|

Non-IFRS Measures |

63 |

|

Financial Position |

34 |

|

Selected Quarterly Information |

68 |

|

Financial Instruments |

34 |

|

Controls and Procedures |

68 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This Management’s Discussion and Analysis (“MD&A”) should be read in conjunction with our audited 2012 consolidated financial statements and our 2013 Annual Information Form. Our consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) for Canadian publicly accountable enterprises. All dollar amounts in the following discussion, including the tables, are in millions of Canadian dollars unless otherwise noted. This MD&A is dated Feb. 26, 2013. Additional information respecting TransAlta Corporation (“TransAlta”, “we”, “our”, “us”, or “the Corporation”), including our Annual Information Form, is available on SEDAR at www.sedar.com, on EDGAR at www.sec.gov, and on our website at www.transalta.com. | |

|

|

|

|

|

|

|

TransAlta Corporation | 2012 Annual Report |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

management’s discussion and analysis |

|

|

|

|

|

|

|

|

|

|

Highlights

Generation Results

§ Availability, adjusted for economic dispatching at Centralia Thermal, of our overall fleet increased by almost two per cent from 2011 levels to 90.0 per cent availability despite significantly higher planned major maintenance in 2012.

§ Comparable gross margins in Western Canada increased $77 million to $855 million, largely due to the impact of lower Alberta coal Power Purchase Arrangements (“PPAs”) penalties due to lower prices in Alberta and higher hydro margins.

§ Comparable gross margins in Eastern Canada increased $11 million to $342 million primarily due to lower contracted gas input costs.

§ Our International comparable gross margins decreased $43 million to $300 million due to lower merchant pricing, including margins on purchased power.

§ Comparable Operations, Maintenance, and Administration (“OM&A”) costs have been reduced by $32 million to $381 million due to continued efforts to lower costs and focus on productivity.

Energy Trading Results

§ Gross margins decreased by $134 million to $3 million, primarily due to unfavourable market expectations on power and gas prices for our trading positions held.

§ OM&A costs decreased by $15 million to $28 million, primarily due to lower compensation costs as a result of lower earnings.

Financial Highlights

§ Comparable earnings were $118 million ($0.50 per share), down from $230 million ($1.04 per share) in 2011. The decrease in comparable earnings is primarily due to lower gross margins in Energy Trading. Reported net loss attributable to common shareholders was $614 million ($2.61 per share), down from net earnings of $290 million ($1.31 per share) in 2011, which included the following non-comparable amounts, net of tax:

§ Impairment of $226 million ($347 million pre-tax) at the Centralia Thermal plant and the writeoff of the associated deferred income tax asset of $169 million due to signing a long-term power agreement that will retire the plant in 2025,

§ Impairment of $31 million ($41 million pre-tax) was subsequently reversed as a result of the additional years expected to be realized at Sundance Units 1 and 2 due to amendments to the Canadian federal regulations. Net penalties of $189 million as a result of the arbitration panel concluding that Sundance Units 1 and 2 were not economically destroyed, but meet the criteria of force majeure until they are returned to service,

§ Impairment of $13 million ($18 million pre-tax) related to assets in the renewable fleet,

§ Reversal of a $47 million loss recognized on de-designated hedges primarily at Centralia Thermal,

§ Gain on sale of collateral at MF Global Inc. of $11 million,

§ Income tax recovery of $9 million, and

§ Restructuring charge of $10 million.

§ Comparable Earnings Before Interest, Taxes, Depreciation, and Amortization (“EBITDA”) decreased $31 million to $1,014 million compared to 2011.

§ Funds from operations decreased $33 million to $776 million compared to 2011.

§ We have maintained investment grade ratings to support our access to multiple sources of capital.

Progress on Growth Projects through Acquisition and Strategic Partnership

§ We completed the acquisition of the 125 megawatt (“MW”) natural gas-fired and diesel-fired Solomon power station in Western Australia for $318 million. The power station is fully contracted and is expected to generate pre-financing cash flows of approximately $40 million per year, and is expected to be commissioned during the first half of 2013.

§ We have created a new strategic partnership with MidAmerican Energy Holdings Company (“MidAmerican”) through which the two companies will work together to develop, build, and operate new natural gas-fueled electricity generation projects in Canada.

§ We continue to build our 68 MW New Richmond wind project on the Gaspé Peninsula, which is expected to be commissioned in the first quarter of 2013.

|

|

|

|

|

|

|

|

TransAlta Corporation | 2012 Annual Report |

|

|

|

|

|

|

|

|

management’s discussion and analysis |

Summary of Results

The following table depicts key financial results and statistical operating data:

|

Year ended Dec. 31 |

2012 |

2011 |

2010 |

|

Availability (%)1 |

88.4 |

85.4 |

88.9 |

|

Adjusted availability (%)1,2 |

90.0 |

88.2 |

88.9 |

|

Production (GWh)1 |

38,750 |

41,012 |

48,614 |

|

Revenues |

2,262 |

2,663 |

2,673 |

|

Gross margin3 |

1,453 |

1,716 |

1,488 |

|

Operating income (loss)3 |

42 |

645 |

459 |

|

Comparable operating income4 |

470 |

553 |

452 |

|

Net earnings (loss) attributable to common shareholders |

(614) |

290 |

255 |

|

Net earnings (loss) per share attributable to common shareholders, basic and diluted |

(2.61) |

1.31 |

1.16 |

|

Comparable earnings per share4 |

0.50 |

1.04 |

0.97 |

|

Comparable EBITDA4 |

1,014 |

1,045 |

963 |

|

Funds from operations4 |

776 |

809 |

805 |

|

Funds from operations per share4 |

3.30 |

3.64 |

3.68 |

|

Cash flow from operating activities |

520 |

690 |

852 |

|

Free cash flow4 |

85 |

185 |

172 |

|

Dividends paid per common share |

1.16 |

1.16 |

1.16 |

|

|

|

|

|

|

As at Dec. 31 |

2012 |

2011 |

|

|

Total assets |

9,451 |

9,729 |

|

|

Total long-term liabilities |

4,726 |

4,911 |

|

Business Environment

Overview of the Business

We are a wholesale power generator and marketer with operations in Canada, the United States (“U.S.”), and Australia. We own, operate, and manage a highly contracted and geographically diversified portfolio of assets and utilize a broad range of generation fuels including coal, natural gas, hydro, wind, and geothermal. During 2012, we completed uprates at Keephills Units 1 and 2 and Sundance Unit 3, which we expect will add an additional 41 MW of power to our generation portfolio and increased our total generating capacity to 8,200 MW. Please refer to the Significant Events section of this MD&A for more information. Although we completed the uprate at Sundance Unit 3, the resulting increased capacity will not be realized until we replace the generator stator.

We operate in a variety of markets to generate electricity, find buyers for the power we generate, and arrange for its transmission. The major markets we operate in are Western Canada, the Western U.S., and Eastern Canada. The key characteristics of these markets are described below.

Demand

Demand for electricity is a fundamental driver of prices in all of our markets. Economic growth is the main driver of longer-term changes in the demand for electricity. Historically, demand for electricity in all three of our major markets has grown at an average rate of one to three per cent per year. In recent years, demand growth has been weaker in Ontario and the Pacific Northwest due to economic conditions, while Alberta has shown steady growth.

1 Availability and production includes all generating assets (generation operations, finance leases, and equity investments).

2 Adjusted for economic dispatching at Centralia Thermal.

3 These items are Additional IFRS Measures. Refer to the Additional IFRS Measures section of this MD&A for further discussion of these items.

4 These comparable items are not defined under IFRS. Presenting these items from period to period provides management and investors with the ability to evaluate earnings trends more readily in comparison with prior periods’ results. Refer to the Non-IFRS Measures section of this MD&A for further discussion of these items, including, where applicable, reconciliations to measures calculated in accordance with IFRS.

|

TransAlta Corporation | 2012 Annual Report |

|

management’s discussion and analysis |

|

Alberta has seen annual average demand growth of about three per cent over the past three years. The fourth quarter of 2012 in particular showed a higher growth rate of four per cent on average. Investment in oil sands development is a key driver of electricity demand growth in the province, and several large projects are underway that will bring new demand over the next several years. In the Pacific Northwest and Ontario demand growth was flat in 2012.

Supply

Reserve margins measure available capacity in a market over and above the capacity needed to meet normal peak demand levels. Falling reserve margins indicate that generation capacity is becoming relatively scarce and results in increased power prices. During 2012, reserve margins increased in Ontario and were relatively flat in Alberta and the Pacific Northwest.

Renewable generation growth has been strong in all regions, driven to a varying degree by public policy. The Pacific Northwest has seen a large amount of new wind generation in the last several years, and Ontario is also developing wind and solar capacity through its Feed-in Tariff program. Wind generation in Alberta is also growing rapidly, as over 200 MW of new wind capacity was brought online during 2012, which represents a 26 per cent increase in capacity from the previous year.

Transmission

Transmission refers to the bulk delivery system of power and energy between generating units and wholesale and/or retail customers. Power lines serve as the physical path, transporting electricity from generating units to customers. Transmission systems are designed with reserve capacity to allow for an amount of “real-time” fluctuations in both energy supply and demand caused by generation plants or loads increasing or decreasing output or consumption.

Transmission capacity refers to the ability of the transmission line, or lines, to safely and reliably transport electricity in an amount that balances the dispatched generating supply with demand, and allows for contingency situations on the system. Most transmission businesses in North America are still regulated.

In the North American market, we believe investment in transmission capacity has not kept pace with the growth in demand for electricity. Lead times in new transmission infrastructure projects are significant, subject to extensive consultation processes with landowners, and subject to regulatory requirements that can change frequently. As a result, existing generation or additions of generating capacity may not have ready access to markets until key bulk transmission upgrades and additions are completed.

In 2009, the Government of Alberta declared several important transmission projects as being critical, including lines between the Edmonton and Calgary regions, and between Edmonton and northeast Alberta. In late 2011, the Government of Alberta initiated a review of critical transmission projects. The results of the review by an independent panel were released in early 2012 with the panel recommending proceeding as soon as possible with development of two high-voltage direct current transmission lines between the Edmonton and Calgary regions. In response to the panel recommendations, the provincial government introduced Bill 8 in the Alberta legislature. Bill 8 effectively removes the concept of Critical Transmission Infrastructure (“CTI”) from the Electric Utilities Act. Existing projects designated as CTI will remain designated as CTI. All new transmission projects will be subject to a needs review by the Alberta Utilities Commission (“AUC”). The CTI projects between Edmonton and northeast Alberta will be subject to a competitive procurement process as set out in the Electric Statutes Amendment Act, 2009. The competitive procurement process has been developed by the Alberta Electric System Operator (“AESO”) and is currently being considered by the AUC. The AESO has issued a Project Information Brief for the first of two 500 kilovolt alternating current transmission lines that will be subject to a competitive procurement process.

On Nov. 15, 2012, the AUC released its decision approving the Eastern Alberta Transmission Line between the Edmonton and Calgary regions. The decision by the AUC approving a second high-voltage direct current transmission line between the Edmonton and Calgary regions, the Western Alberta Transmission Line, was released on Dec. 6, 2012, albeit with some changes to the preferred route and the use of monopole structures in a 12-kilometre portion of the transmission line.

The existing transmission system is congested and aging, resulting in excessive energy loss and constraints on our generation operations as expected electricity flows exceed the system’s current limits. The reinforcement of the transmission system as provided by the two transmission lines will alleviate these constraints, reduce transmission line losses, and allow for the development of additional generation.

|

|

TransAlta Corporation | 2012 Annual Report |

|

|

management’s discussion and analysis |

Environmental Legislation and Technologies

Environmental issues and related legislation have, and will continue to have, an impact upon our business. Since 2007, we have incurred costs as a result of Greenhouse Gas (“GHG”) legislation in Alberta. Please refer to the Climate Change and the Environment section of this MD&A for additional information on the changes to Alberta’s GHG legislation that occurred in 2012. Our exposure to increased costs as a result of environmental legislation in Alberta is mitigated through change-in-law provisions in our PPAs. In the State of Washington, the TransAlta Energy Bill (the “Bill”) was signed into law and provides a framework to transition from coal to other forms of generation. Legislation in other jurisdictions is in various stages of maturity and sophistication.

While TransAlta discontinued its Pioneer carbon capture and storage project (“Pioneer”) in April 2012, the detailed Front-End Engineering Design (“FEED”) study that was completed provided us with a comprehensive analysis of this technology, which will provide ongoing value in the assessment of other carbon control strategies. We also are actively and broadly disseminating the knowledge from Pioneer to others who may benefit from it.

Economic Environment

The economic environment showed signs of weakness during 2012 and in 2013 we expect slow to moderate growth in Alberta and Australia, and low growth in other markets. We continue to monitor global events and their potential impact on the economy and our supplier and commodity counterparty relationships.

Contracted Cash Flows

During the year, 90 per cent of our consolidated power portfolio was contracted through the use of PPAs and other long-term contracts. We also entered into short-term physical and financial contracts for the remaining volumes, which are primarily for periods of up to five years, with the average price of these contracts in 2012 ranging from $60 to $65 per megawatt hour (“MWh”) in Alberta, and from U.S.$50 to $55 per MWh in the Pacific Northwest.

Electricity Prices

|

|

Spot electricity prices are important to our business as our merchant natural gas, wind, hydro, and thermal facilities are exposed to these prices. Changes in these prices will affect our profitability, economic dispatching, and any contracting strategy. Our Alberta plants, operating under PPAs, receive contracted capacity payments based on targeted availability and will pay penalties or receive payments for production outside targeted availability based upon a rolling 30-day average of spot prices. The PPAs and long-term contracts covering a number of our generating facilities help minimize the impact of spot price changes.

Spot electricity prices in our markets are driven by customer |

demand, generator supply, natural gas prices, and the other business environment dynamics discussed above. We monitor these trends in prices, and schedule maintenance, where possible, during times of lower prices.

For the year ended Dec. 31, 2012, average spot prices in all three markets decreased compared to the same period in 2011, partially due to lower natural gas prices. In Alberta, spot prices also decreased as a result of overall higher availability. In the Pacific Northwest, spot prices also decreased as a result of increased wind and hydro generation. Spot prices in Ontario also decreased compared to 2011 due to increased supply resulting from facilities returning to service.

In 2013, power prices in Alberta are expected to be lower than 2012 due to fewer planned turnarounds and increased capacity due to additional generation facilities coming online, partially offset by load growth. In the Pacific Northwest, we expect prices to be modestly stronger than in 2012; however, overall prices will still remain weak because of low natural gas prices and slow load growth.

For the year ended Dec. 31, 2011, average spot prices increased in Alberta compared to 2010 due to load growth from the prior year and supply tightening in the market. In the Pacific Northwest and Ontario, average spot prices decreased compared to 2010 due to lower natural gas prices and increased hydro generation in both regions.

|

TransAlta Corporation | 2012 Annual Report |

|

management’s discussion and analysis |

|

Spark Spreads

|

|

Spark spreads measure the potential profit from generating electricity at current market rates. A spark spread is calculated as the difference between the market price of electricity and its cost of production. The cost of production is comprised of the total cost of fuel and the efficiency, or heat rate, with which the plant converts the fuel source to electricity. For most markets, a standardized plant heat rate is assumed to be 7,000 British Thermal Units (“Btu”) per Kilowatt hour (“KWh”).

Spark spreads will also vary between plants due to their design, the geographical region in which they operate, and customer and/or market requirements. The change in the prices of electricity and natural gas, and the resulting spark spreads in our three major markets, affect our Generation and Energy Trading Segments. |

For the year ended Dec. 31, 2012, average spark spreads in Alberta decreased compared to the same period in 2011 due to lower power prices. In the Pacific Northwest and Ontario, average spark spreads increased as a result of lower natural gas prices compared to 2011. The decrease in natural gas prices was greater than the decrease in spot prices in both the Pacific Northwest and Ontario, causing the spark spread to increase compared to 2011.

For the year ended Dec. 31, 2011, average spark spreads increased in Alberta compared to 2010 due to higher power prices. In the Pacific Northwest, average spark spreads decreased due to strong hydro generation, which caused power prices to decrease more than natural gas prices compared to 2010. In Ontario, spark spreads decreased as power prices weakened more than natural gas prices compared to 2010.

Strategy

Our goals are to deliver shareholder value by delivering solid returns through a combination of dividend yield and disciplined comparable Earnings Per Share (“EPS”) and funds from operations growth, while striving for a low to moderate risk profile, balancing capital allocation, and maintaining financial strength. Our comparable EPS and funds from operations growth are driven by optimizing and diversifying our existing assets and further expanding our overall portfolio and operations in the western regions of Canada, the U.S, and Australia. We are focusing on these geographic areas as our expertise, scale, and access to numerous fuel resources, including coal, wind, geothermal, hydro, and natural gas, allow us to create expansion opportunities in our core markets. Our strategy to achieve these goals has the following key elements:

Financial Strategy

Our financial strategy is to maintain a strong financial position and investment grade credit ratings to provide a solid foundation for our long-cycle, capital-intensive, and commodity-sensitive business. A strong financial position and investment grade credit ratings improve our competitiveness by providing greater access to capital markets, lowering our cost of capital compared to that of non-investment grade companies, and enabling us to contract our assets with customers on more favourable commercial terms. We value financial flexibility, which allows us to selectively access the capital markets when conditions are favourable.

Contracting Strategy

In 2012, we continued to see some demand growth in our Alberta market; however, demand in the Pacific Northwest and Ontario remained flat. While we are not immune to lower power prices, the impact of these lower prices is expected to be mitigated as approximately 85 per cent of 2013 and approximately 78 per cent of 2014 expected capacity across our fleet is contracted. On an aggregated portfolio basis, depending on market conditions, we target being up to 90 per cent contracted for the upcoming year. This contracting strategy helps protect our cash flow and our financial position through economic cycles.

Operational Strategy

We manage our facilities to achieve stable and predictable operations that are comparatively low cost and balanced with our fleet availability target. Our target for 2013 is to increase productivity and achieve overall fleet availability of 89 to 90 per cent. Over the last three years, our average adjusted availability has been 89.0 per cent, which is in line with our corporate target.

|

|

TransAlta Corporation | 2012 Annual Report |

|

|

management’s discussion and analysis |

Growth Strategy

During 2012, we completed efficiency uprates, which we expect will add an additional 26 MW at Keephills Units 1 and 2 and an expected 15 MW at Sundance Unit 3. Please refer to the Significant Events section of this MD&A. Although we completed the uprate at Sundance Unit 3, the resulting increased capacity will not be realized until we replace the generator stator. During the year we also had 68 MW of wind generation under construction at our New Richmond facility and we completed the acquisition from Fortescue Metals Group Ltd. (“Fortescue”) of its 125 MW natural gas-fired and diesel-fired Solomon power station in Western Australia.

Our growth strategy is also focused upon greening and diversifying our portfolio to reduce our carbon footprint and develop long-term, sustainable power generation in our core markets. We continue to explore and selectively develop opportunities for future sustainable power projects.

Capability to Deliver Results

We have the following core competencies and non-capital resources that give us the capability to achieve our corporate objectives. Refer to the Liquidity and Capital Resources section of this MD&A for further discussion of the capital resources available that will assist us in achieving our objectives.

Operational Excellence

We seek to optimize our generating portfolio by owning and managing a mix of relatively low-risk assets and fuels to deliver an acceptable and predictable return. Our strategic focus is primarily on improving base operations, repositioning coal, and diversifying our portfolio.

Financial Strength

We manage our financial position and cash flows to maintain financial strength and flexibility throughout all economic cycles. This financial discipline will continue to be important during 2013. We continue to maintain $2.0 billion in committed credit facilities, and as of Dec. 31, 2012, $0.8 billion was available to us. Our investment grade credit rating, available credit facilities, funds from operations, and our manageable debt maturity profile provide us with financial flexibility. As a result, we can be selective if and when we go to the capital markets for funding.

The funding required for our growth strategy is supported by our financial strength. In 2012, we took advantage of favourable capital markets by completing the sale of $225 million of Series E Preferred Shares, an offering of U.S.$400 million senior notes, and a public offering of 21.2 million common shares. Looking forward, we expect continued capital market support for projects that meet our return requirements and risk profile.

In the third quarter of 2012, Standard and Poor (“S&P”) downgraded our corporate credit rating and senior unsecured debt rating from BBB negative outlook to BBB- stable and our preferred shares from P-3 (high) to P-3. Moody’s Investor Services (“Moody's”) downgraded our senior unsecured debt rating from Baa2 negative outlook to Baa3 stable. In addition, DBRS placed our unsecured debt rating under review with developing implications.

Following our preferred share offering of 21.2 million common shares, DBRS revised our credit rating back to BBB stable. Participation in the Dividend Reinvestment and Share Purchase (“DRASP”) plan continues to be strong and is generating approximately $50 million of new equity on a quarterly basis.

Disciplined Capital Allocation

We are committed to optimizing the balance between returning capital to shareholders and meeting our liquidity requirements, base business investment, and growth opportunities. We believe we have a proven track record of maintaining our long-term financial stability, which includes balancing the cash distributions to our shareholders through dividends with making investments in growth projects that will deliver stable long-term cash flow.

We continue to selectively grow our diversified generating fleet to increase production and meet future demand requirements, with growth projects that have the ability to meet or exceed our targeted rate of return. We currently have 68 MW of wind generation under construction and during the year we completed the acquisition from Fortescue of its 125 MW natural gas-fired and diesel-fired Solomon power station in Western Australia.

|

TransAlta Corporation | 2012 Annual Report |

|

management’s discussion and analysis |

|

People

Our experienced leadership team is made up of senior business leaders who bring a broad mix of skills in the electricity sector, finance, law, government, regulation, engineering, operations, construction, risk management, and corporate governance. The leadership team’s experience and expertise, our employees’ knowledge and dedication to superior operations, and our entire organization’s knowledge of the energy business, in our opinion, has resulted in a long-term proven track record of financial stability. During 2012, we completed a restructuring of our resources as part of our ongoing strategy to continuously improve operational excellence and accelerate growth.

Performance Metrics

We have key measures that, in our opinion, are critical to evaluating how we are progressing towards meeting our goals. These measures, which include a mix of operational, risk management, and financial metrics, are discussed below.

Availability

|

|

We strive to optimize the availability of our plants throughout the year to meet demand. However, this ability to meet demand is limited by the requirement to shut down for planned maintenance and unplanned outages, as well as by reduced production as a result of derates. Our goal is to minimize these events through regular assessments of our equipment and a comprehensive review of our maintenance plans in order to balance our maintenance costs with optimal availability targets. Over the past three years, we have achieved an average adjusted availability of 89.0 per cent, which is in line with our long-term target of 89 to 90 per cent. Our availability in 2012, after adjusting for economic dispatching at Centralia Thermal, was 90.0 per cent (2011 – 88.2 per cent). |

For the year ended Dec. 31, 2012, availability increased compared to the same period in 2011 primarily due to lower planned and unplanned outages at Centralia Thermal and lower unplanned outages at the Alberta coal PPA facilities and at Genesee Unit 3, partially offset by higher planned outages at the Alberta coal PPA facilities and at Genesee Unit 3.

Availability for the year ended Dec. 31, 2011 decreased compared to 2010 primarily due to higher planned and unplanned outages at Centralia Thermal and higher unplanned outages at Genesee Unit 3, partially offset by lower planned and unplanned outages at the Alberta coal PPA facilities and lower planned outages at Genesee Unit 3.

The outages at Centralia Thermal did not negatively impact our gross margins for the years ended Dec. 31, 2012 and 2011 as we were able to extend some of our planned outages to take advantage of lower market prices to purchase power on the market to fulfill our power contracts.

Productivity

|

|

Our OM&A costs reflect the operating cost of our facilities. These costs can fluctuate due to the timing and nature of planned maintenance activities. The remainder of OM&A costs reflects the cost of day-to-day operations. Our target is to offset the impact of inflation in our recurring operating costs as much as possible through cost control and targeted productivity initiatives. We measure our ability to maintain productivity on OM&A based on the cost per installed MWh of capacity. |

For the year ended Dec. 31, 2012, OM&A costs per installed MWh decreased compared to 2011 primarily due to lower compensation costs as a result of productivity initiatives and a continued focus on costs.

For the year ended Dec. 31, 2011, OM&A costs per installed MWh increased compared to 2010 due to higher compensation costs associated with favourable results in the Energy Trading Segment, the writeoff of certain wind development costs and costs associated with several productivity initiatives, partially offset by lower costs associated with the discontinuation of managing the base plant at Poplar Creek.

|

|

TransAlta Corporation | 2012 Annual Report |

|

|

management’s discussion and analysis |

Sustaining Capital and Productivity Expenditures

We are in a long-cycle capital-intensive business that requires significant capital expenditures. Our goal is to undertake sustaining capital and productivity expenditures that ensure our facilities operate reliably and safely over a long period of time. Our sustaining capital and productivity is comprised of three components: (1) routine and mine capital, (2) planned maintenance, and (3) productivity capital.

|

|

In 2012, we spent $139 million more on sustaining capital and productivity expenditures compared to 2011, which was made up of $18 million more on routine and mine capital, $102 million more on planned maintenance, and $19 million more on productivity. The increase in routine and mine capital was due to non-turnaround maintenance projects. Planned maintenance increased primarily due to planned outages at Keephills Units 1 and 2 and Sundance Units 3 and 5. A significant part of the expenditures at the Keephills facility relate to more comprehensive planned major maintenance, including significant component replacements that are not expected to be replaced again over the balance of the life of the plant. Productivity increased as a result of costs associated with several corporate improvement initiatives. |

In 2011, we spent $2 million more on sustaining capital and productivity expenditures compared to 2010, which was made up of $29 million more on productivity capital, $17 million less on routine and mine capital, and $10 million less on planned maintenance. The decrease in routine and mine capital was due to lower information technology capital and non-turnaround maintenance costs, as well as a decrease in mine capital due to lower land costs. Planned maintenance decreased primarily due to fewer major coal outages due to the shutdown of Sundance Units 1 and 2, partially offset by higher gas plant outages. The increase in productivity expenditures was primarily due to instrument and controls projects at the Keephills and Sundance facilities, site improvements at our Sundance facility, and the implementation of new software programs.

Safety

Safety is our top priority with all of our staff, contractors, and visitors. Our objective is to maintain our Injury Frequency Rate (“IFR”) at less than 1.00 for 2013. Our ultimate goal is to achieve zero injury incidents.

|

|

2012 |

2011 |

2010 |

|

IFR |

0.89 |

0.89 |

1.19 |

In 2012, our IFR was consistent with 2011. In 2011, our IFR decreased due to fewer injuries at our Alberta coal facilities, primarily at our Keephills and Sundance facilities. These improvements are a result of continuous efforts to enhance our safety programs through near miss reporting, safety improvement, education, and awareness.

Earnings and Funds from Operations

We focus our base business on delivering strong earnings and funds from operations growth. Our goal is to steadily grow comparable EBITDA, comparable EPS, and funds from operations over the long term, recognizing that the amount of growth may fluctuate year over year with the commodity cycle.

|

|

2012 |

2011 |

2010 |

|

Comparable EBITDA |

1,014 |

1,045 |

963 |

|

Comparable EPS |

0.50 |

1.04 |

0.97 |

|

Funds from operations |

776 |

809 |

805 |

|

Funds from operations per share |

3.30 |

3.64 |

3.68 |

In 2012, comparable EPS and comparable EBITDA decreased compared to 2011 primarily due to lower comparable earnings as a result of the decrease in Energy Trading’s gross margins. In 2011, comparable EPS and comparable EBITDA increased compared to 2010 primarily due to higher comparable earnings due to strong trading results in the Western regions.

In 2012, funds from operations decreased compared to 2011 due to lower comparable net earnings, after excluding the impact of the Sundance Units 1 and 2 arbitration from earnings. In 2011, funds from operations increased compared to 2010 due to higher net earnings.

|

TransAlta Corporation | 2012 Annual Report |

|

management’s discussion and analysis |

|

Investment Grade Ratios

Investment grade ratings support contracting activities and provide better access to capital markets through commodity and credit cycles. We are focused on maintaining a strong financial position and cash flow coverage ratios to support stable investment grade credit ratings.

|

|

2012 |

2011 |

2010 |

|

Adjusted cash flow to interest coverage (times)1 |

4.4 |

4.4 |

4.6 |

|

Adjusted cash flow to debt (%)1 |

18.9 |

20.1 |

19.6 |

|

Debt to invested capital (%) |

55.7 |

52.5 |

53.1 |

Adjusted cash flow to interest coverage in 2012 was comparable to 2011. Cash flow to interest coverage decreased in 2011 compared to 2010 primarily due to lower capitalized interest. Our goal is to maintain this ratio in a range of four to five times.

Adjusted cash flow to debt decreased in 2012 compared to 2011 due to higher average debt levels in 2012. Cash flow to debt improved in 2011 compared to 2010 due to lower average debt levels in 2011. Our goal is to maintain this ratio in a range of 20 to 25 per cent.

Debt to invested capital increased as at Dec. 31, 2012 compared to 2011 due to higher debt levels. Debt to invested capital decreased as at Dec. 31, 2011 compared to 2010 due to lower debt levels and higher net earnings. Our goal is to maintain this ratio in a range of 50 to 55 per cent.

These targets represent a prudent range for the Corporation. At times and over a short-term period, the credit ratios may be outside of the specified target ranges while we realign the capital structure. During 2012, we took several steps to reduce debt, including adding a Premium DividendTM component to our dividend reinvestment plan and issuing approximately $300 million of common shares and approximately $225 million of preferred shares. In 2013, the dividend reinvestment plan is expected to generate proceeds of approximately $200 million. Please refer to Note 28 of our audited consolidated financial statements within our 2012 Annual Report for additional information regarding the amendments.

We seek to maintain financial flexibility by using multiple sources of capital to finance capital allocation plans effectively, while maintaining a sufficient level of available liquidity to support contracting and trading activities. Further, financial flexibility allows our commercial team to contract our portfolio with a variety of counterparties on terms and prices that are beneficial to our financial results.

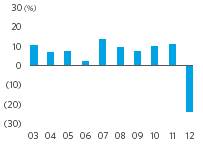

Shareholder Value

Our business model is designed to deliver low to moderate risk-adjusted sustainable returns and maintain financial strength and flexibility, which enhances shareholder value in a capital-intensive, long-cycle, commodity-based business. Our goal is to grow Total Shareholder Return (“TSR”)2 by achieving a return of eight to ten per cent per year over the long term, with four to five per cent resulting from yield and four to five per cent resulting from growth.

The table below shows our historical performance on this measure:

|

|

2012 |

2011 |

2010 |

|

TSR (%) |

(22.5) |

4.9 |

(5.0) |

While the TSR has been below our target of eight to ten per cent, we continue to focus on delivering strong shareholder returns. We are actively seeking growth opportunities in Western U.S., Western Australia, and Canada, as demonstrated by the Solomon plant acquisition in Western Australia in 2012. We are focused on delivering cash flow to fund the dividend and growth and maintain investment grade credit ratings. We have declared total dividends of $1.16 per share on common shares over the course of the last three years, returning value to shareholders.

1 Adjusted for the impacts associated with Sundance Units 1 and 2 arbitration.

2 This measure is not defined under IFRS. We evaluate our performance and the performance of our business segments using a variety of measures. This measure is not necessarily comparable to a similarly titled measure of another company. TSR is the total amount returned to investors over a specific holding period and includes capital gains, capital losses, and dividends.

|

|

TransAlta Corporation | 2012 Annual Report |

|

|

management’s discussion and analysis |

Results of Operations

Our results of operations are presented on a consolidated basis and by business segment. We have three business segments: Generation, Energy Trading, and Corporate. Some of our accounting policies require management to make estimates or assumptions that in some cases may relate to matters that are inherently uncertain. Some of our critical accounting policies and estimates include: revenue recognition, valuation and useful life of Property, Plant, and Equipment (“PP&E”), financial instruments, decommissioning and restoration provisions, valuation of goodwill, income taxes, and employee future benefits. Refer to the Critical Accounting Policies and Estimates section of this MD&A for further discussion.

In this MD&A, the impact of foreign exchange fluctuations on foreign currency denominated transactions and balances is discussed with the relevant items from the Consolidated Statements of Earnings (Loss) and the Consolidated Statements of Financial Position. While individual line items on the Consolidated Statements of Financial Position may be impacted by foreign exchange fluctuations, the net impact of the translation of individual items relating to foreign operations to our presentation currency is reflected in Accumulated Other Comprehensive Income (Loss) (“AOCI”) in the equity section of the Consolidated Statements of Financial Position.

Net Earnings Attributable to Common Shareholders

The primary factors contributing to the change in net earnings attributable to common shareholders for the years ended Dec. 31, 2012 and 2011 are presented below:

|

Net earnings applicable to common shareholders for the year ended Dec. 31, 2010 |

255 |

|

Increase in Generation comparable gross margins |

48 |

|

Mark-to-market movements and de-designations – Generation |

84 |

|

Increase in Energy Trading gross margins |

96 |

|

Increase in operations, maintenance, and administration costs |

(35) |

|

Increase in depreciation and amortization expense |

(18) |

|

Increase in gain on sale of assets |

16 |

|

Decrease in asset impairment charges |

11 |

|

Increase in net interest expense |

(37) |

|

Increase in equity earnings |

7 |

|

Increase in income taxes expense |

(82) |

|

Increase in net earnings attributable to non-controlling interests |

(14) |

|

Increase in preferred share dividends |

(14) |

|

MF Global Inc. collateral |

(18) |

|

Other |

(9) |

|

Net earnings attributable to common shareholders for the year ended Dec. 31, 2011 |

290 |

|

Increase in Generation comparable gross margins |

45 |

|

Mark-to-market movements and de-designations – Generation |

(199) |

|

Decrease in Energy Trading gross margins |

(134) |

|

Decrease in operations, maintenance, and administration costs |

52 |

|

Increase in depreciation and amortization expense |

(27) |

|

Decrease in gain on sale of assets |

(13) |

|

Increase in asset impairment charges |

(307) |

|

Increase in inventory writedown, net of consumption |

(19) |

|

Increase in restructuring charges |

(13) |

|

Increase in net interest expense |

(27) |

|

Decrease in equity income |

(29) |

|

Impact of Sundance Units 1 and 2 arbitration |

(254) |

|

Increase in preferred share dividends |

(16) |

|

MF Global Inc. collateral |

33 |

|

Other |

4 |

|

Net loss attributable to common shareholders for the year ended Dec. 31, 2012 |

(614) |

|

TransAlta Corporation | 2012 Annual Report |

|

management’s discussion and analysis |

|

For the year ended Dec. 31, 2012, Generation comparable gross margins, excluding the impact of mark-to-market movements, increased compared to the same period in 2011 primarily due to the impact of lower Alberta coal PPA penalties due to lower prices in Alberta, higher hydro margins, and lower unplanned outages at the Alberta coal PPA facilities and at Genesee Unit 3, partially offset by higher planned outages at the Alberta coal PPA facilities and Genesee Unit 3, unfavourable coal costs, and market curtailments.

In 2011, Generation comparable gross margins, excluding the impact of mark-to-market movements, increased compared to 2010 primarily due to higher hydro margins, the commencement of commercial operations of Keephills Unit 3 in 2011, higher wind volumes, lower planned and unplanned outages at the Alberta coal PPA facilities, and lower planned outages at Genesee Unit 3, partially offset by lower recoveries from the Poplar Creek base plant that we no longer operate, the sale of the Meridian facility, the impact of higher Alberta coal PPA penalties due to higher prices in Alberta during outages, the decommissioning of Wabamun, and higher unplanned outages at Genesee Unit 3. The lower recoveries at the Poplar Creek base plant were offset by lower OM&A costs.

Mark-to-market movements decreased for the year ended Dec. 31, 2012 compared to the same period in 2011 due to the recognition of higher mark-to-market gains in 2011 resulting from certain power hedging relationships being deemed ineffective. Included in these gains are amounts that are adjusted as a non-comparable item. Please refer to the Non-IFRS Measures section of this MD&A for further discussion.

In 2011, mark-to-market movements increased compared to 2010 due to the recognition of unrealized gains resulting from certain hedges being deemed ineffective for accounting purposes and increased weakening in market prices in the Pacific Northwest relative to our hedged prices.

For the year ended Dec. 31, 2012, Energy Trading gross margins decreased compared to the same period in 2011 primarily due to the impact of unexpected weather patterns, plant outages, and unfavourable market expectations on power and gas pricing for trading positions held.

In 2011, Energy Trading gross margins increased compared to 2010 primarily due to strong trading results in the Western regions and increased earnings from the acquisition of electricity and natural gas contracts. These positive results were partially offset by lower gross margins in the Pacific Northwest region resulting from lower pricing.

OM&A costs for the year ended Dec. 31, 2012 decreased compared to the same period in 2011 primarily due to lower compensation costs as a result of productivity initiatives and a continued focus on costs.

In 2011, OM&A costs increased compared to 2010 due to higher compensation costs primarily associated with favourable results in the Energy Trading Segment, the writeoff of certain wind development costs and costs associated with several productivity initiatives, partially offset by lower costs associated with the discontinuation of managing the base plant at Poplar Creek.

For the year ended Dec. 31, 2012, depreciation and amortization expense increased compared to 2011 primarily due to an increased asset base, largely due to the commencement of commercial operations at Keephills Unit 3, and asset retirements, partially offset by a reduction in depreciation expense due to a lower depreciable asset base caused by asset impairments and the change in the economic useful lives of Alberta coal-fired plants.

In 2011, depreciation expense increased compared to 2010 primarily due to an increased asset base, the impact of the 2010 decrease in Wabamun decommissioning and restoration costs, and the writedown of capital spares, partially offset by changes to estimated residual values, the sale of the Meridian facility, and favourable foreign exchange rates.

Gain on sale of assets for the year ended Dec. 31, 2012 decreased compared to 2011 due to the sale of our Meridian and Grande Prairie facilities and other development projects in 2011.

In 2011, the gain on sale of assets increased compared to 2010 due to the sale of the Meridian gas facility and the Grande Prairie biomass facility, and other development projects.

Asset impairment charges for the year ended Dec. 31, 2012 increased compared to 2011 due to impairment charges related to Centralia Thermal and our renewables fleet recorded in 2012. Refer to the Asset Impairment Charges section of this MD&A for further discussion.

In 2011, asset impairment charges decreased compared to 2010 due to impairment charges related to Sundance Units 1 and 2 and the Meridian facility recorded in 2010.

|

|

TransAlta Corporation | 2012 Annual Report |

|

|

management’s discussion and analysis |